Embed Size (px)

Citation preview

25th Annual Health Sciences Tax conferenceTransfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

December 8, 2015

Page 1 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Disclaimer

► EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

► This presentation is © 2015 Ernst & Young LLP. All rights reserved. No part of this document may be reproduced, transmitted or otherwise distributed in any form or by any means, electronic or mechanical, including by photocopying, facsimile transmission, recording, rekeying, or using any information storage and retrieval system, without written permission from Ernst & Young LLP. Any reproduction, transmission or distribution of this form or any of the material herein is prohibited and is in violation of US and international law. Ernst & Young LLP expressly disclaims any liability in connection with use of this presentation or its contents by any third party.

► Views expressed in this presentation are those of the speakers and do not necessarily represent the views of Ernst & Young LLP.

► This presentation is provided solely for the purpose of enhancing knowledge on tax matters. It does not provide tax advice to any taxpayer because it does not take into account any specific taxpayer’s facts and circumstances.

► These slides are for educational purposes only and are not intended, and should not be relied upon, as accounting advice.

Page 2 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Presenters

► Collin ImhofCelgene CorporationBerkeley Heights, NJ

► Bob PepeFormerly at Forest Laboratories Inc. and Pernix Therapeutics Holdings, Inc.

► Barbara AngusErnst & Young LLPWashington, [email protected]+1 202 327 5824

► Gerrit GroenErnst & Young LLPNew York, [email protected]+1 212 773 8627

► Siv SchultzErnst & Young LLPNew York, NY [email protected]+1 212 773 3818

Page 3 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Agenda

► Update on Organisation for Economic Co-operation and Development (OECD) BEPS project

► BEPS final reports – Immediate impacts to life sciences industry► Intangibles► Cost sharing► Risk and return► Transfer pricing documentation

► Reactions outside the US► Status of adoption of BEPS► Actions 8-10► Action 13

► Conclusions

Page 4 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Update on OECD BEPS project

Page 5 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

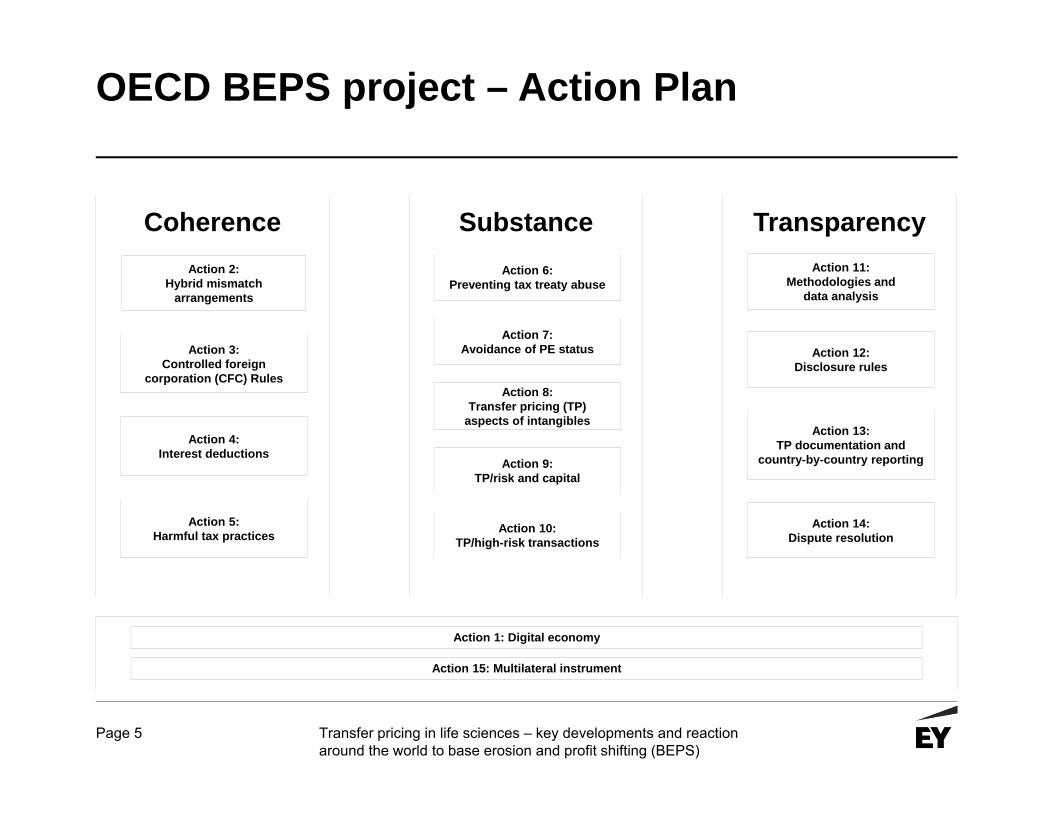

OECD BEPS project – Action Plan

SubstanceAction 6:

Preventing tax treaty abuse

Action 7:Avoidance of PE status

Action 8:Transfer pricing (TP)

aspects of intangibles

Action 9:TP/risk and capital

Action 10:TP/high-risk transactions

TransparencyAction 11:

Methodologies and data analysis

Action 12:Disclosure rules

Action 13:TP documentation and

country-by-country reporting

Action 14:Dispute resolution

Action 1: Digital economy

Action 15: Multilateral instrument

Coherence

Action 3: Controlled foreign

corporation (CFC) Rules

Action 4:Interest deductions

Action 5:Harmful tax practices

Action 2:Hybrid mismatch

arrangements

Page 6 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

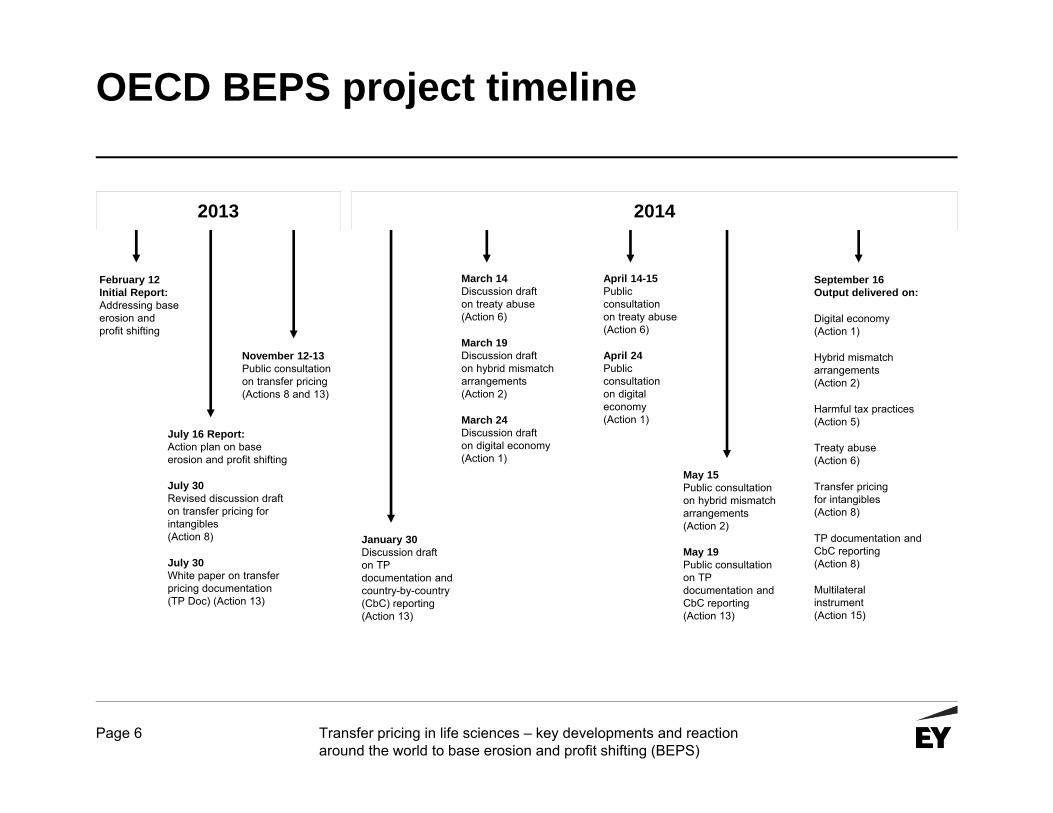

OECD BEPS project timeline

February 12Initial Report:Addressing base erosion andprofit shifting

November 12-13Public consultationon transfer pricing(Actions 8 and 13)

July 16 Report:Action plan on baseerosion and profit shifting

July 30Revised discussion drafton transfer pricing forintangibles(Action 8)

July 30White paper on transferpricing documentation(TP Doc) (Action 13)

January 30Discussion drafton TP documentation andcountry-by-country(CbC) reporting(Action 13)

March 14Discussion drafton treaty abuse(Action 6)

March 19Discussion drafton hybrid mismatcharrangements(Action 2)

March 24Discussion drafton digital economy(Action 1)

April 14-15Publicconsultationon treaty abuse(Action 6)

April 24Publicconsultationon digitaleconomy(Action 1)

May 15Public consultationon hybrid mismatcharrangements(Action 2)

May 19Public consultationon TP documentation and CbC reporting(Action 13)

September 16Output delivered on:

Digital economy(Action 1)

Hybrid mismatcharrangements(Action 2)

Harmful tax practices(Action 5)

Treaty abuse(Action 6)

Transfer pricingfor intangibles(Action 8)

TP documentation andCbC reporting(Action 8)

Multilateralinstrument(Action 15)

2013 2014

Page 7 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

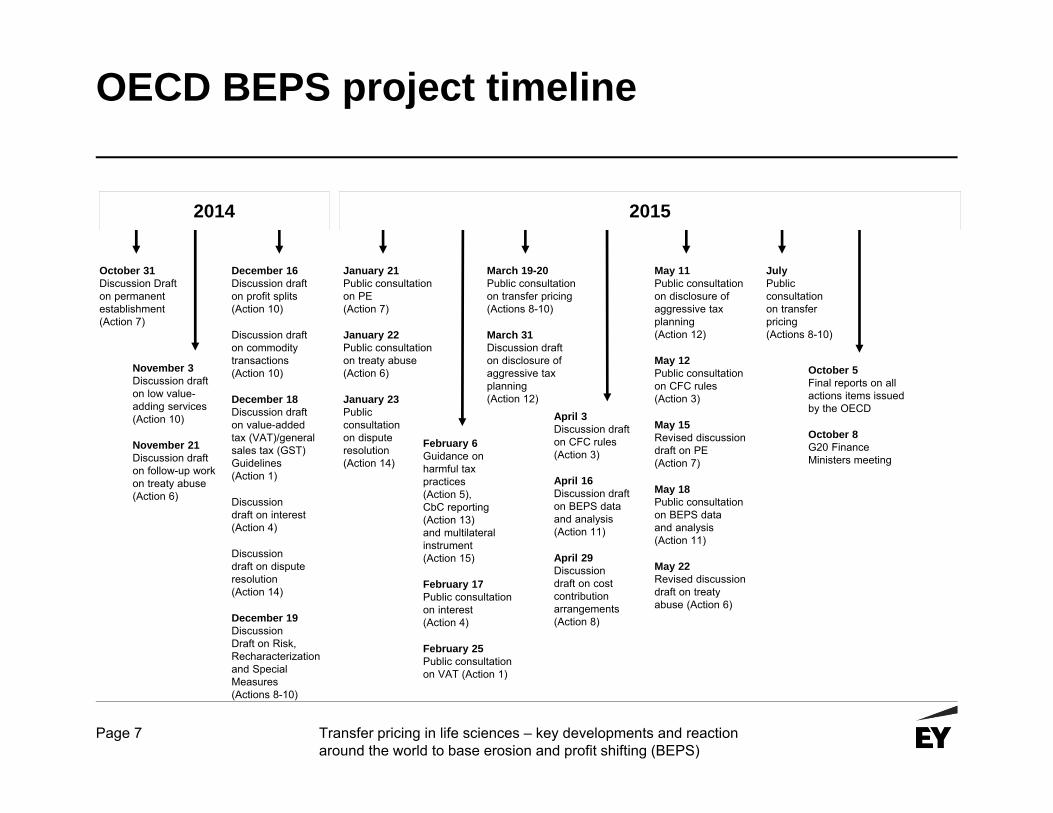

OECD BEPS project timeline

October 31Discussion Drafton permanentestablishment(Action 7)

2014 2015

November 3Discussion drafton low value-adding services(Action 10)

November 21Discussion drafton follow-up workon treaty abuse(Action 6)

December 16Discussion drafton profit splits(Action 10)

Discussion drafton commoditytransactions(Action 10)

December 18Discussion drafton value-added tax (VAT)/general sales tax (GST)Guidelines(Action 1)

Discussiondraft on interest(Action 4)

Discussiondraft on disputeresolution(Action 14)

December 19DiscussionDraft on Risk,Recharacterizationand Special Measures(Actions 8-10)

January 21Public consultationon PE(Action 7)

January 22Public consultationon treaty abuse(Action 6)

January 23Publicconsultationon disputeresolution(Action 14)

February 6Guidance onharmful taxpractices(Action 5),CbC reporting(Action 13)and multilateralinstrument(Action 15)

February 17Public consultationon interest(Action 4)

February 25Public consultationon VAT (Action 1)

March 19-20Public consultationon transfer pricing(Actions 8-10)

March 31Discussion drafton disclosure ofaggressive taxplanning(Action 12)

April 3Discussion drafton CFC rules(Action 3)

April 16Discussion drafton BEPS dataand analysis(Action 11)

April 29Discussiondraft on costcontributionarrangements(Action 8)

May 11Public consultationon disclosure ofaggressive taxplanning(Action 12)

May 12Public consultationon CFC rules(Action 3)

May 15Revised discussiondraft on PE(Action 7)

May 18Public consultationon BEPS dataand analysis (Action 11)

May 22Revised discussiondraft on treatyabuse (Action 6)

JulyPublicconsultationon transferpricing(Actions 8-10)

October 5Final reports on all actions items issued by the OECD

October 8G20 FinanceMinisters meeting

Page 8 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

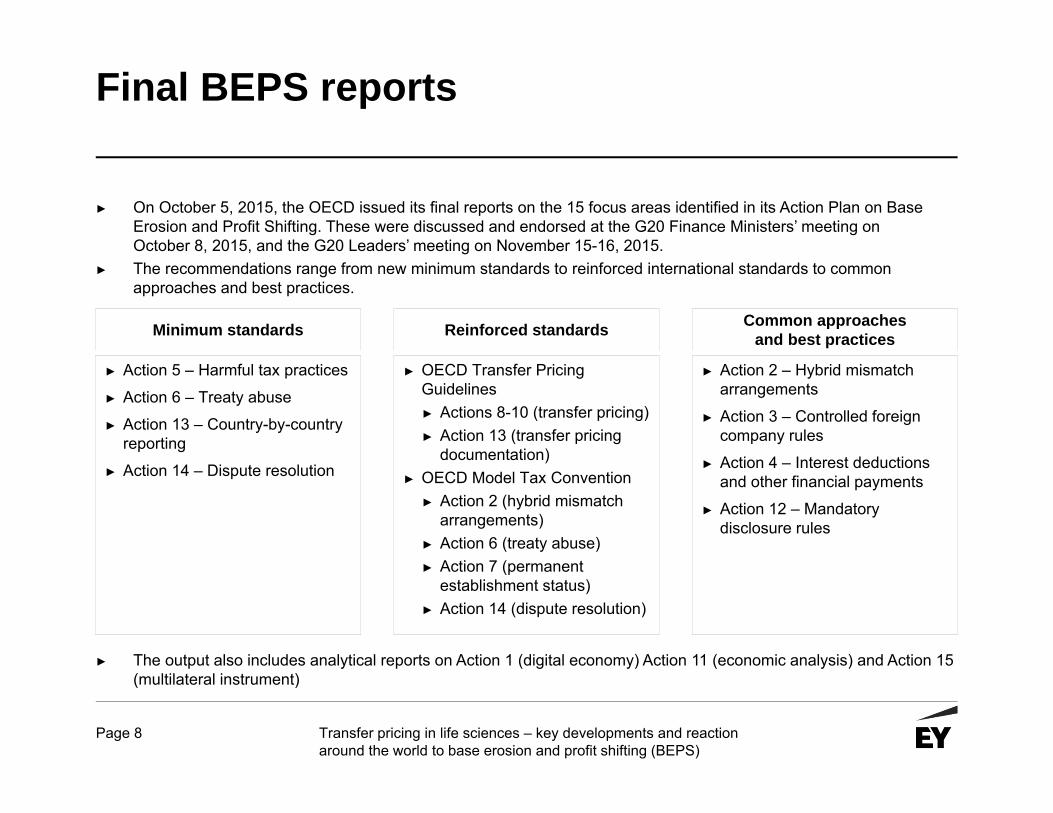

Final BEPS reports

► On October 5, 2015, the OECD issued its final reports on the 15 focus areas identified in its Action Plan on Base Erosion and Profit Shifting. These were discussed and endorsed at the G20 Finance Ministers’ meeting on October 8, 2015, and the G20 Leaders’ meeting on November 15-16, 2015.

► The recommendations range from new minimum standards to reinforced international standards to common approaches and best practices.

Common approaches and best practicesMinimum standards Reinforced standards

► Action 2 – Hybrid mismatch arrangements

► Action 3 – Controlled foreign company rules

► Action 4 – Interest deductions and other financial payments

► Action 12 – Mandatory disclosure rules

► Action 5 – Harmful tax practices

► Action 6 – Treaty abuse

► Action 13 – Country-by-country reporting

► Action 14 – Dispute resolution

► OECD Transfer Pricing Guidelines► Actions 8-10 (transfer pricing)► Action 13 (transfer pricing

documentation)► OECD Model Tax Convention

► Action 2 (hybrid mismatch arrangements)

► Action 6 (treaty abuse)► Action 7 (permanent

establishment status)► Action 14 (dispute resolution)

► The output also includes analytical reports on Action 1 (digital economy) Action 11 (economic analysis) and Action 15 (multilateral instrument)

Page 9 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

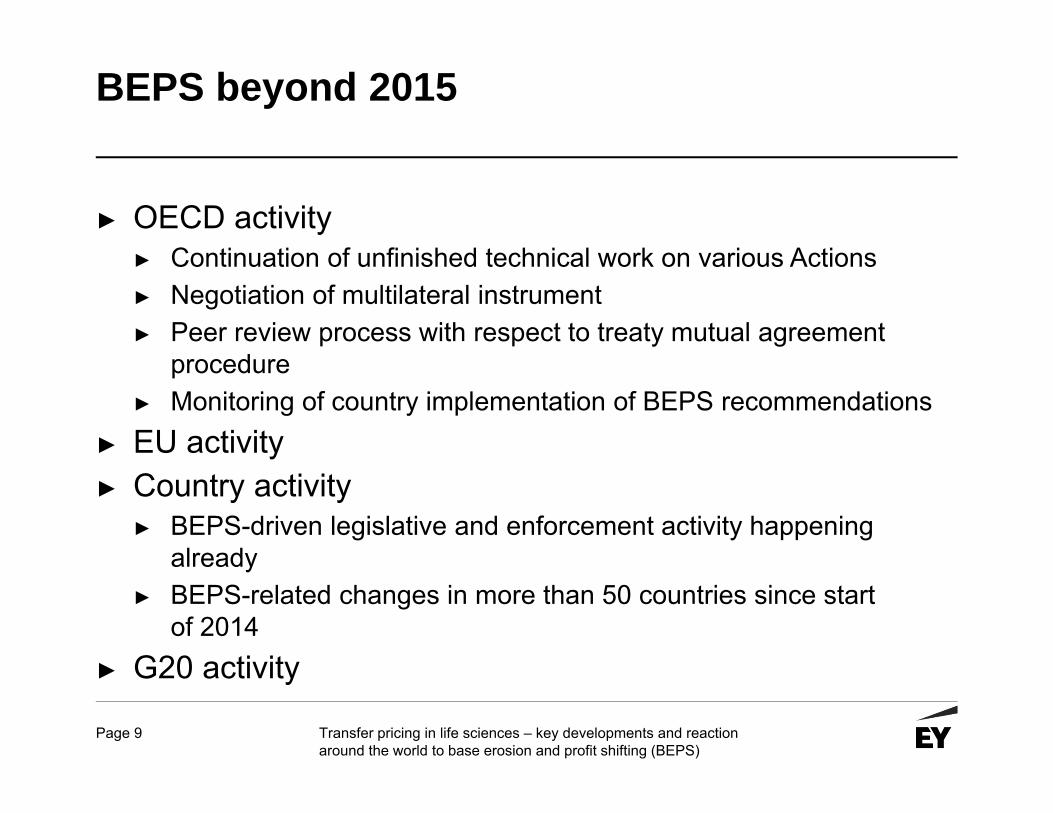

BEPS beyond 2015

► OECD activity► Continuation of unfinished technical work on various Actions► Negotiation of multilateral instrument► Peer review process with respect to treaty mutual agreement

procedure► Monitoring of country implementation of BEPS recommendations

► EU activity► Country activity

► BEPS-driven legislative and enforcement activity happening already

► BEPS-related changes in more than 50 countries since start of 2014

► G20 activity

Page 10 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

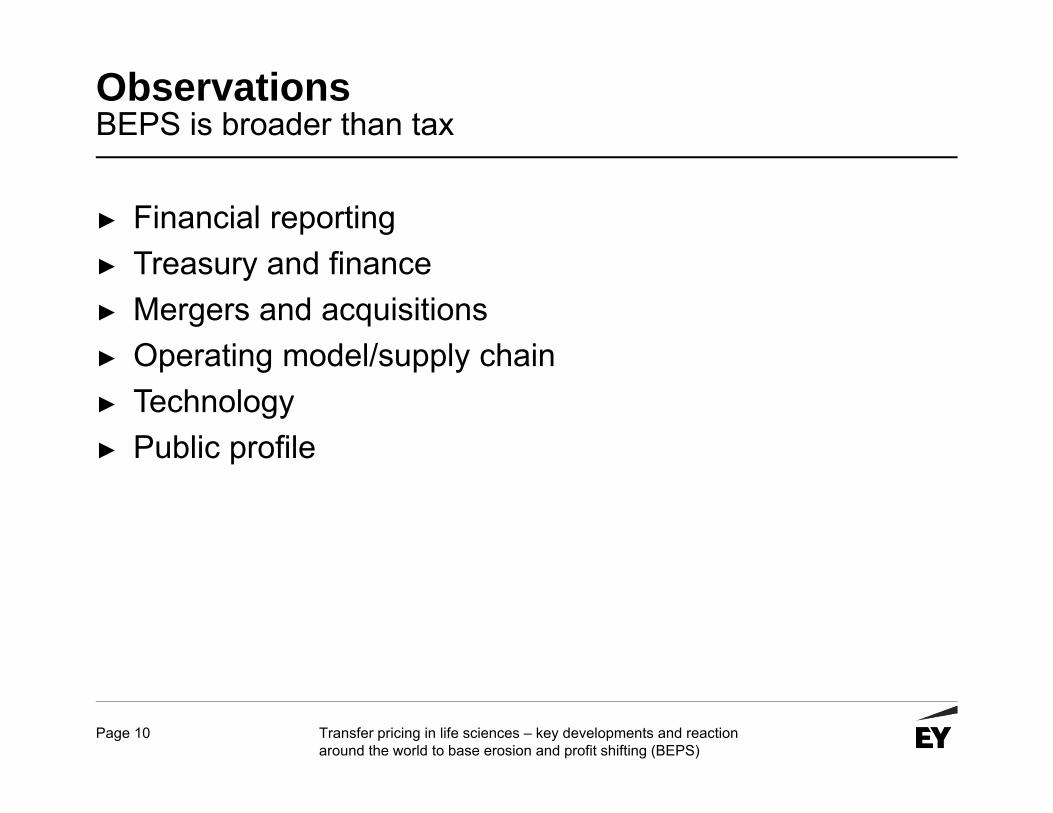

ObservationsBEPS is broader than tax

► Financial reporting► Treasury and finance► Mergers and acquisitions► Operating model/supply chain► Technology► Public profile

Page 11 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

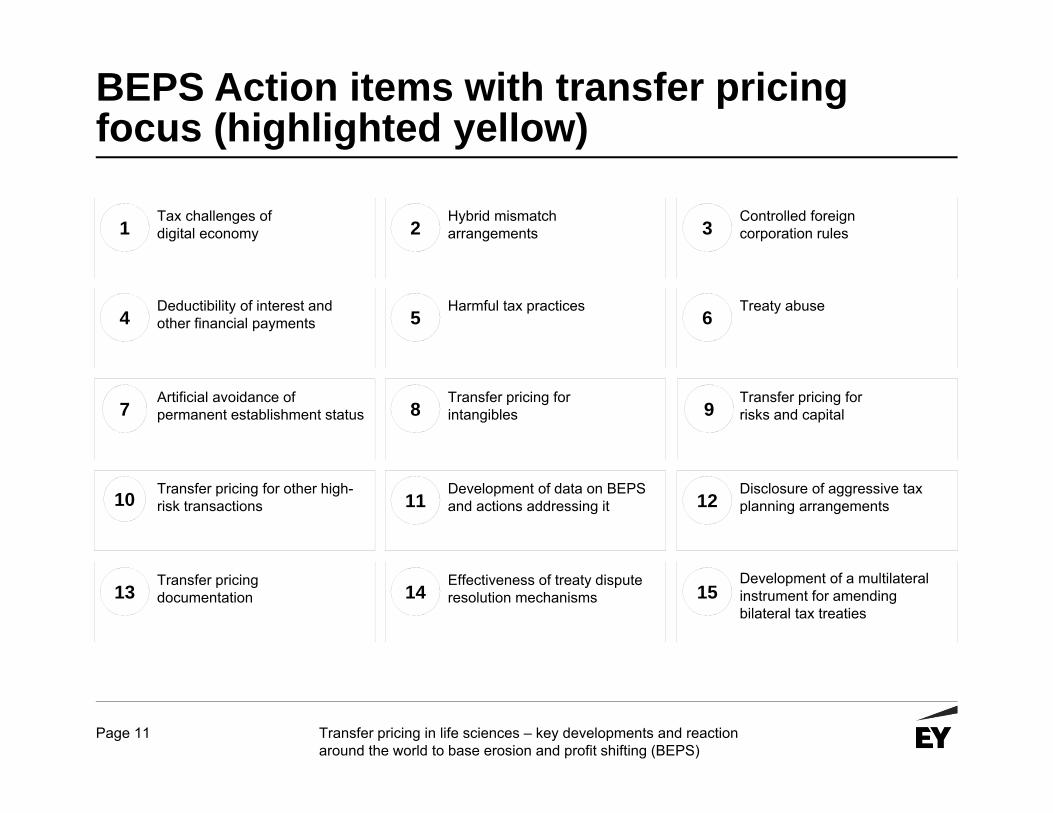

BEPS Action items with transfer pricing focus (highlighted yellow)

Tax challenges of digital economy 1 3

Controlled foreign corporation rules2

Hybrid mismatch arrangements

4Deductibility of interest and other financial payments 6

Treaty abuse5

Harmful tax practices

7Artificial avoidance of permanent establishment status 9

Transfer pricing for risks and capital8

Transfer pricing for intangibles

10 Transfer pricing for other high-risk transactions 12

Disclosure of aggressive tax planning arrangements11

Development of data on BEPS and actions addressing it

13Transfer pricing documentation 15

Development of a multilateral instrument for amending bilateral tax treaties

14Effectiveness of treaty dispute resolution mechanisms

Page 12 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

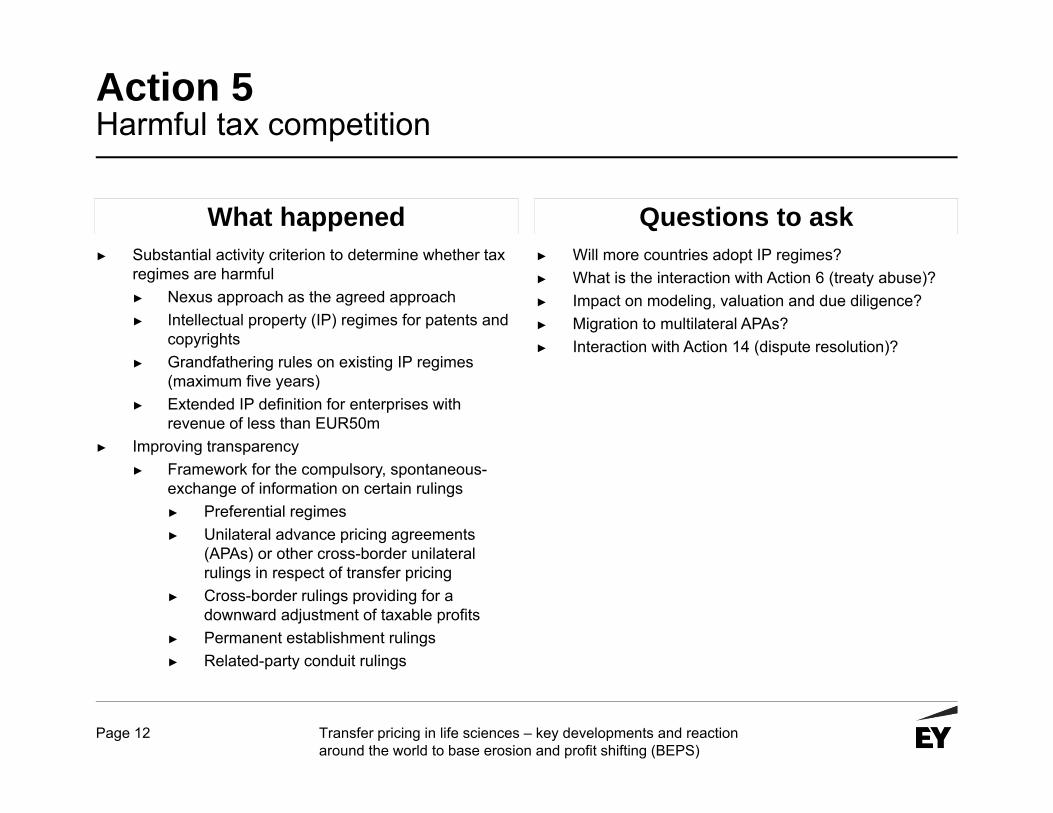

Action 5Harmful tax competition

What happened Questions to ask► Substantial activity criterion to determine whether tax

regimes are harmful► Nexus approach as the agreed approach► Intellectual property (IP) regimes for patents and

copyrights ► Grandfathering rules on existing IP regimes

(maximum five years)► Extended IP definition for enterprises with

revenue of less than EUR50m► Improving transparency

► Framework for the compulsory, spontaneous-exchange of information on certain rulings► Preferential regimes ► Unilateral advance pricing agreements

(APAs) or other cross-border unilateral rulings in respect of transfer pricing

► Cross-border rulings providing for a downward adjustment of taxable profits

► Permanent establishment rulings► Related-party conduit rulings

► Will more countries adopt IP regimes?► What is the interaction with Action 6 (treaty abuse)?► Impact on modeling, valuation and due diligence?► Migration to multilateral APAs?► Interaction with Action 14 (dispute resolution)?

Page 13 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

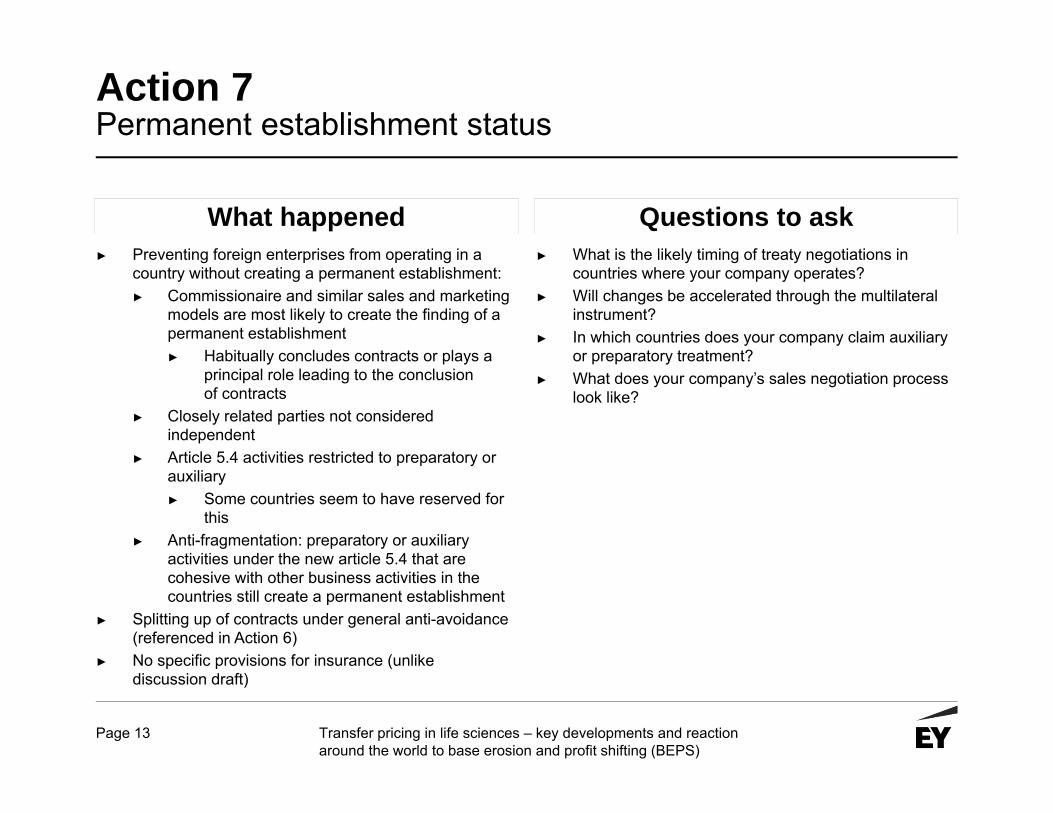

Action 7Permanent establishment status

What happened Questions to ask► Preventing foreign enterprises from operating in a

country without creating a permanent establishment:► Commissionaire and similar sales and marketing

models are most likely to create the finding of a permanent establishment► Habitually concludes contracts or plays a

principal role leading to the conclusion of contracts

► Closely related parties not considered independent

► Article 5.4 activities restricted to preparatory or auxiliary► Some countries seem to have reserved for

this► Anti-fragmentation: preparatory or auxiliary

activities under the new article 5.4 that are cohesive with other business activities in the countries still create a permanent establishment

► Splitting up of contracts under general anti-avoidance (referenced in Action 6)

► No specific provisions for insurance (unlike discussion draft)

► What is the likely timing of treaty negotiations in countries where your company operates?

► Will changes be accelerated through the multilateral instrument?

► In which countries does your company claim auxiliary or preparatory treatment?

► What does your company’s sales negotiation process look like?

Page 14 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

BEPS final reports – immediate impacts to life sciences industry

Page 15 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

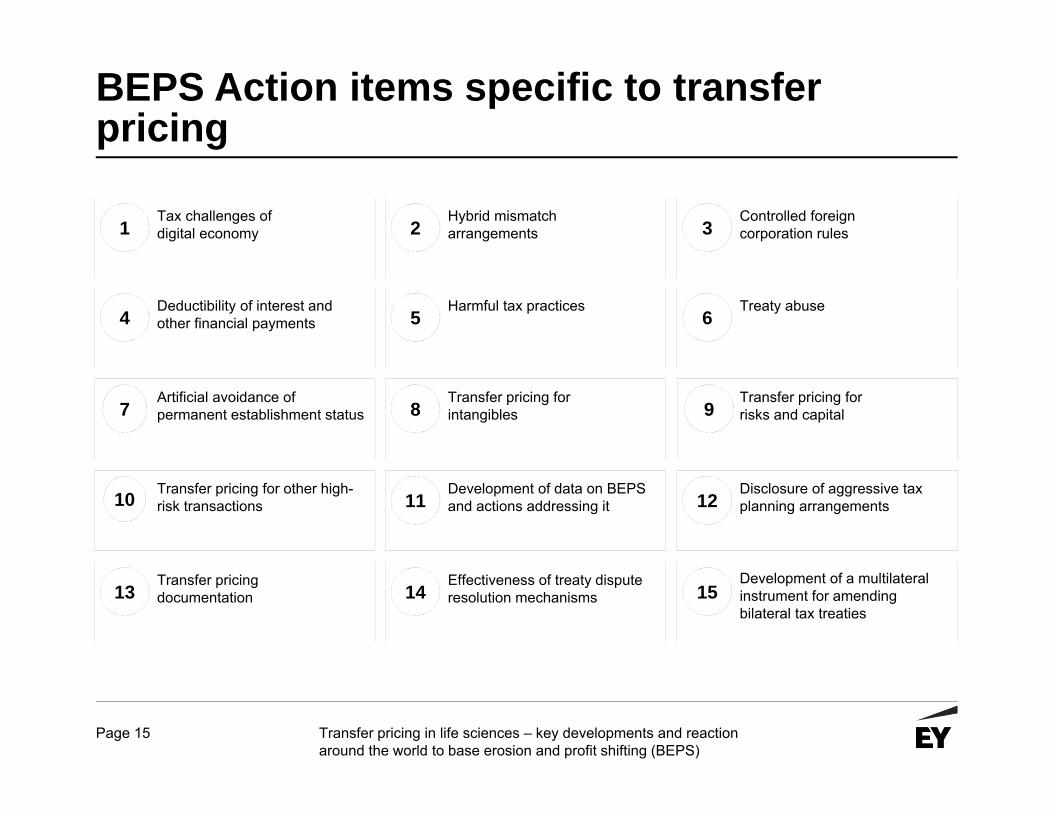

BEPS Action items specific to transfer pricing

Tax challenges of digital economy 1 3

Controlled foreign corporation rules2

Hybrid mismatch arrangements

4Deductibility of interest and other financial payments 6

Treaty abuse5

Harmful tax practices

7Artificial avoidance of permanent establishment status 9

Transfer pricing for risks and capital8

Transfer pricing for intangibles

10 Transfer pricing for other high-risk transactions 12

Disclosure of aggressive tax planning arrangements11

Development of data on BEPS and actions addressing it

13Transfer pricing documentation 15

Development of a multilateral instrument for amending bilateral tax treaties

14Effectiveness of treaty dispute resolution mechanisms

Page 16 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

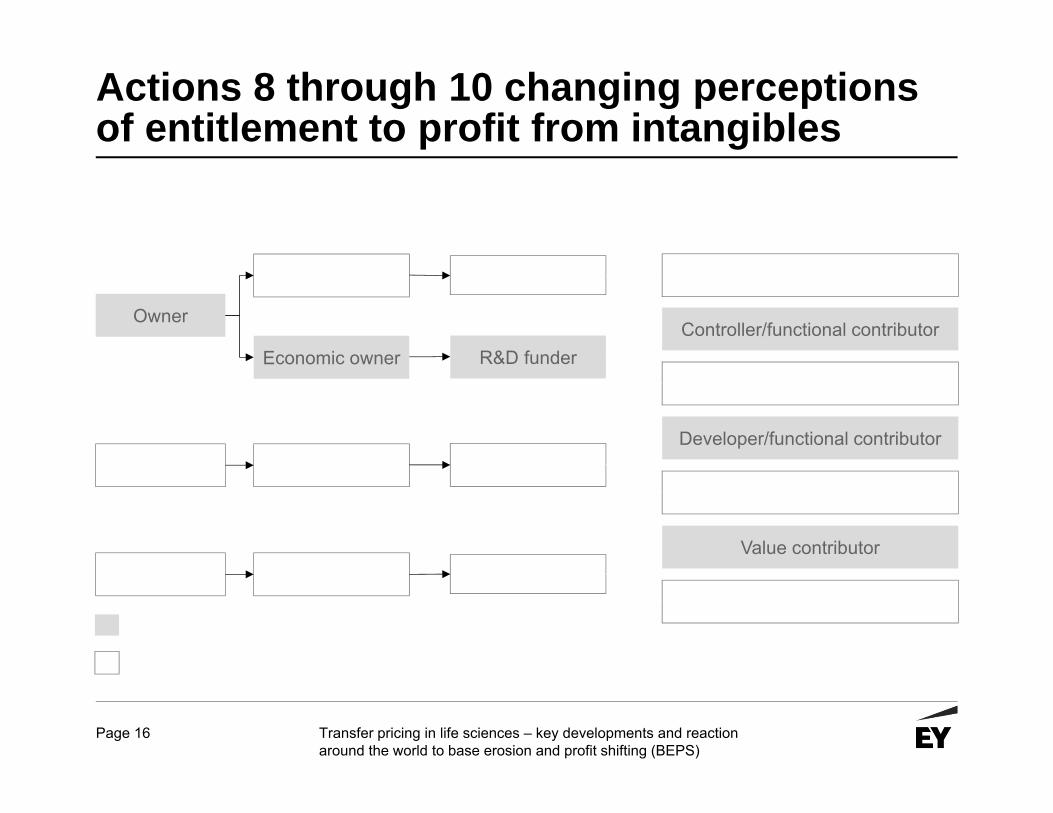

Actions 8 through 10 changing perceptions of entitlement to profit from intangibles

1980s 2015 1990s

Owner

Legal owner Legal owner

R&D funderInvestor

Controller/functional contributor

Developer DeveloperRoutine Developer

Developer/functional contributor

User UserPure user

Value contributor

Non-routine (residual claimant)

Routine

Legal owner

Economic owner

Developer

User

2000s

Page 17 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

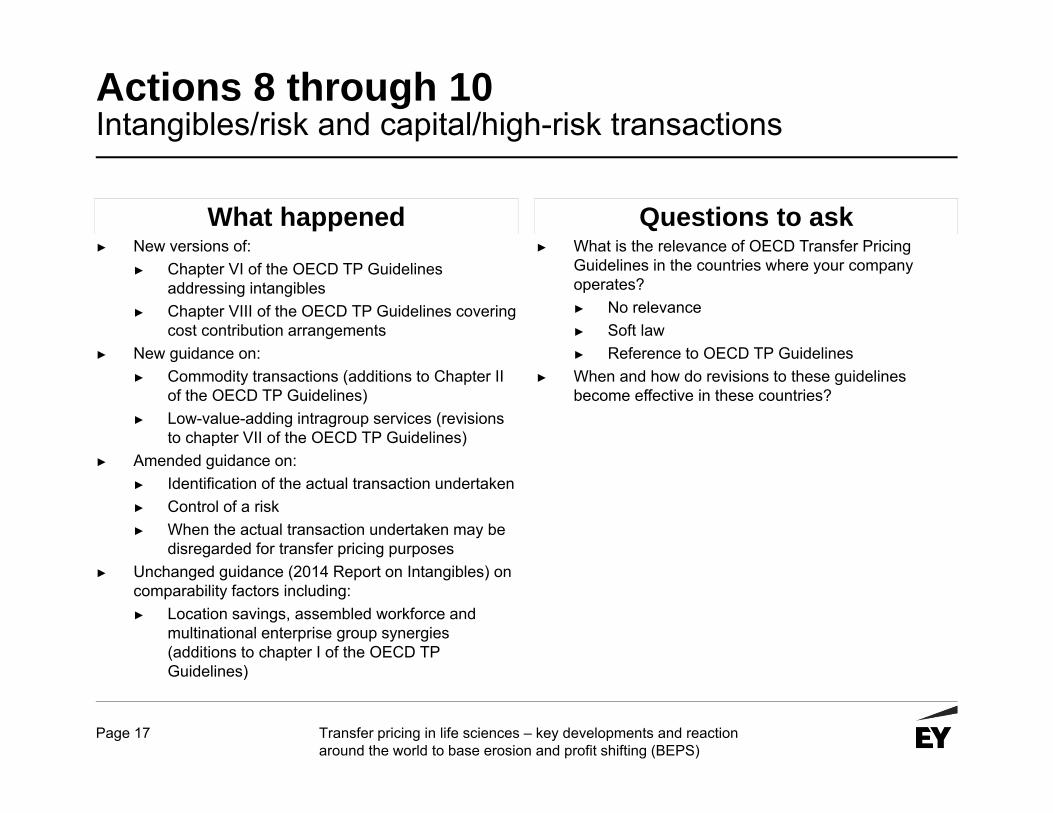

Actions 8 through 10Intangibles/risk and capital/high-risk transactions

What happened Questions to ask► New versions of:

► Chapter VI of the OECD TP Guidelines addressing intangibles

► Chapter VIII of the OECD TP Guidelines covering cost contribution arrangements

► New guidance on:► Commodity transactions (additions to Chapter II

of the OECD TP Guidelines)► Low-value-adding intragroup services (revisions

to chapter VII of the OECD TP Guidelines)► Amended guidance on:

► Identification of the actual transaction undertaken ► Control of a risk► When the actual transaction undertaken may be

disregarded for transfer pricing purposes► Unchanged guidance (2014 Report on Intangibles) on

comparability factors including:► Location savings, assembled workforce and

multinational enterprise group synergies (additions to chapter I of the OECD TP Guidelines)

► What is the relevance of OECD Transfer Pricing Guidelines in the countries where your company operates?► No relevance► Soft law► Reference to OECD TP Guidelines

► When and how do revisions to these guidelines become effective in these countries?

Page 18 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

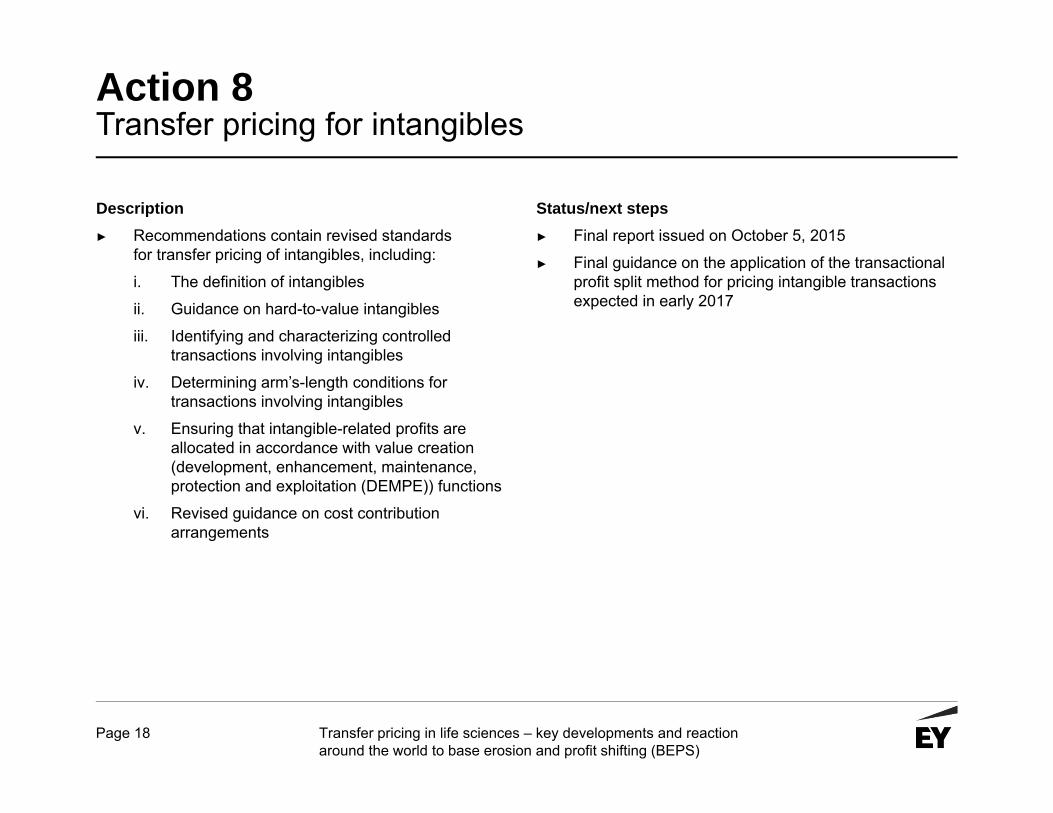

Action 8Transfer pricing for intangibles

Description► Recommendations contain revised standards

for transfer pricing of intangibles, including:

i. The definition of intangibles

ii. Guidance on hard-to-value intangibles

iii. Identifying and characterizing controlled transactions involving intangibles

iv. Determining arm’s-length conditions for transactions involving intangibles

v. Ensuring that intangible-related profits are allocated in accordance with value creation (development, enhancement, maintenance, protection and exploitation (DEMPE)) functions

vi. Revised guidance on cost contribution arrangements

Status/next steps► Final report issued on October 5, 2015

► Final guidance on the application of the transactional profit split method for pricing intangible transactions expected in early 2017

Page 19 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

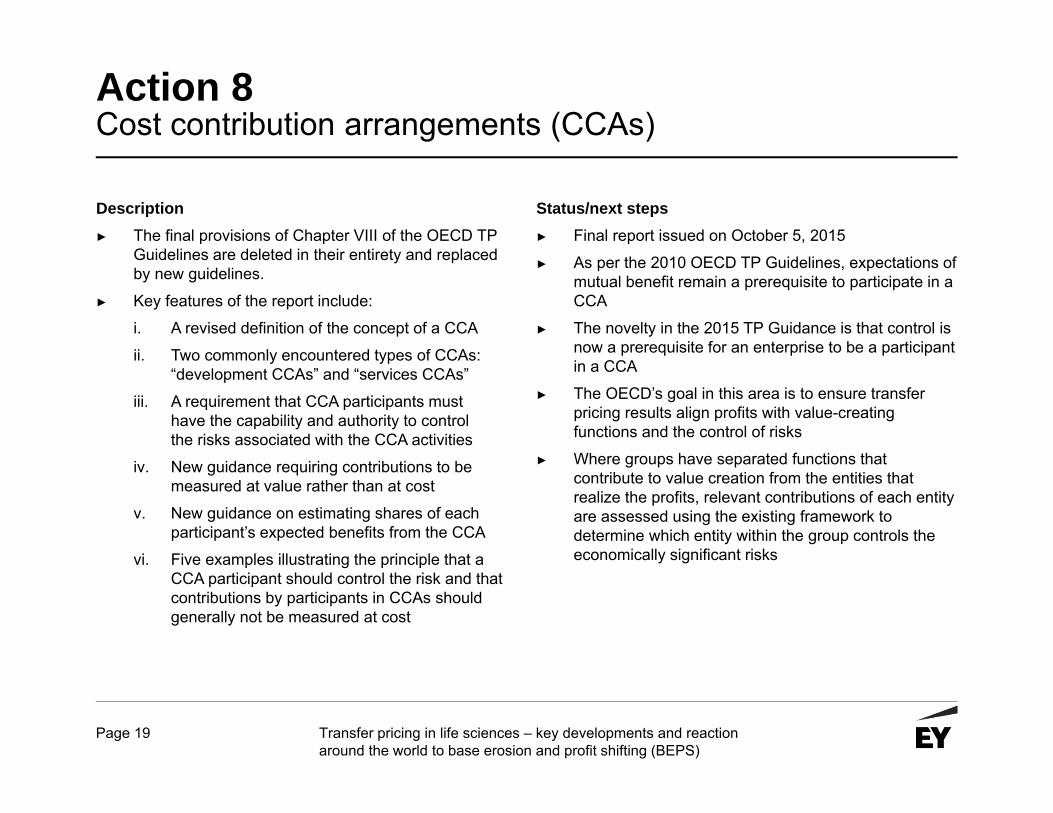

Action 8 Cost contribution arrangements (CCAs)

Description► The final provisions of Chapter VIII of the OECD TP

Guidelines are deleted in their entirety and replaced by new guidelines.

► Key features of the report include:

i. A revised definition of the concept of a CCA

ii. Two commonly encountered types of CCAs: “development CCAs” and “services CCAs”

iii. A requirement that CCA participants must have the capability and authority to control the risks associated with the CCA activities

iv. New guidance requiring contributions to be measured at value rather than at cost

v. New guidance on estimating shares of each participant’s expected benefits from the CCA

vi. Five examples illustrating the principle that a CCA participant should control the risk and that contributions by participants in CCAs should generally not be measured at cost

Status/next steps► Final report issued on October 5, 2015

► As per the 2010 OECD TP Guidelines, expectations of mutual benefit remain a prerequisite to participate in a CCA

► The novelty in the 2015 TP Guidance is that control is now a prerequisite for an enterprise to be a participant in a CCA

► The OECD’s goal in this area is to ensure transfer pricing results align profits with value-creating functions and the control of risks

► Where groups have separated functions that contribute to value creation from the entities that realize the profits, relevant contributions of each entity are assessed using the existing framework to determine which entity within the group controls the economically significant risks

Page 20 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Actions 8 through 10 – transfer pricing for risks and capital and other high-risk transactions

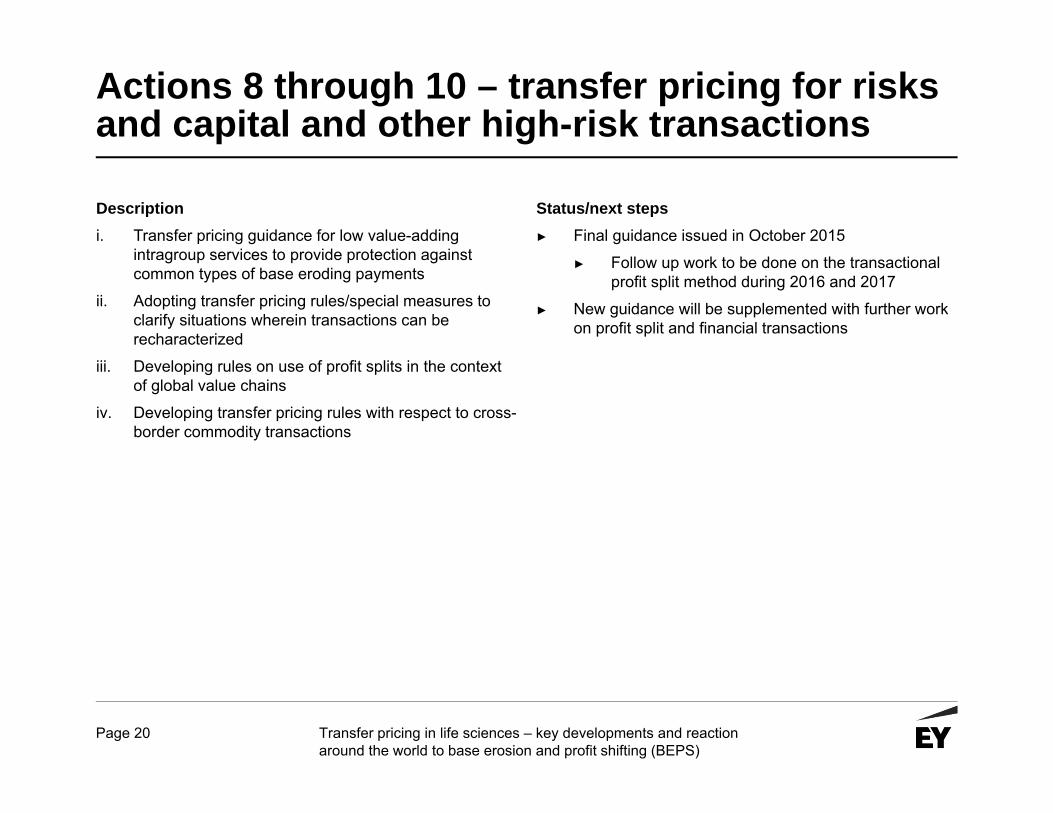

Descriptioni. Transfer pricing guidance for low value-adding

intragroup services to provide protection against common types of base eroding payments

ii. Adopting transfer pricing rules/special measures to clarify situations wherein transactions can be recharacterized

iii. Developing rules on use of profit splits in the context of global value chains

iv. Developing transfer pricing rules with respect to cross-border commodity transactions

Status/next steps► Final guidance issued in October 2015

► Follow up work to be done on the transactional profit split method during 2016 and 2017

► New guidance will be supplemented with further work on profit split and financial transactions

Page 21 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

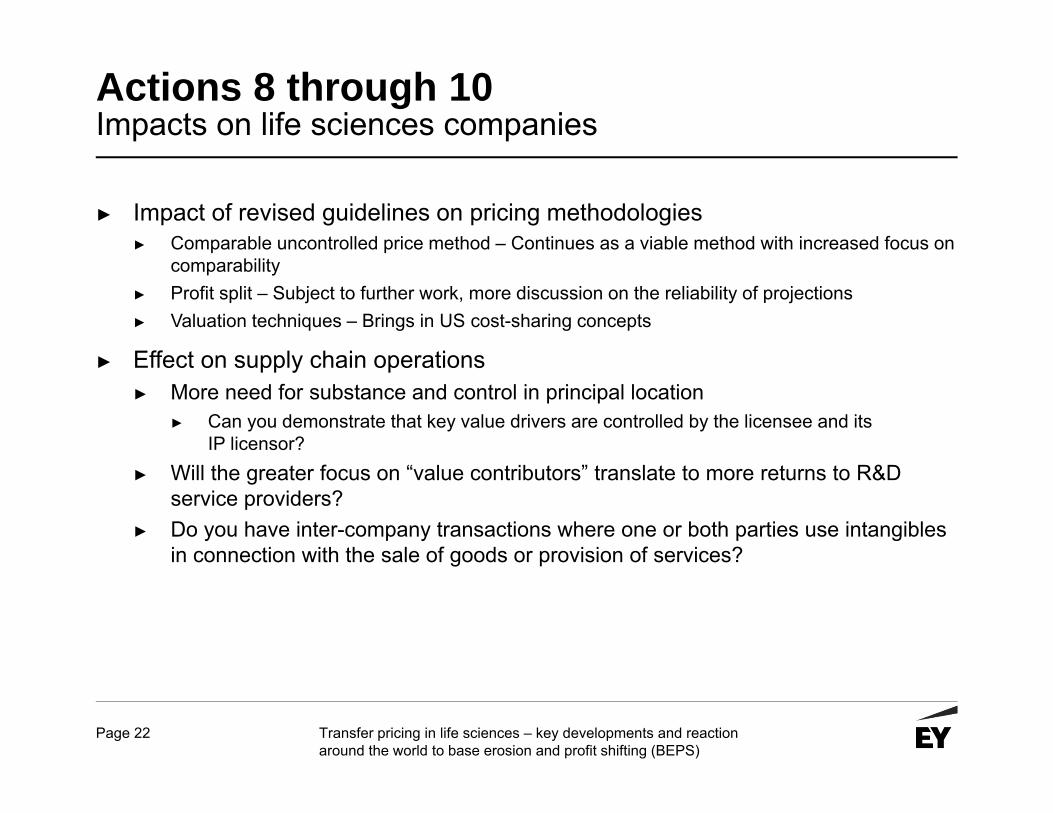

Actions 8 through 10 Impacts on life sciences companies

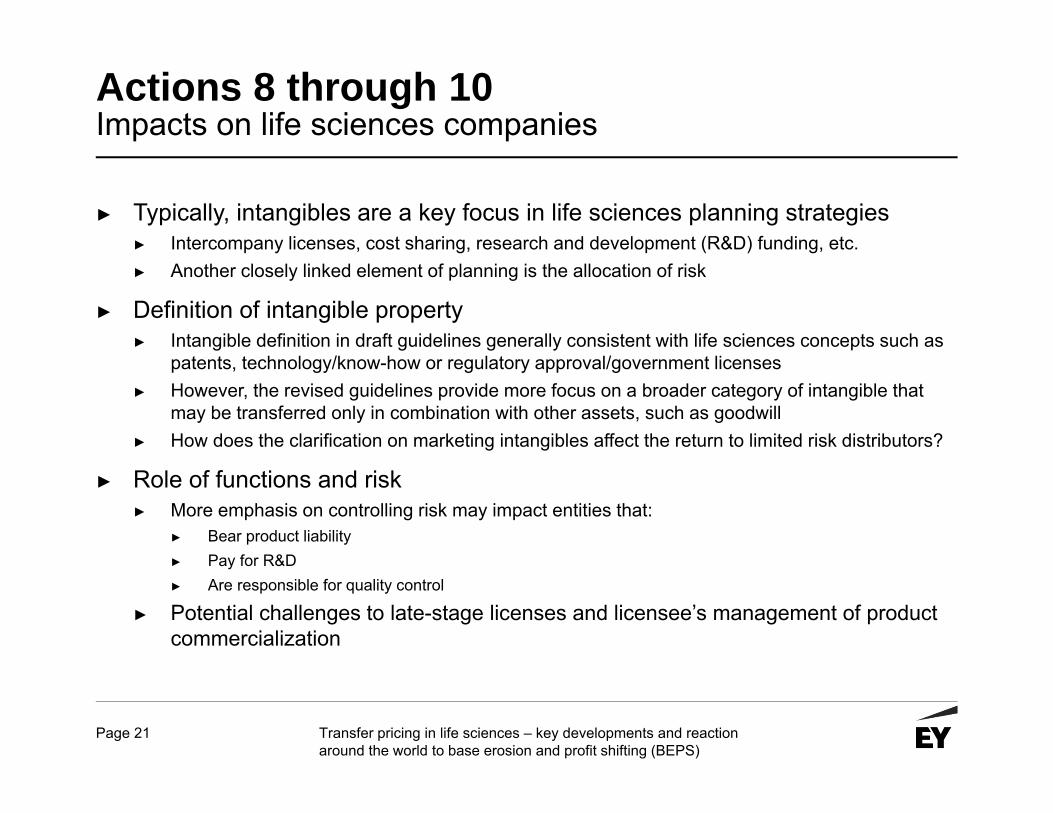

► Typically, intangibles are a key focus in life sciences planning strategies► Intercompany licenses, cost sharing, research and development (R&D) funding, etc.► Another closely linked element of planning is the allocation of risk

► Definition of intangible property► Intangible definition in draft guidelines generally consistent with life sciences concepts such as

patents, technology/know-how or regulatory approval/government licenses► However, the revised guidelines provide more focus on a broader category of intangible that

may be transferred only in combination with other assets, such as goodwill► How does the clarification on marketing intangibles affect the return to limited risk distributors?

► Role of functions and risk► More emphasis on controlling risk may impact entities that:

► Bear product liability► Pay for R&D► Are responsible for quality control

► Potential challenges to late-stage licenses and licensee’s management of product commercialization

Page 22 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Actions 8 through 10Impacts on life sciences companies

► Impact of revised guidelines on pricing methodologies► Comparable uncontrolled price method – Continues as a viable method with increased focus on

comparability► Profit split – Subject to further work, more discussion on the reliability of projections► Valuation techniques – Brings in US cost-sharing concepts

► Effect on supply chain operations► More need for substance and control in principal location

► Can you demonstrate that key value drivers are controlled by the licensee and its IP licensor?

► Will the greater focus on “value contributors” translate to more returns to R&D service providers?

► Do you have inter-company transactions where one or both parties use intangibles in connection with the sale of goods or provision of services?

Page 23 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

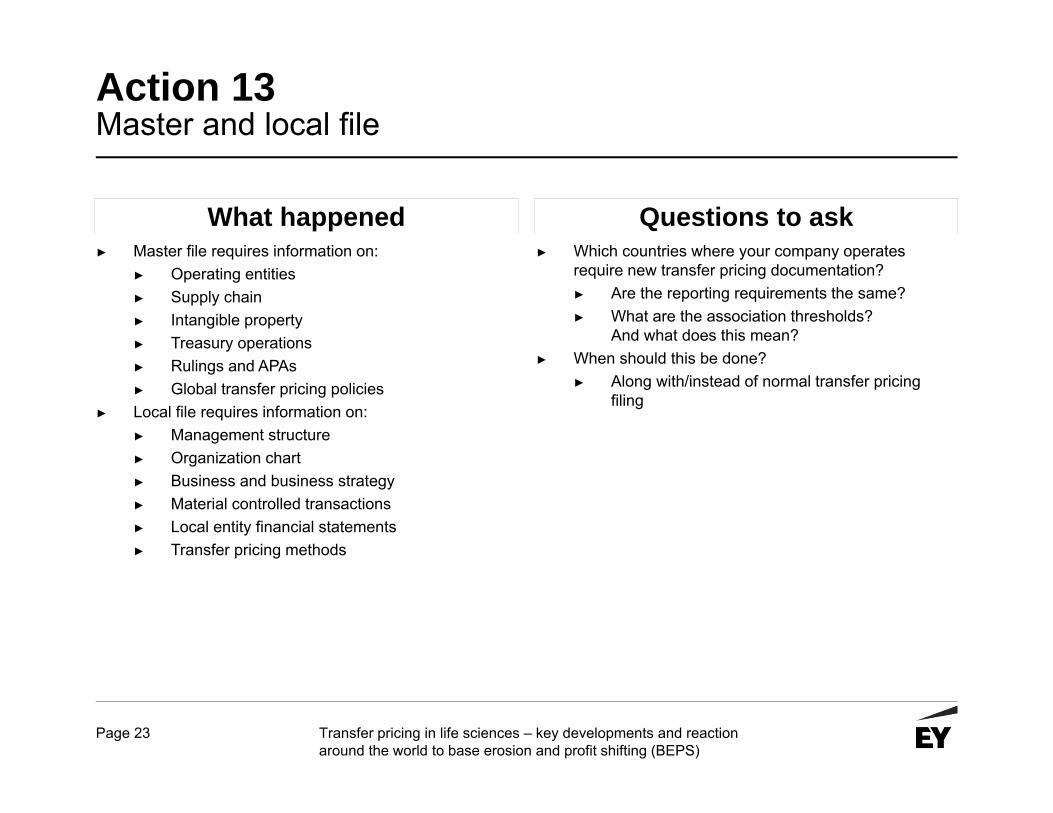

Action 13Master and local file

What happened Questions to ask► Master file requires information on:

► Operating entities ► Supply chain► Intangible property ► Treasury operations ► Rulings and APAs► Global transfer pricing policies

► Local file requires information on:► Management structure ► Organization chart► Business and business strategy► Material controlled transactions ► Local entity financial statements ► Transfer pricing methods

► Which countries where your company operates require new transfer pricing documentation?► Are the reporting requirements the same?► What are the association thresholds?

And what does this mean?► When should this be done?

► Along with/instead of normal transfer pricing filing

Page 24 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

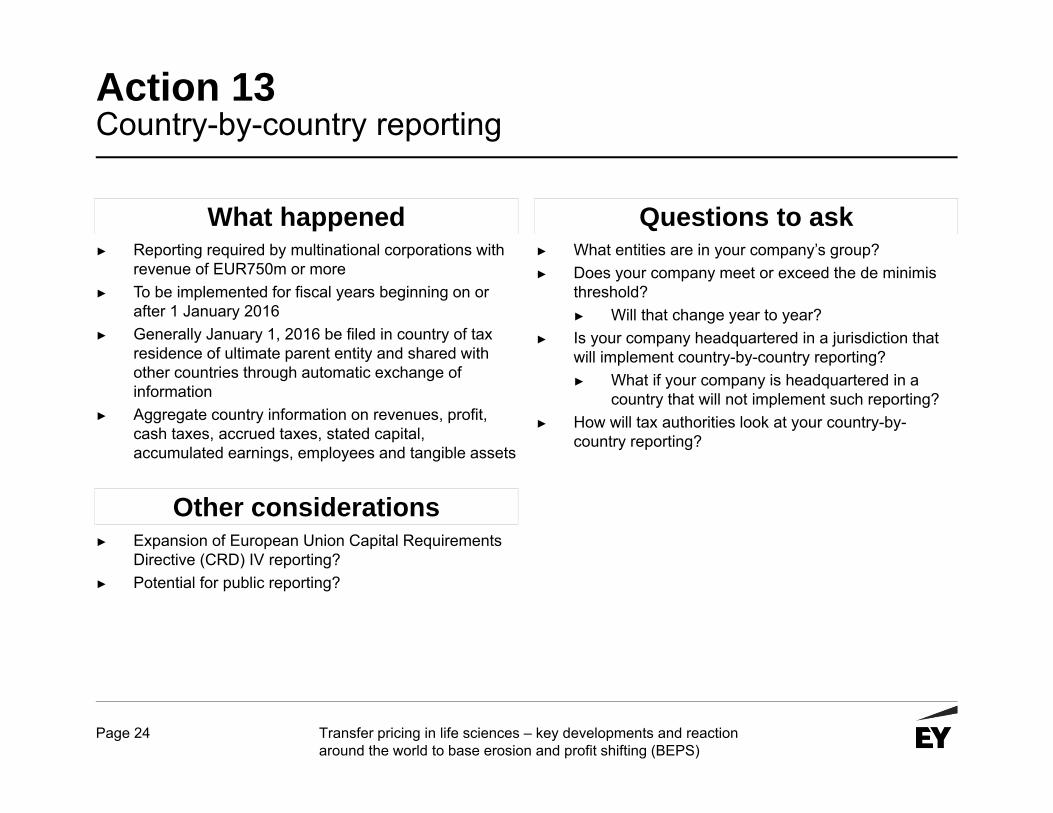

Action 13Country-by-country reporting

What happened Questions to ask► Reporting required by multinational corporations with

revenue of EUR750m or more► To be implemented for fiscal years beginning on or

after 1 January 2016 ► Generally January 1, 2016 be filed in country of tax

residence of ultimate parent entity and shared with other countries through automatic exchange of information

► Aggregate country information on revenues, profit, cash taxes, accrued taxes, stated capital, accumulated earnings, employees and tangible assets

► What entities are in your company’s group?► Does your company meet or exceed the de minimis

threshold?► Will that change year to year?

► Is your company headquartered in a jurisdiction that will implement country-by-country reporting?► What if your company is headquartered in a

country that will not implement such reporting?► How will tax authorities look at your country-by-

country reporting?

Other considerations► Expansion of European Union Capital Requirements

Directive (CRD) IV reporting?► Potential for public reporting?

Page 25 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Reactions outside the US

Page 26 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

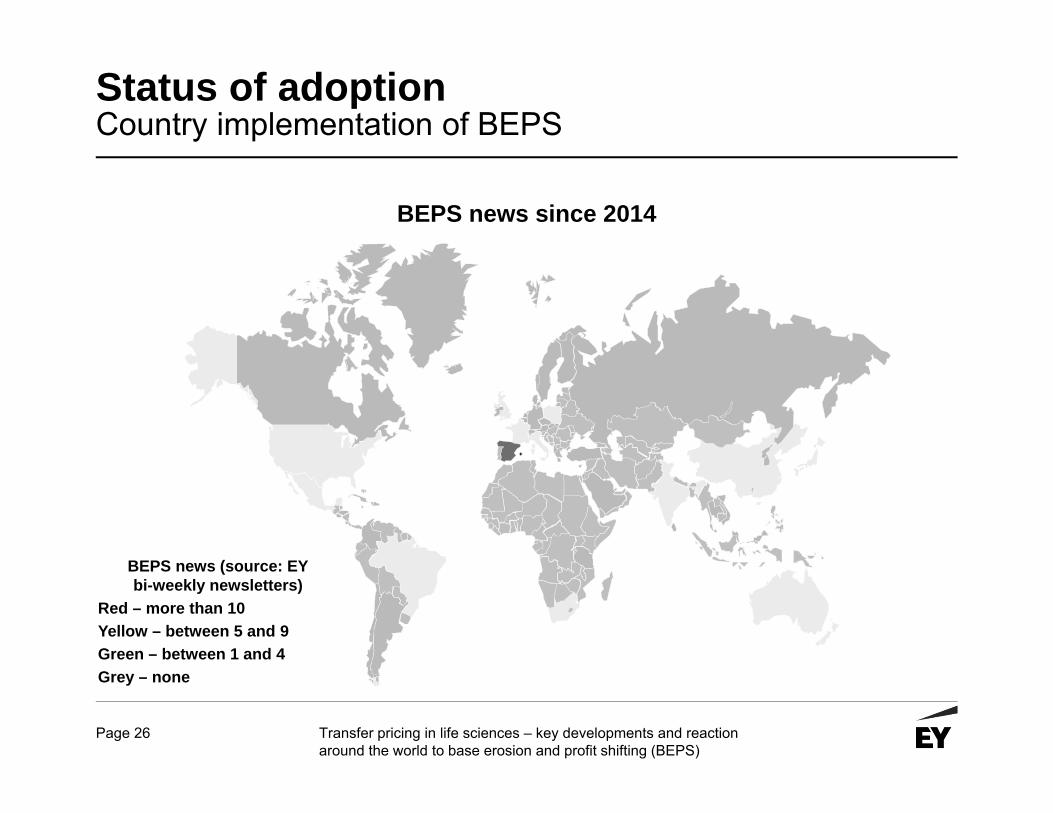

Status of adoption Country implementation of BEPS

BEPS news since 2014

BEPS news (source: EYbi-weekly newsletters)

Red – more than 10Yellow – between 5 and 9Green – between 1 and 4Grey – none

Page 27 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Status of adoption Country implementation of BEPS

► Countries in which the amended OECD TP Guidelines (which reflect the BEPS Actions 8-10 recommendations), will apply automatically without the need for legislative action as soon as they are formally approved by the OECD’s Council: ► Hungary► Mexico► Norway► Ireland (some form of administrative action is required)► Australia (some form of administrative action is required)► UK (an order from the Treasury is needed)

Page 28 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Overview of countries with Actions 8-10 activities

Proposed amendments to Circular 2

Page 29 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

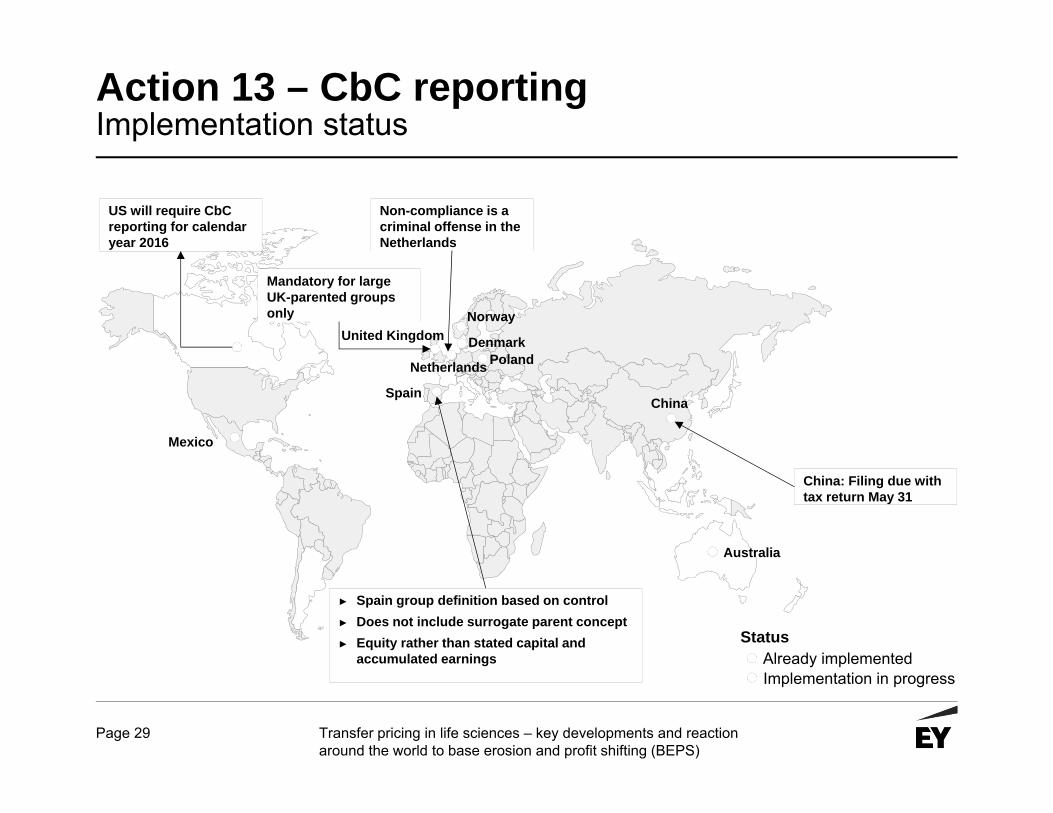

Action 13 – CbC reporting Implementation status

Already implementedImplementation in progress

Status

US will require CbC reporting for calendar year 2016

Non-compliance is a criminal offense in the Netherlands

Mandatory for large UK-parented groups only

► Spain group definition based on control► Does not include surrogate parent concept► Equity rather than stated capital and

accumulated earnings

China: Filing due with tax return May 31

Norway

DenmarkPoland

Spain

Netherlands

United Kingdom

China

Australia

Mexico

Page 30 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

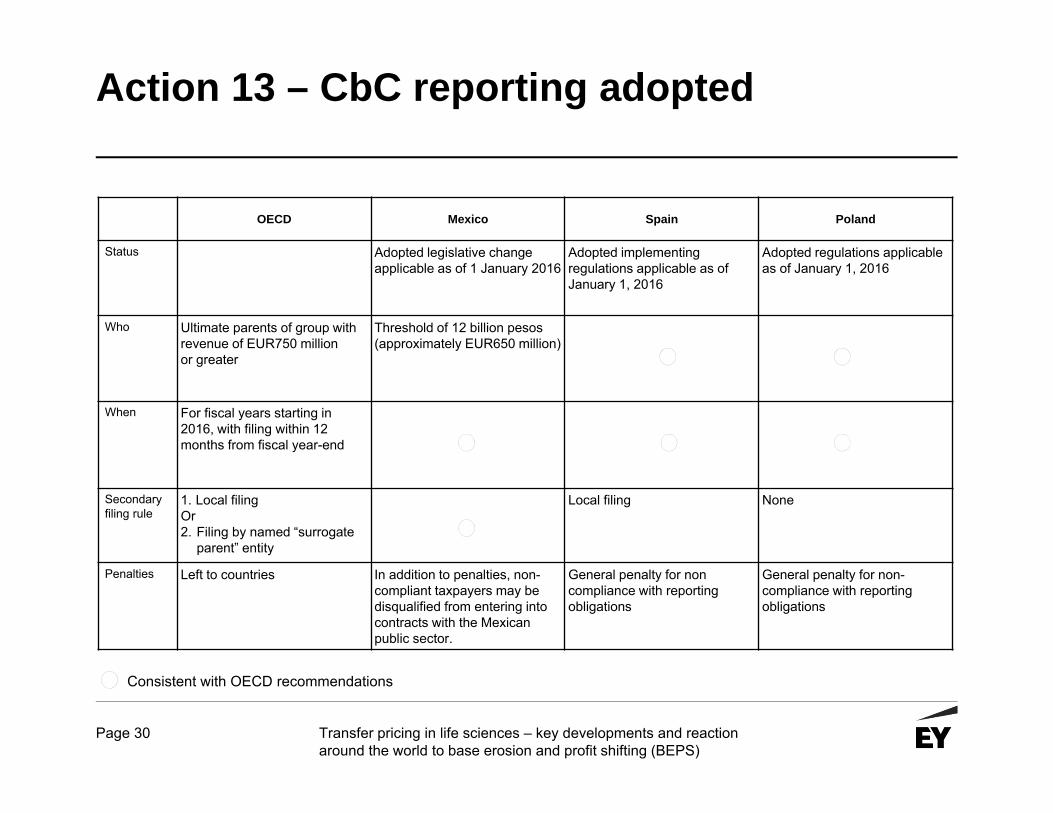

Action 13 – CbC reporting adopted

OECD Mexico Spain Poland

Status Adopted legislative change applicable as of 1 January 2016

Adopted implementing regulations applicable as of January 1, 2016

Adopted regulations applicable as of January 1, 2016

Who Ultimate parents of group with revenue of EUR750 million or greater

Threshold of 12 billion pesos (approximately EUR650 million)

When For fiscal years starting in 2016, with filing within 12 months from fiscal year-end

Secondary filing rule

1. Local filing Or2. Filing by named “surrogate

parent” entity

Local filing None

Penalties Left to countries In addition to penalties, non-compliant taxpayers may be disqualified from entering into contracts with the Mexican public sector.

General penalty for non compliance with reporting obligations

General penalty for non-compliance with reporting obligations

Consistent with OECD recommendations

Page 31 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

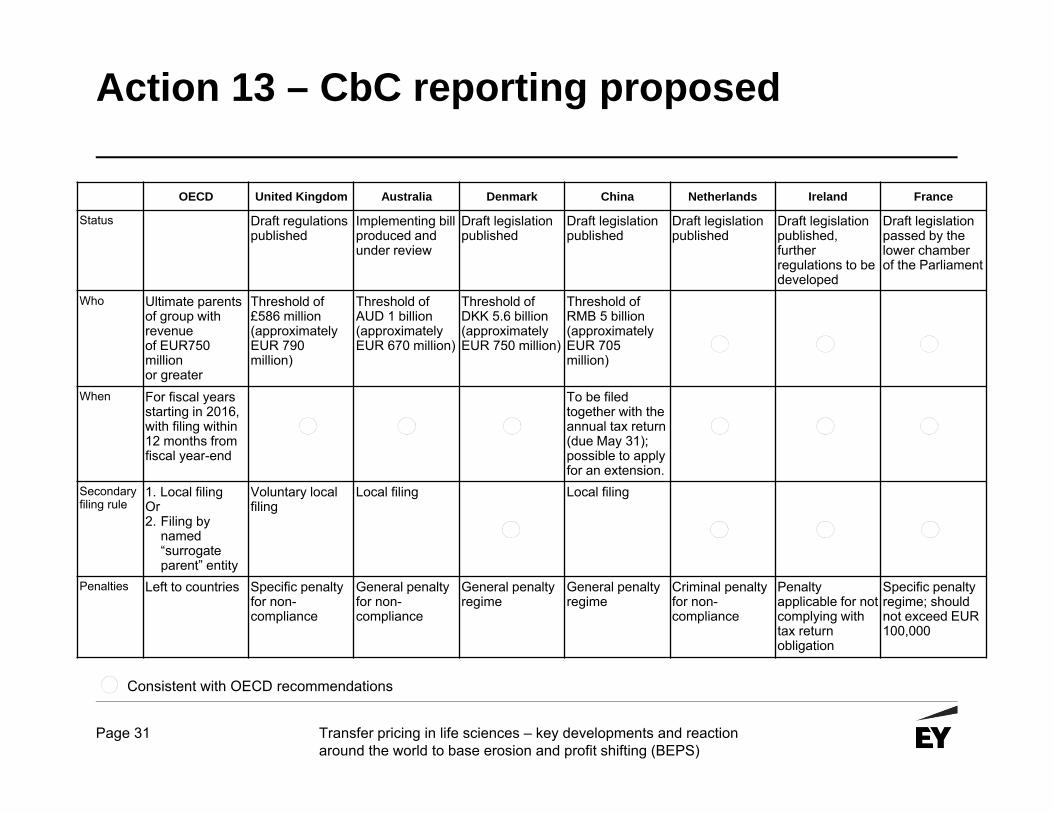

Action 13 – CbC reporting proposed

OECD United Kingdom Australia Denmark China Netherlands Ireland France

Status Draft regulationspublished

Implementing bill produced andunder review

Draft legislation published

Draft legislation published

Draft legislation published

Draft legislation published, further regulations to be developed

Draft legislation passed by the lower chamber of the Parliament

Who Ultimate parents of group with revenue of EUR750 million or greater

Threshold of £586 million (approximately EUR 790million)

Threshold of AUD 1 billion (approximately EUR 670 million)

Threshold of DKK 5.6 billion (approximately EUR 750 million)

Threshold of RMB 5 billion (approximately EUR 705 million)

When For fiscal years starting in 2016, with filing within 12 months from fiscal year-end

To be filed together with the annual tax return (due May 31); possible to apply for an extension.

Secondary filing rule

1. Local filing Or2. Filing by

named “surrogate parent” entity

Voluntary local filing

Local filing Local filing

Penalties Left to countries Specific penalty for non-compliance

General penalty for non-compliance

General penalty regime

General penalty regime

Criminal penalty for non-compliance

Penalty applicable for not complying with tax return obligation

Specific penaltyregime; should not exceed EUR 100,000

Consistent with OECD recommendations

Page 32 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

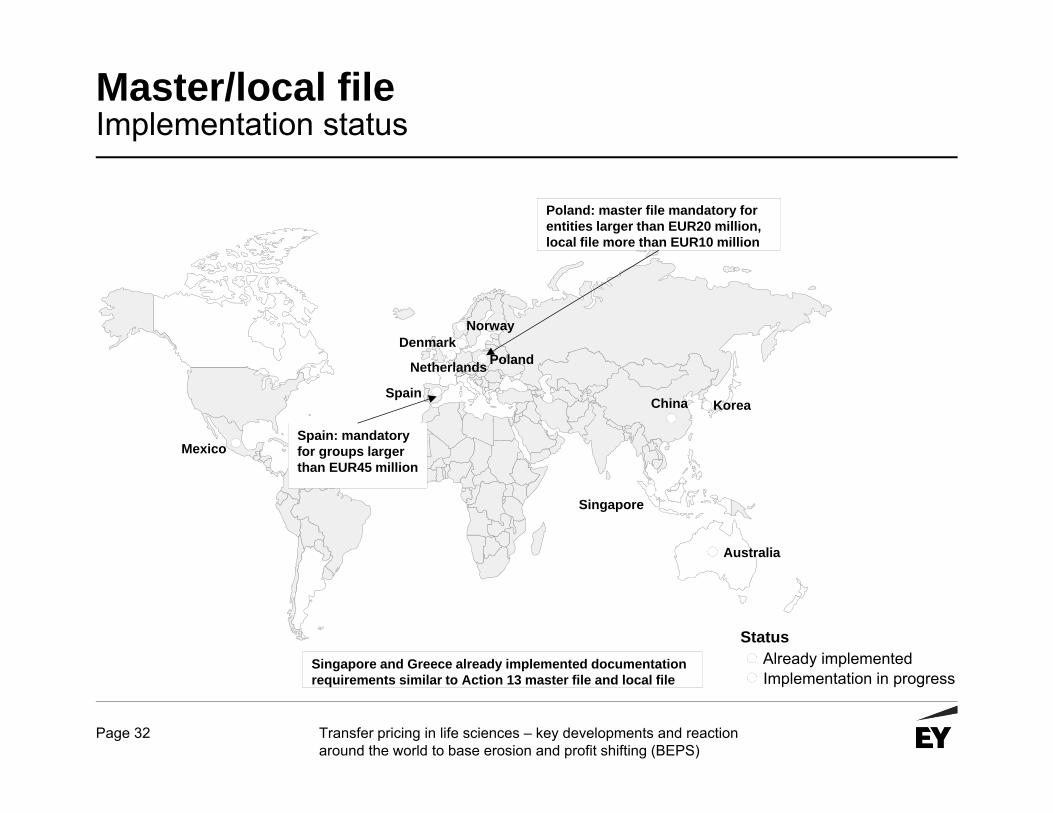

Master/local fileImplementation status

Already implementedImplementation in progress

Status

Poland: master file mandatory for entities larger than EUR20 million, local file more than EUR10 million

Spain: mandatory for groups larger than EUR45 million

Singapore and Greece already implemented documentation requirements similar to Action 13 master file and local file

NorwayDenmark

Poland

Spain

Netherlands

China

Australia

Korea

Singapore

Mexico

Page 33 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

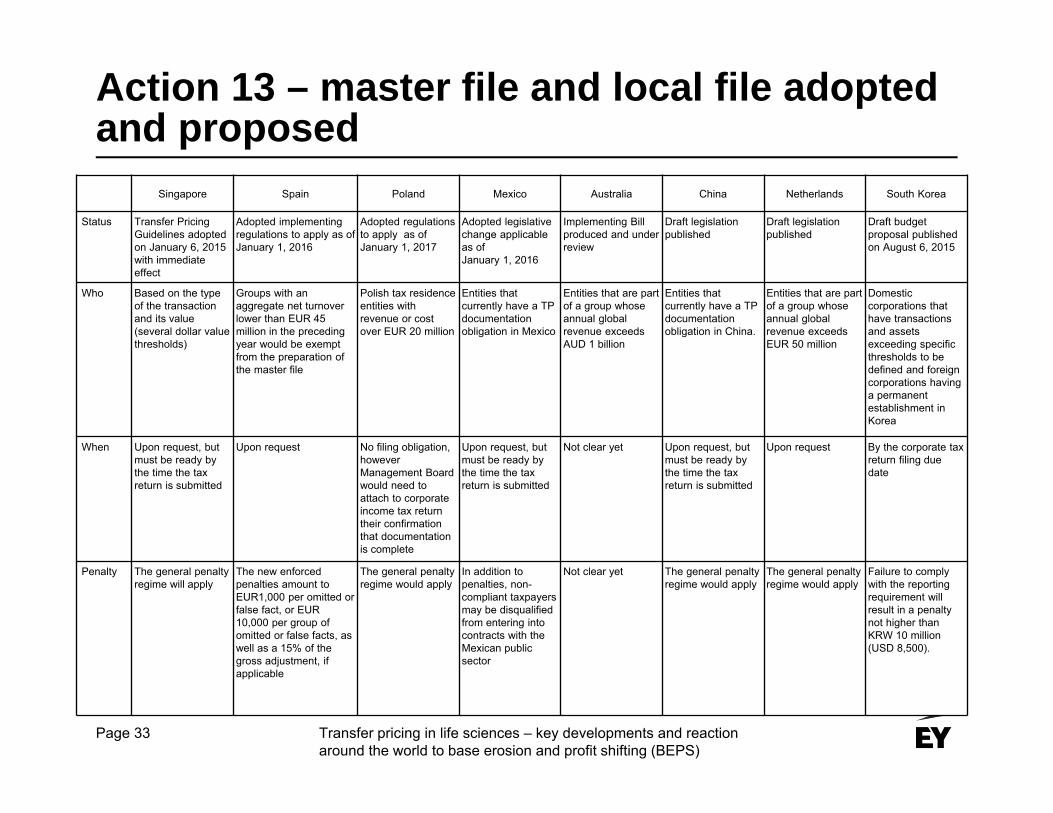

Action 13 – master file and local file adopted and proposed

Singapore Spain Poland Mexico Australia China Netherlands South Korea

Status Transfer PricingGuidelines adopted on January 6, 2015 with immediate effect

Adopted implementing regulations to apply as of January 1, 2016

Adopted regulations to apply as of January 1, 2017

Adopted legislative change applicableas of January 1, 2016

Implementing Bill produced and under review

Draft legislation published

Draft legislation published

Draft budget proposal published on August 6, 2015

Who Based on the type of the transaction and its value (several dollar value thresholds)

Groups with an aggregate net turnover lower than EUR 45 million in the preceding year would be exempt from the preparation of the master file

Polish tax residence entities with revenue or cost over EUR 20 million

Entities that currently have a TP documentation obligation in Mexico

Entities that are part of a group whose annual global revenue exceeds AUD 1 billion

Entities that currently have a TP documentation obligation in China.

Entities that are part of a group whose annual global revenue exceeds EUR 50 million

Domestic corporations that have transactions and assets exceeding specific thresholds to be defined and foreign corporations having a permanent establishment in Korea

When Upon request, but must be ready by the time the tax return is submitted

Upon request No filing obligation, however Management Board would need to attach to corporate income tax return their confirmation that documentation is complete

Upon request, but must be ready by the time the tax return is submitted

Not clear yet Upon request, but must be ready by the time the tax return is submitted

Upon request By the corporate tax return filing due date

Penalty The general penalty regime will apply

The new enforced penalties amount to EUR1,000 per omitted or false fact, or EUR 10,000 per group of omitted or false facts, as well as a 15% of the gross adjustment, if applicable

The general penalty regime would apply

In addition to penalties, non-compliant taxpayers may be disqualified from entering into contracts with the Mexican public sector

Not clear yet The general penalty regime would apply

The general penalty regime would apply

Failure to comply with the reporting requirement will result in a penalty not higher thanKRW 10 million (USD 8,500).

Page 34 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Reactions outside the US

China► In mid-September, China released a consultation draft circular,

“Implementation Measures for Special Tax Adjustments”► The Measures would replace the 2009 “Circular 2,” which governs transfer pricing

in China► Key provisions of the Measures include:

► New chapter on intangibles, similar to BEPS guidance but with a sharper focus on market “promotion” activities; DEMPE operations are repackaged as DEMPEP, with the final P standing for promotion as value creating function► Emphasizes importance of ‘middle value chain activities’ often performed in China (trial

production, etc.)► New chapter on services, following OECD “benefit test” but with broader definition

of “shareholder” activities► Numerous anti-profit-shifting provisions, such as disallowing deductions for

payments to limited-substance affiliates► BEPS “value creation” focus is reflected in extensive requirements for “value chain

analysis”

Page 35 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Reactions outside the US

Singapore► In January 2015, Singapore’s tax authority, the Inland Revenue Authority of

Singapore (IRAS) published its updated e-Tax Guide on Transfer Pricing. The guidelines set out clarifications on the need for companies to prepare contemporaneous transfer pricing documentation, as well as the documentation requirements, exclusions and materiality thresholds, and various procedures that apply.

► The nexus approach requiring substance is somewhat established in Singapore as firms have to demonstrate substance to qualify for tax incentives.

► The Singapore Ministry of Finance indicated that it welcomes the OECD recommendations, and Singapore has already implemented measures that have parallels to the approach outlined in the BEPS reports.

► Singapore is generally expected to implement all BEPS Action items.

Page 36 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Reactions outside the US

Ireland► The Minister announced that Ireland would be one of the first countries in the

world to introduce CbC reporting.► The Irish Strategy Statement Update reaffirms the Irish government’s

commitments in an international tax context and outlines how the country will respond to the OECD BEPS reports and emerging tax-related proposals from the European Union.

► Ireland has actively engaged in the OECD’s BEPS project and will continue to engage in the project’s remaining work.

► In October 2015, Finance Bill 2015 was published. It includes draft legislation on Ireland’s new intellectual property regime – the Knowledge Development Box – following the OECD’s recommendations, expected to be effective as of January 1, 2016 (alignment with modified nexus approach of BEPS Action 5).

Page 37 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Reactions outside the US

UK► On October 5, 2015, the United Kingdom’s (UK) HM Revenue & Customs

(HMRC) published a draft statutory instrument that would implement CbC reporting in the UK for accounting periods beginning on or after January 1, 2016.

► Certain countries have introduced anti-avoidance legislation in response to BEPS Action 7 and Actions 8-10 with the most notable development being the diverted profits tax (DPT) recently introduced in the UK.

► The UK DPT took effect from April 1, 2015, and can potentially affect captive insurers located anywhere in the world whether the affiliated group is headquartered in the UK or overseas.

► Draft patent box legislation expected in December 2015 (alignment with BEPS Action 5) should be limited to jurisdictions where IP research and development is undertaken based on the OECD’s nexus approach

Page 38 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Reactions outside the US

Netherlands► Netherlands is only willing to unilaterally amend its legislation with respect to

BEPS Actions that prescribe clear minimum standards (CbC reporting (BEPS Action 13), treaty abuse (BEPS Action 6) and transparency/exchange of (info on) rulings (BEPS Action 5 and EU standard)). Other actions should be implemented on a multilateral basis through hard law (i.e., multilateral instrument (BEPS Action 15) or EU “specific BEPS” directive).

► An anti-hybrid financing rule has been introduced (implementation of amendments to Parent – Subsidiary Directive and BEPS Action 2) effective as of January 1, 2016.

► An update of the innovation box regime is expected by January 1, 2017 (alignment with BEPS Action 5).

Page 39 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Reactions outside the US

Switzerland► The third series of corporate tax reforms currently under way takes certain

BEPS outcomes into account:► Provision is made for a standard-compliant patent box (or royalty box)► Certain Swiss tax regimes are being abolished (cantonal holding privilege)

► Switzerland will create the necessary legal basis for the exchange of information on tax rulings with the approval of the OECD/Council of Europe multilateral administrative assistance convention.

► The Federal Council has instructed the Federal Department of Finance, in collaboration with the cantons and business circles, to analyze the amendment of Swiss corporate tax law in the light of international developments.

Page 40 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Conclusions

Page 41 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Final thoughts

► Next steps on BEPS► Country reactions► For more information, please visit the EY BEPS website:ey.com/GL/en/Services/Tax/OECD-base-erosion-and-profit-shifting-project

Page 42 Transfer pricing in life sciences – key developments and reaction around the world to base erosion and profit shifting (BEPS)

Questions?

EY | Assurance | Tax | Transactions | AdvisoryAbout EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

Ernst & Young LLP is a client-serving member firm of Ernst & Young Global Limited operating in the US.

© 2015 Ernst & Young LLP.All Rights Reserved.

1507-1591922

ED None