Embed Size (px)

Citation preview

201820172016

Market Monitor

2018South West of England and

South Wales Property Review

Alder King Market Monitor 20181

Contents3 Key Market Trends

5 Key Regional Transactions

7 Bath

9 Bridgwater

11 Bristol

13 Cardiff

15 Exeter

17 Gloucester

19 Newport

21 Plymouth

23 Swindon

25 Taunton

27 Truro

29 Residential Development Land

30 Planning

CGI of 3 Glass Wharf, Bristol. Courtesy of Salmon Harvester Properties.

2www.alderking.com

KeySouthWestCentres

OfficeandIndustrialDemandandSupply(000sqft)

Year OfficeDemand OfficeSupplyIndustrialDemand

IndustrialSupply

2017 1,719 2,490 5,152 3,578

2016 2,023 2,724 8,427 3,694

2015 1,909 3,235 5,852 4,320

2014 2,207 3,862 4,969 5,695

2013 1,481 4,761 4,544 6,815

Cardiff&Newport

OfficeandIndustrialDemandandSupply(000sqft)

Year OfficeDemand OfficeSupplyIndustrialDemand

IndustrialSupply

2017 768 1,073 1,111 957

2016 762 1,183 725 1,340

2015 748 1,209 1,008 1,459

2014 646 1,360 983 2,102

2013 378 1,345 957 2,088

Simon Price Head of Agency

Alder King

ForewordMarket Monitor reviews the 2017 occupational and investment markets in 11 key centres in the South West of England and South Wales.

The key features of the market include:

• The region’s commercial property market proved resilient in 2017 and outperformed expectations.

• The occupational market will remain robust with real rental growth being driven across most sectors by strong demand, reducing supply and a subdued appetite for speculative development.

• 2017 witnessed a record volume of investment transactions, mirroring trends nationally. Strong demand linked to the positive occupational backdrop maintained and drove values, with the industrial/logistics sector being the standout performer.

• Ongoing change in structure, occupier requirements and consumer preferences will continue to be felt across the retail, logistics, office and residential sectors in 2018.

• Demand for short term and strategic residential land remains strong. The Build to Rent market continues to build momentum, albeit slowly, but progress is expected in 2018 with a number of major institutionally funded schemes coming to site.

• The major challenge of meeting housing demand will remain a key theme in 2018. The reluctance to roll back green belt will this year be tested at policy level but we expect the themes of higher density and more intense use of existing brownfield land to remain the primary response.

• We anticipate another strong performance across the region from the property market in 2018.

Alder King Market Monitor 20183

(sq m)sq ftKey

(33

4)

31

(86

) 8

(35

0)

32.5

(26

9)

25

(18

8)

17.5

(126

.48

) 11

.75

(172

) 16

(19

1) 1

7.75

(129

) 12

(14

5)

13.5

(94

) 8

.75

(94

) 8

.75

(86

) 8

(86

) 8

(86

) 8

(81)

7.5

(59

) 5

.5

(59

) 5

.5

(72.

65

) 6

.75

(75

) 7

(97

) 9

(16

1) 1

5

(16

2)

15 (237

) 22

(15

6)

14.5

(210

) 19

.5

(20

4.5

) 20

(14

7.25

) 13

.68

(176

.5)

16.4

(19

4)

18

(178

) 16

.5

(10

8)

10

0

10

8

6

4

2

industrial headline rent £psf

0

35

25

30

20

15

10

5

in town headline rent £psf

0

35

25

30

20

15

10

5

out of town headline rent £psf

Swin

don

Glouc

este

r

Newpo

rt

Bristo

l

Cardi

ff

Bridgw

ater

Exete

r

Plymou

thTr

uro

Taun

ton

Swin

don

Glouc

este

r

Newpo

rtBat

h

Bristo

l

Cardi

ff

Bridgw

ater

Exete

r

Plymou

thTr

uro

Taun

ton

Swin

don

Glouc

este

r

Newpo

rtBat

h

Bristo

l

Cardi

ff

Bridgw

ater

Exete

r

Plymou

thTr

uro

Taun

ton

Offices

Industrial

Key Market Trends

occupational summary

• Total take-up in key South West centres decreased in 2017 compared to the record figures achieved in 2016. This is largely due to the lack of good quality immediately available supply, limited large scale speculative development and the loss of consented sites to alternative uses.

• The majority of centres will support speculative development. St Modwen, St Francis/iSec, Chancerygate, KMW, Richardson Barbury and Rockhaven have all started or are about to start schemes which will deliver circa 900,000 sq ft in Bristol alone.

• Demand is increasingly focused on better specified space with new build activity now currently underway in Bristol, Gloucester, Wellington, Bridgwater, Swindon and Plymouth.

• With limited second hand space coming to market, mid-range occupiers are increasingly only able to satisfy their needs via the design and build route.

• There has been a continuing improvement in rentals, lease durations and capital values in the majority of centres, with the potential for further growth.

• Severnside and the North Bristol motorway corridor has reinforced its regional importance as evidenced by Amazon and DHL’s recent acquisitions.

• With the removal of Severn Bridge tolls in December 2018, we anticipate the South West logistics demand triangle will be redefined to include the M4 corridor from the two bridges west to Newport.

• Key areas of growth continue to come from occupiers in the logistics sector and particularly those involved with internet fulfilment, with an increasing number of enquiries from engineering and added value engineering occupiers.

occupational summary

• Some key regional centres saw a step change in headline rental levels in 2017. This is likely to continue through 2018 with Bristol predicted to set a new record city centre rent of £35 per sq ft.

• Supply remains tight with very limited new build development across the region. New speculative development is currently only underway in Bristol, Cardiff and Exeter.

• The supply of available office space across the South West’s key centres has fallen by 48% since 2013 due to strong demand, the conversion of poorer quality stock to alternative uses and a lack of new development.

• During 2018 the level of take-up in key regional centres including Bristol, Bath and Exeter will remain constrained by the lack of modern flexible space now available in each market.

• Changing styles of occupation will continue to impact on take-up and office design/specification.

• We predict strong activity in the serviced/managed office sector with co-working and flexible occupation becoming increasingly popular. Many of the leading market providers are actively seeking opportunities across the region.

• There is continued strong take-up by the public sector with several large requirements active across the region.

• Some locations are witnessing a positive impact on out of town business park take-up as a result of reducing city centre supply and this trend looks set to continue in 2018.

Simon Price | T 0117 317 1084 | E [email protected]

Andrew Ridler | T 0117 317 1071 | E [email protected]

4www.alderking.com

Source: Costar

(2,2

06

) 20

5

(45

2)

42

(2,15

3)

200

(2,4

22)

225

(2,2

60

) 2

10

(1,7

76)

165

(1,0

76)

100

(59

2)

55

(1,6

15)

150

(1,13

0)

105

(1,18

4)

110

107.

3

91.1

6

54

.3

84

.7

31.1

10.1

11.6

1

84

5.4

474

.5

177.

7

62

.7

(18

3)

17

(323

) 30 (430

.5)

40

(377

) 35

(377

) 35

(26

9)

25

(26

9)

25

(26

9)

25

(30

1) 2

8

(20

5)

19

(215

) 20

0

300

200

250

150

100

50

zone A headline rent £psf

0

1,000

800

600

400

200

value of investment transactions £ms

0

50

30

40

20

10

out of town headline rent £psf

Swin

don

Glouc

este

r

Newpo

rtBat

h

Bristo

l

Cardi

ff

Bridgw

ater

Exete

r

Plymou

thTr

uro

Taun

ton

Swin

don

Glouc

este

r

Newpo

rtBat

h

Bristo

l

Cardi

ff

Bridgw

ater

Exete

r

Plymou

thTr

uro

Taun

ton

Swin

don

Glouc

este

r

Newpo

rtBat

h

Bristo

l

(Cab

otC

ircus

)Car

diff

Bridgw

ater

Exete

r

Plymou

thTr

uro

Taun

ton

Investment

Retail & Leisure

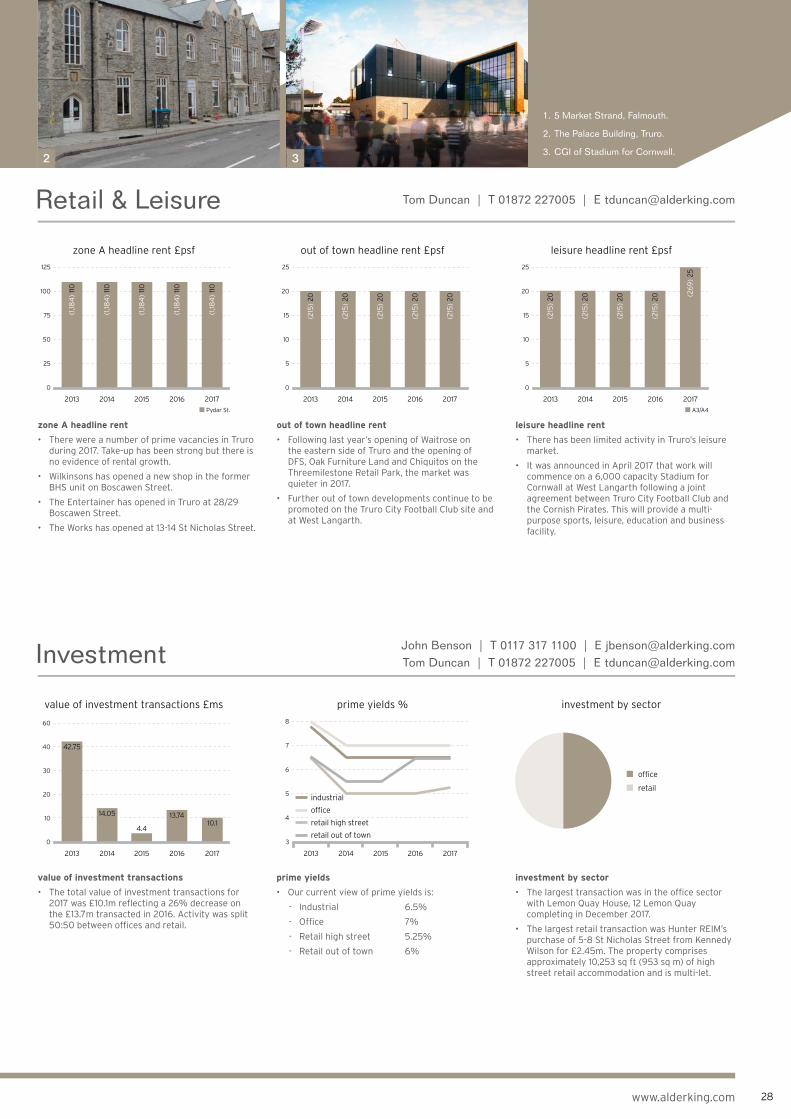

zone A headline rent

• Consumer confidence and sales volumes remained encouragingly robust throughout the majority of 2017. However 2018 is likely to see further pressure on retailers’ costs. In addition household spending will continue to be squeezed. Existing property portfolios will be rationalised through closures, relocations and right sizings.

• Online sales are growing but retailers remain committed to bricks and mortar representation.

• There is a reasonable level of occupational demand for prime locations in the larger retail centres throughout our regions. Demand in secondary locations remains subdued.

• Leisure and food and beverage uses continue to underpin traditional town centre pitches and will be of growing importance in 2018.

• Major retail-led expansions are being promoted at both Cabot Circus and The Mall at Cribbs Causeway. Further clarity on delivery timescales will emerge throughout 2018. Elsewhere new city/town centre developments are planned in Gloucester, Taunton and Swindon.

out of town headline rent

• Out of town occupational demand for well located parks remains robust. There is a growing representation from discount food, leisure and food and beverage operators. New entrants include the likes of Bunnings which is looking for new sites across our regions.

• There is an appetite from developers for new opportunities. Mero Retail Park has opened in Bath and Next are on site at Marsh Mills, Plymouth. Developments are being promoted in Truro, St Austell, Exeter and Bristol.

• Lidl and Aldi continue to dominate the foodstore sector. Others are cautiously looking at new opportunities predominantly in a convenience format. However Morrisons is on site in Abergavenny and will open a 25,000 sq ft net store in early 2018.

investment market summary

• National investment transactional volumes recorded significant growth in 2017 and the South West and South Wales region followed this trend with an estimated increase of 127% on the volume recorded in 2016.

• Market momentum was driven off the back of a robust occupational market, characterised by strong rental growth, falling supply and limited speculative development. Investment in UK commercial property during 2017 continued to defy worries about political stability, the state of the economy and uncertainty about Brexit negotiations.

• Prime yields were generally stable during 2017, although the retail market was characterised by a growing disparity between prime and secondary asset values. In some sectors, pricing reflects a slight discount on pre-referendum levels.

• The industrial sector was the standout performer of 2017. Buoyed by positive supply/demand dynamics and structural change in the sector, it was the first time that industrial volumes exceeded retail.

• Under increasing pressure to generate additional revenue streams, local authorities were particularly acquisitive throughout 2017 and this trend looks set to continue, but further informed by the outcome of the ongoing consultation over local government investments.

• Regional UK markets continue to offer higher and more attractive yields to investors than London and the south east. For Bristol, the increased appetite from investors is supported by the growing supply/demand imbalance in occupational markets.

• Looking ahead to 2018, healthy occupier market fundamentals, the relative value of real estate versus other asset classes and continued overseas demand should keep property yields at low levels in the near term. Longer term, much will depend on the pace of interest rate rises and the continued impact Brexit has upon investor sentiment.

Charles Russell-Smith | T 0117 317 1043 | E [email protected]

John Benson | T 0117 317 1100 | E [email protected]

Alder King Market Monitor 20185

Tower Road North

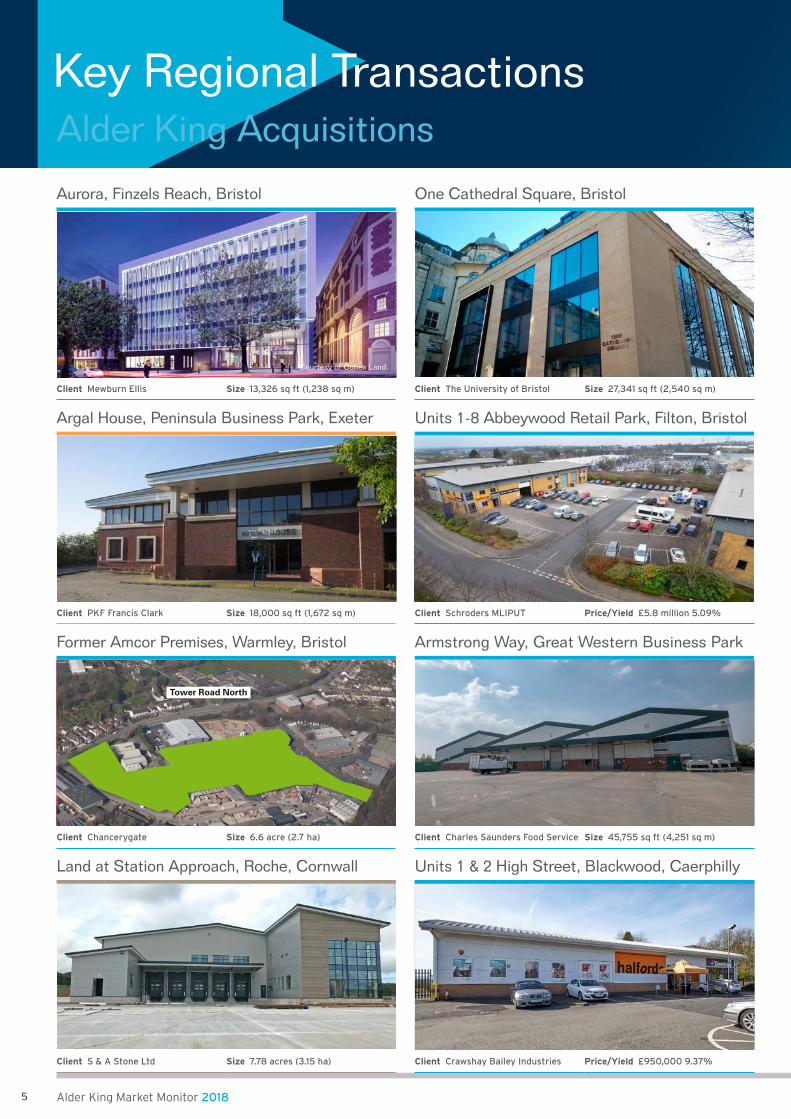

Key Regional TransactionsAlder King Acquisitions

Client TheUniversityofBristol Size 27,341sqft(2,540sqm)

Client SchrodersMLIPUT Price/Yield £5.8million5.09%

Client CharlesSaundersFoodService Size 45,755sqft(4,251sqm)

Client CrawshayBaileyIndustries Price/Yield £950,0009.37%

One Cathedral Square, Bristol

Units 1-8 Abbeywood Retail Park, Filton, Bristol

Units 1 & 2 High Street, Blackwood, Caerphilly

Client MewburnEllis Size 13,326sqft(1,238sqm)

Aurora, Finzels Reach, Bristol

Courtesy of Cubex Land.

Client PKFFrancisClark Size 18,000sqft(1,672sqm)

Argal House, Peninsula Business Park, Exeter

Client Chancerygate Size 6.6acre(2.7ha)

Client S&AStoneLtd Size 7.78acres(3.15ha)

Land at Station Approach, Roche, Cornwall

Former Amcor Premises, Warmley, Bristol Armstrong Way, Great Western Business Park

6www.alderking.com

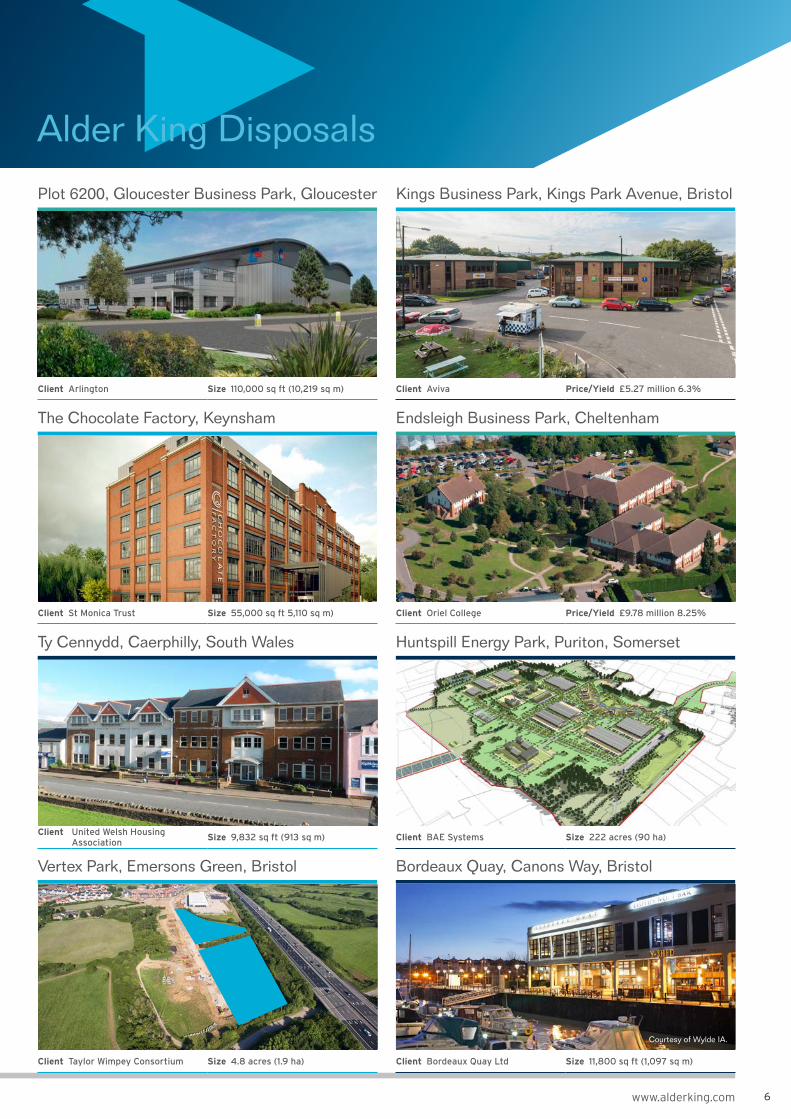

Alder King Disposals

Client Arlington Size 110,000sqft(10,219sqm) Client Aviva Price/Yield £5.27million6.3%

Client StMonicaTrust Size 55,000sqft5,110sqm) Client OrielCollege Price/Yield £9.78million8.25%

Client BAESystems Size 222acres(90ha)

Client TaylorWimpeyConsortium Size 4.8acres(1.9ha) Client BordeauxQuayLtd Size 11,800sqft(1,097sqm)

Client UnitedWelshHousingAssociation

Size 9,832sqft(913sqm)

Plot 6200, Gloucester Business Park, Gloucester Kings Business Park, Kings Park Avenue, Bristol

The Chocolate Factory, Keynsham Endsleigh Business Park, Cheltenham

Vertex Park, Emersons Green, Bristol Bordeaux Quay, Canons Way, Bristol

Ty Cennydd, Caerphilly, South Wales Huntspill Energy Park, Puriton, Somerset

Courtesy of Wylde IA.

Alder King Market Monitor 20187

(sq m)sq ftKey

demand 000s sq ft

50

0

125

2013 2014 2015 2016 2017

75

100

25

82(8)

88(8)

120(11)

90(8)

90(8)

supply 000s sq ft

100

0

250

2013 2015 2016 20172014

2013 2015 2016 20172014

200

150

50

240(22)

125(11.6)

95(8.8) 75

(7)

145(13)

headline rent £psf

20

0

40

30

2013 2015 2016 20172014

2013 2015 2016 20172014

10

(226

) 21

(226

) 21

(28

0)

26 (33

4)

31

(33

4)

31demand 000s sq ft

20

0

60

80

100

40

headline rent £psf

4

0

8

10

6

2

(81)

7.5

(91)

8.5

(91.5

0)

8.5

(94

) 8

.75

(86

) 8

supply 000s sq ft

20

0

60

80

100

40

20(2)

85(8)

20(2) 5

(0.5)

85(8)

city centre

7.5(0.7)

10(0.9)

85(7.9)

15(1.4)

15(1.4)

2013 2015 2016 20172014

Offices

Industrial

demand

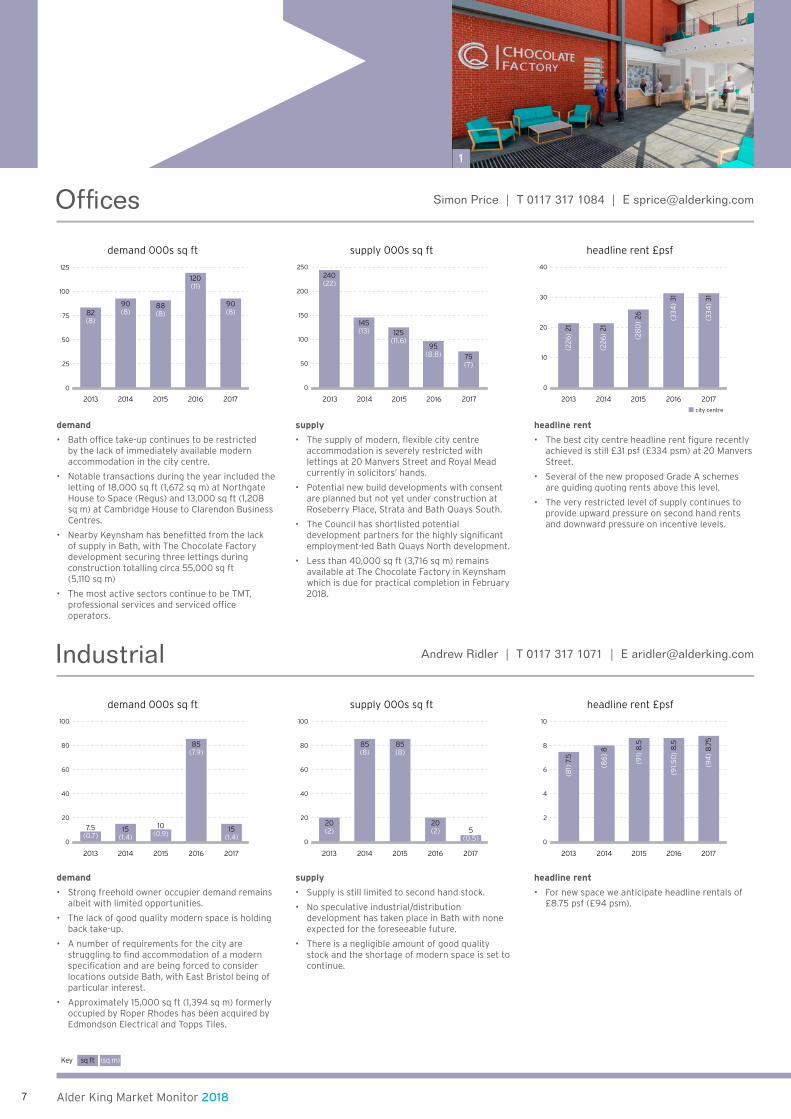

• Bath office take-up continues to be restricted by the lack of immediately available modern accommodation in the city centre.

• Notable transactions during the year included the letting of 18,000 sq ft (1,672 sq m) at Northgate House to Space (Regus) and 13,000 sq ft (1,208 sq m) at Cambridge House to Clarendon Business Centres.

• Nearby Keynsham has benefitted from the lack of supply in Bath, with The Chocolate Factory development securing three lettings during construction totalling circa 55,000 sq ft (5,110 sq m)

• The most active sectors continue to be TMT, professional services and serviced office operators.

supply

• The supply of modern, flexible city centre accommodation is severely restricted with lettings at 20 Manvers Street and Royal Mead currently in solicitors’ hands.

• Potential new build developments with consent are planned but not yet under construction at Roseberry Place, Strata and Bath Quays South.

• The Council has shortlisted potential development partners for the highly significant employment-led Bath Quays North development.

• Less than 40,000 sq ft (3,716 sq m) remains available at The Chocolate Factory in Keynsham which is due for practical completion in February 2018.

headline rent

• The best city centre headline rent figure recently achieved is still £31 psf (£334 psm) at 20 Manvers Street.

• Several of the new proposed Grade A schemes are guiding quoting rents above this level.

• The very restricted level of supply continues to provide upward pressure on second hand rents and downward pressure on incentive levels.

demand

• Strong freehold owner occupier demand remains albeit with limited opportunities.

• The lack of good quality modern space is holding back take-up.

• A number of requirements for the city are struggling to find accommodation of a modern specification and are being forced to consider locations outside Bath, with East Bristol being of particular interest.

• Approximately 15,000 sq ft (1,394 sq m) formerly occupied by Roper Rhodes has been acquired by Edmondson Electrical and Topps Tiles.

supply

• Supply is still limited to second hand stock.

• No speculative industrial/distribution development has taken place in Bath with none expected for the foreseeable future.

• There is a negligible amount of good quality stock and the shortage of modern space is set to continue.

headline rent

• For new space we anticipate headline rentals of £8.75 psf (£94 psm).

Simon Price | T 0117 317 1084 | E [email protected]

Andrew Ridler | T 0117 317 1071 | E [email protected]

1

Bath

8www.alderking.com

50

75

100

125

25

zone A headline rent £psf

150

0

250

300

2013 2015 2016 20172014

200

100

50

(2,15

3)

200

(2,15

3)

200

(2,15

3)

200

(2,15

3)

200

(2,2

06

) 20

5

out of town headline rent £psf

20

0

40

50

2013 2015 2016 20172014

30

10

(323

) 30

(323

) 30

(323

) 30

(323

) 30

(26

9)

25

leisure headline rent £psf

0

10

20

30

50

2013 2015 2016 20172014

cinema health & fitness A3/A4

40

(15

1) 14

(15

1) 14

(15

1) 14

(118

) 11

(118

) 11

(118

) 11

(376

.72

) 35

(376

.72

) 35

(376

.72

) 35

(15

1) 14

(118

) 11

(376

.72

) 35

(15

1) 14

(118

) 11

(376

.72

) 35

value of investment transactions £ms

0

2013 2015 2016 20172014

123.98

33.54

20.4

107.3

13.25

4

2

6

7

5

3

investment by sector

2013 2014 2015 2016 2017

prime yields %

office

retail

other industrial

office

retail high street

retail out of town

29%

57%

14%

Investment

Retail & Leisure

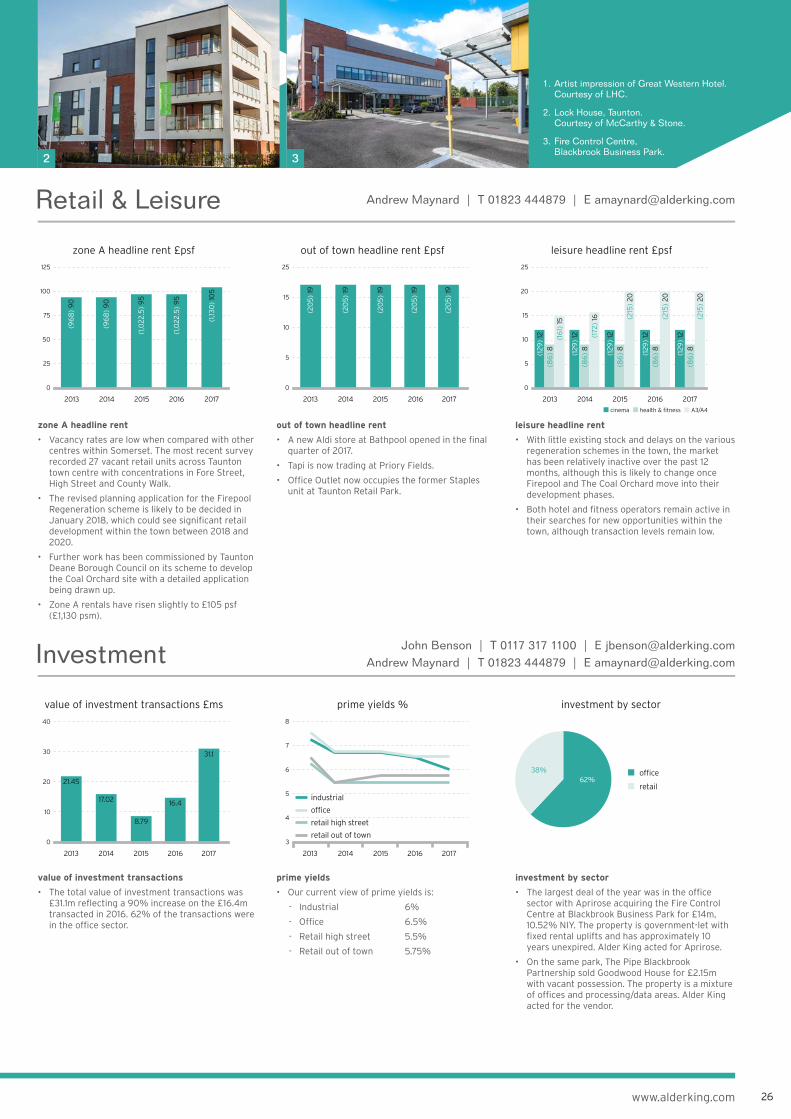

zone A headline rent

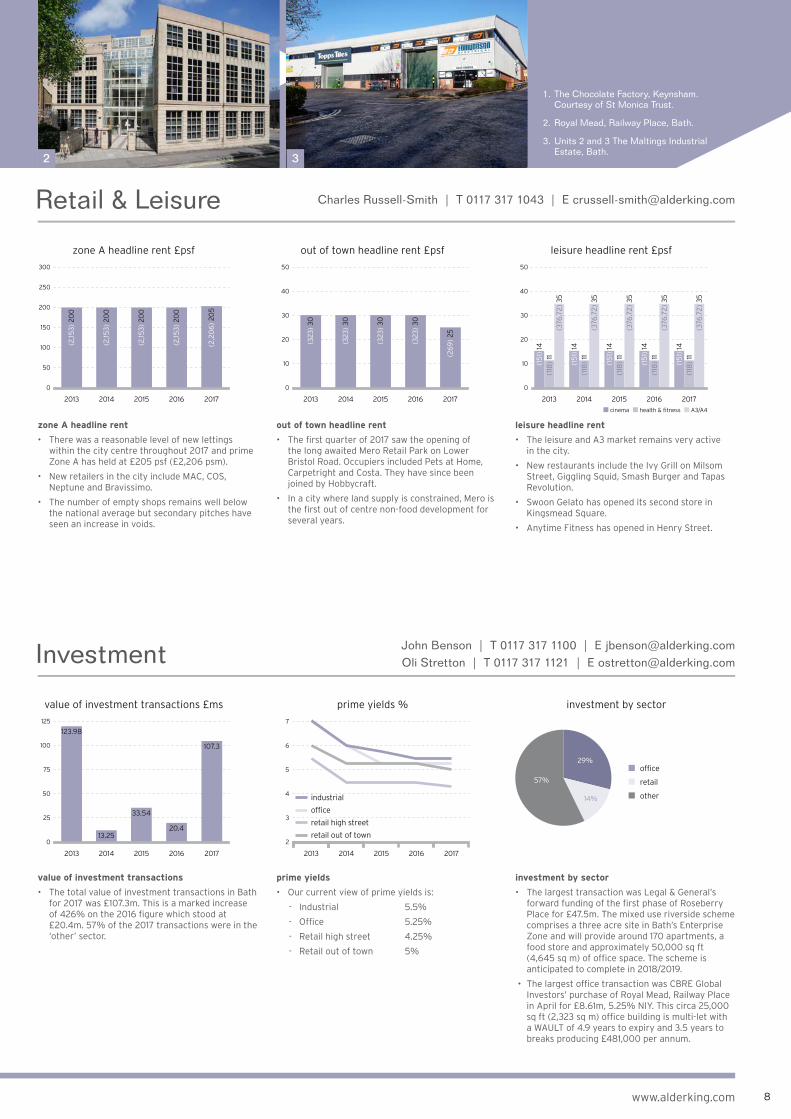

• There was a reasonable level of new lettings within the city centre throughout 2017 and prime Zone A has held at £205 psf (£2,206 psm).

• New retailers in the city include MAC, COS, Neptune and Bravissimo.

• The number of empty shops remains well below the national average but secondary pitches have seen an increase in voids.

out of town headline rent

• The first quarter of 2017 saw the opening of the long awaited Mero Retail Park on Lower Bristol Road. Occupiers included Pets at Home, Carpetright and Costa. They have since been joined by Hobbycraft.

• In a city where land supply is constrained, Mero is the first out of centre non-food development for several years.

leisure headline rent

• The leisure and A3 market remains very active in the city.

• New restaurants include the Ivy Grill on Milsom Street, Giggling Squid, Smash Burger and Tapas Revolution.

• Swoon Gelato has opened its second store in Kingsmead Square.

• Anytime Fitness has opened in Henry Street.

value of investment transactions

• The total value of investment transactions in Bath for 2017 was £107.3m. This is a marked increase of 426% on the 2016 figure which stood at £20.4m. 57% of the 2017 transactions were in the ‘other’ sector.

prime yields

• Our current view of prime yields is:

- Industrial 5.5%

- Office 5.25%

- Retail high street 4.25%

- Retail out of town 5%

investment by sector

• The largest transaction was Legal & General’s forward funding of the first phase of Roseberry Place for £47.5m. The mixed use riverside scheme comprises a three acre site in Bath’s Enterprise Zone and will provide around 170 apartments, a food store and approximately 50,000 sq ft (4,645 sq m) of office space. The scheme is anticipated to complete in 2018/2019.

• The largest office transaction was CBRE Global Investors’ purchase of Royal Mead, Railway Place in April for £8.61m, 5.25% NIY. This circa 25,000 sq ft (2,323 sq m) office building is multi-let with a WAULT of 4.9 years to expiry and 3.5 years to breaks producing £481,000 per annum.

Charles Russell-Smith | T 0117 317 1043 | E [email protected]

John Benson | T 0117 317 1100 | E [email protected] Stretton | T 0117 317 1121 | E [email protected]

1. The Chocolate Factory, Keynsham. Courtesy of St Monica Trust.

2. Royal Mead, Railway Place, Bath.

3. Units 2 and 3 The Maltings Industrial Estate, Bath.

2 3

Alder King Market Monitor 20189

(sq m)sq ftKey

2013 2015 2016 20172014 2013 2015 201720162014

out of town

headline rent £psf

0

10

15

20

5

demand 000s sq ft

20

0

60

80

40

supply 000s sq ft

40

0

80

100

60

20

85(8)

75(7)

60(5.5)55

(5)

demand 000s sq ft

200

0

400

300

100

350(32.5) 325

(30)

190(18)

225(21)

supply 000s sq ft

100

0

400

500

200

325(30) 300

(27.8)

275(25.5)

365(34)

headline rent £psf

0

8

2

4

6

2013 2015 2016 20172014

2013 2015 2016 20172014 2013 2015 2016 20172014 2013

(86

) 8

(86

) 8

(86

) 8

(81)

7.5

2015 2016 20172014

75(7)

80(7.4)

40(3.7)

65(6)

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

town centre

(86

) 8

(86

) 8

(86

) 8

(86

) 8

(16

1) 15

(16

1) 15

(15

6)

14.5

(15

9)

14.7

5

Offices

Industrial

1

BridgwaterAndrew Maynard | T 01823 444879 | E [email protected]

Andrew Maynard | T 01823 444879 | E [email protected]

demand

• The number of Hinkley Point C enquiries rose during the second half of 2017. However overall transaction levels reduced with fewer large transactions than in 2016.

• Leasehold demand strengthened in 2017 and represents a larger percentage than freehold, a reversal on 2016.

• Clustering of demand is evident in the sub 5,000 sq ft (464.5 sq m) size range as in previous years but there is increased demand in the 10,000 to 20,000 sq ft (929 to 1,858 sq m) size range.

supply

• With relatively low levels of new stock entering the market, we have seen a reduction of around 15% in availability over the past 12 month period, with few new build starts and less speculative development than in recent years.

• With limited speculative building on the cards, availability may continue to fall in 2018.

• The start of 2018 will see an increase in the number of design and build projects within the town, with occupiers unable to find suitable existing premises making the decision to go down the new build route.

headline rent

• Headline rents have been consistent over the past few years but land values and capital values continue to increase. This may start to impact on rents over coming months in line with similar conditions along the M5 corridor to the north of the town, where rental growth has followed several years of capital growth.

demand

• Take-up fell throughout 2017 due in large part to a lack of supply, especially for good quality out of town offices.

• Demand from Hinkley related occupiers continues to be a constant in the market, although generally requirements from supply chain companies involved in the project are for sub 3,000 sq ft (279 sq m). These occupiers are also often looking for shorter lease terms in line with the timescales for specific work contracts.

• The popularity of service/managed accommodation continues, with very little available within both The Exchange on Express Park and the Somerset Energy Innovation Centre on Woodlands Business Park.

supply

• The levels of vacant space on the most popular out of town business parks have decreased further, with overall supply down by around 50% compared with the end of 2016.

• Potential new schemes will introduce much needed new build accommodation into the market towards the end of 2018 and 2019, with a further phase of the Somerset Energy Innovation Centre and opportunities at Bridgwater Gateway.

• As with the industrial market, occupiers are now increasingly looking at new build options given the lack of supply of suitable premises.

headline rent

• Headline rental levels remain consistent for both out of town and town centre accommodation.

• The baseline rental levels for managed office space increased in 2017 especially in the 1,000 sq ft (93 sq m) size range.

10www.alderking.com

zone A headline rent £psf

30

0

50

2013 2015 2016 20172014

40

20

10

(474

) 4

4

(45

2)

42

(45

2)

42

(430

) 4

0

out of town headline rent £psf

10

0

20

2013 2015 2016 20172014

15

5

(18

3)

17

(18

3)

17

(18

3)

17

(18

3)

17

leisure headline rent £psf

0

5

10

15

20

2013 2015 2016 20172014

cinema health & fitness A3/A4

(129

) 12

(129

) 12

(129

) 12

(129

) 12

(81)

7.5

(81)

7.5

(81)

7.5

(86

) 8

(16

1) 15

(16

1) 15

(16

1) 15

(16

1) 15

value of investment transactions £ms

20

0

40

2013 2015 2016 20172014

30

10

3.59.15

11.61

31.35

investment by sectorprime yields %

6

4

8

9

7

5

2013 2014 2015 2016 2017

industrial office retail high street retail out of town

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

Not

pre

viou

sly

repo

rted

industrial

office

retail

other

86%

5%8%

2%

Investment

Retail & Leisure

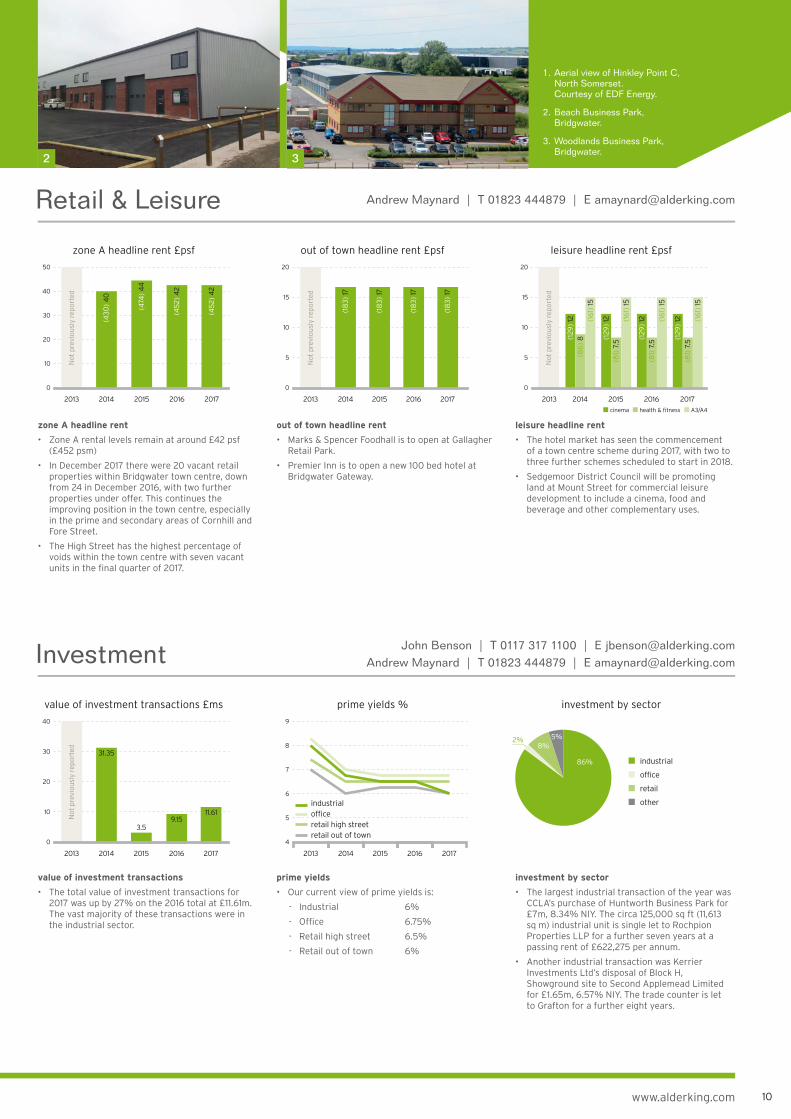

1. Aerial view of Hinkley Point C, North Somerset. Courtesy of EDF Energy.

2. Beach Business Park, Bridgwater.

3. Woodlands Business Park, Bridgwater.

2 3

Andrew Maynard | T 01823 444879 | E [email protected]

John Benson | T 0117 317 1100 | E [email protected] Maynard | T 01823 444879 | E [email protected]

value of investment transactions

• The total value of investment transactions for 2017 was up by 27% on the 2016 total at £11.61m. The vast majority of these transactions were in the industrial sector.

prime yields

• Our current view of prime yields is:

- Industrial 6%

- Office 6.75%

- Retail high street 6.5%

- Retail out of town 6%

investment by sector

• The largest industrial transaction of the year was CCLA’s purchase of Huntworth Business Park for £7m, 8.34% NIY. The circa 125,000 sq ft (11,613 sq m) industrial unit is single let to Rochpion Properties LLP for a further seven years at a passing rent of £622,275 per annum.

• Another industrial transaction was Kerrier Investments Ltd’s disposal of Block H, Showground site to Second Applemead Limited for £1.65m, 6.57% NIY. The trade counter is let to Grafton for a further eight years.

zone A headline rent

• Zone A rental levels remain at around £42 psf (£452 psm)

• In December 2017 there were 20 vacant retail properties within Bridgwater town centre, down from 24 in December 2016, with two further properties under offer. This continues the improving position in the town centre, especially in the prime and secondary areas of Cornhill and Fore Street.

• The High Street has the highest percentage of voids within the town centre with seven vacant units in the final quarter of 2017.

out of town headline rent

• Marks & Spencer Foodhall is to open at Gallagher Retail Park.

• Premier Inn is to open a new 100 bed hotel at Bridgwater Gateway.

leisure headline rent

• The hotel market has seen the commencement of a town centre scheme during 2017, with two to three further schemes scheduled to start in 2018.

• Sedgemoor District Council will be promoting land at Mount Street for commercial leisure development to include a cinema, food and beverage and other complementary uses.

Alder King Market Monitor 201811

(sq m)sq ftKey

2013 2015 2016 20172014

demand 000s sq ft

400

0

800

1,000

1,200

1,400

2013 2015 2016 20172014

600

200

735(68)

783(73)

1,091(101)

1,039(96)

1,250(116)

supply 000s sq ft

1,000

0

2,000

2,500

3,000

1,500

500

2,380(221)

1,250(116)

850(79) 700

(65)

1,650(153)

headline rent £psf

30

0

40

2014 2015 2016 20172013

10

20

(30

7)

28.5

(30

7)

28.5

(30

7)

28.5

(35

0)

32.5

(30

7)

28.5

(231

) 21

.5

(231

) 21

.5

(231

) 21

.5

(237

) 22

(231

) 21

.5

city centre out of town

demand 000s sq ft

2,000

0

4,000

5,000

2013 2015 2016 20172014

3,000

1,000

2,950(274)

4,500(418)

3,000(278)2,600

(242)2,200(204)

supply 000s sq ft

0

500

1,000

1,500

2,000

3,000

2013 2015 2016 20172014

2,500

headline rent £psf

0

8

10

2013 2015 2016 20172014

6

4

2

(81)

7.5

(86

) 8

(86

) 8

.5

(94

) 8

.75

(83

) 7.

75

2,750(255)

1,250(116)

1,250(116)

1,500(140)

1,750(163)

Offices

Industrial

1

Bristol

demand

• Take-up in 2017 totalled 3 million sq ft (27,870 sq m).

• Three sizeable transactions impacted on take-up with DHL and Amazon acquiring 160,000 sq ft (14,864 sq m) and 1.25 million sq ft (116,128 sq m) on Severnside, and Chancerygate purchasing the 156,000 sq ft (14,493 sq m) former Alcan site at Warmley.

• There is a negligible amount of good quality stock and shortages of modern space have impacted on take-up.

• Activity levels are constant and it will be interesting to see what impact increased manufacturing productivity has on take-up over the next 12 months.

supply

• Availability remains at historically low levels with a large proportion comprising obsolete space for which there is limited demand.

• Speculative development is underway at Access 18 and Rockhaven in Avonmouth and at Horizon 38, Filton. Further schemes are planned by Chancerygate at Vertex Park in Emersons Green and at Warmley Business Park. At Severnside Richardson Barbury is planning to commission its 33 acre “mid box” scheme in early 2018. In Weston-super-Mare KMW will soon commence the third phase of Belvedere Court.

• There is strong demand from owner occupiers for freehold space but few opportunities.

headline rent

• With limited new space immediately available, we anticipate that rentals of circa £8.75 psf (£94.15 psm) will be achieved for accommodation below 10,000 sq ft (929 sq m).

• Rents for modern and mid-range buildings have increased to £6.50 - £7.50 psf (£70 - £81 psm). Good quality second hand buildings below 5,000 sq ft (464.5 sq m) are commanding rents of around £7 - £9.50 psf (£75 - £102 psm).

• With the reduced levels of good quality available stock, rental incentives for prime space have reduced significantly with lease durations extending.

demand

• Bristol’s office market recorded another strong year of take-up. Whilst the city centre performed in line with the five year average at circa 615,000 sq ft (57,135 sq m), the out of town market exceeded the five year average performance by circa 33%.

• Notable transactions in the city centre saw the University of Bristol purchase 31,785 sq ft (2,953 sq m) at Augustine’s Courtyard and agree a letting on 27,341 sq ft (2,540 sq m) at Cathedral Square. Out of town Babcock entered into a pre-let on 85,790 sq ft (7,970 sq m) at Bristol Business Park.

• The most active sectors in the market are currently TMT, financial and professional services and the public sector.

supply

• There is now a severe shortage of new or newly refurbished Grade A accommodation in both the city centre and out of town markets.

• The only new speculative Grade A building under construction is Aurora at Finzels Reach where three floors have already been pre-let, with strong interest in the remaining floors.

• Recent city centre refurbishments at One Brunswick Square, Augustine’s Courtyard and Cathedral Square all secured occupiers quickly after practical completion.

• In north Bristol several refurbishments are underway at Aztec West and are already seeing strong occupier interest.

headline rent

• In the city centre, after many years of limited growth, top headline rents finally broke through £30 psf (£322 psm) and ended the year at £32.50 psf (£350 psm).

• The top headline rent at £32.50 psf (£350psm) was achieved at the comprehensively remodelled Cathedral Square development.

• Quoting rents for good quality second hand city centre space are now as high as £28.50 psf (£350 psm).

• The highest out of town headline rent is £22 psf (£250 psm) but there are good prospects for rental growth in North Bristol with quoting levels up to £23 psf (£248 psm) on the best stock.

Simon Price | T 0117 317 1084 | E [email protected]

Andrew Ridler | T 0117 317 1071 | E [email protected]

12www.alderking.com

400

800

1,000

600

200

11%

44%21%

24%

zone A headline rent £psf

0

50

150

250

350

2013 2015 2016 20172014

Broadmead The Mall Cabot Circus

100

200

300

(1,8

84

) 17

4

(1,8

30)

170

(1,8

30)

170

(1,8

30)

170

(1,8

30)

170

(3,2

29)

300

(3,2

29)

300

(3,2

29)

300

(3,2

29)

300

(3,2

29)

300

out of town headline rent £psf

20

0

40

2013 2015 2016 20172014

30

10

(323

) 30

(323

) 30

(323

) 30

(323

) 30

(323

) 30

leisure headline rent £psf

0

5

10

15

35

30

2013 2015 2016 20172014

cinema health & fitness A3/A4

20

25

(16

1.45

) 15

(16

1.45

) 15

(16

1.45

) 15

(16

1.45

) 15

(16

1.45

) 15

(129

.16)

12

(129

.16)

12

(129

.16)

12

(129

.16)

12

(129

.16)

12

(322

.91)

30

(322

.91)

30

(34

9)

32.5

(34

9)

32.5

(377

) 35

value of investment transactions £ms

0

2013 2015 2016 20172014

319

59

5.6

475

.3

84

5.4

55

7.4

prime yields %

4

2

6

7

2014 2015 2016 20172013

5

3

investment by sector

(2,15

3)

200

(2,15

2.7

0)

200

(2,15

3)

200

(2,15

3)

200

(2,15

3)

200

office

industrial

retail

other industrial

office

retail high street

retail out of town

Investment

Retail & Leisure

1. 2 Glass Wharf, Temple Quarter. Courtesy of Salmon Harvester Properties/NFUM.

2. CGI of Unit 5-11 Vertex Park. Courtesy of Chancerygate.

3. Bordeaux Quay, Canons Way, Bristol.

2 3

zone A headline rent

• Proposals for major new development at Callowhill Court, Broadmead of circa 1.1 million sq ft (102,193 sq m) and The Mall at Cribbs Causeway of circa 700,000 sq ft (65,000 sq m) continue to be progressed through the planning process. The Appeal Inquiry into the latter ended in October 2017 and a decision is expected in the first quarter of 2018. An outline application for Callowhill Court will be taken back to committee shortly.

• In early 2018 Metro Bank will open in the former BHS store and TK Maxx in the former Peacocks on Merchant Street.

out of town headline rent

• There was limited activity in the out of town sector in 2017. Prime rents remain unchanged.

• The former B&Q at Filton was subdivided and let to the Range, Poundstretcher and DW Sports Fitness.

• Iceland’s Food Warehouse opened in a 9,700 sq ft (901 sq m) store at South Bristol Retail Park.

leisure headline rent

• The food and beverage sector continues to thrive across the city.

• Following the success of CARGO at Wapping Wharf, a second phase opened in summer 2017. Occupiers include Salt n’ Malt, Gambas and Sputino.

• Cabot Circus enhanced the offer at Quakers Friars with the arrival of L’Osteria, Cote Brasserie and Department of Coffee.

• The Mall also bolstered its provision with GBK and Tortilla.

value of investment transactions

• The total value of investment transactions was £845.4m, up by 78% on the 2016 total of £475.3m. 44% of the deals were in the office sector.

• In Bristol’s CBD, almost half of all prime office stock (by number of buildings) has been traded since 2013. Demand for Grade A investment opportunities remains high as Bristol recorded the strongest average rental growth of the Big Six regional centres in the 12 months to Q3 2017.

prime yields

• Our current view of prime yields is:

- Industrial 5.25%

- Office 5.25%

- Retail high street 4.5%

- Retail out of town 5%

investment by sector

• The largest investment transaction was in the office sector. In November, Topland sold 10 Canons Way, Harbourside to a South Korean investor. The landmark office building, overlooking Bristol’s floating harbour, totals circa 177,000 sq ft (16,443 sq m) and is single let to Scottish Widows Limited until November 2032 with a passing rent of circa £5.04m per annum. The purchase price was £95.5m, 4.95% NIY.

• In the industrial sector, the largest deal was NFU Mutual’s sale of Tesco Distribution Centre, Avonmouth to a South Korean investor. The circa 555,000 sq ft (5,110 sq m) distribution centre is let to Tesco plc with 12.5 years unexpired. The purchase price was £71.4m, 5.10% NIY.

Charles Russell-Smith | T 0117 317 1043 | E [email protected]

John Benson | T 0117 317 1100 | E [email protected] Stretton | T 0117 317 1121 | E [email protected]

Alder King Market Monitor 201813

(sq m)sq ftKey

demand 000s sq ft

0

400

600

800

1,000

2013 2015 2016 20172014

200300(28)

617(57)

685.6(63)

704(65)

531(49)

supply 000s sq ft

400

0

800

1,000

2013 2015 2016 20172014

600

200

1,000(93)

900(84)

788(73) 707

(66)

1,000(93)

headline rent £psf

0

5

10

15

20

25

2013 2015 2016 20172014

city centre out of town

(237

) 22

(237

) 22 (26

9)

25

(26

9)

25

(237

) 22

(129

) 12

(15

0.6

) 14

(15

0.6

) 14

(15

6)

14.5

(129

) 12

demand 000s sq ft

0

600

800

1,000

2013 2015 2016 20172014

200

400

572(53)

402(37)

499(46)

880(82)

763(71)

supply 000s sq ft

0

500

250

1,000

750

1,250

1,500

2013 2015 2016 20172014

1,368(127)

909(84) 839

(78)

515(48)

1,094(102)

headline rent £psf

0

2

3

4

5

6

2013 2015 2016 20172014

1

5(54)

5(54)

5.25(56.5)

5.5(59)5

(54)

Offices

Industrial

demand

• Take-up remains positive, comfortably exceeding the five year average for the fourth consecutive year.

• Three transactions account for over 50% of take-up and include the GPU pre-letting of 269,228 sq ft (25,012 sq m) at 6 Central Square, Cardiff University taking 44,588 sq ft (4,142 sq m) at 2 Central Square and Network Rail taking 31,519 sq ft (2,928 sq m) at St Patrick’s House.

• City centre take-up accounted for 85%, of which 77% was for Grade A accommodation.

supply

• City centre supply has reduced to its lowest level for 15 years.

• Student development continues to accentuate the reduction but we expect decreased demand going forward with a number of sites under construction and others in for planning consent.

• Significant new developments to be completed in 2018 include both 3 and 4 Capital Quarter and the new BBC headquarters. With circa 111,000 sq ft (10,312 sq m) coming to market at Hodge House, we expect supply to increase in 2018.

• Grade A stock currently stands at approximately 127,000 sq ft (13,935 sq m).

headline rent

• Headline rents remain stable and are forecast to remain at the same level during 2018.

• New development around Central Square will be the driver for headline rental growth.

• Small increases in out of town rents are expected with decreased availability at junctions 30 and 32 of the M4 motorway.

demand

• Take-up has increased by 43%, notably through supermarket chain Aldi and film production company Bad Wolf taking 400,000 sq ft (37,161 sq m) at Wentloog and 253,000 sq ft (23,505 sq m) at Trident Park, respectively.

• Other notable transactions include SA Brain & Co’s purchase of Courtney House, 31,000 sq ft (2,880 sq m) located on 1.5 acres.

• Freehold properties, especially with yards, remain in high demand and are driving much needed price growth.

• We have seen competition for better quality stock intensify, with owner occupiers paying above market levels to satisfy requirements.

supply

• Supply has fallen by 39% in the last 12 months.

• In the absence of new development, refurbishment projects are being rewarded including St Catherine’s Park on Newport Road and various buildings along Hadfield Road.

• There is now a real shortage of available stock and we expect imminent increases in rents and prices.

• Positive progress on the M4 relief road, together with scrapping of the Seven Bridge tolls, is expected to further increase demand and new development is required even if just to satisfy existing requirements.

headline rent

• Headline rents have now increased, evident by lettings to Merrylees Construction taking 3,000 sq ft (279 sq m) at Lamby Way and Sedna Lighting taking 3,550 sq ft (330 sq m) at Capital Business Park at £5.50 psf (£59.20 psm).

• With a sustained lack of Grade A options, we envisage a continued increase in rental levels and reducing incentives.

Owen Young | T 029 2038 1996 | E [email protected]

Owen Young | T 029 2038 1996 | E [email protected]

1

Cardiff

14www.alderking.com

200

400

500

300

100

zone A headline rent £psf

0

100

150

200

250

300

2013 2015 2016 20172014

50

out of town headline rent £psf

25

0

35

40

2013 2015 2016 20172014

30

20

15

10

5

(323

) 30

(322

.9)

30 (430

.5)

40

(430

.5)

40

(323

) 30

leisure headline rent £psf

0

10

20

50

2013 2016 201720152014

cinema health & fitness A3/A4

30

40

(14

0)

13

(14

0)

13

(14

0)

13

(14

0)

13

(14

0)

13

(118

) 11

(118

) 11

(118

) 11

(431

) 4

0

(431

) 4

0

(430

.56

) 4

0

(430

.5)

40

(431

) 4

0

value of investment transactions £ms

0

2013 2015 2016 20172014

131.33188.2 169.1

474.5

209

prime yields %

5

3

7

8

2014 2015 2016 2017

6

4

2013

investment by sector

26%

7%

62%

7%

(2,

422

) 22

5

(2,

421

.89

) 22

5

(2,

421

.9)

225

(2,

422

) 22

5

(2,

422

) 22

5

office

industrial

retail

other industrial office retail high street retail out of town

(118

.4)

11

(118

) 11

Investment

Retail & Leisure

zone A headline rent

• St David’s Shopping Centre had another successful year in 2017, securing over 40,000 sq ft (3,716 sq m) of new lettings to occupiers including Virgin Holidays, Caffé Nero, CK Underwear, Oliver Bonas and Jacamo.

• Canadian coffee chain Tim Hortons opened its first shop on Queen Street, with a second currently being fitted out at the former Artigiano site on Working Street.

• Lunch and desserts operator Thirty Nine acquired its first site in Cardiff, with outdoor clothing retailer Regatta taking the former Waitrose unit, both on Queen Street.

out of town headline rent

• There is limited availability within any of the city’s retail parks as owners seek to proactively manage and increase floorspace via new development.

• B&Q and Curry’s/PC World have downsized their property holdings, but closures such as Hadfield Road have not impacted as a result of replacement lettings to Selco and Jump.

leisure headline rent

• The city centre continues to expand its A3 and A4 use offering with Milk & Sugar’s new eatery Llaeth & Siwgar on The Hayes, Gareth Bale’s premium sports bar Elevens opening on Castle Street and the recently refurbished Philharmonic re-opening on St Mary’s Street.

• Budget hotel demand remains strong with easyHotel acquiring Cromwell House on Fitzalan Place and Premier Inn developing the former York Hotel on Custom House Street.

• Hotel Indigo has recently opened at Dominions House on Queen Street, with work undertaken to enhance the original Dominions Arcade beneath to include a dedicated entrance and lift to the Marco Pierre White restaurant on the top floor.

value of investment transactions

• The total value of investment transactions for 2017 is up 180% on the 2016 figure at £474.5m. This is the highest volume of transactions for over five years. 62% of these transactions were in the office sector.

prime yields

• Our current view of prime yields is:

- Industrial 6%

- Office 5.5%

- Retail high street 4.5%

- Retail out of town 5%

investment by sector

• The largest office transaction was Legal & General’s forward commitment of Six Central Square from Rightacres. The circa 266,000 sq ft (24,712 sq m) office building is currently under development and has been pre-let in its entirety to the Government Property Unit (GPU) on a 25 year lease. The transaction completed at £117.2m, 3.5% NIY.

• In the retail sector, La Salle IM purchased The Morgan Quarter from Helical plc for £55m, 5.9% NIY and a reversionary yield of 6.9%. The property is multi-let to tenants including Urban Outfitters, Dr Martens, Moss Bros alongside office space.

Owen Young | T 029 2038 1996 | E [email protected]

John Benson | T 0117 317 1100 | E [email protected] James Nicholas | T 029 2038 1994 | E [email protected]

1. 3 Capital Quarter, Cardiff.

2. Bad Wolf, Trident Park, Cardiff.

3. Tim Hortons Café & Bake Shop, Cardiff.

2 3

Alder King Market Monitor 201815

(sq m)sq ftKey

demand 000s sq ft

50

0

100

125

150

175

200

2013 2015 2016 20172014

75

25

175(16)

200(18.5)

167(15.5)150

(14)135(12)

supply 000s sq ft

100

0

200

250

300

400

450

2013 2015 2016 20172014

150

50

350

410(38)

300(28)

197(18) 179

(16.6)

325(30)

headline rent £psf

0

10

15

20

2013 2015 2016 20172014

5

city centre out of town

(178

) 16

.5

(172

) 16

(16

7)

15.5

(18

8)

17.5

(19

9)

18.5

(210

) 19

.5

(18

8)

17.5

(18

8)

17.5

(18

8)

17.5

(18

8)

17.5

demand 000s sq ft

200

0

400

500

600

800

700

2013 2015 2016 20172014

300

100

310(29) 255

(24)

758(70)

355(33)

330(31)

supply 000s sq ft

150

0

250

300

2013 2015 2016 20172014

200

50

100

300(28)

210(19.5) 195

(18) 165(15)

250(23)

headline rent £psf

3

0

5

8

2013 2015 2016 20172014

4

2

1

6

7

(75

.34

) 7 (8

6)

8

(86

) 8

(86

) 8

(86

) 8

Offices

Industrial

1

ExeterNoel Stevens | T 01392 353093 | E [email protected]

Noel Stevens | T 01392 353093 | E [email protected]

demand

• New build take-up was positive with a new headline rent set following Oneserve taking the top floor of 2 Enterprise Square, SkyPark.

• Emperor House at Exeter Business Park completed in 2017 with LV= taking occupation in December. With an EPC of A-14, it is one of the most energy efficient buildings in the UK.

• Existing buildings traded very well, with occupiers preferring standalone premises such as Argal House, Peninsula Park let to PKF Francis Clark and Jack Walker House at Exeter Airport purchased by Wain Homes.

• A number of 1,500 – 5,000 sq ft (139 – 464 sq m) requirements remain unsatisfied.

supply

• Supply of Grade A stock increased with the completion of 2 Enterprise Square, bringing forward 11,364 sq ft (1,056 sq m) on the ground and first floors.

• Conversion to alternative use continues to diminish supply. The redevelopment of Renslade House has removed 60,000 sq ft (5,574 sq m) while the 35,000 sq ft (3,252 sq m) Quintana Gate has been demolished to make way for a student scheme.

• An additional 66,000 sq ft (6,132 sq m) of new build is consented at Exeter Business Park across two sites. We will also see the completion of major refurbishment projects bringing secondary space to market in 2018.

headline rent

• Headline rents on new build premises will push beyond £19.50 psf (£210 psm) with the next round of deals where £20 psf + (£215 psm) will be required to match the cost of construction.

• Rents on existing space continue to grow as the imbalance between supply and demand continues. This is also putting pressure on incentives.

demand

• Trade counter and developer interest in key industrial markets is extremely strong as shown by the Wheatons, Marsh Barton site sale which completed in December 2017. The 4.2 acre site attracted bids from occupiers and developers.

• Demand from major distributors remains unsatisfied with a number of requirements of 50,000 sq ft + (4,645 sq m) waiting in the wings for suitable sites.

• Well-configured units of all sizes remain popular, particularly freeholds to meet continued demand from the owner occupier sector.

supply

• The forthcoming 1.1 million sq ft (92,903 sq m) of space at Exeter Gateway will add to the availability of development land and meet demand from distributors.

• Exeter is yet to see speculative development on any scale. Where developers are progressing we are seeing strong interest.

• There is an identified lack of consented industrial land around the Sowton Industrial Estate at Junction 29/30 of the M5. Strong demand from trade counter operators remains unsatisfied.

headline rent

• Headline rents remain unchanged although there is growing pressure on rents, driven by construction cost inflation for new build.

• In the secondary market the lack of supply is resulting in increased rents and a drop in incentives.

16www.alderking.com

44%

25%

31%100

150

200

250

50

leisure headline rent £psf

0

10

20

30

50

2013 2015 2016 20172014

40

(18

3)

17

(18

3)

17

(18

3)

17

(18

3)

17

(14

0)

13

(10

8)

10

(10

8)

10

(118

.4)

11

(129

) 12

(129

) 12

(45

2)

42

(45

2)

42

(45

2)

42

(430

.56

) 4

0

(431

) 4

0

value of investment transactions £ms

0

2013 2015 2016 20172014

52.85

18.6 22.7

177.7

190

prime yields %

5

3

7

8

2014 2015 2016 2017

6

4

2013

out of town headline rent £psf

10

0

20

35

2013 2015 2016 20172014

15

5

25

30

(30

1) 2

8 (377

) 35

(377

) 35

(377

) 35

(323

) 30

zone A headline rent £psf

150

0

250

2013 2015 2016 20172014

200

100

50

(2,15

3)

200

(2,2

60

) 21

0

(2,2

60

) 21

0

(2,2

60

) 21

0

(2,15

3)

200

High St.

investment by sector

cinema health & fitness A3/A4

office

retail

other industrial office retail high street retail out of town

Investment

Retail & Leisure

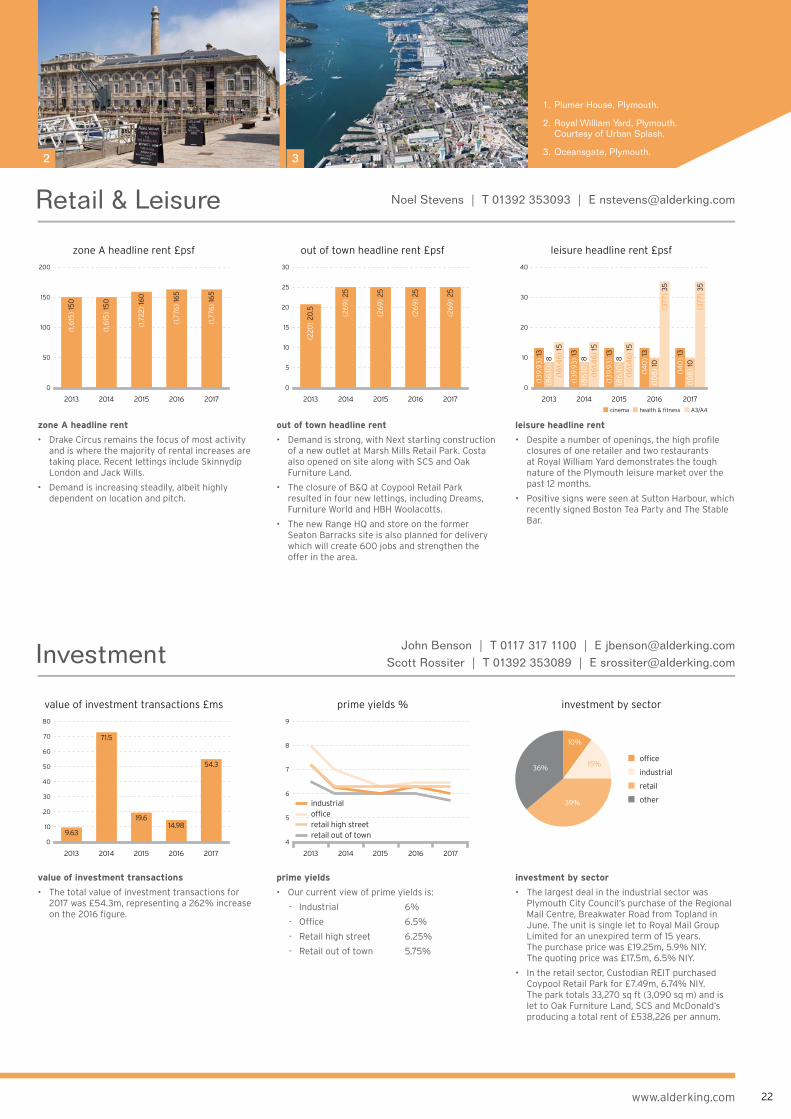

1. Emperor House, Exeter Business Park.

2. Argal House, Peninsula Business Park.

3. Matford Park, Exeter.2 3

Noel Stevens | T 01392 353093 | E [email protected]

John Benson | T 0117 317 1100 | E [email protected] Scott Rossiter | T 01392 353089 | E [email protected]

zone A headline rent

• Existing centres likes Princesshay and the Guildhall continue to be popular with shoppers and retailers, with strong interest in smaller scale units at Queens Street Dining.

• The proposed Bus Station redevelopment has been put on hold following the withdrawal of The Crown Estate. This will be seen as a positive by the existing centres.

out of town headline rent

• The construction of IKEA is changing the face of Exeter. Due to open in April 2018, the 300,000 sq ft (27,871 sq m) store, which sits alongside Sandy Park, will be a major boost to the city.

• To the east of Exeter, Cranbrook town centre has come to market. Alder King has been appointed as agent.

leisure headline rent

• Strong demand continues to come from the fitness sector, with Pure Gym opening at Stone Lane Retail Park.

• The trampoline and alternative leisure markets remain strong although, with a lack of industrial space, finding sites is proving difficult along with complexities in achieving change of use.

value of investment transactions

• The total value of investment transactions for 2017 was £177.7m, representing a 680% increase on the 2016 figure which stood at just £22.7m. 44% of these transactions were in the office sector.

prime yields

• Our current view of prime yields is:

- Industrial 5.5%

- Office 6%

- Retail high street 4.5%

- Retail out of town 5.25%

investment by sector

• The largest office sector transaction was British Steel’s purchase of Peninsula and Fernworthy House, Peninsula Park from an overseas investor. The circa 94,000 sq ft (8,733 sq m) single let office building let to South West Water Ltd on a new 30 year lease, sold for £43.87m, 3.3% NIY. The five yearly rent reviews are in line with RPI, subject to a cap and collar of 1% and 4%.

• The largest deal in the retail sector was Legal & General’s purchase of Exebridge Retail Park for £33.27m, 6.19% NIY. The park comprises a terrace of four units totalling 67,810 sq ft (6,300 sq m) and is multi-let, offering a WAULT of circa 7.5 years.

Alder King Market Monitor 201817

(sq m)sq ftKey

demand 000s sq ft

25

0

75

100

125

150

175

2013 2015 2016 20172014

50

120(11)

145(13.5)

150(14)

150(14)

145(13.5)

supply 000s sq ft

50

0

100

150

200

2013 2015 2016 20172014

120(11)

140(13)

180(17)

140(13)

150(14)

headline rent £psf

5

0

15

20

25

2013 2015 2016 20172014

10

(123

.78

) 11

.5

(123

.78

) 11

.5

(123

.78

) 11

.5

(126

.48

) 11

.75

(126

.48

) 11

.75

(18

8.3

6)

17.5

(19

9)

18.5

(19

9)

18.5

(20

4.5

) 19

(215

) 20

city centre out of town

demand 000s sq ft

300

0

500

600

700

800

2013 2015 2016 20172014

400

100

200

400(37)

400(37)

700(65)

500(46)

300(28)

headline rent £psf

2

0

4

5

6

7

2013 2015 2016 20172014

3

1

(65

) 6

(67

) 6

.25

(70

) 6

.5

(72

.65

) 6

.75

(65

) 6

supply 000s sq ft

300

0

500

600

700

2013 2015 2016 20172014

400

100

200

625(30)

400(37)

250(23)

250(23)

350(33)

Offices

Industrial

1

GloucesterAdrian Rowley | T 01452 627133 | E [email protected]

Adrian Rowley | T 01452 627133 | E [email protected]

demand

• Take-up in 2017 totalled 145,000 sq ft (13,470 sq m), in line with the previous five years.

• Significant transactions included the letting of 12,500 sq ft (1,161 sq m) in Building 1, The Office Campus at Barnwood to River Marketing, the sale of the 37,000 sq ft (3,437 sq m) Building 1, The Office Campus and the 6,000 sq ft (557 sq m) letting of 1260 Lansdowne Court, Gloucester Business Park to Lockheed Martin.

supply

• The supply of available stock in Gloucester is currently 140,000 sq ft (13,000 sq m).

• The long term trend of reducing supply continues in both the prime and secondary sectors, the latter being fuelled by ongoing demand for office to residential conversion opportunities in the city centre.

• Interest in new build space continues as occupiers are often unable to source suitable existing buildings.

headline rent

• The headline rent for Grade A out of town office space is currently £20 psf (£215 psm).

• For secondary space, rents have now risen to £14-15 psf (£150-161 psm).

• Headline rents for city centre space remain at £11.75 psf (£126 psm).

demand

• Take-up in 2017 totalled 500,000 sq ft (46,450 sq m), continuing the strong performance of the industrial sector.

• The most significant transactions included an agreement for a new 110,000 sq ft (10,219 sq m) manufacturing facility, now under construction, for TBS Engineering at Gloucester Business Park and a 41,000 sq ft (3,809 sq m) speculatively built warehouse at Gateway 12 is under offer.

supply

• Supply is currently 350,000 sq ft (32,515 sq m), boosted by new speculative development.

• The shortage of supply is prevalent across all size ranges and grades of space.

• New build speculative activity is good, with St Modwen continuing its development programme at Gateway 12 to provide an additional 115,000 sq ft (10,683 sq m) in three buildings. Prospect Land is also developing 34,000 sq ft (3,159 sq m) in a small unit format at Triangle Park and Gabwell is building 40,000 sq ft (3,716 sq m) in a mid-range configuration at The Quadrant Centre.

headline rent

• The headline rent for Grade A space has increased to £6.75 psf (£72.65 psm) for mid-range space.

• It is anticipated that the upward pressure on rents will continue, fuelled by a continued shortage of stock and an increase in new build construction costs.

18www.alderking.com

zone A headline rent £psf

25

0

75

100

125

2013 2015 2016 20172014

50 15

25

30

35

20

5

10

Eastgate St. Kings Walk

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

(1,0

76)

100

out of town headline rent £psf

20

0

40

50

2013 2015 2016 20172014

30

10

(26

9)

25

(26

9)

25

(377

) 35

(377

) 35

(26

9)

25

leisure headline rent £psf

0

2013 2015 2016 20172014

cinema health & fitness A3/A4

(129

) 12

(129

) 12

(129

) 12

(129

) 12

(129

) 12

(34

4)

32

(34

4)

32

(34

4)

32

(34

4)

32

(34

4)

32value of investment transactions £ms

30

0

60

75

90

105

2013 2015 2016 20172014

45

15

41.632.7

37.2

62.7

97.9

prime yields %

5

3

7

8

2014 2015 2016 2017

6

4

2013

investment by sector

office

industrial

retail

other

(97

) 9

(97

) 9

(97

) 9

(97

) 9

(97

) 9

21%

53%

10%16%

industrial

office

retail high street

retail out of town

Investment

Retail & Leisure

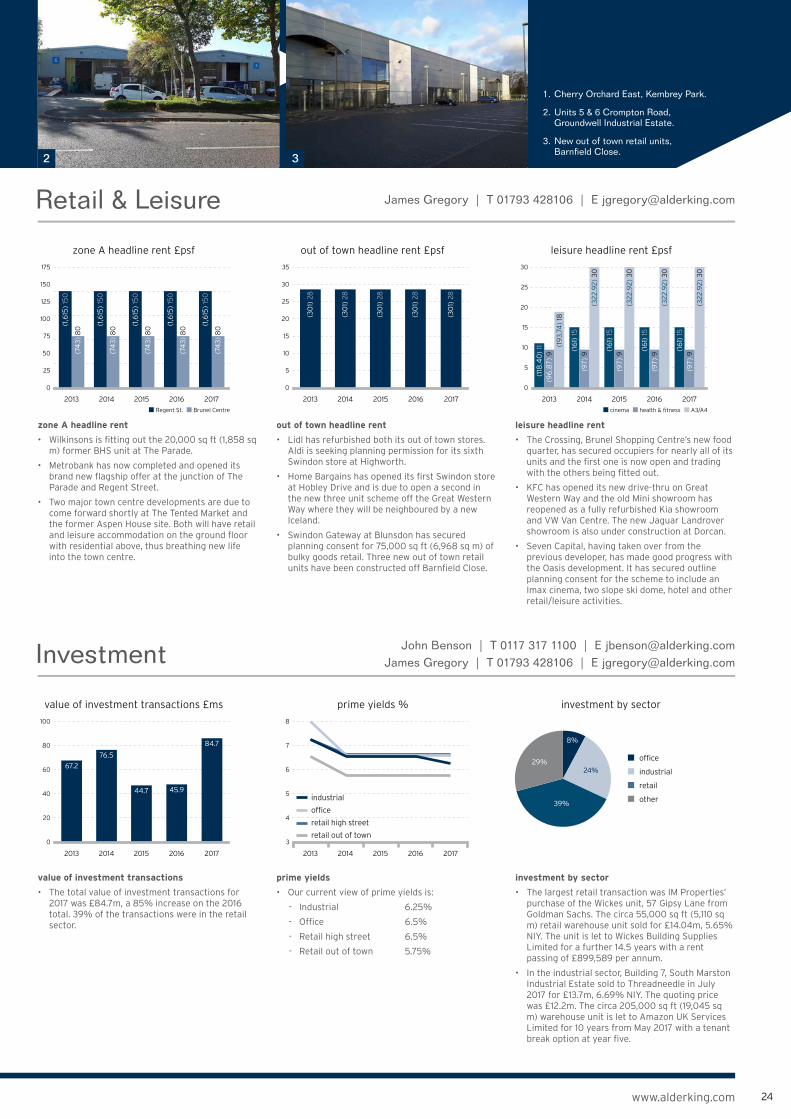

1. Rockhaven’s speculative development, Triangle Park.

2. CGI of TBS Engineering’s development, Gloucester Business Park. Courtesy of Arlington.

3. Gloucester Quays. Courtesy of Peel Land & Property.

2 3

John Hawkins | T 01452 627135 | E [email protected]

John Benson | T 0117 317 1100 | E [email protected] Adrian Rowley | T 01452 627133 | E [email protected]

zone A headline rent

• The opening of TK Maxx on Northgate Street has provided the expected boost for this side of the city centre, and the increased pedestrian traffic flow will give greater encouragement to the Kings Square developers.

• The Kings Square development continues to progress. The much anticipated mixed use redevelopment of this site will have a significant impact on rejuvenating the city centre.

• Demand across the four key streets of the city centre – Eastgate, Westgate, Northgate, and Southgate - remains relatively strong despite the increased competition in the region. There are very few void units.

out of town headline rent

• Demand for out of town units remains strong with limited availability. Whittle Square at Gloucester Business Park and St Oswalds Park are fully let.

• Occupier demand is being led by coffee drive-thrus and the discount food retailers. Starbucks has opened a drive-thru on Eastern Avenue within half a mile of Costa’s latest drive-thru on Triangle Park. Both appear to be trading extremely well, fuelling further demand for neighbouring occupiers.

• Having acquired the former All Cooper site on Hucclecote Road, Aldi is now on site commencing construction of its third Gloucester store. Both Aldi and Lidl continue to seek new sites for further expansion.

leisure headline rent

• The popularity of Gloucester Quays continues to grow, having been driven by the strong restaurant offering. The latest occupiers include more traditional retailers such as Jack Wills and Joules providing an additional draw to The Docks.

• Adjacent to Gloucester Quays is Bakers Quay which will ultimately link into The Quays where a new Costa Coffee and Brewers Fare will be completed and trading in 2018.

• Within the health and fitness sector, the budget gym operators remain active and are keen to acquire a limited supply of suitable properties.

value of investment transactions

• The total value of investment transactions for 2017 was £62.7m, up 68% on the 2016 total.

prime yields

• Our current view of prime yields is:

- Industrial 5.75%

- Office 6%

- Retail high street 6.25%

- Retail out of town 5.75%

investment by sector

• The largest transaction was Reef Estates’ purchase of Kings Walk Shopping Centre from Aviva for £20.5m, 6.2% NIY. The circa 285,000 sq ft (26,477 sq m) centre has over 40 tenants including Primark, River Island, Superdrug, WH Smith and Costa. Reef Estates plans to invest another circa £5m to improve the centre.

• The largest deal in the industrial sector was Telereal Trillium’s acquisition of Chancel Close Industrial Estate for £5.78m, 6.98% NIY. The property is multi-let to 11 tenants with a passing rent of £430,265 per annum.

Alder King Market Monitor 201819

(sq m)sq ftKey

demand 000s sq ft

50

0

100

125

150

2013 2015 2016 20172014

75

25

78(7)

131(12)

76(7) 64

(6)

115(11)

supply 000s sq ft

200

0

400

2013 2015 2016 20172014

300

100

345(32)

308(29)

395(37) 366

(34)360(33)

headline rent £psf

0

5

10

15

20

2013 2015 2016 20172014

city centre out of town

(172

) 16

(172

) 16

(172

) 16

(172

) 16

(172

) 16

(129

) 12

(13

4)

12.5

(13

4)

12.5

(14

7.25

) 13

.68

(129

) 12

demand 000s sq ft

100

0

300

400

500

600

700

2013 2015 2016 20172014

200

385(36)

606(30)

226(21)

231(21)

220(18)

supply 000s sq ft

0

500

750

1,000

1,250

2013 2015 20172014 2016

250

720(67) 555

(52)442(41)

1,008(94)

501(47)

headline rent £psf

0

2

3

4

6

5

2013 2015 20172014 2016

1

4(43)

4(43)

5.5(59)

4(43)

4(43)

Offices

Industrial

Newport

demand

• Take-up remains below the five year average of 97,000 sq ft (9,012 sq m) with two transactions accounting for 70% of the total.

• Notable transactions included the sale of 19,000 sq ft (1,765 sq m) at Glyndwr House, Cleppa Park to Care For The Family and the letting of 25,577 sq ft (2,376 sq m) at Caerleon House, again on Cleppa Park, to Slowhit Ltd.

• There are currently over 100,000 sq ft (9,290 sq m) of active requirements in the county.

supply

• Supply has remained at a similar level for the last six years with 50% available in the city centre. This excludes 63,624 sq ft (5,911 sq m) at the former Post Office sorting office on Mill Street which has recently been purchased for refurbishment / redevelopment.

• The city centre supply is considered to be of poor quality and includes four buildings accounting for 85% of the supply.

• There is virtually no Grade A stock available in the city centre which requires commencement of office schemes such as Scarborough’s Station Quarter.

headline rent

• £16 psf (£172 psm) remains the highest headline rent which has been at this level for the last six years.

• New development of Grade A stock will be required to push the rents as there is already downward pressure on the existing headline levels in better quality buildings such as Nexus House.

demand

• Take-up is low when compared to the five year average of over 400,000 sq ft (37,161 sq m) and is likely to derive from a lack of available stock.

• Significant deals this year include MCL Logistics acquiring 87,000 sq ft (8,082 sq m) on 4.67 acres and UTS Engineering taking 43,765 sq ft (4,252 sq m) at Leeway Industrial Estate.

• There has been increased activity within the trade counter sector evidenced by Toolstation and Screwfix taking space at Langland Park West and Maesglas Industrial Estate respectively.

supply

• Units of under 10,000 sq ft (929 sq m) account for 71% of available stock, leaving a number of large requirements unsatisfied.

• Despite St Modwen’s development of 50,000 sq ft (4,645 sq m) at Celtic Business Park let to Amazon, there still remains a lack of speculative development, hindering replenishment of existing stock levels.

• Newport is geographically best placed to benefit from the new M4 Relief Road and future abolishment of the Severn Bridge tolls, potentially attracting the larger active B8 requirement and thereby stimulating rental increases and development.

headline rent

• As stock levels continue to decrease, we forecast upward pressures on rental levels and a reduction in incentives.

• This has been demonstrated by the letting to Amazon at Celtic Business Park, taking 48,250 sq ft (4,483 sq m) on a 10 year term at a rent equivalent to £5.50 psf (£59.20 psm).

Owen Young | T 029 2038 1996 | E [email protected]

Owen Young | T 029 2038 1996 | E [email protected]

1

20www.alderking.com

investment by sector

zone A headline rent £psf

30

0

60

2013 2015 20172014 2016

40

50

20

10

(59

2)

55

(59

2)

55

(59

2)

55

(59

2)

55

(59

2)

55

out of town rent £psf

10

0

25

30

2013 2015 20172014 2016

15

5

20(2

69

) 25

(26

9)

25

(26

9)

25

(26

9)

25

(26

9)

25

leisure headline rent £psf

0

5

10

15

25

2013 2015 20172014 2016

cinema health & fitness A3/A4

20

(129

) 12

(129

) 12

(129

) 12

(129

) 12

(129

) 12

(86

) 8

(86

) 8

(86

) 8

(86

) 8

(86

) 8

(19

4)

18

(19

4)

18

(19

4)

18

(19

4)

18

(19

4)

18

50

100

75

25

value of investment transactions £ms

0

2013 2015 20172014 2016

8.9

25.1

91.16

52.3

33

prime yields %

6

4

8

9

2014 20162015 20172013

7

5

industrial

office

retail high street

retail out of town

1%

office

industrial

retail

5%

94%

Investment

Retail & Leisure

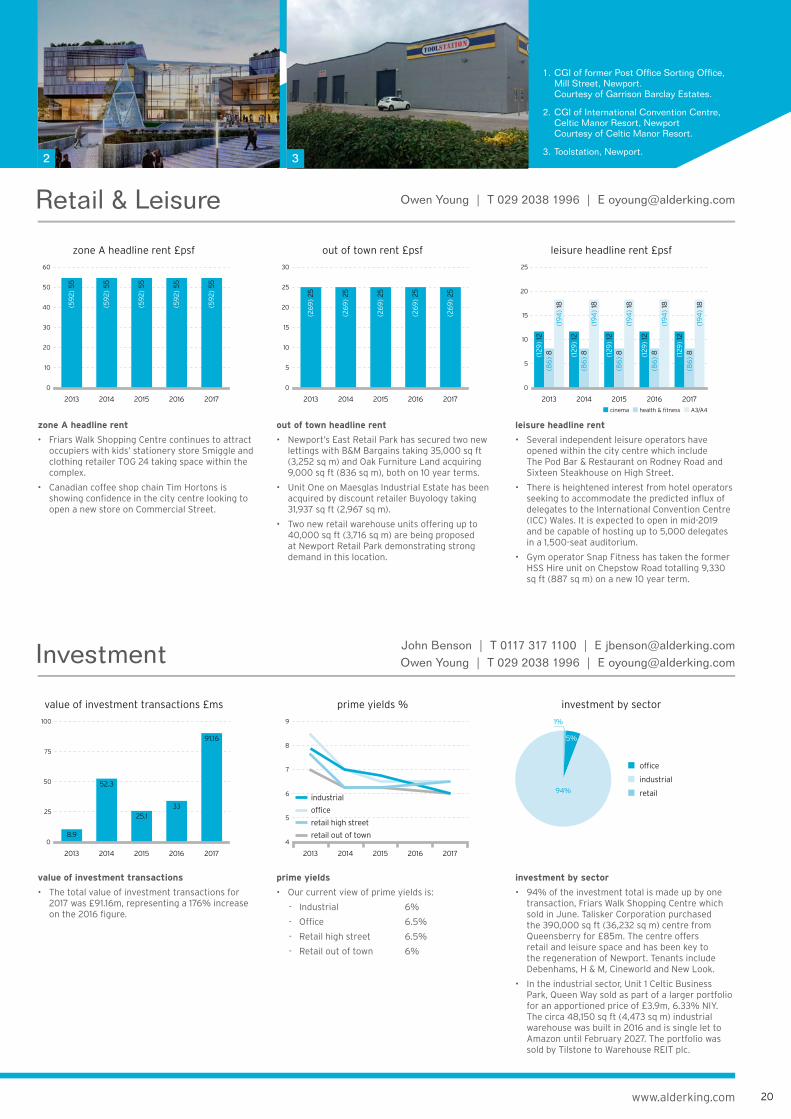

1. CGI of former Post Office Sorting Office, Mill Street, Newport. Courtesy of Garrison Barclay Estates.

2. CGI of International Convention Centre, Celtic Manor Resort, Newport Courtesy of Celtic Manor Resort.

3. Toolstation, Newport.

zone A headline rent

• Friars Walk Shopping Centre continues to attract occupiers with kids’ stationery store Smiggle and clothing retailer TOG 24 taking space within the complex.

• Canadian coffee shop chain Tim Hortons is showing confidence in the city centre looking to open a new store on Commercial Street.

out of town headline rent

• Newport’s East Retail Park has secured two new lettings with B&M Bargains taking 35,000 sq ft (3,252 sq m) and Oak Furniture Land acquiring 9,000 sq ft (836 sq m), both on 10 year terms.

• Unit One on Maesglas Industrial Estate has been acquired by discount retailer Buyology taking 31,937 sq ft (2,967 sq m).

• Two new retail warehouse units offering up to 40,000 sq ft (3,716 sq m) are being proposed at Newport Retail Park demonstrating strong demand in this location.

leisure headline rent

• Several independent leisure operators have opened within the city centre which include The Pod Bar & Restaurant on Rodney Road and Sixteen Steakhouse on High Street.

• There is heightened interest from hotel operators seeking to accommodate the predicted influx of delegates to the International Convention Centre (ICC) Wales. It is expected to open in mid-2019 and be capable of hosting up to 5,000 delegates in a 1,500-seat auditorium.

• Gym operator Snap Fitness has taken the former HSS Hire unit on Chepstow Road totalling 9,330 sq ft (887 sq m) on a new 10 year term.

value of investment transactions

• The total value of investment transactions for 2017 was £91.16m, representing a 176% increase on the 2016 figure.

prime yields

• Our current view of prime yields is:

- Industrial 6%

- Office 6.5%

- Retail high street 6.5%

- Retail out of town 6%

investment by sector