Embed Size (px)

Citation preview

2015: HOW FAR IS THE RECOVERY?

CHINA: CARROT AND STICK

> Rocky TUNG Economist, Asia Pacific, Coface

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 13

/

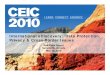

Broad-based economic slowdown: Our logic

Economic growth

Investment

Property

Infrastructure

Consumption

Luxury goods

Necessity items

Government revenue

Commodity demand

Asset price

volatility

Job growth

Quality of life

Source: Coface

~48%

~36%

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 14

/

Content

Macroeconomic environment

Sectoral development

Property

Consumer goods

Steel

Conclusion

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 15

/

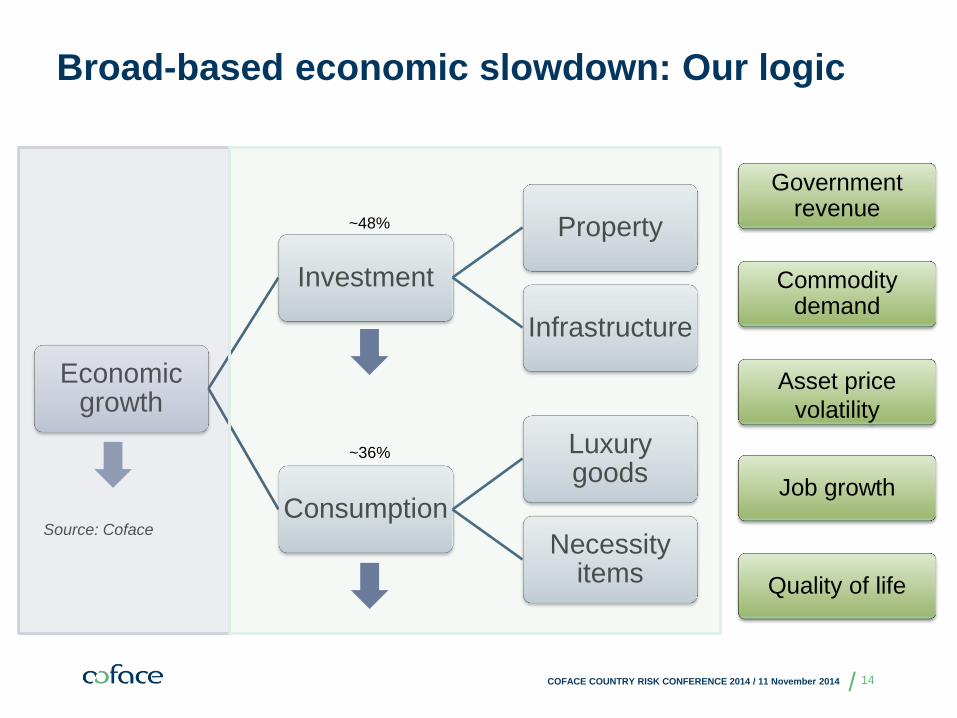

Continuation of the slowing trends

2011 2012 2013 2014F 2015F

GDP growth (%) 9.3 7.8 7.7 7.4 7.0

CPI (%) 5.4 2.7 2.6 2.3 2.9

M2 (%) 13.6 13.8 13.6 13.0 13.0

Fixed Asset

Investment (%) 23.8 20.6 19.6 16.3 16.0

Retail Sales (%) 17.1 14.3 13.1 12.2 11.2

RMB/USD

(year-end) 6.301 6.286 6.097 6.100 5.978

Source: CEIC, Coface estimates

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 16

/

Policy direction

Job creation

Inflation

Growth

Policy stance to revolve around 3 key factors

Source: Coface

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 17

/

GDP Target @ ~7.5%: Falling short

Source: CEIC, Coface estimates

A steady structural shift toward the 7% range

Expectation management matters

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 18

0%

2%

4%

6%

8%

10%

12%

14%

16%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F 2015F

GDP target Actual GDP growth

6%

7%

8%

9%

10%

11%

12%

13%

14%

15%

Slowing GDP growth in China

GDP Growth

YoY

13.4%

10.2%

7.8%

Avg for 2014/15 7.2%

/

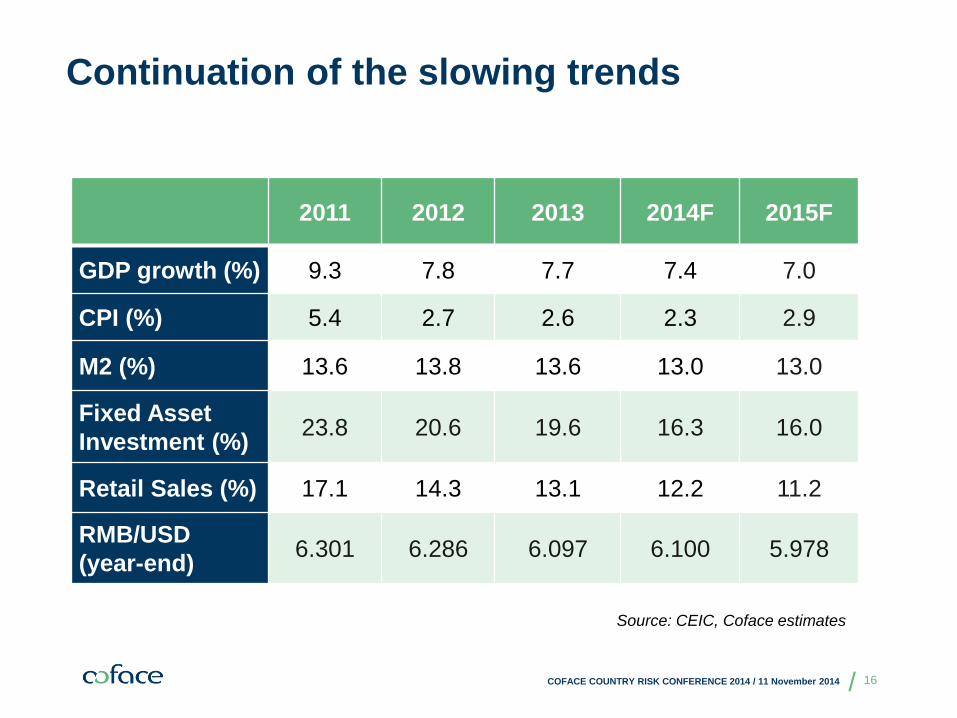

CPI ceiling @ 3.5%: A high-ceiling

Source: CEIC, Coface

On the other hand, lower inflation eases wage pressure on businesses

The lack of inflation is increasingly becoming a concern

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 19

-10%

-5%

0%

5%

10%

15%

20%

25%

CPI CPI (food) PPI6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Average Wage: Urban Non-private Real wage growth

/

New job creation @ 10 million/year:

Good for now, but…

You can’t have your cake and eat it too

Source: CEIC, Coface

Income growth continues its downward trend

Will the halt of new job creation growth be coming soon?

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 20

-1.0%

6.0%4.5% 3.7% 3.5%

1.7%

-10%

-5%

0%

5%

10%

15%

Urban new employment growth (YoY)

11.7m

11m

12.2m

11m

13.1m12.7m11.3%

14.1%

12.6%

9.7%

9.3%

0%

2%

4%

6%

8%

10%

12%

14%

16%

0

5,000

10,000

15,000

20,000

25,000

30,000

3/2010 9/2010 3/2011 9/2011 3/2012 9/2012 3/2013 9/2013 3/2014 9/2014

YTD disposable income per capita (LHS) YTD consumption expenditure (LHS)

Disposable income per capita growth Consumption expenditure growth

RMB/ Yr YoYRMB/ Yr YoY

/

Expected steps going forward

Growth stabilization

Managing expectation

Strengthening economic structure

Targeted stimuli

Lower growth target

Continuation of

structural reform

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 21

/

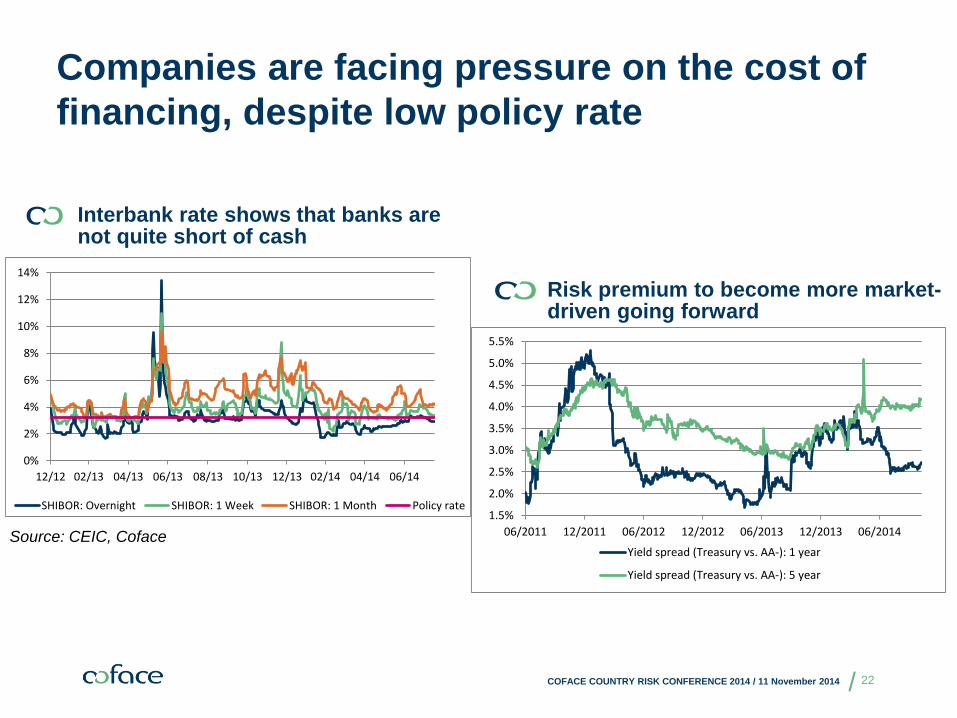

Companies are facing pressure on the cost of

financing, despite low policy rate

Source: CEIC, Coface

Risk premium to become more market-driven going forward

Interbank rate shows that banks are not quite short of cash

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 22

0%

2%

4%

6%

8%

10%

12%

14%

12/12 02/13 04/13 06/13 08/13 10/13 12/13 02/14 04/14 06/14

SHIBOR: Overnight SHIBOR: 1 Week SHIBOR: 1 Month Policy rate1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

06/2011 12/2011 06/2012 12/2012 06/2013 12/2013 06/2014

Yield spread (Treasury vs. AA-): 1 year

Yield spread (Treasury vs. AA-): 5 year

/

But expansion of monetary base is becoming

less effective as a tool

Source: CEIC, Coface estimates

Money supply growth is becoming less-efficient in boosting growth

Slowing non-bank financing activities dragged aggregate financing growth

Nominal GDP M0 M1 M2

1Yr lead 0.1109 0.3961 0.5847 0.3406

3Q-lead 0.3552 0.4965 0.6556 0.2301

2Q-lead 0.6068 0.5783 0.6074 0.0844

1Q-lead 0.8353 0.4529 0.4233 -0.1410

Simultaneous 1.0000 0.4811 0.1991 -0.2671

Nominal GDP/ Money Supply

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 23

-20%

-10%

0%

10%

20%

30%

40%

0

500

1,000

1,500

2,000

2,500

3,000

10/2012 1/2013 4/2013 7/2013 10/2013 1/2014 4/2014 7/2014

Aggregate financing New loan

YTD aggregate financing growth (RHS) YTD new loan growth (RHS)

RMB b YoY

95%

0%

50%

100%

150%

200%

250%

Nominal GDP growth / M1 growth (9M-lead)

Correlation (10-year) @ 0.6610-year average @ 105%

/

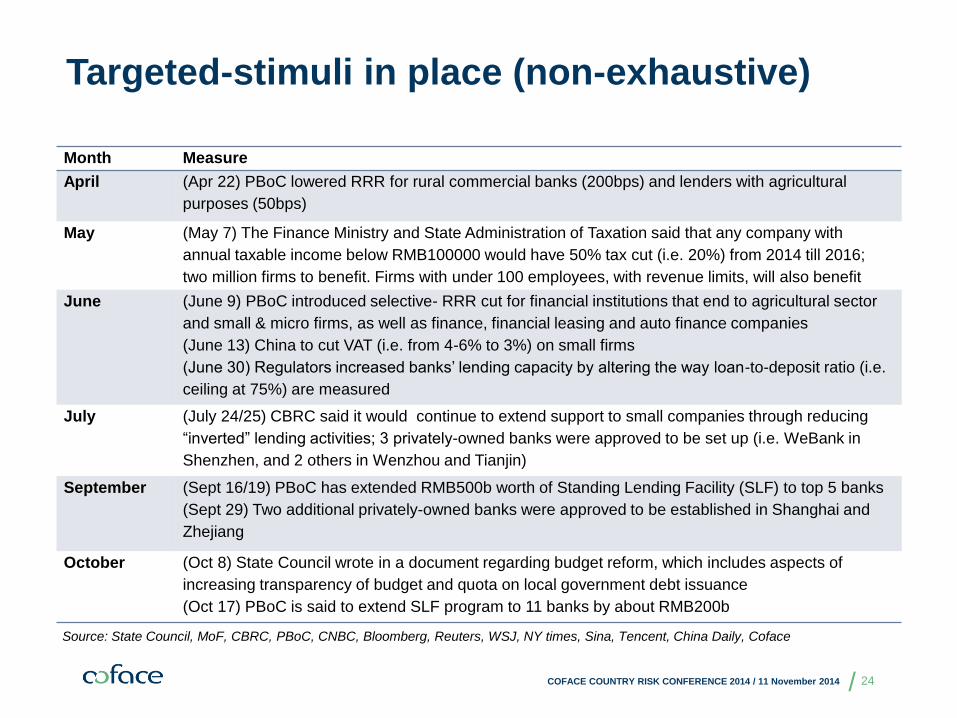

Month Measure

April (Apr 22) PBoC lowered RRR for rural commercial banks (200bps) and lenders with agricultural

purposes (50bps)

May (May 7) The Finance Ministry and State Administration of Taxation said that any company with

annual taxable income below RMB100000 would have 50% tax cut (i.e. 20%) from 2014 till 2016;

two million firms to benefit. Firms with under 100 employees, with revenue limits, will also benefit

June (June 9) PBoC introduced selective- RRR cut for financial institutions that end to agricultural sector

and small & micro firms, as well as finance, financial leasing and auto finance companies

(June 13) China to cut VAT (i.e. from 4-6% to 3%) on small firms

(June 30) Regulators increased banks’ lending capacity by altering the way loan-to-deposit ratio (i.e.

ceiling at 75%) are measured

July (July 24/25) CBRC said it would continue to extend support to small companies through reducing

“inverted” lending activities; 3 privately-owned banks were approved to be set up (i.e. WeBank in

Shenzhen, and 2 others in Wenzhou and Tianjin)

September (Sept 16/19) PBoC has extended RMB500b worth of Standing Lending Facility (SLF) to top 5 banks

(Sept 29) Two additional privately-owned banks were approved to be established in Shanghai and

Zhejiang

October (Oct 8) State Council wrote in a document regarding budget reform, which includes aspects of

increasing transparency of budget and quota on local government debt issuance

(Oct 17) PBoC is said to extend SLF program to 11 banks by about RMB200b

Targeted-stimuli in place (non-exhaustive)

Source: State Council, MoF, CBRC, PBoC, CNBC, Bloomberg, Reuters, WSJ, NY times, Sina, Tencent, China Daily, Coface

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 24

/

Content

Macroeconomic environment

Sectoral development

Property

Consumer goods

Steel

Conclusion

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 25

/

Sectoral Risk Assessment (non-exhaustive)

Source: Datastream data, Coface (September 2014)

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 26

/

Property

A key part of the Chinese government’s urbanization plan

An important source of government revenue

A huge downstream market for other sectors like steel and cement, and thus iron ore, coal and other commodities

Source: Coface

Why do we talk about it?

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 27

/

-15%

-10%

-5%

0%

5%

10%

15%

88

90

92

94

96

98

100

102

104

106

108

Real estate climate index RECI YoY change

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

0%

10%

20%

30%

40%

50%

Other sources (RHS) Self-raised (RHS)

Foreign investment (RHS) Domestic loan (RHS)

Real estate investment source of fund

YoY RMB m

-9.1%

+11.5%

+11.8%

Lack of alternate source of financing hurts

business climate of property sector…

Source: CEIC, Coface

Deteriorated environment for the property market in 2014

*Source of fund, area of land development, area of

building construction, sale price, floor space for sale, etc

Property developers faced difficulty in obtaining financing-facilities from “other sources”

GDP slowed for 6

consecutive quarters;

withdrawal syndrome;

curbing property

sales

GFC Worries of

overdevelopment;

lack of “other”

financing sources

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 28

/

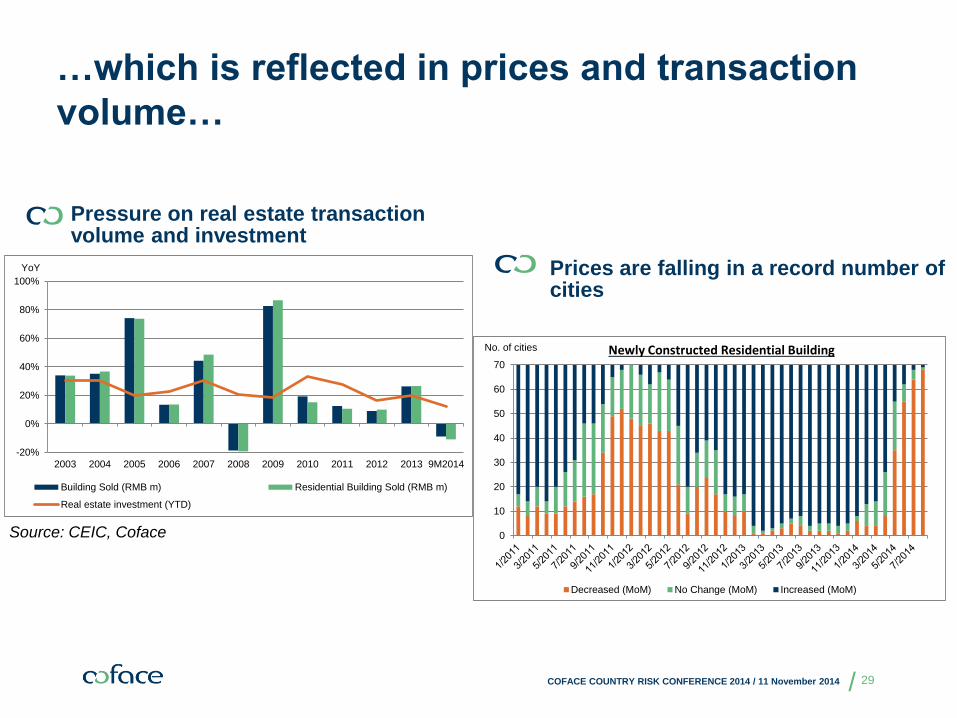

…which is reflected in prices and transaction

volume…

Pressure on real estate transaction volume and investment

Source: CEIC, Coface

Prices are falling in a record number of cities

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 29

0

10

20

30

40

50

60

70

Decreased (MoM) No Change (MoM) Increased (MoM)

No. of cities Newly Constructed Residential Building

-20%

0%

20%

40%

60%

80%

100%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 9M2014

Building Sold (RMB m) Residential Building Sold (RMB m)

Real estate investment (YTD)

YoY

/

…but the property market is too important to

see no support…

And land sales represent a key role in government financing

Property market takes a key position in banks’ portfolio

Source: CEIC, Coface

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 30

18.9%

19.4%

19.9%

20.4%

20.9%

21.4%

0%

20%

40%

60%

80%

100%

3Q10 1Q11 3Q11 1Q12 3Q12 1Q13 3Q13 1Q14

Individual Housing Mortgage/Real Estate Loan

Real Estate Development Loan/Real Estate Loan

Real Estate Loan/Total RMB Loan (RHS)6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

0%

5%

10%

15%

20%

25%

30%

35%

2009 2010 2011 2012 2013

Government revenue (RHS)

Debt issuance / Govt revenue

Income from land usage right transfer/ Govt revenue

RMB m

/

Consumer goods

Designed to be the new growth driver for the economy

Benefited from rising income and new sales channels

Hurt by anti-corruption scheme

Source: Coface

Why do we talk about it?

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 31

/

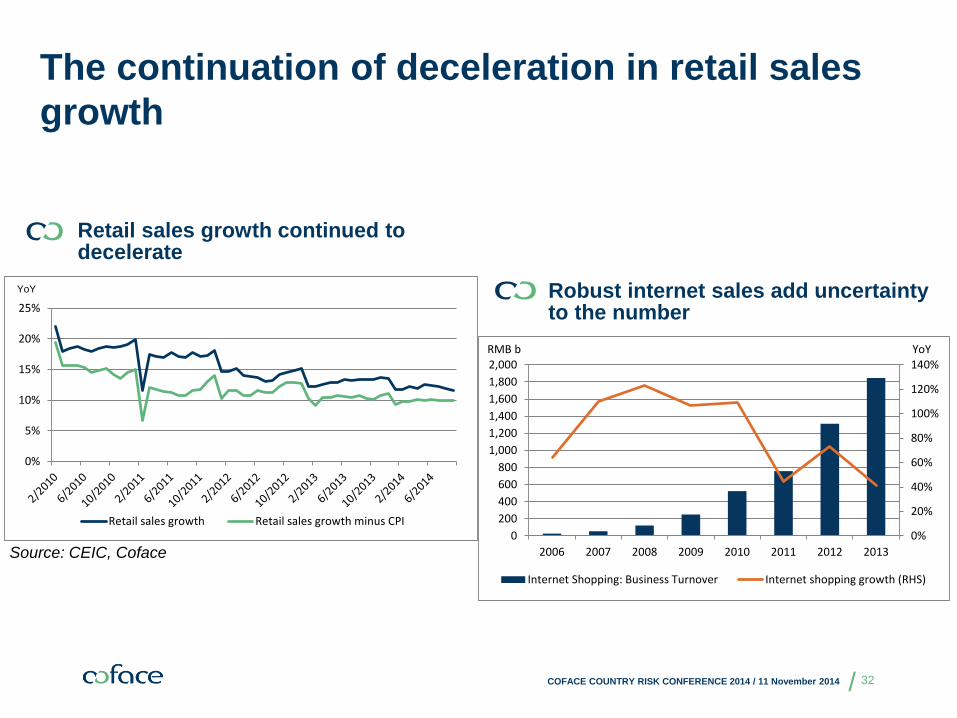

The continuation of deceleration in retail sales

growth

Source: CEIC, Coface

Retail sales growth continued to decelerate

Robust internet sales add uncertainty to the number

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 32

0%

20%

40%

60%

80%

100%

120%

140%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2006 2007 2008 2009 2010 2011 2012 2013

Internet Shopping: Business Turnover Internet shopping growth (RHS)

RMB b YoY

0%

5%

10%

15%

20%

25%

Retail sales growth Retail sales growth minus CPI

YoY

/

Consumptions hurt via anti-corruption regime

But liquor and other luxury goods are hurt extensively by the anti-corruption scheme

Demand for necessity items continue to benefit from income growth

Source: CEIC, Coface

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

社會消費品零售總額(200家最大零售企業):食品

社會消費品零售總額(200家最大零售企業):飲料

社會消費品零售總額(200家最大零售企業):生活用品

同比增長

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

社會消費品零售總額(200家最大的零售企業):白酒

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 33

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Retail sales of 200 largest retail enterprise: food

Retail sales of 200 largest retail enterprise: beverage

Retail sales of 200 largest retail enterprise: articles for daily use

YoY

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Retail sales of 200 largest retail enterprise: liquor

/

Other barriers of a breakthrough in retail

sales

Widening gap between urban and rural households may be a barrier

Consumers are less-eager to spend with positive interest rate

Source: CEIC, Coface estimates

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 34

0

5,000

10,000

15,000

20,000

0%

5%

10%

15%

20%

25%

Difference between urban and rural per capita income (RHS)

Cash income per capita for rural household

Disposable income per capita for urban households

YoY RMB

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

Saving deposit rate minus CPI 1-year time-deposit rate minus CPI

/

Steel

A barometer for the other sectors in China (property, construction, shipping, automobile, electronics, etc.)

A traditionally important industry that is facing tremendous pressure – provides indication of government policy direction

Arguably a price-setter for the regional market

Source: Coface

Why do we talk about it?

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 35

/

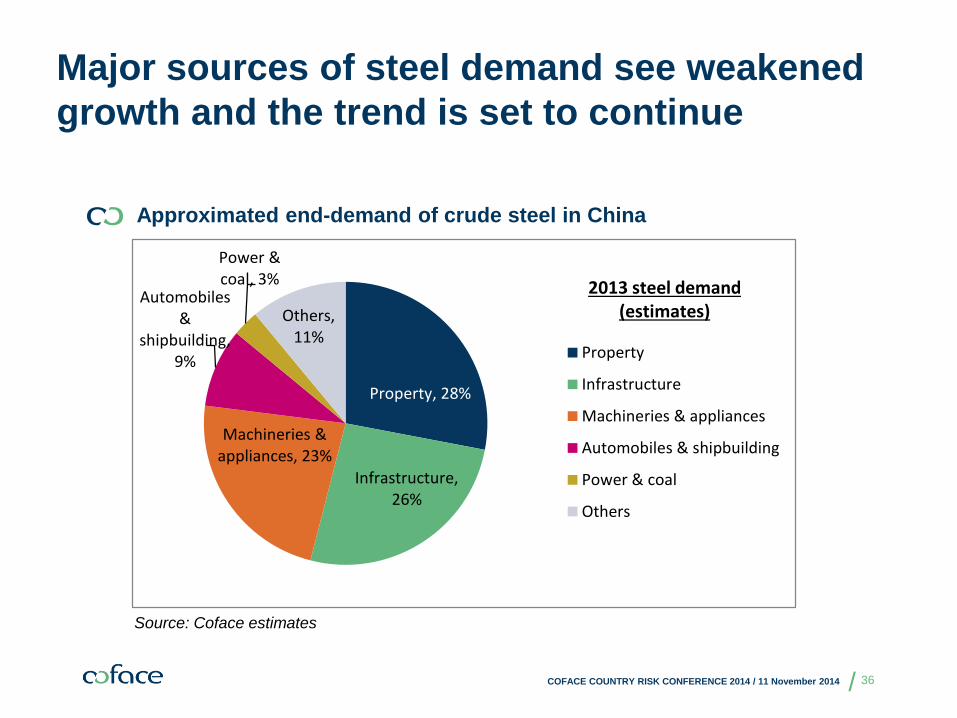

Major sources of steel demand see weakened

growth and the trend is set to continue

Approximated end-demand of crude steel in China

Source: Coface estimates

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 36

Property, 28%

Infrastructure, 26%

Machineries & appliances, 23%

Automobiles &

shipbuilding, 9%

Power & coal, 3%

Others, 11%

Property

Infrastructure

Machineries & appliances

Automobiles & shipbuilding

Power & coal

Others

2013 steel demand (estimates)

/

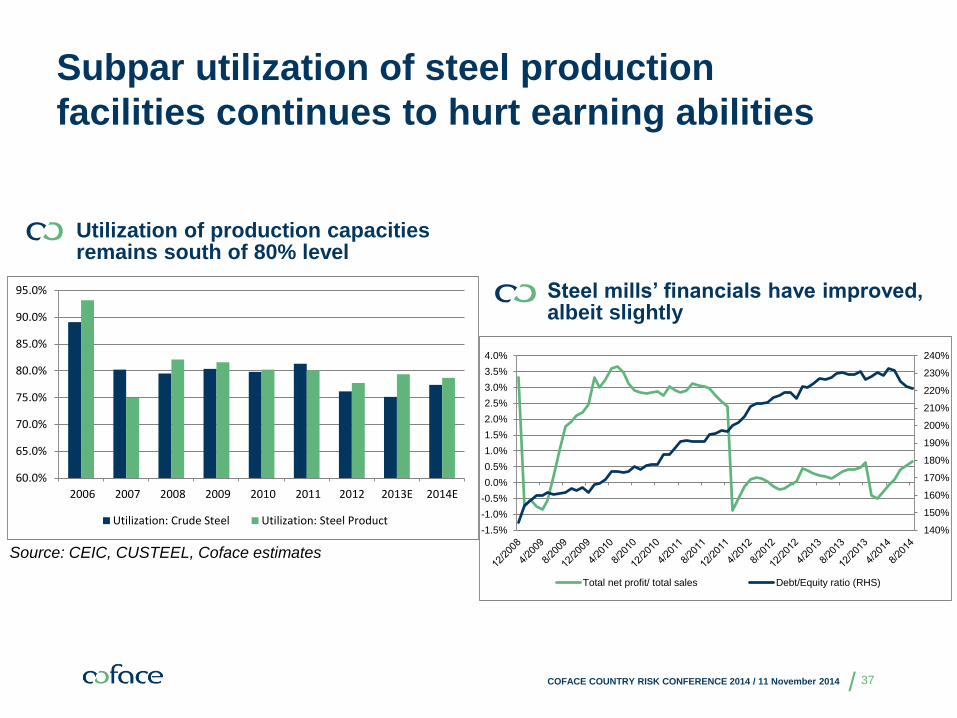

Subpar utilization of steel production

facilities continues to hurt earning abilities

Steel mills’ financials have improved, albeit slightly

Utilization of production capacities remains south of 80% level

Source: CEIC, CUSTEEL, Coface estimates

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 37

140%

150%

160%

170%

180%

190%

200%

210%

220%

230%

240%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Total net profit/ total sales Debt/Equity ratio (RHS)

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%

95.0%

2006 2007 2008 2009 2010 2011 2012 2013E 2014E

Utilization: Crude Steel Utilization: Steel Product

/

Crude steel = Coke (from coking coal) + iron ore

+ scrap steel

Already depressed coal prices have limited downside unless we will see a collapse of the industry

High iron ore inventory is depressing prices

Source: CEIC, Coface

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 38

0

20,000

40,000

60,000

80,000

100,000

120,000

Iron ore inventory at Ports

'000 tons

3,500

4,000

4,500

5,000

5,500

6,000

6,500

7,000

7,500

8,000

8,500

360

410

460

510

560

610

660

710

01/13 03/13 05/13 07/13 09/13 11/13 01/14 03/14 05/14 07/14 09/14

Coal Inventory: Port: Qinhuangdao 5800 Calorie: Datong High-quality

5500 Calorie: Shanxi High-quality 5000 Calorie: Shanxi Common

4500 Calorie: Common

RMB/t k tons

/

Content

Macroeconomic environment

Sectoral development

Property

Consumer goods

Steel

Conclusion

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 39

/

Companies concern most on Chinese economic slowdown and tightening monetary policy and

access to credit.

Coface’s Payment Survey :

Most Concerning Factors in 2014

61.2%

16.3%

25.6%

50.0%

8.8% 3.3%

0%

20%

40%

60%

80%

Chinese economicslowdown

global economicslowdown

rising labour costs tightening monetarypolicy and access to

credit

RMB appreciation others

Most concerning factors in 2014

Multiple answers

Source: Coface (February)

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 40

/

Expectation of near-term development

Policy stance

• Reform to continue at a managed pace

• Continuation of targeted-stimulus approach as a stabilizer for growth

• Growth target to moderate in 2015

Liquidity

• More active open market operations to manage liquidity

• Stricter regulations on shadow-banking facilitators

• Further assistance extended to SMEs and micro firms

Property market

• Demand to stay at low level

• Price pressure remains as inventory awaits to be digested

• Less-strict policy stance expected to be used as a “stimulus” for the market, but effectiveness is unclear

Retail sales

• Slower demand growth for necessity items with moderated income growth

• Anti-corruption scheme to have lesser effect on consumption as a result of base-effect

• Rising competition for sales outlets with bricks and mortar

Steel

• Accelerated dismantling of outdated production capacity

• Medium-sized steel mills to face liquidity pressure

• Profitability to remain at depressed level

• Low value-added traders to be out of business

Source: Coface

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 41

/

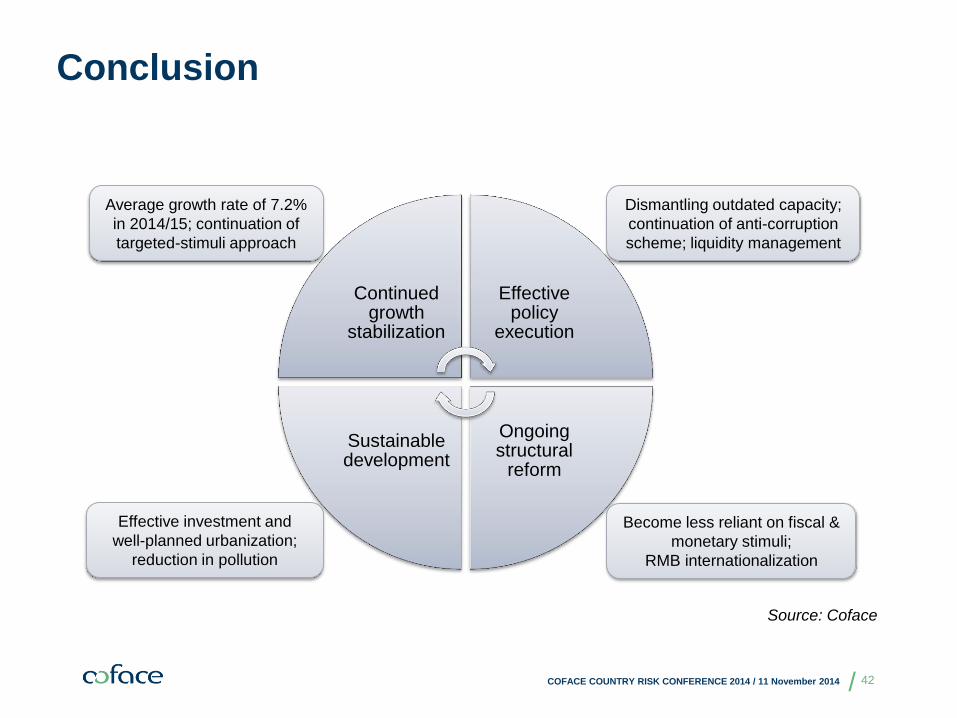

Conclusion

Continued growth

stabilization

Effective policy

execution

Ongoing structural

reform

Sustainable development

Source: Coface

Average growth rate of 7.2%

in 2014/15; continuation of

targeted-stimuli approach

Effective investment and

well-planned urbanization;

reduction in pollution

Dismantling outdated capacity;

continuation of anti-corruption

scheme; liquidity management

Become less reliant on fiscal &

monetary stimuli;

RMB internationalization

COFACE COUNTRY RISK CONFERENCE 2014 / 11 November 2014 42