Embed Size (px)

Citation preview

2013 ENERGY SECTOR PROGRAM PHASE-2 PROJECT

EU IPA13/CS-02.a

Energy Market Development

GAS TARIFF TRAINING

Ankara, 7-9 January 2019

Training contents – Day 1

1. Basic economics of tariff and price regulation

2. Overview of the main international market models and related tariff regimes

3. The tariffs regulatory process in the U.S. and Europe

4. Revenue Requirement calculation

a. The asset base

b. The rate of return

c. Depreciation and operational costs

d. Excel Work: RAB calculation, WACC and depreciation

2

Training contents – Day 2

5. Tariff review and adjustment

a. North American approach

b. Revenue/Price Cap

c. Excel Work: Implementing tariff adjustment and a regulatory account

6. Transmission Tariff Design

a. Main approaches: Point-to Point, Postage Stamp, Entry-Exit

b. Issues in entry-exit tariff setting

c. The EU Tariff Network Code and practices

d. Excel Work: Transmission Tariff Design

3

Training contents – Day 3

7. LNG Regasification and Storage tariffs

8. Distribution tariff design and Benchmarking (Annex 2)

9. End user pricing

10. Discussion of current Turkish tariffs

11. Optional: Role Game on Transmission tariff regulatory

regimes and design

4

5

Part 1

PRICING AND REGULATION:

A BIT OF THEORY

6

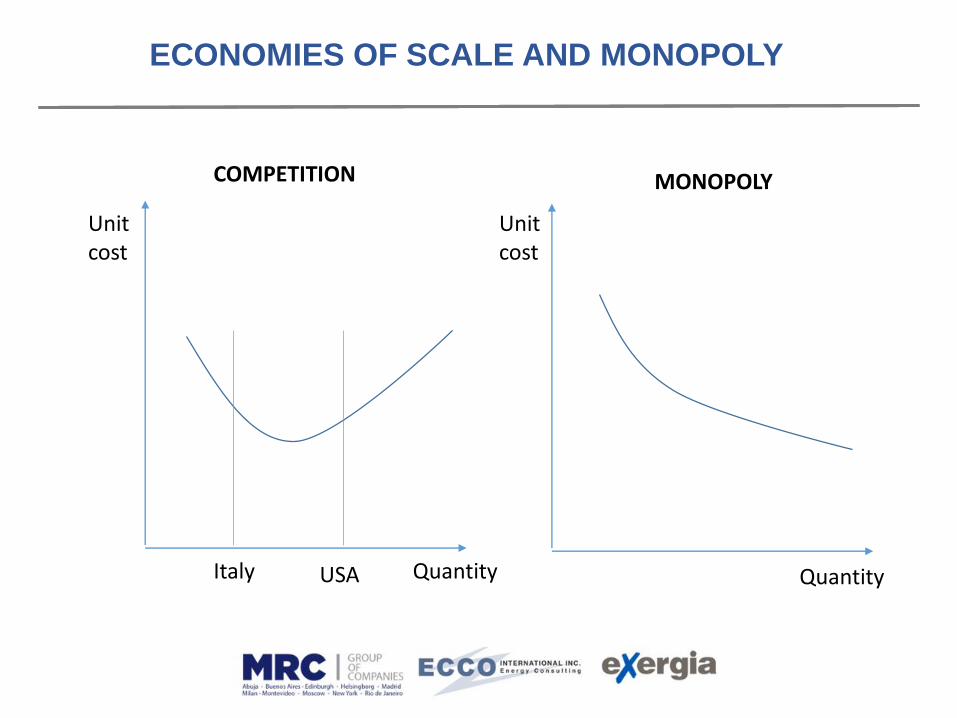

ECONOMIES OF SCALE AND MONOPOLY

In most industries, unit production costs tend to decrease with production level, but increase beyond a certain level

However, in several network industries (railways, roads, power and gas transmission and distribution, water…), the larger the production, the lower the cost

Therefore, companies tend to concentrate (merge) to achieve lower cost, within the relevant marketMonopoly

Competition may be impossible, therefore price regulation is necessary

It often depends on market size: competition between gas transportation companies may be feasible in the USA, but not in Italy

ECONOMIES OF SCALE AND MONOPOLY

Unit cost

Unit cost

Quantity Quantity

COMPETITION MONOPOLY

Italy USA

8

WHY REGULATE PRICES? (THE ECONOMIC CASE / 1)

Suppliers and network operators may abuse market power

• If gas supply is bundled, supplier enjoys monopoly position oftransmission and/or distribution and requires regulation

• Gas network operators are almost always in a monopoly position atnational, local or intermediate level

• Even if the network is unbundled and regulated, the supplier mayhave a strong market power

• Competition from other fuels usually weak, except in early stage ofdevelopment

• Exception: Competition from coal for power generator often strongif coal fire power stations available

9

PRICING UNDER INTERFUEL COMPETITION (1)

Companies may have no rivals in gas supply but face substantial competition from other energy sources that can be used for the same purposes: coal, fuel oil, fuelwood, renewable energy, nuclear…)

Competition is stronger in power generation, cement, steel but weaker in other industries and in the residential & commercial sector

Monopolistic or dominant gas suppliers carefully study consumption patterns and related costs, so as to be able to get the highest price from consumers that are able to pay more (price discrimination)

Individual pricing is usually confidential

10

PRICING UNDER INTERFUEL COMPETITION (2)

Profits may be used to cross-subsidise other consumers, provided

they can pay at least the gas purchase price

From an economic analysis perspective, perfect price

discrimination is efficient, as it does not lead to sales restriction

But, price discrimination may be seen as unfair and exploitative

If the regulatory framework or moral feelings do not allow

individual pricing, the company may still choose imperfect

discrimination:

• Decreasing block tariffs, where larger consumers pay less

• Fixed and or capacity-related charges, whereby stable (high load)

consumers pay less

• Discrimination may also be achieved on a geographical basis

11

WHY REGULATE PRICES? THE SOCIAL / ENVIRONMENTAL CASE

Gas and/or goods produced with it are key universalservices or essential goods for economic development• Mostly electricity, food, fertilisers, cement, space heating

Gas is less polluting than other fossil fuels and it should be incentivized to lure consumers away from other fuels, fighting:• Harmful use of traditional fuels (fuelwood, charcoal, peat, solid

wastes) in less developed areas

• Urban air pollution in cities

• Regional pollution (acid rain, dust)

• Climate change

by substituting coal, oil derivatives and fuelwood in thermal uses and power generation

12

PM

Q

PS

Marginal

cost

Demand

CS

PR

Q

PS Demand

Marginal

cost

CS

HOW TO REGULATE PRICES: ECONOMIC ANALYSIS

• Golden rule: Price = Long Run Marginal Cost (PC), to be set below monopoly price PM

• If prices are “too high” or “too low”, social welfare (i.e. sum of Consumer and Producer Surplus) is not optimal (maximised)

• If regulated prices = average cost, CS may be higher than under P = LRMC, but social welfare (CS+PS) will be lower

• Political support for regulated price PR = AC < LRMC

• Monopoly price may be too high, but regulated price may be too low

• Too low prices would hamper development and trigger shortages

Averagecost

PC

13

Part 2

OVERVIEW OF GAS MARKET MODELS

14

THE GAS VALUE CHAIN: DRAWING THE LINE BETWEEN COMPETITION & MONOPOLY

EXPORTS

EXPLORATION

PRODUCTIONIMPORTS

LOW PRESSURE

DISTRIBUTION

LARGE CUSTOMERS

(POWER GENERATORS,

INDUSTRY)

HIGH PRESSURE PIPELINE SYSTEM

GAS

STORAGE

SMALL CUSTOMERS (HOUSEHOLDS, SMEs)

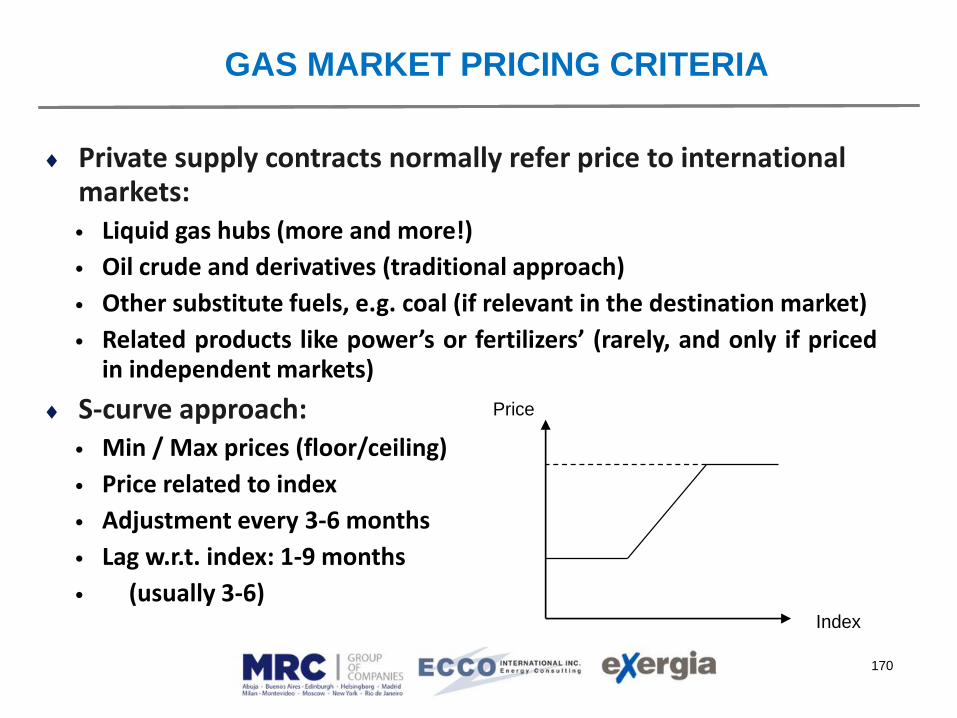

GAS PRICING WITHOUT REGULATION?

Gas industry often developed in competition with other energy sources (oil derivatives, coal, electricity)

Interfuel competition can be effective in the early stages of the industry and in new locations, hence price regulation not needed

Pipeline to pipeline (and LNG) competition may also be substantial in some regions (North America only?)

Unregulated natural gas pricing has prevailed in some countries (Germany, Italy, Netherlands…), notably for large customers

15

TARIFF REGULATION: WHY & WHERE (1)

If a monopolist sells gas, it could exploit consumers by settingprices well above average costs, achieving excess profits

In the traditional market model, gas is sold (in the wholesalemarket) by a monopolist (integrated company)

• Thus, the whole selling price should be regulated

• Transmission and distribution tariff are just parts of the integratedregulated price

In the liberalised market model, gas is sold at market pricesat least to some (eligible) customers

• Commercial flows tend to diverge from physical flows

• Tariff regulation in principle limited to networks (transmission,distribution) and essential facilities (storage? LNG terminals?)

16

17

THE TRADITIONAL MODEL

Integrated gas transportation and supply by amonopolist• Gas produced or purchased by long term contracts

Gas selling price (formally or informally) regulated• For large customers and power generation, competition by

alternative fuels (oil derivatives, coal…)

• Collective agreements or state/local govt. control often replaceformal regulation

No retail competition for smaller customers

Limited pipe to pipe competition

18

THE TRADITIONAL MARKET MODEL

DOMESTIC

PRODUCTION

GAS

IMPORTS

DISTRIBUTION AND

RETAIL COMPANIESLARGER

CUSTOMERS

INTEGRATED TRANSPORTATION AND WHOLESALE COMPANIES

GAS

STORAGE

SMALLER

CUSTOMERS

Individual or collective

negotiation, State control

Regulation

19

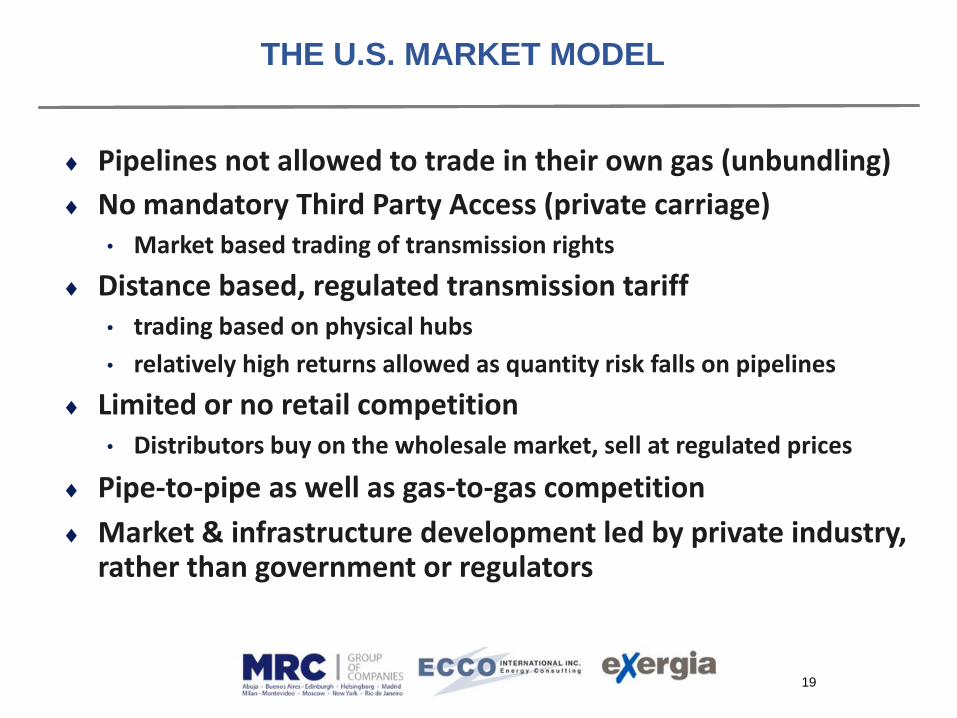

THE U.S. MARKET MODEL

Pipelines not allowed to trade in their own gas (unbundling)

No mandatory Third Party Access (private carriage)• Market based trading of transmission rights

Distance based, regulated transmission tariff• trading based on physical hubs

• relatively high returns allowed as quantity risk falls on pipelines

Limited or no retail competition• Distributors buy on the wholesale market, sell at regulated prices

Pipe-to-pipe as well as gas-to-gas competition

Market & infrastructure development led by private industry, rather than government or regulators

THE EU MARKET MODEL

Ownership unbundling (or tight regulatory control) oftransmission networks

Tariff regulation of transmission:• Entry-exit model

• Productivity incentives through “price caps”

• May also regulate storage and LNG regasification

• Temporary retail price control, notably for small customers

Detailed market rules, included in Network Codes Retail competition for all customers

• Liquidity promoted in the “virtual hub” created “on the grid”

• Measures for competition transparency and/or gas release

• Quality of service, consumer rights regulated

New infrastructure subject to govt./regulatory approval

20

21

THE EU MARKET MODEL

DOMESTIC

PRODUCTION

PIPELINE

IMPORTS

DISTRIBUTION (TPA)ELIGIBLE

CUSTOMERS

SHIPPERS (TRADERS, SUPPLIERS)

UNDERGROUND STORAGE

TRANSPORTATION (TPA)

FRANCHISED CUSTOMERS

LNG

REGASIFICATION

Regulated activities

22

Question 1: Which gas market model is best for Turkey?

(Please give an opinion whatever the current market model)

1. Traditional: Monopoly with fully regulated tariffs and prices

2. Liberalised market US-style, unbundled transmission but no mandatory TPA, trading in physical hubs, retail competition for large customers and distributors

3. Liberalised market EU-style, unbundled transmission and mandatory TPA, trading in virtual hubs, retail competition for all customers

4. No regulation is necessary, because of inter-fuel competition

23

EU: THE “THIRD PACKAGE”

Strong unbundling

• ownership, or strengthened regulatory control (IndependentTransmission Operator), or ISO (TSO w/o assets

• regulatory checks on investments

European TSO co-ordination (ENTSO-G)

European Regulators’ Coordination Agency (ACER) born with limited powers • notably on cross border disputes, market monitoring

Security of Supply Regulation

Infrastructure Package

Part 3

THE TARIFF SETTING PROCESS

OBJECTIVES OF TARIFF SYSTEM (1)

Objectives of the “market liberalisation” wave, starting inthe 1980s:

• Provide consumers with a choice between suppliers, at least on thewholesale market

• Allow Third Party Access at least to the Transmission network(possibly, also to distribution and other services)

• Provide level playing field between suppliers, including theincumbent (network owner), with a view to encourage entry andinvestment by new suppliers

• Ensure that costs of transmission operators are covered, providedthey are efficient

• Incentivize network companies to become more efficient

25

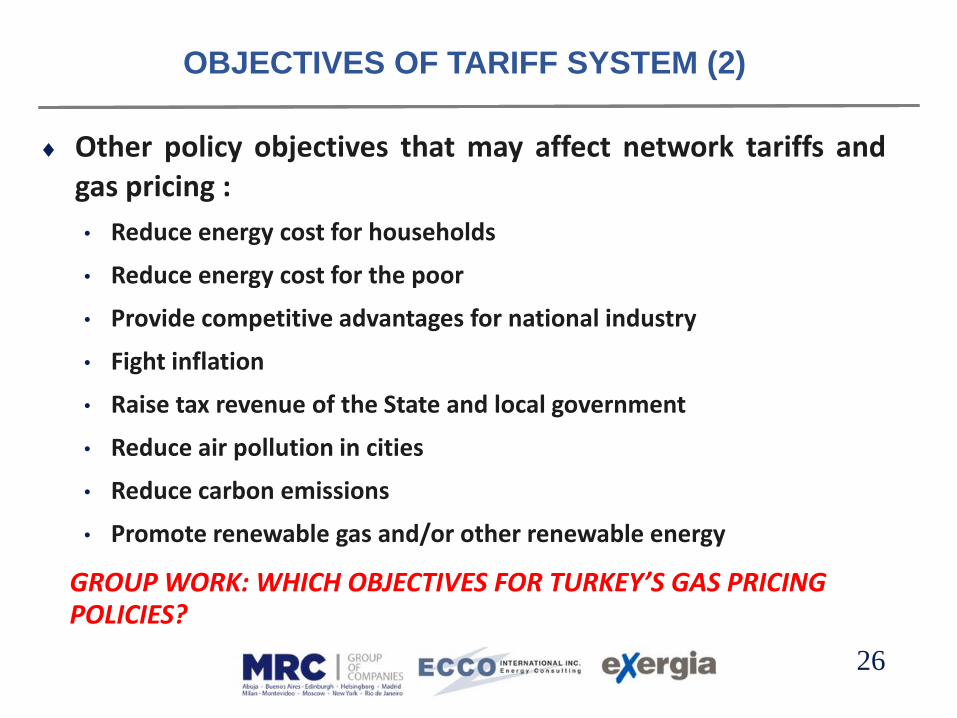

OBJECTIVES OF TARIFF SYSTEM (2)

Other policy objectives that may affect network tariffs andgas pricing :

• Reduce energy cost for households

• Reduce energy cost for the poor

• Provide competitive advantages for national industry

• Fight inflation

• Raise tax revenue of the State and local government

• Reduce air pollution in cities

• Reduce carbon emissions

• Promote renewable gas and/or other renewable energy

GROUP WORK: WHICH OBJECTIVES FOR TURKEY’S GAS PRICING POLICIES?

26

COMMON KEY REGULATORY VALUES

Independence from regulated industry

Independence from elected governments

Transparency of decisions

Accountability towards Parliament, public opinion

Involvement of stakeholders, including weak ones

Fact based decision making process

Decisions subject to appeal

Notice: Achievement of such values is a long process!

27

Part 3.1

NORTH AMERICAN APPROACH: THE RATE CASE

(Based on information kindly provided byChristopher G. Lipscombe, Senior Attorney Advisor, District of Columbia Public Service Commission )

PUBLIC UTILITY COMMISSIONS (1)

Public Utility (or Public Service) Commissions in the U.S. areestablished in each State, plus D.C.

The Commissioners are appointed by Governor, subject toState Senate approval, staggered terms

Federal Energy Regulatory Commission (FERC), is in charge ofInterstate activities, and other issues of Federal relevance

• Appointed by President, subject to U.S. Senate approval, with

staggered terms

Canadian Provincial Regulatory Tribunals are similar to PUCs

29

PUBLIC UTILITY COMMISSIONS (2)

PUCs in the U.S. operate as Quasi Judicial Agencies

The Commissioners are the judges

All staff involved in formal cases are advisors to theCommissioners

The Budget of PUCs and FERC is raised through charges onthe sales of regulated companies

Special fees are charged for rate cases (not more than 0.25%of the company’s legal value)

30

THE STAKEHOLDERS

Private or Government owned regulated companies

Public Utility Customers

Office of the People’s Counsel (OPC) – Consumer Advocate

Other Government Agencies (e.g. FERC, other State orFederal Agencies / Departments)

Private Intervenors – e.g. Apartment & Office BuildingAssociation, Competitive Suppliers

31

RULEMAKING PROCESS STEPS

A stakeholder (normally the regulated company) ask theCommission for Rulemaking

The Commission issues a Notice of Proposed Rulemaking(sometimes preceded by Notice of Investigation)

Further Notice of Proposed Rulemaking (if necessary)

Notice of Final Rulemaking

Commission issues a Report and Order

Stakeholders may ask for Reconsideration

If granted a final Order is issued

32

RATE CASE PROCESS (1)

Most rate cases take 9-10 months to litigate

The utility company files an application for a rate increase,along with supporting documentation.

The Commission issues an Order, defining issues to beconsidered in the case.

The utility company files evidence on designated issues (e.g.proof of increased costs.

Other parties may file data requests, to which the utilitycompany responds.

Parties may file their own evidence

The Commission considers and discusses all evidence

33

RATE CASE PROCESS (2)

The Commission conducts a formal evidentiary hearingwherein the attorneys for each party cross-examine thewitnesses (experts) and the Commissioners ask questions

The Commission holds 3 community hearings in 3 differentwards of the District (State); one on a Saturday; one in theafternoon, and one during the evening.

Within 90 days of the close of the record, the Commissionissues a decisional order, after which parties have 30 days tofile an application for reconsideration.

34

RATE CASE PROCESS (3)

The utility is directed to file revised rate schedules, afterwhich the new rates go into effect.

After the Commission issues its Order, the parties can appealall or part of the decision to the relevant Court of Appeals.

In the U.S., rate cases are usually started by regulatedcompanies, but could be started by other stakeholders as well

It is a costly and long process, for PUC charges, legal costs,documentation preparation

Rate cases are usually undertaken only in case costs haveseriously increased

35

Part 3.2

EUROPEAN APPROACH:

REGULATED TARIFF SETTING

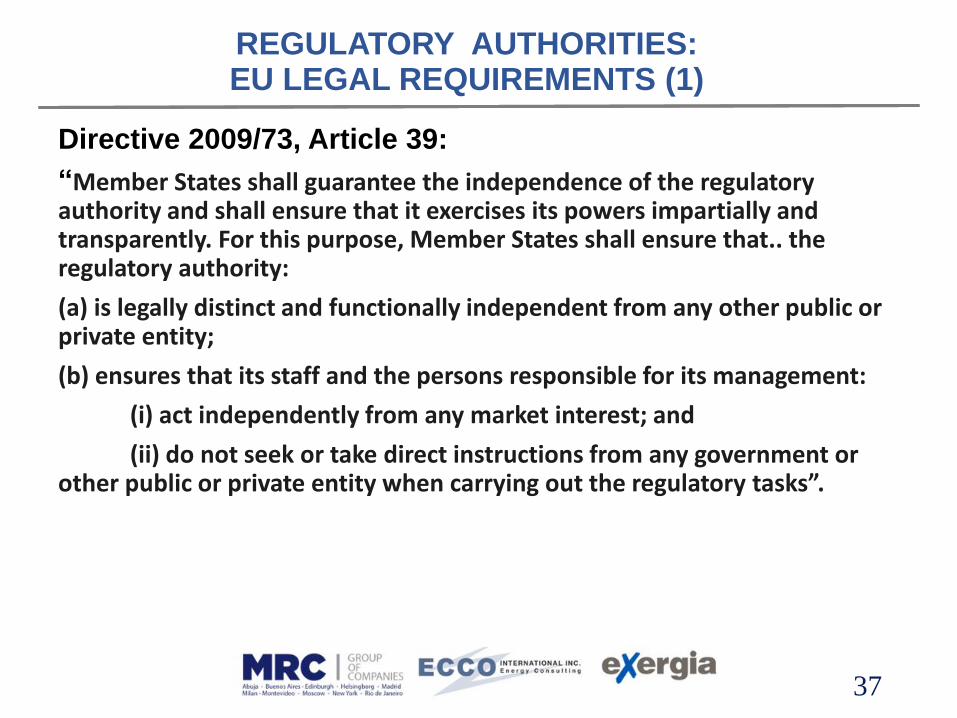

REGULATORY AUTHORITIES: EU LEGAL REQUIREMENTS (1)

Directive 2009/73, Article 39:

“Member States shall guarantee the independence of the regulatory authority and shall ensure that it exercises its powers impartially and transparently. For this purpose, Member States shall ensure that.. the regulatory authority:

(a) is legally distinct and functionally independent from any other public or private entity;

(b) ensures that its staff and the persons responsible for its management:

(i) act independently from any market interest; and

(ii) do not seek or take direct instructions from any government or other public or private entity when carrying out the regulatory tasks”.

37

REGULATORY AUTHORITIES: EU LEGAL REQUIREMENTS (2)

Directive 2009/73, Article 40 (Objectives):

• Promoting… a competitive, secure and environmentally sustainableinternal market in natural gas

• Effective market opening for all customers and suppliers

• Eliminating restrictions on trade between Member States

• Helping to achieve, in the most cost-effective way, the developmentof secure, reliable and efficient non-discriminatory systems that areconsumer oriented

• Promoting system adequacy and energy efficiency

• Grant appropriate incentives to increase efficiencies in systemperformance and foster market integration

• Promoting competition, protection of consumers (esp. vulnerable);

• Helping to achieve high standards of public service for natural gas,

• Facilitating customer switching.

38

REGULATORY AUTHORITIES: EU LEGAL REQUIREMENTS (3)

Directive 2009/73, Article 41 (Duties and powers):

• Fixing or approving, in accordance with transparent criteria,transmission or distribution tariffs or their methodologies;

• Ensuring compliance of transmission and distribution systemoperators… with the Directive and other relevant Communitylegislation

• Reporting annually on its activity and the fulfilment of its duties tothe relevant authorities of the Member States, the Agency and theCommission

• Ensuring that there are no cross-subsidies between transmission,distribution, storage, LNG and supply activities

• Issuing binding decisions on regulated companies and entities

• Investigating and accessing data

• Issuing penalties for non-compliance

39

ISSUING TARIFFS OR METHODOLOGIES?

Case 1. Regulator calculates and issues tariffs, after collectingnecessary data from companies

Case 2. Regulator issues a calculation methodology

• Sub-case 2.1. Company calculates tariffs, submits for check and

approval/rejection by Regulator (e.g. Italy)

• Sub-case 2.2. Company calculates and issues tariffs. Regulator checks

them (ex-post), may change them if found wrong (e.g. Austria,

Germany)

• Sub-case 2.3. Company calculates and issues tariffs. Regulator checks

them (ex-post), if wrong refers company to higher level body (e.g. UK)

40

REGULATORY AUTHORITIES: EU LEGAL REQUIREMENTS (4)

Directive 2009/73, Article 41 (Monitoring responsibilities):

• Investment plans of the transmission system operators, and assessinginvestment plans’ consistency with the Community-wide networkdevelopment plan

• Market transparency

• Effective market opening

• Restrictive commercial practices

• Access to storage and ancillary services

• Connection and disconnection services

• Supply prices (in relation to their cost reflectivity)

• Consumer consumption data

• Effectiveness of customer protection measures

• Implementation of market rules and obligations of system operators

41

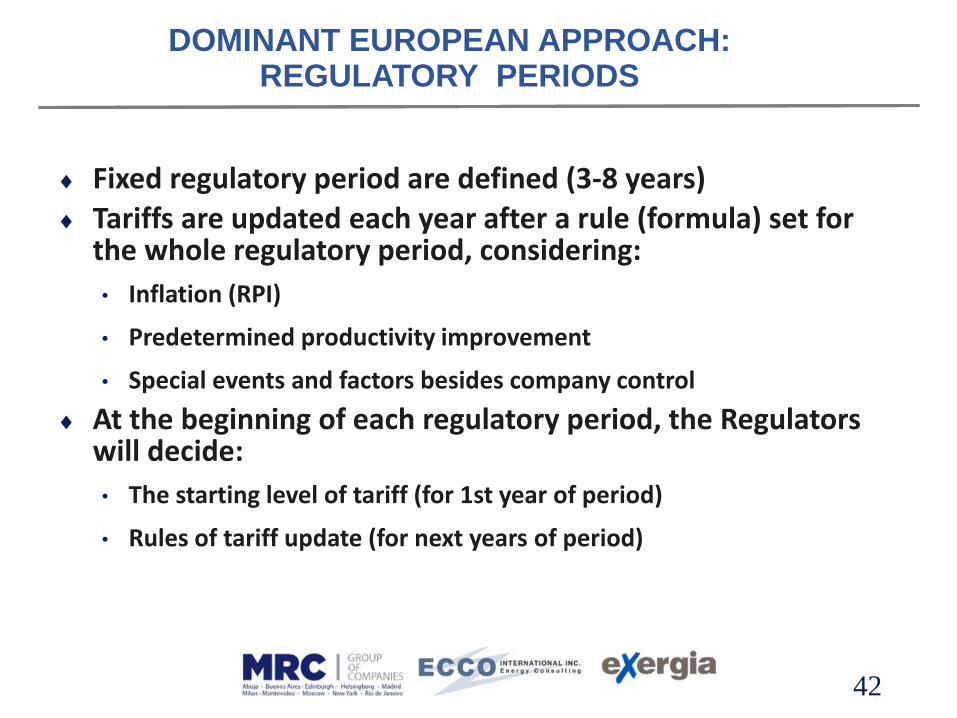

DOMINANT EUROPEAN APPROACH: REGULATORY PERIODS

Fixed regulatory period are defined (3-8 years) Tariffs are updated each year after a rule (formula) set for

the whole regulatory period, considering:

• Inflation (RPI)

• Predetermined productivity improvement

• Special events and factors besides company control

At the beginning of each regulatory period, the Regulators will decide:

• The starting level of tariff (for 1st year of period)

• Rules of tariff update (for next years of period)

42

EUROPEAN TARIFF SETTING PROCESS: MAIN STEPS

1. Collection of costs and technical data

2. Preparation of proposals and internal discussion

3. (One to three) public consultation papers issued

4. Collection of stakeholders’ comments and answers to proposal

5. Final consultation paper and draft decision issued

6. Public hearings held, stakeholders invited

7. Decision and illustration of its reasons

8. Appeal and litigation (if any)

43

DATA COLLECTION & INTERNAL DISCUSSION

1. Regulatory staff to collect costs and technical data, as necessary for tariff calculation

• Preliminary data collection to start 18-24 month before period expiry

• Good mastering of data and technical issues by the regulator’s staff

increases mutual trust and underpins satisfactory decisions

• Further data collection may be needed close to period expiry

• New tariff is typically based on data from 2 years before new period

2. Staff discuss proposals for new regulatory period, present them to Board/Chair

• Including simulation of several scenario assumptions to facilitate

Board/Chair decision

44

FIRST PUBLIC CONSULTATION

3. Preliminary consultation paper issued, outlining broad proposals for the new regulatory period

• Underlines starting point, issues, relationship with other major

regulations (e.g. Network Code)

• Formulates questions for stakeholders (e.g. how long should the

period be? Should rates of return be calculated as WACC?)

• Plain language, may have technical annexes but no draft legal

decision at this stage

• Stakeholders encouraged to react by set deadline

4. Written answers are collected

• Staff may prepare a summary of collected answers for internal,

possibly external use

45

THE ISSUES AT STAKE: EXAMPLES

Calculation criteria for the asset base, operational costs, depreciation

Indices used for re-evaluation of asset values

Calculation criteria for the rate of return

X (productivity growth) factors

Special factors for tariff adjustments (e.g. incentives for quality of service)

Geographical segmentation (national, regional…)

Tariff structure and its drivers (e.g. blocks, fixed/variable charges)

…

46

THE STAKEHOLDERS

Private or Government owned regulated companies and their Associations

Shippers (suppliers, producers, traders...) and their Associations

Customers and their Associations (usually split into those representing households, commerce, industry, power generators, etc.)

Governmental Institutions may take part, but are more likely to raise their points separately

NGOs (e.g. environmental protection associations, representatives of minorities and of vulnerable customers)

47

FURTHER PUBLIC CONSULTATION

5. Second (and possibly more) consultation paper(s) issued, outlining detailed proposals for the new regulatory period

• Recalls preliminary proposals and summarises stakeholders’ reactions

and main points

• Explains Regulator’s position on issues, including those raised by

stakeholders (if important)

• Formulates detailed proposals

• May include detail questions for stakeholders (e.g. Should 10-year

Govt. bonds be the basis for WACC calculation?)

• Draft decision (legal specimen) may be attached

• Stakeholders are encouraged to react by set deadline

48

PUBLIC HEARINGS

6. Stakeholders are invited to one or more public hearings

• Main stakeholders are invited, consultation papers are attached

• Hearings advertised through website, official journals

• May be held in different parts of the country to facilitate participation

• Regulator may illustrate the main proposals in their introduction

• Stakeholders state their points, may ask questions but no legal

obligation to answer

• Hearings may be recorded and/or broadcasted online

49

DECISION

7. After hearings, Board or Chair issue a Decision – may take different forms according to country’s legal system

• A plain language decision document, supported by modifications of

the License (UK & common law countries)

• A legal regulation, with the form of a by-law (most Continental, civil

law countries)

• Decisions are justified in the premises of the by-law or by a separate

technical report

• A Regulatory Impact Assessment is required in some countries,

analysing economic, social, environmental impacts of decisions

50

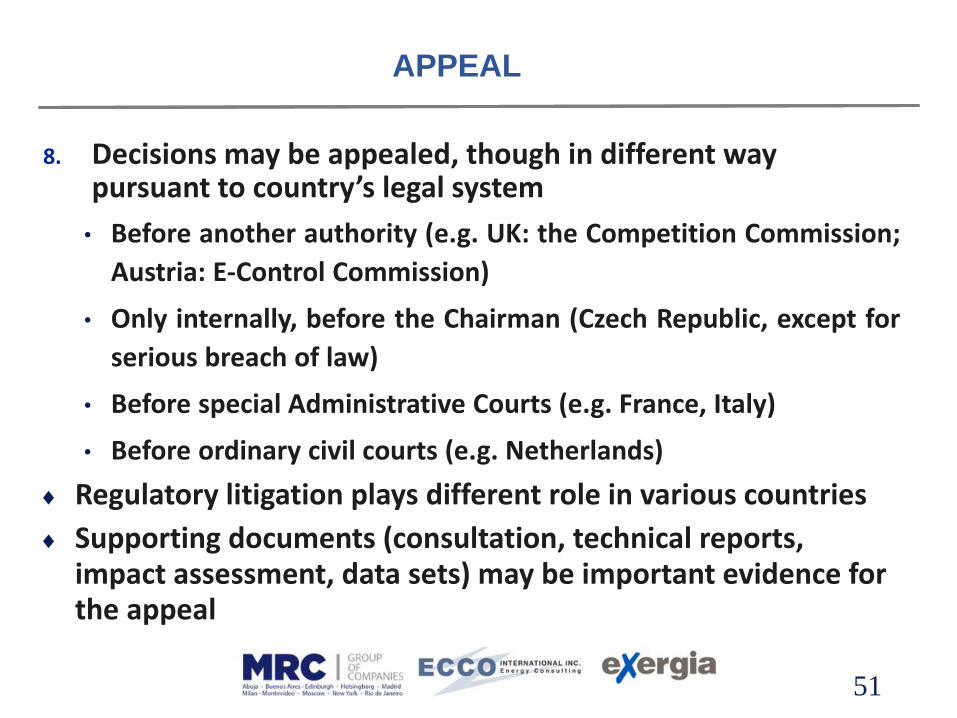

APPEAL

8. Decisions may be appealed, though in different way pursuant to country’s legal system

• Before another authority (e.g. UK: the Competition Commission;

Austria: E-Control Commission)

• Only internally, before the Chairman (Czech Republic, except for

serious breach of law)

• Before special Administrative Courts (e.g. France, Italy)

• Before ordinary civil courts (e.g. Netherlands)

Regulatory litigation plays different role in various countries

Supporting documents (consultation, technical reports, impact assessment, data sets) may be important evidence for the appeal

51

THE EUROPEAN APPROACH: COMMENTS

Degree of transparency (including publication of data, detailed proposals, etc.) depends on country’s standards, usually increases over time

The tariff setting process is very long in most experienced countries (up to 2-3 years), but may be shorter at the start

In early stages, transparency helps Regulators’ independence

Stakeholders’ involvement to be actively sought in early stages of the Regulator’s activity, strengthen its role

Consumers and market newcomers are likely to benefit from the establishment of an independent and strong Authority

52

Part 4

TARIFF LEVEL

BASIC PRINCIPLES

Two-step approach:

• Set Allowed Revenue (AR), and hence the average tariff level

• Determine or approve tariff design (tariff structure), allocating costs

to network users

Cost of efficient companies to be covered

• Choice: actual vs. standard (efficient) costs

• Only costs of the regulated activities

• Only costs actually incurred by operators, net of subsidies

• Principle: Use market values if available, “simulate” if not

54

REGULATORY APPROACHES

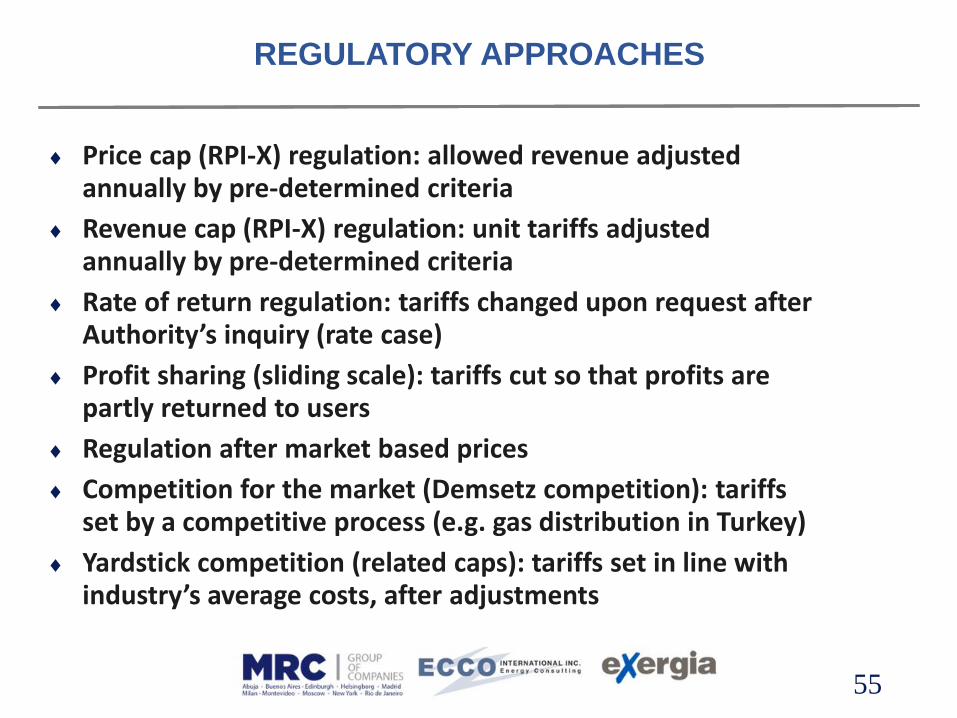

Price cap (RPI-X) regulation: allowed revenue adjusted annually by pre-determined criteria

Revenue cap (RPI-X) regulation: unit tariffs adjusted annually by pre-determined criteria

Rate of return regulation: tariffs changed upon request after Authority’s inquiry (rate case)

Profit sharing (sliding scale): tariffs cut so that profits are partly returned to users

Regulation after market based prices

Competition for the market (Demsetz competition): tariffs set by a competitive process (e.g. gas distribution in Turkey)

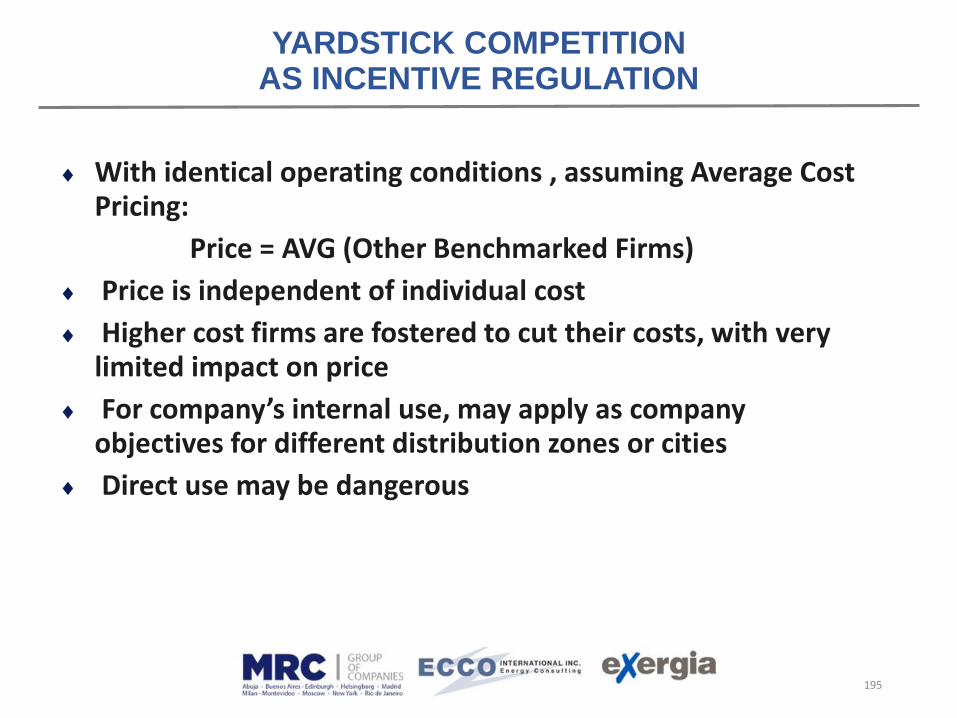

Yardstick competition (related caps): tariffs set in line with industry’s average costs, after adjustments

55

56

Question 2: Which regulatory approach is currently used in Turkey for gas transmission?

1. U.S. style rate of return regulation, tariffs changed

upon request

2. Revenue cap: allowed revenue adjusted annually by

pre-determined criteria

3. Price cap: unit tariffs adjusted annually by pre-

determined criteria

4. Annual setting of tariffs by Authority, no link with

previous/following years

www.kahoot.it

57

APPROACHES OTHER THAN REVENUE/PRICE CAP (1)

Rate of Return (Cost plus) : P = Total cost x (1+RoR)

• Case by case analysis of costs

• Allow a regulated, normal profit margin (see below)

• Do not change tariffs; If productivity growth > inflation rate,

companies may earn more Improvement incentive

Rate of Return regulation: Problems

• Under high inflation, companies must ask frequent tariff hikes

• Incentives depend upon external factors (inflation)

• Companies may inflate cost base, colluding with input suppliers, in

order to increase profits (Averch-Johnson effect)

• To (partly) avoid this problem, regulators need strong staff to

analyse costs – never enough!

58

APPROACHES OTHER THAN REVENUE/PRICE CAP (2)

Profit sharing (sliding scale)• A share (e.g.50%) of profits to be transferred to customers/users, by

reducing prices/tariffs

• Only partly addresses problem of excess profits

• Used sometimes in combination with other approaches

• Useful for the transition between regulatory periods, where excess profitsmay appear (see below)

Market based tariffs for monopolies?

• May use tariffs of similar services used in competitive situations

• Rarely used in Europe, for TSO that compete in transit

Benchmarking Approaches

• Particularly useful for distribution, where several comparable companies/district exist

• See Annex 2

59

THE ALLOWED REVENUE (AR)

Also known as Revenue Requirement Calculation methods may apply to both European

(Revenue/Price Cap) and American (Rate of Return) approaches

AR = RAB * RoR + DEPR + OPEX

Where:

• RAB = Regulated Asset Base (capital)

= GRAB (Gross RAB or carrying value) – cumulated depreciation

• DEPR = annual depreciation

• OPEX = operating cost from company accounts

• RoR (rate of return), usually defined as WACC (weighted average cost

of capital)

60

PREFERRED EUROPEAN REGULATORY APPROACH: REVENUE CAP (1)

Fixed regulatory period (3-8 years)

Every year, AR is adjusted to allow for:

• Cost inflation (RPI)

• Predetermined productivity improvement (X)

• Factors besides company control (Y)

• Errors in tariff drivers’ estimation (E)

Tariffs are adjusted every year according to revised AR and tariff parameters (e.g. capacity, volume,…)

Tariff change is largely predictable

61

PREFERRED EUROPEAN REGULATORY APPROACH: REVENUE CAP (2)

Formally:

ARt = ARt-1 (1+RPIt-X+Yt+Et)

ARt = Ti Di

• Di are tariff drivers (capacity, volume, energy, …), to be discussed in

Part 4

• Yt are special incentives and penalties (e.g. for quality of service)

• Et are factors beyond control of the companies (e.g. fuel costs)

All revenues must be included in the revenue calculation, including connection charges, imbalance charges, etc...

Revenue adjustment may be applied to parts of the AR only (e.g. OPEX only)

62

REGULATORY ASSET BASE (RAB): VALUATION (1)

General principle: all subsidies, grants, connection charges etc. received from customers, government, donors etc., should be subtracted from RAB

Preliminary unbundling of accounts is always necessary Commonly used valuation criteria:

• Book value: Use the value of assets included in the latest official

balance sheet

• Ad-hoc appraisal of assets

• Stock market value of regulated company

• Re-evaluated historical investment cost (Current cost)

• Modern equivalent Asset Value

63

REGULATORY ASSET BASE (RAB): VALUATION (2)

Official balance sheet (Book Value)

• Use the value of assets included in the latest official balance sheet

• May not reflect actual economic value, due to (e.g.) accelerated

depreciation, subsidies…

• In some cases, the Book Value better reflects the cost that has been

actually paid by investors

• Customers should not pay for the network investment cost “twice” –

once as taxpayers, once as gas consumers

• In some countries, the Book Value is re-evaluated so that it is close

to current cost

• In some countries, use of the Book Value is mandatory

64

REGULATORY ASSET BASE (RAB): VALUATION (3)

Ad-hoc appraisal• Regulated companies often hire external auditor to evaluate assets

• The appraisal may be biased if done by companies, cumbersome if doneby regulator, and is always quite costly

• Auditors may end up using the same methodologies (Current cost, MEAV)so that their assessment is not really different

Stock exchange value • Logical circularity with tariff setting process, as the market value (as

assessed by financial analysts) usually depends on tariffs

• Deep fluctuations may occur, affected by regulation, market trends

• Stock market value may be available for an integrated company or Group

rather than the network or distribution system

• Therefore, regulators should look at market values but not use them,

except for companies that have been privatised before regulation

65

REGULATORY ASSET BASE (RAB): VALUATION (4)

Re-evaluated balance sheets (Current Cost method)

• Preferred European approach

• Requires long (often>20 yrs.), reliable investment data series

• If some data are missing, may use statistical estimate

• Results are affected by price index that is used for re-evaluation

Modern Equivalent Asset Value (MEAV)

• Uses value of equivalent modern assets

• Preferred if no long reliable investment data series available

• Uncertain impact of technical progress, as “modern” assets may be

cheaper than original ones – but cost of pipeline steel has lately

increased

May use Current Cost where data available, MEAV where not

66

67

Question 3: Which asset valuation methodology is mainly used in Turkey for gas transmission?

1. Book value

2. Current cost (re-evaluated historical value)

3. Modern Equivalent Asset Value (MEAV)

4. Other

CURRENT COST METHOD: RAB AND DEPRECIATION

68

kt k

t

k

t

kkt t

k

t

kt t

k

t

UL

PIDEPR

UL

tTPIRAB

PIGRAB

,

0

,

,

1

Where:t = year of entry into service (> T0-UL)T0 = first year of tariff periodULk = useful technical life of cat. k itemsk = item category ; Pt = price deflator

RAB UNDER OTHER VALUATION METHODS

Under MEAV, GRAB valuation differs but RAB valuation is the same as for “current cost” methodology

Under Stock Exchange Value RAB is defined, GRAB may be evaluated by reverse process, adding depreciated asset value

Appraisal would normally yield both GRAB and RAB

Not easy to compare methods, as accounting principles can lead to book values to be close to current in a few cases

Most likely, RAB valuation is:BV < MEAV <> CC < SEV

69

RAB : NEW INVESTMENTS

Normally regulators allow inclusion of new assets into RAB only after they enter into service

• However, EU regulation 347/2013 suggests early inclusion as a

possible way of fostering capacity and interconnection

enhancement, where appropriate

Higher returns on new investments also envisaged and welcome, implemented in a few countries (usually + 1 - 4%)

National regulators in Europe not fond of incentives as they lead to tariff increases

70

CURRENT COST METHOD: DEPRECIATION

71

Technical & linear depreciation preferred in EU

DEPR = GRAB / Useful Life (UL) (of each item)

Other depreciation methods may be used e.g. double declining

Typical useful life UL (years) by category of asset:

• Buildings 50-60

• Pipes 40-60

• Compressor stations 20-30

• Other fixed assets 10

If need use legal or fiscal useful lives, distortions may occur, corrections may be necessary

THE RATE OF RETURN

e

D

e

E

t

t

ED

DK

ED

E

t

KWACC

1

1

1

• KE = rf + β MRP is the cost of equity

• rf = “risk-free” rate

• MRP = Market Risk Premium

• KD = cost of debt

• t = debt tax shield

• te = corporate tax rate

Actual financial costs normally not used

Rate of return from Capital Asset Pricing Model (CAPM): weighted average cost of capital WACC

72

WACC: THE «RISK-FREE» RATE

Risk-free rates are normally those of Govt. Bonds

• It already includes country risk!

Must choose duration

• Normally long term (e.g. 10 years)

Latest values or moving averages?

• Preferable to use 3-5 years moving average to avoid possible short

term bond rate fluctuations

• Some regulators have adopted indexation of free-risk rates to

indicators of international rates

If tariffs are defined in the national currency, then should use rates of bonds denominated in national currency

If tariffs are defined in foreign currency may use currency-denominated bonds (if available)

73

WACC: THE MARKET RISK PREMIUM

Market Risk Premium should be national

• Long term average

In many emerging markets, data about long term market (equity yield) premiums with respect to government bonds are not available or very volatile

Therefore, international financial institutions and advisers suggest to use risk MRP from international markets, then add country risk, e.g.:

𝑀𝑅𝑃𝑍=𝑀𝑅𝑃AAA + Country Risk Premium

Likewise, for the debt premium, may use debt premium from international markets, then add country risk

For data, may look for: Damodaran

74

WACC: DEBT/EQUITY, BETA, TAXES

Debt/Equity ratio often set as target (e.g. = 1)

• Want to encourage more debt, to reduce financial costs

• Based on mature peers’

• Sometimes actual D/E is used

Risk index (beta) for transmission is usually taken from analysis of an international sample of peers

For both D/E and Beta, should carefully consider actual company values

• Unbundled TSOs can afford higher leverage than integrated companiesand have lower risk

Tax & shield rates must be related to national tax codes

Actual (real, pre-tax) WACC values in the EU lie in the 5.5% –9.1% range

75

WACC: NOMINAL VS. REAL

In the U.S. and in other countries, where tariffs are fixed and not adjusted for cost inflation (or are set for one year only), the calculated nominal WACC applies

In Europe, where multi-year regulatory periods are used and tariffs are protected from cost inflation through the RPI-X adjustment formula, regulators normally allow only the real rate (i.e. nominal rate minus expected inflation)

Compensation is foreseen in case actual inflation differs from expectations

76

THE RATE OF RETURN: DCF METHOD

“Discounted Cash Flow”, also known as DividendGrowth Model

Based on the idea that the cost of equity capital can berevealed by markets

Where:

• D are dividends per share,

• P is equity price and 𝐷 ̇is the time evolution rate of dividends

Rarely used outside the U.S., not popular in Europe

Less transparent than WACC

77

𝐾𝑒 =𝐷

𝑃+ 𝐷

OPERATIONAL COSTS (OPEX)

Evaluated after accounting unbundling, i.e. after checking for cross subsidies with other activities

Only costs of relevant activity to be allowed

• When unbundling, regulated companies tend to attribute common

costs to network rather than supply subsidiaries

Actual costs normally used as starting point for the calculation of the Allowed Revenue

• Peer-checked if possible (e.g. check OPEX/GRAB, OPEX/customer,

OPEX/Km, …)

• May use advanced benchmarking techniques (see Annex 2)

• If ratios found far from peers, X-factor may be used for gradual

adjustment

78

ALLOWED REVENUE & TARIFF STRUCTURE

79

May have to adjust values from the last available data to the starting year of the new regulatory regime

• Inflation

• Tariff drivers (volume, capacity, No. of connected users…)

• New investment?

Tariff structure defined to be consistent with AR

• ARt = Ti Di

• Consistency ensured by using expected values of tariff

parameters for the start of new tariffs

• Further discussion under Part 6 (Tariff Design)

THE INVESTMENT CYCLE

Network investments usually have a bumpy trend, due to bulky assets that are developed in relatively short time (compared to useful life)

• Examples: major interconnectors, compressor stations, SCADA systems,

primary pressure reduction stations, LNG terminals, storage sites

Companies would prefer fast depreciation

Regulators normally prefer stable tariffs

In any case, large investments’ entry into the asset base lead to tariff increases

Depreciation practice largely defines how tariffs are affected by investments

No simple rules to smooth investment impact on tariffs, it all depends on the time structure of past investments

DEPRECIATION AND AMORTIZATION: EXAMPLE 1

The tariff impact of investments is lower:

• With constant rates

• The longer the depreciation period

DEPRECIATION AND AMORTIZATION: EXAMPLE 2

The relationship between allowed revenue and depreciation time (useful life) is neither obvious nor monotonic

• Example from an actual TSO pipeline database, with constant depreciation

• The relationship between AR and useful life depends on the rate of return

DEPRECIATION AND THE INVESTMENT CYCLE: CONCLUSIONS

No general rules about way of smoothing the impact of bulky investments

Regulators should keep a long-term database of companies’ investments

Longer depreciation lives reduce impact of recent investments but may increase the Asset Base, as depreciation of current assets is slower

If regulators can choose useful depreciation lives and depreciation method, they may be able to find an optimal balance

Part 5

TARIFF UPDATING

MAIN REGULATORY APPROACHES

North American: fixed tariffs (rates), to be reviewed whennecessary

European: regulatory period set in advance (3-8 years),tariffs updated yearly by rules that are issued as part of thetariff decisions

• For example by price cap: unit tariffs updated every year by the

inflation rate (RPI) minus expected productivity growth (X)

Widely spread practice: Tariffs defined on an annual basisor at regulators’ will, with no inter-temporal links

• Not recommended, as it triggers regulatory uncertainty,

jeopardizing investments and efficiency improvements

85

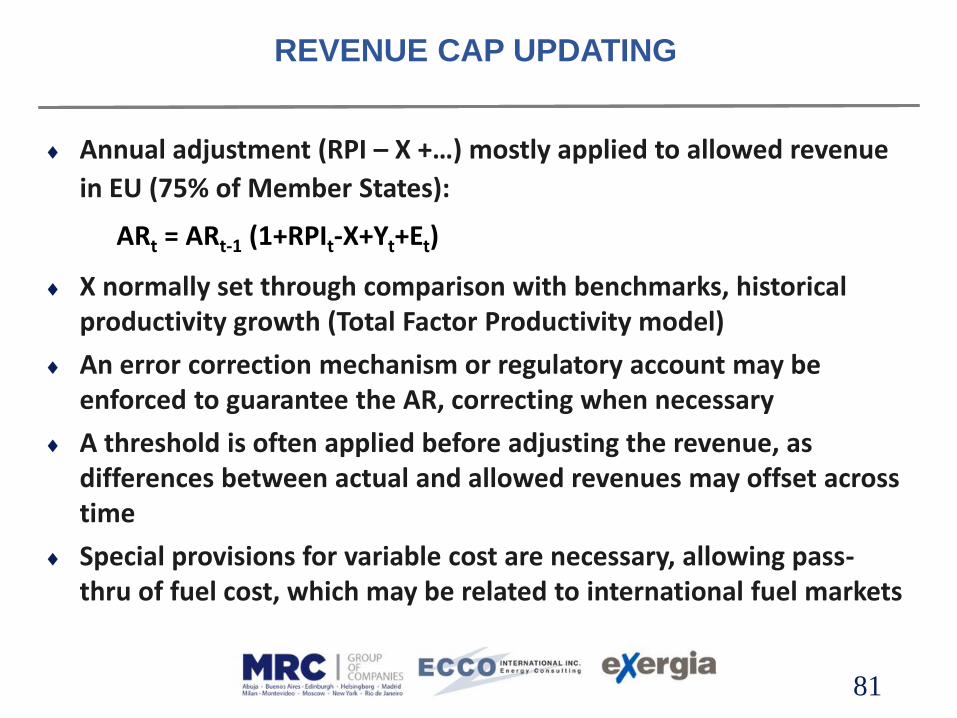

REVENUE CAP UPDATING

Annual adjustment (RPI – X +…) mostly applied to allowed revenue

in EU (75% of Member States):

ARt = ARt-1 (1+RPIt-X+Yt+Et)

X normally set through comparison with benchmarks, historical productivity growth (Total Factor Productivity model)

An error correction mechanism or regulatory account may be enforced to guarantee the AR, correcting when necessary

A threshold is often applied before adjusting the revenue, as differences between actual and allowed revenues may offset across time

Special provisions for variable cost are necessary, allowing pass-thru of fuel cost, which may be related to international fuel markets

81

PRICE CAP UPDATING

Under Price Cap, RPI-X+… is applied to unit tariffs for capacity, fixed commodity and/or commodity (price cap):

Tit = Ti

t-1 (1+RPIt-X+Yt+Et)

Under price cap, X must also consider volume increase

• Network cost (except variable cost, i.e. compression cost and leakages)is basically independent of the gas volume (throughput)

• If consumption increases and unit prices remain the same, actualrevenue would exceed the AR

• Expected growth rate

The allowed revenue is not necessarily met, revenue may be <> AR

Under price cap, volume risk is left upon the transport company, hence the WACC should be higher

82

REVENUE / PRICE CAP UPDATING: COMMON ISSUES

Under both Revenue- and Price-Cap, special provisions are necessary, allowing pass-thru of fuel cost,

Fuel costs may be indexed to international fuel markets

For special objectives (e.g. quality of service, a “sliding scale” mechanism may be envisaged, allowing higher margins if objectives are exceeded while penalties are applied if minimum objectives are not achieved

Components (+/-) are sometimes included for:

• Incentives for new investments, e.g. increased returns

• Revenues/Costs from compensation mechanisms from/to otherTSOs/DSOs

• Costs of social tariffs for subsidized consumers

• Environmental support schemes, e.g. for renewable gas

83

89

GUARANTEED TSO INCOME?

Most transmission costs are fixed (all except compression and leakages)

Unbundled TSOs do not control gas flows – they are up to shippers

Under Revenue cap , tariffs are adjusted to offset demand change that may lead to cost under-recovery (regulatory account)

Under price cap (or in the U.S.): no such adjustments, TSOs carry demand risk

Regulatory account

• If actual revenue diverges from allowed, tariffs will be adjusted

• Threshold usually introduced to avoid too frequent changes

• Example provided in Excel file

TRADITIONAL RATE OF RETURN REGULATION (COST PLUS: NORTH AMERICAN APPROACH)

In the traditional approach (Rate of Return regulation), prices are defined by adding a “fair” rate of return to the average cost

P* = AC (1+ROR)

Adjustment only at stakeholders’ (usually regulated companies’) request, followed by public inquiry

Ratio: avoid excess profit, only allow fair one

Calculation of capital costs, OPEX, Rate of Return is similar to what has been described for the AR approach

90

TRADITIONAL COST PLUS VS. REVENUE/PRICE CAP

Revenue / price caps offer more efficiency incentives and regulatory stability, but:

• companies can neutralise some of them by strategic behaviour (e.g.postponing improvements until after base year)

• Sharing of further productivity improvements after the end of theregulatory period may reduce this problem

• Choice of X factor may be questionable, but no serious disputes lately –often limited to OPEX

• If costs and tariffs diverge during the period, the company may increaseits profits in a way regulator may be embarrassed

• If cost inflation is high, RoR requires frequent, costly reviews

Recent EU evolution: towards longer regulatory periods or predetermined links between periods

91

COMMON PROBLEMS

Costs may be too high (inefficiency)

If high costs are related to past inefficiency (e.g. in purchase of long lasting inputs), regulation can hardly solve it

Regulation based on actual costs may trigger excess investments (gold plating) or “too high” quality of service

Hard to assess, as the regulator has never the same information as the company

Benchmarking provides limited help

In the first implementation (first year of first period) both EU and US approaches share the same problems

92

Part 6

TRANSMISSION TARIFF DESIGN

For information about actual tariffs in the EU: Market Monitoring Report 2017, www.acer.europa.eu/en/Electricity/Mar

ket%20monitoring/Pages/Current-edition.aspx

TARIFF DRIVERS

Transportation tariffs should be related to costs, hence to cost drivers:

• capacity

• distance

• shipped volume (energy)

• connection points

Different criteria may be used for primary (national) and secondary grid

94

TARIFF STRUCTURES: ALTERNATIVE METHODS

Point to point (P2P or distance-related)• traditional, preferred by integrated companies

Zonal tariff

• American simple version of P2P

National postage stamp

• Politically supported, hardly cost reflective

Entry – exit

• Recommended by regulators, EC

Capacity auctions

• OK for entries, but risky if market power

• May lead to cost under-recovery

• Adopted for entries in EU, but subject to minimum tariffs

95

ENTRY - EXIT TARIFFS FOR PRIMARY GAS TRANSMISSION

One entry charge for each point, independent of chosen exit + one exit-related charge for each point, independent of entry (see Annex 1 for example)

Entry – exit charges are usually capacity-related

• E.g. 20.4 €/(kWh/d)/year

• Other charges may apply , e.g. Commodity related or fixed

components

• Postage stamp frequently used for lower level network

VTP

Import

Production

Storage

LNG

Large customers

Distribution

Storage

Export

ENTRY-EXIT METHODOLOGY: PROs & CONs

Intermediate solution between postage stamp and P2P

• Tariffs are closer to postage or P2P, depending on network topology

Good cost reflectivity, notably if gas arrives from several directions (but less than P2P)

Maximum flexibility for shippers, who can choose any exit from any entry even in short term

Creates a Virtual Trading Point located “on the grid” between all entries and all exits

• maximising liquidity for national markets

Lower capacity than P2P (for the same infrastructure) may be the price of flexibility

97

THE ENTRY-EXIT CAPACITY BURNING PROBLEM: QUESTION

A simple transmission network:

One import entry point A (Technical capacity 50 GWh/day)

Two export exit points B (15), C (10)

Domestic exit V (25, Virtual Trading Point)

If a simple entry-exit model is implemented in this network, shippers are in principle free to choose any exit point for gas entering at A.

Q: What max. capacity will the TSO offer for sale at A?

98

THE ENTRY-EXIT CAPACITY BURNING PROBLEM: ANSWER

If all shippers choose exit C, only 10 GWh/d can be transported through the system

The TSO would therefore offer only a firm capacity of 10GWh/d at entry point A, with any other capacity made available on an interruptible basis

However, if some capacity could be offered at A conditional upon delivery at (e.g.) export point B, then total capacity offered at A could be increased to 30 GWh/d, as the risk of all gas diverted to C would be void

In practice, TSOs may offer more than would be allowed by offering total flexibility, as the probability of all shippers choosing C is very low – in fact some gas will be necessary for demand at B & V

But, entry capacity offered at A on a totally flexible basis is probably less than 50 GWh/d (as it would occur under P2P)

99

100

ENTRY-EXIT TRANSMISSION TARIFFS: MAIN ISSUES

Choice of entry and exit points: actual points vs. zones

• Exit may be postalised, usually for domestic exit points

Cost basis: average vs. incremental cost

• Incremental cost preferred in case of congestion

Entry / Exit cost allocation criteria

• Avoiding discrimination between domestic and cross border

trade is the key objective of TAR Network Code

Tariffs for special services (Conditional, Interruptible,

Reverse flow, Shorter capacity products)

Capacity / commodity split

101

ENTRY-EXIT TRANSMISSION TARIFFS: ALTERNATIVE COST ALLOCATION CRITERIA (1)

Calculation of capacity charges TE, TU for the primary

grid can be done in several ways, still debated in the

EU:

1. Matrix. Solve min Σij (TEi + TXj - COSTij)2

Where:

• TEi is the entry charge for entry point I;

• TXj is the exit charge for exit point j;

• COSTij is the point-to-point cost of transport from entry point i to exit zone j)

102

ENTRY-EXIT TRANSMISSION TARIFFS: ALTERNATIVE COST ALLOCATION CRITERIA (2)

2. Calculated TEi as capacity weighted average distance of entry point ifrom all exit points, and TXj likewise:

𝑪𝑾𝑫𝒊 = 𝒆𝒙𝒊𝒕=𝒋=𝑿,𝒀,𝑯

𝒆𝒏𝒕𝒓𝒚=𝒊

𝑫𝒊𝒔𝒕𝒂𝒏𝒄𝒆𝒊𝒋𝑪𝒂𝒑𝒂𝒄𝒊𝒕𝒚𝒋

3. Define a physical or virtual point in the network where most gas converges and calculate TEi + TXj in relation to distance of each entry or exit from the virtual point

Capacity weighted distance is the preferred cost

allocation methodology against which all other must

be benchmarked in the EU

103

ENTRY-EXIT TRANSMISSION: SPECIAL SERVICES (1)

Conditional Capacity Products• Short-haul products, introduced to avoid by-pass of

short-distance transmission users; usually @ very low tariffs (5-10%)

• Wheeling: short distance transfers between interconnected pipeline systems; usually @ very low tariffs

• Products conditional upon choice of related entry and exit points, with no access to VTP; used mainly for transit, discounted (70-80%)

• Products conditional upon certain climatic(flow conditions, with interruptible access to VTP; slightly discounted (90-95%)

104

ENTRY-EXIT TRANSMISSION: SPECIAL SERVICES (1)

Interruptible services

• Interruption conditions must be clearly specified

• Discounts related to interruption probability (may be very low)

Virtual Reverse Flow (backhaul) services

• Special interruptible service to be offered at significant discount, but logical basis to define discount uncertain

• Various cases in EU, e.g. 20%, 50%,…

SHORT TERM PRODUCTS

In the EU and other liberalised systems, TSOs increasingly offer short term capacity products

In the EU, the CAM Network Code requires the offer of annual, quarterly, monthly, daily, and within-day products

Products are auctioned, but regulated reserve (minimum) tariffs are defined by NRAs

TSOs tend to request higher unit prices for short term capacity products, due to: • relatively higher administrative burden

• higher risk of loss of TSO revenue

Regulators support ST products as a tool for boosting competition

Ratios between ST and annual capacity tariffs (multipliers) are capped by the Tariff Network Code

105

CAPACITY – COMMODITY SPLIT

Pure cost structure reflectivity would require 95% capacity and fixed components (straight fixed variable approach)

Applied in most EU countries (and US)

Competition would lead to “commoditisation”

Regulatory decision: commodity component may be higher than variable cost, to share demand risk between transport companies and shippers (Britain, Italy, Poland…)

15/23 EU Member States have capacity components 90%

Availability of short term capacity products reduces relevance of capacity charges, as shippers can buy for the flows they need only

106

CONNECTION CHARGES

Connection charges are often regulated only for small customers, connected to distribution networks

Regulatory protection of large customers may be needed if TSO (or integrated suppliers) require them to pay for assets that they will not own (e.g. long and costly connecting pipelines)

Protection is achieved:

• By strict application of the principle that connection charges are

subtracted from the RAB

• By allowing customers to build and own their connections

• By requiring TSOs (or integrated suppliers) to tender the

construction of connection assets, so that lowest cost is achieved

107

Part 7

STORAGE & LNG REGASIFICATION

STORAGE TARIFF: IS REGULATION NECESSARY?

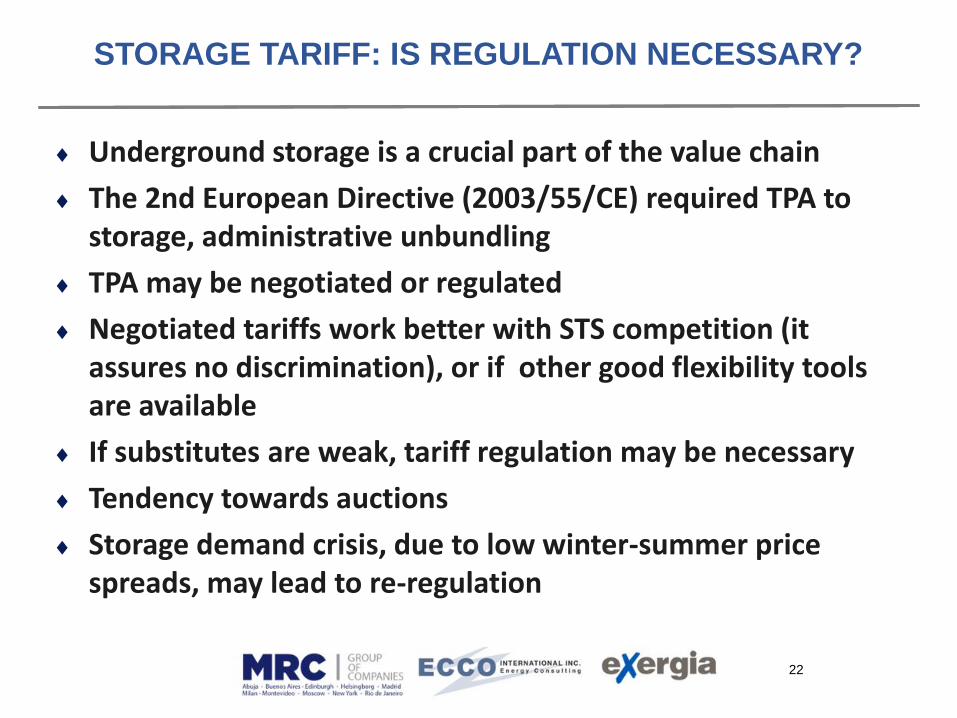

Underground storage is a crucial part of the value chain

The 2nd European Directive (2003/55/CE) required TPA to storage, administrative unbundling

TPA may be negotiated or regulated

Negotiated tariffs work better with STS competition (it assures no discrimination), or if other good flexibility tools are available

If substitutes are weak, tariff regulation may be necessary

Tendency towards auctions

Storage demand crisis, due to low winter-summer price spreads, may lead to re-regulation

10922

110

Regulated vs. negotiated TPA

Similar weight of both approaches but negotiated larger by capacity (67%)

Some “hybrids” and “N.A.”, actually mostly negotiated in CZ, IE, GB, regulated in HU, BG, SK

111

Regulatory regimes and main allocation rules

• Wide use of auctions

Country Access Main allocation procedure

AUSTRIA negotiated FCFS/Auction

BULGARIA regulated Merit order

CZECH REPUBLIC negotiated Auction

DENMARK negotiated FCFS/Auction

FRANCE negotiated Merit order

GERMANY negotiated FCFS/Auction

HUNGARY regulated Auction

ITALY regulated Auction

POLAND regulated Pro-rata

PORTUGAL regulated Auction

SPAIN regulated Auction

UNITED KINGDOM negotiated* Auction

*The study focuses only on facilities which are not exempt from the nTPA provisions.

STORAGE: REGULATED TARIFF CRITERIA

Valuation criteria as for transport

Cushion Gas valuation at opportunity cost

• often most difficult issue

Rate of return by same criteria as for transmission

• Higher value likely if demand risk borne by storage operator

RPI – X price or revenue updating

Cost attributed to tariff components:

• underground facilities and CG to space

• surface facilities to peak capacity

• energy (compression) costs to commodity

11222

113

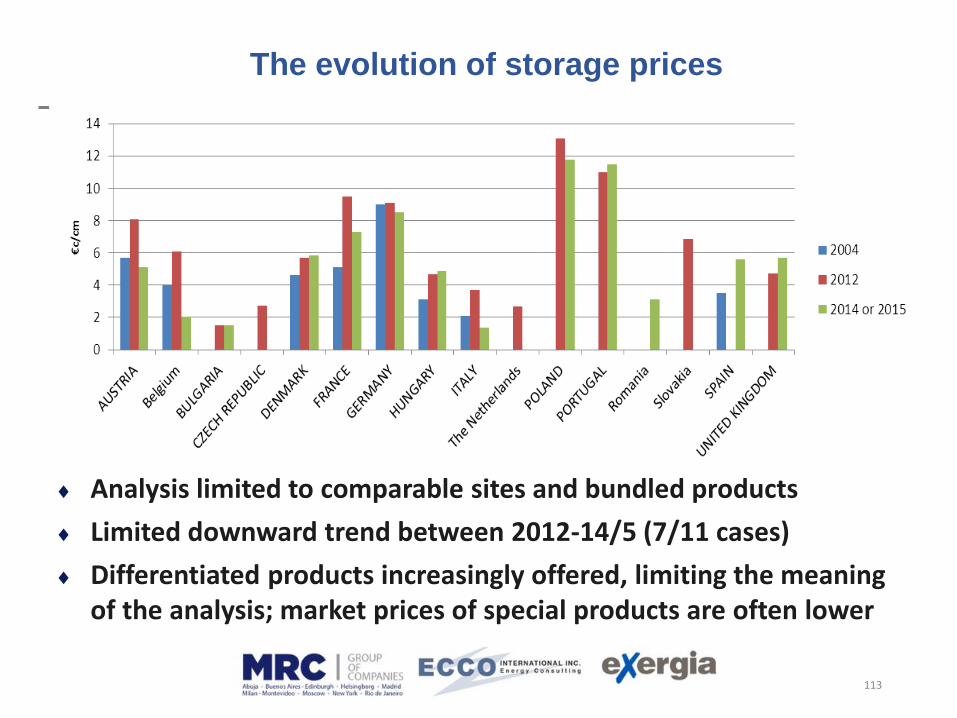

The evolution of storage prices

Analysis limited to comparable sites and bundled products

Limited downward trend between 2012-14/5 (7/11 cases)

Differentiated products increasingly offered, limiting the meaning of the analysis; market prices of special products are often lower

114

The composition of storage prices (2015)

Several countries have discounted or zero transmission tariffs to / from storage

Analysis based on posted prices, market prices often lower

115

The determinants of storage prices

Faster facilities command higher prices

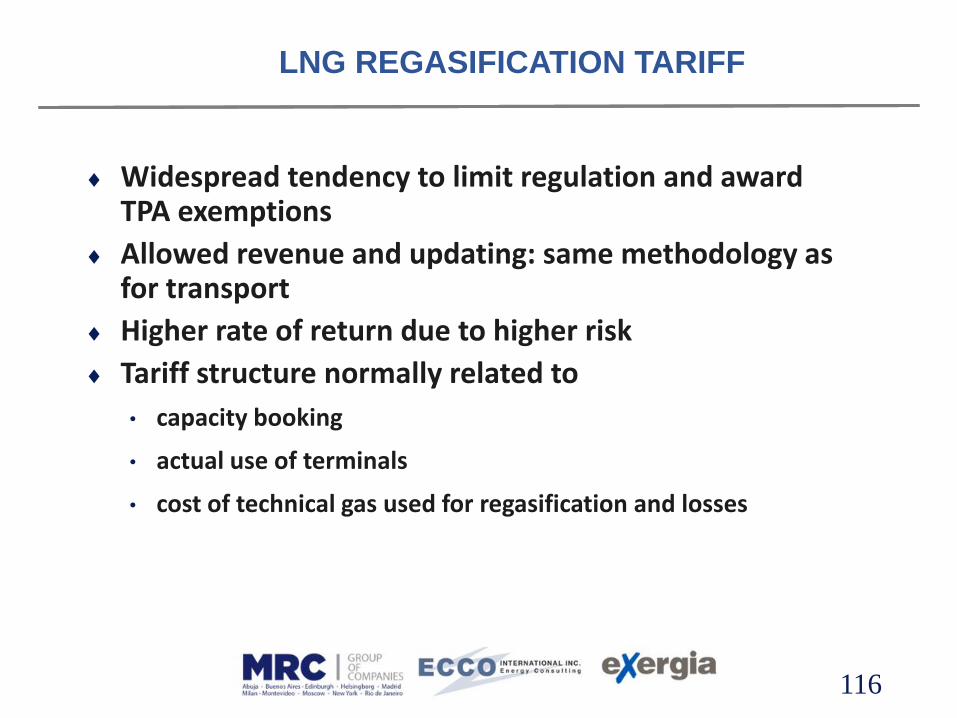

LNG REGASIFICATION TARIFF

Widespread tendency to limit regulation and award TPA exemptions

Allowed revenue and updating: same methodology as for transport

Higher rate of return due to higher risk

Tariff structure normally related to

• capacity booking

• actual use of terminals

• cost of technical gas used for regasification and losses

116

Part 8

DISTRIBUTION TARIFFS

Partly based on the European Commission’s Distribution Study by AF-Mercados, REF-E & Indra, 2014-15

For details: https://ec.europa.eu/energy/sites/ener/files/documents

/20150313%20Tariff%20report%20fina_revREF-E.PDF

118

Geographical outreach (City, Province, Country…)

Service tendering

Separate distribution and supply tariffs?

Case by case regulation vs. competition simulation by benchmarking

Main distribution tariff regulatory approaches in Europe

Tariff structures and levels across Europe

Connection charges

KEY ISSUES IN DISTRIBUTION TARIFF REGULATION

119

GEOGRAPHICAL OUTREACH

In Europe, gas distribution is mostly performed at localgovernment level (e.g. Germany) or intermediate (county, district, province, Land…)

120

Average gas DSOs size

Gas distribution is a national business only in Ireland, Slovakia

121

DISTRIBUTION SERVICE LICENSING

May be used for tariff setting, notably in new networks (Example: Turkey)

Risk that lower prices affect quality of service

Risk that winners ask for renegotiation

Hard to beat incumbent when licenses are up for renewal

Service tendering examples in Italy, Argentina, Turkey…

In most advanced countries, long or indefinite licenses are preferred

If DSOs are private, buyouts by more efficient suppliers are possible

121

122

Distribution tariffs: Turkey’s approach (1)

Distribution franchise in each province (81 in Turkey), with monopoly selling rights for 8 years

Franchise is awarded by auction to the bidder offering the lowest average distribution tariff (without gas cost)

The winning company must start works within 6 months and serve all requesting customers within five years

Wholesale gas cost is passed through to customers

Distributors cannot buy more than 50% of their gas from the same supplier

After 8 years, the market is opened and third party access is implemented

The distribution tariff may be revised by the National Regulatory Authority, based on company costs

123

Private companies bid very low tariffs, even negative ones!

Why?

• Companies hoped to become incumbent in the province and retain a fair

share of customers

• Companies hoped to increase distribution tariffs under a cost based

regulatory regime

• Suppliers tried to create a captive market

65 provinces awarded until 2014 (+6 already active in 2004)

All distribution companies are private or have been privatised (except Istanbul, run by the municipality)

For 23 of them, the monopoly 8-year period has expired, new regulated (cost based) tariffs have been approved

Distribution tariffs: Turkey’s approach (2)

124

Distribution investment: Turkey’s results

Invested 3.9 billion TL (~1 billion US$) until 2013 (+ 5.4 BTL invested in original 6 provinces)

Consumption has significantly increased in industry and the residential sector, beyond major urban areas

Source: ESMAP / World Bank, 2015

125

DISTRIBUTION: UNBUNDLING

In Europe, legal unbundling is between distribution and retail supply is mandatory

For companies with less than 100,000 end customers, only unbundling of accounts is required

Separate tariffs are defined for distribution and retail supply

Metering may also be seen as a separate activity but this is a rare choice in Europe (In gas, U.K. and France only)

125

126

SETTING THE ALLOWED REVENUE OF DISTRIBUTION COMPANIES

Tariffs can be individually set for each distributor, as for transmission

However, special approaches are sometimes used for distribution:

• Define tariff by tendering the distribution service: not used in Europe,but it partly happens in Italy (and other countries), as municipalitiestypically require a licensing fee or part of distribution profits

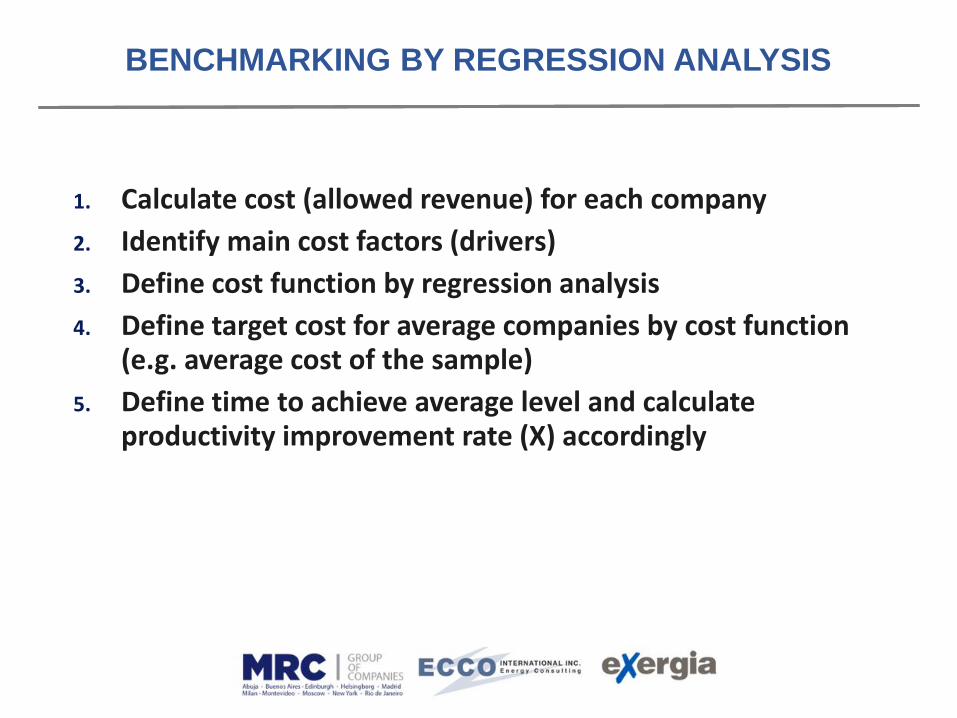

• Use benchmarking methods: allowed revenue calculated by means ofstandard costs, depending on objective parameters – see Annex 2

• Standard costs estimated by statistical or engineering techniques, asindustry average or “best practice” – see Annex 2 for furtherinformation

127

Actual costs vs. Benchmarking

Use of benchmarking techniques is spreading, at least for OPEX

Actual costs used mostly at start of period and for CAPEX

No. of countriesWhere would Turkey fit?

128

Tariff regulatory model

Most EU Member States use incentive regulations, with some “passthrough” items

Where would Turkey fit?

129

Volume Risk on DSOs

Even in the few cases where some volume risk falls on DSO’s, exposure is limited

No Risk = if volumes fall, unit tariffs are increased so that the allowed revenue is achieved anyway

No. of countries

Where wouldTurkey fit?

130

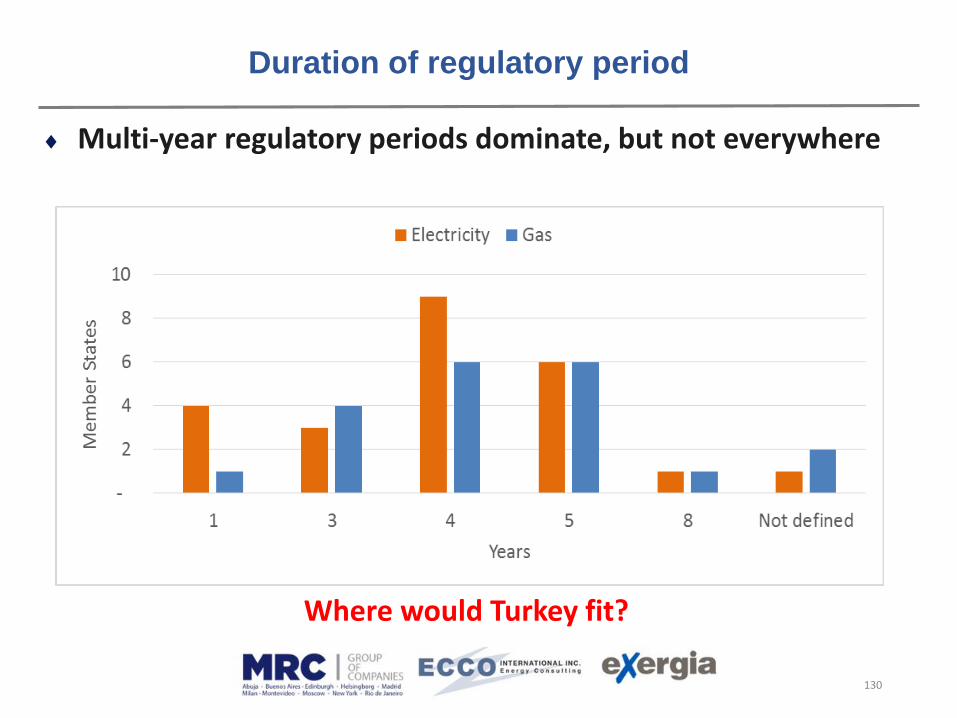

Duration of regulatory period

Multi-year regulatory periods dominate, but not everywhere

Where would Turkey fit?

131

DISTRIBUTION TARIFF STRUCTURE

Economic theory of optimal (Ramsey) pricing: less elastic demand sectors get higher tariff

Hence: should the tariff structure be proposed by distributors, who better know how demand react to prices in each sector?

Regulators often not at ease with Ramsey pricing, seen as “discriminatory”

Regulators usually prefer objective criteria like

• Consumption level

• Pressure class

• Type of consumer (e.g. households, commerce, industry…)

Capacity-related charges often used for large customers, endowed with hourly / daily meters

132

0

2

4

6

8

10

12

14

16

18

20

Pressure Level AnnualConsumption

Used Capacity Meter capabilities

Nu

mb

er

of

Me

mb

er

Stat

es

Variables used to define tariff structures

Tariff structure in Europe

In most countries the annual consumption (In Kwh/year or m3/year) is the key variable to define the tariff structure levels

The pressure level is used in combination with annual consumption in some countries like: AT, CZ, LU, ES, PT

In DE, HU, NL & PL the tariff are set according to annual consumption and used capacity

Only in AT, tariff blocks are also defined on the basis of metering capabilities

132

Where wouldTurkey fit?

133

Gas tariff components: Households & Commerce

In most countries the network tariff consists of a fixed charge and an energy charge…

• …with some exceptions: the NL tariff does not have an energy component, while DK, EE, LT and LU use volume based charges only

• Other components include metering

134

Gas tariff components: Industry

In most countries the network tariff consists of a capacity charge and an energy charge

• Most countries apply a capacity charge (13) rather than a fixed charge (9)

• In all countries, except NL, there is a volumetric charge (€/KWh).

• Only PT has time of use differentiation.

913

19

5

117

1

15

1 1 1 1

5 5 5 5

Fixed Charge Capacity Charge Energy/Comodity Charge Other

Distribution tariff components in EU Countries by consumer group: Industrial

Yes No Could apply in some tariffs Data no available

134

135

29%

73%

0%

52%

0%0%16%

77%82%

15%

66%

0%

39%

71%

27%

100%

48%

100%100%84%

23%18%

85%

34%

100%

0%

61%

ATCZEEFRITLTLUPOSKSIESSENLAve.

15%

74%

0%

56%

0%0%18%

78%85%

14%

66%

0%

39%

85%

26%

100%

44%

100%100%82%

22%15%

86%

34%

100%

0%

61%

ATCZEEFRITLTLUPOSKSIESSENLAve.

12%35%

0%

53%35%

0%0%5%31%28%20%23%26%

88%65%

100%

47%65%

100%100%95%69%72%80%77%

0%

74%

ATCZEEFRITLTLUPOSKSIESSENLAve.

60%

2%

36%47%

30%

1%14%

47%

92%84%64%

87%

20%

66%80%

38%

100%

9%

46%

40%

98%

64%53%

70%

99%86%

53%

8%16%36%

13%

100%80%

34%20%

62%

91%

54%

ATCYCZFIFRDEELHUITLUPLPOROSKSIESSENLGBAve.

Fixed + Capacity components Energy component

Ho

us

eh

old

Ind

us

tria

l, 5

0 G

Wh

ind

us

tria

l, 5

0 G

Wh

• The active energycomponent recoversmore of the half ofnetwork allowed costs

• Household average:74%

• Industrial: 61%

• For household consumersthe energy charge hasmore relevance than forother consumercategories

Weight of tariff components

Ave. 74%

Ave.61%

Ave. 61%

Gas network allowed costs are mostly recovered though energy tariff components

135

136

Gas network average allowed costs

The variability of average allowed costs is in a range between 2.17 EUR/MWh and 14.61 EUR/MWh

Gas distribution network allowed costs per energy delivered in 2013. (Euros per MWh)

Gas distribution network allowed costs per connection point in 2013. (Euros per connection point)

12.26

9.29

9.60

5.76

3.31

3.53

2.15

0.96

2.65

0.49

0.26

0.27

1.39

-

1.33

11.99

9.00

8.77

8.54

7.09

6.53

6.09

5.98

5.82

5.49

4.86

2.97

2.17

0 2 4 6 8 10 12 14 16

SI

IE

PO

FR

IT

ES

SE

SK

CZ

DE

AT

PL

HR

LT

DK

HU

GB

LU

NL

FI

Distribution (Networkonly)

Metering

Customer Management

Others

Distribution revenues(Details by distributionactivity are not available)

14.61

13.27

10.09

14.61

13.27

14.61

13.27

10,09

14,61

13,27

6,02

3,72

3,59

2,41

401

321

285

197

157

79

-

2240

426

397

252

225

200

197

149

147

95

87

0 500 1000 1500 2000 2500

SE

DE

AT

LU

SI

FR

IE

SK

PO

ES

CZ

NL

IT

PL

HR

HU

LT

Distribution (Networkonly)

Metering

Customer Management

Others

Distribution revenues(Details by distributionactivity are not available)

420

383

299

282

177

91

136

137

Gas total (€) and average distribution network charges (cent€/kWh) for households, 2013

Spain: average network tariff includes transmission cost.

3.59 3.572.69

1.73 1.55 1.52 1.37 1.14 1.01 0.97 0.82 0.74 0.68 0.33

539 536

403

259233 228

205171 151 145 123 111 102

50

SE PO ES AT Ave. FR SK SI CZ NL IT LU LT EE

cen€/KWh Total €/year

137

138

Gas total (€) and average distribution network charges (€c/kWh) for Industry (90 Gwh), 2013

Spain: average network tariff includes transmission cost.

2.17 0.45 0.43 0.41 0.34 0.33 0.32 0.31 0.26 0.23 0.20 0.15 0.04

1,953

401

390 365 304 299 287 283 234 203 183 133 40

SE SI Ave. LU LT EE ES PO SK AT CZ FR IT

cen€/KWh Total Thousands of €/year

138

139

OTHER TARIFF ISSUES

139

«Deep» connection charges include costs of network reinforcement; «shallow» only include costs of «last mile»: which is better?

Social tariffs could be applied to vulnerable customers (e.g. poor, elderly, disabled…)

Tariffs should be geographically uniform across the country or province

Tariffs should be related to time/day/season of gas consumption

140140

No. of countries

Other tariff issues: What does Europe do?

141

SUMMARY OF EU’S TARIFF REGULATORY SCHEMES

Allowed revenue, mostly defined on a multi-year basis, with price-cap or revenue-cap adjustment

Distributors typically do not bear volume risk and the risk that their investment turn out to be less useful than expected

Revenue setting mechanisms based on benchmarking or standard costs are often used where distribution sectors are fragmented

Tariff structures reflect limited availability of information on each consumer’s responsibility in causing distribution cost

141

142

RULES FOR MARKET OPENING

142

Market rules framework: common or individual network code

Capacity allocation a less serious problem than for transmission

Rucksack principle: capacity allocated to the supplier who wins the end customer

Switching issues:

• End customer switching procedures

• Market rules usually banning long term contracts that would hampercustomer switching

Metering problems of smaller customers, not endowed with daily/hourly meters

Complex load profiling methodologies developed, involving important distributors’ role

Part 9

END USER PRICES

144

WHY REGULATE END USER PRICES? (1)

In principle, gas supply is a competitive business if the market

is open and networks are regulated

Therefore, end user price regulation should not be necessary

But, even in open markets, competition may be weak, due to:

• Legacy contracts in upstream supply and/or retail

• Bottlenecks in the supply chain, e.g. in international transportation,LNG regasification, storage, production, treatment etc.

• Cartels or other collusive behaviour of suppliers

• Inadequate / ineffective consumer information, hampering consumerswitching to cheaper opportunities

145

WHY REGULATE END USER PRICES? (2)

Yet competition may be strong:

• Pipe to pipe competition in very large markets (North America)

• Gas to gas competition in unbundled supply in several EU MemberStates

• Interfuel competition in some markets

Social and/or environmental reasons may also justify end

user price controls (See part 1)

146

PRICING IN COMPETITIVE MARKETS: SOME EMPIRICAL RESULTS

Consumer representatives have often complained that retail prices tend to increase fast when wholesale prices rise but decrease slowly after wholesale markets crash (rocket-feather effect)

Evidence for this effect found in US, Australia, but mixed

Retail margin declined after liberalisation in Europe

Most academic comments point to inadequacies in the way liberalisation process was implemented rather than advocating return of price controls

Yet, many governments are not persuaded

147

PRICING: ITEMS & ISSUES (1)

Marginal cost means cost of the most expensive source (field or import) • conveying information about cost of further consumption

Supply price must include:• Infrastructure cost

• Exploration costs

• Natural gas scarcity value

Infrastructure cost• Includes: wells, upstream pipelines, treatment plants, long distance

pipelines, LNG liquefaction/shipping/regasification facilities

• Approach may be similar to networks:

Price = (Cost of “marginal” supply) / Quantity =

= RAB*Rate of Return+Depreciation+OPEX) / Quantity

148

HOW TO REGULATE GAS PRICES: KEY ISSUES (1)

The Retail Margin• Methodology (RAB/WACC) used for infrastructure pricing not suitable

for retail (trading) margin, as capital is very small

• May use empirically based margins

• In Italy and France, such margins have been recently assessed at 10-13%, including costs of the retailing companies

Rate Of Return• In producing countries, it is often hard to define market risk premium

or industry risk (beta factor)

• Must consider risk of oil&gas industry, far higher than networks’

• Typical (hard currency) rates of return for oil & gas productionbetween 12 and 16%

149

HOW TO REGULATE GAS PRICES: KEY ISSUES (2)

Gas Purchase Incentives

• If the gas purchase price is passed through to end users, suppliers mayhave an incentive to collude with producers and agree on higher thannecessary prices

• Therefore some EU & US regulators have linked the pass-thru to publicindexes, so that purchasers are incentivised to “bargain hard” and canretain the gains

• Profit sharing may also be used as an incentive, e.g. 50% of lower costw.r.t. benchmark retained by supplier

150

GAS PRICE CONTROLS: PROBLEMS OF PRODUCING COUNTRIES

In producing countries, regulators:• Tend to use average supply costs rather than marginal ones• Often neglect the scarcity value of gas and costs of unsuccessful

exploration• Sometimes prefer stable prices, neglecting market price swings• Want to keep gas price low, for social reasons and as support to

industry (including power generation)

As a consequence:• Prices are often too low to encourage new exploration and

development

• Consumption grows faster than under market-reflective pricing

• Domestic consumption uses up resources, reducing exports

These problems have occurred in many countries, e.g.:• US (1960s-70s); New Zealand (1995-2002)

• Egypt, UAE, Saudi Arabia, Algeria (to date)

• Argentina, India (after 2000)

151

• Several Middle Eastern & North African countries have lost self-sufficiency or reduced exports

Source: BP

Production & Consumption in some Middle East / North African countries

152

• Production stalled in both Argentina and India, despite significantresources. Both became net importers. Low regulated prices widelyblamed

Source: BP

Production & Consumption in Argentina and India

SUPPLY PRICING / REGULATION IN SELECTED COUNTRIES

153

Country Wellhead /

Wholesale

Residential &

Commercial

Industry Power

generation

US GOG HUB/RCS GOG GOG

Brazil RCS RCS RCS RSP

Argentina RBC RSP RSP RSP

Netherlands GOG GOG GOG GOG

France GOG HUB/RCS HUB/RCS GOG

Italy GOG HUB/RCS GOG GOG

Algeria RCS RSP RSP RSP

Egypt RCS RSP RSP RSP

Nigeria RCS RSP RSP RSP

Russian Federation GOG or RCS RBC RBC/GOG GOG

China RCS RPS NET NET

India RCS RCS RCS/GOG RCS/GOG

New Zealand GOG GOG GOG GOG

GOG = gas on gas competitionHUB = regulated after hub priceRCS = cost based regulationRSP = regulated after social criteriaRBC = regulated after but below costNET = netback from produced good

Source: NEWES Study for Israeli PUA, 2014

WHOLESALE GAS PRICING: WORLD SURVEY 2016 (International Gas Union, 2017 Report)

154

GOG = gas on gas competitionOPE = market pricing with oil price escalationBIM = Bilateral monopoly negotiationHUB = regulated after hub priceNET = netback from produced goodRCS = cost based regulationRSP = regulated after social criteriaRBC = regulated after but below costNP =No priceNK = Not known

Between 2006 and 2016:• Market based pricing rose from 61.5% to 69%• Regulated pricing declined from 38.5% to 31%• Oil price indexation still dominant in Asia & Pacific

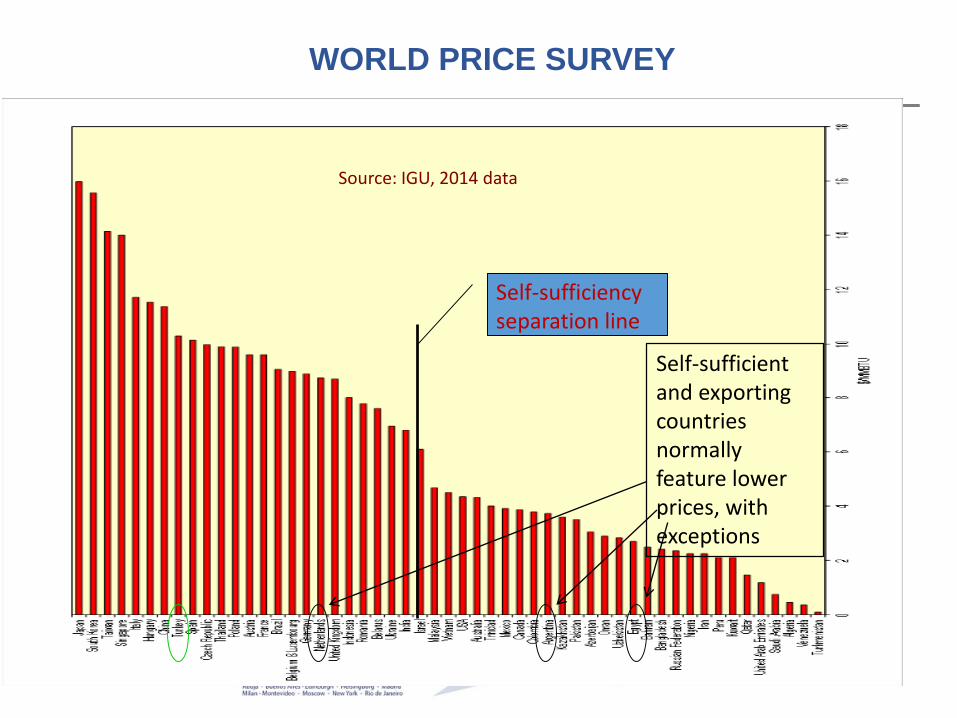

WORLD PRICE SURVEY

155

155

Self-sufficiency separation line

Self-sufficient and exporting countries normally feature lower prices, with exceptions

Source: IGU, 2014 data