Embed Size (px)

Citation preview

2013

Legislative

Presentation

Lake Charles Harbor & Terminal District

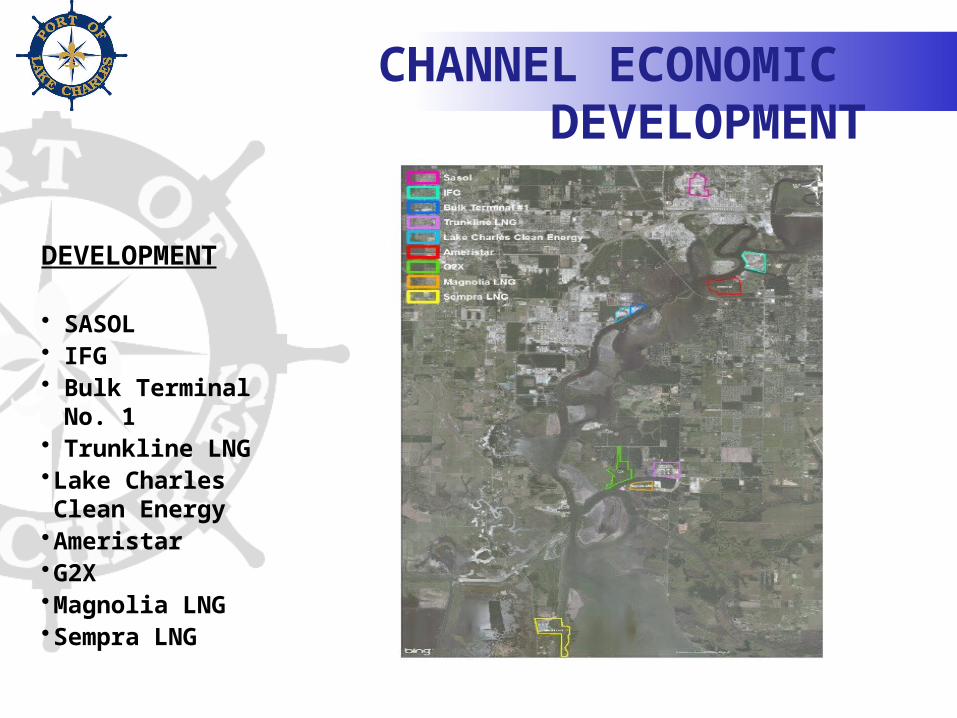

CHANNEL ECONOMIC DEVELOPMENT

DEVELOPMENT

• SASOL• IFG• Bulk Terminal No. 1• Trunkline LNG•Lake Charles Clean Energy

•Ameristar•G2X•Magnolia LNG•Sempra LNG

IFG UPDATE• IFG Construction

– New Concrete Silos Complete

– Conveyors, Dock Improvements & Ship Loader Scheduled

– Facilities Complete

March 2014

• UP Construction– Ladder Tracks & Wye by

Chennault

• Port Infrastructure– Loop Tracks– Dredging– Port Cleat Road

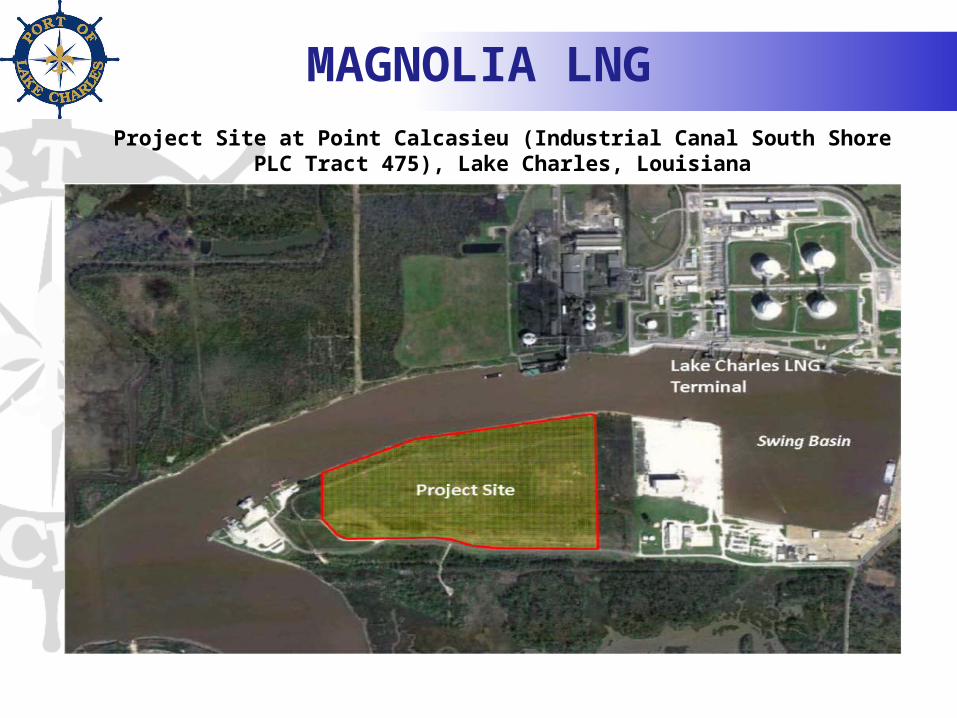

MAGNOLIA LNG

MAGNOLIA LNGProject Site at Point Calcasieu (Industrial Canal South Shore PLC Tract 475), Lake

Charles, Louisiana

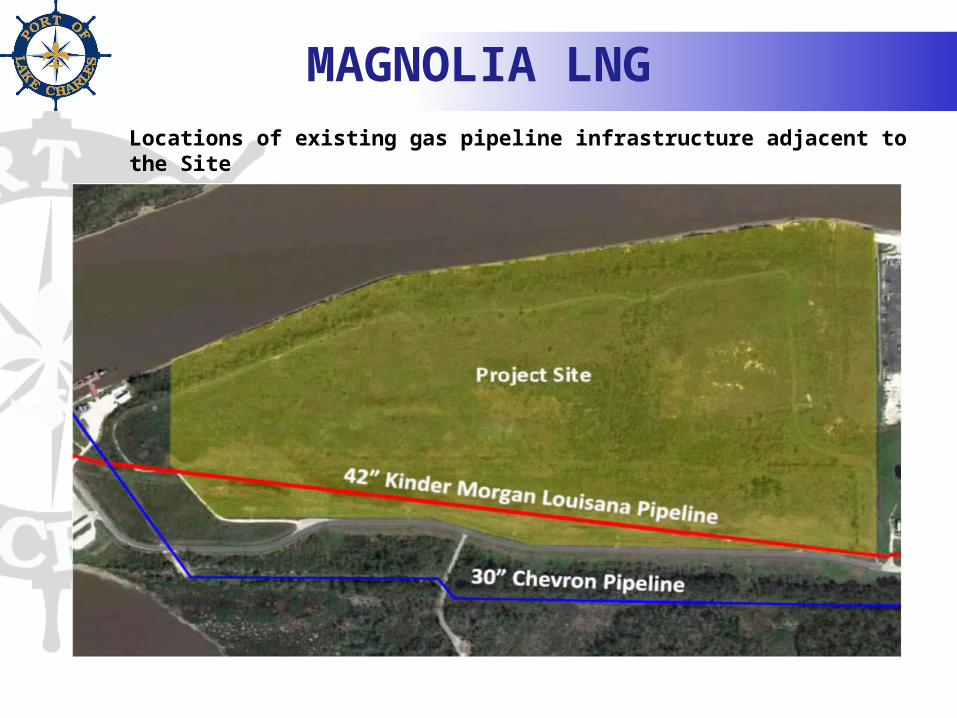

MAGNOLIA LNGLocations of existing gas pipeline infrastructure adjacent to the Site

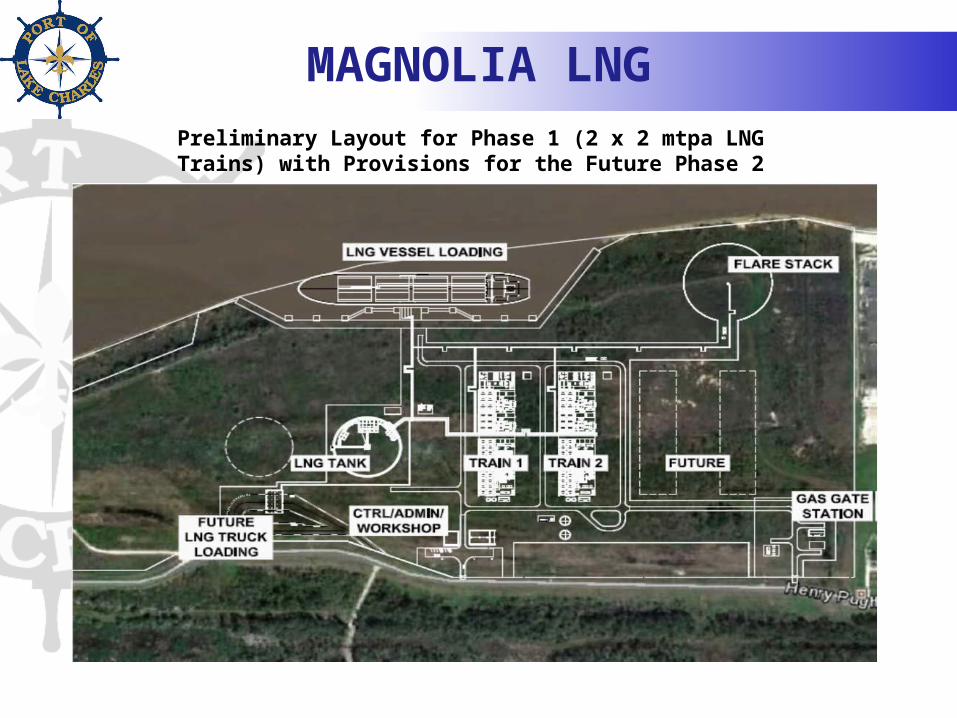

MAGNOLIA LNGPreliminary Layout for Phase 1 (2 x 2 mtpa LNG Trains) with

Provisions for the Future Phase 2

MAGNOLIA LNG

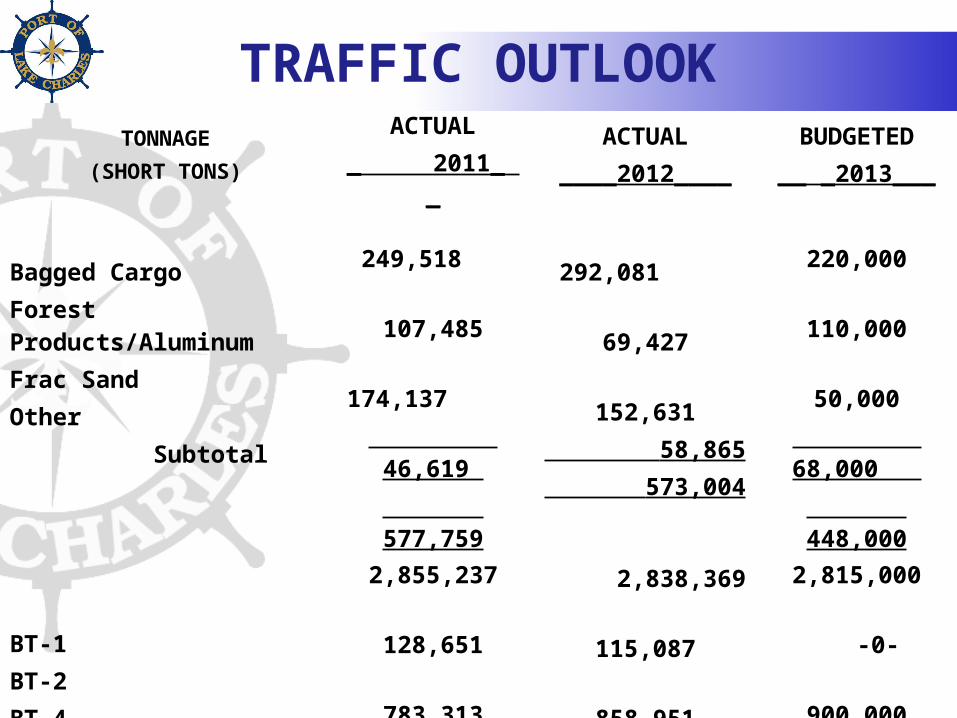

TRAFFIC OUTLOOKTONNAGE

(SHORT TONS)ACTUAL

_ 2011_ _ACTUAL

____2012____BUDGETED__ _2013___

Bagged CargoForest Products/AluminumFrac SandOther Subtotal

249,518 107,485

174,137 46,619 577,759

292,081 69,427 152,631 58,865 573,004

220,000 110,000 50,000

68,000 448,000

BT-1BT-2BT-4LNGAlcoa SubtotalTotal Port Traffic

2,855,237 128,651 783,313 482,335 641,056 4,890,592 5,468,351

2,838,369 115,087 858,951 180,011 605,462 4,597,880__ 5,170,884

2,815,000 -0- 900,000 100,000

529,740

4,344,740 4,855,740

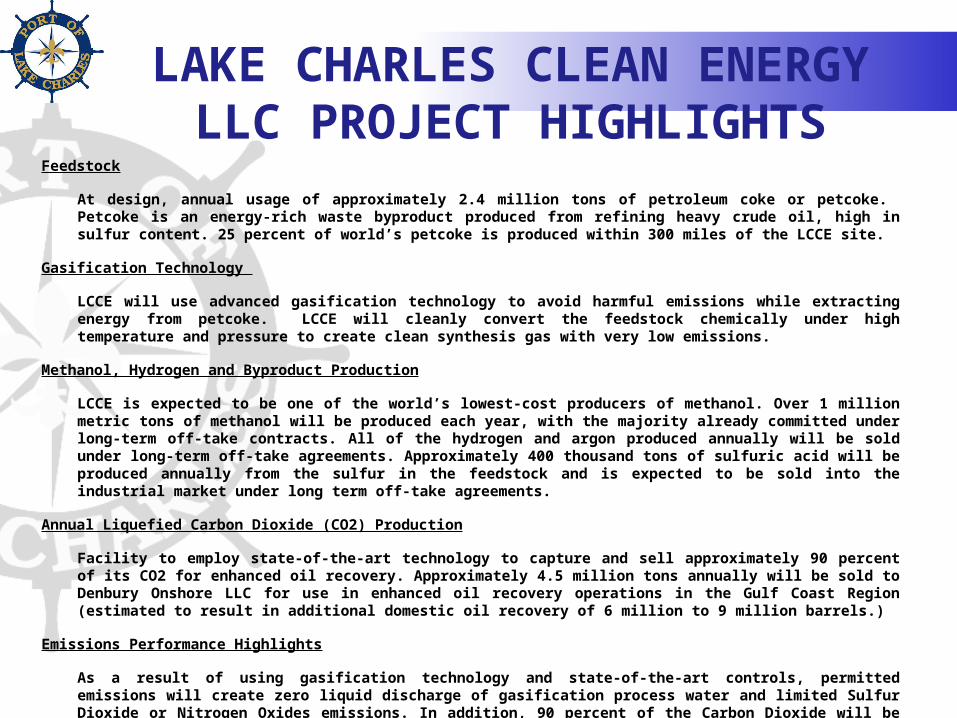

LAKE CHARLES CLEAN ENERGY LLC PROJECT HIGHLIGHTS

LAKE CHARLES CLEAN ENERGY LLC PROJECT HIGHLIGHTS

Feedstock

At design, annual usage of approximately 2.4 million tons of petroleum coke or petcoke. Petcoke is an energy-rich waste byproduct produced from refining heavy crude oil, high in sulfur content. 25 percent of world’s petcoke is produced within 300 miles of the LCCE site.

Gasification Technology

LCCE will use advanced gasification technology to avoid harmful emissions while extracting energy from petcoke. LCCE will cleanly convert the feedstock chemically under high temperature and pressure to create clean synthesis gas with very low emissions.

Methanol, Hydrogen and Byproduct Production

LCCE is expected to be one of the world’s lowest-cost producers of methanol. Over 1 million metric tons of methanol will be produced each year, with the majority already committed under long-term off-take contracts. All of the hydrogen and argon produced annually will be sold under long-term off-take agreements. Approximately 400 thousand tons of sulfuric acid will be produced annually from the sulfur in the feedstock and is expected to be sold into the industrial market under long term off-take agreements.

Annual Liquefied Carbon Dioxide (CO2) Production

Facility to employ state-of-the-art technology to capture and sell approximately 90 percent of its CO2 for enhanced oil recovery. Approximately 4.5 million tons annually will be sold to Denbury Onshore LLC for use in enhanced oil recovery operations in the Gulf Coast Region (estimated to result in additional domestic oil recovery of 6 million to 9 million barrels.)

Emissions Performance Highlights

As a result of using gasification technology and state-of-the-art controls, permitted emissions will create zero liquid discharge of gasification process water and limited Sulfur Dioxide or Nitrogen Oxides emissions. In addition, 90 percent of the Carbon Dioxide will be captured and used for enhanced oil recovery operations.

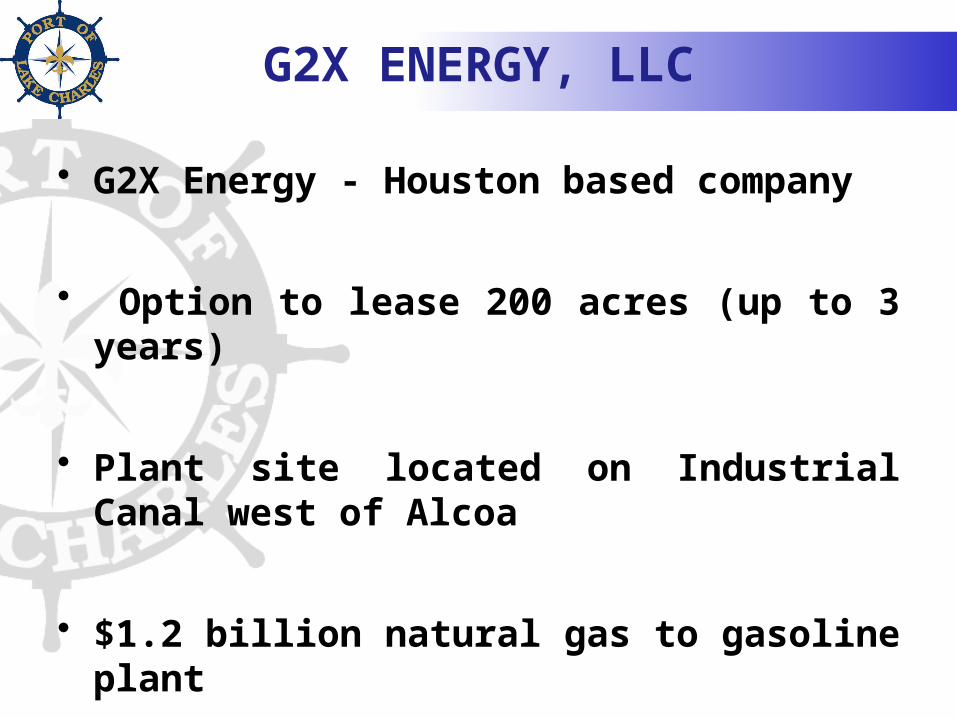

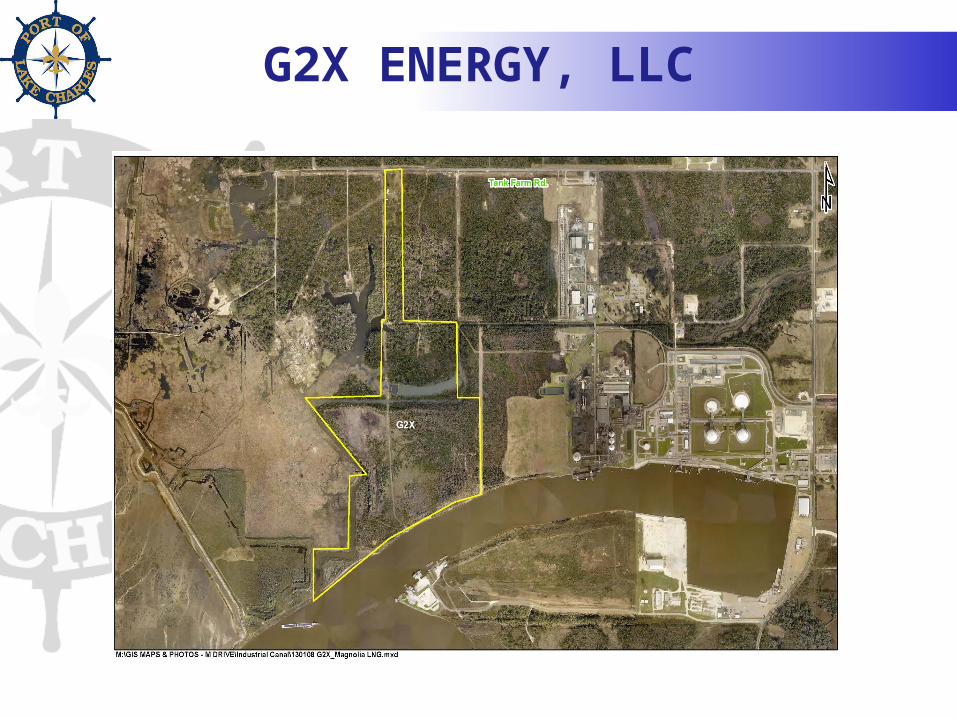

G2X ENERGY, LLC

• G2X Energy - Houston based company

• Option to lease 200 acres (up to 3 years)

• Plant site located on Industrial Canal west of Alcoa

• $1.2 billion natural gas to gasoline plant

G2X ENERGY, LLC

G2X ENERGY, LLC

• G2X is mostly owned and controlled by two major other companies - Southern Chemical Company and The Proman Group.

• Proman is a large international company based in Switzerland, Germany, and Trinidad, which constructs, operates, and maintains large methanol and other manufacturing facilities.

G2X ENERGY, LLC

• Proman is the largest world-wide manufacturer of methanol. Southern Chemical is also a major producer of methanol.

• G2X has obtained from ExxonMobil a proven process of manufacturing methanol from natural gas and then further processing it to produce gasoline.

• The plant will produce 12,500 barrels of gasoline per day. The gasoline will be sent out by pipeline and by barge or vessel.

NAVIGATION

• Channel Dredging and Funding

• Beneficial Use of Dredged Material

• The Future

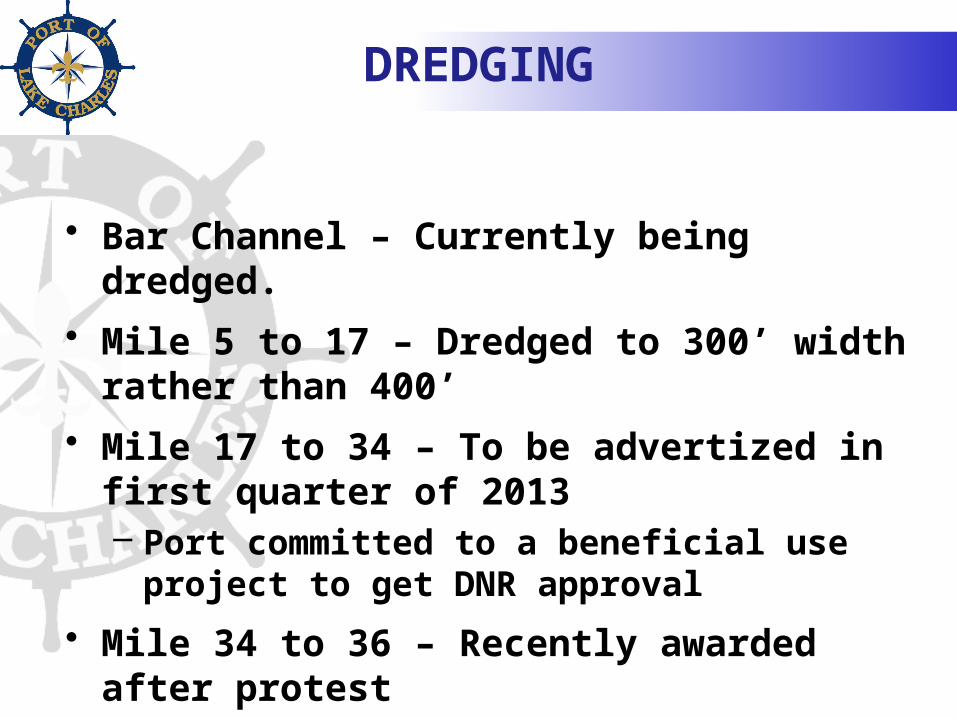

DREDGING

• Bar Channel – Currently being dredged.

• Mile 5 to 17 – Dredged to 300’ width rather than 400’

• Mile 17 to 34 – To be advertized in first quarter of 2013– Port committed to a beneficial use project to

get DNR approval

• Mile 34 to 36 – Recently awarded after protest

FUNDING

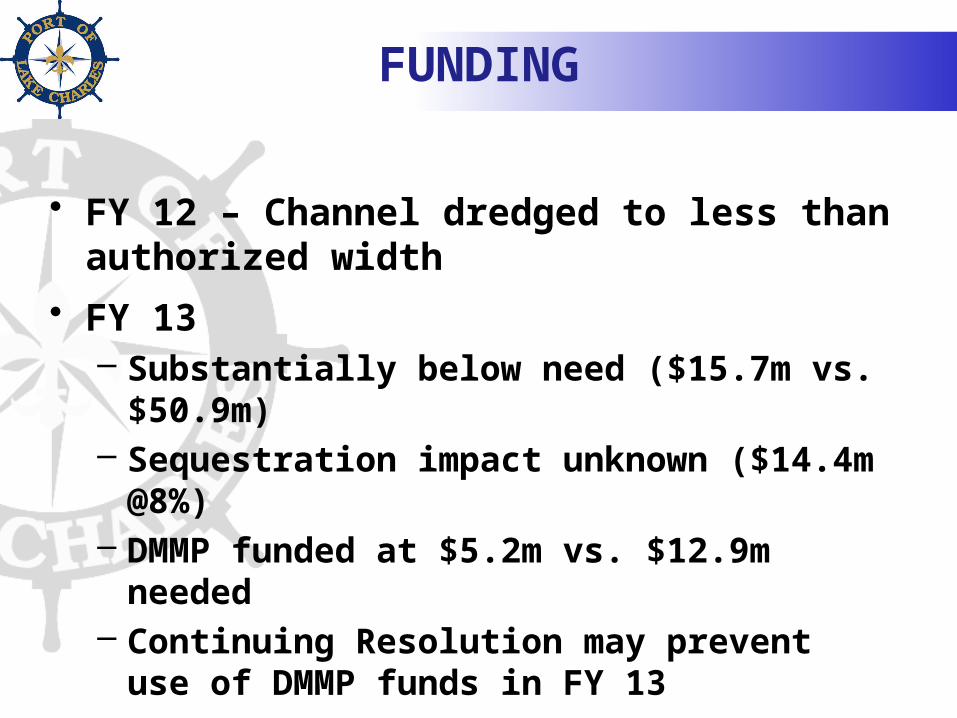

• FY 12 – Channel dredged to less than authorized width

• FY 13– Substantially below need ($15.7m vs. $50.9m)– Sequestration impact unknown ($14.4m @8%)– DMMP funded at $5.2m vs. $12.9m needed– Continuing Resolution may prevent use of

DMMP funds in FY 13

• FY 14 – No budget yet; Need $50m for O&M and DMMP

BENEFICIAL USE OF DREDGED MATERIAL

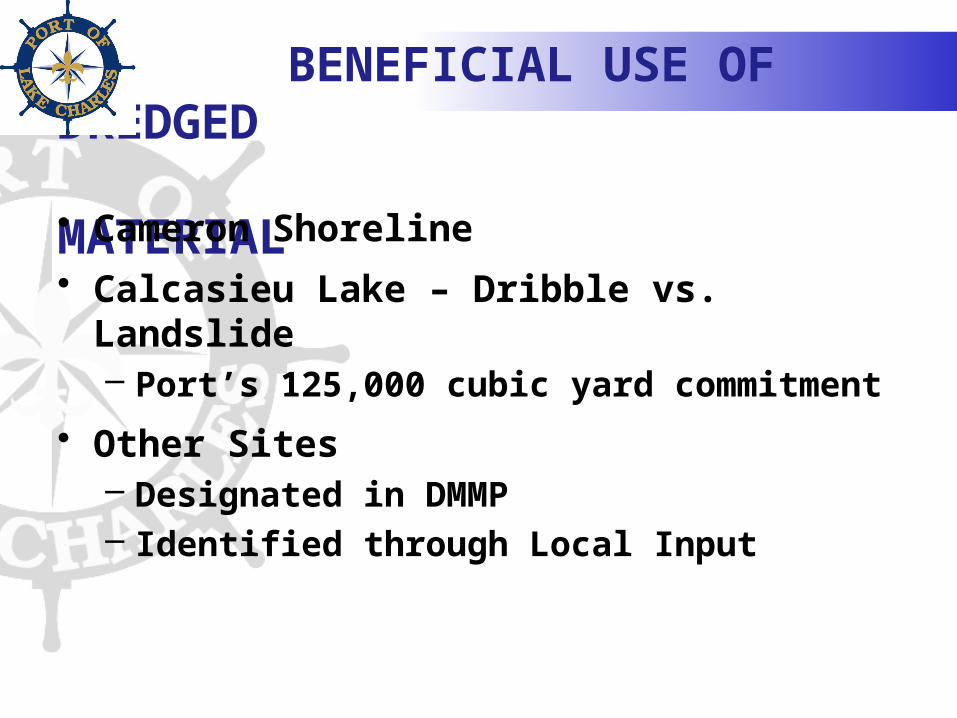

• Cameron Shoreline

• Calcasieu Lake – Dribble vs. Landslide– Port’s 125,000 cubic yard commitment

• Other Sites– Designated in DMMP– Identified through Local Input

FUTURE ISSUES

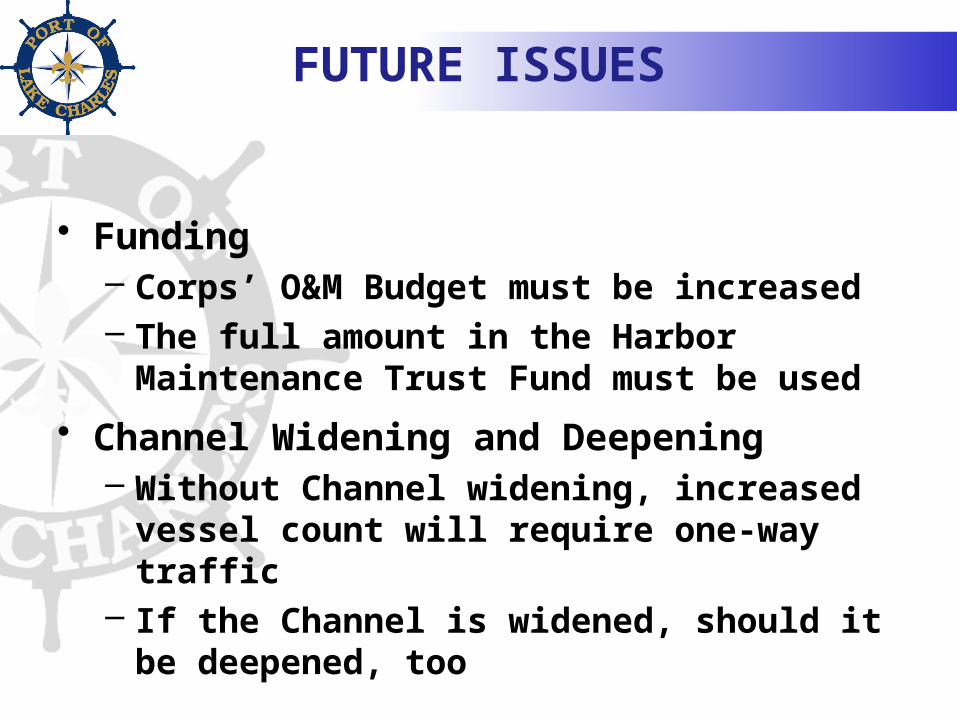

• Funding– Corps’ O&M Budget must be increased– The full amount in the Harbor Maintenance

Trust Fund must be used

• Channel Widening and Deepening– Without Channel widening, increased vessel

count will require one-way traffic – If the Channel is widened, should it be

deepened, too

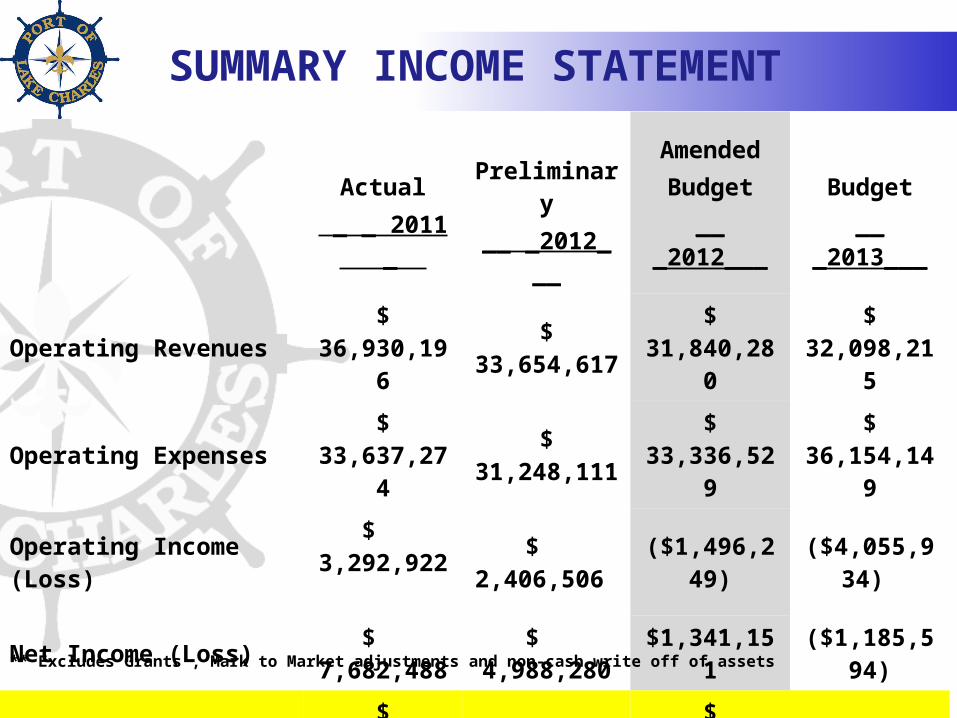

SUMMARY INCOME STATEMENT

Actual _ _ 2011 _

Preliminary__ _2012_ __

AmendedBudget

__ _2012___Budget

__ _2013___

Operating Revenues $ 36,930,196 $ 33,654,617 $ 31,840,280 $ 32,098,215

Operating Expenses $ 33,637,274 $ 31,248,111 $ 33,336,529 $ 36,154,149

Operating Income (Loss)

$ 3,292,922

$ 2,406,506 ($1,496,249) ($4,055,934)

Net Income (Loss) $ 7,682,488 $ 4,988,280 $1,341,151 ($1,185,594)

** Cash Flow $ 18,866,560 $ 16,287,925 $ 13,517,060 $12,738,346

** Excludes Grants , Mark to Market adjustments and non-cash write off of assets

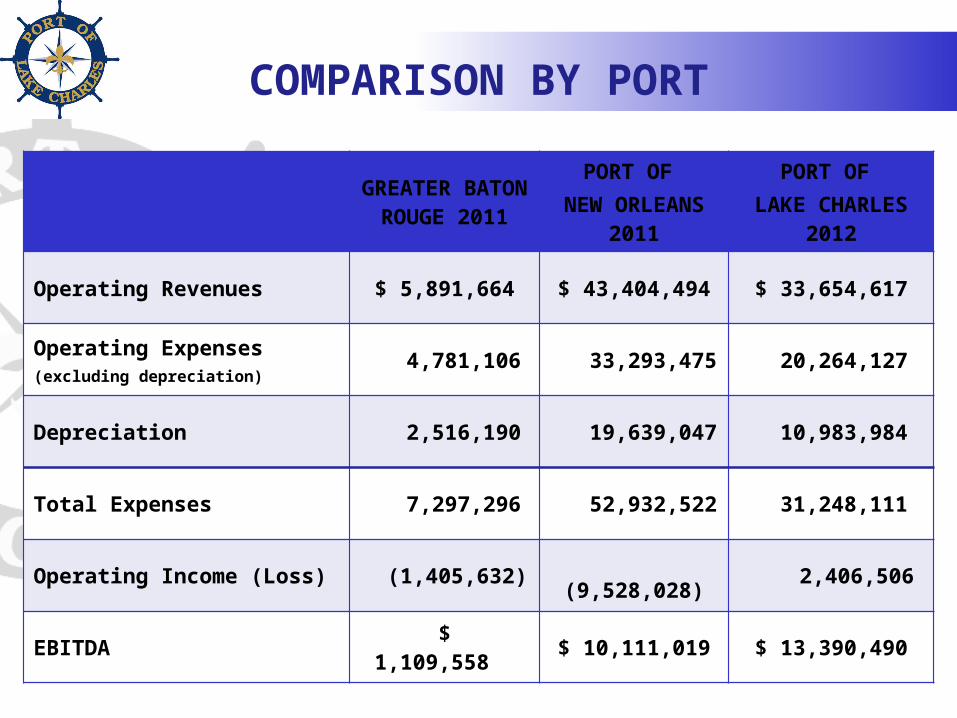

GREATER BATON ROUGE

2011

PORT OF NEW ORLEANS

2011

PORT OF LAKE CHARLES

2012

Operating Revenues $ 5,891,664 $ 43,404,494 $ 33,654,617

Operating Expenses(excluding depreciation)

4,781,106 33,293,475 20,264,127

Depreciation 2,516,190 19,639,047 10,983,984

Total Expenses 7,297,296 52,932,522 31,248,111

Operating Income (Loss) (1,405,632) (9,528,028) 2,406,506

EBITDA $ 1,109,558 $ 10,111,019 $ 13,390,490

COMPARISON BY PORT

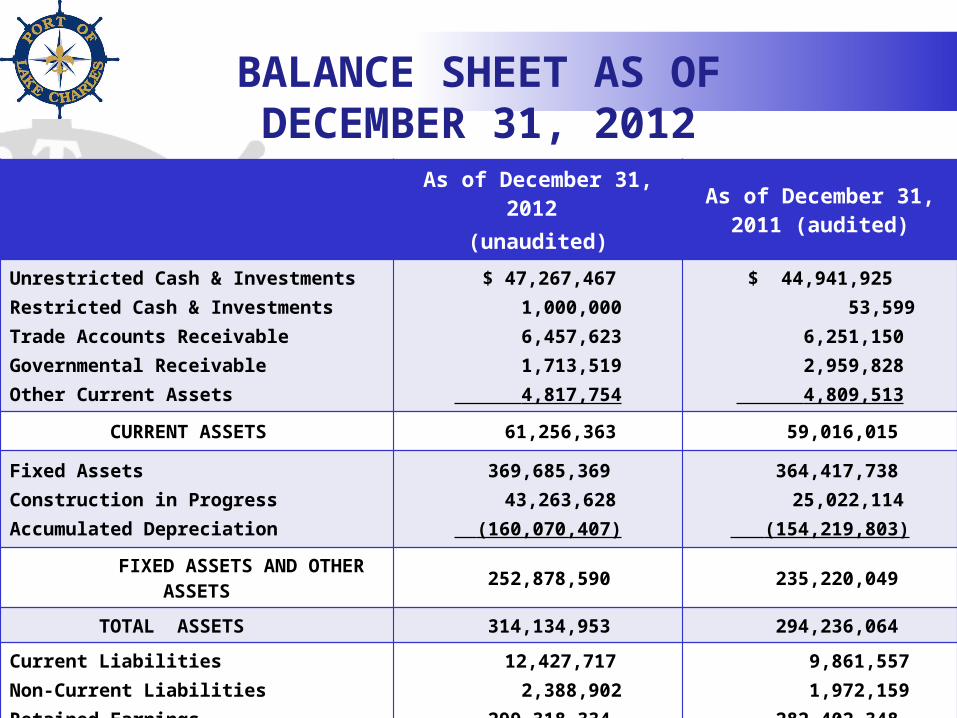

As of December 31, 2012 (unaudited)

As of December 31, 2011 (audited)

Unrestricted Cash & InvestmentsRestricted Cash & InvestmentsTrade Accounts ReceivableGovernmental ReceivableOther Current Assets

$ 47,267,467 1,000,000 6,457,623 1,713,519 4,817,754

$ 44,941,925 53,599 6,251,150 2,959,828 4,809,513

CURRENT ASSETS 61,256,363 59,016,015

Fixed AssetsConstruction in ProgressAccumulated Depreciation

369,685,369 43,263,628

(160,070,407)

364,417,738 25,022,114

(154,219,803)

FIXED ASSETS AND OTHER ASSETS 252,878,590 235,220,049

TOTAL ASSETS 314,134,953 294,236,064

Current LiabilitiesNon-Current LiabilitiesRetained Earnings

12,427,717 2,388,902 299,318,334

9,861,557 1,972,159 282,402,348

TOTAL LIABILITIES & EQUITY $314,134,953 $294,236,064

BALANCE SHEET AS OFDECEMBER 31, 2012

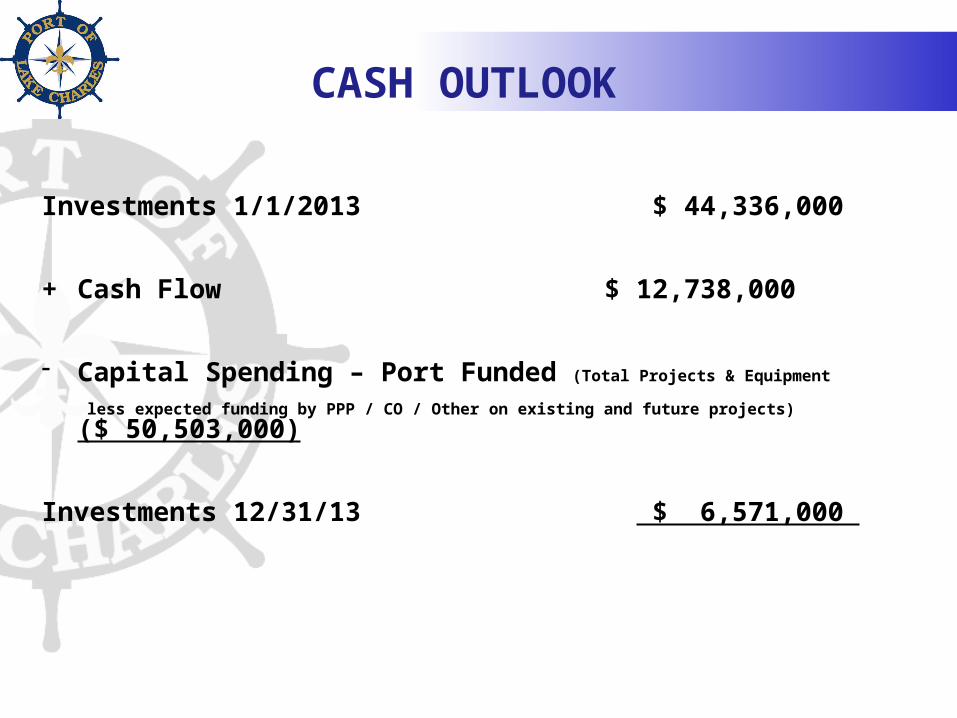

CASH OUTLOOK

Investments 1/1/2013 $ 44,336,000

+ Cash Flow $ 12,738,000

- Capital Spending – Port Funded (Total Projects & Equipment

less expected funding by PPP / CO / Other on existing and future projects) ($ 50,503,000)

Investments 12/31/13 $ 6,571,000

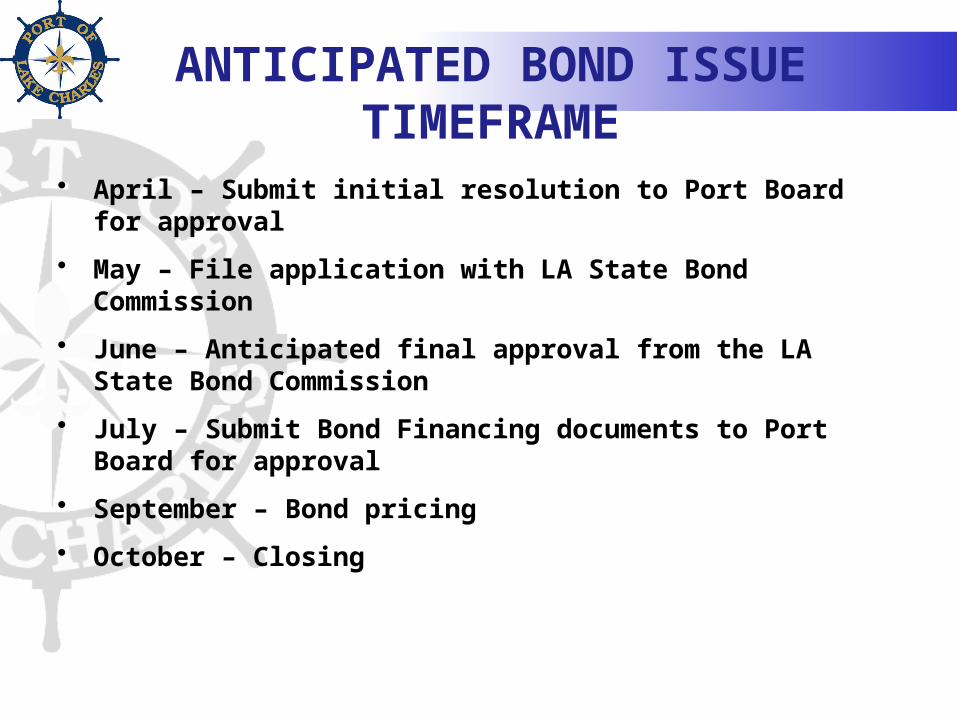

ANTICIPATED BOND ISSUE TIMEFRAME

• April – Submit initial resolution to Port Board for approval

• May – File application with LA State Bond Commission

• June – Anticipated final approval from the LA State Bond Commission

• July – Submit Bond Financing documents to Port Board for approval

• September – Bond pricing

• October – Closing

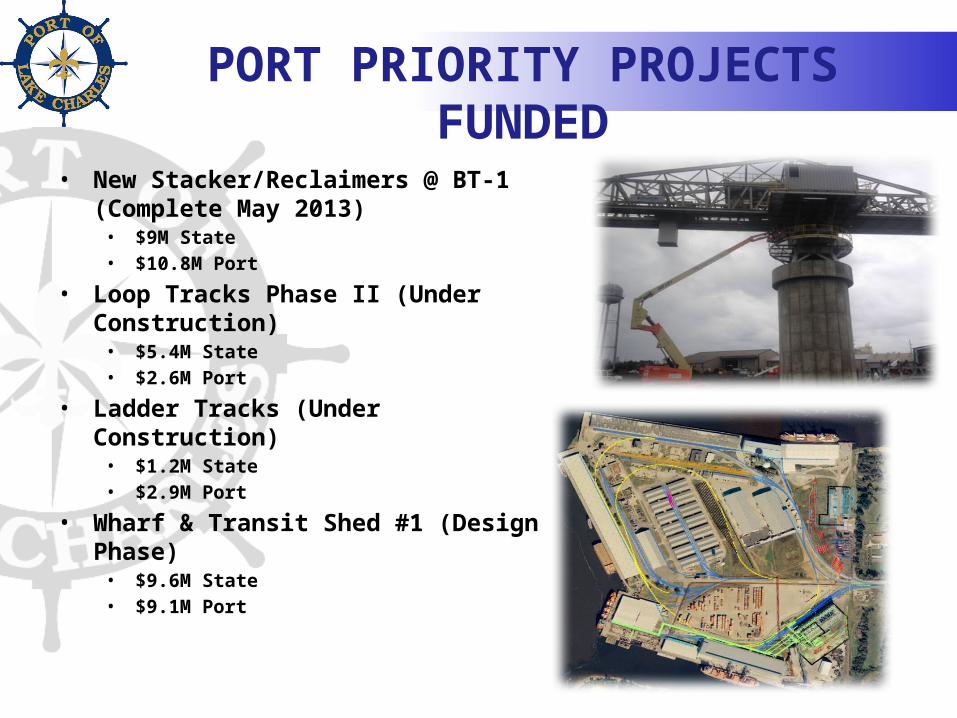

PORT PRIORITY PROJECTS FUNDED

• New Stacker/Reclaimers @ BT-1 (Complete May 2013)• $9M State• $10.8M Port

• Loop Tracks Phase II (Under Construction)• $5.4M State• $2.6M Port

• Ladder Tracks (Under Construction)• $1.2M State• $2.9M Port

• Wharf & Transit Shed #1 (Design Phase)• $9.6M State• $9.1M Port

PORT PRIORITY PROJECTS REQUESTED

• New Dry Bulk Dock @ BT-1– $5.4M State (requested)– $34.6M Port

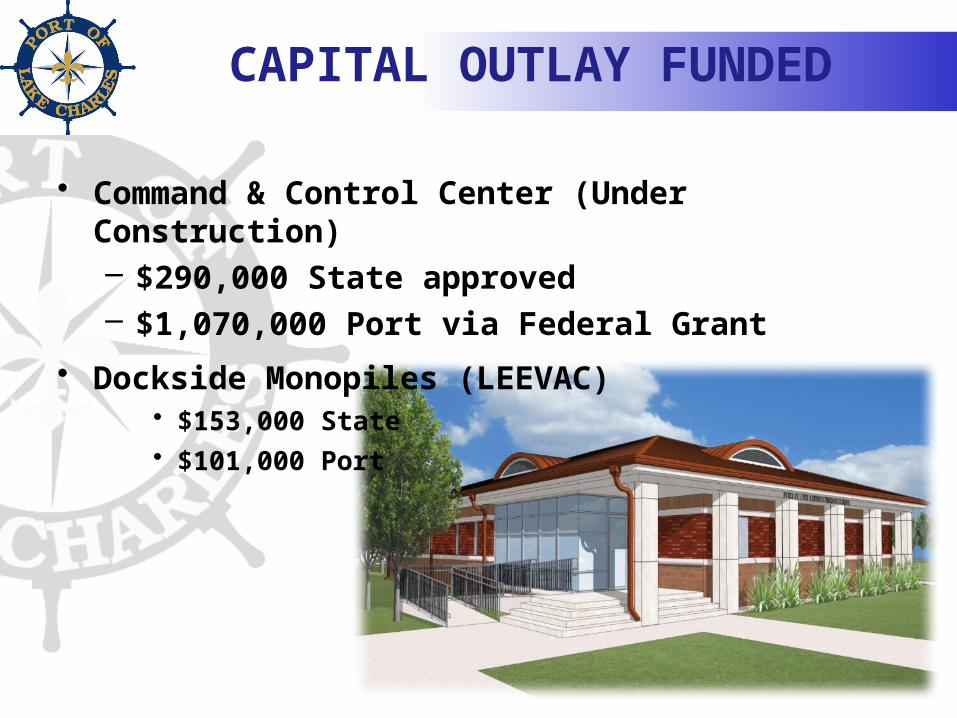

CAPITAL OUTLAY FUNDED

• Command & Control Center (Under Construction)– $290,000 State approved– $1,070,000 Port via Federal Grant

• Dockside Monopiles (LEEVAC)• $153,000 State• $101,000 Port

CAPITAL OUTLAY REQUESTED

• Sallier Lead Track Relocation– $1M

• Berth 8 Dredging– $250,000

• New Administration Building– $500,000

![Erasmus University Rotterdam · bodies, A Laboratory Manual (Cold Spring Harbor Lab- oratory, Cold Spring Harbor, NY, 1988)]. Rabbit anti- bodies to the COOH-terminal amino acids](https://img.pdfslide.us/doc/110x75/607b213bb9713323502f80da/erasmus-university-rotterdam-bodies-a-laboratory-manual-cold-spring-harbor-lab-.jpg)