Embed Size (px)

Citation preview

31st Annual Conference of The International Organization of Securities Commissions (IOSCO)

8th June 2006 Hong Kong

Panel 3: Bond Markets – Should Their Transparency be Enhanced?

Michele Faissola

Managing Director, Global Head of Rates Deutsche Bank AG, United Kingdom

Bond Markets: Should Transparency Be Enhanced? Michele Faissola, Deutsche Bank Head of Global Rates

IOSCO Annual ConferenceHong Kong, 8 June 2006

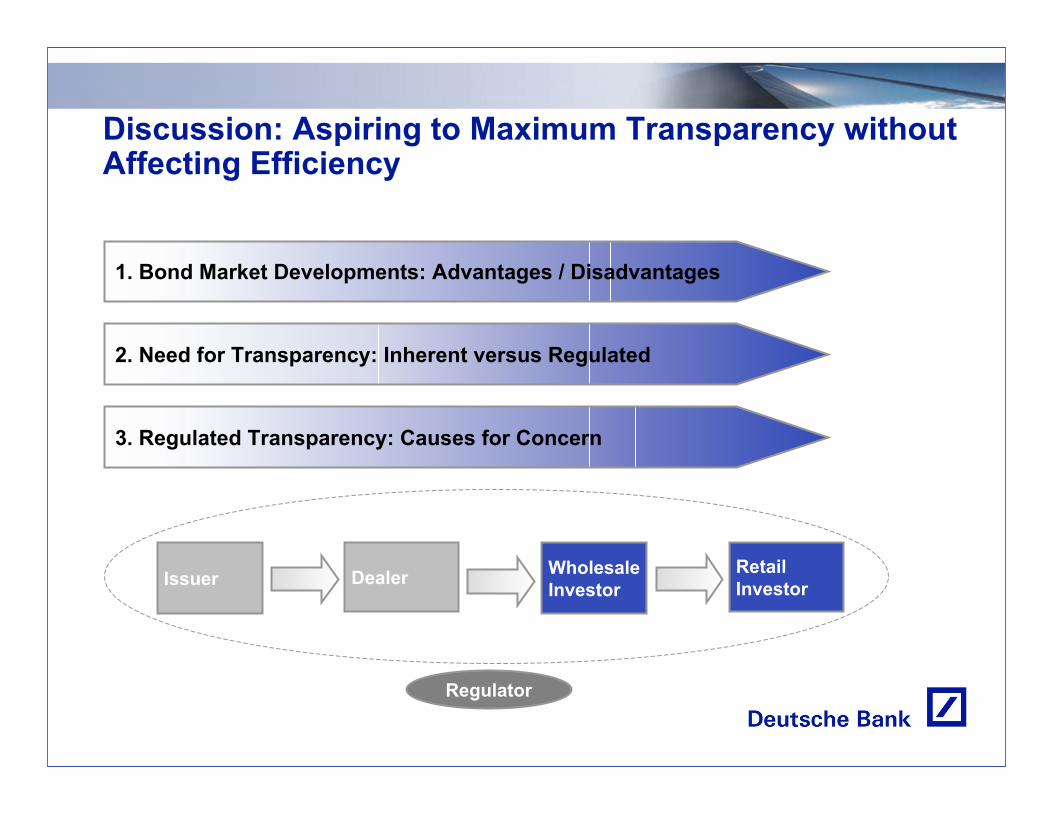

Discussion: Aspiring to Maximum Transparency without Affecting Efficiency

1. Bond Market Developments: Advantages / Disadvantages

2. Need for Transparency: Inherent versus Regulated

3. Regulated Transparency: Causes for Concern

Issuer Dealer WholesaleInvestor

Retail Investor

Regulator

Bond Market Developments

Bond Market DevelopmentsA Brief History of Structured Products

Early 1990s 2001 onwards1994-1996 1997-2000

Big BangSimple structured products

Range accrualsInverse floatersVanilla options

Ice AgeStructured products market into hibernation

Bronze AgeResurgence in exoticsIncreasingly sophisticated clientsStructured products established as separate asset class

Digital AgeLow interest ratesTechnology advances leading to hybrid and multi asset productsDramatic growth

Bond Market DevelopmentsInnovation Broadens Financing for Borrowers

Flexible instruments available to borrowersDifferent risks, tenors, maturities, and payouts broaden financing opportunities

Innovation

New market Opportunities for capital raisingFinancing made available more cheaply

Access

Issuers have access to different capital structuresAll segments of the economy have benefited

Leverage

AutomotiveInsuranceWaterTelecommunicationsEnergy production & DistributionRetailOil & GasTrading/LeasingConsumer Electronics/appliancesAerospace & DefenceReal EstateFood/Beverages/TobaccoDiversified industrialTransportConstruction & Building MaterialsForestry productsMediaChemicals

Segment4,5444,4902,0871,8821,3821,2509237165463672832762398074746128

US $ mn702656

2279

7049113322253

No of MTNs

Source: MTN-I

Bond Market DevelopmentsInnovation Has Allowed New Market Segments to BorrowMTN issuance 2000 – 2005

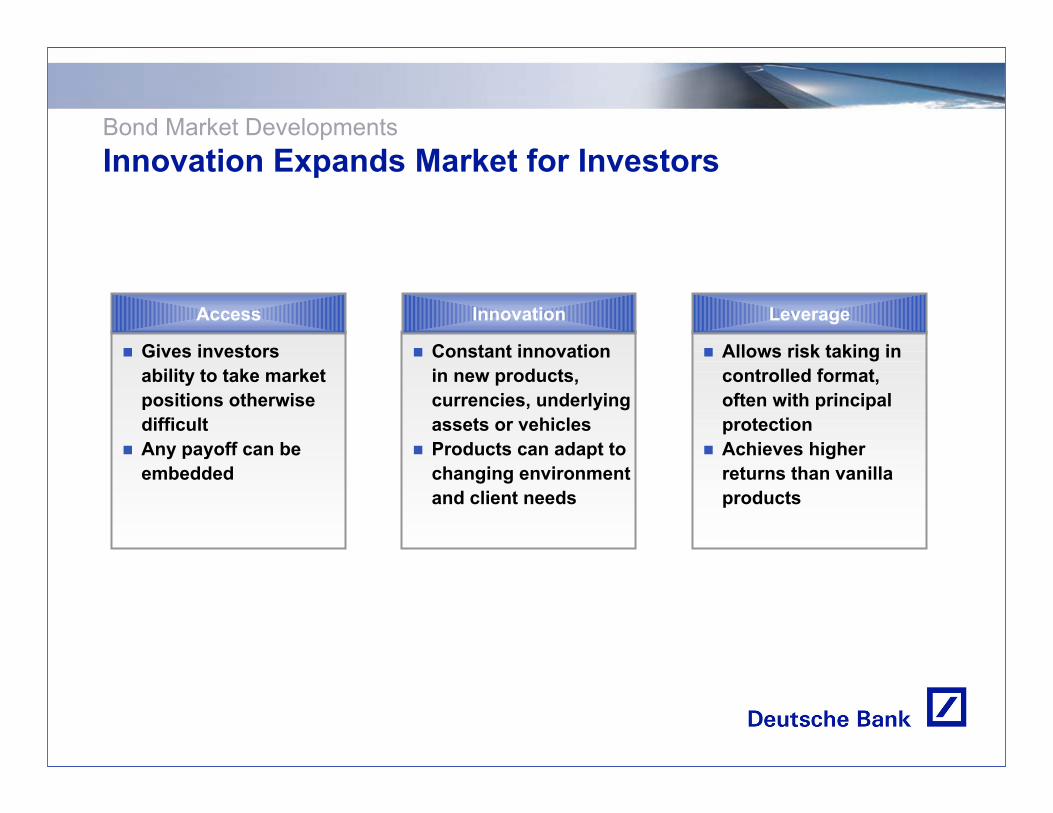

Bond Market DevelopmentsInnovation Expands Market for Investors

Constant innovationin new products, currencies, underlyingassets or vehiclesProducts can adapt to changing environmentand client needs

Innovation

Gives investorsability to take marketpositions otherwisedifficult Any payoff can be embedded

Access

Allows risk taking incontrolled format, often with principalprotectionAchieves higher returns than vanilla products

Leverage

Bond Market DevelopmentsInvestor Sophistication Drives Dynamic Market Growth

Global Bond Issuance

Source: Dealogic / BondwareNoteData for North America not available

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2000 2001 2002 2003 2004 2005

Europe Asia Pacific Americas

Global Capital Distribution in 2005

0%

20%

40%

60%

80%

100%Tier I Upper Tier II Lower Tier II

Europe Asia Pacific

€ tn

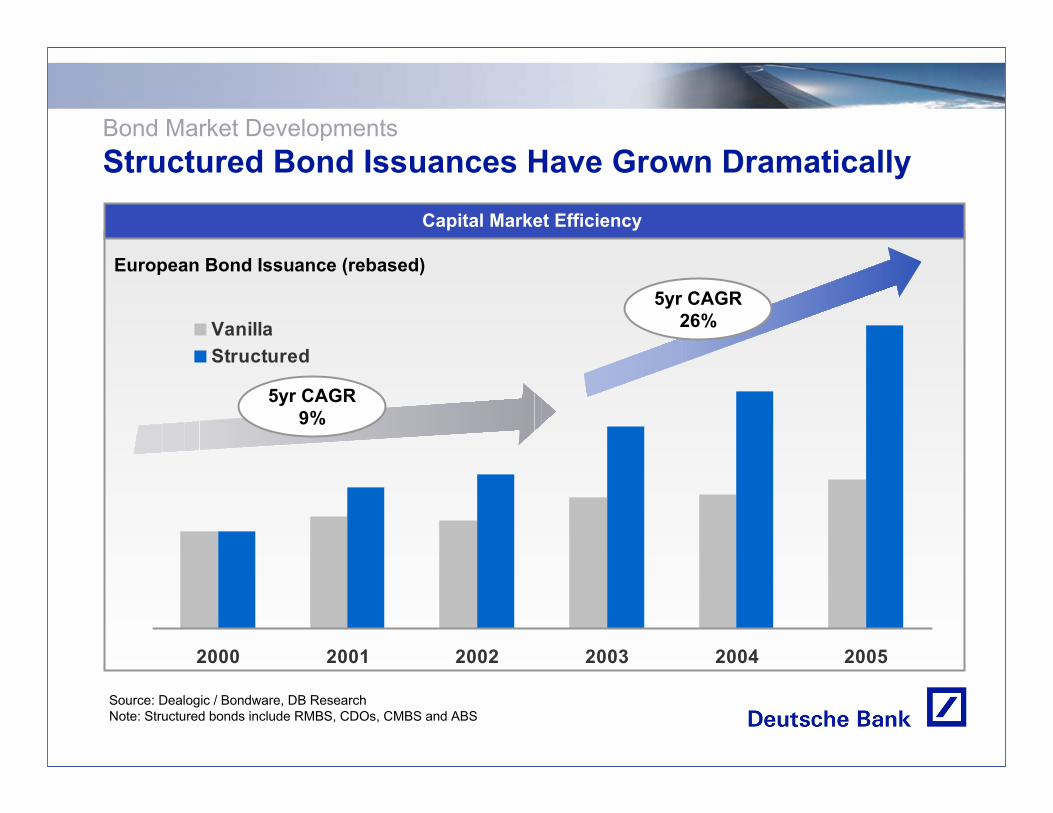

Capital Market Efficiency

Source: Dealogic / Bondware, DB ResearchNote: Structured bonds include RMBS, CDOs, CMBS and ABS

2000 2001 2002 2003 2004 2005

VanillaStructured

European Bond Issuance (rebased)

Bond Market DevelopmentsStructured Bond Issuances Have Grown Dramatically

5yr CAGR9%

5yr CAGR26%

Need for Transparency – Inherent vs. Regulated

Need for Transparency: Inherent vs. RegulatedTechnology Creates Transparency

Pricing TransparencyE-trading Volume by Client Segment

Source: Bond Markets Association

25%

24%

19%

57%

55%

36%

33%

28%

0% 20% 40% 60%

Retail/CommercialBank

Private Bank

Asset Management

Primary Dealers

Pension Fund

Insurance

Central Bank/Treasury

Hedge Fund

Market place electronification has created significant transparency across all asset classes, resulting in massive decrease in bid-offer spreads

76% of buy-side firms now execute over 40% of overall trading volume electronically

65% of buy-side firms and 81% of sell-side have seen their electronic volume trading increase by over 20% over the past 2 years

Price transparency is quoted as the most important factor in opting for electronic trading

US Cash Equities

Prime Brokerage

Commodities

Residential Mortgage Backed Securities

Emerging Markets

Capital Structure Regulation Flexibility

Need for Transparency: Inherent vs. RegulatedCapital Raising Activity is Already Highly Regulated

AB/ Non Recourse

Tier 2

Tier 1

ShareholderEquity

SeniorUnsecured

Regulated Transparency: Causes for Concern

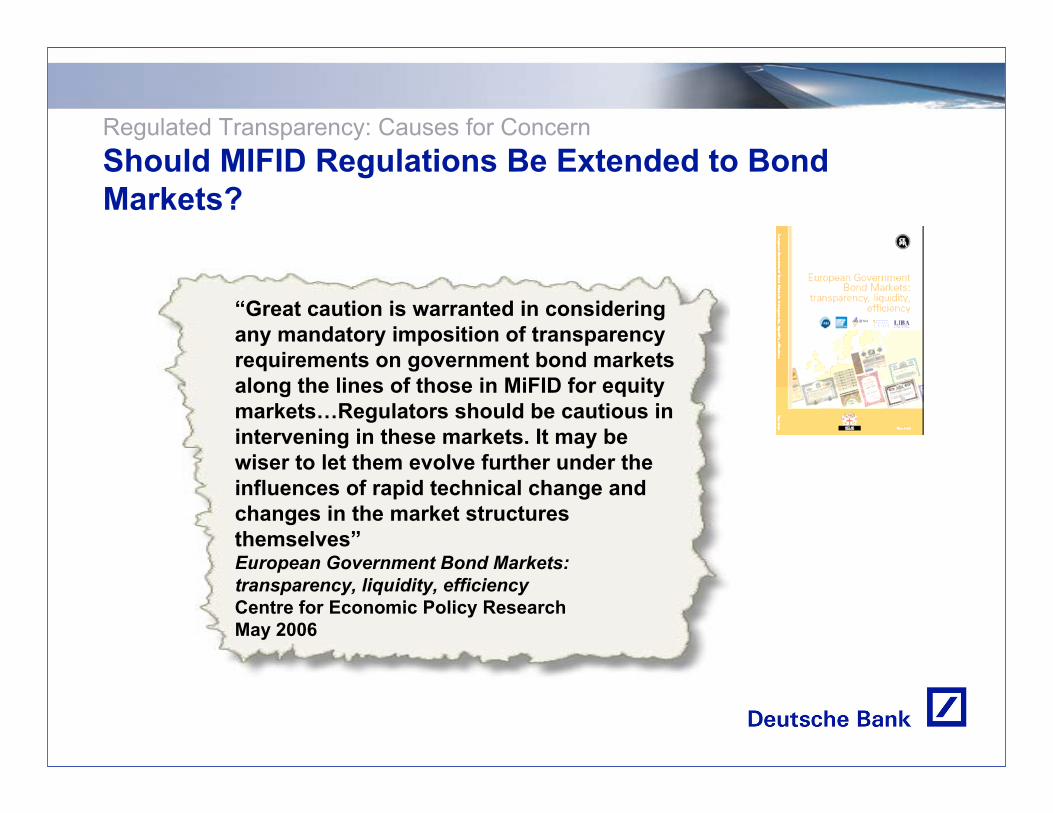

Regulated Transparency: Causes for ConcernShould MIFID Regulations Be Extended to Bond Markets?

“Great caution is warranted in considering any mandatory imposition of transparency requirements on government bond markets along the lines of those in MiFID for equity markets…Regulators should be cautious in intervening in these markets. It may be wiser to let them evolve further under the influences of rapid technical change and changes in the market structures themselves”European Government Bond Markets: transparency, liquidity, efficiencyCentre for Economic Policy ResearchMay 2006

![GMM ESTIMATION WITH PERSISTENT PANEL …uctp39a/blundell-Bond-ER.pdf · Downloaded By: [University College London] At: 16:01 25 June 2007 324 BLUNDELL AND BOND The model has a dynamic](https://img.pdfslide.us/doc/110x75/5b6ee5957f8b9a58578b7fdf/gmm-estimation-with-persistent-panel-uctp39ablundell-bond-erpdf-downloaded.jpg)