Embed Size (px)

DESCRIPTION

Central Appalachian Sustainable Economies (CASE) is an interactive regional network of innovators cultivating new ideas and resources in central Appalachia to grow healthy communities. The “CASE study” component of this network expands upon past and present regional successes of the CASE network in order to operate as a guide or set of best practices for the region as a whole. This research component will also actively identify “smart approaches” for expanding CASE projects as well as assessing the growth of applied sustainability throughout the region. This particular CASE study focuses specifically on economic diversification through energy integration with a specific focus on solar development in West Virginia.

Citation preview

0

1

Special thanks to: Steve Kominar, Peni Adams, Roger Ford, Kelley Goes, David Levine, Pat Esposito, Joseph Weidman, Ken Nemeth, Jennifer Hudson, Murphy Poindexter, Dino Beckett, Darrin McCormick, Ben Carraux, Christian Smith, Jamie Throwbridge, Rob and Melissa Taylor, Jerry Mounts, Edna Thompson, Mark Mitchell, Kelly Jo Drey, Rebecca Prokity, David Mitchell, Keith Pauley, Steve Owen, Christopher Burgess, Claire Austin, Larry Sherwood, Mark Muchow, Bart Krishnamoorthy, Tom Tarka, Greg Adolfson, Kent Spellman, Mary Hunt-Lieving, Mike McKechnie, the late Mike Whitt, Leasha Johnson, Terrry Sammons, Thom Worlledge, Jessie Sayer, Billy Perish, Gonzalo Vizcardo, Crystal Good, Stephen Smith and all our family and others we forgot to mention. Special thanks to all residents of Williamson and West Virginia as a whole – your passion never ceases to inspire our work.

CASE Study

Central Appalachian Sustainable Economies (CASE) is an interactive regional network of innovators cultivating new

ideas and resources in central Appalachia to grow healthy communities. The “CASE study” component of this

network expands upon past and present regional successes of the CASE network in order to operate as a guide or

set of best practices for the region as a whole. This research component will also actively identify “smart

approaches” for expanding CASE projects as well as assessing the growth of applied sustainability throughout the

region. This particular CASE study focuses specifically on economic diversification through energy integration with a

specific focus on solar development in West Virginia.

Organization Information

Sustainable Williamson

1130 Midland Ave. Williamson, WV 25661

Tel 304-601-9091

sustainablewilliamson.org

Research Team

Primary Investigator – J. Eric Mathis: Executive Director of Sustainable Williamson

Research Director – Frank Fineis: Intern for Sustainable Williamson

Research Assistant – Alex Donesky: Intern for the City of Williamson

2

Table of Contents

I. Acronyms .............................................................................................................................. 1

II. Introduction .......................................................................................................................... 2

III. Market Analysis ..................................................................................................................... 8

IV. Solar Initiatives .................................................................................................................... 31

V. Financing options ................................................................................................................ 32

VI. Regulatory Framework ........................................................................................................ 48

VII. Utilities' Best Case Scenerios .............................................................................................. 70

VIII. References........................................................................................................................... 76

IX. Appendix A .......................................................................................................................... 83

X. Appendix B .......................................................................................................................... 84

1

AEP: American Electric Power ALEC: American Legislative Exchange Council AIRE: Appalachian Institute for Renewable Energy AMI: Advanced metering infrastructure API: Application programming interface ARC: Appalachian Regional Commission AREC: Alternative renewable energy credit ARPS: Alternative renewable portfolio standard BCCAP: Bergen County Community Action Partnership BNEF: Bloomberg New Energy Finance BOD: Board of directors CAGR: Compound annual growth rate CCA: Community Choice Aggregation CDE: Community development entity CMC: Competency Model Clearinghouse DER: Distributed Energy Resources DOE: Department of Energy DP&L: Dayton Power and Light DSIRE: Database of State Incentives for Renewables & Efficiency DSM: Demand-side Management EEI: Edison Electrical Institute EEPA: Electric energy purchase agreement EIA: Energy Information Administration E-ON: Energy Optimization Network EPA: Environmental Protection Agency FERC: Federal Energy Regulatory Commission GATS: Generation Attribute Tracking System GW(h): Gigawatt (hour) IEP: Integrated Energy Park

TM

IOU: Investor owned utility IPO: Initial public offering IREC: Interstate Renewable Energy Council ITC: Investment tax credit kW(h): Kilowatt (hour) LCOE: Leveraged cost of energy MTR: Mountaintop removal MW(h): Megawatt (hour) NABCEP: North American Board of Certified Energy Practicioners NARUC: National Association of Regulatory Utility Commissioners NEG: Net excess generation

NEM: Net energy metering NG: Natural gas NMTC: New market tax credit NREL: National Renewable Energy Laboratory O&M: Operations and Maintenance PACE: Property Assessed Clean Energy PJM: PJM Interconnection LLC PPA: Power purchase agreement PSC: Public Services Commission PUC: Public Utilities Commission PUCO: Public Utilities Commission of Ohio PURPA: Public Utility Regulatory Policies Act PV: Photovoltaic QEI: Qualified equity investor QF: Qualifying facility RE: Renewable energy REC: Renewable energy credit REPI: Renewable Energy Production Incentive RFP: Request for proposals RPS: Renewable portfolio standard REW: Renewable Energy World (magazine) ROI: Return on Investment SAPC: Solar Access to Public Capital SBA: Small Business Administration SEIA: Solar Energy Industries Association SEPA: Solar Electric Power Association SGIP: Small Generator Interconnection Procedures SPPA: Solar power purchase agreement SREC: Solar renewable energy credit TOU: Time-of-use TPO: Third-party ownership USDA: United States Department of Agriculture VPP: Virtual power plant WVEDA: West Virginia Economic Development Authority WVEC: West Virginia Environmental Council WVU: West Virginia University

Acronyms

2

Within America’s present energy paradigm of drawing lines in the sand, we have come to a

crossroads as we consider the future sustainability of America’s global position in traditional as

well as emerging energy markets. A strict demarcation has been drawn where we as a country

either take the high road and adopt a genuine “all-the-above” energy strategy or continue down

our present path of politicizing energy markets. In a January 2013 article written for Renewable

Energy World (REW), the principle investigator of this report explains the shifts in this faltering

energy paradigm, which is emerging in the least likely of places: “as the age old ‘us vs. them’

debate continues, many West Virginia residents, companies, and entrepreneurs are beginning

to identify synergies between renewable energy and fossil fuels, specifically building

unexpected coalitions in the heart of coal country.” (Mathis, 2012, para. 2).

As this study will thoroughly explain and outline, our research team, after comprehensive

research on the subject, concluded that it is in the immediate interest of the residents,

government and energy industry stakeholders of West Virginia to pursue an “integrated path

forward.” It is through the lens of Sustainable Williamson that our teams believes that this

process should not be done at the expense of the existing fossil fuels industry, but rather, adopt

an “all-of-the-above” energy policy, also referred to as an “energy mix” or “integrated energy”

approach. For example, in Clean Edge, the world’s first renewable energy research and advisory

firm, highlights in its 2013 annual report the importance of an integrated or “energy mix”

approach when it notes that:

Some argue that America’s cheap natural gas will crowd out clean energy technologies,

but we strongly believe this is not the case, as solar and wind have seen repeated record

deployment in recent years and state-based RPS [renewable portfolio standards] keep

deployment targets on track. Instead, it appears that the future of energy in the U.S.

belongs to a mix of clean energy, improved efficiency, and responsible natural gas

resource development.

Moreover, a 2012 report by Ernst & Young entitled “Cleantech Matters: Global

Competitions (Global cleantech insights and trends report)” conducted a survey of 100

executives involved in developing corporate energy strategies. Given Ernst & Young’s

impeccable reputation as a global leader in assurance, tax transaction, and advisory services

perhaps the following conclusion may provide an objective snap shot of what some could

Introduction

3

consider an “all-the-above” corporate strategy already being adopted within the private

sector:

Energy mix has become a strategic issue at the C-suite level of billion dollar corporations

as a significant – and rising – share of operating costs go to energy. While reducing

energy costs through energy efficiency measures is often the foremost objective of

energy strategy, a number of other subsidiary goals are also driving strategy, such as

energy security, carbon reduction and price stability. Regulatory compliance, together

with reputational and brand aspects, also plays a part (Ernst & Young, 2012, p. 5).

Reflecting the above “energy mix” approach, this CASE study provides a glimpse into the

potential West Virginia has for rapidly integrating solar throughout the state by targeting

residential, commercial and industrial energy markets by way of utility-scale energy

development. This potential is being actualized in real-world projects that are emerging both in

the coalfields of Southern WV and throughout the state. In a more recent REW piece written on

April 30th, 2013, the aforementioned author noted recent progress in the heart of coal country

with an emerging project of Sustainable Williamson called Energy Optimization. He stated that

Sustainable Williamson “hopes that these projects will provide a working framework for ‘energy

optimization’ in the region – transitioning communities from an aging monolithic fossil fuel

economy to a rejuvenating diversified energy mix economy without picking winners or losers”

(Mathis, 2013, para. 2).

Keeping this integrative path in mind, the following case study will examine one component of

this approach - solar.1 Additionally, given the primary purpose of this report is to provide a

comprehensive “dashboard” for West Virginia state leaders and elected officials, our team

focused on the emerging solar market in a nation-wide and state-specific context with a

particular focus on solar financing models as well as regulatory frameworks and incentive

structures. From this analysis we provide several recommendations including virtual rooftop

solar, expanded access to virtual net metering, third-party solar financing options and utility

decoupling to name a few.

In order to fully assess specific integrative approaches to energy development, our team at

Sustainable Williamson is presently conducting several experimental pilot programs in the

Southern West Virginia town of Williamson. The significant market barriers found in Williamson

provide valuable information for addressing general market barriers to solar development

1 Please note that our emphasis upon solar is not to be considered a specific bias of the proposed “integrated path

forward.” To the contrary, our team and partners are dedicated to the development of all energy resources given their market maturity/viability.

4

throughout the state and beyond. These include, most prominently, large divisions between

traditional and emerging energy resources and difficulties in attaining market penetration in

areas other than the normative “moral-markets” found within more progressive and/or

prosperous northern regions of the state (e.g., purchasing RE = saving the planet or becoming

energy independent) where return on investment (ROI) is peripheral at best. When considering

these barriers as well as our research to date, our team has developed a comprehensive

roadmap that considers five of the fundamental pre-requisites to effective solar market

penetration. The breakdown is as follows:

Market Analysis: Overview of present market conditions as well as a synthesized

roadmap for West Virginia.

Solar Initiatives: Overview of solar industry support network.

Financing Options: Overview of solar financing options.

Regulatory Framework: Specific analysis as it relates to financing options and virtual net

metering.

Utilities’ Best Case Scenarios: Potential measures that will ensure utility industry

success during solar expansion

The following two projects are underway in Williamson, WV and to a large extent, across

Southern WV to begin implementing the underpinnings of an energy and industrially diverse

West Virginia rooted in a genuine all-the-above approach:

Sustainable Williamson’s vision is to connect community stakeholders with specific programs

under the banner of “applied-sustainability” and to activate personal engagement with

economic development through market-driven projects. Williamson residents believe that

central Appalachian communities will choose to actively participate in community development

while making efforts to retain their investment within local economies by creating reliable well-

paid jobs and an expanded local tax base. Diverse participation in the development of triple-

bottom line markets will stimulate vital economic growth, thus improving health, wealth, and

well-being. It should be noted that Sustainable Williamson’s specific focus on applied

sustainability as opposed to sustainable development2 in general simply translates to

2 The authors understand this concept as it is defined by the United Nations Brudtland Report. When assessing

most literature and more importantly projects that utilize this concept, we find that there is an over emphasis

Sustainable Williamson

5

Sustainable Williamson’s emphasis upon and utilization of market-driven models that will

bolster America’s competitive position in contemporary global energy markets which considers

the merits of sustainability, that is, a strong emphasis is placed on considering the impacts our

present decisions will make on future generations (e.g., America’s national debt).

This citywide effort became possible when Williamson Mayor Darrin McCormick spoke at a city

council meeting encouraging the council and local citizens to accept energy efficiency and

renewable energy as a means to sustain a way of life for future generations. In 2011, the

Williamson Redevelopment Authority adopted a new slogan: “Where Development Meets

Sustainability.” The city, with the help of Sustainable Williamson, now hosts several community

gardens, a weekly farmers’ market, and a monthly 5k race amongst many other public health

initiatives that accompany its commitments to sustainable energy integration; the latter

commitment is the specific focus of this report.

Challenges and Opportunities

Once a favorite retailer for shoppers in Mingo and surrounding counties as well as a hub for the

coal and banking industries in the region, the City of Williamson is no longer a bustling center of

commerce it once was. Williamson’s economic decline began as a result of the devastating 1977

flood, only to be followed by another flood in 1984, just as most businesses were beginning to

recover from debt. In 1990, the Clean Air Act regulations began to affect the coal industry as

fewer mining permits were issued in the region. In Appalachia, local and state governments are

dependent on the coal industry; 40% of jobs are directly reliant on the coal industry in some

counties (West Virginia Office of Miners' Health, Safety and Training, 2012). In Williamson, the

coal industry provides financial support to community schools, local organizations, and political

campaigns.

The Appalachian Regional Commission ranks Mingo County as one of the most economically

distressed counties in Appalachia based on three economic indicators: average unemployment

rate, per capita income, and poverty rate. According to the U.S. Census Bureau, 21% of local

residents in Williamson are living below the poverty threshold, compared to the national

average of 14.3%, and in 2012 Mingo County had an annual average unemployment rate of

9.9%, compared to a national average of only 8.1% (U.S. Bureau of Labor Statistics, 2013).

upon the ecological and social components with little to no applied component regarding the economic pillar. This accounts for our use of applied sustainability which serves as a direct response to the profound shortcoming or ignoring the important role market systems play in sustaining the other two pillars.

6

According to the West Virginia Health Statistics Center, much of the state's out-migration has

been younger people who have been forced to move away to find work in other regions

because of fewer economic opportunities, a phenomenon referred to as “brain drain.”

According to a Health Statistics Center’s 2002 report, “they marry and raise their families

elsewhere. Then, after they retire, many West Virginians come back home to enjoy life in the

Mountain State” (WV Health Statistics center, 2002). Indeed, the state has the second highest

percentage of persons aged 65 and older and the third lowest percentage of people under age

18 in the nation (U.S. Census Bureau, 2008).

After years of low economic growth, Williamson’s city government leaders are consistently

looking for new ways to survive and spark economic recovery. The city has attempted hiring

freezes, layoffs, and levying greater percentages of employee contribution to health care

insurance, and yet, the essential services that the city provides continue to decline.

The consideration of geographic and topographic disadvantages plays an important role in

shaping our strategy to diversify the economic backbone of coal dependent communities, that

is, energy. According to the Appalachian Regional Commission (ARC), rural communities in

mountainous regions experience limited economic opportunity and slow growth rates. These

regions typically lack diverse inter-industry relationships between counties; coal field

communities typically mirror the coal-dependent economies of their spatial neighbors. More

importantly and to highlight the un-sustainable nature of the prevailing mono-economies found

in Southern West Virginia, the heavily coal-dependent West Virginia economy is sensitive a host

of factors – national coal demand, environmental legislation, the health of the national

economy, etc. – without having other reserve industries for potentially laid-off coal industry

workers.

Building upon a strong energy economy in southern West Virginia, Sustainable Williamson aims

to negotiate and actuate economic diversification by catalyzing local investment in municipal

and neighborhood solar/energy-efficiency projects. Residents and municipal officials are already

demonstrating widespread support for these projects because of their immediate benefits of

reducing energy burdens for households and city municipal buildings. Sustainable energy

professionals from across the nation have traveled to Williamson to share knowledge with

professionals in coal-based industries and community residents, including at-risk youth.

7

Discussions have focused on the economic feasibility, research and development, operations

and maintenance, design and installation of new sustainable energy technologies.

Gilliam Solar, a West Virginia company based in “The Heart of the Billion Dollar Coalfield”

(Williamson, WV), is a solution-based company specifically designed to bridge the gap between

the fossil fuel and solar industries. It’s a simple concept. Both energy resources are more

productive when they work in a collaborative or “integrative” fashion, rather than an

ideologically driven environment of division or “us vs. them.”3 Given this fact, Gilliam Solar is

uniquely poised to bring the promise of renewable technologies and West Virginia’s fossil fuel

based energy expertise together to the same table.

Photovoltaic (PV) Design & Installation

Through its collaborative partnerships, Gilliam Solar is presently developing several novel

approaches to developing residential-, commercial- and utility-scale solar. While potential exists

for expansion into other well-established renewable energy markets outside of central

Appalachia, Gilliam Solar is first and foremost am integrative PV company.

Target Markets

To date, Gilliam Solar has initiated important discussions and research to assess the

development of coupled generation (by means of utility-scale natural gas and solar) on both

active and inactive mine sites throughout the central Appalachian region. Gilliam Solar has

developed an innovative financing model believed to be economically attractive to coal

companies and landowners alike. Gilliam Solar is presently organizing a cross-sector coalition in

order to procure the necessary support for these projects. Perhaps their logo says it all:

3 See REW article entitled “The Importance of Understanding our Renewable Energy Worldview: Why Fossil Fuels

Are our Friends” http://www.renewableenergyworld.com/rea/blog/post/2013/05/disruptive-threatsstrategic-considerations-

a-utility-lobbying-group-keeps-it-real

Gilliam Solar

8

Market Analysis

Sustainable Williamson’s research team has analyzed several challenges facing the West

Virginia economy, its coal companies, and its electric utilities. We propose a solution to these

challenges: solar energy growth on the residential, commercial, and utility-scale levels, through

the rollout of Virtual Power Plants.

Declining Appalachian Coal Industry

The United States Energy Information Administration (EIA) projects in their Annual Energy

Outlook for 2013 that the renewable energy (RE) sector will nearly double its output from 2009

to 2035, while in the same period, it predicts that Appalachian coal production will decrease

(EIA, 2013, pp. 6, 85). Significant declines in mining productivity over the past decade have

substantially reduced the long term sustainability of Appalachian coal. This has resulted in

higher prices for the commodity, causing the market to replace it with coal from other regions,

namely from mines farther

west with more easily

accessible deposits.

Appalachian coal output is

expected to continue on this

decline for an indefinite

period. According to the EIA’s

latest Quarterly Coal Report,

between March 2012 and

March 2013 West Virginia

coal production fell by 12.3%,

and total U.S. coal

production declined 8%

between this time as well

(EIA, 2013, p. 6).

In 1940, 1-in-5 workers in West Virginia were employed at or in support of a coal mine. Due to

mechanization and a host of other causes, by 2011 less than 5% of the state’s workers were

employed in a coal-related field, even though production had increased through 1980’s and

90’s. With Appalachian coal production predicted to decrease and employment within the

Appalachian coal production predicted to decline (USGS, 2009).

Market Analysis

9

industry to decrease even more rapidly, West Virginia needs to strongly consider adopting an

integrated path forward.

Our team suspects that the state’s dependence on price-unstable fossil fuels paired with the

growing scarcity of coal have resulted in a steeper residential electricity price increase over the

last ten years compared to nationally averaged retail prices and prices in neighboring states

Pennsylvania and Ohio (using a linear regression based upon EIA data).4 West Virginia saw an

4 The EIA calculates that West Virginia derives 96% of electricity from coal. National bituminous coal prices

increased from $39.92/short-ton in 2006 to $60.88/short-ton 2010. Sub-bituminous coal prices have likewise increased 98% between 2000 and 2010. Appalachian coal is also the most expensive in the nation. Table 7.9 Coal Prices, Selected Years, 1949-2011 [Data file]. (2011). Retrieved from Energy Information Administration website: http://www.eia.gov/coal/data.cfm#prices.

Historical employment at mines in West Virginia (left axis) and coal production in millions of tons (right axis).

10

average of .131 cents/kWh/quarter increase from October 2004 to February 2013, while the

national average was only .080 cents/kWh/quarter. That figure for Pennsylvania and Ohio was

.111 and .103 cents/kWh/quarter, respectively. It is important to note that this rate increase

discrepancy occurred despite both PA and OH establishing solar carve-outs, i.e. legislation

mandating a solar energy quota fulfilled by electrical utilities, prior to 2010. The normative

assumption is that rates increase with solar penetration. The following findings say otherwise:

In addition to the above findings, Ohio Public Utilities Commission’s recent study (August, 2013)

examined the relationship between renewable resource additions and wholesale electricity

markets in Ohio. The Staff of the Public Utilities Commission of Ohio conducted this study in an

attempt to quantify the changes in wholesale electricity prices and generator emissions that are

likely to occur as a result of the state’s Alternative Energy Portfolio Standard (AEPS)

requirements. The report concluded:

“The model simulations indicate that, consistent with theoretical expectations, Ohioans

are already benefiting from renewable resource additions through downward pressure

on wholesale market prices and reduced emissions. No severe congestion issues or

emergency curtailments were observed, even after incorporating all approved projects,

11

which suggests that the electric grid in Ohio is sufficiently robust to support the

continued development of utility-scale renewable projects.” (Ohio PUC, 2013, p. 7)

Disruptive Challenges for the Electric Utility Industry

According to a 2013 report from the Edison Electric Institute (EEI), although distributed energy

resources (DER) such as PV, wind, and geothermal systems account for less than 1% of

nationwide load, DER and demand-side management (DSM) technologies such as smart-grid

technology and energy efficiency tools pose significant “disruptive challenges” to the electric

utility industry. Along with a more energy conscious consumer and a national dialogue in favor

of efficiency, DER and DSM pose two large threats to the current utility model: decreased

growth in energy demand and additional costs to integrate and maintain these new

technologies within the existing grid infrastructure. In tandem, these effects will reduce electric

utility revenue and force electricity costs upwards, further alienating non-DER participants and

increasing the chance that these customers will consider alternative energy sources. Circling

back to the conclusions found in the Ernst & Young’s report further unpacks the demographics

and trends found within the diverse pool of utility customers as they relate to “C-suite level of

billion dollar corporations.” Indeed, these large/corporate customers are becoming more

conscious consumers by valuing the “reputational and brands aspects” of DER/DSM integration

as well as the obvious, lower energy costs.

Company self-generation of energy and integration of renewables into the energy supply

have been implemented at significant rates to meet these ends, with these practices set

to accelerate over the next five years. The main barriers to self-generation and use of

renewables are mostly related to risks and financial returns, suggesting that adoption

could come even faster with financing innovations and increase cost competitiveness of

renewables. In summary, only those corporations that have a comprehensive and diverse

energy strategy will be able to create a competitive advantage in the new world of a

more resource-efficient and low-carbon economy (Ernst & Young, 2012, p. 5).

Given this corporate trend, currently, distributed energy does not pose a near-term threat to

the utility model. However, in the next seven years this will most likely change. According to the

EEI, Bloomberg New Energy Finance (BNEF) projects that nationwide solar system installations

will continue at a 22% compound annual growth rate, reaching a total capacity of 30 gigawatts

by 2020. BNEF also projects by 2020 distributed energy resources will account for 10% of energy

capacity in the United States. This energy market shift, which corresponds to a 10% decrease in

utility load, will cause a 100% increase in electricity rates for non-DER customers. As DER

generation becomes only more widespread, “the cost of providing interconnection and back-up

12

supply for variable resources [intermittent resources without base load capacity such as wind

and PV] will add to the utility cost burden” (EEI, 2013, p. 5).

DER and DSM also have the potential to expose the electric utility to stranded costs, i.e. the

unrecovered costs associated with the investment in new generation plants and transmission

lines in the present that will go un-utilized in the future. Stranded costs will further exacerbate

retail electricity costs as well. While electricity prices are expected to increase due to scarcity as

well as socio-political trends favoring DER/DSM integration, less time will be required to achieve

PV price-parity. For approximately 16% of the U.S. retail electricity market where rates are

$0.15/kWh or above, solar has achieved price-parity with traditional energy sources. This is a

state referred to as being “in the money” or cost competitive where the cost to produce solar is

at or below the cost of producing energy from traditional resources. By 2017 the amount of the

U.S. retail electricity market “in the money” for PV will increase to 33% (EEI, 2013, p. 13). If

retail energy prices continue to increase over the next seven years at the same rate that they

have been increasing since 2005, combined with Clean Edge’s projections for trends in the

levelized cost of energy (LCOE) of solar PV, solar could be as affordable as traditional residential

electricity prices as soon as midyear of 2016. Solar energy could be affordable to all sectors of

the retail electricity market – residential, commercial, industrial, and transportation – by

midyear of 2017(EIA, 2005 – 2013) (Pernick & Wilder, 2012, p. 9).

The total effect of DER/DSM and the declining cost of PV creates what the EEI refers to as the

“vicious cycle,” illustrated below.

0

5

10

15

20

25

30

35

40

45

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Ce

nts

/ k

Wh

West Virginia Solar PV "In the Money"

Possible PVLCOE

Retail Res.

Retail All Sect.

13

As revenues decline and new energy competition evolves, the public utility credit quality rating

– currently a BBB majority, down from the AA norm during the 1980’s – will continue to erode

until public utilities face severely reduced access to low-cost capital, once the heralded strength

of the industry. The higher cost of capital will be pushed onto the consumer, who will then

further consider DER and DSM systems. This, in turn, further reduces utilities’ revenues, the

industry’s access to low-cost capital, and the competiveness of their electricity in the retail

market. EEI’s insight is recognizing similar trends that have occurred in other public regulated

sectors, that is, public utilities industry must avoid this scenario lest it die out in a similar fashion

as the airlines and telecommunications giants of the 1970’s.

The Institute highlights several beneficial industry responses to energy efficiency and

distributed generation: a stranded cost charge paid by DER and fully departing customers; a

customer advance to aid construction that recovers some upfront costs of capital expenditures

and mitigates stranded costs; and “identify[ing] new business models and services that can be

provided by electric utilities in all states to customers in order to recover lost margin while

providing valuable customer service” (EEI, 2013, p. 18). Shortly, we will address the ideal

examples and scenarios for the West Virginian electric utility industry that allow for the

recovery of stranded costs while ameliorating their structural disincentives towards DER

integration and energy efficiency measures.

Growing Solar Industry

When assessing the global energy markets, we can no longer frame renewable energy as a

marginal or alternative energy resource. With its rise in demand both nationally as well as

internationally, renewable energy generation is quickly becoming a dominant force that we

must all contend with. For example, the European Photovoltaic Industry Association’s “Global

Market Outlook for Photo-voltaics 2013-2017” major finds include:

14

Around the world, 31.1 GW of PV systems were installed in

2012, up from 30.4 GW in 2011; PV remains, after hydro and

wind power, the third most important renewable energy

source in terms of globally installed capacity.

Germany was the top market for 2011, with 7.6 GW of

newly connected systems; followed by China with an

estimated 5GW; Italy with 3.4 GW, the USA with 3.3 GW;

and Japan with an estimated 2 GW.

Under a pessimistic “business‐as‐usual” scenario, the global

annual market could reach 48 GW in 2017; under a “policy‐

driven” scenario, it could be as high as 84 GW in 2017.

IREC’s projections for U.S. solar PV capacity

We can already see from European markets that government policies incentivizing solar energy

development and use are effective in motivating consumers to buy and businesses to innovate.

For example, Germany’s implementation of a feed-in-tariff policy guaranteeing long-term power

purchasing agreements at an agreed upon price – this policy has accounted for up to 75% of all

solar deployment. Net metering and financial incentives, such as Solar Renewable Energy

Credits and feed-in tariffs for solar-generated electricity, have supported solar PV installations

both nationally and on an individual state level within the US. Though German feed-in tariffs

have begun to stifle innovation and price improvements, this is merely the result of poor tariff

design; the tariffs have served their purpose of jump-starting the renewables market

wonderfully but their slow rate decreases have created too much demand at high prices

Quick facts

Utility PV installations have

grown 670% between

2010 and 2012 (SEIA,

2013, “Introduction”).

Cumulative operating PV

capacity now stands at

7,962 MW (SEIA, 2013,

“Key Findings”)

From Q1 of 2012 to Q1 of

2013, residential system

prices fell 15.8% from

$5.86/Watt to just

$4.93/Watt (“Installed

Price”).

For the second year in a

row, PV was the number‐

one new source of

electricity generation

installed in Europe.

15

preventing competition and cost-reductions. We will discuss the solutions to this issue in the

“Financial Options” section below (Pernick & Wilder, 2013: p. 38).

In 2012, the United States’ total

installed solar capacity reached

3,328 MW, representing a 76%

growth from 2011, and it is

expected that installed capacity

will reach 4,375 MW by the end of

2013 2013 (SEIA, 2013, “Market

Outlook”). In 2012, the U.S. had

3,328 MW of installed PV capacity,

representing 10.7% of global

capacity (EPIA, 2012, p. 36). This

rapid growth rate was substantially

driven by the rise of utility-scale

solar projects across the nation (IREC, 2012, p. 17).

The Solar Foundation claims in their National Solar Job Consensus 2012 that 44.2% of all

surveyed solar firms expect to add new employees between 2012 and 2013, while only 3.6%

expect to cut solar jobs (The Solar Foundation, 2012, p. 15). While there are a range of

employment opportunities across the solar sector, many are well paid. According to the Bureau

of Labor Statistics, the mean annual wage in 2010 for electricians at a solar power plant was

$59,020, for residential/commercial solar water heater plumbers that figure was $50,550, and

solar power plant welders, cutters, solders, and brazers earned $45,990. The BLS claims that

"According to industry sources, solar installers usually have starting salaries between $30,000

and $40,000 per year," while positions requiring more education such as electrical and industrial

engineers can earn more than $90,000 annually (Hamilton, 2011, pp. 9, 16, 18). These jobs

require various levels of education and training; they include installation, manufacturing, sales,

and engineering. As the solar job force increases, new training and education programs have

rapidly developed. There will also be continuing demand across the solar financial sector as the

U.S. has been a huge innovator in project finance through the invention of no-money-down

solar leases and power purchase agreements.

As of September of 2012, there were 119,016 solar industry jobs in the United States, a 13%

increase from the 105,145 jobs twelve months prior(The Solar Foundation, 2012, p. 5). Between

August 2011 and August 2012, the fossil fuel electric generation sector lost 4,000 jobs (a 3.77%

U.S. Solar is growing exponentially (taken from SEIA, 6/2012)

16

decline), and 850 coal mining jobs were lost (a 0.83% decline). 2013 is expected to have a 17%

growth in solar industry employment with 44.2% of firms slated to hire new workers, all while

the employment growth for the nation is projected to be a modest 1.5% (p. 14).

Within the industry there will be immense growth across each solar occupation between 2012

and 2013:

1. Photovoltaic installers (21% growth)

2. Manufacturing (9% growth)

3. Sales and distribution (22% growth)

4. Project development (14% growth)

5. Other (18% growth)

These developments in the solar industry are supplemented by employment growth in energy

efficiency technologies. The Department of Energy concludes that a full deployment of smart

grid technology across West Virginia will induce $215 million of job creation (DOE NETL, 2009, p.

9). Solar DER growth must also be considered alongside the large strides made in energy

efficiency through the implementation of demand-side management technologies and the first

steps towards a smarter grid.

Developments in Demand Side Management

Perhaps the most widely implemented DSM technology is the smart meter, which allows for

semi-real-time to real-time energy data transfer between supplier and consumer. The energy

supplier may create a tiered pricing system for on-peak and off-peak load rates and the

consumer are then incentivized to reduce consumption during those hours of higher electricity

17

prices. This system will also provide the necessary information for the consumer to curtail

consumption in general. Between 2007 and 2011, the growth in smart meter installations

experienced a compound annual growth rate of around 47% and accounted for 14.1% of all

energy served in the U.S. in 2011, up from just 2.2% in 2007. Also during 2011, 20% of all public

and state owned utilities had deployed smart-meters and 31% of their employees had them as

well (Zpryme, 2013, p. 6).

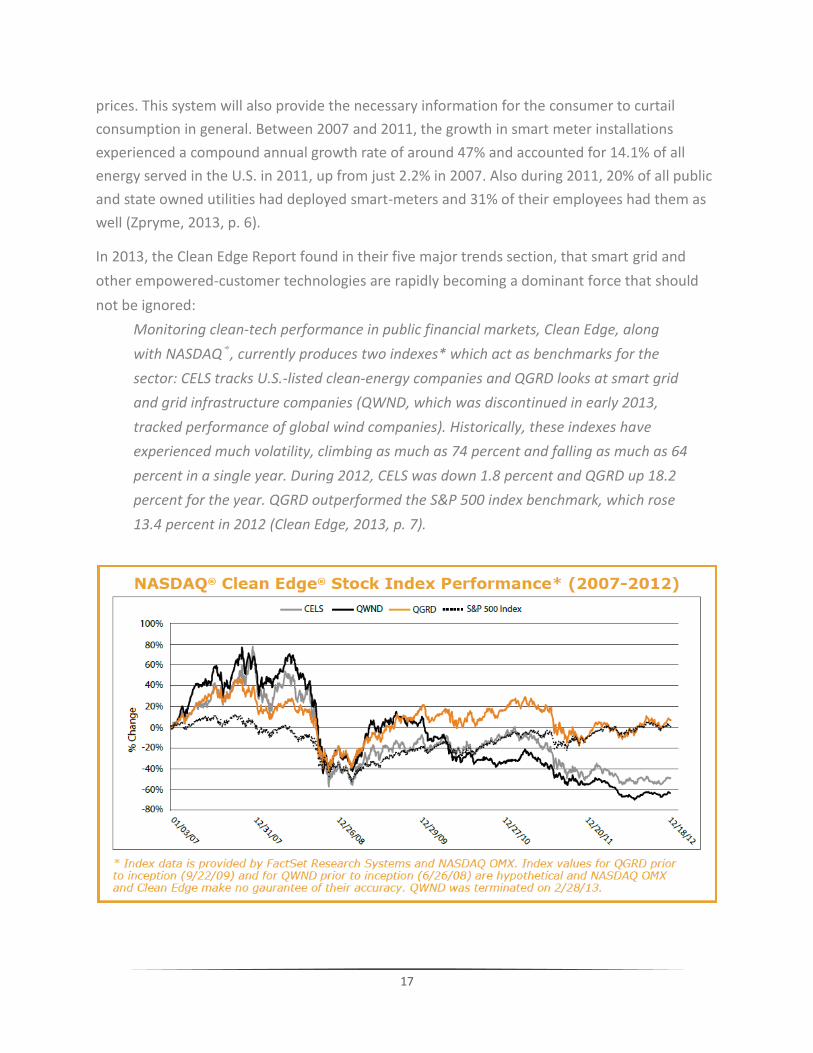

In 2013, the Clean Edge Report found in their five major trends section, that smart grid and

other empowered-customer technologies are rapidly becoming a dominant force that should

not be ignored:

Monitoring clean-tech performance in public financial markets, Clean Edge, along

with NASDAQ®, currently produces two indexes* which act as benchmarks for the

sector: CELS tracks U.S.-listed clean-energy companies and QGRD looks at smart grid

and grid infrastructure companies (QWND, which was discontinued in early 2013,

tracked performance of global wind companies). Historically, these indexes have

experienced much volatility, climbing as much as 74 percent and falling as much as 64

percent in a single year. During 2012, CELS was down 1.8 percent and QGRD up 18.2

percent for the year. QGRD outperformed the S&P 500 index benchmark, which rose

13.4 percent in 2012 (Clean Edge, 2013, p. 7).

18

Synergies between the clean tech and high tech sectors have spurred numerous firms

dedicated to utility data usage software. Silicon Valley’s darling Nest Labs ships 45,000

programmable thermostats a month; these devices analyze homeowners’ energy usage

patterns, weather forecasts, and other data to maximize energy efficiency through a

smartphone application interface (Clean Edge, 2013, p. 8). Founded in 2007, tech firm Opower

delivers utility data usage via a smart thermostat to its customers so that they can compete

with their neighbors, even Facebook friends, for energy savings. Opower estimates that its

services have saved a cumulative two terawatt-hours of electricity since its inception (p. 8).

Further application of smart grid technologies will continue to reduce consumer electrical

demand, consequently augmenting the chances of an electricity price increase, thus making PV

systems more affordable – an application of “the vicious cycle” mentioned in the above Edison

Electric Institute report.

Utilities are beginning to make use of smart grid technologies as well, thus further enabling a

more empowered-customer, a trend not unlike those seen across the high tech sectors

(cellphones that report data usage, hybrid automobiles that track fuel economy) and the

Internet (formerly top-down generated content has been supplanted by user-generated

content):

In Texas, utility Reliant Energy installs a free Nest thermostat for customers of its

Learn & Conserve energy-saving plan, while TXU Energy reported 100,000 downloads

of its iPhone and Android smart-phone app for remote thermostat control by the end

of 2012. Reliant and TXU are two of seven utilities that have implemented the Green

Button, a U.S. Department of Energy initiative for smart meter-enabled customers to

track their energy use on their utility’s web site; nearly 30 other utilities in 17 states

have committed to do the same (Clean Edge, 2013, p. 9).

Solar Development in West Virginia

Within the state of West Virginia, economic benefits from solar PV deployment are largely the

product of job-creation and expanded local tax bases. A 2010 report from Berkley concludes

that PV development creates more jobs per megawatt of capacity than any other electricity

generation option with 20 manufacturing and 13 installation/maintenance jobs created per

installed megawatt. This represents substantial potential job growth for West Virginia in an

otherwise faltering economy. While the installation and maintenance jobs created are all

intrinsically linked to local job creation, the manufacturing jobs that are created are linked to

19

the factories where the PV panels are built. We strongly believe that PV module, wafer, and

inverter manufacturing plants will be developed in WV as well.5 PV companies locate

manufacturing facilities near thriving markets to cut down on transportation costs and areas

with appealing incentives, therefore, West Virginia is uniquely suited to capitalize on the

manufacturing job creation potential associated with the growing PV market for the following

reasons (see Appendix A).

West Virginia’s location would allow manufacturers overnight access to over half of the

population of the United States markets by means of the state’s access to enormous railway

infrastructure. Also, business costs in the state are 13% below the national average according to

the West Virginia Department of Commerce. These factors, along with the presence of a labor

force already trained in the energy industry (coal and natural gas), can be utilized to establish

West Virginia as the hub for the PV industry on the eastern seaboard of the United States.

Furthermore, the coal fields of West Virginia are ripe with potential for the deployment of

utility-scale PV generation capacity, increasing aggregate demand for solar on the East Coast.

While former strip mine sites may not be attractive for most forms of investment, they are

prime locations for PV electricity generation. This massive reservoir of electrical generation can

be exported to the energy hungry population hubs of the Northeast through, for example, the

PJM power pool. The PV industry has the potential to redefine West Virginia’s economic

landscape through research, development, construction, and implementation of a domestic

renewable energy source. This can all be achieved by adopting an integrative path forward that

is built upon synergies between traditional and emerging energy resources.

Moreover, and in lieu of West Virginia supporting an integrative path forward to economic

diversification, there are additional spin offs that may spur unforeseen developments in other

sectors essentially exemplifying an emergent quality founded upon what some have called

open-innovation. In a recent report by the National Renewable Energy Lab entitled “Energy

Systems Integration: A Convergence of Ideas” it highlights some of these emergent qualities

when the authors state that “energy systems have evolved from small, local, single-service

systems (e.g., the steam engines that powered the Industrial Revolution) into highly integrated,

continental systems that deliver energy services (e.g., natural gas and electricity

transmission/distribution systems that deliver to our homes and businesses).” The report goes

on to note that “integration is also increasing between the energy system and other systems -

such as data and information networks and water systems - that traditionally have not been

5 Due to the proprietary nature of some assumptions that are informing our teams analysis, we cannot fully

disclose what we “strongly believe” to be a highly probable path forward for economic diversification in West Virginia as it relates specifically to manufacturing.

20

linked with energy” (DOE NREL, 2012, p. 3). More pointedly, the report specifically unpacks the

open-innovation quality that an integrative path forward provides:

The combination of low-cost monitoring and control and the integration of data and

information networks with energy systems is enabling advanced control and

coordination across energy pathways and scales. For example, general Electric monitors

a significant number of turbines worldwide from two locations (Schenectady, New York,

and Salzbergen, Germany) provide maintenance and operation support. In addition,

improved monitoring and control, reductions in local power production costs (e.g., from

cost-competitive photovoltaics), interactive local energy management systems, and

potential electrification of automobiles allow consumers to play an increasingly

influential role in the future of energy systems by giving them the opportunity to act as

producers as well as consumers of energy and provide services to the larger energy

system (p. 4).

With these potentials in mind as well as considering West Virginia’s most underutilized asset –

surface mining sites – perhaps the EPA has many faces within our proposed paradigm of energy

integration, one of a collaborative partner to West Virginia’s economy as opposed to an enemy.

Through its “RE-Powering America’s Land Initiative,” the U.S. EPA has instituted policies to

encourage the use of former strip mine sites for solar development. Under the terms of the

initiative, contaminated lands, landfills, and mine sites, referred to as “brownfields,” are

considered ideal hosts for renewable energy resources. Since the Initiative’s commencement in

2008, it has seen a 40% compounded annual growth rate, with large utility-scale solar projects

(10 MW +) making up nearly 60% of the total installed capacity on contaminated lands (EPA,

2013, p.1).

The EPA partnered with the U.S. Department of Energy’s National Renewable Energy

Laboratory (NREL) in August of 2010 to evaluate the potential of eight brownfield sites in Nitro,

West Virginia for utility-scale PV systems. The sites within the study were primarily used-

chemical sites and capped landfills; none were coal mines. Their report was heavily in support

of solar development, concluding that the eight sites “are all feasible areas in which to

implement solar PV systems.” The report goes on to assert that “developing solar facilities on

brownfields can provide an economically viable reuse option for sites with significant cleanup

costs or for sites where local economic conditions prohibit traditional reuse of the site, as is the

case with Nitro,[West Virginia]” (NREL, 2010, p. 35). This positive development from Nitro is

further evidence that West Virginia is well-positioned to lead the East Coast PV market.

21

IEP

Industrial

Commercial

Residential

VPP

Synthesized Roadmap for West Virginia

When considering both Sustainable Williamson and Gilliam Solar along with the findings below,

we are presented with an exciting opportunity to develop an innovative approach to solar

integration that targets both residential, commercial and industrial applications of solar PV

without ever stepping foot on a rooftop. Built upon the existing progress made by Gilliam Solar

in establishing an Integrated Energy Park TM model (IEP) for coupled generation of Natural Gas

and Solar on post-mine land use sites in southern West Virginia, Sustainable Williamson is

assessing an integrated path forward that may provide a novel strategy for the integration of

multiple energy resources in the central Appalachian coalfields and beyond which include coal,

natural gas, biomass, hydro and solar. Phase 1 of this model begins with a coupled-generation

scenario (typically 1MW of solar for every 5MW of natural gas) blending both utility-scale

Natural Gas and Solar in a profitable manner with the intention of developing a load-matching

scenario (for every MW of solar installed there is a MW of natural gas installed) by building

from WV’s existing NEM rules. This shift from coupled-generation to load-matching essentially

renders the utility-scale solar component as the primary production technology (NG -> Solar) as

opposed to a supplementary technology (Solar -> NG). In turn, it is likely that this will provide a

“north star” in terms of how West Virginia may begin developing a policy strategy with the

following delineation in mind:

To further explain this policy strategy, our team at Sustainable Williamson has developed the

following video (Energy Optimization) which specifically unpacks IEPs and how they relate to

developing virtual power plants (VPP) where the key component to this is how virtual net-

metering will provide an integrated path forward for coal country as America continues its

integration of sustainable energy resources over the coming years. The following sections

provide suggested recommendations to lower the cost of solar through enriching existing net-

metering policies as they may potentially relate to a variety of innovative financing models.

Coupled Generation

Virtual Net-Metering

Load-Matching

Virtual Power Plants

Energy Integration

22

To serve as a real world example of energy integration as it relates to Sustainable Williamson’s

pilot Energy Optimization program and the aforementioned IEPs, the City of Williamson will

follow in the footsteps of Siemens Distributed Energy Management Systems (DEMS) 2008

8.6MW pilot in Germany where the baseload will primarily be Natural Gas. With the stated goal

of the “development of marketable virtual power plant,” Siemens outlined several points that is

presently informing Williamson’s efforts:

Definition of business models in different energy markets

Definition and implementation or optimal operation strategies for distributed

generation

Implementation of innovative communication concepts between distributed generation

and DEMS (Seimens, 2013, p. 5)

It is also important to note the intended expansion of Siemens pilot to 200MW which began

merging approximately 20MW in 2012 with the objective of integrating “different distributed

energy sources such as biomass plants, biogas block heating plants, wind turbines, and

hydroelectric plants throughout the whole of Germany.” (p. 7)

The innovative nature of Sustainable Williamson’s efforts should be obvious given that “the

integrated operation of multiple integrated renewable resources, energy storage, demand

response are largely uncharted” (Seimens, 2013, p. 10) as well as considering the novelty of

IEPs which are an essential part of the energy integration equation, that is, bridging the gap

between traditional and emerging energy resources in a synergistic fashion. According to

NREL’s insightful whitepaper entitled “Energy Systems Integration: A convergence of Ideas,” an

emphasis upon synergies or a “holistic approach” is paramount because “there is significant

danger that local optimizations may produce a solution that is far from global or societal

optimum.” Given the integrative nature of the Energy Optimization program that seeks to

develop linkages between IEP’s (global optimization) and local micro-grid (local optimization)

build out, it should be noted that our approach plays a significant role in filling knowledge gaps

or management uncertainties where a “set of optimal subsystems may improve global results

and resilience, but the boundaries between subsystems are unclear, and interactions between

subsystems have not been defined” (NREL, 2012, p. 6). Moreover, “if these systems are well

integrated into the larger energy system with correct control signals, the same local controls

can be used to provide ancillary services to the grid to facilitate the use of more wind and solar

energy” (p. 7). A case in point are the load matching pursuits related to the IEP model which

involve a 1 to 1 ratio of Natural Gas to Solar (NG -> Solar).

23

Utility Sector Solar and the Probable Rise of Virtual Rooftop Solar

Paradoxically, our team has found that the paradigm of rooftop installations may be

decreasingly relevant due to the various cost efficiencies resulting from an aggregated solar

approach. These include but are not limited to: lower transaction cost, economies of scale,

lower labor cost through mechanization, and the availability of federal loan guarantees. Within

the solar energy market, there are primarily three market sectors: residential, non-residential,

and utility. Together, the residential and non-residential sectors make up “distributed

generation installations.” There is a very simple and obvious trend within the solar market, as

summarized by the Interstate Renewable Energy Council: “PV installations are getting larger,”

especially among utility-sector installations (IREC, 2012, p. 22). From 2010 to 2011 the average

size of a distributed PV installation grew by 46% to 18kW, and the average size of a utility-

sector PV installation increased by 250% to 4.62 MW.

Average size of distributed generation PV installations (IREC 2012).

The industry is clearly embracing the benefits of utility PV, as demonstrated by the sector’s

enormous growth. The rise of utility-sector solar projects began with an increase from almost

0% to 15% of all grid installed PV capacity in 2009. These projects increased to 32% of all

capacity in 2010, 38% in 2011, and finally in 2012 utility solar made up 53% of all solar capacity

in the United States, and it is the fastest-growing application of solar power plants in the PV

industry (IREC, 2013, p. 7). Large-scale solar projects will continue to grow as more states enact

higher renewable standards portfolio requirements, create larger solar-carve outs, develop

their solar renewable energy credit markets, and continue tax rebate programs that augment

24

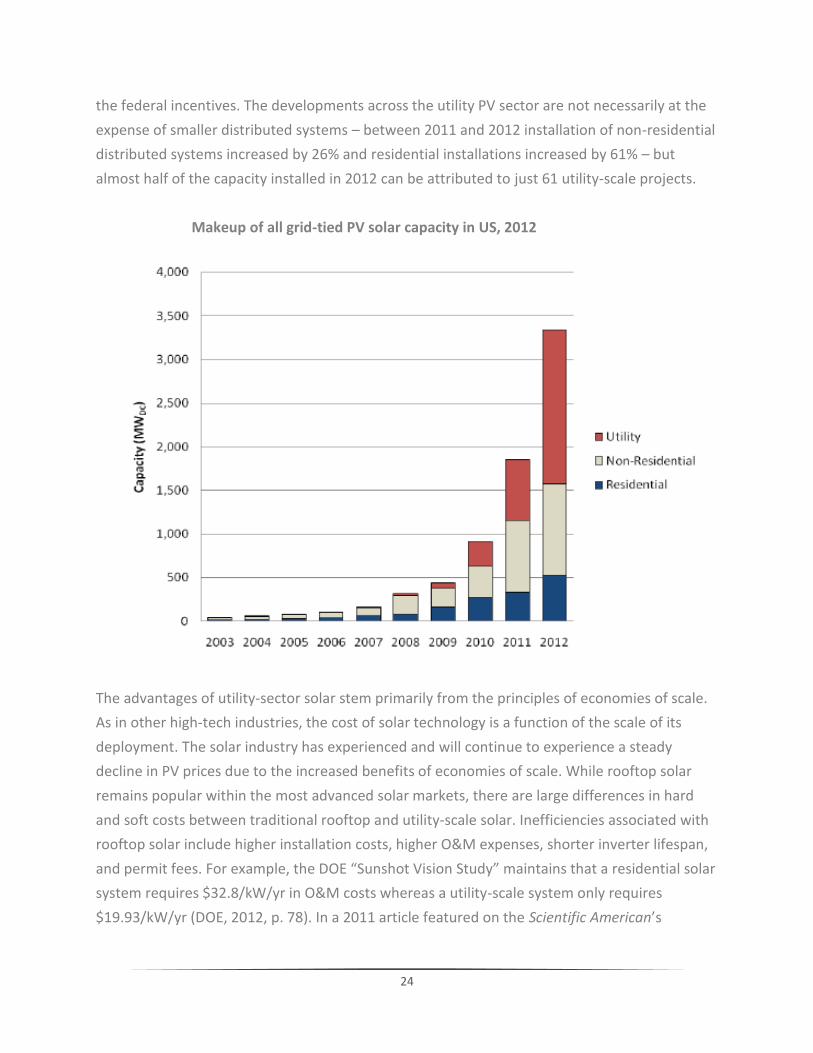

the federal incentives. The developments across the utility PV sector are not necessarily at the

expense of smaller distributed systems – between 2011 and 2012 installation of non-residential

distributed systems increased by 26% and residential installations increased by 61% – but

almost half of the capacity installed in 2012 can be attributed to just 61 utility-scale projects.

Makeup of all grid-tied PV solar capacity in US, 2012

The advantages of utility-sector solar stem primarily from the principles of economies of scale.

As in other high-tech industries, the cost of solar technology is a function of the scale of its

deployment. The solar industry has experienced and will continue to experience a steady

decline in PV prices due to the increased benefits of economies of scale. While rooftop solar

remains popular within the most advanced solar markets, there are large differences in hard

and soft costs between traditional rooftop and utility-scale solar. Inefficiencies associated with

rooftop solar include higher installation costs, higher O&M expenses, shorter inverter lifespan,

and permit fees. For example, the DOE “Sunshot Vision Study” maintains that a residential solar

system requires $32.8/kW/yr in O&M costs whereas a utility-scale system only requires

$19.93/kW/yr (DOE, 2012, p. 78). In a 2011 article featured on the Scientific American’s

25

website, DOE NREL data on the average cost per solar watt between the years 1980 and 2009

was demonstrated to follow an almost straight line on a logistic scale, implying that the cost of

solar PV falls exponentially with deployment, which suggests there may be a “Moore’s law for

solar” (Naam, 2011). When interviewed by our research team, SEPA Senior Research Associate

Bart Krishnamoorthy stated that “it is typically cheaper to install a 1 MW ground mounted over

one-hundred 10 kW rooftop systems because of soft costs and labor costs. Rather than

interconnecting one hundred systems, which takes additional time, money and permits, a 1

MW system would be a better value proposition. The price of modules also typically goes down

through large purchase orders as well; this also includes other components such as inverters

and racking supplies” (personal communication, June, 14 2013). These economies of scale are

well represented by the discrepancies between residential and utility-scale solar prices -

$4.93/Watt and $2.27/Watt, respectively, and over the past three years the cost decline has

been greater for utility installations than it has for distributed installations (SEIA, 2013,

“Installed Price”) (IREC, 2013: p 6).

Electricity prices over time, by sector. (SEIA 2013).

Another huge shortfall of rooftop solar – not all rooftops are suitable for solar installation.

Many rooftops do not face true south, the direction relevant to Northern Hemisphere solar

26

applications. Furthermore, certain rooftops are at an improper angle with the sun to

accommodate efficient solar panels. A 2012 study by the NREL found that only 22% to 27% of

residential rooftop area is suitable for hosting an on-site PV system (DOE NREL, 2012, p. 3).

Current trends across the public utility sector indicate that most of the industry remains

hesitant to develop and operate their own solar systems. In 2011, utility companies owned only

28% of utility sector PV installations, while two-thirds of the industry’s solar was obtained

through power purchase agreements, a financial tool discussed below (this was using data

extrapolated from 86% of utility-sector installations according to Larry Sherwood of IREC). For

instance, the largest two utility-scale solar projects developed in 2011, the 49 MW Mesquite

Solar 1 Plant in Arlington, AZ and the 35 MW plant in Webberville, TX, are owned by third party

financers. These third parties sell the solar energy to Pacific Gas and Electric Co. and Austin

Energy, respectively (IREC, 2012, p. 19). Many utilities seemingly go to great lengths to avoid

having to manage their own solar systems; many have developed rigorous solar purchasing

models, such as Dominion’s Solar Purchasing Program, a form of feed-in-tariff arrangement that

accounted for 2% of “utility-owned” solar capacity in 2012. In 2012 only 5% of utility-scale solar

installations were utility-owned, according to Sherwood, while 93% of utility PV is obtained

through PPAs.

Private solar financer-installers have begun to recognize the value of larger-scale solar projects

as well. Solar Mosaic, a three-year-old solar energy firm based in Oakland, CA, obtained over

$300,000 in private investments for a crowd-sourced solar initiative in a matter of twenty-four

hours in January 2013. The model works through small private contributors who may invest as

little as $25 into a given solar project and who are rewarded with a typical return of 4.5% once

the project begins operation for local energy consumers. Solar Mosaic’s first five projects were

their smallest – PV systems ranging from 1.5 kW to 29 kW – and they did not include a return

on investment (Solar Mosaic, “Browse Investments”). Since the firm’s sixth project, which

began the return on investment trend, their projects have been growing to full commercial-

scale capacity, reaching 114 kW and 487 kW systems as of late.

Perhaps more importantly, the solar installer-financer market leader, SolarCity, launched a

successful IPO at the end of 2012. Since 2008, the company has integrated large distributed

installations with power agreements to supply corporations such as Wal-Mart, Toyota, SpaceX,

and eBay with solar energy. SolarCity is also beginning to incorporate ground-mounted PV

27

systems, as in the case of the 947 kW King Estate Winery project. SolarStrong’s largest

completed project to date is a 6 MW ground-mount and rooftop system for the Davis-Monthan

Air Force base in Tucson, AZ (SolarCity, “Military”). Be it small 2kW residential rooftop solar or

multi-megawatt systems, SolarCity views itself as a utility company. “We sell energy, not

equipment,” says SolarCity CEO Lyndon Rive. Terry Grant, managing director at investment

bank Marathon Capital states, “SolarCity said to the investment world: people always pay their

utility bill…If they can act like a utility that happens to be solar, that’s a really good thing” (Clean

Edge, 2013, p. 11). SolarCity is also aware of the large risks and inconveniences that may come

with installing larger systems – non-residential solar market volatility, longer project timelines,

lengthy RFP bidding processes, and the fact that municipal, industrial, and commercial clients

typically face different electricity rates and rate structures than residential clients, among other

issues. Thus, compared to the first quarter of 2012 when non-residential systems made up

45.5% of the firm’s new installations, 190 of SolarCity’s 250 MW to be installed for 2013 will be

dedicated to residential systems (Kurlewitz, 2013). We suspect that SolarCity will remain

focused on its residential third party ownership model due to these difficulties in working

across sectors. Nonetheless, IREC’s 2013 “U.S. Solar Market Trends” report concludes “U.S. PV

market growth will continue in 2013, with larger utility-scale projects leading the way” (IREC,

2013, p. 17).

A virtual rooftop system, i.e. a local offsite utility-scale solar array that distributes energy to

individual residences, avoids the inefficiencies of rooftop solar (higher installation costs, higher

O&M expenses, shorter inverter lifespan, etc.). This model should make use of “virtual” meter

aggregation, or virtual net metering, a practice currently in place in a number of states including

West Virginia. Within a virtual net metering system multiple electric meters are collected into

one inflow-outflow mechanism so that more than one consumer may benefit from a single

solar array. A virtual rooftop system is one in which many residents will acquire energy from

the centralized generation array as well as supplemental energy from conventional utility

generation when load cannot be met by solar such as the load-matching scenario mentioned

above (NG -> Solar). This system must be net-metered: the offsite solar array will be monitored

for both the energy it feeds into the grid (outflow) and the energy required on the opposite side

of the system when solar does not satisfy demand (inflow). Net generation credits will be

passed on to the virtual rooftop participants, further incentivizing investment through low

energy prices. A virtual rooftop system, similar to a solar garden, is very much akin to a type of

Community Shared Solar model, discussed in the “Financial Options” section below. For

28

example, the Clean Energy Collective, LLC (CEC) located in Carbondale, CO, provides a member-

owned model that enables individuals to directly own panels in a commercial-scale community

shared solar farm through power purchase agreements with the local electric utilities (DOE

NREL, 2012, p. 22). Moreover, given that a dominant trend in any given market is a tendency to

migrate towards economies of scale, these recent trends in utility-scale solar development and

integration should be considered when assessing the almost ideological nature of rooftop solar

for the sake of VPP deployment.

Job Creation and Tax Revenue

The first step in assessing job output from each potential IEP required a baseline density of

natural gas wells within a reasonable distance from the site – 5 miles. Using natural gas

wellhead data from the West Virginia Geologic and Economic Survey’s interactive online maps,

an average production for each wellhead was evaluated based upon production between the

years 2008 and 2012. Using .KMZ files pinpointing ten “AM active” and “A2 active, reclamation”

surface coal mining sites across six West Virginia counties, natural gas wellhead data from the

West Virginia Geological and Economic Survey’s interactive maps, and information from the gas

generator suppliers, it was determined that around 13 wells on average would be able to

supply our 10 MW natural gas facility (see Appendix B). Our team found at least 60 active

surface mining sites, all of which were in close proximity to over 13 wellheads. Running NREL’s

Jobs and Economic Development Impact models for 2 MW of solar capacity and 10 MW of

natural gas capacity, the following table displays potential job growth for West Virginia given a

full deployment of IEP’s across the state:

Construction

period* jobs per

site

Operations

period** jobs per

site

Full

deployment

construction

period* jobs

Full deployment

operations period**

jobs

Solar 16 1 960 60

Natural gas 28 12 1680 720

Total 44 13 2640 780

*Construction period jobs are defined in full-time job equivalents, or 2080 hour/year units; that is, the number of full-time

jobs sustained for one year during the span of IEP construction. Full deployment refers to the construction of 60 IEP’s.

**Operations period jobs are sustained throughout the lifespan of the IEP.

29

Again, this is a conservative estimate of job creation, especially given that these figures only

include solar and natural gas deployment, neglecting biomass and smart coal

development/research potential on these sites.

As for tax estimates, each integrated energy park would be subject to the West Virginia

business and operations (B&O) tax as well as the local property tax. According to data provided

by Mark Muchow and Jeff Amburgey of the West Virginia Department of Revenue, as well as

being subject to a 6.5% corporation net income tax, each 12 MW IEP would be expected to

contribute around $54,500 per year in B&O tax. As for property taxes, each IEP would be

subject to an average 2.21% or 2.85% tax on 60% of assessed land value, depending on whether

the site is located outside of or within a municipality. In total, the IEP model presents large job

creation and tax revenue growth for West Virginia as well as for coal companies with

performance bonds tied up in the reclamation process.

30

Recommendation: Activate the West Virginia Solar Energy Industry Association (WV-SEIA) and

develop the board of directors (BOD). The Solar Energy Industry Association is a national trade

association dedicated to the many aspects of solar project development, and it has well-

established state chapters operating in fourteen states. The WV-SEIA board of directors should

represent a diverse body of solar industry and energy policy experts throughout West Virginia.

This association should actively remain a neutral market-development entity and avoid any and

all relationships with entrenched environmental groups6 in order to develop a collaborative and,

in the end, successful policy strategy.

At present, there are few programs that encourage collaboration across the energy sector. To

date, Community Power Network has initiated an open discussion group entitled WV-SUN to

encourage emerging advocates of solar to engage in open discussion regarding developing the

solar industry in West Virginia. Additionally, the West Virginia Environmental Council (WVEC)

has been the primary legislative body for the solar industry to date.

The WVEC

In July 2008 the West Virginia Environmental Council published the “West Virginia

Citizens’ Energy Plan” recommending that the state implement a renewable portfolio

standard requiring public electric utilities to generate 25% of their energy from

renewables (WVEC, 208, p.9). The legislature passed RPS legislation in 2009 with a goal

of 25% of energy to be derived from renewable and alternative energy sources including

natural gas and clean coal technologies. The WVEC also recommended the

implementation of a state tax incentive for solar systems, in particular, solar water

heaters. This was also enacted in 2009.

According to Don Garvin, Legislative Coordinator for the WVEC, the group’s “most

important legislative accomplishment regarding solar is the $2000 residential solar tax

credit passed by the legislature in 2009.” This state income tax credit allows for a private

resident to receive up to a credit worth 30% of the installed cost of the solar system,

6 Environmental groups that are explicitly anti-fossil fuel and would not be supportive of a collaborative approach

suggested by this report, that is, an integrated path forward.

Solar Initiatives

31

with a cap at $2000 (personal communication, July 26, 2013). The state income tax

credit for solar is slated to expire in July of 2014.

In 2012 the WVEC successfully lobbied for House Bill 2740. The bill reads as follows:

“Therefore, any covenant, restriction, or condition contained in any governing

document of a housing association executed or recorded after the effective date of this

section that effectively prohibits or restricts the installation or use of a solar energy

system is void and unenforceable…” That a housing association can refuse or deny the

implementation of solar systems in “common areas” and “common structures” remains

valid.

Universities

West Virginia University’s participation in the Department of Energy’s Solar Decathlon:

WVU is competing in the 2013 Solar Decathlon with their entry, a house entitled

“PEAK.” PEAK is a self-sustaining log cabin structure that utilizes a PV generation system

as well as a solar powered hot water system, along with structural insulated panels and

many smart-technology applications that minimize energy usage (WVU Solar Decathlon,

“The Design”).

Marshall University’s Center for Environmental, Geotechnical, and Applied Sciences

completed a 6 kW solar project atop University High School in Huntington in partnership

with the West Virginia Department of Energy and the West Virginia Brownfields

Assistance Center. University High School itself is located on a reclaimed surface mine

site. The system includes real-time data monitoring that will be incorporated into the

school’s science classes (Marshall University, 2012).

The American Public University System in Charles Town, WV is currently home to the

largest solar array in the state. The system was successfully completed in the middle

part of 2012, and it is a 407 kW-capacity, 1600-panel array.

32

Recommendation: Upon consideration of regulatory recommendations (below), the following financing options should be aggressively pursued in collaboration with our team of finance experts to further reduce barriers to market penetration.

The three main pillars of competitiveness in the solar industry are the ability to acquire

customers at low cost, install inexpensively, and achieve low cost of capital for leases or power

purchase agreements. To realize a low cost of capital solar, dealers and developers must often

partner with so-called “tax equity” investors due to the structure of state and federal solar

incentives. Successful solar financing models make strategic use of as many municipal, state

and federal incentives as possible but maintain consideration of market trends and technical

details. The current market orientation away from rooftop and towards utility scale solar – as

discussed in the market analysis – and the technical efficiencies of the latter which account for

this shift, weigh heavily in the financial analyses and recommendations for our own projects.

Organizations seeking to develop solar energy on their own facilities (“hosts”) should

thoroughly review the relative advantages and disadvantages of the precedent solar financing

models when designing their own approach. They should also research any relevant

government incentives applicable to their jurisdiction and local solar energy service providers

should they choose to develop solar energy. This section discusses some of the major solar

energy financing models and is intended to assist policymakers, businesses, nonprofits,

government agencies, suppliers, service providers and contractors, and others prospectively

pursuing solar energy development.

Below are a variety of models that have been devised by a broad range of solar investors and

developers to most effectively take advantage of state and federal incentive structures given

their circumstances.

Commercial Enterprises and Private Individuals

Self-Ownership and Self-Financing

Simply put, in the self-ownership and self-financing model a company (the host) purchases and

develops a solar project from a solar energy developer, paying the up-front costs. The energy

Financing Options

33