Embed Size (px)

Citation preview

WHITE v SHORTALL

SUPREME COURT OF NEW SOUTH WALES — EQUITY DIVISION

CAMPBELL J

24 October, 3, 7, 8 November, 15 December 2006 — Sydney

[2006] NSWSC 1379

Contract — Trusts — Shares — Evidence — Taxation — Succession — Whether testfor intention to enter contractual obligation is subjective or objective — Measure ofdamages for breach — Time of essence provisions in contract — Objective orsubjective test for creating trust — Equitable compensation for breach of trust —Principles for calculation of equitable compensation for breach of trust — Trusts forpart of debt — Identification of shares on share-by-share basis or otherwise —Burden of proof of payment being loan — Timing of evidence given late in case andits significance — Capital gains tax and its operation when trust declared part oflarger holding of shares — Specific legacy of number of shares out of larger holdingof shares executor’s assent — (UK) Companies Act 1862 — (CTH) Corporations Act2001 — (CTH) Income Tax Assessment Act 1936 — (CTH) Income Tax AssessmentAct 1997 — (NSW) Securities Industry Code — (CTH) Taxation Administration Act1953 — (NSW) Uniform Civil Procedure Rules 2005.

The parties had been in a domestic relationship for several years prior to final separationand the commencement of this litigation. The defendant, a shareholder in a companyknown as Unitract Pty Ltd, wanted to raise public share capital through a publicly listedcompany known as Musgrave Block Holdings Pty Ltd. An agreement was made betweenboth companies on 11 July 2002 for acquisition by Musgrave of all the shares of the othercompany. Musgrave changed its name to Unitract. At the same time the Australian StockExchange (ASX) imposed a restriction condition on the shares of Unitract which expiredon 1 November 2004. For the period from 1 November 2004 until 1 May 2005 all of thedefendant’s shares in Unitract, and for the next 6 months thereafter, 500,000 of thedefendant’s shares in that company were subject to a voluntary escrow. Over the next 6months the plaintiff gave several amounts comprising a total figure of $47,600 to thedefendant which she claimed were loans. The allegation was also made by the plaintiff thatthe defendant had agreed to make good to her a loss of about $10,000 on another sharetransaction. There was agreement between the parties that some of these payments weremade to the defendant, but not all of them.

The question arose as to whether or not any such payments were by way of loan to thedefendant from the plaintiff. The defendant had offered to hold a certain number of sharesin Unitract in trust for the plaintiff, with a view to transferring them to her after thecompany had been floated. This offer was accepted by the plaintiff.

Several questions had to be determined by the court in the matter.The arrangements between the parties were further complicated by the receipt by the

plaintiff of an amount of $20,000 on 28 August 2002. The defendant persuaded theplaintiff to give him that money to invest in the shares of Unitract. In exchange for suchan investment the defendant wrote a letter in which he declared that he wanted 222,000shares transferred to the plaintiff if he were to die.

The plaintiff sought equitable remedies for an alleged contractual breach, such remediesto include equitable compensation for the defendant’s failure to transfer the shares to heras agreed.

Held, with a verdict in favour of the plaintiff:

654

(i) As a matter of fact, the plaintiff would probably have sold the shares by January 2004if the defendant had transferred them to her. As a whole the evidence of the plaintiff wasmore consistent and reliable than the defendant’s, and was accepted as such.

(ii) On the question of the type of intention necessary to create a trust, the law is settled.However, the subjective intention of the settlor is critical for a declaration of trust. Suchsubjective intention may be apparent from objective circumstances. The factual evidencewas sufficient in this case for an inference to be drawn of an intention of the parties todeclare a trust and enter into a contract.

(iii) The common law would have regarded the contract between the parties as one inwhich time was of the essence, given the nature of the subject matter of the contract, whichconsisted of shares in a newly listed company.

(iv) The defendant breached his obligation under the contract to transfer the shares toher upon her request.

(v) Compensation for breach of contract was assessed at $548,452, which wascalculated on the basis of the value of the shares which were not transferred.

(vi) While there is no doubt that shares can be held on trust, the question arises whetheror not only some of a particular parcel of shares can be the subject of a trust. A trustcreated in this manner is not void for uncertainty. Just as a testamentary legacy of anumber of shares would be valid, so too is the trust of 222,000 shares in this case.

(vii) The nature of a company share was defined as a chose in action, being a right toa specified amount of the share capital of a company. This definition is contained in theCorporations Act 2001 (Cth) also. There is no significance in the fact that shares areunnumbered, provided that they are fully paid up and are of equal rank.

(viii) In this case the declaration of trust was of a fund, with the shares being held forthe plaintiff and the defendant.

(ix) This situation was distinguished from that where a person purports to hold part ofmoneys in a bank account in trust for another party.

(x) The measure of damages for breach of trust is identical to that for breach of contract.(xi) The question arose as to whether or not the stock exchange listing rules prevented

the transfer of shares by the defendant to the plaintiff as agreed in the contract, and underthe trust. The defendant had entered into a restriction agreement as required by the stockexchange rules. In the court’s view a declaration of trust of any of the 1.5m securitieswould have been a breach of cl 1 of the restriction agreement. Such a breach would haveto be remedied by enforcement action by Unilife, and not the ASX. The AustralianSecurities and Investments Commission can also take enforcement action. Unitract, andnot the defendant, would have been in breach of an obligation under the listing rules if theshares were the subject of a declaration of trust or were transferred by the defendant to theplaintiff in accordance with the trust.

(xii) Nevertheless, if the defendant were found to be in breach, the court would have nomore than a discretionary power to enforce the rules. In this case the shares in questionwere subject to a holding lock when the defendant declared a trust over them. Thevoluntary escrow imposed on the shares by the defendant had no legal recognition in theASX listing rules.

(xiii) Equitable compensation for breach of trust is assessed by reference to what thesituation would have been if the trustee had performed his duty. In this case such anamount is calculated on the basis that the shares could have been transferred at any timeafter 1 November 2004. This figure was assessed as $266,400.

(xiv) Verdict and judgment for the plaintiff for $548,452, being the amount of damagesfor breach of contract.

Hyhonie Holdings Pty Ltd v Leroy [2004] NSWCA 72; Lord Strathcona SteamshipCo Ltd v Dominion Coal Co Ltd [1926] AC 108; Re Clifford [1912] 1 Ch 29; SydneyFutures Exchange Ltd v Australian Stock Exchange (1995) 56 FCR 236; 128 ALR417; 16 ACSR 148; Target Holdings Ltd v Redferns [1996] 1 AC 421; (1995)17 ACSR 582, followed.

Kauter v Hilton (1953) 90 CLR 86, cited.

WHITE v SHORTALL60 ACSR 654 655

5

10

15

20

25

30

35

40

45

50

Hunter v Moss [1994] 3 All ER 215; [1994] 1 WLR 452, discussed.

Browne v Dunn (1893) 6 R 67, referred to.

Application

This was a dispute between two parties who had been involved in a domesticrelationship for some years and had rather complicated financial dealings inwhich several payments of money had allegedly been made by the plaintiff to thedefendant in exchange for which the defendant had allegedly made promises ofa transfer of shares to the plaintiff in a newly listed company. The matter involvedan alleged breach of contract and breach of trust by the defendant, for whichequitable compensation was sought by the plaintiff.

K Ryan and P Castley instructed by Stephen Bottrill Solicitors & Attorneys forthe plaintiff.

G Curtin and D Jenkins instructed by Middletons for the defendant.

[1] Campbell J. This is primarily a claim for damages for breach of a contractrelating to transfer of shares, and to enforce a trust over those shares.

[2] It raises the following issues:(a) Did the plaintiff make seven loans of money to the defendant, on the

basis that they would be secured by certain shares that the defendantwould hold in trust for her? I conclude that the plaintiff made the sevenpayments of money to the defendant that she asserted she made, that thefirst five of them were not loans when originally made, and that theparties came to agree that the amounts of money that the plaintiff hadprovided to the defendant would be treated as in effect the purchaseprice of shares that the defendant would hold in trust for the plaintiff.

(b) Did the parties contract that 222,000 shares would be transferred to theplaintiff on the plaintiff’s request after 1 August 2003? I conclude thatthey did.

(c) Independently of that contract, did the defendant show an intention todeclare a trust of 222,000 shares for the plaintiff, on terms that they weretransferable to the plaintiff after 1 August 2003? I conclude that he did.

(d) Did the plaintiff request transfer of the shares soon after 1 August 2003?I conclude she made such a request soon after 11 August 2003.

(e) Did the plaintiff tell the defendant in January 2005 that she did not wantto receive the shares? I conclude she did not.

(f) What damage has the plaintiff sustained by reason of the defendant’sbreach of contract? I conclude $548,452.

(g) Is the trust that the defendant purported to declare one that is invalidbecause it has insufficient certainty of subject matter? I conclude it isvalid.

(h) What equitable compensation is payable to the plaintiff by reason of thedefendant’s failure to transfer the shares to her when asked? I concludethat, subject to issue (j) below, the quantum is the same as the damagesfor breach of contract.

(i) Has the plaintiff established that certain shares held by RogerWilliamson or Merkaba Ltd are held on trust for the defendant?I conclude she has not established this.

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS656 NSWSC

(j) Does the fact that the shares in relation to which the trust was declaredwere restricted securities at the time of declaration of the trust, underwhich the shares could not be transferred from the defendant until after1 November 2004, affect the remedy to which the plaintiff would beentitled for breach of trust? I conclude that it does, by requiring thequantum of the equitable compensation payable to the plaintiff to bemeasured by reference to the value of the shares held on trust, at a timeafter the expiry of the restriction.

(k) Does the fact that, after declaration of the trust, the defendant imposeda “voluntary holding lock” on his shareholding, affect the remedy towhich the plaintiff would be entitled for breach of trust? I conclude itdoes not.

(l) Has the plaintiff made out any breach of fiduciary duty, independentlyof a breach of trust? I conclude she has not.

(m) Has the plaintiff established an estoppel by convention concerning theexistence of a trust? I conclude she has not.

Part A — facts

The relationship between plaintiff and defendant

[3] In 1999, the plaintiff was either divorced or separated from her husband,and had the care of their two children, Jackson and Maverick, then aged aboutfive and seven. Throughout the time that is relevant to this case, she has had fewfinancial resources of her own.

[4] In the course of 1999, she developed a relationship with the defendant, aman with considerably more financial resources than the plaintiff had.He arranged, in August 1999, for the plaintiff to move out of the old house thatshe had been living in, that was in a state of disrepair, and into more suitableaccommodation at Mermaid Beach. The defendant paid the rental for that newaccommodation, and various other household expenses.

[5] In January 2000, the defendant moved into that rented house at MermaidBeach.

[6] After a brief separation, the plaintiff and the defendant began living togetheronce again at Alcorn St, Suffolk Park in March 2002.

[7] By the end of June 2002, the defendant was making arrangements to acquirean option to purchase a property in Cooper’s Shoot Rd, Byron Bay. By this time,the defendant wished to marry the plaintiff. The location of the land at Cooper’sShoot Rd was influenced by the plaintiff’s desire to live somewhere near herparents.

[8] Over the period from August 1999 until May 2005 the defendant paid largesums of money towards the household and general living expenses of theplaintiff. He paid the rental of the premises in which she lived, paidapproximately $20,000 of the purchase price of a new car that was registered inthe plaintiff’s name, paid telecommunications bills and electricity bills, paidmedical expenses for the plaintiff and her sons, and paid numerous otherhousehold expenses. He took the plaintiff on a holiday to Mexico, London andHong Kong for a month in December 1999/January 2000, and on another holidayto the Maldives from 30 July to 11 August 2003. He is able to provide vouchersdemonstrating expenditure on such items of the order of $230,000 over the periodfrom August 1999 to May 2005. It is likely that his actual expenditure exceededthat amount.

WHITE v SHORTALL (Campbell J)60 ACSR 654 657

5

10

15

20

25

30

35

40

45

50

The launch of Unitract Ltd

[9] The defendant was a shareholder in a company called Unitract Pty Ltd. Thatcompany had the benefit of a patent application relating to a syringe, the needleof which would retract automatically and permanently inside the barrel once thesyringe had been used. That was thought to be advantageous in preventing spreadof infection arising from re-use of syringes or needlestick injuries. Theshareholders in Unitract Pty Ltd set about arranging for a public share capitalraising by a company that would exploit the patent.

[10] The chosen vehicle for making the initial public offering was MusgraveBlock Holdings Pty Ltd (Musgrave), a company that was already listed on thestock exchange, but whose shares were suspended. On 11 July 2002, anagreement was entered between Musgrave and Unitract Pty Ltd, under whichMusgrave would acquire from the shareholders in Unitract Pty Ltd all theirshares. In return Musgrave would issue shares in itself to the former shareholdersin Unitract Pty Ltd and certain other people nominated by Unitract Pty Ltd. Thatagreement was conditional upon Unitract issuing shares in itself to raise$400,000 by 19 July 2002, a further capital raising (by means of an issue of 11mshares at 20c each) occurring no later than 11 October 2002, Musgrave issuinga prospectus by no later than 12 September 2002, and reinstatement of quotationof the shares occurring on or before 15 October 2002. The agreement providedfor the defendant selling the 1.5m shares he held in Unitract Pty Ltd, and beingissued with 1.5m shares in Musgrave. At the time of completion of theagreement, Musgrave would change its name to Unitract Ltd. I will sometimesrefer to Musgrave as “Unitract”.

[11] The Australian Stock Exchange (ASX) imposed a condition on Unitract’sshares being quoted. That condition required that the defendant’s 1.5m shares (aswell as certain other shares of promoters and people connected with thepromotion) would be restricted securities. In broad terms, that restrictionprohibited dealing in the shares to which it applied, meant that the particularshares to which it applied were not quoted on the stock exchange (and so couldnot be sold by an on-market transfer), and were subject to a “holding lock” thatwas designed to prevent any transfer of the shares being registered. (I consider itin more detail at [312] below.) For the defendant’s shares, that restriction wouldbe for 2 years from the date of listing. Quotation of Unitract’s shares was in factachieved on 1 November 2002. Hence the restriction on the defendant’s 1.5mshares expired on 1 November 2004.

[12] From 1 November 2004 to 1 May 2005 all 1.5m of the defendant’s shares,and from 1 May to 1 November 2005, 500,000 of the defendant’s shares havebeen subject to a “voluntary escrow”.

The first six payments by the plaintiff to the defendant

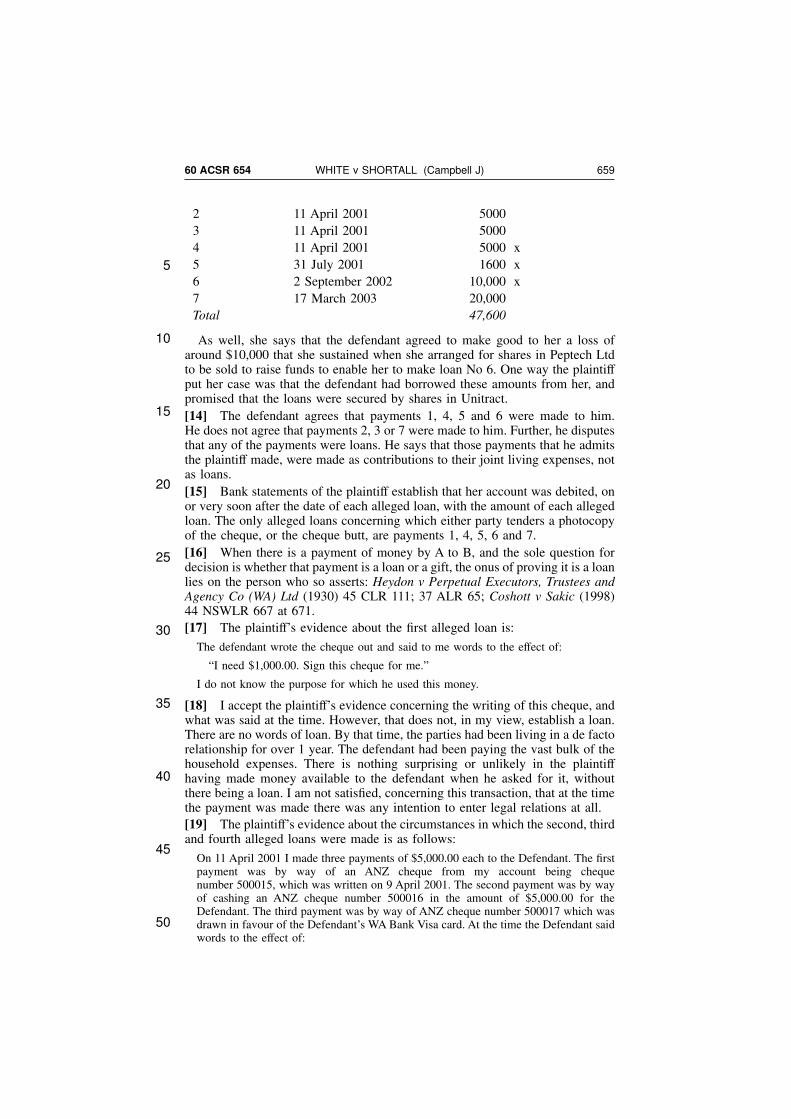

[13] The plaintiff had a cheque account with the ANZ Bank at Bundall. Sheasserts that seven amounts drawn on that account were lent to the defendant.Those amounts are:

Payment No Date $ Agreed bydefendant

1 21 March 2001 1000 x

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS658 NSWSC

2 11 April 2001 5000

3 11 April 2001 5000

4 11 April 2001 5000 x

5 31 July 2001 1600 x

6 2 September 2002 10,000 x

7 17 March 2003 20,000

Total 47,600

As well, she says that the defendant agreed to make good to her a loss ofaround $10,000 that she sustained when she arranged for shares in Peptech Ltdto be sold to raise funds to enable her to make loan No 6. One way the plaintiffput her case was that the defendant had borrowed these amounts from her, andpromised that the loans were secured by shares in Unitract.

[14] The defendant agrees that payments 1, 4, 5 and 6 were made to him.He does not agree that payments 2, 3 or 7 were made to him. Further, he disputesthat any of the payments were loans. He says that those payments that he admitsthe plaintiff made, were made as contributions to their joint living expenses, notas loans.

[15] Bank statements of the plaintiff establish that her account was debited, onor very soon after the date of each alleged loan, with the amount of each allegedloan. The only alleged loans concerning which either party tenders a photocopyof the cheque, or the cheque butt, are payments 1, 4, 5, 6 and 7.

[16] When there is a payment of money by A to B, and the sole question fordecision is whether that payment is a loan or a gift, the onus of proving it is a loanlies on the person who so asserts: Heydon v Perpetual Executors, Trustees andAgency Co (WA) Ltd (1930) 45 CLR 111; 37 ALR 65; Coshott v Sakic (1998)44 NSWLR 667 at 671.

[17] The plaintiff’s evidence about the first alleged loan is:

The defendant wrote the cheque out and said to me words to the effect of:

“I need $1,000.00. Sign this cheque for me.”

I do not know the purpose for which he used this money.

[18] I accept the plaintiff’s evidence concerning the writing of this cheque, andwhat was said at the time. However, that does not, in my view, establish a loan.There are no words of loan. By that time, the parties had been living in a de factorelationship for over 1 year. The defendant had been paying the vast bulk of thehousehold expenses. There is nothing surprising or unlikely in the plaintiffhaving made money available to the defendant when he asked for it, withoutthere being a loan. I am not satisfied, concerning this transaction, that at the timethe payment was made there was any intention to enter legal relations at all.

[19] The plaintiff’s evidence about the circumstances in which the second, thirdand fourth alleged loans were made is as follows:

On 11 April 2001 I made three payments of $5,000.00 each to the Defendant. The firstpayment was by way of an ANZ cheque from my account being chequenumber 500015, which was written on 9 April 2001. The second payment was by wayof cashing an ANZ cheque number 500016 in the amount of $5,000.00 for theDefendant. The third payment was by way of ANZ cheque number 500017 which wasdrawn in favour of the Defendant’s WA Bank Visa card. At the time the Defendant saidwords to the effect of:

WHITE v SHORTALL (Campbell J)60 ACSR 654 659

5

10

15

20

25

30

35

40

45

50

“I need $10,000.00 in cash but I do not want a cheque for this amount. Sign 2 chequesfor $5,000.00 each. I do not want to have to fill out the disclosure forms required ifI cash a cheque for $10,000.00.”

To the best of my recollection, I was with the Defendant when he cashed the twocheques for $5,000.00 each, although I do not know the purpose for which theDefendant used this money.

[20] It is the payment of $5000 to the defendant’s Visa card account that thedefendant admits receiving. By April 2001, the plaintiff was an additionalcardholder on the defendant’s Visa card. It is not established to what extent, if atall, the plaintiff actually used that card.

[21] I accept the plaintiff’s evidence about the making of these three payments.For the same reasons as I have given concerning the first alleged loan, I am notsatisfied that the plaintiff has discharged the onus of establishing that any of thepayments made on 11 April 2001 were loans.

[22] Initially, the plaintiff’s evidence about the making of the fifth loan was:

On 31 July 2001 I made a payment of $1,600.00 to the Defendant by way of cashingANZ cheque number 001081 which was written on 25 July 2001, for the Defendant.The Defendant wrote out the cheque and said words to me to the effect of:

“I need $1,600.00. Sign this cheque for me.”

After the defendant had denied in his affidavit that he had written out that cheque,and exhibited a copy of the four cheques that he admitted receiving, the plaintiffaccepted that it was her handwriting on the cheque, “and that I made an error inparagraph 4(iv) of my affidavit sworn 28 August 2006”. If the plaintiff wrote outthe cheque herself, that makes implausible the words she attributed to thedefendant on that occasion. I do not accept that the defendant said such words.Further, even if the plaintiff’s initial version had been correct, that would not havebeen enough to establish that it was agreed that there would be a loan, for thesame reasons as I have given concerning the first alleged loan.

[23] On 14 and 16 November 2001, soon after the plaintiff had received$20,000 from her former husband, the plaintiff’s parents purchased two parcelsof shares in Peptech Ltd, 4800 shares in all, for a total outlay of $19,972.31. Theshares were purchased through a broker, Mr David Missen, of Bell Securities.He is the same broker who acted for the defendant. These shares were treated asthough they were the plaintiff’s.

[24] The plaintiff’s account, in her affidavit of 28 August 2006, of how thepayment on 2 September 2002 came to be made is as follows:

Prior to me making this payment to the Defendant, the Defendant said to me words tothe effect of:

“I need $10,000.00 for payment of part of the deposit on land which I am purchasingat Coopers Shoot. I know that you bought $20,000.00 worth of Peptech shares. If youlet me sell them and lend the proceeds of sale to me, I will repay you the $20,000.00which you originally used to purchase the shares so that you do not make a loss. I willmake this repayment to you by way of $20,000.00 worth shares in Unitract at20 cents per share.”

[25] In her affidavit in reply of 31 October 2006 she confirmed her earlieraccount, and added:

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS660 NSWSC

… he said “I need this for the purchase of the Cooper’s Shoot property” and he said“I will treat the loss on your shares as a loan which will make your loans to me totalabout $40,000.00”.

[26] The cheque by which this payment was made was filled out by thedefendant, and signed by the plaintiff. The defendant originally wrote that thecheque was payable to “Underline Pty Ltd”, but above that the defendant wrote“Please pay cash” and the plaintiff signed the alteration.

[27] The broker’s contract note establishes that the 4800 Peptech shares weresold on 21 August 2002, and produced total net proceeds of $10,586.26.

[28] By July 2002, some difficulties had re-emerged in the relationship betweenthe plaintiff and the defendant. Around 31 July 2002 the plaintiff first attended aconsulting psychologist, Mr Kieran Riordan, about various difficulties she wasencountering, including in her relationship with the defendant. She continued tosee Mr Riordan from time to time until May 2005. The defendant paid the feesassociated with those consultations, at least so far as consultations occurring after16 September 2002 are concerned. At a time she puts at “before August 2002”she had told the defendant that she did not want to marry him, but in September2002 she was still wearing an engagement ring he had given her, and she was stillcontemplating an ongoing domestic relationship with him.

[29] The defendant denies the plaintiff’s account of the circumstances ofpayment of $10,000 in September 2002. According to him, at the time of handingover the cheque the plaintiff said: “I would like to contribute towards the cost ofthe land and the house so that I can feel it is my home and not just yours”.He says he did not need $10,000 from the plaintiff. The cheque account ofUnderline International Pty Ltd, that he used to fund ordinary living expenses,had a deposit of $10,000 made to it on 2 September 2002. This might be theplaintiff’s cheque, but it is not possible on the evidence to make a positivefinding, and if it was the plaintiff’s cheque one wonders why the defendant hadthe cheque altered to be payable to cash. That account of Underline InternationalPty Ltd on 2 September 2002 also had another amount, of $59,500, deposited toit. The trust account ledger of the solicitor who acted for the defendantconcerning acquisition of the Cooper’s Shoot Rd property shows one amount of$19,982.80 identified as “deposit moneys” passing through the trust account inJuly 2002, and a further amount of $49,980.80 identified as a “deposit” passingthrough the trust account in March 2003, but nothing passing through the trustaccount between those times. The defendant was incurring architectural fees inconnection with the proposed house at Cooper’s Shoot Rd, but the evidence doesnot disclose when those fees became due. At least some of the architectural feeswere paid, but the evidence does not disclose when. In this situation, it is notpossible to make any positive finding about what the defendant did with the$10,000 he received in September 2002.

[30] I will defer making findings about the basis on which the $10,000 was paidin September 2002 until other factual matters have been recounted.

[31] The relationship between the plaintiff and the defendant broke down inOctober 2002. Around that time, they concluded that they should separate, butthey did not separate immediately. They discussed the defendant providing someform of financial assistance to the plaintiff, because she did not have any incometo support herself and her two sons. It was he who offered to provide support —it is not as though she had to drag a promise out of him. He told her he waswilling to pay for the rent on the home for a period of time, and some other

WHITE v SHORTALL (Campbell J)60 ACSR 654 661

5

10

15

20

25

30

35

40

45

50

expenses such as medical expenses, and the boys’ tutoring and sports expenses.He also indicated his willingness to continue to pay for her counselling withMr Riordan. At no time during those discussions did the plaintiff assert that thedefendant owed her the various amounts that she had paid him prior to that time,and which she now alleges were loans.

[32] That the defendant made this offer of financial support is consistent withhis treatment of the plaintiff throughout the relationship — concerning financialmatters, he was considerate and generous.

[33] Various of the notes that Mr Riordan made in the course of counsellingsessions were admitted as business records. Some care needs to be exercised inusing those notes, because Mr Riordan himself makes clear that he was not tryingto maintain a complete record of things said to him in the course of consultations,and he recognises that sometimes — particularly when emotions were runninghigh in the consultations — the notes might be simply inaccurate. Even so, someof his notes assist in clarifying the facts.

[34] On 24 August 2002, Mr Riordan made some notes at a conference with theplaintiff. He said concerning them:

Louise White came to me hysterical and deeply distressed and very — it was like in ahysterical or distressed manner, described me money that was outstanding with Alan.And I jotted down some notes which have absolutely no — well, to my mind I wouldn’tguarantee their accuracy in terms of those numbers there on the page, okay?

[35] When the notes were made under those circumstances, I would not drawanything from them beyond the fact that on that day the plaintiff asserted that thedefendant owed her money, that an amount of $10,000 was at least part of it, andthat it had something to do with the Cooper’s Shoot land. I note that thisconference was 3 days after the Peptech shares were sold.

[36] On 16 September 2002, the plaintiff told Mr Riordan that she wantedfinancial support — a solid commitment, written down.

[37] On 28 September 2002, Mr Riordan made a note, in the course of aconsultation with the plaintiff “my $10,000 invested in the land now”. Aftercross-examination of both the plaintiff and Mr Riordan, I am satisfied that theimport of that note is not that the plaintiff told him that she had made aninvestment of $10,000 in the land. Rather, it is that she had told Mr Riordan thatshe had provided $10,000 to the defendant, and that he had invested it in the land.

[38] In her affidavit in reply, of 31 October 2006, the plaintiff gives manydetails, that she had not previously given, concerning conversations about moneyor shares that she had with the defendant. That evidence includes:

From as early as August 2002, the Defendant would say words to the effect of:

“I will hold shares in trust for you.”“You are going to be a wealthy woman when you get your shares.”“You will be able to buy a house for you and the boys with the money that you willreceive from the shares.”

At various times when the Defendant asked me for money, before the float of Unilifehe would say words to me to the effect of:

“I need your money so that I can buy shares in the company before it floats. I am ableto buy shares at the promoter’s rate of four cents per share.”

Since floating Unitract has changed its name again, to Unilife Medical SolutionsLtd. It is Unitract that the plaintiff refers to as “Unilife”.

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS662 NSWSC

[39] She says that at the time of handing over the cheque for $10,000 inSeptember 2002 he said to her:

I am holding the shares in trust for you and once the company is floated, I will transferthe shares to you.

The defendant at about October 2002 rarely talked of anything else other than thesubject matter of Unilife shares, as the company was about to float. The defendant oftensaid words to the effect:“You will be a rich woman when you get your $40,000.00 worth of shares. You will beable to buy a house.”

Later on in about the middle of November, he said to me words to the effect of:

“I made five million dollars last Friday from the shares.”

[40] She also says that:

When discussing the shares with me, the defendant would always say, “I am holdingthese in trust for you Louise”.

and:

The defendant had said to me about his calculation of about $40,000 in loans to him,that “I will be able to get in before the float and buy shares at four cents each”.

[41] In November 2002, the defendant and plaintiff moved to a differentresidence, at unit 25, The Links, 76 Broken Head Rd, Byron Bay. These premiseswere rented, with the defendant still paying the rent.

[42] On 6 January 2003, the plaintiff and the defendant separated.

[43] Pursuant to leave to give oral evidence on a topic that her affidavit of28 August 2002 had dealt with in inadmissible form, the plaintiff said that aroundChristmas 2002 she received a $20,000 payment from her former husband.In early January 2003, she says that she had a conversation with the defendant asfollows:

He said … “I want you to think about a deal I’m going to propose to you. If you giveme the $20,000 I will, in turn, give you shares at 90 cents a share and I want you to thinkabout this because it is a good deal for you as the shares are trading at a dollar twentyso you are making a profit” and he brought up that conversation a number of times, whata deal it was for me, telling me — he said — Alan said, “you know this is a good dealfor you”.

Q — And when you say he brought up that again was that in person or over thetelephone? A — Stressed in person but it was reiterated over the phone.

[44] Mr Riordan’s notes of a session with the plaintiff on 5 February 2003include the entry:

$40,000

[200,000 shares] In Alan’s name until he can sell

[July 2003/4] …? Anytime as needed?

Also on 5 February 2003, immediately below the note just quoted, Mr Riordanwrote, “Tax issues? Centrelink issues?”

[45] Mr Riordan’s evidence concerning the topic of that note was:

Louise is concerned about money, amongst other issues she is bringing to this session,roughly, I am not sure if it was 200 or more than that, but at least around 200,000 shares.She is saying in Alan’s name until she can sell in July 2003/4 anytime as needed. I am

WHITE v SHORTALL (Campbell J)60 ACSR 654 663

5

10

15

20

25

30

35

40

45

50

not sure what the tax issues are or Centrelink issues are if I cash these shares or achieveownership of these shares in that tax year. That is one of her worries. That is what Ithink it means.

Q — Does the figure $40,000 bring back any memory in calculation of the 200,000shares? A — It is obvious to me that Louise associates — she checks in with me thatthe $40,000 equates to 200,000 shares held in Alan’s name on her behalf. That is whatshe is saying to me in this session.

[46] Mr Riordan had earlier explained:

Q — Can I just ask you were the tax issue and Centrelink issues concerning LouiseWhite? A — Yeah, recently separated single mum, wondering how she’s going to gether life together and considering tax and Centrelink issues, around when she has accessto it is written 200,000 shares in July.

Q — I think the dates after July are 2003/2004? A — Yes, she was working out whatearnings were in the tax years in 2003/2004. I remember in this and other sessionssaying go to your accountant and get advice about this. Obviously it is of stress, it iscausing anxiety for you and it an issue you need to take to the appropriate professionaladvisor.

[47] I accept that evidence of Mr Riordan.

[48] After the plaintiff and the defendant had separated, but prior to 17 March2003, the plaintiff wrote the defendant an undated letter that asked the defendantfor assurance that he would honour an agreement she said he had made in anearlier session with Mr Riordan, concerning payment of the first year’s rent, andfor the next 2 years half the rent, providing particular types of benefits for theboys, and paying for her ongoing sessions with Mr Riordan. She said:

Please re-affirm your stated commitment as I need asurety [sic] & a basis for budgetingand planning right now.

[49] That letter says nothing about shares held on trust, or any alleged loans,but I do not regard that as something that detracts from the plaintiff’s case. Theletter had one topic, namely seeking reassurance about a particular agreementpreviously made about the defendant assisting with her ordinary householdexpenditure, when there was an immediate need for the plaintiff to know whatincome would be available to her for those purposes in the immediate future.

[50] Some indication of the state of relations between the plaintiff and thedefendant at that stage comes from the ending of the letter:

Maverick & Jax send their love.

Hoping you are well and not too jetlagged.

Love to you always.

Louise X.

[51] At the plaintiff’s request, the defendant agreed to attend one counsellingsession with Mr Riordan. That counselling session took place on 17 March 2003,at Mr Riordan’s office. Early in the session he asked each to state their goals forthe session. For the plaintiff, he recorded: “clarity re Alan’s $ support postseparation and question of shares held by him that are ‘mine’: no security. nopaperwork”. His note about the defendant’s goal was: “Ditto re above”, plus atopic relating to the emotional side of their relationship. He records, at one stage,the plaintiff saying “want support with boys, rent, ‘transition’” and “what youowe me and when I can get it”.

[52] His notes of 17 March 2003 also record:

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS664 NSWSC

[Alan] + [Louise] agree roughly on a few issues:

1. $25,000 shares to each boy from July ‘03

2. [Louise] to ring [Alan] for big bills with boys up to Uni age. Then [Alan] dealdirect with boys,

3. [Alan] agrees — 100% rent up to 450 p.w. 1yr + 50% rent two further years.

4. medical tuition sports education expenses [Alan] happy to contributesignificantly.

[Louise] “Nervous re no security with my shares” “They are in your name — I have nosecurity. What if you die?”

[Alan] Agrees to write letter indicating what shares are held in trust for Louise. Explainsavailable in August ‘03.

[53] Mr Riordan amplified that note in oral evidence, saying:

Louise was concerned there was no paperwork with shares held by him on her behalf.That is one of Louise’s major goals, was for that session to clarify that and achievepaperwork on that.

[54] The defendant gives a lengthy account, extending over approximatelythree pages of his affidavit, of the events of 17 March 2003. It is to the followingeffect. The plaintiff was very distraught through the meeting with Mr Riordan,and the defendant was also very upset. The plaintiff at various times expressedconcern that he would abandon her and not pay her rent or help her, and that shewould end up on the street. He tried to reassure her, by pointing to the way thathe had provided for her during the relationship. Mr Riordan then said “yes butwhat happens if you die, she has nothing in writing to give her security that therent would continue to be paid for a reasonable time”. Up to that time there hadbeen no mention of Unitract shares. The defendant said that he would be willingto put something in writing to give the plaintiff some level of comfort.Mr Riordan then suggested “why not agree to issue shares to cover the level offunding that would give Louise some comfort if you died? Then the executor willhave something in writing.” The defendant enquired how many shares theplaintiff would expect, to which Mr Riordan said “Well I understand Louisecontributed some money to the household while you were in a relationship, sowhy not use the amount of shares that are of similar value to that?” When thedefendant said he had no record of how much she might have contributed, theplaintiff then said “It’s about $40,000, I estimate it would be approximately222,000 shares”. Mr Riordan enquired whether the defendant would be willing toput that in writing for Louise, and he agreed. The defendant continues:

At that time I was aware that Unilife shares were trading at approximately $0.90 pershare. At the time, however, I was upset, and this conversation was taking place in anemotionally charged atmosphere. I desired to assist the plaintiff with some expenses fora reasonable time given her financial circumstances and apparent distress. For thosereasons, together with the statement to the effect that any document concerning theshares was to be some form of comfort to her, I agreed with this proposal.

[55] The defendant says that he did not calculate the figure of 222,000 shares,and that he adopted that figure because that was the number that the plaintiffsuggested to him. He says he did not consider that he was undertaking any legallybinding obligation, and:

I did not give any thought to the fact that the value of 222,000 at that time was some$200,000, well exceeding the figure given to me as being the approximate total of the

WHITE v SHORTALL (Campbell J)60 ACSR 654 665

5

10

15

20

25

30

35

40

45

50

plaintiff’s contributions. Nor did I consider how the value of those shares mightcompare to the total of my expected future contributions for the plaintiff’s rent and otherexpenses.I was aware, although I cannot recall thinking of it at the time, that I would not be ableto transfer any of my shares to the plaintiff after 1 August 2003 but before 1 November2004 because of the mandatory escrow applying to my shares.

[56] According to the defendant, Mr Riordan virtually dictated the terms of adocument, which the plaintiff signed then and there.

[57] According to the plaintiff, at Mr Riordan’s office:

Alan said — I am holding $40,000 worth of shares at 20 cents a share and $20,000 at90 cents a share — and Alan calculated that — I calculated that to be 222,000 shares.Q — When you used the words “I calculated that to be 222,000 shares” were youreferring to Alan or yourself? A — Alan.Q — At that stage had you paid him the $20,000 that was mentioned there? A — NoI had not.

She says no letter was written at Mr Riordan’s office.

[58] According to the plaintiff, she and the defendant then returned home, to theLinks. There, the defendant said he would not write the letter until she signed acheque for $20,000 over to him. The defendant then wrote out, in the plaintiff’schequebook, a cheque dated 17 March 2003, marked “Please pay cash”, in thesum of $20,000.

[59] The cheque is in evidence, and it is common ground that all of the writingon the face of the cheque, apart from the signature, is that of the defendant. Thecheque butt relating to the cheque is also in evidence. It is entirely in thedefendant’s handwriting, and reads:

17/3/03.Alan.$20,000.

[60] The face of the cheque bears a stamp showing it as being processed by thebank on 18 March 2003. The plaintiff’s cheque account pass sheet also recordsthe cheque as being presented on 18 March 2003.

[61] According to the plaintiff, it was when she had signed and handed over thecheque on 17 March 2003 that the defendant wrote out a document that is ofcentral importance to the plaintiff’s case. That document is undoubtedly in thehandwriting of the defendant, and signed by him. Now, it reads as follows:

Louise White,25 THE LINKS.BYRON BAY.NSW 2481 17/3/03.Dear Louise,THIS LETTER IS TO CONFIRM THAT I AM HOLDING IN TRUST FOR YOU222,000 UNITRACT SHARES. THESE SHARES WILL BE TRANSFERRED TOYOUR NAME AND CONTROL, AT ANY TIME THAT YOU REQUEST, AFTER1/AUGUST/2003. IN THE CASE OF MY DEATH, THE ABOVE TRANSFER OF222,000 UNITRACT, TO YOUR NAME, WILL BE AUTHORISED BY MYEXECUTOR, STEVEN SHORTALL.I FURTHER COMMITT TO MAKE AVAILABLE 25,000 UNITRACT SHARES, FORFINANCIAL SUPPORT FOR [AS] EACH [AS] BOTH MAVERICK AND JACKSON,ON OR AFTER 1/AUGUST/2003.[ALAN SHORTALL].

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS666 NSWSC

ALAN DENIS SHORTALL.18/3/03.[AS].

[62] The plaintiff says that the defendant wrote that letter when she had justsigned the cheque made out to the defendant for $20,000. She says that asoriginally written, the final sentence included the phrase “for each Maverick andJackson”, that on 18 March 2003 the defendant amended that phrase to read “forboth Maverick and Jackson”, and that on 18 March 2003 he initialled thatalteration, on either side of the “each” that he had crossed out, dated thedocument “18/3/03” at its end, and also initialled that dating. The defendant leftthe original of the letter with the plaintiff, and she has had possession of it eversince.

[63] Mr Riordan, in evidence, denied that he was present when the documentcame into existence, denied that he suggested the wording to Mr Shortall, andsays that the first time he saw the document was when the plaintiff brought aphotocopy of it to his attention, in distress, in about August 2003. He says thatin the course of the counselling session on 17 March 2003 the defendant:

… expressed a sincere desire to offer a generous level of support to Louise whilst shemade a transition into independence as a sole mother.

[64] Mr Riordan says:

My clear recollection in that session, I asked both parties to get independent legalcounsel for any financial agreement they would come to post separation.

[65] After his suggestion, on 17 March, of legal advice:

Q — Was there any response from either of the parties? A — I do recall Alan sayingthat won’t be necessary because he’s CEO or director and he’s got lots of experience inthese matters and they can sort that out for themselves.

Digression regarding procedure

[66] I interrupt the narrative to record here some matters concerning theprocedural history of this case that are relevant to assessments of credit. Theproceedings were begun on 12 May 2006 with the filing of a summons in court,and the seeking of short service of it. An application for expedition was made,that resulted in Young CJ in Eq on 29 September 2006 fixing it for hearing beforeme for 1 day on 24 October 2006. At that stage his Honour noted:

No amendment to the Statement of Claim is proposed. Note that all the evidence is filed.

[67] By that stage, the plaintiff had filed two affidavits-in-chief, one made on11 May 2006, and the other on 28 August 2006. Both affidavits containedmaterial that was clearly inadmissible concerning critical parts of the plaintiff’scase.

[68] At that stage, the defendant had filed only an affidavit that was ultimatelynot read at the trial. On 20 October 2006, after advice from counsel who had onlyrecently been briefed, the defendant swore another, and more detailed, affidavit.

[69] When the matter came on for hearing before me on 24 October 2006, thedefendant sought leave to read the affidavit of 20 October 2006. It was necessaryto seek that leave, because Brereton J, on 25 August 2006, had directed that thedefendant not be entitled to rely, without leave of the court, on any affidavitevidence that had not been served by 21 September 2006. I granted the leave, on

WHITE v SHORTALL (Campbell J)60 ACSR 654 667

5

10

15

20

25

30

35

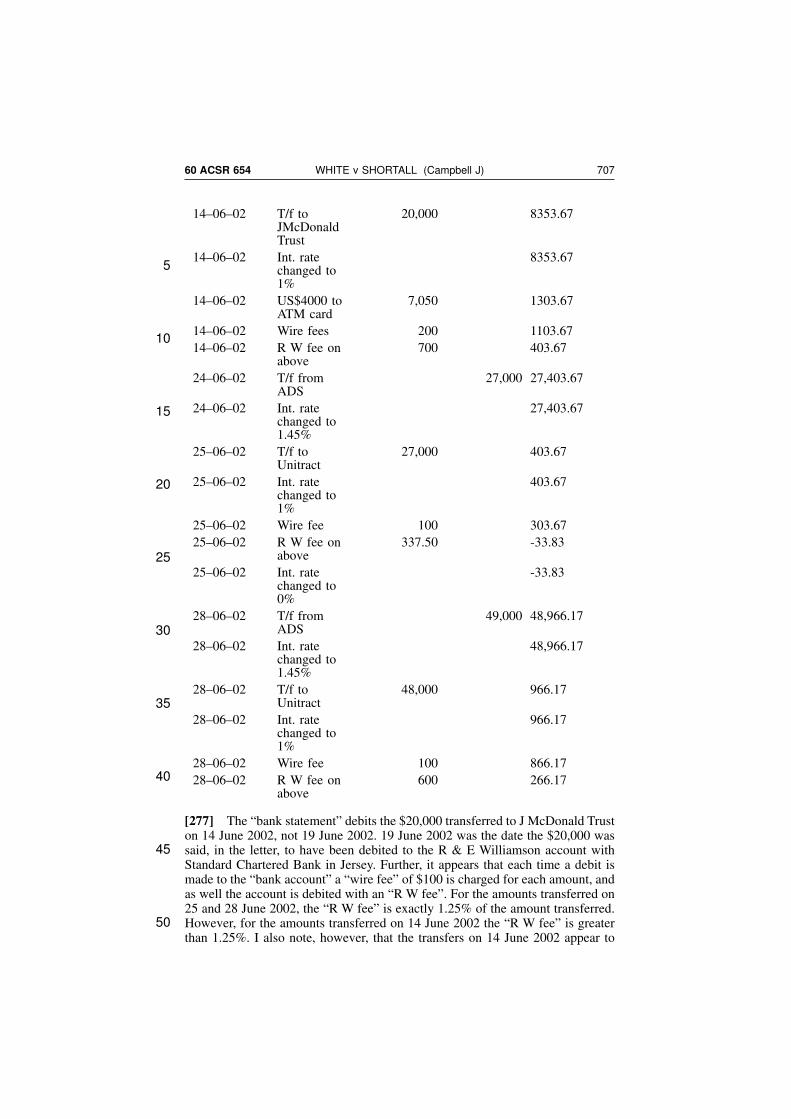

40

45

50

the basis that it was necessary for the late affidavit to be read to enable the realissues to be decided. That resulted in an adjournment, during which the plaintiffswore, on 31 October 2006, an affidavit in reply to the defendant’s affidavit of20 October 2006. In that affidavit in reply she gave evidence of numerous mattersrelevant to her case for the first time.

[70] As was inevitable as soon as objection was taken, central parts of theplaintiff’s affidavit-in-chief were struck out. I then granted leave for the plaintiffto give evidence on those topics orally. As well, oral evidence was also receivedfrom the plaintiff on some topics on which she had not given affidavit evidenceat all.

[71] Frequently, it is very damaging to the credibility of a plaintiff’s case ifimportant evidence relating to it emerges only late in the course of evidence. Thereason for this is that the court is usually justified in assuming that the legalrepresentatives of a plaintiff embarking on something as significant andpotentially expensive as Supreme Court litigation will properly proof their client,obtain from their client all relevant details of the story relevant to the case, andinclude that material in affidavits-in-chief.

[72] I cannot make that assumption in the present case. The plaintiff’sevidence-in-chief was so clearly inadequate it could not have been properlyprepared. The statement of claim pleads evidence (contrary to r 14.7 of theUniform Civil Procedure Rules 2005 (NSW)), and claims something unknown tothe law, namely an interlocutory declaration. Notwithstanding the assurancegiven to Young CJ in Eq, in the course of the trial the plaintiff sought, and wasgranted, leave to amend her statement of claim in significant ways. At the end ofthe trial the plaintiff sought leave to make yet another amendment to thestatement of claim which leave was refused.

[73] The case was originally set down for 1 day. The first day’s hearingconcluded at 2.30 pm, because of the adjournment that I have mentioned. Whenthe hearing resumed, it continued for a further 3 days. On each of those 3 daysthe hearing concluded after ordinary court hours — at 4.30 pm, 4.50 pm and5.25 pm. Even with those extended hours, the plaintiff’s counsel needed to makehis submissions-in-reply in writing. The plaintiff’s counsel sought to callMr Riordan to give oral evidence, as a witness-in-reply, when on at least sometopics he should have been a witness-in-chief. The evidence of Mr Riordan thatwas really in chief was ultimately received only because the defendant could notpoint to any prejudice in its having been given out of the usual order. In fairnessto the plaintiff’s lawyers, though, I should say that the reason why no affidavitfrom Mr Riordan was filed, was because he felt that his obligations ofconfidentiality to his clients precluded him from giving an affidavit or statementwhen there was no legal compulsion for him to do so. Even taking into accountthat part of the extra length of the trial arose from the defendant’s late affidavit,I have difficulty in seeing how a lawyer who understood what was involved in thecase could have thought it would have been concluded in 1 day.

[74] The plaintiff was cross-examined about why she had not included in anyof her affidavit evidence mention of the defendant asking for $20,000 at any timeprior to the counselling session on 17 March 2003. Her answer was, in substance,that she did not have an answer, and didn’t realise it was important to put it inthe affidavit. I accept that her response is truthful.

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS668 NSWSC

Findings on central factual matters

[75] I accept the plaintiff’s evidence in [24] above about the circumstances inwhich the payment of $10,000 was made on 2 September 2002. While thedefendant talked about that $10,000 being “lent”, the conversation makes clearthat what he was proposing was not a “loan” of the conventional type. Rather,what he was proposing was that if she paid him the money, he would in returncause her to have $20,000 worth of shares in Unitract at 20c per share. That isin substance a purchase, even though he called it a loan.

[76] I accept that, possibly at the time of making the advance of $10,000 fromthe Peptech shares, and more likely than not prior to the time of the float on1 November 2002, the defendant told the plaintiff, in substance, that all themoney she had provided to him, which he quantified at $40,000, would be treatedas loans — and that he made clear that what he meant was “loans” of the sametype and on the same basis as he had proposed concerning the proceeds of saleof the Peptech shares. At some stage, and prior to 5 February 2003, the defendanthad stated to the plaintiff the result of the calculation that was involved inapplying that basis to $40,000, namely, that he would hold 200,000 shares in trustfor her.

[77] I do not accept the defendant’s account of the meeting on 17 March 2003,nor his account of how the document sued on came into existence. I accept theevidence of Mr Riordan and the plaintiff on those matters. At Mr Riordan’s office,on 17 March 2003, the defendant clearly stated that the shares he held in trust forthe plaintiff were ones that could be transferred in August 2003.

[78] I am not prepared to accept uncorroborated evidence of the plaintiff aboutthe precise date that particular conversations occurred — she has demonstrated,and herself admits to, some unreliability concerning dates. However, apart fromthe precise dating, I accept that conversations of the general type that she deposesto, about shares (in general), and 200,000 shares in particular, being held in trustfor her, occurred. In general, I find her a credible witness. I also accept that, inthe early months of 2003, the defendant proposed to the plaintiff that if she wouldprovide him with another $20,000 he would hold shares for her on the basis thatthey cost 90c each.

[79] The defendant gave evidence with clarity, precision, and confidence.Unfortunately some of it is inconsistent with other independent evidence that Iaccept. Other parts of it are unusual, and tell the sort of story that requires veryclose scrutiny before it is accepted. In these circumstances, I do not regard hisuncorroborated word as sufficient to discharge an onus of proof, save concerningmatters that, by reference to other established facts, have a very real possibilityof being correct.

[80] The defendant’s evidence (at [54] above) that at 17 March 2003 the priceof Unitract shares was approximately 90c is wrong. On that day, the closing priceof the shares was $1.23. The lowest closing price they had achieved during thewhole of March 2003 was $1.12, on 7 March 2003. By contrast, in January 2003the shares ranged between a closing price of 62c on 2 January 2003 (a day ofcomparatively low trading volumes, hardly a surprise at that time of the year) toa high of 91c on 14 January 2003. On all days bar two in January 2003 their pricewas below 90c. Thus, it seems to me unlikely that the defendant would have said,in January 2003, “it is a good deal for you as the shares are trading at $1.20”, asthe plaintiff contends: at [43] above.

WHITE v SHORTALL (Campbell J)60 ACSR 654 669

5

10

15

20

25

30

35

40

45

50

[81] The shares (which had been offered in the float at 20c) had closed at 24con the first day of listing, 1 November 2002. Thereafter, the trend of share priceswas steadily up. I accept that, before he would sign an acknowledgement ofholding 222,000 shares in trust, he insisted on being paid the $20,000 that wasneeded to notionally pay for the additional 22,000 shares. He actually signed theletter only after he had her cheque for $20,000.

Events after execution of the document of 17/18 March

[82] Relations between the plaintiff and the defendant continued to be cordial,even affectionate, after the letter of 17/18 March 2003 was signed. The defendantcontinued to visit the plaintiff and stay with her from time to time. He took heron a holiday in the Maldives between 30 July and 11 August 2003. That holidaycost him of the order of $40,000, and his itemisation of the expenses suggests itwas quite luxurious. During their stay in the Maldives, the defendant said to theplaintiff words to the effect of:

You are a rich woman now Louise.You will be able to set yourself up in a home for you and the boys when we get back.Trust me Lou, I’ll take care of everything for you.Have you thought about where you would like to buy a house.There is no need to worry about anything Louise, I will sort out the transfer of shareswhen we get home.

[83] After their return, the defendant spoke to the plaintiff about the shares, andsaid words to the effect of:

I will look after things with your shares.

I will make sure that they are transferred to you, you will be a rich woman and can buya house. Trust me.

[84] Soon after their return from the Maldives, the plaintiff asked him totransfer the shares to her, but he did not do so. The following conversationensued:

DEFENDANT: “It’s not the right time to transfer the shares now Louise”.

PLAINTIFF: “But I need these shares as you have promised so that I can sell them.I need this money”.

DEFENDANT: “I can’t transfer the shares to you now, I will give you some money forChristmas”.

[85] That response was not an indication of a permanent inability, or anunwillingness to transfer the shares. Rather, as the plaintiff said in oral evidence,the theme of his reply was “I can’t do it right now, I am too busy, I have too muchgoing on, don’t worry you will get your shares”.

[86] The defendant continued to subsidise the plaintiff’s rental, and pay otherexpenses connected with her and her children, in the way he had said he would.An indication of the state of relations between them is that in September 2003 hegave her a new mobile phone. He responded, on 22 September 2003, to amessage in which she thanked him for it, saying:

I miss you and no matter what we will always be soul mates, in my mind. You still havea large part of my heart in your hands. I miss you.

Love, Alan.

While in the Maldives, though, he had told her he would be taking anotherwoman to his son’s wedding.

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS670 NSWSC

[87] On 29 October 2003, an electronic transfer of funds to the plaintiff’s bankaccount occurred, in the sum of $5000, accompanied by the message “love AlanShortall”. On 12 December 2003, another electronic transfer of $5000 was madeto her account, this time accompanied by the message “happy Christmas AlanShortall”. These were amounts additional to the financial benefits he hadpromised in March 2003.

[88] In about the middle of January 2004 the defendant rang the plaintiff andtold her that there would be a newspaper story published which would be criticalof him. He said, “if Ben Hills contacts you, you are to deny everything. I cannottransfer the shares to you now as everyone is watching me”. He also said to her“tell anyone who asks not to sell their shares, the price will probably drop, butit will go up again”. Ben Hills is the journalist who wrote the newspaper story.

[89] On the weekend of 17–18 January 2004 the article that the defendant hadbeen talking about appeared in the Sydney Morning Herald. It was critical of boththe defendant, and of Unitract. It raised allegations that Roger Williamson, whoheld about 24% of the shares in Unitract, was someone about whom very littlewas known or could be found out.

[90] The plaintiff continued to make requests, through 2004, for the transfer ofthe shares.

[91] By January 2005, the plaintiff had discovered that a form of transfer ofshares could easily be downloaded from the Internet. She downloaded one, filledout her own name and address on it, signed it, and posted it to the defendant witha letter saying:

Dear Alan,Here is the form I said I would send down to you for the transfer of my shares. Not sureif you are going to give me the boys their shares as promised or not. I am thinking thatit would be easiest to only go through this process once. But as it really is up to you Iam unsure where I stand on this matter.My account number with Commsec is [account number].I hope you can get to this soon. Also hope your trip to the States was fun. Take care.Love.Louise.

Did the plaintiff say she no longer wanted the shares?

[92] The defendant did not reply in writing to that letter.

[93] He says he telephoned the plaintiff, expressing surprise about her askingfor a transfer of shares. When she reminded him that he had signed a letter forher previously, he says he told her that he had only provided it on the basis thatit would provide some comfort that he would continue to pay the rent and herexpenses for a reasonable period of time, or in case he died. According to him,he said it was never considered to be in any way additional.

[94] He also asserts that the plaintiff then said to him:

My circumstances have changed since I sent the letter and I no longer want anythingfrom you because I am being investigated for social security fraud.

[95] I do not accept any of that evidence of the defendant.

[96] Even after January 2005, the defendant continued to pay certain expensesof the plaintiff. He paid amounts that she debited in the period 21 March–9 April2005, to a Visa Gold Card. He continued to pay fees to Mr Riordan forconsultations the plaintiff had between 26 January and 1 May 2005.

WHITE v SHORTALL (Campbell J)60 ACSR 654 671

5

10

15

20

25

30

35

40

45

50

[97] The plaintiff denies that there was any mention of fraud by Centrelink toher, and denies that she said anything about fraud to the defendant. I accept thosedenials.

[98] She accepts that she “had been queried” by “the Department” (who I taketo be Centrelink), but the only letter she received was one that said “yourParenting Payment Single will stop after 8 February 2005 because you are nowa member of a couple and no longer want to receive this payment fromCentrelink”, and went on to tell her about her appeal rights concerning thatdecision.

[99] Four passages in Mr Riordan’s notes were cross-examined on concerningthis topic of whether the plaintiff told the defendant that she was beinginvestigated by Centrelink for fraud. One of them was his note on 5 February2003 “tax issues? Centrelink issues?”. I have already made findings about thecircumstances of the making of that note at [45]–[46] above.

[100] The second is a note he made on 4 November 2003 “Centrelink notsorted out”. The third is a note made on 15 June 2004 “5 letters from Centrelink”.The fourth is a note made 13 February 2005 “rang Allan — explained beinginvestigated. Don’t want to involve Allan”.

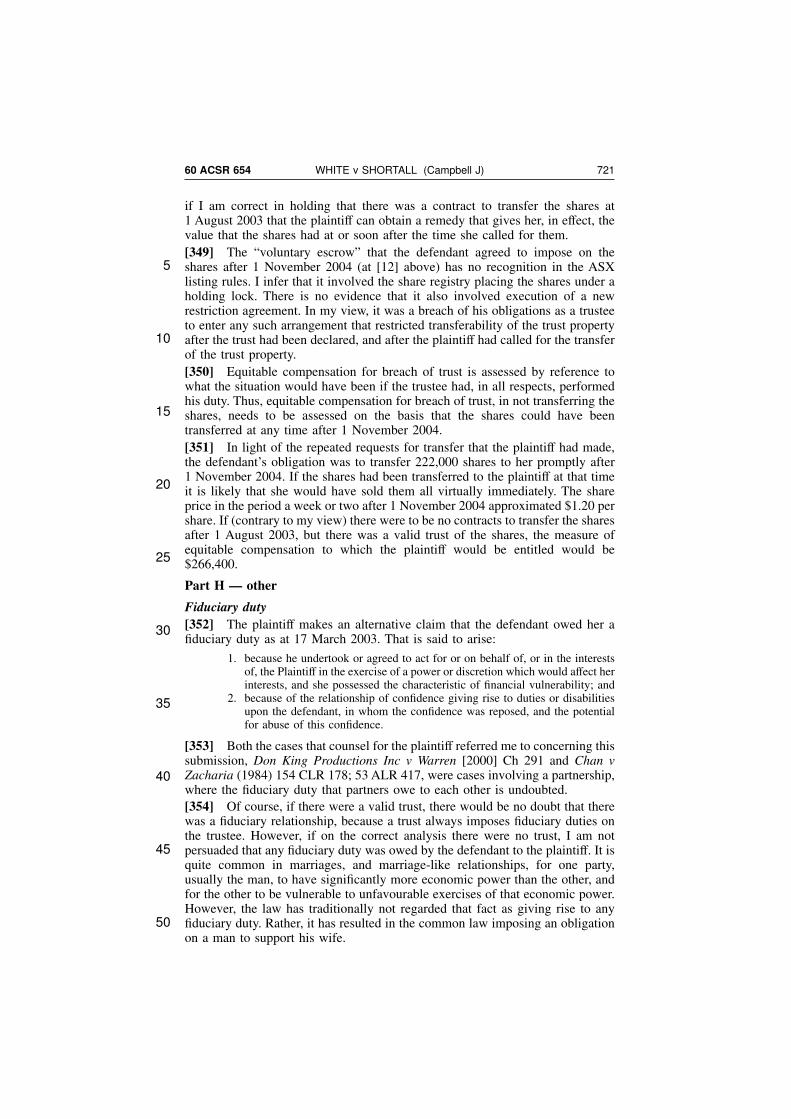

[101] Mr Riordan explains the second and third of these entries by saying:

There was an ongoing issue in counselling with regards to the standing firm andpersistent in order to achieve from the Child Support Agency (CSA) in relation to herex-partner Steve in coming up with the money in, income in terms of support for herchildren.

And;

It reached a head in late 04 with Louise and the Child Support Agency and what —actually, I remember now. It was what Steve was saying he was giving to her, Louise,was far more than what she was actually getting and that affected her Centrelinkpayments. There was some argy bargy with Centrelink which related to her, yeah, thelack of financial support from her partner.

[102] Mr Riordan’s explanation of the note of 13 February 2005 is:

I think that note is saying: I rang Alan. I have explained to him that Centrelink areasking me some difficult questions and Louise is explaining to Alan I don’t want to dragyou into this. That would be a reasonable interpretation.

I accept this evidence of Mr Riordan.

[103] The plaintiff’s evidence, when cross-examined about “5 letters fromCentrelink”, was “it is actually child support agency, not from Centrelink”, thatshe did not write any letters to Centrelink in about January/February 2005, butthat “I went into Centrelink and filled out the appropriate form the day after thegentleman rang me”. I accept that the plaintiff told the defendant, in aroundFebruary 2005, that she had been queried by Centrelink, to which he replied“I can’t transfer them to you now as I don’t want to get mixed up in anyinvestigation”. The plaintiff did not agree that the shares should not betransferred.

A final request for transfer

[104] It is common ground that the plaintiff and the defendant saw each otherin Sydney on the day of Unilife’s annual general meeting, in November 2005.I accept that, after the meeting, the plaintiff telephoned the defendant and askedwhen he would transfer the shares, to which the defendant replied “I will do itfirst thing tomorrow morning”.

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS672 NSWSC

[105] He did not do so.

[106] On 15 November 2005, a solicitor who the plaintiff had engaged wrote tothe defendant saying:

Dear Mr Shortall,

Declaration of Trust — Louise White

I act for Louise White who has sought my advice regarding Unilife shares. These sharesare held in Trust by you, and owned beneficially by her in accordance with theDeclaration of Trust signed by you on 18 March 2003.

Pursuant to the provisions of that Declaration, Ms White now requires that you transfer247,000 shares in Unilife to her. 222,000 of these shares she will hold as beneficialowner, and the remaining 25,000 she will hold as Trustee for Maverick and JacksonWhite.

I look forward to receiving a Standard Transfer Form executed in favour of Ms White.

[107] The defendant did not reply to that letter.

Would the plaintiff have sold the shares?

[108] The plaintiff asserts that if she had received the shares in August 2003 shewould have sold them with the exception of $60,000 worth at that time. She saysthat she would have sold them all after the defendant called her in January 2004,and the Sydney Morning Herald article appeared.

[109] Mr Curtin, counsel for the defendant, submits that I should not acceptthat evidence. First, Mr Curtin reminds me that evidence given by a person, aboutwhat he or should would have done if some event in the past had happeneddifferently, needs to be looked at with caution. In Cackett v Keswick [1902]2 Ch 456, a case about a material omission from a prospectus, Farwell J said(at 463–4):

Now, it cannot be enough for a man to swear that he would not have entered into thecontract if he had known something that was concealed from him. It is easy to be wiseafter the event, and many men can honestly persuade themselves when a company hasfailed that they would have been influenced by a circumstance which in all probabilitywould have made no impression whatever on their mind when considering aninvestment or speculation.

[110] Farwell J is not there saying, however, that such testimony should not beaccepted. Rather, he is saying it is not sufficient in itself. He goes on to say(at 464):

… if the Court sees that the fact omitted is of such a nature that it might reasonablydeter, or tend to deter, the ordinary investor from entering into the contract, this issufficient. It is in great measure an inference of fact to be drawn by the Court or a juryfrom the circumstances of the case … It would no doubt be matter of comment if aplaintiff was not called nowadays to swear that the fact omitted would have deterredhim from contracting; but neither his testimony nor his absence is conclusive.

[111] That decision was upheld by the Court of Appeal (the judgmentscommencing at [1902] 2 Ch 471), on grounds that did not depend upon how theplaintiff’s evidence of how he would have reacted in a hypothetical situationshould be treated.

[112] Mr Curtin also reminds me that in Rosenberg v Percival (2001) 205 CLR434; 178 ALR 577; [2001] HCA 18, a medical negligence case concerning failureto warn of a slight but foreseeable risk, McHugh J said (at [26]):

WHITE v SHORTALL (Campbell J)60 ACSR 654 673

5

10

15

20

25

30

35

40

45

50

[26] … human nature being what it is, most persons who suffer harm as the result of amedical procedure and sue for damages genuinely believe that they would not haveundertaken the procedure, if they had been warned of the risk of that harm.

[113] Mr Curtin also points out that Kirby J, in Rosenberg v Percival at [158]referred to his own remarks in Chappel v Hart (1998) 195 CLR 232; 156 ALR517; [1998] HCA 55. There, in considering whether in a medical negligence casethe court should adopt a “subjective” approach to causation of damage whichlooked at what the particular patient’s response would have been had properinformation been given, or an “objective” approach, which looked at the responseof a reasonable person in the patient’s situation, Kirby J said (at [7]):

[7] … The subjective criterion involves the danger of the “malleability of therecollection” even of an upright witness. Once a disaster has occurred, it would be rare,at least where litigation has commenced, that a patient would not be persuaded, in hisor her own mind, that a failure to warn had significant consequences for undertaking themedical procedure at all (where it was elective) or for postponing it and getting a moreexperienced surgeon (as in this case). Yet, these dangers should not be overstated.Tribunals of fact can be trusted to reject absurd, self-interested assertions.[Footnotes omitted]

McHugh J in Chappel v Hart at [32], footnote 64, made similar remarks.

[114] In Seltsam Pty Ltd v McNeill [2006] NSWCA 158 at [115]–[123]Bryson JA, with whom Handley and Tobias JJA agreed, held that evidence by awitness of what he or she would have done, if some aspect of the past hadoccurred differently to the way it in fact occurred, is admissible, though its weightshould be carefully assessed because (at [121]):

[121] … Observations on the limited value, and self-serving and hindsight nature ofevidence of this kind have considerable force.

[115] One objective circumstance that Mr Curtin points to concerns the way inwhich the plaintiff acted concerning some Unitract shares in a superannuationfund that she and her former husband were involved in. That superannuation fundobtained around 520,000 shares in Unitract when it floated. The plaintiff and herformer husband were the trustees of that fund. The former husband made all thedecisions in relation to that fund, and was the sole signatory on the bankaccounts. The plaintiff did not obtain control of the fund by herself untilSeptember 2005. Unitract shares in the superannuation fund were not sold until16 June 2005 (when 130,000 were sold), 10 August 2006 (when a further 378,000were sold) and 11 August 2006 (when 10,500 were sold).

[116] The plaintiff contacted her former husband in January 2004, after theSydney Morning Herald article, and discussed the movement in the share priceof Unitract. However, she did not suggest, or ask, that he sell the shares inUnitract that the fund held. At that time relations between the plaintiff and herformer husband were difficult, and she was reluctant to say anything to him at all.

[117] As well, the plaintiff explains her reason for not asking her formerhusband to sell the Unitract shares as being that the fund bought the shares as along-term investment.

[118] If the defendant had transferred 222,000 shares to the plaintiff in August2003, it cannot be concluded that the plaintiff would have dealt with those sharesin the same way that the superannuation fund dealt with its shares in Unitract.In the last few months of 2003, the situation that the plaintiff was in was that ofa single mother, with two children to look after. While the defendant had said he

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS674 NSWSC

would pay the whole of the rent for a year, and half of the rent for 2 years, on herpremises, she was close to the end of the time when his full rental subsidy wouldexpire. She and the defendant had previously discussed a possibility that, whenshe got her shares, she would buy a house for herself and the boys. Housing washer single greatest need.

[119] The price of Unitract shares had trended upwards in the first half of 2003.On 3 January 2003, the first day on which the volume of trades exceeded 100,000in the year, the closing price was 65c. From 9 April 2003, the price wasconsistently above $2, and reached its highest point at $2.93 on 18 August 2003.Thereafter, the trend was down until the end of 2003, but not markedly so — thelowest price achieved in that period was $2.06 on 9 October 2003 (a day whenan unusually large number of shares traded) and in December prices were in arange from $2.23 to $2.55. The appearance of the Sydney Morning Herald articlecoincided with the price dropping from $2.17 on 16 January 2004 to $1.87 on19 January 2004. Thereafter, the trend of prices was down until 17 March (whenit reached $1.35), but the price then recovered somewhat, to $2.12 by 4 May2004. After that, the trend has been continually down. The share price had sunkbelow $1 by 26 October 2004, below 70c by 18 March 2005, below 60c by23 June 2005, below 50c by November 2005, and have continued a generaldownward trend until, on 1 November 2006 the price was 22c.

[120] The agreement between Musgrave and Unitract Pty Ltd (at [10] above)provided for the company to have an issued capital of over 66m shares. Theentire on-market trading history of the company since flotation is in evidence,and suggests that even if a sale of 222,000 shares occurred on a single day, thatwould not have a significantly depressing effect on the share price.

[121] If the plaintiff had received 222,000 shares in August 2003, and the shareprice had been rising from its high on 18 August 2003, I think it possible that theplaintiff may have held onto the shares at least for another few months. Her needfor money would be acute when the defendant’s full rent subsidy ceased, inJanuary 2004. However, when the trend of the price was down, and the timewhen the plaintiff’s need for money would become particularly pressing was onlya few months away, it seems to me likely that if she had received the shares on1 August 2003, or promptly after she first asked for them, she would have soldthem by mid-September 2003. There was some volatility in the market pricearound that time. Two dollars and fifty-five cents is a fair estimate of the amountshe would have received for the shares, taking into account that a small amountof brokerage would have been payable.

[122] I see no reason to reject the plaintiff’s admission that she would not havesold $60,000 worth of the shares at that time. No explanation was given inevidence of where that figure came from, but I note that it is approximately equalto the amount of money that she paid to the defendant in the course of therelationship, and up to 17 March 2003, including the loss made on sale of thePeptech shares. Thus, it is approximately equal to what amounts to the purchaseprice of the 222,000 shares that the defendant agreed to hold on trust.

[123] It seems to me that the plaintiff was likely to have sold such Unilifeshares as she kept within a few days of appearance of the Sydney Morning Heraldarticle. The defendant had told her before the article had published that the shareprice would probably be detrimentally affected. He had also told her that the pricewas likely to recover, but in my view it is likely that the plaintiff would not haveseen herself as able to afford the risk that it might not recover. As well, if the

WHITE v SHORTALL (Campbell J)60 ACSR 654 675

5

10

15

20

25

30

35

40

45

50

share price recovered, there were shares in the superannuation fund that had beenbought at the float price, and that would benefit from any such recovery.

[124] In my view, the remaining shares would be likely to have been sold bythe end of January 2004. Given the range of prices over the period from 19 to30 January 2004, a fair estimate of the price that would have been realised is$1.80 per share.

Part B — intention to enter legal relations

[125] The defendant submits that there was no intention to enter legal relationsin the execution of the document dated 17 and 18 March 2003, or in any of theconversations that immediately preceded its execution.

[126] In assessing that submission, one needs to bear in mind that (as Mr Ryanput it in address) there are “two limbs of the plaintiff’s case, the declaration oftrust and the promised transfer of the shares after the 1 August”. Mr Ryan submitsthat “we have this declaration of trust sitting on top of a contract or promise totransfer the shares for consideration”.

[127] When one considers whether there is an intention to enter legal relations,the objective theory of contract formation has the consequence that thoseobjective circumstances from which an observer would reach a conclusion aboutwhether contractual relations were intended or not, play a significant, andpossibly exclusive, role. The reason for putting it that way is that subjectiveintention can be relevant to whether a contract is formed, in the sense that it canstop what would otherwise be a contract from being a contract — as when thereare words which on their face are sufficient to amount to a contract, but bothparties know that the other does not intend to contract, as happens withplayacting. As well in Air Great Lakes Pty Ltd v KS Easter (Holdings) Pty Ltd(1985) 2 NSWLR 309 at 330–1 Mahoney JA says that it is “relevant” that partiesintend to enter a contract, although his Honour gives no guidance as to how orby reference to what principles that relevant information is applied.

[128] So far as the type of intention that is needed to create a trust is concerned,the law is settled, for a judge of first instance in New South Wales, by thedecision of the Court of Appeal in Hyhonie Holdings Pty Ltd v Leroy [2004]NSWCA 72. In that case Hodgson JA (with whom Mason P and Handley JAagreed) accepted, at [43] the following statement made by Bray CJ inRe Lamshed [1970] SASR 224 at 239:

It is clear law that despite the unambiguous words of the declaration the trustapparently created by them can be rebutted by evidence of a contrary intention(Commissioner of Stamp Duties (Qld) v Jolliffe (1920) 28 CLR 178). But the onus is onthose who seek to prove such an intention and strong evidence is required for thepurpose (In Re Steele [1925] SASR 272). Many cases were cited to me where this hadbeen done successfully. In some of these cases the depositor was alive and gaveevidence of his own intention and was believed (Jolliffe’s case; Starr v Starr [1935]SASR 263). In other cases when the depositor was deceased there was evidence ofspecific declarations made by him during his life time (Winter v Grady (1921) SR(NSW) 686 at 691), though sometimes these related to the interest only and the truststood as to the principal (Kauter v Hilton (1953) 90 CLR 86; Re Armstrong (Deceased)[1960] VR 202 at 206). And in some cases the trust was held to be rebutted after thedeath of the depositor by evidence entirely or largely circumstantial (In Re Appleby’sEstate (1930) 25 Tas LR 126; Re McGuire, Deceased (1937) 41 WALR 120; Teasdalev Webb (1940) 57 WN(NSW) 151; Abbot v Miles (unreported, Supreme Court of SouthAustralia, Napier, CJ, 12 May 1952); Jeffrey v Miles (unreported, Supreme Court ofSouth Australia, Mayo J, 10 December 1952).

AUSTRALIAN CORPORATIONS AND SECURITIES REPORTS676 NSWSC