Embed Size (px)

Citation preview

2014 Professional Ethics & Conduct

Accounting

It Is Not Just An Occupation;

It Is A Profession.

A Profession Is:

A Group’s Collective Effort

To Pursue A Learned Art

With A Common Calling

To Act In The Spirit Of Public Service

For The End Good Of The Public.

2

The Accounting Profession

A discipline that is practiced by a credentialed individual with a complex body of knowledge.

Has standards for admission.

Is vital to continuing social organization.

Requires public confidence.

Failure on the part of one

diminishes the whole

3

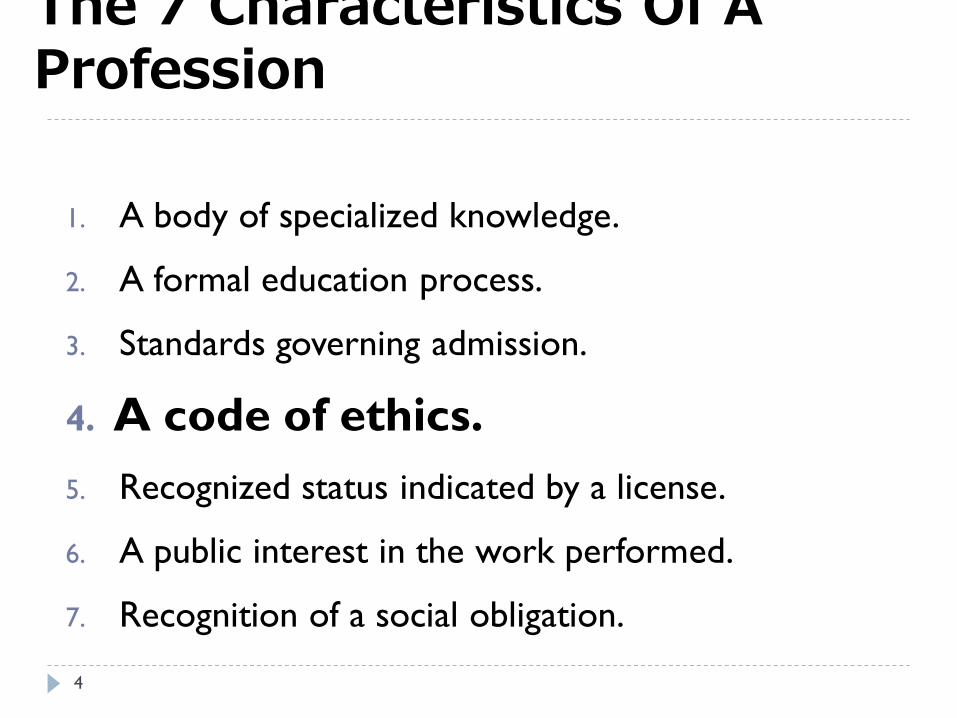

The 7 Characteristics Of A Profession

1. A body of specialized knowledge.

2. A formal education process.

3. Standards governing admission.

4. A code of ethics.

5. Recognized status indicated by a license.

6. A public interest in the work performed.

7. Recognition of a social obligation.

4

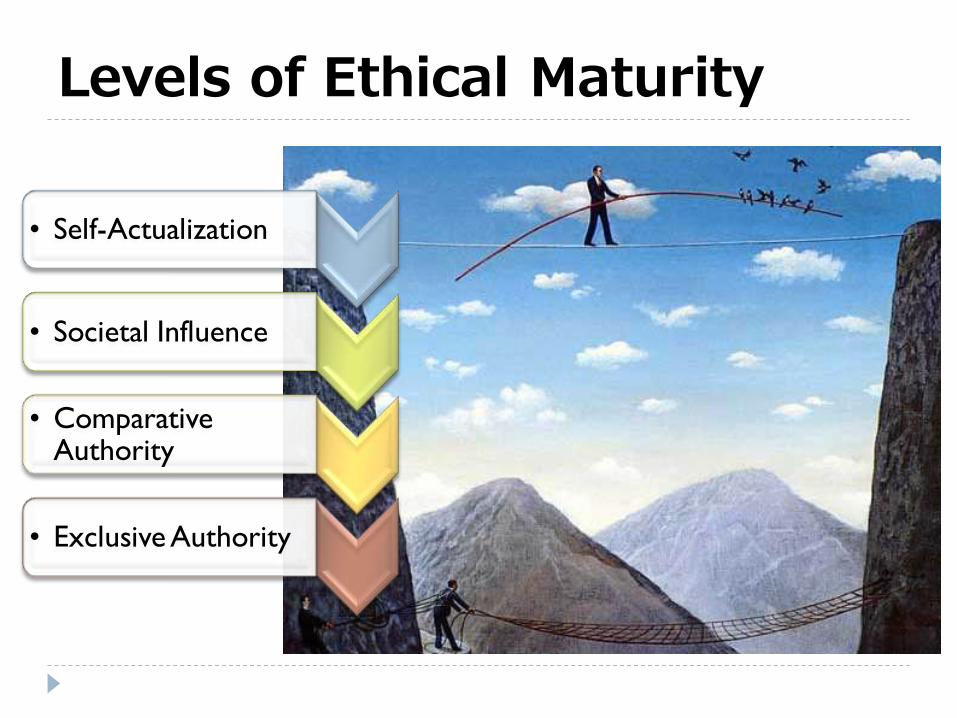

Levels of Ethical Maturity

• Self-Actualization

• Societal Influence

• Comparative Authority

• Exclusive Authority

What do you see?

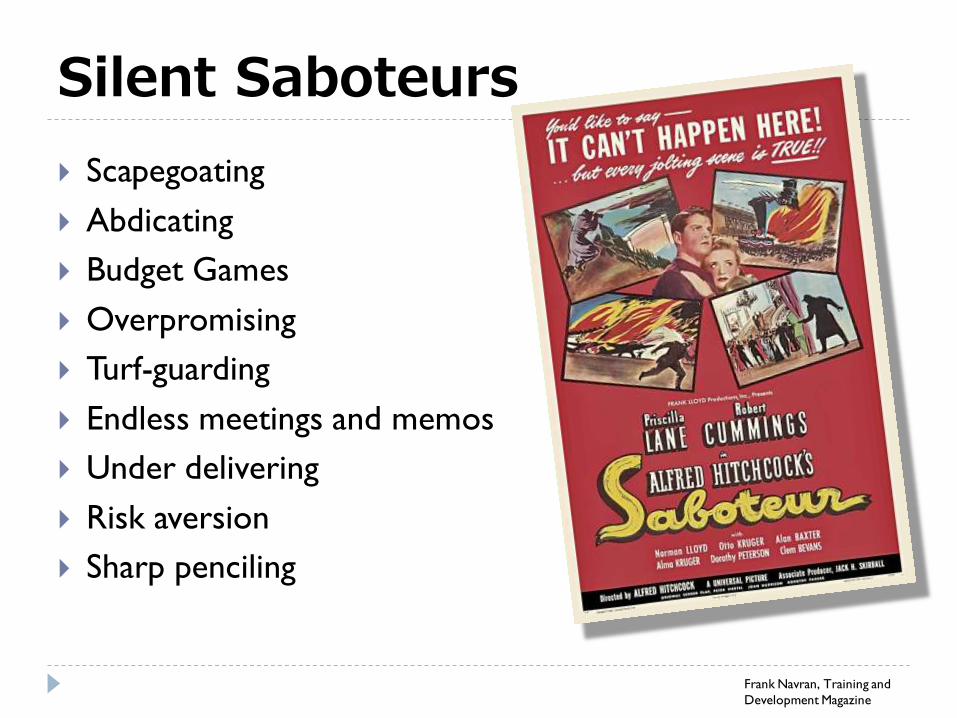

Silent Saboteurs

Scapegoating

Abdicating

Budget Games

Overpromising

Turf-guarding

Endless meetings and memos

Under delivering

Risk aversion

Sharp penciling

Frank Navran, Training and

Development Magazine

More “Silent Saboteurs”

I’ve Got a Secret

Credit Taking

Lack of Recognition

Attention to Detail

Let People Know

Nursing a Grievance

Smoke, but No Fire

Emergency, or Just Poor Planning

Robin Hood

Pushing the Limits

Frank Navran, Training and

Development Magazine

Sweat the Small Stuff

A recent company shared from their ethics compliance

office that the most complaints result from an employee

observing another employee’s improper use of the

company’s assets. The thoughts are:

It’s only a pen

Nobody will care

Everybody does it

It doesn’t belong to anybody

Nobody will find out

Ethical issues that should concern us the most are the ones

we face everyday.

Is it ever OK to lie?

If you were interviewing

someone for a job and it

was brought up that he lied

to his current employer

about where he was, would

it affect your views on his

trustworthiness?

The Ultimatum Game

What time is it?

Time to Decide: Why are We Here?

Can accounting ethics be taught?

OR

Can we teach accountants to be ethical?

13

To contact:

N.C. State Board of Certified Public

Accountant Examiners

www.nccpaboard.gov

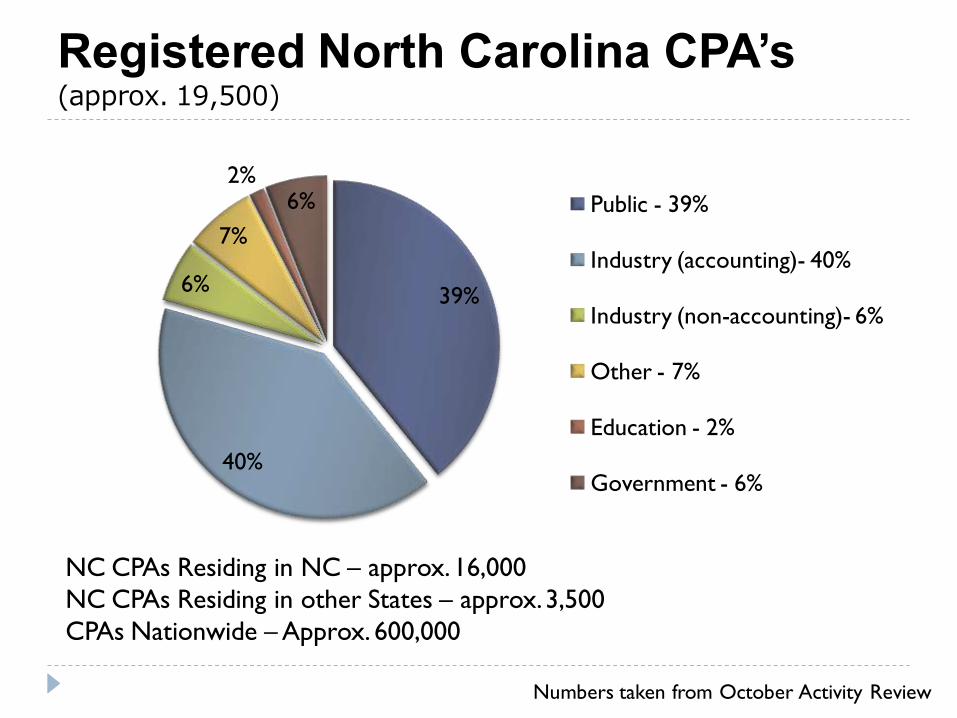

Registered North Carolina CPA’s (approx. 19,500)

39%

40%

6%

7%

2% 6% Public - 39%

Industry (accounting)- 40%

Industry (non-accounting)- 6%

Other - 7%

Education - 2%

Government - 6%

NC CPAs Residing in NC – approx. 16,000

NC CPAs Residing in other States – approx. 3,500

CPAs Nationwide – Approx. 600,000

Numbers taken from October Activity Review

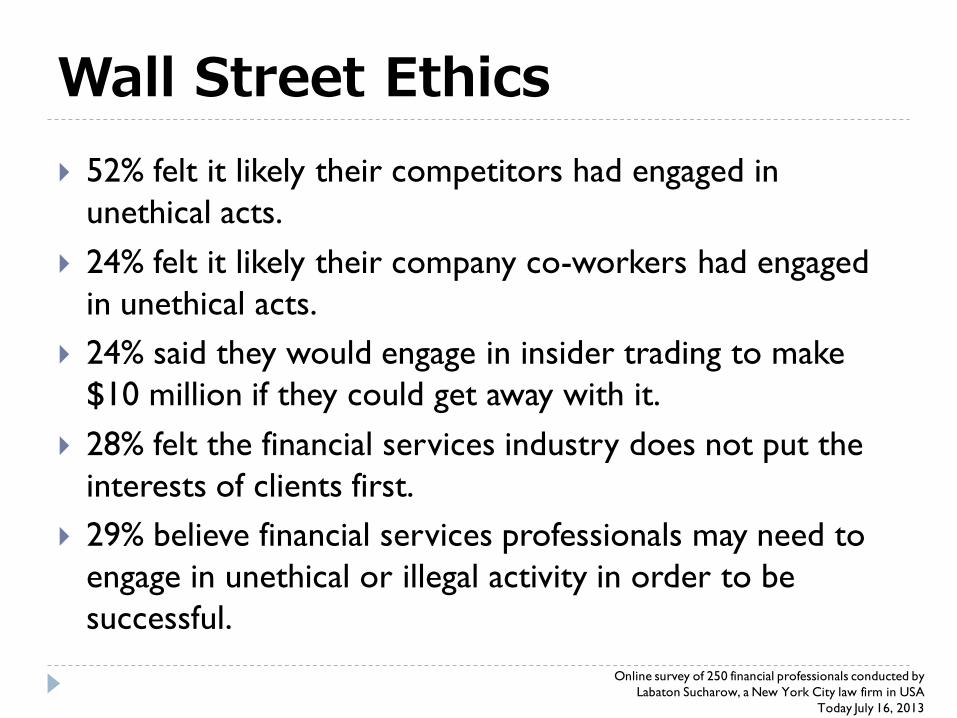

Wall Street Ethics

52% felt it likely their competitors had engaged in

unethical acts.

24% felt it likely their company co-workers had engaged

in unethical acts.

24% said they would engage in insider trading to make

$10 million if they could get away with it.

28% felt the financial services industry does not put the

interests of clients first.

29% believe financial services professionals may need to

engage in unethical or illegal activity in order to be

successful.

Online survey of 250 financial professionals conducted by

Labaton Sucharow, a New York City law firm in USA

Today July 16, 2013

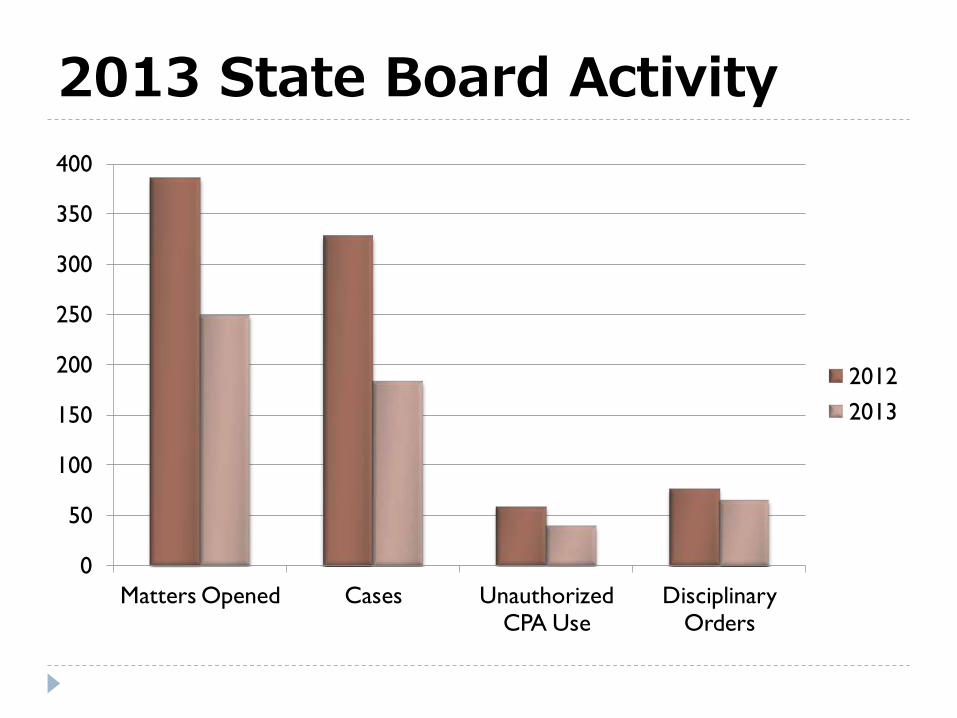

2013 State Board Activity

0

50

100

150

200

250

300

350

400

Matters Opened Cases Unauthorized CPA Use

Disciplinary Orders

2012

2013

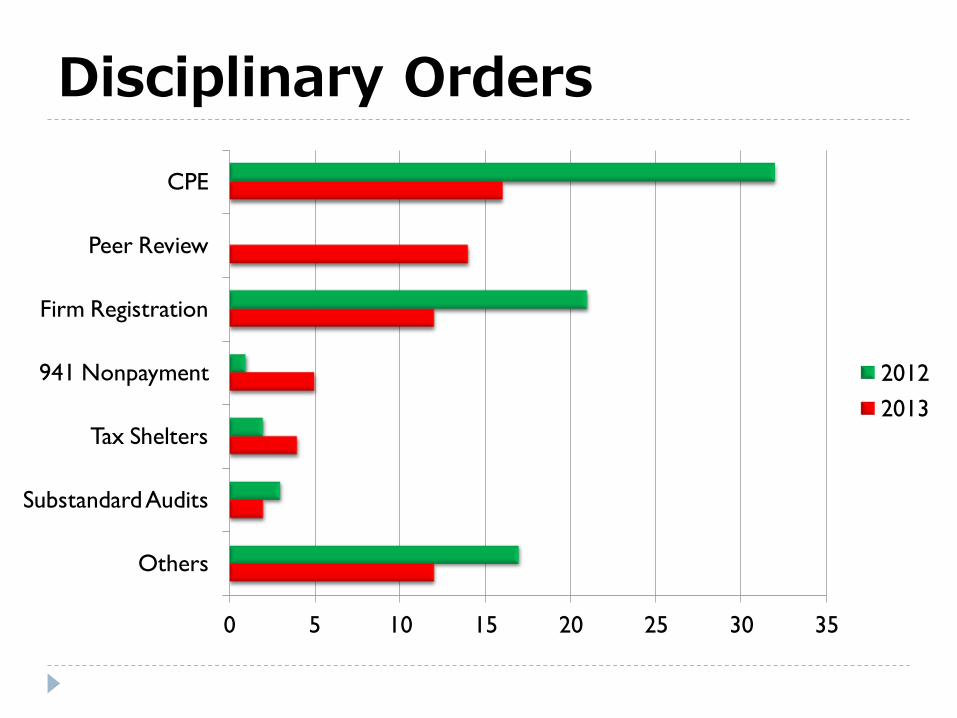

Disciplinary Orders

Others

Substandard Audits

Tax Shelters

941 Nonpayment

Firm Registration

Peer Review

CPE

0 5 10 15 20 25 30 35

2012

2013

Time for an obvious question

Is CPE important?

Is CPE Important?

An integral part of professional development

Does little to improve professional competency

Too expensive

Doesn’t apply to my job

Not enough time to meet the requirement each year

The requirements are too confusing

So this happened…

Do you take CPE seriously?

Reading the paper

Texting

Checking email

Shopping online

Playing games

Preparing a tax return

Reviewing workpapers

Knitting

Taking online CPE during live class

Time for another obvious question

Why do we have a CPE requirement?

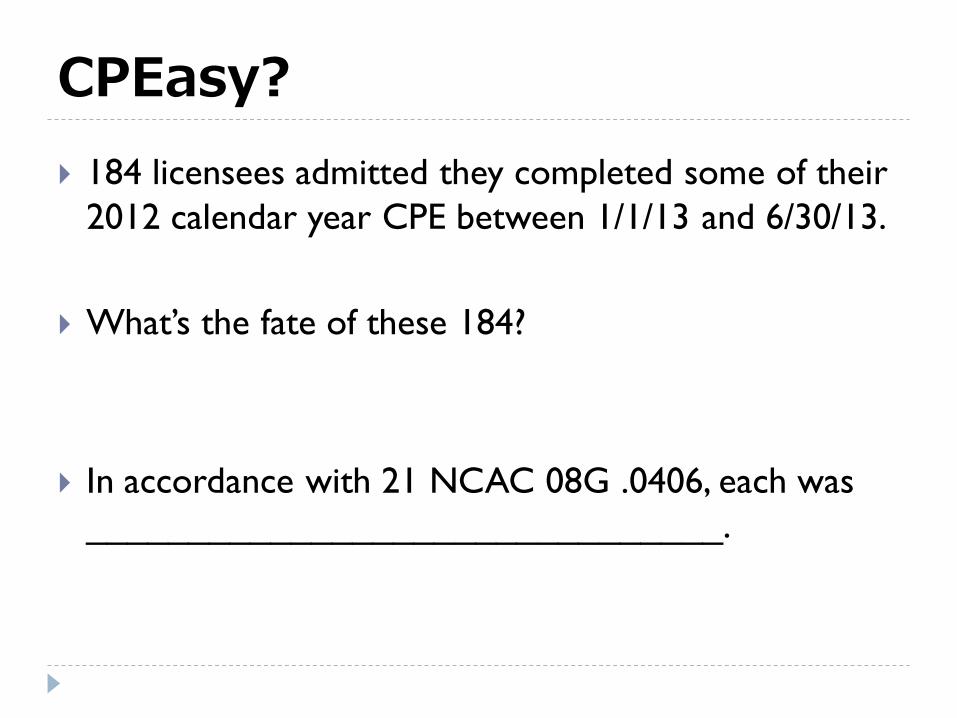

CPEasy?

184 licensees admitted they completed some of their

2012 calendar year CPE between 1/1/13 and 6/30/13.

What’s the fate of these 184?

In accordance with 21 NCAC 08G .0406, each was

_______________________________.

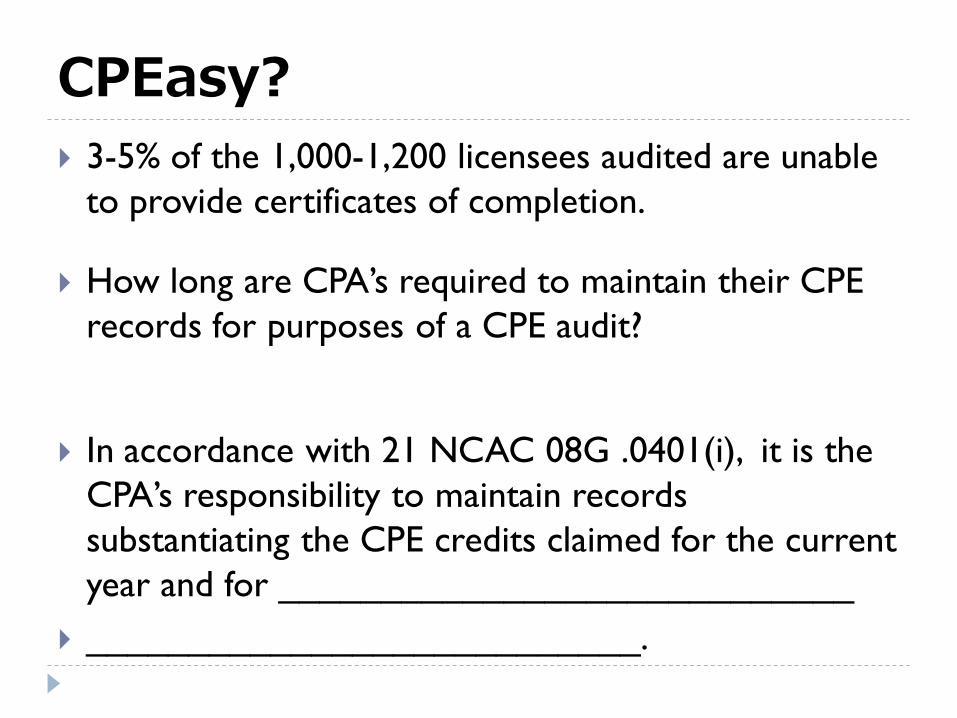

CPEasy?

3-5% of the 1,000-1,200 licensees audited are unable

to provide certificates of completion.

How long are CPA’s required to maintain their CPE

records for purposes of a CPE audit?

In accordance with 21 NCAC 08G .0401(i), it is the

CPA’s responsibility to maintain records

substantiating the CPE credits claimed for the current

year and for ____________________________

___________________________.

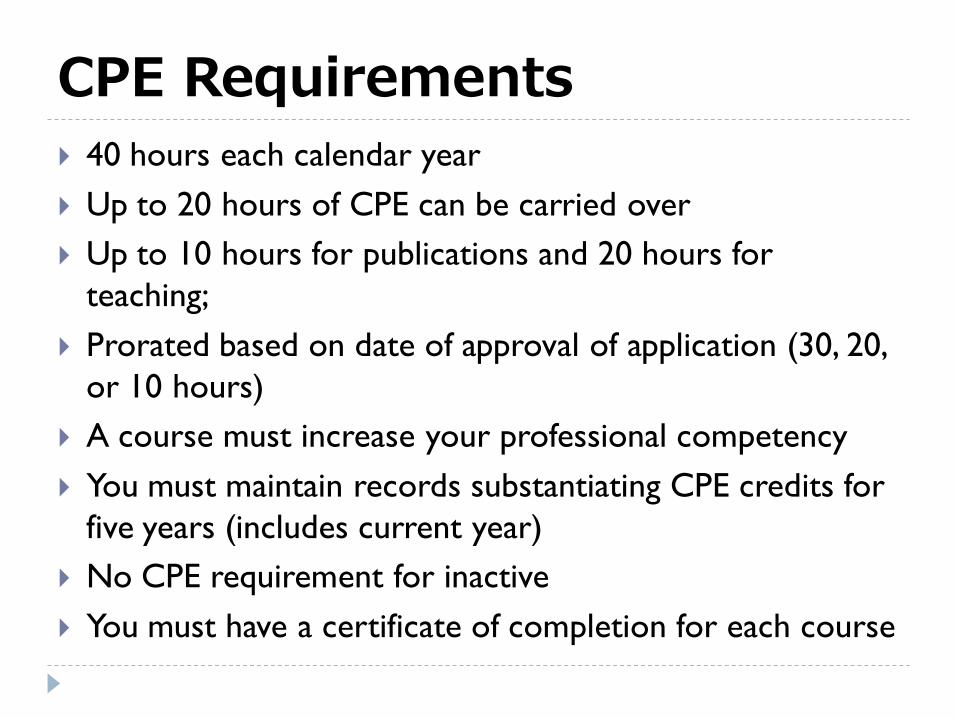

CPE Requirements

40 hours each calendar year

Up to 20 hours of CPE can be carried over

Up to 10 hours for publications and 20 hours for

teaching;

Prorated based on date of approval of application (30, 20,

or 10 hours)

A course must increase your professional competency

You must maintain records substantiating CPE credits for

five years (includes current year)

No CPE requirement for inactive

You must have a certificate of completion for each course

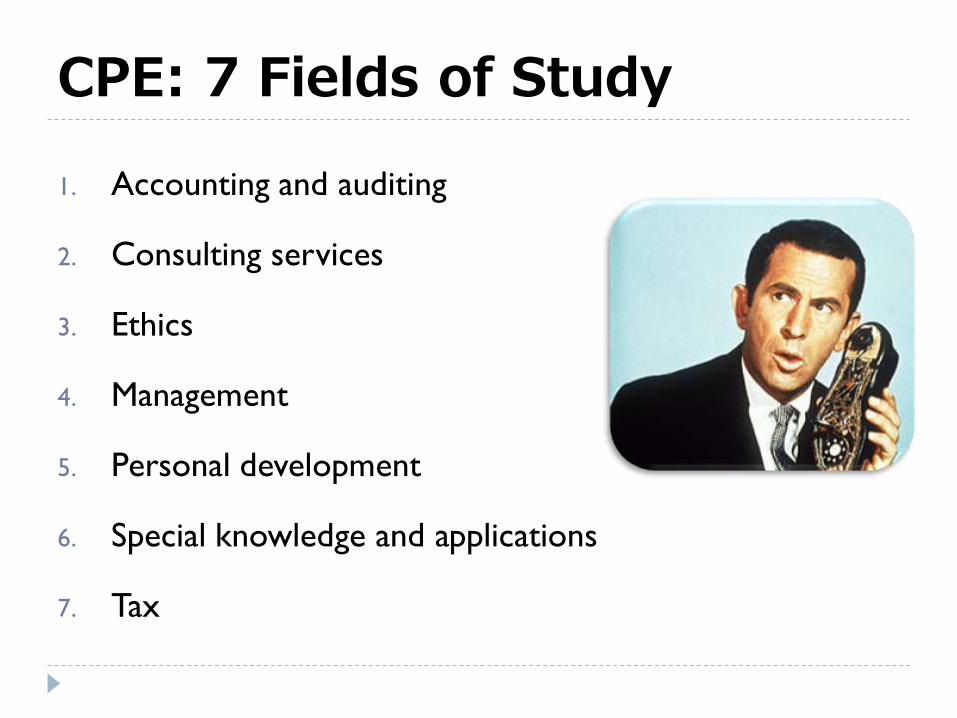

CPE: 7 Fields of Study

1. Accounting and auditing

2. Consulting services

3. Ethics

4. Management

5. Personal development

6. Special knowledge and applications

7. Tax

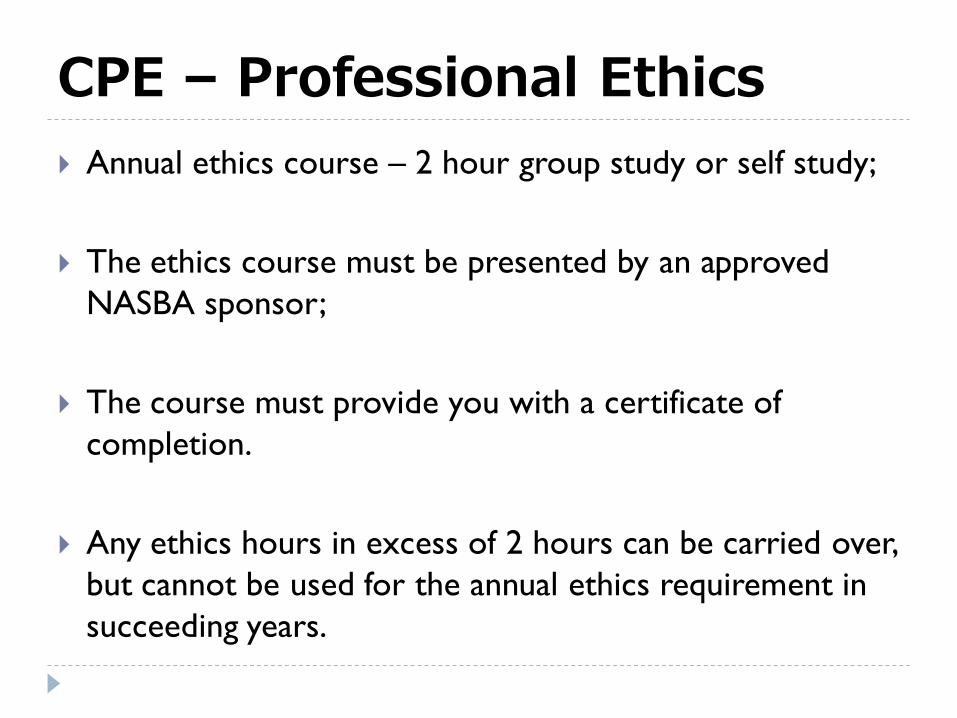

CPE – Professional Ethics

Annual ethics course – 2 hour group study or self study;

The ethics course must be presented by an approved

NASBA sponsor;

The course must provide you with a certificate of

completion.

Any ethics hours in excess of 2 hours can be carried over,

but cannot be used for the annual ethics requirement in

succeeding years.

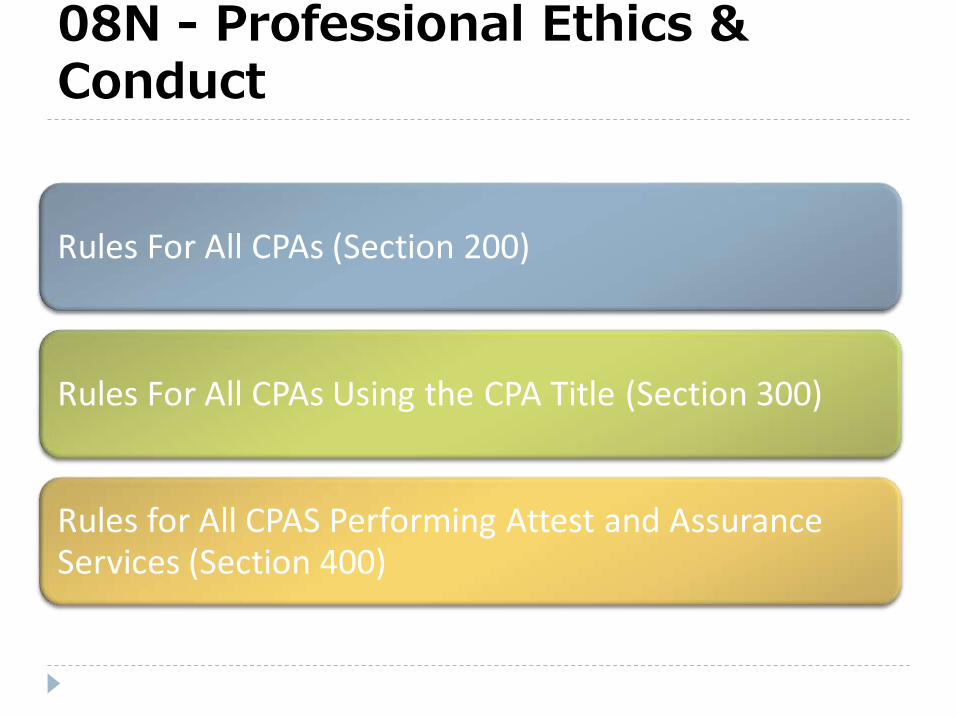

08N - Professional Ethics & Conduct

Rules For All CPAs (Section 200)

Rules For All CPAs Using the CPA Title (Section 300)

Rules for All CPAS Performing Attest and Assurance Services (Section 400)

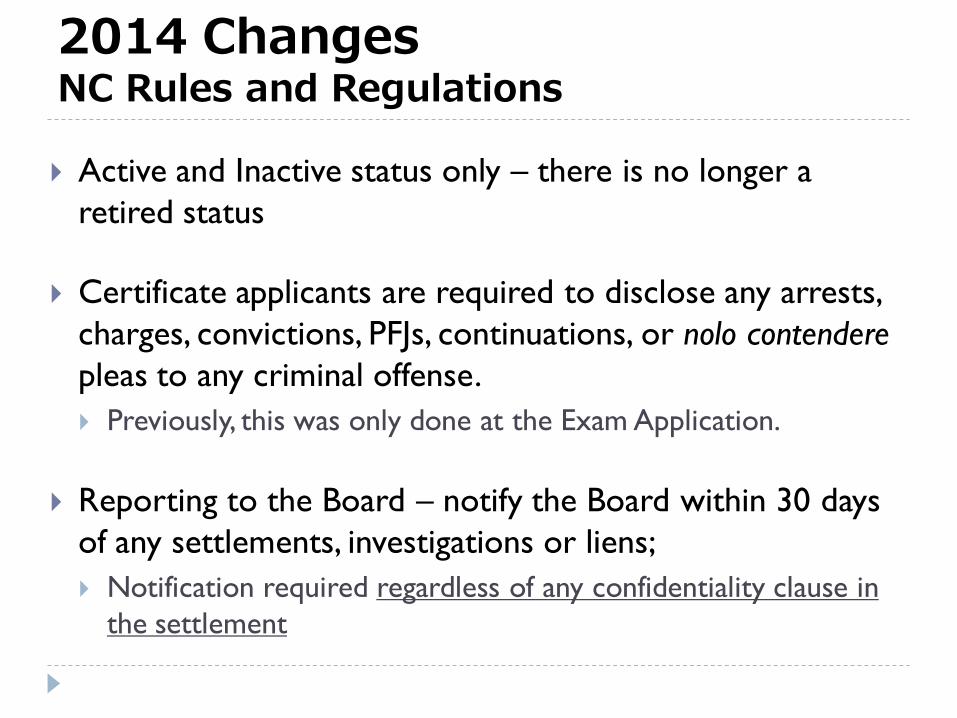

2014 Changes NC Rules and Regulations

Active and Inactive status only – there is no longer a

retired status

Certificate applicants are required to disclose any arrests,

charges, convictions, PFJs, continuations, or nolo contendere

pleas to any criminal offense.

Previously, this was only done at the Exam Application.

Reporting to the Board – notify the Board within 30 days

of any settlements, investigations or liens;

Notification required regardless of any confidentiality clause in

the settlement

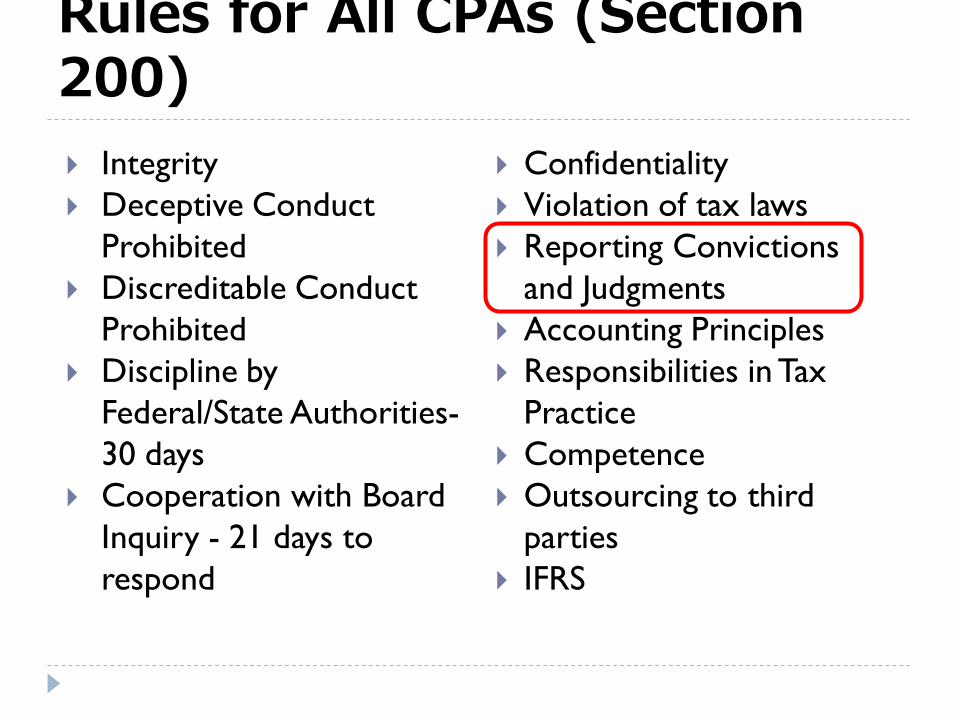

Rules for All CPAs (Section 200)

Integrity

Deceptive Conduct

Prohibited

Discreditable Conduct

Prohibited

Discipline by

Federal/State Authorities-

30 days

Cooperation with Board

Inquiry - 21 days to

respond

Confidentiality

Violation of tax laws

Reporting Convictions

and Judgments

Accounting Principles

Responsibilities in Tax

Practice

Competence

Outsourcing to third

parties

IFRS

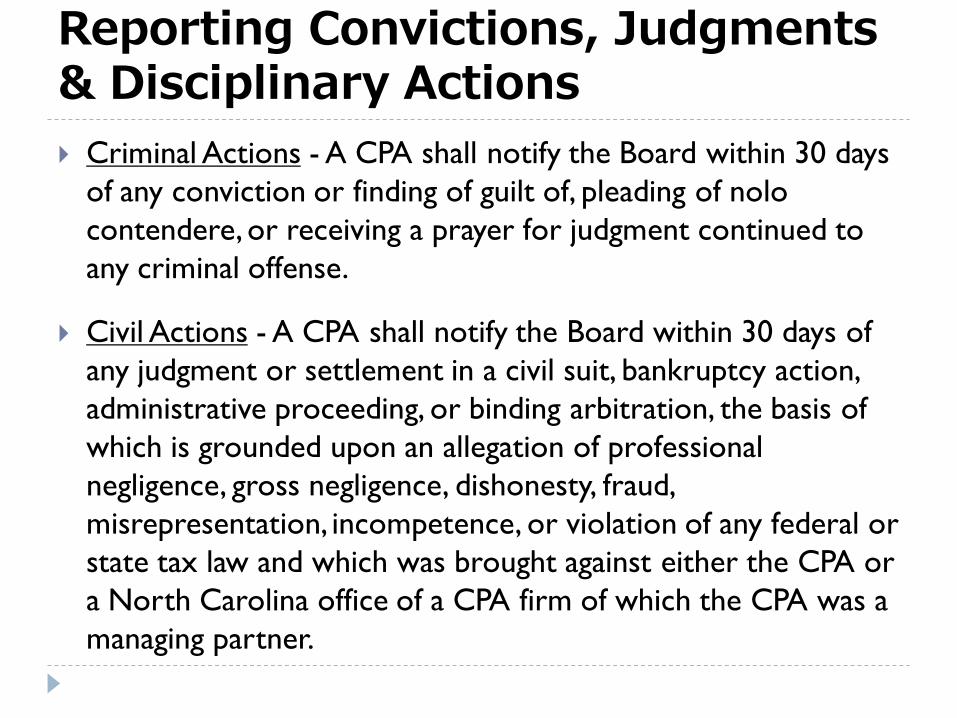

Reporting Convictions, Judgments & Disciplinary Actions

Criminal Actions - A CPA shall notify the Board within 30 days

of any conviction or finding of guilt of, pleading of nolo

contendere, or receiving a prayer for judgment continued to

any criminal offense.

Civil Actions - A CPA shall notify the Board within 30 days of

any judgment or settlement in a civil suit, bankruptcy action,

administrative proceeding, or binding arbitration, the basis of

which is grounded upon an allegation of professional

negligence, gross negligence, dishonesty, fraud,

misrepresentation, incompetence, or violation of any federal or

state tax law and which was brought against either the CPA or

a North Carolina office of a CPA firm of which the CPA was a

managing partner.

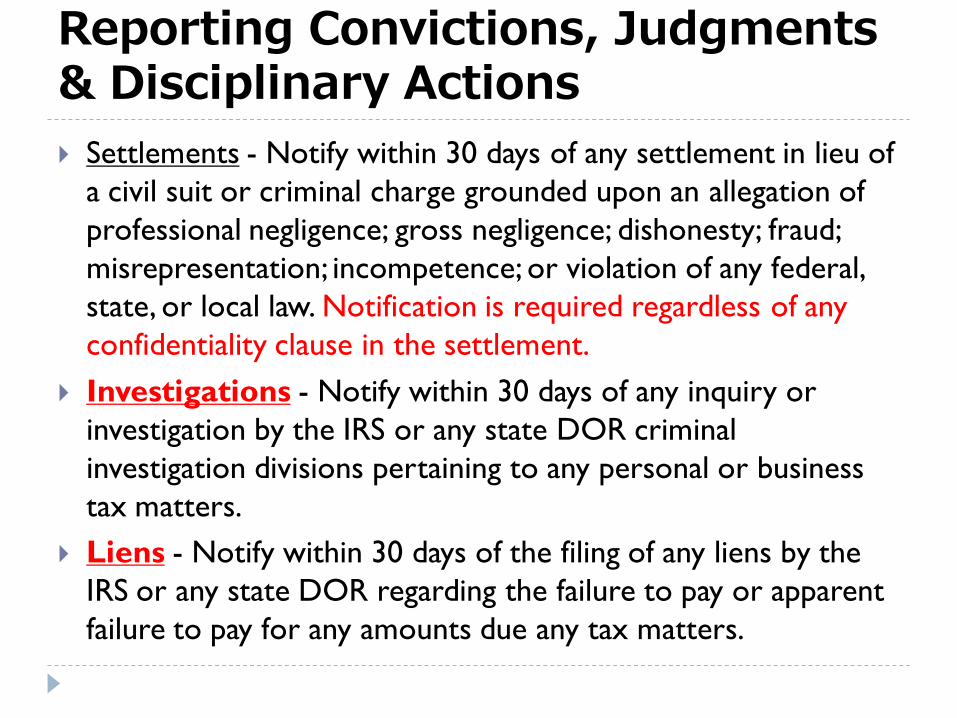

Reporting Convictions, Judgments & Disciplinary Actions

Settlements - Notify within 30 days of any settlement in lieu of

a civil suit or criminal charge grounded upon an allegation of

professional negligence; gross negligence; dishonesty; fraud;

misrepresentation; incompetence; or violation of any federal,

state, or local law. Notification is required regardless of any

confidentiality clause in the settlement.

Investigations - Notify within 30 days of any inquiry or

investigation by the IRS or any state DOR criminal

investigation divisions pertaining to any personal or business

tax matters.

Liens - Notify within 30 days of the filing of any liens by the

IRS or any state DOR regarding the failure to pay or apparent

failure to pay for any amounts due any tax matters.

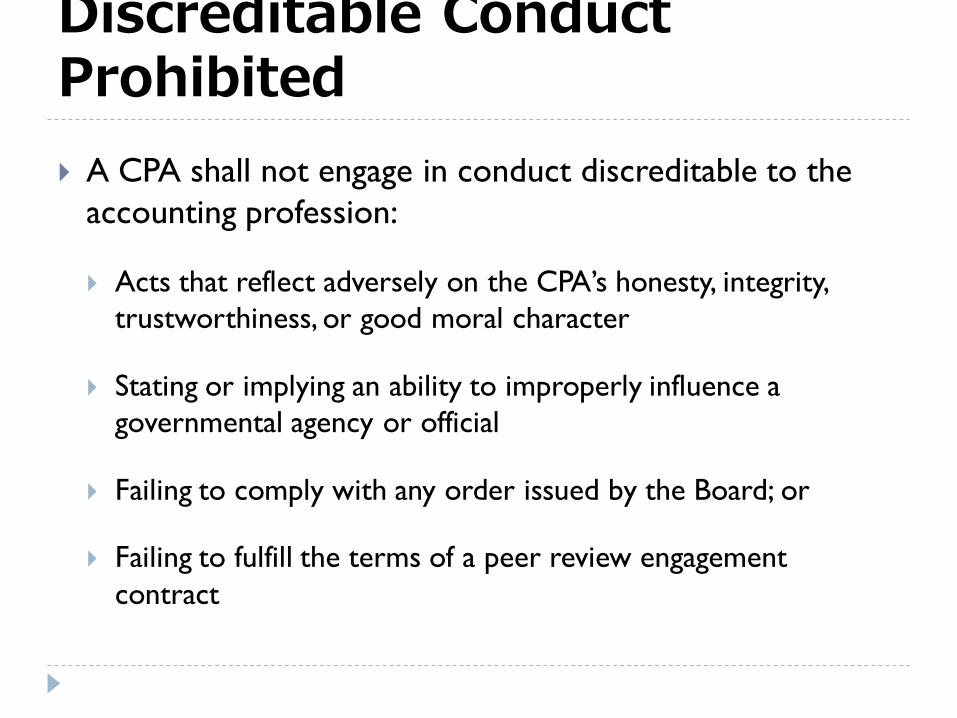

Discreditable Conduct Prohibited

A CPA shall not engage in conduct discreditable to the

accounting profession:

Acts that reflect adversely on the CPA’s honesty, integrity,

trustworthiness, or good moral character

Stating or implying an ability to improperly influence a

governmental agency or official

Failing to comply with any order issued by the Board; or

Failing to fulfill the terms of a peer review engagement

contract

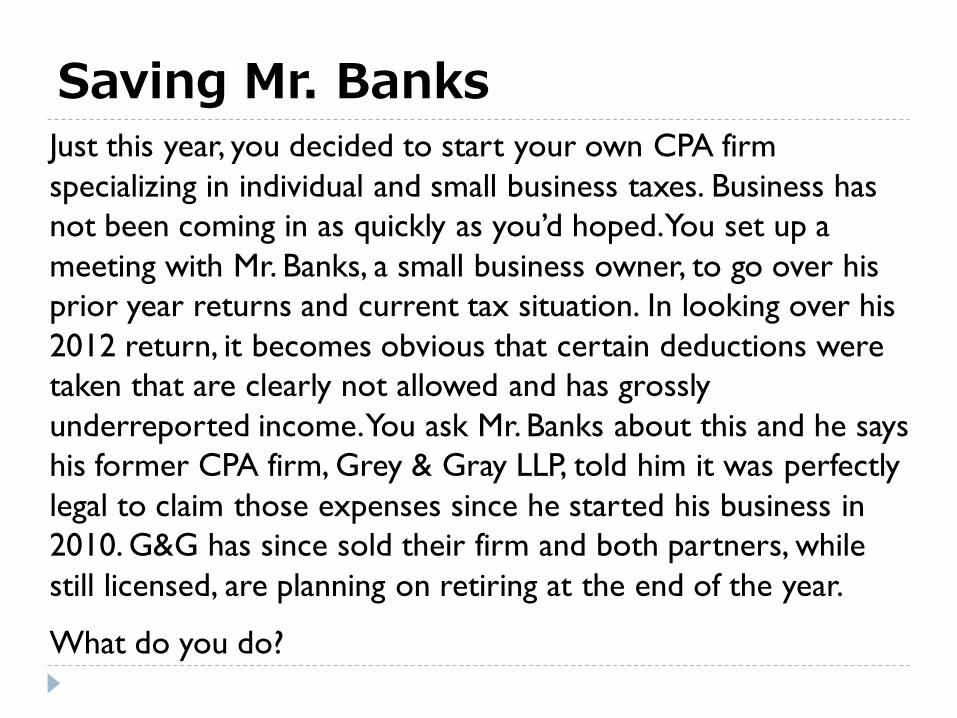

Saving Mr. Banks Just this year, you decided to start your own CPA firm

specializing in individual and small business taxes. Business has

not been coming in as quickly as you’d hoped. You set up a

meeting with Mr. Banks, a small business owner, to go over his

prior year returns and current tax situation. In looking over his

2012 return, it becomes obvious that certain deductions were

taken that are clearly not allowed and has grossly

underreported income. You ask Mr. Banks about this and he says

his former CPA firm, Grey & Gray LLP, told him it was perfectly

legal to claim those expenses since he started his business in

2010. G&G has since sold their firm and both partners, while

still licensed, are planning on retiring at the end of the year.

What do you do?

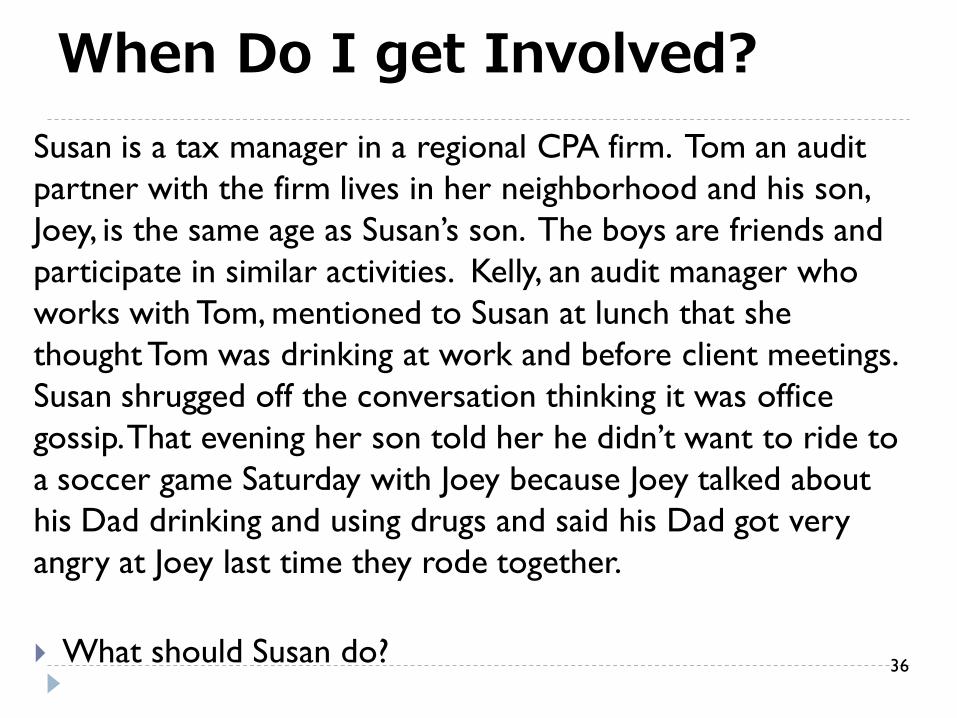

When Do I get Involved?

Susan is a tax manager in a regional CPA firm. Tom an audit

partner with the firm lives in her neighborhood and his son,

Joey, is the same age as Susan’s son. The boys are friends and

participate in similar activities. Kelly, an audit manager who

works with Tom, mentioned to Susan at lunch that she

thought Tom was drinking at work and before client meetings.

Susan shrugged off the conversation thinking it was office

gossip. That evening her son told her he didn’t want to ride to

a soccer game Saturday with Joey because Joey talked about

his Dad drinking and using drugs and said his Dad got very

angry at Joey last time they rode together.

What should Susan do? 36

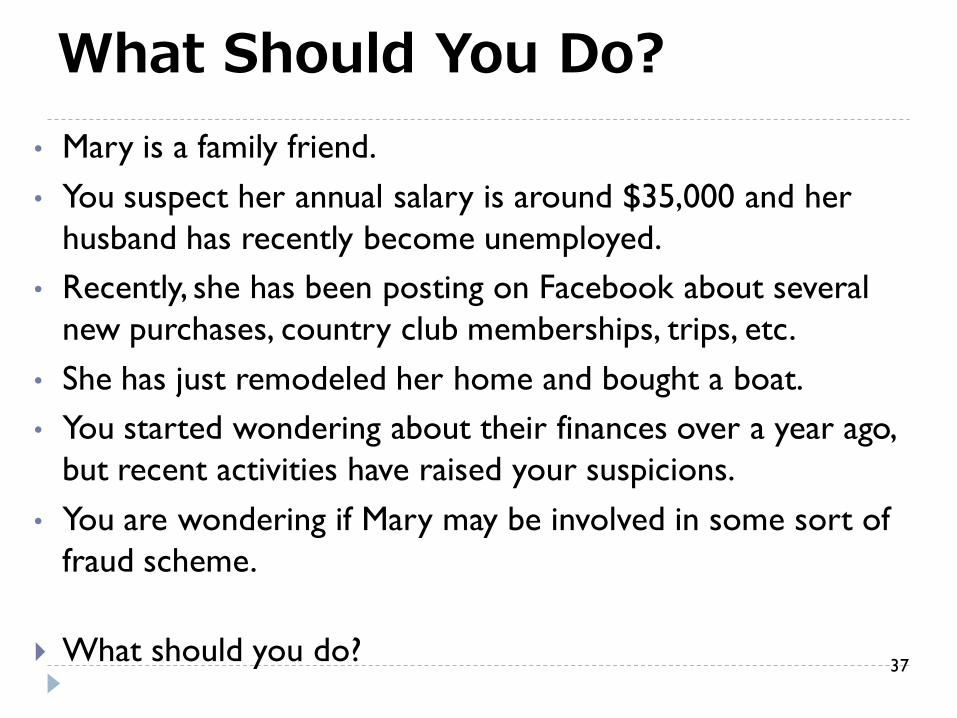

What Should You Do?

• Mary is a family friend.

• You suspect her annual salary is around $35,000 and her

husband has recently become unemployed.

• Recently, she has been posting on Facebook about several

new purchases, country club memberships, trips, etc.

• She has just remodeled her home and bought a boat.

• You started wondering about their finances over a year ago,

but recent activities have raised your suspicions.

• You are wondering if Mary may be involved in some sort of

fraud scheme.

What should you do? 37

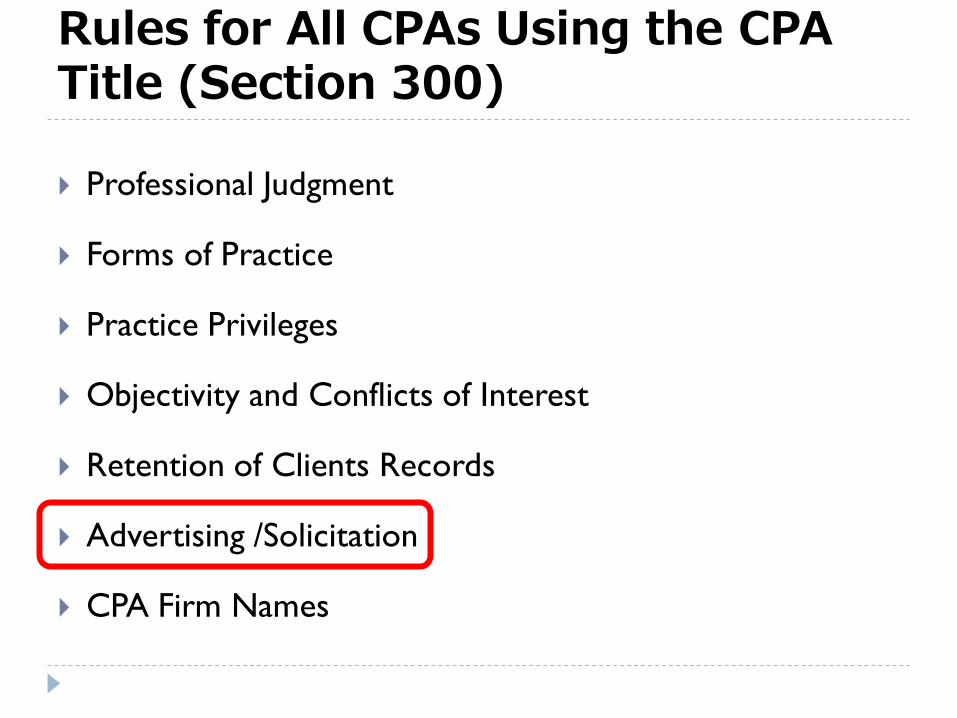

Rules for All CPAs Using the CPA Title (Section 300)

Professional Judgment

Forms of Practice

Practice Privileges

Objectivity and Conflicts of Interest

Retention of Clients Records

Advertising /Solicitation

CPA Firm Names

Advertising vs. Networking

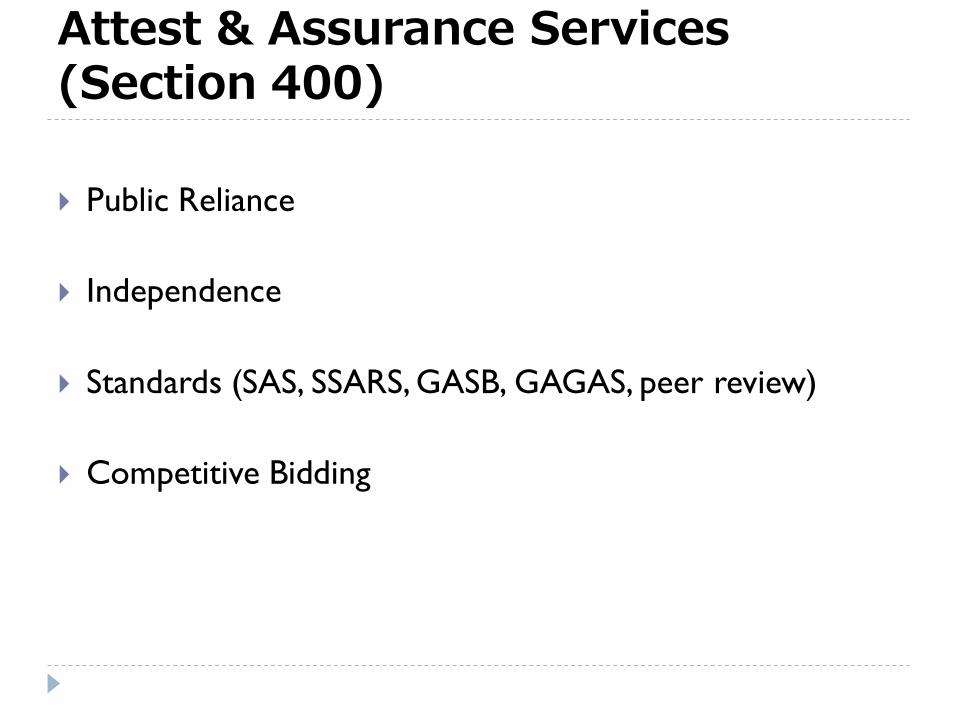

Rules for All CPAs Performing Attest & Assurance Services (Section 400)

Public Reliance

Independence

Standards (SAS, SSARS, GASB, GAGAS, peer review)

Competitive Bidding

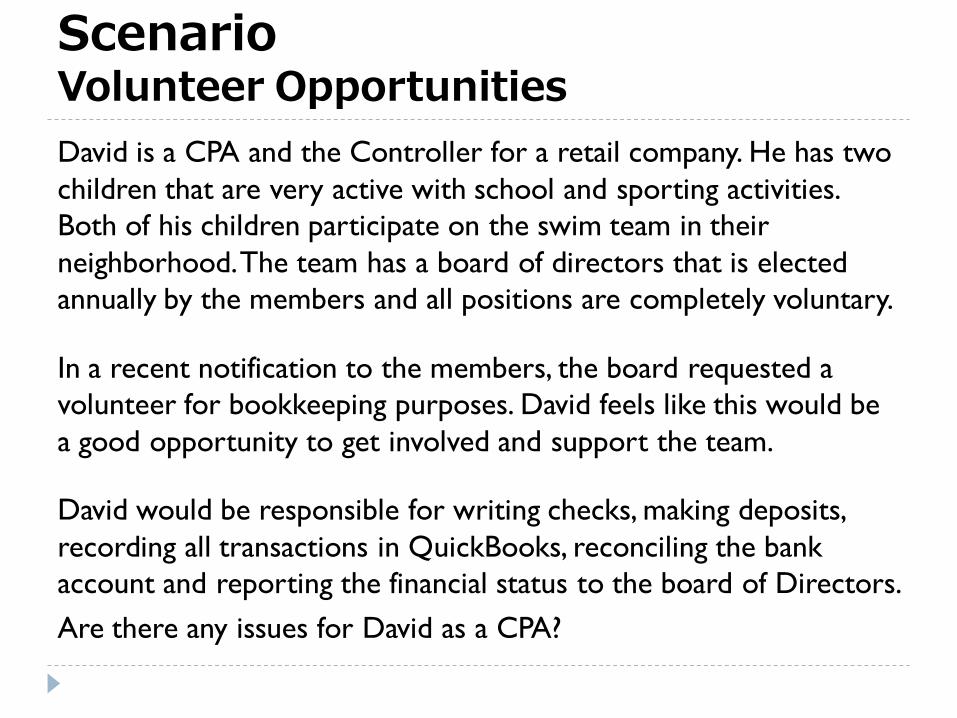

Scenario Volunteer Opportunities

David is a CPA and the Controller for a retail company. He has two

children that are very active with school and sporting activities.

Both of his children participate on the swim team in their

neighborhood. The team has a board of directors that is elected

annually by the members and all positions are completely voluntary.

In a recent notification to the members, the board requested a

volunteer for bookkeeping purposes. David feels like this would be

a good opportunity to get involved and support the team.

David would be responsible for writing checks, making deposits,

recording all transactions in QuickBooks, reconciling the bank

account and reporting the financial status to the board of Directors.

Are there any issues for David as a CPA?

Scenario Serving on a Board of Directors

What are the duties?

Are the Duties Heightened for CPAs?

Typical Claims Brought against Board Members

What are the Risks?

How Can the Risks be Mitigated?

What are the Key Steps to Consider before Accepting?

Are you a robot?

Are you a

robot?

2013 National Business Ethics Survey

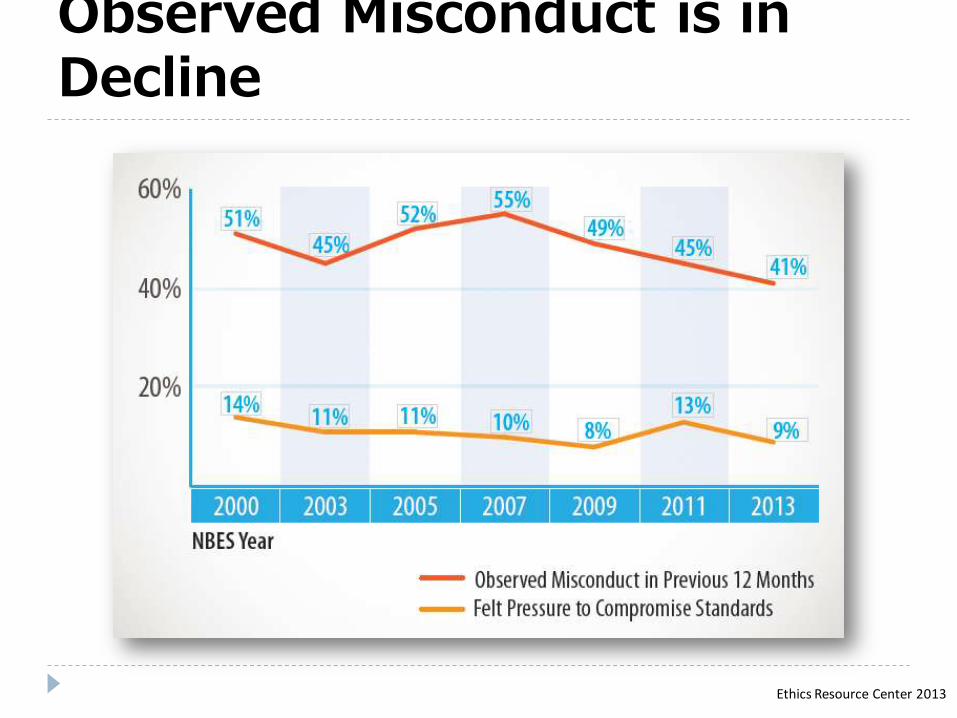

Observed Misconduct is in Decline

Ethics Resource Center 2013

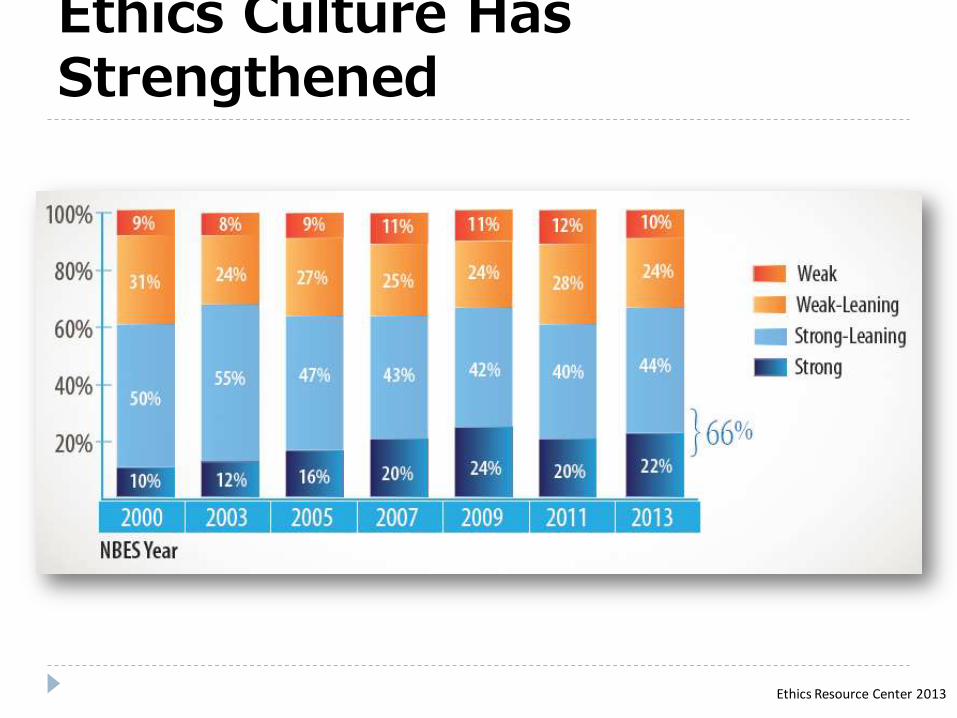

Ethics Culture Has Strengthened

Ethics Resource Center 2013

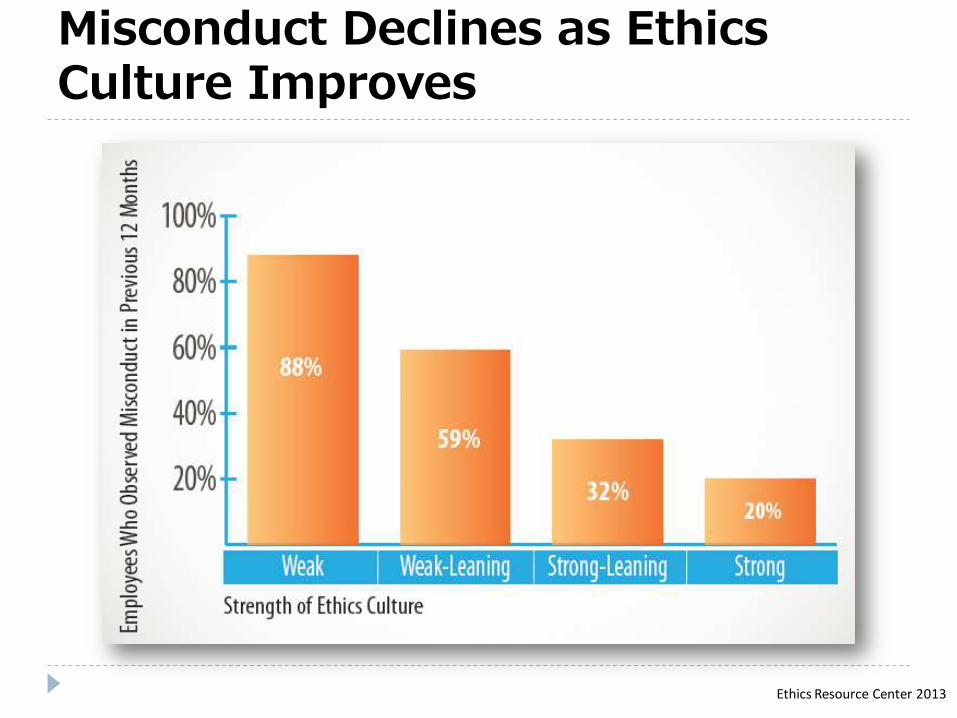

Misconduct Declines as Ethics Culture Improves

Ethics Resource Center 2013

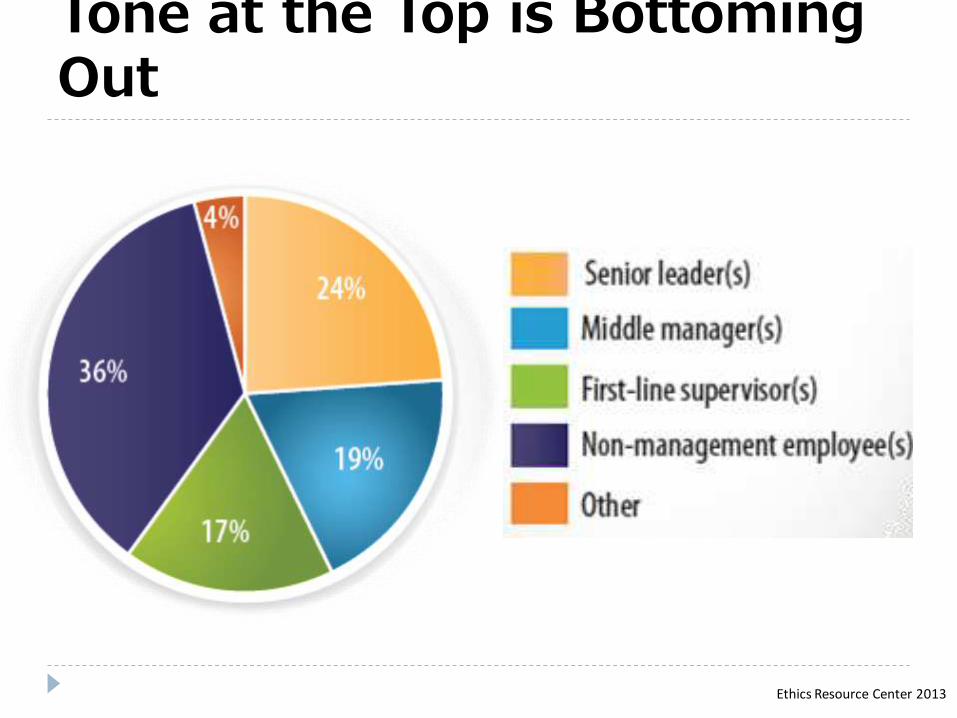

Tone at the Top is Bottoming Out

Ethics Resource Center 2013

Moving Up the Ranks

You have been with the company for 7 years and moved up the

ranks now supervising 12 employees. Your company has just

announced a merger with a larger company. Some layoffs in your

department are inevitable. Your supervisor, Pat, asks you to rank

your 12 employees and turn in the list in a week. After wrestling

with the list all week by using performance metrics, former

evaluations, observation and input from peers and clients, you turn

the list in to Pat. After looking at the list, Pat says it looks good,

but to switch #5 (Corey) and #9 (Jamie). Pat hired Jamie 2 years

ago who moved from Pennsylvania for this job.

What do you do?

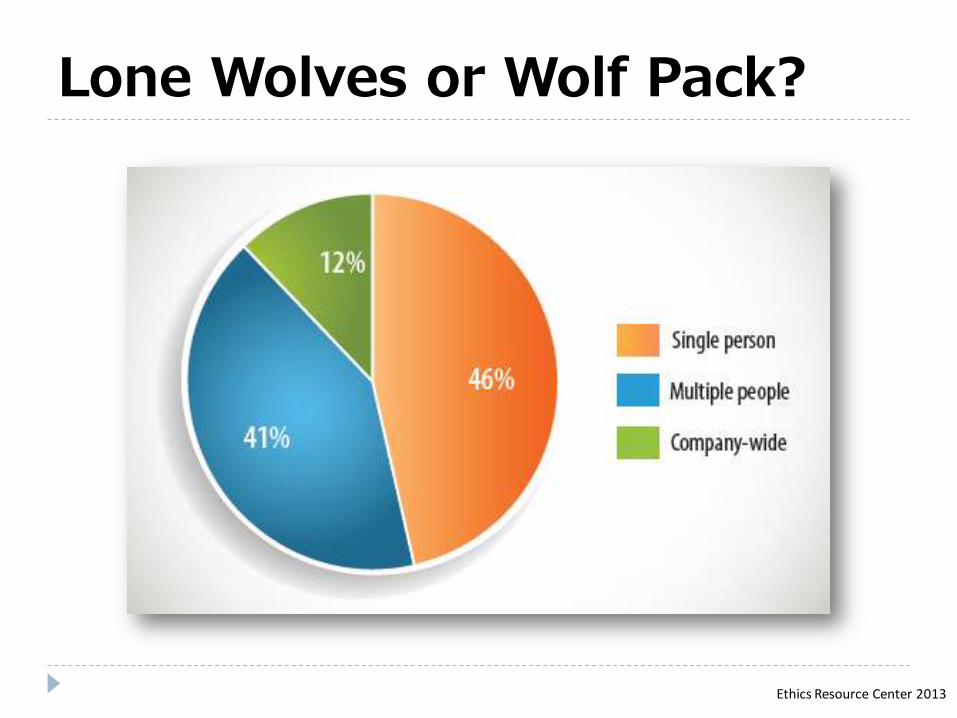

Lone Wolves or Wolf Pack?

Ethics Resource Center 2013

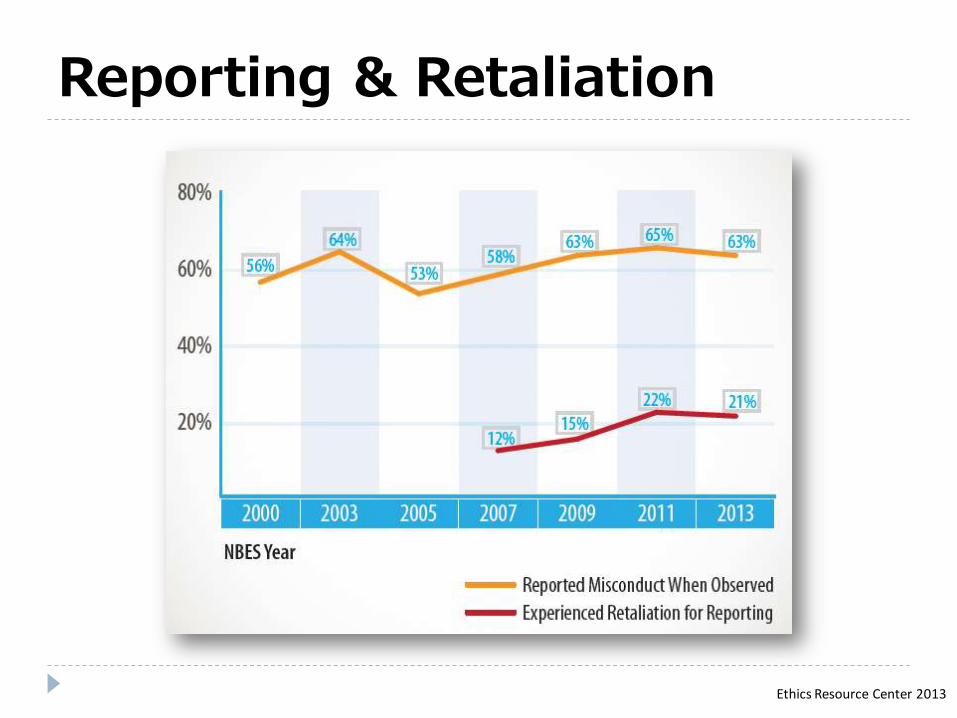

Reporting & Retaliation

Ethics Resource Center 2013

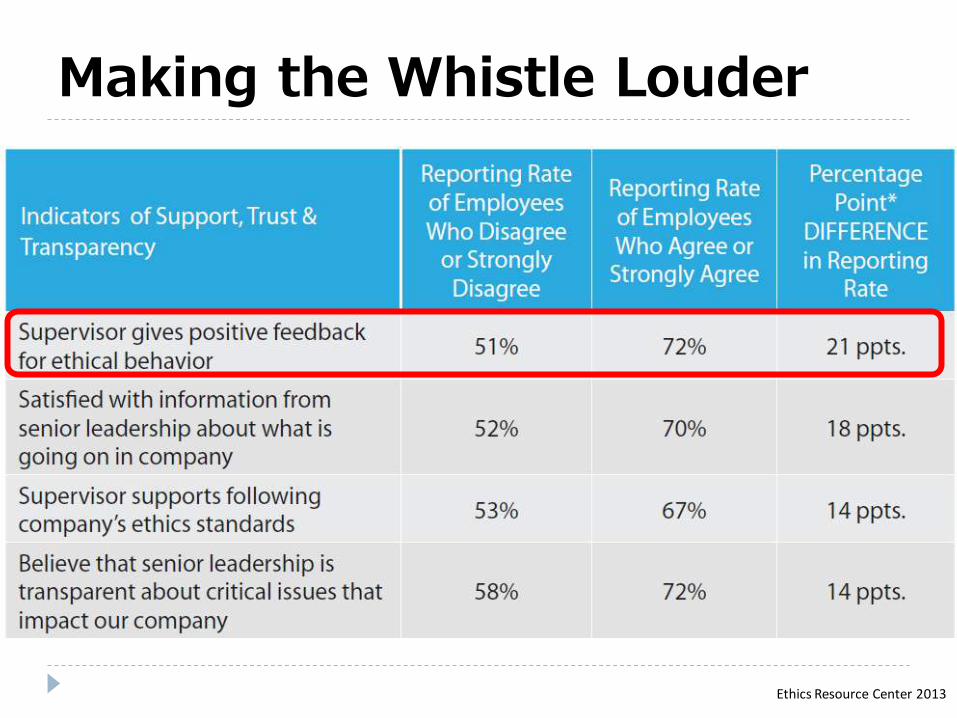

Making the Whistle Louder

Ethics Resource Center 2013

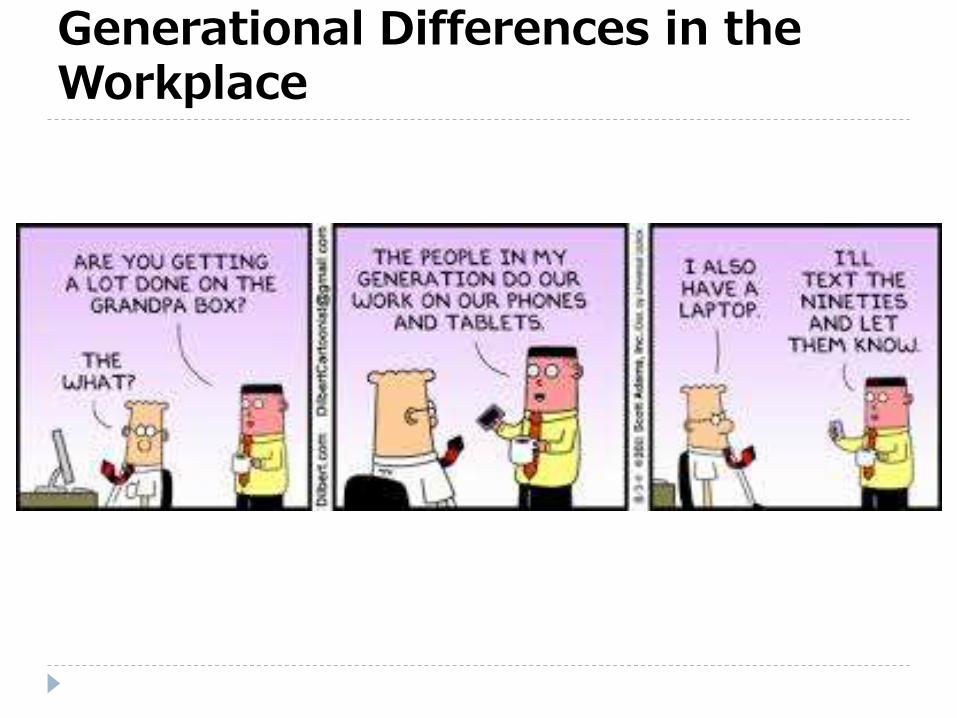

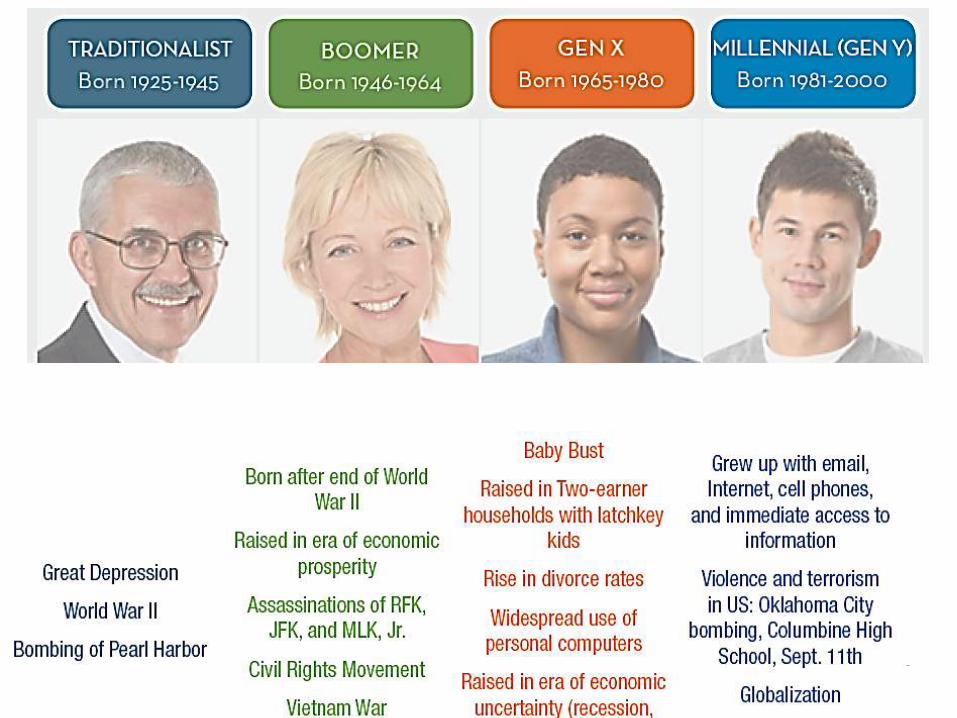

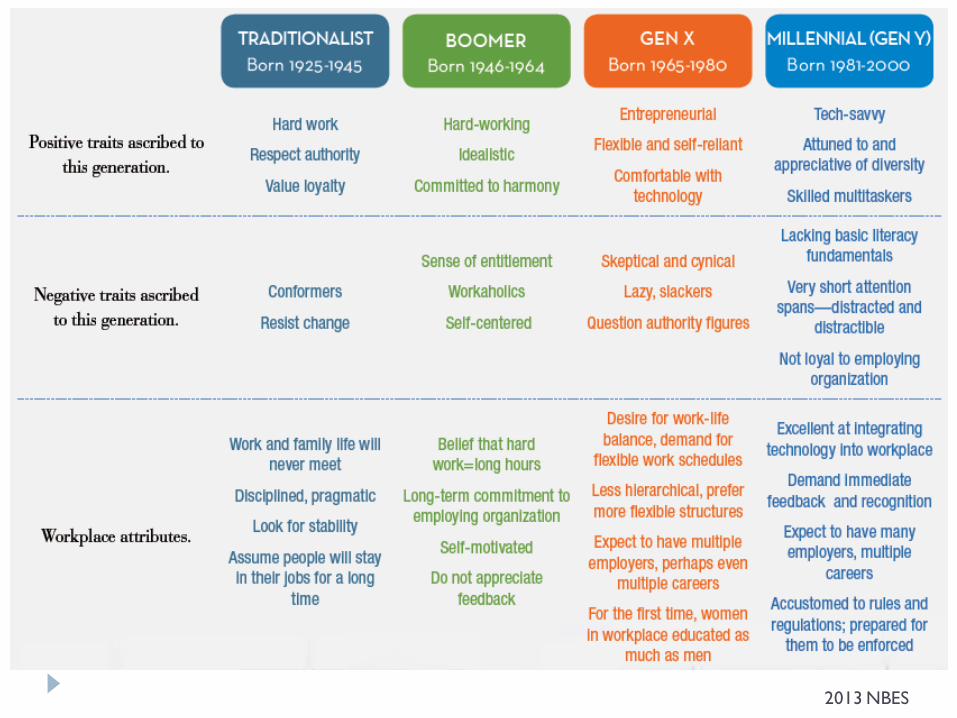

Generational Differences in the Workplace

Generational Differences in the Workplace

Which one are you?

2013 NBES

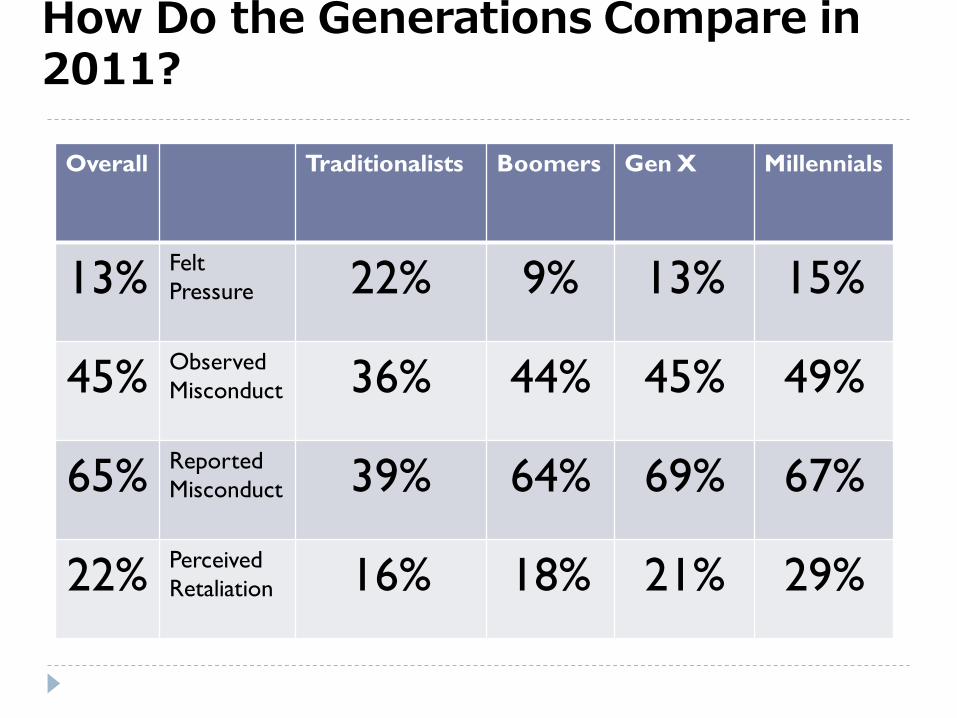

How Do the Generations Compare in 2011?

Overall Traditionalists Boomers Gen X Millennials

13% Felt

Pressure 22% 9% 13% 15%

45% Observed

Misconduct 36% 44% 45% 49%

65% Reported

Misconduct 39% 64% 69% 67%

22% Perceived

Retaliation 16% 18% 21% 29%

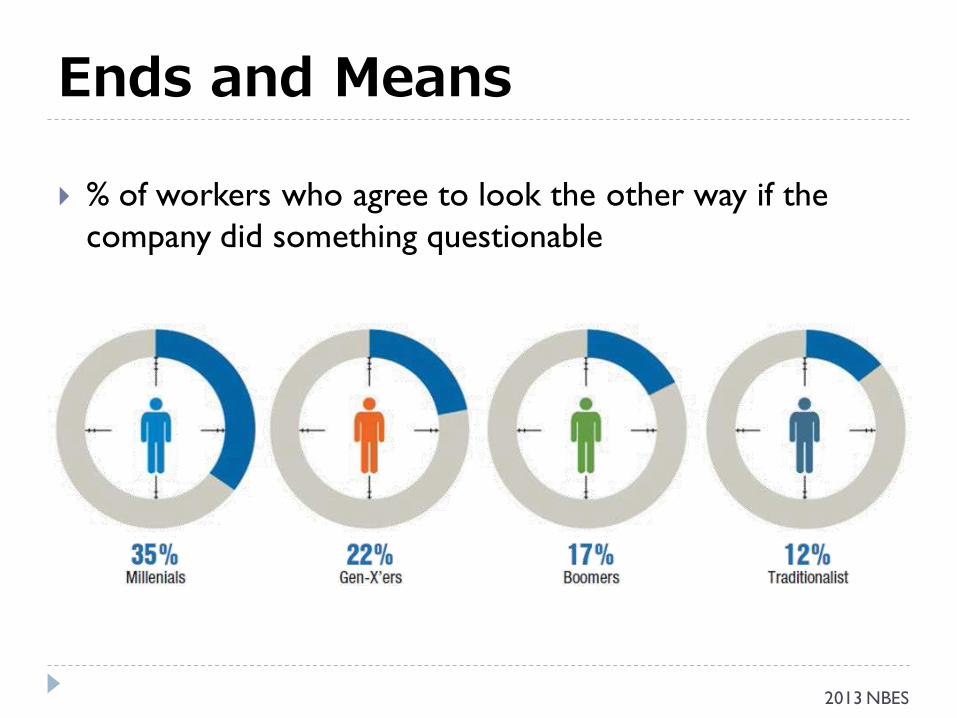

Ends and Means

% of workers who agree to look the other way if the

company did something questionable

2013 NBES

Recommendations

Best way to address challenges of

a workplace spanning multiple

generations is…

Implement effective ethics and

compliance program

Build strong ethics culture that

encourages employees to do

right thing

Do this in a way that reaches

and influences each generation

Case Study

Susan, a senior manager, notices as she walks by Andrew’s desk (a new

employee) that he is on the social media site LinkedIn. When Andrew

realized that Susan was looking at his computer screen he quickly

exited the website.

Susan proceeded to walk away while thinking to herself that she was

going to have to talk to Andrew and remind him about the Company’s

policy regarding company resources used for personal reasons. She

also considers what else Andrew is doing that he feels the need to

cover up.

Andrew grimaces as Susan walks by shaking her head. Even though he

was screening the website, as well as other social media sites, for

opportunities and networking possibilities with potential business

partners, Andrew worries that these activities are not understood or

valued.

Stopping the Tsunami

Employees are engaging in social

networking at work

Increasingly, it’s how business gets

done

Stopping it is not feasible

They don’t need your network or

computers to do it!

They have smartphones and tablets that can

access the internet

Their devices are small and portable

2012 NBES-SN

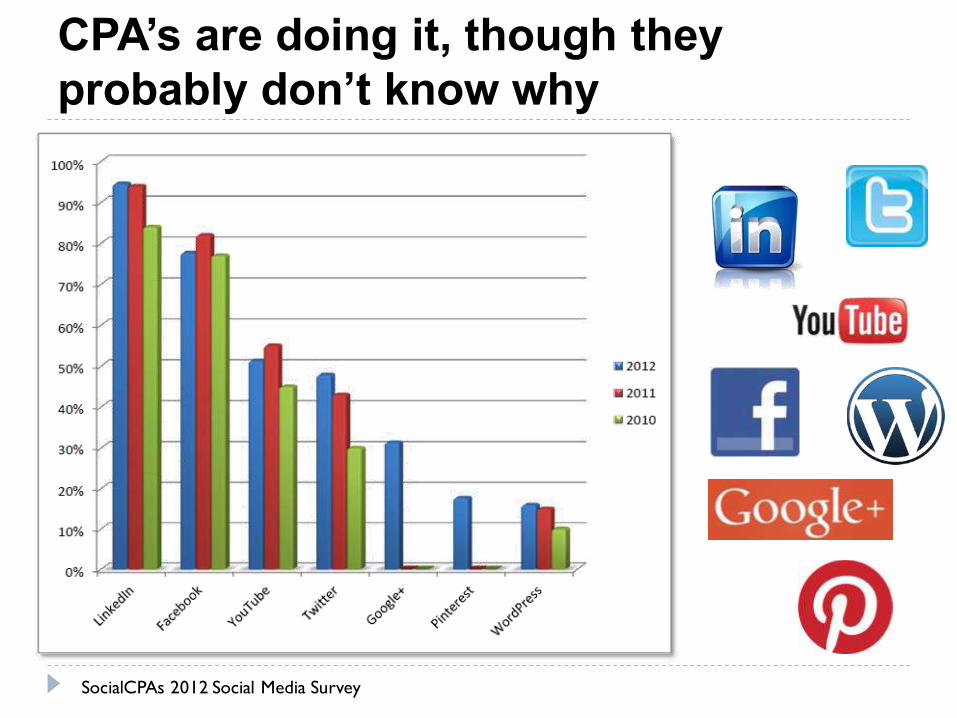

CPA’s are doing it, though they

probably don’t know why

SocialCPAs 2012 Social Media Survey

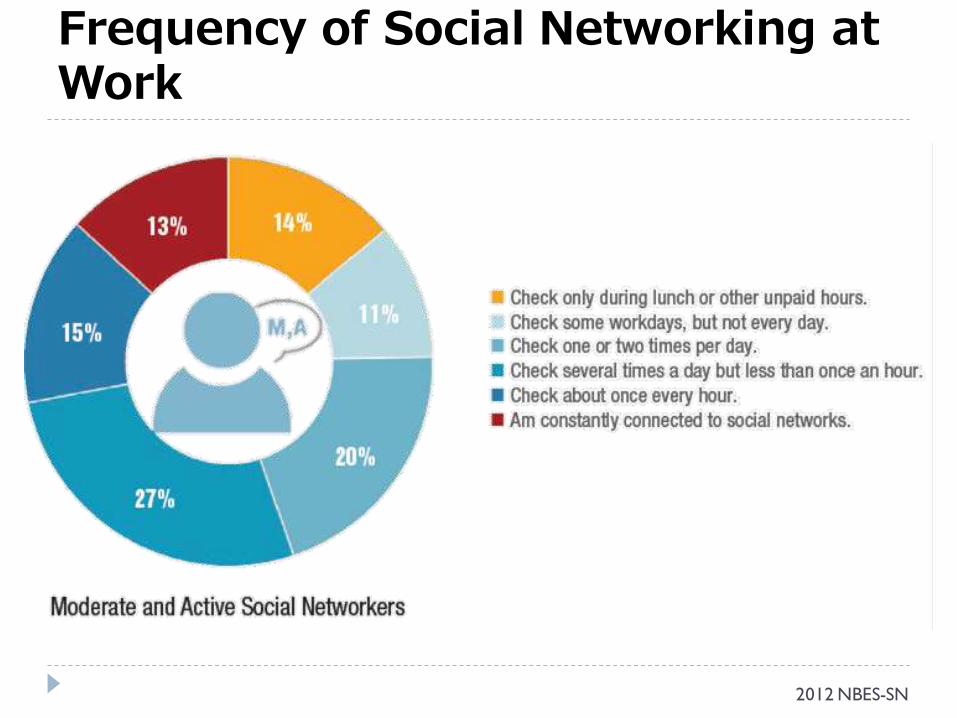

Frequency of Social Networking at Work

2012 NBES-SN

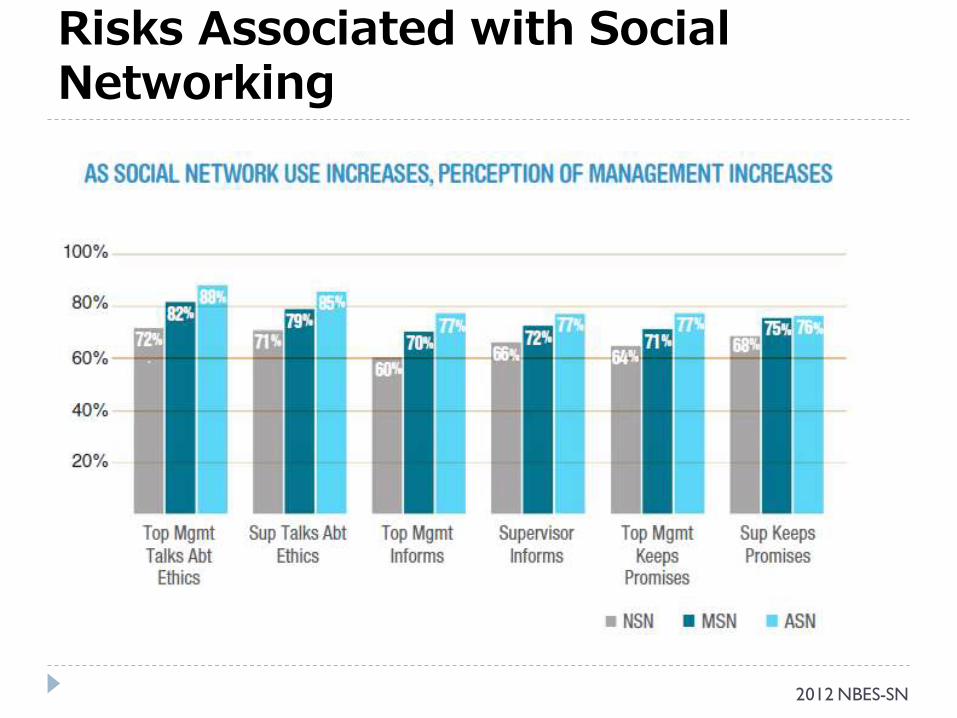

Risks Associated with Social Networking

2012 NBES-SN

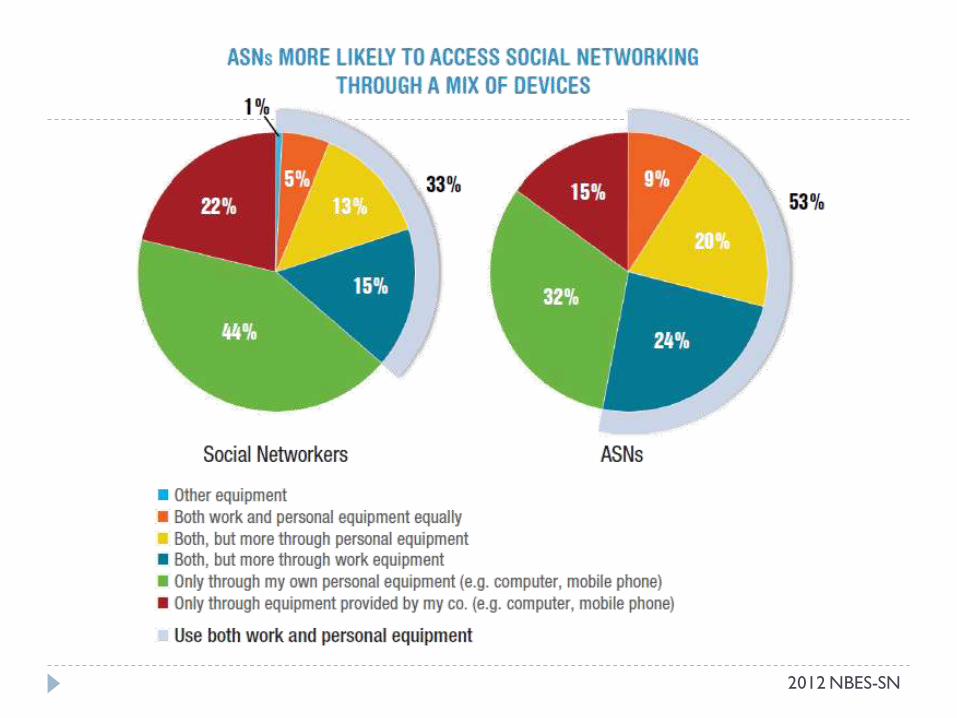

2012 NBES-SN

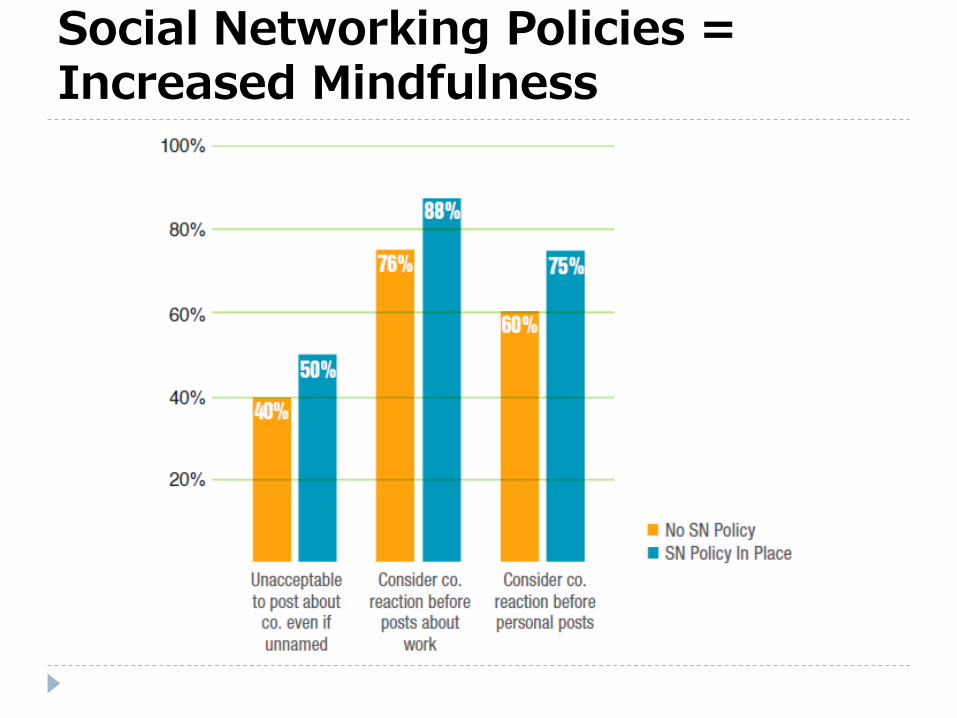

Social Networking Policies = Increased Mindfulness

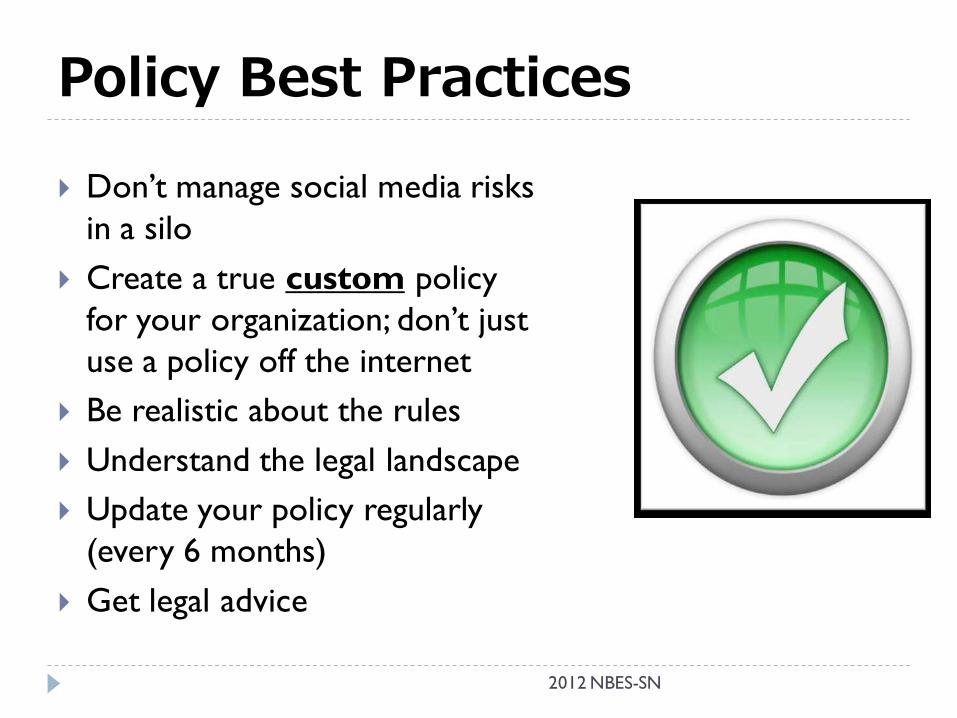

Policy Best Practices

Don’t manage social media risks

in a silo

Create a true custom policy

for your organization; don’t just

use a policy off the internet

Be realistic about the rules

Understand the legal landscape

Update your policy regularly

(every 6 months)

Get legal advice

2012 NBES-SN

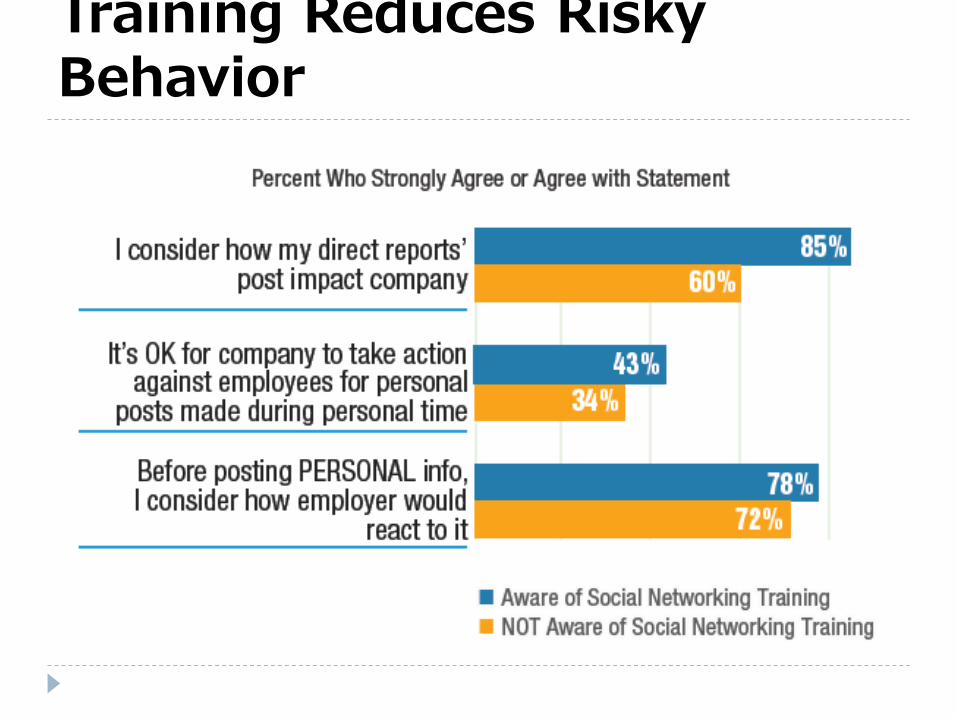

Training Reduces Risky Behavior

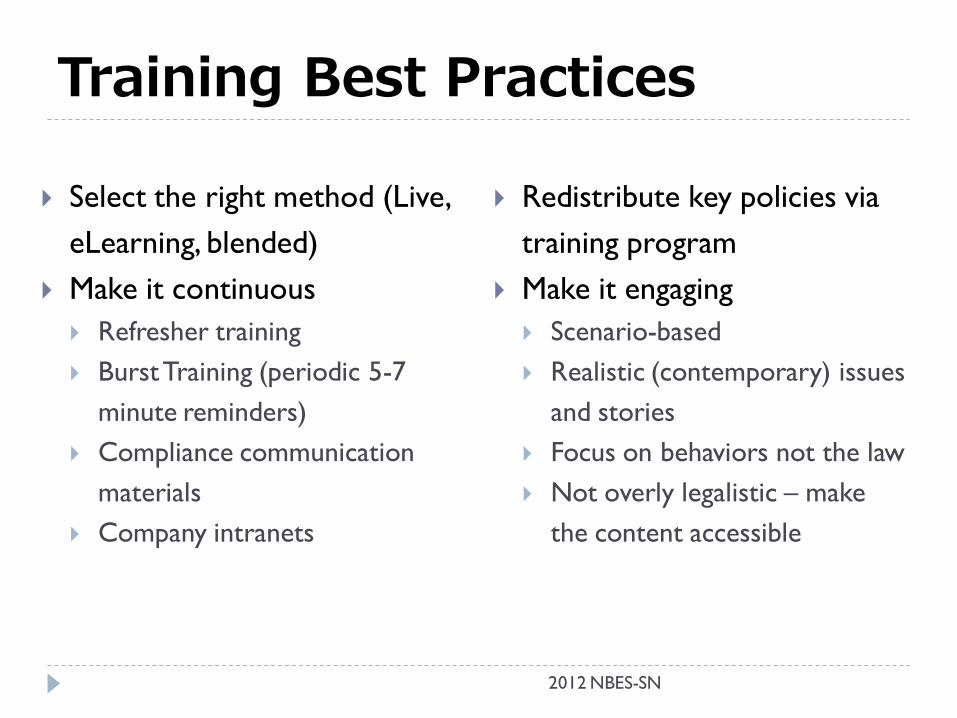

Training Best Practices

Select the right method (Live,

eLearning, blended)

Make it continuous

Refresher training

Burst Training (periodic 5-7

minute reminders)

Compliance communication

materials

Company intranets

Redistribute key policies via

training program

Make it engaging

Scenario-based

Realistic (contemporary) issues

and stories

Focus on behaviors not the law

Not overly legalistic – make

the content accessible

2012 NBES-SN

It’s Not Just Facebook & YouTube

Significant missteps are

happening in HR and recruiting: Profiling

Third party recruitment practices

LinkedIn New connections = leak of confidential

information

Endorsements = job search

Endorsements destroy your reference

policy

Email notices continue long after you have

left your company

Resume fraud and material

misrepresentations

2012 NBES-SN

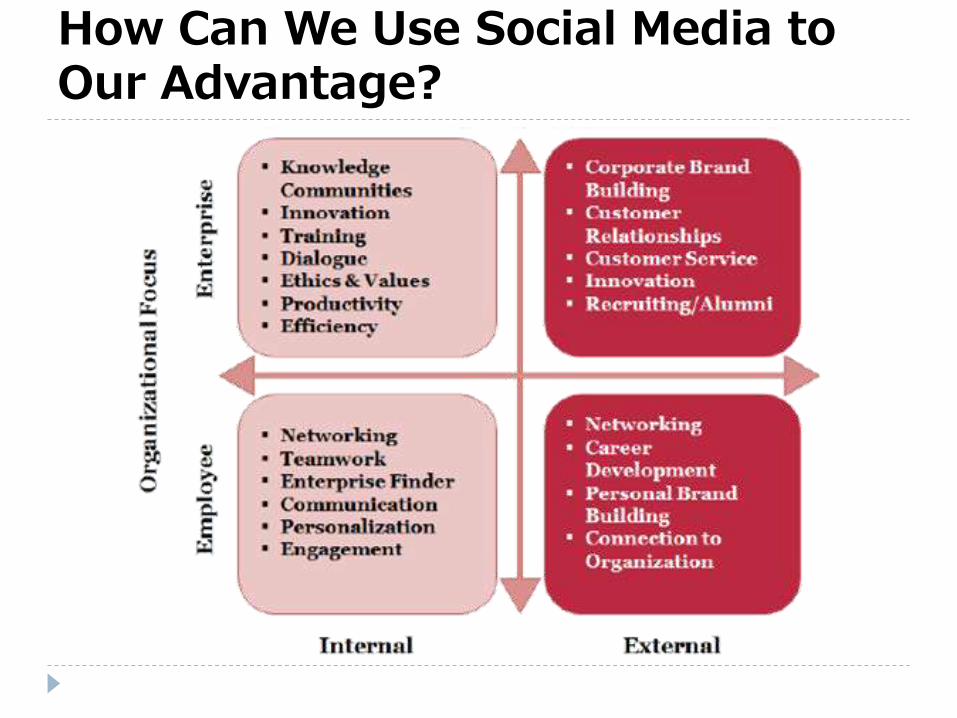

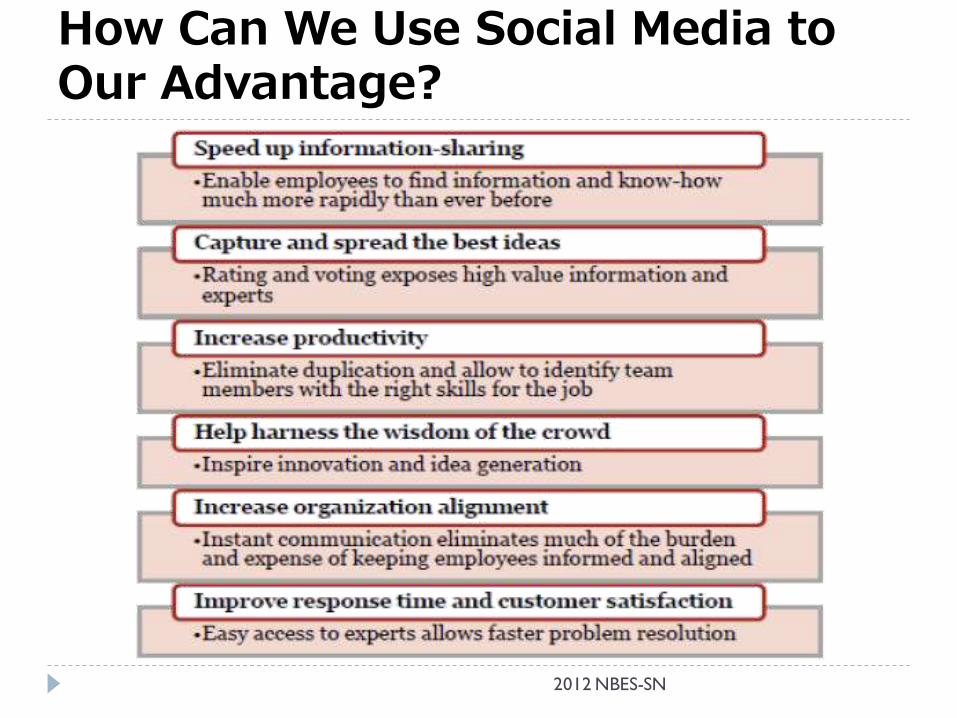

How Can We Use Social Media to Our Advantage?

2012 NBES-SN

How Can We Use Social Media to Our Advantage?

How Can We Use Social Media to Our Advantage?

Companies can learn from social

networking employees to get a

better picture of what employees

do and how they communicate.

Engaging social networkers will

ultimately help:

Enhance the company’s

reputation

Strengthen employees’ ethical

performance

Create a closer relationship

between company and

employees

2012 NBES-SN

The Future Ethical/Fraud Issues: What’s Coming

IT Security

Cybercrime

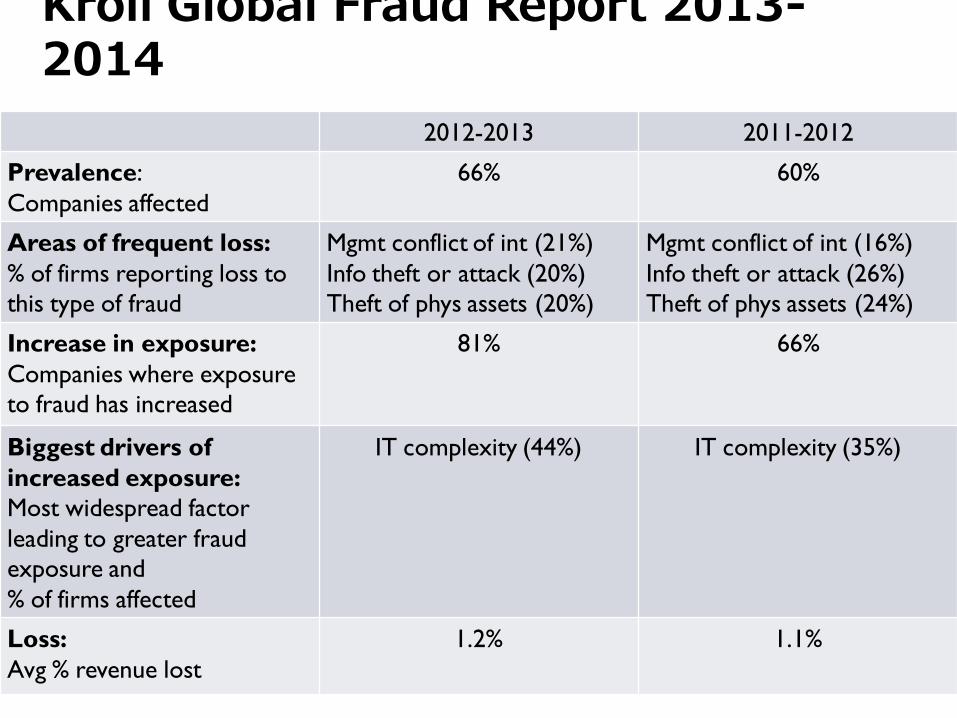

Kroll Global Fraud Report 2013-2014

2012-2013 2011-2012

Prevalence:

Companies affected

66% 60%

Areas of frequent loss:

% of firms reporting loss to

this type of fraud

Mgmt conflict of int (21%)

Info theft or attack (20%)

Theft of phys assets (20%)

Mgmt conflict of int (16%)

Info theft or attack (26%)

Theft of phys assets (24%)

Increase in exposure:

Companies where exposure

to fraud has increased

81% 66%

Biggest drivers of

increased exposure:

Most widespread factor

leading to greater fraud

exposure and

% of firms affected

IT complexity (44%) IT complexity (35%)

Loss:

Avg % revenue lost

1.2% 1.1%

We are building our lives around our wired and wireless networks. The question is, are we ready to work together to defend them?

Cal Christian

Melissa Critcher

Jonathan Kraftchick

Joanne Rockness

Appendix

Qualifications of CPE Sponsors

The Board does not register sponsors of CPE courses.

The Board does not register CPE courses.

CPE sponsors in good standing with NASBA shall be in

compliance with CPE requirements.

Qualifications of CPE Sponsors

CPE that is not a NASBA sponsor must:

Have an individual that did not prepare the course review the

course;

Provide documentation that states:

The general content of the course and skill level taught,

Any prerequisites or preparation required,

The level of the course (basic, intermediate, etc.),

The teaching methods used,

The amount of recommended CPE credit, and

The date the course is offered.

Qualifications of CPE Sponsors

Ensure the instructors are qualified

Evaluate the performance of the instructor

Attendees must have an opportunity to evaluate the quality of

the course,

Systematically review the evaluation process.

Encourage participation by those with appropriate

education and experience level

Distribute course materials

Use appropriate physical facilities

Qualifications of CPE Sponsors

Accurately assign the number of CPE credits by either

Monitoring attendance or

Testing to see if material was learned

Inform instructors the results of their evaluations

Retain for five years

A record of participants

An outline of the course

The date and location of presentation

The participant evaluations

Documentation of the presenters qualifications and

The number of contact hours recommended

Qualifications of CPE Sponsors

Have a visible, continuous, and identifiable contact person,

Develop and promulgate policies and procedures for

grievances, and

Provide persons completing course requirements with a

written proof of completion.

Deceptive Conduct Prohibited

A CPA shall not engage in deceptive

conduct. Deception includes fraud or

misrepresentation and representations

or omissions which a CPA either knows

or should know have a capacity or

tendency to deceive. Deceptive conduct

is prohibited whether or not anyone

has been actually deceived.

AICPA Ethics Interpretation 101-3

• Revisions to the “Activities Related to Attest Services”

are effective for engagements covering periods

beginning on or after December 15, 2014.

• Has involvement become so extensive that it would

constitute performing a separate service:

• The following are considered outside of the scope of

an attest engagement:

• Financial statement preparation,

• Cash-to-accrual conversions, and

• Reconciliations

AICPA Ethics Interpretation 101-3

1. The member should not assume management

responsibilities for the attest client.

2. Before performing nonattest service, the member should

determine that the client has agreed to:

Assume all management responsibilities.

Oversee the service

Evaluate the adequacy and results of the services performed.

Accept responsibility for the results of the services

AICPA Ethics Interpretation 101-3

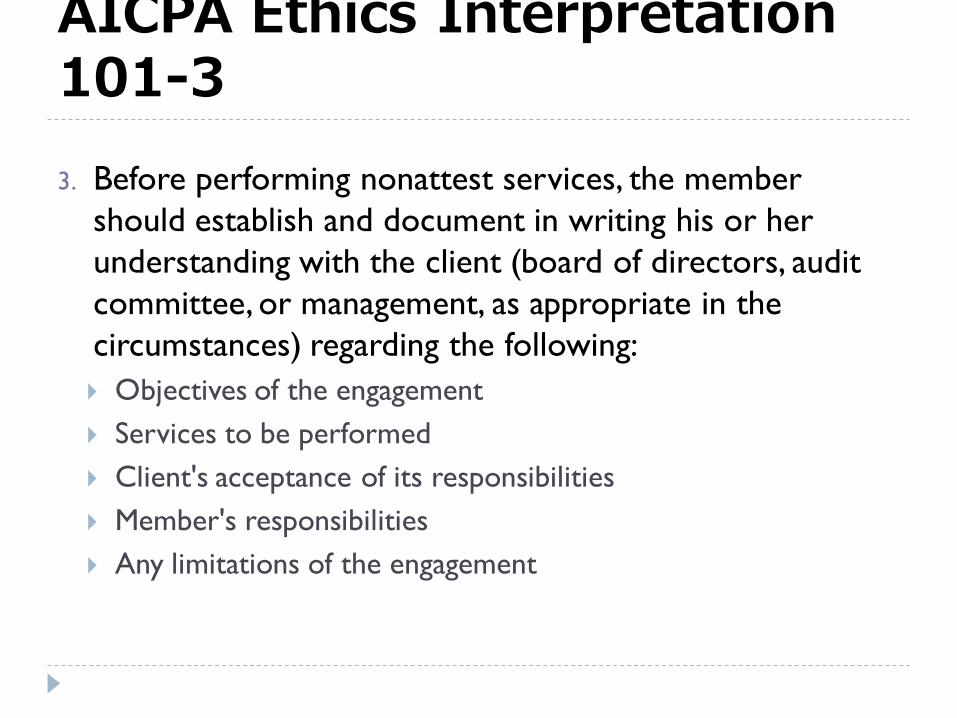

3. Before performing nonattest services, the member

should establish and document in writing his or her

understanding with the client (board of directors, audit

committee, or management, as appropriate in the

circumstances) regarding the following:

Objectives of the engagement

Services to be performed

Client's acceptance of its responsibilities

Member's responsibilities

Any limitations of the engagement

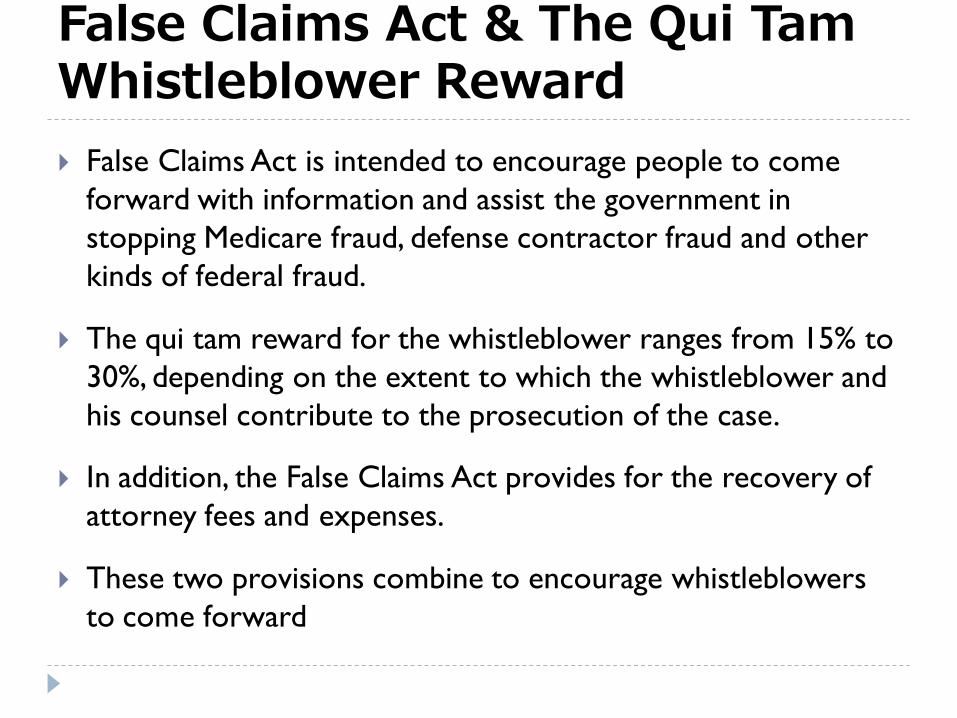

False Claims Act & The Qui Tam Whistleblower Reward

False Claims Act is intended to encourage people to come

forward with information and assist the government in

stopping Medicare fraud, defense contractor fraud and other

kinds of federal fraud.

The qui tam reward for the whistleblower ranges from 15% to

30%, depending on the extent to which the whistleblower and

his counsel contribute to the prosecution of the case.

In addition, the False Claims Act provides for the recovery of

attorney fees and expenses.

These two provisions combine to encourage whistleblowers

to come forward

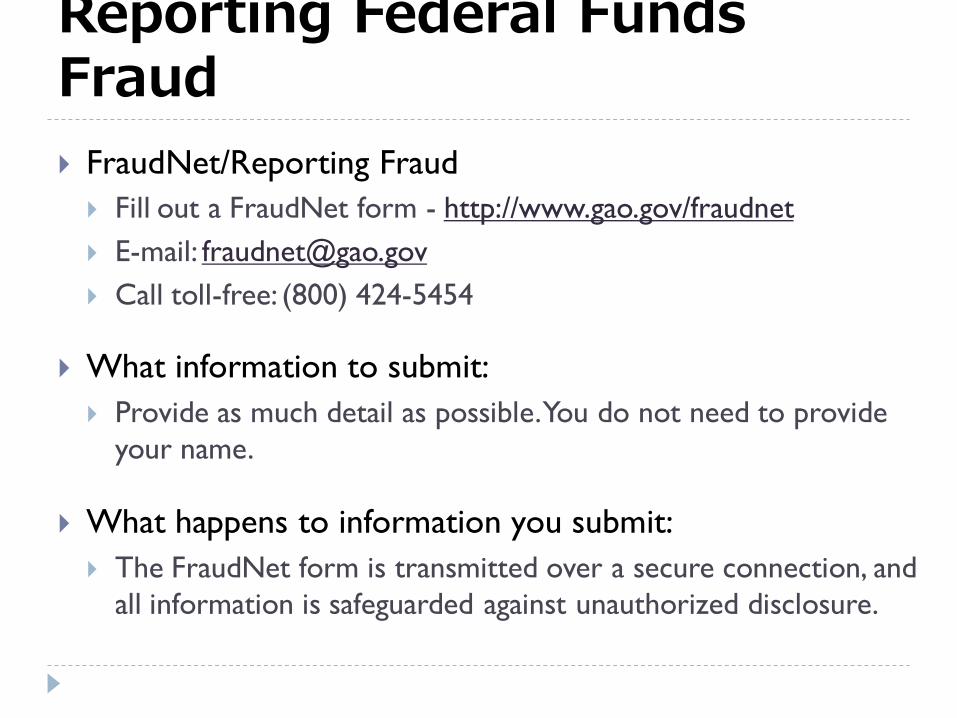

Reporting Federal Funds Fraud

FraudNet/Reporting Fraud

Fill out a FraudNet form - http://www.gao.gov/fraudnet

E-mail: [email protected]

Call toll-free: (800) 424-5454

What information to submit:

Provide as much detail as possible. You do not need to provide

your name.

What happens to information you submit:

The FraudNet form is transmitted over a secure connection, and

all information is safeguarded against unauthorized disclosure.

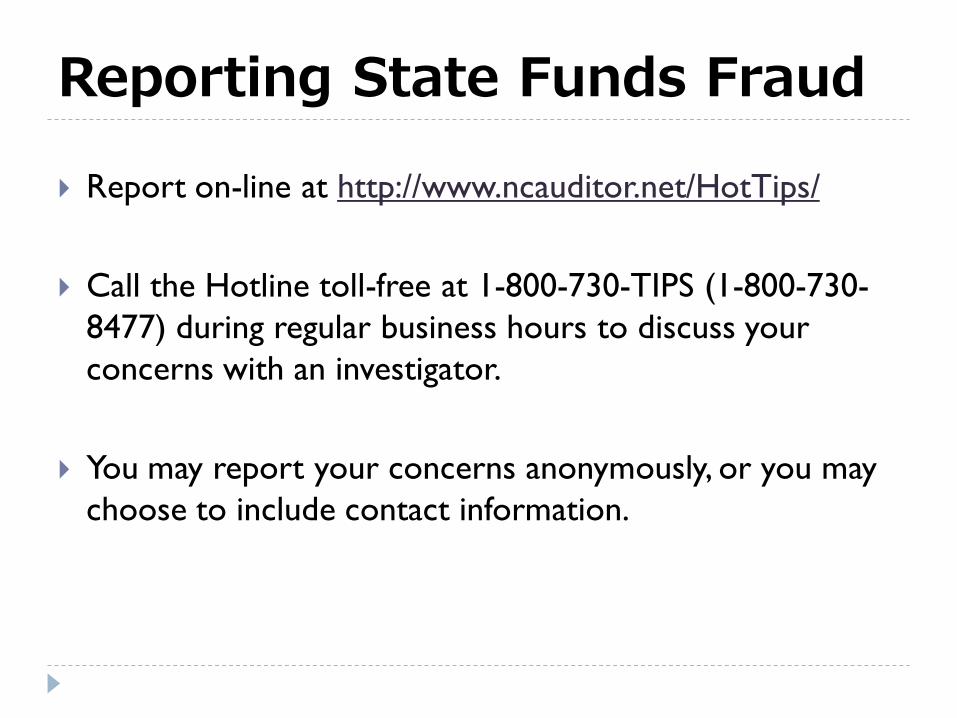

Reporting State Funds Fraud

Report on-line at http://www.ncauditor.net/HotTips/

Call the Hotline toll-free at 1-800-730-TIPS (1-800-730-

8477) during regular business hours to discuss your

concerns with an investigator.

You may report your concerns anonymously, or you may

choose to include contact information.

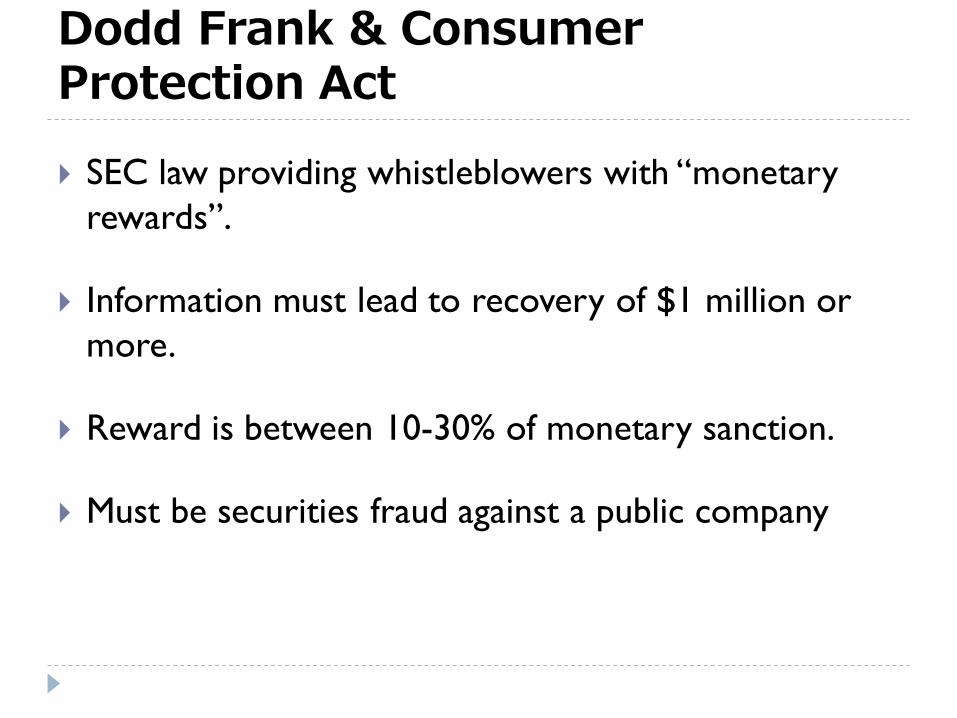

Dodd Frank & Consumer Protection Act

SEC law providing whistleblowers with “monetary

rewards”.

Information must lead to recovery of $1 million or

more.

Reward is between 10-30% of monetary sanction.

Must be securities fraud against a public company

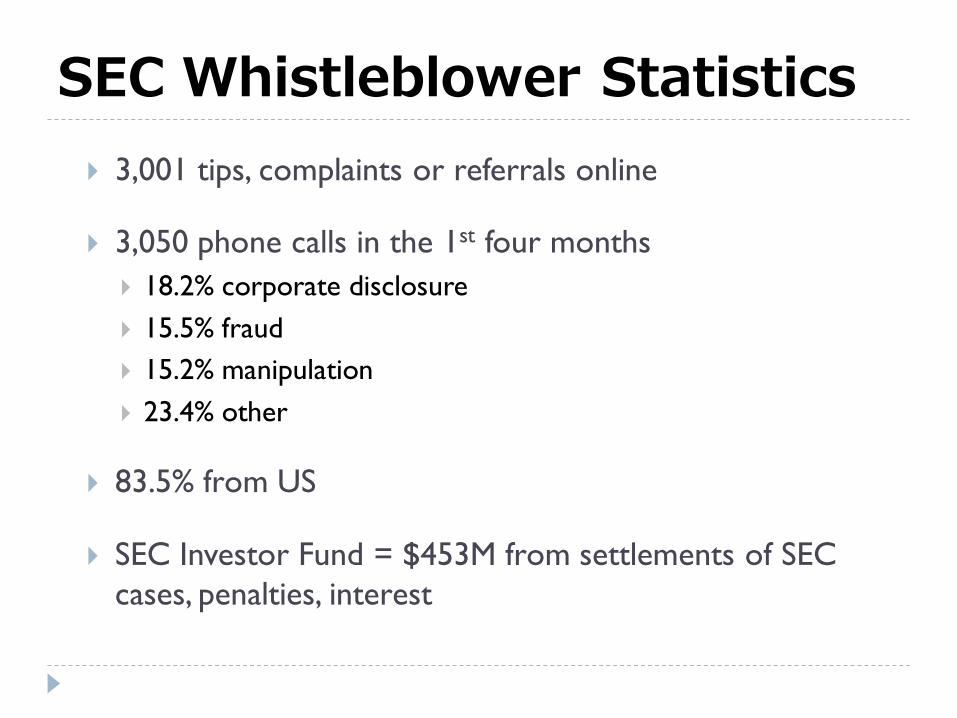

SEC Whistleblower Statistics

3,001 tips, complaints or referrals online

3,050 phone calls in the 1st four months

18.2% corporate disclosure

15.5% fraud

15.2% manipulation

23.4% other

83.5% from US

SEC Investor Fund = $453M from settlements of SEC

cases, penalties, interest

Computer Intrusions

Bots

Worms

Viruses

Spyware

Malware

Hacking

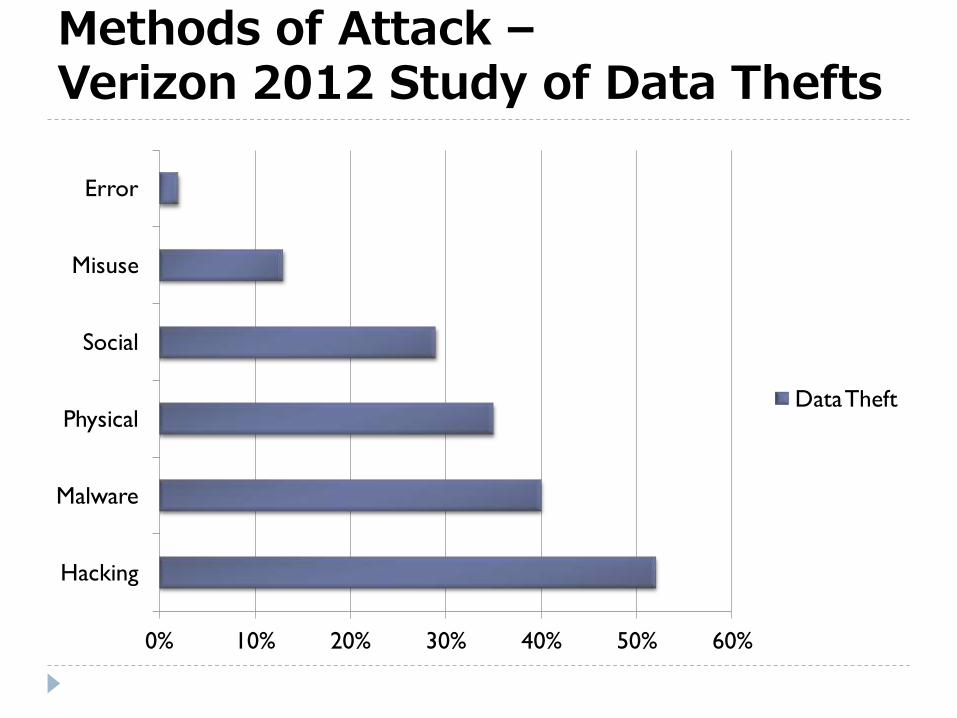

Methods of Attack – Verizon 2012 Study of Data Thefts

0% 10% 20% 30% 40% 50% 60%

Hacking

Malware

Physical

Social

Misuse

Error

Data Theft

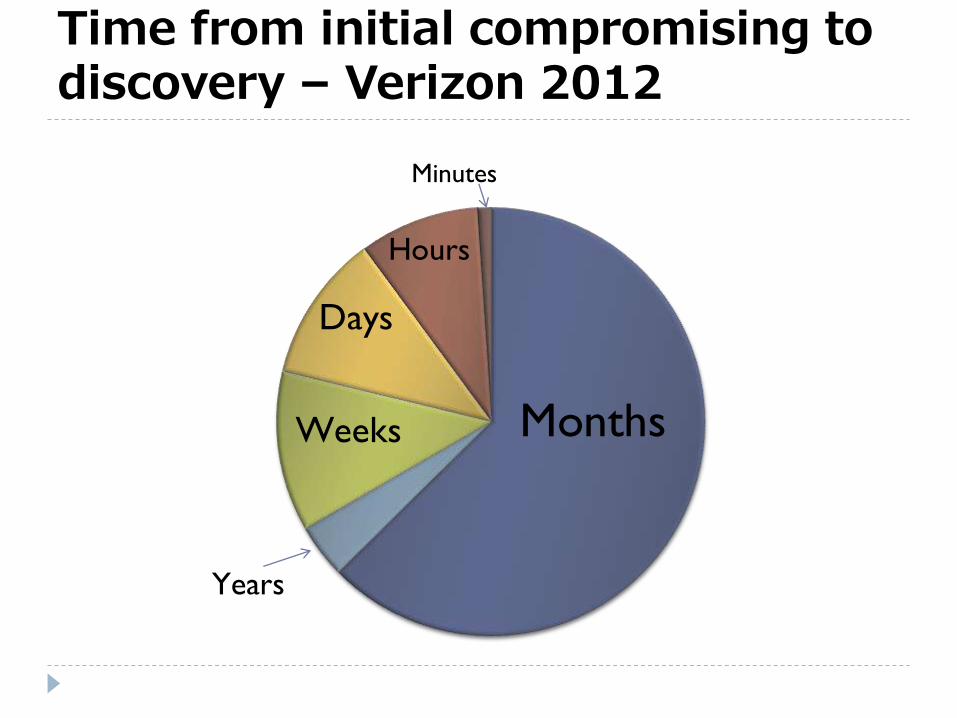

Time from initial compromising to discovery – Verizon 2012

Months Weeks

Days

Hours

Years

Minutes

PWC 2013 State of Cybercrime Survey

1. Leaders do not know who is responsible for their

organization’s cybersecurity, nor are security experts

effectively communicating on cyberthreats, cyberattacks,

and defensive technologies.

2. Leaders underestimate their cyber-adversaries’

capabilities and the strategic financial, reputational, and

regulatory risks they pose.

PWC 2013 State of Cybercrime Survey

3. Leaders are unknowingly increasing their digital

attack vulnerabilities by adopting social

collaboration, expanding the use of mobile devices,

moving the storage of information to the cloud,

digitizing sensitive information, moving to smart grid

technologies, and embracing workforce mobility

alternatives—without first considering the impact these

technological innovations have on their cybersecurity

profiles.

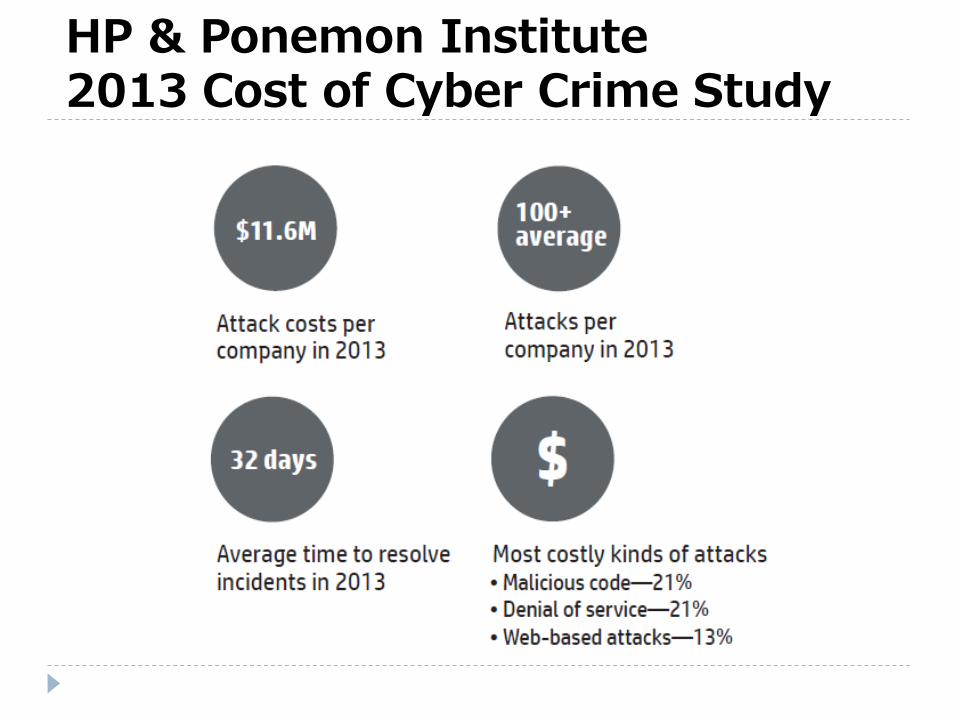

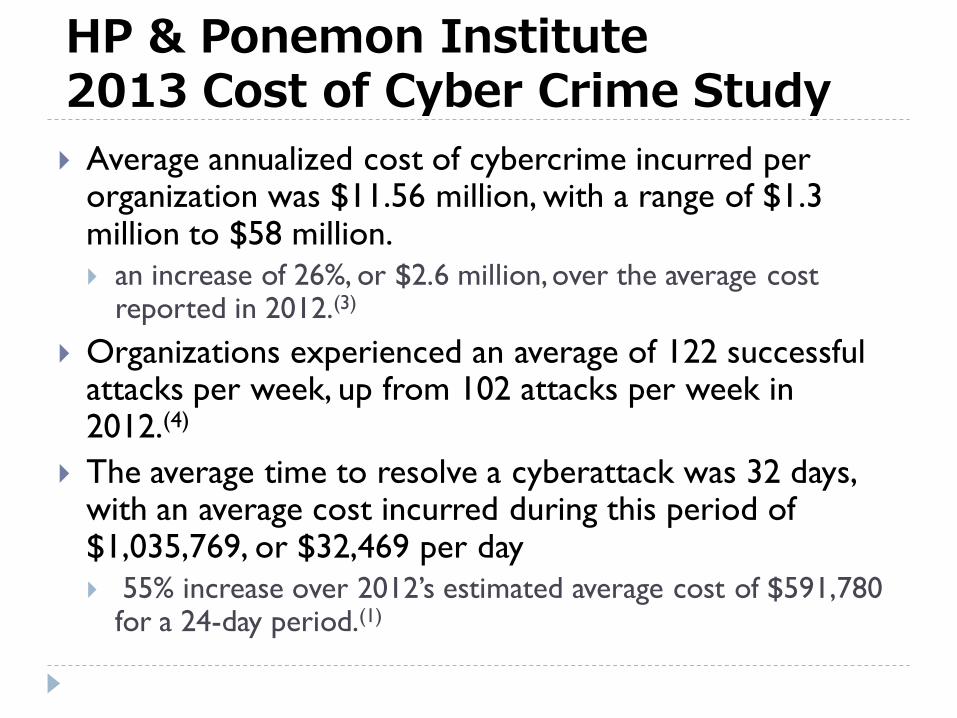

HP & Ponemon Institute 2013 Cost of Cyber Crime Study

HP & Ponemon Institute 2013 Cost of Cyber Crime Study

Average annualized cost of cybercrime incurred per organization was $11.56 million, with a range of $1.3 million to $58 million.

an increase of 26%, or $2.6 million, over the average cost reported in 2012.(3)

Organizations experienced an average of 122 successful attacks per week, up from 102 attacks per week in 2012.(4)

The average time to resolve a cyberattack was 32 days, with an average cost incurred during this period of $1,035,769, or $32,469 per day

55% increase over 2012’s estimated average cost of $591,780 for a 24-day period.(1)

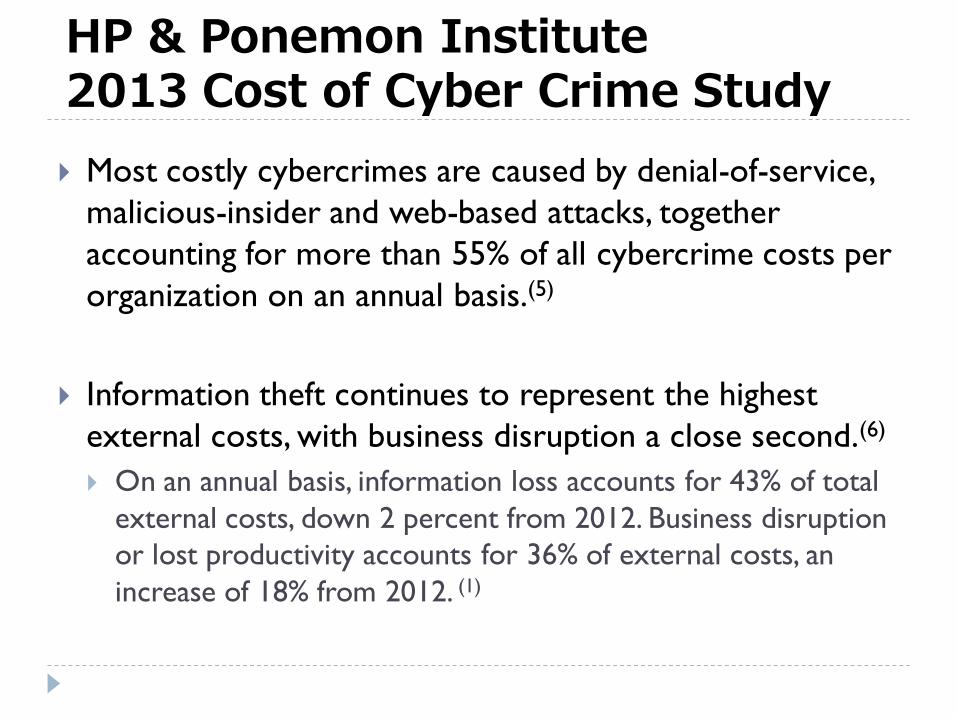

HP & Ponemon Institute 2013 Cost of Cyber Crime Study

Most costly cybercrimes are caused by denial-of-service,

malicious-insider and web-based attacks, together

accounting for more than 55% of all cybercrime costs per

organization on an annual basis.(5)

Information theft continues to represent the highest

external costs, with business disruption a close second.(6)

On an annual basis, information loss accounts for 43% of total

external costs, down 2 percent from 2012. Business disruption

or lost productivity accounts for 36% of external costs, an

increase of 18% from 2012. (1)

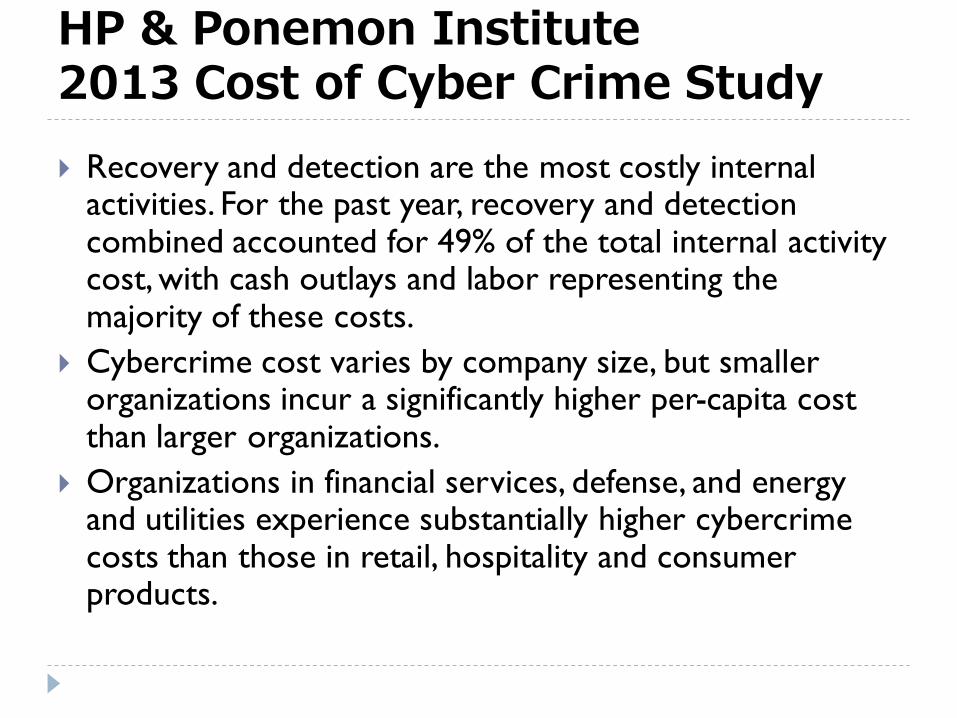

HP & Ponemon Institute 2013 Cost of Cyber Crime Study

Recovery and detection are the most costly internal activities. For the past year, recovery and detection combined accounted for 49% of the total internal activity cost, with cash outlays and labor representing the majority of these costs.

Cybercrime cost varies by company size, but smaller organizations incur a significantly higher per-capita cost than larger organizations.

Organizations in financial services, defense, and energy and utilities experience substantially higher cybercrime costs than those in retail, hospitality and consumer products.

Heads Up

Stephen and John both started around the same time at

their company 6 years ago and have become close friends.

Stephen becomes aware that John is going to be accused of

sexual harassment in the next few days. John knows that

Stephen would never do anything like this.

What does John do?