Embed Size (px)

Citation preview

In This Issue

Editor: Cathya Djanogly

People

Our perspective on recent casesProcedure•Cornwallis Care Services Ltd v HMRC [2012] UKFTT 724•Total Technology (Engineering) Limited v HMRC [2011] UKFTT 473

Substance•Mark Young T/A The St Helens v HMRC [2012] UKFTT 702 (TC) •Bonik Food C-285/11•B. W. Male & Sons Limited v HMRC [2012] UKFTT 719•MBG Associates v HMRC [2012] UKFTT 723

Recent Articles•The Autumn Statement: Enforcement and Compliance

by James Bullock•Sector Focus: Infrastructure

Events 21The next edition of PM-Tax will be published on 16th January 2013. Best wishes for the festive season.

News and Views from the Pinsent Masons Tax team

Combining the experience, resources and international reachof McGrigors and Pinsent Masons

PM-TaxIssue 15 Wednesday 19 December 2012

22

18

5

Our Comment•Members of the Tax Department comment on the Autumn

Statement and the Finance Bill for PLC•Jason Collins comments on the Government’s initiative to make

tax avoidance records relevant to the procurement process

2

Pinsent Masons

Members of the Tax Department comment on the Autumn Statement and the Finance Bill for PLC. These

comments were first published on the PLC website on Thursday 13 December.

James Bullock: Enforcement and compliance

The Treasury is set on raising increased revenues from enhanced enforcement and compliance. The Chancellor has confirmed that HMRC would be allocated an additional £77million to target avoidance, evasion and fraud, with the estimated tally being a staggering £22 million a year by the end of this Parliament. The GAAR is likely to be a key Government weapon against aggressive avoidance. However, the focus on “high risk promoters” with a commitment to develop a “package of penalty and information powers” will also play a significant role in the deterrence of aggressive tax planning. In addition, there were two fascinating suggestions buried in the small print of the Autumn Statement.

The first is the commitment to “use HMRC’s resources to accelerate its resolution of avoidance schemes, including long-standing avoidance schemes involving partnership losses”. This could mean that some long running tax enquiries are closed at last according to some form of settlement strategy.

The second is the intention of this Government to consult with the Cabinet Office on the use of the procurement process to deter tax avoidance and evasion. Tax compliance records of private sector bidders could become a relevant factor in the award of government contracts.

John Christian: Property

The proposed changes to the SDLT transfer of rights rules will introduce complexity and uncertainty into commercial transactions. The introduction of a tax avoidance test on top of the heavily rewritten legislation (and the existing SDLT anti- avoidance provisions) is unnecessary. This will be particularly difficult to operate as the test looks not only at the purpose of the party claiming sub-sale relief but also at the purposes of other parties to the arrangements. The sub-sale relief is relied on in many

straightforward commercial transactions, including by house builders and in development joint ventures, and it is important that those that may be affected by the changes review them and provide feedback on the issues that will arise in practice.”“The changes to REITs investing in REITs were previously announced and will allow REITs to diversify their risk and facilitate REIT joint ventures. The conclusion that no changes should be made to accommodate social housing REITs was also announced earlier . It is however surprising that the Government have still not accepted the incompatibility of the REIT regime with residential assets. A social housing REIT was always going to be unlikely because of the yields available but a bigger issue for the sector is the fact that the REIT rules do not work with the residential business model and this is proving an obstacle to the use of REITs in the private rented sector.Eloise Walker: International tax and infrastructure

At 1073 pages of legislation and explanatory notes, this year’s draft Finance Bill is so far looking like a lot of sound and fury indicating not a lot that’s new, and you have to weep for the trees that have died to print the thing. The drop in the mainline corporation tax rate is nice to see, and everyone will be feeling

relief to see it confirmed that the GAAR will not be going live until Royal Assent. There is of course the annual (nay, almost traditional by this point) amendment to the debt cap rules, and an alteration to the new controlled foreign companies rules before they even commence (I’m not sure whether to applaud HMRC for trying to fix quirks in advance or deplore the poor drafting that means they need to). Also to be noted with amusement is HMRC finally bowing to the Court of Justice of the European Union and first permitting the deferral of paying exit taxes when a UK company moves its tax residence to elsewhere in the EU, and second removing some restrictions on when EEA resident companies can surrender losses from their UK branches as group relief in the UK – but given HMRC’s track record in this area, it’ll be a wonder if the new draft legislation turns out to be EU compliant. Here we go again….

For the infrastructure sector, it’s not what is in the Finance Bill but what is missing from it that is a cause for concern - when we heard from the Chancellor that extra funding would be invested in infrastructure, it was exciting to speculate (briefly) that we might be about to see the much lobbied-for infrastructure

> continued on next page

PM-Tax | Issue 15 Wednesday 19 December 2012

2

Our Comment

Members of the Tax Department comment on the Autumn Statement and the Finance Bill for PLCThese comments were first published on the PLC website on Thursday 13 December 2012

Pinsent Masons

tax relief become reality. No such luck - it looks like high effective corporate tax rates for infrastructure projects are with us to stay for the time being. What we don’t yet have enough detail on is the planned review of partnerships, and what the Chancellor intends in using the procurement process to deter tax avoidance. It is to be hoped that the Government is not going to kick an already strained sector when it’s down.”

Ian Hyde: Anti-avoidance provisions

The Autumn statement reflects the current political climate of trying to clamp down on unacceptable tax avoidance. It is striking how the Government has not only devoted more resources to anti avoidance but also in contrast with years gone by, broadened the range of weapons it intends to use. We not only have specific anti avoidance rules on identified problems (for example on stamp duty sub sales) and the General Anti Avoidance Rule but, perhaps most significantly using the leverage of potentially withholding government contracts to persuade companies to behave. The further the Government gets away from direct legislation and into generic solutions

the greater the risks of creating a woollier system of tax administration. A predictable tax system is as much a hallmark of an attractive international destination as a competitive headline tax rate and HMRC have to make sure the new rules pass that test.

Conor Brindley: Corporation tax

Apart from the GAAR, none of the corporation tax related announcements were particularly earth shattering except for the confirmation that an “above the line” R&D credit would be introduced.

Further minor changes were made to the controlled foreign company (CFC) rules to ensure that they “work as intended, and to counter two tax planning opportunities”. Those improvements are welcome, however the fact that the CFC legislation already requires amendments – it has not come into force yet - does not bode well.

Both the exit charge provisions (which apply when a company leaves the UK) and the group relief rules (following the recent CJ-EU ruling in Philips Electronics UK Ltd) will be amended to comply with EU law.

However, the confirmation that the “above the line” tax credit will be introduced is the main good news, particularly for companies operating in the life science and oil and gas sectors. The relief will move “above the line” – i.e. it will be accounted for as a reduction in R&D costs. Its incentive effect will therefore be felt directly by the scientists performing the R&D. It also means that if the credit exceeds the company’s tax liability, it will be paid out in cash..

> continued from previous page

Members of the Tax Department comment on the Autumn Statement and the Finance Bill for PLC (continued)

PM-Tax | Issue 15 Wednesday 19 December 2012

3

Our Comment

Pinsent Masons

One of the announcements buried in the Autumn

Statement was that the Cabinet Office and HMRC will ‘consult on the use of the procurement process to deter tax avoidance and evasion’. To put it in more common parlance, Danny Alexander said at the Liberal Democrats’ Autumn conference that ‘If you want to work for us, you should play by our rules. Taxpayers’ money should not be funding tax dodgers’.

It is not difficult to see why the government has taken this tack. It may not be able to defeat every form of tax avoidance through counteraction, so it hopes to use its purchasing power to change business culture around tax – in the same way it uses that power to try to change, say, diversity in the workplace. But will an effective blacklist actually work in practice?

There are issues which will need to be navigated deftly – for example, how to define ‘tax dodging’. Ever since the Ramsay judgment more than 30 years ago, the courts have grappled with setting the boundaries of legitimate tax avoidance – and it is rarely as easy to define as politicians and policy-makers might hope.

One approach might be to define the measure by reference to arrangements which are reportable under DOTAS. The government might for example give a higher score to a bidder who has not engaged in such arrangements or has wound them up. Given the measure is intended to deter avoidance, the measure may also extend to professional services firms which help their clients to avoid tax – which would be warmly welcomed by team Margaret Hodge. The Public Accounts Committee was reportedly told

recently that 10% of disclosable schemes are still emanating from the big four accounting and magic circle law firms, who also unsurprisingly do a lot of work for government.

This measure will have to comply ultimately with EU law which requires procurement rules to be objective, fair and transparent. Domestic rules already contain provisions dealing with convictions for tax evasion and non-payment of tax where the liability is not disputed. These are clearly delineated concepts – could the same be said for tax avoidance?

Because of these legal problems, the measure may never see the light of day. However, the government may feel that, while there may be legal skirmishes in individual cases, this would not be enough to prevent HMRC from pressing ahead. The measure is an extension of

HMRC’s ‘tax on the boardroom’ agenda initiative – which itself has no legal standing. The policy objective would be achieved even if the mere existence of the measure is enough to put some bidders off having a higher risk tax strategy.

The government procures a very wide range of services – including construction, IT, outsourcing and consultancy services, to name a few. The boards of companies in these sectors will need to take note. If they haven’t been overly concerned thus far with HMRC’s view of their attitude to tax risk, this measure may mean that will soon change. The consultation begins soon and the measure is timetabled to come into effect on 1 April 2013..

PM-Tax | Issue 15 Wednesday 19 December 2012

4

Our Comment

Jason Collins is a Partner in the Litigation and Compliance Group, Head of the Tax group and also Head of client relationships for the Financial Services Sector.

Jason is one of the leading tax practitioners in the UK. He specialises in the resolution of complex disputes with HM Revenue & Customs in all aspects of direct tax and VAT.

Email: [email protected]: +44 (0)207 054 2727

The Government hopes to use purchasing power to change business culture on tax By Jason Collins

First published in the Tax Journal on 18 December 2012

Pinsent Masons

The Autumn Statement put compliance and enforcement right at the forefront of the government’s

tax raising (and deficit reduction) strategy, with significant investment in HMRC providing them with the tools to bring in the cash. There is also an interesting angle for the construction, infrastructure and outsourcing sectors – and for any corporate involved in government procurement.

The ‘glossy’ brochure Closing in on Tax Evasion published on 3 December 2012 could have told us all that we needed to know.

Bluntly, the chancellor now regards the collection of tax unaccounted for through evasion and avoidance as one of (if not the) principal means of raising additional revenue. The fact that HMRC is authorised to spend money on a ‘billboard campaign’ – ‘We’re closing in on undeclared income’ –reinforces the fact that the government now feels sufficiently confident as to boast about significant additional resource for HMRC,

when all other government departments are required to reduce their operational budgets. ‘Spend to save’ – launched back in 1996 by the then chancellor Kenneth Clarke – has finally come of age.

And much of what followed in the Autumn Statement itself centred around investment in greater – and increasingly sophisticated – enforcement techniques. An additional £77m is being allocated to target avoidance, evasion and fraud, with the anticipated amount of tax to be recovered in the last year of this parliament being a staggering £22bn – a 70% increase on the amount recovered in 2010/11. Most significantly this will extend to tackling multinationals in relation to the type of corporate tax planning that has attracted so much recent publicity. One gets the distinct impression that (public and press criticism notwithstanding) the government is very happy with the work HMRC has been doing in this regard.

Apart from an additional power extending bulk information notices to credit card

‘merchant acquirers’, the announcements made in the Autumn Statement in relation to enforcement and compliance were highly practical. The 3 December document even includes a calendar (along the lines of a ‘society events’ diary running right up to May 2013 – and detailing ‘further action’ beyond) of the action HMRC proposes to take. A notable theme is the targeting of ‘affluent’ (note the change of emphasis from ‘high net worth’) taxpayers, now defined as those with a net worth over £1m. Such taxpayers who are non-compliant can expect a very rough ride. Likewise, there is a clear determination to meet the target of a five-fold increase in criminal investigations by 2014/15. A tally of 400 criminal convictions in 2011/12 is trumpeted (including, specifically, the prosecution of a doctor for a £92,000 evasion). But it will be interesting to see whether HMRC starts to target the seriously wealthy for criminal investigations. A pledge to ‘increase the number of criminal investigations into offshore tax evaders’ suggests that they might. A new – and comprehensive – offshore evasion

> continued on next page

PM-Tax | Issue 15 Wednesday 19 December 2012

5

James Bullock is Head of the Litigation and Compliance Group.

He is one of the UK’s leading tax practitioners and has been recognised as such in the leading legal directories for many years. James has over nineteen years of experience advising in relation to large and complex disputes with HMRC for large corporates and high net worth individuals, including in particular leading negotiations and handling tax litigation at all levels from the Tax Tribunal to the Supreme Court and European Court of Justice.

Email: [email protected]: +44 (0)207 054 2726

The Autumn Statement: Enforcement and ComplianceBy James Bullock

First published in the Tax Journal on 7 December 2012

Recent Articles

Pinsent Masons

strategy – will be published in Spring 2013. This ties in neatly with the implementation of the UK/Swiss agreement – and the anticipated flight of ‘dirty’ money from Switzerland at the start of 2013.

There are two very significant announcements buried in the ‘small print’ of the Autumn Statement itself. The first is a commitment to ‘use HMRC’s resources to accelerate its resolution of avoidance schemes, including long-standing avoidance schemes involving partnership losses.’ This follows from the announcement in the press release introducing Closing in on tax evasion which states that the additional £77m of resource will fund (amongst other things) a ‘settlement opportunity’ that offers ‘a good deal to the Exchequer.’ This is something I and others have been calling for over a period of some time. Hopefully this at last means that additional resource will be allocated to ensure that avoidance schemes (some of which can trace their implementation back to the very early 2000s) still under enquiry may finally be brought to closure. HMRC must now decide which schemes it wishes to pursue through the Tribunal – and must then do so with expediency. The introduction of the GAAR (for which we now have confirmation that the draft legislation will be published later this month) will present an excellent

opportunity to ‘clean up’ the past whilst at the same time drawing a line under it.

The second significant announcement is the news that HMRC will immediately consult with the Cabinet Office ‘on the use of the procurement process to deter tax avoidance and evasion and the proposed definitions of key concepts’. Following this consultation, ‘new arrangements’ will come into effect from April 2013 and the assumption must be that the tax compliance record of private sector bidders will become a relevant factor in relation to the award of government contracts. Corporates wishing to bid for such contracts need urgently to be looking at their tax affairs – and potentially those of their senior management as well. This is a fascinating and innovative development aimed at ‘changing behaviours’ in the way that has previously been applied to issues such as diversity, the Bribery Act and CSR policies. It will affect (amongst others) construction companies looking to tender for major infrastructure projects (such as the proposed Northern Line extension and HS2) as well as those looking to secure IT procurement projects with public bodies and a host of other public-private contracts..

> continued from previous page

The Autumn Statement: Enforcement and Compliance (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

6

Pinsent Masons

Workforce issues: to employ or not to employ?

Eloise WalkerCorporate tax partner and tax lead for Infrastructure, Pinsent Masons

Whether it is issues with service providers and IR35, problems with the 24 month temporary workplace rule, or the over-burdensome nature of the construction industry scheme, the infrastructure sector has many obstacles to overcome with its workforce provision. Given

the difficulties that infrastructure companies face, it’s a wonder that anything ever gets built.

Where the government seem keen to actively support other sectors (especially those which are easily mobile and can therefore leave the UK without too much hassle), the infrastructure sector seems to be continually drawing the short straw, which is odd when you consider that the sector funds, constructs and maintains some of the most important functions of British society – our roads, railways, power stations, water treatment works and hospitals, to name but a few.

A significant area of difficulty for the Infrastructure sector is its workforce, and here companies find themselves between the devil and the deep blue sea – use third party service providers, or employ one’s own.

Third partiesThe trouble with using third parties is that one has to be very careful of their status to make sure they aren’t treated as employees by HMRC. Sub-contractors and other service providers come in a variety of favours, but those of most concern are those acting as sole traders or through noncorporate bodies. Such contractors are often treated as third parties, so payments are made gross of NICs and PAYE, but this triggers two problem areas:

• Are they really employees on the payroll, so is there a risk that PAYE and NICs should be (and have been) accounted for?

• If they are contractors within the construction industry scheme (CIS) regime, the compliance horrors of CIS come into play.

The smaller the sub-contractor is, the trickier the employment question becomes. Trickiest of all are those service providers who are not treated as employees but are providing services outside of CIS, so they are (in theory) just self-employed third party suppliers. There can be very little to distinguish such workers from employees, and whilst procedures and controls can be put in place around contract, control, provision of equipment, substitution and payment to reduce the risk, a significant PAYE and NICs exposure remains.

Ironically, although IR35 is generally viewed with disfavour, infrastructure companies using individual sub-contractors who act through personal service companies may (at present) be better off, because if employment is an issue the PAYE and NICs problems lie with the service company more than the infrastructure ‘employer’. But don’t expect this to last – HMRC and HM Treasury have been consulting on ‘false

> continued on next page

This report, prepared by Pinsent Masons LLP, discusses some of the key challenges facing the infrastructure sector in the current economic and political landscape. In particular, it examines:

• practical problems with using sub-contractors, CIS anomalies and the 24 month temporary workplace rule;

• quirks and pitfalls in the capital allowances regime around short life/long life assets and integral features;

• the use of partnership vehicles to fund local infrastructure;• investors’ needs in the PFI secondary market;• international issues in EPC contracts;• the loss of IBAs and its effects on the sector; and• particular tensions caused by the general anti-abuse rule.

PM-Tax | Issue 15 Wednesday 19 December 2012

7

Sector Focus: InfrastructureThis report was first published in the Tax Journal on 30th November 2012.

Recent Articles

Pinsent Masons

self-employment’, particularly in the construction industry, for some time, and punitive changes to the IR35 regime aimed directly at the infrastructure sector may be on the horizon once the economy improves.

CIS issuesEven if one gets comfortable on the employment question, one still has to deal with CIS, a regime so cumbersome and outmoded it should have been scrapped long since. One could write an entire article on the problems with CIS, but it is just worth mentioning the onerous compliance requirements, the ridiculously low threshold for loss of gross status (where a single late return or short payment delay can have serious consequences), and the economic insanity of sanctions where a company making small net profits can be fined a big proportion of its turnover for non-compliance (often resulting in bankruptcy). The level playing field

it purports to engender has long since shifted from where it originally stood so it misses the point – the game is no longer really about ‘preventing evasion of tax by subcontractors working in the industry and who are unknown to HMRC’ (per HMRC’s Construction Industry Scheme Manual CISR11020) but about those infrastructure companies who evade their PAYE responsibilities by treating employees as self-employed subcontractors and those who accept their obligations: that’s not a game unique to infrastructure, so why discriminate against one sector? Even where exemptions exist to ease the burden they may not be as helpful as they first seem. Take the ‘PFI exemption’ (the Income Tax (Construction Industry Scheme) Regulations, SI 2005/2045, reg 23), for example, which provides that payments by a public sector body are outside the scope of the CIS scheme where they are made under a ‘private finance transaction’. Sounds helpful, doesn’t it? The problem is, it creates anomalies, where certain contracts between any given infrastructure contractor and any given public body may be subject to CIS or not depending on whether the contract provides for payment by instalments or something else (e.g. by reference to work

performed over a specific period). It allows payment by the public body free of CIS compliance headaches, but does not help the administrative burden on the PFI special purpose vehicle through which the payments flow to related party sub-contractors; especially when, almost always, those sub-contractors will be large entities with gross payment status which the SPV will have to monitor for up to 30 years.

Those infrastructure companies who have abandoned using individual service providers and have taken in such contractors as employees are in many respects no better off. They may have certainty of PAYE and NICs treatment, but moving employees around building sites has its own problems.

The 24 month ruleOne particularly annoying fault in the current law is the 24 month temporary workplace rule. As a general rule, it sounds fair enough that there is no deduction available for the cost of travel to an employee’s permanent workplace, whilst the cost of travel to a temporary workplace is deductible. And one has to set some limits on what counts as ‘temporary’ if an employee is going to be continuously attending

a workplace for a particular task. It probably made sense to HMRC to make it a permanent workplace (and deny the deduction) where the employee attends that workplace for a period that lasts, or is likely to last, more than 24 months, because for most sectors a ‘temporary’ workplace for that long does not look very temporary. The problem is, this simply does not work for the infrastructure sector, where project sites are obviously temporary but commonly last more than 24 months – just look at the Olympic park project, or Crossrail, for two recent examples. In this sector the 24 month rule has a damaging effect on labour mobility, and HMRC failed to fix this problem when it recently looked at the regime. It is to be hoped that, given the government’s rhetoric in support of British business, it will revisit this issue again and eventually amend the rules to make them work better for a sector on which so many important areas of British business depend.

> continued from previous page

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

8

Infrastructure companies using individual sub-contractors who act through personal service companies may (at present) be better off ... But don’t expect this to last

Pinsent Masons

An in-house view: Infrastructure and tax competitiveness

Robert FortTax director, Amey and UK head of tax, Ferrovial

A competitive tax regime for all – as long as you don’t want to build anything?

We have heard a lot about UK tax competitiveness since the coalition government first launched its ambition to ‘create the most competitive tax regime in the G20, whilst protecting manufacturing industry’. There are many questions about how this policy objective relates to infrastructure.

As articulated in the Corporate Tax Road Map, the structural components of the programme focus on improvements to the CFC regime and taxation of intellectual property. Both these are entirely laudable and overdue improvements to the UK tax system, but are targeted at mobile industries where the threat of UK plc emigration was highest.

What do these reforms do for the infrastructure sector and how do we

stand in terms of competitiveness? Here the picture is far from rosy. Yes, we have a generous tax regime for interest costs, and infrastructure projects do tend to be highly leveraged, but the fundamental structural weakness of the UK tax system is the absence of relief for the cost or even the amortisation of ‘structures’. The immediate impact of this is seen in the Oxford University Centre for Business Taxation CBT Corporate Tax Ranking 2012 which ranks the UK low in terms of international tax competitiveness. On the key measure of effective marginal tax rate, the UK is ranked 15 out of 19 in the G20 and 31 out of 33 in the OECD in 2012 – and the biggest single reason for this is ‘the low allowances available in the UK for capital investment, particularly in industrial buildings’. The message is clear.

Historically, the UK tax system provides that depreciation is not an allowable cost, being replaced by a patchwork of ‘capital allowances’ which are in essence a codified means of giving tax relief for depreciation. Only with such an alternative measure of relief for depreciation (a genuine business expense) do we have a tax system that taxes commercial profits. Until Gordon Brown’s infamous 2007 Budget, this patchwork included industrial buildings

allowances (IBAs), disparaged in the 2007 Budget statement as ‘poorly targeted’ and ‘worth [only] £230m’. This ‘poor targeting’ was amplified in the 2008 HMRC Budget Note 06 as encompassing ‘structures like tunnels, bridges … highway concessions …’ Since abolition of IBAs, the UK is unique in the EU and the G20 in not giving tax relief for the depreciation of such assets, not to mention the structural (non- ‘plant’) components of (inter alia):

• waste treatment plants;• power stations;• railways; and• airport terminals/runways.

These are all key components of the National Infrastructure Plan 2011 (HM Treasury, dated November 2011), which sets out ambitious targets for spending on critical areas of national infrastructure – without once mentioning the role that tax plays in investment decisions. It is instructive to refer back to Helen Jones’ commentary in this journal (‘Sector focus: pharmaceutical companies’, Tax Journal, dated 26 October 2012) to read that: ‘When a government wants to create an attractive environment for investment, therefore, it makes sense that a competitive tax regime is a priority. There is now an acknowledgment that

tax is a commercial factor influencing investment decisions – and more often than not an important one.’ But not, apparently, for infrastructure.

The removal of IBAsWhat does the removal of IBAs mean for the infrastructure sector? Crucially, as the Oxford University reports demonstrate, the denial of tax relief for a fundamental business expense outweighs any benefit from the reduction in headline rates. Effective tax rates on infrastructure projects are significantly higher than the statutory rate. For example, recent successful bids for projects to build and operate waste treatment plants have been at tax rates some 5–7% points above the statutory rate, whereas it appears to be accepted in the market that use of CFCs for intangible assets can result in effective tax rates as low as one quarter of the statutory rate. From this point of view, the infrastructure sector is paying for the remarkably low rates that more mobile industries can secure through CFC and IP planning and it is clearly seen that the priorities of UK tax policy favour those other sectors at the expense of rebuilding the national infrastructure. Additional consequences, all equally damaging to

> continued from previous page

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

9

Pinsent Masons

the UK’s competitiveness and to the UK’s ability to attract resource to invest in infrastructure, include:

• the cost of UK projects is increased;• funding requirements are increased;• procurement options are reduced;• the procurement market is distorted

by tax assumptions; and

• services become more expensive to the customer.

In the context of attracting private sector investment into infrastructure, the tax situation is particularly unfortunate. Leaving aside the pricing impact of no or uncertain tax relief, the lack of tax relief means that many projects are affordable only if the asset sits on the public sector balance sheet, which inherently limits the risk and control that can be passed to the private sector. Certain projects which historically sat in the private sector with the benefit of IBAs, such as the earlyroad PFI projects or the channel tunnel, could no longer be procured in the same way.

Where we are competing for scarce capital on the international market, infrastructure projects in countries which deliver the same post-tax returns

at lower post-tax cost of investment will always appear more attractive – unless the UK guarantees much higher prices. And so the UK consumer ends up paying more for transport, waste and energy because the pricing has to compensate for the lack of tax relief.

What can be done?Amongst a number of options, the simplest solution is perhaps that the UK should immediately reintroduce IBAs, or an equivalent form of ‘infrastructure allowances’. This could simultaneously provide a significant boost to the UK’s objective tax competitiveness rating and eliminate some of the costs and distortions in the UK’s infrastructure procurement process. Politically, one might think that reversal of a short-sighted and damaging ‘New Labour’ own goal would appeal to the coalition – but HM Treasury argue that it is now caught between the proverbial rock and hard place, in that:

• a tax measure directed at the infrastructure sector could be construed as illegal State aid; whereas

• a general allowance for commercial buildings, sufficiently wide to avoid the State aid risk, is simply unaffordable.

Recent government announcements of targeted tax arrangements for the video game, animation and TV sectors, and the proposed targeted tax regime for shale gas, suggest that State aid is a manageable risk. The funding arguments are more complex but, even if we dismiss as fanciful the £230m figure used to justify abolition of IBAs, it remains perfectly possible to justify infrastructure capital allowances by reference to the economic benefits that will accrue from a completed asset long before the tax cost of an allowance is felt.

The continuing failure to address these concerns leaves those of us in the infrastructure sector to wonder whether the government is as committed to tax competitiveness and infrastructure development as they would have us believe.

Capital allowances: points to watch

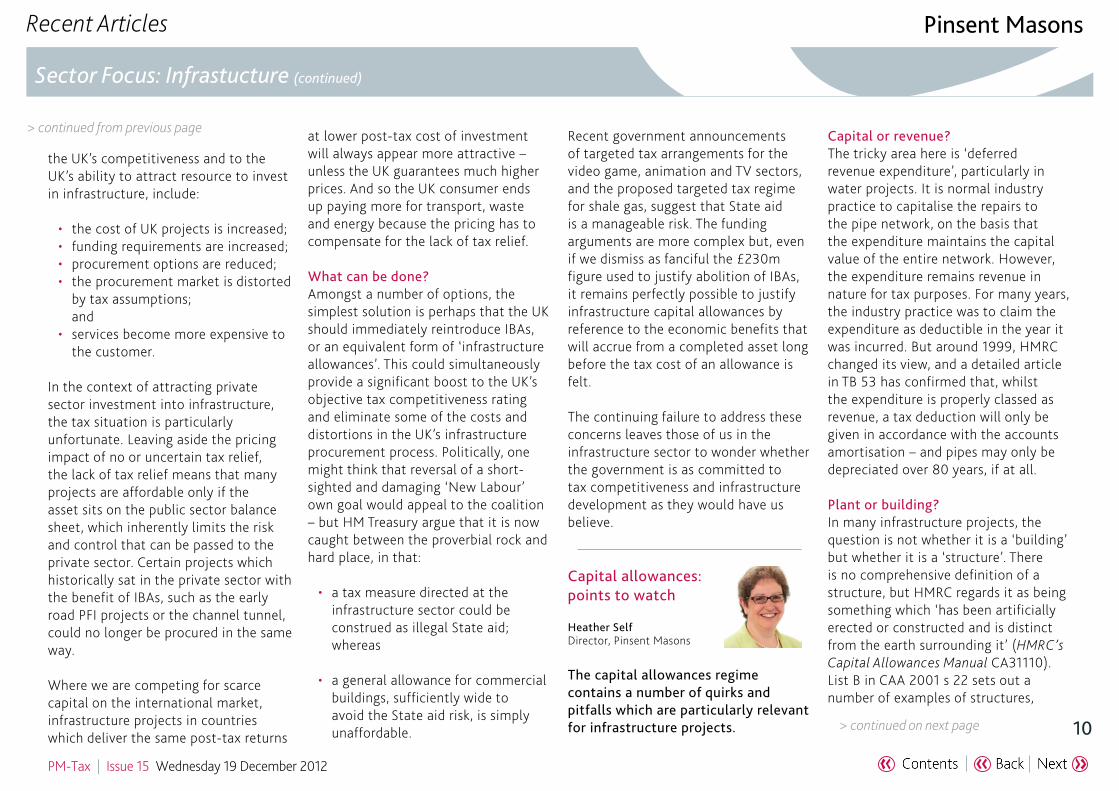

Heather SelfDirector, Pinsent Masons

The capital allowances regime contains a number of quirks and pitfalls which are particularly relevant for infrastructure projects.

Capital or revenue?The tricky area here is ‘deferred revenue expenditure’, particularly in water projects. It is normal industry practice to capitalise the repairs to the pipe network, on the basis that the expenditure maintains the capital value of the entire network. However, the expenditure remains revenue in nature for tax purposes. For many years, the industry practice was to claim the expenditure as deductible in the year it was incurred. But around 1999, HMRC changed its view, and a detailed article in TB 53 has confirmed that, whilst the expenditure is properly classed as revenue, a tax deduction will only be given in accordance with the accounts amortisation – and pipes may only be depreciated over 80 years, if at all.

Plant or building?In many infrastructure projects, the question is not whether it is a ‘building’ but whether it is a ‘structure’. There is no comprehensive definition of a structure, but HMRC regards it as being something which ‘has been artificially erected or constructed and is distinct from the earth surrounding it’ (HMRC’s Capital Allowances Manual CA31110). List B in CAA 2001 s 22 sets out a number of examples of structures,

> continued from previous page

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

10

Pinsent Masons

including tunnels, railways, reservoirs and docks.

In the early days of onshore windfarms, HMRC was wont to argue that a wind turbine was a ‘structure’. After some debate, they accepted that only the concrete base is the structure, and the turbine itself is plant. When it came to offshore wind, Ofgem were keen to ensure that bids in the OFTO licensing process were prepared on a comparable basis, and so liaised with HMRC to agree a template with estimated percentages for structures, long life and short life plant.

Developing a good relationship with HMRC, and explaining the commercial detail of the project at an early stage, is crucial in enabling bids to be prepared on a robust and realistic basis

In any infrastructure project, the key will be to identify as much plant (preferably non-long life) content as possible. Developing a good relationship with HMRC, and explaining the commercial detail of the project at an early stage, is crucial in enabling bids to be prepared on a robust and realistic basis.

Integral featuresWith the abolition of IBAs came the introduction of ‘integral features’. The policy aim was ‘to re-draw the boundary between buildings, including their main features, and other equipment’ and to ensure that items which are ‘normally integral to a modern building’ would attract the same rate of writing down allowances (WDAs) as long life plant.

The problem for infrastructure projects is that certain items which were previously on list C in CAA2001 s 23, and so could qualify for main pool WDAs, are now specified as integral features and hence get the equivalent of long life allowances. Key examples are lifts, escalators and moving walkways, and water cooling systems in a power station. Whilst many such assets will be long-life assets in any case, it seems unfair that any such assets which have a shorter life can only qualify at the reduced rate.

Long-life assets?The obvious assumption is that most infrastructure projects will be long-life assets – since most projects are expected to have a life of more than 25 years. This is true, but sometimes there can be arguments that a particular

technology will not last for more than 25 years. Remember it is the economic life, not the physical life, which is important: an asset is a long-life asset if it is ‘reasonable to assume’ that it will have a useful economic life of at least 25 years when it is new.

Where technology is developing and maturing, the question of when it is reasonable to expect it will last more than 25 years becomes an interesting debate. For example, some of the early wind farms are more than 25 years old, but the turbines are fundamentally different from those being installed now – and it is still generally accepted by HMRC that they are not long-life assets.

In the case of power stations, most will have an economic life of more than 25 years (although not necessarily, particularly given the very rapid changes in the energy supply market expected over the next 20 years or so). Note that an upgrade to an existing station may well not be a long-life asset, unless the expected life of the station after the upgrade is still in excess of 25 years. It is necessary to look at the ‘entirety’ of the asset in assessing the life of a component.

EntiretyThis is a concept which was originally directed at the question of whether expenditure is a repair (revenue) or improvement (capital), but is also very relevant in considering the rate of allowances given to expenditure on a major project. If the whole project is a single ‘entirety’, and has an expected economic life of more than 25 years, then long life asset treatment will apply to the whole asset, even if major components have a shorter life.

For example, in a sewage treatment plant, the two key elements are the concrete housing and the machinery which processes the sewage. If the machinery has a life of (say) 20 years, then the rate of capital allowances will depend on whether the housing is regarded as a structure or as long-life plant – if the former, there will be no allowances on the housing, but main pool rates on the machinery; if the latter, the ‘entirety’ will qualify for long life allowances, with replacement of the machinery being regarded as a repair. Which takes us back to the beginning, and the example of water pipes.

> continued from previous page

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

11

Pinsent Masons

Funding local infrastructure

John ChristianTax partner, Head of transaction and advisory tax, Pinsent Masons

Partnering structures to fund local infrastructure will become increasingly common as a result of the government drive to bring institutional funding into infrastructure investment. Partnership vehicles are the usual option for these projects but current tax rules, particularly on SDLT, do not fit well with the commercial requirements of such projects.

A developing trend over recent years has been the growth of partnering arrangements between the public and private sector to develop local infrastructure. A number of trends have converged, including the use of surplus public sector land to fund projects to deliver local initiatives and the urgent need to improve the nation’s housing stock.

In times of austerity, the accessing of pension and other institutional investment funds to develop

infrastructure is seen as key and a number of government initiatives are looking to achieve this. The Montague report on institutional investment in private rented housing is a recent example.

A general feature of public/private structures is that they will involve a number of financial stakeholders – typically, a local authority providing land, funders (either specialist funders or institutional investors), a housing association where social housing is involved, and possibly a developer or contractor. A recent trend in housing infrastructure has been the emergence of ‘build to let’ structures (identified in the Montague report) where contractors and funders will partner to develop rented housing, often with public sector property.

Although PFI has a reasonably settled template and framework of HMRC guidance (and, in the case of SDLT, some legislation: FA 2003 Sch 4 para 17), there are no specific tax rules

applying to public/private structures and general principles need to be applied when looking at these.

Direct taxFrom a tax perspective, the structure needs to accommodate the different tax positions of the stakeholders. Local authorities are exempt from corporation tax, as are pension fund investors, so the structure is generally based on a partnership so as to be tax transparent. This is seen as particularly important for attracting institutional investment.

Limited partnerships formed under the Limited Partnership Act 1907 are generally used as Limited liability partnerships which are property investment partnerships are, in effect, not transparent for tax exempt pension fund investors (FA 2004 s 186(2) and TCGA 1992 s 271(12)).

The direct tax issues are similar to those arising on any partnership based investment structure and will not be reviewed in detail in this piece.

A particular issue in relation to structures involving housing is that all or part of the activity may be development or trading, rather than investment. The funding model may

rely on the sale of units which will be treated as trading. Shared ownership structures where ownership can be acquired over a period, can also involve trading activity.

Trading activity will be an issue for institutional investors as exempt funds will be taxable on trading profits, although the issue can usually be addressed by suitable feeder structures for exempt investors (as acknowledged in the recent consultation and response on unauthorised unit trusts).

SDLTA key point which is emerging on these structures is in relation to the SDLT treatment. The structures are generally property based as the public sector will contribute property as its financial contribution to the project. Property is generally brought into the structure without a direct tax charge (because the property is usually contributed by a local authority which is exempt from tax on any gain arising) but SDLT can be a significant cost on formation and subsequent refinancing of the vehicle.

The issues arise from the application of the SDLT partnership rules in FA 2003 Sch 15. As mentioned, a partnership

> continued from previous page

An approach by government to mitigate the SDLT [on these asset-backed models] would be welcome

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

12

Pinsent Masons

structure is the market standard approach because of familiarity and the tax position of local authorities and exempt investor participants.

The application of the Sch 15 regime to the initial contribution of the land by the local authority to the vehicle can result in a SDLT saving. Applying the provisions of para 10, SDLT is assessed on the market value which moves to the non-contributing partners. Effectively, no SDLT is payable on the value referable to the local authority’s interest in the vehicle.

However, the partnership regime can give rise to unintended SDLT charges on future events in relation to the vehicle. The clawback provisions of para 17A for example can be triggered by the contributing partner receiving funds, including loan repayments, from the vehicle within three years of the contribution unless it is a payment of income profit. This causes particular issues where the land contribution is in stages.

Bringing in further funding can cause issues under the complex provisions of para 14 which identifies that new cash invested in a property

investment partnership can be treated as a land transaction if it is part of an arrangement involving withdrawal of money from the vehicle.

On an exit, an investor which disposes of an interest in the vehicle will be treated as entering into a land transaction and SDLT will be payable on the transaction.

The impact of the clawback provisions and the para 14 provisions can be mitigated by an election made under para 12 at the time of the contribution so that SDLT is charged in full on the contribution without the ‘relief ’ under para 10 applying. As this increases the formation cost, it is not a practical solution.

As vehicles established a number of years ago are reaching the end of their lifecycle, a number of structures are being exited or refinanced.

The partnership SDLT regime is in some cases proving an obstacle to the commercial aims of the parties, particularly where there may be little commercial value to be realised but SDLT is triggered by reference to market value of the assets on a break up of the structure.

ConclusionThese asset-backed models will be an important feature of local infrastructure, particularly in relation to housing. An approach by government to mitigate the SDLT costs on formation and operation of these structures would be welcome.

Tax risk management issues for international EPC contracting

David MurphyRegional head of tax Europe, Africa, Middle East at Bechtel

Large infrastructure projects not only present huge logistical challenges but also give rise to a number of tax compliance challenges. As jurisdictions increasingly demand more sophisticated tax compliance regimes, EPC organisations need to provide strong support for their tax function if they are to maintain a strong compliance record.

My fellow contributors to this infrastructure feature are commenting in some detail on UK technical issues. In this section I will review some

international issues experienced by engineering, procurement and construction (EPC) organisations.

What EPC organisations do is generally very big and very clever and I have great respect for colleagues who execute projects often in difficult and sometimes dangerous environments which present logistical, safety, security and other challenges which many other businesses do not face.

EPC projects include airports, seaports, motorways, bridges, onshore and offshore oil and gas installations and pipelines and associated petrochemical plant, aluminium smelters, mining infrastructure and processing facilities, hydroelectric installations, fossil and nuclear power plant and even entire industrial cities.

Such large infrastructure projects tend to attract attention because they are sensitive for environmental/sustainability reasons or because they are controversial for other reasons, usually political/financial. Projects and the contractors responsible for building them also attract attention because large international contractors are perceived to have deep pockets,

> continued from previous page

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

13

Pinsent Masons

especially in times of economic difficulty.

Aside from matters of environmental etc concerns mentioned above, being a good corporate citizen in relation to tax matters and managing tax and related reputational risk has become very important. Some of the many practical issues we have to manage are considered below.

An international EPC organisation tends to have a distributed execution model for complex projects. This means that projects involve personnel from many different locations travelling to other locations, for example:

• locations where detailed engineering is being performed prior to and during mobilisation to the project site;

• fabrication and supplier locations to oversee construction of equipment to budget and schedule which is to be installed at the project site; and

• the project site itself.

This model gives rise to a number of tax compliance challenges.

Transfer pricingCross-border activity gives rise to transfer pricing concerns, One of which is the ability to find meaningful comparables for benchmarking purposes. The distributed execution model means a single entity does not perform all parts of the work scope (design, detailed engineering, procurement, construction, construction management/project management) and contracts may not neatly price separately for individual components. Thrid party comparables are therefore unlikely to be meaningful because it is not possible to tell from a given entity’s results (a) what scope(s) of work it performs and (b) the balance of work as between different sectors (oil & gas, civil infrastructure, power, mining and metals etc.) since returns in the different sectors do vary.

Tax treaty protection for offshore business profits

In the distributed execution model, segregation of on- and offshore revenues is important to prevent double taxation and the resultant administration can be complex even in a jurisdiction with remedies such as competent authority procedures. We can gain some comfort from OECD

Model Convention article 7. However, there are countries which have signed up to OECD-type treaties for foreign investment purposes but some have said signing a treaty does not mean they have signed up to all the OECD principles as per the Commentary to the Model Convention (the Middle East comes to mind here). Where possible, an EPC contractor will seek scope segregation between on- and offshore work by having split contracts preferably or, if a single contract is required by the customer, by clear statements as to what constitutes the on- and offshore scope with separate pricing for those scopes of work.

Tax auditsAn international EPC organisation will often go to a country to execute a project for a few years, then move on once it is completed and tax audits may not take place until near the end of the project or after the project has packed up and left. This presents challenges in terms of tracking both documentation and people to assist after the event and requires that the tax function has strong support from senior management to enable it to manage tax audits effectively in such circumstances. Clear audit trails and a robust document management and retention policy are

required to manage audits in these circumstances. Regular contact with the project, local advisers and a good relationship with the tax authority are also de rigeur to avoid problems later.

Global mobilityPersonnel will travel either as expats or business travellers: the former can give rise to issues as to how some tax authorities perceive remuneration policies designed to protect employees from additional foreign taxes which may arise while on assignment in a higher tax host country. Local law in certain countries does not allow an employer to pay tax on behalf of employees (for example under an equalisation policy) and this can result in disallowed deductions for personnel costs; the latter can become accidental expats and subject to tax if they accumulate more than a relatively modest number of days in a country and may also create service permanent establishments (PEs) if there are enough of them in and out of a country, e.g. where experts are required to assist projects, travel to a number of different countries but are not assigned as an expat to any of them because of the difficulty corporately and individually of managing what would be multiple assignments. The principal

> continued from previous page

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

14

Pinsent Masons

issue is one of tracking and this is not particular to the EPC sector but applies across many other sectors. One common way of tracking is to require location markers in timesheets because EPC companies use timesheets to record project hours; another method is to require locations to be given via drop down menus in expense reports – the sanction being that expenses are not paid unless location data is stated. Reports can be generated on a regular basis to monitor business traveller activity and remedial action taken where necessary.

Where does this leave us?As mentioned above, dealing with these issues so as not to make mistakes in order to maintain a strong compliance record is not getting any easier as each jurisdiction’s tax compliance requirements are becoming more sophisticated and more developed countries lend support to less developed countries to improve administration and collection, either bilaterally or under the auspices of supranational organisations such as the EU, OECD or UN. These issues require coordinated resources in terms of back office support, promoting awareness of tax requirements across EPC organisations

and finding innovative ways of tracking people and managing data to assist their tax functions with management of the relevant tax and associated reputational risks.

Funding infrastructure: the secondary market

Alison WalkerSenior associate, Pinsent Masons

The secondary market offers significant opportunities for investors to finance lower-risk brown field or operational projects (which have progressed beyond the construction phase). From a tax perspective, a key to attracting investors into the secondary market is simplicity and predictability in tax treatment.

The government has made investment in infrastructure one of its priorities for achieving long-term growth in the UK economy. The challenge lies in funding this investment without increasing public sector debt against a backdrop of changes in banking regulation and commercial banks’ desire to conserve capital, which make investment in infrastructure less attractive to the

traditional funder of these projects, commercial banks.

With these constraints on traditional sources of finance, other investors need to step in and meet the shortfall. There is a significant potential pool of finance in the hands of private investors, listed companies, pension funds (including the proposed pension infrastructure platform, through which pension funds would pool resources to invest in infrastructure), sovereign wealth funds and other institutional investors.

Infrastructure is an ideal investment for such investors offering protection against inflation and long-term predictable income for matching long-term liabilities. However, to date infrastructure has been an unattractive investment option: often due to a dislike of leverage and the high risk profile associated with the delivery and operation of infrastructure, particularly construction or ‘green field’ risks.

DebtFrom a tax perspective, debt funding is attractive as relief is available for arm’s length interest payments made by the project vehicle. Whilst tax-paying investors pay tax on interest accruals, tax exempt investors (such as pension funds) do not. Interest payments may be subject to withholding tax, depending on the identity of the recipient.

As project vehicle receipts are based on post-tax returns, the lower levels of tax generally mean better returns for investors without charging unaffordable prices.

Listed debt instruments offer investors liquidity. From a tax perspective, no stamp duty will usually be payable on an acquisition of debt. Further, no tax should be payable on a future disposal of listed debt provided it has not been treated as impaired by the investor for accounting purposes.

EquityInvestment in equity provides investors with greater transparency on their investment and a more direct exposure to the underlying profits of the project vehicle.

> continued from previous page

The lack of tax relief and credit for underlying tax paid by the project vehicle means high effective tax rates, which can often deter pension funds and other tax exempt investors

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

15

Pinsent Masons

In contrast to debt financing, the availability of tax relief (in the form of capital allowances) on equity-financed infrastructure projects varies significantly from project to project. As project vehicle receipts are based on post-tax returns, the lack of significant tax relief means higher profits must be generated on projects with a low level of capital allowances, such as waste treatment plants, and water and energy projects, to produce comparable returns to infrastructure projects where a higher level of capital allowances are available, or projects which are highly leveraged. The CBI has proposed the introduction of ‘infrastructure allowances’ to counteract this distortion (see Robert Fort’s commentary, above, on this point).

Dividends are not deductible for tax purposes but UK tax resident corporate shareholders should not be subject to corporation tax on dividends provided the dividends fall within an exempt class and certain other conditions are met. It is expected that dividends would usually be exempt.

The lack of tax relief and credit for underlying tax paid by the project vehicle means high effective tax rates, which can often deter pension funds

and other tax exempt investors. A possible compromise position for tax exempt investors, which would not require a change of law, may be for the project vehicle to assign its profits/income stream for a lump sum, which the project vehicle can use to repay existing debt. This should give the tax exempt investor direct exposure to the underlying profits of the project vehicle with a more tax efficient result. The project vehicle will be taxed on the lump sum as income, applying tax anti-avoidance rules, but should only be taxed on its net return going forward provided the arrangements are structured correctly.

Equity will also offer investors liquidity. From a tax perspective, stamp duty will be payable at 0.5% on an acquisition of shares. The substantial shareholding exemption should exempt any gain on a future disposal of shares where the specified conditions are met although HMRC has been known to question the trading status of project vehicles in some cases.

There are significant inconsistencies in the current tax treatment of debt and equity financing which have a knock-on effect on investment returns – a, if not the, key driver for investors in the secondary market. We wait to see

what, if any, changes the government proposes in the Autumn Statement to level the playing field.

The draft GAAR: PFI and ‘composite trader’ treatment

Alison WalkerSenior associate, Pinsent Masons

The government is committed to delivering savings across operational PFI projects and ensuring taxpayers get value for money from PFI contracts. As PFI receipts are based on post-tax returns, lower effective tax rates are a key component of affordable pricing. What impact will the general anti-abuse rule (GAAR) have?

Many PFI projects adopt composite trader tax treatment and this can make the difference as to the commercial viability of a PFI project. Where composite trader treatment is adopted, any expenditure is incurred by the service provider in the course of a single trading activity, usually of constructing and supplying the building and ancillary services.

It follows that the service provider should be entitled to tax relief for the costs of constructing the building as those costs accrue in its accounts. For this reason, the effective tax rate on a PFI project where composite trader treatment is applicable is generally significantly less than a comparable PFI project where tax relief is available through capital allowances, and those benefits can be reflected in the pricing of the bid.

Composite trader treatment is not applicable where design and construction costs of the property are recognised as incurred on a capital asset of the service provider so may only be available where the service provider has a licence to occupy the property, as such an interest is unlikely to be shown on the service provider’s balance sheet.

Although there may be little to distinguish a lease from a licence in

> continued from previous page

The question is whether the use of a licence to obtain composite trader treatment will be the type of potentially abusive arrangement that may be caught by the draft GAAR

> continued on next page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

16

Pinsent Masons

some cases, there appears to be a cliff edge in terms of the tax treatment for PFI projects. The question is whether the use of a licence to obtain composite trader treatment will be the type of potentially abusive arrangement that may be caught by the draft GAAR. If the GAAR were to apply, HMRC may counteract the tax advantage on a just and reasonable basis. To the extent construction costs are disallowed, this will have a significant knock-on effect on pricing.

Where a licence is used to obtain the beneficial composite trader treatment, it will fall within the wide definition of a ‘tax arrangement’. The application of the GAAR then turns on whether that tax arrangement is ‘abusive’, applying the double reasonableness test: a tax arrangement is abusive if, having regard to all the circumstances, entering into or carrying out the arrangements cannot reasonably be regarded as a reasonable course of action.

The position is not clear. However, it is arguable that composite trader treatment, whereby the service provider obtains tax relief for expenses wholly and exclusively incurred for the purposes of the trade carried on by the service provider (within the meaning and spirit of that legislation), should be regarded as

a ‘reasonable course of action’ (the first part of the test) particularly given that

there is no exploitation of loopholes in the legislation to achieve the result.

Further, none of the specific indications that an arrangement is abusive apply. In fact, the opposite, as composite trader treatment results in the tax treatment reflecting the economics of the transaction.

The second part of the test is more difficult to apply. This is an objective test applying the views of the hypothetical person. Are ‘usual’ commercial transactions in the context of a PFI deal acceptable tax planning in the current economic climate, particularly given the public policy view of providing cheaper services to taxpayers? My instinct is that they are but this remains to be seen.

Much has been written of the effect of the draft GAAR on increased uncertainty in the UK tax system, and the same concerns apply to PFI projects. With so much focus on PFI projects in the press, the importance of certainty in post-tax cash flows cannot be underestimated and if the draft GAAR is applied to counteract composite trader treatment, the impact on pricing could be catastrophic for new PFI projects..

> continued from previous page

Sector Focus: Infrastucture (continued)

Recent Articles

PM-Tax | Issue 15 Wednesday 19 December 2012

17

Pinsent Masons

Cornwallis Care Services Ltd v HMRC [2012] UKFTT 724A genuine belief that a deferred payment agreement has been reached with HMRC can be a ‘reasonable excuse’ for failure to pay PAYE on time.

Schedule 56 to the Finance Act 2009 sets out the penalties which are chargeable in respect of failure to pay PAYE on or before the due date. These penalties cannot, however, be applied during a period when there is an agreement for deferred payment between HMRC and the taxpayer.

Cornwallis ran a number of care homes in Cornwall but faced financial difficulties during 2010 and consequently imposed a cost cutting programme across its business. During this time, the company was under financial pressure from its bankers and was late in meeting PAYE liabilities. Cornwallis had various meetings and conversations with local tax inspectors and an oral schedule of deferred PAYE payments was agreed. However, no written confirmation of the schedule was issued, and the parties disputed which PAYE periods the agreement covered.

The First-Tier Tribunal concluded that Cornwallis’ late payments for the periods in question were the result of a genuine belief that they had a deferred payment agreement with HMRC based on conversations with local tax inspectors. It was clear from HMRC’s submissions to the tribunal that they themselves were not clear about the terms which had been agreed with Cornwallis. In these circumstances, the tribunal held that Cornwallis’ genuine belief that they had been given a longer period to make

these payments should be treated as a ‘reasonable excuse’ for their late payments.

The tribunal noted that there is no statutory definition of what constitutes a ‘reasonable excuse’ for these purposes and, on the basis of earlier case law, reliance on information or guidance from HMRC that turns out to be misleading should be deemed a reasonable excuse.

Total Technology (Engineering) Limited v HMRC [2011] UKFTT 473The surcharge penalty regime – although it is highly mechanistic - is not fatally flawed. In particular, the fact that a penalty does not take into account the period of delay does not make it disproportionate.

The taxpayer company had paid small adjustments to the total VAT due on two occasions with the result that its rate of surcharge had reached 5% when it had been one day late in paying its entire VAT bill due for the quarter ended November 2008. The company had therefore been imposed a £4,000 surcharge and had appealed on the grounds of reasonable excuse and disproportionality.

The FTT had rejected the reasonable excuse argument which was based mainly on the adoption of a new accounting system which had proved unreliable.

However, the FTT had accepted that under both ECJ and European Court of Human Rights case law, it has a duty to intervene in circumstances where a penalty is disproportionate to the gravity of an offence. Having no power to reduce the penalty, the FTT had simply discharged it.

HMRC appealed the FTT’s decision and the UT allowed the appeal, finding that the penalty was harsh but not disproportionate.

Having reviewed the case law of the ECJ and of the European Court of Human Rights, the UT concluded that the UK had discretion to set penalties but that the imposition of penalties should not be manifestly inappropriate in relation to the objective that it sought to achieve.

The specific aim of the default surcharge was to penalise the failure to deliver a return or pay the tax by the due date. The legislation did not have the objective of ensuring that the tax was paid as soon after the due date as possible and so the length of the delay was not relevant in assessing the proportionality of the penalty. The UT emphasised the advantages of a mechanistic penalty regime easy to administer by “hard-pressed” HMRC officers. It noted that HMRC sends out surcharge liability notices (after the imposition of the first surcharge), so that “taxpayers know their position”. Furthermore, the penalty is “geared to the amount of outstanding VAT” and the reasonable excuse exception “strikes a fair balance”..

Our perspective on recent cases

PM-Tax | Issue 15 Wednesday 19 December 2012

18

Procedure

Pinsent Masons

Mark Young T/A The St Helens v HMRC [2012] UKFTT 702 (TC) The grant of a lease over the premises of a restaurant, following their repossession by the Landlord can constitute a transfer as a going concern for VAT purposes.

Mr Young had operated a restaurant through a company called Bonne Bouchee Caterers Limited (“Bonne Bouchee”). When the company became insolvent, the landlord repossessed the premises. Mr Young reopened the restaurant as a sole trader two weeks later, following negotiations for a new lease of Bonne Bouchee’s premises.

HMRC’s argued that Mr Young was liable to be registered for VAT as his business’s revenue had reached the relevant threshold. This was on the basis that supplies made by Bonne Bouchee should be treated as supplies made by Mr.Young under s.49 VATA.

Mr Young accepted that if there had been a transfer of the business as a going concern from Bonne Bouchee, he would be liable, but argued that no such transfer had taken place.

The Tribunal found that a transfer as a going concern had taken place, relying on the following points:

• The transfer of possession of the premises, fixtures and fittings to an intermediate person (the landlord) did not preclude the transfer of

the business as a going concern. The Tribunal noted that s.49 VATA was intended to prevent businesses from avoiding the registration threshold by transferring to a new legal entity.

• The time lapse in ownership of two to three weeks did not prevent the transfer from being a transfer as a going concern.

• Although Mr Young did not receive any stock or goodwill from the landlord, the premises, fixtures and fittings were sufficient to conclude that substantially the same business as before was being carried out.

The tribunal also considered a secondary issue; whether Mr Young had a legitimate expectation to rely on advice he had received through HMRC’s VAT helpline. On this and on whether as a matter of law the Tribunal has any jurisdiction, the appeal was stayed pending the outcome of Noor and Trade Sales Ltd, both of which are under consideration by the UT.

Bonik Food C-285/11The right to a deduction of input tax cannot be denied in circumstances where the tax authorities have not established that the relevant supplies to the taxpayer have not taken place nor that the taxpayer committed a fraud or knew or should have known that the supplies were connected with fraud.

The Bulgarian tax authorities denied Bonik a deduction for VAT on purchases of wheat and sunflower on the ground that the supplies had not taken place. This was based on various investigations

which had revealed in particular that the purported suppliers of Bonik had not had sufficient quantities of goods to make the supplies to Bonik.

The CJ-EU noted (inter alia) that the Bulgarian tax authorities did not dispute that Bonik had carried out subsequent supplies of goods of the same type as those in question and in the same quantity. The court also stressed that the right to a deduction – which is a fundamental principle – cannot be relied on for fraudulent purposes. This is the position when the taxpayer himself has committed tax fraud.The court added (referring to Kittel) that a person who knew or should have known that, by his purchase, he was taking part in a transaction connected with fraud must, for the purposes of Directive 2006/112, be regarded as a participant in the fraud.

The court concluded that, although, in view of regularities upstream, the supplies may be considered not to have actually taken place, the Kittel test had not been established and so the right to deduct should not be denied.

B. W. Male & Sons Limited v HMRC [2012] UKFTT 719 Trustees can be intermediaries despite the fact that they have fiduciary duties.

In 2002, BW Male & Sons Limited established the “B W Male & Sons Employee Benefit Trust” for the benefit of the company’s employees and made

Our perspective on recent cases

> continued on next page

PM-Tax | Issue 15 Wednesday 19 December 2012

19

Substance

Pinsent Masons

contributions (totalling £265,000) to the trust. The monies were paid to the trustees and the company charged them against profits. HMRC disallowed the deduction on the ground that no actual emoluments had been paid by the trustees within nine months of the end of the relevant accounting period (Section 43 FA 1989).

HMRC argued that the sum was a relevant potential payment in that it was an amount held by trustees as intermediaries with a view to it becoming a “relevant payment” upon the exercise of the trustees’ discretion to pay the sum to those entitled.

The Appellant’s main argument was that trustees have fiduciary duties and that they must act impartially in accordance with those duties. In the Appellant’s view, this precludes trustees from being intermediaries.

Following Sempra, the tribunal rejected the Appellant’s contention and dismissed the appeal.The Tribunal noted that the fiduciary duty only comes in play when the trustees decide who should receive “what and when”. The second part of the trustees’ function – which is to distribute funds – is “merely a mechanical function” of a person acting as an intermediary.

MBG Associates v HMRC [2012] UKFTT 723A business degree graduate who is presented with a series of “pre-packaged deals” in relation to mobile phones should know that the transactions are connected with fraud.

Olivier Murray had completed a four year course in European Business at a UK university and had obtained a degree. He had then joined a post-graduate program at a packaging company and had subsequently managed retail accounts for a smaller business. At the age of 25 (in 2005), he had set up MGB and registered it for VAT. The place of business was given as the home of the taxpayer’s parents and the business activity was described as “general brokering – essentially within mobiles/telecommunications”. HMRC had visited Olivier Murray and warned him about the risks of getting involved with MTIC fraud.

In 2006, Olivier Murray was introduced to a Mr Anthony Rose who presented him with the opportunity to sell mobile phones to one of his customers in France. Apparently, Mr Rose had explained that he did not have the sufficient cash-flows to enter the transaction himself – as a result of difficulties in obtaining repayments of VAT. Several deals followed with the French customer as well as with a Spanish customer.

Each of the deals came to Mr Murray “pre-packaged”; the supplier, the customer, the exact amount of goods, the date and the freight forwarder were

provided to Mr Murray. There was no good reason why Mr Rose (or his company GC) should have passed the opportunity of making the profit on the mobiles. The date chosen for each of the deals was the last day of MGB’s quarterly accounting period so that the VAT repayment could be obtained quickly, and the checks carried out by Olivier Murray were both “inadequate and inexistent”. The profit on each deal (4.5%) was substantial and the work required was minimal.

Applying Kittel and Mobilx, the FTT found that the conclusion that Mr Murray knew of the fraud was “inescapable”. Interestingly, the tribunal pointed to Mr Murray’s business degree and his two positions in commerce as support for the fact that he was “no slow learner”..

Our perspective on recent cases

> continued from previous page

PM-Tax | Issue 15 Wednesday 19 December 2012

20

Substance

Tax Planning – is there life after the GAAR? and New Year’s drinks reception

The proposed new GAAR will be targeted at “contrived and artificial” and “abusive” schemes, which “make a mockery of the will of Parliament” and exploit rules “in a way that Parliament could not rationally have contemplated”. It will not apply to “the centre ground of responsible tax planning.”

What will constitute “responsible tax planning”?

Heather Self, Director at Pinsent Masons Tax, will lead a seminar at which a panel of experts will consider:

• The impact of the GAAR on business planning • The GAAR in action – potential areas of dispute • Implications for High Net Worth Individuals • Impact on employee remuneration

Date: Thursday 24th JanuaryVenue: Pinsent Masons, 30 Crown Place, London EC2A 4ES