Embed Size (px)

Citation preview

OLD MUTUAL RETIREMENT FUNDS SURVEY 2010

OLD MUTUAL RETIREMENT MONITOR 2010

RETIREMENT FUNDS SURVEY 2010

Agenda: Old Mutual Retirement Funds Survey 2010

Survey objectives

Research method

Key highlights

Key trends Key trends & factors shaping the Retirement Fund industry

How will Service Providers have to change in the future?

Response of the industry to environmental changes

Key findings Umbrella Funds

Member Communication

Shifting Investment Strategies

Preservation in a changing environment

Adequacy of retirement benefits

Member perception of Trustees

Impact of legislation and views on Retirement Fund Reform

Panel Q&A

4

Survey Objectives

Understand changes in the retirement fund industry

Evaluate retirement fund investment

Gauge attitudes and needs with regard to preservation

Assess adequacy of benefits

Establish levels of confidence and trust in trustees

Evaluate Fund Governance

Establish industry views on Umbrella funds

Examine communication to members

5

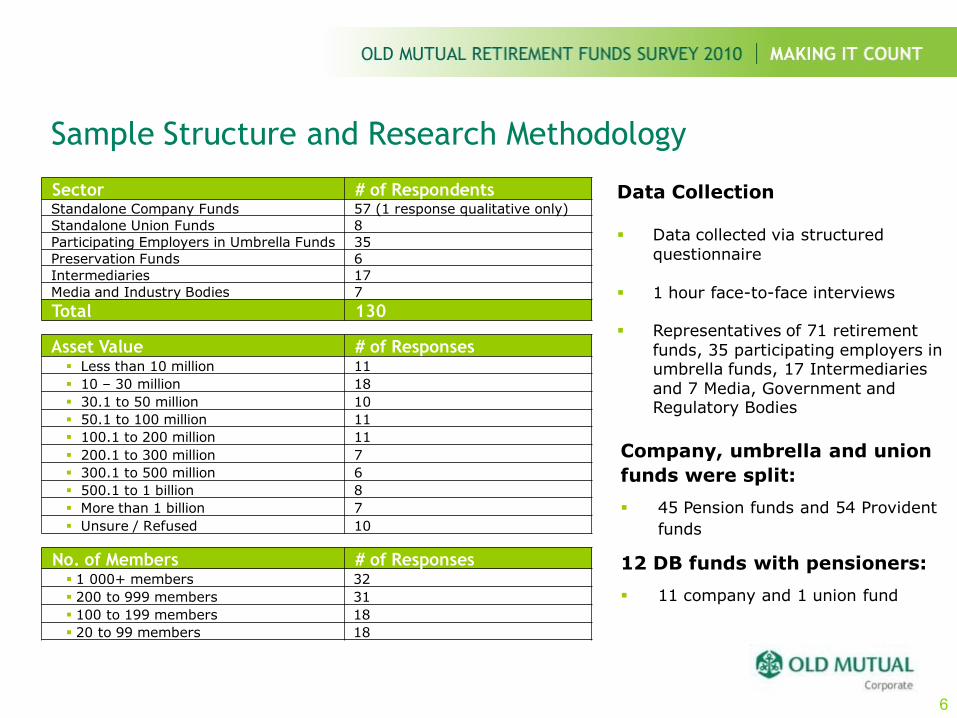

Sample Structure and Research Methodology

Data Collection

Data collected via structured

questionnaire

1 hour face-to-face interviews

Representatives of 71 retirement

funds, 35 participating employers in umbrella funds, 17 Intermediaries

and 7 Media, Government and Regulatory Bodies

Company, umbrella and union

funds were split:

45 Pension funds and 54 Provident

funds

12 DB funds with pensioners:

11 company and 1 union fund

Sector # of RespondentsStandalone Company Funds 57 (1 response qualitative only)

Standalone Union Funds 8

Participating Employers in Umbrella Funds 35

Preservation Funds 6

Intermediaries 17

Media and Industry Bodies 7

Total 130

Asset Value # of Responses Less than 10 million 11

10 – 30 million 18

30.1 to 50 million 10

50.1 to 100 million 11

100.1 to 200 million 11

200.1 to 300 million 7

300.1 to 500 million 6

500.1 to 1 billion 8

More than 1 billion 7

Unsure / Refused 10

No. of Members # of Responses 1 000+ members 32

200 to 999 members 31

100 to 199 members 18

20 to 99 members 18

6

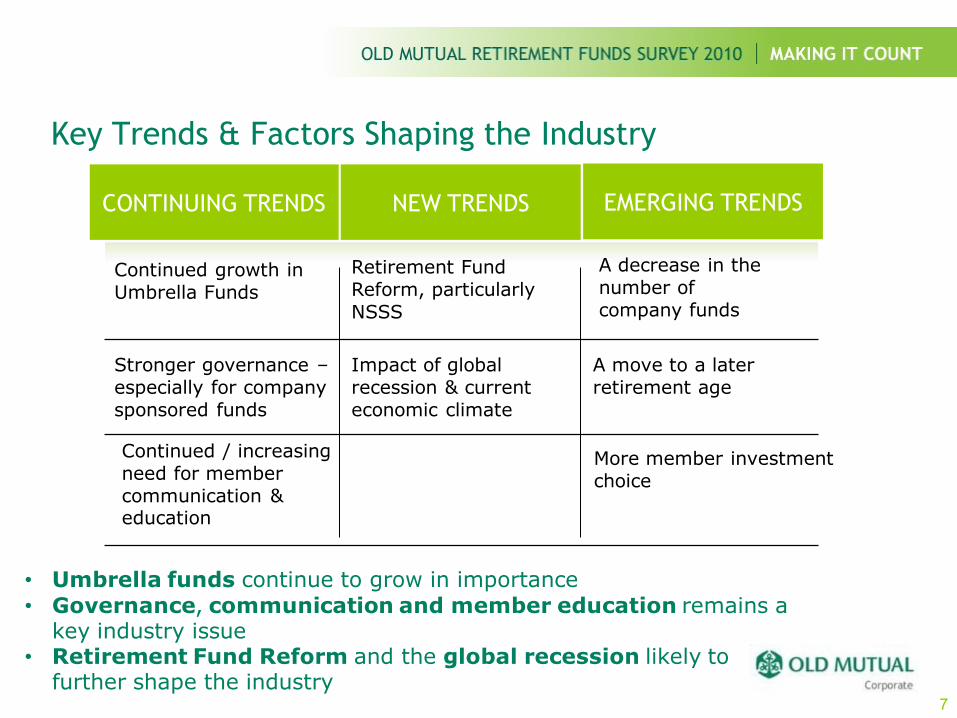

Key Trends & Factors Shaping the Industry

Continued / increasing need for member

communication & education

More member investment choice

CONTINUING TRENDS NEW TRENDS EMERGING TRENDS

Continued growth in Umbrella Funds

Retirement Fund Reform, particularly

NSSS

A decrease in the

number of company funds

Stronger governance –

especially for company sponsored funds

Impact of global

recession & current economic climate

A move to a later

retirement age

• Umbrella funds continue to grow in importance• Governance, communication and member education remains a

key industry issue• Retirement Fund Reform and the global recession likely to

further shape the industry7

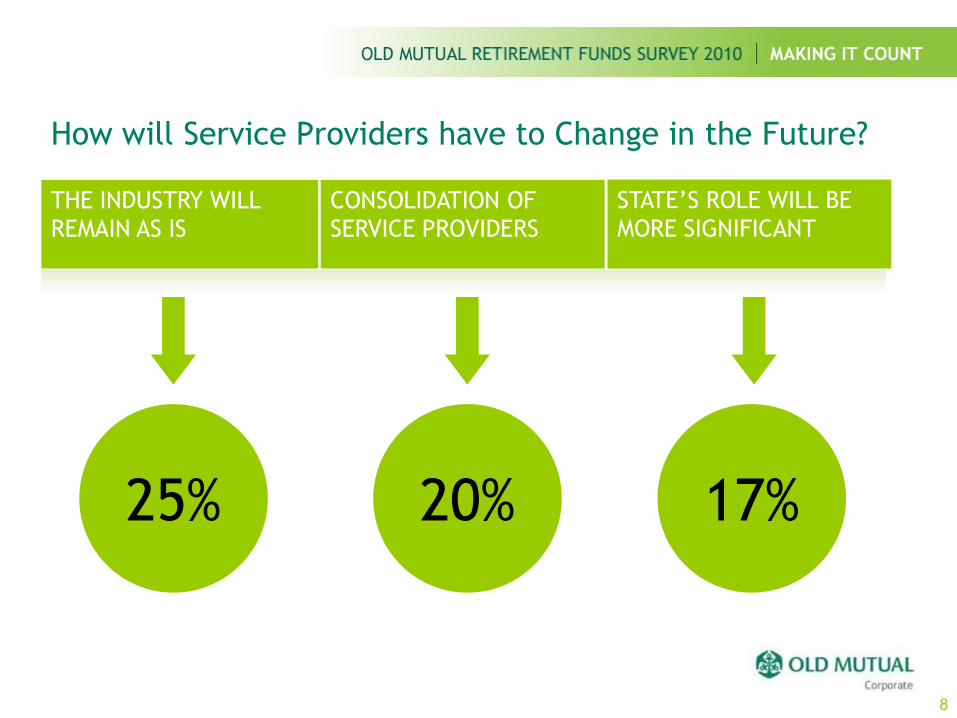

How will Service Providers have to Change in the Future?

25% 20% 17%

THE INDUSTRY WILL

REMAIN AS IS

CONSOLIDATION OF

SERVICE PROVIDERS

STATE’S ROLE WILL BE

MORE SIGNIFICANT

8

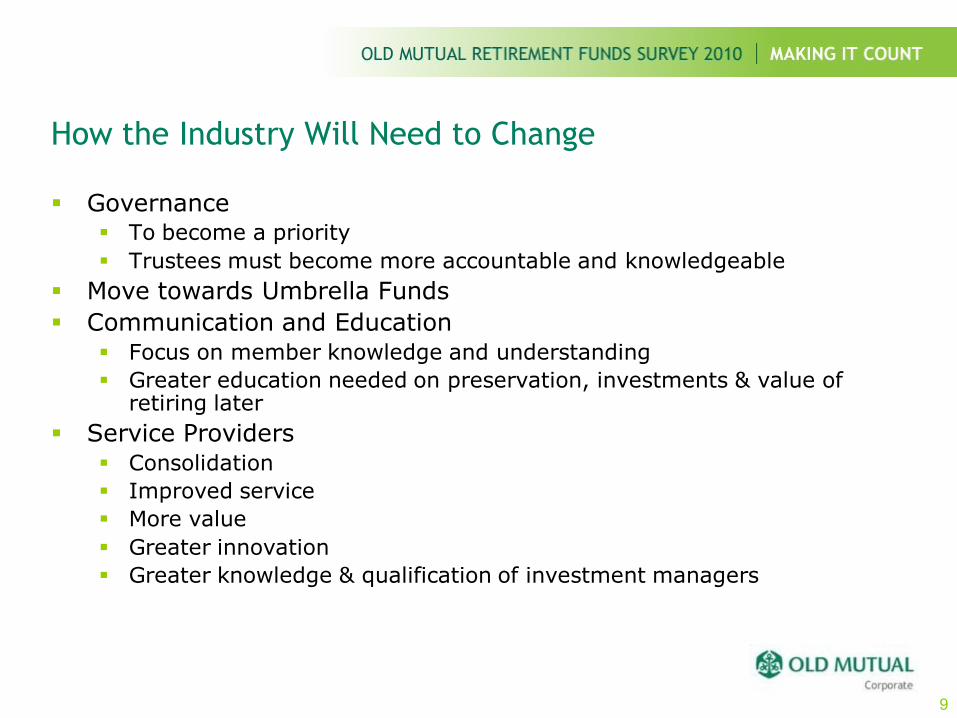

How the Industry Will Need to Change

Governance To become a priority

Trustees must become more accountable and knowledgeable

Move towards Umbrella Funds

Communication and Education Focus on member knowledge and understanding

Greater education needed on preservation, investments & value of retiring later

Service Providers Consolidation

Improved service

More value

Greater innovation

Greater knowledge & qualification of investment managers

9

Views on Retirement Reform

National Social Security Scheme [NSSS]

Number of respondents aware of the issues tabled:

Company funds: 52%

Umbrella Fund participating employers: 34%

Mixed feelings around NSSS

Exception of Unions: where 63% are positive

50% of Union funds think their funds will shrink/disappear with NSSS

Perceived benefits of NSSS:

All South Africans will be covered

Higher levels of saving

Compulsory preservation continues to receive strong support

Low levels of awareness and mixed feelings about the NSSS

11

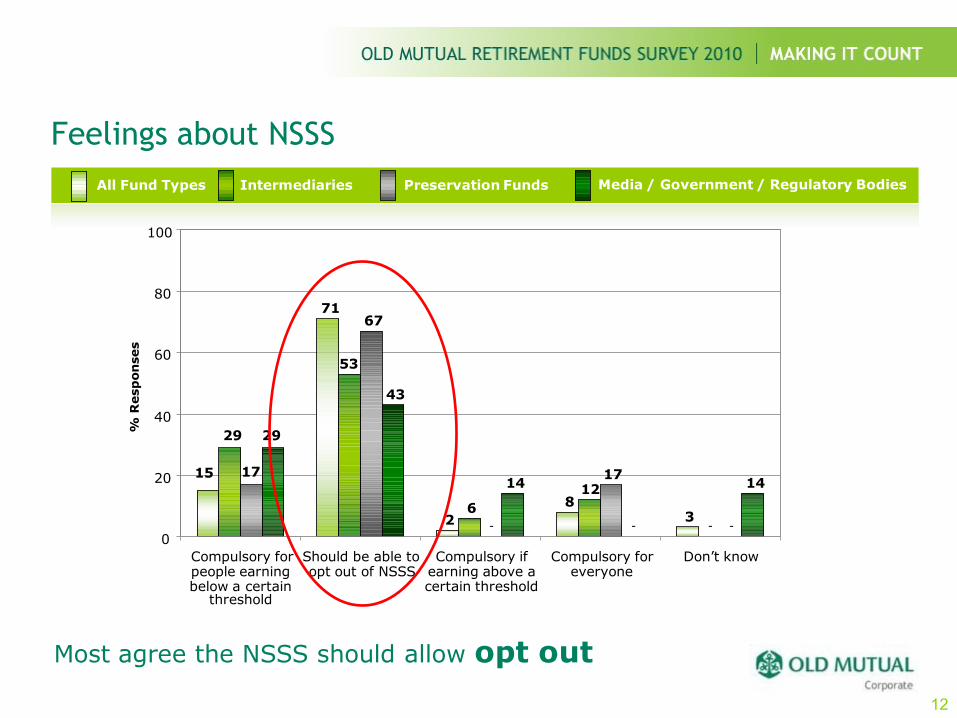

Feelings about NSSS

All Fund Types Intermediaries Preservation Funds Media / Government / Regulatory Bodies

15

71

2

83

29

53

6

12

17

67

17

29

43

14 14

- -- -

0

20

40

60

80

100

Compulsory forpeople earningbelow a certain

threshold

Should be able toopt out of NSSS

Compulsory ifearning above acertain threshold

Compulsory foreveryone

Don‟t know

% R

esp

on

ses

Most agree the NSSS should allow opt out

12

Major concerns raised about the NSSS

Concerns about ability to

Implement

Manage effectively

Fear of

Low returns

Possible corruption

13

Shifting Investment Strategies

-20

to

-2

4

-15

to

-1

9

-10

to

-1

4

20

to

29

31

74

2

10 96 9

11 1 2 35 4

2419

75

1

28

-

18

1

27

9

3122

813

105

0

20

40

60

-5 t

o -

9

-1 t

o -

4 0

1 t

o 4

5 t

o 9

10

to

14

15

to

19

30

+

Do

n’t

kn

ow

% R

esp

on

ses

2008

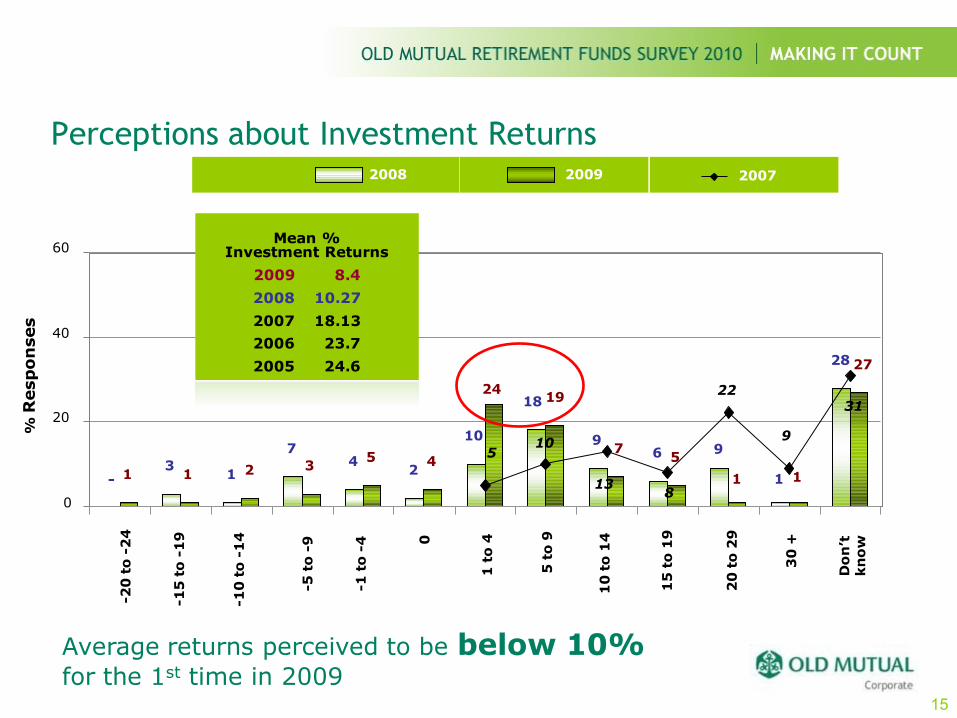

Perceptions about Investment Returns2009 2007

Mean % Investment Returns

2009 8.4

2008 10.27

2007 18.13

2006 23.7

2005 24.6

Average returns perceived to be below 10%for the 1st time in 2009

15

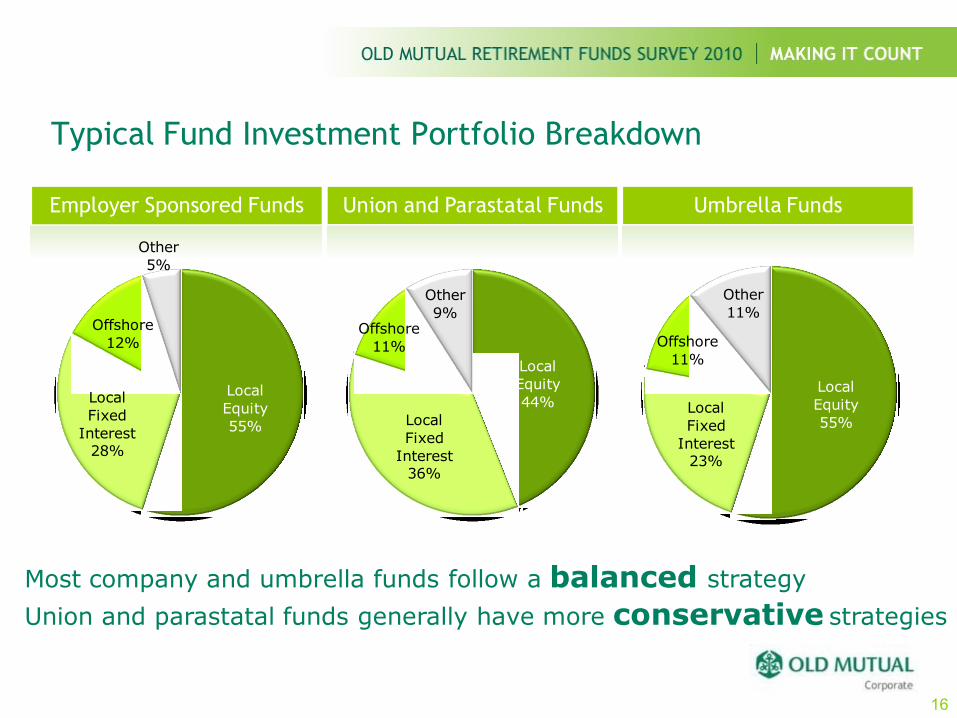

Typical Fund Investment Portfolio Breakdown

Union and parastatal funds generally have more conservative strategies

Union and Parastatal Funds

Most company and umbrella funds follow a balanced strategy

Local

Equity

55%

Local

Fixed

Interest 28%

Offshore

12%

Other

5%

Local

Equity

44%

Local

Fixed

Interest 36%

Offshore

11%

Other

9%

Local

Equity

55%Local

Fixed

Interest 23%

Offshore

11%

Other

11%

Employer Sponsored Funds Umbrella Funds

16

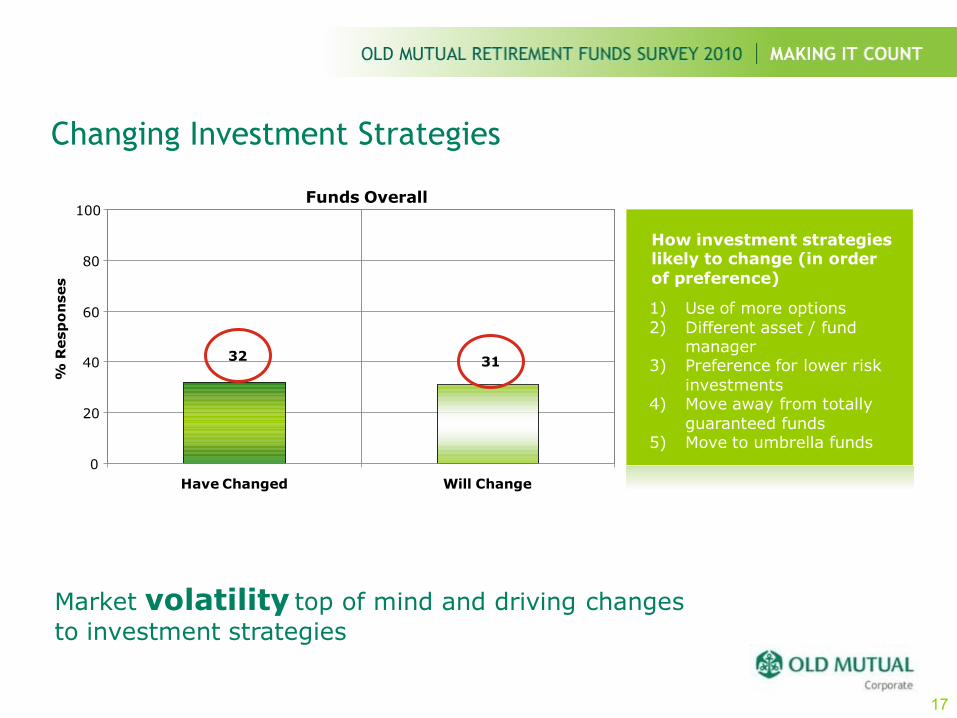

Changing Investment Strategies

3132

0

20

40

60

80

100

Have Changed Will Change

% R

esp

on

ses

1) Use of more options

2) Different asset / fund manager

3) Preference for lower risk

investments4) Move away from totally

guaranteed funds5) Move to umbrella funds

How investment strategies likely to change (in order

of preference)

Funds Overall

Market volatility top of mind and driving changes

to investment strategies

17

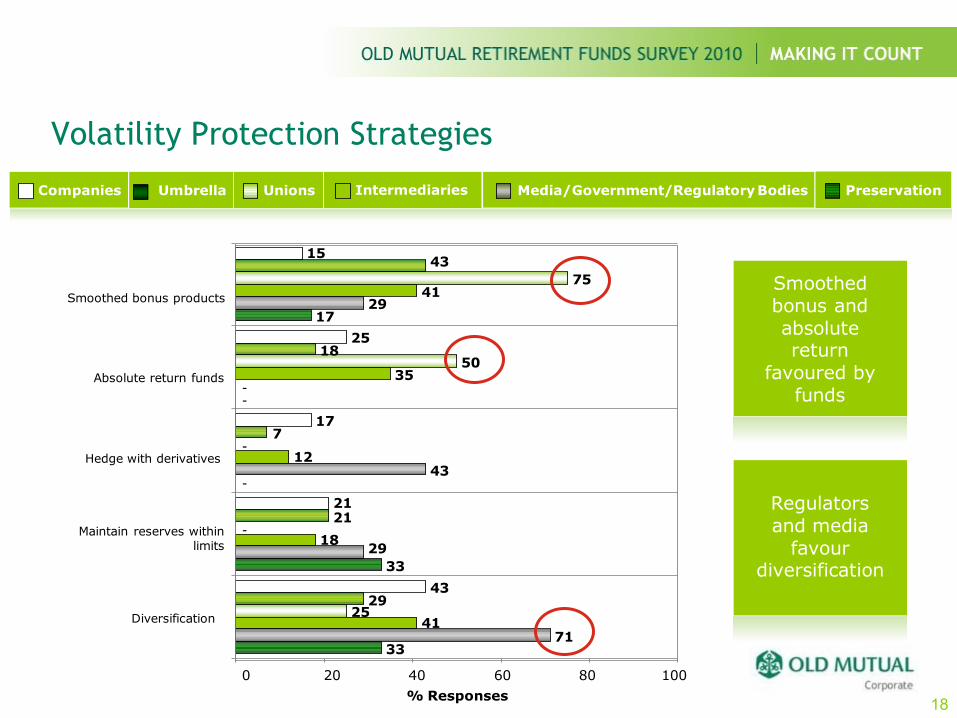

IntermediariesCompanies Umbrella Unions Media/Government/Regulatory Bodies Preservation

Volatility Protection Strategies

15

25

17

21

43

43

18

7

21

29

75

50

25

41

35

12

18

41

29

43

29

71

17

33

33

-

-

-

-

-

Smoothed bonus and

absolute return

favoured by funds

0 20 40 60 80 100

Smoothed bonus products

Absolute return funds

Hedge with derivatives

Maintain reserves withinlimits

Diversification

% Responses

Regulators

and media favour

diversification

18

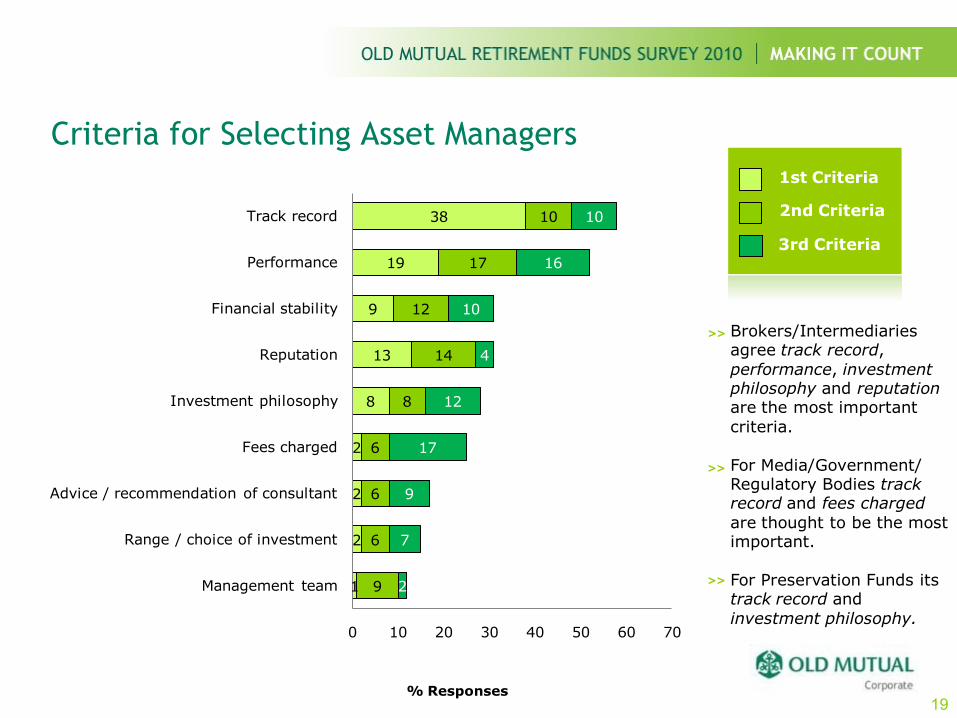

Criteria for Selecting Asset Managers

Brokers/Intermediaries agree track record,

performance, investment philosophy and reputationare the most important

criteria.

For Media/Government/Regulatory Bodies track record and fees charged

are thought to be the most important.

For Preservation Funds its track record and

investment philosophy.

>>

>>

>>

19

1

2

2

2

8

13

9

19

38

9

6

6

6

8

14

12

17

10

2

7

9

17

12

4

10

16

10

0 10 20 30 40 50 60 70

Management team

Range / choice of investment

Advice / recommendation of consultant

Fees charged

Investment philosophy

Reputation

Financial stability

Performance

Track record

1st Criteria

2nd Criteria

3rd Criteria

% Responses

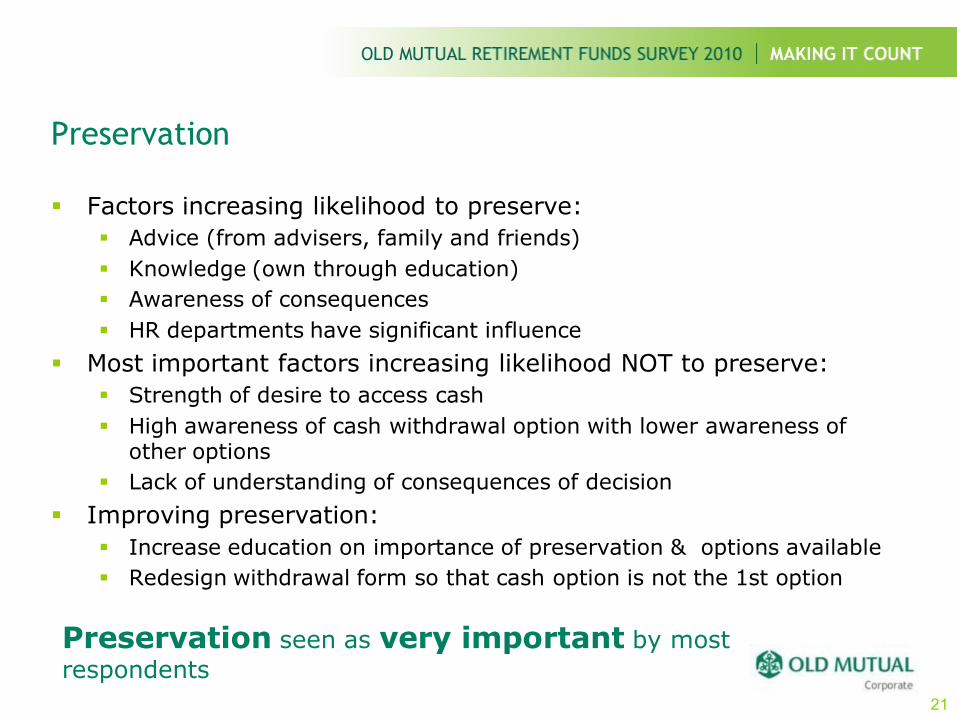

Preservation in a Changing Environment

Preservation

Factors increasing likelihood to preserve:

Advice (from advisers, family and friends)

Knowledge (own through education)

Awareness of consequences

HR departments have significant influence

Most important factors increasing likelihood NOT to preserve:

Strength of desire to access cash

High awareness of cash withdrawal option with lower awareness of other options

Lack of understanding of consequences of decision

Improving preservation:

Increase education on importance of preservation & options available

Redesign withdrawal form so that cash option is not the 1st option

Preservation seen as very important by most

respondents

21

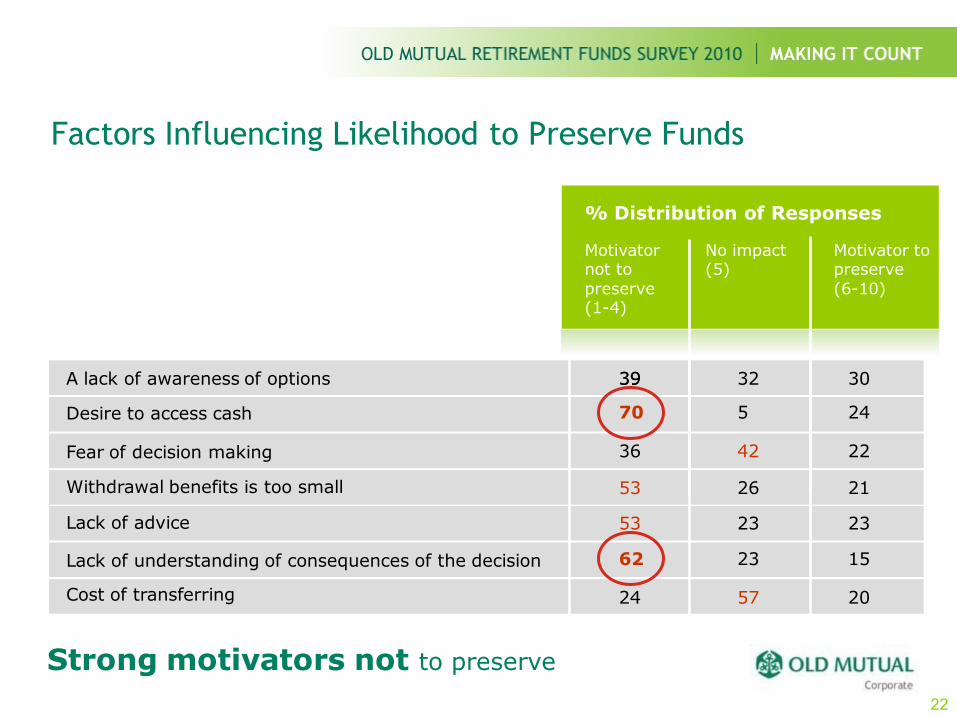

Factors Influencing Likelihood to Preserve Funds

% Distribution of Responses

Motivator not to

preserve(1-4)

No impact(5)

Motivator to preserve

(6-10)

A lack of awareness of options

Desire to access cash

Fear of decision making

Withdrawal benefits is too small

Lack of advice

Lack of understanding of consequences of the decision

Cost of transferring

3939 32 30

70 5 24

36 42 22

53 26 21

53 23 23

62 23 15

24 57 20

Strong motivators not to preserve

22

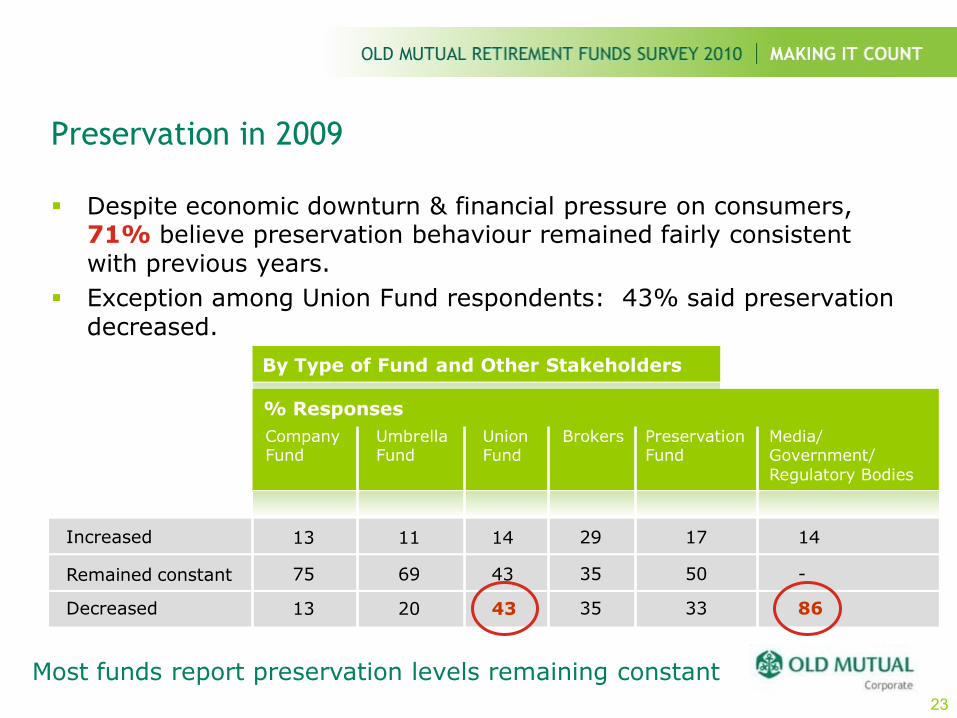

Preservation in 2009

Despite economic downturn & financial pressure on consumers, 71% believe preservation behaviour remained fairly consistent with previous years.

Exception among Union Fund respondents: 43% said preservation decreased.

By Type of Fund and Other Stakeholders

Increased

% Responses

CompanyFund

UmbrellaFund

UnionFund

Brokers PreservationFund

Media/Government/

Regulatory Bodies

Remained constant

Decreased

13 11 14 29 17 14

75 69 43 35 50 -

13 20 43 35 33 86

Most funds report preservation levels remaining constant

23

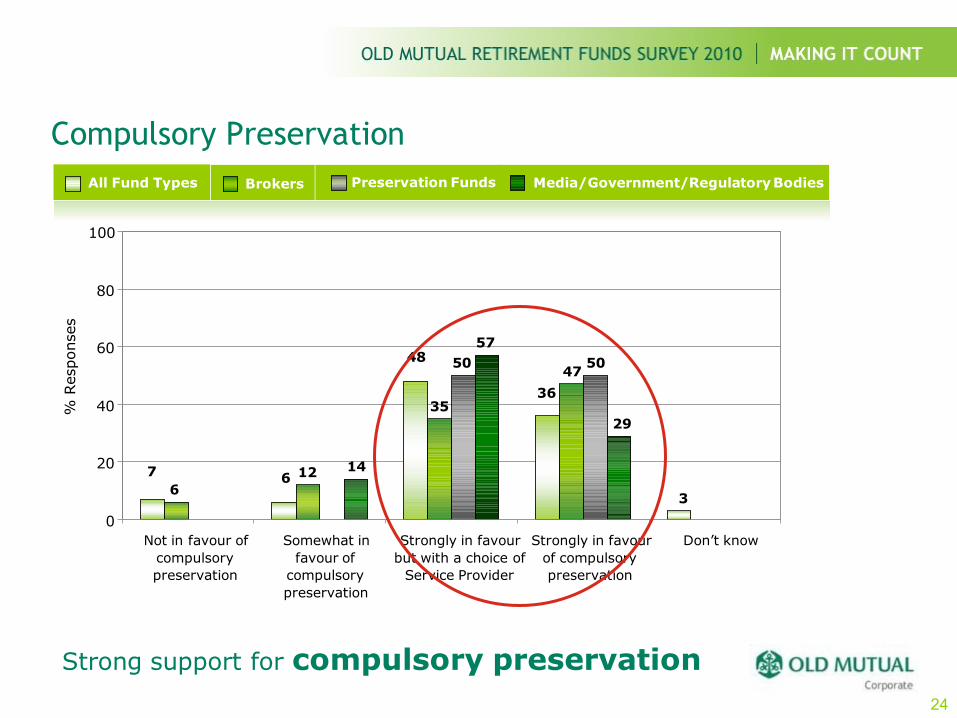

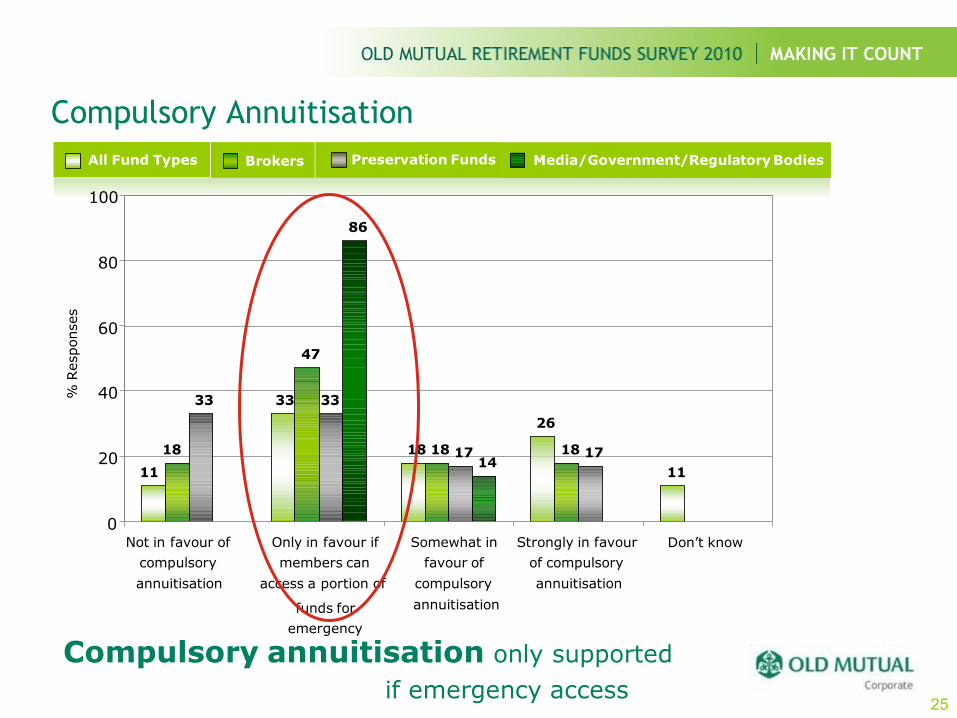

Compulsory Preservation

36

12

35

4750 50

14

57

29

7 6

48

36

0

20

40

60

80

100

Not in favour of

compulsory

preservation

Somewhat in

favour of

compulsory

preservation

Strongly in favour

but with a choice of

Service Provider

Strongly in favour

of compulsory

preservation

Don‟t know

% R

esponses

Preservation FundsBrokersAll Fund Types Media/Government/Regulatory Bodies

Strong support for compulsory preservation

24

11

33

18

26

11

18

47

18 18

33 33

17 17

86

14

0

20

40

60

80

100

% R

esponses

Compulsory Annuitisation

Preservation FundsBrokersAll Fund Types Media/Government/Regulatory Bodies

Not in favour of

compulsory

annuitisation

Only in favour if

members can

access a portion of

funds for

emergency

Somewhat in

favour of

compulsory

annuitisation

Strongly in favour

of compulsory

annuitisation

Don‟t know

Compulsory annuitisation only supported

if emergency access25

Adequacy of Retirement Benefits

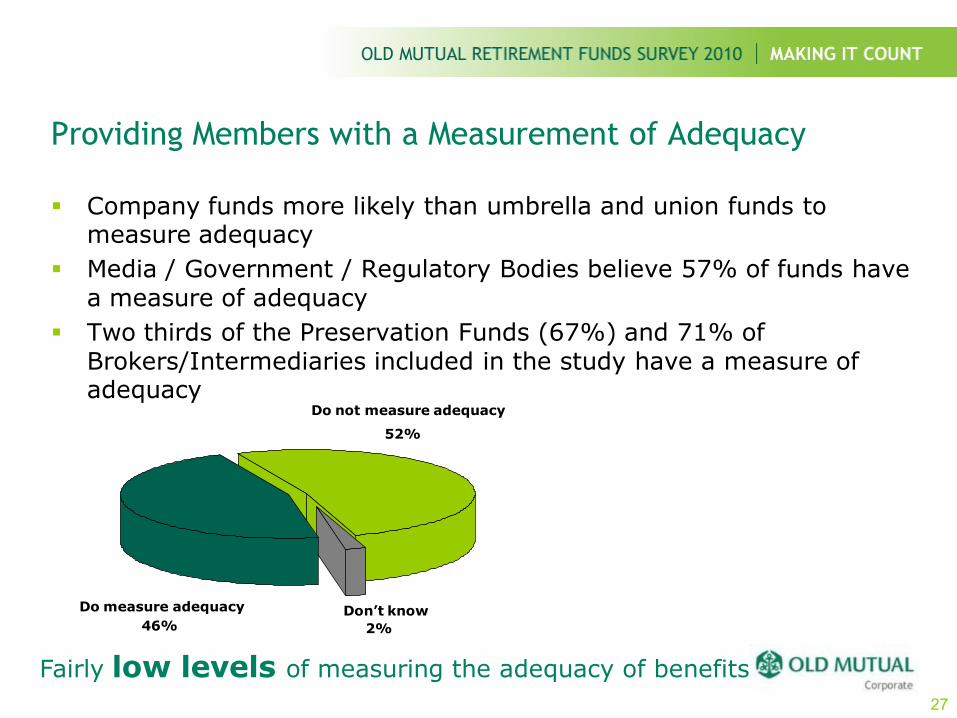

Providing Members with a Measurement of Adequacy

Company funds more likely than umbrella and union funds to measure adequacy

Media / Government / Regulatory Bodies believe 57% of funds have a measure of adequacy

Two thirds of the Preservation Funds (67%) and 71% of Brokers/Intermediaries included in the study have a measure of adequacy

Do not measure adequacy

52%

46%Don’t know

2%

Do measure adequacy

Fairly low levels of measuring the adequacy of benefits

27

Adequacy of Benefits

43% of respondents believe members think they have enough money to retire

Respondents believe benefits are actually enough only 26% of the time

% of salary at retirement most common measure of adequacy

70 – 79% of final salary (73% average) seen asadequate benefit

Companies & unions seeing more members retiring before 65 –main reasons given relate to needing a slower lifestyle & starting their own business

Generally low levels of adequacy of benefits

Discrepancy between members‟ perception of benefits and reality

28

Perception of Trustees

Perception of Trustees

Fund trustees/principal officers strongly believe members have confidence in the knowledge & abilities of trustees

Intermediaries, the Media, Industry bodies and Umbrella Funds less positive regarding member perceptions of trustees

76% of fund respondents agree the additional costs to ensure good governance are beneficial (55% in 2008)

30

Governance remains in important topic

Member Level Investment Choice

Member Level Investment Choice [MLIC]

MLIC becoming more popular: More Company funds introduced MLIC in 2009 (12% on 2008)

1/3 of respondents introduced choice in last year

Another 10% intend to introduce choice in next year

But number of different choices offered to members not seen to increase significantly in the next 3-5 years

Default option remains the most popular option: 68% of members in all types of funds

% Umbrella fund members using default option has decreased from 80% to 66%

Most popular choices: Company funds - Balanced, multi-manager and life-stage mandates

Umbrella funds - Fully guaranteed, money market and life-stage mandates

Life stage mandates look to become more popular investment choice in Company funds in next 12 months

Rising levels of MLIC despite most members

choosing the default 32

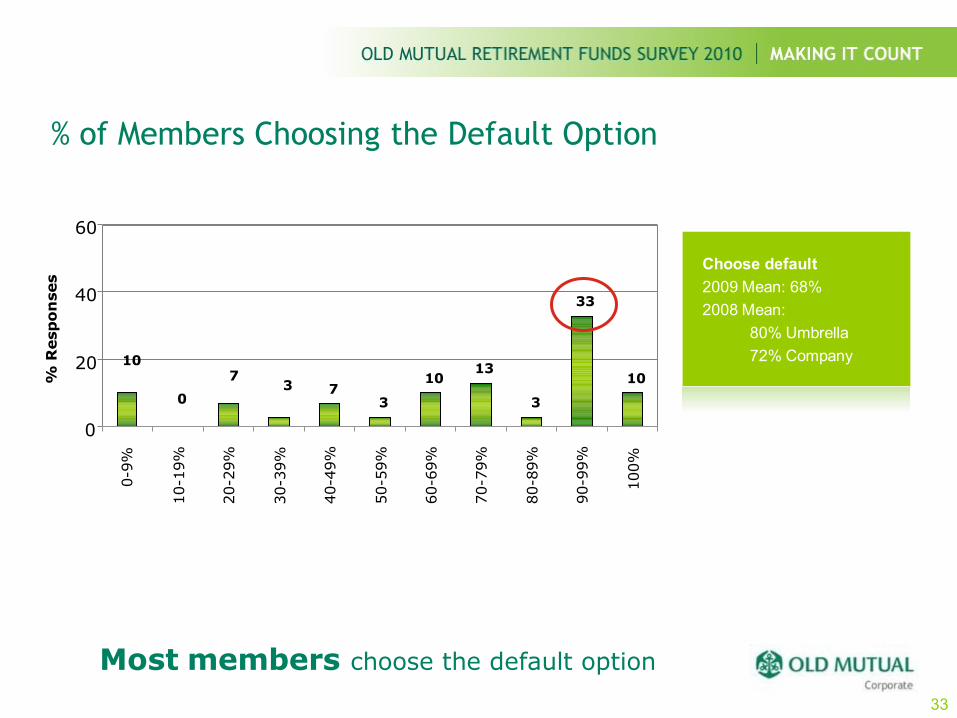

% of Members Choosing the Default Option

Choose default

2009 Mean: 68%

2008 Mean:

80% Umbrella

72% Company

73

1013

3

33

103

7

0

10

0

20

40

60

0-9

%

10-1

9%

20-2

9%

30-3

9%

40-4

9%

50-5

9%

60-6

9%

70-7

9%

80-8

9%

90-9

9%

100%

% R

esp

on

ses

Most members choose the default option

33

Umbrella Funds

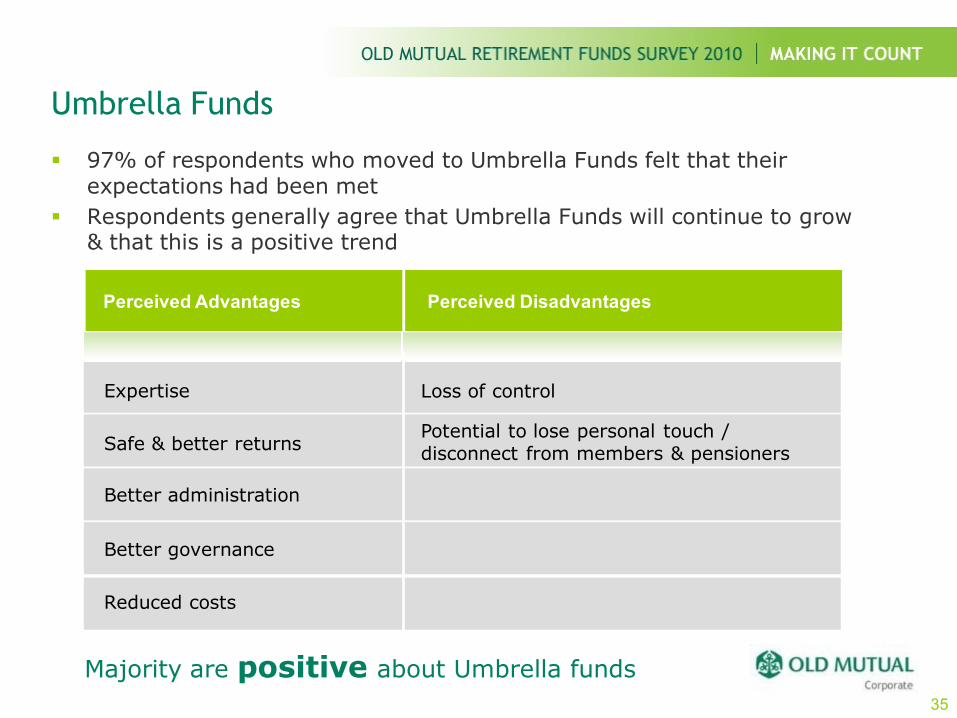

Umbrella Funds

97% of respondents who moved to Umbrella Funds felt that their expectations had been met

Respondents generally agree that Umbrella Funds will continue to grow & that this is a positive trend

Loss of control

Potential to lose personal touch / disconnect from members & pensioners

Perceived Advantages Perceived Disadvantages

Expertise

Safe & better returns

Better administration

Better governance

Reduced costs

Loss of control

Majority are positive about Umbrella funds

35

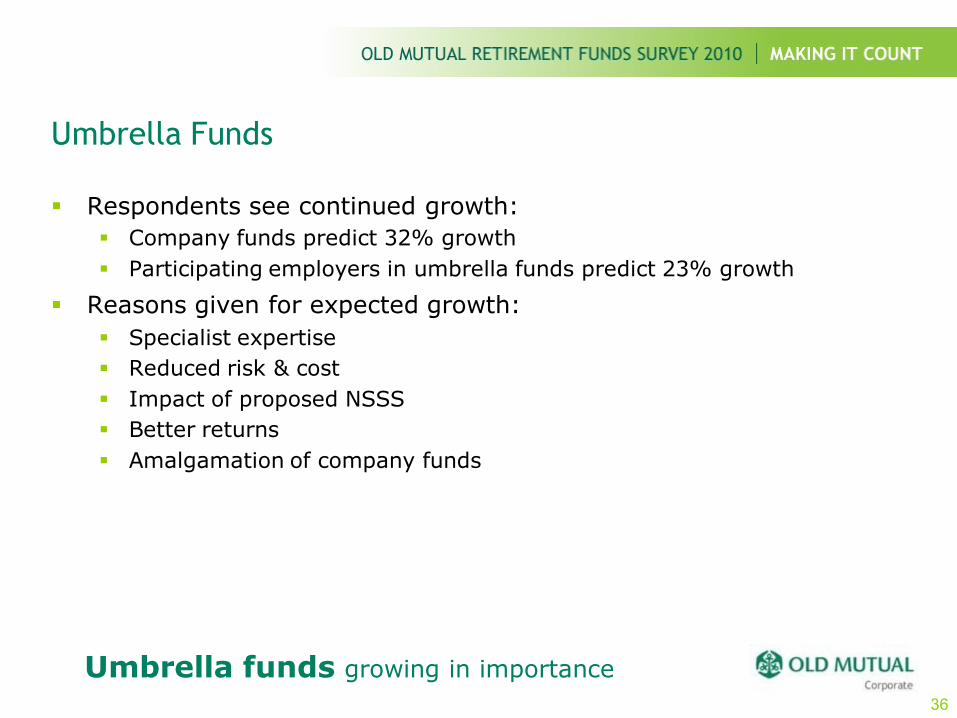

Umbrella Funds

Respondents see continued growth:

Company funds predict 32% growth

Participating employers in umbrella funds predict 23% growth

Reasons given for expected growth:

Specialist expertise

Reduced risk & cost

Impact of proposed NSSS

Better returns

Amalgamation of company funds

36

Umbrella funds growing in importance

Member Communication

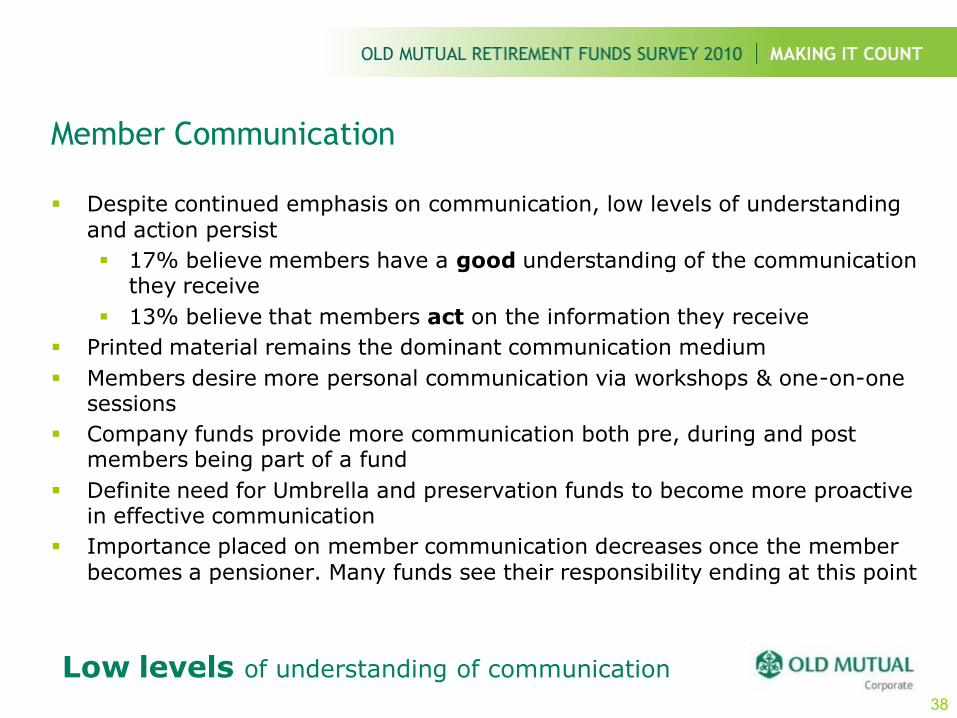

Member Communication

Despite continued emphasis on communication, low levels of understanding and action persist

17% believe members have a good understanding of the communication they receive

13% believe that members act on the information they receive

Printed material remains the dominant communication medium

Members desire more personal communication via workshops & one-on-one sessions

Company funds provide more communication both pre, during and post members being part of a fund

Definite need for Umbrella and preservation funds to become more proactive in effective communication

Importance placed on member communication decreases once the member becomes a pensioner. Many funds see their responsibility ending at this point

Low levels of understanding of communication

38

Member Communication

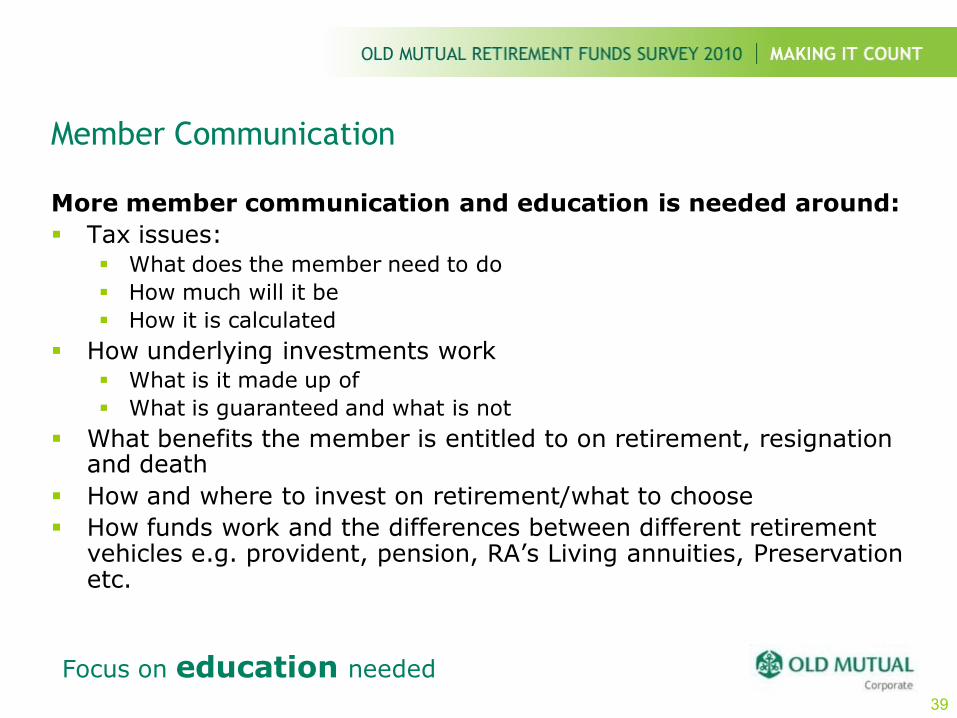

More member communication and education is needed around:

Tax issues: What does the member need to do

How much will it be

How it is calculated

How underlying investments work What is it made up of

What is guaranteed and what is not

What benefits the member is entitled to on retirement, resignation and death

How and where to invest on retirement/what to choose

How funds work and the differences between different retirement vehicles e.g. provident, pension, RA‟s Living annuities, Preservation etc.

Focus on education needed

39

RETIREMENT

MONITOR 2010

MAKING IT COUNT

Agenda:

Old Mutual Retirement Monitor 2010

Survey Purpose

Sample & Methodology

Retirement Fund Membership

Key Survey Findings Retirement Planning Confidence

Attitudes to Retirement

Anticipated Source of Retirement Funding

Attitudes to Trustees & Fund Administration

Member Level Investment Choice

Member Communication

Contribution Levels & Adequacy

Preservation

Panel Q&A

42

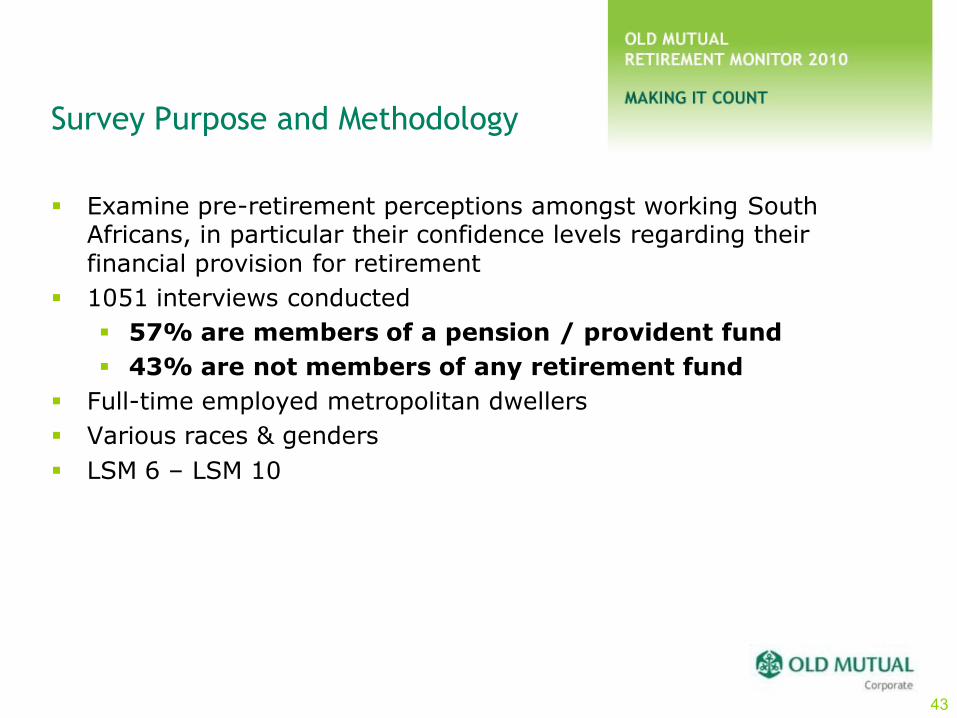

Survey Purpose and Methodology

Examine pre-retirement perceptions amongst working South Africans, in particular their confidence levels regarding their financial provision for retirement

1051 interviews conducted

57% are members of a pension / provident fund

43% are not members of any retirement fund

Full-time employed metropolitan dwellers

Various races & genders

LSM 6 – LSM 10

43

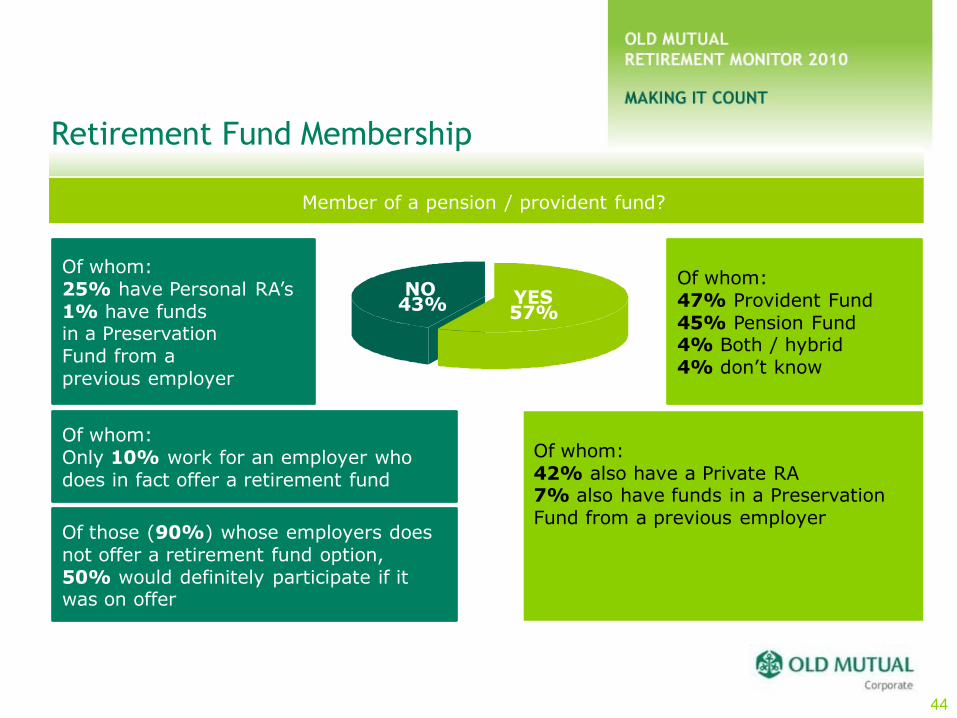

Retirement Fund Membership

Of whom:

42% also have a Private RA7% also have funds in a Preservation

Fund from a previous employer

Member of a pension / provident fund?

YES57%

NO43%

44

Of whom: 47% Provident Fund

45% Pension Fund4% Both / hybrid

4% don‟t know

Of whom:

25% have Personal RA‟s

1% have fundsin a Preservation

Fund from a

previous employer

Of whom:

Only 10% work for an employer who

does in fact offer a retirement fund

Of those (90%) whose employers does

not offer a retirement fund option,50% would definitely participate if it was on offer

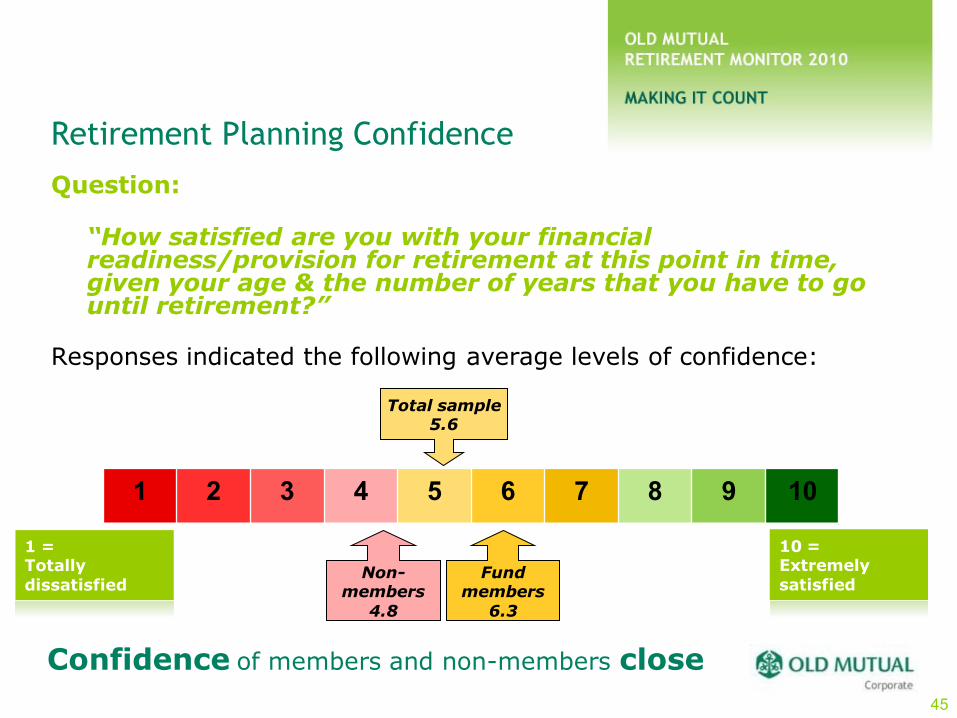

Retirement Planning Confidence

Question:

“How satisfied are you with your financial readiness/provision for retirement at this point in time, given your age & the number of years that you have to go until retirement?”

Responses indicated the following average levels of confidence:

Confidence of members and non-members close

45

1 2 3 4 5 6 7 8 9 10

Total sample5.6

Fundmembers

6.3

1 =Totally

dissatisfied

10 =Extremely

satisfiedNon-

members

4.8

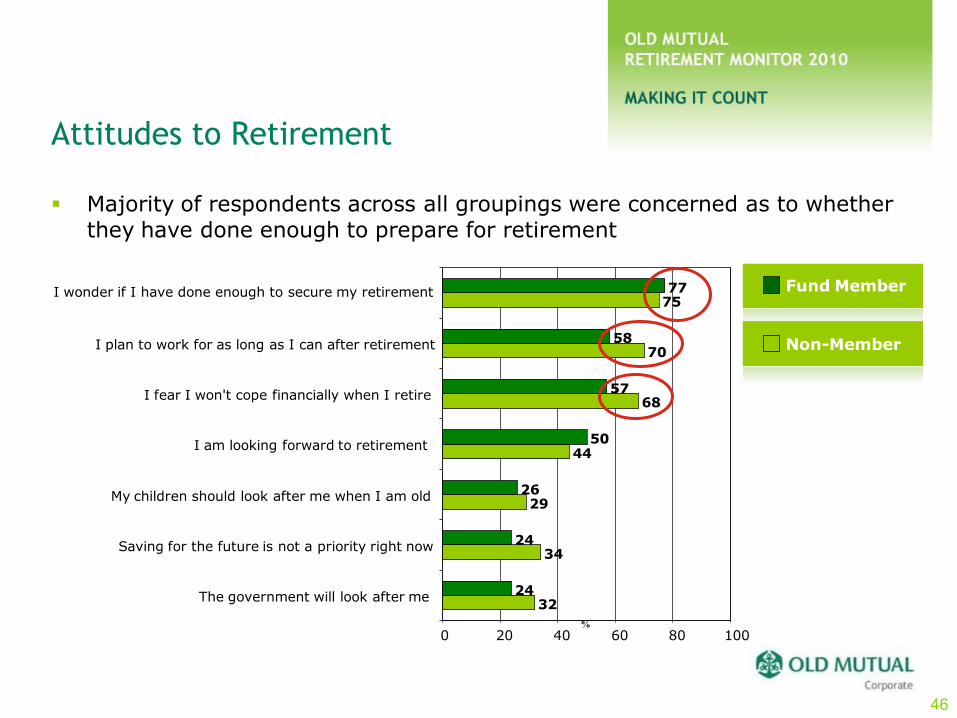

Attitudes to Retirement

Majority of respondents across all groupings were concerned as to whether they have done enough to prepare for retirement

32

34

29

44

68

70

75

24

24

26

50

57

58

77

0 20 40 60 80 100

The government will look after me

Saving for the future is not a priority right now

My children should look after me when I am old

I am looking forward to retirement

I fear I won't cope financially when I retire

I plan to work for as long as I can after retirement

I wonder if I have done enough to secure my retirement

%

Fund Member

Non-Member

46

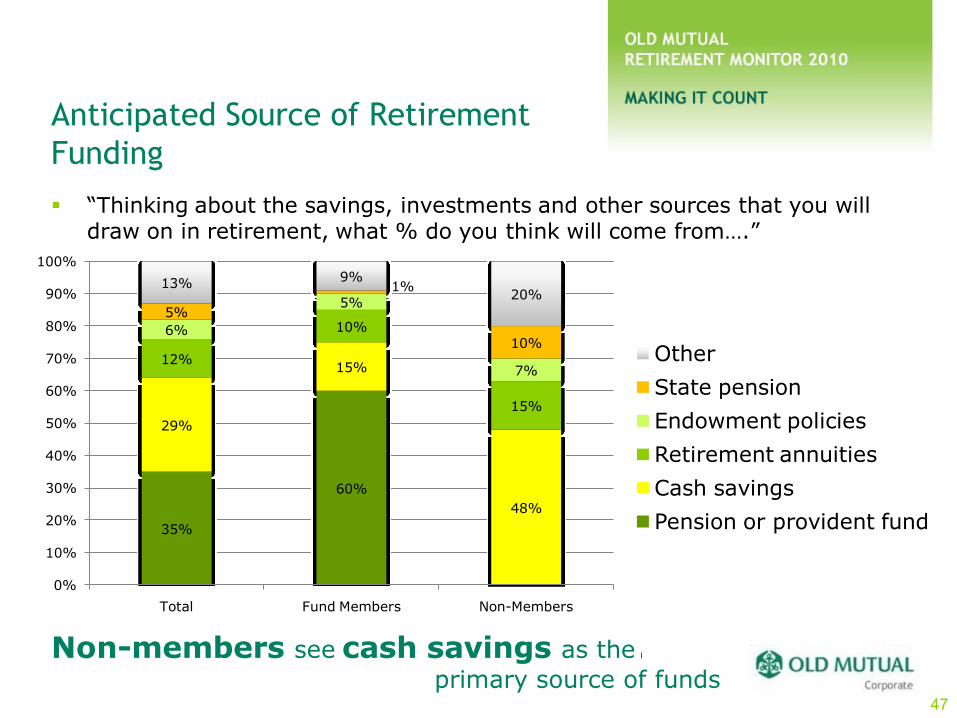

Anticipated Source of Retirement

Funding

“Thinking about the savings, investments and other sources that you will draw on in retirement, what % do you think will come from….”

Non-members see cash savings as the

primary source of funds47

35%

60%

29%

15%

48%

12%

10%

15%

6%

5%

7%

5%

10%

13% 9%

20%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Total Fund Members Non-Members

Other

State pension

Endowment policies

Retirement annuities

Cash savings

Pension or provident fund

1%

Low Levels of Engagement Among

Fund Members

Trustees

Investments

45% know whomanages the investment

55% don‟t know or are unsure who manages the investment of their retirement fund

18% vague

58% don‟t know wherethe assets are invested

24% claim good knowledge of where the assets of their retirement fund are invested

20% know trustees by name

50% don‟t know who the trustees of their retirement fund are

30% know the company they are from

85% did not vote

15% voted in the most recent election

48

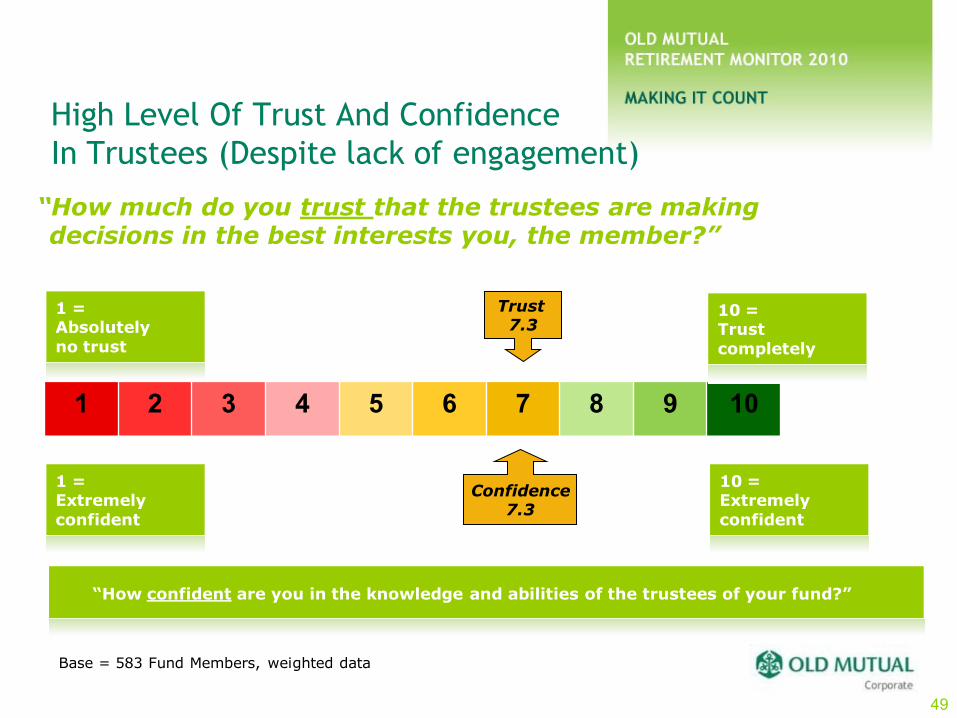

High Level Of Trust And Confidence

In Trustees (Despite lack of engagement)

“How much do you trust that the trustees are making decisions in the best interests you, the member?”

Base = 583 Fund Members, weighted data

1 2 3 4 5 6 7 8 9 10

Trust 7.3

Confidence7.3

1 =Extremely

confident

1 =Absolutely

no trust

10 =Trust

completely

10 =Extremely

confident

“How confident are you in the knowledge and abilities of the trustees of your fund?”

49

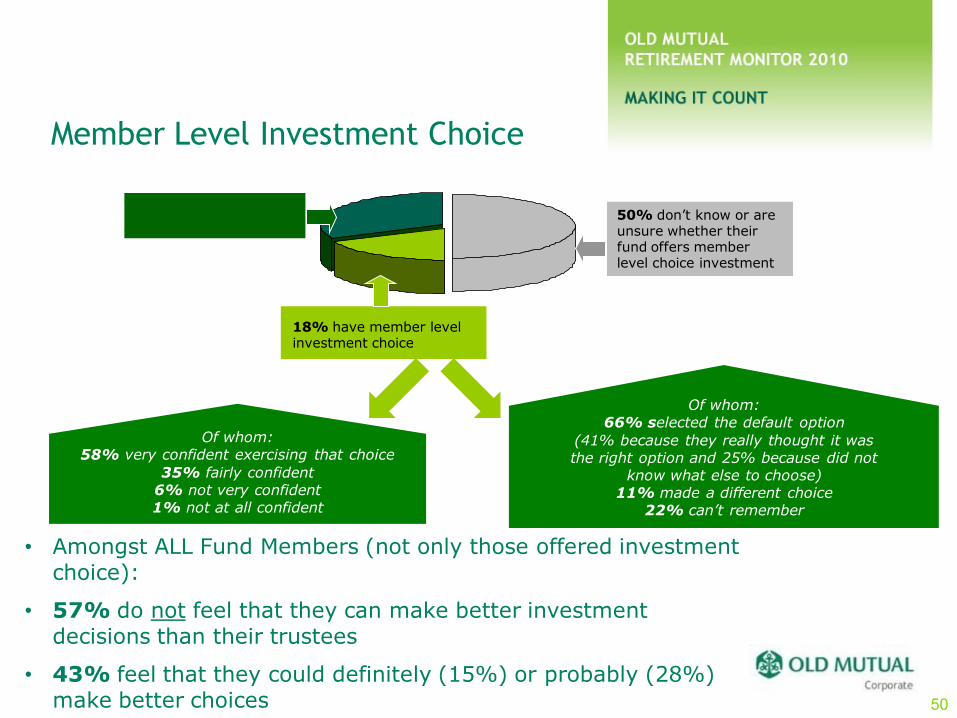

Member Level Investment Choice

Of whom: 58% very confident exercising that choice

35% fairly confident6% not very confident1% not at all confident

Of whom: 66% selected the default option

(41% because they really thought it wasthe right option and 25% because did not

know what else to choose)11% made a different choice

22% can’t remember

• Amongst ALL Fund Members (not only those offered investment choice):

• 57% do not feel that they can make better investment decisions than their trustees

• 43% feel that they could definitely (15%) or probably (28%) make better choices

32% not offered

18% have member level investment choice

50% don‟t know or are unsure whether their fund offers member level choice investment

50

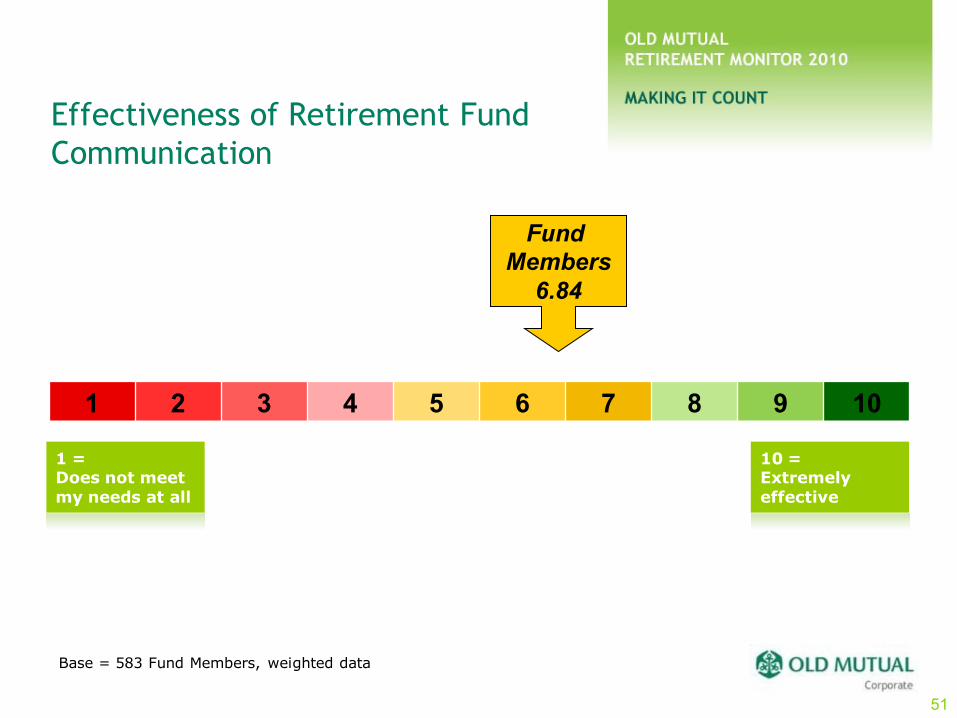

Effectiveness of Retirement Fund

Communication

Base = 583 Fund Members, weighted data

1 2 3 4 5 6 7 8 9 10

Fund

Members

6.84

1 =Does not meet

my needs at all

10 =Extremely

effective

51

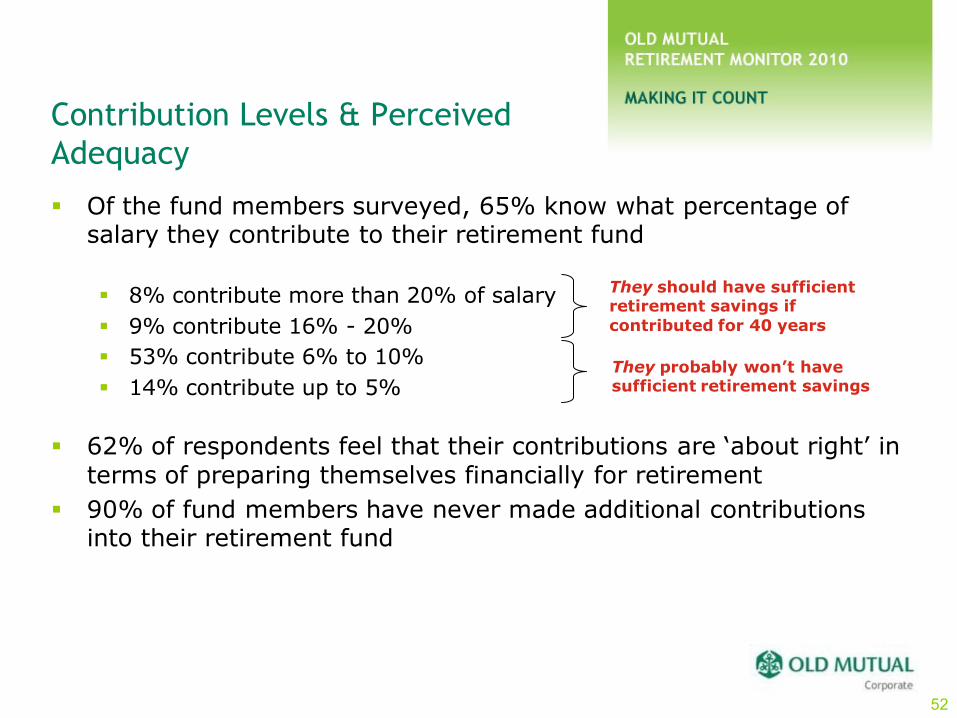

Contribution Levels & Perceived

Adequacy

Of the fund members surveyed, 65% know what percentage of salary they contribute to their retirement fund

8% contribute more than 20% of salary

9% contribute 16% - 20%

53% contribute 6% to 10%

14% contribute up to 5%

62% of respondents feel that their contributions are „about right‟ in terms of preparing themselves financially for retirement

90% of fund members have never made additional contributions into their retirement fund

They probably won’t have sufficient retirement savings

They should have sufficient retirement savings if

contributed for 40 years

52

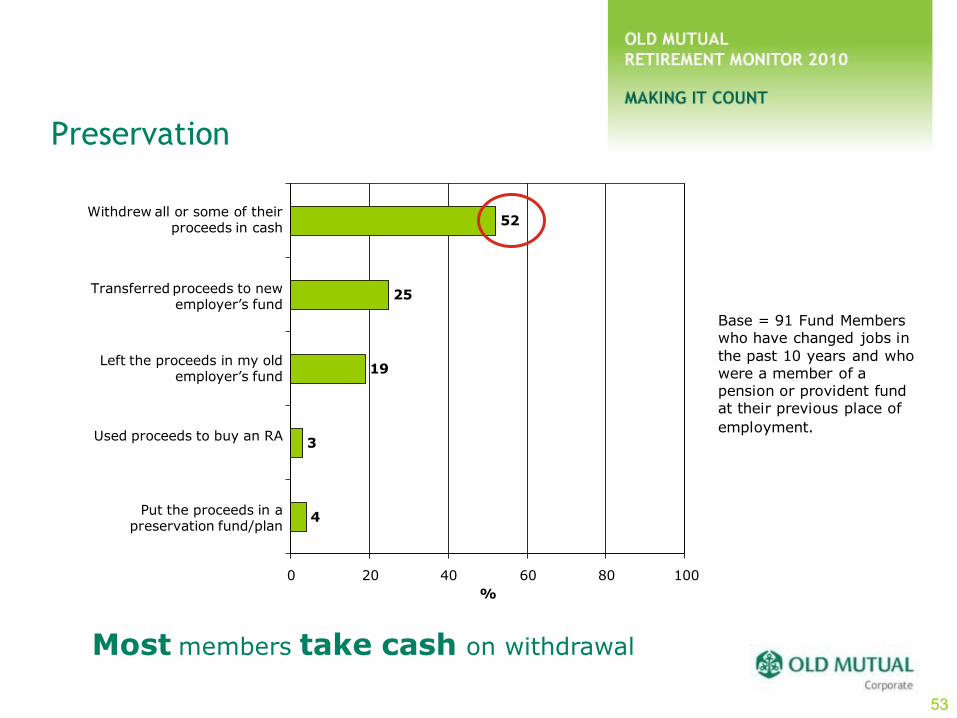

Preservation

Base = 91 Fund Members who have changed jobs in

the past 10 years and who were a member of a pension or provident fund at their previous place of

employment.

4

3

19

25

52

0 20 40 60 80 100

Withdrew all or some of their proceeds in cash

%

Transferred proceeds to new employer‟s fund

Left the proceeds in my old employer‟s fund

Used proceeds to buy an RA

Put the proceeds in apreservation fund/plan

Most members take cash on withdrawal

53

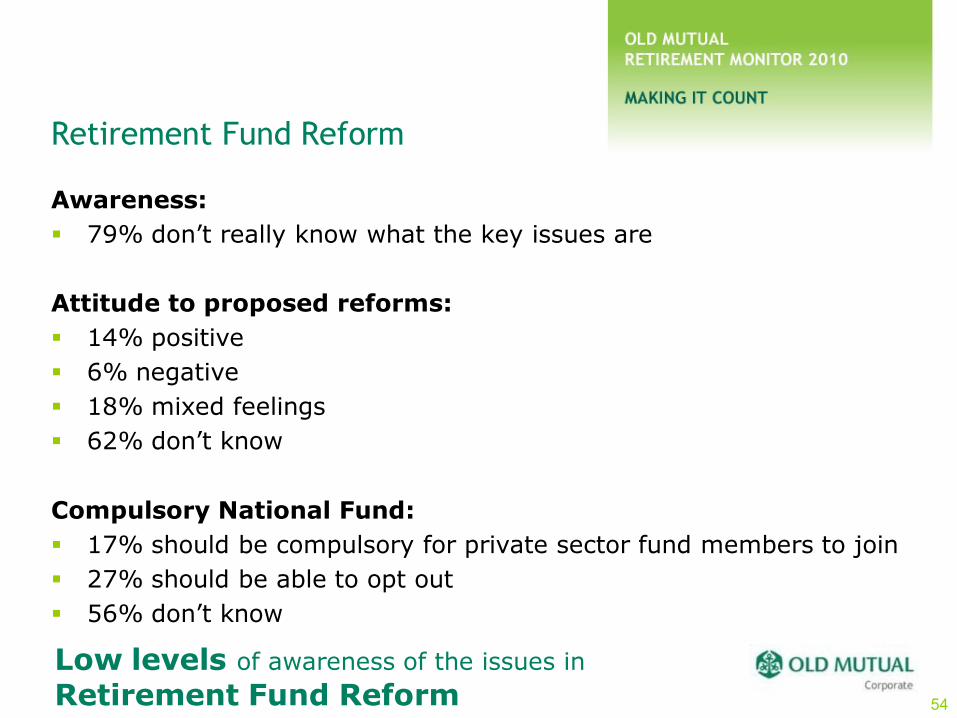

Retirement Fund Reform

Awareness:

79% don‟t really know what the key issues are

Attitude to proposed reforms:

14% positive

6% negative

18% mixed feelings

62% don‟t know

Compulsory National Fund:

17% should be compulsory for private sector fund members to join

27% should be able to opt out

56% don‟t know

Low levels of awareness of the issues in

Retirement Fund Reform 54

Pensioner Sample

MAKING IT COUNT

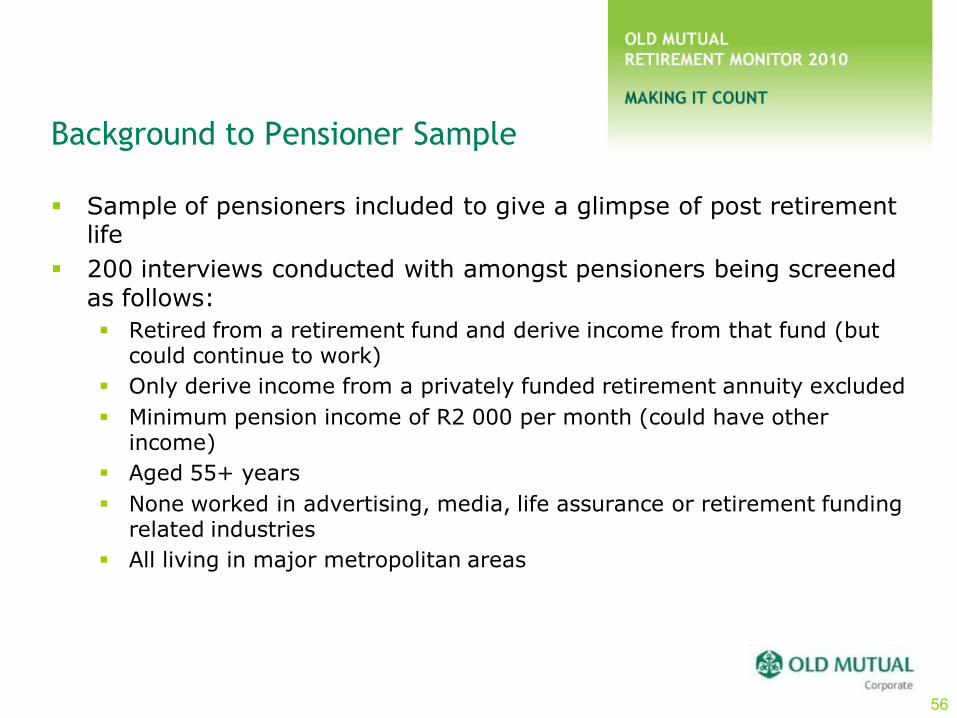

Background to Pensioner Sample

Sample of pensioners included to give a glimpse of post retirement life

200 interviews conducted with amongst pensioners being screened as follows:

Retired from a retirement fund and derive income from that fund (but could continue to work)

Only derive income from a privately funded retirement annuity excluded

Minimum pension income of R2 000 per month (could have other income)

Aged 55+ years

None worked in advertising, media, life assurance or retirement funding related industries

All living in major metropolitan areas

56

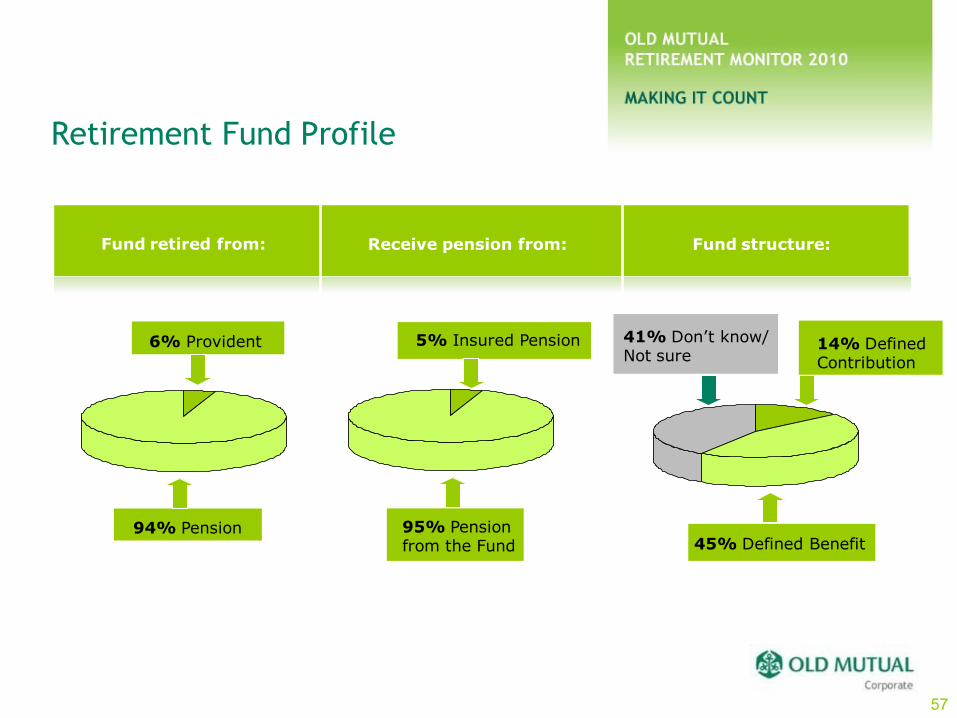

Retirement Fund Profile

Fund retired from: Receive pension from: Fund structure:

6% Provident

94% Pension 95% Pension from the Fund

5% Insured Pension

45% Defined Benefit

14% Defined Contribution

41% Don‟t know/Not sure

57

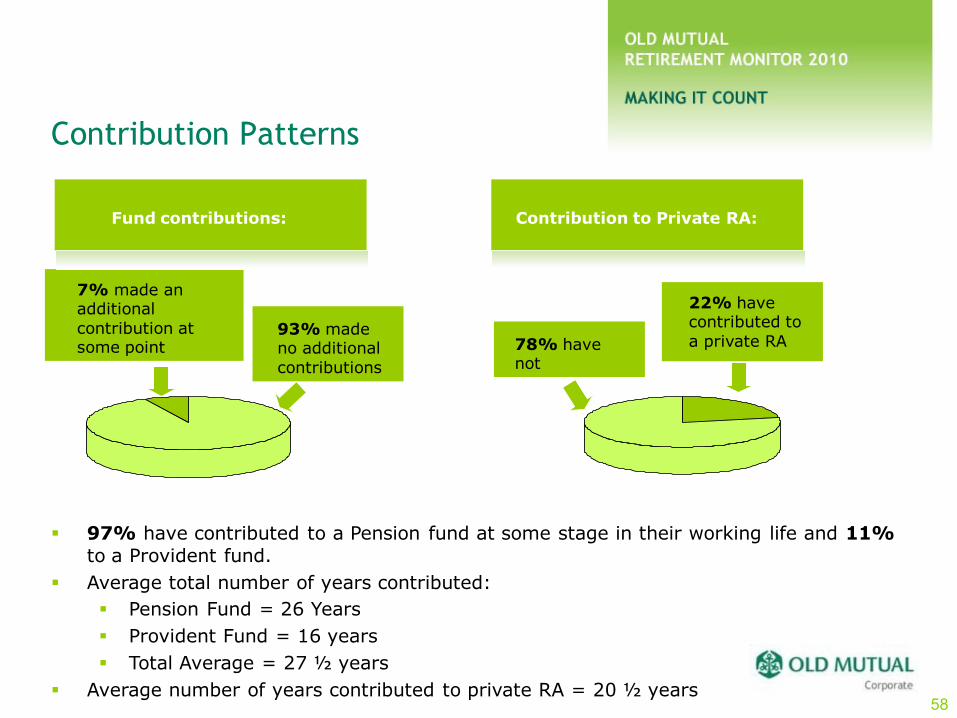

Contribution Patterns

Fund contributions: Contribution to Private RA:

7% made an additional

contribution at some point

93% made no additional

contributions

78% have not

22% have contributed to

a private RA

97% have contributed to a Pension fund at some stage in their working life and 11%

to a Provident fund.

Average total number of years contributed:

Pension Fund = 26 Years

Provident Fund = 16 years

Total Average = 27 ½ years

Average number of years contributed to private RA = 20 ½ years58

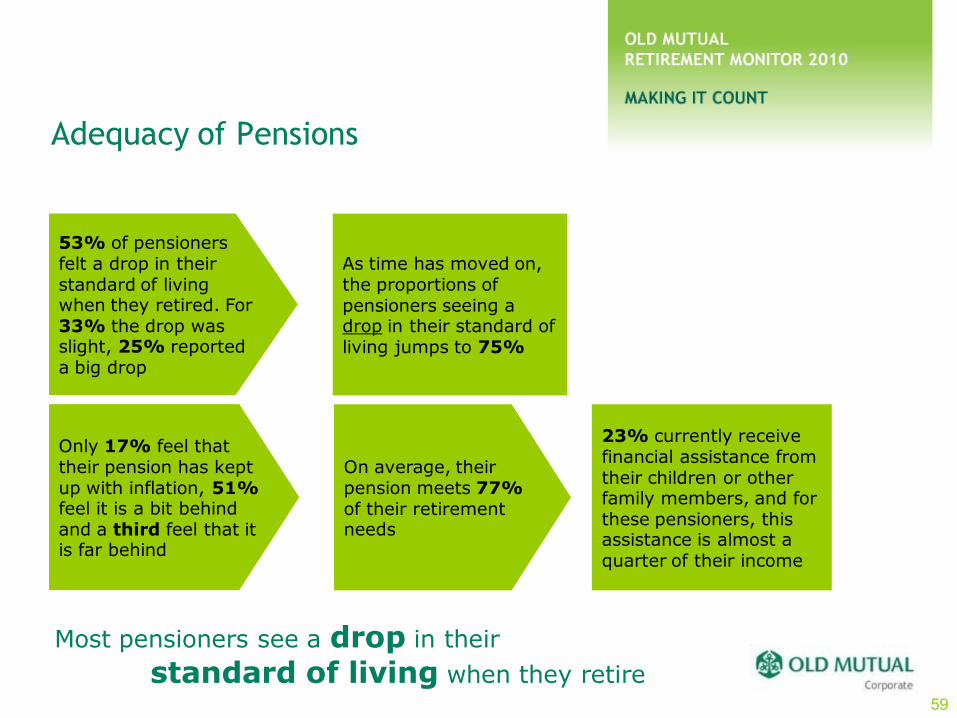

Adequacy of Pensions

53% of pensioners felt a drop in their standard of living when they retired. For 33% the drop was slight, 25% reported a big drop

As time has moved on, the proportions of pensioners seeing a drop in their standard of living jumps to 75%

Only 17% feel that their pension has kept up with inflation, 51%feel it is a bit behind and a third feel that it is far behind

On average, their pension meets 77%of their retirement needs

23% currently receive financial assistance from their children or other family members, and for these pensioners, this assistance is almost a quarter of their income

Most pensioners see a drop in their

standard of living when they retire59

OMAC MeRCI

MAKING IT COUNT

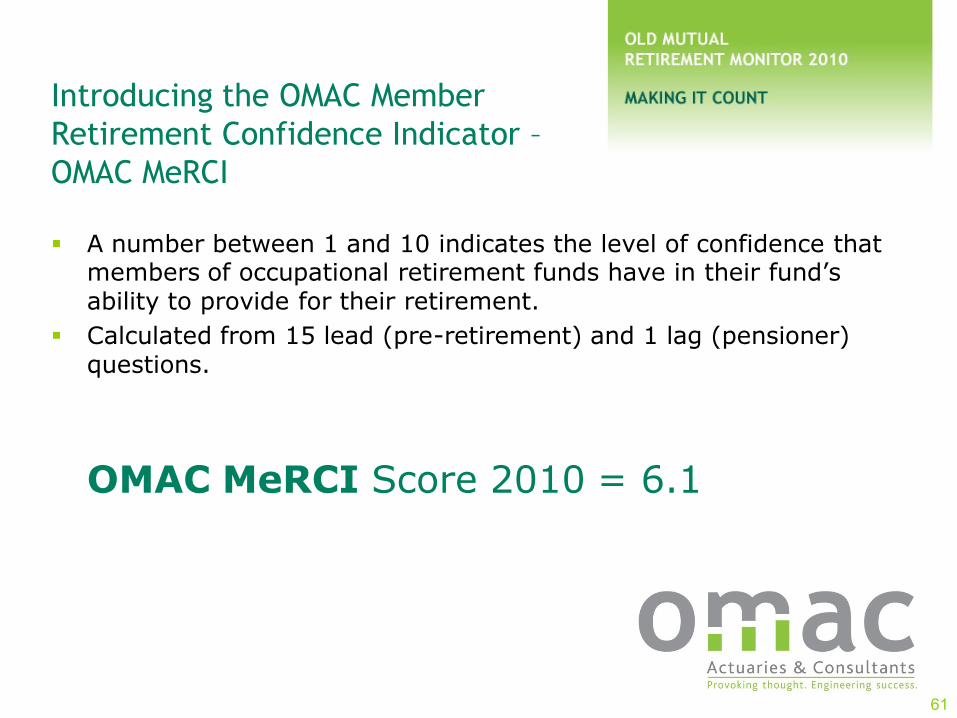

Introducing the OMAC Member

Retirement Confidence Indicator –

OMAC MeRCI

A number between 1 and 10 indicates the level of confidence that members of occupational retirement funds have in their fund‟s ability to provide for their retirement.

Calculated from 15 lead (pre-retirement) and 1 lag (pensioner) questions.

OMAC MeRCI Score 2010 = 6.1

61

Seelan Gobalsamy

MD, Old Mutual Corporate

Hugh Hacking

Umbrella Fund Product Manager,

Old Mutual

De Wet van der Spuy

Head: Consultant Relationships,

Old Mutual Corporate

Craig Aitchison

MD, Old Mutual Actuaries &

Consultants

Panel Q & A