Embed Size (px)

DESCRIPTION

- Overview of 2016 legislative issues - Guiding principles for state taxation - Simplify the Limited Liability Entity Tax (LLET) - Estimated tax interest and penalty reform

Citation preview

2016 Legislative Issues

OVERVIEW OF

2016 LEGISLATIVE ISSUES

GUIDING PRINCIPLES FOR

STATE TAXATION

SIMPLIFY THE

LIMITED LIABILITY ENTITY TAX (LLET)

ESTIMATED

TAX INTEREST & PENALTY REFORM

kycpa.org

Kentucky Society of Certified Public AccountantsFounded in 1924, the Kentucky Society of Certified Public Accountants (KyCPA) is a statewide, non-profit professional organization serving nearly 5,000 CPAs in public accounting firms, business, industry, government, and education. KyCPA supports all CPAs in Kentucky with timely information, outstanding educational opportunities, career development, helpful resources, the promotion of high ethical standards and public advocacy on behalf of the profession and the public good.

Kentucky Society of CPAs1735 Alliant Avenue Louisville, Ky. 402999502.266.5272kycpa.org

Contact:

Penny GoldChief Executive [email protected]: 502.724.6553

Charles GeorgeGovernment Affairs [email protected]: 502.445.9981

@KyCPAdvocacy@KyCPAnews

empowering

CPE. Networking. Advocacy. More.members

OVERVIEW OF

2016 LEGISLATIVE ISSUES

GUIDING PRINCIPLES FOR

STATE TAXATION

SIMPLIFY THE

LIMITED LIABILITY ENTITY TAX (LLET)

ESTIMATED

TAX INTEREST & PENALTY REFORM

Contents

5

8

12

14

OVERVIEW OF

2016 LEGISLATIVE ISSUES

Protect and enhance taxpayer rights

Filed as HB 361 and HB 399 (2015), the Taxpayer Rights Enhancement Act (TREA) and companion legislation bring much-needed transparency, efficiency, and equity to the administration of our tax code. The fair administration of our tax code plays an incredibly important role in the Commonwealth’s economic development efforts. TREA:• Requires the Department of

Revenue (DOR) to enhance its tax education and information program to help taxpayers better understand our tax code, possibly through additional funding.

• Requires the DOR to publish on its Web site in redacted form any final rulings, determination rulings, forms and instructions, training manuals, or any other material stating its policies or positions.

• Requires the DOR to issue tax notices so taxpayers can clearly understand what tax is owed and why.

• Requires the DOR to maintain a record if taxpayer information is shared or

exchanged with other agencies or states, and provide such records to the taxpayer if requested.

• Improves dispute resolution process to increase efficiency and lessen redundancy; provides the DOR flexibility to waive interest during settlement.

• Ensures updated or revised forms and instructions do not contain substantive changes without proper notice.

• Places Kentucky’s Taxpayer Ombudsman office directly under the Secretary of Finance (instead of the DOR Commissioner) for greater independence.

• Prohibits the state from contracting with third parties to audit taxpayers on a contingency fee basis.

• KyCPA also believes the DOR should be provided additional flexibility in Kentucky’s regulatory statute (KRS Chapter 13A) so guidance can be issued without fear of violating Chapter 13A

P. 5

Filed as HB 136 (2014) and HB 331 (2015), this bill clarifies the ambiguous cost of goods sold (COGS) definition in Kentucky’s limited liability entity tax (LLET) statute to make it simple, fair and easy for businesses and tax preparers to comply. This bill has bipartisan support and the endorsement of more than 20 business organizations.

Filed as HB 346 (2014) and included in HB 399 (2015), this legislation simplifies Kentucky’s estimated tax rules. Kentucky’s rules are very different from federal rules, making compliance confusing for taxpayers and tax preparers – especially those who cope with tax rules in multiple states. The current rules make it much more difficult to calculate “safe” Kentucky estimated tax payments than it is for federal taxes.

Filed as HB 345 (2014) and included in HB 399 (2015), this bill returns to a balanced interest rate on taxes owed to and by the Commonwealth. In 2008, the Kentucky legislature created a differential between: 1) the interest rate taxpayers must pay if they owe taxes (prime plus 2 percent), and; 2) the interest rate that they receive on amounts owed to them (prime minus 2 percent). This 4 percent differential is inherently unfair. The Blue Ribbon Commission on Tax Reform recommended a similar return to a balanced interest rate in its 2012 recommendations.

Simplify the LLET (cost of goods sold)

Simplify estimated tax rules

Return to balanced interest rate

P. 6

The starting point in calculating Kentucky’s income tax is the federal income tax return. In 2014, Kentucky updated its reference date to the Internal Revenue Code to Dec. 31, 2013. While helpful, this update should be considered every year. The state should also consider the impact of conforming with IRC Section 179 depreciation rules.

Update IRC reference date

P. 7

Sen. Ernie Harris with KyCPA members during a legislative reception.

Rep. Rita Smart with former KyCPA Board President Stephen Lukinovich and KyCPA member Glenn Jennings.

General Statement on Tax ReformMany state tax provisions are complex, and their full effects are not always readily apparent. KyCPA members are uniquely qualified to help analyze tax policy alternatives and to articulate their likely effects. KyCPA stands ready to use its unique expertise and experience to advise legislators, administrators, industry groups, and taxpayers.

GUIDING PRINCIPLES FOR

STATE TAXATION

The power to tax is the power to control public and private behavior. It is one of the essential powers of federal, state and local governments. When tax statutes and regulations embody sound, clear tax policy, everyone benefits: corporate and individual taxpayers can predict the tax consequences of their actions; administrators can produce clear rules and collect taxes easily; and governmental units can get the revenue they need.

Conversely, when tax policies are complex, vague, contradictory, or unpredictable, everyone loses: taxpayers get confused and don’t pay taxes they owe; administrators can’t produce clear regulations or collect taxes easily; and governments struggle because they don’t get the tax revenue they expect.

P. 8

Senate President Robert Stivers addresses athe crowd at KyCPA Government Relations Day.

KyCPA recommends Kentucky tax policy be based on these 10 principles:

Clear administrative guidance Kentucky should strive to be a model of state tax administration. Given the dynamics of tax laws and everyone’s interest in full compliance, taxpayers (and their advisors, such as CPAs) need clear and reliable guidance. Before Tax Modernization a decade ago, the Kentucky Department of Revenue had a long history of publishing helpful guidance that assisted taxpayers and auditors in interpreting Kentucky’s sometimes complicated tax laws. Guidance appeared in the form of instructions for tax forms and, importantly, in the Department’s published Policies and industry-specific Circulars.

While many Policies and Circulars needed revision, the Department revoked the majority of them, leaving taxpayers, advisors, and administrators without reliable guidance. Then the Department reissued most of its administrative regulations – minus the helpful examples found in the old regulations.

We urge the Department of Revenue to resume publishing its internal policies, continuing education materials, examples, and other helpful guidance as would have been required by KyCPA’s proposed Taxpayer Rights Enhancement Act of 2015. Ultimately, this will minimize the cost of tax administration and improve the state’s cash flow by minimizing errors and unnecessary disputes.

Certainty Continual change and lags in administrative guidance heighten taxpayer uncertainty. Reducing the frequency of rule changes and using consistent concepts and definitions is an important element of a sound and enforceable tax policy.

1

2

P. 9

Speaker Greg Stumbo speaks to CPAs during their visit to the Capitol.

Equity, fairness, and neutrality Not only must state tax law be fair, but the public must perceive it as being fair. Narrow or targeted exemptions from sales, use, or any other state tax create perceptions of favoritism and unfairness. Kentucky should avoid taxes that apply only to a small group of taxpayers or are unevenly enforced. Social equity demands that similarly situated taxpayers should pay the same taxes.

Simplification and economy of collection Simplification should be a high priority. It will minimize the costs of the Department of Revenue, including the administrative costs associated with collecting taxes, examining returns, and resolving disputes.

Economic growth Tax policy should not divert government or business resources from productive activities into excessive and non-productive compliance costs. Kentucky tax policy should be formulated to make the state a welcoming place to do business for existing businesses and new businesses. The state should continue to recognize that sales and use, income, and other taxes have economic development implications, and many existing Kentucky businesses often compete with businesses across state lines. Coherent tax policy encourages economic development, the creation of jobs and the enhancement of Kentuckians’ well-being.

Transparency and clarity It is self-evident that taxpayers, their advisors and tax administrators should be able to understand how the tax law applies. Kentucky would benefit by minimizing compliance burdens, which would, in turn, narrow the tax gap (the difference between taxes owed and taxes paid voluntarily).

Predictability Kentucky should enact tax laws only prospectively to give the Department of Revenue, practitioners, software vendors, businesses, and individuals enough time to prepare for changes. Retroactive tax laws should not be enacted – and tax laws should provide for clear, bright-line rules whenever possible.

3

4

5

6

7

P. 10

Consistency The Commonwealth should generally retain the structure of any given tax from one year to the next, absent compelling reasons for change.

Uniformity with other jurisdictions and federal procedures

Kentucky should strive to adopt uniform laws and compliance procedures that conform to federal procedures and those of other states. Specifically, we note three areas that add excessive incremental burdens to Kentucky’s current system:• Lags in adapting to the federal Internal Revenue Code (IRC)

changes, which cause interpretative, administrative, and compliance problems. Currently, Kentucky tax statutes are based upon the IRC as it existed on Dec. 31, 2013.

• Kentucky does not conform with IRC Section 179 (the election to expense some equipment) which creates problematic differences between federal and Kentucky depreciation calculations. These and other depreciation differences cause businesses to make separate – and sometimes massively different – depreciation calculations for federal and Kentucky income tax purposes.

• Kentucky’s nexus consolidated return rules are unclear and ambiguous. Clarifying and conforming these rules to those of other states would ease compliance and keep multiple states from taxing the same income.

Avoid double taxation and pyramiding of taxes Kentucky should enact and retain tax laws that apply only one level of tax to a transaction or taxpayer. For example, Kentucky law appropriately exempts inventory purchased for resale. Sales tax is imposed only when the ultimate consumer buys the inventory.

P. 11

8

9

10

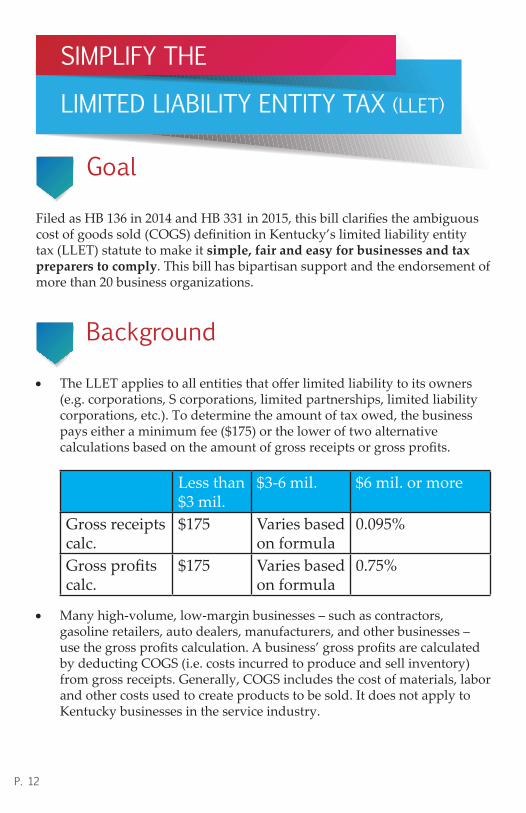

Goal

Filed as HB 136 in 2014 and HB 331 in 2015, this bill clarifies the ambiguous cost of goods sold (COGS) definition in Kentucky’s limited liability entity tax (LLET) statute to make it simple, fair and easy for businesses and tax preparers to comply. This bill has bipartisan support and the endorsement of more than 20 business organizations.

Background

• The LLET applies to all entities that offer limited liability to its owners (e.g. corporations, S corporations, limited partnerships, limited liability corporations, etc.). To determine the amount of tax owed, the business pays either a minimum fee ($175) or the lower of two alternative calculations based on the amount of gross receipts or gross profits.

Less than $3 mil.

$3-6 mil. $6 mil. or more

Gross receipts calc.

$175 Varies based on formula

0.095%

Gross profits calc.

$175 Varies based on formula

0.75%

• Many high-volume, low-margin businesses – such as contractors, gasoline retailers, auto dealers, manufacturers, and other businesses – use the gross profits calculation. A business’ gross profits are calculated by deducting COGS (i.e. costs incurred to produce and sell inventory) from gross receipts. Generally, COGS includes the cost of materials, labor and other costs used to create products to be sold. It does not apply to Kentucky businesses in the service industry.

SIMPLIFY THE

LIMITED LIABILITY ENTITY TAX (LLET)

P. 12

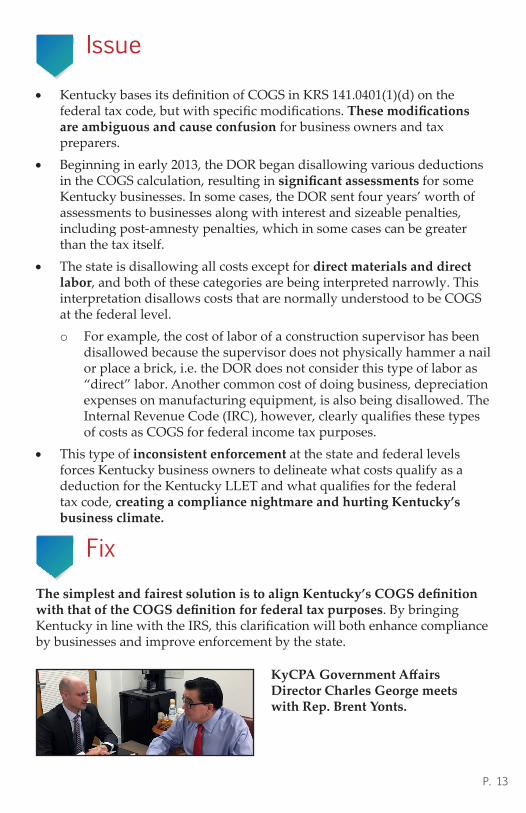

Issue

• Kentucky bases its definition of COGS in KRS 141.0401(1)(d) on the federal tax code, but with specific modifications. These modifications are ambiguous and cause confusion for business owners and tax preparers.

• Beginning in early 2013, the DOR began disallowing various deductions in the COGS calculation, resulting in significant assessments for some Kentucky businesses. In some cases, the DOR sent four years’ worth of assessments to businesses along with interest and sizeable penalties, including post-amnesty penalties, which in some cases can be greater than the tax itself.

• The state is disallowing all costs except for direct materials and direct labor, and both of these categories are being interpreted narrowly. This interpretation disallows costs that are normally understood to be COGS at the federal level. o For example, the cost of labor of a construction supervisor has been

disallowed because the supervisor does not physically hammer a nail or place a brick, i.e. the DOR does not consider this type of labor as “direct” labor. Another common cost of doing business, depreciation expenses on manufacturing equipment, is also being disallowed. The Internal Revenue Code (IRC), however, clearly qualifies these types of costs as COGS for federal income tax purposes.

• This type of inconsistent enforcement at the state and federal levels forces Kentucky business owners to delineate what costs qualify as a deduction for the Kentucky LLET and what qualifies for the federal tax code, creating a compliance nightmare and hurting Kentucky’s business climate.

FixThe simplest and fairest solution is to align Kentucky’s COGS definition with that of the COGS definition for federal tax purposes. By bringing Kentucky in line with the IRS, this clarification will both enhance compliance by businesses and improve enforcement by the state.

P. 13

KyCPA Government Affairs Director Charles George meets with Rep. Brent Yonts.

• Filed as HB 346 in 2014 and included in HB 399 in 2015, this bill simplifies Kentucky’s estimated tax rules. Kentucky’s rules are very different from federal rules, making compliance confusing for taxpayers and tax preparers – especially those who cope with tax rules in multiple states. The current rules make it much more difficult to calculate “safe” Kentucky estimated tax payments than it is for federal taxes.In some cases, it is impossible to make Kentucky estimated tax payments that are “safe” from penalties and interest.

• This bill changes Kentucky’s estimated tax rules to conform to the federal rules that provide a safe harbor for estimated tax payments based on prior year tax, current year tax, or an annualized amount of tax.

Under existing Kentucky law, taxpayers can be subject to multiple layers of penalties and interest resulting from the timing of their tax payments – and often it is impossible to avoid them.

ESTIMATED

TAX INTEREST & PENALTY REFORM

P. 14

KyCPA Government Affairs Director Charles George with Sen. Chris McDaniel (left) and Rep. Rick Rand (right).

Specifically, the existing estimated tax penalty and interest provisions for individuals and corporations should be simplified for the following reasons:o The existing Kentucky interest provision overlaps with the

existing penalty provision, so that interest and penalties can both apply at the same time. Federal estimated tax rules provide penalties for late

quarterly estimated tax payments but do not impose interest until the original due date of the return. That is, while estimated tax penalties can apply prior to the April 15 due date, interest does not begin until after April 15 – the Federal interest and penalty calculations do not overlap.

o The existing interest provision often results in interest charges on quarterly underpayments of any size. If 100 percent of the tax is not paid in quarterly installments or through withholding, the taxpayer pays interest on the underpayment. There is no room for error.

o The existing interest provision is an annual computation that does not take into account when income is earned during the year. This may result in interest charges for periods during which a taxpayer did not have any taxable income.For example, if a taxpayer realizes a taxable gain late in the year, the interest computation assumes the fiction that the gain occurred evenly throughout the year. Thus, interest is back-charged as if the gain had been realized evenly throughout the year.This bill establishes an annualized income installment method to allow a taxpayer with fluctuating income throughout the year to base the installments on income earned at applicable months during the year. This prevents a taxpayer with fluctuating income from being penalized by a sudden or unexpected gain in income.

Interest and penalty provisions are not intended to raise revenue but instead to incentivize taxpayers to make tax payments during the year (rather than at year-end). Thus, effective estimated tax rules tend to accelerate the timing of payments to the Commonwealth.

P. 15

Kentucky Society of CPAs1735 Alliant Avenue

Louisville, Ky. 402999502.266.5272

kycpa.org