Embed Size (px)

Citation preview

1

2014 final results presentation

27 February 2015James Henderson, CEONeil Cooper, Group Finance Director

19 times Champion Jockey AP McCoy has announced his retirement in 2015. Small pictures, top to bottom: entering the parade ring on Carlingford Lough after winning the Hennessy Gold Cup during the Hennessy Gold Cup Day at Leopardstown Racecourse, Ireland, February 2015; and on Binocular on his way to victory in the williamhill.com Christmas Hurdle Race, January 2011

2

This presentation has been prepared by William Hill PLC (“William Hill”). This presentation includes statements that are,or may be deemed to be, “forward-looking statements”. These forward-looking statements can be identified by the useof forward-looking terminology, including the terms "believes", "estimates", "anticipates", "expects", "intends", "plans","goal", "target", "aim", "may", "will", "would", "could" or "should" or, in each case, their negative or other variations orcomparable terminology. These forward-looking statements include all matters that are not historical facts. They appearin a number of places throughout this presentation and the information incorporated by reference into this presentation,and include statements regarding the intentions, beliefs or current expectations of the directors, William Hill or theGroup concerning, amongst other things, the results of operations, financial condition, liquidity, prospects, growth,strategies and dividend policy of William Hill and the industry in which it operates.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and dependon circumstances that may or may not occur in the future and may be beyond William Hill's ability to control or predict.Forward-looking statements are not guarantees of future performance and hence may prove to be erroneous. TheGroup's actual results of operations, financial condition, liquidity, dividend policy and the development of the industry inwhich it operates may differ materially from the impression created by the forward-looking statements contained in thispresentation and/or the information incorporated by reference into this presentation. In addition, even if the results ofoperations, financial condition, liquidity and dividend policy of the Group and the development of the industry in which itoperates are consistent with the forward-looking statements contained in this presentation and/or the informationincorporated by reference into this presentation, those results or developments may not be indicative of results ordevelopments in subsequent periods.

Other than in accordance with its legal or regulatory obligations (including under the Listing Rules, the Disclosure andTransparency Rules and the Prospectus Rules), William Hill does not undertake any obligation to update or revisepublicly any forward-looking statement, whether as a result of new information, future events or otherwise.

Disclaimer

3

2014: a record year

£372.2m 40% 18%

276.8 275.7

330.6 335.0

372.2

2010 2011 2012 2013 2014

Record operating profit1, up 11%

of net revenue from digital businesses2

of net revenue from international markets

61%57%

30%32%

6% 8%3%

2013 2014

Retail Online Australia Other

3%

85% 82%

15% 18%

2013 2014

UK Non-UK

1. Operating profit/loss is defined as pre-exceptional profit/loss before interest and tax, and the amortisation of specific identified intangible assets recognised on acquisitions

2. Online and William Hill Australia

World Cup

4

Neil Cooper2014 financial results

My Tent Or Yours ridden by Tony McCoy wins the williamhill.com Christmas Hurdle Race during Day One of the William Hill Winter Festival at Kempton Park Racecourse, December 2013

5

A year of record operating profit

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

Amounts wagered1 8,945.7 7,800.8 +15%

Net revenue 1,609.3 1,486.5 +8%

Operating profit2 372.2 335.0 +11%Amortisation (9.0) (10.9) -17%

Net finance costs (45.9) (44.3) +4%

Tax (63.1) (32.2) +96%

Non-controlling interest - (15.3) -

Retained profit 254.2 232.3 +9%Basic, adjusted EPS (p)3 29.9 28.8 +4%Net debt for covenant purposes 602.8 796.0 -24%

Dividend per share (p) 12.2 11.6 +5%

Numbers are presented on a pre-exceptional basis.1. Amounts wagered comprises the gross takings in OTC, Telephone, US, Australia and Online Sportsbook, and

net revenue in Retail gaming machines and Online gaming products.2. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific

intangible assets recognised on acquisitions.3. Basic, adjusted EPS is based on profit for the period before exceptional items and before the amortisation of

specific intangible assets arising on acquisitions.

6

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

Accelerated Australian brand amortisation (44.5) -

One-off shop portfolio closure (19.4) -

European indirect taxation provision (9.7) -

tomwaterhouse.com integration (3.3) (2.0)

Revaluation of tomwaterhouse.com earn-out (2.2) -

Write-off of unamortised finance fees (2.0) -

Write-off of fees on bridge loan - (1.7)

Australia management restructuring cost (1.8) -

Repayment of VAT refund and interest (0.5) (5.6)

Sportingbet acquisition and integration - (13.5)

Pre-tax (83.4) (22.8)Release of tax provision 15.4 -

Tax consequence of exceptional items 20.1 1.7

Post-tax (47.9) (21.1)

Exceptional items

7

Retail gaming growth and strong cost control mitigate OTC margin decline

1. Adjusting for the Machine Games Duty effect, Retail net revenue was flat.2. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of

specific intangible assets recognised on acquisitions.

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

OTC amounts wagered 2,452.2 2,439.9 +1%

OTC gross win 449.7 472.8 -5%

OTC gross win margin 18.3% 19.4% -1.1 ppts

Machines gross win 461.8 440.0 +5%

Total gross win 911.5 912.8 -0%Net revenue1 911.4 907.0 +0%Cost of sales (209.9) (203.3) +3%

Gross profit 701.5 703.7 -0%Operating costs (508.3) (507.4) +0%

Operating profit2 193.2 196.3 -2%

8

Retail OTC wagering and margin trendsAmounts wagered: H1 2014 v H1 2013

Amounts wagered: H2 2014 v H2 2013

Gross win margin: full year trend

-3% -5%

35%

-1%

2%

-10%

0%

10%

20%

30%

40%

% C

hang

e in

am

ount

s w

ager

ed

Horseracing Greyhounds Football Other Total

-1%

-5%

0%

3%

-1%

-6%

-4%

-2%

0%

2%

4%

% c

hang

e in

am

ount

s w

ager

ed

Horseracing Greyhounds Football Other Total

0%

5%

10%

15%

20%

25%

30%

35%

Ret

ail g

ross

win

mar

gin

2014 2013

9

Retail gross win per machine shows good growth

1. Compared with 52 weeks of 2012

52 weeks ended 30 Dec 2014

52 weeks ended 31 Dec 2013

% Change

Average number of LBOs 2,406 2,401 +0%

Average number of machines 9,458 9,431 +0%

Machine density 3.93 3.93 -

Gross win per machine per week £939 £897 +5%

Machine gross win margin 3.44% 3.37% +0.07 ppts

4.8% 4.3%

7.6%

3.3%

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%

109110111112113114115116117118

Q1 2014 Q2 2014 Q3 2014 Q4 2014

£m

Machine quarterly gross win growth

Gross win Growth % (2014 v 2013)

10

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

Employee costs (195.2) (199.9) -2%

Property costs (101.4) (102.8) -1%

Content costs (70.2) (64.3) +9%

Depreciation (29.5) (28.4) +4%

Other costs incl. recharges (112.0) (112.0) -

Operating costs (508.3) (507.4) +0%

Retail demonstrates good cost control

507.4 508.3

0.8

5.3 1.10.3 8.6(4.3)

(2.6)(1.3) (7.0)

490492494496498500502504506508510

£m

Retail cost causal

11

Online revenue growth from both Sportsbook and Casino

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

Sportsbook 253.3 212.9 +19%Casino 235.5 191.0 +23%

Poker 14.9 18.2 -18%

Bingo 23.7 24.2 -2%

Gaming net revenue 274.1 233.4 +17%

Net revenue 527.4 446.3 +18%Cost of sales (51.0) (40.2) +27%

Gross profit 476.4 406.1 +17%Operating costs (298.7) (258.3) +16%

Operating profit1 177.7 147.8 +20%

1. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific intangible assets recognised on acquisitions.

74%

5%4%

17%

2014 Online net revenue by geographic split

UK Italy Spain Other

12

Online wagering increased, pre-match margins weaker

52 weeks ended 30 Dec 2014

52 weeks ended 31 Dec 2013

% Change

Unique active players (’000)1 2,467.9 2,360.7 +5%

Revenue per unique active player (£) 213.7 189.1 +13%

New accounts (’000)2 1,225.2 1,141.0 +7%

Average cost per acquisition (£)3 107.8 107.4 +0%

Sportsbook amounts wagered (£m) 3,758.2 2,931.7 +28%

- Pre-match amounts wagered (£m) 2,116.1 1,724.5 +23%

- In-play amounts wagered (£m) 1,642.1 1,207.2 +36%

Sportsbook gross win margin 7.6% 8.1% -0.5 ppts

- Pre-match gross win margin 9.3% 10.0% -0.7 ppts

- In-play gross win margin 5.3% 5.3% -

1. Placed a bet within the period2. Registered and transacted within the period3. Including affiliates

13

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

Employee costs (53.0) (45.1) +18%

Marketing (132.1) (122.5) +8%

Finance charges (20.3) (16.6) +22%

Depr. and amortisation1 (26.6) (18.9) +41%

Other costs incl.recharges

(66.7) (55.2) +21%

Operating costs (298.7) (258.3) +16%

1. Excludes £1.3m of Online amortisation relating to acquired intangibles (2013: £4.0m)

Business expansion drives cost base expansion

• Sportsbook free bets / amounts wagered ratio 0.8%• Marketing / net revenue ratio 25%

14

Doubling of Australian profit

52 weeks ended 30 Dec 2014

£m

41 weeks ended 31 Dec 2013

£m

% Change Pro-forma local currency

change %

Amounts wagered 1,388.7 1,177.1 +18% +0%

Gross win 129.4 92.5 +40% +12%

Win margin 9.3% 7.9% +1.4ppts +1.0 ppts

Net revenue 121.9 86.7 +41% +11%Cost of sales (30.1) (20.2) +49% +19%

Gross profit 91.8 66.5 +38% +9%Operating costs (67.1) (54.5) +23% -8%

Operating profit1 24.7 12.0 +106% +121%

Unique active players (’000) 324.0 247.9 +31% +15%

Revenue per unique active (£) 376.2 349.7 +8% -3%

New accounts (’000) 142.1 95.9 +48% +4%

Average cost per acquisition (£) 192.5 298.7 -36% -25%

1. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific intangible assets recognised on acquisitions.

15

Good progress but Australian returns lag expectation

• Achievements to date– Systems upgrades– tomwaterhouse.com (TW) purchase and integration– Management restructure– Marketing mix rebalanced, CPA lowered

• Rebranding has commenced

• Headwinds– Currency– Race field fees

• Now expect returns of Sportingbet and TW taken together to exceed WACC by 2018

– Previous guidance of 2016, inclusive of TW– Earnings enhancing from 2014

16

William Hill US

1. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific intangible assets recognised on acquisitions.

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change Local currency % change

Amounts wagered 375.7 310.2 +21% +27%

Gross win margin 7.9% 7.3% +0.6 ppts +0.6 ppts

Net revenue 29.7 22.7 +31% +36%Cost of sales (2.5) (2.0) +25% +32%

Gross profit 27.2 20.7 +31% +36%Operating costs (17.5) (15.8) +11% +16%

Operating profit1 9.7 4.9 +98% +99%

17

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

Change £m

Pre-exceptional EBITDA 438.0 390.3 47.7

Pension contribution (9.1) (8.1) (1.0)

Exceptional cash (34.6) (16.0) (18.6)

Working capital 47.1 (12.5) 59.6

Tax (34.5) (55.9) 21.4

Interest (43.6) (41.3) (2.3)

Other 4.9 11.1 (6.2)

Cash flow from operating activities

368.2 267.6 100.6

Strong cash inflows

• Cessation of non-controlling interest broadly offsets cash dividend increase, to £104m in total

• Capex shortfall versus expectations (£75m versus £80-90m)

18

Capex

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

Retail development1 25.2 38.8

Online 35.6 31.9

Australia 5.8 2.8

US 2.2 2.6

Other (including IT) 5.8 8.5

Total cash capital expenditure 74.6 84.6

• Estate fell by a net 70 shops to 2,362 (52 openings, 14 closures, eight re-sites and 108 portfolio closures)

• 2015 cash capex expected to be £80-90m• Exceptional provision of £12.4m relating to portfolio closure at year-end

1. Gross of proceeds on disposal

19

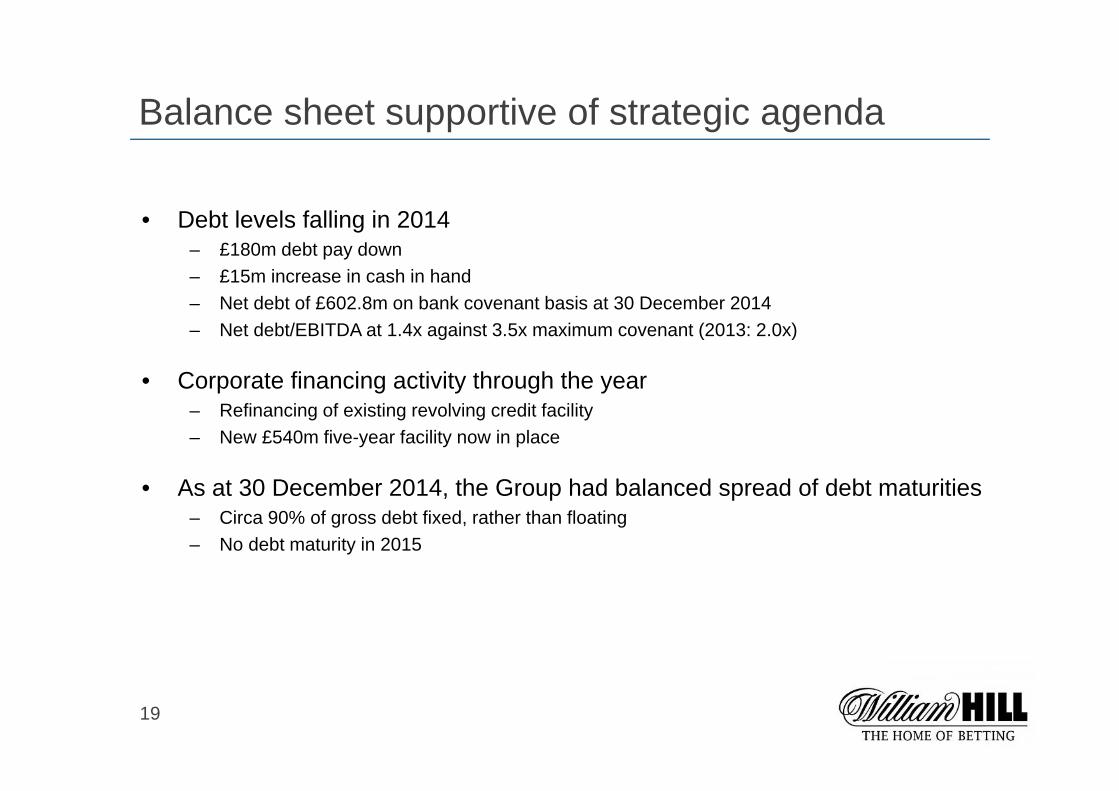

Balance sheet supportive of strategic agenda

• Debt levels falling in 2014– £180m debt pay down– £15m increase in cash in hand– Net debt of £602.8m on bank covenant basis at 30 December 2014– Net debt/EBITDA at 1.4x against 3.5x maximum covenant (2013: 2.0x)

• Corporate financing activity through the year– Refinancing of existing revolving credit facility– New £540m five-year facility now in place

• As at 30 December 2014, the Group had balanced spread of debt maturities– Circa 90% of gross debt fixed, rather than floating– No debt maturity in 2015

20

Other finance matters

• Effective pre-exceptional income statement tax rate of 19.9%– Prior year rate, at 11.5%, benefited from deferred tax credit– Effective full-year income statement rate expected to be 19% in 2015, expected cash tax rate to

be 20% in 2015

• Formal three-year actuarial pension valuation process completed– c£9.4m annual deficit repair payment to May 2019– Accounting surplus, driven by reduced liability valuation and strong investment returns

• Dividend:2014 2013 % Change

Interim 4.0p 3.7p +8.1%

Final 8.2p 7.9p +3.8%

Full 12.2p 11.6p +5.2%

21

James HendersonPerformance and strategy update

AP McCoy winning the Connolly's Red Mills Horsecare Cubes Novices' Chase on Malt Master at Huntingdon, January 2013

22

2014 achievements in a record year

• Another resilient Retail performance

• Continued strong growth in Online

• William Hill US operating profit up 98%1,2

• William Hill Australia operating profit1 doubles during period of substantial change

• Good progress on responsible gambling measures

0

100

200

300

400

500

600

2013 2014

Desktop Mobile

70%

30%

57%

43%

Mobile as % of Online net revenue

+48%growth in mobile

Sportsbook net revenue

+117%growth in mobile

gamingnet revenue

1. Operating profit/loss is defined as pre-exceptional profit/loss before interest and tax, and the amortisation of specific identified intangible assets recognised on acquisitions

2. On a statutory basis

£m

23

Assessing the ‘black swan’ effect

While football margins are stable… …and accumulators are now a higher % of mobile1

46% 39% 38%

54% 61% 62%

2012/13 2013/14 2014/15

Singles Accas

0%

5%

10%

15%

20%

25%

30%

2011/12 2012/13 2013/14 2014/15 todate

Singles Accumulators Pre-match average

1. By amounts wagered on football during the UK domestic football season

10%

11%

12%

13%

14%

2012 2013 2014

Online pre-match betting gross win margin by calendar year

Online pre-match betting gross win margin by football season

…margins are affected by accas…

24

Substantial progress on responsible gambling

April 2015Launch of the £50 journey

January 2015‘Set Your Limits’

is made mandatory

Q4 2014 ASA, BCAP, CAP

advertising reviews concluded, voluntary restrictions agreed

Launched October 2014

Implemented March 2014

Research published December 2014

GambleAware Week January 2015

25

Regulatory update

• £50 journey to be implemented 6 April 2015

• Point of Consumption Tax implemented December 2014

• Consultations on the Horserace Betting Levy, contributions from offshore operators and possible replacement with a betting right

• 4th EU Money Laundering Directive

• Responses awaited on planning and advertising

+29%Net revenue

+7%New accounts

+17%Unique actives

+10%Revenue per active

+4%Cost per acquisition

Online UK performance in H2 2014

26

• Video walls in 16% of shops• Digital window display trial

Further technology enhancements

Retail remains resilient

Continued product evolution

Strong cost focus

• 5% CAGR in football turnover1

• 50% increase in SSBT football markets with Online feed

• Eclipse in 70% of estate2

• B2 gross win +3%, B3 +11%3

• Extended single manning successfully implemented

• Like-for-like rent flat in 2014• Rolling onto CPI/RPI increases

for content costs 2015-2017• Closure portfolio benefits cost

progression

59% 52%

14% 17%

17% 15%

6% 7%4% 9%

2010 2014

Horse racing FootballGreyhounds VirtualOther

25% 20%

12% 11%

10%8%

3%4%

4% 6%

46% 51%

2010 2014Horse racing FootballGreyhounds VirtualOther Gaming

OTC turnover Retail gross win

783.1 789.7 837.9907.0 911.4

204.5 196.8 211.5 196.3 193.2

2010 2011 2012 2013 2014

Net revenue Operating profit

Retail five-year financial performance (£m)

1. 2010 to 20142. As at 2014 year-end3. Year on year

27

Priority Access card

Darts app

Vegas app

Product expansion:

horse racing

Product expansion:

other

Cash In My Bet

Vegas Mayfair games

AccaInsurance

Live Casino and scratchcards

Online leadership through innovation

• Italy: Sportsbook and Casino iOS• Spain: Sportsbook and Casino• Darts• Vegas iPad• Live Casino iPhone• Sportsbook, Casino, Vegas refreshes

28

Online leadership through innovation

Priority Access card

Darts app

Vegas app

Product expansion:

horse racing

Product expansion:

other

Cash In My Bet

Vegas Mayfair games

AccaInsurance

Live Casino and scratchcards

• Launching shortly• By invitation only• Priority access to the funds in your Online account

29

Online leadership through innovation

Priority Access card

Darts app

Vegas app

Product expansion:

horse racing

Product expansion:

other

Cash In My Bet

Vegas Mayfair games

AccaInsurance

Live Casino and scratchcards

• Extensive ‘Daily Meeting Markets’ range

30

Online leadership through innovation

Priority Access card

Darts app

Vegas app

Product expansion:

horse racing

Product expansion:

other

Cash In My Bet

Vegas Mayfair games

AccaInsurance

Live Casino and scratchcards

62,606Football events covered, +6%

39,392Tennis events

covered, +19%

17,015Basketball events

covered, +17%

138,419Events covered in

total, +11%

39% 39% 41%

23%

36%

28%

Football Tennis Basketball Pre-match In-play Total

Further strong turnover growth in key products

31

Online leadership through innovation

Priority Access card

Darts app

Vegas app

Product expansion:

horse racing

Product expansion:

other

Cash In My Bet

Vegas Mayfair games

AccaInsurance

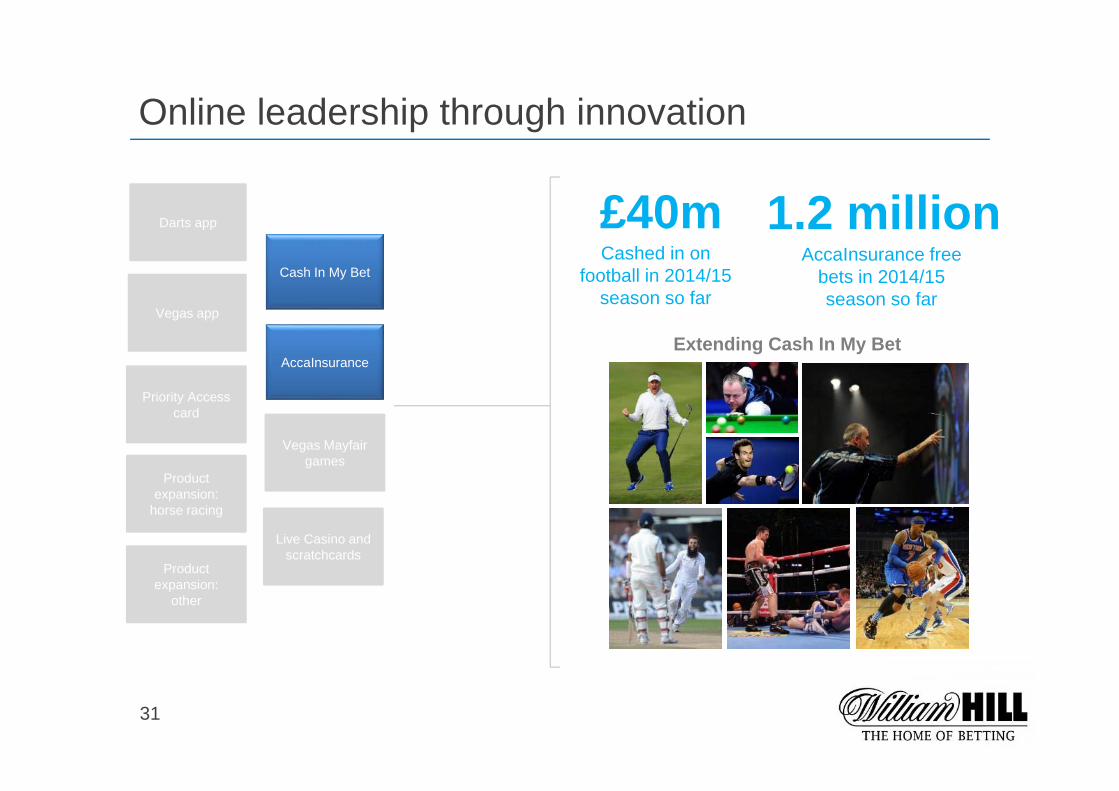

Live Casino and scratchcards

£40mCashed in on

football in 2014/15 season so far

1.2 millionAccaInsurance free

bets in 2014/15 season so far

Extending Cash In My Bet

32

Online leadership through innovation

Priority Access card

Darts app

Vegas app

Product expansion:

horse racing

Product expansion:

other

Cash In My Bet

Vegas Mayfair games

AccaInsurance

Live Casino and scratchcards

+68%growth in net revenue from

proprietary Vegas platform

+50%growth in net revenue from Live Casino

33

Strategic priorities: omni-channel

Maximising multi-channel share of wallet

54%of Online’s regular

customers regularly bet in LBOs

Customer-focused, technology-led

experience

‘One William Hill’ product

and content

Tip Advisor in Retail

Retail TV to Online

US racing to Online

Online football content to

SSBTs

Gantry alignment

34%of Retail’s regular

customers regularly bet online

34

Strategic priorities: international

William Hill brand launch

Live Casino launch in Spain

US turnover ($m)1

US operating profit1,2 ($m)

Australia operating profit (A$m)2,3

PalinsestoSupplementarerollout in Italy

1. 2012 numbers are on a statutory reporting basis from the date of ownership2. Operating profit/loss is defined as pre-exceptional profit/loss before interest and tax, and the amortisation

of specific identified intangible assets recognised on acquisitions 3. On a pro forma basis4. Source: AAMS5. Source: company estimates

Italy Sportsbook market share4

Spain Sportsbook market share5

Australia management

change

Australia product

expansion

Australia responsive design

launch

tomwaterhouse.com integration

US mobile turnover +65%

Net revenue: Italy +39%

Spain +64%

174338 370

36

150247

2012 2013 2014Retail Mobile

-0.97.9

15.7

2012 2013 2014

17.020.4

45.1

2012 2013 2014

Bet36546%

Bwin20%

William Hill19%

Sportium8%

Other7%

Bet36528%

Lottomatica10%

Eurobet9%

William Hill9%

Bwin8%

Sisal8%

Paddy Power7%

Snai7%

Others, 14%

35

Strategic priorities: technology

OpenBet

William Hill

Playtech

Increased front-end

independence: Project Trafalgar

Flexible framework:

William Hill API, Central Feeds

Ring-fenced back-end solution

700 people in IT

team globally

£98mIT opex and

capex in 20141

PRO

DU

CT

TRA

DIN

G

VEG

AS

CO

MM

UN

ITY

DATA WAREHOUSE

BUSINESS INTELLIGENCE

WILLIAM HILL API (SERVICE LAYER)TR

ADING HUB

SECU

RITY

MONITORING

TRAFALGAR FRONT END FRAMEWORK

CA

SIN

O,

PO

KE

R, B

ING

O

EXTERNAL GATEWAY

RETAIL DISPLAY GAMING SPORTSBOOK UI MOBILE BETTING UI

CORE SYSTEMS

FRONT END

ACCOUNT PAYMENT

BE

T C

AP

TUR

E

SE

TTLE

ME

NT

WALLET

1. Excludes depreciation and amortisation

36

Summary

• Record 2014 performance

• Continued strong Online growth

• Underpinned by cash-generative Retail

• Good operating profit progress from US and Australia

• Clear strategy for continued digital and international diversification

37

1/5 Hung Parliament

4/1 Conservative-Liberal Democrat coalition

9/2 Coalition involving SNP

9/2 Conservative minority government

11/2 Conservative majority

11/2 Labour-Liberal Democrat coalition

7/1 Coalition involving UKIP

9/1 Labour majority

20/1 Coalition involving Greens

33/1 Conservative-Labour coalition

50/1 UKIP majority

500/1 Liberal Democrat majority

5/1 Labour minority government

38

APPENDICES

39

Performance by division

1. Group, Retail and gaming machine net revenue growth is flattered by the transition from VAT and Amusement Machine Licence Duty to Machine Games Duty on 1 February 2013.

2. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific intangible assets recognised on acquisitions.

Net revenue1 Operating profit2

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change 52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

Retail 911.4 907.0 +0% 193.2 196.3 -2%

Online 527.4 446.3 +18% 177.7 147.8 +20%

Telephone 11.8 16.5 -28% (0.8) (0.0) n/a

William Hill Australia 121.9 86.7 +41% 24.7 12.0 +106%

William Hill US 29.7 22.7 +31% 9.7 4.9 +98%

Other 7.1 7.3 -3% (0.1) 0.2 -150%

Corporate - - - (32.2) (26.2) +23%

Total 1,609.3 1,486.5 +8% 372.2 335.0 +11%

40

Net operating expenses by division1

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

Retail (508.3) (507.4) +0%

Online (298.7) (258.3) +16%

Telephone (12.5) (16.5) -24%

William Hill Australia (67.1) (54.5) +23%

William Hill US (17.5) (15.8) +11%

Other (6.3) (6.2) +2%

Corporate (33.2) (29.6) +12%

Group net operating expenses (943.6) (888.3) +6%

1. Numbers are presented on a pre-exceptional basis, excluding the amortisation of the specific intangible assets arising on acquisitions and net of other income.

41

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

% Change

Amounts wagered 212.2 252.0 -16%

Gross win 12.6 17.4 -28%

Gross win margin 6.0% 6.9% -0.9 ppts

Net revenue 11.8 16.5 -28%Cost of sales (0.1) (0.0) -

Gross profit 11.7 16.5 -29%Staff costs (1.0) (1.7) -41%

Marketing costs (2.3) (2.4) -4%

Other costs incl. recharges (9.2) (12.4) -26%

Operating costs (12.5) (16.5) -24%Operating (loss)/profit1 (0.8) 0.0 -

Telephone

1. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific intangible assets recognised on acquisitions.

42

Net finance costs

52 weeks ended 30 Dec 2014

£m

52 weeks ended 31 Dec 2013

£m

Interest receivable (1.0) (1.1)

Bank loan interest 6.5 10.6

Bond interest 37.2 30.4

Amortisation of finance fees 2.6 3.7

Net interest on pension scheme net liability 0.6 0.7

Total pre-exceptional net finance costs 45.9 44.3

43

Net debt for covenant purposes

As at 30 Dec 2014

£m

As at 31 Dec 2013

£m

Bank loans 50.0 230.0

Corporate bonds 675.0 675.0

Cash (222.1) (206.7)

Net debt 502.9 698.3

Obligations under bank guarantees 3.2 3.0

Restricted cash – client balances 89.7 85.8

Other restricted cash 7.0 8.9

Net debt for covenant purposes 602.8 796.0

• Net debt: EBITDA of 1.4x vs maximum covenant of 3.5x (31 Dec 2013: 2.0x)• EBITDA: Net cash interest of 10.4x vs minimum covenant of 3.0x• BB+/Ba1 stable outlook credit ratings from S&P/Moody’s

44

Australia performance in local currency (pro forma)

1. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific intangible assets recognised on acquisitions.

52 weeks ended 30 Dec 2014

A$m

52 weeks ended 31 Dec 2013

A$m

% Change

Amounts wagered 2,542.9 2,530.3 +0%

Gross win 236.7 211.0 +12%

Win margin 9.3% 8.3% +1.0 ppts

Net revenue 223.0 200.5 +11%Cost of sales (55.2) (46.5) +19%

Gross profit 167.8 154.0 +9%Operating costs (122.7) (133.6) -8%

Operating profit1 45.1 20.4 +121%

Unique active players (’000) 324.0 282.1 +15%

Revenue per unique active (A$) 688 711 -3%

New accounts (’000) 142.1 136.8 +4%

Average cost per acquisition (A$) 351.9 467.8 -25%

45

US performance in local currency

1. Operating profit is defined as pre-exceptional profit before interest and tax, before the amortisation of specific intangible assets recognised on acquisitions.

52 weeks ended 30 Dec 2014

$m

52 weeks ended 31 Dec 2013

$m

% Change

Amounts wagered 617.3 487.6 +27%

Gross win 48.6 35.8 +36%

Win margin 7.9% 7.3% +0.6 ppts

Net revenue 48.6 35.8 +36%Cost of sales (4.1) (3.1) +32%

Gross profit 44.5 32.7 +36%Operating costs (28.8) (24.8) +16%

Operating profit1 15.7 7.9 +99%

![[XLS]2006 Canadian Election Final Results - SFU.ca - Simon ...aheard/elections/2006-final-results.xls · Web view2006 Election Final Results 2006 Canadian Election - Official Results](https://img.pdfslide.us/doc/110x75/5b1b856c7f8b9a23258ead47/xls2006-canadian-election-final-results-sfuca-simon-aheardelections2006-final-.jpg)