Embed Size (px)

Citation preview

5.4 Retirement Funds

1

Section 5.4

Annuities (Retirement Funds)

Alaysia

5.4 Retirement Funds

2

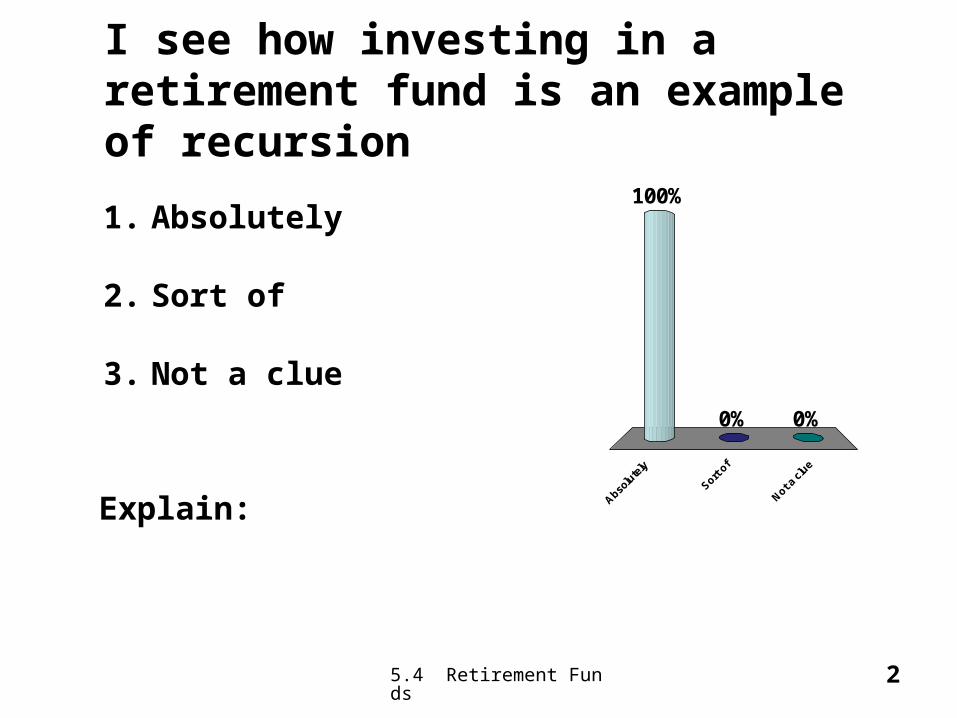

I see how investing in a retirement fund is an example of recursion

Abso

lute

ly

Sort

of

Not a

clu

e

100%

0%0%

1. Absolutely

2. Sort of

3. Not a clue

Explain:

5.4 Retirement Funds

3

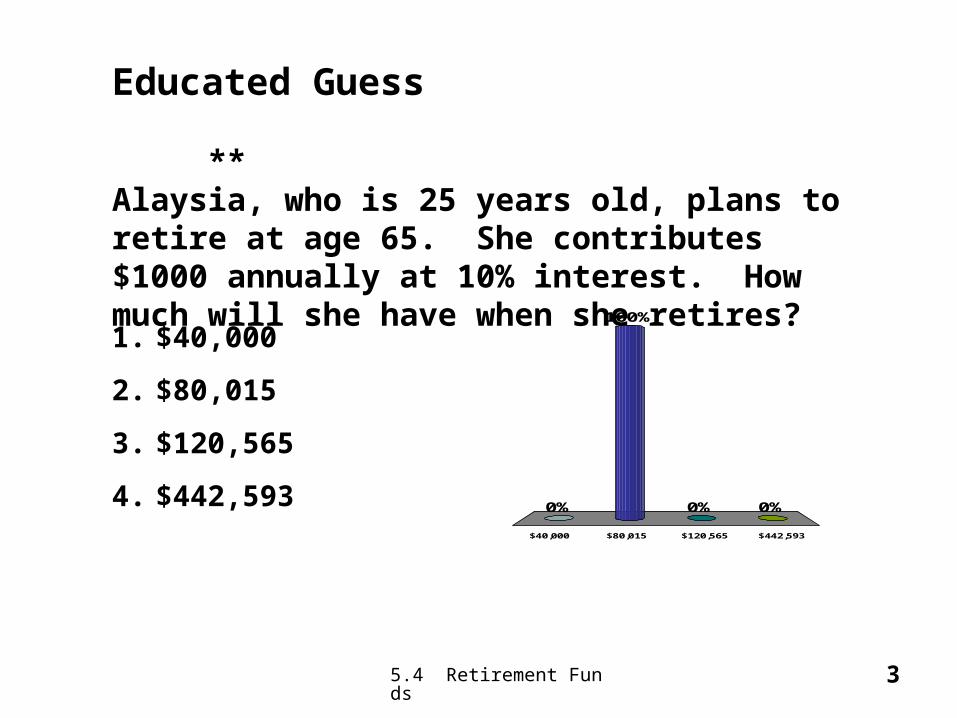

Educated Guess **Alaysia, who is 25 years old, plans to retire at age 65. She contributes $1000 annually at 10% interest. How much will she have when she retires?

$40,000 $80,015 $120,565 $442,593

0% 0%0%

100%

1. $40,000

2. $80,015

3. $120,565

4. $442,593

5.4 Retirement Funds

4

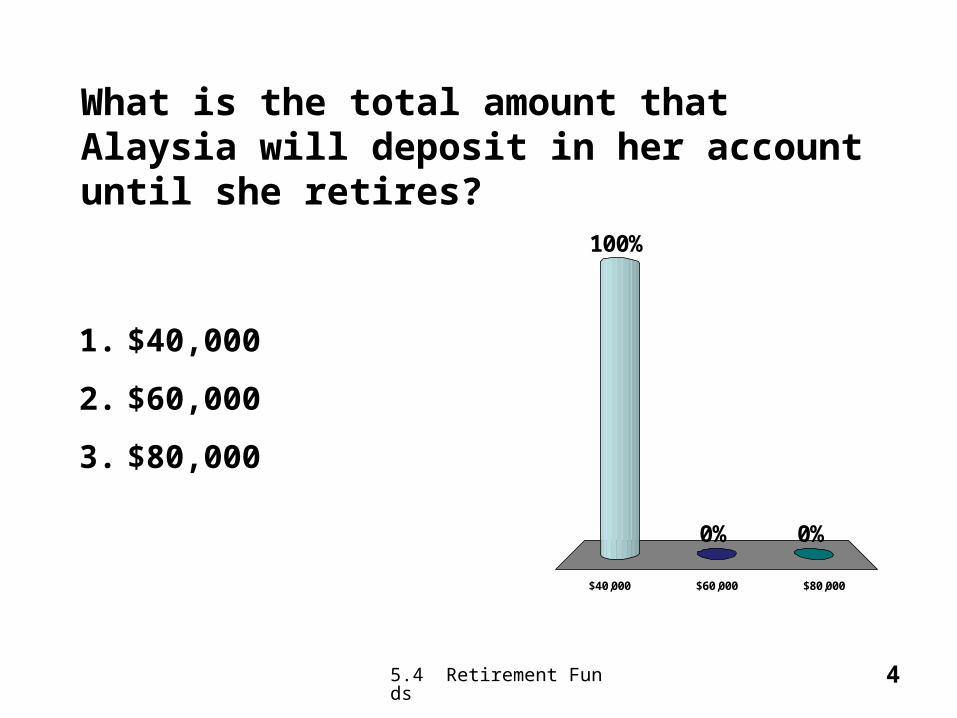

What is the total amount that Alaysia will deposit in her account until she retires?

$40,000 $60,000 $80,000

100%

0%0%

1. $40,000

2. $60,000

3. $80,000

5.4 Retirement Funds

5

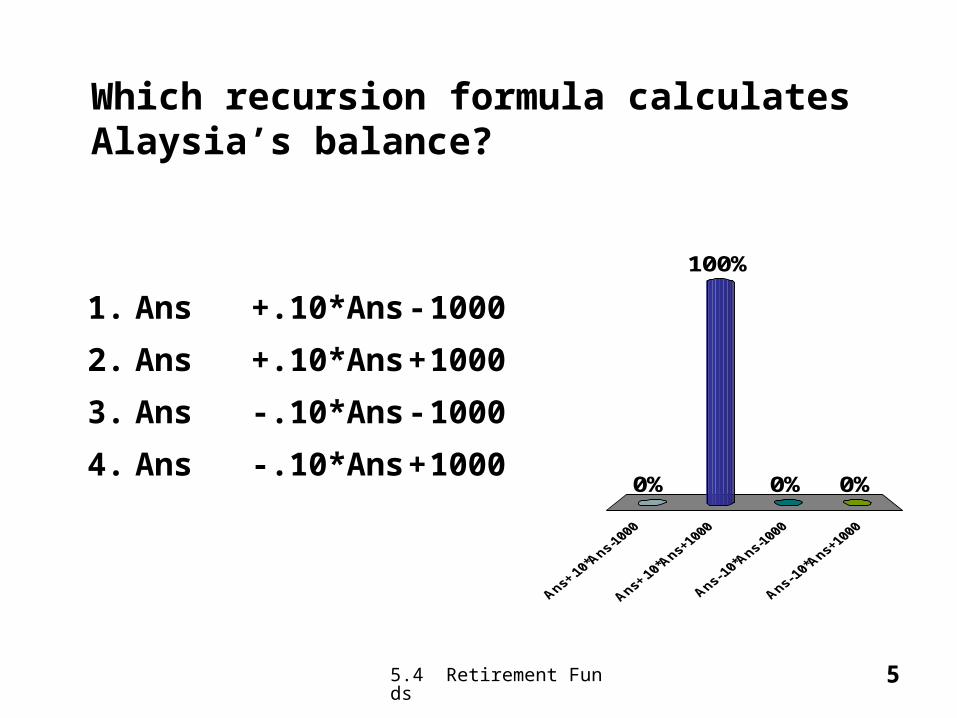

Which recursion formula calculates Alaysia’s balance?

0% 0%0%

100%

1. Ans +.10*Ans-1000

2. Ans +.10*Ans+1000

3. Ans -.10*Ans -1000

4. Ans -.10*Ans+1000

5.4 Retirement Funds

66

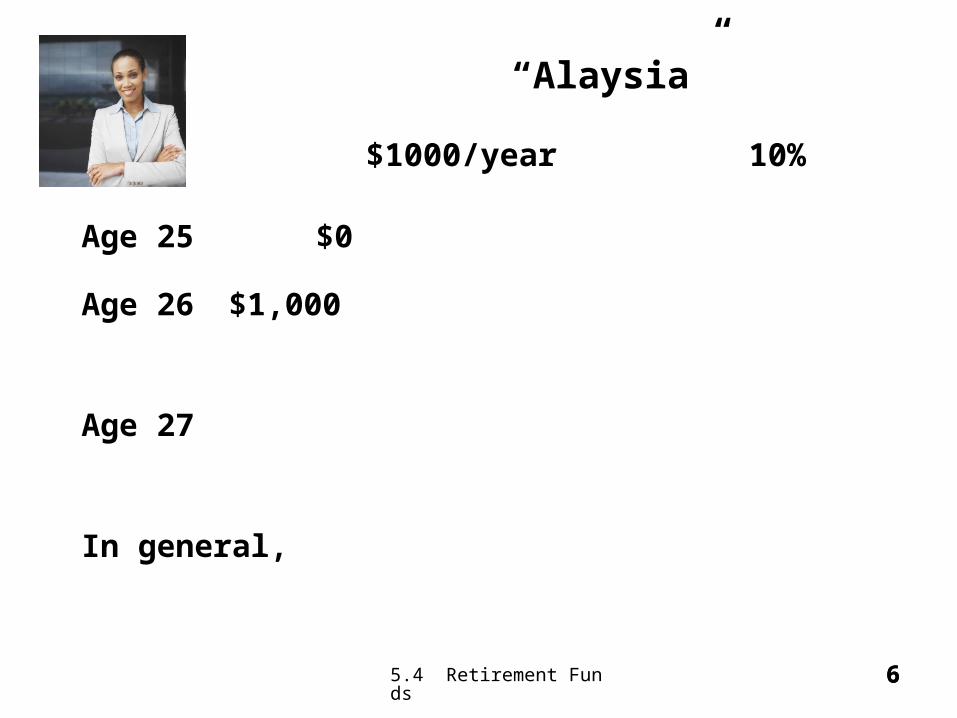

Age 25 $0

Age 26 $1,000

Age 27

In general,

“Alaysia”

$1000/year 10%

5.4 Retirement Funds

7

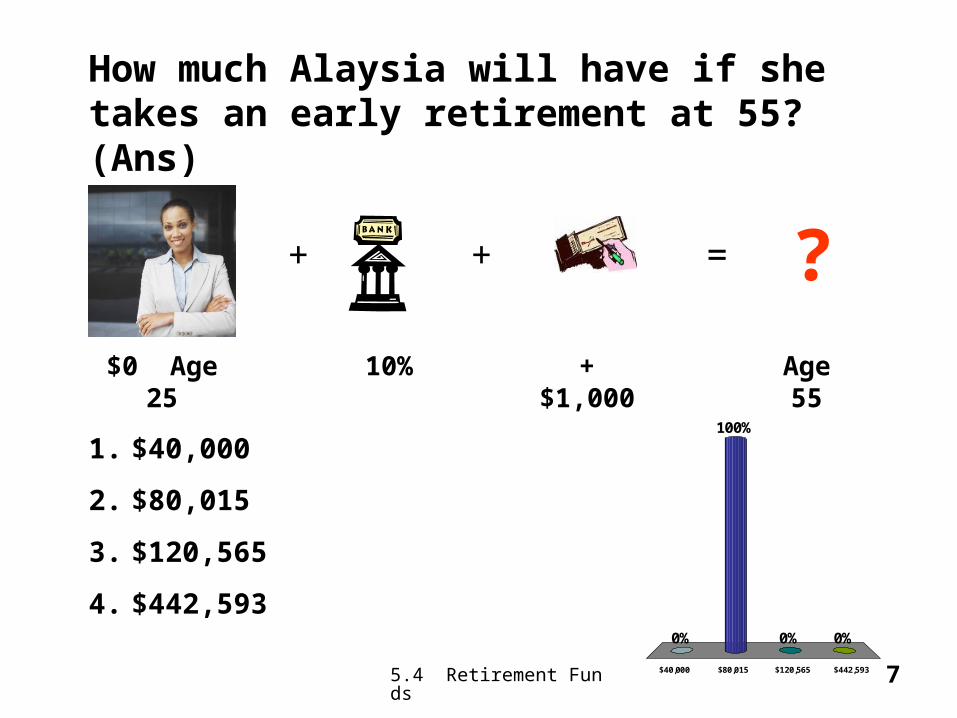

How much Alaysia will have if she takes an early retirement at 55? (Ans)

$40,000 $80,015 $120,565 $442,593

0% 0%0%

100%

10%

+ + =

+ $1,000

Age 55

$0 Age 25

?

1. $40,000

2. $80,015

3. $120,565

4. $442,593

5.4 Retirement Funds

8

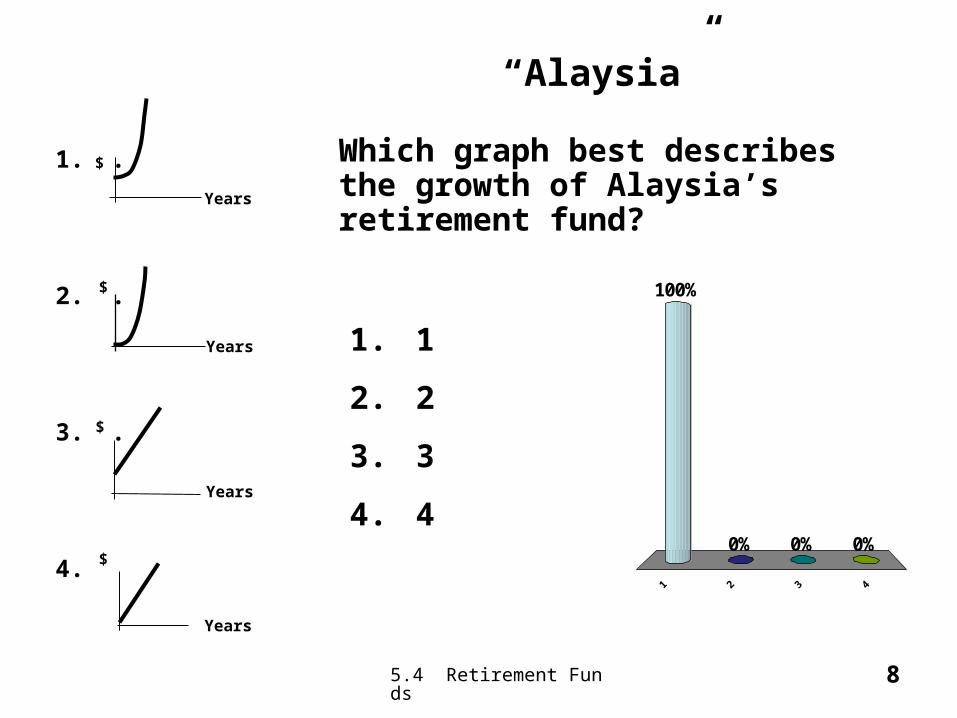

“Alaysia”

100%

0%0%0%

1. .

2. .

3. .

4.

$

Years

$

Years

Which graph best describes the growth of Alaysia’s retirement fund?

Years

$

$

Years 1. 1

2. 2

3. 3

4. 4

5.4 Retirement Funds

9

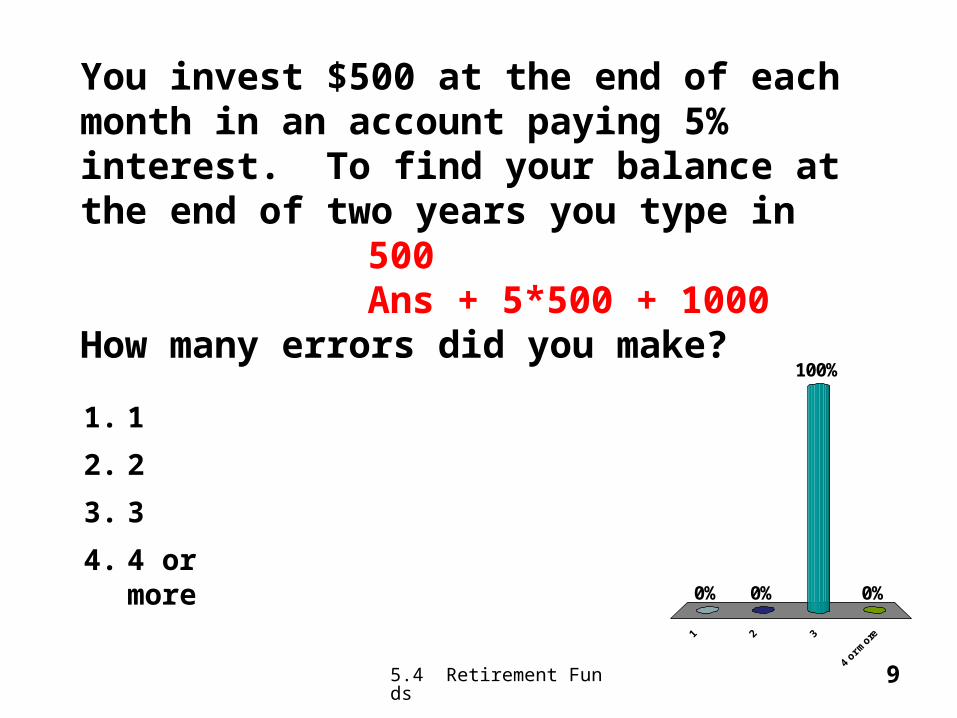

You invest $500 at the end of each month in an account paying 5% interest. To find your balance at the end of two years you type in

500Ans + 5*500 + 1000

How many errors did you make?

1 2 3

4 o

r more

0% 0%

100%

0%

1. 1

2. 2

3. 3

4. 4 or more

5.4 Retirement Funds

1010

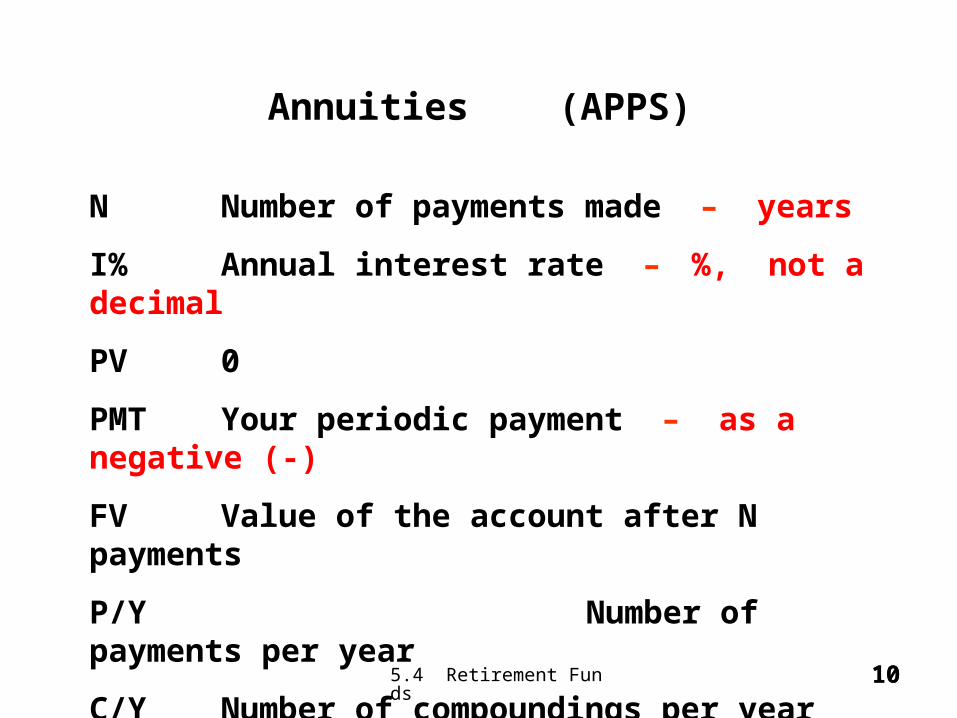

Annuities (APPS)

N Number of payments made – years

I% Annual interest rate – %, not a decimal

PV 0

PMT Your periodic payment – as a negative (-)

FV Value of the account after N payments

P/Y Number of payments per year

C/Y Number of compoundings per year

5.4 Retirement Funds

11

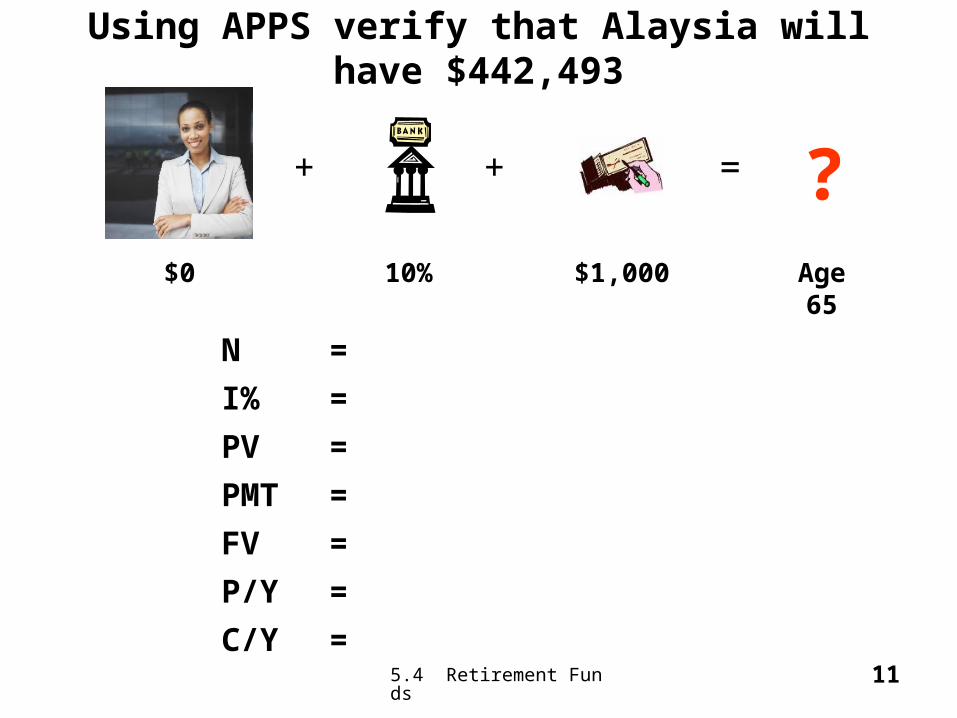

Using APPS verify that Alaysia will have $442,493

10%

+ + =

$1,000 Age 65

$0

?

N =

I% =

PV =

PMT =

FV =

P/Y =

C/Y =

5.4 Retirement Funds

1212

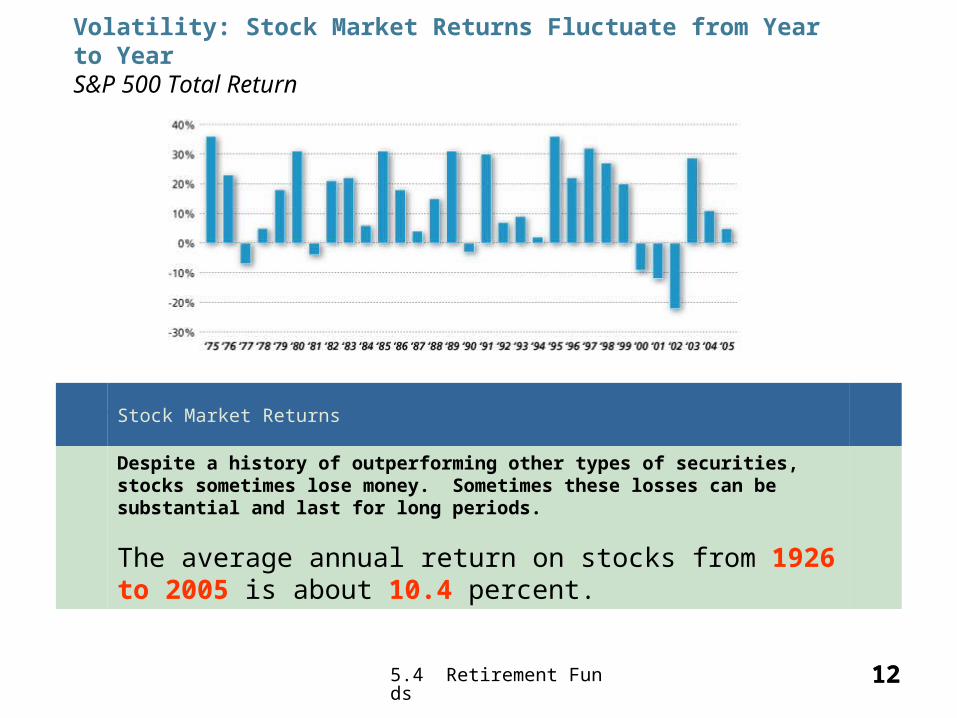

Volatility: Stock Market Returns Fluctuate from Year to Year S&P 500 Total Return

Source: Bloomberg

Stock Market Returns

Despite a history of outperforming other types of securities, stocks sometimes lose money. Sometimes these losses can be substantial and last for long periods.

The average annual return on stocks from 1926 to 2005 is about 10.4 percent.

5.4 Retirement Funds

1313

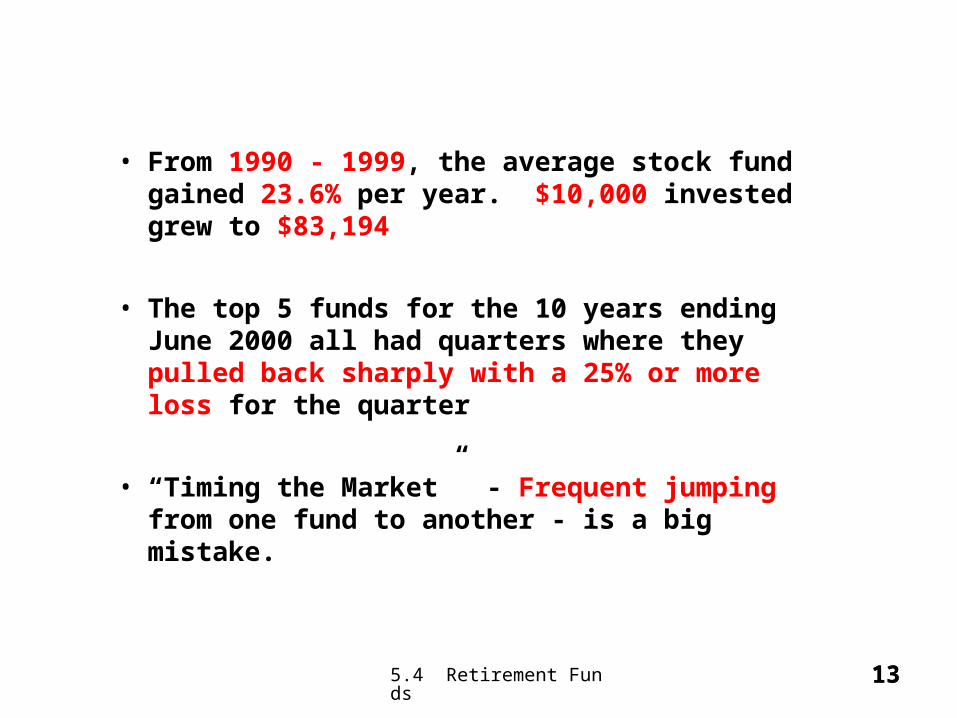

• From 1990 - 1999, the average stock fund gained 23.6% per year. $10,000 invested grew to $83,194

• The top 5 funds for the 10 years ending June 2000 all had quarters where they pulled back sharply with a 25% or more loss for the quarter

• “Timing the Market” - Frequent jumping from one fund to another - is a big mistake.

5.4 Retirement Funds

14

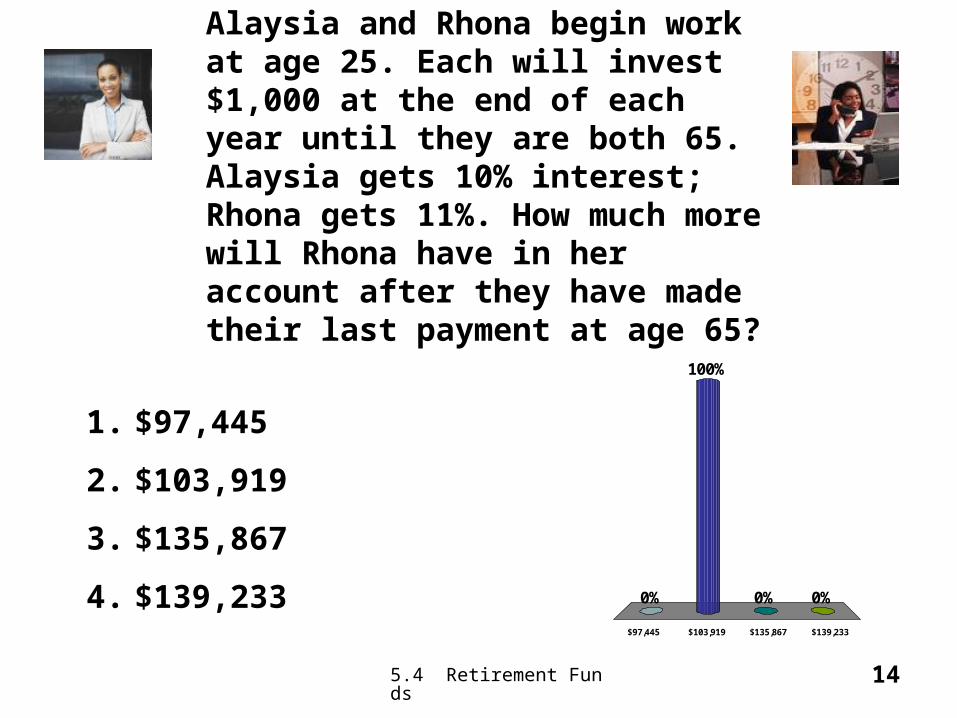

Alaysia and Rhona begin work at age 25. Each will invest $1,000 at the end of each year until they are both 65. Alaysia gets 10% interest; Rhona gets 11%. How much more will Rhona have in her account after they have made their last payment at age 65?

$97,445 $103,919 $135,867 $139,233

0% 0%0%

100%

1. $97,445

2. $103,919

3. $135,867

4. $139,233

5.4 Retirement Funds

1515

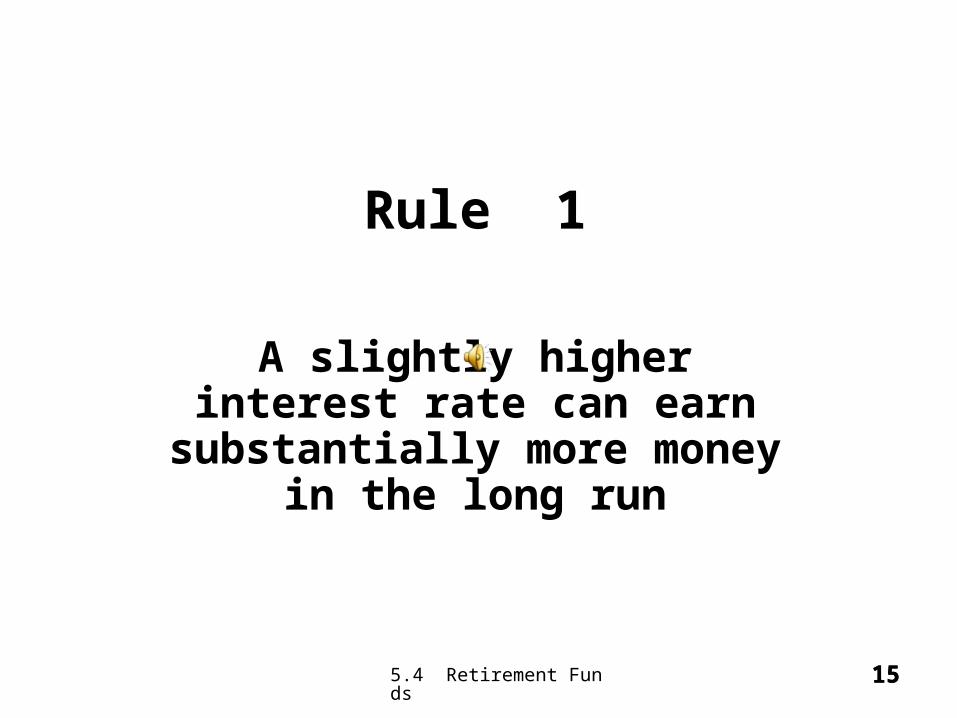

Rule 1

A slightly higher interest rate can earn substantially

more money in the long run

5.4 Retirement Funds

1616

5.4 Retirement Funds

1717

Rule 2

Small payments over time can earn huge amounts of

money

5.4 Retirement Funds

18

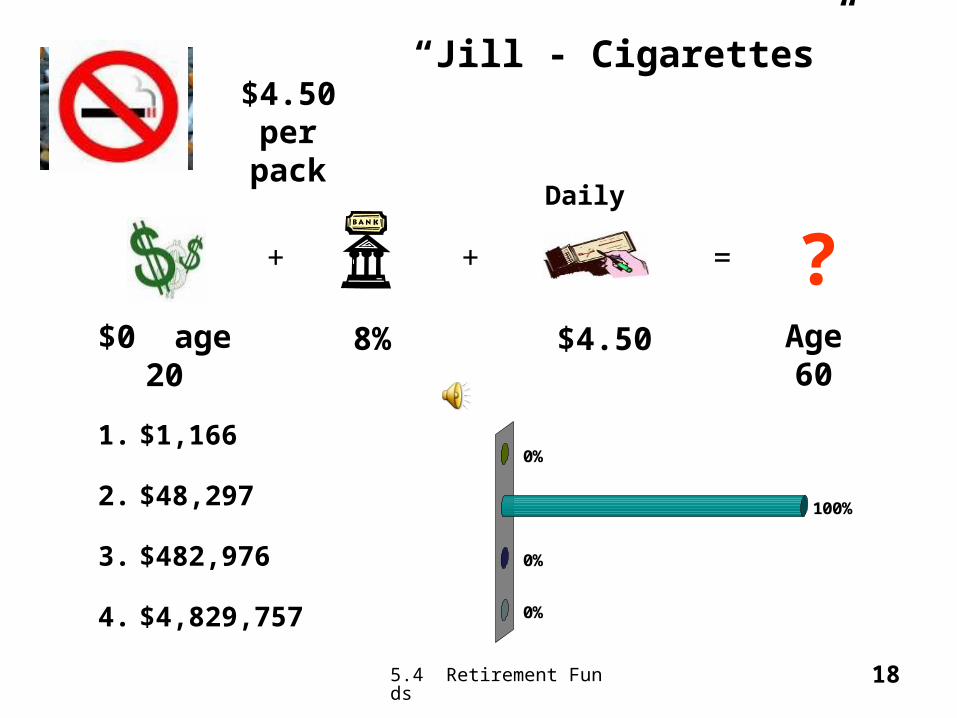

“Jill - Cigarettes”

8%

+ + =

$4.50 Age 60

$0 age 20

?

$4.50 per

pack

0%

0%

100%

0%1. $1,166

2. $48,297

3. $482,976

4. $4,829,757

Daily

5.4 Retirement Funds

19

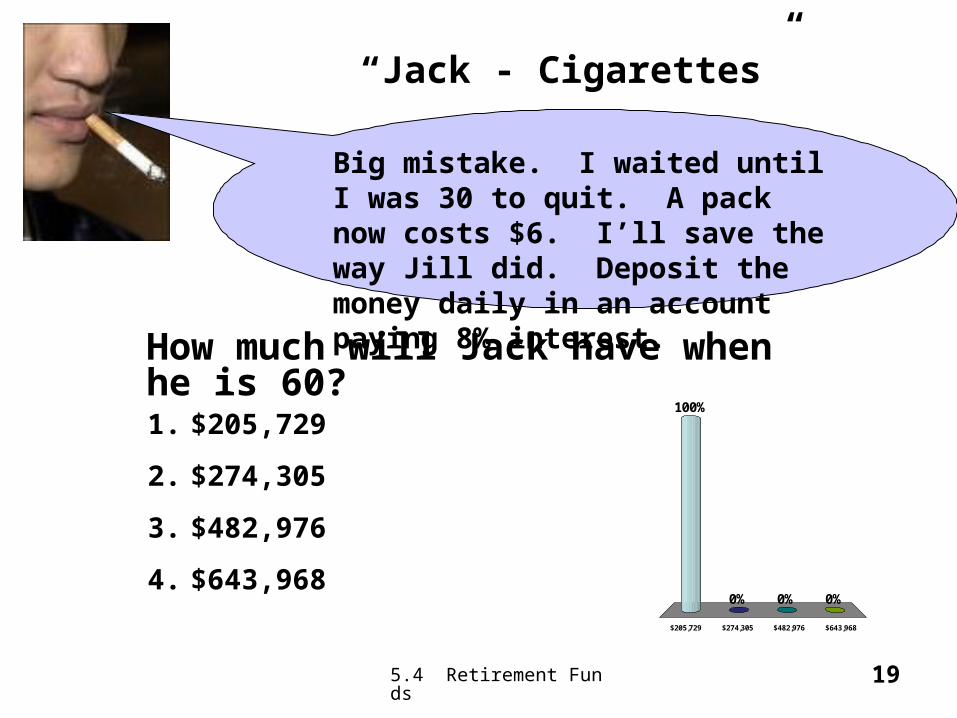

“Jack - Cigarettes”

$205,729 $274,305 $482,976 $643,968

100%

0%0%0%

1. $205,729

2. $274,305

3. $482,976

4. $643,968

How much will Jack have when he is 60?

Big mistake. I waited until I was 30 to quit. A pack now costs $6. I’ll save the way Jill did. Deposit the money daily in an account paying 8% interest.

5.4 Retirement Funds

20

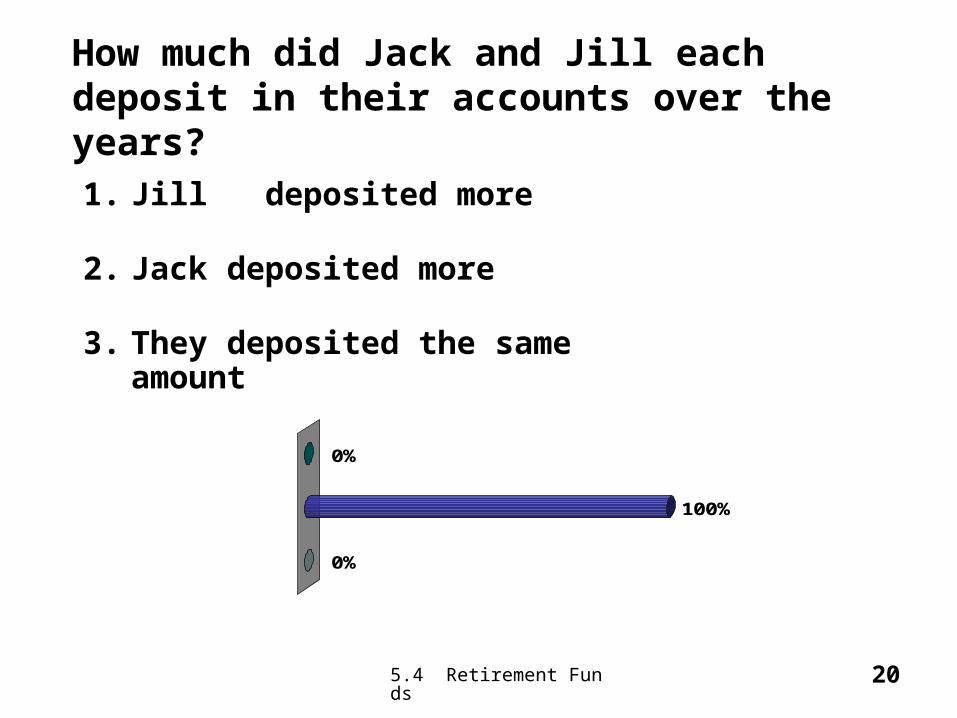

How much did Jack and Jill each deposit in their accounts over the years?

0%

100%

0%

1. Jill deposited more

2. Jack deposited more

3. They deposited the same amount

5.4 Retirement Funds

2121

Rule 3

The earlier you begin to invest the better

Chart

5.4 Retirement Funds

22

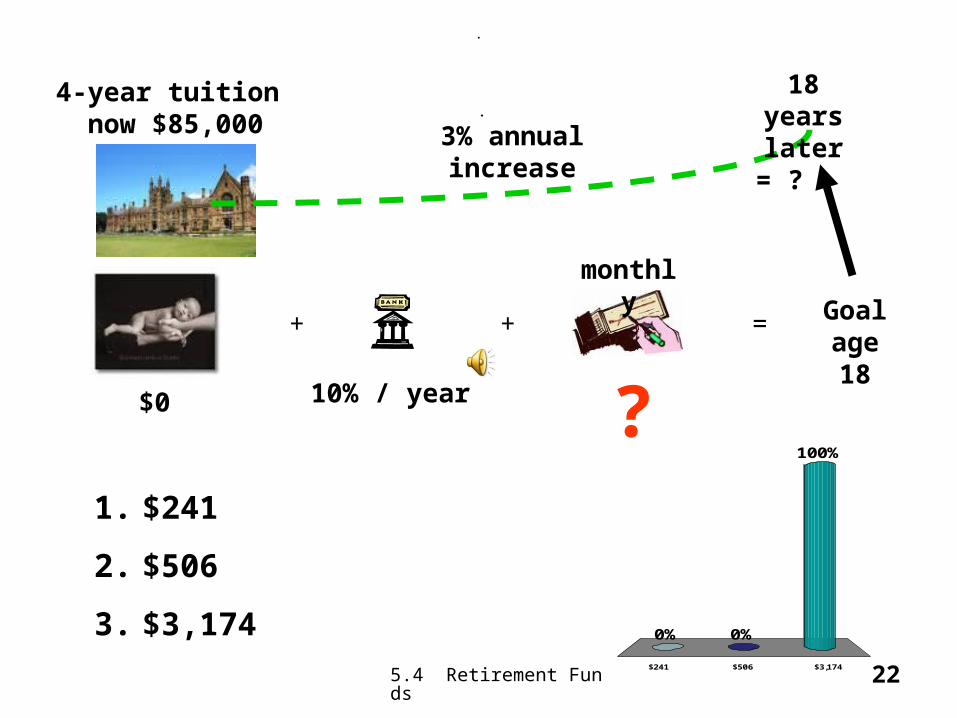

.

$241 $506 $3,174

0%

100%

0%

1. $241

2. $506

3. $3,174

+ + = Goalage 18

$0 10% / year

4-year tuition now $85,000 3% annual

increase

18 years later = ?

?

.

monthly

5.4 Retirement Funds

2323

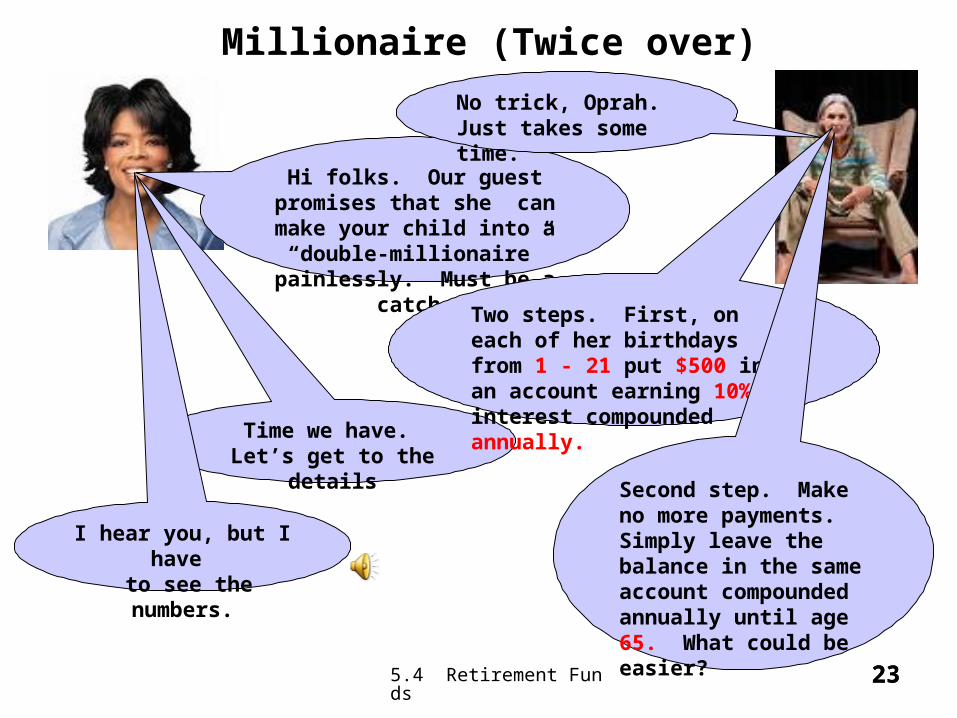

Millionaire (Twice over)

Hi folks. Our guest promises that she can make your child into a “double-millionaire” painlessly. Must be a

catch.

No trick, Oprah. Just takes some time.

Time we have. Let’s get to the

details

Two steps. First, on each of her birthdays from 1 - 21 put $500 in an account earning 10% interest compounded annually.

Second step. Make no more payments. Simply leave the balance in the same account compounded annually until age 65. What could be easier?

I hear you, but I have

to see the numbers.

5.4 Retirement Funds

24

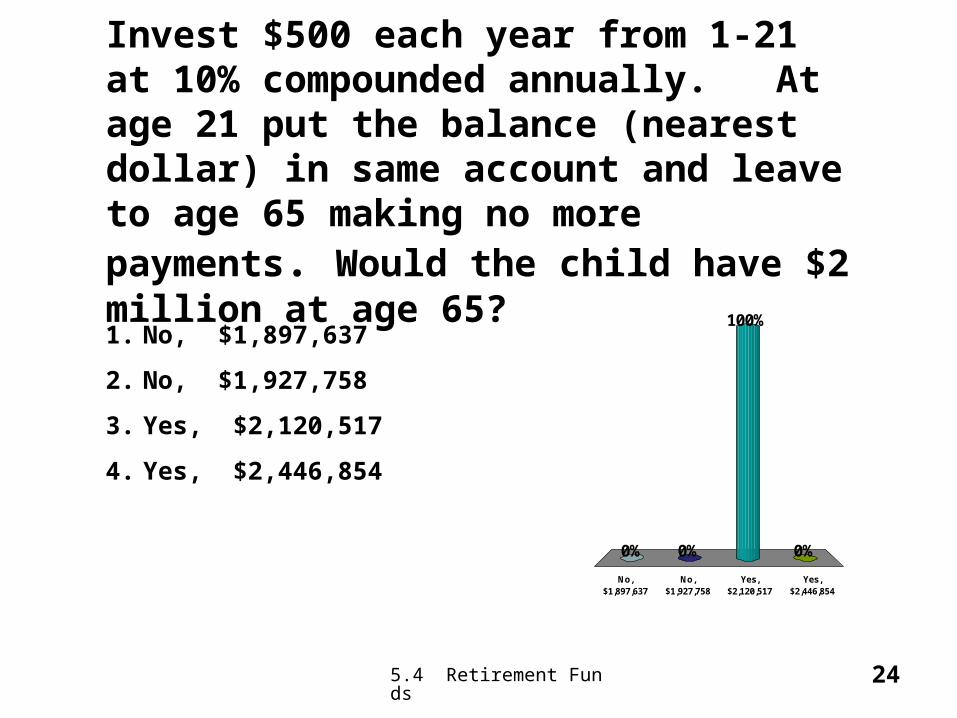

Invest $500 each year from 1-21 at 10% compounded annually. At age 21 put the balance (nearest dollar) in same account and leave to age 65 making no more payments. Would the child have $2 million at age 65?

No, $1,897,637

No, $1,927,758

Yes, $2,120,517

Yes, $2,446,854

0% 0%

100%

0%

1. No, $1,897,637

2. No, $1,927,758

3. Yes, $2,120,517

4. Yes, $2,446,854

5.4 Retirement Funds

25

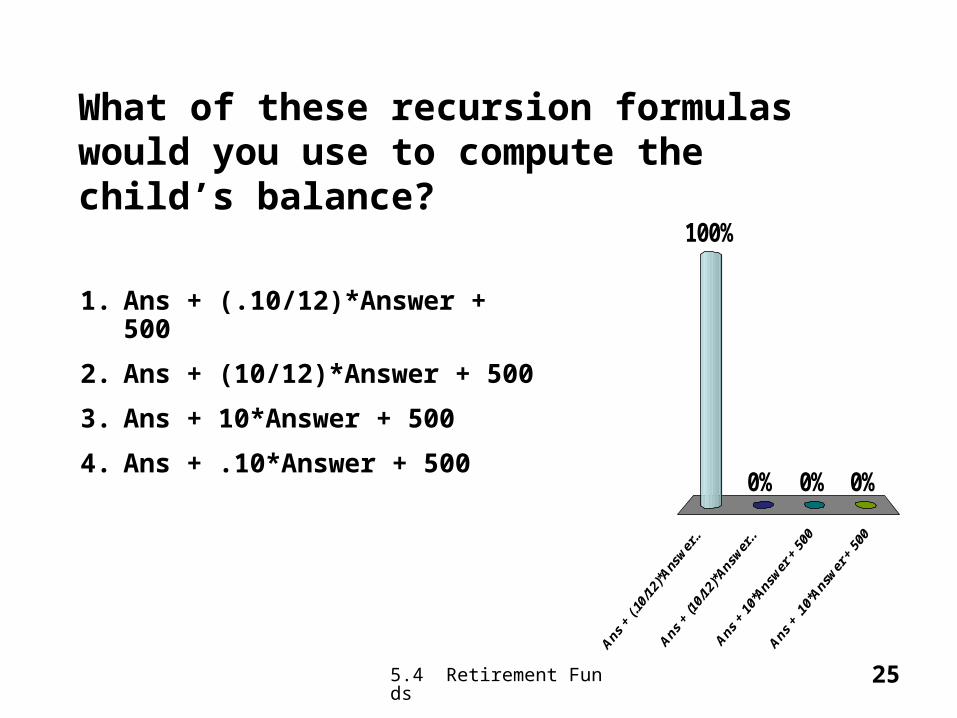

What of these recursion formulas would you use to compute the child’s balance?

100%

0%0%0%

1. Ans + (.10/12)*Answer + 500

2. Ans + (10/12)*Answer + 500

3. Ans + 10*Answer + 500

4. Ans + .10*Answer + 500

5.4 Retirement Funds

26

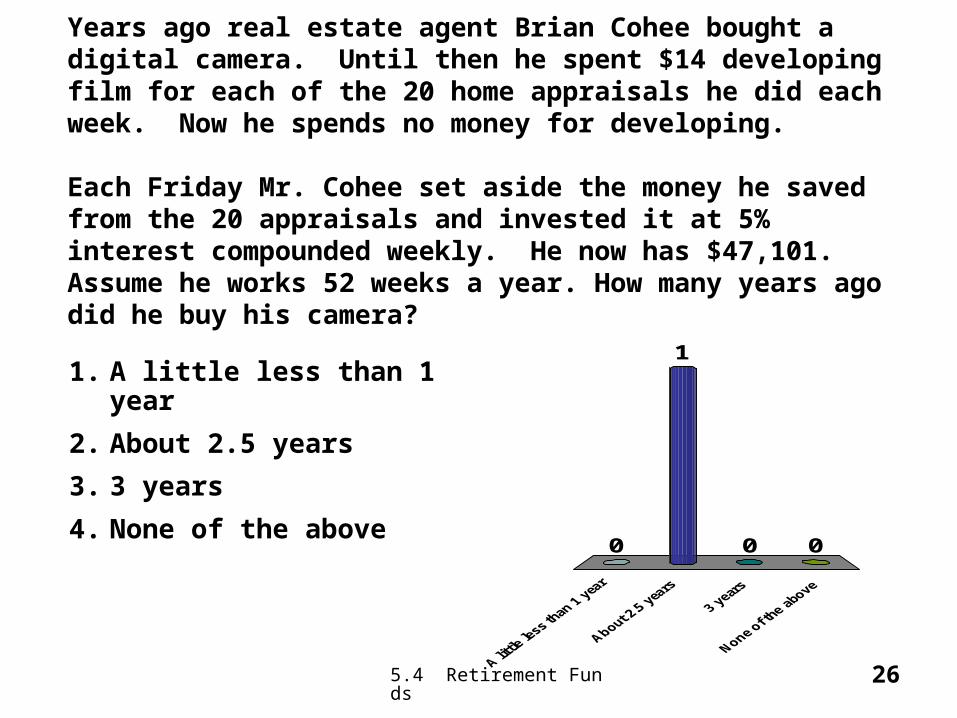

Years ago real estate agent Brian Cohee bought a digital camera. Until then he spent $14 developing film for each of the 20 home appraisals he did each week. Now he spends no money for developing.

Each Friday Mr. Cohee set aside the money he saved from the 20 appraisals and invested it at 5% interest compounded weekly. He now has $47,101. Assume he works 52 weeks a year. How many years ago did he buy his camera?

0 00

11. A little less than 1

year

2. About 2.5 years

3. 3 years

4. None of the above

5.4 Retirement Funds

2727

End of 5.5

5.4 Retirement Funds

2828

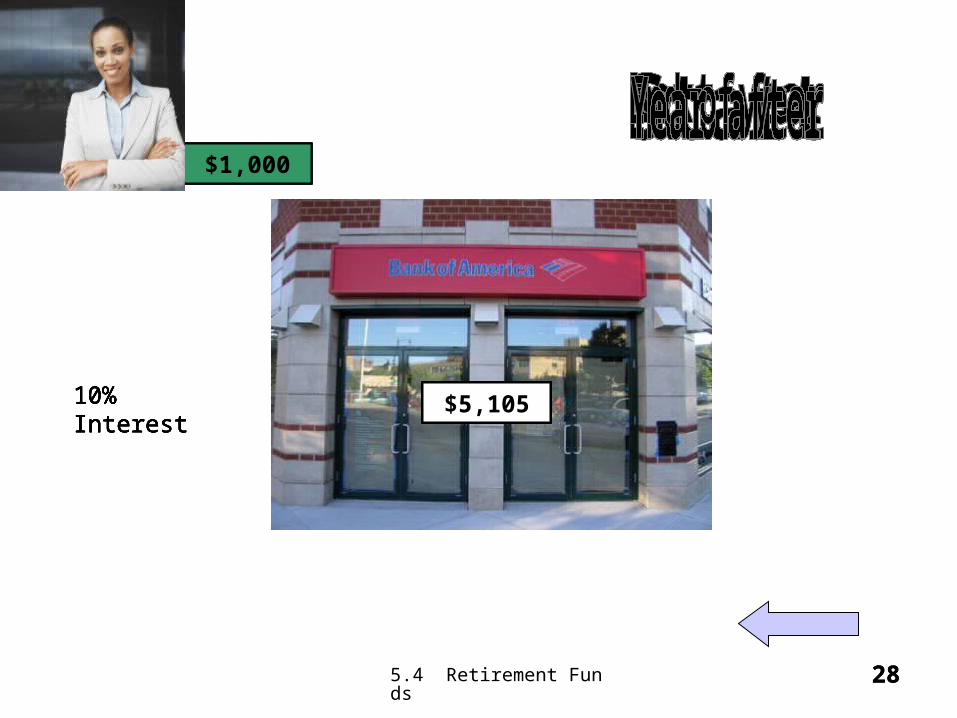

$0$1,100$2,100$1,000$2,310$3,310$3,641$4,641$5,105

$1,000$1,000$1,000$1,000

10% Interest10% Interest10% Interest10% Interest10% Interest

5.4 Retirement Funds

29

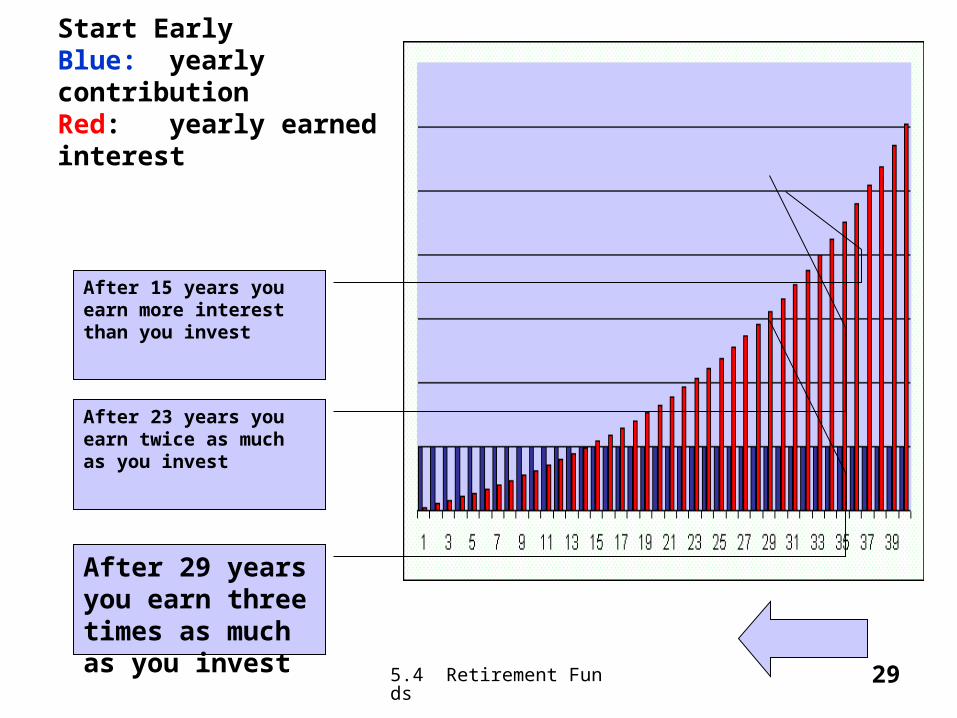

Start Early Blue: yearly contributionRed: yearly earned interest

After 29 years you earn three times as much as you invest

After 23 years you earn twice as much as you invest

After 15 years you earn more interest than you invest

5.4 Retirement Funds

3030

Meta-Material