Embed Size (px)

Citation preview

UK HOTEL CAPITAL MARKETS INVESTMENT REVIEW 2018

HIGHLIGHTS

RESEARCH

UK Hotel investment totalled £5.5 billion in 2017, with Regional UK representing 56% of total investment

Private equity investors ranked as the top investor type with investment totalling approximately £1.5 billion

Overseas investors accounted for over £2.3 billion of investment, with a growing acceptance to deploy funds into prime regional UK cities

2

TRANSACTION OVERVIEW An exceptionally strong level of investment activity in the UK hotel market during the second half of 2017 has resulted in total investment volumes of £5.5 billion recorded for the year.

This equates to a 44% rise in investment activity compared to the previous year, on par with the transaction volume witnessed in 2007 and significantly above the 11-year average of annual hotel investment activity of £3.4 billion per annum. Furthermore, in 2017 total UK hotel transaction activity represented 33% of total investment volumes in the UK Specialist Property sector, an increase of 4% compared to the previous year, demonstrating the attractiveness of the UK hotel property sector as a means of providing enhanced, longer-term income in the alternative property sector.

Following a modest start to the year with hotel investment totalling £1.7 billion in the first six months, corporate portfolio activity dominated during the second half of the year with investment totalling £1.9 billion and London deal

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2017

2016

2015

2014

2013

2012

2011

2010

2009

2008

2007

Development 11-Year investment volumne

Single asset Portfolio Investment

Source: Knight Frank Research

FIGURE 1

UK total hotel investment volumes 2007-2017

flow at its peak with approximately £1.5 billion of asset sales transacting.

Investment from overseas investors was particularly active, with total overseas investment accounting for 42% of the total UK transaction volume, a sharp rise compared to 2016. Whilst the Brexit induced fall in the value of sterling has contributed significantly to the increase in overseas investment, 2017 has witnessed the acceptance by overseas investors to deploy their funds into assets located in prime regional UK cities, with the potential for both income and capital growth. In 2017, overseas investors accounted for over £2.3 billion of investment into UK hotel assets, divided equally between London and regional UK, with foreign investment successfully targeting 38% of the total regional UK sales volume and 48% of total investment activity in London.

The Crown Hotel, Harrogate (Fragrance Group)

3

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2017201620152014201320122011

(£ m

illion

)

7-YR average regional UK7-YR average London

Regional UKLondon

Source: Knight Frank Research

FIGURE 3

UK Hotel transactional activity London v Regional UK 2011-2017

3

UK HOTEL CAPITAL MARKETS 2018 RESEARCH

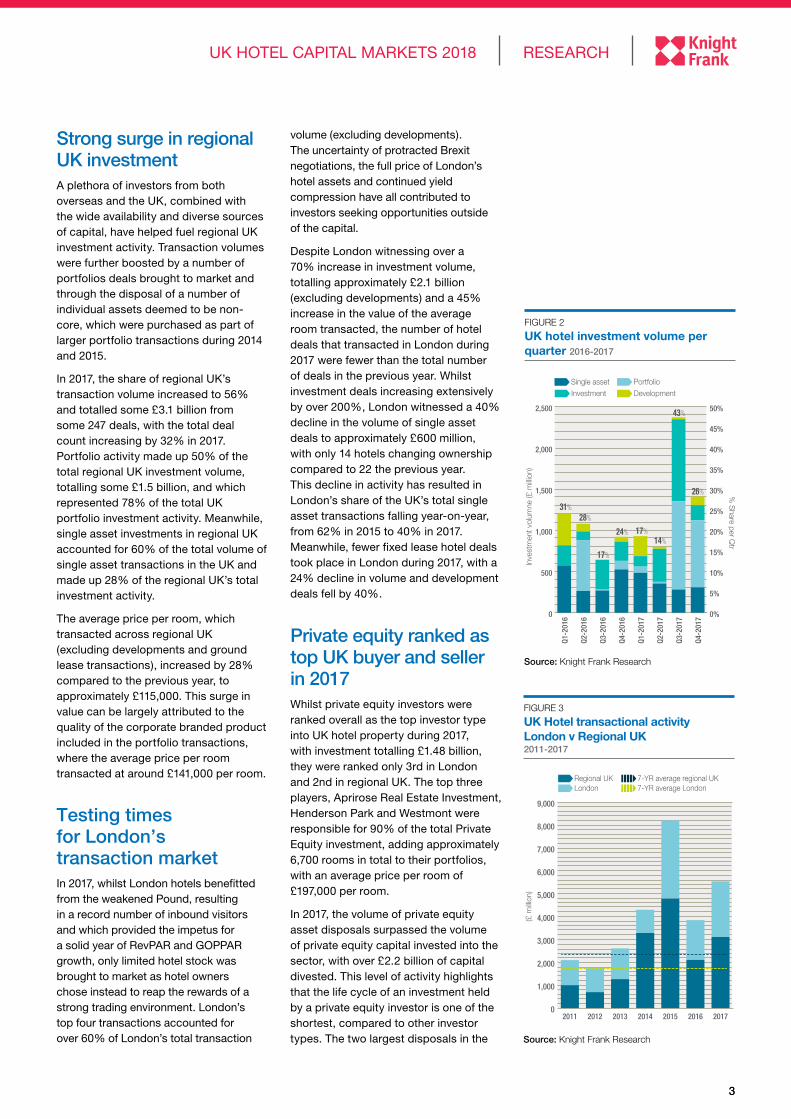

Strong surge in regional UK investment A plethora of investors from both overseas and the UK, combined with the wide availability and diverse sources of capital, have helped fuel regional UK investment activity. Transaction volumes were further boosted by a number of portfolios deals brought to market and through the disposal of a number of individual assets deemed to be non-core, which were purchased as part of larger portfolio transactions during 2014 and 2015.

In 2017, the share of regional UK’s transaction volume increased to 56% and totalled some £3.1 billion from some 247 deals, with the total deal count increasing by 32% in 2017. Portfolio activity made up 50% of the total regional UK investment volume, totalling some £1.5 billion, and which represented 78% of the total UK portfolio investment activity. Meanwhile, single asset investments in regional UK accounted for 60% of the total volume of single asset transactions in the UK and made up 28% of the regional UK’s total investment activity.

The average price per room, which transacted across regional UK (excluding developments and ground lease transactions), increased by 28% compared to the previous year, to approximately £115,000. This surge in value can be largely attributed to the quality of the corporate branded product included in the portfolio transactions, where the average price per room transacted at around £141,000 per room.

Testing times for London’s transaction market In 2017, whilst London hotels benefitted from the weakened Pound, resulting in a record number of inbound visitors and which provided the impetus for a solid year of RevPAR and GOPPAR growth, only limited hotel stock was brought to market as hotel owners chose instead to reap the rewards of a strong trading environment. London’s top four transactions accounted for over 60% of London’s total transaction

volume (excluding developments). The uncertainty of protracted Brexit negotiations, the full price of London’s hotel assets and continued yield compression have all contributed to investors seeking opportunities outside of the capital.

Despite London witnessing over a 70% increase in investment volume, totalling approximately £2.1 billion (excluding developments) and a 45% increase in the value of the average room transacted, the number of hotel deals that transacted in London during 2017 were fewer than the total number of deals in the previous year. Whilst investment deals increasing extensively by over 200%, London witnessed a 40% decline in the volume of single asset deals to approximately £600 million, with only 14 hotels changing ownership compared to 22 the previous year. This decline in activity has resulted in London’s share of the UK’s total single asset transactions falling year-on-year, from 62% in 2015 to 40% in 2017. Meanwhile, fewer fixed lease hotel deals took place in London during 2017, with a 24% decline in volume and development deals fell by 40%.

Private equity ranked as top UK buyer and seller in 2017 Whilst private equity investors were ranked overall as the top investor type into UK hotel property during 2017, with investment totalling £1.48 billion, they were ranked only 3rd in London and 2nd in regional UK. The top three players, Aprirose Real Estate Investment, Henderson Park and Westmont were responsible for 90% of the total Private Equity investment, adding approximately 6,700 rooms in total to their portfolios, with an average price per room of £197,000 per room.

In 2017, the volume of private equity asset disposals surpassed the volume of private equity capital invested into the sector, with over £2.2 billion of capital divested. This level of activity highlights that the life cycle of an investment held by a private equity investor is one of the shortest, compared to other investor types. The two largest disposals in the

Source: Knight Frank Research

FIGURE 2

UK hotel investment volume per quarter 2016-2017

0

500

1,000

1,500

2,000

2,500

Q4-2

017

Q3-2

017

Q2-2

017

Q1-2

017

Q4-2

016

Q3-2

016

Q2-2

016

Q1-2

016 0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

31% 28%

17%

24% 17% 14%

43%

26%

Development

Inve

stm

ent v

olum

ne (£

milli

on)

% S

hare per Qtr

Single asset PortfolioInvestment

4

hotel sector in 2017 came from portfolios sales unloaded by private equity investors. Lonestar traded the Jurys Inn portfolio for £800 million, having acquired the portfolio in 2015. Meanwhile, Bain Capital Credit & Canyon Partners agreed the £525 million sale of The Q Hotels portfolio to the private equity investor, Aprirose Real Estate, having acquired the distressed loan portfolio in 2014. This transaction then resulted in further investment activity, with the simultaneous structuring of a ground lease deal, involving the sale of the freehold of 17 of the assets to an institutional investor.

In order to generate the high level of investment returns projected, private equity funds employ strong asset management teams, often with specialist hotel-sector expertise, in order to develop a clear vision prior to purchase and to unlock the value during the term of the investment, driving untapped potential from the property and operating business. In order to deliver the superior returns required by private equity investors, asset managing the bricks and mortar remains a key element, but having confidence in the strength of the operating business, management team, brands and concepts are equally all critical components, prior to executing a planned, finite exit strategy.

Private equity investment will remain a strong feature of the hotel investment market in 2018, with a number of investors further diversifying by offering

structured loan facilities from the creation of specialist dedicated credit funds, with the purpose of providing customised hotel funding solutions.

Institutional investor demand on the rise Over the past investment cycle, as hotel real estate has cemented its position as a mainstream asset class, the resurgence and renewed popularity of leases, as a means of separating the risk of owning the property from the hotel operating business, has provided institutional investors with an attractive, low-risk, long-term strategic model, in which to invest and diversify their portfolios.

With the increasing demand for commercial investments involving fixed, variable and ground-leases as well as forward funding hotel developments, it comes as no surprise that Institutional Investors were strong buyers during 2017, ranked as second, with investment totalling £1.38 billion. This illustrates that hotel real estate remains an attractive long-term investment in a diversified investment portfolio, whereby hotel investments have the potential for higher returns and the ability to match long-term liabilities with long-term investments.

Over 60% of institutional capital invested in hotel transactions was secured with either a fixed, variable, ground or long lease interest. Meanwhile, 26% of institutional investment targeted Source: Knight Frank Research

Managed / FranchisedLong LeaseholdGround Lease

Vacant PossessionDevelopment Fixed LeaseVariable Lease

London Regional UK

Fixed Lease

24%

3%

34%

5%

7%

15%

2%

38%

23%

37%

12%

FIGURE 5

Institutional investment activity by investment model

Source: Knight Frank Research Note: The Average Price Per Room Transacted excludes the sale of Grosvenor House, A JW Marriott Hotel.

FIGURE 4

Total UK hotel investment volume 2017 – by investor profile (buyers v sellers)

Tran

sact

ion

volu

me

(£ m

illion

)

Average price per room transacted (£)

0

500

1,000

1,500

2,000

2,500

UK CorporateInvestor

UK CorporateHotelier

OverseasCorporate Investor

OverseasCorporate Hotelier

InstitutionalInvestor

Private Equity

Seller Buyer – average price per room transactionBuyer

0

50,000

100,000

150,000

200,000

250,000

300,000

The appetite for quality regional UK hotels will remain buoyant in 2018, with strong demand from institutional, private equity and overseas

investors. Investment decisions will be determined by income security, strong covenants,

potential upside and competent management. HENRY JACKSON, KNIGHT FRANK,

HEAD OF REGIONAL UK AGENCY

5

UK HOTEL CAPITAL MARKETS 2018 RESEARCH

developments, secured with an operational fixed lease in place upon the project completion. Regional UK attracted over 50% share of the total institutional investment volume in 2017, however, the number of deals transacting in the provincial markets was four times higher than compared to London, with over 40 deals.

Fixed or ground lease investments comprised over 70% of institutional activity in regional UK, compared to just over a quarter of activity in London. Institutional investment from overseas represented less than 3% of the total volume, with their investment targeting properties sold on a vacant possession basis and now operated by third-party management companies, such as Kew Green and Bespoke Hotels.

The attractive risk-return profile of the hotel sector, combined with the opportunity for diversification and favourable as well as alternative demographics compared to other sectors in commercial property, have given rise to strong and growing demand in the sector by institutional investors, fuelling the overall level of hotel investment in 2017. The acquisition of a trading asset, by LGIM Real Assets (Legal & General), of the 357-room Hampton by Hilton Stansted Airport, which operates under a management Source: Knight Frank Research

European OtherSweden / IsraelUSA

East AsiaUK

16%

14%

1%

9%

2%

58%

FIGURE 6

UK hotel investment – investor origin 2017

and franchise agreement, confirms the strong appetite by institutional investors for hotels with solid fundamentals.

The high quality location of the newly developed hotel, combined with the strength of the brand, the proximity to a major demand generator and the highly cash generative capability of the newly trading asset were all major factors in the investment consideration, a trend set to continue as institutional capital intensifies.

Overseas buyers attracted by the weak poundIn London, Overseas Corporate Investors ranked as the highest spending investor by transaction volume in 2017, whilst in regional UK, Overseas Corporate Hoteliers achieved the top spot. This endorses the level of overseas investor interest into the sector, with over £2 billion of investment from these two investor groups. Significantly, the net capital flowing into the sector, from the Overseas Corporate market was the highest of all investor types at £1.2 billion, with relatively few asset disposals during 2017.

Such activity suggests that despite the ongoing uncertainty surrounding Brexit, overseas investors continue to

The Q Hotel Group, Oulton Hall, Near Leeds (Aprirose Real Estate Investment)

6 *Vacant Possession refers to hotels that are for sale, free and clear of incumbent management, excluding franchised properties

have confidence in the UK hotel sector, taking advantage of an increase in overseas visitors to the UK and a period of robust trading, whilst also taking into consideration the exchange rate and the cost implications of currency fluctuations when transferring funds overseas.

Pandox and the Fattal Hotel Group’s £800m joint acquisition of the Jurys Inn portfolio, was instrumental in taking the Overseas Corporate Hotelier to prime position as the regional UK’s highest investor group. Nevertheless, over 30 separate hotel transactions were completed by this investor group, reinforcing the attractiveness and resilience of the regional UK hotel market.

Investment from the Asia Pacific region increased by over 65% to approximately £500 million in 2017, of which Singaporean capital represented 63% of the investment. Corporate hoteliers from Singapore were particularly active, which included CDL Hospitality Trust’s acquisition of the Lowry Hotel in Manchester for £52.5 million; HPL Properties acquisition of the Hilton London Olympia for £115 million and the Fragrance Group organically acquiring a collection of seven hotels located nationwide, some 750 rooms with total investment in excess of £50 million.

In London, meanwhile, leading transactions from overseas corporate investors came from the USA with Ashkenazy Acquisition Corporation’s

£600 million purchase of the Grosvenor House JW Marriott Hotel; Pandox’s £80 million purchase of Hilton London Heathrow Terminal 4 and Tian An China Investments acquisition of the South Place Hotel for £67 million.

Overseas Private Equity investors were the only other main source of overseas capital, with approximately £250 million of investment, all of which originated from the USA.

Vacant possession transactions dominate the UK hotel market in 2017In 2017, hotels that sold with vacant possession* represented the largest group of hotels changing hands in the UK, in terms of investment volume and rooms transacted, with a total value of over £2 billion, equating to a market share of 40% in terms of investment volume and 48% of the total room stock. The two major UK regional hotel portfolio transactions sold on a vacant possession basis, acting as the major catalyst behind the increase in volume and contributed significantly to the 50% rise in the average value per room, for regional UK hotels sold on a vacant possession basis.

Significant variation existed between regional UK and London, with less

INVESTMENT FROM THE ASIAPACIFIC REGION INCREASEDBY OVER 65% TO APPROX£500 MILLION IN 2017, OFWHICH SINGAPOREAN CAPITALREPRESENTED

63% OF THEINVESTMENT.

INVESTMENTFROM THEASIA PACIFICREGIONINCREASED BY OVER 65% TOAPPROXIMATELY £500 MILLIONIN 2017, OF WHICH SINGAPOREANCAPITAL REPRESENTED 63% OFTHE INVESTMENT.

The Q Hotel Group, The Midland, Manchester (Aprirose Real Estate Investment)

7

UK HOTEL CAPITAL MARKETS 2018 RESEARCH

During 2017, the hotel sector, particularly in regional UK, fully exploited the commercial ground rent market, with a strong uptake in demand. Over £265 million of ground rent transactions completed, across 12 separate transactions, involving some 29 properties and over 4,200 rooms. The insatiable demand from institutional investors ensured that this investor type swept the market for all ground lease transactions, with record yields achieved, between 2.3%-3.3%.

With hotel cash flows typically growing in line with inflation and hotel assets considered less likely to become

HOTEL GROUND RENTS – A RISING PHENOMENON, FAST BECOMING MAINSTREAM INVESTMENTS

functionally obsolete, due to the ongoing level of capex invested by the tenant, this form of investment structure lends itself favourably to hotels as an asset class. A hotel ground lease, acts as a hedge against inflation and offers the institutional investor the opportunity to diversify their investment strategy, with the structure considered to offer a highly secure, long-term income stream, derived from prime assets.

The largest hotel ground rent transaction to take place in 2017 followed the successful acquisition by Aprirose Real Estate of the Q Hotel

portfolio, who simultaneously carved out a ground rent for 17 of the freehold properties to PGIM Real Estate for approximately £160 million. In doing so, this ground rent transaction can be regarded as an innovative means of providing an additional source of funds to help finance the acquisition.

The demand for ground rent transactions is strong, with a wealth of institutional investors having the appetite for exposure and driving money into the market, viewing the returns as highly attractive and are ready to seek out creative opportunities. Investors non-reliant on debt to fund acquisitions, dominate the ground rent market, with their ability to execute transactions swiftly.

The hotel ground rent market will continue to evolve, albeit going forward the level of transactional activity will be dependent upon the ability to create suitable hotel ground rents, which appeal to both the institutional investor and the operator. The ground rent market, however, is not without its trepidations, with concern that in a latter stage of the investment cycle, the operator could become over exposed in terms of its debt commitment, particularly given the cyclical nature of the hotel trading environment.

Hotels as an asset class are uniquely placed to create ground rents structures. They enable owners to enhance return,

essentially securing long term financing at a fixed rate that doesn’t have to be repaid. Institutions crave this type of

stock – it provides them with an over collateralised asset, with an income profile that enables them to match long-term

liabilities. The demand will continue to outstrip demand – even if we do see the anticipated rate rise.

SHAUN ROY, KNIGHT FRANK, HEAD OF SPECIALIST PROPERTY INVESTMENT.

than 10% of the transaction volume in London selling with the benefit of vacant possession, compared to 62% in the provinces. Furthermore, in London, the volume of activity declined by 51% compared to 2016, with no big-ticket hotel assets transacting on a vacant possession basis.

Subsequent to the sale of the Q Hotel portfolio, Redefine BDL Hotels were selected as the third-party operator for the portfolio, and in doing so became the most active operator in the UK in 2017, with the net addition of over 30 hotels, some 4,600 rooms, to its management portfolio.

Meanwhile, following the sale of the Jurys Inn portfolio and the Portland Hotel Group in Scotland, Leonardo Hotels became a major national operator in the UK, adding over 4,500 UK hotel rooms to its portfolio and the operations platform for the Jurys Inn brand. Continuing the growing trend of operating leases and a renewed willingness by operators to commit to leases, 2018 will see the restructuring of the Jurys Inn portfolio, involving 20 properties, whereby Leonardo Hotels will enter into a revenue-based lease agreement, with minimum rent guarantees, for a consideration of approximately £120 million. The Crown Hotel, Harrogate (Fragrance Group)

8

Source: Knight Frank Research Note: Variable Lease Average Value per Room excludes the sale of the Grosvenor House, A JW Marriott Hotel

FIGURE 8

Average price per room transacted 2017 v 2016 by investment structure – regional UK (£)

£ av

erag

e pr

ice

per r

oom

% C

hange in value

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

All Asset TypesFixed LeaseGround LeaseVacantPossession

Managed / Franchised

ManagedFranchised

2017 % change in value2016

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

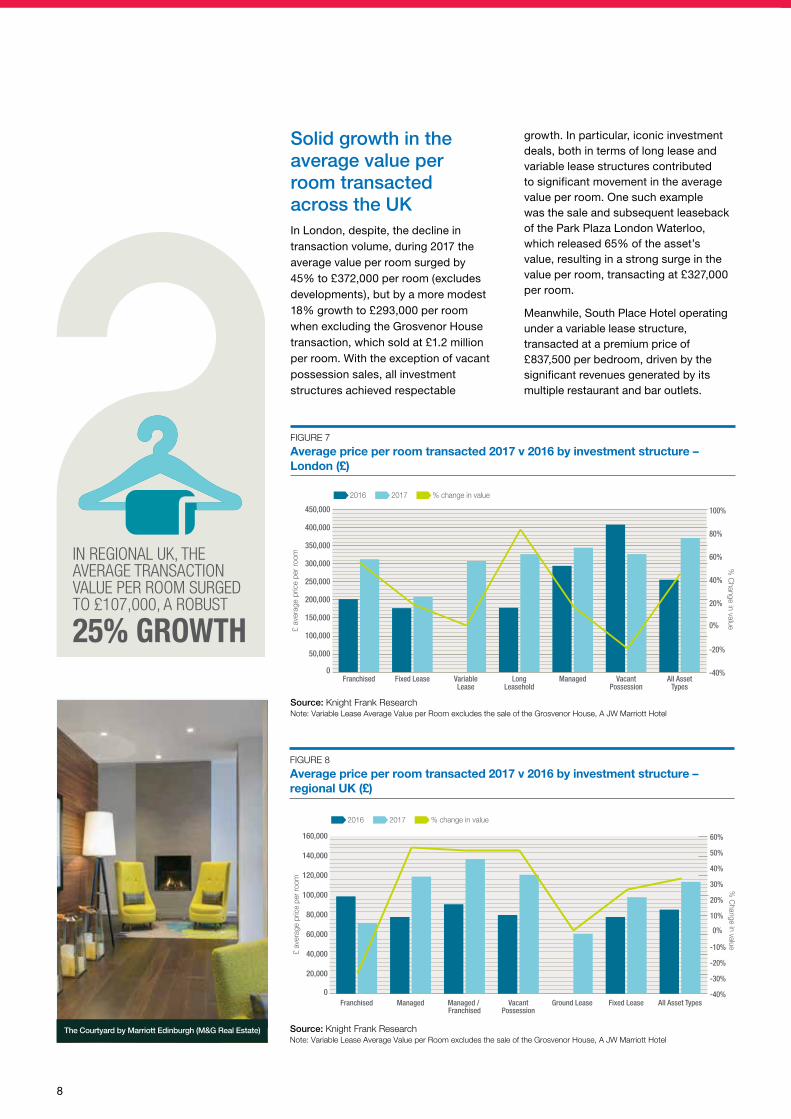

Solid growth in the average value per room transacted across the UKIn London, despite, the decline in transaction volume, during 2017 the average value per room surged by 45% to £372,000 per room (excludes developments), but by a more modest 18% growth to £293,000 per room when excluding the Grosvenor House transaction, which sold at £1.2 million per room. With the exception of vacant possession sales, all investment structures achieved respectable

growth. In particular, iconic investment deals, both in terms of long lease and variable lease structures contributed to significant movement in the average value per room. One such example was the sale and subsequent leaseback of the Park Plaza London Waterloo, which released 65% of the asset’s value, resulting in a strong surge in the value per room, transacting at £327,000 per room.

Meanwhile, South Place Hotel operating under a variable lease structure, transacted at a premium price of £837,500 per bedroom, driven by the significant revenues generated by its multiple restaurant and bar outlets.

IN REGIONAL UK, THEAVERAGE TRANSACTIONVALUE PER ROOM SURGEDTO £107,000, A ROBUST

25% GROWTH

Source: Knight Frank Research Note: Variable Lease Average Value per Room excludes the sale of the Grosvenor House, A JW Marriott Hotel

FIGURE 7

Average price per room transacted 2017 v 2016 by investment structure – London (£)

£ av

erag

e pr

ice

per r

oom

% C

hange in value

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

All AssetTypes

VacantPossession

ManagedLongLeasehold

VariableLease

Fixed LeaseFranchised

2017 % change in value2016

-40%

-20%

0%

20%

40%

60%

80%

100%

The Courtyard by Marriott Edinburgh (M&G Real Estate)

9

UK HOTEL CAPITAL MARKETS 2018 RESEARCH

Source: Knight Frank Research Note: Variable Lease Average Value per Room excludes the sale of the Grosvenor House, A JW Marriott Hotel

FIGURE 9

Regional UK Hotel transactions 2017 by UK region

Tran

sact

ion

volu

me

(£'0

00)

Average value per room

transacted (£)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

UK Is

les

&Hi

ghla

nds

Wal

es

Scot

land

Sec

onda

ry

York

shire

&Th

e Hu

mbe

r

East

Mid

land

s

Nor

th E

ast

East

of E

ngla

nd

Scot

land

Prim

e

Sout

h W

est

Sout

h Ea

st

Nor

th W

est

Wes

t Mid

land

s

Average price per roomVolume

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Finally, a number of full-service, luxury and upscale hotels, transacted, resulting in a strong growth in the average value per room for franchised properties, such as the sale of the DoubleTree by Hilton Westminster Hotel, which sold for £413,000 per bedroom.

In regional UK, the average transaction value per room surged to £107,000, a robust 25% growth. Hotels operating under a management agreement, (including properties also operated under a franchise agreement) achieved significant uplift in the average value per room, albeit, this was due to a much greater proportion of assets transacting in the four-star, full service market, compared to the previous year. The sale of the 790-room Hilton Birmingham Metropole, the largest hotel by number of bedrooms in the provincial UK market, further helped boost the average value per room.

West Midlands ranked as the most attractive region for hotel investment in 2017The West Midlands was the most liquid region in the UK in 2017, recording over £305 million of transactions from some 23 deals, with 71% of the investment targeted in Birmingham. Manchester, which accounted for 60% of investment in the north-west of England, was the UK’s second most attractive city with over £155 million of investments, followed by Edinburgh with over £115 million of deals transacted.

The West Midlands region further consolidated its 1st position, with the highest average value per room of all UK regions (excluding London), achieving an average value of £113,000 per room, closely followed by the north west of England, at £111,000 per room.

Edinburgh’s hotel market was most buoyant, recording a total of ten hotel transactions, followed by Birmingham and Manchester. Two of the top five hotels transacting in regional UK (on an average value per room basis) were located in Manchester, with both assets selling to overseas investors.

On an average value per room basis, based upon transaction activity over £25 million, Manchester was the highest scoring city at £167,000 per room, followed by Birmingham at £136,000 per room and Stansted Airport was ranked third (at £135,000 per room), boosted by the £48.3 million sale of the Hampton by Hilton. Due to the spread of assets transacting in Edinburgh across all market sectors, the average value per room was considerably lower than

other prime destinations at £106,000

per room, despite having some of the

highest trading assets by price.

This high level of transactional activity

in regional UK, in particular the prime

regional hubs, is evidence of the

continued level of confidence from

both overseas and domestic investors

in the sustainability of the UK hotel

market, both in terms of income

growth and driving added value.

The Courtyard by Marriott Edinburgh (M&G Real Estate)

10

LEADING INVESTOR 2017

TOTAL INVESTMENT

PRIVATE EQUITY Aprirose Real Estate£625 million

(£143,000/room)

UK INSTITUTIONAL INVESTOR PGIM REAL ESTATE

£200 million(£66,000/room)

OVERSEAS CORPORATE HOTELIER (excluding portfolios)

HPL Properties £155 million

(£251,000/room)

UK CORPORATE HOTELIER

Europoint Holdings Ltd CONFIDENTIAL

Bowling Green Asset Management

£23 million (£105,000/Room)

LEADING UK HOTEL TRANSACTIONS BY INVESTMENT STRUCTURE

ACQUISITION INVESTOR INVESTMENT

LARGEST PORTFOLIO TRANSACTION Jurys Inn Portfolio Pandox & Fattal Hotel Group £800 million (£175,000/room)

LARGEST SINGLE ASSET TRANSACTION LONDON

Doubletree by Hilton Westminster

Westmont £190 million (£413,00/room)

LARGEST SINGLE ASSET TRANSACTION REGIONAL UK

Holiday Inn Manchester (City Centre)

Starwood Capital £54 million (£181,000/room)

LARGEST FIXED LEASE TRANSACTION LONDON

Novotel London City South La Salle Investment

Management£64 million (£350,000/room)

LARGEST FIXED LEASE TRANSACTION REGIONAL UK

Portfolio of 4 Premier Inn HotelsKnight Frank Investment

Management£38 million (£112,000/room)

LARGEST VARIABLE LEASE TRANSACTION

Grosvenor House, a JW Marriott Hotel

Ashkenazy Acquisition Corp (GH Equity UK)

£600 million (£1.2m/room)

Despite strong growth in new hotel supply, prime regional UK cities have continued to observe a robust trading performance. With ongoing structural opportunities outside of London, the ripple effect will continue to result in solid investment going forward in regional UK.

Investment opportunities 2018Investment activity has been buoyant during Q1 2018, continuing at a similar pace to investment levels in the second half of 2017, with over a £1 billion of assets having already exchanged or completed. Portfolio transactions include Lonestar’s exit from the hotel sector, with the £600m disposal of the final 23 hotels held by its Amaris Hospitality platform; and the £430m sale of SACO, the Serviced Apartment business owned by Oaktree Capital Management, comprising some 39 properties and a development pipeline of some 900 rooms.

The appetite for investment in Europe as a whole remains strong and despite the increasingly intensive global competitive

landscape, we are optimistic the UK will remain attractive to international investors in the long-term. Despite the continued opacity over the outcome of Brexit and the political volatility that will follow, combined with government plans to force overseas investors to pay capital gains tax on commercial property from April 2019,

the weight of money continuing to target hotel investment is significant. Recent transactional activity is evidence that investors have confidence in the inherent structural growth of the hotel sector and with investment decisions determined by income security rather than geography alone, the strong demand for quality

£

11

Sizeable portfolios offering a good base in terms of profitability and which further encompass the opportunity to add value, through margins or development potential remain in hot pursuit by investors and operators. However, add in to the equation the opportunity to acquire and package together a collection of assets, which offer the potential to carve out long-term ground rents; fixed leases or variable leases with minimum guaranteed rent structures; this is what makes the hotel sector appealing to the wider investment market.

There is certain value to be added, through the creation of clean, simplistic, uniform property portfolios, which

KNIGHT FRANK VIEWoffer the potential to drive guaranteed, sustainable income in the long-term and which act as a hedge against inflation. Furthermore, with increased competition in the debt markets, from non-traditional lenders and the creation of credit funds, there is much wider availability of finance to fund customised, innovative investment deals. Both the Jurys Inn and Q Hotel portfolio transactions offered the opportunity for innovative structures on scale, albeit the challenge going forward is to find the quantum of suitable hotel stock to match this level of commercial interest.

With renewed vigour by certain operators to enter into lease agreements, such as Dalata, Leonardo Hotels and StayCity, we

envisage that the focus of institutional funds will shift beyond the budget sector, increasing their exposure instead to quality, full service assets, with the potential for income and capital growth. The challenge for the global hotel operator, many of whom have invested heavily in a franchise model, will be to maintain market share and brand exposure, particularly in the fragmented mid-market sector. An increase in joint venture deals between corporate investors and hoteliers willing to take leases, backed by the covenant strength of a global hotel operator is likely to become a more prominent strategy going forward.

regional UK hotels, from a diverse group of buyers is set to remain positive throughout 2018.

As such, transaction activity in the UK regions is set to remain robust in 2018, with investment deals, led by private equity and institutional capital anticipated to continue to rise. Investment activity in London is

likely to continue to remain somewhat subdued in 2018, whilst the protracted Brexit negotiations continue and the impact on the wider economy remains obscured. Nevertheless, transaction activity in London will focus on prime assets, with investors, particularly from overseas, willing to pay a premium for long-term, inflation-linked

investments, offering a high residual value and the security of a major global hotel operator. With positive fundamentals and evidence of a strong transactional market already in 2018, there is good reason for the optimism to continue and for UK hotel investment levels to rise above the strong performance witnessed in 2017.

UK HOTEL CAPITAL MARKETS 2018 RESEARCH

Travelodge London Tower Bridge (CCLA Investment Management)

Important Notice

© Knight Frank LLP 2018 – This report is published for general information only and not to be relied upon in any way. Although high standards have been used in the preparation of the information, analysis, views and projections presented in this report, no responsibility or liability whatsoever can be accepted by Knight Frank LLP for any loss or damage resultant from any use of, reliance on or reference to the contents of this document. As a general report, this material does not necessarily represent the view of Knight Frank LLP in relation to particular properties or projects. Reproduction of this report in whole or in part is not allowed without prior written approval of Knight Frank LLP to the form and content within which it appears. Knight Frank LLP is a limited liability partnership registered in England with registered number OC305934. Our registered office is 55 Baker Street, London, W1U 8AN, where you may look at a list of members’ names.

HOTEL RESEARCH

Philippa Goldstein Hotel Analyst +44 (0) 203 826 0600 [email protected]

HOTELS

Julian Evans FRICS Head of Healthcare, Hotels & Leisure +44 20 7861 1147 [email protected]

Alex Sturgess MRICS Head of Hotel Agency +44 (0) 20 7861 1164 [email protected]

Henry Jackson MRICS Head of Regional UK Agency + 44 20 7861 1085 [email protected]

CAPITAL MARKETS

Shaun Roy MRICS Head of Specialist Property Investment +44 20 7861 1222 [email protected]

Knight Frank Research Reports are available at KnightFrank.com/Research

Trading Performance Review - 2017

RECENT MARKET-LEADING RESEARCH PUBLICATIONS

HIGHLIGHTS (12-MONTH PERIOD SEPTEMBER-AUGUST 2016/17)

London’s GOPPAR up 5.8%, driven by strong growth in the Average Room Rate.

Regional UK Hotels average a Gross Operating Profit of 32% compared to 45.5% in London.

Payroll costs continue to rise and equate to 24% of Total Revenue in London and 31% in Regional UK.

RESEARCH

2017

UK HOTEL TRADING PERFORMANCE REVIEW

UK Hotel: Spring 2018 Market Overview

Knight Frank Research provides strategic advice, consultancy services and forecasting to a wide range of clients worldwide including developers, investors, funding organisations, corporate institutions and the public sector. All our clients recognise the need for expert independent advice customised to their specific needs.

Front Cover Picture: The Hampton by Hilton London Stansted Airport (LGIM Real Assets)

Specialist Property Report - 2017

SPECIALIST PROPERTYREST ASSURED

2017

RESEARCH

OVERVIEW OPPORTUNITIES WHERE TO INVEST

Hotel Development Opportunities 2017

UK HOTEL DEVELOPMENT OPPORTUNITIES 2017

HIGHLIGHTS

RESEARCH

UK hotel supply grew by 2.7% in 2016 with a third of all new supply found in London. The Capital was boosted by 5,000 new hotel rooms.

Bath, Brighton, Edinburgh, Cambridge and Belfast rank as the Top 5 cities in Knight Frank’s inaugural UK Hotel Development Index.

The budget hotel sector accounted for 50% of all new UK hotel supply in 2016. It now represents a quarter of the UK’s total hotel supply.

A

UK HOTEL & LEISURE PROPERTY 2018

SPRING MARKET OVERVIEW