Embed Size (px)

Citation preview

© 2015 3M. All Rights Reserved.

March 3, 2015

Inge ThulinChairman of the Board, President & Chief Executive Officer

2 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Forward Looking StatementsThis presentation contains forward-looking information about 3M's financial results and estimates and business prospects that involve substantial risks and uncertainties. You can identify these statements by the use of words such as "anticipate," "estimate,” "expect," "project," "intend," "plan," "believe," "will," "target," "forecast" and other words and terms of similar meaning in connection with any

discussion of future operating or financial performance or business plans or prospects. Among the factors that could cause actual results to differ materially are the following: (1) worldwide economic and capital markets conditions and other factors beyond 3M's control,

including natural and other disasters affecting the operations of 3M or its customers and suppliers; (2) 3M's credit ratings and its cost of capital; (3) competitive conditions and customer preferences; (4) foreign currency exchange rates and fluctuations in those rates; (5) the

timing and market acceptance of new product offerings; (6) the availability and cost of purchased components, compounds, raw materials and energy (including oil and natural gas and their derivatives) due to shortages, increased demand or supply interruptions

(including those caused by natural and other disasters and other events); (7) the impact of acquisitions, strategic alliances, divestitures, and other unusual events resulting from portfolio management actions and other evolving business strategies, and possible

organizational restructuring; (8) generating fewer productivity improvements than estimated; (9) unanticipated problems or delays with the phased implementation of a global enterprise resource planning (ERP) system, or security breaches and other disruptions to 3M's information technology infrastructure; and (10) legal proceedings, including significant developments that could occur in the legal and regulatory proceedings described in the Company's Annual Report on Form 10-K for the year ended December 31, 2014. Changes in such assumptions or factors could produce significantly different results. A further description of these factors is located in the Annual Report under “Cautionary Note Concerning Factors That May Affect Future Results” and “Risk Factors” in Part I, Items 1 and 1A. The

information contained in this presentation is as of the date indicated. The Company assumes no obligation to update any forward-looking statements contained in this presentation as a result of new information or future events or developments.

3 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Executing our playbook to create value for customers and shareholders

Investing in Innovation

Portfolio Management

Business Transformation

4 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

5 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

6 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Free Cash Flow Conversion

~100%

ROIC

~20%

Organic Revenue Growth

4-6%

EPS Growth

9-11%

We are tracking toward the objectives we established in 2012 (2013 – 2017)

Aggressive and realistic targets

7 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

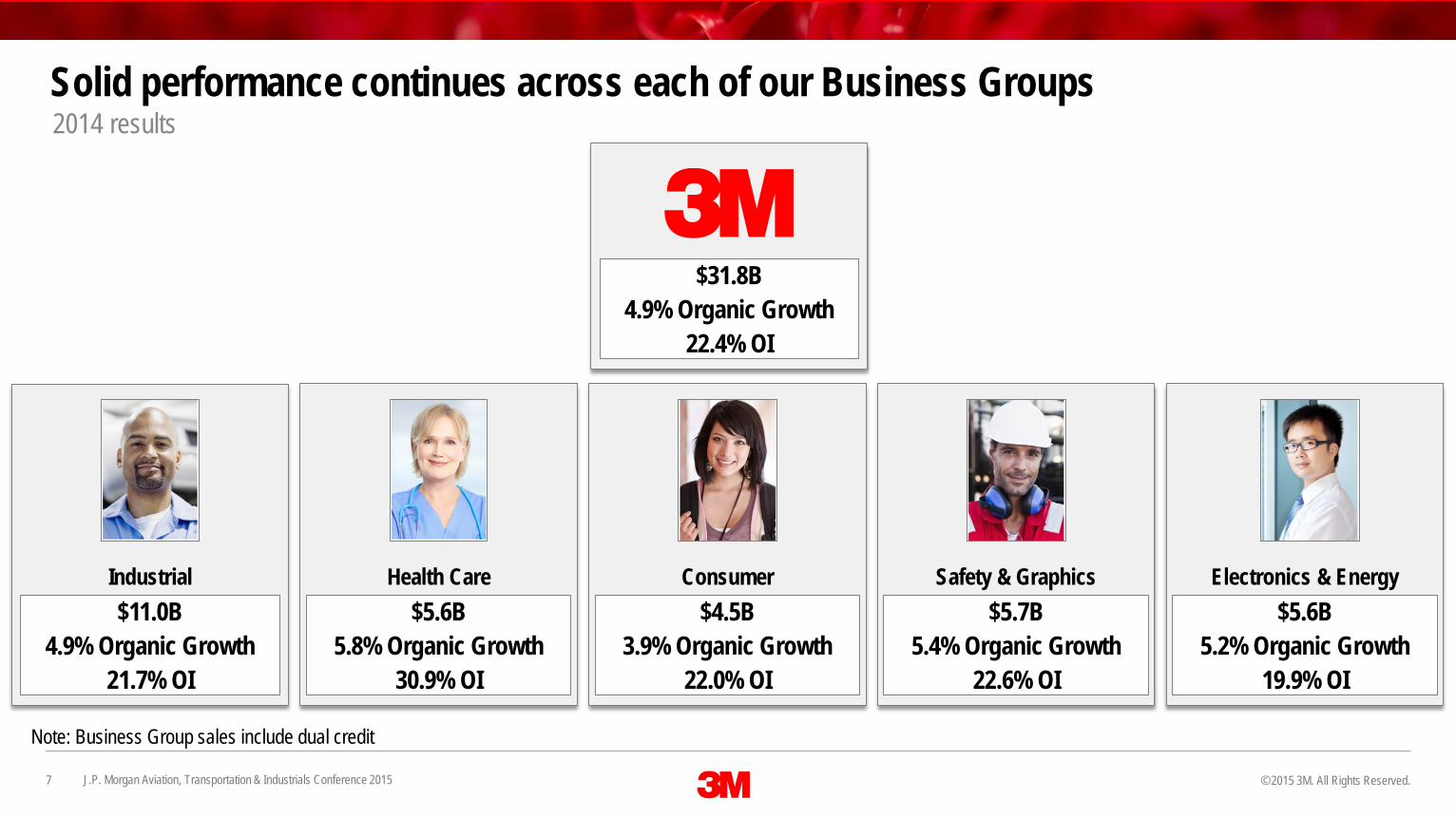

Solid performance continues across each of our Business Groups2014 results

Industrial$11.0B

4.9% Organic Growth21.7% OI

Health Care$5.6B

5.8% Organic Growth30.9% OI

Consumer$4.5B

3.9% Organic Growth22.0% OI

Safety & Graphics$5.7B

5.4% Organic Growth22.6% OI

Electronics & Energy$5.6B

5.2% Organic Growth19.9% OI

$31.8B4.9% Organic Growth

22.4% OI

Note: Business Group sales include dual credit

8 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Leveraging and building our Fundamental Strengths

Leveraging these assets creates value; strengthening them ensures our future

9 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Key levers will drive value creation going forward

Investing in Innovation Business TransformationPortfolio Management

These levers, combined with more aggressive capital deployment, will drive enhanced value creation

10 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Portfolio Management roadmap

Portfolio actions continue to create value

Continue portfolio management deployment across the corporation

Reallocate resources to 3M’s best opportunities

Augment organic growth through M&A playbookPortfolio Management

11 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

We have a stronger portfolio of businesses today than when we startedRe

lative

Stra

tegi

c Attr

activ

enes

s

Relative Shareholder Attractiveness

Strategic Review

Heartland

Push Forward

12 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

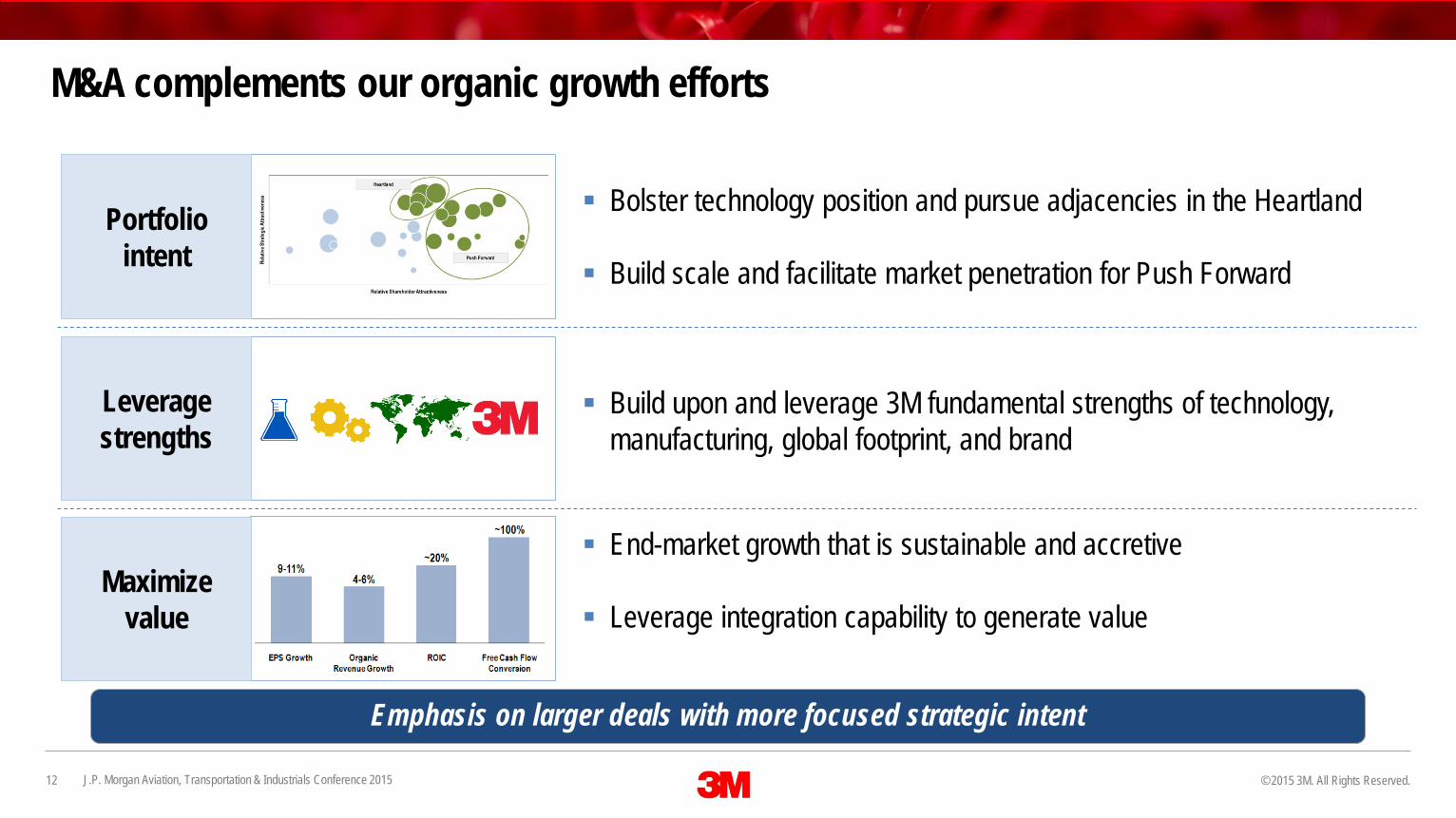

M&A complements our organic growth efforts

Emphasis on larger deals with more focused strategic intent

Portfolio intent

Leverage strengths

Maximize value

Bolster technology position and pursue adjacencies in the Heartland

Build scale and facilitate market penetration for Push Forward

Build upon and leverage 3M fundamental strengths of technology, manufacturing, global footprint, and brand

End-market growth that is sustainable and accretive

Leverage integration capability to generate value

13 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

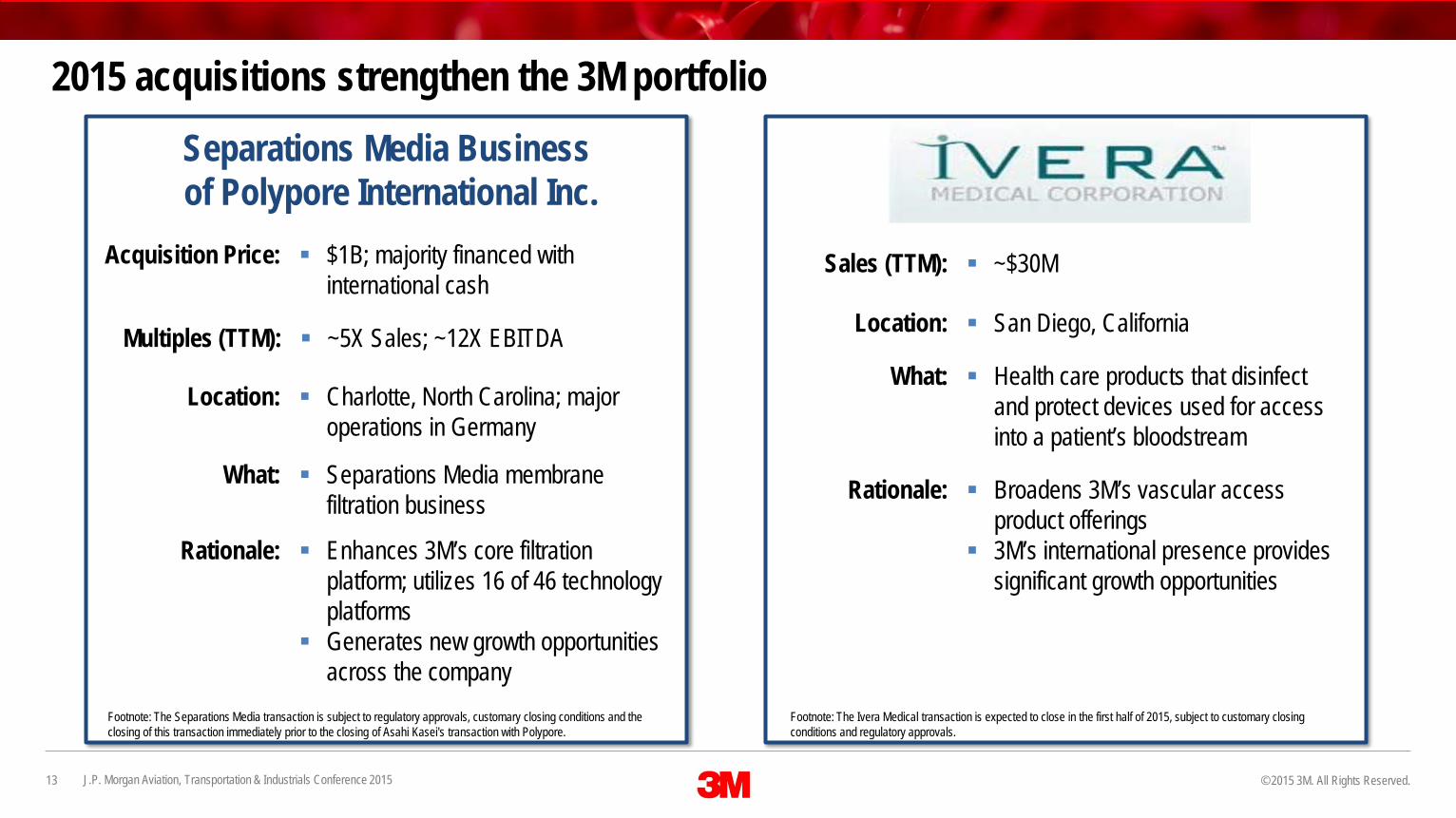

2015 acquisitions strengthen the 3M portfolio

Charlotte, North Carolina; major operations in Germany

Location:

Separations Media membrane filtration business

What:

$1B; majority financed with international cash

Acquisition Price:

Enhances 3M’s core filtration platform; utilizes 16 of 46 technology platforms

Generates new growth opportunities across the company

Rationale:

San Diego, CaliforniaLocation:

Health care products that disinfect and protect devices used for access into a patient’s bloodstream

What:

Broadens 3M’s vascular access product offerings

3M’s international presence provides significant growth opportunities

Rationale:

~5X Sales; ~12X EBITDAMultiples (TTM):

~$30MSales (TTM):

Separations Media Businessof Polypore International Inc.

Footnote: The Separations Media transaction is subject to regulatory approvals, customary closing conditions and the closing of this transaction immediately prior to the closing of Asahi Kasei's transaction with Polypore.

Footnote: The Ivera Medical transaction is expected to close in the first half of 2015, subject to customary closing conditions and regulatory approvals.

14 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Investing in Innovation roadmap

Increasing customer relevance through innovation

Enhance commercialization effectiveness through customer insights

Increase R&D investment and productivity

Build new platforms for growth by extending the core and investing in disruptive technologies

Investing in Innovation

15 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

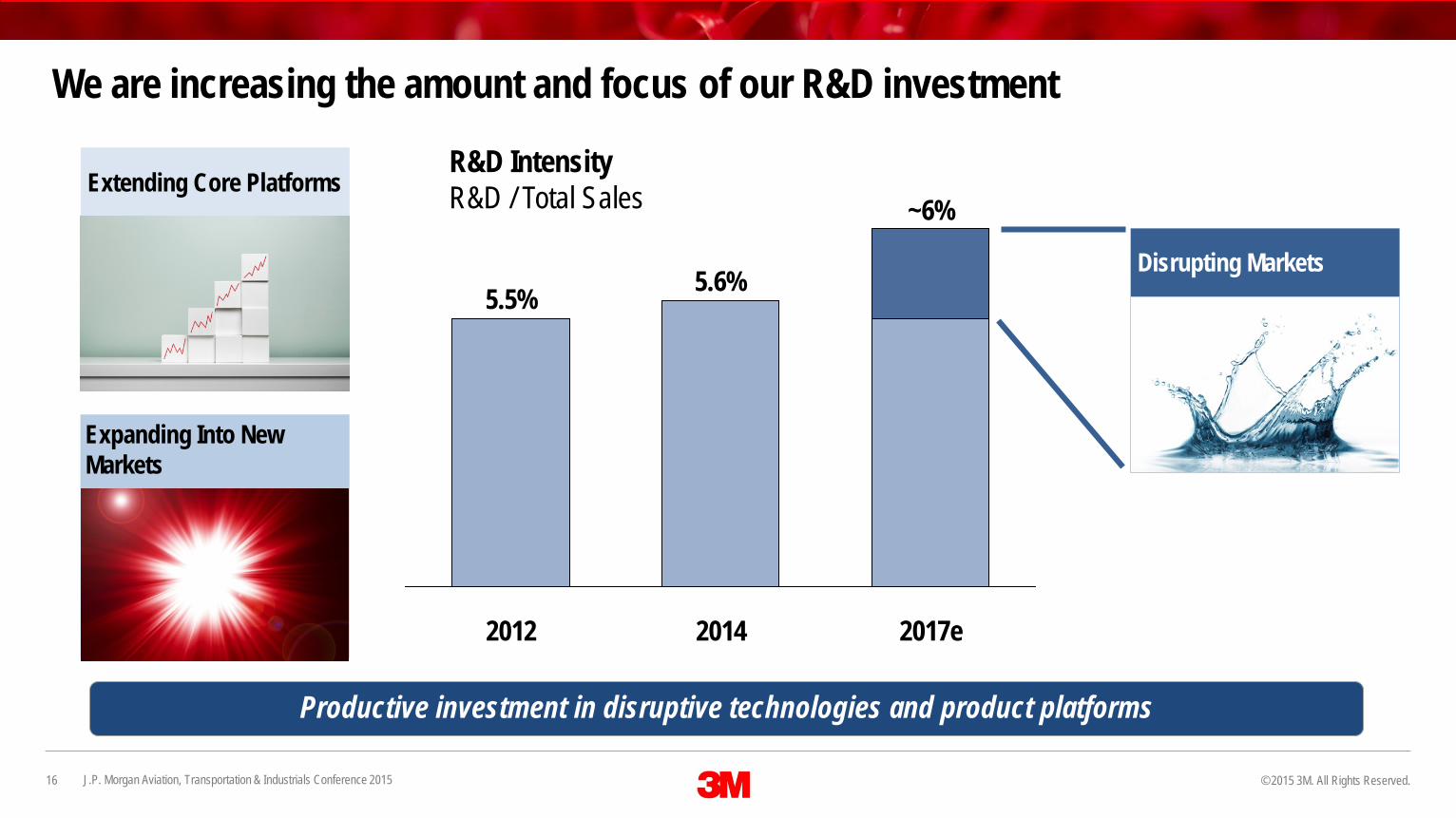

Investing in Innovation

46 technology platforms: A shared innovation engine that all businesses leverage

16 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

We are increasing the amount and focus of our R&D investment

R&D IntensityR&D / Total Sales

5.6%5.5%

2014 2017e

~6%

2012

Productive investment in disruptive technologies and product platforms

Extending Core Platforms

Expanding Into New Markets

Disrupting Markets

17 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Business Transformation roadmap

Business Transformation creating value for customers and shareholders

Realize benefits gained through ERP deployments

Deliver productivity through enhanced supply chain and manufacturing capabilities

Increase service levels to customers and reduce cost to serve

Business Transformation

18 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

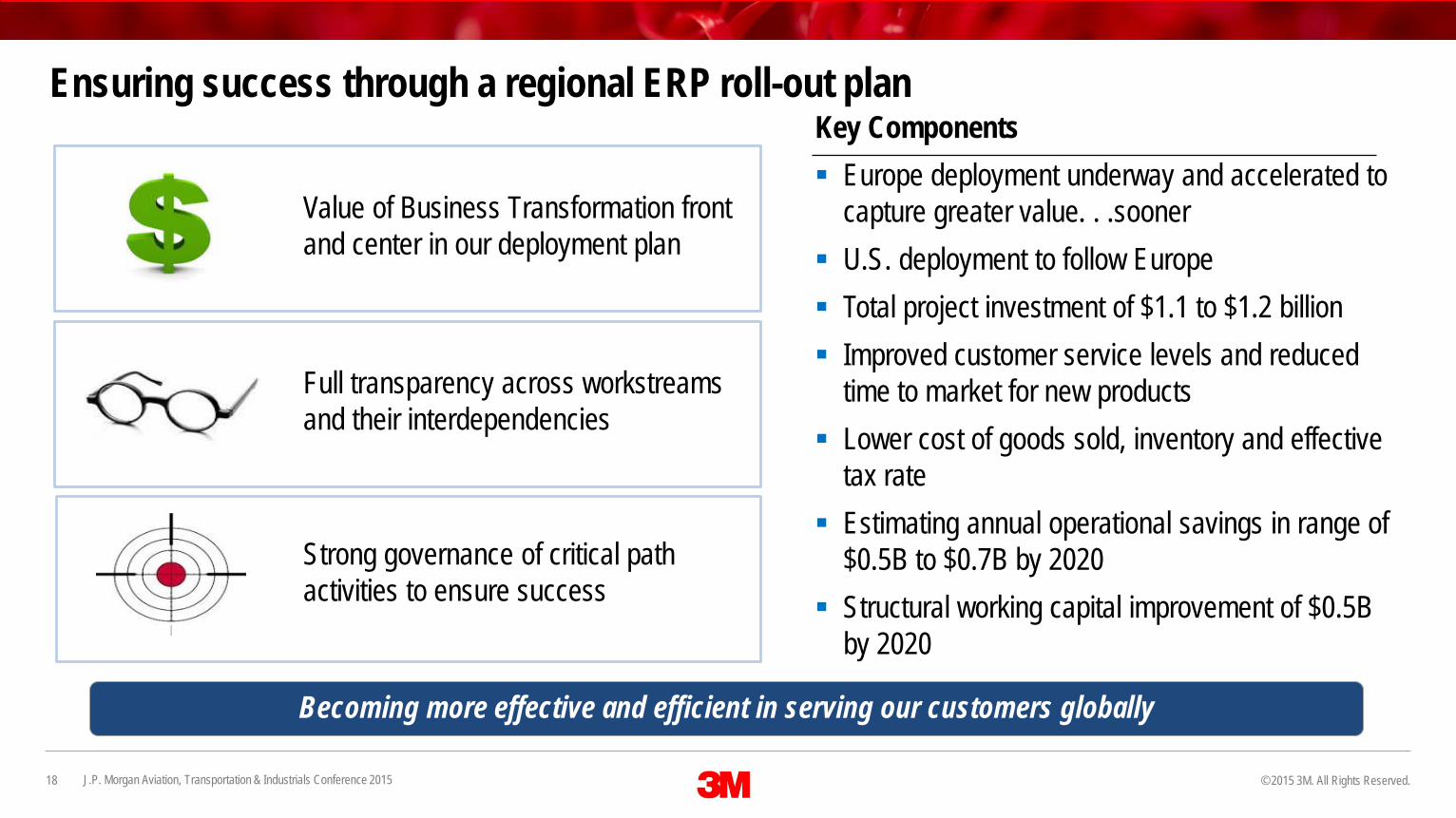

Ensuring success through a regional ERP roll-out planKey Components Europe deployment underway and accelerated to

capture greater value. . .sooner U.S. deployment to follow Europe Total project investment of $1.1 to $1.2 billion Improved customer service levels and reduced

time to market for new products Lower cost of goods sold, inventory and effective

tax rate Estimating annual operational savings in range of

$0.5B to $0.7B by 2020 Structural working capital improvement of $0.5B

by 2020

Full transparency across workstreams and their interdependencies

Strong governance of critical path activities to ensure success

Value of Business Transformation front and center in our deployment plan

Becoming more effective and efficient in serving our customers globally

19 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

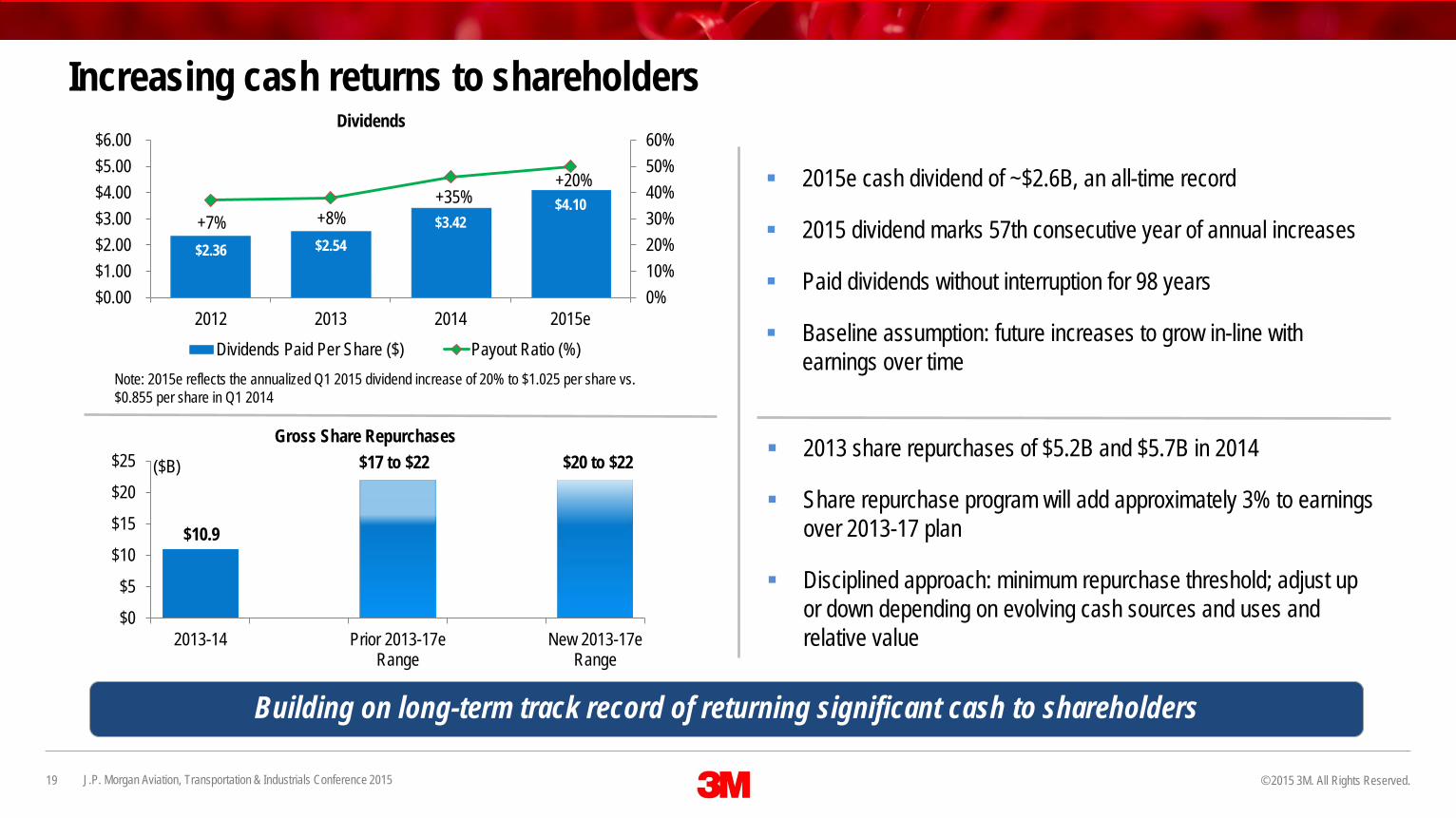

$10.9

$0

$5

$10

$15

$20

$25

2013-14 Prior 2013-17eRange

New 2013-17eRange

Gross Share Repurchases$20 to $22$17 to $22

$2.36 $2.54 $3.42

$4.10

0%10%20%30%40%50%60%

$0.00$1.00$2.00$3.00$4.00$5.00$6.00

2012 2013 2014 2015e

Dividends

Dividends Paid Per Share ($) Payout Ratio (%)

Increasing cash returns to shareholders

2015e cash dividend of ~$2.6B, an all-time record

2015 dividend marks 57th consecutive year of annual increases

Paid dividends without interruption for 98 years

Baseline assumption: future increases to grow in-line with earnings over time

Building on long-term track record of returning significant cash to shareholders

+7% +8%+35%

Note: 2015e reflects the annualized Q1 2015 dividend increase of 20% to $1.025 per share vs. $0.855 per share in Q1 2014

$15Bto

$7.5B

2013 share repurchases of $5.2B and $5.7B in 2014

Share repurchase program will add approximately 3% to earnings over 2013-17 plan

Disciplined approach: minimum repurchase threshold; adjust up or down depending on evolving cash sources and uses and relative value

($B)

+20%

20 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Strong financial results GAAP EPS of $7.49, up 11.5% year-on-year Organic local-currency sales growth +4.9% Operating margins of 22.4%, up 0.8 percentage

points year-on-year Free cash flow conversion of 104% ROIC of 22%

Investing in the business: capital expenditures $1.5 billion, R&D $1.8 billion, acquisitions $1.0 billion

Significant progress on our three key levers: portfolio management, investing in innovation, business transformation

Returned $7.9 billion to shareholders via dividends and gross share repurchases

A solid 2014 full-year performance

Refer to 3M’s January 27, 2015 press release for full details.

21 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

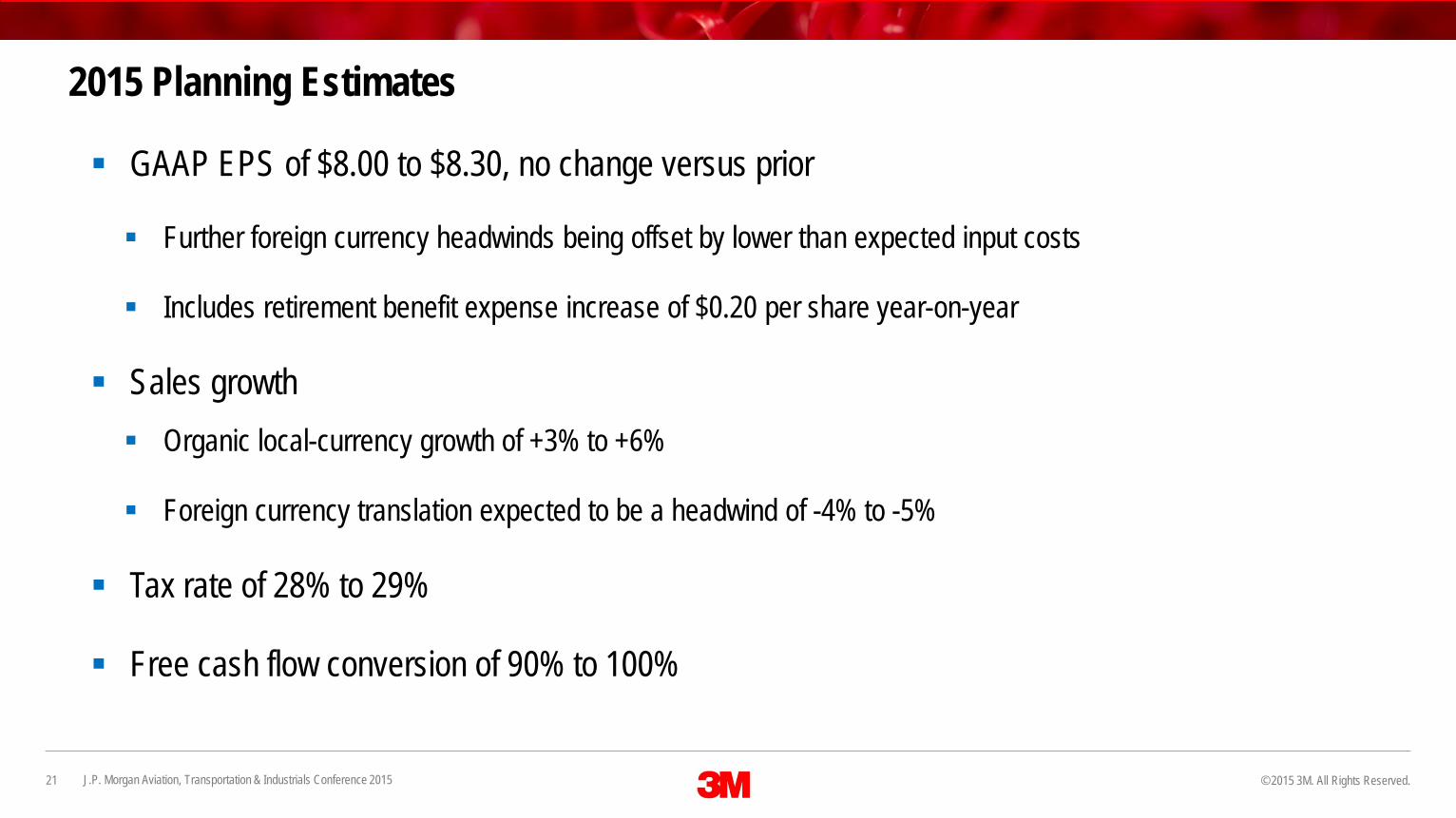

2015 Planning Estimates

GAAP EPS of $8.00 to $8.30, no change versus prior

Further foreign currency headwinds being offset by lower than expected input costs

Includes retirement benefit expense increase of $0.20 per share year-on-year

Sales growth Organic local-currency growth of +3% to +6%

Foreign currency translation expected to be a headwind of -4% to -5%

Tax rate of 28% to 29%

Free cash flow conversion of 90% to 100%

22 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

AppendixRefer to 3M's Form 8-K furnished on March 5, 2014 and 3M's Form 8-K filed on May 15, 2014 for a

discussion of the product move between business segments and other changes within business segments that were effective in the first quarter of 2014. As discussed in 3M's second-quarter Form 10-Q

filed on July 31, 2014, 3M made changes within the Electronics and Energy business segment. 3M combined three existing divisions into two new divisions, creating the Electronics Materials Solutions Division and the Display Materials and Systems Division. In addition, in October 2014, 3M merged its Personal Care Division into the Industrial Adhesives and Tapes Division. This presentation reflects the

impact of these changes for all periods presented.

23 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

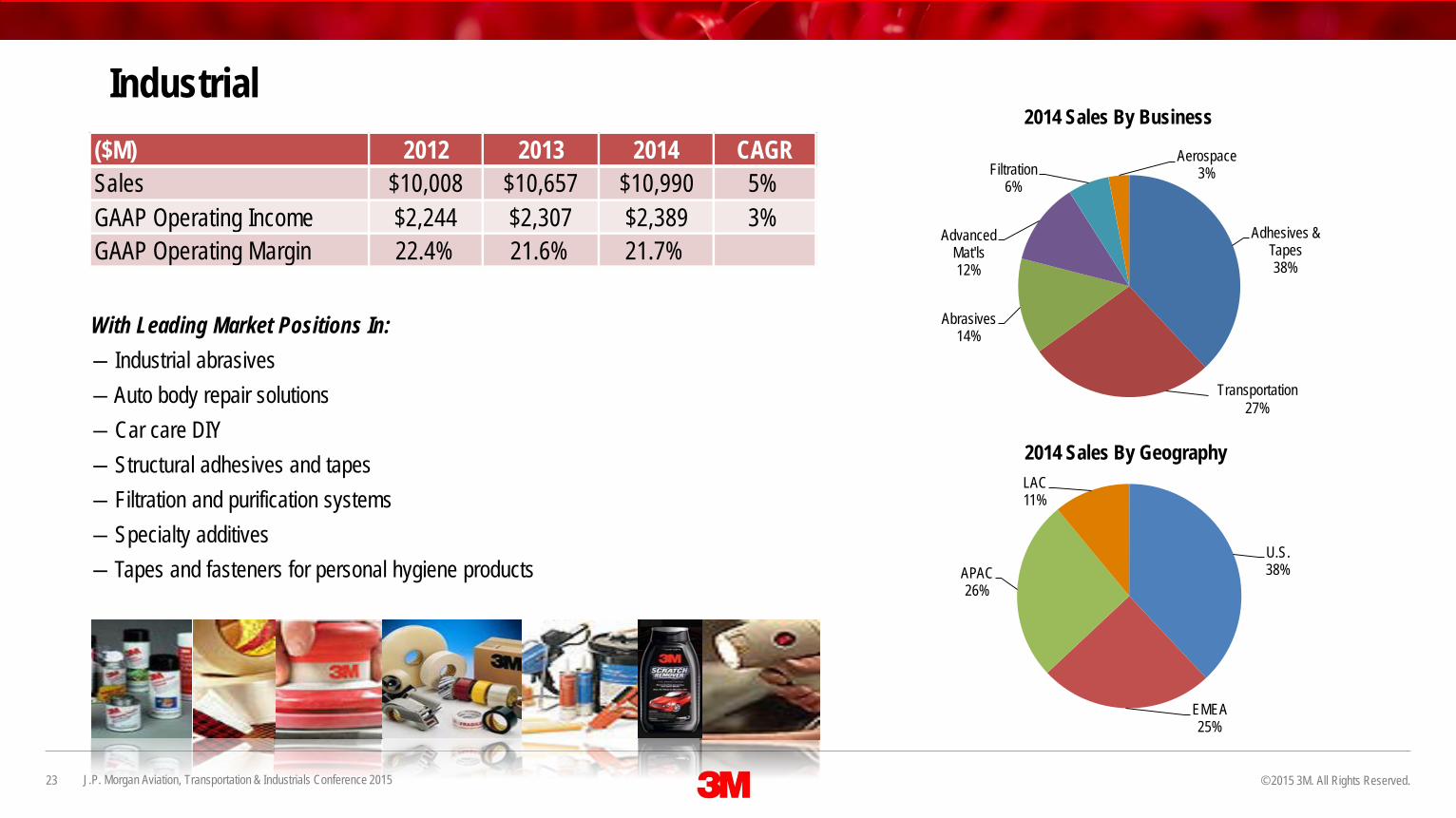

Industrial

With Leading Market Positions In:― Industrial abrasives― Auto body repair solutions― Car care DIY― Structural adhesives and tapes― Filtration and purification systems― Specialty additives― Tapes and fasteners for personal hygiene products

Adhesives & Tapes38%

Abrasives14%

Advanced Mat'ls12%

Filtration6%

Aerospace3%

Transportation 27%

U.S.38%

EMEA25%

APAC26%

LAC11%

2014 Sales By Business

2014 Sales By Geography

($M) 2012 2013 2014 CAGR Sales $10,008 $10,657 $10,990 5%GAAP Operating Income $2,244 $2,307 $2,389 3%GAAP Operating Margin 22.4% 21.6% 21.7%

24 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

Safety & Graphics

Personal Safety42%

Traffic Safety & Security

27%

Commercial Solutions

26%

Roofing granules

5%

U.S.36%

EMEA27%

APAC22%

LAC15%

2014 Sales By Business

2014 Sales By Geography

With Leading Market Positions In:― Respiratory, hearing and eye protection solutions― Reflective signage for highway and construction safety and license plates― Premium large format graphic films for advertising and fleet signage― Roofing granules for asphalt shingles― Personal identification issuance and authentication products― Building safety solutions― Architectural design solutions for surfaces and lighting applications

($M) 2012 2013 2014 CAGR Sales $5,406 $5,584 $5,732 3%GAAP Operating Income $1,210 $1,227 $1,296 3%GAAP Operating Margin 22.4% 22.0% 22.6%

25 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

U.S.17%

EMEA12%

APAC64%

LAC7%

2014 Sales By Business

2014 Sales By Geography

Display Matls & Systems

38%

Electronics Matls

Solutions24%

Electrical Markets

23%

Telecom8%

Renewable Energy

7%

Electronics & Energy

With Leading Market Positions In:― Optically clear adhesives, Novec™ fluorochemicals, transport solutions and flexible

circuits for electronic components― Light management films that enhance brightness and provide energy efficiency in

liquid crystal displays (LCD)― Electrical vinyl rubber and mastic tapes― Medium voltage cable accessories, OEM insulation tapes― Telecommunications copper splicing ― Fiber splicing/connectivity

($M) 2012 2013 2014 CAGR Sales $5,458 $5,393 $5,604 1%GAAP Operating Income $1,026 $954 $1,115 4%GAAP Operating Margin 18.8% 17.7% 19.9%

26 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

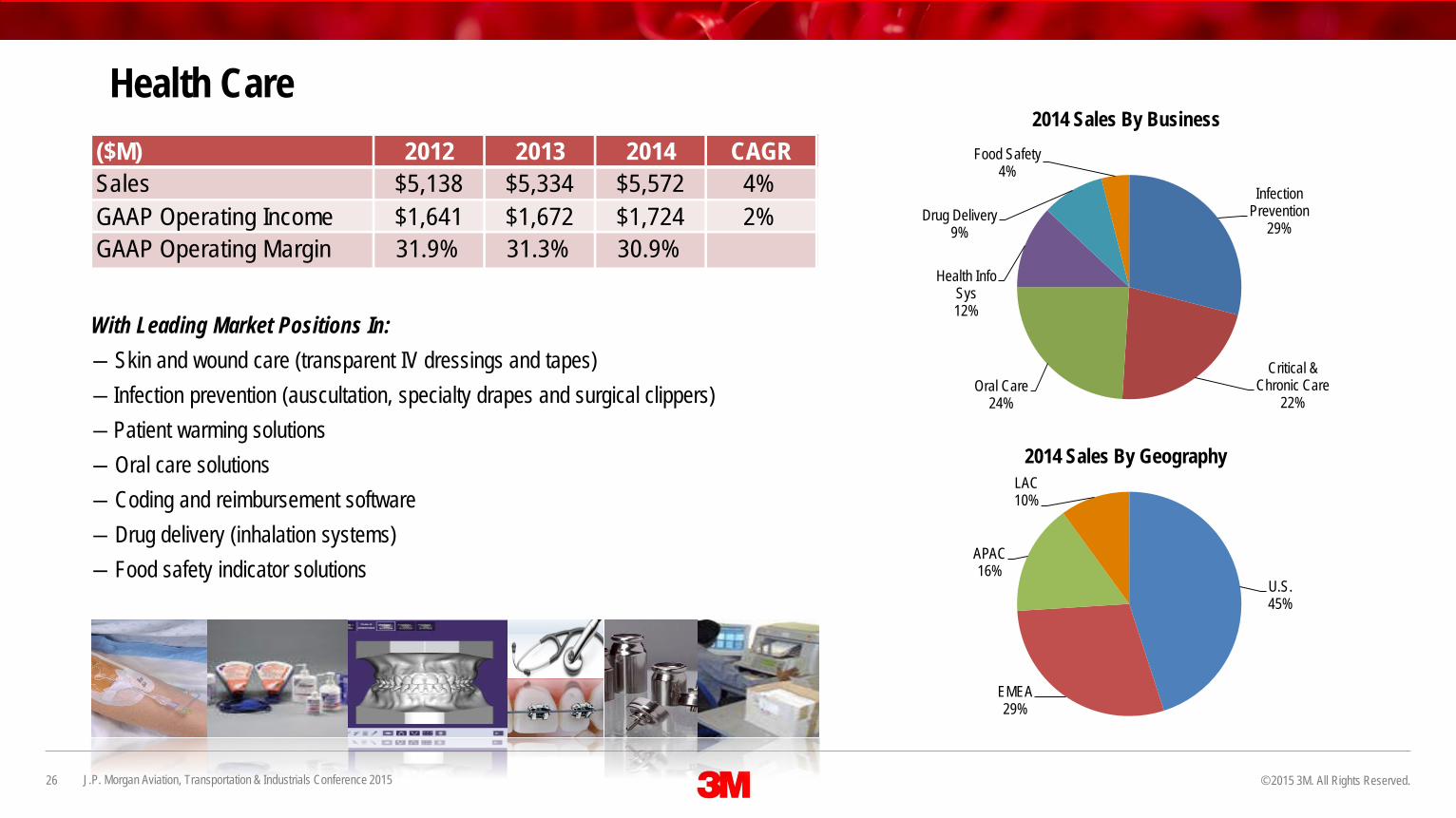

Health Care

Infection Prevention

29%

Critical & Chronic Care

22%Oral Care

24%

Health Info Sys12%

Drug Delivery9%

Food Safety4%

U.S.45%

EMEA29%

APAC16%

LAC10%

2014 Sales By Business

2014 Sales By Geography

With Leading Market Positions In:― Skin and wound care (transparent IV dressings and tapes)― Infection prevention (auscultation, specialty drapes and surgical clippers)― Patient warming solutions― Oral care solutions― Coding and reimbursement software― Drug delivery (inhalation systems)― Food safety indicator solutions

($M) 2012 2013 2014 CAGR Sales $5,138 $5,334 $5,572 4%GAAP Operating Income $1,641 $1,672 $1,724 2%GAAP Operating Margin 31.9% 31.3% 30.9%

27 © 2015 3M. All Rights Reserved.J.P. Morgan Aviation, Transportation & Industrials Conference 2015

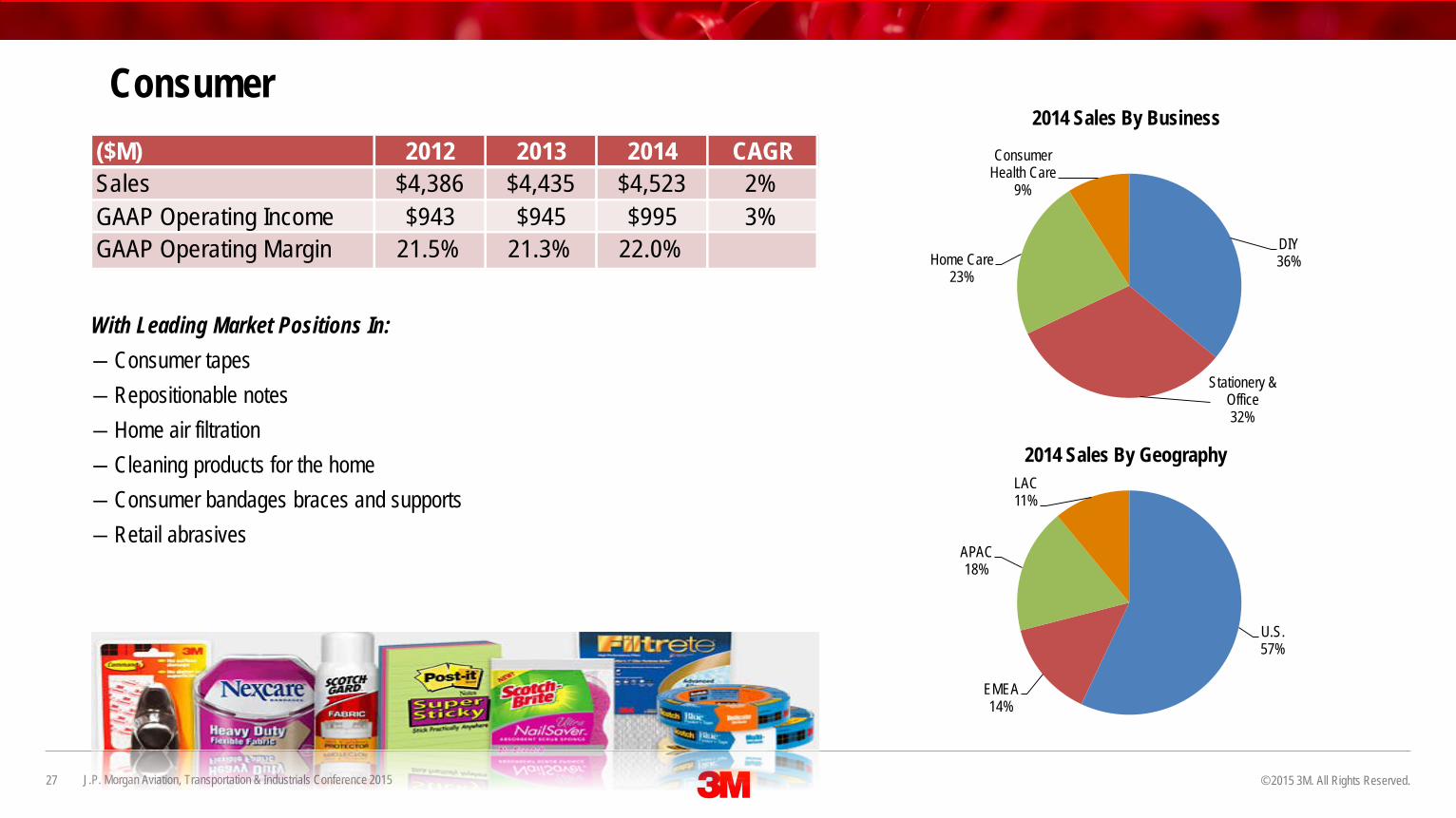

Consumer

U.S.57%

EMEA14%

APAC18%

LAC11%

2014 Sales By Business

2014 Sales By Geography

DIY36%

Stationery & Office32%

Home Care23%

Consumer Health Care

9%

With Leading Market Positions In:― Consumer tapes― Repositionable notes― Home air filtration― Cleaning products for the home― Consumer bandages braces and supports― Retail abrasives

($M) 2012 2013 2014 CAGR Sales $4,386 $4,435 $4,523 2%GAAP Operating Income $943 $945 $995 3%GAAP Operating Margin 21.5% 21.3% 22.0%

© 2015 3M. All Rights Reserved.