Embed Size (px)

Citation preview

Offshore ‘Beta’ Trade: Laggards Hold Greatest Upside in Recovery

Darren Gacicia Managing Director

Senior Oilfield Services Analyst KLR Group, LLC 713-352-0887

For definitions and the distribution of analyst ratings, and other disclosures, please refer to pages 72 - 73 of this report

Set Up for Improving Fundamentals Align Offshore Stocks as the “Beta” Trade Within Oilfield Services Offshore Drillers & Equipment Stocks Highest “Beta” in Recovery. Fueled by prospects of a later cycle recovery and high leverage (Net Debt/EV), the offshore driller stocks represent the highest “beta” to a recovery in the oil services group. With better credit profiles, the offshore equipment group runs a close second in the “beta” rankings. In our view, a traditional lagged recovery of offshore activity leave shares with offshore exposure more leveraged to the level/trajectory of oil prices. Since we see tighter commodity markets ahead, we believe portfolios should have offshore exposure to capture “beta” as sentiment turns positive. Likewise, we are wary of the long onshore/short offshore trade, which is dangerous as the bearish paradigm for the group shifts. With an inflection in energy sector prospects and shift in risk/reward, we suspect offshore companies with higher leverage and fundamentals most challenged by the downturn may outperform. Multiple expansion, driven in part by a de-risking and re-rating of high leverage ratio stocks and better prospect for earnings recoveries (pgs. 11-13), may move offshore shares higher without an increase in near term earnings. We are not calling for a dramatic near term recovery in offshore rig or equipment demand in 2016 or 2017, but we see an increasing chance that improving fundamentals may surprise our conservative estimates.

Upgrade ATW & DO to Buy. We are upgrading ATW to Buy from Accumulate. Following ATW’s agreement to eliminate covenants on its revolver until July 2018, we see potential for these shares to de-risk and re-rate higher. We are willing to move further out on the risk frontier with ATW, as covenant issues move to the sidelines. We are raising our price target to $16, as a function of a lower WACC (160 bps reduction) and a marginal improvement in our long term rig utilization estimates. We are also upgrading DO to Buy from Accumulate. Given that we have retired numerous older rigs from the DO fleet, we are raising our longer term utilization assumptions (~91%) from more punitive levels. As a result, our price target increases to $33.

Estimate Changes & Price Target Increases. We are lowering our estimates for the offshore drillers as we cut near term dayrate assumptions closer to more recent fixture levels (pg. 22-23). Our normalized dayrate assumptions remain unchanged and tied to an assumption that rigs will work at dayrates that return on par with a 10% cost of capital. We sense that dayrates sit near trough levels, but should begin to recover more meaningfully in 2018 as rig attrition meets demand recovery. As we reviewed our offshore driller models and updated estimates, we are raising price targets for ATW, DO, ESV and adjusting our price target for PACD to reflect the reverse share split (pg. 3).

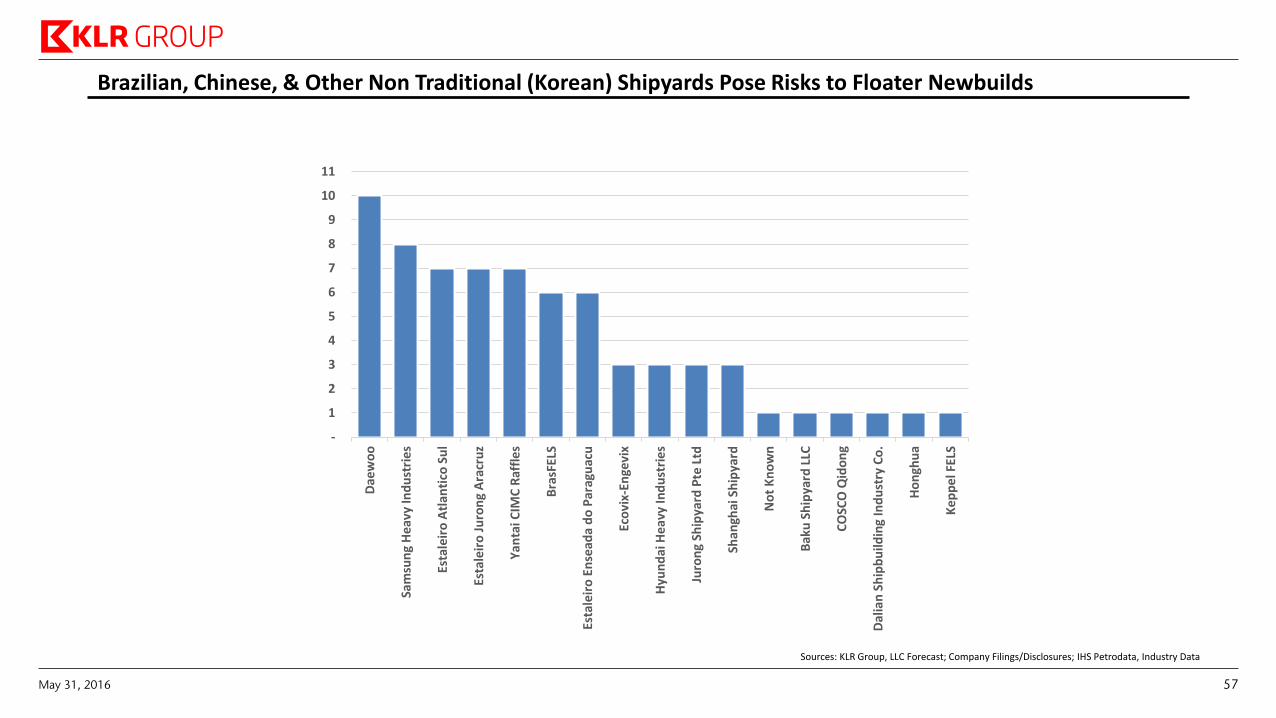

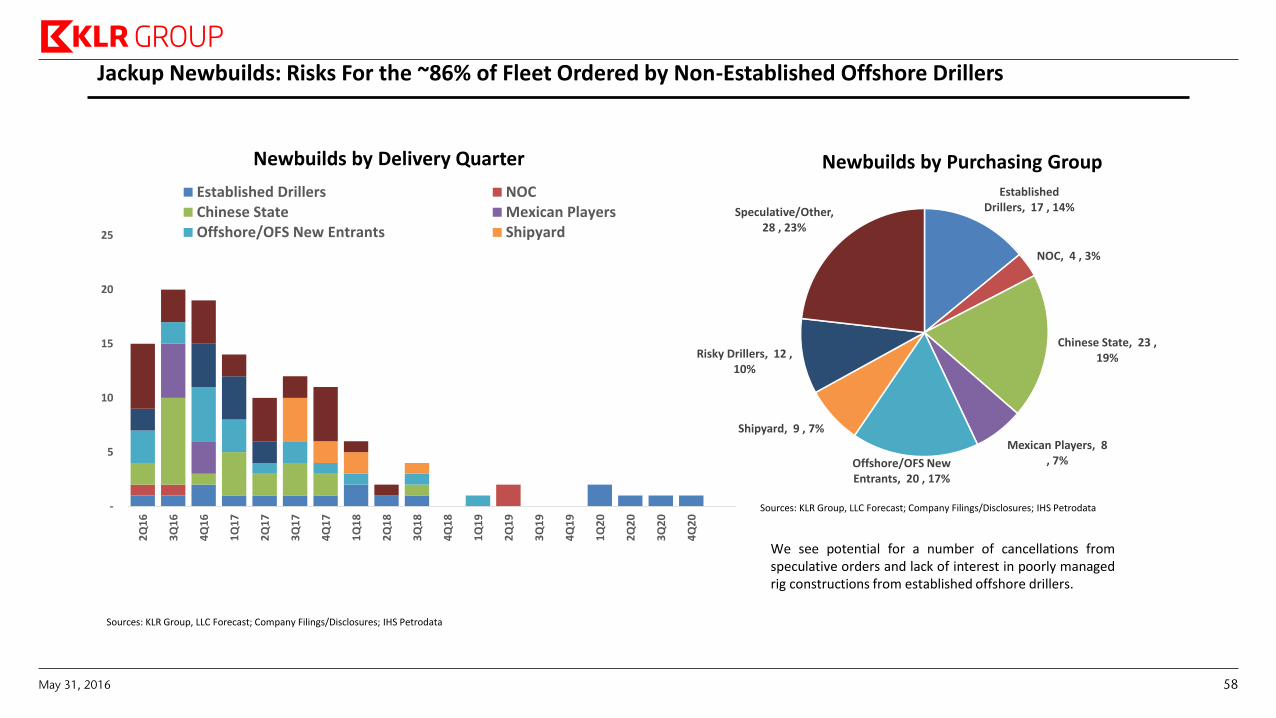

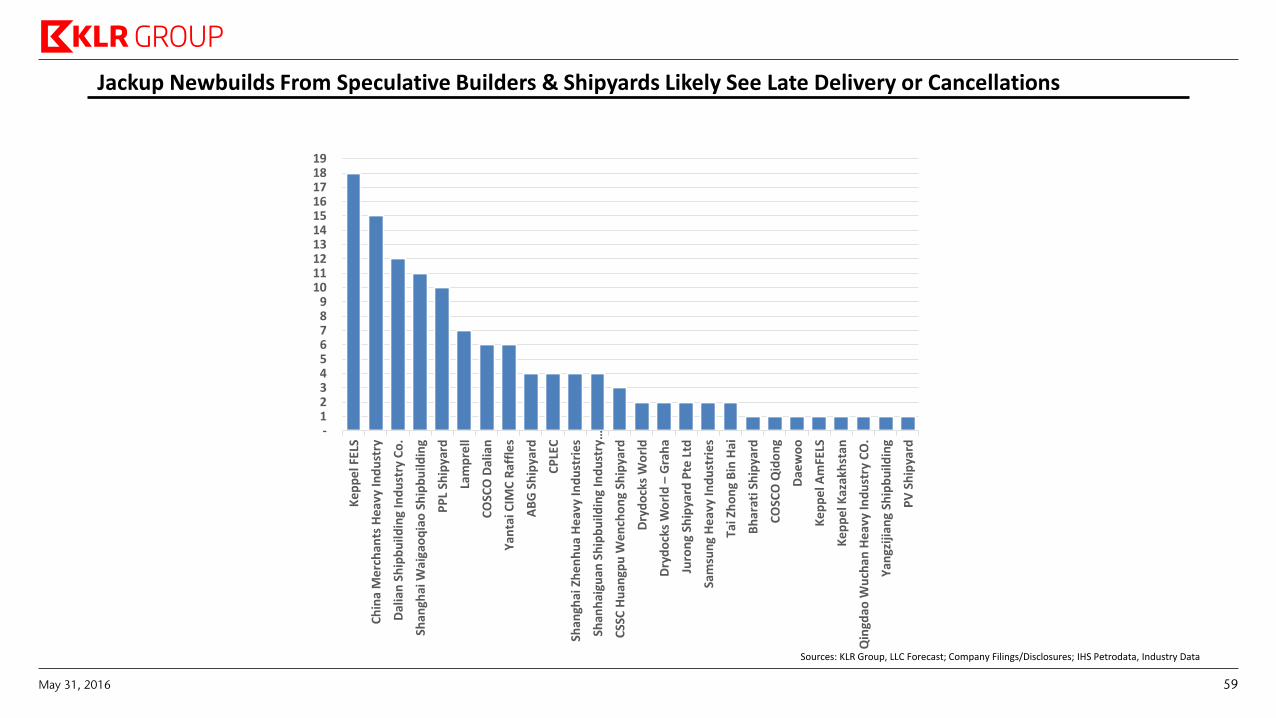

Rig Attrition, Cold Stacking, & Modest Demand Recovery Suggest More Bullish 2018 Offshore Driller Economics. We forecast that a demand recovery by 2018, met with floater and jackup cold stacking and retirements (pg. 46-59) should bring utilization of the marketed floater and jackup fleets above 85% (pgs 27, 41). Tighter offshore drilling markets should drive pricing power for offshore drillers in 2018. In our view, rig attrition should continue with rising oil prices, as offshore drillers may choose to retire assets versus commit capital to older assets for maintenance and surveys (pg. 54-55). Our estimates suggest ~70 floaters retire/stack in 2016-2017 and ~115 jackups retire/stack between 2016-2018. Given risk to floater and jackup newbuilds from speculative builders and unproven shipyards, our fleet tally assumes only 75% of floaters and jackups will be delivered on schedule. We have updated our floater and jackup demand forecasts. Our field-by-field development demand analysis for floaters continues to see flattish demand through 2020, but we see a steady uptick in exploration and appraisal activity from extremely low current levels (pg. 31). After development demand delays during the downturn, we see potential for demand to pull forward and probabilities for project approvals (FID) to rise in our model if commodity markets strengthen (pg. 32-33). A vast majority of near term development work remains tied to existing and FID approved projects, rather than new project starts (pgs. 36-38). Industry commentary around project redesign and standardization, lower break even costs, and potential for incremental development work for project with existing infrastructure may prove catalysts to pull forecasted demand forward. Reduced rig supply, a positive bias toward incremental development demand, and the need for exploration for reserve replacement may all suggest a better risk/reward for the group than currently discounted in a rising commodity price environment. We continue to prefer offshore driller exposure in RIG, NE, and ESV.

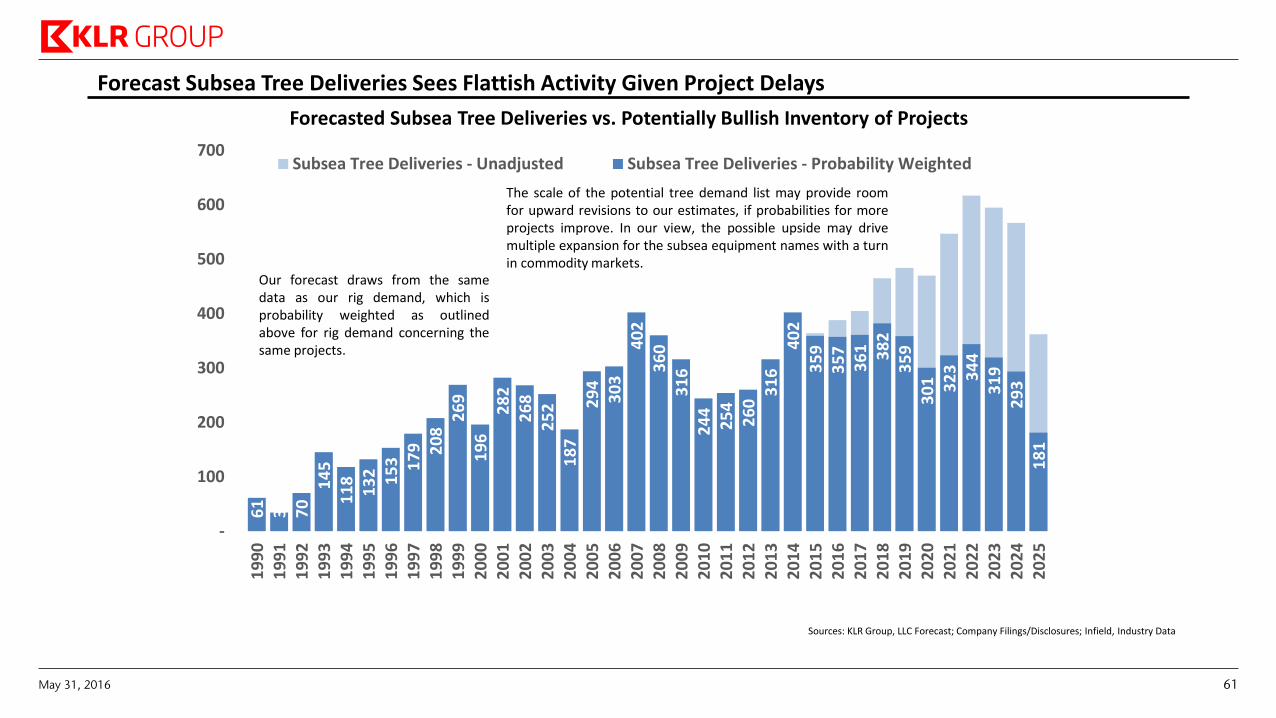

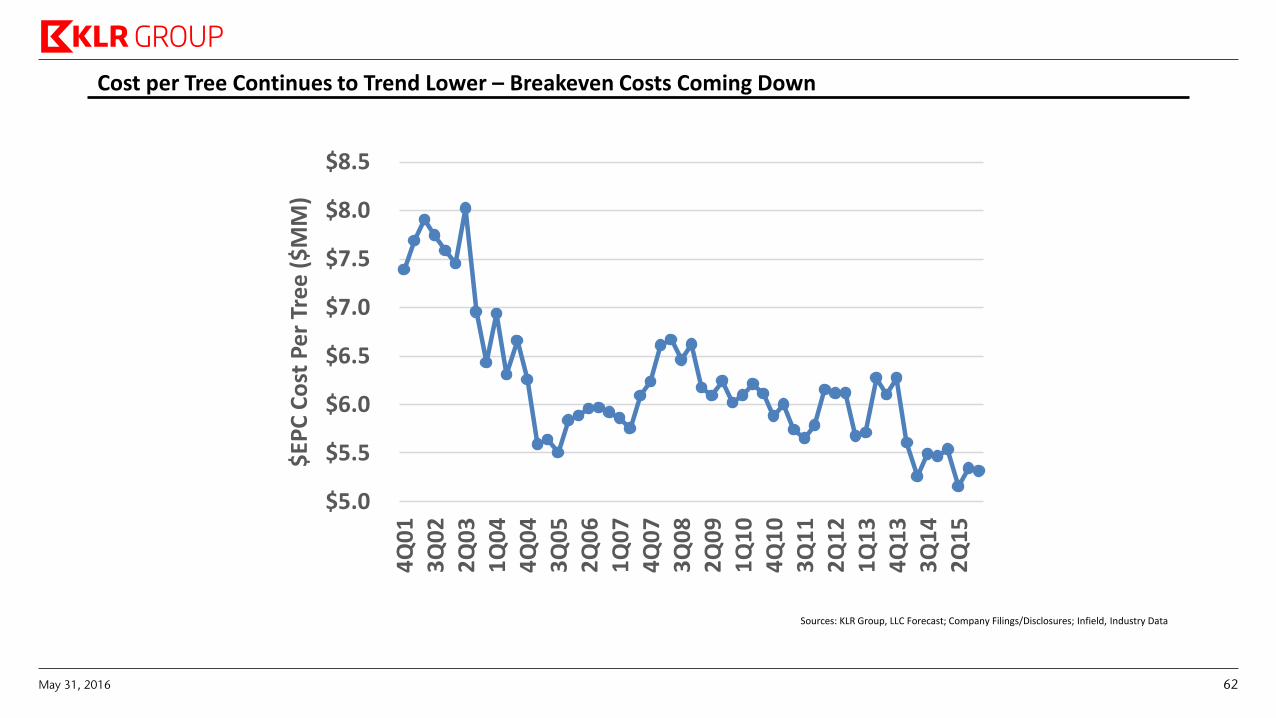

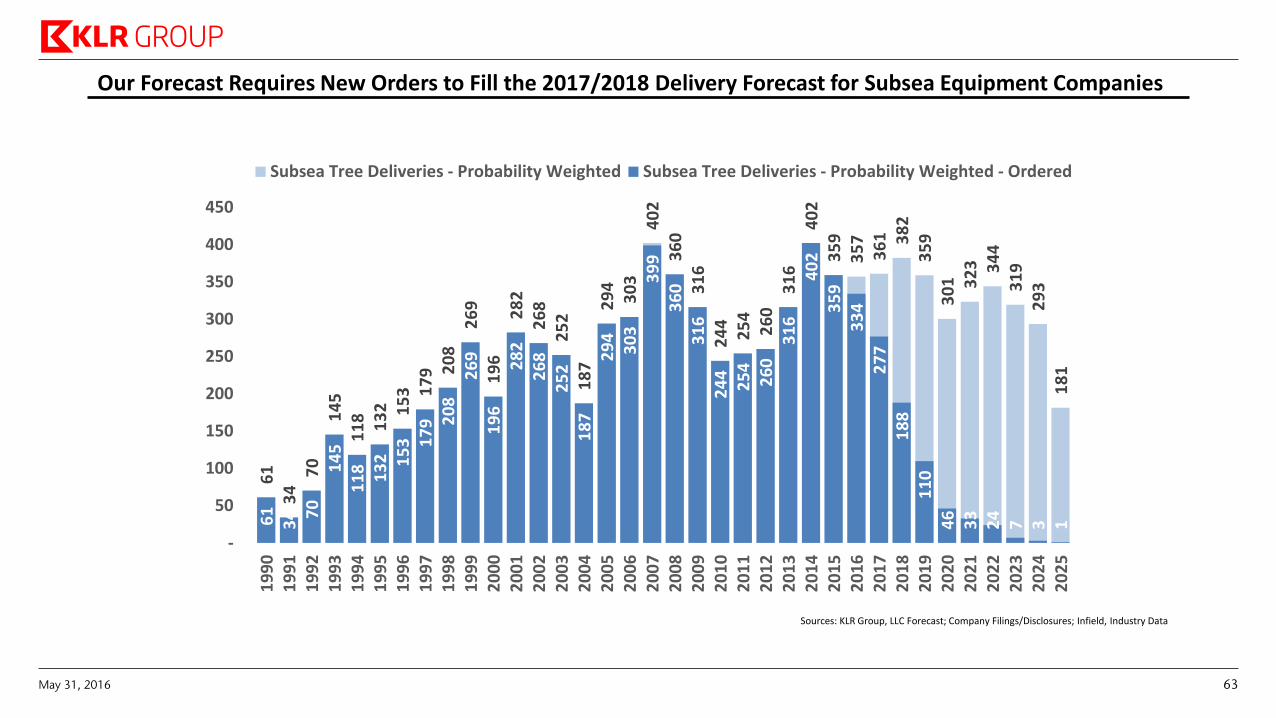

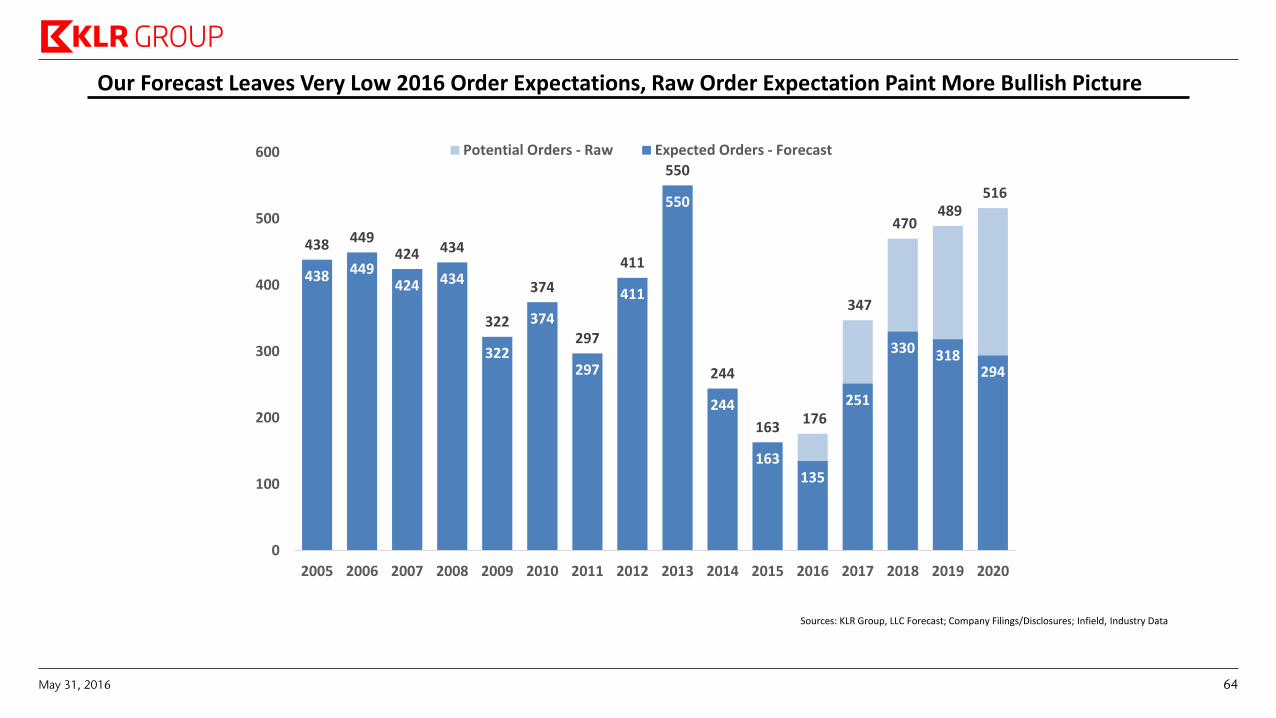

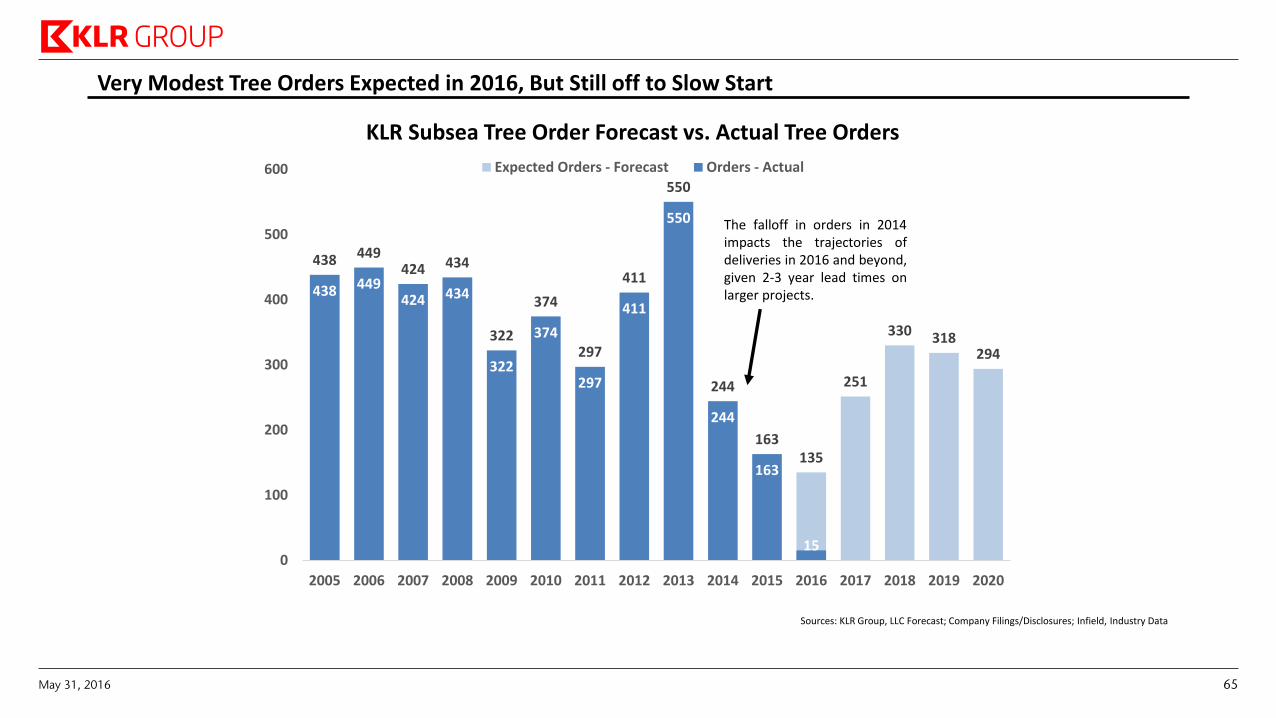

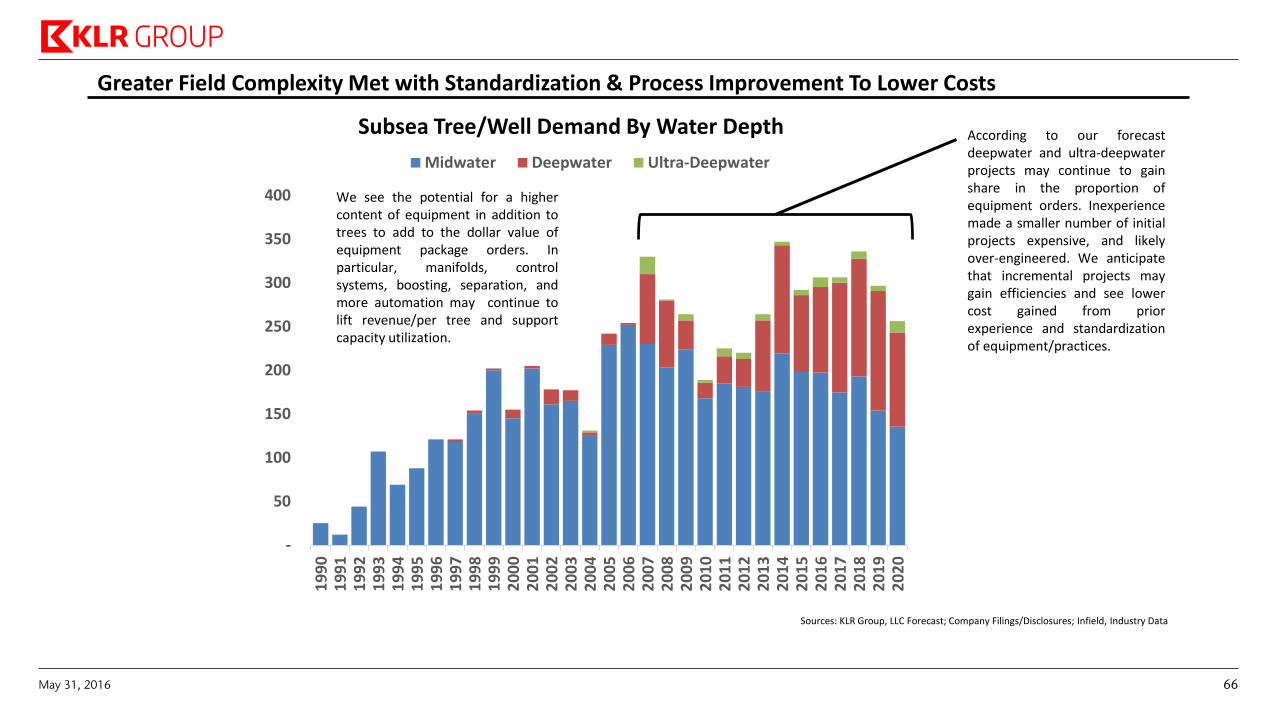

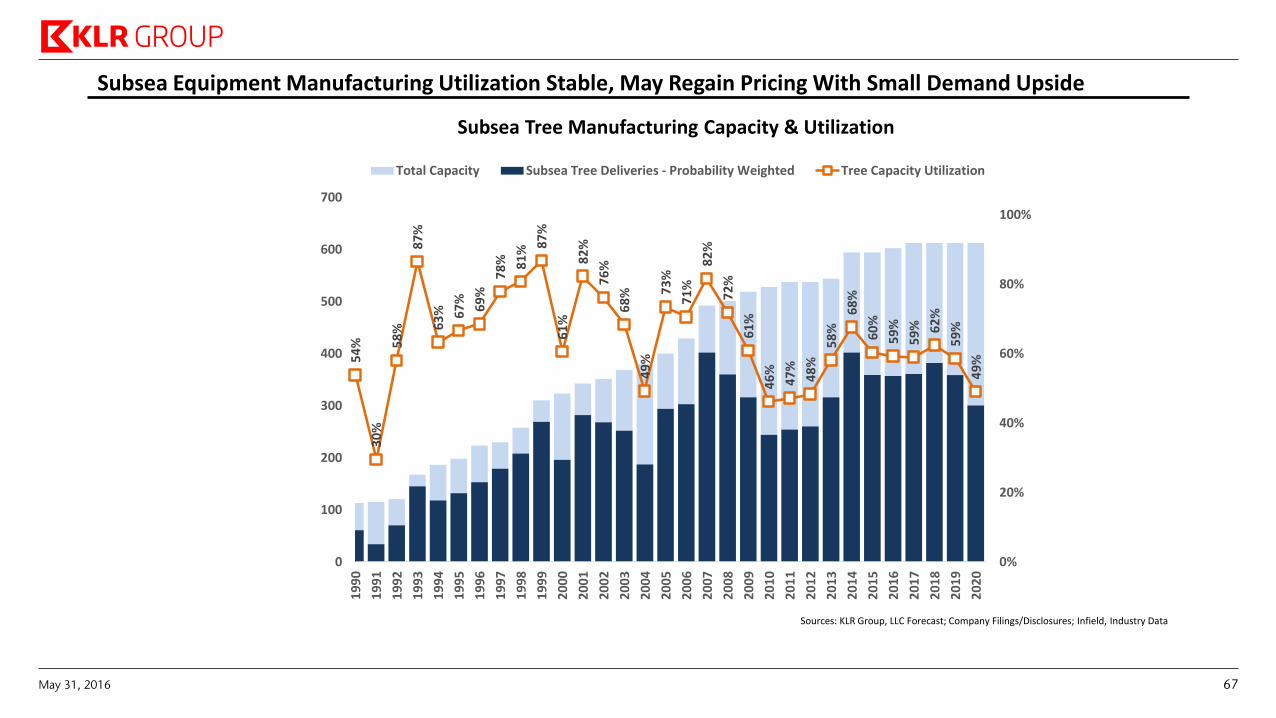

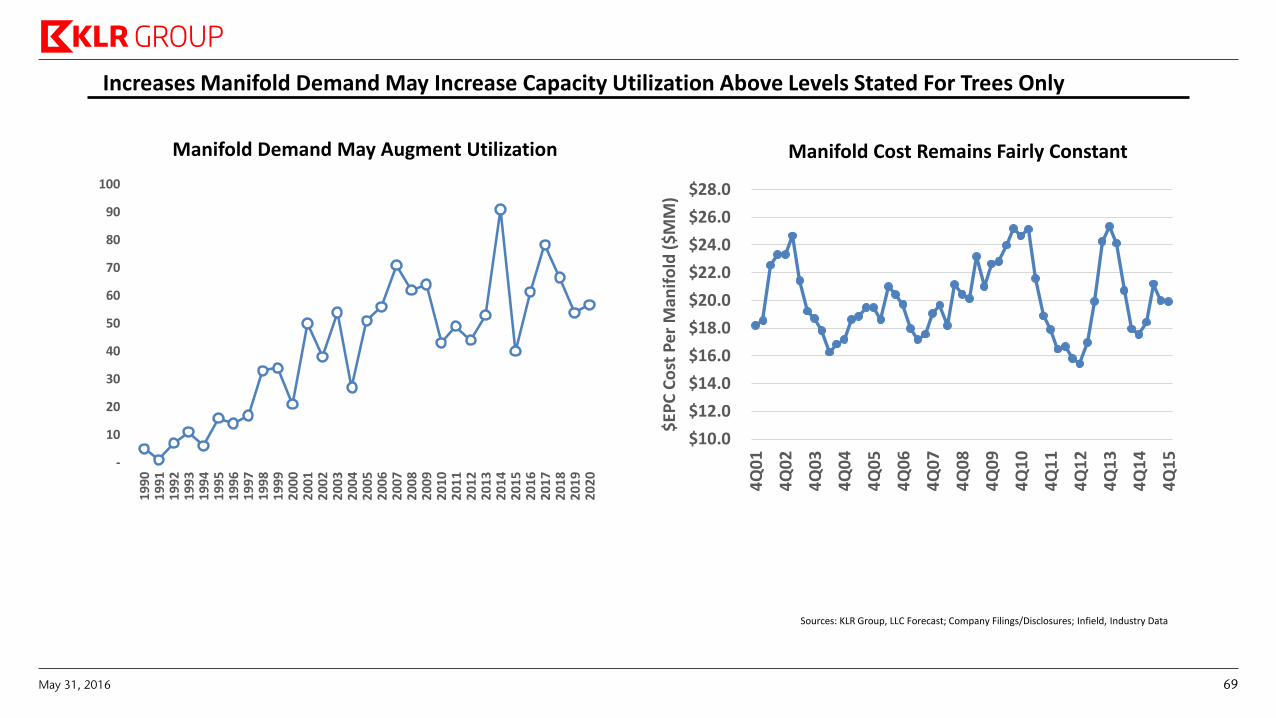

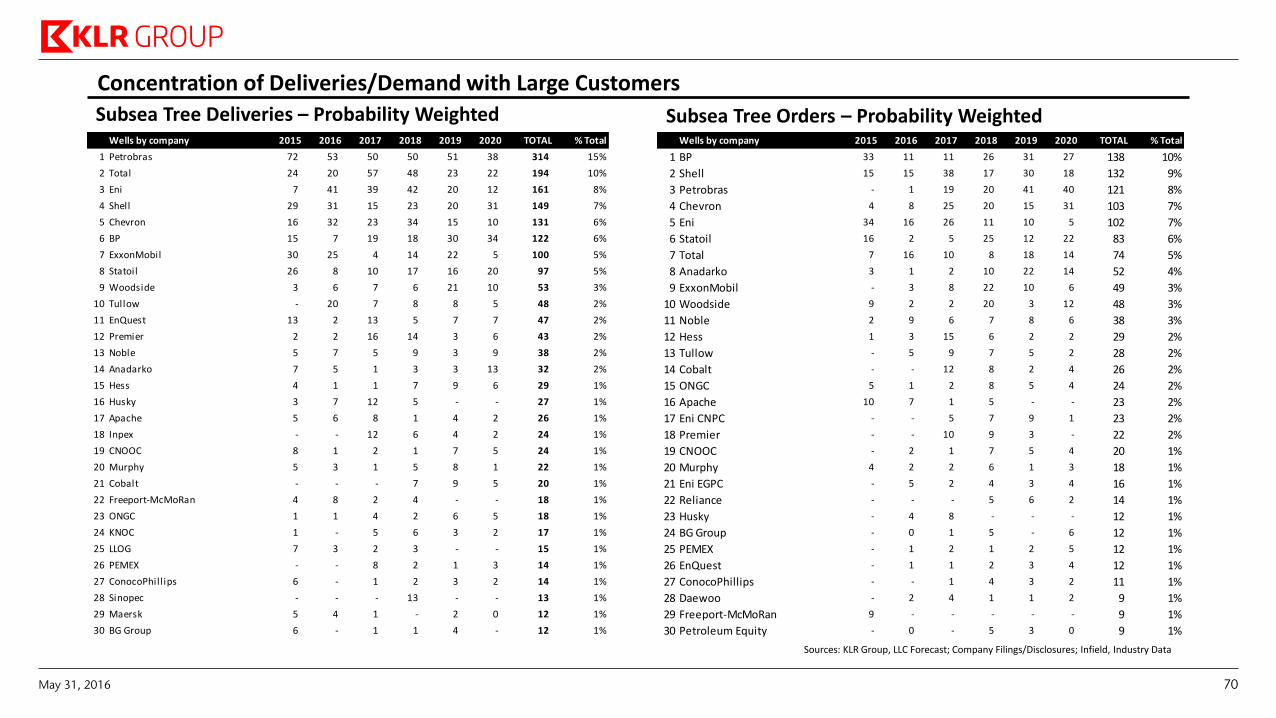

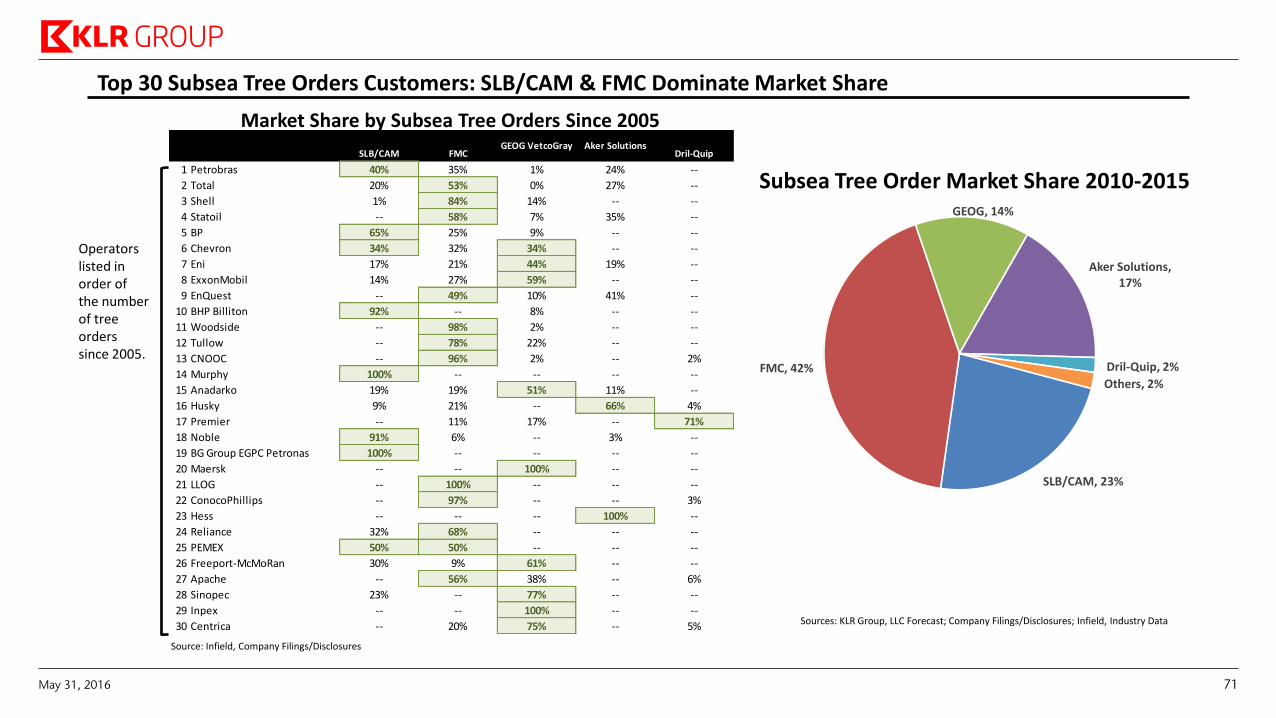

Subsea Equipment Demand Stable, Higher 2017 Tree Orders Should Improve Optics. The subsea equipment and offshore infrastructure portion of our coverage maintains a fairly constructive set up under our offshore forecast. Again, we see potential for low expectations to become more optimistic with a recovery in commodity prices and a reversal of revision momentum to pull project times forward versus push them later. Our subsea tree/equipment forecast maintains a stable delivery profile that is congruent with a flat development drilling demand outlook (pg. 31). Subsea tree orders remain low in 2016 (135, pg. 65), but move higher in 2017 to support future field developments in our forecast. Akin to floater development demand, our probability-weighted estimates remain largely tied to existing and approved projects, where near term forecasted deliveries in 2016 and 2017 have largely been ordered (pgs. 63). Our data shows a trend of costs per tree coming down, which supports the view that breakeven project costs are falling (pg. 62). As deepwater expands as part of the demand mix (pg. 66), development cost reductions may play a key role to pull forward demand that has slipped into later years and accelerate field developments with existing infrastructure. Non-probability weighted demand suggests potential for significant upside for new tree orders and deliveries in the event that our adjusted numbers prove conservative. We like exposure to NOV, FTI, and OIS for offshore exposure, with a bias to get more constructive on OII and DRQ.

May 31, 2016 2

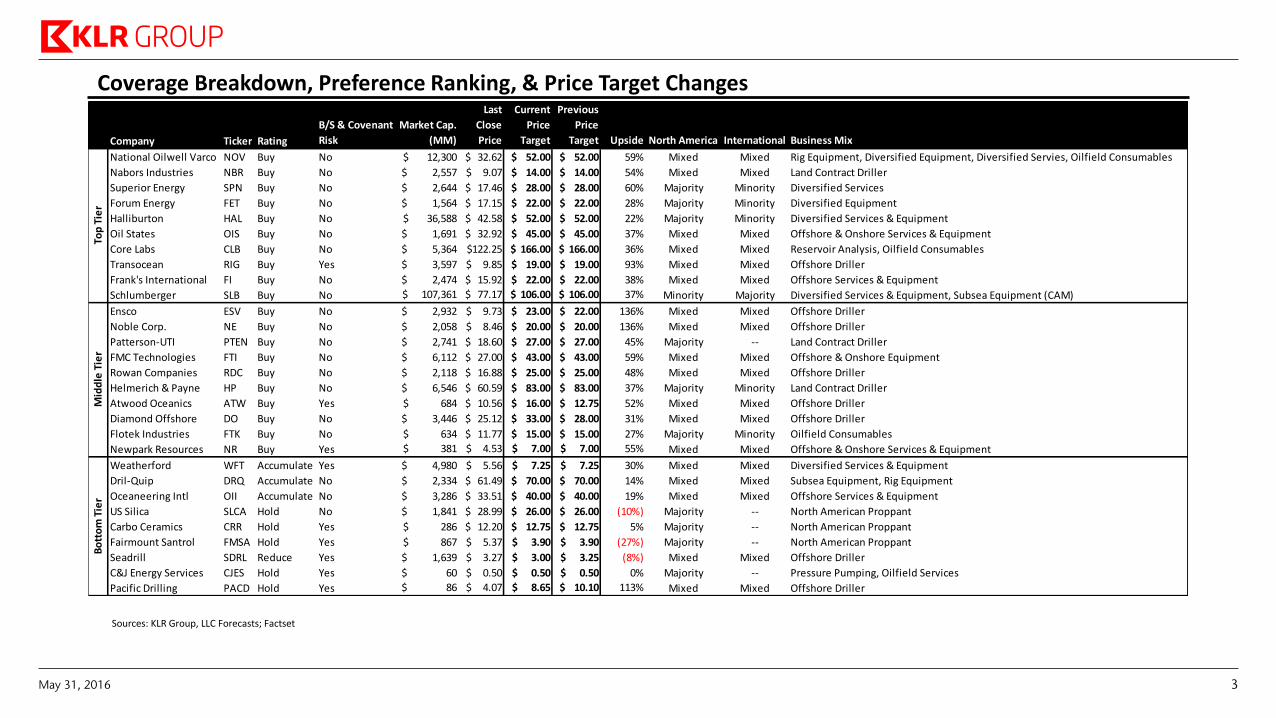

Coverage Breakdown, Preference Ranking, & Price Target Changes

Sources: KLR Group, LLC Forecasts; Factset

Company Ticker Rating

B/S & Covenant

Risk

Market Cap.

(MM)

Last

Close

Price

Current

Price

Target

Previous

Price

Target Upside North America International Business Mix

National Oilwell Varco NOV Buy No $ 12,300 $ 32.62 $ 52.00 $ 52.00 59% Mixed Mixed Rig Equipment, Diversified Equipment, Diversified Servies, Oilfield Consumables

Nabors Industries NBR Buy No $ 2,557 $ 9.07 $ 14.00 $ 14.00 54% Mixed Mixed Land Contract Driller

Superior Energy SPN Buy No $ 2,644 $ 17.46 $ 28.00 $ 28.00 60% Majority Minority Diversified Services

Forum Energy FET Buy No $ 1,564 $ 17.15 $ 22.00 $ 22.00 28% Majority Minority Diversified Equipment

Halliburton HAL Buy No $ 36,588 $ 42.58 $ 52.00 $ 52.00 22% Majority Minority Diversified Services & Equipment

Oil States OIS Buy No $ 1,691 $ 32.92 $ 45.00 $ 45.00 37% Mixed Mixed Offshore & Onshore Services & Equipment

Core Labs CLB Buy No $ 5,364 $122.25 $ 166.00 $ 166.00 36% Mixed Mixed Reservoir Analysis, Oilfield Consumables

Transocean RIG Buy Yes $ 3,597 $ 9.85 $ 19.00 $ 19.00 93% Mixed Mixed Offshore Driller

Frank's International FI Buy No $ 2,474 $ 15.92 $ 22.00 $ 22.00 38% Mixed Mixed Offshore Services & Equipment

Schlumberger SLB Buy No $ 107,361 $ 77.17 $ 106.00 $ 106.00 37% Minority Majority Diversified Services & Equipment, Subsea Equipment (CAM)

Ensco ESV Buy No $ 2,932 $ 9.73 $ 23.00 $ 22.00 136% Mixed Mixed Offshore Driller

Noble Corp. NE Buy No $ 2,058 $ 8.46 $ 20.00 $ 20.00 136% Mixed Mixed Offshore Driller

Patterson-UTI PTEN Buy No $ 2,741 $ 18.60 $ 27.00 $ 27.00 45% Majority -- Land Contract Driller

FMC Technologies FTI Buy No $ 6,112 $ 27.00 $ 43.00 $ 43.00 59% Mixed Mixed Offshore & Onshore Equipment

Rowan Companies RDC Buy No $ 2,118 $ 16.88 $ 25.00 $ 25.00 48% Mixed Mixed Offshore Driller

Helmerich & Payne HP Buy No $ 6,546 $ 60.59 $ 83.00 $ 83.00 37% Majority Minority Land Contract Driller

Atwood Oceanics ATW Buy Yes $ 684 $ 10.56 $ 16.00 $ 12.75 52% Mixed Mixed Offshore Driller

Diamond Offshore DO Buy No $ 3,446 $ 25.12 $ 33.00 $ 28.00 31% Mixed Mixed Offshore Driller

Flotek Industries FTK Buy No $ 634 $ 11.77 $ 15.00 $ 15.00 27% Majority Minority Oilfield Consumables

Newpark Resources NR Buy Yes $ 381 $ 4.53 $ 7.00 $ 7.00 55% Mixed Mixed Offshore & Onshore Services & Equipment

Weatherford WFT Accumulate Yes $ 4,980 $ 5.56 $ 7.25 $ 7.25 30% Mixed Mixed Diversified Services & Equipment

Dril-Quip DRQ Accumulate No $ 2,334 $ 61.49 $ 70.00 $ 70.00 14% Mixed Mixed Subsea Equipment, Rig Equipment

Oceaneering Intl OII Accumulate No $ 3,286 $ 33.51 $ 40.00 $ 40.00 19% Mixed Mixed Offshore Services & Equipment

US Silica SLCA Hold No $ 1,841 $ 28.99 $ 26.00 $ 26.00 (10%) Majority -- North American Proppant

Carbo Ceramics CRR Hold Yes $ 286 $ 12.20 $ 12.75 $ 12.75 5% Majority -- North American Proppant

Fairmount Santrol FMSA Hold Yes $ 867 $ 5.37 $ 3.90 $ 3.90 (27%) Majority -- North American Proppant

Seadrill SDRL Reduce Yes $ 1,639 $ 3.27 $ 3.00 $ 3.25 (8%) Mixed Mixed Offshore Driller

C&J Energy Services CJES Hold Yes $ 60 $ 0.50 $ 0.50 $ 0.50 0% Majority -- Pressure Pumping, Oilfield Services

Pacific Drilling PACD Hold Yes $ 86 $ 4.07 $ 8.65 $ 10.10 113% Mixed Mixed Offshore Driller

Top

Tie

rM

idd

le T

ier

Bo

tto

m T

ier

May 31, 2016 3

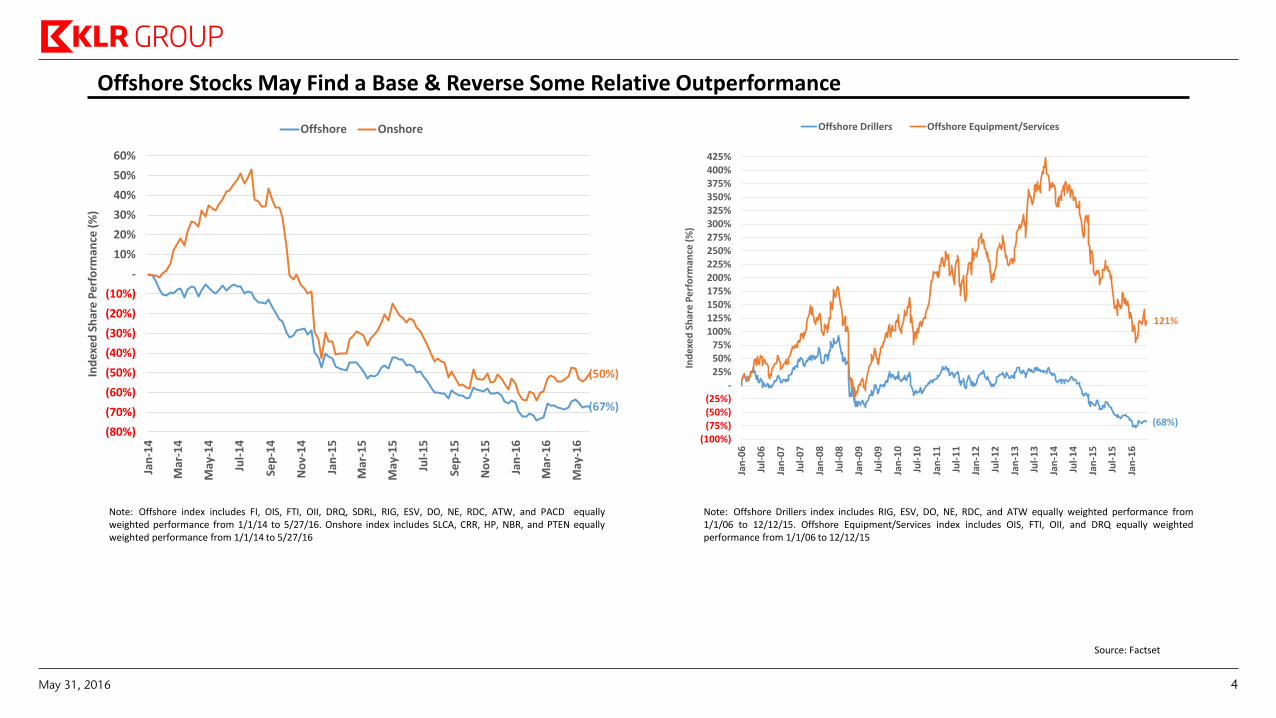

Offshore Stocks May Find a Base & Reverse Some Relative Outperformance

(68%)

121%

(100%) (75%) (50%) (25%)

-25%50%75%

100%125%150%175%200%225%250%275%300%325%350%375%400%425%

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Jan

-16

Ind

exe

d S

har

e P

erf

orm

ance

(%

)

Offshore Drillers Offshore Equipment/Services

(67%)

(50%)

(80%)

(70%)

(60%)

(50%)

(40%)

(30%)

(20%)

(10%)

-

10%

20%

30%

40%

50%

60%Ja

n-1

4

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

May

-16

Ind

exe

d S

har

e P

erf

orm

ance

(%

)

Offshore Onshore

Note: Offshore index includes FI, OIS, FTI, OII, DRQ, SDRL, RIG, ESV, DO, NE, RDC, ATW, and PACD equally weighted performance from 1/1/14 to 5/27/16. Onshore index includes SLCA, CRR, HP, NBR, and PTEN equally weighted performance from 1/1/14 to 5/27/16

Source: Factset

Note: Offshore Drillers index includes RIG, ESV, DO, NE, RDC, and ATW equally weighted performance from 1/1/06 to 12/12/15. Offshore Equipment/Services index includes OIS, FTI, OII, and DRQ equally weighted performance from 1/1/06 to 12/12/15

May 31, 2016 4

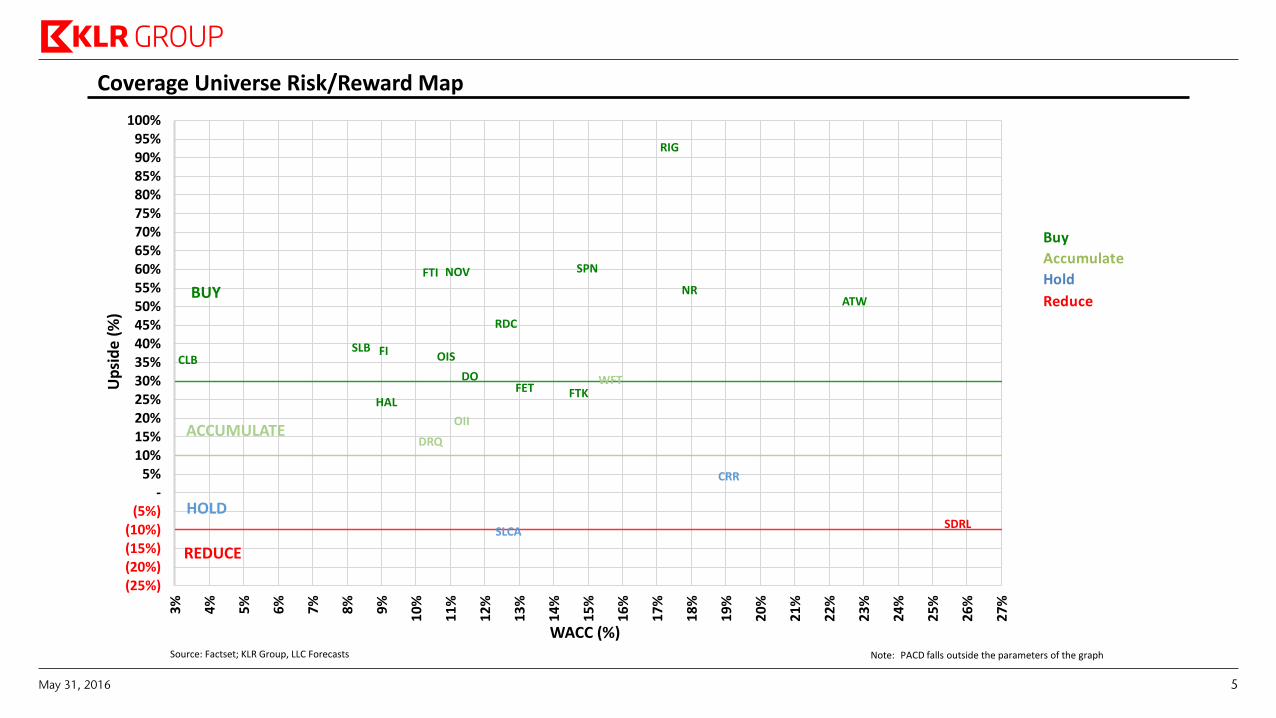

Coverage Universe Risk/Reward Map

Source: Factset; KLR Group, LLC Forecasts

Buy

Accumulate

Hold

Reduce

Note: PACD falls outside the parameters of the graph

ACCUMULATE

BUY

SLB

HAL

CLBFI

NR

OIS

FTK

NOVFTI

FET

RIG

DO

RDC

ATW

SPN

WFT

OII

DRQ

SLCA

CRR

SDRL

HOLD

REDUCE

(25%)(20%)(15%)(10%)

(5%)-

5%10%15%20%25%30%35%40%45%50%55%60%65%70%75%80%85%90%95%

100%

3%

4%

5%

6%

7%

8%

9%

10

%

11

%

12

%

13

%

14

%

15

%

16

%

17

%

18

%

19

%

20

%

21

%

22

%

23

%

24

%

25

%

26

%

27

%

Up

sid

e (

%)

WACC (%)

May 31, 2016 5

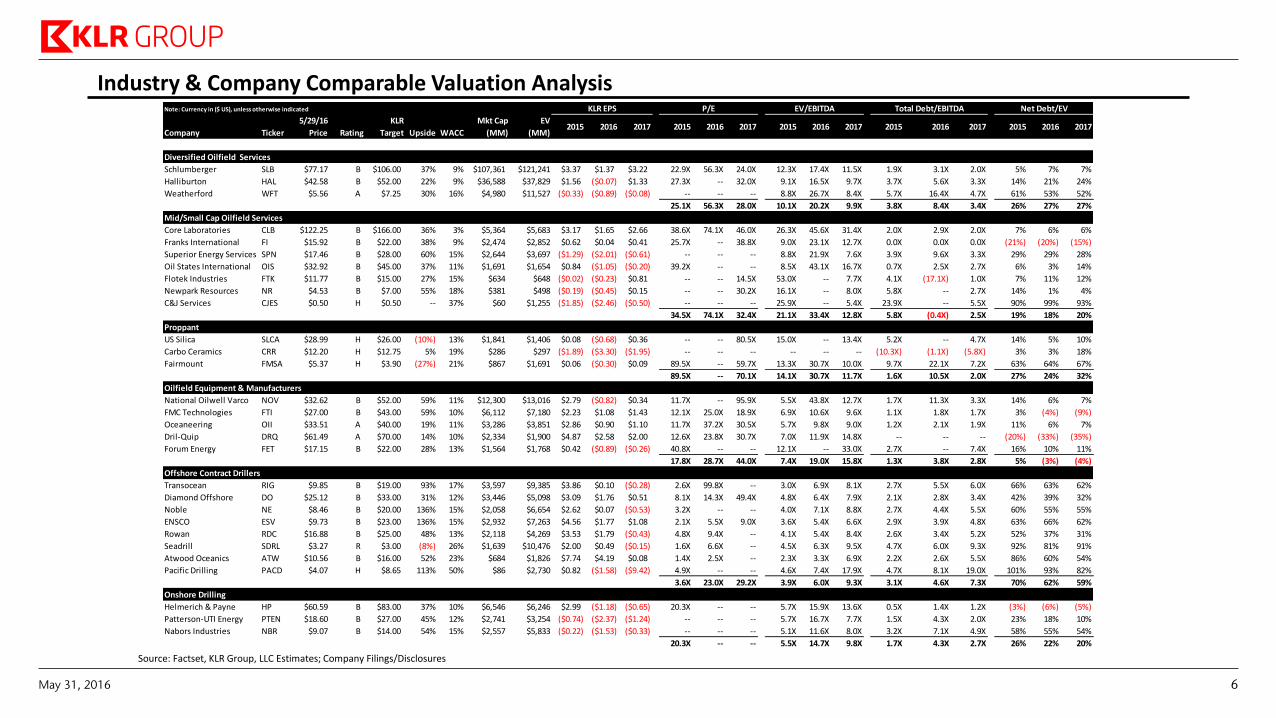

Industry & Company Comparable Valuation Analysis

Source: Factset, KLR Group, LLC Estimates; Company Filings/Disclosures

Note: Currency in ($ US), unless otherwise indicated

Company Ticker

5/29/16

Price Rating

KLR

Target Upside WACC

Mkt Cap

(MM)

EV

(MM)2015 2016 2017 2015 2016 2017 2015 2016 2017 2015 2016 2017 2015 2016 2017

Diversified Oilfield Services

Schlumberger SLB $77.17 B $106.00 37% 9% $107,361 $121,241 $3.37 $1.37 $3.22 22.9X 56.3X 24.0X 12.3X 17.4X 11.5X 1.9X 3.1X 2.0X 5% 7% 7%

Halliburton HAL $42.58 B $52.00 22% 9% $36,588 $37,829 $1.56 ($0.07) $1.33 27.3X -- 32.0X 9.1X 16.5X 9.7X 3.7X 5.6X 3.3X 14% 21% 24%

Weatherford WFT $5.56 A $7.25 30% 16% $4,980 $11,527 ($0.33) ($0.89) ($0.08) -- -- -- 8.8X 26.7X 8.4X 5.7X 16.4X 4.7X 61% 53% 52%

25.1X 56.3X 28.0X 10.1X 20.2X 9.9X 3.8X 8.4X 3.4X 26% 27% 27%

Mid/Small Cap Oilfield Services

Core Laboratories CLB $122.25 B $166.00 36% 3% $5,364 $5,683 $3.17 $1.65 $2.66 38.6X 74.1X 46.0X 26.3X 45.6X 31.4X 2.0X 2.9X 2.0X 7% 6% 6%

Franks International FI $15.92 B $22.00 38% 9% $2,474 $2,852 $0.62 $0.04 $0.41 25.7X -- 38.8X 9.0X 23.1X 12.7X 0.0X 0.0X 0.0X (21%) (20%) (15%)

Superior Energy Services SPN $17.46 B $28.00 60% 15% $2,644 $3,697 ($1.29) ($2.01) ($0.61) -- -- -- 8.8X 21.9X 7.6X 3.9X 9.6X 3.3X 29% 29% 28%

Oil States International OIS $32.92 B $45.00 37% 11% $1,691 $1,654 $0.84 ($1.05) ($0.20) 39.2X -- -- 8.5X 43.1X 16.7X 0.7X 2.5X 2.7X 6% 3% 14%

Flotek Industries FTK $11.77 B $15.00 27% 15% $634 $648 ($0.02) ($0.23) $0.81 -- -- 14.5X 53.0X -- 7.7X 4.1X (17.1X) 1.0X 7% 11% 12%

Newpark Resources NR $4.53 B $7.00 55% 18% $381 $498 ($0.19) ($0.45) $0.15 -- -- 30.2X 16.1X -- 8.0X 5.8X -- 2.7X 14% 1% 4%

C&J Services CJES $0.50 H $0.50 -- 37% $60 $1,255 ($1.85) ($2.46) ($0.50) -- -- -- 25.9X -- 5.4X 23.9X -- 5.5X 90% 99% 93%

34.5X 74.1X 32.4X 21.1X 33.4X 12.8X 5.8X (0.4X) 2.5X 19% 18% 20%

Proppant

US Silica SLCA $28.99 H $26.00 (10%) 13% $1,841 $1,406 $0.08 ($0.68) $0.36 -- -- 80.5X 15.0X -- 13.4X 5.2X -- 4.7X 14% 5% 10%

Carbo Ceramics CRR $12.20 H $12.75 5% 19% $286 $297 ($1.89) ($3.30) ($1.95) -- -- -- -- -- -- (10.3X) (1.1X) (5.8X) 3% 3% 18%

Fairmount FMSA $5.37 H $3.90 (27%) 21% $867 $1,691 $0.06 ($0.30) $0.09 89.5X -- 59.7X 13.3X 30.7X 10.0X 9.7X 22.1X 7.2X 63% 64% 67%

89.5X -- 70.1X 14.1X 30.7X 11.7X 1.6X 10.5X 2.0X 27% 24% 32%

Oilfield Equipment & Manufacturers

National Oilwell Varco NOV $32.62 B $52.00 59% 11% $12,300 $13,016 $2.79 ($0.82) $0.34 11.7X -- 95.9X 5.5X 43.8X 12.7X 1.7X 11.3X 3.3X 14% 6% 7%

FMC Technologies FTI $27.00 B $43.00 59% 10% $6,112 $7,180 $2.23 $1.08 $1.43 12.1X 25.0X 18.9X 6.9X 10.6X 9.6X 1.1X 1.8X 1.7X 3% (4%) (9%)

Oceaneering OII $33.51 A $40.00 19% 11% $3,286 $3,851 $2.86 $0.90 $1.10 11.7X 37.2X 30.5X 5.7X 9.8X 9.0X 1.2X 2.1X 1.9X 11% 6% 7%

Dril-Quip DRQ $61.49 A $70.00 14% 10% $2,334 $1,900 $4.87 $2.58 $2.00 12.6X 23.8X 30.7X 7.0X 11.9X 14.8X -- -- -- (20%) (33%) (35%)

Forum Energy FET $17.15 B $22.00 28% 13% $1,564 $1,768 $0.42 ($0.89) ($0.26) 40.8X -- -- 12.1X -- 33.0X 2.7X -- 7.4X 16% 10% 11%

17.8X 28.7X 44.0X 7.4X 19.0X 15.8X 1.3X 3.8X 2.8X 5% (3%) (4%)

Offshore Contract Drillers

Transocean RIG $9.85 B $19.00 93% 17% $3,597 $9,385 $3.86 $0.10 ($0.28) 2.6X 99.8X -- 3.0X 6.9X 8.1X 2.7X 5.5X 6.0X 66% 63% 62%

Diamond Offshore DO $25.12 B $33.00 31% 12% $3,446 $5,098 $3.09 $1.76 $0.51 8.1X 14.3X 49.4X 4.8X 6.4X 7.9X 2.1X 2.8X 3.4X 42% 39% 32%

Noble NE $8.46 B $20.00 136% 15% $2,058 $6,654 $2.62 $0.07 ($0.53) 3.2X -- -- 4.0X 7.1X 8.8X 2.7X 4.4X 5.5X 60% 55% 55%

ENSCO ESV $9.73 B $23.00 136% 15% $2,932 $7,263 $4.56 $1.77 $1.08 2.1X 5.5X 9.0X 3.6X 5.4X 6.6X 2.9X 3.9X 4.8X 63% 66% 62%

Rowan RDC $16.88 B $25.00 48% 13% $2,118 $4,269 $3.53 $1.79 ($0.43) 4.8X 9.4X -- 4.1X 5.4X 8.4X 2.6X 3.4X 5.2X 52% 37% 31%

Seadrill SDRL $3.27 R $3.00 (8%) 26% $1,639 $10,476 $2.00 $0.49 ($0.15) 1.6X 6.6X -- 4.5X 6.3X 9.5X 4.7X 6.0X 9.3X 92% 81% 91%

Atwood Oceanics ATW $10.56 B $16.00 52% 23% $684 $1,826 $7.74 $4.19 $0.08 1.4X 2.5X -- 2.3X 3.3X 6.9X 2.2X 2.6X 5.5X 86% 60% 54%

Pacific Drilling PACD $4.07 H $8.65 113% 50% $86 $2,730 $0.82 ($1.58) ($9.42) 4.9X -- -- 4.6X 7.4X 17.9X 4.7X 8.1X 19.0X 101% 93% 82%

3.6X 23.0X 29.2X 3.9X 6.0X 9.3X 3.1X 4.6X 7.3X 70% 62% 59%

Onshore Drilling

Helmerich & Payne HP $60.59 B $83.00 37% 10% $6,546 $6,246 $2.99 ($1.18) ($0.65) 20.3X -- -- 5.7X 15.9X 13.6X 0.5X 1.4X 1.2X (3%) (6%) (5%)

Patterson-UTI Energy PTEN $18.60 B $27.00 45% 12% $2,741 $3,254 ($0.74) ($2.37) ($1.24) -- -- -- 5.7X 16.7X 7.7X 1.5X 4.3X 2.0X 23% 18% 10%

Nabors Industries NBR $9.07 B $14.00 54% 15% $2,557 $5,833 ($0.22) ($1.53) ($0.33) -- -- -- 5.1X 11.6X 8.0X 3.2X 7.1X 4.9X 58% 55% 54%

20.3X -- -- 5.5X 14.7X 9.8X 1.7X 4.3X 2.7X 26% 22% 20%

KLR EPS P/E EV/EBITDA Total Debt/EBITDA Net Debt/EV

May 31, 2016 6

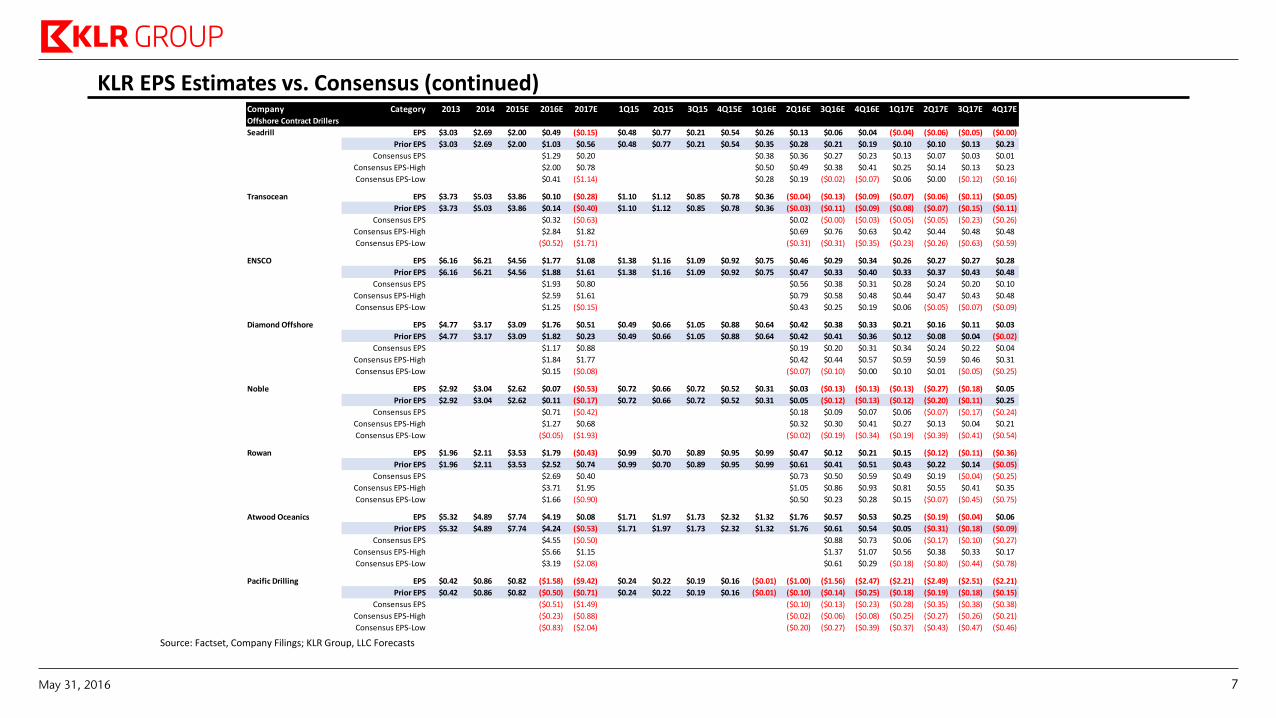

KLR EPS Estimates vs. Consensus (continued)

Source: Factset, Company Filings; KLR Group, LLC Forecasts

Company Category 2013 2014 2015E 2016E 2017E 1Q15 2Q15 3Q15 4Q15E 1Q16E 2Q16E 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17EOffshore Contract Drillers

Seadrill EPS $3.03 $2.69 $2.00 $0.49 ($0.15) $0.48 $0.77 $0.21 $0.54 $0.26 $0.13 $0.06 $0.04 ($0.04) ($0.06) ($0.05) ($0.00)

Prior EPS $3.03 $2.69 $2.00 $1.03 $0.56 $0.48 $0.77 $0.21 $0.54 $0.35 $0.28 $0.21 $0.19 $0.10 $0.10 $0.13 $0.23

Consensus EPS $1.29 $0.20 $0.38 $0.36 $0.27 $0.23 $0.13 $0.07 $0.03 $0.01

Consensus EPS-High $2.00 $0.78 $0.50 $0.49 $0.38 $0.41 $0.25 $0.14 $0.13 $0.23

Consensus EPS-Low $0.41 ($1.14) $0.28 $0.19 ($0.02) ($0.07) $0.06 $0.00 ($0.12) ($0.16)

Transocean EPS $3.73 $5.03 $3.86 $0.10 ($0.28) $1.10 $1.12 $0.85 $0.78 $0.36 ($0.04) ($0.13) ($0.09) ($0.07) ($0.06) ($0.11) ($0.05)

Prior EPS $3.73 $5.03 $3.86 $0.14 ($0.40) $1.10 $1.12 $0.85 $0.78 $0.36 ($0.03) ($0.11) ($0.09) ($0.08) ($0.07) ($0.15) ($0.11)

Consensus EPS $0.32 ($0.63) $0.02 ($0.00) ($0.03) ($0.05) ($0.05) ($0.23) ($0.26)

Consensus EPS-High $2.84 $1.82 $0.69 $0.76 $0.63 $0.42 $0.44 $0.48 $0.48

Consensus EPS-Low ($0.52) ($1.71) ($0.31) ($0.31) ($0.35) ($0.23) ($0.26) ($0.63) ($0.59)

ENSCO EPS $6.16 $6.21 $4.56 $1.77 $1.08 $1.38 $1.16 $1.09 $0.92 $0.75 $0.46 $0.29 $0.34 $0.26 $0.27 $0.27 $0.28

Prior EPS $6.16 $6.21 $4.56 $1.88 $1.61 $1.38 $1.16 $1.09 $0.92 $0.75 $0.47 $0.33 $0.40 $0.33 $0.37 $0.43 $0.48

Consensus EPS $1.93 $0.80 $0.56 $0.38 $0.31 $0.28 $0.24 $0.20 $0.10

Consensus EPS-High $2.59 $1.61 $0.79 $0.58 $0.48 $0.44 $0.47 $0.43 $0.48

Consensus EPS-Low $1.25 ($0.15) $0.43 $0.25 $0.19 $0.06 ($0.05) ($0.07) ($0.09)

Diamond Offshore EPS $4.77 $3.17 $3.09 $1.76 $0.51 $0.49 $0.66 $1.05 $0.88 $0.64 $0.42 $0.38 $0.33 $0.21 $0.16 $0.11 $0.03

Prior EPS $4.77 $3.17 $3.09 $1.82 $0.23 $0.49 $0.66 $1.05 $0.88 $0.64 $0.42 $0.41 $0.36 $0.12 $0.08 $0.04 ($0.02)

Consensus EPS $1.17 $0.88 $0.19 $0.20 $0.31 $0.34 $0.24 $0.22 $0.04

Consensus EPS-High $1.84 $1.77 $0.42 $0.44 $0.57 $0.59 $0.59 $0.46 $0.31

Consensus EPS-Low $0.15 ($0.08) ($0.07) ($0.10) $0.00 $0.10 $0.01 ($0.05) ($0.25)

Noble EPS $2.92 $3.04 $2.62 $0.07 ($0.53) $0.72 $0.66 $0.72 $0.52 $0.31 $0.03 ($0.13) ($0.13) ($0.13) ($0.27) ($0.18) $0.05

Prior EPS $2.92 $3.04 $2.62 $0.11 ($0.17) $0.72 $0.66 $0.72 $0.52 $0.31 $0.05 ($0.12) ($0.13) ($0.12) ($0.20) ($0.11) $0.25

Consensus EPS $0.71 ($0.42) $0.18 $0.09 $0.07 $0.06 ($0.07) ($0.17) ($0.24)

Consensus EPS-High $1.27 $0.68 $0.32 $0.30 $0.41 $0.27 $0.13 $0.04 $0.21

Consensus EPS-Low ($0.05) ($1.93) ($0.02) ($0.19) ($0.34) ($0.19) ($0.39) ($0.41) ($0.54)

Rowan EPS $1.96 $2.11 $3.53 $1.79 ($0.43) $0.99 $0.70 $0.89 $0.95 $0.99 $0.47 $0.12 $0.21 $0.15 ($0.12) ($0.11) ($0.36)

Prior EPS $1.96 $2.11 $3.53 $2.52 $0.74 $0.99 $0.70 $0.89 $0.95 $0.99 $0.61 $0.41 $0.51 $0.43 $0.22 $0.14 ($0.05)

Consensus EPS $2.69 $0.40 $0.73 $0.50 $0.59 $0.49 $0.19 ($0.04) ($0.25)

Consensus EPS-High $3.71 $1.95 $1.05 $0.86 $0.93 $0.81 $0.55 $0.41 $0.35

Consensus EPS-Low $1.66 ($0.90) $0.50 $0.23 $0.28 $0.15 ($0.07) ($0.45) ($0.75)

Atwood Oceanics EPS $5.32 $4.89 $7.74 $4.19 $0.08 $1.71 $1.97 $1.73 $2.32 $1.32 $1.76 $0.57 $0.53 $0.25 ($0.19) ($0.04) $0.06

Prior EPS $5.32 $4.89 $7.74 $4.24 ($0.53) $1.71 $1.97 $1.73 $2.32 $1.32 $1.76 $0.61 $0.54 $0.05 ($0.31) ($0.18) ($0.09)

Consensus EPS $4.55 ($0.50) $0.88 $0.73 $0.06 ($0.17) ($0.10) ($0.27)

Consensus EPS-High $5.66 $1.15 $1.37 $1.07 $0.56 $0.38 $0.33 $0.17

Consensus EPS-Low $3.19 ($2.08) $0.61 $0.29 ($0.18) ($0.80) ($0.44) ($0.78)

Pacific Drilling EPS $0.42 $0.86 $0.82 ($1.58) ($9.42) $0.24 $0.22 $0.19 $0.16 ($0.01) ($1.00) ($1.56) ($2.47) ($2.21) ($2.49) ($2.51) ($2.21)

Prior EPS $0.42 $0.86 $0.82 ($0.50) ($0.71) $0.24 $0.22 $0.19 $0.16 ($0.01) ($0.10) ($0.14) ($0.25) ($0.18) ($0.19) ($0.18) ($0.15)

Consensus EPS ($0.51) ($1.49) ($0.10) ($0.13) ($0.23) ($0.28) ($0.35) ($0.38) ($0.38)

Consensus EPS-High ($0.23) ($0.88) ($0.02) ($0.06) ($0.08) ($0.25) ($0.27) ($0.26) ($0.21)

Consensus EPS-Low ($0.83) ($2.04) ($0.20) ($0.27) ($0.39) ($0.37) ($0.43) ($0.47) ($0.46)

May 31, 2016 7

RIG

DO

NE

ESV

RDC

SDRL

ATW

PACD

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

15% 20% 25% 30% 35% 40% 45% 50%

Net

De

bt

/ EV

Net Debt / Capital

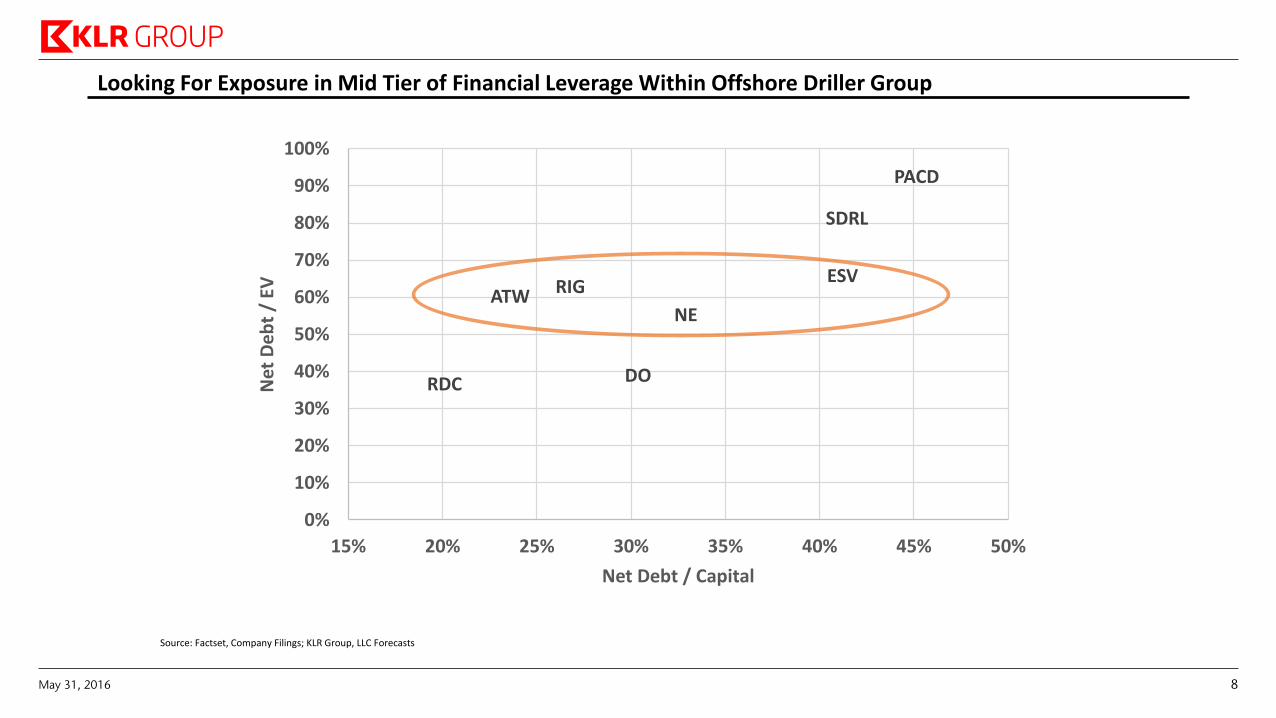

Looking For Exposure in Mid Tier of Financial Leverage Within Offshore Driller Group

Source: Factset, Company Filings; KLR Group, LLC Forecasts

May 31, 2016 8

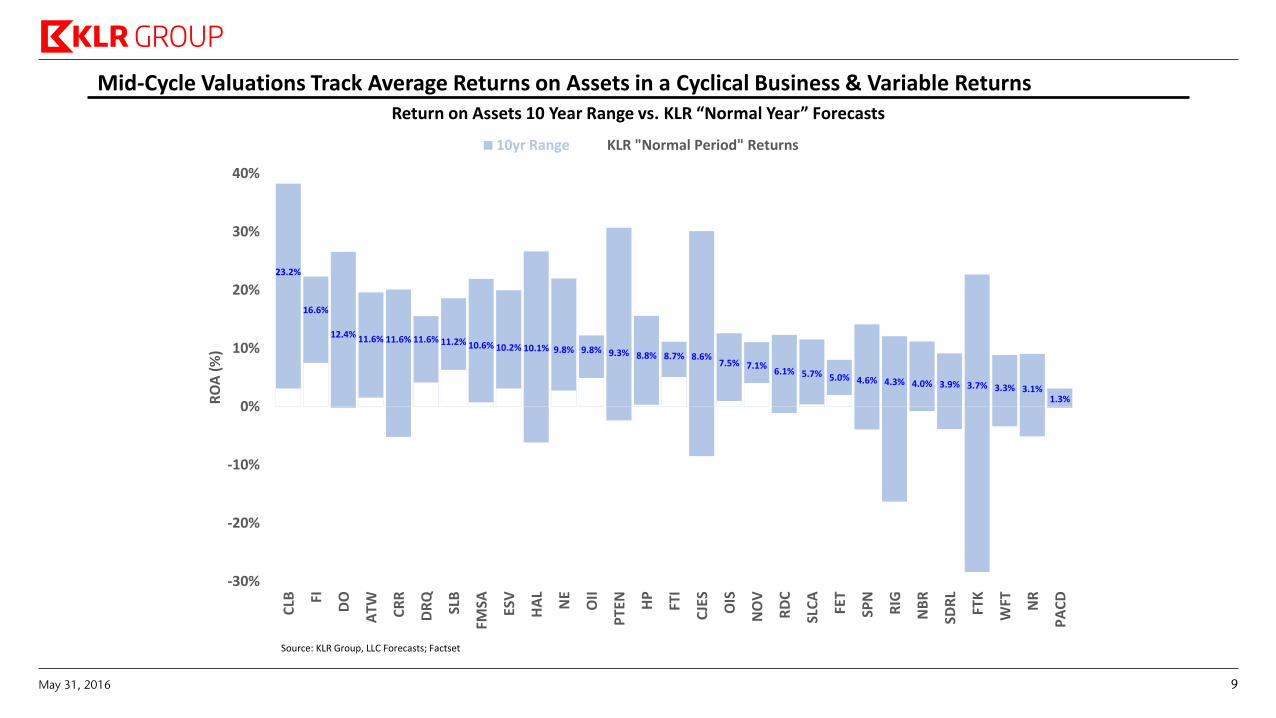

Mid-Cycle Valuations Track Average Returns on Assets in a Cyclical Business & Variable Returns

Source: KLR Group, LLC Forecasts; Factset

Return on Assets 10 Year Range vs. KLR “Normal Year” Forecasts

23.2%

16.6%

12.4% 11.6% 11.6% 11.6% 11.2% 10.6% 10.2% 10.1% 9.8% 9.8% 9.3% 8.8% 8.7% 8.6%7.5% 7.1%

6.1% 5.7% 5.0% 4.6% 4.3% 4.0% 3.9% 3.7% 3.3% 3.1%1.3%

-30%

-20%

-10%

0%

10%

20%

30%

40%

CLB FI

DO

ATW CR

R

DR

Q

SLB

FMSA ES

V

HA

L

NE

OII

PTE

N

HP

FTI

CJE

S

OIS

NO

V

RD

C

SLC

A

FET

SPN

RIG

NB

R

SDR

L

FTK

WFT NR

PA

CD

RO

A (

%)

10yr Range KLR "Normal Period" Returns

May 31, 2016 9

Potential Upside from De-Risking & Re-Rating

May 31, 2016 10

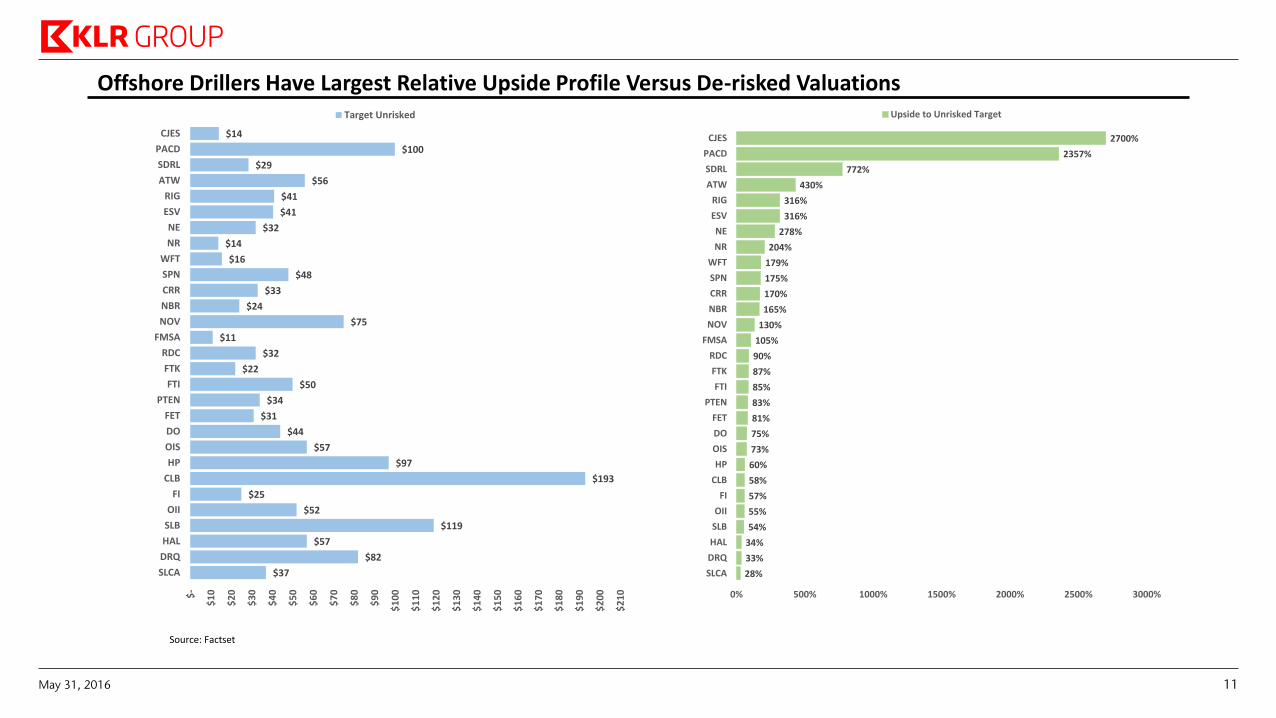

$37

$82

$57

$119

$52

$25

$193

$97

$57

$44

$31

$34

$50

$22

$32

$11

$75

$24

$33

$48

$16

$14

$32

$41

$41

$56

$29

$100

$14

$-

$1

0

$2

0

$3

0

$4

0

$5

0

$6

0

$7

0

$8

0

$9

0

$1

00

$1

10

$1

20

$1

30

$1

40

$1

50

$1

60

$1

70

$1

80

$1

90

$2

00

$2

10

SLCA

DRQ

HAL

SLB

OII

FI

CLB

HP

OIS

DO

FET

PTEN

FTI

FTK

RDC

FMSA

NOV

NBR

CRR

SPN

WFT

NR

NE

ESV

RIG

ATW

SDRL

PACD

CJES

Target Unrisked

Offshore Drillers Have Largest Relative Upside Profile Versus De-risked Valuations

Source: Factset

28%

33%

34%

54%

55%

57%

58%

60%

73%

75%

81%

83%

85%

87%

90%

105%

130%

165%

170%

175%

179%

204%

278%

316%

316%

430%

772%

2357%

2700%

0% 500% 1000% 1500% 2000% 2500% 3000%

SLCA

DRQ

HAL

SLB

OII

FI

CLB

HP

OIS

DO

FET

PTEN

FTI

FTK

RDC

FMSA

NOV

NBR

CRR

SPN

WFT

NR

NE

ESV

RIG

ATW

SDRL

PACD

CJES

Upside to Unrisked Target

May 31, 2016 11

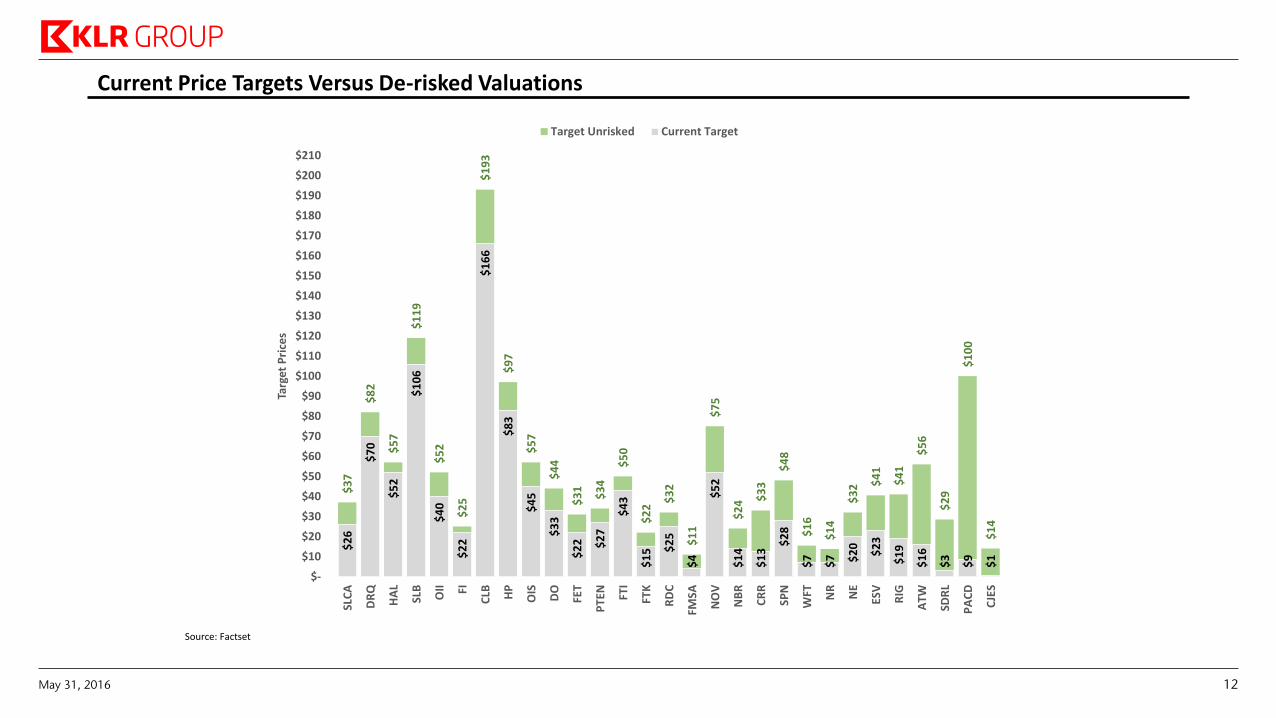

Current Price Targets Versus De-risked Valuations

Source: Factset

$3

7

$8

2

$5

7

$1

19

$5

2

$2

5

$1

93

$9

7

$5

7

$4

4

$3

1

$3

4

$5

0

$2

2 $

32

$1

1

$7

5

$2

4 $3

3

$4

8

$1

6

$1

4

$3

2 $4

1

$4

1

$5

6

$2

9

$1

00

$1

4

$2

6

$7

0

$5

2

$1

06

$4

0

$2

2

$1

66

$8

3

$4

5

$3

3

$2

2

$2

7

$4

3

$1

5 $2

5

$4

$5

2

$1

4

$1

3 $

28

$7

$7

$2

0

$2

3

$1

9

$1

6

$3

$9

$1

$-

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

$140

$150

$160

$170

$180

$190

$200

$210

SLC

A

DR

Q

HA

L

SLB

OII FI

CLB HP

OIS

DO

FET

PTE

N

FTI

FTK

RD

C

FMSA

NO

V

NB

R

CR

R

SPN

WFT NR

NE

ESV

RIG

ATW

SDR

L

PA

CD

CJE

S

Targ

et P

rice

s

Target Unrisked Current Target

May 31, 2016 12

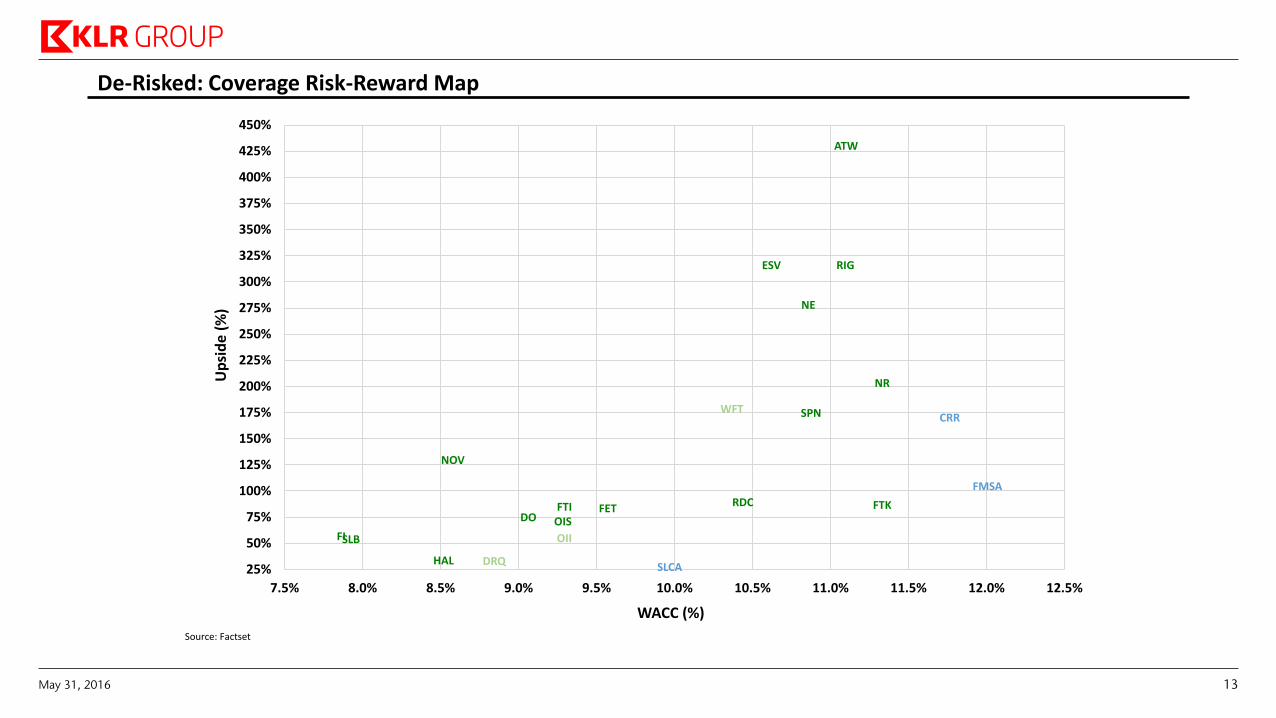

De-Risked: Coverage Risk-Reward Map

Source: Factset

HAL

SLB FI OISDO

FET FTI FTKRDC

NOV

SPN

NR

NE

ESV RIG

ATW

DRQ

OII

WFT

SLCA

FMSA

CRR

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

275%

300%

325%

350%

375%

400%

425%

450%

7.5% 8.0% 8.5% 9.0% 9.5% 10.0% 10.5% 11.0% 11.5% 12.0% 12.5%

Up

sid

e (

%)

WACC (%)

May 31, 2016 13

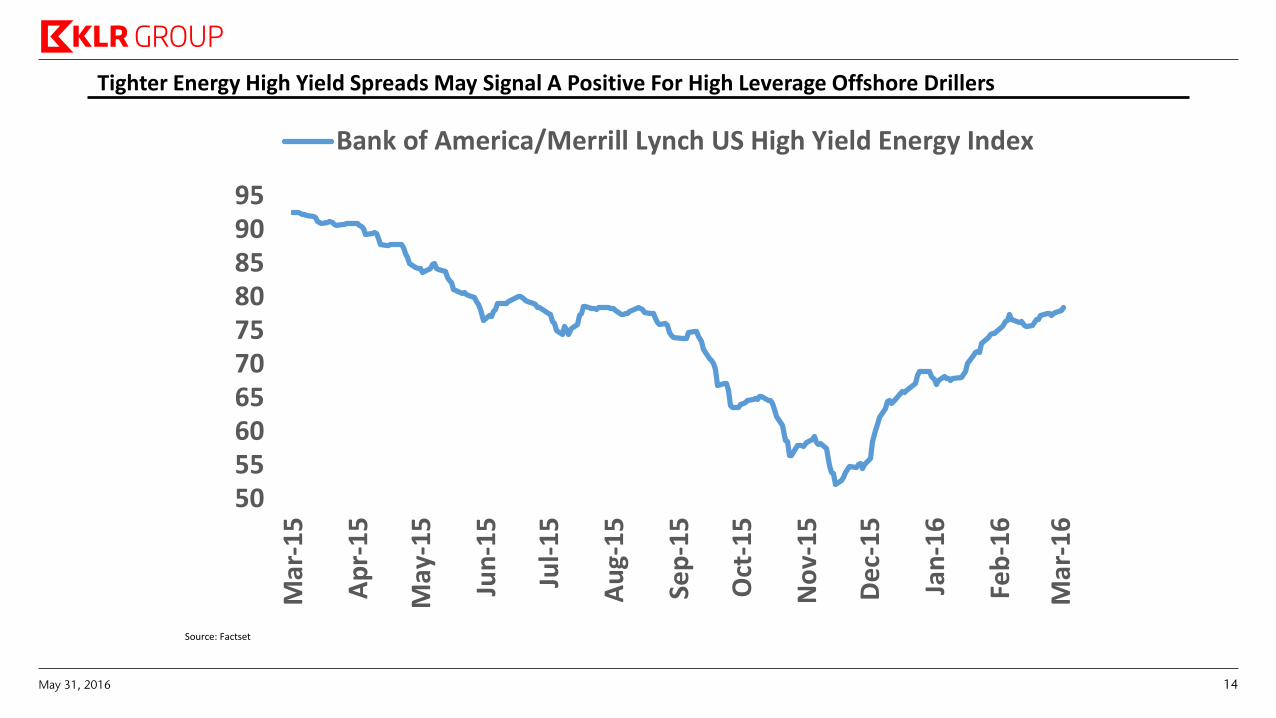

Tighter Energy High Yield Spreads May Signal A Positive For High Leverage Offshore Drillers

Source: Factset

50556065707580859095

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Bank of America/Merrill Lynch US High Yield Energy Index

May 31, 2016 14

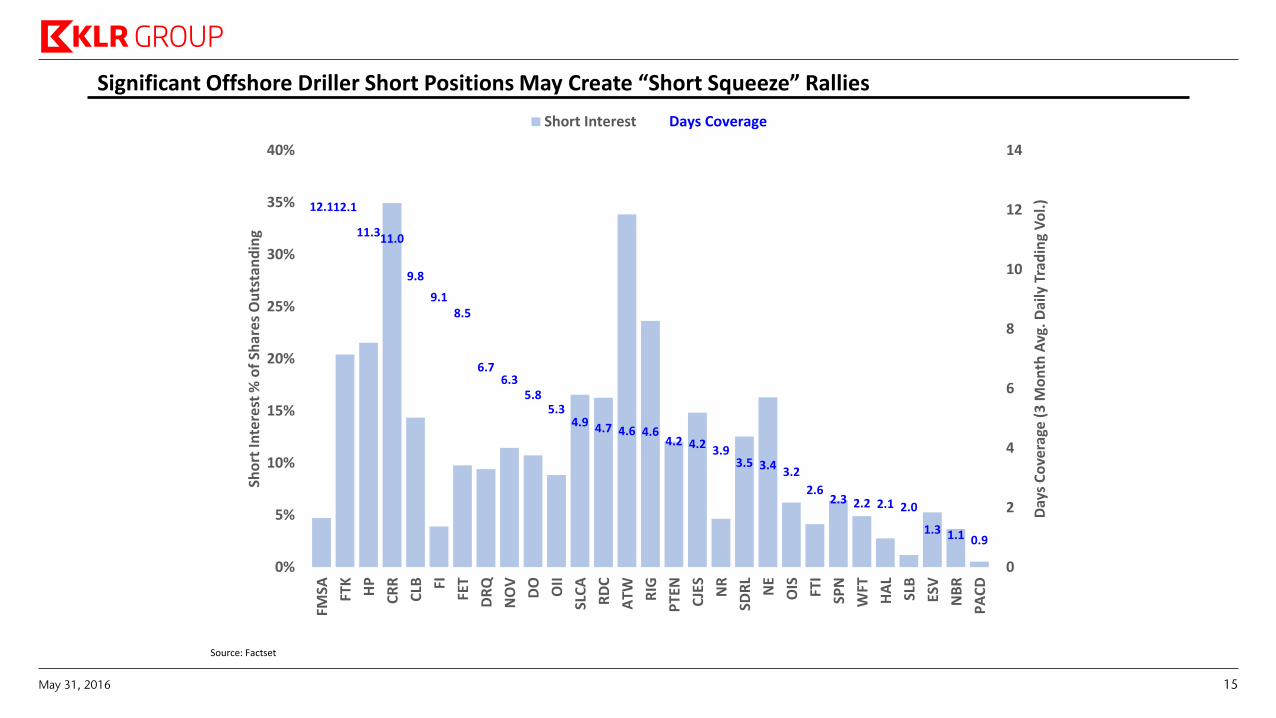

Significant Offshore Driller Short Positions May Create “Short Squeeze” Rallies

Source: Factset

12.1 12.1

11.3 11.0

9.8

9.1 8.5

6.7 6.3

5.8 5.3

4.9 4.7 4.6 4.6 4.2 4.2 3.9

3.5 3.4 3.2

2.6 2.3 2.2 2.1 2.0

1.3 1.1 0.9

0

2

4

6

8

10

12

14

0%

5%

10%

15%

20%

25%

30%

35%

40%

FMSA FT

K

HP

CR

R

CLB FI

FET

DR

Q

NO

V

DO

OII

SLC

A

RD

C

ATW R

IG

PTE

N

CJE

S

NR

SDR

L

NE

OIS FT

I

SPN

WFT

HA

L

SLB

ESV

NB

R

PA

CD

Day

s C

ove

rage

(3

Mo

nth

Avg

. Dai

ly T

rad

ing

Vo

l.)

Sho

rt In

tere

st %

of

Shar

es

Ou

tsta

nd

ing

Short Interest Days Coverage

May 31, 2016 15

Commodity & Macro Drivers

May 31, 2016 16

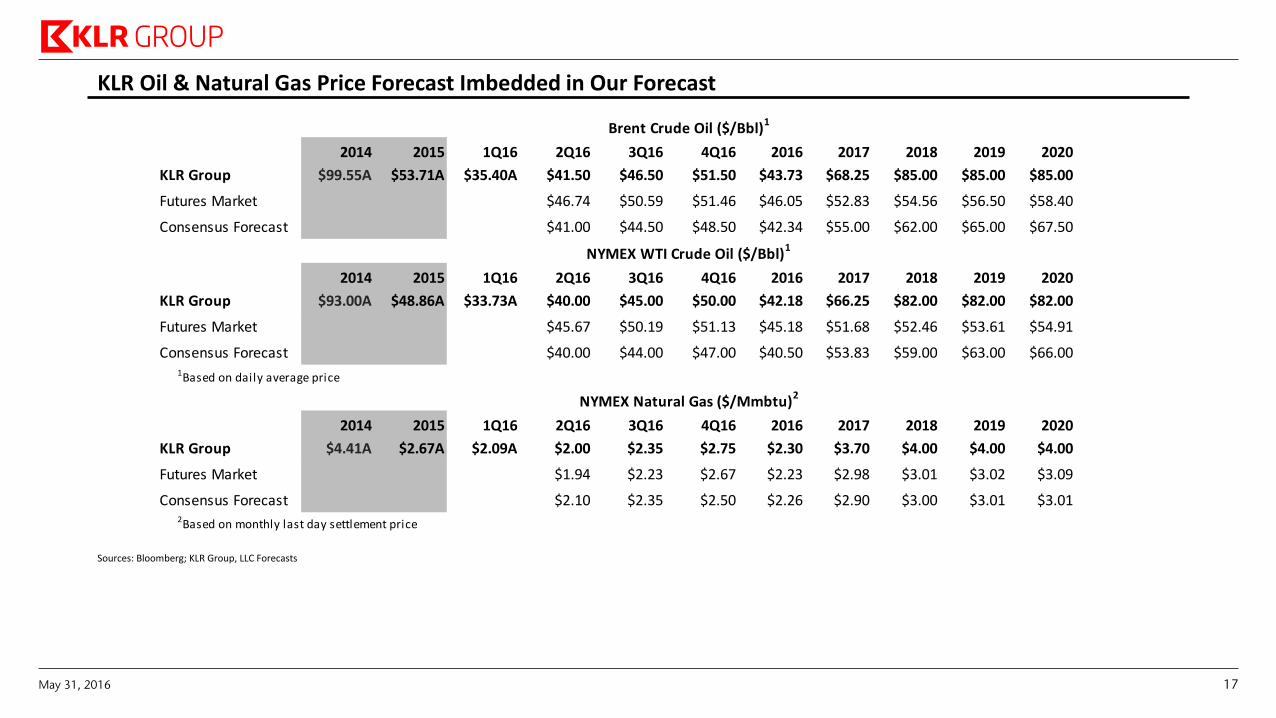

KLR Oil & Natural Gas Price Forecast Imbedded in Our Forecast

Sources: Bloomberg; KLR Group, LLC Forecasts

2014 2015 1Q16 2Q16 3Q16 4Q16 2016 2017 2018 2019 2020

KLR Group $99.55A $53.71A $35.40A $41.50 $46.50 $51.50 $43.73 $68.25 $85.00 $85.00 $85.00

Futures Market $46.74 $50.59 $51.46 $46.05 $52.83 $54.56 $56.50 $58.40

Consensus Forecast $41.00 $44.50 $48.50 $42.34 $55.00 $62.00 $65.00 $67.50

2014 2015 1Q16 2Q16 3Q16 4Q16 2016 2017 2018 2019 2020

KLR Group $93.00A $48.86A $33.73A $40.00 $45.00 $50.00 $42.18 $66.25 $82.00 $82.00 $82.00

Futures Market $45.67 $50.19 $51.13 $45.18 $51.68 $52.46 $53.61 $54.91

Consensus Forecast $40.00 $44.00 $47.00 $40.50 $53.83 $59.00 $63.00 $66.001Based on daily average price

2014 2015 1Q16 2Q16 3Q16 4Q16 2016 2017 2018 2019 2020

KLR Group $4.41A $2.67A $2.09A $2.00 $2.35 $2.75 $2.30 $3.70 $4.00 $4.00 $4.00

Futures Market $1.94 $2.23 $2.67 $2.23 $2.98 $3.01 $3.02 $3.09

Consensus Forecast $2.10 $2.35 $2.50 $2.26 $2.90 $3.00 $3.01 $3.012Based on monthly last day settlement price

NYMEX WTI Crude Oil ($/Bbl)1

Brent Crude Oil ($/Bbl)1

NYMEX Natural Gas ($/Mmbtu)2

May 31, 2016 17

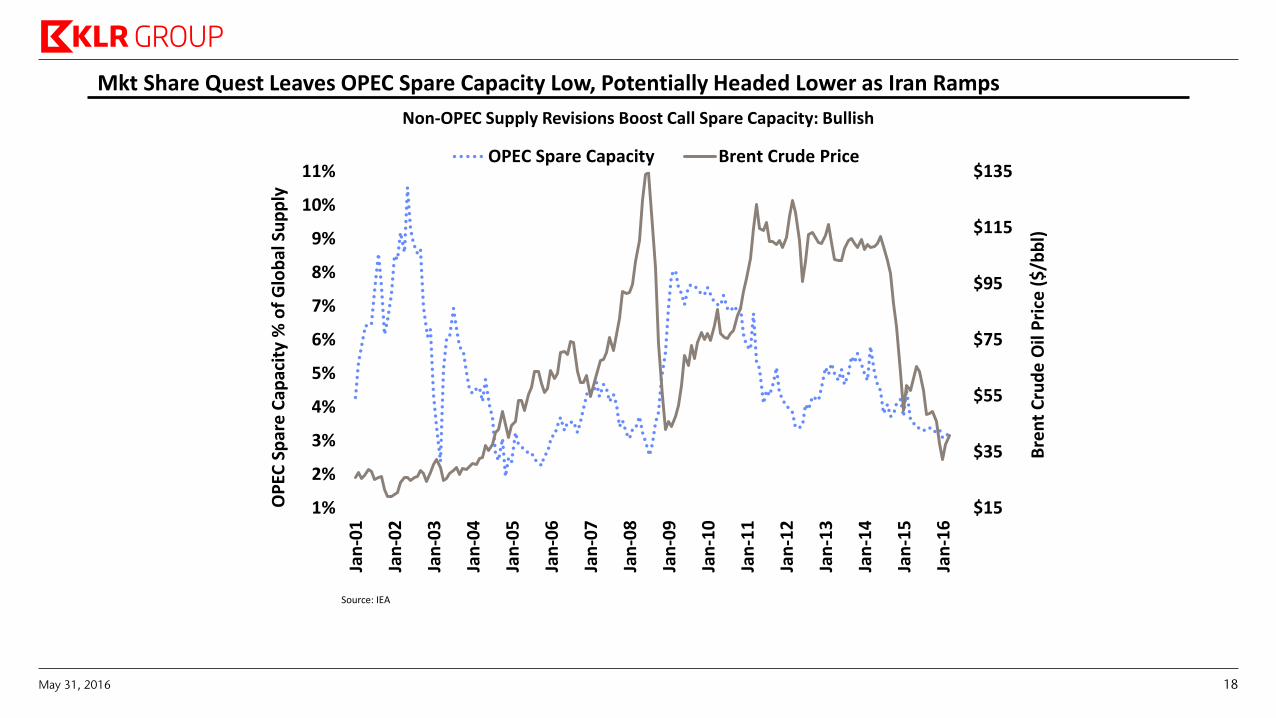

Mkt Share Quest Leaves OPEC Spare Capacity Low, Potentially Headed Lower as Iran Ramps

Source: IEA

Non-OPEC Supply Revisions Boost Call Spare Capacity: Bullish

$15

$35

$55

$75

$95

$115

$135

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Bre

nt

Cru

de

Oil

Pri

ce (

$/b

bl)

OP

EC S

par

e C

apac

ity

% o

f G

lob

al S

up

ply

OPEC Spare Capacity Brent Crude Price

May 31, 2016 18

$30

$50

$70

$90

$110

$130

$150

48

49

50

51

52

53

54

55

56

57

58

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Act

ual

Bre

nt

Cru

de

Oil

Pri

ce (

$/b

bl)

An

nu

al N

on

-OP

EC S

up

ply

Fo

reca

st (

mm

b/d

)

Vintage of Forecast

2009 IEA Supply 2010 IEA Supply 2011 IEA Supply 2012 IEA Supply 2013 IEA Supply

2014 IEA Supply 2015 IEA Supply 2016 IEA Supply Brent Crude

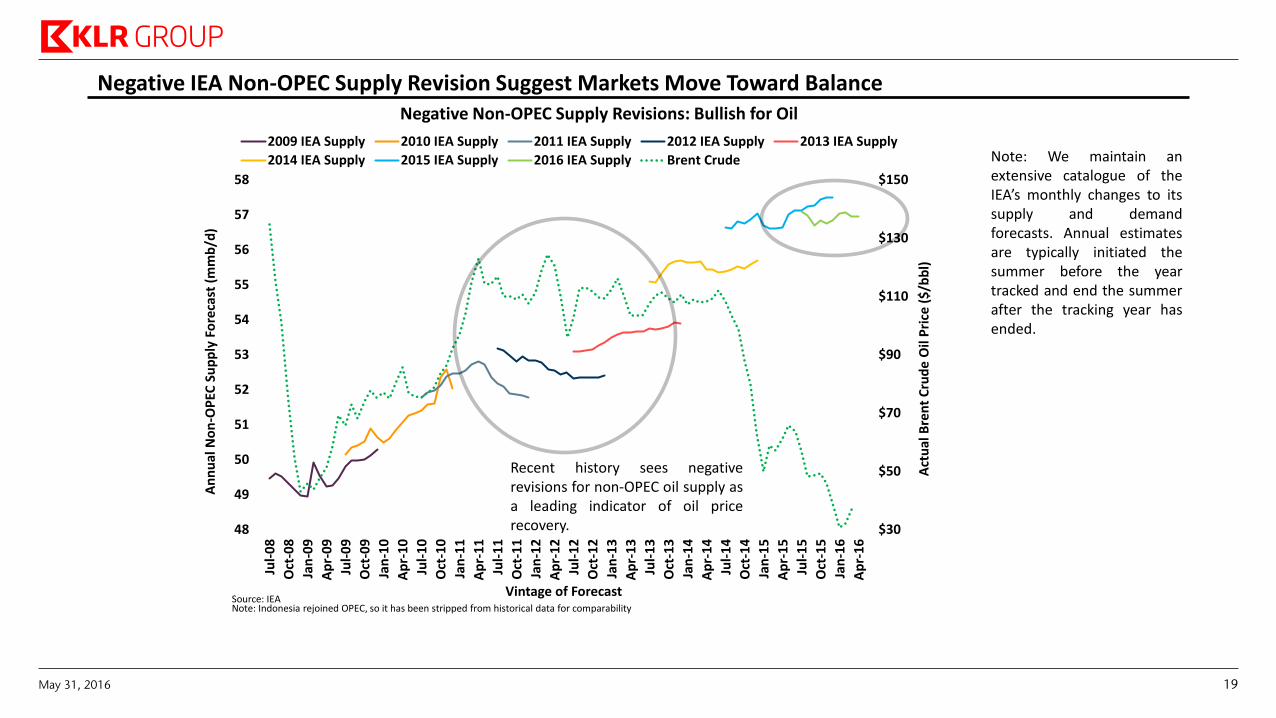

Negative IEA Non-OPEC Supply Revision Suggest Markets Move Toward Balance

Source: IEA

Negative Non-OPEC Supply Revisions: Bullish for Oil

Note: We maintain an extensive catalogue of the IEA’s monthly changes to its supply and demand forecasts. Annual estimates are typically initiated the summer before the year tracked and end the summer after the tracking year has ended.

Recent history sees negative revisions for non-OPEC oil supply as a leading indicator of oil price recovery.

Note: Indonesia rejoined OPEC, so it has been stripped from historical data for comparability

May 31, 2016 19

$30

$50

$70

$90

$110

$130

$150

83

84

85

86

87

88

89

90

91

92

93

94

95

96

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Act

ual

Bre

nt

Cru

de

Oil

Pri

ce (

$/b

bl)

Glo

bal

De

man

d F

ore

cast

(m

mb

/d)

Vintage of Forecast

2009 IEA Demand 2010 IEA Demand 2011 IEA Demand 2012 IEA Demand 2013 IEA Demand

2014 IEA Demand 2015 IEA Demand 2016 IEA Demand Brent Crude

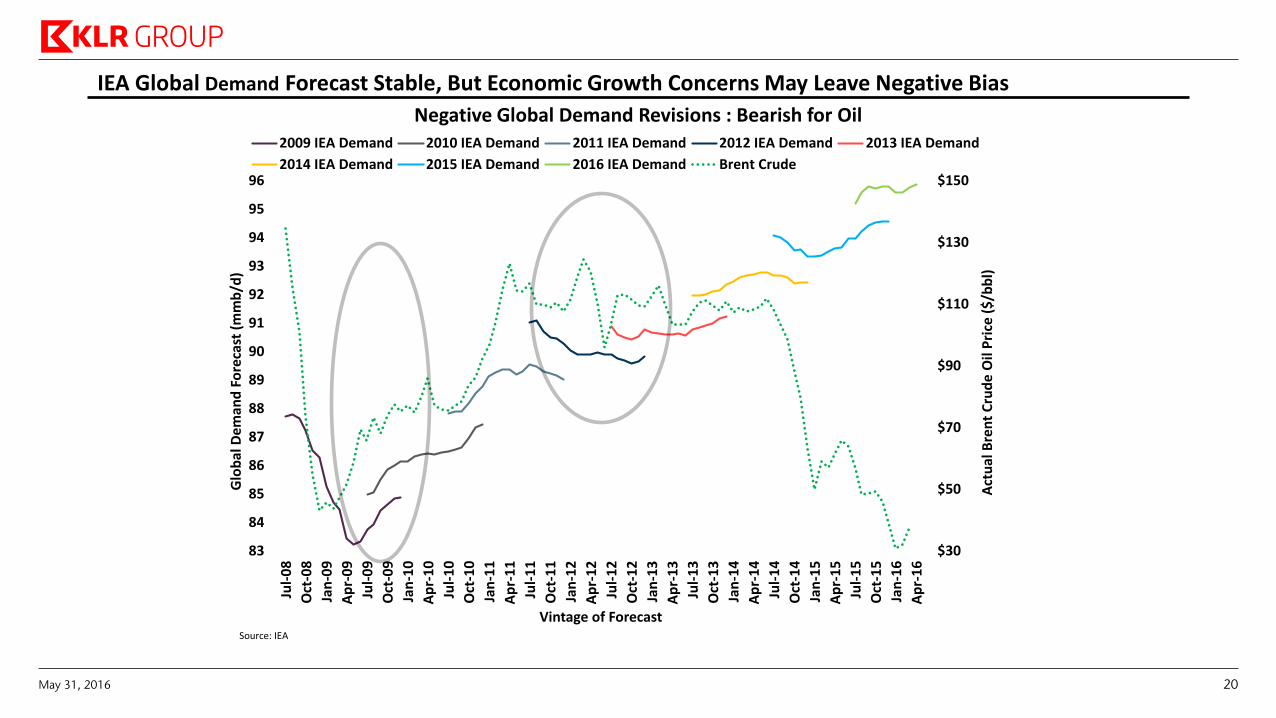

IEA Global Demand Forecast Stable, But Economic Growth Concerns May Leave Negative Bias

Source: IEA

Negative Global Demand Revisions : Bearish for Oil

May 31, 2016 20

Offshore Driller Dayrates & Fleet Breakdowns

May 31, 2016 21

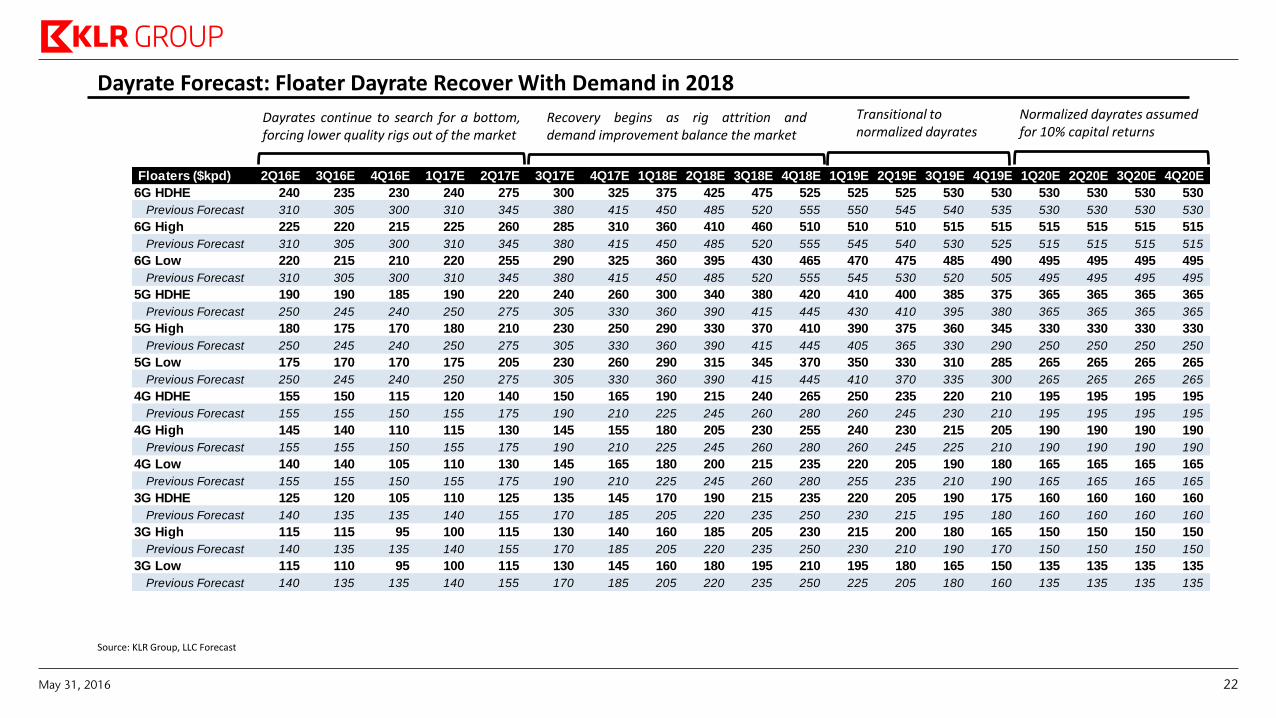

Dayrate Forecast: Floater Dayrate Recover With Demand in 2018 Normalized dayrates assumed

for 10% capital returns Transitional to normalized dayrates

Recovery begins as rig attrition and demand improvement balance the market

Dayrates continue to search for a bottom, forcing lower quality rigs out of the market

Source: KLR Group, LLC Forecast

Floaters ($kpd) 2Q16E 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 1Q18E 2Q18E 3Q18E 4Q18E 1Q19E 2Q19E 3Q19E 4Q19E 1Q20E 2Q20E 3Q20E 4Q20E

6G HDHE 240 235 230 240 275 300 325 375 425 475 525 525 525 530 530 530 530 530 530

Previous Forecast 310 305 300 310 345 380 415 450 485 520 555 550 545 540 535 530 530 530 530

6G High 225 220 215 225 260 285 310 360 410 460 510 510 510 515 515 515 515 515 515

Previous Forecast 310 305 300 310 345 380 415 450 485 520 555 545 540 530 525 515 515 515 515

6G Low 220 215 210 220 255 290 325 360 395 430 465 470 475 485 490 495 495 495 495

Previous Forecast 310 305 300 310 345 380 415 450 485 520 555 545 530 520 505 495 495 495 495

5G HDHE 190 190 185 190 220 240 260 300 340 380 420 410 400 385 375 365 365 365 365

Previous Forecast 250 245 240 250 275 305 330 360 390 415 445 430 410 395 380 365 365 365 365

5G High 180 175 170 180 210 230 250 290 330 370 410 390 375 360 345 330 330 330 330

Previous Forecast 250 245 240 250 275 305 330 360 390 415 445 405 365 330 290 250 250 250 250

5G Low 175 170 170 175 205 230 260 290 315 345 370 350 330 310 285 265 265 265 265

Previous Forecast 250 245 240 250 275 305 330 360 390 415 445 410 370 335 300 265 265 265 265

4G HDHE 155 150 115 120 140 150 165 190 215 240 265 250 235 220 210 195 195 195 195

Previous Forecast 155 155 150 155 175 190 210 225 245 260 280 260 245 230 210 195 195 195 195

4G High 145 140 110 115 130 145 155 180 205 230 255 240 230 215 205 190 190 190 190

Previous Forecast 155 155 150 155 175 190 210 225 245 260 280 260 245 225 210 190 190 190 190

4G Low 140 140 105 110 130 145 165 180 200 215 235 220 205 190 180 165 165 165 165

Previous Forecast 155 155 150 155 175 190 210 225 245 260 280 255 235 210 190 165 165 165 165

3G HDHE 125 120 105 110 125 135 145 170 190 215 235 220 205 190 175 160 160 160 160

Previous Forecast 140 135 135 140 155 170 185 205 220 235 250 230 215 195 180 160 160 160 160

3G High 115 115 95 100 115 130 140 160 185 205 230 215 200 180 165 150 150 150 150

Previous Forecast 140 135 135 140 155 170 185 205 220 235 250 230 210 190 170 150 150 150 150

3G Low 115 110 95 100 115 130 145 160 180 195 210 195 180 165 150 135 135 135 135

Previous Forecast 140 135 135 140 155 170 185 205 220 235 250 225 205 180 160 135 135 135 135

May 31, 2016 22

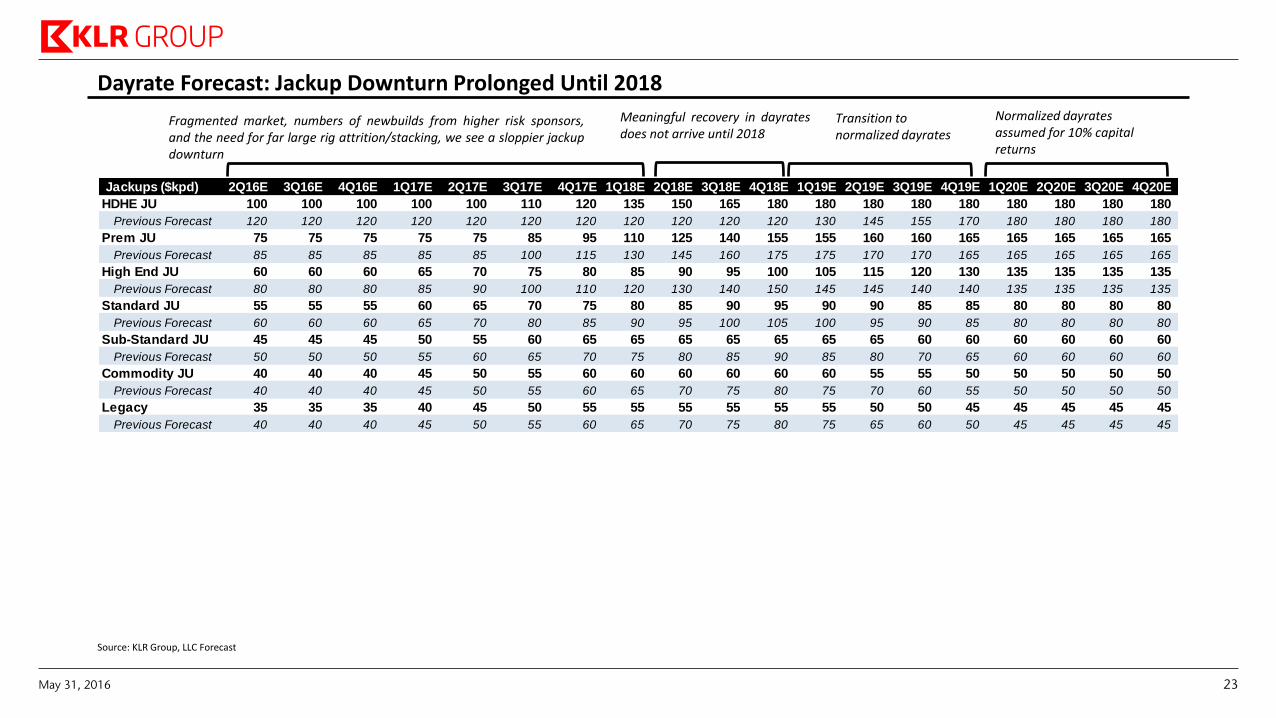

Fragmented market, numbers of newbuilds from higher risk sponsors, and the need for far large rig attrition/stacking, we see a sloppier jackup downturn

Dayrate Forecast: Jackup Downturn Prolonged Until 2018 Normalized dayrates assumed for 10% capital returns

Transition to normalized dayrates

Meaningful recovery in dayrates does not arrive until 2018

Source: KLR Group, LLC Forecast

Jackups ($kpd) 2Q16E 3Q16E 4Q16E 1Q17E 2Q17E 3Q17E 4Q17E 1Q18E 2Q18E 3Q18E 4Q18E 1Q19E 2Q19E 3Q19E 4Q19E 1Q20E 2Q20E 3Q20E 4Q20E

HDHE JU 100 100 100 100 100 110 120 135 150 165 180 180 180 180 180 180 180 180 180

Previous Forecast 120 120 120 120 120 120 120 120 120 120 120 130 145 155 170 180 180 180 180

Prem JU 75 75 75 75 75 85 95 110 125 140 155 155 160 160 165 165 165 165 165

Previous Forecast 85 85 85 85 85 100 115 130 145 160 175 175 170 170 165 165 165 165 165

High End JU 60 60 60 65 70 75 80 85 90 95 100 105 115 120 130 135 135 135 135

Previous Forecast 80 80 80 85 90 100 110 120 130 140 150 145 145 140 140 135 135 135 135

Standard JU 55 55 55 60 65 70 75 80 85 90 95 90 90 85 85 80 80 80 80

Previous Forecast 60 60 60 65 70 80 85 90 95 100 105 100 95 90 85 80 80 80 80

Sub-Standard JU 45 45 45 50 55 60 65 65 65 65 65 65 65 60 60 60 60 60 60

Previous Forecast 50 50 50 55 60 65 70 75 80 85 90 85 80 70 65 60 60 60 60

Commodity JU 40 40 40 45 50 55 60 60 60 60 60 60 55 55 50 50 50 50 50

Previous Forecast 40 40 40 45 50 55 60 65 70 75 80 75 70 60 55 50 50 50 50

Legacy 35 35 35 40 45 50 55 55 55 55 55 55 50 50 45 45 45 45 45

Previous Forecast 40 40 40 45 50 55 60 65 70 75 80 75 65 60 50 45 45 45 45

May 31, 2016 23

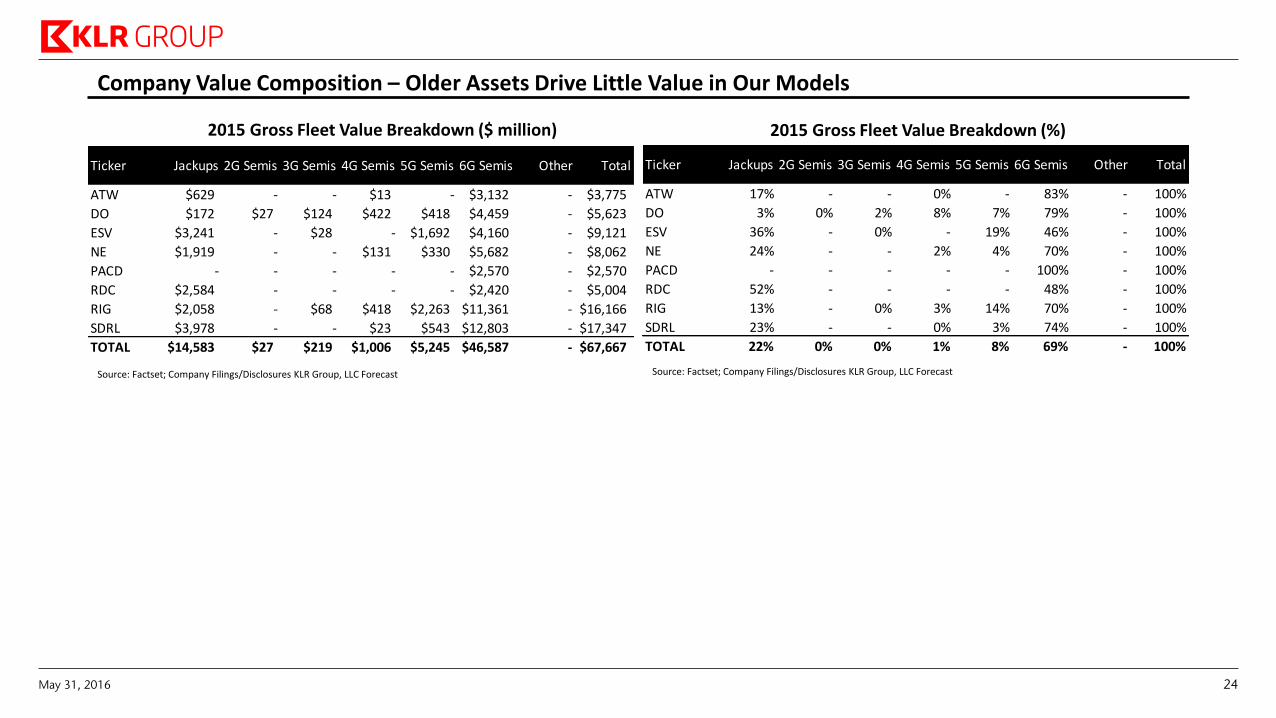

Company Value Composition – Older Assets Drive Little Value in Our Models

Source: Factset; Company Filings/Disclosures KLR Group, LLC Forecast

2015 Gross Fleet Value Breakdown ($ million) 2015 Gross Fleet Value Breakdown (%)

Source: Factset; Company Filings/Disclosures KLR Group, LLC Forecast

Ticker Jackups 2G Semis 3G Semis 4G Semis 5G Semis 6G Semis Other Total

ATW $629 - - $13 - $3,132 - $3,775

DO $172 $27 $124 $422 $418 $4,459 - $5,623

ESV $3,241 - $28 - $1,692 $4,160 - $9,121

NE $1,919 - - $131 $330 $5,682 - $8,062

PACD - - - - - $2,570 - $2,570

RDC $2,584 - - - - $2,420 - $5,004

RIG $2,058 - $68 $418 $2,263 $11,361 - $16,166

SDRL $3,978 - - $23 $543 $12,803 - $17,347

TOTAL $14,583 $27 $219 $1,006 $5,245 $46,587 - $67,667

Ticker Jackups 2G Semis 3G Semis 4G Semis 5G Semis 6G Semis Other Total

ATW 17% - - 0% - 83% - 100%

DO 3% 0% 2% 8% 7% 79% - 100%

ESV 36% - 0% - 19% 46% - 100%

NE 24% - - 2% 4% 70% - 100%

PACD - - - - - 100% - 100%

RDC 52% - - - - 48% - 100%

RIG 13% - 0% 3% 14% 70% - 100%

SDRL 23% - - 0% 3% 74% - 100%

TOTAL 22% 0% 0% 1% 8% 69% - 100%

May 31, 2016 24

0%

18%

0%

11%

22%

27%

34%

0%

30%

2%

27%

33%

46%

65%

20%

55%

55%

58%

60%

63%

88%

0% 20% 40% 60% 80% 100%

DO

ESV

ATW

RIG

SDRL

RDC

NE

2016E 2017E 2018E

29%

14%

27%

36%

17%

25%

16%

2%

38%

19%

29%

45%

46%

49%

46%

63%

49%

52%

53%

58%

61%

75%

89%

100%

0% 20% 40% 60% 80% 100%

RIG

PACD

NE

DO

ESV

SDRL

ATW

RDC

2016E 2017E 2018E

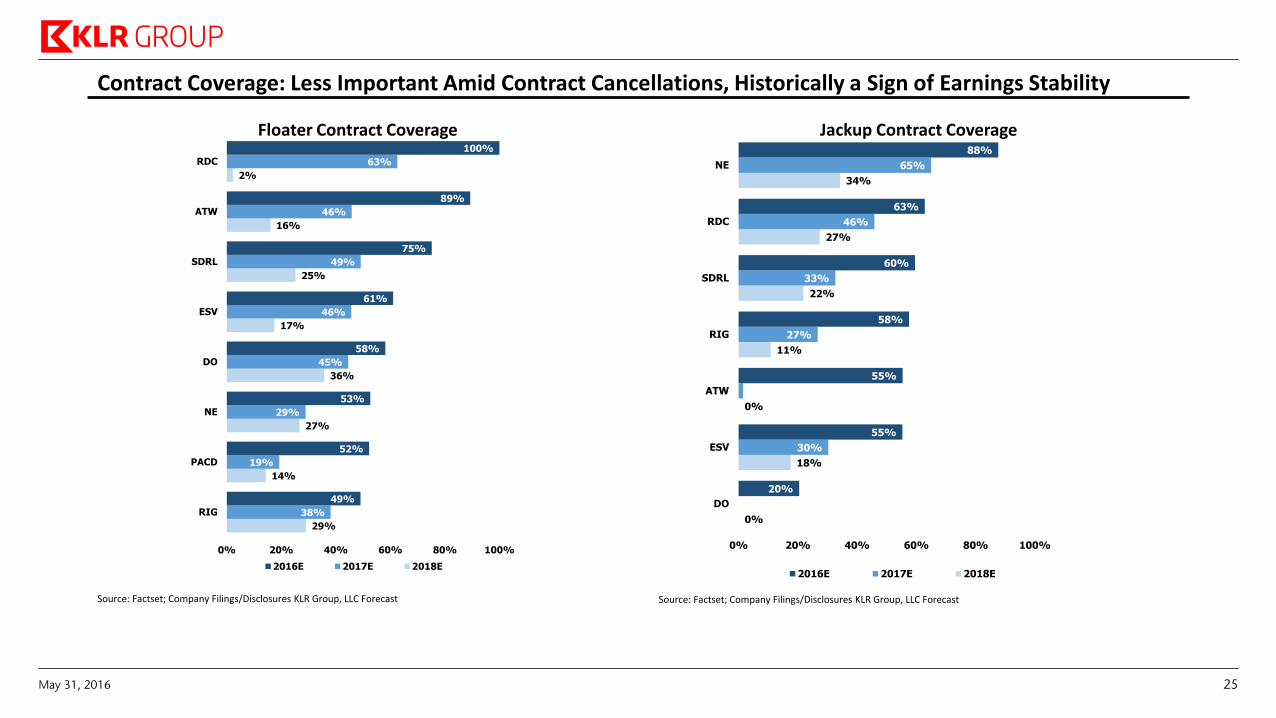

Contract Coverage: Less Important Amid Contract Cancellations, Historically a Sign of Earnings Stability

Source: Factset; Company Filings/Disclosures KLR Group, LLC Forecast

Floater Contract Coverage Jackup Contract Coverage

Source: Factset; Company Filings/Disclosures KLR Group, LLC Forecast

May 31, 2016 25

Offshore Floater Market

May 31, 2016 26

197 200 212

226

241

258

282 296

312

281

241 240 251

264 271

167 173 181

191 199

211

244

258 262

225

181 188

213 224 230

85%86% 86% 85%

83% 82%

86% 87%84%

80%

64%

78%

89% 89%87%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

50

100

150

200

250

300

350

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Uti

lizat

ion

Nu

mb

er o

f R

igs

Market Supply, EOP Contracted / Demand Implied Utilization

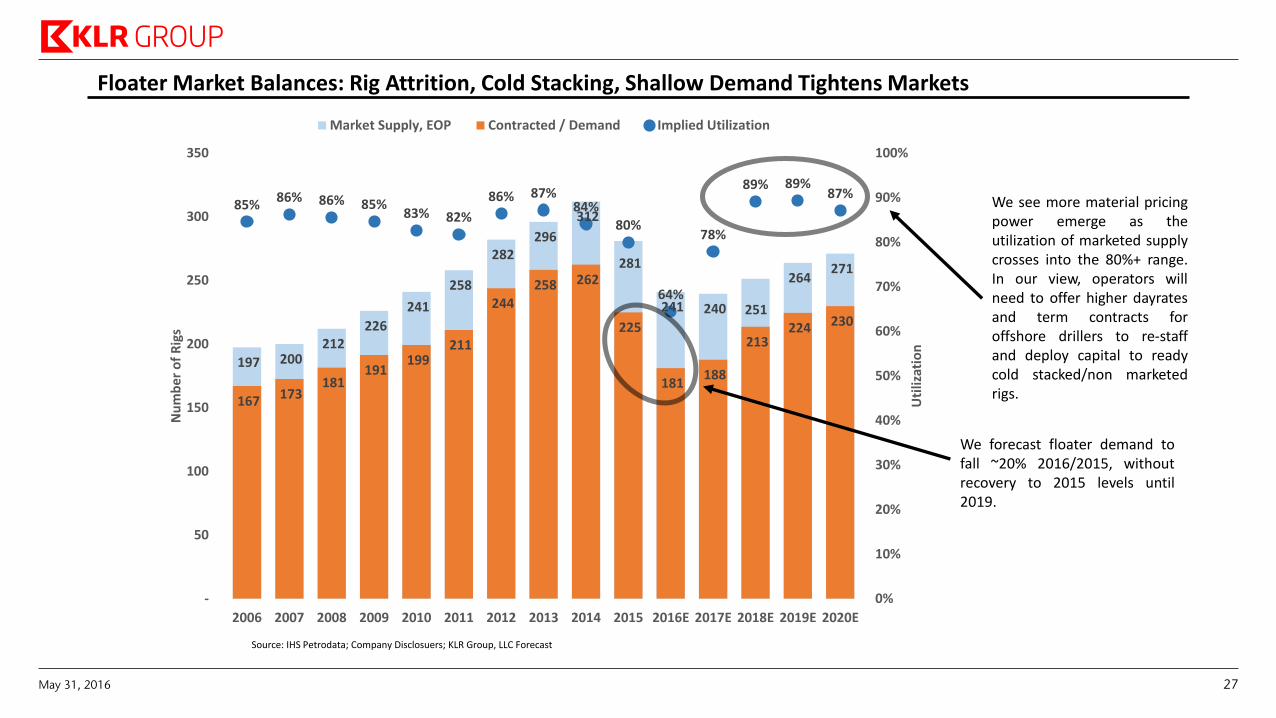

Floater Market Balances: Rig Attrition, Cold Stacking, Shallow Demand Tightens Markets

We forecast floater demand to fall ~20% 2016/2015, without recovery to 2015 levels until 2019.

We see more material pricing power emerge as the utilization of marketed supply crosses into the 80%+ range. In our view, operators will need to offer higher dayrates and term contracts for offshore drillers to re-staff and deploy capital to ready cold stacked/non marketed rigs.

Source: IHS Petrodata; Company Disclosuers; KLR Group, LLC Forecast

May 31, 2016 27

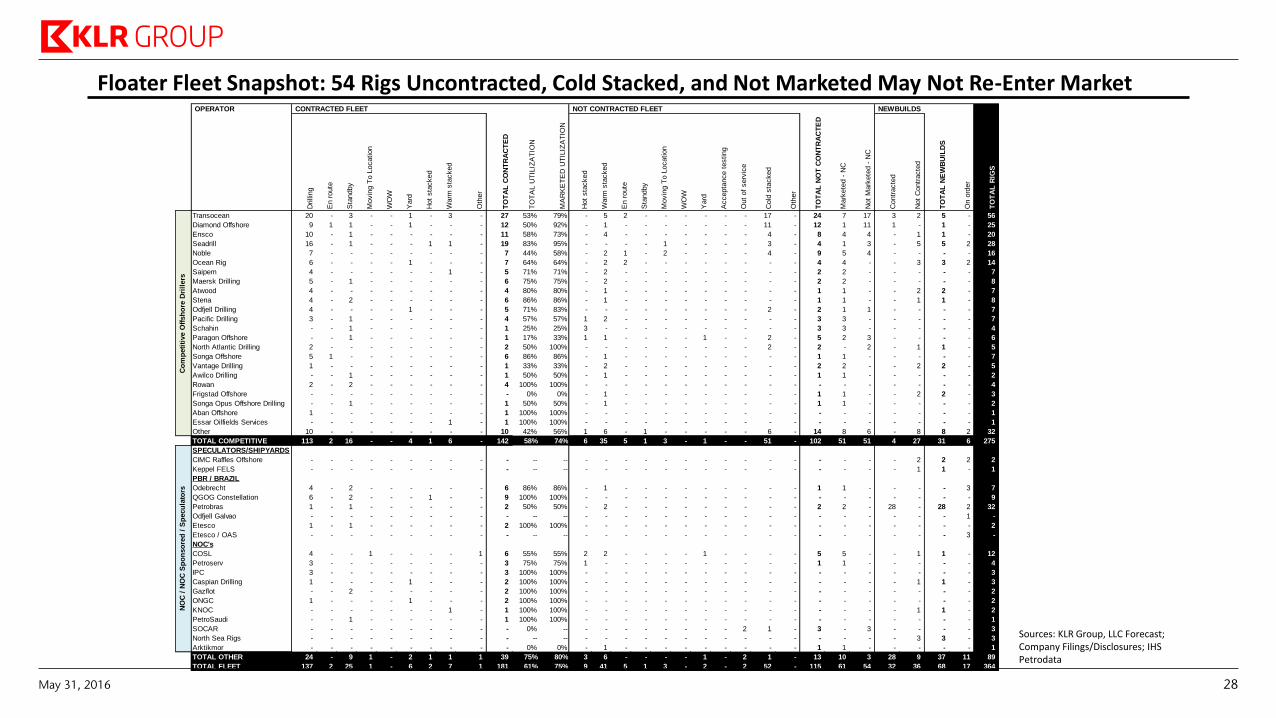

Floater Fleet Snapshot: 54 Rigs Uncontracted, Cold Stacked, and Not Marketed May Not Re-Enter Market

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata

OPERATOR CONTRACTED FLEET NOT CONTRACTED FLEET NEWBUILDS

Drilli

ng

En r

oute

Sta

ndby

Movin

g T

o L

ocation

WO

W

Yard

Hot

sta

cked

Warm

sta

cked

Oth

er

TO

TA

L C

ON

TR

AC

TE

D

TO

TA

L U

TIL

IZA

TIO

N

MA

RK

ET

ED

UT

ILIZ

AT

ION

Hot

sta

cked

Warm

sta

cked

En r

oute

Sta

ndby

Movin

g T

o L

ocation

WO

W

Yard

Accepta

nce t

esting

Out

of

serv

ice

Cold

sta

cked

Oth

er

TO

TA

L N

OT

CO

NT

RA

CT

ED

Mark

ete

d -

NC

Not

Mark

ete

d -

NC

Contr

acte

d

Not

Contr

acte

d

TO

TA

L N

EW

BU

ILD

S

On o

rder

TO

TA

L R

IGS

Transocean 20 - 3 - - 1 - 3 - 27 53% 79% - 5 2 - - - - - - 17 - 24 7 17 3 2 5 - 56

Diamond Offshore 9 1 1 - - 1 - - - 12 50% 92% - 1 - - - - - - - 11 - 12 1 11 1 - 1 - 25

Ensco 10 - 1 - - - - - - 11 58% 73% - 4 - - - - - - - 4 - 8 4 4 - 1 1 - 20

Seadrill 16 - 1 - - - 1 1 - 19 83% 95% - - - - 1 - - - - 3 - 4 1 3 - 5 5 2 28

Noble 7 - - - - - - - - 7 44% 58% - 2 1 - 2 - - - - 4 - 9 5 4 - - - - 16

Ocean Rig 6 - - - - 1 - - - 7 64% 64% - 2 2 - - - - - - - - 4 4 - - 3 3 2 14

Saipem 4 - - - - - - 1 - 5 71% 71% - 2 - - - - - - - - - 2 2 - - - - - 7

Maersk Drilling 5 - 1 - - - - - - 6 75% 75% - 2 - - - - - - - - - 2 2 - - - - - 8

Atwood 4 - - - - - - - - 4 80% 80% - 1 - - - - - - - - - 1 1 - - 2 2 - 7

Stena 4 - 2 - - - - - - 6 86% 86% - 1 - - - - - - - - - 1 1 - - 1 1 - 8

Odfjell Drilling 4 - - - - 1 - - - 5 71% 83% - - - - - - - - - 2 - 2 1 1 - - - - 7

Pacific Drilling 3 - 1 - - - - - - 4 57% 57% 1 2 - - - - - - - - - 3 3 - - - - - 7

Schahin - - 1 - - - - - - 1 25% 25% 3 - - - - - - - - - - 3 3 - - - - - 4

Paragon Offshore - - 1 - - - - - - 1 17% 33% 1 1 - - - - 1 - - 2 - 5 2 3 - - - - 6

North Atlantic Drilling 2 - - - - - - - - 2 50% 100% - - - - - - - - - 2 - 2 - 2 - 1 1 - 5

Songa Offshore 5 1 - - - - - - - 6 86% 86% - 1 - - - - - - - - - 1 1 - - - - - 7

Vantage Drilling 1 - - - - - - - - 1 33% 33% - 2 - - - - - - - - - 2 2 - - 2 2 - 5

Awilco Drilling - - 1 - - - - - - 1 50% 50% - 1 - - - - - - - - - 1 1 - - - - - 2

Rowan 2 - 2 - - - - - - 4 100% 100% - - - - - - - - - - - - - - - - - - 4

Frigstad Offshore - - - - - - - - - - 0% 0% - 1 - - - - - - - - - 1 1 - - 2 2 - 3

Songa Opus Offshore Drilling - - 1 - - - - - - 1 50% 50% - 1 - - - - - - - - - 1 1 - - - - - 2

Aban Offshore 1 - - - - - - - - 1 100% 100% - - - - - - - - - - - - - - - - - - 1

Essar Oilfields Services - - - - - - - 1 - 1 100% 100% - - - - - - - - - - - - - - - - - - 1

Other 10 - - - - - - - - 10 42% 56% 1 6 - 1 - - - - - 6 - 14 8 6 - 8 8 2 32

TOTAL COMPETITIVE 113 2 16 - - 4 1 6 - 142 58% 74% 6 35 5 1 3 - 1 - - 51 - 102 51 51 4 27 31 6 275

SPECULATORS/SHIPYARDS

CIMC Raffles Offshore - - - - - - - - - - -- -- - - - - - - - - - - - - - - - 2 2 2 2

Keppel FELS - - - - - - - - - - -- -- - - - - - - - - - - - - - - - 1 1 - 1

PBR / BRAZIL

Odebrecht 4 - 2 - - - - - - 6 86% 86% - 1 - - - - - - - - - 1 1 - - - - 3 7

QGOG Constellation 6 - 2 - - - 1 - - 9 100% 100% - - - - - - - - - - - - - - - - - - 9

Petrobras 1 - 1 - - - - - - 2 50% 50% - 2 - - - - - - - - - 2 2 - 28 - 28 2 32

Odfjell Galvao - - - - - - - - - - -- -- - - - - - - - - - - - - - - - - - 1 -

Etesco 1 - 1 - - - - - - 2 100% 100% - - - - - - - - - - - - - - - - - - 2

Etesco / OAS - - - - - - - - - - -- -- - - - - - - - - - - - - - - - - - 3 -

NOC's

COSL 4 - - 1 - - - - 1 6 55% 55% 2 2 - - - - 1 - - - - 5 5 - - 1 1 - 12

Petroserv 3 - - - - - - - - 3 75% 75% 1 - - - - - - - - - - 1 1 - - - - - 4

IPC 3 - - - - - - - - 3 100% 100% - - - - - - - - - - - - - - - - - - 3

Caspian Drilling 1 - - - - 1 - - - 2 100% 100% - - - - - - - - - - - - - - - 1 1 - 3

Gazflot - - 2 - - - - - - 2 100% 100% - - - - - - - - - - - - - - - - - - 2

ONGC 1 - - - - 1 - - - 2 100% 100% - - - - - - - - - - - - - - - - - - 2

KNOC - - - - - - - 1 - 1 100% 100% - - - - - - - - - - - - - - - 1 1 - 2

PetroSaudi - - 1 - - - - - - 1 100% 100% - - - - - - - - - - - - - - - - - - 1

SOCAR - - - - - - - - - - 0% -- - - - - - - - - 2 1 - 3 - 3 - - - - 3

North Sea Rigs - - - - - - - - - - -- -- - - - - - - - - - - - - - - - 3 3 - 3

Arktikmor - - - - - - - - - - 0% 0% - 1 - - - - - - - - - 1 1 - - - - - 1

TOTAL OTHER 24 - 9 1 - 2 1 1 1 39 75% 80% 3 6 - - - - 1 - 2 1 - 13 10 3 28 9 37 11 89

TOTAL FLEET 137 2 25 1 - 6 2 7 1 181 61% 75% 9 41 5 1 3 - 2 - 2 52 - 115 61 54 32 36 68 17 364

NO

C /

NO

C S

po

nso

red

/ S

pecu

lato

rsC

om

peti

tive O

ffsh

ore

Dri

llers

May 31, 2016 28

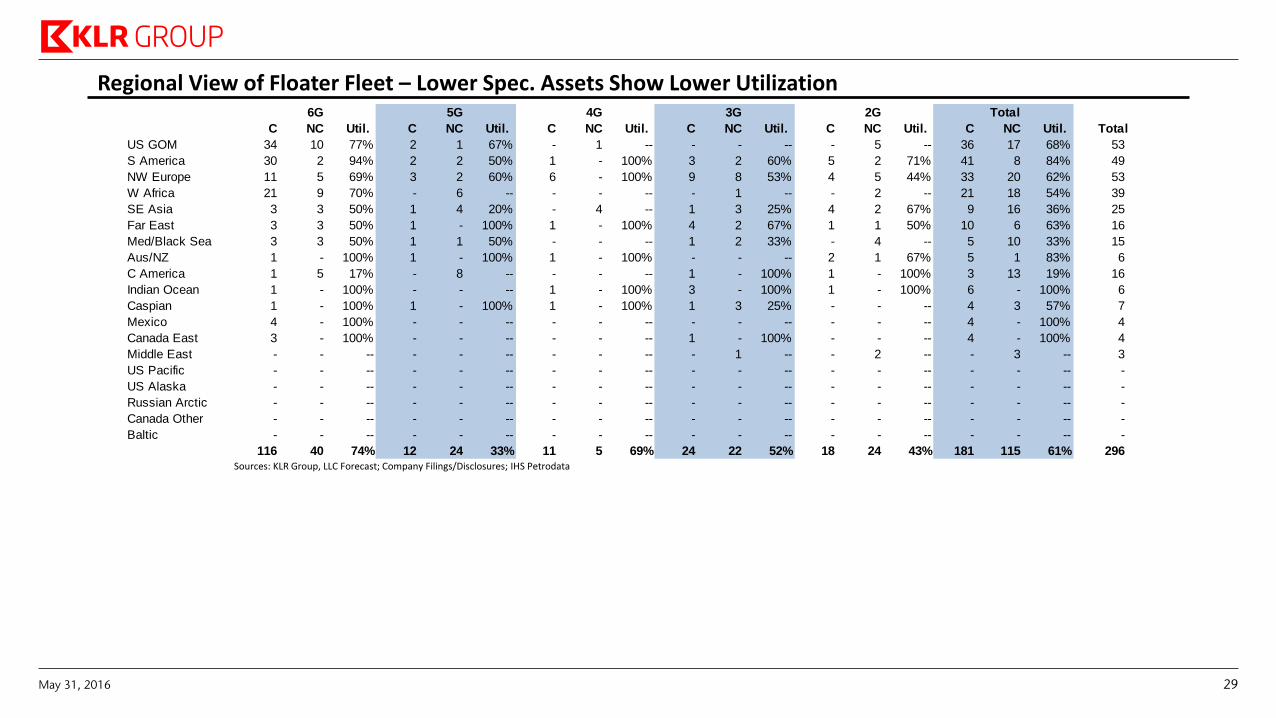

Regional View of Floater Fleet – Lower Spec. Assets Show Lower Utilization

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata

6G 5G 4G 3G 2G Total

C NC Util. C NC Util. C NC Util. C NC Util. C NC Util. C NC Util. Total

US GOM 34 10 77% 2 1 67% - 1 -- - - -- - 5 -- 36 17 68% 53

S America 30 2 94% 2 2 50% 1 - 100% 3 2 60% 5 2 71% 41 8 84% 49

NW Europe 11 5 69% 3 2 60% 6 - 100% 9 8 53% 4 5 44% 33 20 62% 53

W Africa 21 9 70% - 6 -- - - -- - 1 -- - 2 -- 21 18 54% 39

SE Asia 3 3 50% 1 4 20% - 4 -- 1 3 25% 4 2 67% 9 16 36% 25

Far East 3 3 50% 1 - 100% 1 - 100% 4 2 67% 1 1 50% 10 6 63% 16

Med/Black Sea 3 3 50% 1 1 50% - - -- 1 2 33% - 4 -- 5 10 33% 15

Aus/NZ 1 - 100% 1 - 100% 1 - 100% - - -- 2 1 67% 5 1 83% 6

C America 1 5 17% - 8 -- - - -- 1 - 100% 1 - 100% 3 13 19% 16

Indian Ocean 1 - 100% - - -- 1 - 100% 3 - 100% 1 - 100% 6 - 100% 6

Caspian 1 - 100% 1 - 100% 1 - 100% 1 3 25% - - -- 4 3 57% 7

Mexico 4 - 100% - - -- - - -- - - -- - - -- 4 - 100% 4

Canada East 3 - 100% - - -- - - -- 1 - 100% - - -- 4 - 100% 4

Middle East - - -- - - -- - - -- - 1 -- - 2 -- - 3 -- 3

US Pacific - - -- - - -- - - -- - - -- - - -- - - -- -

US Alaska - - -- - - -- - - -- - - -- - - -- - - -- -

Russian Arctic - - -- - - -- - - -- - - -- - - -- - - -- -

Canada Other - - -- - - -- - - -- - - -- - - -- - - -- -

Baltic - - -- - - -- - - -- - - -- - - -- - - -- -

116 40 74% 12 24 33% 11 5 69% 24 22 52% 18 24 43% 181 115 61% 296

May 31, 2016 29

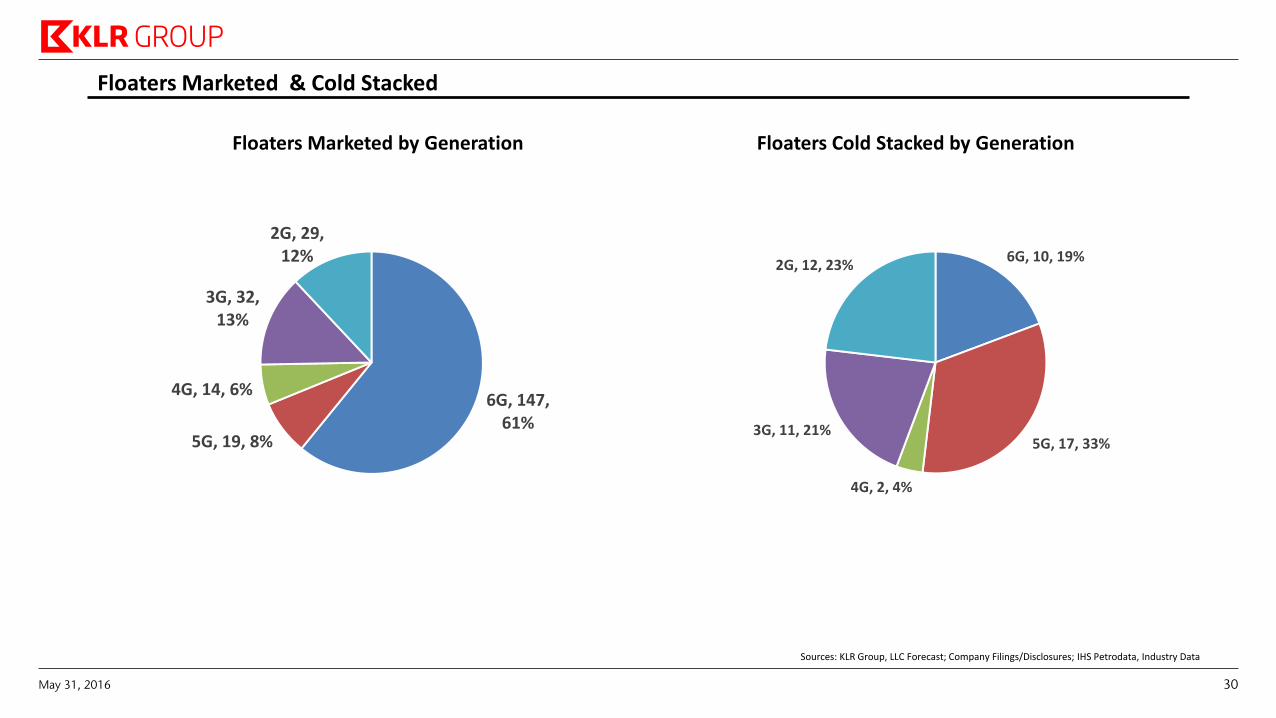

Floaters Marketed & Cold Stacked

6G, 147, 61%

5G, 19, 8%

4G, 14, 6%

3G, 32, 13%

2G, 29, 12% 6G, 10, 19%

5G, 17, 33%

4G, 2, 4%

3G, 11, 21%

2G, 12, 23%

Floaters Marketed by Generation Floaters Cold Stacked by Generation

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 30

69

80 82

107 113 114

122

137

122 117

90

58

79

102

121

132

50

60

70

80

90

100

110

120

130

140

150

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

58

73 69 74

78 83

87

106

136 145

135

123

112 121

115 111

50

60

70

80

90

100

110

120

130

140

150

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

E

20

17

E

20

18

E

20

19

E

20

20

E

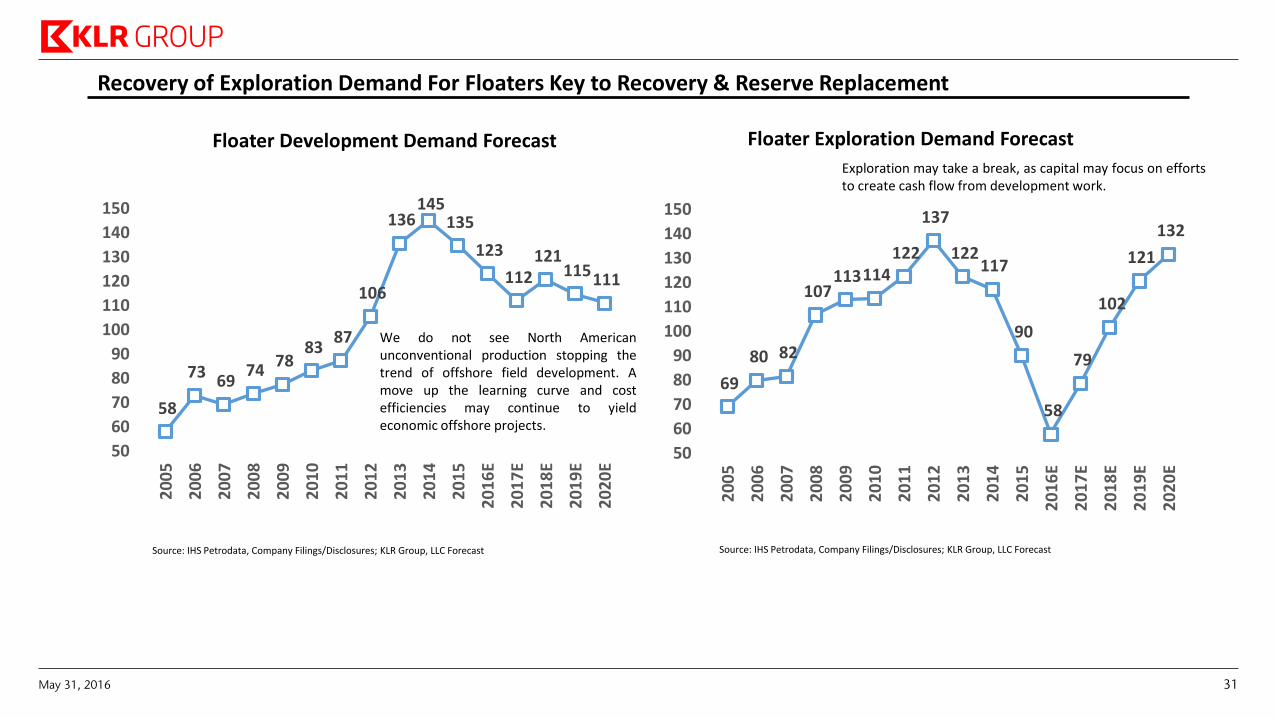

Recovery of Exploration Demand For Floaters Key to Recovery & Reserve Replacement

Floater Development Demand Forecast Floater Exploration Demand Forecast

We do not see North American unconventional production stopping the trend of offshore field development. A move up the learning curve and cost efficiencies may continue to yield economic offshore projects.

Exploration may take a break, as capital may focus on efforts to create cash flow from development work.

Source: IHS Petrodata, Company Filings/Disclosures; KLR Group, LLC Forecast Source: IHS Petrodata, Company Filings/Disclosures; KLR Group, LLC Forecast

May 31, 2016 31

165

189

225

256

274

306

240

184

158

140

181 188

213 224

230

244

210

171

151

138

100

150

200

250

300

350

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

TOTAL RAW FLOATER DEMAND TOTAL FLOATER DEMAND (KLR Forecast)

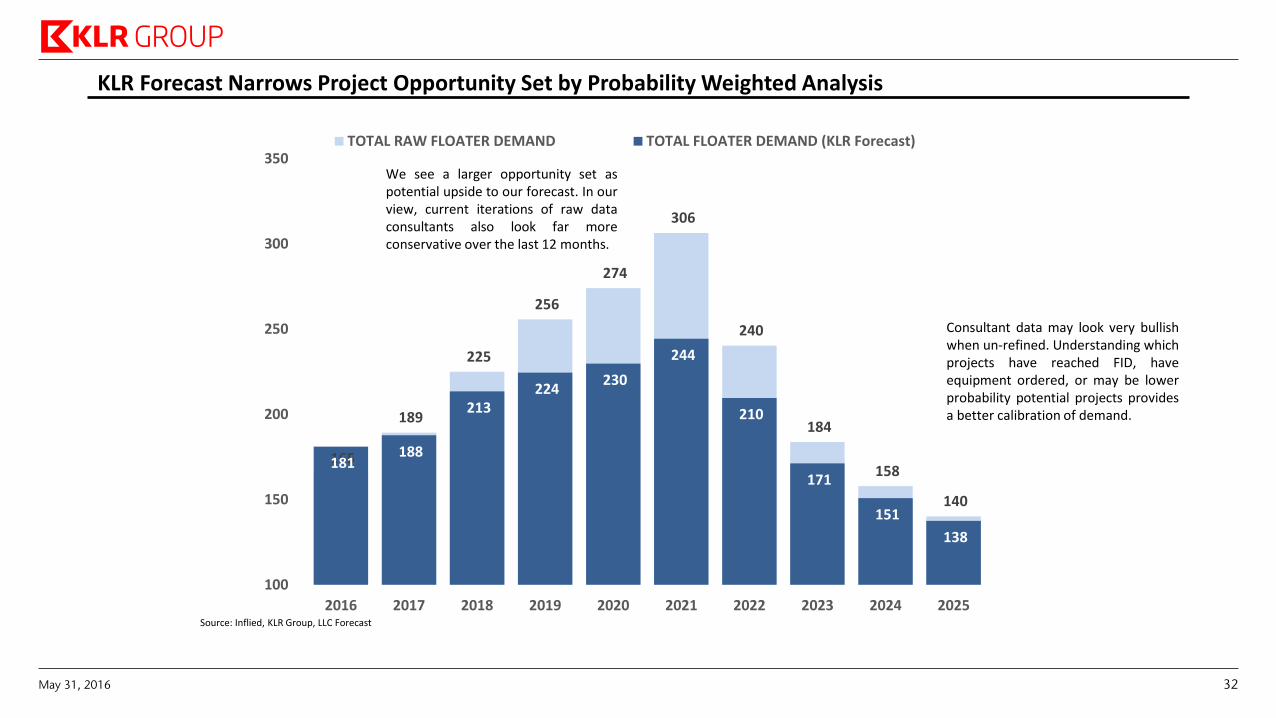

KLR Forecast Narrows Project Opportunity Set by Probability Weighted Analysis

Consultant data may look very bullish when un-refined. Understanding which projects have reached FID, have equipment ordered, or may be lower probability potential projects provides a better calibration of demand.

We see a larger opportunity set as potential upside to our forecast. In our view, current iterations of raw data consultants also look far more conservative over the last 12 months.

Source: Inflied, KLR Group, LLC Forecast

May 31, 2016 32

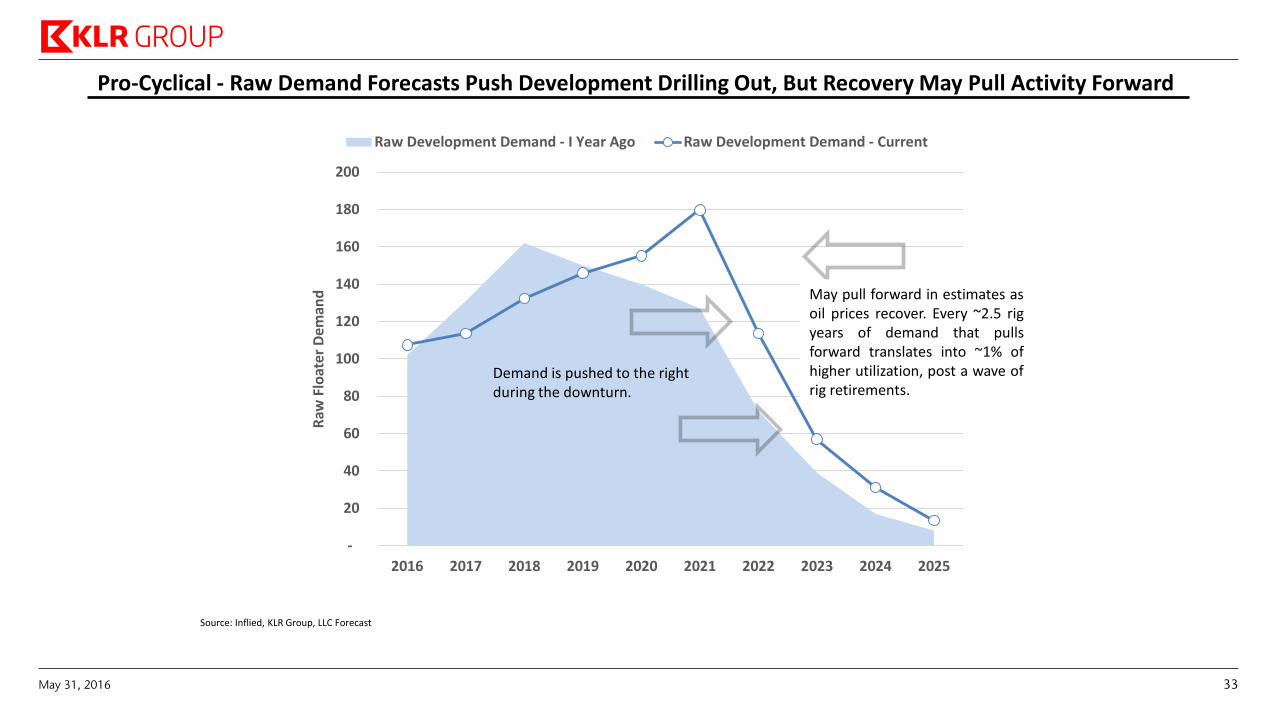

Pro-Cyclical - Raw Demand Forecasts Push Development Drilling Out, But Recovery May Pull Activity Forward

-

20

40

60

80

100

120

140

160

180

200

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Raw

Flo

ater

Dem

and

Raw Development Demand - I Year Ago Raw Development Demand - Current

Source: Inflied, KLR Group, LLC Forecast

Demand is pushed to the right during the downturn.

May pull forward in estimates as oil prices recover. Every ~2.5 rig years of demand that pulls forward translates into ~1% of higher utilization, post a wave of rig retirements.

May 31, 2016 33

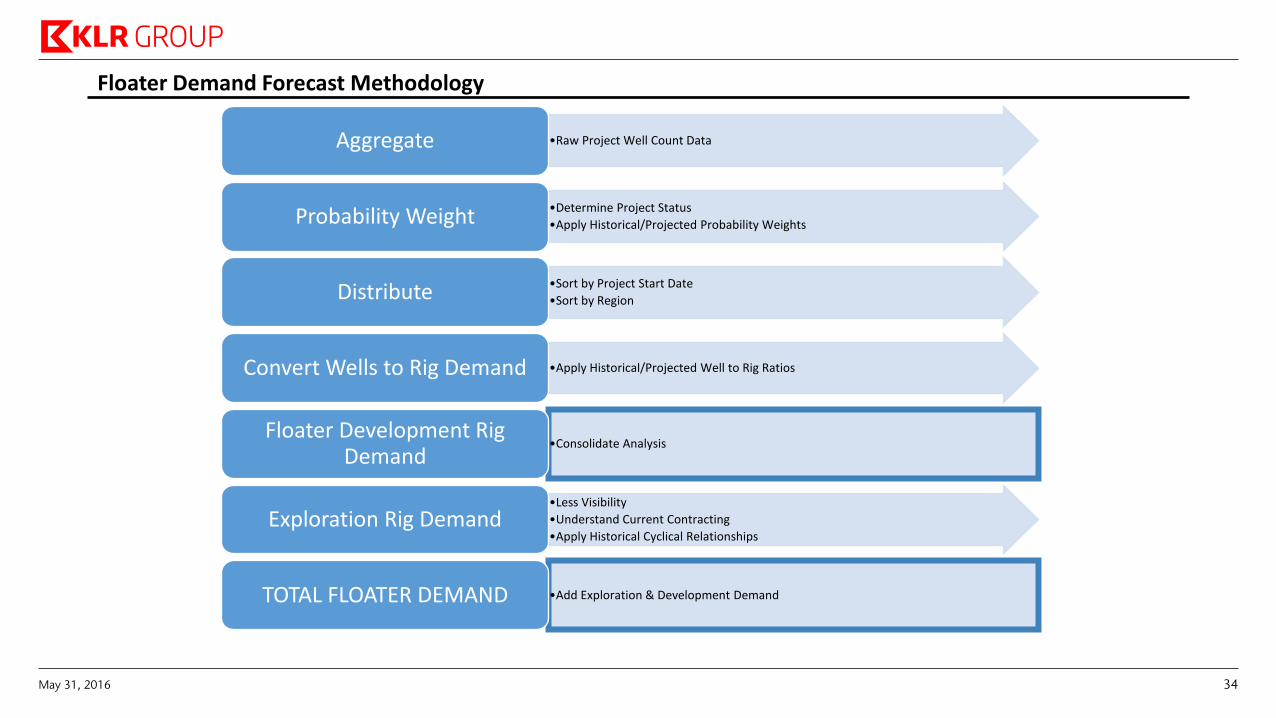

Floater Demand Forecast Methodology

•Raw Project Well Count Data Aggregate

•Determine Project Status

•Apply Historical/Projected Probability Weights Probability Weight

•Sort by Project Start Date

•Sort by Region Distribute

•Apply Historical/Projected Well to Rig Ratios Convert Wells to Rig Demand

•Consolidate Analysis Floater Development Rig

Demand

•Less Visibility

•Understand Current Contracting

•Apply Historical Cyclical Relationships Exploration Rig Demand

•Add Exploration & Development Demand TOTAL FLOATER DEMAND

May 31, 2016 34

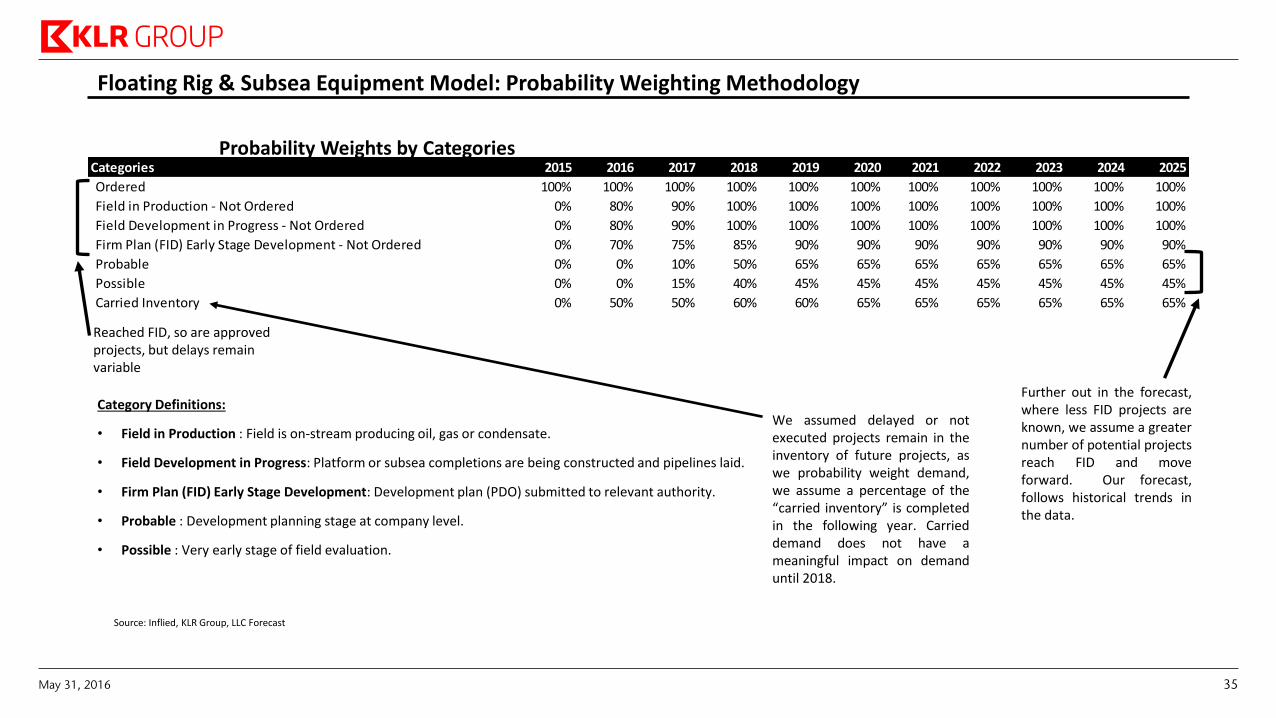

Categories 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Ordered 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Field in Production - Not Ordered 0% 80% 90% 100% 100% 100% 100% 100% 100% 100% 100%

Field Development in Progress - Not Ordered 0% 80% 90% 100% 100% 100% 100% 100% 100% 100% 100%

Firm Plan (FID) Early Stage Development - Not Ordered 0% 70% 75% 85% 90% 90% 90% 90% 90% 90% 90%

Probable 0% 0% 10% 50% 65% 65% 65% 65% 65% 65% 65%

Possible 0% 0% 15% 40% 45% 45% 45% 45% 45% 45% 45%

Carried Inventory 0% 50% 50% 60% 60% 65% 65% 65% 65% 65% 65%

Floating Rig & Subsea Equipment Model: Probability Weighting Methodology

Category Definitions:

• Field in Production : Field is on-stream producing oil, gas or condensate.

• Field Development in Progress: Platform or subsea completions are being constructed and pipelines laid.

• Firm Plan (FID) Early Stage Development: Development plan (PDO) submitted to relevant authority.

• Probable : Development planning stage at company level.

• Possible : Very early stage of field evaluation.

Probability Weights by Categories

Reached FID, so are approved projects, but delays remain variable

We assumed delayed or not executed projects remain in the inventory of future projects, as we probability weight demand, we assume a percentage of the “carried inventory” is completed in the following year. Carried demand does not have a meaningful impact on demand until 2018.

Further out in the forecast, where less FID projects are known, we assume a greater number of potential projects reach FID and move forward. Our forecast, follows historical trends in the data.

Source: Inflied, KLR Group, LLC Forecast

May 31, 2016 35

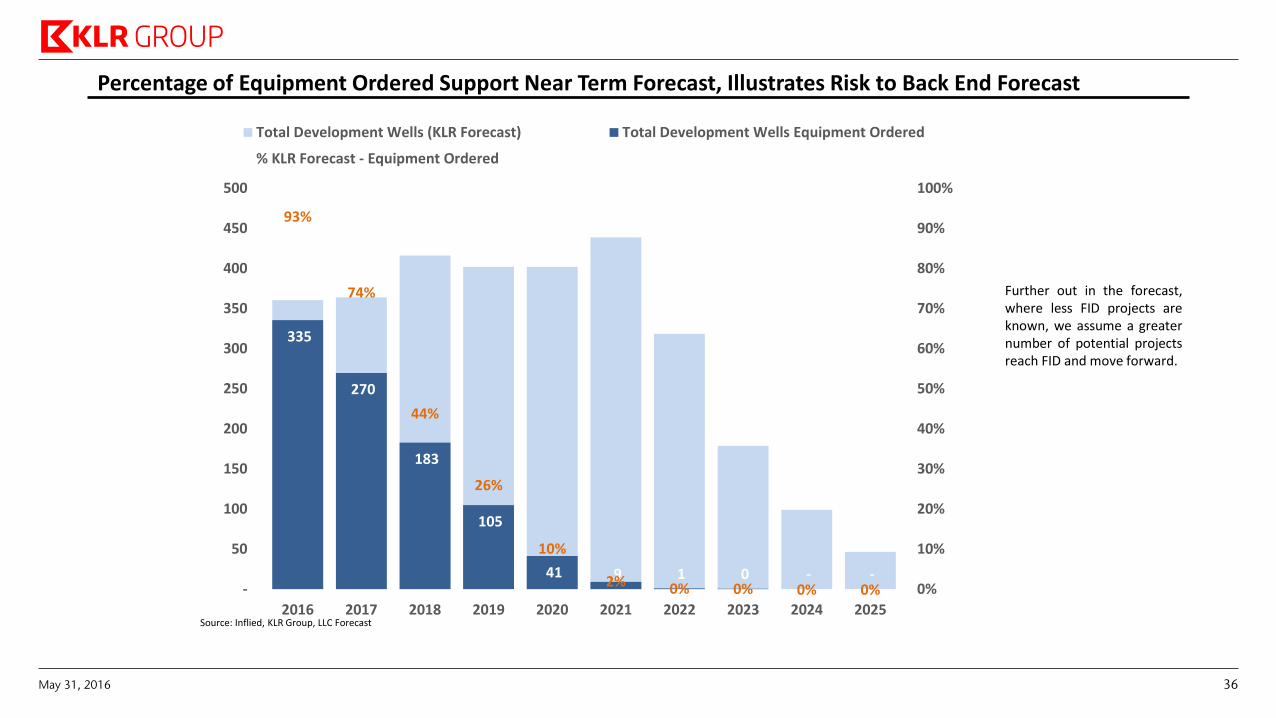

Percentage of Equipment Ordered Support Near Term Forecast, Illustrates Risk to Back End Forecast

Further out in the forecast, where less FID projects are known, we assume a greater number of potential projects reach FID and move forward.

Source: Infield, KLR Group, LLC Forecast

335

270

183

105

41 9 1 0 - -

93%

74%

44%

26%

10%

2% 0% 0% 0% 0% 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

50

100

150

200

250

300

350

400

450

500

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Total Development Wells (KLR Forecast) Total Development Wells Equipment Ordered

% KLR Forecast - Equipment Ordered

Source: Inflied, KLR Group, LLC Forecast

May 31, 2016 36

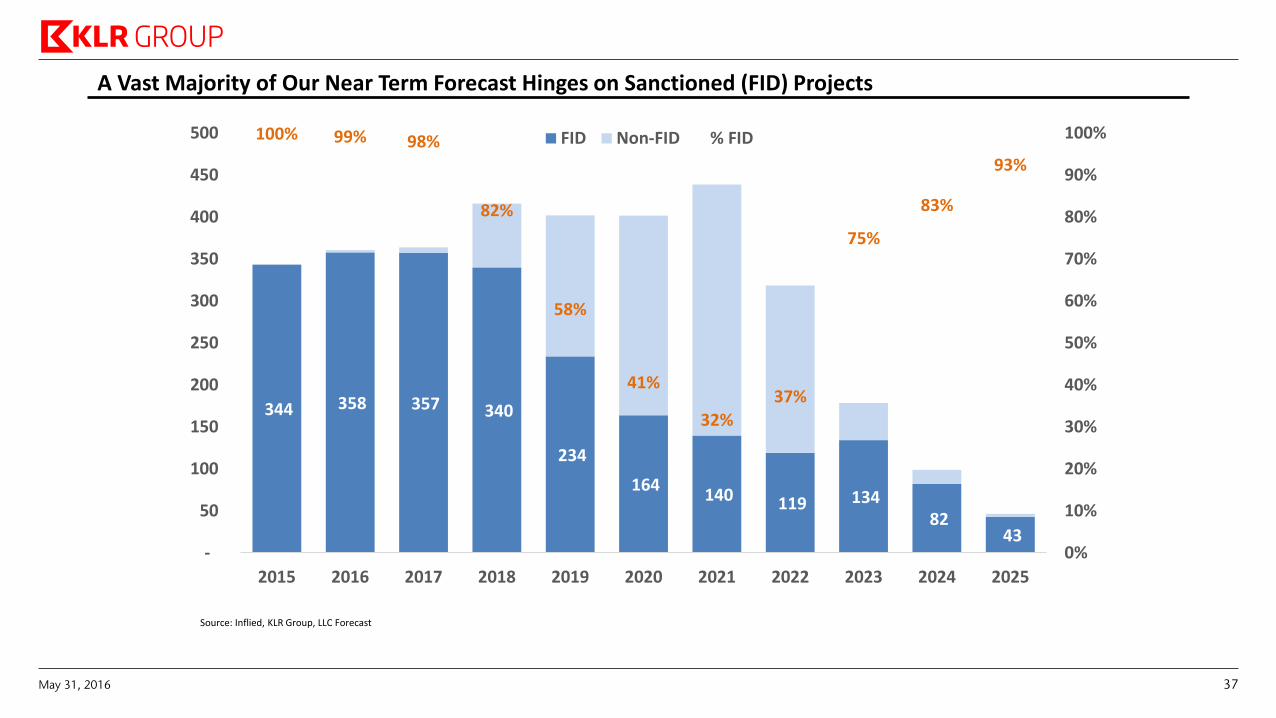

A Vast Majority of Our Near Term Forecast Hinges on Sanctioned (FID) Projects

344 358 357 340

234

164 140 119 134

82 43

100% 99% 98%

82%

58%

41%

32%

37%

75%

83%

93%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

50

100

150

200

250

300

350

400

450

500

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

FID Non-FID % FID

Source: Inflied, KLR Group, LLC Forecast

May 31, 2016 37

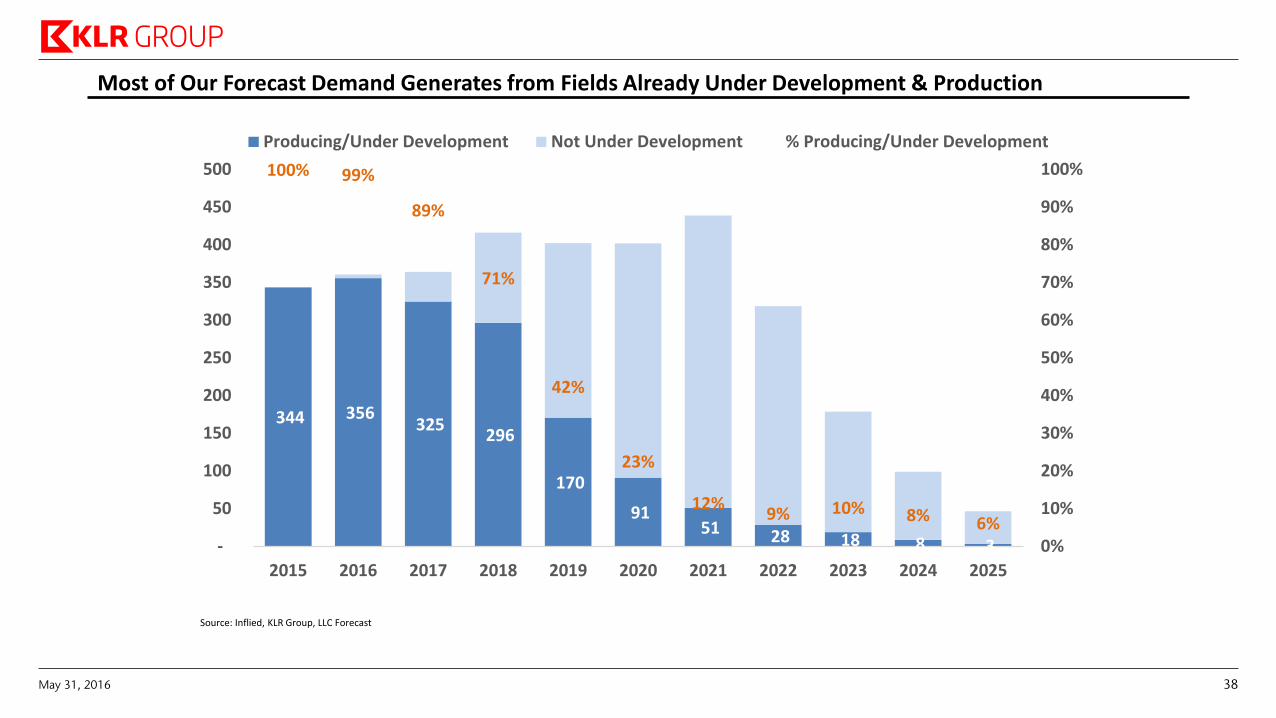

Most of Our Forecast Demand Generates from Fields Already Under Development & Production

344 356 325

296

170

91 51 28 18 8 3

100% 99%

89%

71%

42%

23%

12%9% 10% 8% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

50

100

150

200

250

300

350

400

450

500

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Producing/Under Development Not Under Development % Producing/Under Development

Source: Inflied, KLR Group, LLC Forecast

May 31, 2016 38

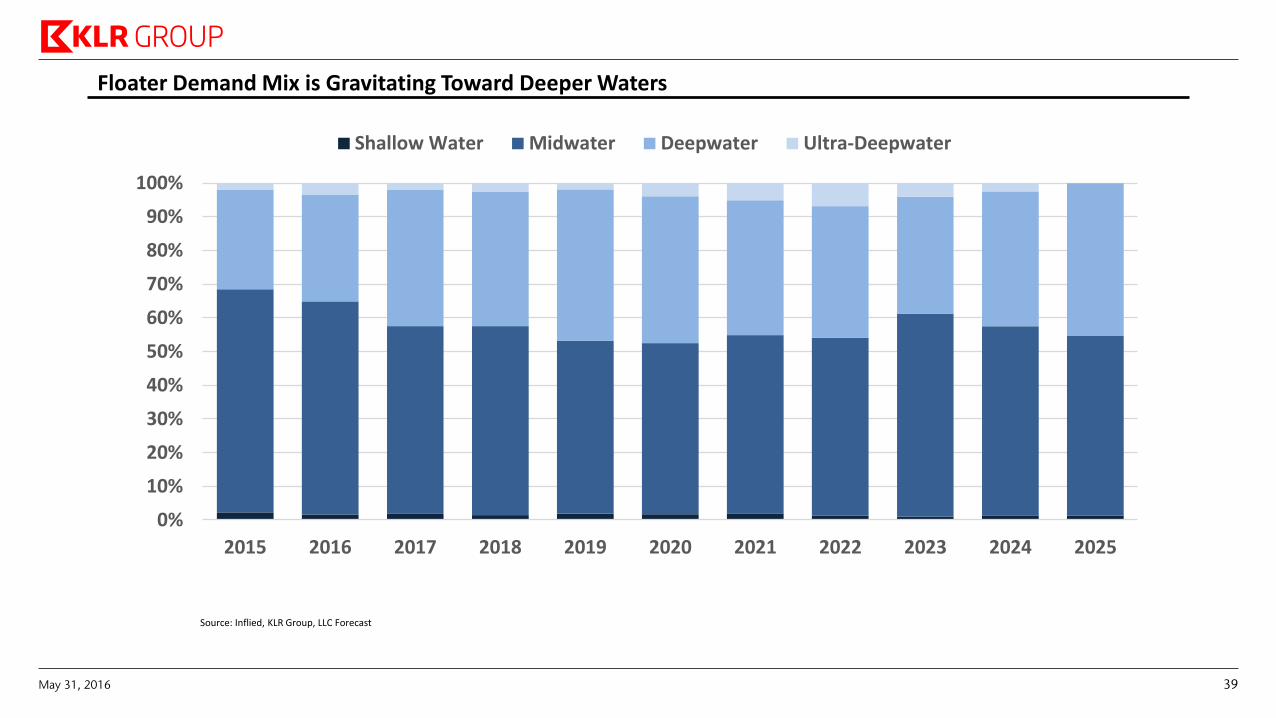

Floater Demand Mix is Gravitating Toward Deeper Waters

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Shallow Water Midwater Deepwater Ultra-Deepwater

Source: Inflied, KLR Group, LLC Forecast

May 31, 2016 39

Offshore Jackup Market

May 31, 2016 40

382 398

417 396

409 416 431

470 496 487

457 459 467 479

493

232

347 368

325 317 327

356

401 418

378

318 341

392 416

431 61%

87% 88%

82%

77% 78%83%

85% 84%

78%

70%

74%

84% 87% 87%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E 2017E 2018E 2019E 2020E

Uti

lizat

ion

Nu

mb

er

of

Rig

sMarket Supply, EOP Contracted / Demand Implied Utilization

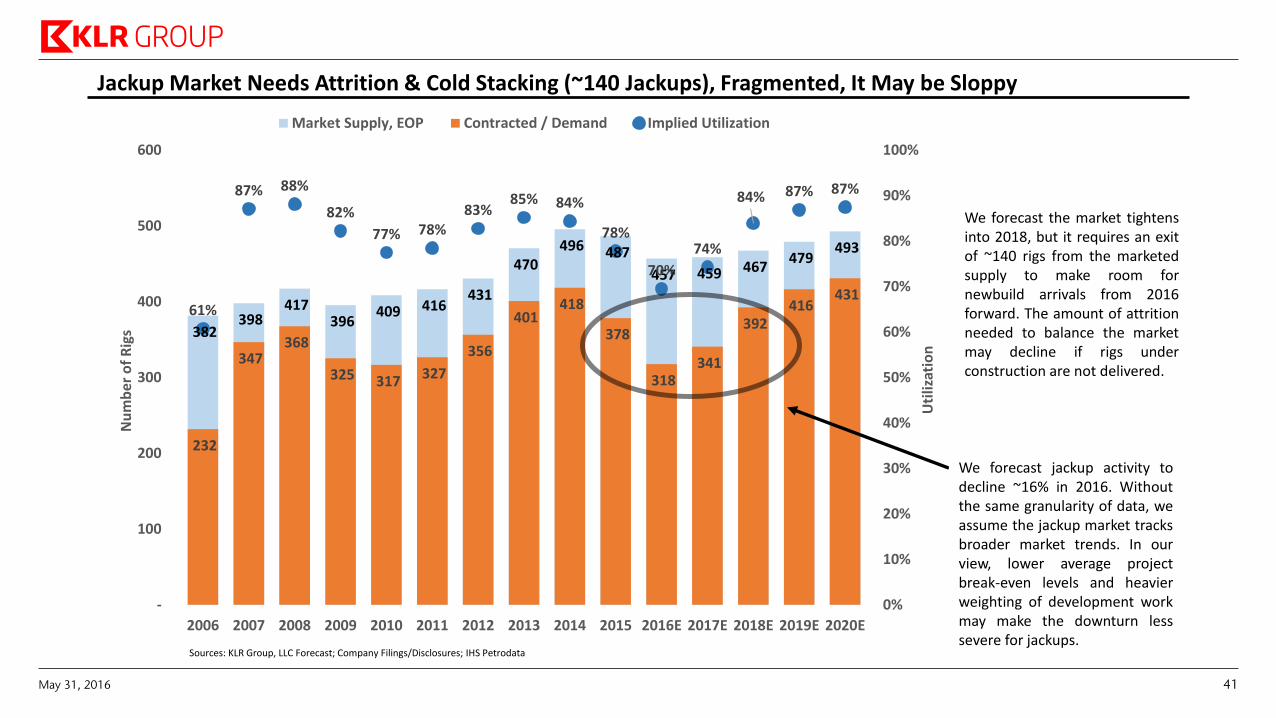

Jackup Market Needs Attrition & Cold Stacking (~140 Jackups), Fragmented, It May be Sloppy

We forecast jackup activity to decline ~16% in 2016. Without the same granularity of data, we assume the jackup market tracks broader market trends. In our view, lower average project break-even levels and heavier weighting of development work may make the downturn less severe for jackups.

We forecast the market tightens into 2018, but it requires an exit of ~140 rigs from the marketed supply to make room for newbuild arrivals from 2016 forward. The amount of attrition needed to balance the market may decline if rigs under construction are not delivered.

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata

May 31, 2016 41

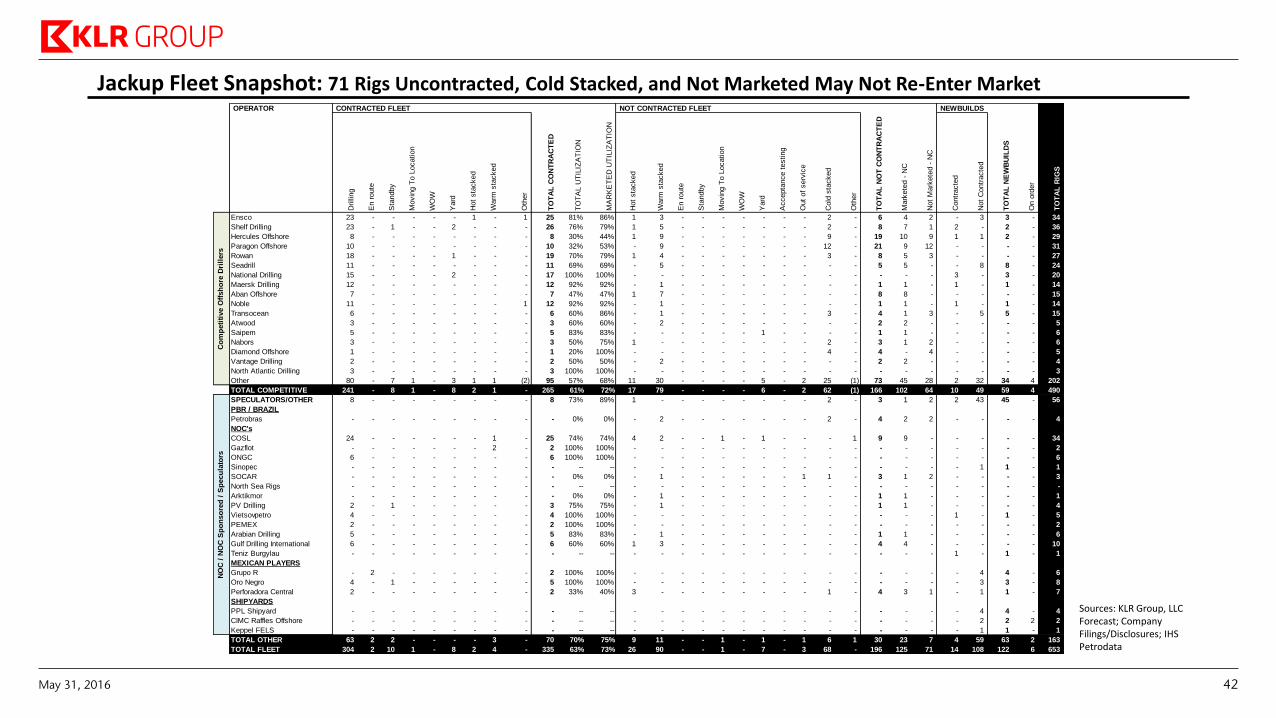

Jackup Fleet Snapshot: 71 Rigs Uncontracted, Cold Stacked, and Not Marketed May Not Re-Enter Market

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata

OPERATOR CONTRACTED FLEET NOT CONTRACTED FLEET NEWBUILDS

Drilli

ng

En r

oute

Sta

ndby

Movin

g T

o L

ocation

WO

W

Yard

Hot

sta

cked

Warm

sta

cked

Oth

er

TO

TA

L C

ON

TR

AC

TE

D

TO

TA

L U

TIL

IZA

TIO

N

MA

RK

ET

ED

UT

ILIZ

AT

ION

Hot

sta

cked

Warm

sta

cked

En r

oute

Sta

ndby

Movin

g T

o L

ocation

WO

W

Yard

Accepta

nce t

esting

Out

of

serv

ice

Cold

sta

cked

Oth

er

TO

TA

L N

OT

CO

NT

RA

CT

ED

Mark

ete

d -

NC

Not

Mark

ete

d -

NC

Contr

acte

d

Not

Contr

acte

d

TO

TA

L N

EW

BU

ILD

S

On o

rder

TO

TA

L R

IGS

Ensco 23 - - - - - 1 - 1 25 81% 86% 1 3 - - - - - - - 2 - 6 4 2 - 3 3 - 34

Shelf Drilling 23 - 1 - - 2 - - - 26 76% 79% 1 5 - - - - - - - 2 - 8 7 1 2 - 2 - 36

Hercules Offshore 8 - - - - - - - - 8 30% 44% 1 9 - - - - - - - 9 - 19 10 9 1 1 2 - 29

Paragon Offshore 10 - - - - - - - - 10 32% 53% - 9 - - - - - - - 12 - 21 9 12 - - - - 31

Rowan 18 - - - - 1 - - - 19 70% 79% 1 4 - - - - - - - 3 - 8 5 3 - - - - 27

Seadrill 11 - - - - - - - - 11 69% 69% - 5 - - - - - - - - - 5 5 - - 8 8 - 24

National Drilling 15 - - - - 2 - - - 17 100% 100% - - - - - - - - - - - - - - 3 - 3 - 20

Maersk Drilling 12 - - - - - - - - 12 92% 92% - 1 - - - - - - - - - 1 1 - 1 - 1 - 14

Aban Offshore 7 - - - - - - - - 7 47% 47% 1 7 - - - - - - - - - 8 8 - - - - - 15

Noble 11 - - - - - - - 1 12 92% 92% - 1 - - - - - - - - - 1 1 - 1 - 1 - 14

Transocean 6 - - - - - - - - 6 60% 86% - 1 - - - - - - - 3 - 4 1 3 - 5 5 - 15

Atwood 3 - - - - - - - - 3 60% 60% - 2 - - - - - - - - - 2 2 - - - - - 5

Saipem 5 - - - - - - - - 5 83% 83% - - - - - - 1 - - - - 1 1 - - - - - 6

Nabors 3 - - - - - - - - 3 50% 75% 1 - - - - - - - - 2 - 3 1 2 - - - - 6

Diamond Offshore 1 - - - - - - - - 1 20% 100% - - - - - - - - - 4 - 4 - 4 - - - - 5

Vantage Drilling 2 - - - - - - - - 2 50% 50% - 2 - - - - - - - - - 2 2 - - - - - 4

North Atlantic Drilling 3 - - - - - - - - 3 100% 100% - - - - - - - - - - - - - - - - - - 3

Other 80 - 7 1 - 3 1 1 (2) 95 57% 68% 11 30 - - - - 5 - 2 25 (1) 73 45 28 2 32 34 4 202

TOTAL COMPETITIVE 241 - 8 1 - 8 2 1 - 265 61% 72% 17 79 - - - - 6 - 2 62 (1) 166 102 64 10 49 59 4 490

SPECULATORS/OTHER 8 - - - - - - - - 8 73% 89% 1 - - - - - - - - 2 - 3 1 2 2 43 45 - 56

PBR / BRAZIL

Petrobras - - - - - - - - - - 0% 0% - 2 - - - - - - - 2 - 4 2 2 - - - - 4

NOC's

COSL 24 - - - - - - 1 - 25 74% 74% 4 2 - - 1 - 1 - - - 1 9 9 - - - - - 34

Gazflot - - - - - - - 2 - 2 100% 100% - - - - - - - - - - - - - - - - - - 2

ONGC 6 - - - - - - - - 6 100% 100% - - - - - - - - - - - - - - - - - - 6

Sinopec - - - - - - - - - - -- -- - - - - - - - - - - - - - - - 1 1 - 1

SOCAR - - - - - - - - - - 0% 0% - 1 - - - - - - 1 1 - 3 1 2 - - - - 3

North Sea Rigs - - - - - - - - - - -- -- - - - - - - - - - - - - - - - - - - -

Arktikmor - - - - - - - - - - 0% 0% - 1 - - - - - - - - - 1 1 - - - - - 1

PV Drilling 2 - 1 - - - - - - 3 75% 75% - 1 - - - - - - - - - 1 1 - - - - - 4

Vietsovpetro 4 - - - - - - - - 4 100% 100% - - - - - - - - - - - - - - 1 - 1 - 5

PEMEX 2 - - - - - - - - 2 100% 100% - - - - - - - - - - - - - - - - - - 2

Arabian Drilling 5 - - - - - - - - 5 83% 83% - 1 - - - - - - - - - 1 1 - - - - - 6

Gulf Drilling International 6 - - - - - - - - 6 60% 60% 1 3 - - - - - - - - - 4 4 - - - - - 10

Teniz Burgylau - - - - - - - - - - -- -- - - - - - - - - - - - - - - 1 - 1 - 1

MEXICAN PLAYERS

Grupo R - 2 - - - - - - - 2 100% 100% - - - - - - - - - - - - - - - 4 4 - 6

Oro Negro 4 - 1 - - - - - - 5 100% 100% - - - - - - - - - - - - - - - 3 3 - 8

Perforadora Central 2 - - - - - - - - 2 33% 40% 3 - - - - - - - - 1 - 4 3 1 - 1 1 - 7

SHIPYARDS

PPL Shipyard - - - - - - - - - - -- -- - - - - - - - - - - - - - - - 4 4 - 4

CIMC Raffles Offshore - - - - - - - - - - -- -- - - - - - - - - - - - - - - - 2 2 2 2

Keppel FELS - - - - - - - - - - -- -- - - - - - - - - - - - - - - - 1 1 - 1

TOTAL OTHER 63 2 2 - - - - 3 - 70 70% 75% 9 11 - - 1 - 1 - 1 6 1 30 23 7 4 59 63 2 163

TOTAL FLEET 304 2 10 1 - 8 2 4 - 335 63% 73% 26 90 - - 1 - 7 - 3 68 - 196 125 71 14 108 122 6 653

NO

C /

NO

C S

po

nso

red

/ S

pecu

lato

rsC

om

peti

tive O

ffsh

ore

Dri

llers

May 31, 2016 42

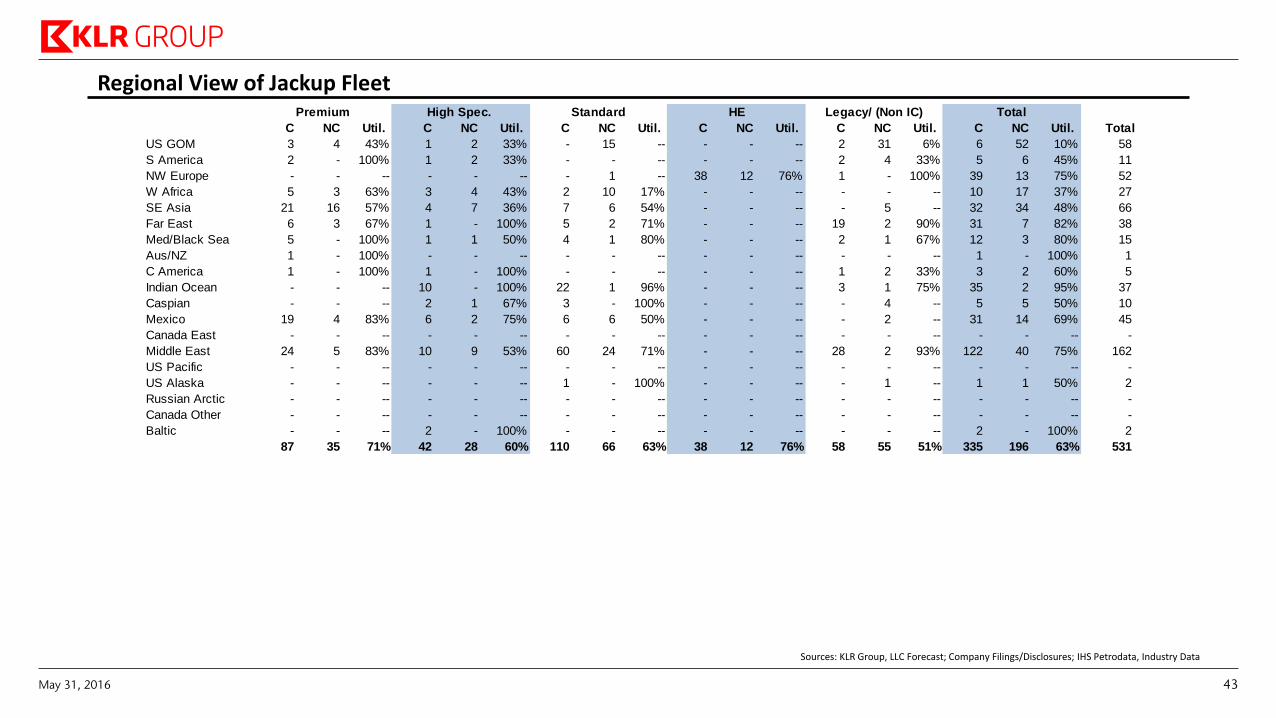

Regional View of Jackup Fleet Premium High Spec. Standard HE Legacy/ (Non IC) Total

C NC Util. C NC Util. C NC Util. C NC Util. C NC Util. C NC Util. Total

US GOM 3 4 43% 1 2 33% - 15 -- - - -- 2 31 6% 6 52 10% 58

S America 2 - 100% 1 2 33% - - -- - - -- 2 4 33% 5 6 45% 11

NW Europe - - -- - - -- - 1 -- 38 12 76% 1 - 100% 39 13 75% 52

W Africa 5 3 63% 3 4 43% 2 10 17% - - -- - - -- 10 17 37% 27

SE Asia 21 16 57% 4 7 36% 7 6 54% - - -- - 5 -- 32 34 48% 66

Far East 6 3 67% 1 - 100% 5 2 71% - - -- 19 2 90% 31 7 82% 38

Med/Black Sea 5 - 100% 1 1 50% 4 1 80% - - -- 2 1 67% 12 3 80% 15

Aus/NZ 1 - 100% - - -- - - -- - - -- - - -- 1 - 100% 1

C America 1 - 100% 1 - 100% - - -- - - -- 1 2 33% 3 2 60% 5

Indian Ocean - - -- 10 - 100% 22 1 96% - - -- 3 1 75% 35 2 95% 37

Caspian - - -- 2 1 67% 3 - 100% - - -- - 4 -- 5 5 50% 10

Mexico 19 4 83% 6 2 75% 6 6 50% - - -- - 2 -- 31 14 69% 45

Canada East - - -- - - -- - - -- - - -- - - -- - - -- -

Middle East 24 5 83% 10 9 53% 60 24 71% - - -- 28 2 93% 122 40 75% 162

US Pacific - - -- - - -- - - -- - - -- - - -- - - -- -

US Alaska - - -- - - -- 1 - 100% - - -- - 1 -- 1 1 50% 2

Russian Arctic - - -- - - -- - - -- - - -- - - -- - - -- -

Canada Other - - -- - - -- - - -- - - -- - - -- - - -- -

Baltic - - -- 2 - 100% - - -- - - -- - - -- 2 - 100% 2

87 35 71% 42 28 60% 110 66 63% 38 12 76% 58 55 51% 335 196 63% 531

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 43

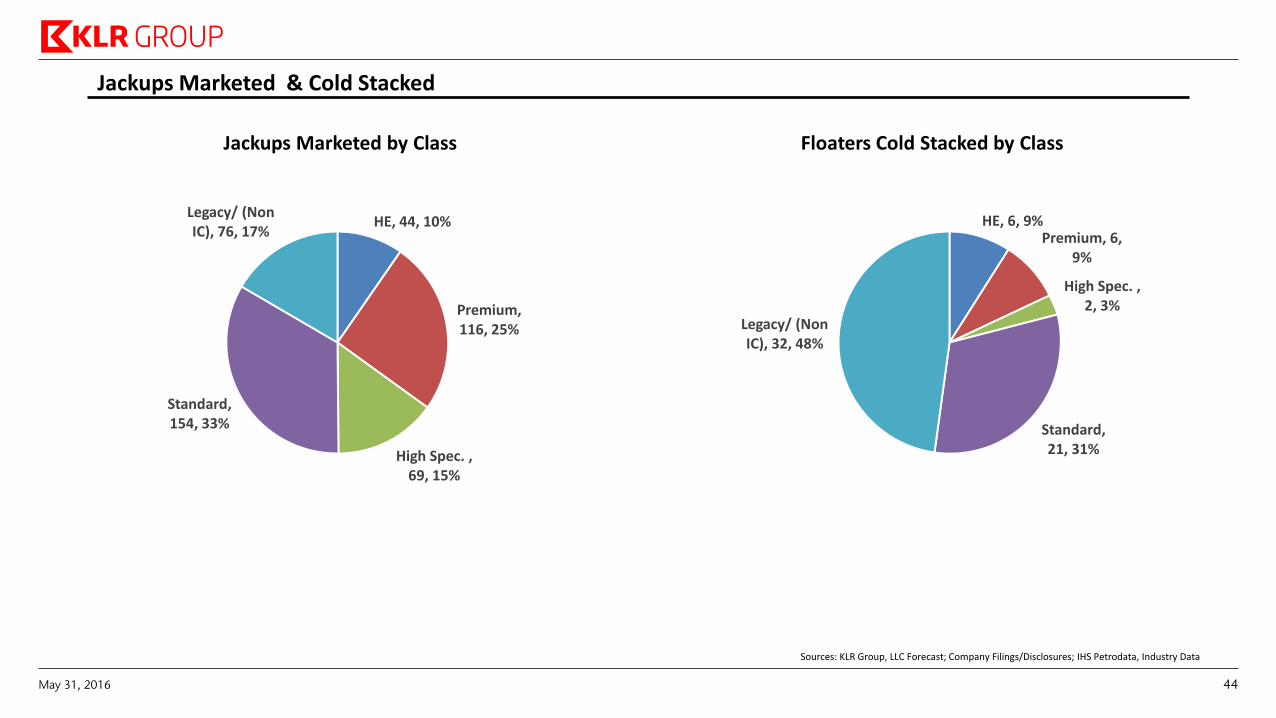

Jackups Marketed & Cold Stacked

HE, 44, 10%

Premium, 116, 25%

High Spec. , 69, 15%

Standard, 154, 33%

Legacy/ (Non IC), 76, 17%

HE, 6, 9%Premium, 6,

9%

High Spec. , 2, 3%

Standard, 21, 31%

Legacy/ (Non IC), 32, 48%

Jackups Marketed by Class Floaters Cold Stacked by Class

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 44

Offshore Rig Supply & Attrition

May 31, 2016 45

Floater Supply Forecast

Jackup Supply Forecast

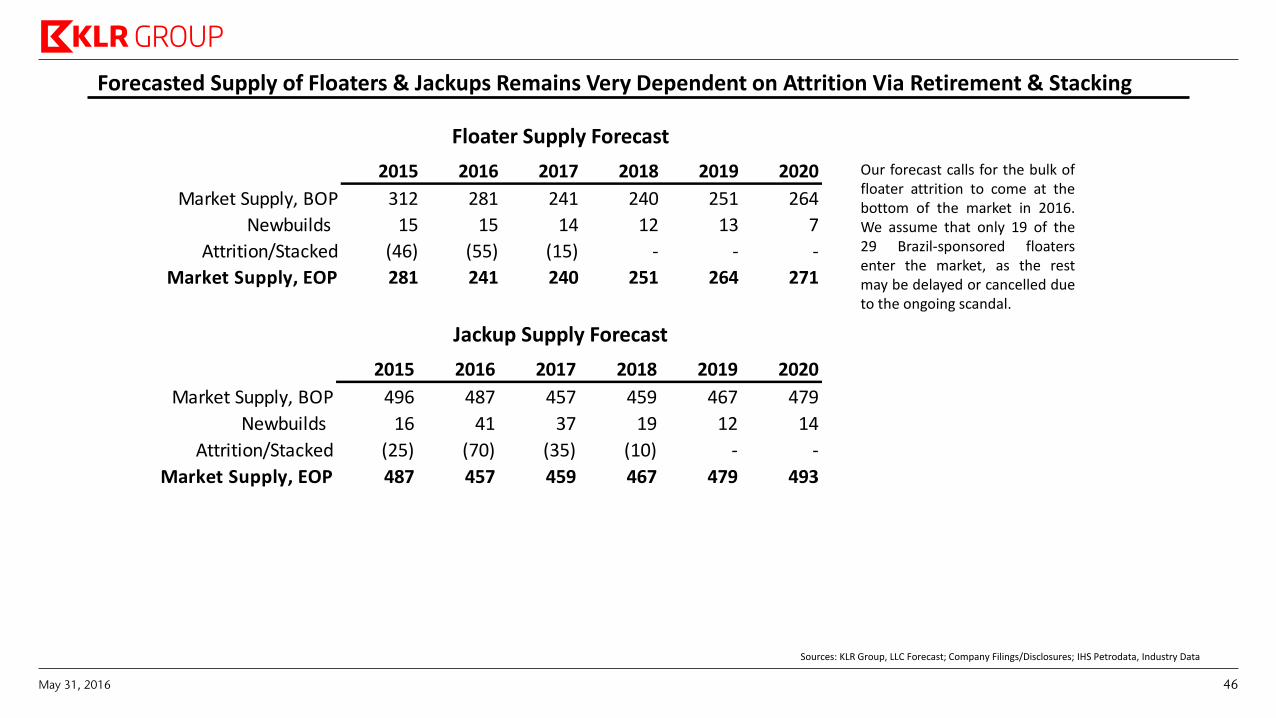

Forecasted Supply of Floaters & Jackups Remains Very Dependent on Attrition Via Retirement & Stacking

Our forecast calls for the bulk of floater attrition to come at the bottom of the market in 2016. We assume that only 19 of the 29 Brazil-sponsored floaters enter the market, as the rest may be delayed or cancelled due to the ongoing scandal.

2015 2016 2017 2018 2019 2020

Market Supply, BOP 496 487 457 459 467 479

Newbuilds 16 41 37 19 12 14

Attrition/Stacked (25) (70) (35) (10) - -

Market Supply, EOP 487 457 459 467 479 493

2015 2016 2017 2018 2019 2020

Market Supply, BOP 312 281 241 240 251 264

Newbuilds 15 15 14 12 13 7

Attrition/Stacked (46) (55) (15) - - -

Market Supply, EOP 281 241 240 251 264 271

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 46

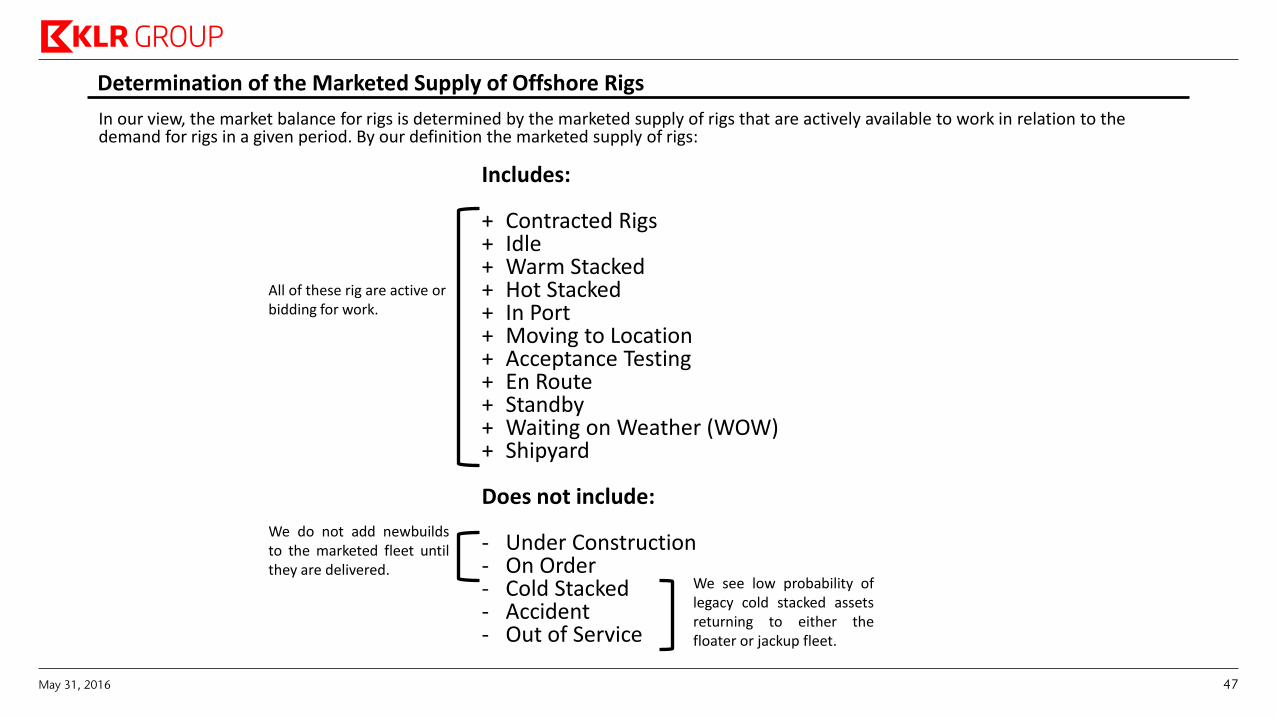

Determination of the Marketed Supply of Offshore Rigs

In our view, the market balance for rigs is determined by the marketed supply of rigs that are actively available to work in relation to the demand for rigs in a given period. By our definition the marketed supply of rigs:

Includes: + Contracted Rigs + Idle + Warm Stacked + Hot Stacked + In Port + Moving to Location + Acceptance Testing + En Route + Standby + Waiting on Weather (WOW) + Shipyard

Does not include:

- Under Construction - On Order - Cold Stacked - Accident - Out of Service

All of these rig are active or bidding for work.

We do not add newbuilds to the marketed fleet until they are delivered.

We see low probability of legacy cold stacked assets returning to either the floater or jackup fleet.

May 31, 2016 47

0 0 0

6

14 14 10

1 1 4 4

0 1

9

21 22

31

19

13

24

15 15

(4)(2) (1) (1)

0 0 0 0 (3)

(7)(4)

0 (1)

0

0

(2) (1) (2)0

(15)

(30)

(15)

(40)

(30)

(20)

(10)

-

10

20

30

40

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Rig

s (R

etir

ed

) /

Ad

de

dNewbuilds Retirements

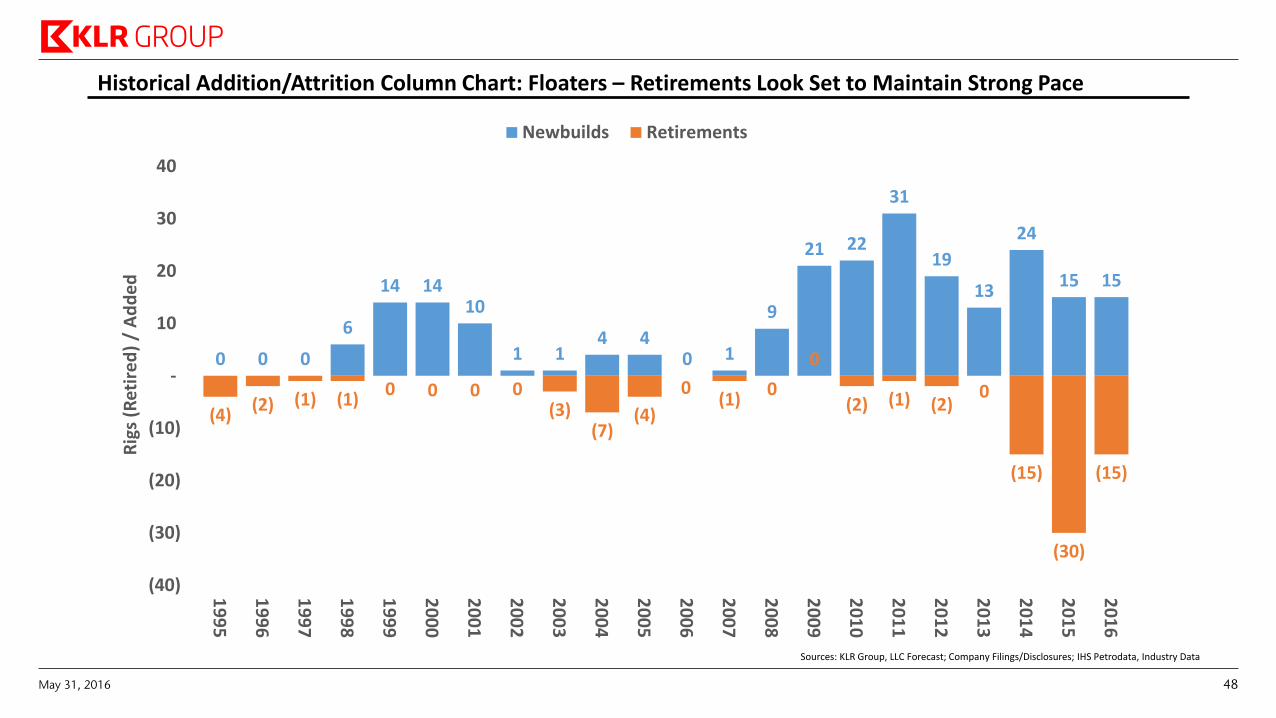

Historical Addition/Attrition Column Chart: Floaters – Retirements Look Set to Maintain Strong Pace

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 48

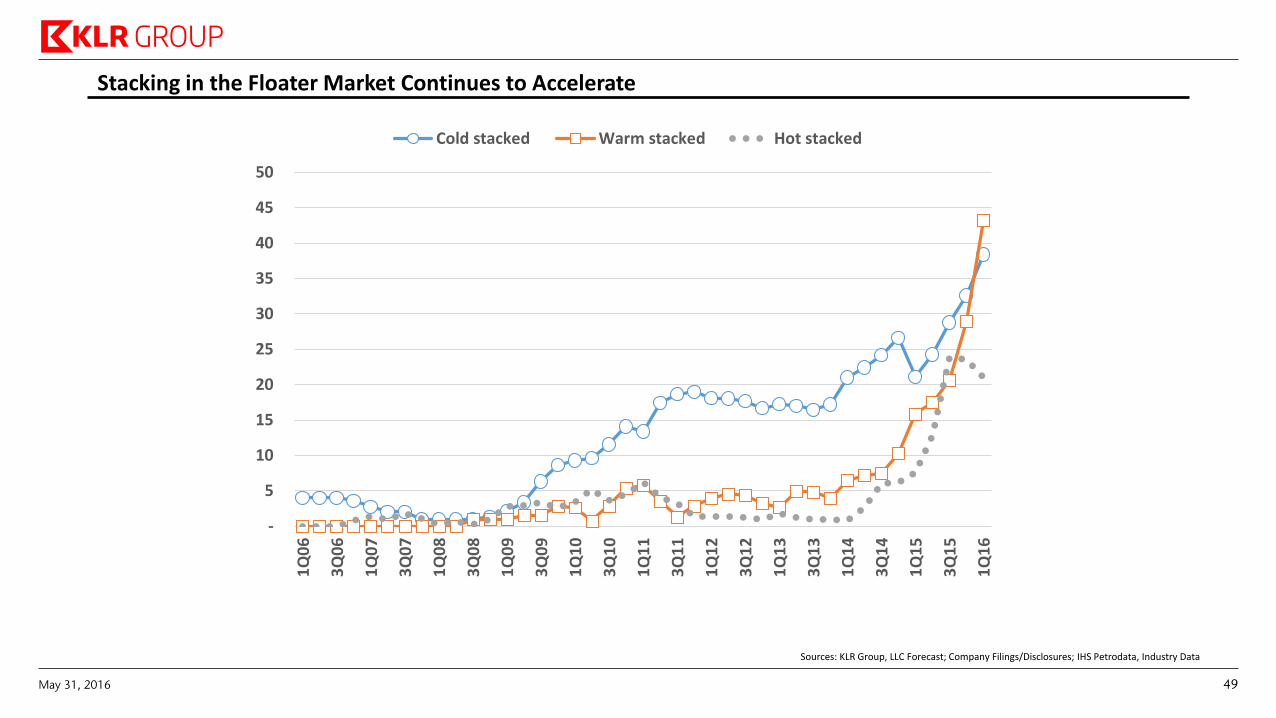

Stacking in the Floater Market Continues to Accelerate

-

5

10

15

20

25

30

35

40

45

50

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

Cold stacked Warm stacked Hot stacked

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 49

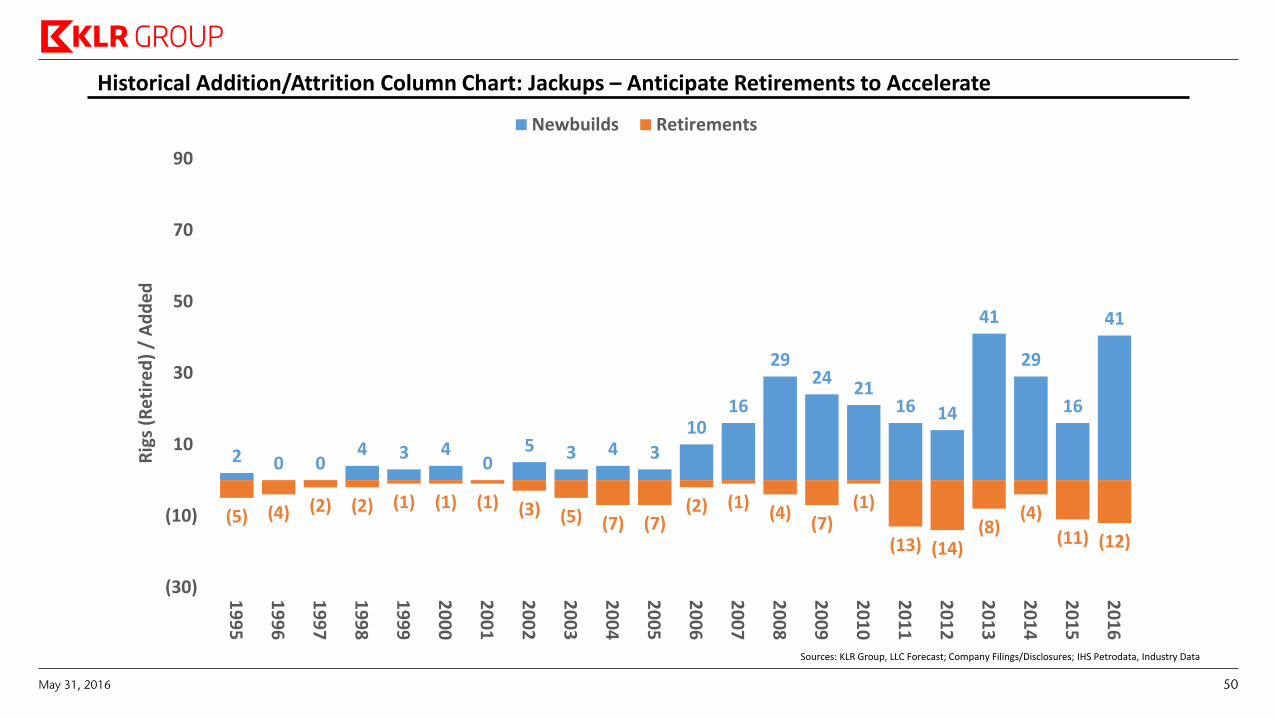

Historical Addition/Attrition Column Chart: Jackups – Anticipate Retirements to Accelerate

2 0 0 4 3 4

0 5 3 4 3

10 16

29 24

21 16 14

41

29

16

41

(5) (4) (2) (2) (1) (1) (1) (3) (5) (7) (7)(2) (1)

(4)(7)

(1)

(13) (14)(8)

(4)

(11) (12)

(30)

(10)

10

30

50

70

90

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Rig

s (R

etir

ed

) /

Ad

de

dNewbuilds Retirements

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 50

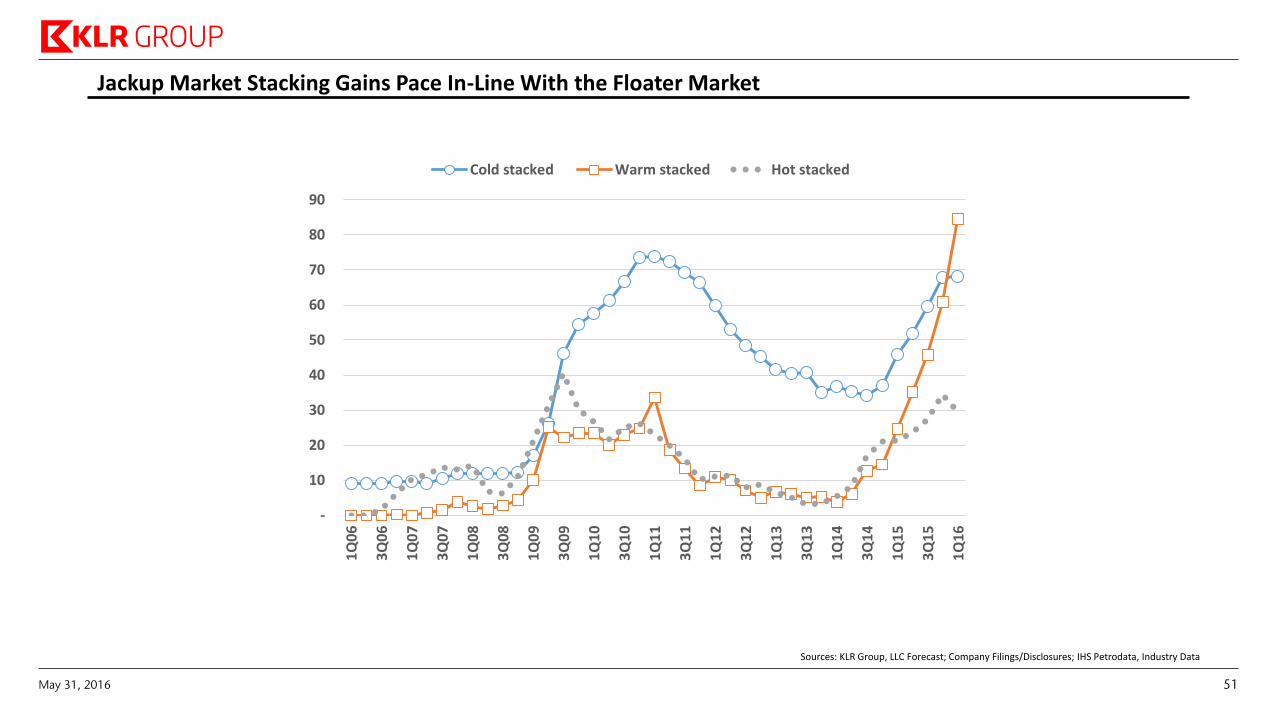

Jackup Market Stacking Gains Pace In-Line With the Floater Market

-

10

20

30

40

50

60

70

80

90

1Q

06

3Q

06

1Q

07

3Q

07

1Q

08

3Q

08

1Q

09

3Q

09

1Q

10

3Q

10

1Q

11

3Q

11

1Q

12

3Q

12

1Q

13

3Q

13

1Q

14

3Q

14

1Q

15

3Q

15

1Q

16

Cold stacked Warm stacked Hot stacked

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 51

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Rig

Fac

tor

Sco

re

Rig Delivery Year

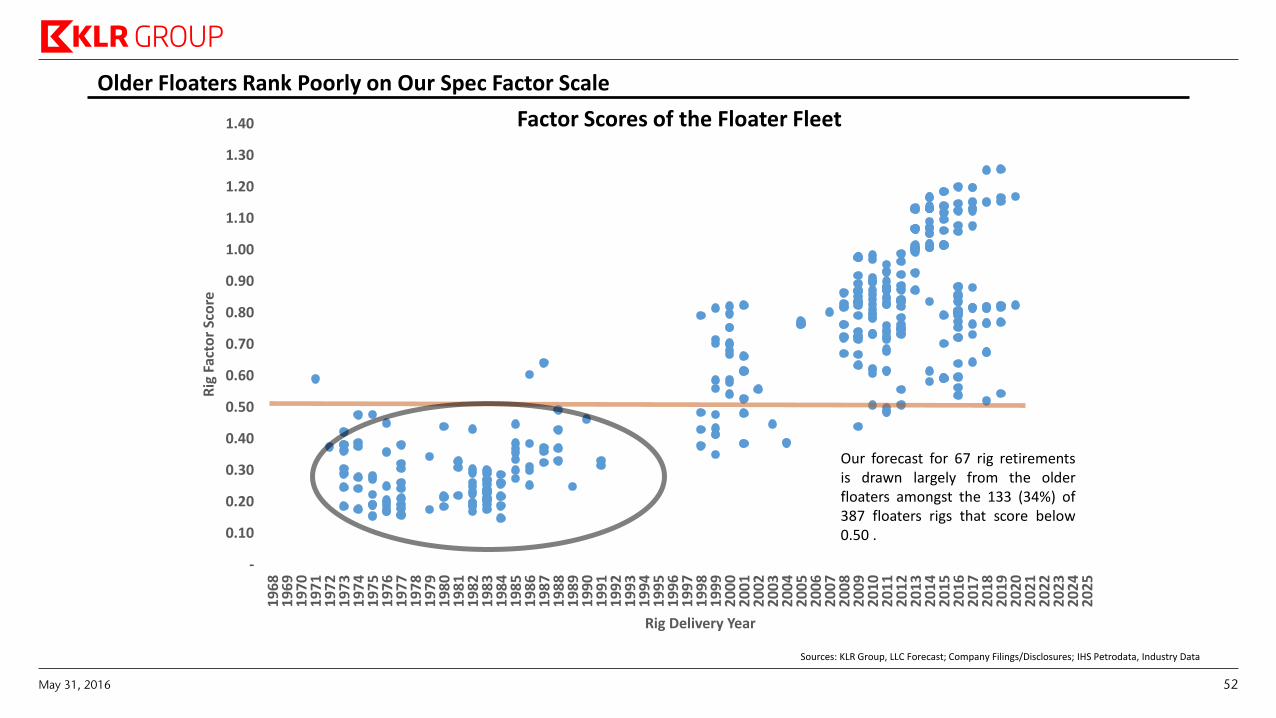

Older Floaters Rank Poorly on Our Spec Factor Scale

Our forecast for 67 rig retirements is drawn largely from the older floaters amongst the 133 (34%) of 387 floaters rigs that score below 0.50 .

Factor Scores of the Floater Fleet

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 52

-

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

1.40

1.50

1.60

19

60

19

61

19

62

19

63

19

64

19

65

19

66

19

67

19

68

19

69

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Rig

Fac

tor

Sco

re

Rig Delivery Year

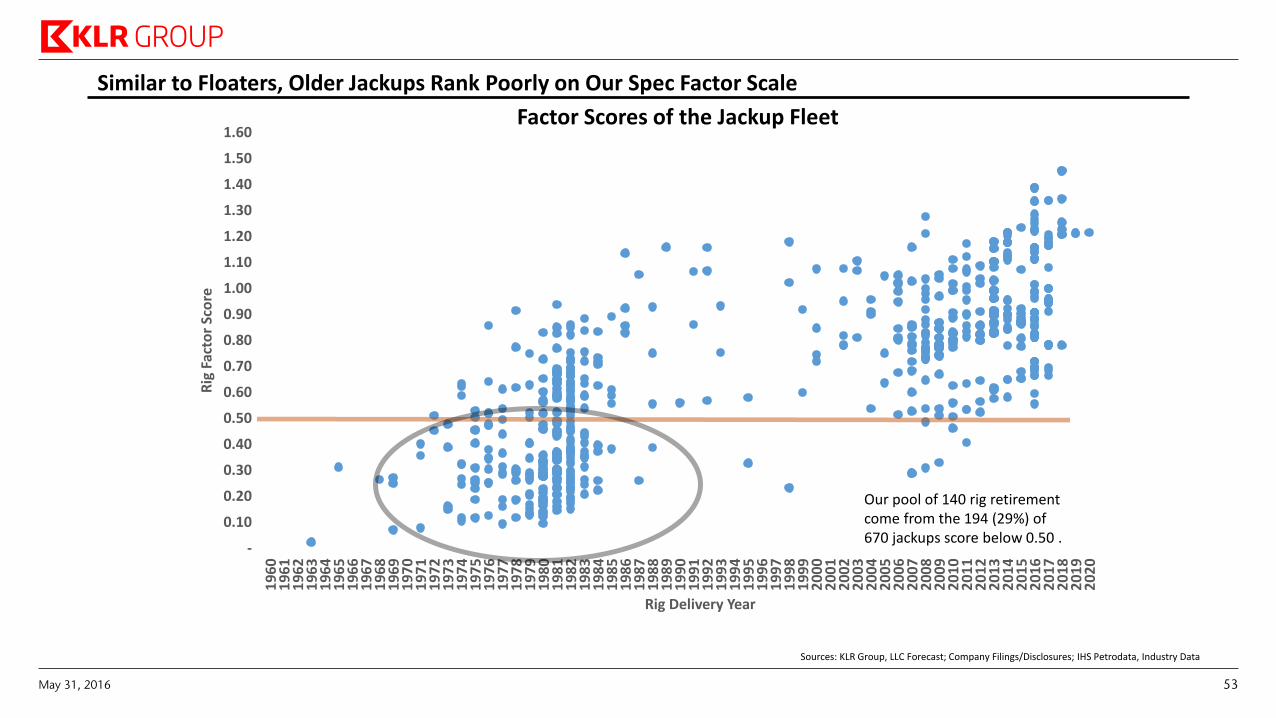

Similar to Floaters, Older Jackups Rank Poorly on Our Spec Factor Scale

Our pool of 140 rig retirement come from the 194 (29%) of 670 jackups score below 0.50 .

Factor Scores of the Jackup Fleet

Sources: KLR Group, LLC Forecast; Company Filings/Disclosures; IHS Petrodata, Industry Data

May 31, 2016 53

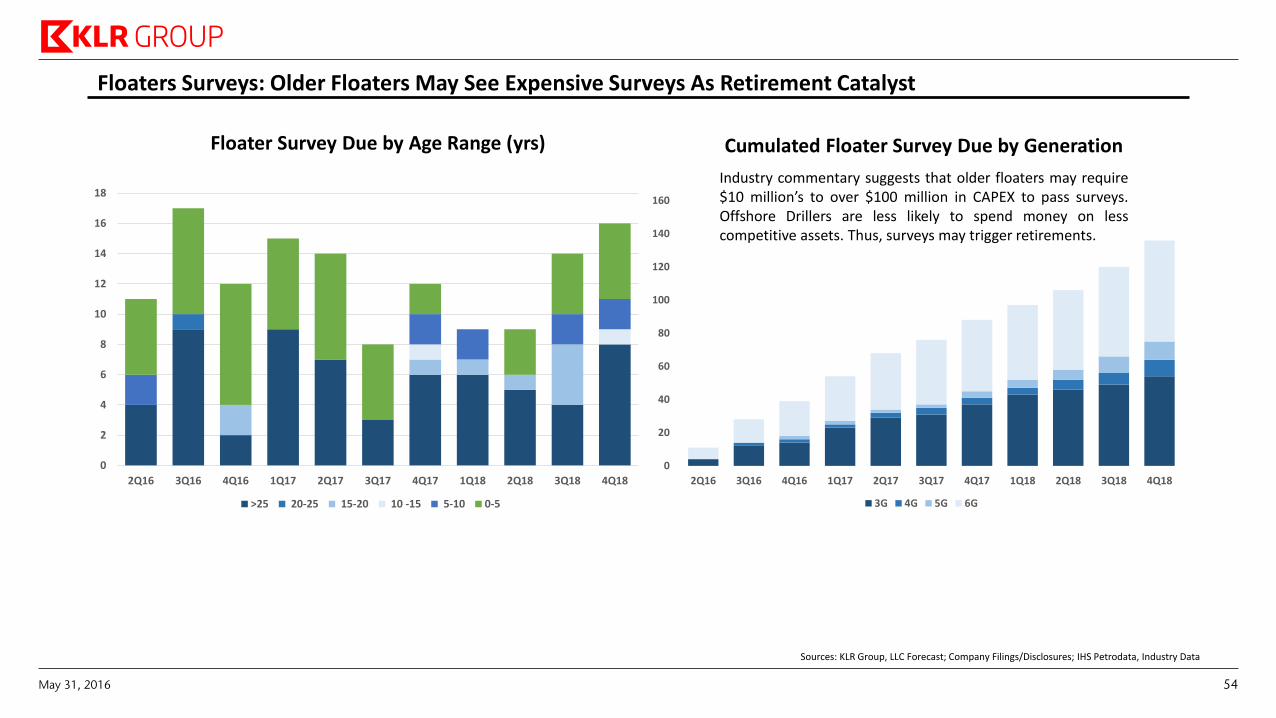

Floaters Surveys: Older Floaters May See Expensive Surveys As Retirement Catalyst

0

2

4

6

8

10

12

14

16

18

2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

>25 20-25 15-20 10 -15 5-10 0-5

0

20

40

60

80

100

120

140

160

2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

3G 4G 5G 6G