Embed Size (px)

Citation preview

Journal ofRural Development

Vol. 31 January - March 2012 No. 1

CONTENTS

1. Drinking Water Collection and Cost-Benefit Analysis of a 1

Rural Water Supply Scheme in Uttarakhand State

– Fahimuddin

2. Water Use Pattern Of Rural Community In Gangetic 17

West Bengal – A Case Study

– Arijit Roy

3. Incremental Housing and Housing Transformation of the 25

Poor in Karnataka : Problems and Prospects

– M. Mahadeva

4. Rural Banking Scenario in India and the Opportunity for 43

Commercial Banks

– Manoj Kumar Joshi

5. Coping Mechanisms of People In Drought-prone Areas of Rural Orissa 61

– Sujit Kumar Mishra

6. Impact of Farmers' Participation in Farmer Field Schools 85

– Gopala .Y.M1, B. Krishnamurthy2, K.P. Raghuprasad3,

K.Nagabhushanam4 and K. Shivaramu5

7. Management of School Education : Role of Panchayati Raj Institutions 95

– R. S. Tyagi

8. Financial Inclusion - A Gateway to Sustainable 115

Development for the Impoverished

– Kartick Das

BOOK REVIEWS

1. Towards Financial Inclusion in India 129

by K.G. Karmakar, G.D. Banerjee, N.P. Mohapatra

– Dr. B.K. Swain

2. Administration and Development Planning in India 130

by V.Nath

– Dr. K. Jayalakshmi

3. Micro-finance and Women Empowerment 131

by B. Malleshwari

– Dr. Gyanmudra

4. Socio-Economic Profile of Rural India Series-II 133

Edited by S.C. Patra and Ashish Vachhani

– Dr. R. Murugesan

5. Environment and Social Concerns 134

Edited by Venu Trivedi and VK Shrivastava

– Dr. G. Rajani Kanth

6. Participatory Monitoring and Evaluation 135

Edited by M.J.Chandre Gowda

– Dr. R.Chinnadurai

7. Economic Analysis of Institutions : A Practical Guide 136

by V. Santha Kumar

– Dr. V.Annamalai

Fahimuddin*

DRINKING WATER COLLECTIONAND COST-BENEFIT ANALYSIS OFA RURAL WATER SUPPLY SCHEMEIN UTTARAKHAND STATE

Journal of Rural Development, Vol. 31, No. (1) pp. 1 - 15NIRD, Hyderabad.

* Senior Fellow, Giri Institute of Development Studies, Sector-O, Aliganj, Lucknow-226 024.E-Mail:[email protected]

ABSTRACT

In the State of Uttarakhand, availability of safe drinking water has been aserious problem. In order to tackle the problem, State government installed severalrural water supply schemes in the past, but efforts could not yield desired results dueto lack of community participation in operation and maintenance of these schemes.Few years back, State government with funding support from World Bank installedRural Water Supply and Environmental Sanitation Projects with NGOs and communitysupport. The idea was that with the installation of such projects, time used in watercollection would be considerably saved which a rural household can utilise ineconomic activities to earn additional income. The total income, thus, earned wouldprovide an economic advantage when such benefits exceeded the costs incurred inthese projects.

The analysis in the paper focused on two issues. (i) The situational analysis ofvarious dimensions of drinking water collection in the State. (ii) The cost-benefitanalysis of a rural water supply scheme. The findings revealed that drinking watercollection was arduous and a time-consuming activity for the rural households inthe State. The economic benefits which resulted due to time savings from ruralwater supply scheme were higher than the investment made and rural watersupply schemes of the Uttarakhand State provided a model of replicability inother hilly areas of the country.

Availability of safe drinking water is oneof the major problems in most of the ruralareas of India. As a result, people in rural areasdevote substantial part of their working hoursin the arduous task of water collection. In orderto minimise the scarcity of safe drinking water,state governments implemented largenumber of Rural Water Supply Schemes(RWSS). However, it is a known fact that mostof these schemes became non-operational or

functioning irregularly on account of non-participation of beneficiaries in their operationand maintenance. Therefore, the need wasfelt that a fresh strategy was to be evolvedincorporating Government, community-basedNon-Governmental Organisations (NGO's) andthe community to support such water supplyschemes to sustain for a longer period. TheGovernment of Uttarakhand, with World Bankassistance, implemented such schemes in

2 Fahimuddin

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

different districts of the State known as RuralWater Supply and Environmental SanitationProjects (RWSESP). The core of the strategy wasthat water is to be treated like othercommodities and benefits should exceedcosts. The process involved a small ProjectManagement Unit contracting large numberof independent Non-GovernmentalOrganisations to assist the communities inplanning, implementation and maintenance ofwater supply schemes.

The paper examines, on the basis ofprimary data, the involvement of ruralhouseholds in drinking water fetching byfinding the time taken to collect safe drinkingwater, number of water collection tripsundertaken and quantity of water collected.The quantification of time saving ofhouseholds due to introduction of a Rural WaterSupply Scheme was done. The cost-benefitanalysis was attempted to ascertain theassumption that in case of a planned ruralwater supply scheme, estimated benefits arecertainly higher than the costs incurred interms of different types of investment made.

Objectives

The objectives of the paper are :

1. To estimate the time involved incollection of drinking water, number oftrips undertaken for drinking watercollection and the quantity of drinkingwater collected in rural hilly areas ofUttarakhand State.

2. To find out the time usage pattern ofhouseholds for different activities andquantify it in value terms by finding outthe local rural wage rate.

3. To estimate the possible savings in timeafter the introduction of a water supplyscheme.

4. To estimate the benefits over the costs.

5. To draw conclusions and suggestions forwider replication of the model in otherparts of the country.

Methodology

The above issues have been examinedon the basis of primary data collected from102 households, covering a population of 556persons from 10 villages of two districts inUttarakhand State. The districts of Almora andPauri were randomly selected out of thedistricts where rural water supply schemeswere proposed by the World Bank assistedProject Management Unit of the State. Thevillages and their households were alsoselected randomly. The financial viability hasbeen analysed on the basis of costs and returnsestimates provided by the ProjectManagement Unit of the State. Data werecollected through personal interviews fromheads of households in ten sample villageswhich have been covered under drinkingwater supply schemes installed by thegovernment. Results have been analysed intabular form which presents number of tripsper person and per household of different agegroups involved in water collection. Quantityof water fetched per trip and time taken pertrip have also been examined. In the analysis,data relating to number of sample households,average size of population and time usepattern of water collection have been analysedto calculate benefit-cost ratios. The details ofsample design are shown in Table 1.

On the basis of above Table, it is evidentthat the sample consisted of 2 districts, 10villages, 102 households and 556 populationin Uttarakhand State.

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Drinking Water Collection and Cost-Benefit Analysis of a Rural Water Supply Scheme ... 3

Table 1 : Sampling Design of the Study

Districts Blocks Villages Households Population

Almora Bageshwar 1. Nandigaon 10 61

2. Karuli 10 62

3. Chirang 10 50

4. Anarsa 10 52

5. Choura 10 60

Pauri Pauri 6. Thalli 12 58

7. Rawat-ka Falna 10 45

8. Pali 10 53

9. Padul 10 59

10. Sirauli 10 56

Total 2 2 10 102 556

Households and Population : Out of total102 households, 6.86 per cent householdswere of scheduled castes, 1.96 per cent ofbackward castes and 91.18 per cent of uppercastes. The average family size was 5.45

persons. The sex ratio was 100 males per 94females. The ratio of males in total populationwas 52 per cent versus 48 per cent of females.The details are shown in Table 2.

Table 2 : Population, Family Size and Sex Ratio

Particulars Scheduled Backward Upper TotalCastes Castes Castes

No. of Households 7 2 93 102(6.86) (1.96) (91.18) (100.00)

Population : 36 12 508 556

Male 22 5 263 290

Female 14 7 245 266

Family Size 5.14 5.5 5.47 5.45

Sex Ratio 64 120 94 94

Source : Primary data based.

4 Fahimuddin

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Occupational Characteristics : Theoccupational characteristics of the samplepopulation revealed that 74.23 per cent of totalworkers were dependent on agriculture foremployment in the State. It became evidentthat the workers were employed in fouroccupational groups namely, agriculture,agricultural labour, household industry andservices. Though agriculture was the mostimportant activity followed by the serviceswhich provided employment to 23.60 per centof total workers.

Sources of Water : The village communityin the State depended upon four types of watersources. These were Dhara, Naula, tap and river.The average volume of water collected wasfound to be 118.6 litres from Dharas, followedby 74.44 litres, 29.59 litres and 8.55 litres fromNaulas, taps and rivers, respectively. On anaverage, 30 litres of potable water wascollected per household. The tap water supplywas observed to be erratic, interrupted andundependable. The natural sources of waterwere found to be unprotected, exposed tovarious sanitational hazards to be unfit and

Table 3 : Source-wise Volume of Water Collected

Water Source No. of Volume Percentage of Average perhouseholds collected water collected household

Dhara 80 12097 51.30 118.60

Naula 38 7593 32.20 74.44

Tap 59 3018 12.80 29.59

River 43 872 3.70 8.55

Total 220 23580 100.00 231.18

Source : Primary data based.

unsafe. Table 3 shows source-wise watercollected.

Source-wise Time Taken to CollectWater : Average time taken to fetch waterdepends upon the speed of walking to thewater source and the location of a watersource. On an average, sample householdsrequired 30.18 minutes to reach water sourcesin each trip to get water from different sources.Time required to take water from tap workedout to be 7 minutes. Actual time taken to fetchwater from each source was used to arrive ataverage time taken to fetch water. Sincefrequency of water fetching from each sourcevaries, this has been used as weight. Actualnumber of trips to each source was added andpercentage of trips to each source in total trips

was drawn. Thus, source-wise time taken tofetch water is shown in Table 4.

Table 4 : Source-wise Average Time Taken toCollect Water

Source Actual Weights WeightedTime Values

Dhara 35.15 0.27 9.49

Naula 38.40 0.30 11.52

Tap 7.00 0.28 1.96

River 48.03 0.15 7.21

Average Time 31.17 1.00 30.18

Source: Primary data based.

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Drinking Water Collection and Cost-Benefit Analysis of a Rural Water Supply Scheme ... 5

Average Distance Between Householdsand Water Sources : Average distance ofhouseholds from the existing sources of waterworked out to be 900 metres in case of Dhara,950 metres in case of Naula, 310 metres and2100 metres in case of tap and river,respectively as given in Table 5. It is evidentthat distance covered for water fetching wasa time-consuming activity as people had towalk roughly a distance of 1 km. to get waterwhich required more than half an hour in eachtrip.

30.18 minutes to fetch water. Data showedthat average trip time of males and femalesin the age-group of 40-59 years was lowest,i .e. 23.07 minutes and 26.67 minutes,respectively. Maximum members of this age-

Table 6 : Number of Trips for WaterCollection by Gender and Age-Group

Age-Group Gender Numberof Trips

10 - 15 Male 4.04Female 5.10

15 - 40 Male 3.21Female 5.91

40 - 59 Male 2.23Female 6.21

59 & Above Male 2.78Female 3.36

Total Male 3.96Female 5.44

Grand Total 4.89

Source: Primary data based.

Table 7 : Average Time Taken per Person toCollect Water by Gender and Age

Age Group Gender Time per person(Minute)

10 - 15 Male 32.79Female 39.91

16 - 40 Male 27.94Female 30.49

41 - 59 Male 23.07Female 22.67

60 & Above Male 25.21Female 27.11

Total Male 30.41Female 29.67

Grand Total 30.18

Source: Primary data based.

Table 5 : Average Distance of WaterSources from Households

Source Distance (in Metres)

Dhara 900

Naula 950

Tap 310

River 2100

Average Distance 1065

Source: Primary data based.

Number of Trips Undertaken to CollectWater : Average number of trips undertakenper day to collect water by all samplehouseholds worked out to be 4.89 (Table 6).Data showed that females made more tripsper day to collect water as against malesirrespective of their age-groups. The femalesin the age-group of 40-59 years mademaximum number of trips, i.e. 6.21 trips whichwere three times more trips made by males inthe same age group. Results also indicated thatthose involved in water fetching made at leastmore than two trips in a day. The number oftrips increased to six which depended uponthe age-group.

Average Time Taken to Collect Water :Table 7 explains average time taken by a maleor female of different age groups on a trip tofetch water. On an average, a person had taken

6 Fahimuddin

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

group in both the sexes were also involved inwater fetching. On the whole, average timetaken per person to fetch water appeared tobe quite high.

Trip-wise Time Consumed in WaterCollection : Table 8 presents trip-wise averagetime taken in fetching water. It was observedthat average distance covered to reach watersources was more than 1 km. As a result, timespent on a trip was quite long. It is reflectedfrom the Table that on an average 30.18minutes were needed for a trip to fetch water.Out of these, 30.18 minutes, 10.35 minutesand 12.25 minutes were needed for going andreturning, respectively and remaining was thewaiting time at the water source. Sinceavailability of water from Dhara, Naula and tapwas not enough, people had to wait and thencollect water from these sources. As a result,average waiting time during water collectionworked out to be 4.76 minutes.

Table 8 : Average Time Consumedin Water Collection

Activity Time (In Minutes)

Going 10.35

Waiting 4.76

Collecting 2.82

Returning 12.25

Total 30.18

Source : Primary data based.

Trip-wise Time Consumed in AlliedActivities During Water Fetching : People alsogo to water sources for washing clothes,fetching water for animals and for otherrequirements. They spent around 13.43minutes on washing clothes and 6.28 minuteson fetching water for animals. Thus, 20.81minutes were spent per trip on these activities.Table 9 showed trip-wise average time spentin allied activities during water fetching.

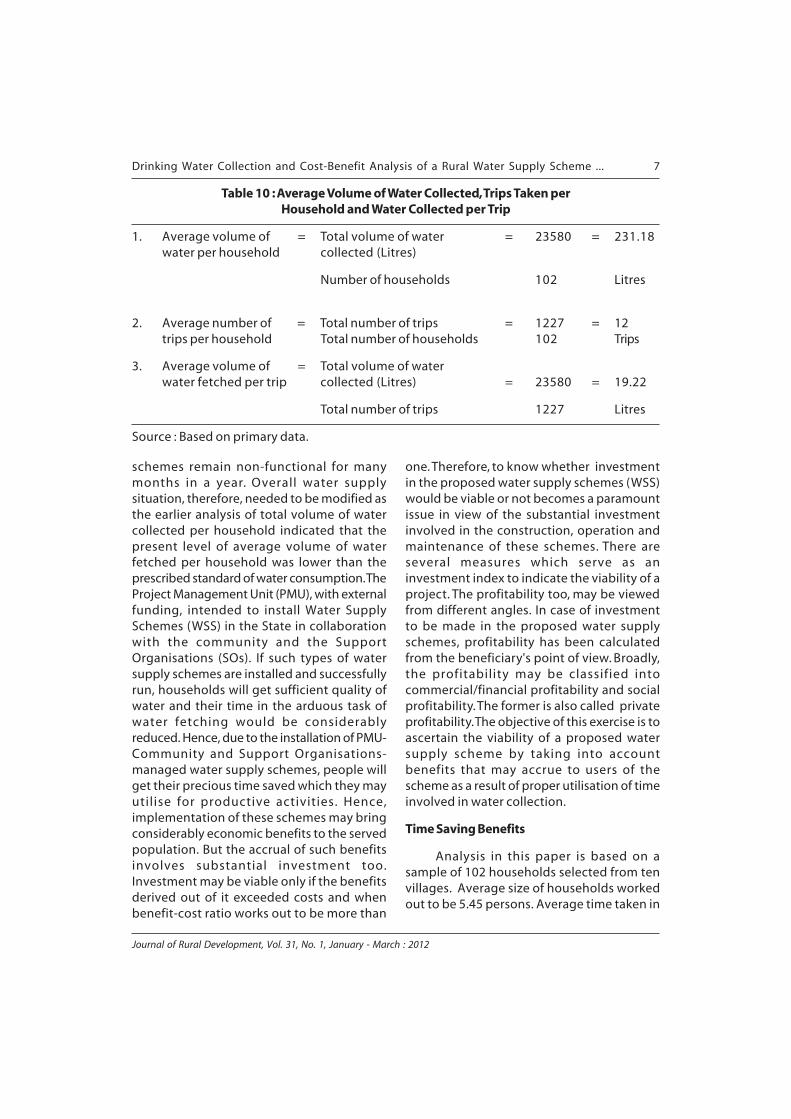

Volume of Water Collected, Trips Taken andWater Collected per Trip : Primary data relatingto volume of water collected, number of tripsundertaken and volume of water fetched pertrip were processed to get an idea as to howmuch average volume of water was beingcollected and average number of trips wereundertaken per household in the State. Theaverage volume of water fetched per trip wasalso analysed. The analysis of data on theseaspects is presented in Table 10.

The above Table revealed that on anaverage 231.18 litres of water was beingcollected per household. Average size ofhousehold was found to be 5.45 persons.When average volume of 231.18 litres of watercollected per household was divided byaverage household size of 5.45 persons, wegot per capita water consumption of 42.42litres. Average number of trips taken perhousehold was found to be 12 in theaggregate sample and 19.22 litres of waterwas being collected per trip. In this way, on anaverage less than one and a half buckets (eachbucket of 15 litres) was being fetched per trip.

Economic Viability of a Water Supply Scheme

People in the hilly State of Uttarakhandcollected water mostly from natural sources.Government also implemented water supplyschemes for some villages. However, due tolack of proper maintenance, most of these

Table 9 : Average Time Spent in AlliedActivities during Water Fetching

Activity Time (in Minutes)

Gossiping 1.10

Washing clothes 13.43

Water fetching andbatching of animals 6.28

Total 20.81

Source : Primary data based.

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Drinking Water Collection and Cost-Benefit Analysis of a Rural Water Supply Scheme ... 7

Table 10 : Average Volume of Water Collected, Trips Taken perHousehold and Water Collected per Trip

1. Average volume of = Total volume of water = 23580 = 231.18water per household collected (Litres)

Number of households 102 Litres

2. Average number of = Total number of trips = 1227 = 12trips per household Total number of households 102 Trips

3. Average volume of = Total volume of waterwater fetched per trip collected (Litres) = 23580 = 19.22

Total number of trips 1227 Litres

Source : Based on primary data.

schemes remain non-functional for manymonths in a year. Overall water supplysituation, therefore, needed to be modified asthe earlier analysis of total volume of watercollected per household indicated that thepresent level of average volume of waterfetched per household was lower than theprescribed standard of water consumption. TheProject Management Unit (PMU), with externalfunding, intended to install Water SupplySchemes (WSS) in the State in collaborationwith the community and the SupportOrganisations (SOs). If such types of watersupply schemes are installed and successfullyrun, households will get sufficient quality ofwater and their time in the arduous task ofwater fetching would be considerablyreduced. Hence, due to the installation of PMU-Community and Support Organisations-managed water supply schemes, people willget their precious time saved which they mayutilise for productive activities. Hence,implementation of these schemes may bringconsiderably economic benefits to the servedpopulation. But the accrual of such benefitsinvolves substantial investment too.Investment may be viable only if the benefitsderived out of it exceeded costs and whenbenefit-cost ratio works out to be more than

one. Therefore, to know whether investmentin the proposed water supply schemes (WSS)would be viable or not becomes a paramountissue in view of the substantial investmentinvolved in the construction, operation andmaintenance of these schemes. There areseveral measures which serve as aninvestment index to indicate the viability of aproject. The profitability too, may be viewedfrom different angles. In case of investmentto be made in the proposed water supplyschemes, profitability has been calculatedfrom the beneficiary's point of view. Broadly,the profitability may be classified intocommercial/financial profitability and socialprofitability. The former is also called privateprofitability. The objective of this exercise is toascertain the viability of a proposed watersupply scheme by taking into accountbenefits that may accrue to users of thescheme as a result of proper utilisation of timeinvolved in water collection.

Time Saving Benefits

Analysis in this paper is based on asample of 102 households selected from tenvillages. Average size of households workedout to be 5.45 persons. Average time taken in

8 Fahimuddin

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

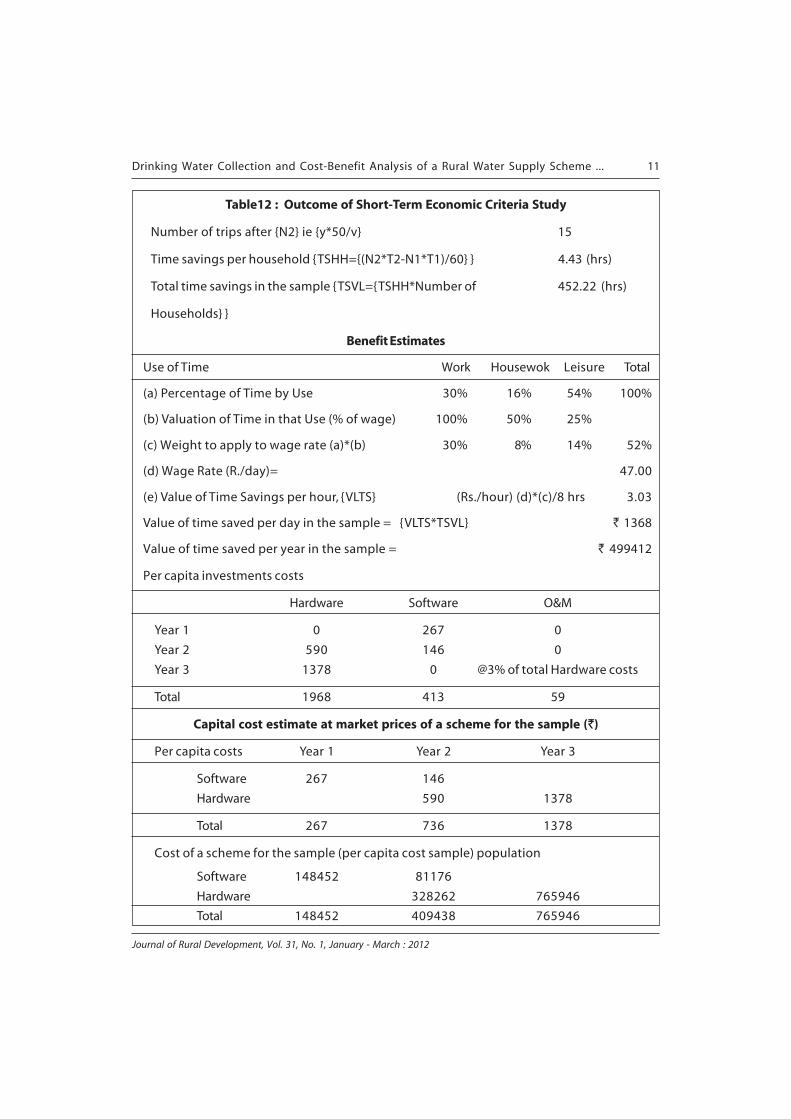

collecting water per trip was calculated in caseof sample households which worked out to30.18 minutes in going, waiting, collectingand returning. This entire time will beminimised considerably when sufficient waterwould be made available by the water supplyscheme. However, all the beneficiaries will notbe using water supply scheme uniformly. It wassuggested by the Project Management Unit(PMU) that 30 per cent of total beneficiarieswould have private tap connections whileremaining 70 per cent will depend uponpublic connections and would not have tospend much time in going, waiting andreturning. Water collection time of a bucketof both types of households would also bereduced, because of high water pressure abucket will be filled in 55 seconds as observedduring field survey. The 70 per cent householdswould spend lesser time in going and waitingas public tap-stands would be installed at anaverage distance of 200 meters which wouldbe far lower than the present average distanceof 1065 meters of households from allavailable water sources. The future waitingtime would also be lesser as compared to thepresent time required in waiting as the size ofthe queue would be smaller because 30 percent households who were part of the queueearlier would be using their own private taps.In this way, average time consumed incollecting water per trip has been estimatedto be 6.47 minutes in future.

Average time taken per trip at presentwhich is referred as time before (T1) was 30.18minutes and average time taken per trip infuture which is referred as time after (T2) wasestimated to be 6.47 minutes. Average volumeof water collected per household before was231.18 litres. Average volume of collectedwater per trip before (V) was 19.22 litres or1.28 buckets (15 litres of one bucket) and thenumber of trips taken per household before(N1) was 12. After giving weights to the 'after'water consumption @40 lpcd for 70 per cent

population using public tap stands and 70 lpcdfor 30 per cent population using privateconnections, the number of trips 'after' (N2)were calculated. The number of such tripswould be after (N2) i.e. (Y *50/V) = 15 trips.Where N2 was the number of trips after, Y wasthe average size of household (5.45 persons),50 lpcd was weighted per capita waterconsumption and V was the average volumeof water collected per trip before.

Thus, the resultant time savings perhousehold (TSHH) are calculated as :

TSSH = {(N2 * T2 - N1 * T1) / 60} = 4.43 hours

The total time savings(TSVL) in the sample is :

TSVL = {(TSHH * Number of Households)} =452.22 hours

Benefit Estimate

Total benefits in value terms can simplybe calculated by multiplying total time savingsin the sample by the prevalent average wagerate in sample villages. However, it isimpossible that the total time savings in thesample that would result on account ofproposed water supply scheme will be usedtotally for work purpose. It is natural that someof the time saved by the households may beused in household activities or leisure. FrankMichel has used in his analysis that 52 per centof the total time saved in water fetching willbe utilised for different work purposes. Hence,we have also adopted the same 52 per cent oftotal time saved to be used in working. Theaverage wage rate of ` 47 per day in thesample which has been arrived at from thesample data was divided by the 8 hours andmultiplied by the 52 per cent of the total timesaved. The resultant figures provided ` 3.03which was the value of time savings per hour(VLTS). The value of time saved per day in thesample was = VLTS * TSVL, which came to

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Drinking Water Collection and Cost-Benefit Analysis of a Rural Water Supply Scheme ... 9

` 1368. This value of time saved per day in thesample has been multiplied by the 365 daysto arrive at the value of time saved per year inthe sample which worked out to ` 49, 9,412.According to the results of our sample data,25 per cent of whole day time was devotedfor work, 35 per cent of total time was devoted

for household activities and 40 per cent oftotal time was given to leisure activities.According to these figures, 53 per cent of totaltime saved was utilised and BC ratio workedout to be 2.06 (net benefit) and 2.24 (netbenefit hardware only). Detailed results arepresented in Table 11.

Table 11 : Outcome of Short Term Economic Criteria Study

Calculation of BC Ratio

Total population Total households Average persons perin sample in sample household (y)

556 102 5.45

Average distances involved and time taken in collecting water per trip

Distance (mtrs) Time (In Minutes)

Going Waiting Collecting Returning Total

Present 1065 10.35 4.76 2.82 12.25 30.18

Future

Public 200 1.94 3.33 1.17 2.30 8.74

Pvt. Conn. 0 0.00 0.00 1.17 0.00 1.17

Average 140 1.36 2.33 1.17 1.61 6.47

Average time taken per trip Average time taken per trip

before (T1) 30.18 Min after (T2) 6.47 Min

Consumption levels

Avg. Vol. of water collected Average volume fetched per trip Number of trips taken

per household 231.18 Litres before (v) 19.22 Litres per household 12

before (1.28 buckets) before (N1)

Weighted consumption 'after'

From public stand posts (@ 40 lpcd for 70 per cent population) 28 lpcd

From private connections (@ 70 lpcd for 30 per cent population) 21 lpcd

Total 49 lpcd

Say 50 lpcd

10 Fahimuddin

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Explanatory Notes

* These figures are based on a sample of102 households in 10 villages of the Hillregion.

* Present distances and time taken arebased on the empirical data taken fromthe above sample. Collection at presentis from more than one type of source.

* It has been assumed that in future notapstand shall be more than 200 mtsfrom any household. It has also beenassumed that there will be 30 per centprivate connections.

Formulae for future times taken are asfollows

Going/ returning time

= (Actual time in going/ returning atpresent) * 200

Actual distance covered at present

Waiting time = Actual time in waiting atpresent * 0.70

Collecting time = Time taken to fill 1.28buckets from a tap

(A tap fills a bucket in 55 seconds).

* Avg.Vol. of water collected perhousehold/ number of trips before arebased on empirical data taken fromabove sample.

Investment Costs

Investment costs comprise hardwarecosts (HC), software costs (SC) and operationand maintenance costs (O&M). Hardware costsare to be incurred on pipes and plant andmachinery etc. Software cost denotes the costto be incurred on training and orientationprogrammes. It has been proposed by ProjectManagement Unit (PMU) that the entirehardware costs would be incurred within threeyears from the initiation of the project. ThePMU further suggested that no hardware costsare required in year-1 while 30 per cent and70 per cent hardware costs would be spent inyear-2 and year-3. The per capita software costswould be ` 267 in year-1 which was theplanning phase cost and ̀ 146 in year-2 whichis the implementation and post-implemen-tation cost. No software cost was required inthird year. In case of hardware costs, it was notrequired in year-1 while it will be ` 590 inyear-2 and ` 1378 in year-3. In this way, totalper capita capital costs estimate at marketprice of a scheme for the same worked out tobe ` 267 in year-1, ` 736 in year-2 and `1524in year-3. The per capita capital costs have beenmultiplied by the sample population. Theresultant figures were the cost of a scheme.These costs figures were ` 1,48,452 forhardware and ` 1,48,452 the total in year-1.In the year-2, ` 81,176 and ` 32,826 and` 4, 09,438 were software, hardware and totalcosts of a scheme respectively. In the year-3,` 7, 65,946 and ` 7,65,946 were the softwareand total costs, respectively (Table 12).

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Drinking Water Collection and Cost-Benefit Analysis of a Rural Water Supply Scheme ... 11

Table12 : Outcome of Short-Term Economic Criteria Study

Number of trips after {N2} ie {y*50/v} 15

Time savings per household {TSHH={(N2*T2-N1*T1)/60} } 4.43 (hrs)

Total time savings in the sample {TSVL={TSHH*Number of 452.22 (hrs)

Households} }

Benefit Estimates

Use of Time Work Housewok Leisure Total

(a) Percentage of Time by Use 30% 16% 54% 100%

(b) Valuation of Time in that Use (% of wage) 100% 50% 25%

(c) Weight to apply to wage rate (a)*(b) 30% 8% 14% 52%

(d) Wage Rate (R./day)= 47.00

(e) Value of Time Savings per hour, {VLTS} (Rs./hour) (d)*(c)/8 hrs 3.03

Value of time saved per day in the sample = {VLTS*TSVL} ` 1368

Value of time saved per year in the sample = ` 499412

Per capita investments costs

Hardware Software O&M

Year 1 0 267 0

Year 2 590 146 0

Year 3 1378 0 @3% of total Hardware costs

Total 1968 413 59

Capital cost estimate at market prices of a scheme for the sample (`)

Per capita costs Year 1 Year 2 Year 3

Software 267 146

Hardware 590 1378

Total 267 736 1378

Cost of a scheme for the sample (per capita cost sample) population

Software 148452 81176

Hardware 328262 765946

Total 148452 409438 765946

12 Fahimuddin

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

* The number of trips after have beencalculated on the basis of 'weightedconsumption' after.

* Distribution of use and valuation of timehas been assumed.

* These cost figures at market prices havebeen worked out from the project costtables used by the Dec. 1995 Mission.The following assumptions have beenmade.

Hardware

- No hardware in year 1

- 30 per cent and 70 per cent costs in year2 and 3, respectively.

Software

- Planning phase cost in year 1

- Implementation and post-implemen-tation cost in year 2.

O & M

From year 3 onwards

Benefit- Cost Flows

Year-wise costs to be incurred onhardware, software and operation andmaintenance of a water supply scheme for thesample are shown in Table 13.

It has been assumed that the populationof sample would increase by 2 per centannually. The values of the time saved per yearin case of sample have also been depicted inthe same table. The benefit-cost flows (`) havebeen calculated year-wise up to 24 years assuggested by the PMU. The net benefits havebeen arrived at by deducting the total capitalcosts of a scheme from the value of time savedper year in the sample. It is evident from thevalues of the net benefits and the net benefitsof hardware that the net gains would be

negative in the first, second and third yearsafter the implementation of the scheme asthe beneficiaries would not get any timesavings up to the three years which shall bethe planning and implementation years. Sincefourth year onwards, the net benefits andbenefits on hardware would accrue and go onincreasing up to 15 years, serving thepopulation with the 2 per cent increase eachyear. The scheme would be unable to meetthe requirements of the water of growingpopulation after 15 years and hence benefitswill stagnate. The value of benefit-cost ratiofor the entire period works out to be 2 in caseof net benefits and 2.18 in respect of netbenefits of hardware only which implied thatthe scheme is economically viable to beimplemented in the State. A discount rate of11 per cent in the net present values has beengiven to take into account the impact of theinflation, changes in the interest rates and therisk factor. The basis of 11 per cent discountfactor is also based on Frank Michel'sestimation.

Summary and Conclusions

The State of Uttarakhand, which was partof the U.P. State earlier, is largely a mountainousregion in the lap of Great Himalaya. In the State,availability of safe drinking water has been aserious problem because of larger availabilityand dependency on natural sources of waterlike Dhara, Naula and river for various waterneeds. But due to their natural open flows,water gets contaminated and becomes unsafefor human consumption. To make available thesafe water to the people, State governmenthad installed many water supply schemes inthe past which could not be successfulbecause of lack of community participation inthier operation and maintenance. Few yearsback, State government, with financial supportfrom the World Bank, decided to install WaterSupply and Sanitation Projects with the helpof NGOs and community. The idea was thatwith the installation of such projects,

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Drinking Water Collection and Cost-Benefit Analysis of a Rural Water Supply Scheme ... 13

Table 13 : Outcome of Short Term Economic Criteria Study

Project Costs Benefits Net Net PopulationYear Benefits Benefit Served

Hardware Software O&M Total Time Hardwaresavings only

1 2 3 4 5=(2+3+4) 6 7=(6-5) 8=(6-5-3) 9

1 0 148452 0 148,452 0 (148,452) (148,452) 0

2 328262 81176 0 409,438 0 (409,438) (409,438) 0

3 765946 32,826 798,772 499,412 (299,360) (266,533) 578

4 32,826 32,826 509,400 476,574 509,400 590

5 32,826 32,826 519,588 486,762 519,588 602

6 32,826 32,826 529,980 497,154 529,980 614

7 32,826 32,826 540,580 507,754 540,580 626

8 32,826 32,826 551,391 518,565 551,391 639

9 32,826 32,826 562,419 529,593 562,419 651

10 32,826 32,826 573,668 540,841 573,668 664

11 32,826 32,826 585,141 522,315 585,141 678

12 32,826 32,826 596,844 564,018 596,844 691

13 32,826 32,826 608,781 575,954 608,781 705

14 32,826 32,826 620,956 588,130 620,956 719

15 32,826 32,826 633,375 600,549 633,375 734

16 32,826 32,826 633,375 600,549 633,375 734

17 32,826 32,826 633,375 600,549 633,375 734

18 32,826 32,826 633,375 600,549 633,375 734

19 32,826 32,826 633,375 600,549 633,375 734

20 32,826 32,826 633,375 600,549 633,375 734

21 32,826 32,826 633,375 600,549 633,375 734

22 32,826 32,826 633,375 600,549 633,375 734

23 32,826 32,826 633,375 600,549 633,375 734

24 32,826 32,826 633,375 600,549 633,375 734

NPV at Disc. Rate of

0.11 826,478 199,625 217,822 1,243,925 3,736,411 2,492,486 2,710,308

BC Ratio 2.00 2.18

* An annual increase of 2 per cent in population has been assumed.

(in `)

14 Fahimuddin

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

substantial time of the people used in waterfetching would be saved considerably whichpeople can use in economic activities to earnadditional income. Thus, the water supplyprojects would give time savings in watercollection whose total returns would be higherthan the costs to be incurred on the schemesfor a longer time period of 15 years. The paperhas examined these hypotheses to ascertainas to what extent the assumptions turn intoreality. To study it, primary data were collectedfrom the sample households relating to theirsize, water fetching practices, sources of water,quantity of water fetched by the households,time involved and time savings that wouldresult due to easy and adequate availability ofsafe water from the new scheme. The averagefamily size in State was found to be 5.45persons. The village community was found tobe dependent upon four types of watersources, namely, Dhara, tap, Naula and river.The most important water source was Dharafrom which 51.30 per cent of total quantity ofwater was fetched by the sample households.Only 12.80 per cent of total water procurementwas made by tap, which was the only sourceof potable water. The river has been reportedto be the water source from which only 3.70per cent of total water was obtained. The Naulawas also one of the major natural watersources which provided 32.70 per cent of totalwater used by sample population. An averagequantity of water collected per household perday was found to be 15.41 buckets in thesample. It worked out to around 42 litres percapita per day. For drinking water purpose, 11litres per capita was the water volume fetched.

The figure of 11 lpcd was calculated fromaverage volume of water collected perhousehold for different uses. The perhousehold water use for drinking purpose wasfound to be 61.82 litres. When this figure wasdivided by the average household size of 4.45persons, we got the 11 lpcd for drinkingpurpose. The sample households required30.18 minutes to reach the water source ineach trip. Average distance of samplehouseholds from the existing water sourcesworked out to be 10365 metres. Averagedistance of natural water sources like Dhara,Naula and River was found to be 1 km. andmore. Average number of trips taken to fetchwater per person by gender and age-grouprevealed that 5 trips per person engaged inwater collection were undertaken. The averagetime taken per person to fetch water by genderand age-group showed that 30 minutes wererequired. On the whole, average volume ofwater collected per household worked out tobe 231 litres. The average number of trips perhousehold were 12 and the average volumeof water collected per trip was estimated tobe 19 litres.

Financial viability of the proposed watersupply scheme was analysed for samplepopulation. The value of the benefit-cost ratioworked out to be 2 in case of net-benefits and2.18 in respect of net-benefits of hardwareonly which implied that the scheme wasfinancially viable for implementation in theState of Uttarakhand. It also indicated that suchtype of water supply schemes have viablereplicability in other parts of the country.

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Drinking Water Collection and Cost-Benefit Analysis of a Rural Water Supply Scheme ... 15

References

1. Jim Dowing and Pooja Sharma, (2002), Sustainability of Rural Water Supply Projects : Lessons from thePast, Revisiting Community Based Rural Water Supply Projects in Uttar Pradesh, World Bank.

2. B.K. Bajpai and Fahimuddin, (1996), Time Usage and Short Term Economic Criteria Study, Hill andBundelkhand Regions of Uttar Pradesh, Project Management Unit, Lucknow.

3. Water Supply and Sanitation, (2002), A WHO-UNICEF Sponsored Study, Planning Commission, Governmentof India.

4. Uttarakhand Rural Water Supply Projects, World Bank, 2006.

Arijit Roy*

WATER USE PATTERN OFRURAL COMMUNITY INGANGETIC WEST BENGAL –A CASE STUDY

Journal of Rural Development, Vol. 31, No. (1) pp. 17 - 23NIRD, Hyderabad.

* Assistant Professor in Economics, Department of Commerce, V.M. Mahavidyalaya, Chaitanyapur, EastMidnapore, West Bengal - 721645. E-mail : [email protected]

ABSTRACT

Water is the most precious natural resource acting as the lifeline of the ruralcommunity. It can be highly productive and support prosperous communities ifproperly used. This paper attempts to explore the water use pattern of ruralcommunity in Gangetic West Bengal. Primary data were collected in the EastMidnapore district of West Bengal during 2008-2009. It has been observed thatthe level of per capita income does have a positive influence on the level of percapita domestic water consumption. Also, the proximity of the water source doesincrease domestic water consumption. Agriculture is the major occupation withthe highest water dependence. It has also been found that water consumed foragriculture is directly influenced by the level of per capita income, the proximityof water source and water-intensive cropping pattern.

Introduction

Water is commonly regarded as plentifulin gangetic plain of West Bengal. However, thesupply for man’s use is definitely limited andits volume and quality are determined, to agreat extent, by human activities. In rural partof gangetic West Bengal, water ispredominantly consumed for drinking,sanitation and farm irrigation.

Kumar, A.C., Malhotra, K.C., Raghuram, S.and Pais, M. (2000) considered the waterconsumption behaviour of rural community ofTumkur district, Karnataka. This study had alsoshown the significance of water rights toincrease equity in water use, systems ofincentives for the use of water-saving devicesand recycled water in agriculture, managingwater systems including drinking water used

by local communities, providing watereducation, introducing community managedirrigation systems and empowering womenin water resource management. Bhattacharyya,D., Roy, G.B. and Das, J.K. (2008) studied thepattern and efficiency of water use on the basisof different socio- economic classes in Howrahdistrict of West Bengal. Another study byKumar, M., Gaur, D.R., Goel, M. and Mishra, R.(2009) revealed the water use pattern andbehaviour of rural community in Beri block ofJhajjar district of Haryana.

The present study attempts toinvestigate the water use pattern of ruralcommunity in gangetic plain of West Bengalaccording to different socio–economic classes,different occupations, ease of access to waterand different cropping patterns.

18 Arijit Roy

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Methodology

A two-stage stratified random samplingtechnique was used for the purpose of thestudy. With similar geographical and socio –economic features, two villages, namely, Bardaand Chaitanyapur under No.3-ChaitanyapurGram Panchayat, Sutahata Block of EastMidnapore of West Bengal were selected. Inthe second stage, a complete enumeration ofhouseholds according to monthly per headincome(Y in `) was made. The householdswere then stratified into three major groups,i.e. ,the Poor Class (Y<1500),the Middle Class(1500 < Y <4000) and the Rich Class (Y >4000). From the total population, 100households were selected at randomconsisting of 32 poor households, 56 middleclass households and 12 rich households. Thesample households were administered withwell-designed semi-structured questionnairesto find required information. The data werecollected in the year 2008-2009. The simplestatistical tools like percentage and mean havebeen used to interpret the data in tabular form.Multiple Regression technique has beenemployed to know the impacts of income andproximity of water source upon the domesticconsumption of water. We have also analysedthe impacts of income, proximity of watersource and cropping pattern on theconsumption of water for farming. For this, weuse the following log-lin equations:

ln DWC = β1 + β2 ln Y + β3 PX + u,

ln FWC = α1 + α2 ln Y + α3 PX + α4 CP + v,

where DWC = Domestic waterconsumption in liter per capita per day (lpcd),

FWC = Water consumption for farming(lit/ bigha),

Y = per head income ( `/month ),

PX = proximity of the water source ; PX= 1 for distance < 300 meter,

= 0 otherwise

CP = Cropping pattern ;

CP = 1 for water-intensive croppingpattern, = 0 otherwise.

u and v are random error terms normallydistributed with zero mean and finite varianceand satisfying the assumptions of the ClassicalLinear Regression Model. β1 and α1 areintercept coefficients. β2, β3, α2, α3 and α4are the partial slope coefficients.

Study Area

Barda (22 09’33’’N, 8808’30’’E ) andChaitanyapur (2207’47’’ N, 8801’28’’ E ) villagesare under No. 3 Chaitanyapur Gram Panchayat,Sutahata Block of East Midnapore district ofWest Bengal. The area comes under thegangetic plain agro-climatic zone of the State.The area is covered with loamy soil. Theaverage temperature varies between 120C -350C, while the average annual rainfall variesbetween 150 cm – 175 cm.

Table 1 reveals that the average per headdrinking water consumption is the highest forrich people (4.9 lpcd) followed by the middleclass (4.8 lpcd) and the poor class (4.0 lpcd).The average per head consumption of waterfor sanitation is the highest for rich people (6.3lpcd) followed by the middle class (4.8 lpcd)and the poor class (3.8 lpcd). The average totalconsumption of domestic water is the highestfor the rich class (11.20 lpcd) followed by themiddle class (9.60 lpcd) and the poor class(7.80 lpcd).

Table 2 shows that the average totaldomestic water consumption is the highestfor households in farming (9.15 lpcd) followedby service (9.10 lpcd) and business (8.92 lpcd).

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Water Use Pattern of Rural Community in Gangetic West Bengal – A Case Study 19

Result and Discussion

Table 1 : Domestic Consumption of Water by Different Income Classes and Occupations inChaitanyapur and Barda, Sutahata Block, East Midnapore

Social Status No. of No. of Water Water Average TotalFamilies Members Consumption Consumption Domestic

for Drinking for Sanitation Water(a) (b) Consumption

(a+b)Total Average Total Average

(lit/day) (lpcd) (lit/day) (lpcd)

Farming 22 118 477.50 4.05 452.80 3.84 7.89

Poor Non-farming 10 44 170.50 3.86 162.80 3.70 7.56

Total 32 162 648.00 4.00 615.60 3.80 7.80

Farming 40 213 1032.00 4.85 1029.60 4.83 9.68

Middle Non-farming 16 48 220.80 4.60 223.20 4.65 9.25

Total 56 261 1252.80 4.80 1252.80 4.80 9.60

Farming 4 12 64.80 5.40 81.60 6.80 12.20

Rich Non-farming 8 30 141.00 4.70 183.00 6.10 10.80

Total 12 42 205.80 4.90 264.60 6.30 11.20

Total 100 465 2106.60 2133.00

Mean 4.53 4.59 9.12

Source : Field Survey.

Table 2 : Domestic Consumption of Water by Different Occupational Groups inChaitanyapur and Barda, Sutahata Block, East Midnapore

Occupation No. of No. of Water Water Average TotalFamilies Members Consumption Consumption Domestic

for Drinking for Sanitation Water(a) (b) Consumption

(a+b)Total Average Total Average

(lit/day) (lpcd) (lit/day) (lpcd)

Farming 66 343 1574.30 4.59 1564.00 4.56 9.15

Business 14 50 230.50 4.61 215.50 4.31 8.92

Service 20 72 301.80 4.19 353.50 4.91 9.10

Total 100 465 2106.60 4.53 2133.00 4.59 9.12

Source : Field Survey.

20 Arijit Roy

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Table 3 shows that the average waterconsumption for farming is 2600 lit/bigha forthe poor families who do not have enoughmoney to spend on irrigation. The averagewater consumption for farming for the middle

class families is 3500 lit/bigha who can affordto spend on irrigation. The average waterconsumption for farming is the highest (4100lit/bigha) for the rich families.

Social Status No. of Source of Water for Source of WaterFamilies Domestic Purpose for Farming

Poor Farming 22 Small pond in the backyard Rain water, canal waterfor 17 families, common tube- supplied throughwell established by Panchayat. manual system.

Non-farming 10 Common tubewell establishedby Panchayat, small pond in thebackyard for 7 families.

Middle Farming 40 Small pond in the backyard and Rain water, canal watercommon tubewell established supplied through pump-by Panchayat for 30 families, set.large pond and own submersiblepump for 10 families.

Non-farming 16 Pond and common tubewellfor 5 families, own submersiblepump for 11 families.

Rich Farming 4 Own submersible pump. Rain water, canal watersupplied throughpumpset.

Non-farming 8 Own submersible pump.

Source : Field Survey.

Table 3 : Consumption of Water for Farming by Different Income Classes in Chaitanyapur& Barda, Sutahata Block, East Midnapore

Social Status Occupation No. of Average WaterFamilies Consumption

for Farming(lit/ bigha)

Poor Farming 22 2600

Middle Farming 40 3500

Rich Farming 4 4100

Source : Field Survey.

Table 4 : Source of Water for Domestic Purpose and Farming Purpose

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Water Use Pattern of Rural Community in Gangetic West Bengal – A Case Study 21

All the poor farming and non-farmingfamilies have small ponds in the backyard fordomestic use except in the peak dry season.For drinking water, they depend on Panchayat-established common tubewells. Rainwater isthe biggest source of water for farming forpoor families. Besides this, they supply canalwater manually to their lands when necessary.Most of the middle class farming and non-farming families rely upon own ponds forsanitation. For drinking water, 30 families usecommon tubewell provided by the Panchayat,15 families use own tubewell and 11 familiesuse own submersible pump. For farming, allthe 40 families use rain water and canal watersupplied through pumpset. All the rich familiesuse own submersible pump for sanitation aswell as drinking water. Rich farming familiesuse rain water along with canal water suppliedthrough pumpset for irrigation.

Table 5 : Cropping Pattern of the Families

Water-intensity Crops cultivated

High Aman paddy, jute, auspaddy, boro paddy, betel-nut, vegetables.

Low Wheat, khesari (lowquality pulse), sunflower,vegetables.

Source : Field Survey.

The common crops in our study area canbe divided into two groups : (a) crops withhigh water intensity e.g. aman paddy, jute, auspaddy, boro paddy, betel-nut and vegetableswhich require heavy irrigation; and (b) cropswith low water intensity e.g. wheat, khesari(low quality pulse), sunflower and somevegetables which require low to mediumirrigation.

Determinants of Domestic and Farm WaterConsumption Disparity

We have tried to analyse the contributionof income(Y) and proximity of water source(PX) to domestic water consumption (DWC)disparity between sample households. In ourlog-lin model, natural log of (DWC) isregressed upon natural log of (Y) and (PX)dummy. The estimated regression results areshown in Table 6.

Table 6 : Regression Result of DomesticWater Consumption Disparity

Co- Standard t-statistic pefficient error value

Intercept 0.382 0.152 2.508 0.028

ln Y 0.214 0.019 11.076 0.000

PX 0.107 0.035 3.101 0.009

N = 100, k = 3.

F- (2,97)d.f. = 72.698 , p value = 0.000.

R² = 0.924 , Adj R² = 0.911.

N (= 100) is the sample size and k (= 3 )is the number of parameters to be estimated.The high t-values are indicative of the fact thatall the estimated coefficients are statisticallysignificant. The intercept coefficient ? β1 takesthe value of 0.382 and is significant at 5 percent level. The coefficient β2 (= 0.214) is theelasticity of ' domestic water consumption 'with respect to income . If per head incomeincreases by 1 per cent, per head waterconsumption increases by 21 per cent. β2 issignificant at any level. β3, the proximitydummy coefficient takes the value of 0.107and is significant at 1 per cent level. β3 = 0.107signifies that the average domestic waterconsumption increases by 11 per cent

22 Arijit Roy

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

(approx.) for the households living near thewater source compared to the others. F =72.698 implies that all the coefficients arestatistically different from zero and aresignificant at any level , d.f. = (2,97). R² = 0.924signifies that approximately 92 per cent of thevariation in the dependent variable (DWC) isexplained by the regression model , R beingthe coefficient of multiple correlation. R²becomes 0.911 when adjusted for thedegrees of freedom.

We have also studied the contributionof income(Y), proximity of water source (PX)and cropping pattern (CP) to farming waterconsumption (FWC) disparity between samplehouseholds. In our log-lin model, natural logof (FWC) is regressed upon natural log of (Y),(PX) dummy and (CP) dummy. The estimatedregression results are shown in Table 7.

Table 7 : Regression Result of Farm WaterConsumption Disparity

Co- Standard t-statistic pefficient error value

Intercept 2.078 0.156 13.287 0.000

ln Y 0.535 0.021 25.903 0.000

PX 0.299 0.122 2.455 0.032

CP 0.271 0.089 3.042 0.049

N = 66, k = 4.

F- (3,62)d.f. = 404.17, p value = 0.000.

R² = 0.991 , Adj R² = 0.989.

N (= 66) is the sample size and k (= 4 ) isthe number of parameters to be estimated .The high t-values are indicative of the fact thatall the estimated coefficients are statisticallysignificant. The intercept coefficient α1 takesthe value of 2.078 and is significant at any level.

The coefficient α2 (= 0.535) is the elasticity of' farming water consumption' with respect toincome . If per head income increases by 1per cent, per head water consumption forfarming increases by 54 per cent. α2 issignificant at any level. α3, the proximitydummy coefficient takes the value of 0.299and is significant at 5 per cent level.α3 = 0.299 signifies that the average farmingwater consumption increases by 35 per cent(approx.) for the households living near thewater source compared to the others. a4 , thecoefficient for cropping pattern dummy takesthe value of 0.271 and is significant at 5 percent level. α4=0.271 signifies that the averagefarming water consumption increases by 31per cent (approx.) for the households whopractise high water-intensive cropping patterncompared to the others. F = 404.17 impliesthat all the coefficients are statisticallydifferent from zero and are significant at anylevel, d.f. = (3,62). R² = 0.991 signifies thatapproximately 99 per cent of the variation inthe dependent variable (FWC) is explained bythe regression model, R being the coefficientof multiple correlation. R² becomes 0.989when adjusted for the degrees of freedom.

Conclusion

The case study reveals some interestingresults. Water consumption is positivelyinfluenced by the level of income therebyjustifying the claim by Frank, B. and Netboy, A.(1978) that "rising living standards meanhigher per capita water consumption". The easeof access to water, captured by the proximitydummy, positively influences the domestic andfarming water consumption. Last, but not least,it is the cropping pattern that influences thelevel of water consumption for farming and itis definitely supported by the findings of thecase study.

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Water Use Pattern of Rural Community in Gangetic West Bengal – A Case Study 23

References

1. Bhattacharyya, D., Roy, G.B., Das, J.K., (2008), Water Use Efficiency on the Basis of Socio-Economic Classes- A Study in Howrah District of W.B., Journal of Interacademicia, 12(4), pp. 478 - 482.

2. Frank, B. & Netboy, A. (1978), Water, Land and People, Alfred A Knopf Inc. London.

3. Kumar, A.C., Malhotra, K.C., Raghuram, S. and Pais, M. (2000), Case Study : India , Water & Pollution Dynamicsin a Rural Area of Tumkur District, Karnataka State, Water & Population Dynamics : Case Studies & PolicyImplications Edited by Sherbinin, A.D. and Dompke, V., HTML Document, Date & Time of Access :17.05.2009,8-15 A.M.

4. Kumar, M., Gaur, D. R., Goel, M., Mishra, R., (2009), Water Collection and Consumption Behaviour in RuralHaryana, The Internet Journal of Epidemiology, 6(2).

M. Mahadeva*

INCREMENTAL HOUSING ANDHOUSING TRANSFORMATIONOF THE POOR IN KARNATAKA :PROBLEMS AND PROSPECTS

Journal of Rural Development, Vol. 31, No. (1) pp. 25 - 42NIRD, Hyderabad.

* Member, Karnataka Public Service Commission (KPSC), Udyoga Soudha, Park House Road, Bangalore-560001. Email: [email protected]

Acknowledgement

* This paper is based on a completed research project at the Institute for Social and Economic Change(ISEC), Bangalore, when the author was a faculty member in Economics. The author is grateful to theManaging Director and the administrative authorities of the Rajiv Gandhi Rural Housing CorporationLimited, Bangalore for their support to the study. The research assistance of Mr. K. Keshavamurthy, Mr.Nitin Tagade and the academic support of Dr. KG Gayathri Devi at ISEC are gratefully remembered. Butfor their support this research would not have been possible. The author is especially grateful to theanonymous referee for the valuable comments on the earlier version of the paper. The views expressedin this paper are entirely of the author and do not reflect on the current institutional affiliation.

ABSTRACT

Social housing schemes have historically played a very significant role inalleviating the housing poverty in the rural and urban areas of the country and inrealising the dreams of houseless poor families at the national and sub-nationallevels. With the national and state governments' financial commitments for theimplementation of the social housing schemes, additional housing stock has beencreated and thereby the housing deprivation has been minimised, especially inthe rural areas of the country. These schemes have contributed for the increase inthe housing stock in the pucca and semi-pucca streams and thereby the incidenceof the dilapidated units has been brought down substantially. Also these schemeshave been successful in bringing about housing comforts as well as increasedaccess to housing amenities like household electricity, sanitation, drinking waterand drainage. Besides, a good number of beneficiary families have successfullyundertaken a few economic activities and have enhanced their family income tosome extent. Despite these positive impacts on the poorer sections, the functioningof the social housing schemes has been bogged down by a number of problemsfrom panchayat, beneficiary and village corners. Inadequacy of housing benefits,prevalence of corruption, various costs involved in receiving the housing benefitsand use of the external influence are some of the problems identified. This paper,after having considered all these issues in greater detail based on an empiricalresearch in Karnataka, suggests alternatives for better administration of the socialhousing schemes.

26 M. Mahadeva

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Introduction

Incremental housing refers to overallimprovement in the housing and livingconditions among the beneficiary familiesunder various social housing schemes. To bespecific, it is a situation in which thebeneficiary families experience a betterhousing structure or transformation of thefamilies' dwelling from deficient housing unitsto better structured units, on account ofreceiving the housing benefits. With theincremental housing, the families would haveovercome the insecurity feeling they werefacing in the deficient housing. It is a situationthat provides improved space for the familymembers thereby experiencing privacy withinthe housing environment. Further, being therecipient of the housing benefit, the familieshave been experiencing increased access tobasic housing amenities like the householddrinking water, sanitation, electricity anddrainage connection. In other words, thebeneficiary families with the changingcircumstances would have minimised thesedeprivations. Finally, incremental housing maylead to the use of their housing units forundertaking some economic activities by thebeneficiary families and would have led toimprovement in employment and income oftheir households.

Ever since Independence, IndianGovernment is committed to the developmentof the housing sector to ensure housing facilityto the houseless people and has particularlyengaged itself to meet this critical basic needfor the poorer sections, as they cannot affordit by themselves or can obtain from the privatesector and the market. Social housing schemesare one of the prominent interventions of thenational government, which have beenintroduced from the very First Five Year Planin the country to meet the housing needs ofthe vulnerable groups, both in the rural andurban areas (Mahadeva, 1994). The socialhousing schemes (like Subsidised Industrial

Housing, Low Income Group Housing, MiddleIncome Group Housing, Rental HousingScheme, Village Housing Project Scheme,Plantation Labour Housing Scheme and RuralHouse Sites Scheme) introduced by thenational government were implemented bythe state governments till early nineties. Withthe declaration of the year 1987 as the“International Year of the Shelter for theHomeless” by the United Nations Assemblyand after enacting the first National HousingPolicy in 1987 in the countr y, stategovernments have started playing their ownrole for the development of housing sector atthe sub-national level. In fact, the NationalHousing and Habitat Policy-1998 has been amilestone in clearly defining the role of thestate governments in the development ofhousing sector (GoI, 1998). These initiativespaved ways for laying a strong foundation atthe sub-national level to meet the housingneeds of the various sections, particularly thepoorer sections by the state itself, byintroducing their own social housing schemes,in addition to the implementation of thenational schemes.

Karnataka is one of the prominent Statesin south India to have committed itself to meetthe housing needs of the houseless families,particularly of the poorer sections, weakersections and socially distanced sections(Mahadeva, 2004). In fact, of the five differentsocial housing schemes in vogue for meetingthe housing requirement of the variousvulnerable groups, four have been introducedby the State government with its own publicpolicy and financial commitment, since earlynineties. Setting up of a specialised institutionfor the administration of housing benefitsunder the social housing schemes andfinancing these schemes on a continuum basishave been the testimony for the sustainableconcern of the State. Correspondingly, theseschemes have also lived up to their own goalsand mission, by and large, in giving the

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Incremental Housing and Housing Transformation of the Poor ... 27

homestead rights to the targetedbeneficiaries and in meeting the housingneeds of the poorer sections. However, therehave been a number of misconceptions on theworking of these schemes, in terms of coveringthe genuine beneficiaries, financingcommitment of the state and on the impactof the social housing schemes on the housingstock and on the beneficiary families, withregard to housing security, incrementalhousing, increasing access to housingamenities, improvement in the familyconditions, corruption in the administrationand other problems etc. Thesemisconceptions have come to the fore frommany corners of the society, mainly on accountof the fact that there are hardly any empiricalresearch studies on the social housingschemes, either at the national or sub-nationallevel. More so, in the case of Karnataka,empirical research on the functioning andimpact on the social housing schemes arealtogether absent. Therefore, addressing theseissues, particularly on the misconceptionsabout the social housing schemes in the Stateis the main purpose of the paper, which isbased on an empirical research study.

The principal objectives of the paper are:(a) to study the role of the State in terms ofthe administrative and financial commitmentstowards the social housing schemes; (b) toassess the impact of the existing social housingschemes in terms of the housing stock createdand residential sites distributed in the State;(c) to examine the impact of the social housingschemes on the beneficiary families in regardto the incremental housing, access to basichousing amenities, new economic activitiesundertaken and family income; (d) to analysethe various problems encountered by thebeneficiaries in receiving the housing benefitsunder the social housing schemes; and (e) tooffer various policy alternatives for making thesocial housing schemes more effective, interms of attaining the goals and achieving

better results. This study was conducted intwenty taluks, including the nine identified asbackward by the High Power Committee(HPCFRRI, 2002), spread into eleven districtsof the State and used both secondary andprimary data for the analysis. Primary data werecollected through a specially designed andtested questionnaire from 1, 632 beneficiaries,covering the representative samples from allthe five social housing schemes implementedin the study area. Secondary data werecollected from various official documents,maintained by the Rajiv Gandhi Rural HousingCorporation (RGRHC), a nodal agency for theadministration of the social housing schemesin the State.

The State Intervention

The role of the State government inregard to the administration of the socialhousing schemes can be captured under threedifferent domains viz, (a) Social HousingSchemes (in terms of the core purpose, targetgroup, financial assistance available); (b)institutional arrangement-RGRHC; and (c)public expenditure on the social housingschemes. Since the success of any publicintervention largely depends on politicalcommitment, these three parameters havebeen analysed, as they roughly refer to thepolitical will of the State.

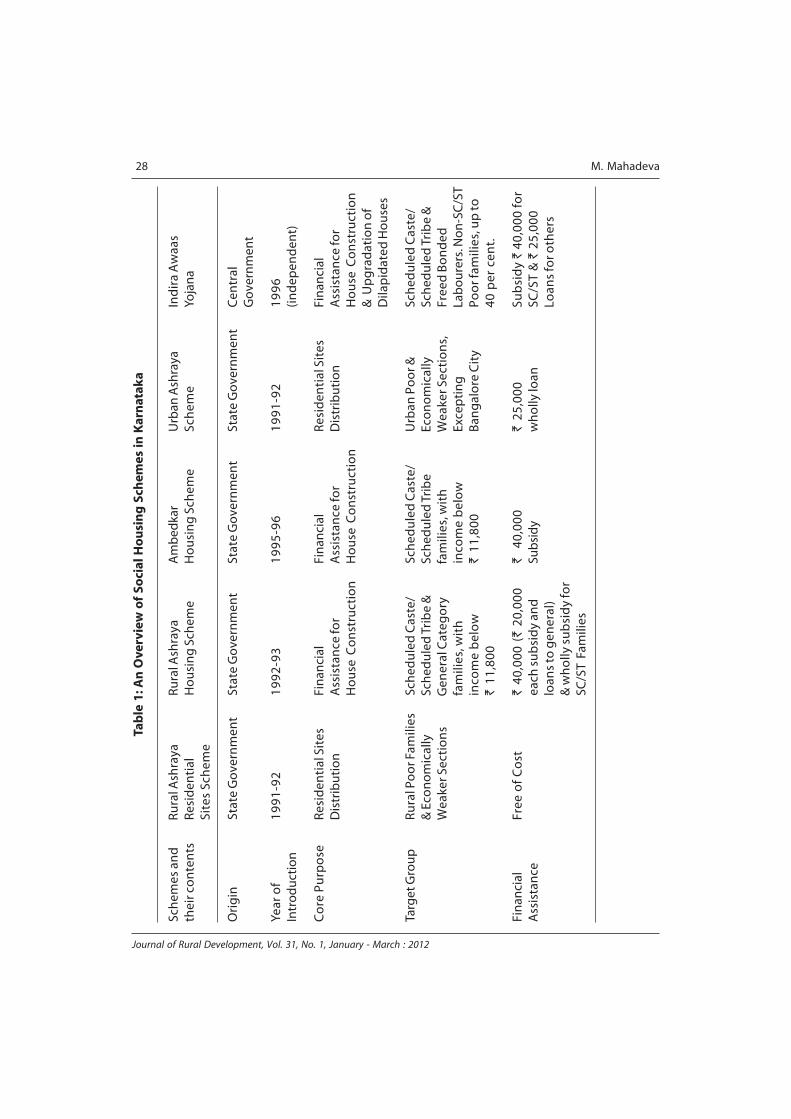

Social Housing Schemes : By design ofthe social housing schemes, the Stategovernment has been intending to achievetwo important ends of the poorer sections.First, provide residential site, which is one ofthe critical inputs of housing, for the familiesof poorer sections who want to construct theirhouses but are not prepared to do soimmediately. This strategy would giveopportunity to these families to preparethemselves and to plan their houseconstruction. Two of the schemes (RuralAshraya Residential Sites Scheme and UrbanAshraya Scheme) have been designed to

28 M. Mahadeva

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Tab

le 1

: An

Ove

rvie

w o

f So

cial

Ho

usi

ng

Sch

emes

in K

arn

atak

a

Sch

emes

an

dR

ura

l Ash

raya

Ru

ral A

shra

yaA

mb

edka

rU

rban

Ash

raya

Ind

ira

Aw

aas

thei

r co

nte

nts

Res

iden

tial

Ho

usi

ng

Sch

eme

Ho

usi

ng

Sch

eme

Sch

eme

Yoja

na

Site

s Sc

hem

e

Ori

gin

Stat

e G

ove

rnm

ent

Stat

e G

ove

rnm

ent

Stat

e G

ove

rnm

ent

Stat

e G

ove

rnm

ent

Cen

tral

Go

vern

men

t

Year

of

19

91

-92

19

92

-93

19

95

-96

19

91

-92

19

96

Intr

od

uct

ion

(in

dep

end

ent)

Co

re P

urp

ose

Res

iden

tial

Sit

esFi

nan

cial

Fin

anci

alR

esid

enti

al S

ites

Fin

anci

alD

istr

ibu

tio

nA

ssis

tan

ce fo

rA

ssis

tan

ce fo

rD

istr

ibu

tio

nA

ssis

tan

ce fo

rH

ou

se C

on

stru

ctio

nH

ou

se C

on

stru

ctio

nH

ou

se C

on

stru

ctio

n&

Up

gra

dat

ion

of

Dila

pid

ated

Ho

use

s

Targ

et G

rou

pR

ura

l Po

or F

amili

esSc

hed

ule

d C

aste

/Sc

hed

ule

d C

aste

/U

rban

Po

or &

Sch

edu

led

Cas

te/

& E

con

om

ical

lySc

hed

ule

d T

rib

e &

Sch

edu

led

Tri

be

Eco

no

mic

ally

Sch

edu

led

Tri

be

&W

eake

r Sec

tio

ns

Gen

eral

Cat

ego

ryfa

mili

es, w

ith

Wea

ker S

ecti

on

s,Fr

eed

Bo

nd

edfa

mili

es, w

ith

inco

me

bel

ow

Exce

pti

ng

Lab

ou

rers

. No

n-S

C/S

Tin

com

e b

elo

w`

11,

800

Ban

gal

ore

Cit

yP

oo

r fam

ilies

, up

to`

11,

800

40 p

er c

ent.

Fin

anci

alFr

ee o

f C

ost

` 4

0,00

0 (`

20,

000

`

40,0

00`

25,

000

Sub

sid

y `

40,

000

for

Ass

ista

nce

each

su

bsi

dy

and

Sub

sid

yw

ho

lly lo

anSC

/ST

& `

25,

000

loan

s to

gen

eral

)Lo

ans

for o

ther

s&

wh

olly

su

bsi

dy

for

SC/S

T F

amili

es

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Incremental Housing and Housing Transformation of the Poor ... 29

distribute residential sites to the poor familiesand economically weaker sections in rural andurban areas (excluding the Bangalore City) ofthe State. It may be noted that the residentialsites are distributed free of cost for the ruralbeneficiaries. Secondly, distribution of financialassistance for the houseless families owningresidential sites for house construction is theother strategy of the State. While doing so,there are no guidelines prohibiting/barringdistribution of financial assistance for thereconstruction of the existing houses by thebeneficiaries and therefore, distribution offinancial assistance for reconstruction of theexisting is also widely practised. Two schemes(Rural Ashraya Housing Scheme and AmbedkarHousing Scheme) are exclusively intended toprovide financial assistance for houseconstruction for their respective target group.Scheduled caste and scheduled tribe familiesbeing the major constituents in the totalhousing shortage of the State (Mahadeva,2008a), the beneficiaries of thesecommunities get full financial assistance in theform of subsidy under the schemes. A notablefeature of Indira Awaas Yojana, a Centrallysponsored scheme, is that it earmarks financialassistance up to 20 per cent of the totalallocation for upgradation of the houses and` 10,000 subsidy for individual beneficiaries.

Institutional Arrangement : One of thebetter reflections of the housingadministration is to establish Rajiv Gandhi RuralHousing Corporation Limited (RGRHCL) in theyear 2000 to implement all the social housingprogrammes for the economically weakersections and for the special occupationalcategories in rural and urban areas in the Stateof Karnataka with greater efficiencies inbuilding housing infrastructure in the State.The main objectives of the RGRHCL are to (a)provide affordable housing for EconomicallyWeaker Sections (EWS) in the State; (b)promote partnership with Gram Panchayat andNGOs in rural areas; (c) provide choice to

people in housing design, materials andtechnologies through self-help; (d) promotecost-effective building technologies in ruralareas through Nirmithi Kendras; (e) raiseresources and ensure recirculation of thefunds; and (f ) promote sustainable housingprogramme through encouragingbeneficiaries to save for housing and repayhousing loans. The RGRHCL has three mainstrategies to achieve its objectives viz, (a)implementing social housing schemes withself-help method, involving the beneficiaries;(b) enabling smooth flow of funds for theimplementation of the social housingschemes; (c) organising manufacture or bulkprocurement of cost-effective buildingmaterials; and (d) recovering the loans fromthe beneficiaries through a beneficiary–friendly mechanism. RGRHCL has beendesignated as a nodal agency forimplementation of the social housing schemesin the State in general and the rural areas inparticular.

Public Expenditure on Social HousingSchemes : The problem of housing of thepoorer sections cannot be solved by meredesigning a range of social housing schemesbut by financing them by public source. In fact,the success of the social housing schemesentirely depends upon financing them by theState to the extent that the higher the publicexpenditure on social housing schemes, themore the housing stock created and morebeneficial for the beneficiaries. It can be evensaid that the commitment of the State forhousing the poorer sections is better judgedby the public expenditure towards the same.In this regard, public expenditure on the socialhousing schemes has not only constantlyincreased in the State during the decade from2001-02, but is also spent to the tune of` 4677.02 crore during the period (Table 2).Interestingly, a total expenditure of ̀ 3646.18crore (78 per cent) has been incurred on theState-owned social housing schemes and the

30 M. Mahadeva

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Table 2 : Public Expenditure on Social Housing Schemes in Karnataka2001-02 to 2009-10 (Rupees in Crore)

Year Social Housing Schemes in Rural and Urban Areas

Rural Rural Indira Awaas Urban TotalAshraya Ambedkar Yojana Ashraya

2001-02 143.59* (55.97) 35.24 (13.73) The scheme was 77.75 (30.30) 256.58

2001.02 273.77 (65.31) 52.98 (12.67) not implemented 91.80 (21.92) 418.55

2002-03 230.53 (71.85) 36.83 (11.48) by RGRHCL during 53.50 (16.67) 320.86

2003-04 217.49 (75.46) 32.55 (11.29) the years. 38.17 (13.25) 288.21

2004-05 174.76 (61.74) 18.11 (06.39) 59.73 (21.11) 30.46 (10.76) 283.06

2005-06 156.01 (49.82) 13.01 (04.15) 121.50 (38.80) 22.64 (07.23) 313.16

2006-07 255.90 (63.73) 13.47 (03.35) 118.07 (29.40) 14.08 (03.52) 401.52

2007-08 617.15 (83.04) 23.26 (03.13) 99.14 (13.34) 3.63 (00.49) 743.18

2008-09 558.69 (62.08) 36.34 (04.04) 299.11 (33.24) 5.79 (00.64) 899.93

2009-10** 373.04 (49.61) 38.11 (05.07) 333.29 (44.32) 7.53 (01.00) 751.97

Total 3,000.93(64.16) 299.90 (06.41) 1,030.84 (22.05) 345.35 (7.38) 4677.02

Note: Figures in the parentheses indicate percentages to the total.

* includes the amount spent under the scheme Neralina Bhagya.

** Figures are up to January 2010.

Source : RGRHCL, Bangalore.

rest of `1030.84 crore (22 per cent) on theCentrally sponsored scheme. With this, theaverage housing expenditure works out at` 467.70 crore; this has increased from` 256.58 crore in 2001-02 to ` 751.97 crorein 2009-10. While doing so, greater impetushas been accorded to the development ofhousing in rural areas, with a total expenditureof 92.38 per cent and the same is justifiableconsidering the highest magnitude of theincidence of housing shortage in rural areasof the State. Further, across the various socialhousing schemes, given the coverage of the

beneficiaries, Rural Ashraya schemeaccounted for over 64 per cent of the totalexpenditure (` 3000.93 crore), on an average` 300 crore every year. Further, one of thesignificant features of the scheme has beenthat the public expenditure incurred isenhanced by more than two and a half foldfrom ` 143.59 crore in 2001-02 to ` 373.04crore in 2009-10 in nominal terms. However,in the relative terms, the percentage share inexpenditure has fallen from almost 56 in 2001-02 to 50 in 2009-10. Indira Awaas Yojana (IAY),the second largest scheme implemented in

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012

Incremental Housing and Housing Transformation of the Poor ... 31

the State has got a total expenditure of` 1030.84 crore in a span of six years or` 171.81 crore per year. But, unlike the RuralAshraya scheme, expenditure on the IAY hasincreased in both absolute and relative termsfrom ` 59.73 crore (21 per cent) in 2004-05to ` 333.29 crore (over 44 per cent) in 2009-10. In the case of Rural Ambedkar HousingScheme, the total expenditure incurred wasonly around ̀ 300 crore and the relative shareof the scheme is drastically reduced from 14per cent to only 5 per cent during the reviewperiod. Finally, under the Urban Ashrayascheme, a total expenditure of ̀ 345.35 crorehas been incurred and it comes to ` 34.53crore per annum or only 7.38 per cent of thetotal expenditure. The irony is that the schemewas the second largest in 2001-02 with a totalexpenditure of ̀ 77.75 crore or 30.30 per cent,but it lost its importance with a totalexpenditure of only ` 7.53 crore or just 1 percent in the total expenditure.

Impact Assessment

The impact of the social housing schemescan be better judged initially by the numberof houses constructed and the residential sitesdistributed in the State during the period ofassessment, as they mirror the politicalcommitment of the State. Secondly, nothingshould undermine the importance of the socialhousing schemes, as long as they contributeto overall improvement of welfare of thetarget group. This can be better reflected withregard to improvement in quality stock,promotion of housing privacy, improvementin housing amenities and better prospects forhousehold economic activities, as detailedbelow.

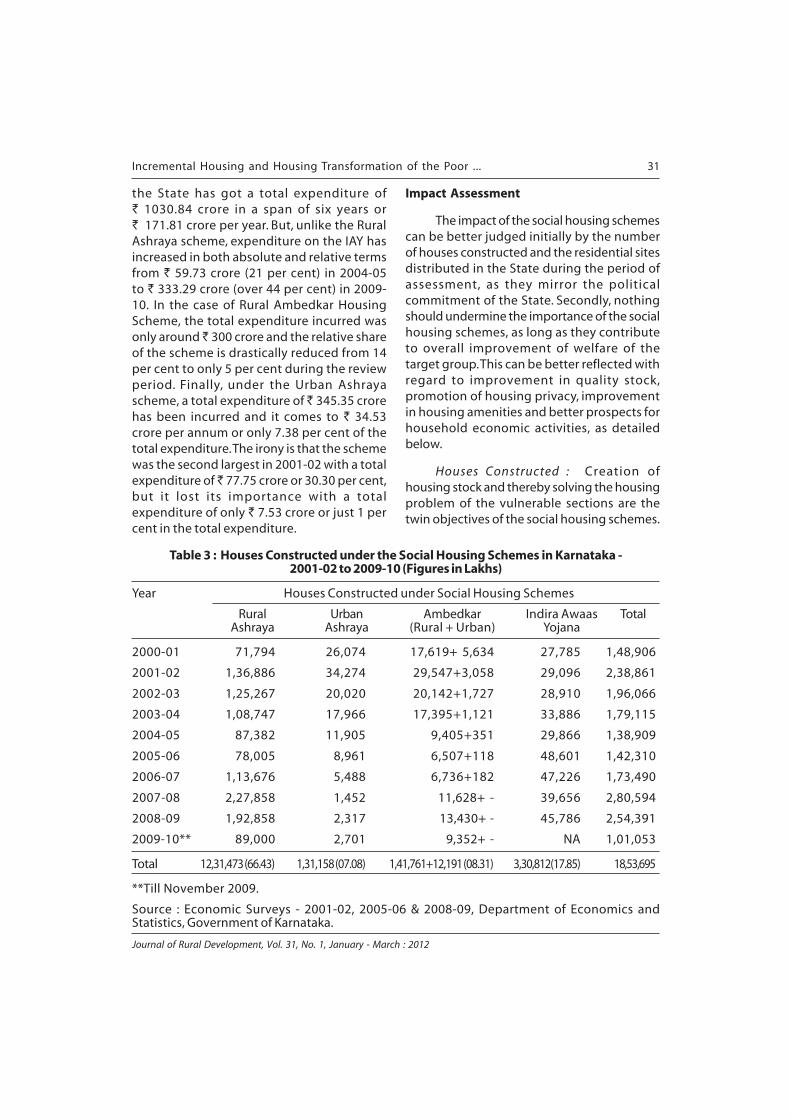

Houses Constructed : Creation ofhousing stock and thereby solving the housingproblem of the vulnerable sections are thetwin objectives of the social housing schemes.

Table 3 : Houses Constructed under the Social Housing Schemes in Karnataka -2001-02 to 2009-10 (Figures in Lakhs)

Year Houses Constructed under Social Housing Schemes

Rural Urban Ambedkar Indira Awaas TotalAshraya Ashraya (Rural + Urban) Yojana

2000-01 71,794 26,074 17,619+ 5,634 27,785 1,48,906

2001-02 1,36,886 34,274 29,547+3,058 29,096 2,38,861

2002-03 1,25,267 20,020 20,142+1,727 28,910 1,96,066

2003-04 1,08,747 17,966 17,395+1,121 33,886 1,79,115

2004-05 87,382 11,905 9,405+351 29,866 1,38,909

2005-06 78,005 8,961 6,507+118 48,601 1,42,310

2006-07 1,13,676 5,488 6,736+182 47,226 1,73,490

2007-08 2,27,858 1,452 11,628+ - 39,656 2,80,594

2008-09 1,92,858 2,317 13,430+ - 45,786 2,54,391

2009-10** 89,000 2,701 9,352+ - NA 1,01,053

Total 12,31,473 (66.43) 1,31,158 (07.08) 1,41,761+12,191 (08.31) 3,30,812(17.85) 18,53,695

**Till November 2009.

Source : Economic Surveys - 2001-02, 2005-06 & 2008-09, Department of Economics andStatistics, Government of Karnataka.

32 M. Mahadeva

Journal of Rural Development, Vol. 31, No. 1, January - March : 2012