Embed Size (px)

Citation preview

2015 Annual Governmental GAAP Update Government Finance Officers Association

November 5, 2015 & December 3, 2015

1

Program Overview

2

Fair Value Measurement and Application (GASB 72) • Definition of fair value

• Measuring fair value

• Application to investments

• Disclosure

• Fair value vs. acquisition value

3

Postemployment benefits

• Pensions not administered through trusts (GASB 73)

• Technical amendments for plans and employers (GASB 73)

• Other postemployment benefits – OPEB (GASB 74 & 75)

• Employer implementation (GASB 68 & 71)

• Journal entries for first year

• Allocation to proprietary and fiduciary funds

• Covered payroll vs. covered-employee payroll

• Audit impact

• Funding impact

• Explaining the change

4

Other new standards

• The Hierarchy of Generally Accepted Accounting Principles for State and Local Governments (GASB 76)

• Tax Abatement Disclosures (GASB 77)

5

Recent exposure drafts

• Accounting and Financial Reporting for Certain External Investment Pools (June 2015)

• Blending Requirements for Certain Component Units (June 2015)

• Accounting and Financial Reporting for Irrevocable Split-Interest Agreements (June 2015)

• Accounting and Financial Reporting for Pensions Provided through Certain Multiple-Employer Defined Benefit Pension Plans (October 2015)

6

Forthcoming exposure drafts

• Financial Reporting for Fiduciary Responsibilities – 4Q15

• Asset Retirement Obligations – 4Q15

• Leases – 1Q16

7

Other topics

• GASB Technical Plan

• Reexamination of the Financial Reporting Model

• Reporting deficiencies

8

Fair Value Measurement and Application GASB 72 (issued February 2015)

9

Background and content

• Motivation

• Private-sector changes and international changes

• Disclosure concerns raised by 2008/2009 credit crisis

• Alignment with GASB Concepts Statement No. 6, Measurement of Elements of Financial Statements

• Only affects items now reported at fair value

• Liabilities = certain amounts related to derivatives

10

Definition of fair value

• The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date

• Market transactions

• Perspective of one selling an asset (transferring a liability) vs. buying an asset (assuming a liability)

• Exit price vs. entry price

11

Market transactions (1/4)

• Issues

• Sale can take place in a variety of circumstances

• Factors specific to a government could affect price

• Resolution

• Fair value based on real or potential market transactions

• Fair value unaffected by factors irrelevant to market participants

• Circumstances characteristic of the seller rather than of the asset being sold

12

Market transactions (2/4)

• Multiple markets?

• Principal market

• Most advantageous market (in absence of a principal market)

• Transaction costs relevant?

• Determination of most advantageous market - Yes

• Amount reported - No

• Transportation costs ≠ transaction cost

• Relevant if location is a characteristic of the asset (commodities)

13

Market transactions (3/4)

• Nonfinancial assets?

• Starting point for assessment = government’s current use

• Highest and best use considering what is:

• Physically possible (e.g., size and location of property)

• Legally permissible (e.g., current zoning rules)

• Financially feasible for potential buyers

14

Market transactions (4/4)

• Liabilities

• Amount to transfer the obligation to a third party

• Not the amount to settle with the counterparty

• Normally = fair value of corresponding asset

15

Measuring fair value (1/3)

• Three acceptable techniques

• Market approach

• Actual market transactions for identical or similar items

• Cost approach

• Current cost to replace the service capacity of an asset

• Takes into account obsolescence and physical deterioration

• Income approach

• Discounted future cash flows

• All three require inputs

16

Measuring fair value (2/3)

• Types of inputs

• Observable

• Independently verifiable

• Unobservable

• Example: amount based on internally generated data

• Goal

• Maximize use of observable inputs

• Minimize use of unobservable inputs

17

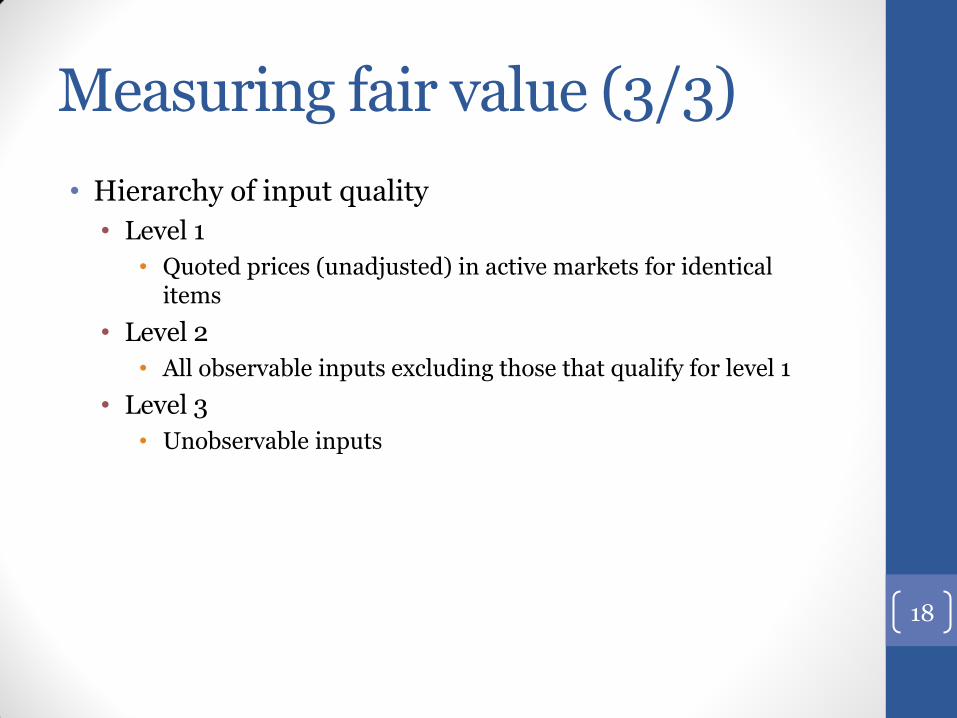

Measuring fair value (3/3)

• Hierarchy of input quality

• Level 1

• Quoted prices (unadjusted) in active markets for identical items

• Level 2

• All observable inputs excluding those that qualify for level 1

• Level 3

• Unobservable inputs

18

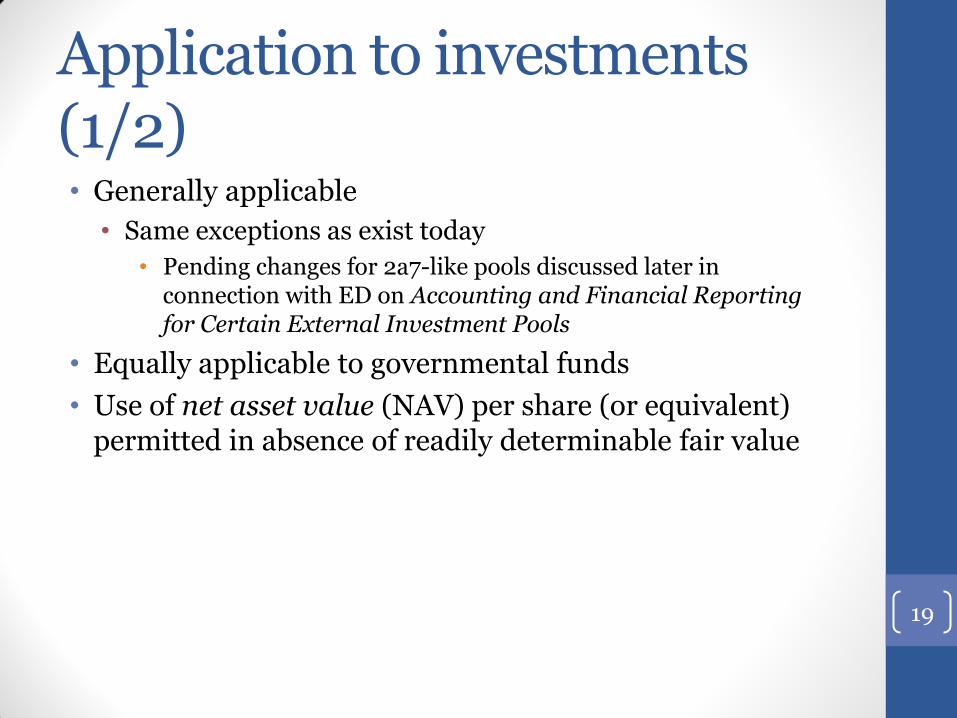

Application to investments (1/2) • Generally applicable

• Same exceptions as exist today

• Pending changes for 2a7-like pools discussed later in connection with ED on Accounting and Financial Reporting for Certain External Investment Pools

• Equally applicable to governmental funds

• Use of net asset value (NAV) per share (or equivalent) permitted in absence of readily determinable fair value

19

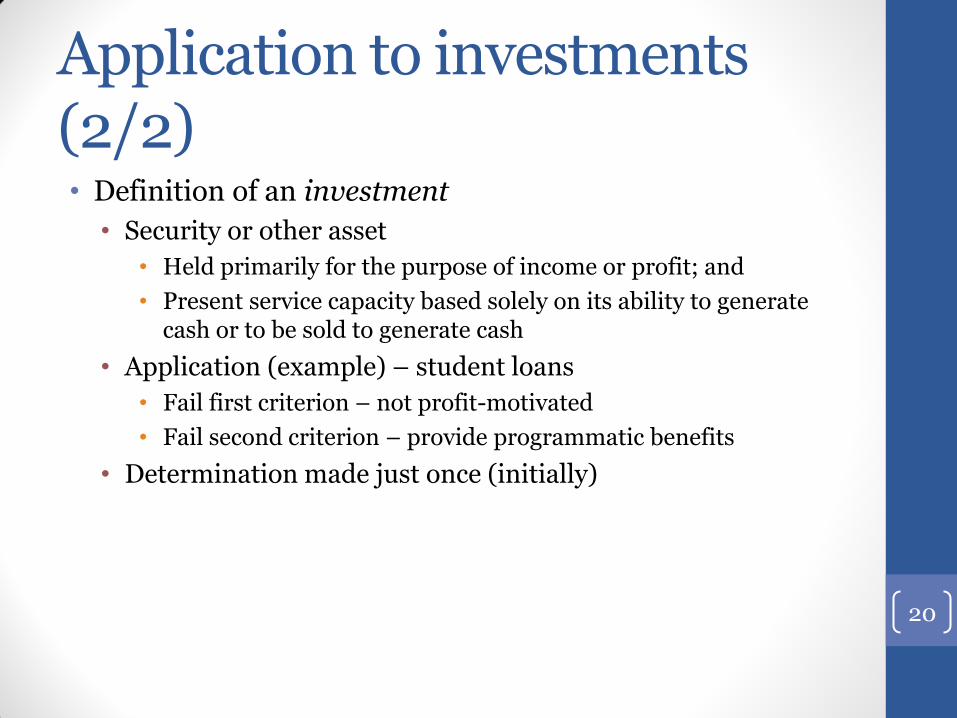

Application to investments (2/2) • Definition of an investment

• Security or other asset

• Held primarily for the purpose of income or profit; and

• Present service capacity based solely on its ability to generate cash or to be sold to generate cash

• Application (example) – student loans

• Fail first criterion – not profit-motivated

• Fail second criterion – provide programmatic benefits

• Determination made just once (initially)

20

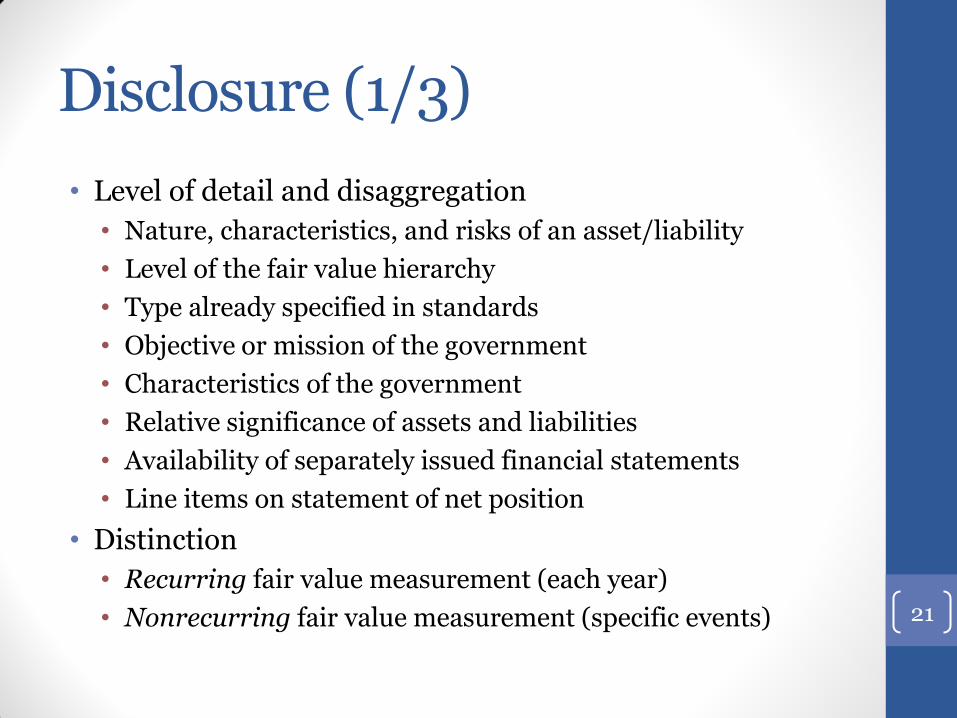

Disclosure (1/3)

• Level of detail and disaggregation

• Nature, characteristics, and risks of an asset/liability

• Level of the fair value hierarchy

• Type already specified in standards

• Objective or mission of the government

• Characteristics of the government

• Relative significance of assets and liabilities

• Availability of separately issued financial statements

• Line items on statement of net position

• Distinction

• Recurring fair value measurement (each year)

• Nonrecurring fair value measurement (specific events) 21

Disclosure (2/3)

• For both recurring and nonrecurring measurement items

• Fair value as of reporting date

• Level of inputs used (unless NAV per share)

• Valuation techniques

• Change in valuation techniques with significant impact and reason for change

• For nonrecurring measurement items

• Reason for measurement

22

Disclosure (3/3)

• Additional disclosure for NAV per share if:

• NAV per share calculated

• Fair value not readily determinable

• Measured at fair value during the period

• Disclosure objectives

• Nature and risks of the investments

• Whether sale at a different amount is probable

23

Fair value vs. acquisition value

• Term fair value previously sometimes used to describe entry (buy) price

• Donated capital assets and similar items (donated works of art and historical treasures)

• Capital assets generated in connection with service concession arrangements

• Terminology change

• Now acquisition value

24

Question 1

Fair value should be based on

A. Exit price

B. Entry price

C. Normally A but sometimes B

25

Question 2

Transaction costs are

A. Relevant to determining fair value

B. Relevant to determining a government’s most advantageous market for purposes of determining fair value

C. Both A and B

D. Neither A nor B

26

Question 3

A city owns a building that originally was constructed as a school, but which it currently uses as a warehouse. What should the city’s starting point be for assessing the building’ s fair value?

A. Use as a school building

B. Use as a warehouse

C. Either A or B

D. Lower of A or B

27

Question 4

The fair value of a liability should be determined based on

A. The amount necessary to pay off the liability (settlement amount)

B. The amount necessary for a third-party to assume the liability

C. Either A or B

D. Higher of A or B

28

Question 5

Unobservable inputs may properly be classified as

A. Level 2 inputs

B. Level 3 inputs

C. Both A and B

29

Question 6

Which of the following would qualify as investments?

A. Timber rights associated with park lands

B. Securities held as deposits for contractors

C. Student loans

D. All the above

E. None of the above

30

Question 7

Which of the following statements is true regarding the valuation of donated capital assets?

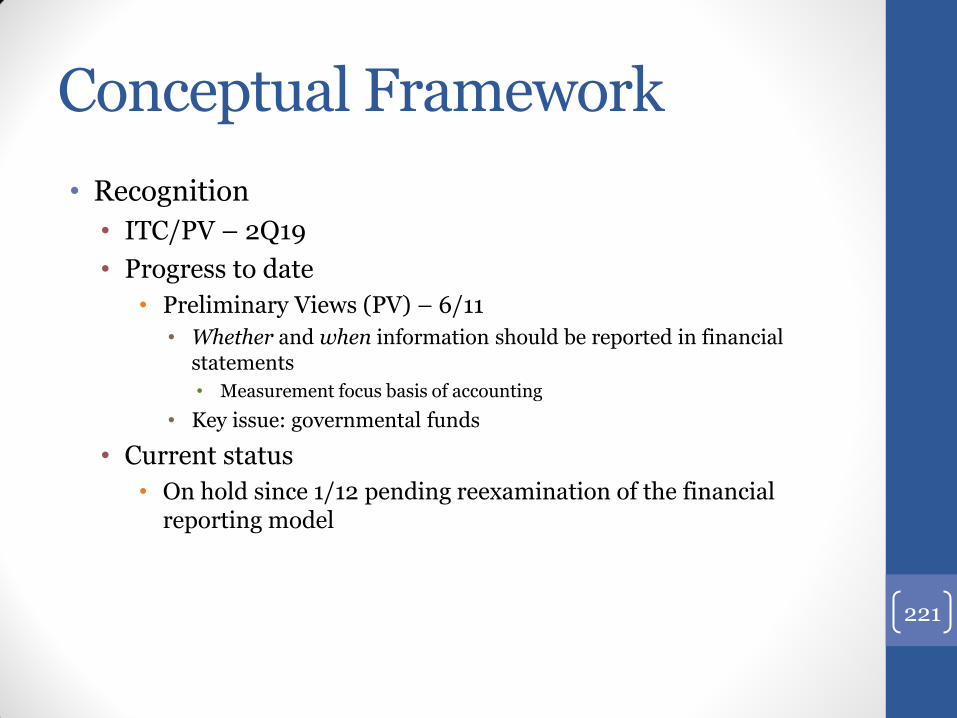

A. They should be reported at fair value, defined as an entry price for this purpose

B. They should be reported at fair value, defined as an exit price for this purpose

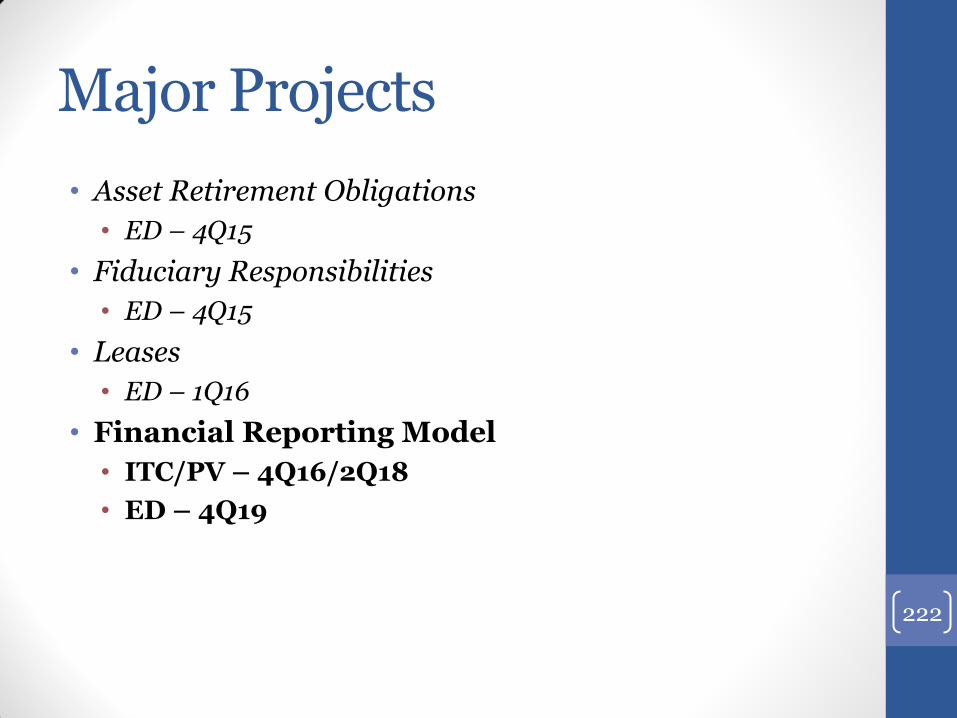

C. They should be reported at an amount equal to A, but not described as fair value

31

Postemployment benefits Pension issues for employers (GASB 68, 71, 73)

OPEB (GASB 74-75)

32

PENSIONS NOT ADMINISTERED THROUGH TRUSTS (GASB 73)

Part 1

33

Scope of GASB pension standards • Plans administered through trusts or equivalent

arrangements

• Contributions are irrevocable

• Assets may be used only to provide pensions to plan members in accordance with plan terms

• Legally protected from creditors

34

Overview

• Analysis

• Pension arrangements not administered through a trust or equivalent arrangement

• Same objectives as other pension arrangements

• Only difference = no fiduciary net position (FNP)

• Conclusion

• Apply the provisions of GASB 67 and GASB 68 accordingly

• No netting of related assets against employer liability

• Total pension liability vs. net pension liability

• Use discount rate for an unfunded liability

• High-grade municipal rate

35

Treatment of assets

• Employers

• Single-employer plan

• Report as employer assets

• Multiple-employer plan

• Report employer’s proportionate share of accumulated resources as employer assets

• Plans

• Report in an agency fund (like OPEB)

36

TECHNICAL AMENDMENTS FOR PLANS AND EMPLOYERS (GASB 73)

Part 2

37

Three changes

1. Notes to schedules of required supplementary information (RSI)

2. Payables to defined benefit (DB) pension plans

3. Revenue recognition for support of nonemployer contributing entities not in a special funding situation

38

1. Notes to schedules of RSI

• Original requirement

• Information about investment-related factors that significantly affect trends in the amounts reported

• Clarifying amendment

• Limited to those factors over which the pension plan or participating governments have influence

• Changes in investment policies? Yes

• Changes in market prices? No

39

2. Payables to DB pension plans (1/2) • Separately financed specific liability

• Examples

• An increase in the total pension liability due to an individual employer joining a pension plan

• An increase in the total pension liability due to a change of benefit terms specific to an individual employer

• A contractual commitment for a nonemployer contributing entity to make a one-time contribution for purposes of reducing the net pension liability

• Not obligations associated with pooled obligation

• Even if separate payment terms

40

Payables to DB pension plans (2/2) • Amendments

• Defines separately financed specific liability

• A specific contractual liability to a DB pension plan for a one-time assessment to an individual employer or nonemployer contributing entity

• Clarifies exclusion of payables for unpaid (legal, contractual, or statutory) financing obligations associated with the pooled portion of the total pension liability (even if separate payment terms)

• Provides revenue recognition guidance

41

3. Revenue – support other than special funding situation • Clarifying amendment

• Recognize revenue in the reporting period in which the contribution of the nonemployer contributing entity is reported as a change in the net pension liability (or collective net pension liability)

42

Effective date

• Plans not administered through trusts

• Fiscal year ending 6/30/17

• Amendments to GASB 67 and GASB 68

• Fiscal year ending 6/30/16

• Earlier application encouraged in both cases

43

OTHER POSTEMPLOYMENT BENEFITS – OPEB (GASB 74 & GASB 75)

Part 3

44

Background

• Economic substance of OPEB

• Employee compensation paid in a later period

• Substantively equivalent to pensions

• Treatment until now

• Parallel treatment for pensions and OPEB

• Compromised by new pension guidance

• New GASB OPEB standards

• Restore parallel treatment

45

Fundamental OPEB changes

• Employer liability

• Net employer liability vs. unfunded contributions

• Employer expense

• Recognition divorced from funding

• Cost-sharing plans

• Employer’s proportionate share of total liability and expense

46

Other observations (1/2)

• Incorporates guidance on pensions not administered through a trust

• Retains requirement to consider an implicit rate subsidy as OPEB

• Preserves alternative measurement method for small employers and plans

47

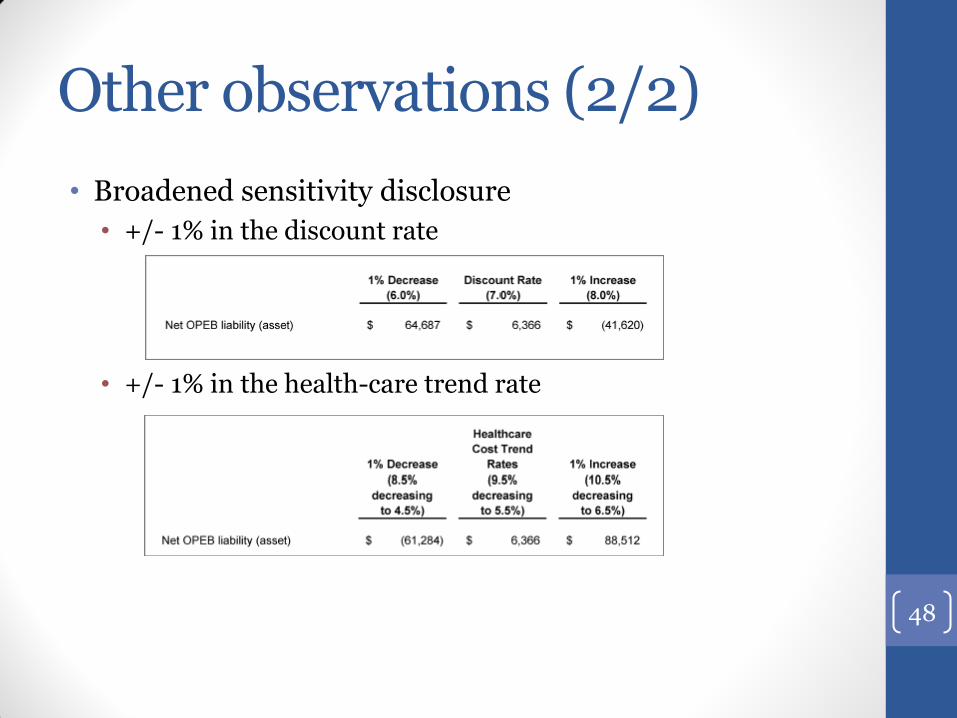

Other observations (2/2)

• Broadened sensitivity disclosure

• +/- 1% in the discount rate

• +/- 1% in the health-care trend rate

48

Effective date

• Plans

• Fiscal year ending 6/30/17

• Employers

• Fiscal year ending 6/30/18

49

SAMPLE EMPLOYER JOURNAL ENTRIES (GASB 68 & GASB 71)

Employer implementation

Part 4

50

Background

• The City sponsors a single defined benefit pension plan

• City fiscal year end = 9/30

• Plan fiscal year end = 6/30

• GASB 67 requires the plan to perform a valuation as of the plan’s fiscal year end

• Because the plan performs an annual valuation, the simplest approach is to also use the valuation date as the measurement date

• The plan has elected not to record initial deferred outflows and deferred inflows of resources

51

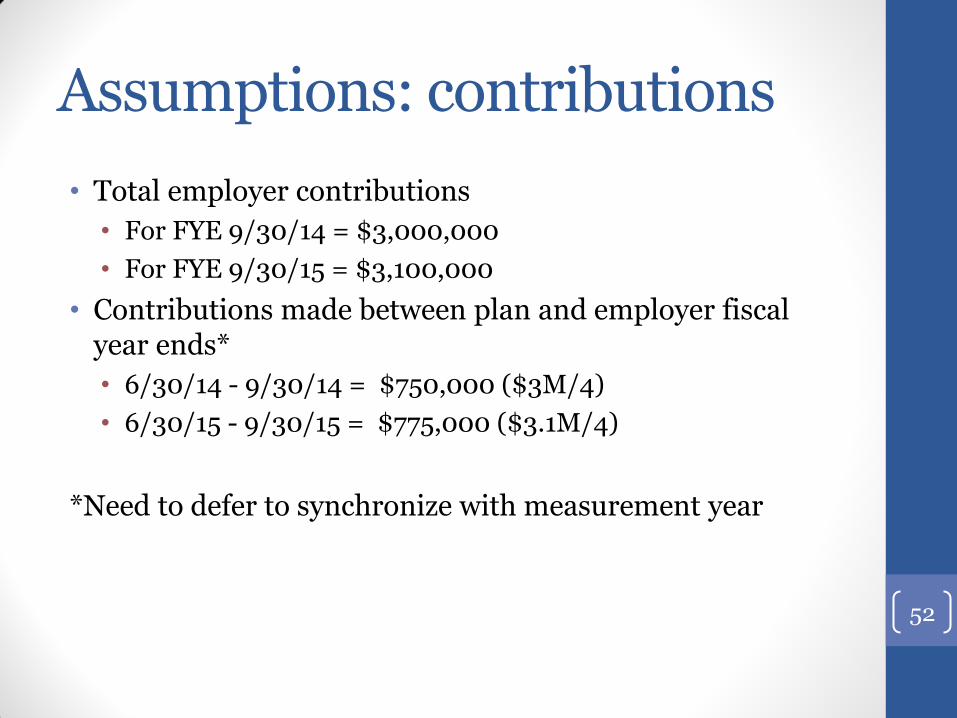

Assumptions: contributions

• Total employer contributions

• For FYE 9/30/14 = $3,000,000

• For FYE 9/30/15 = $3,100,000

• Contributions made between plan and employer fiscal year ends*

• 6/30/14 - 9/30/14 = $750,000 ($3M/4)

• 6/30/15 - 9/30/15 = $775,000 ($3.1M/4)

*Need to defer to synchronize with measurement year

52

Assumptions: change in plan terms • Measurement year ending 6/30/15

• Loss due to change in plan terms = $600,000

• Immediate recognition required

53

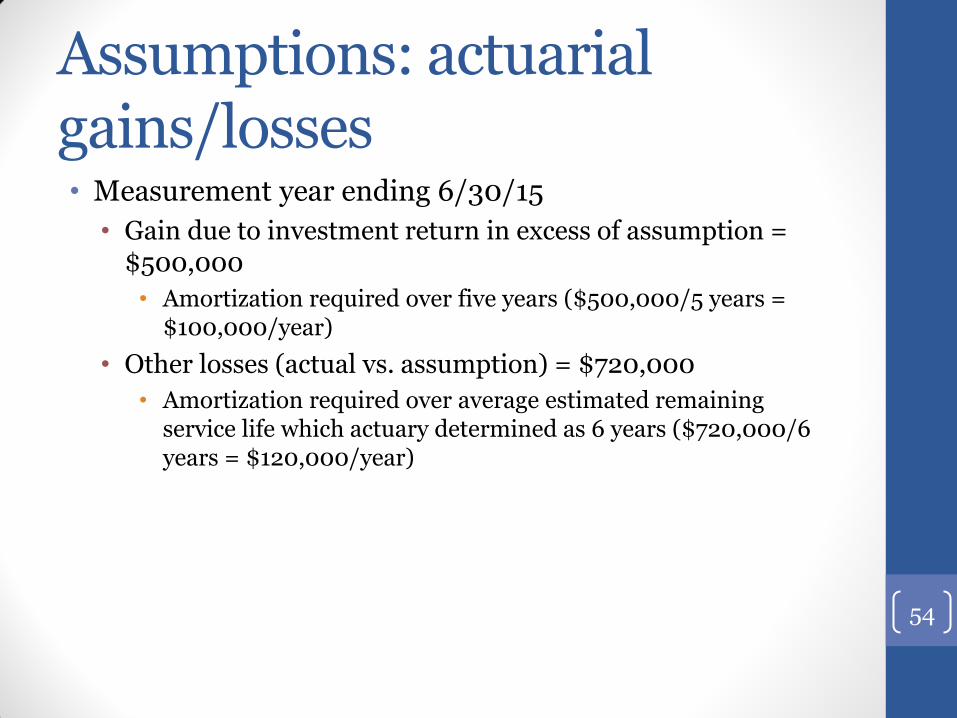

Assumptions: actuarial gains/losses • Measurement year ending 6/30/15

• Gain due to investment return in excess of assumption = $500,000

• Amortization required over five years ($500,000/5 years = $100,000/year)

• Other losses (actual vs. assumption) = $720,000

• Amortization required over average estimated remaining service life which actuary determined as 6 years ($720,000/6 years = $120,000/year)

54

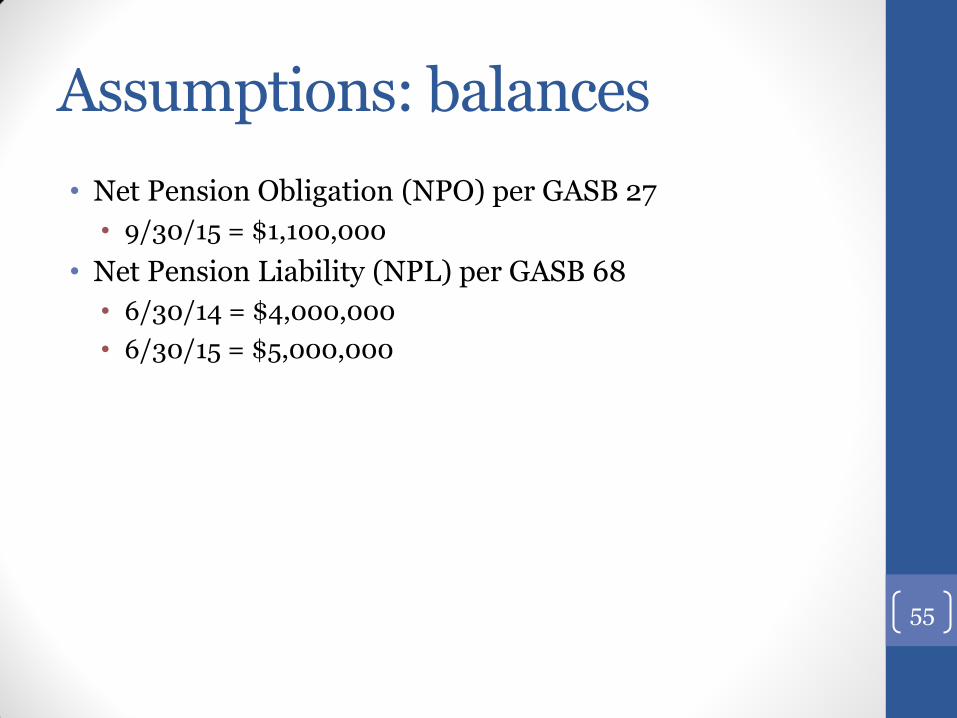

Assumptions: balances

• Net Pension Obligation (NPO) per GASB 27

• 9/30/15 = $1,100,000

• Net Pension Liability (NPL) per GASB 68

• 6/30/14 = $4,000,000

• 6/30/15 = $5,000,000

55

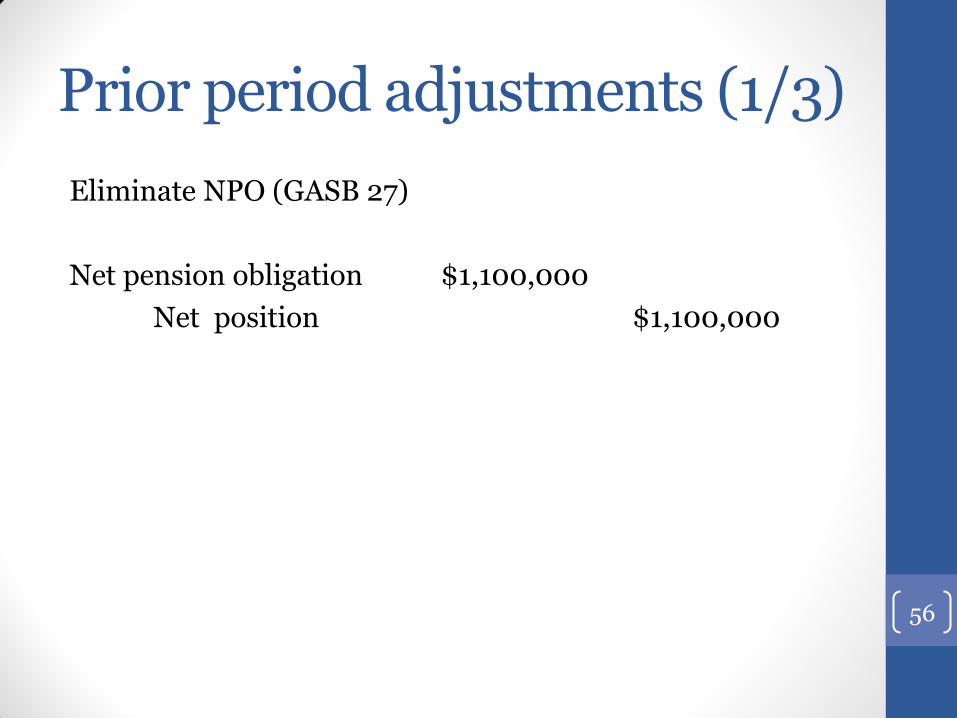

Prior period adjustments (1/3)

Eliminate NPO (GASB 27)

Net pension obligation $1,100,000

Net position $1,100,000

56

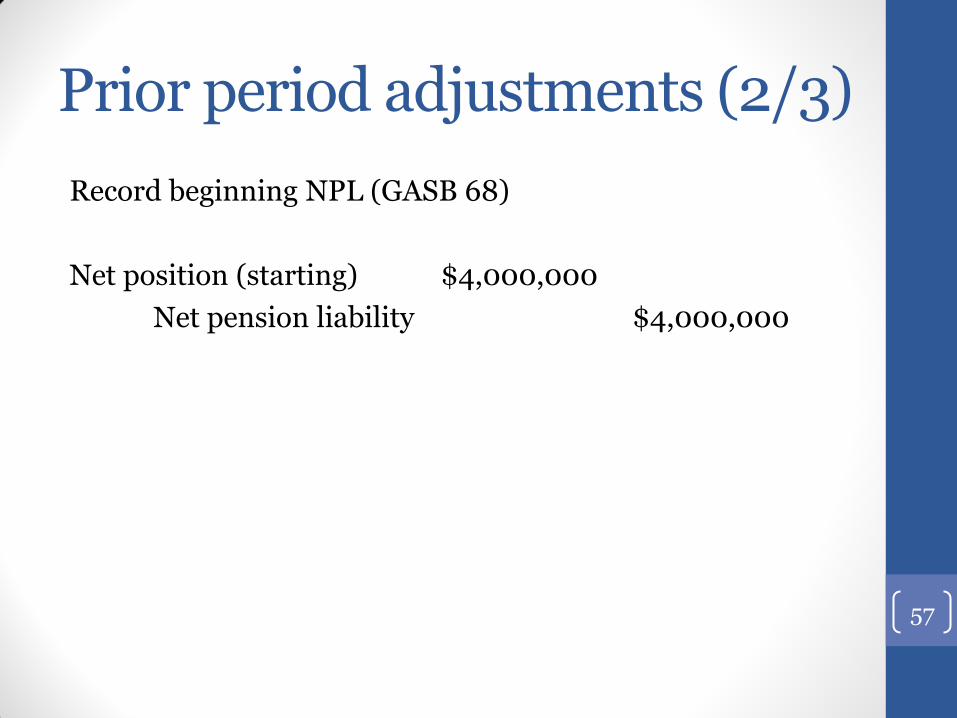

Prior period adjustments (2/3)

Record beginning NPL (GASB 68)

Net position (starting) $4,000,000

Net pension liability $4,000,000

57

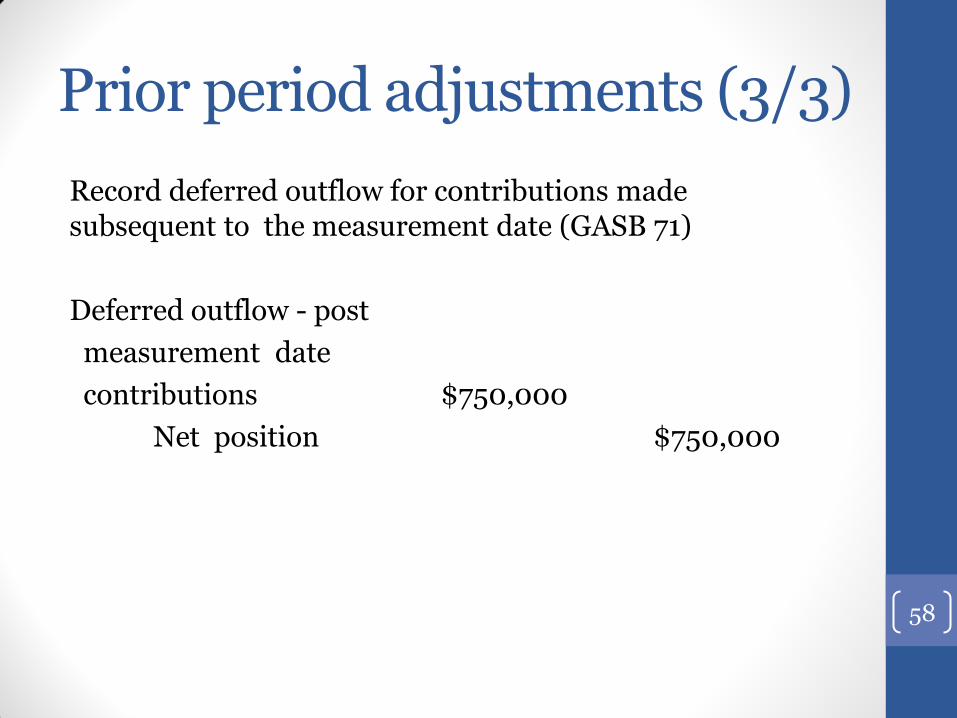

Prior period adjustments (3/3)

Record deferred outflow for contributions made subsequent to the measurement date (GASB 71)

Deferred outflow - post

measurement date

contributions $750,000

Net position $750,000

58

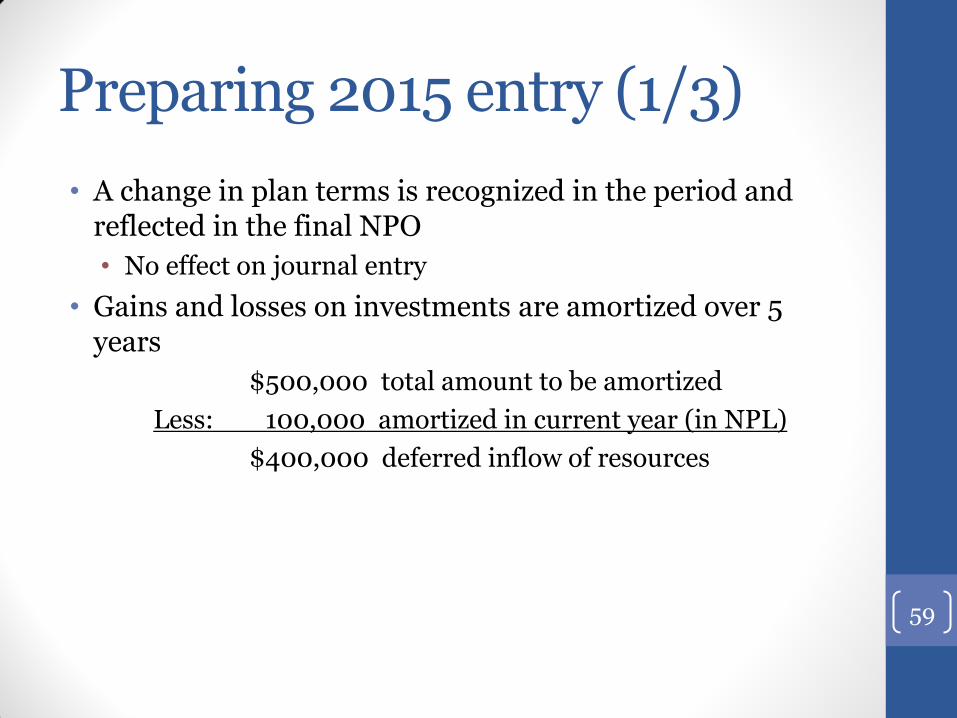

Preparing 2015 entry (1/3)

• A change in plan terms is recognized in the period and reflected in the final NPO

• No effect on journal entry

• Gains and losses on investments are amortized over 5 years

$500,000 total amount to be amortized

Less: 100,000 amortized in current year (in NPL)

$400,000 deferred inflow of resources

59

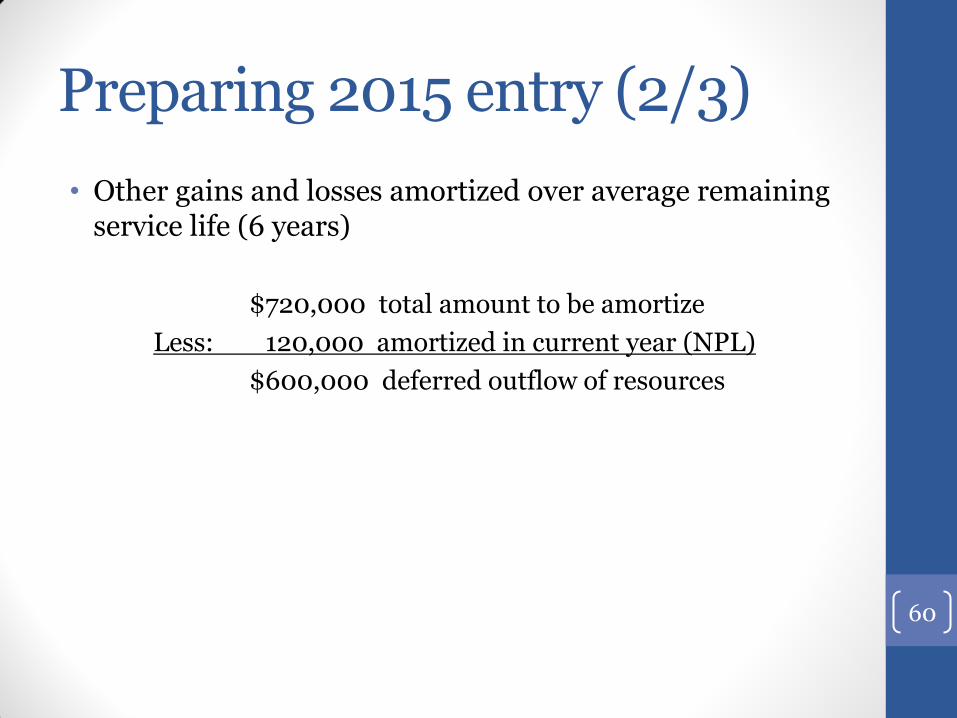

Preparing 2015 entry (2/3)

• Other gains and losses amortized over average remaining service life (6 years)

$720,000 total amount to be amortize

Less: 120,000 amortized in current year (NPL)

$600,000 deferred outflow of resources

60

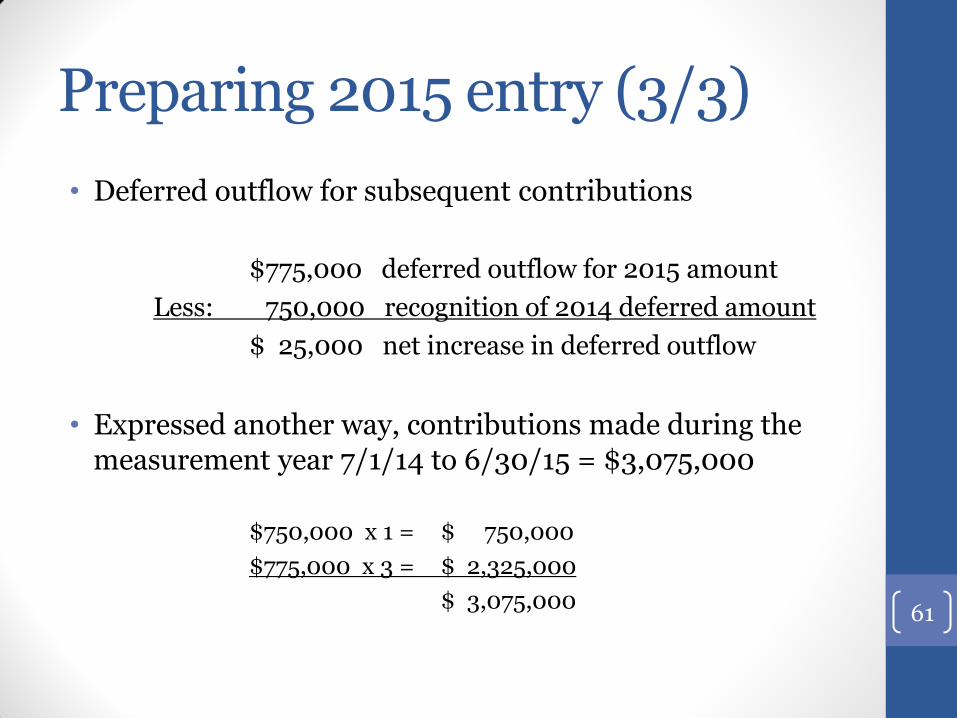

Preparing 2015 entry (3/3)

• Deferred outflow for subsequent contributions

$775,000 deferred outflow for 2015 amount

Less: 750,000 recognition of 2014 deferred amount

$ 25,000 net increase in deferred outflow

• Expressed another way, contributions made during the measurement year 7/1/14 to 6/30/15 = $3,075,000

$750,000 x 1 = $ 750,000

$775,000 x 3 = $ 2,325,000

$ 3,075,000

61

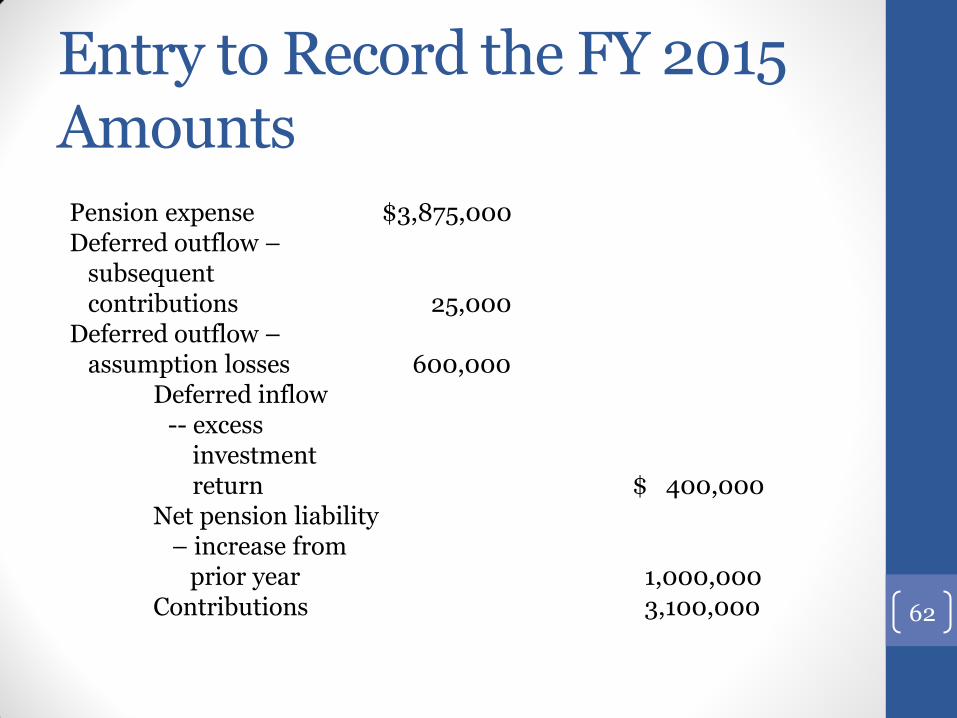

Entry to Record the FY 2015 Amounts

Pension expense $3,875,000 Deferred outflow – subsequent contributions 25,000 Deferred outflow – assumption losses 600,000 Deferred inflow -- excess investment return $ 400,000 Net pension liability – increase from prior year 1,000,000 Contributions 3,100,000

62

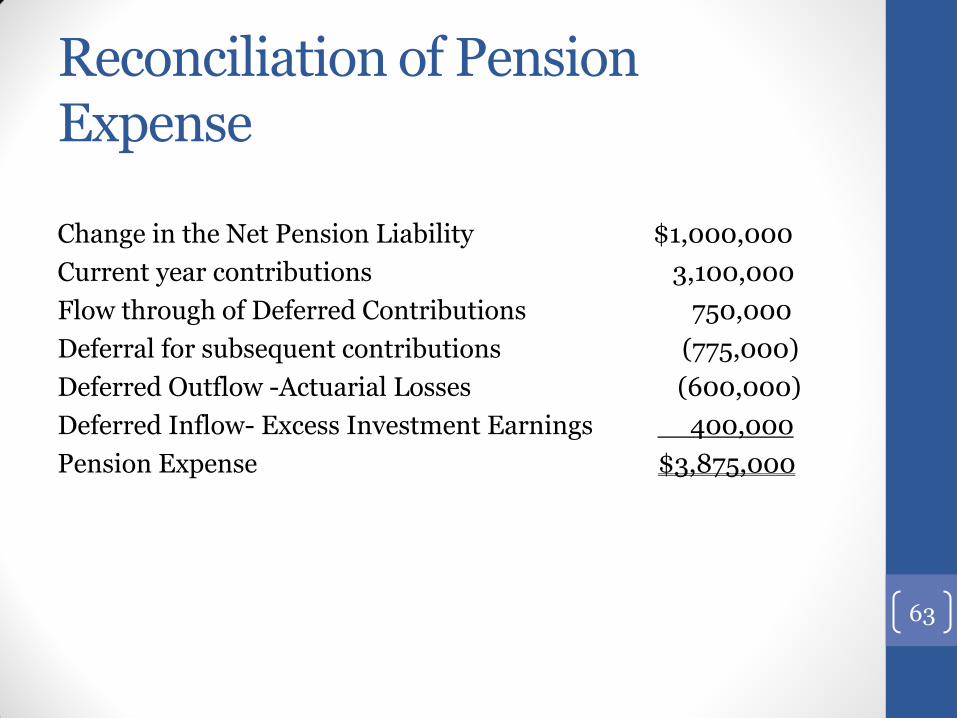

Reconciliation of Pension Expense

Change in the Net Pension Liability $1,000,000

Current year contributions 3,100,000

Flow through of Deferred Contributions 750,000

Deferral for subsequent contributions (775,000)

Deferred Outflow -Actuarial Losses (600,000)

Deferred Inflow- Excess Investment Earnings 400,000

Pension Expense $3,875,000

63

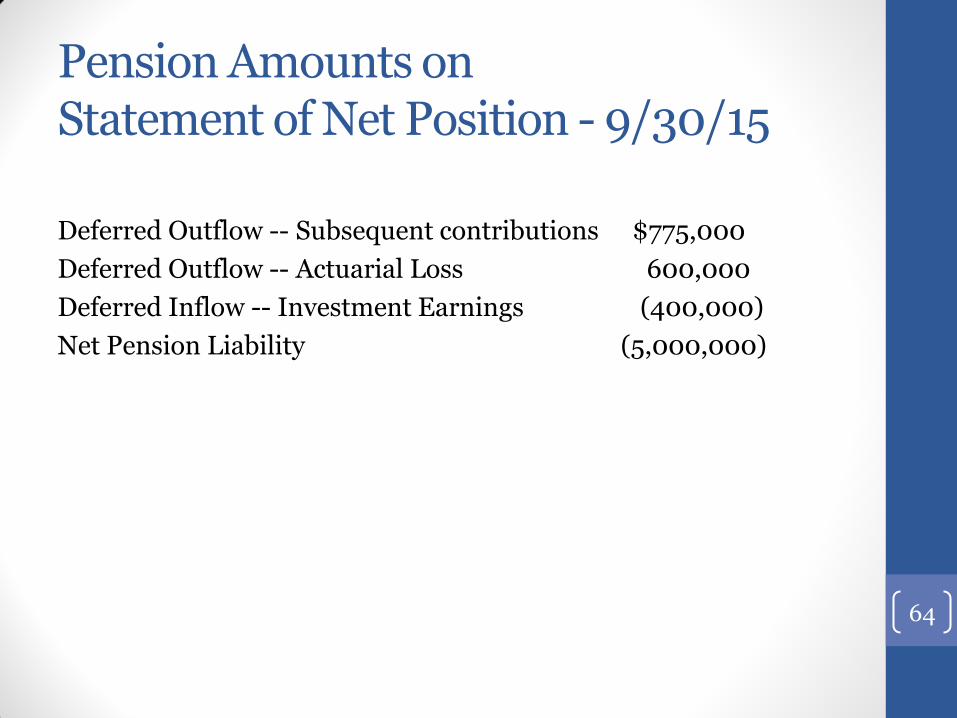

Pension Amounts on Statement of Net Position - 9/30/15

Deferred Outflow -- Subsequent contributions $775,000

Deferred Outflow -- Actuarial Loss 600,000

Deferred Inflow -- Investment Earnings (400,000)

Net Pension Liability (5,000,000)

64

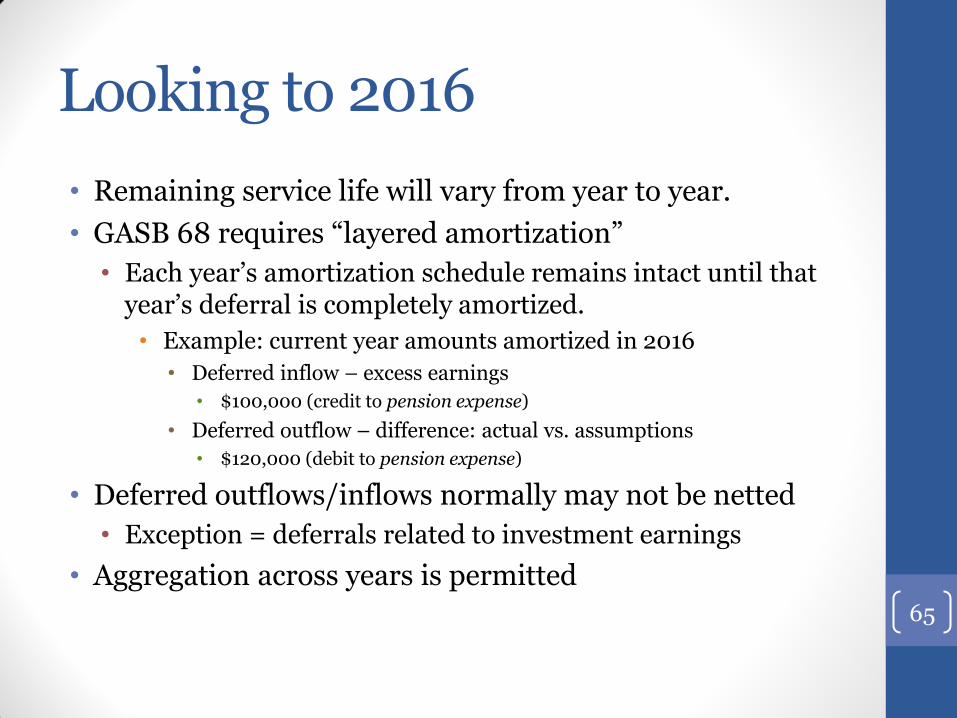

Looking to 2016

• Remaining service life will vary from year to year.

• GASB 68 requires “layered amortization”

• Each year’s amortization schedule remains intact until that year’s deferral is completely amortized.

• Example: current year amounts amortized in 2016

• Deferred inflow – excess earnings

• $100,000 (credit to pension expense)

• Deferred outflow – difference: actual vs. assumptions

• $120,000 (debit to pension expense)

• Deferred outflows/inflows normally may not be netted

• Exception = deferrals related to investment earnings

• Aggregation across years is permitted

65

ALLOCATION OF PENSION/OPEB TO PROPRIETARY AND FIDUCIARY FUNDS

Employer implementation

Part 5

66

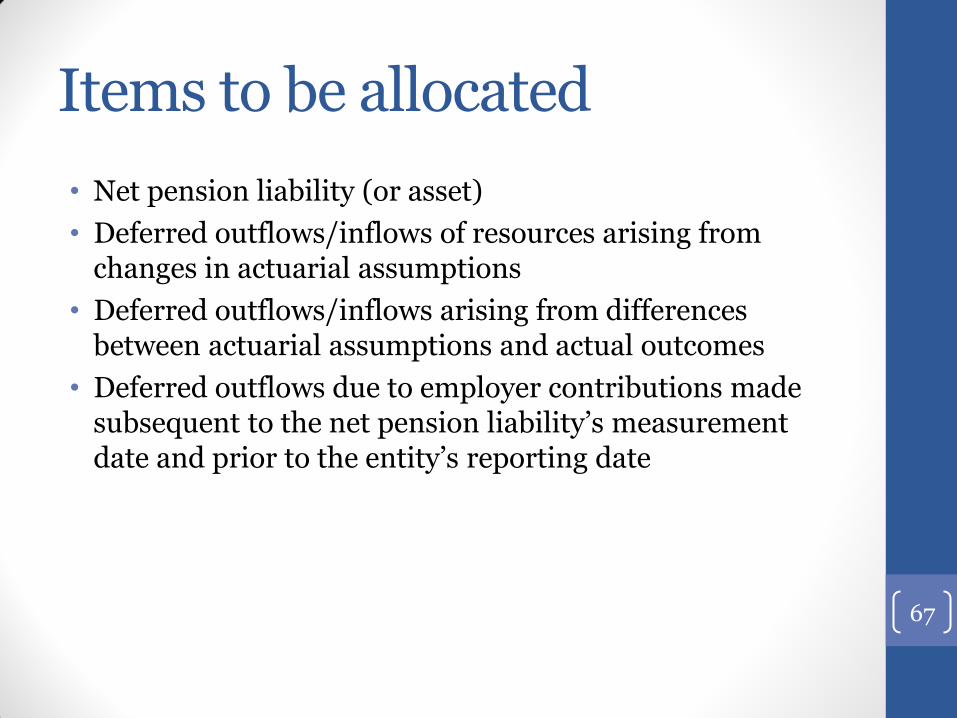

Items to be allocated

• Net pension liability (or asset)

• Deferred outflows/inflows of resources arising from changes in actuarial assumptions

• Deferred outflows/inflows arising from differences between actuarial assumptions and actual outcomes

• Deferred outflows due to employer contributions made subsequent to the net pension liability’s measurement date and prior to the entity’s reporting date

67

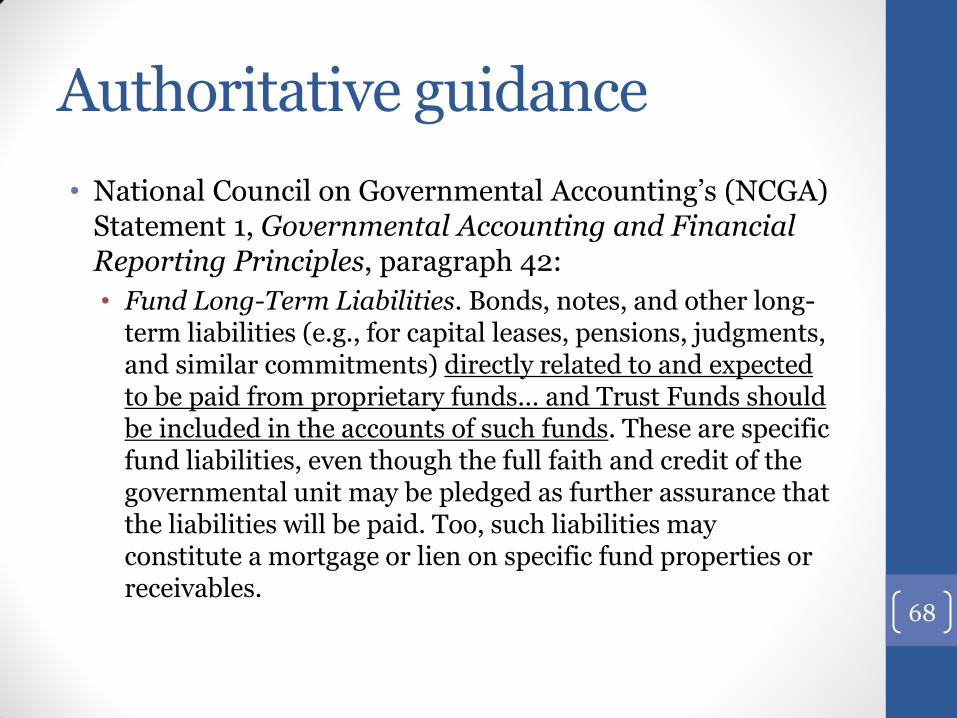

Authoritative guidance

• National Council on Governmental Accounting’s (NCGA) Statement 1, Governmental Accounting and Financial Reporting Principles, paragraph 42:

• Fund Long-Term Liabilities. Bonds, notes, and other long-term liabilities (e.g., for capital leases, pensions, judgments, and similar commitments) directly related to and expected to be paid from proprietary funds… and Trust Funds should be included in the accounts of such funds. These are specific fund liabilities, even though the full faith and credit of the governmental unit may be pledged as further assurance that the liabilities will be paid. Too, such liabilities may constitute a mortgage or lien on specific fund properties or receivables.

68

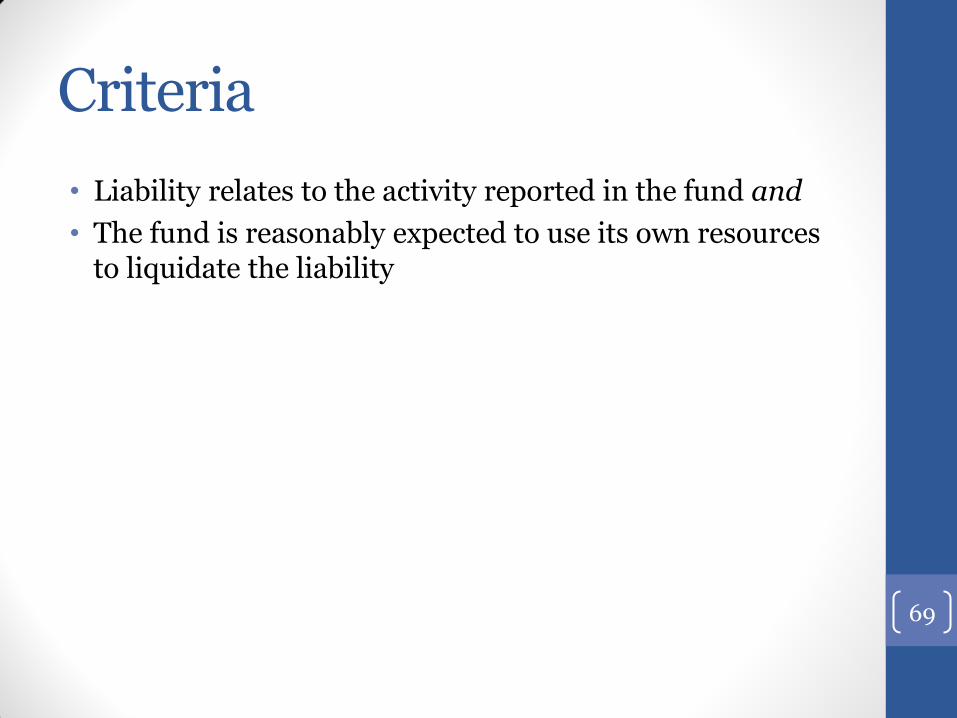

Criteria

• Liability relates to the activity reported in the fund and

• The fund is reasonably expected to use its own resources to liquidate the liability

69

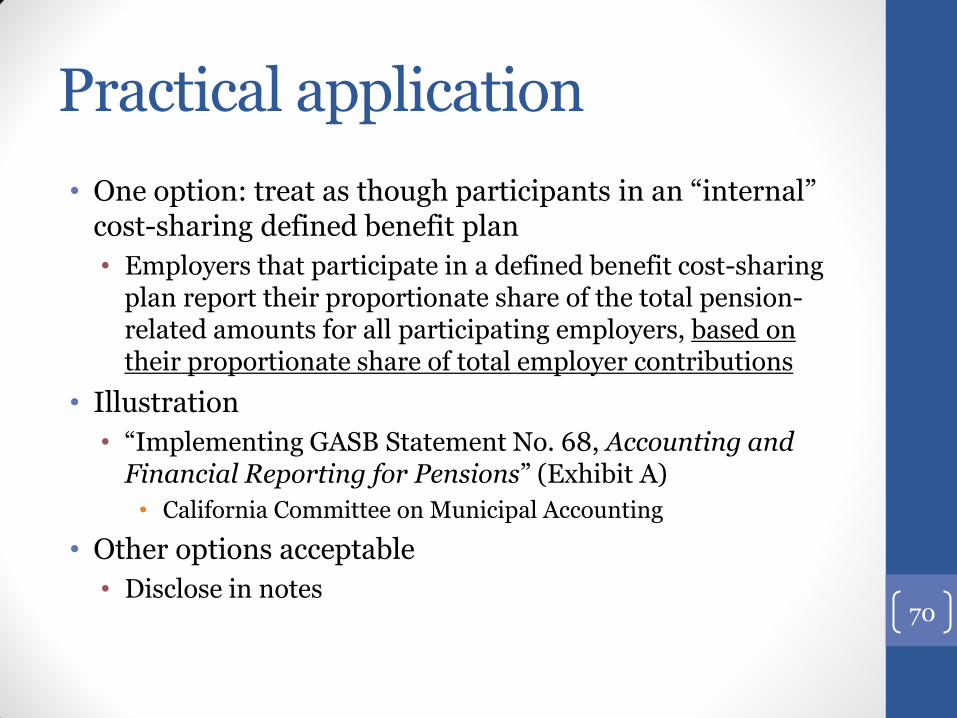

Practical application

• One option: treat as though participants in an “internal” cost-sharing defined benefit plan

• Employers that participate in a defined benefit cost-sharing plan report their proportionate share of the total pension-related amounts for all participating employers, based on their proportionate share of total employer contributions

• Illustration

• “Implementing GASB Statement No. 68, Accounting and Financial Reporting for Pensions” (Exhibit A)

• California Committee on Municipal Accounting

• Other options acceptable

• Disclose in notes

70

COVERED VS. COVERED-EMPLOYEE PAYROLL (GASB 67 & GASB 68)

Employer implementation

Part 6

71

Definitions

• Covered payroll (“pensionable” payroll)

• All elements included in compensation paid to active employees on which contributions to a pension plan are based. For example, if pension contributions are calculated on base pay, including overtime, covered payroll includes overtime compensation.

• Covered-employee payroll

• Total payroll for covered employees, including non-pensionable amounts

72

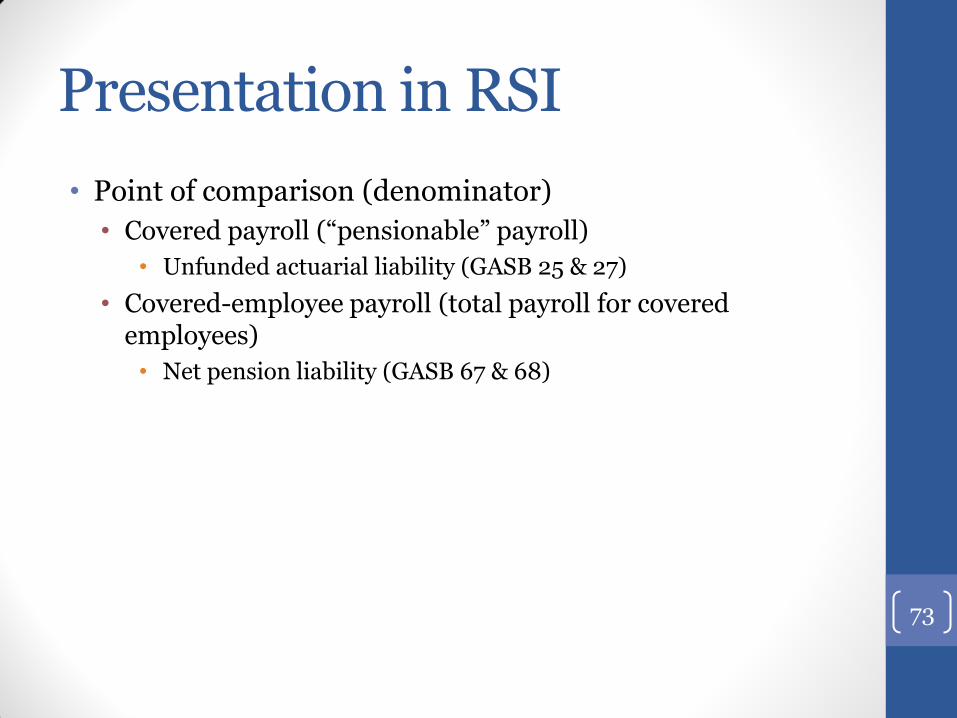

Presentation in RSI

• Point of comparison (denominator)

• Covered payroll (“pensionable” payroll)

• Unfunded actuarial liability (GASB 25 & 27)

• Covered-employee payroll (total payroll for covered employees)

• Net pension liability (GASB 67 & 68)

73

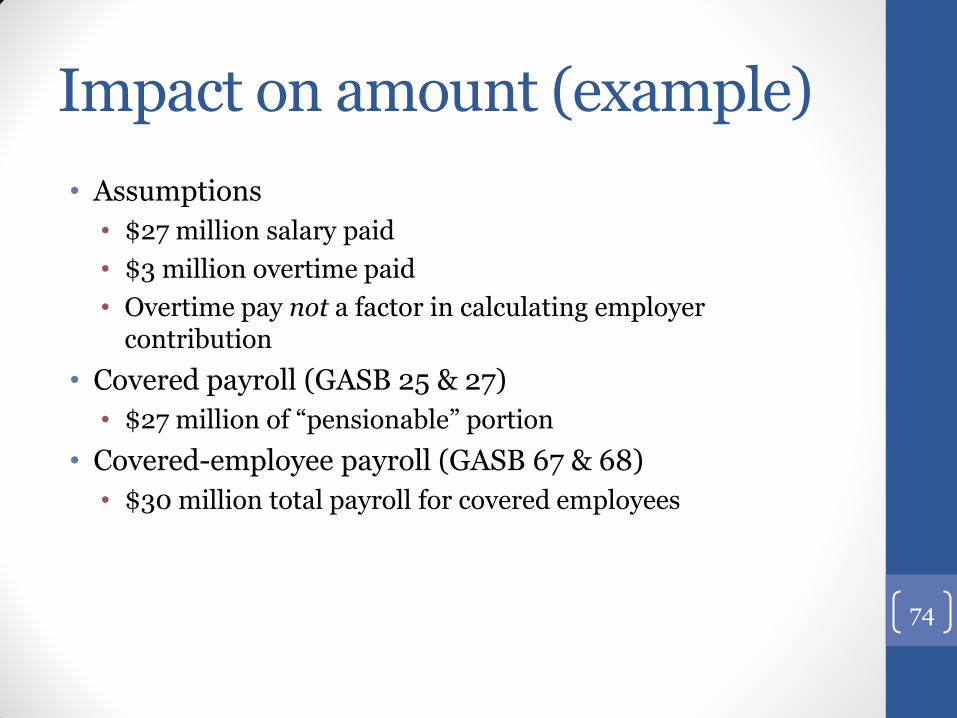

Impact on amount (example)

• Assumptions

• $27 million salary paid

• $3 million overtime paid

• Overtime pay not a factor in calculating employer contribution

• Covered payroll (GASB 25 & 27)

• $27 million of “pensionable” portion

• Covered-employee payroll (GASB 67 & 68)

• $30 million total payroll for covered employees

74

Challenge

• Pension plans not necessarily able to determine total payroll for covered employees if different from “pensionable” portion

• Employers will need to provide both amounts to plan

75

AUDIT IMPACT

Employer implementation

Part 7

76

Agent plans – preliminaries

• Responsibility

• Ultimate audit responsibility

• Employer auditor

• Responsibility for reviewing the reasonableness of actuarial assumptions

• Employer

• Employer auditor

• Audit work

• Plan auditor must provide information/perform audit procedures on information maintained by the plan

• Employer auditor must review census data received from the plan, based on employer data regarding current employees

77

Agent plans – available data

• Fiduciary net position (FNP)

• Display at plan level

• Insufficient audit coverage for individual employers

• Total pension liability (TPL)

• Neither Display nor disclosure

• Not for system as a whole

• Not for individual participating employers

78

Agent plans – solution for FNP

• Plan

• Prepares schedule of changes in FNP by employer

• Plan auditor

• Utilize SOC 1 Type 2 to support allocations, or

• Substantive testing of allocations among employers

79

Agent plan – solution for TPL

• Three responsible parties

A. Actuary

B. Plan auditor

C. Employer auditor

80

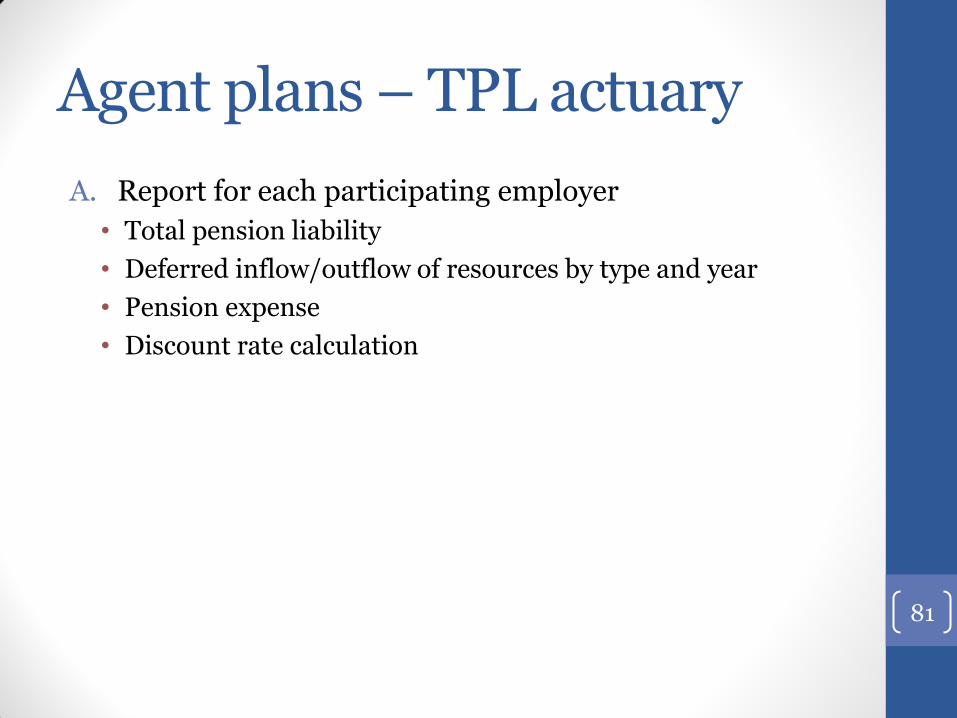

Agent plans – TPL actuary

A. Report for each participating employer

• Total pension liability

• Deferred inflow/outflow of resources by type and year

• Pension expense

• Discount rate calculation

81

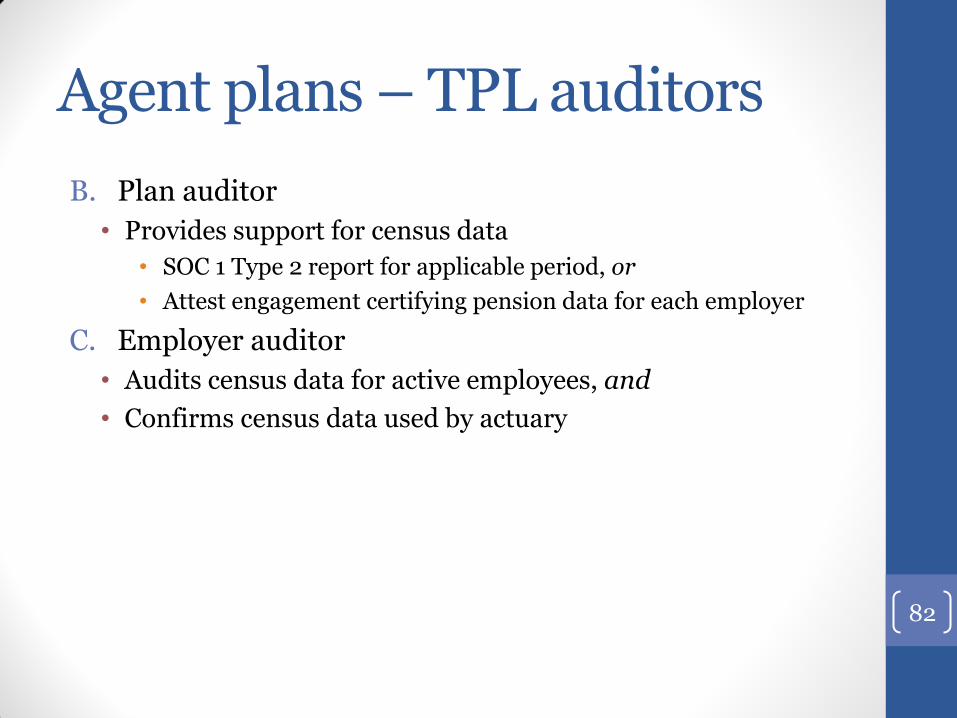

Agent plans – TPL auditors

B. Plan auditor

• Provides support for census data

• SOC 1 Type 2 report for applicable period, or

• Attest engagement certifying pension data for each employer

C. Employer auditor

• Audits census data for active employees, and

• Confirms census data used by actuary

82

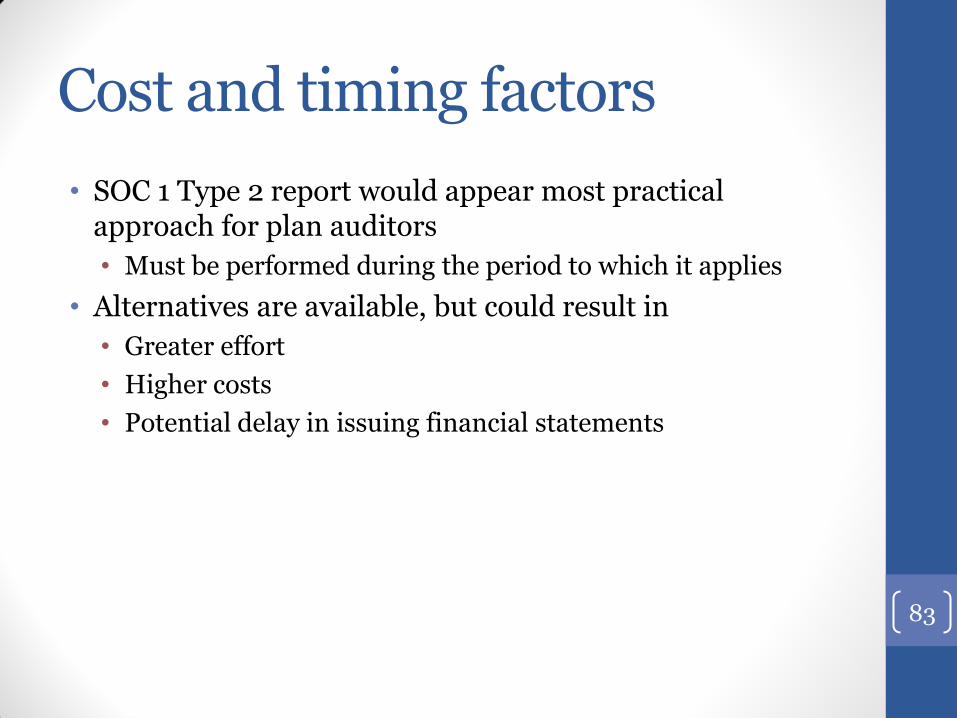

Cost and timing factors

• SOC 1 Type 2 report would appear most practical approach for plan auditors

• Must be performed during the period to which it applies

• Alternatives are available, but could result in

• Greater effort

• Higher costs

• Potential delay in issuing financial statements

83

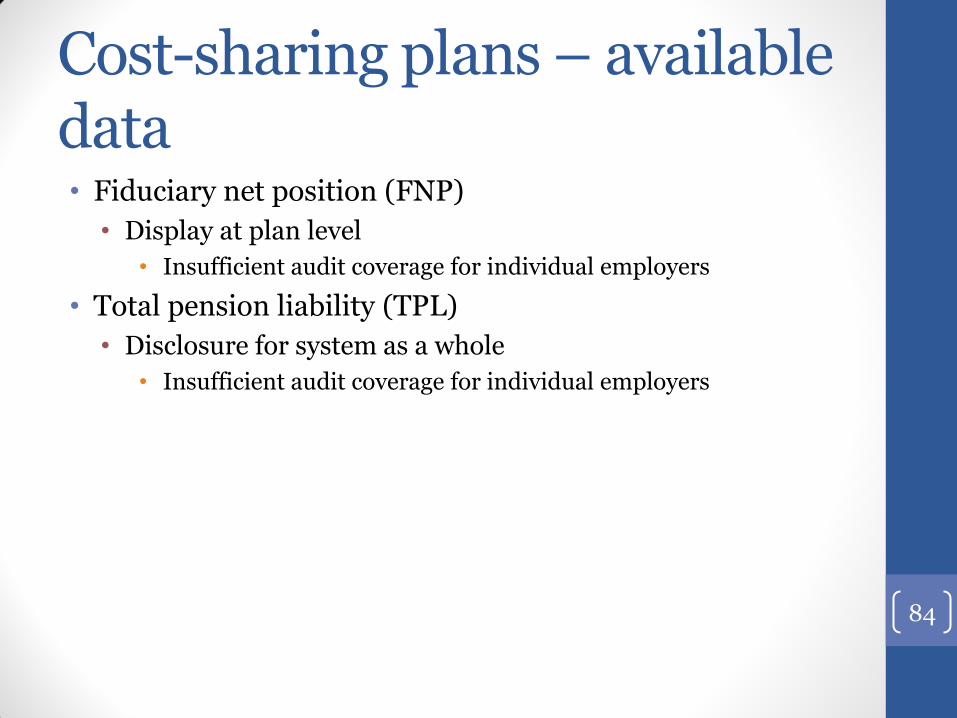

Cost-sharing plans – available data • Fiduciary net position (FNP)

• Display at plan level

• Insufficient audit coverage for individual employers

• Total pension liability (TPL)

• Disclosure for system as a whole

• Insufficient audit coverage for individual employers

84

Cost-sharing plans – solution

• Information on the employer’s proportionate share of total for all employers (audited by plan auditor)

• Supplemental schedule of employer allocations, or

• Schedule of plan pension amounts by employer

85

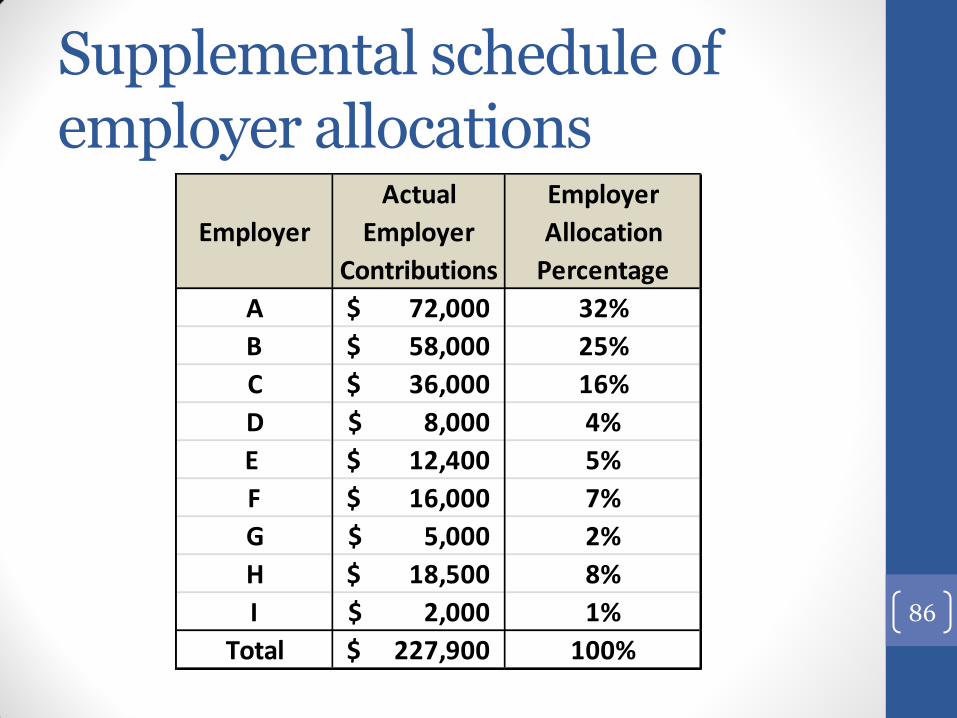

Supplemental schedule of employer allocations

86

Employer

Actual

Employer

Contributions

Employer

Allocation

Percentage

A 72,000$ 32%

B 58,000$ 25%

C 36,000$ 16%

D 8,000$ 4%

E 12,400$ 5%

F 16,000$ 7%

G 5,000$ 2%

H 18,500$ 8%

I 2,000$ 1%

Total 227,900$ 100%

FUNDING IMPACT

Employer implementation

Part 8

87

Need for funding guidelines

• Close historical link between

• Accounting and financial reporting for pensions

• Funding (budgeting) pensions

• Same actuarial method used for both

• GASB 68 breaks this link

• Single actuarial method now required for accounting and financial reporting purposes, regardless of funding

• That method not well adapted to funding

• Resulting concerns

• GAAP information no longer directly useful in assessing the adequacy of funding

• Loss of GASB-mandated parameters on application of actuarial methods

88

Development of common guidelines for sustainable funding • “Big 7” public interest groups

• National Governors Association

• National Conference of State Legislatures

• Council of State Governments

• National Association of Counties

• National League of Cities

• U.S. Conference of Mayors

• International City/County Management Association

• Government Finance Officers Association

• National Association of State Auditors, Comptrollers, and Treasurers

• National Association of State Retirement Administrators

• National Council on Teacher Retirement 89

• Use actuarially determined contributions (ADC) as a basis for actual employer contributions

• Guidelines for making principled decisions regarding the calculation of the ADC

• Actuarial cost method

• Asset smoothing

• Amortization

• Provide information needed to assess funding progress

90

Essential elements

• Adopts and adapts funding guidelines

• Specific recommendations on how to apply the guidelines

• Recognition that a transition period may be necessary

91

GFOA best practice

EXPLAINING THE CHANGE

Employer implementation

Part 9

92

Accounting change vs. event

• The underlying factual situation has not changed

• Should not be a surprise to bond rating agencies

• Similar information previously disclosed in notes

• Actuarial value of assets (net fiduciary position)

• Actuarial accrued liability (total pension liability)

• Unfunded actuarial accrued liability (net pension liability)

93

Response to NPL

• Different liabilities are funded differently

• Vacation leave

• Key consideration with postemployment benefits = disciplined, systematic funding over time

• Assured by using actuarially determined contributions

• Selection of appropriate actuarial method and assumptions

94

Plan contributions vs. employer expense • Difference

• What something costs (expense)

• How we pay for it (contributions)

95

Question 8

If a pension plan is not administered through a trust or equivalent arrangement, the employer should report

A. Accumulated assets

B. Total pension liability

C. Net pension liability

D. All the above

E. Both A and B

96

Question 9

Which of the following should be included in the notes to RSI for pensions?

A. Change in investment policies

B. Change in market prices

C. Both A and B

D. None of the above

97

Question 10

Any employer payable to a multiple-employer pension plan with employer-specific payment terms qualifies as a separately financed specific liability.

A. True

B. False

98

Question 11

Which of the following will remain true under GASB 75?

A. Employers sometimes have to recognize OPEB expense for retirees who pay the full amount of their healthcare premium

B. Some employers may have the option of using an alternative measurement method that eliminates the need to engage the services of a professional actuary

C. Both A and B

D. None of the above

99

Question 12

Which of the following statements best describes the relationship between sensitivity disclosure for pensions and sensitivity disclosure for OPEB?

A. There is more required sensitivity disclosure for OPEB than for pensions

B. There is less required sensitivity disclosure for OPEB than for pensions

C. There is no difference in required sensitivity disclosure for OPEB and for pensions

100

Question 13

Which of the following statements is true?

A. Pension expense must always be allocated to enterprise funds

B. Pension expense must sometimes be allocated to enterprise funds

C. Pension expense must never be allocated to enterprise funds

101

Question 14

Which of the following commonly is described as “pensionable payroll”?

A. Covered payroll

B. Covered-employee payroll

102

Question 15

Which of the following information should be available at the plan level for an agent plan?

A. Fiduciary net position

B. Total pension liability

C. Both A and B

D. None of the above

103

Question 16

Which of the following information should be available at the plan level for a cost-sharing plan?

A. Fiduciary net position

B. Total pension liability

C. Both A and B

D. None of the above

104

Question 17

Differences between accounting and financial reporting and funding should be minimal if the entry age (level percentage of pay) actuarial cost method is used for both.

A. True

B. False

105

Other new standards GAAP Hierarchy (GASB 76)

Tax Abatement Disclosures (GASB 77)

106

THE HIERARCHY OF GAAP FOR STATE AND LOCAL GOVERNMENTS

GASB 76

107

Scope

• Changes “chain of command” of sources of authoritative guidance

• Current hierarchy

• Four levels of authoritative sources of GAAP

• Other accounting literature

• New hierarchy

• Two levels of authoritative sources of GAAP

• Highest level – requires GASB approval

• Second level – requires GASB clearance

• Nonauthoritative accounting literature

108

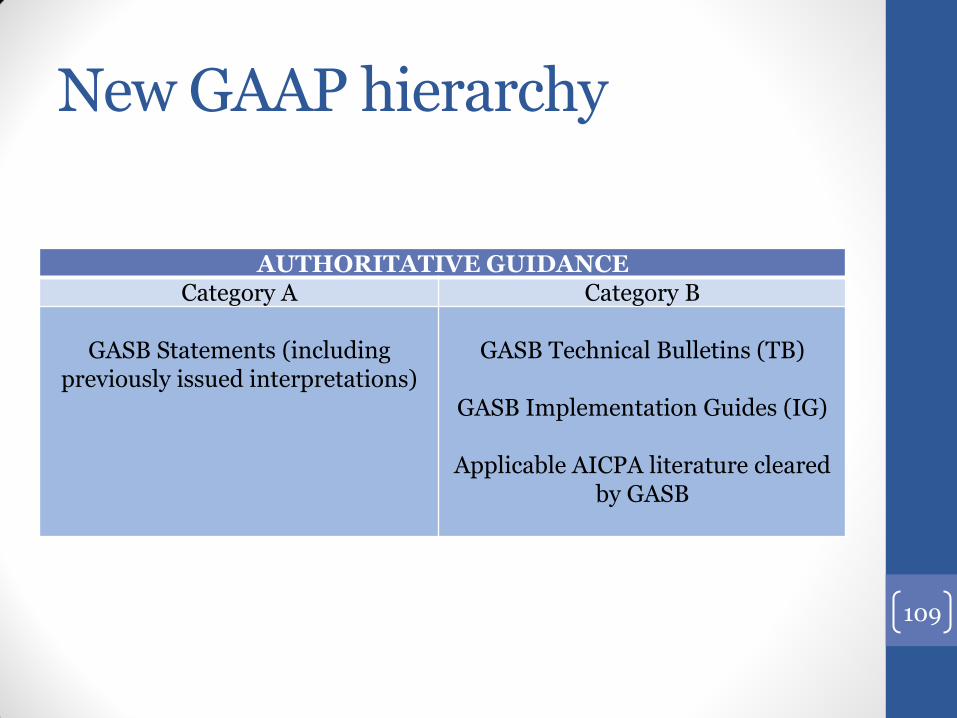

New GAAP hierarchy

AUTHORITATIVE GUIDANCE Category A Category B

GASB Statements (including

previously issued interpretations)

GASB Technical Bulletins (TB)

GASB Implementation Guides (IG)

Applicable AICPA literature cleared

by GASB

109

Key changes

• No future GASB Interpretations

• Role to be filled by statements/technical bulletins

• Implementation Guides now authoritative

• Need for “due process”

• Limited to “clarifying, explaining, or elaborating”

• “Widely recognized and prevalent practice” no longer authoritative

110

Citing authoritative guidance

• Equal authority

• GASB Original Pronouncements

• GASB Codification of Governmental Accounting and Financial Reporting Standards

111

Nonauthoritative guidance

• GASB Concepts Statements

• Literature of other standard-setting bodies

• Financial Accounting Standards Board

• Federal Accounting Standards Advisory Board

• International Public Sector Accounting Standards Board

• International Accounting Standards Board

• Relevant AICPA guidance not cleared by the GASB

• Widely recognized and prevalent practices

• Literature of other professional associations

• Literature of regulatory agencies

• Accounting textbooks, handbooks, and articles

112

Application

• No specific authoritative guidance?

• Consider authoritative guidance for similar transactions and events

• Unless application by analogy prohibited

• How to evaluate nonauthoritative sources?

• Consistency with GASB Concepts Statements

• Relevance to the particular circumstances

• Specificity of the literature

• General recognition of the issuer/author as an authority

113

Impact on new 2015-1 Implementation Guide • Material eliminated from this new edition

• Verbatim excerpts or paraphrases of authoritative standards

• Definitions of terms provided in authoritative standards

• Explanation of the reasoning behind authoritative standards

• Discussions of the applicability of nonauthoritative accounting literature

• All illustrative material consigned to nonauthoritative appendices

• No new questions added this year

114

TAX ABATEMENT DISCLOSURES

GASB 77

115

Tax expenditures

• “Opportunity cost” of foregoing the collection of taxes to which otherwise entitled

• Subcategories

• Tax exemptions

• Tax deductions

• Tax abatements

116

Definition: tax abatements

• A reduction in tax revenues that results from an agreement between one or more governments and an individual or entity in which (a) one or more governments promise to forgo tax revenues to which they are otherwise entitled and (b) the individual or entity promises to take a specific action after the agreement has been entered into that contributes to economic development or otherwise benefits the governments or the citizens of those governments

117

Essential characteristics

• Type of revenue

• A tax (not a fee or charge)

• Existence of an agreement

• Identifiable agreement with a specific individual or entity

• Government promises to reduce the counterparty’s tax liability

• The counterparty promises to take certain actions

• Must precede any reduction in taxes

• Does not have to be in writing

• Does not have to be legally enforceable

• Purpose

• Promote economic development or otherwise benefit the government or its citizens

118

Two types of tax abatements

• Agreements of the government itself

• Agreements of others that reduce the government’s revenue

119

General presentation

• Distinguish:

• Government’s own agreements

• Agreements of others that reduce the governments revenue

• Individual display must be based on a quantitative threshold

• Different thresholds may be used for government’s own agreements and agreements of others

• Required only as long as abatements are outstanding

• Information on a government’s associated commitments not necessary once fulfilled

• Governments are not required to present information if they are legally prohibited from doing so (although that fact must be disclosed)

120

Specific disclosures

• Agreements of the government

• Organized by major tax abatement program, even for abatements that are disclosed individually

• Agreements of others that reduce the government’s revenue

• Organized by government and specific tax abated, even for abatements that are disclosed individually

121

Disclosure: agreements of the government (1/2) • A brief description that includes:

• Names and purposes of tax abatement programs

• Specific taxes being abated

• Authority for entering into the tax abatement agreement

• Eligibility criteria for recipients

• Abatement mechanism

• How taxes are reduced (reduction of tax liability, rebate, reduction of assessed value)

• How the amount is determined (specific dollar amount or percentage of taxes owed)

• Provisions for recapturing abated taxes (“claw-back” provisions) and the conditions for recapture

• Type of commitments made by recipients 122

Disclosure: agreements of the government (2/2) • Gross dollar amount of revenue reduction in period

(accrual basis)

• If amounts received/receivable from other governments

• Names

• Authority

• Dollar amount received/receivable

• Commitments in addition to tax reduction (until fulfilled)

• Types

• Most significant individual commitments

• Quantitative threshold for disclosure by individual agreement

• Description of general nature of information omitted because of legal prohibition and specific source of latter

123

Disclosure: agreements of other governments • A brief description that includes:

• Names of governments

• Specific taxes being abated

• Gross dollar amount of revenue reduction in period (accrual basis)

• If amounts received/receivable from other governments

• Names

• Authority

• Dollar amount received/receivable

• Quantitative threshold for disclosure by individual agreement

• Description of general nature of information omitted because of legal prohibition and specific source of latter

124

Disclosure: discretely presented component units • Essential to fair presentation?

• Yes? – disclose like an agreement of the government

• No? – disclose like an agreement of another government

125

Effective date

• Implementation required for fiscal year ending 12/31/16

• Earlier application encouraged

126

Question 18

Which of the following statements best describes the difference between Category A guidance and Category B guidance on the new GAAP Hierarchy?

A. Category A guidance is authoritative, whereas Category B guidance is not

B. Category A guidance has to be approved by the GASB, whereas Category B guidance only needs to be cleared

C. Both A and B

127

Question 19

Which of the following statements is true under the new GAAP Hierarchy?

A. GASB Implementation Guides have become more authoritative

B. GASB Implication Guides will be subject to more “due process”

C. Both A and B

128

Question 20

In the absence of specific authoritative guidance, financial statement preparers should first consider applying authoritative guidance for similar transactions and events by analogy (unless a standard prohibits them from doing so).

A. True

B. False

129

Question 21

Which of the following has greater authoritative standing for purposes of citation?

A. Original Pronouncements

B. Codification of Governmental Accounting and Financial Reporting Standards

C. Neither A nor B

130

Question 22

Which of the following would qualify as a tax abatement?

A. A property tax exemption for elderly disabled homeowners

B. An income tax deduction for qualifying energy-saving home improvements

C. Reduction in future service fees for businesses that agree to relocate to the community

D. All of the above

E. None of the above

131

Question 23

Which of the following statements is true regarding the level of detail needed for tax abatement disclosures?

A. Information on a government’s own agreements should be reported separately from information on the agreements of other governments that reduce its revenue

B. A quantitative threshold should be used to ensure consistent reporting for individual agreements

C. The same quantitative threshold for presentation by individual agreement should be used for both the government’s own agreements and the agreements of other governments that reduce its revenue

D. All of the above

E. Both A and B

132

Question 24

The requirement to present tax abatement disclosures by major tax abatement program (for a government’s own agreements) or by government and specific tax abated (for agreements of other governments that reduce its revenue) also applies to agreements reported individually in both categories.

A. True

B. False

133

Question 25

Governments that are not legally permitted to disclose certain information regarding tax abatements are not required to do so to comply with GAAP.

A. True

B. False

134

Question 26

How should tax abatement agreements of discretely presented component units be treated?

A. As agreements of the government itself

B. As agreements of another government that reduce the government’s revenue

C. Either A or B

D. None of the above

135

RECENT EXPOSURE DRAFTS

Accounting and Financial Reporting for Certain External Investment Pools

Blending Requirements for Certain Component Units

Accounting and Financial Reporting for Irrevocable Split-Interest Agreements

Accounting and Financial Reporting for Pensions Provided through Certain Multiple-Employer Defined Benefit Pension Plans

136

ACCOUNTING AND FINANCIAL REPORTING FOR CERTAIN EXTERNAL INVESTMENT POOLS

Exposure draft – June 2015

[Final statement scheduled for 4Q15]

137

Background

• Amortized cost would be expected to approximate fair value for money market funds

• Nature of money market investments limits deviation

• Consequently:

• Such pools have been permitted to report all of their investments at amortized cost

• Participants in such pools have been permitted to report their position based on share value prices that reflect amortized cost

• Until now, SEC rule 2a7 has provided the criteria for defining qualifying pools

• Recent changes make it impractical to continue to rely on SEC rule 2a7

138

Objective

• GASB proposes to replace 2a7 criteria with its own criteria for pools that operate like money market funds

139

Nature of exception

• Use of amortized cost remains purely optional

• Use of fair value always permitted

• Once a pool has elected to use fair value, it cannot subsequently reverse that election

140

Criteria for being permitted to report at amortized cost • Stable net asset value (NAV) per share

• Additional requirements

A. Meets portfolio maturity requirements

B. Meets portfolio quality requirements

C. Meets portfolio diversification requirements

D. Meets portfolio liquidity requirements

E. Meets shadow price requirements

141

A. Maturity requirements

• Remaining maturity ≤ 397 days

• Weighted average maturity ≤ 60 days

• Takes into account maturity shortening features

• Weighted average life ≤ 120 days

• Ignores maturity shortening features

142

B. Quality requirements

• Denominated in U.S. dollars

• Highest credit rating category at acquisition

143

C. Diversification requirements

• Single issuer ≤ 5% total assets

• Not applicable to U.S. government securities

144

D. Liquidity requirements (1/2)

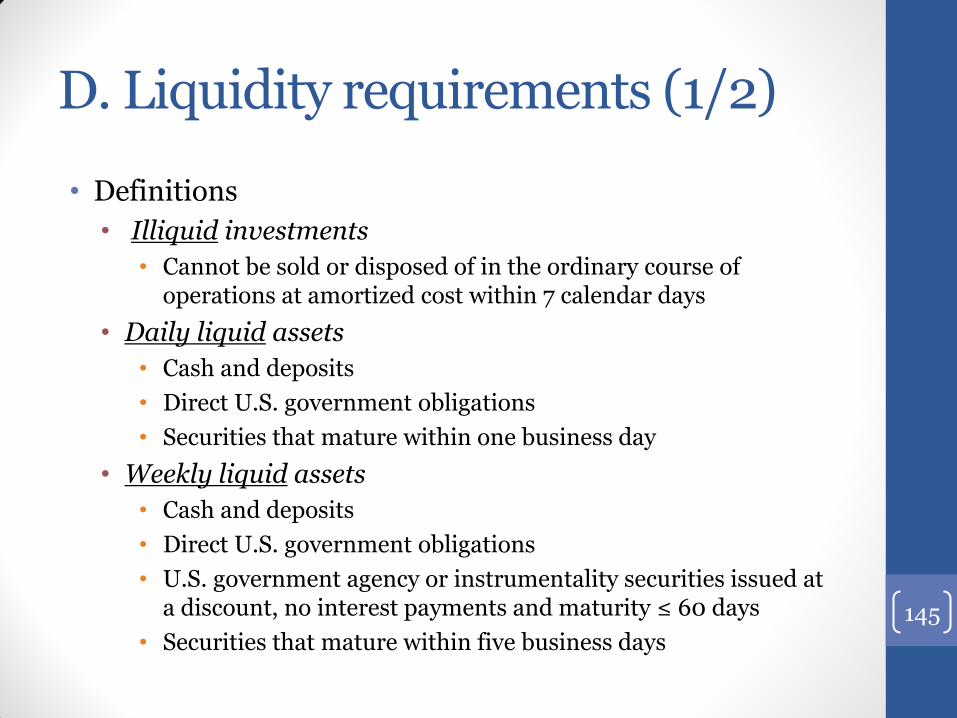

• Definitions

• Illiquid investments

• Cannot be sold or disposed of in the ordinary course of operations at amortized cost within 7 calendar days

• Daily liquid assets

• Cash and deposits

• Direct U.S. government obligations

• Securities that mature within one business day

• Weekly liquid assets

• Cash and deposits

• Direct U.S. government obligations

• U.S. government agency or instrumentality securities issued at a discount, no interest payments and maturity ≤ 60 days

• Securities that mature within five business days

145

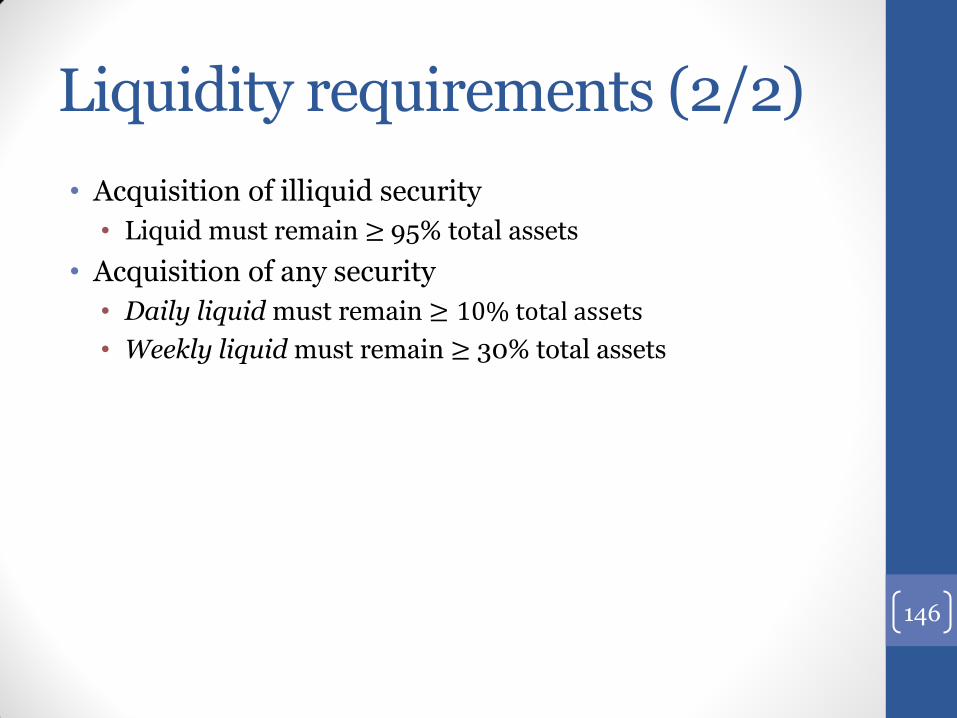

Liquidity requirements (2/2)

• Acquisition of illiquid security

• Liquid must remain ≥ 95% total assets

• Acquisition of any security

• Daily liquid must remain ≥ 10% total assets

• Weekly liquid must remain ≥ 30% total assets

146

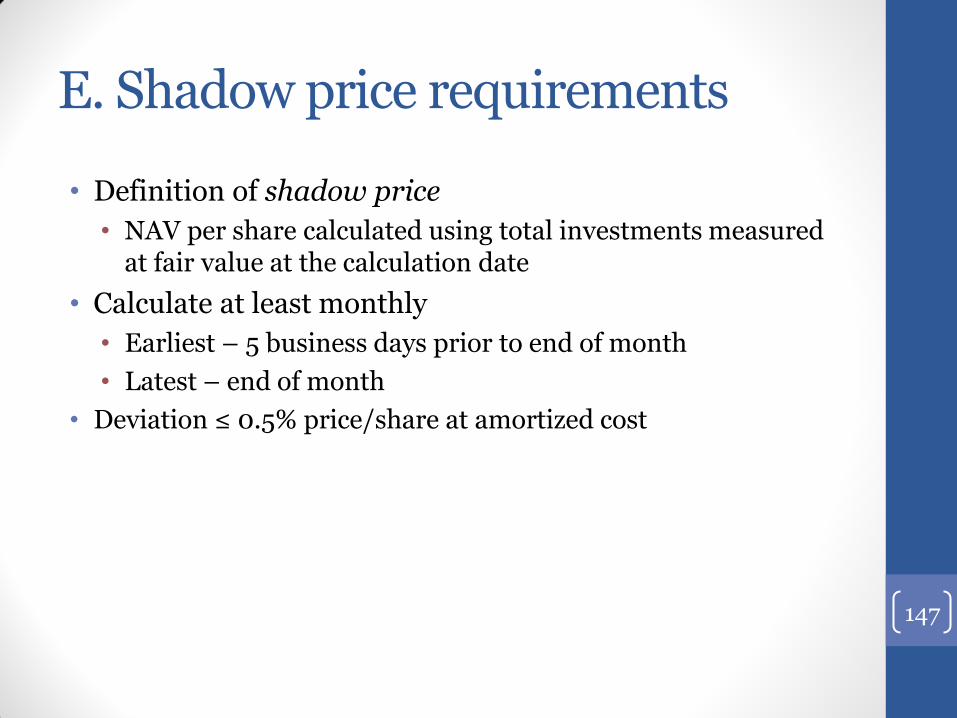

E. Shadow price requirements

• Definition of shadow price

• NAV per share calculated using total investments measured at fair value at the calculation date

• Calculate at least monthly

• Earliest – 5 business days prior to end of month

• Latest – end of month

• Deviation ≤ 0.5% price/share at amortized cost

147

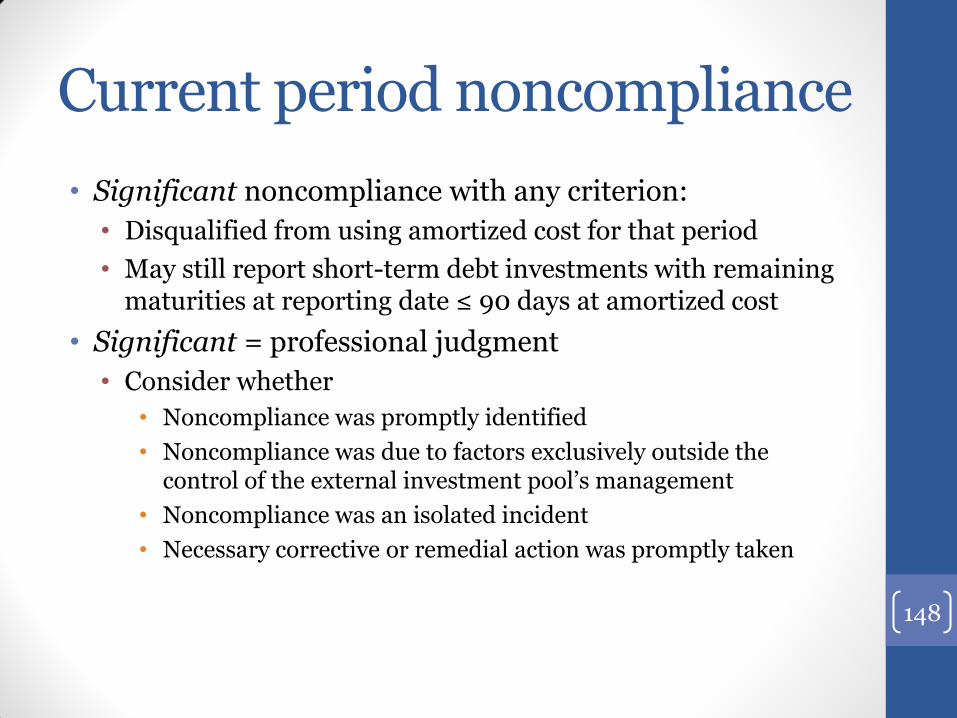

Current period noncompliance

• Significant noncompliance with any criterion:

• Disqualified from using amortized cost for that period

• May still report short-term debt investments with remaining maturities at reporting date ≤ 90 days at amortized cost

• Significant = professional judgment

• Consider whether

• Noncompliance was promptly identified

• Noncompliance was due to factors exclusively outside the control of the external investment pool’s management

• Noncompliance was an isolated incident

• Necessary corrective or remedial action was promptly taken

148

Previous noncompliance

• Significant noncompliance with any of the criteria during a previous reporting period?

• Still qualifies for reporting at amortized cost in current period if previous noncompliance due to exceptional circumstances

149

Disclosure requirements

• Pools

• Disclosure already required for fair value measurement per GASB 31 and GASB 72

• Any limitations or restrictions on participant withdrawals

• Notice periods

• Maximum transaction amounts

• Pool’s authority to impose liquidity fees or redemption gates

• Participants

• Any limitations or restrictions on withdrawals

• Notice periods

• Maximum transaction amounts

• Pool’s authority to impose liquidity fees or redemption gates 150

Effective date

• Generally FYE 6/30/16

• Additional 6 months (certain credit risk requirements)

151

BLENDING REQUIREMENTS FOR CERTAIN COMPONENT UNITS

Exposure draft – June 2015

[Final statement scheduled for 1Q16]

152

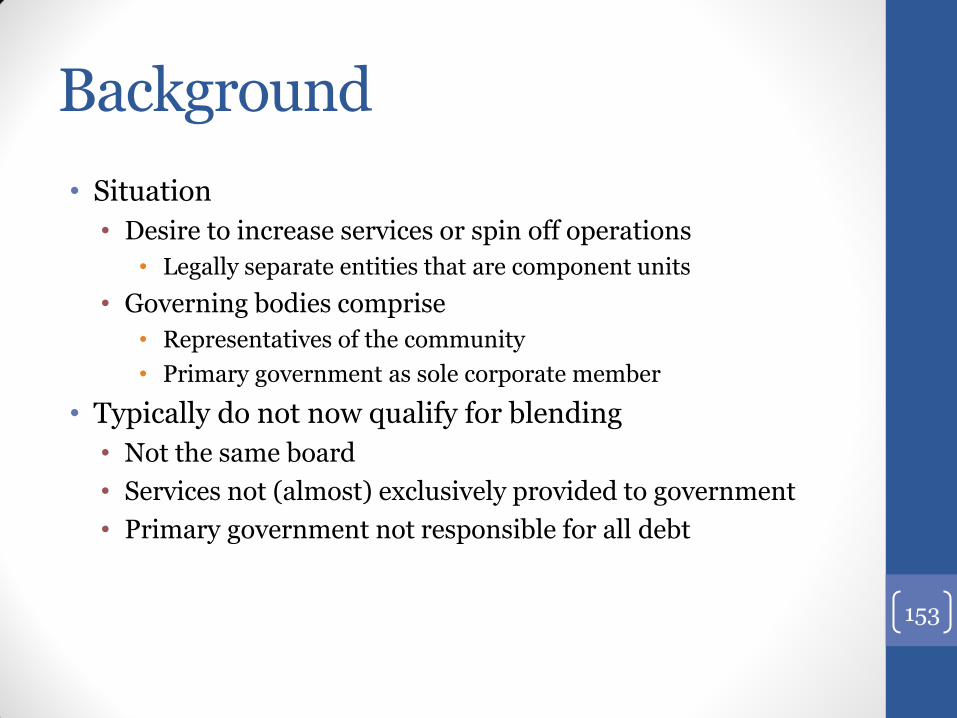

Background

• Situation

• Desire to increase services or spin off operations

• Legally separate entities that are component units

• Governing bodies comprise

• Representatives of the community

• Primary government as sole corporate member

• Typically do not now qualify for blending

• Not the same board

• Services not (almost) exclusively provided to government

• Primary government not responsible for all debt

153

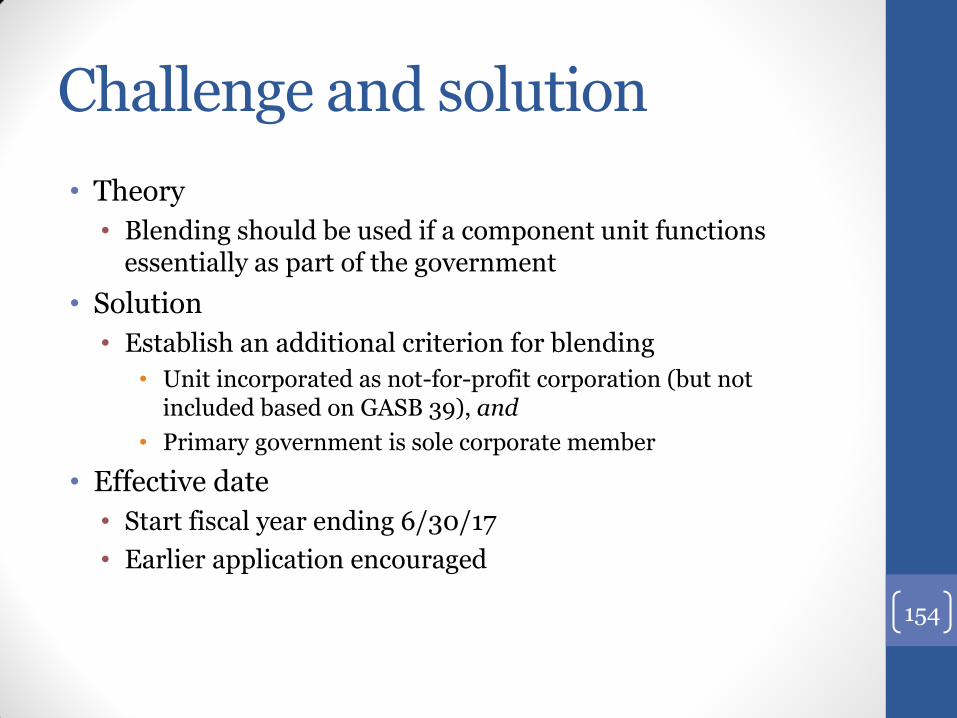

Challenge and solution

• Theory

• Blending should be used if a component unit functions essentially as part of the government

• Solution

• Establish an additional criterion for blending

• Unit incorporated as not-for-profit corporation (but not included based on GASB 39), and

• Primary government is sole corporate member

• Effective date

• Start fiscal year ending 6/30/17

• Earlier application encouraged

154

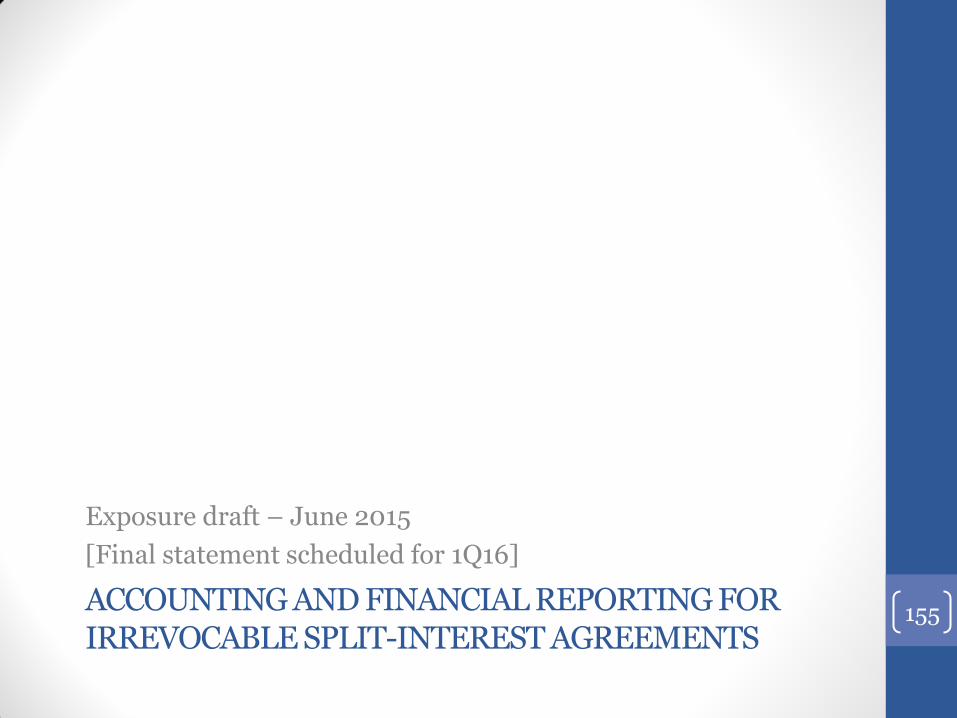

ACCOUNTING AND FINANCIAL REPORTING FOR IRREVOCABLE SPLIT-INTEREST AGREEMENTS

Exposure draft – June 2015

[Final statement scheduled for 1Q16]

155

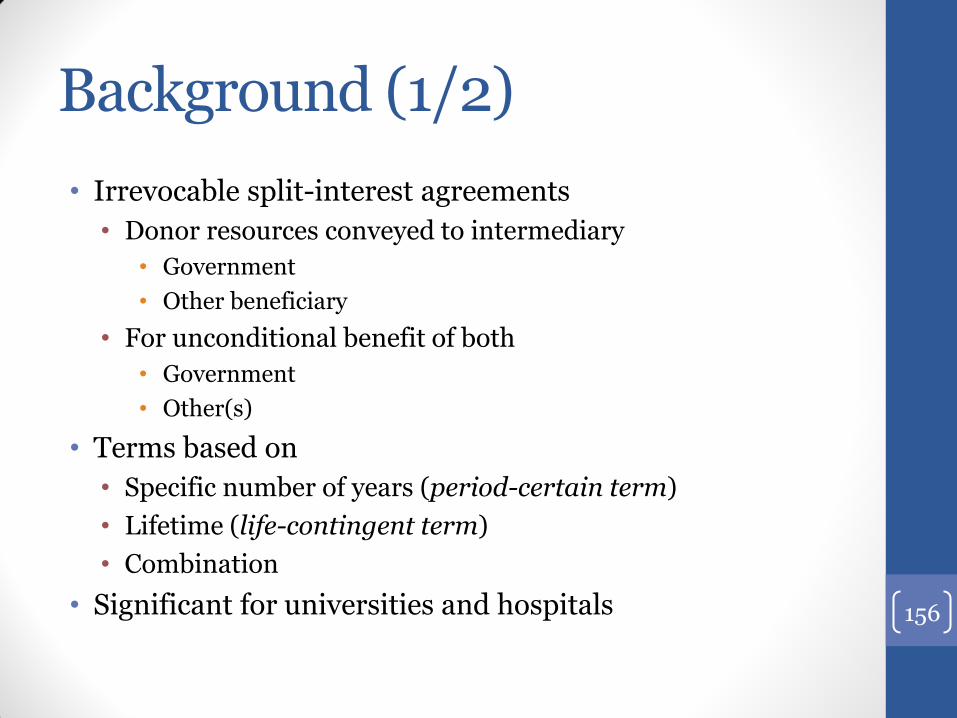

Background (1/2)

• Irrevocable split-interest agreements

• Donor resources conveyed to intermediary

• Government

• Other beneficiary

• For unconditional benefit of both

• Government

• Other(s)

• Terms based on

• Specific number of years (period-certain term)

• Lifetime (life-contingent term)

• Combination

• Significant for universities and hospitals

156

Background (2/2)

• Lead interest

• Access to resources during term of agreement

• Annuity

• Percentage of fair value (unitrust)

• Remainder interest

• Access to resources at termination of agreement

157

Government as intermediary (1/5)

• Timing of recognition

• Agreement executed and

• Assets received

• Elements recognized

• Assets for donated resources

• Liability to third party (= “split” interest)

• Deferred inflow of resources (= government’s share)

158

Government as intermediary (2/5)

• Measurement of assets

• Dependent on use (investment vs. capital asset)

• Regular recognition rules apply

• Measurement of liability/deferred inflow

• Lead interest = settlement amount for payment stream

• Use established valuation technique

• Consider

• Specific provisions and underlying assumptions

• Estimated return on assets

• Discount rate (if reported at present value)

• Mortality rate (if life-contingent)

• Adjust only for mortality (if life-contingent)

• Remainder interest = balance

159

Government as intermediary (3/5)

• Application: government as remainder interest beneficiary

• Liability to beneficiary of the lead interest

• Calculated at settlement amount

• Adjusted only for mortality

• Reduced by subsequent payments to the beneficiary not attributable to interest expense (if the obligation is reported at present value)

• Deferred inflow of resources for the government’s remainder interest

• Recognized as revenue at the term of the agreement

160

Government as intermediary (4/5)

• Application: government as lead interest beneficiary

• Deferred inflow of resources for the government’s lead interest

• Calculated at settlement amount

• Adjusted only for mortality

• Reduced by subsequent payments to the beneficiary not attributable to interest (if the deferred inflow is reported at present value)

• Liability to the beneficiary of the remainder interest

• Difference between asset and deferred inflow of resources for government’s lead interest

161

Government as intermediary (5/5)

• Life interests in real estate

• Government = remainder interest

• Asset recognized at time of donation

• Capital asset

• Investment

• Liability – obligation to sacrifice financial resources

• Insurance, maintenance, repairs (reduced as fulfilled)

• Deferred inflows of resources (2 separate items)

• Remainder interest

• Recognized as revenue at term of the agreement

• Donor’s ongoing right to use property

• Present value of estimated rent payments based on actual life expectancy (no subsequent adjustments)

• Amortized as revenue over term of the agreement

162

Third party as intermediary (1/2)

• Criteria for recognizing deferred inflow

• Government aware of agreement

• Measurable

• Government specified by name as beneficiary in legal document

• Unconditional beneficial interest

• Agreement irrevocable

• Intermediary without unilateral power to redirect the use of the resources to another beneficiary (variance power)

• Intermediary not under control of donor

• Intermediary’s approval not required for assignment of beneficial interest

• Actual attempt to assign beneficial interest would not invalidate that interest and thereby terminate the agreement

163

Third party as intermediary (2/2)

• Asset recognized at fair value of government’s beneficial interest

• Lead interest = deferred inflow reduced by periodic payments

• Remainder interest = deferred inflow eliminated at the term of the agreement

164

Effective date

• Fiscal year ending 12/31/17

• Earlier application encouraged

165

ACCOUNTING AND FINANCIAL REPORTING FOR PENSIONS PROVIDED THROUGH CERTAIN MULTIPLE-EMPLOYER DEFINED BENEFIT PENSION PLANS

Exposure draft - October 2015

166

Issue

• GASB 68 covers all employer pension benefits administered through a trust or equivalent arrangement

• Some multiple-employer plans that are used to provide benefits to government employees are not themselves state or local government plans

• Taft-Hartley plans and similar arrangements

• It may be difficult to obtain the necessary information to comply with GASB 68 if the government itself (or some combination of governments) is not the predominant employer

• Governments typically are only a small subset of all participating employers

167

Solution

• Exclude qualifying plans from the scope of GASB 68

• Mandate treatment similar to that used for employers participating in cost-sharing plans prior to GASB 68

• Report required employer contributions related to the period as pension expense/expenditure

• Report liability for deficiencies in required employer contributions

168

Criteria for exemption

• Cost-sharing defined benefit pension plan

• Not a state or local government pension plan

• Serves nongovernmental employees

• Governments are not predominant

169

Note disclosure (1/2)

• Identification

• Name of the pension plan

• Entity that administers

• Cost-sharing plan meeting criteria

• Whether publicly available financial report and how to obtain

• Brief description of benefit terms

• Number of employees covered

• Types of benefits provided

• Authority for establishing/amending

170

Note disclosure (2/2)

• Contribution requirements

• Basis for determining employer contributions

• Authority for establishing/amending

• Required contribution rates for employer and employees

• Employer’s required contributions in dollars

• Expiration date(s) of collective-bargaining agreement(s) requiring contributions

• Minimum contributions required for future periods by the collective-bargaining agreement(s), statutory obligations, or other contractual obligations

• Withdrawal provisions

• Balance of payables resulting from unpaid contributions

171

Required supplementary information (RSI) • 10-year schedule of employer’s required contributions

• Notes: information about factors that significantly affect trends in the amounts reported

172

Effective date

• Fiscal year ending 12/31/16

173

Question 27

Investments now reported at amortized cost by 2a7-like pools and their participants will likely be reported at fair value in the future.

A. True

B. False

174

Question 28

The calculation of which of the following ignores “shortening features”?

A. Weighted average maturity

B. Weighted average life

C. Both A and B

D. None of the above

175

Question 29

Qualifying pools that initially elect to report investments at amortized cost, rather than fair value, will be precluded from later changing to fair value reporting.

A. True

B. False

176

Question 30

Which of the following would permanently preclude an investment pool from using amortized cost to value of investments?

A. Significant noncompliance with portfolio requirements in the current period

B. Significant noncompliance with portfolio requirements in the previous period

C. Voluntary use of fair value reporting in previous period

D. All of the above

E. None of the above

177

Question 31

The GASB plans to expand the criteria for blending to encompass not-for-profit entities for which the primary government functions as the sole corporate member.

A. True

B. False

178

Question 32

When should an irrevocable split-interest agreement be recognized by a government that is functioning as the intermediary?

A. When the agreement is executed

B. When the assets are received

C. Both A and B

179

Question 33

When does the government recognize revenue if it is a remainder interest beneficiary?

A. Immediately

B. Over the life of the agreement

C. At the term of the agreement

180

Question 34

Sometimes a government in a split-interest agreement may need to recognize two separate deferred inflows of resources.

A. True

B. False

181

Question 35

When a third-party functions as the intermediary for a split-interest agreement, the government should recognize its beneficial interest as soon as it becomes aware of the agreement.

A. True

B. False

182

Question 36

How should a governmental employer that participates in a Taft-Hartley plan in which governmental employers are not predominant recognize pension expense?

A. Required employer contributions made during the period

B. Required employer contributions related to the period

C. Proportionate share of total contributions by participating employers

183

FORTHCOMING EXPOSURE DRAFTS

Financial Reporting for Fiduciary Responsibilities

Asset Retirement Obligations

Leases

184

FINANCIAL REPORTING FOR FIDUCIARY RESPONSIBILITIES

Forthcoming GASB ED (scheduled for 4Q15)

185

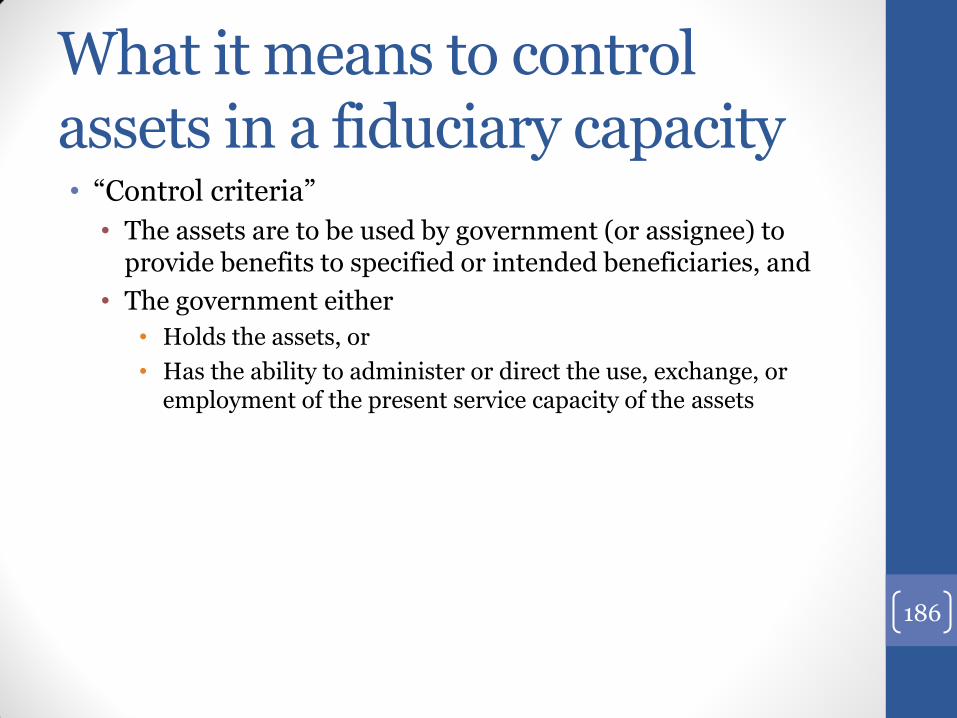

What it means to control assets in a fiduciary capacity • “Control criteria”

• The assets are to be used by government (or assignee) to provide benefits to specified or intended beneficiaries, and

• The government either

• Holds the assets, or

• Has the ability to administer or direct the use, exchange, or employment of the present service capacity of the assets

186

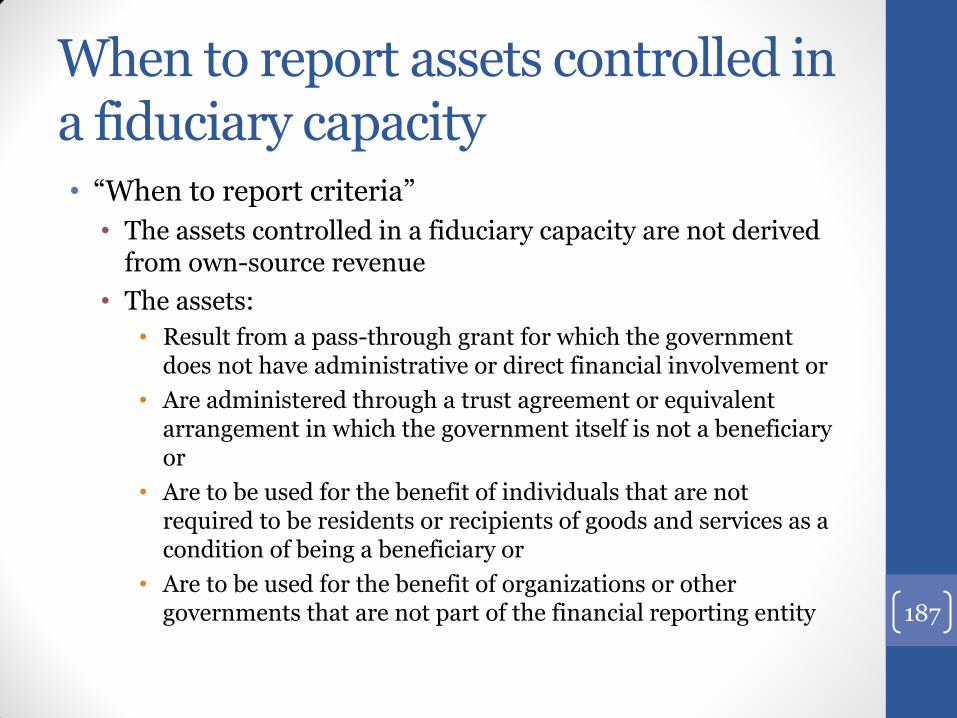

When to report assets controlled in a fiduciary capacity • “When to report criteria”

• The assets controlled in a fiduciary capacity are not derived from own-source revenue

• The assets:

• Result from a pass-through grant for which the government does not have administrative or direct financial involvement or

• Are administered through a trust agreement or equivalent arrangement in which the government itself is not a beneficiary or

• Are to be used for the benefit of individuals that are not required to be residents or recipients of goods and services as a condition of being a beneficiary or

• Are to be used for the benefit of organizations or other governments that are not part of the financial reporting entity 187

When component units are fiduciary in nature • Ignore “control criteria”

• Apply “when to report” criteria

188

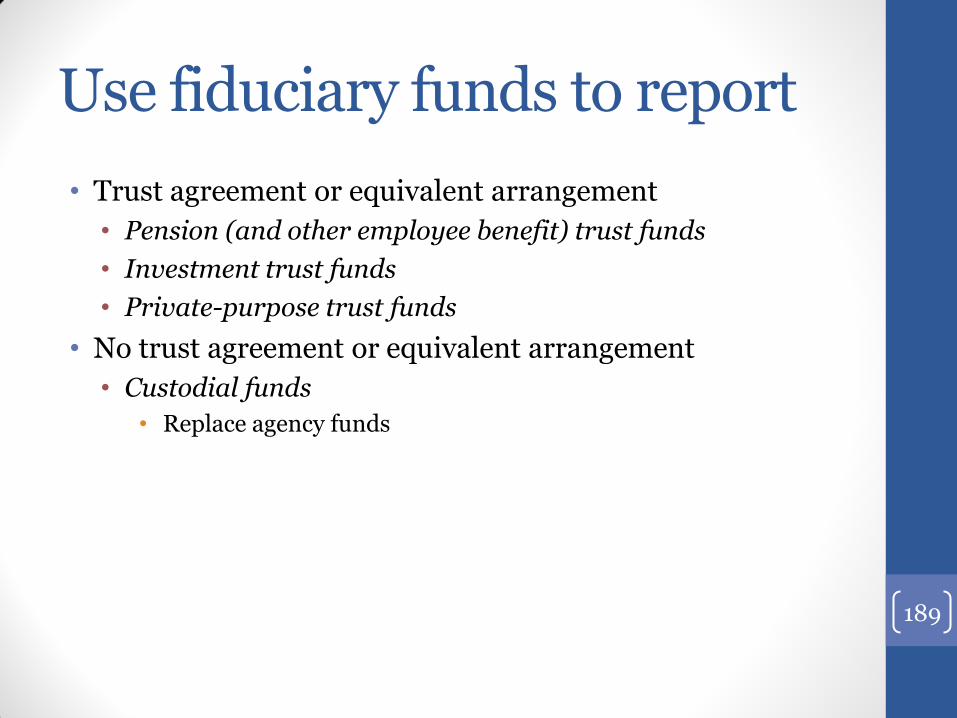

Use fiduciary funds to report

• Trust agreement or equivalent arrangement

• Pension (and other employee benefit) trust funds

• Investment trust funds

• Private-purpose trust funds

• No trust agreement or equivalent arrangement

• Custodial funds

• Replace agency funds

189

Display issues

• Recognize liability when event has occurred that compels the government to disburse fiduciary resources

• Level of detail

• Additions disaggregated by source

• Separately display investment income and investment costs

• Deductions disaggregated by type

• Separately display administrative costs

• Exception: custodial fund that holds resources ≤ 3 months

• May report a single amount in the statement of changes in fiduciary net position for each of the following:

• Additions

• Deductions

• Totals must be described in a way that indicates the nature of the resource flows

190

Other issues

• Business-type activities should report fiduciary funds in their stand-alone financial statements

• Reporting fiduciary-type component units

• Include combined information of component unit(s) with subcomponent units

• Aggregate and combine with the primary government’s fiduciary fund financial statements by fund type

191

ASSET RETIREMENT OBLIGATIONS

Forthcoming exposure draft (scheduled for 4Q15)

192

Definitions

• Retirement of a capital asset

• The other-than-temporary removal of a capital asset from service

• Includes: sale, abandonment, recycling, other type of disposal

• Excludes temporary idling

• Asset retirement obligation (ARO)

• A legal obligation associated with the retirement of a capital asset

• Based on applicable federal, state, or local laws or regulations that have been approved as of the balance sheet date, regardless of their effective date

• Excludes constructive obligations

193

Scope includes

• Legal obligations associated with the retirement of a tangible capital asset that result from

• Acquisition, construction, or development

• Normal operation (including resulting environmental remediation liabilities)

• Disposal of a replaced part

• Obligations of a lessor of a leased property that meet the criteria of an ARO

194

Scope excludes

• Items covered by GASB 49 or GASB 18

• Pollution prevention or control obligations for current operations, fines, penalties, and other nonremediation outlays excluded from GASB 49

• Obligations that arise solely from a plan to sell or otherwise dispose of a capital asset

• Activities necessary to prepare an asset for alternative use

• Obligations of a lessee

• Obligation for asbestos removal that results from other-than-normal operation

• Obligations associated with maintenance

• Cost of replacement part for a capital asset

• Conditional obligations 195

Dual recognition criteria

• External obligating event

• Imposes legal obligation to retire a capital asset

• Approval of laws or regulations

• Creation of a contract

• Court judgment

• Internal obligating event

• Specific trigger

• Occurrence of contamination

• Acquisition

• Capital asset permanently abandoned before being placed into operation

• Placing capital asset into operation

• Placing capital asset into operation + consuming a portion of its usable service capacity in normal operations

196

Measurement (1/2)

• General principle

• Measure ARO liability when

• Incurred

• Reasonably estimable

• Measure based on current costs (not present value)

• Best-estimate approach that takes into account all available evidence (including the likelihood of potential cash flows)

• Probability weighting of potential outcomes if sufficient evidence is available or can be obtained at reasonable cost

• Recognition

• Initially deferred outflow

• Expense over useful life of the asset

197

Measurement (2/2)

• Subsequent measurement of ARO liability

• Periodically evaluate factors that could affect outflows

• General inflation/deflation

• Price increases/reductions for specific outlay elements

• Changes in technology

• Changes in laws, regulations, contracts, or court judgments

• Changes in the type of equipment, facilities, and services that will be used

• Remeasure only if a change

• Prior to retirement?

• Adjust deferred outflow

• Expense over remaining life of asset

• Subsequent to retirement?

• Immediate recognition

198

Fiscal funding and assurance provisions • Do not net liability and assets restricted for repayment

• Disclose assets restricted for repayment in notes (if not displayed on face)

• Exclude costs from calculation of the ARO liability

199

Note disclosure

• General description of: 1) the ARO; 2) the associate capital assets; 3) the source of the ARO (law, regulation, contract, court judgment)

• Amount and cause of each significant increase/decrease in the estimated ARO liability during the reporting period

• Estimated remaining useful life of associate capital assets

• How financial assurance requirements are being met (if applicable)

• Methods and assumptions used to determine liability and

• Fact that all or a portion of an ARO was not recognized because it was not measurable (if applicable)

200

Timeline

• ED

• 4th Quarter 2015

• Final statement

• 4th Quarter 2016

201

LEASES

Forthcoming GASB ED (scheduled for 1Q16)

202

Definition

• A contract that conveys the right to use a nonfinancial asset (the underlying asset) for a period of time in an exchange or exchange-like transaction

• Exclude

• Contracts that transfer ownership of the underlying asset

• Leases of intangible assets

• Contracts for exploration/exploitation of non-regenerative natural resources

• Leases of biological assets, including timber

• Contracts that meet the definition of a service concession arrangement (GASB Statement No. 60)

203

Lease term

• Period during which a lessee has a noncancellable right to use an underlying asset (the noncancellable period) plus (if applicable) the lessee’s optional extension of the lease when exercise of that option is reasonably certain

204

Lessee accounting • Recognize a lease liability at the beginning of a lease

(unless short term)

• Present value of certain payments to be made over the lease term

• Recognize an intangible asset for the right to use the capital asset

• Value of the lease liability plus

• Payments to lessor at or before lease begins

• Initial direct costs necessary to place the asset into service

• Recognize interest expense/expenditure on the lease liability

• Recognize amortization expense for the asset 205

Lessee disclosures

• Certain existing disclosures continue, for example

• Debt service to maturity

• Amount of lease assets reported

• New disclosures, for example

• How variable payments not included in the liability are determined

• Period expense for variable payments not previously in the liability

• Period expense for other payments, such as residual value guarantees not previously in the liability

206

Lessor accounting

• Recognize a lease receivable at the beginning of a lease (unless short term)

• Present value of certain lease payments to be received over the lease term

• Reduced by uncollectibles

• Continue to report the capital asset underlying the lease

• Recognize a deferred inflow of resources

• The lease receivable plus

• Payments received at or before lease begins that relate to future periods (rent for the lease’s last month)

• Recognize interest revenue on the lease receivable

• Recognize lease revenue from the deferred inflow

207

Lessor disclosures

• Examples of such disclosures include

• Conditions for determining variable lease payments (if any)

• Period amount for lease revenues (including interest)

• Schedule of future lease payments

• Each of the next five years

• At a minimum, five-year increments thereafter

208

Short-term leases • Definition

• A lease that, at its beginning, has a maximum possible term under the contract of 12 months or less

• Includes options to extend

• Lessee

• Recognize lease payments as expenses/expenditures primarily on the payment terms of the contract

• Lessor

• Recognize lease payments as revenue primarily on the terms of the contract

209

Summary of key changes (1/2)

• No distinction capital lease vs. operating lease*

• Distinguish long-term leases vs. short-term leases

• Lease accounting only if ownership does not ultimately transfer to the lessee

• Otherwise a financed sale/purchase of an asset

*This represents an important divergence from the direction the FASB is

currently taking in its own lease project.

210

Summary of key changes (2/2)

• Lessees report intangible asset for right to use underlying capital asset

• Not the underlying asset itself

• Lessors continue to report underlying capital asset and a lease receivable

211

Question 37

The GASB proposes to reduce the number of fiduciary fund types from 4 to 3.

A. True

B. False

212

Question 38

Additions and deductions may each be reported as a single line item if certain conditions are met in which of the following fund types?

A. Private-purpose trust funds

B. Pension (and other employee benefits) trust funds

C. Investment trust funds

D. Custodial funds

E. All the above

F. None of the above

213

Question 39

Asset retirement obligations include

A. Legal obligations

B. Constructive obligations

C. Both A and B

214

Question 40

Obligating events for asset retirement obligations include

A. External events

B. Internal events

C. Both A and B

215

Question 41

Which of the following statements would be true for the new lease accounting now under consideration?

A. The current distinction between capital leases and operating leases would no longer apply

B. Lessors would report two assets rather than one

C. Lessees would report an intangible asset rather than a capital asset

D. All of the above

E. None of the above

216

OTHER TOPICS

GASB Technical Plan

Reporting Deficiencies

217

GASB TECHNICAL PLAN

Other topics

218

GASB Technical Plan

• Current Technical Agenda

• Conceptual Framework

• Major Projects

• Practice Issues

• Pre-Agenda Research

• Monitoring Activities

• Potential Projects

219

CURRENT TECHNICAL AGENDA

Conceptual Framework

Major Projects

Practice Issues

220

Conceptual Framework

• Recognition

• ITC/PV – 2Q19

• Progress to date

• Preliminary Views (PV) – 6/11

• Whether and when information should be reported in financial statements

• Measurement focus basis of accounting

• Key issue: governmental funds

• Current status

• On hold since 1/12 pending reexamination of the financial reporting model

221

Major Projects

• Asset Retirement Obligations

• ED – 4Q15

• Fiduciary Responsibilities

• ED – 4Q15

• Leases

• ED – 1Q16

• Financial Reporting Model

• ITC/PV – 4Q16/2Q18

• ED – 4Q19

222

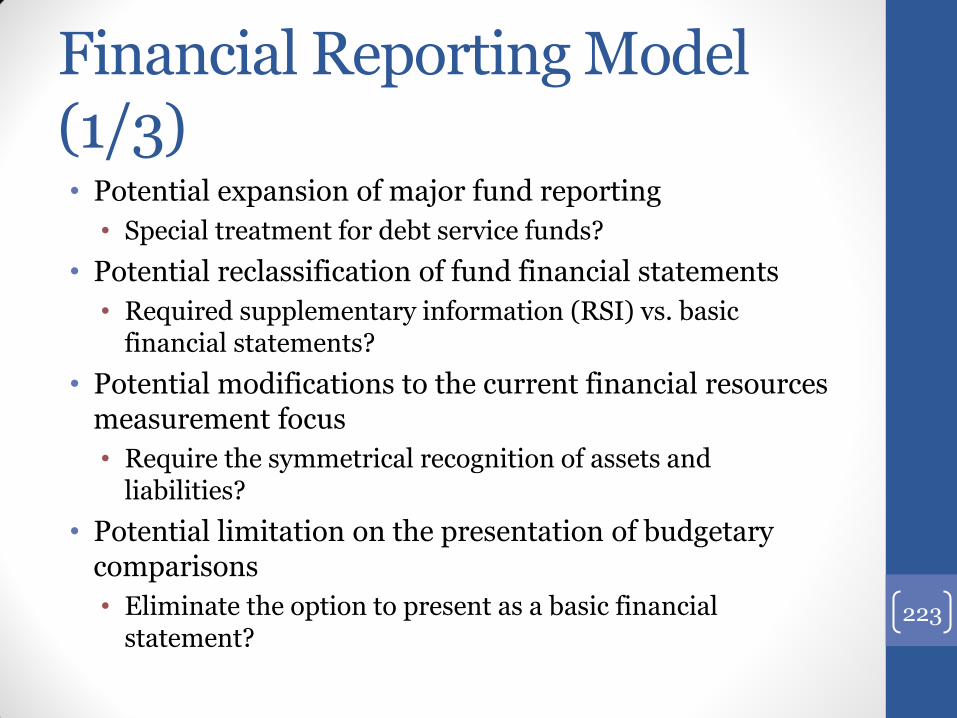

Financial Reporting Model (1/3) • Potential expansion of major fund reporting

• Special treatment for debt service funds?

• Potential reclassification of fund financial statements

• Required supplementary information (RSI) vs. basic financial statements?

• Potential modifications to the current financial resources measurement focus

• Require the symmetrical recognition of assets and liabilities?

• Potential limitation on the presentation of budgetary comparisons

• Eliminate the option to present as a basic financial statement?

223

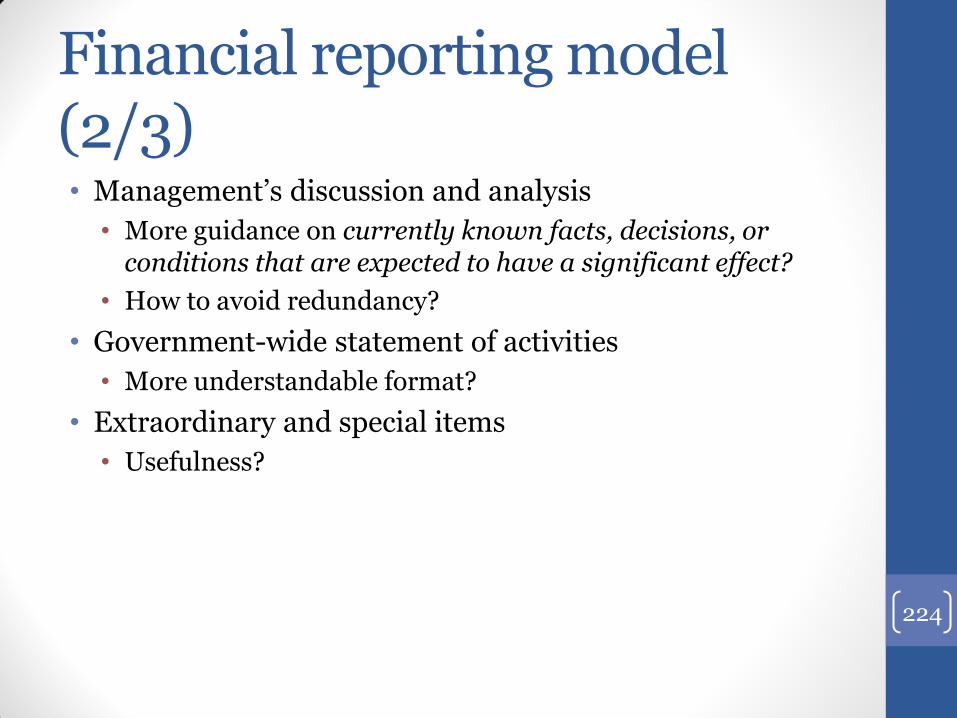

Financial reporting model (2/3) • Management’s discussion and analysis

• More guidance on currently known facts, decisions, or conditions that are expected to have a significant effect?

• How to avoid redundancy?

• Government-wide statement of activities

• More understandable format?

• Extraordinary and special items

• Usefulness?

224

Financial reporting model (3/3) • Government-wide statement of cash flows

• Add as basic financial statement?

• Operating vs. non-operating revenues and expenses

• Provide authoritative guidance/definition?

• Maintain distinction?

• Segment reporting

• Level of detail needed for note disclosure?

225

Practice Issues

• Blending requirements for certain component units

• Final statement – 1Q16

• External investment pools

• Final statement – 4Q15

• Implementation Guidance

• Update – 3Q15

• Irrevocable split-interest agreements

• Final statement 1Q16

• Debt refundings with existing resources

• ED – 3Q16

• Pension benefit issues

• ED – 4Q15 226

Debt refundings with existing resources • Major issues

• Should defeasance be permitted if only existing resources are placed into escrow?

• Should the amount deferred be limited to the portion financed with borrowed resources?

• Should there be additional disclosure?

227

Pension benefit issues

• Implementation issues for GASB 67 and GASB 68

• Issues already considered

• Covered-employee payroll vs. covered payroll

• Tentative agreement – focus on covered payroll

• Employer-paid member contributions

• Tentative agreement

• Should not be considered when determining a cost-sharing employer’s proportion of collective liability/expense for all participating employers.

• Additional pension expense should be recognized for employer-paid member contributions not included as part of salary expense.

• Deviation from Actuarial Standards of Practice (ASOPs)

• Tentative agreement - not consistent with GASB standards in regard to the assumptions to be used for determining the total pension liability.

228

Pre-Agenda Research

• Debt disclosures, including direct borrowing

• Going concern disclosures – reexamination

• Revenue recognition for exchange and exchange-like transactions

229

Debt disclosures

• What transactions constitute “debt” for debt-related disclosures?

• What information about a government’s outstanding debt

• Is essential to users?

• Is currently available?

• Existing note disclosure

• Other sources

• What specific user needs exist regarding covenants in debt transactions?

• Acceleration clauses?

• Subordination clauses? 230

Going-concern disclosures

• Are the current going-concern indicators appropriate for state and local governments?

• Even under severe financial stress, few governments cease to operate even when encountering such indicators

• What other criteria might better achieve the objective of disclosing severe financial stress uncertainties?

• What information do financial statement users need with respect to severe financial stress uncertainties?

231

Revenue recognition – exchange and exchange-like transactions • What issues have arisen in practice?

• Criteria to differentiate

• Exchange-like transactions

• Nonexchange transactions

• What kind of single-element and multiple-element transactions generally occur for state and local governments? How are they accounted for?

• What specific user needs exist regarding revenue recognition?

232

Monitoring Activities

• Electronic Financial Reporting

• Emerging Accounting Issues

• Pension and OPEB Implementation

233

Potential Projects (1/2)

• Emissions Trading (Carbon Credits)

• Equity Interests in Component Units—Acquisition When Legal Separation Is Maintained

• Exchange and Exchange-Like Financial Guarantees

• Financial Transactions with Characteristics of Both Loans and Grants

• Impairments of Assets Other Than Capital Assets

234

Potential Projects (2/2)

• In-Kind Contributions

• Interim Financial Reporting

• Popular Reporting

• Present Value

• Preservation Method

• Reporting Unit Presentations

• Social Security Disclosures

235

Financial projections - update

• Project on hold since 2012

• April 2015 – GASB removed project from current technical agenda

236

REPORTING DEFICIENCIES

Other topics

237

Component unit disclosures

• Incorrect description of blending criteria

• Governing body substantively the same no longer sufficient (GASB 61)

• Also need

• Financial benefit/burden or

• Operational responsibility

• Ability to impose will irrelevant

• Reference to fiscal dependency

• No evidence of financial benefit/burden (also required)

• Criterion itself applied incorrectly

• Failure to identify financial benefit/burden

238

Net investment in capital assets calculation • Common errors

• Including debt whose proceeds have not been spent

• Should be reported in the same category as the unspent proceeds

• Excluding special assessment debt that has been issued for capital purposes

• Excluding deferred outflows/inflows from refundings

• Excluding retainage payable

239

Budgetary reporting

• Budgetary comparisons inappropriately presented for

• Nonmajor special revenue funds

• Debt service funds

• Capital projects funds

• Supplementary budgetary reporting fails to include nonmajor funds (new submissions)