Embed Size (px)

Citation preview

www.macpas.com

hosted by:

2012 Spring ConStruCtion Seminarmay 18, 2012

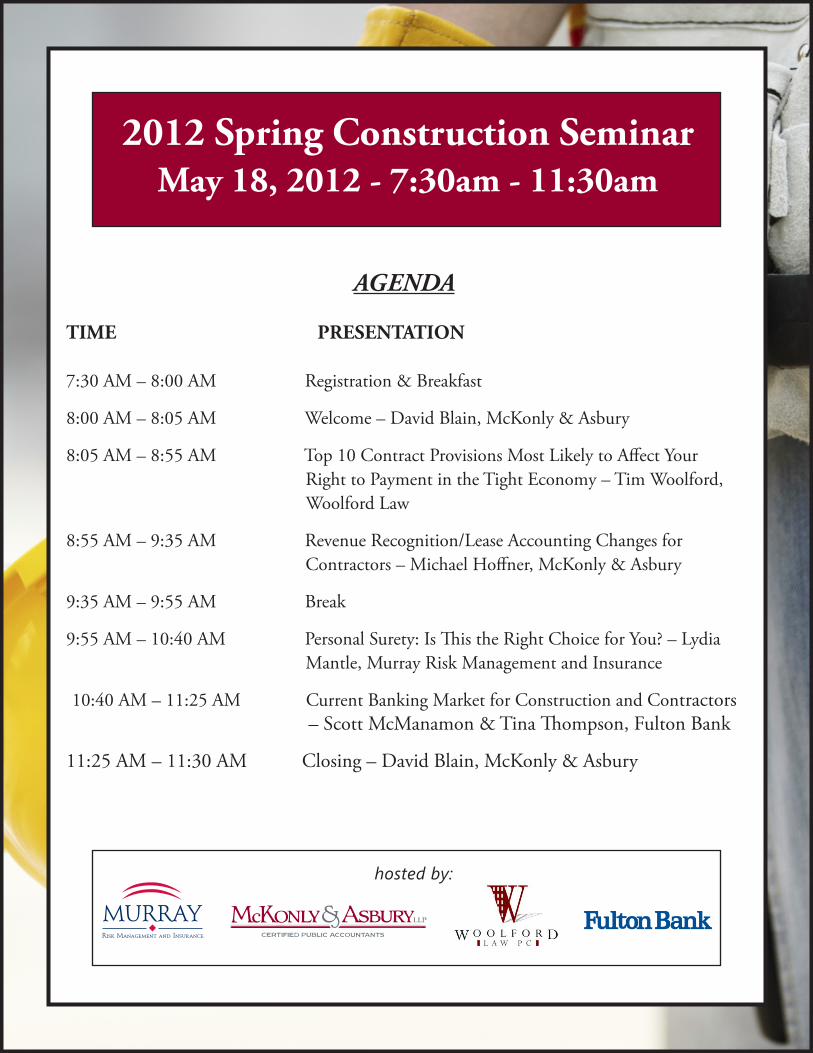

2012 Spring Construction SeminarMay 18, 2012 - 7:30am - 11:30am

AGENDA

TIME PRESENTATION

7:30 AM – 8:00 AM Registration & Breakfast

8:00 AM – 8:05 AM Welcome – David Blain, McKonly & Asbury

8:05 AM – 8:55 AM Top 10 Contract Provisions Most Likely to Affect Your Right to Payment in the Tight Economy – Tim Woolford, Woolford Law

8:55 AM – 9:35 AM Revenue Recognition/Lease Accounting Changes for Contractors – Michael Hoffner, McKonly & Asbury

9:35 AM – 9:55 AM Break

9:55 AM – 10:40 AM Personal Surety: Is This the Right Choice for You? – Lydia Mantle, Murray Risk Management and Insurance

10:40 AM – 11:25 AM Current Banking Market for Construction and Contractors – Scott McManamon & Tina Thompson, Fulton Bank

11:25 AM – 11:30 AM Closing – David Blain, McKonly & Asbury

hosted by:

Speakers at a Glance

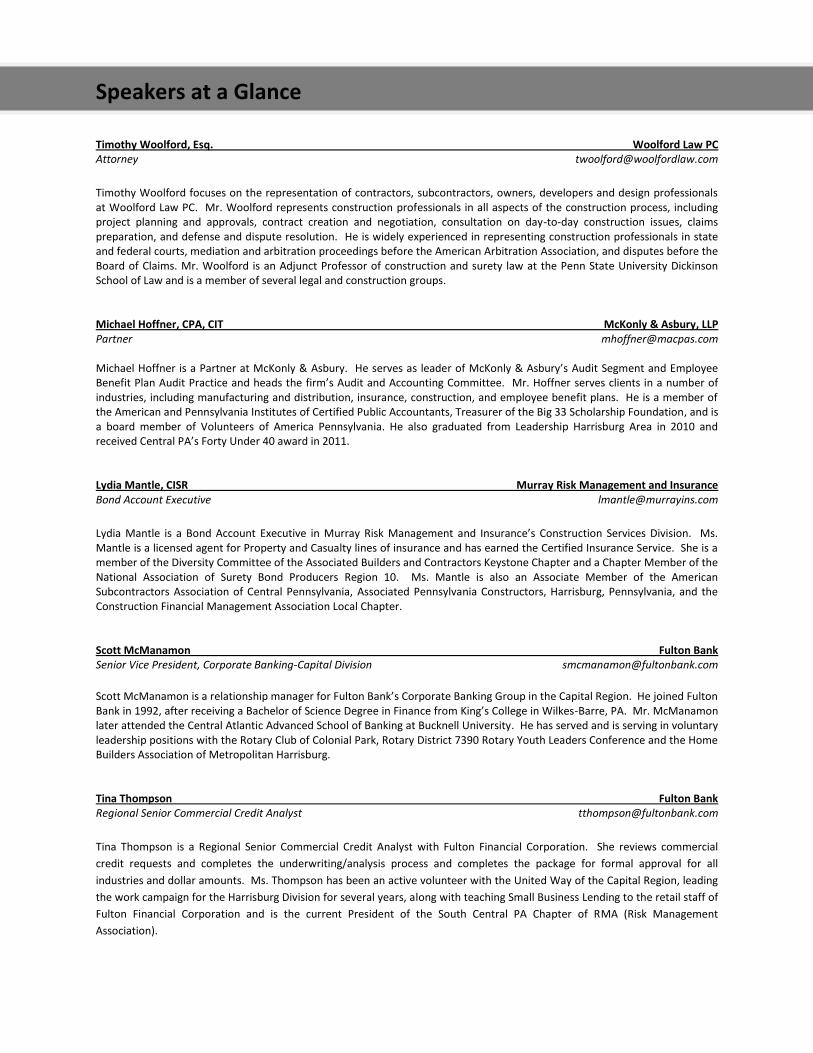

Timothy Woolford, Esq. Woolford Law PC Attorney [email protected]

Timothy Woolford focuses on the representation of contractors, subcontractors, owners, developers and design professionals at Woolford Law PC. Mr. Woolford represents construction professionals in all aspects of the construction process, including project planning and approvals, contract creation and negotiation, consultation on day-to-day construction issues, claims preparation, and defense and dispute resolution. He is widely experienced in representing construction professionals in state and federal courts, mediation and arbitration proceedings before the American Arbitration Association, and disputes before the Board of Claims. Mr. Woolford is an Adjunct Professor of construction and surety law at the Penn State University Dickinson School of Law and is a member of several legal and construction groups. Michael Hoffner, CPA, CIT McKonly & Asbury, LLP Partner [email protected] Michael Hoffner is a Partner at McKonly & Asbury. He serves as leader of McKonly & Asbury’s Audit Segment and Employee Benefit Plan Audit Practice and heads the firm’s Audit and Accounting Committee. Mr. Hoffner serves clients in a number of industries, including manufacturing and distribution, insurance, construction, and employee benefit plans. He is a member of the American and Pennsylvania Institutes of Certified Public Accountants, Treasurer of the Big 33 Scholarship Foundation, and is a board member of Volunteers of America Pennsylvania. He also graduated from Leadership Harrisburg Area in 2010 and received Central PA’s Forty Under 40 award in 2011. Lydia Mantle, CISR Murray Risk Management and Insurance Bond Account Executive [email protected]

Lydia Mantle is a Bond Account Executive in Murray Risk Management and Insurance’s Construction Services Division. Ms. Mantle is a licensed agent for Property and Casualty lines of insurance and has earned the Certified Insurance Service. She is a member of the Diversity Committee of the Associated Builders and Contractors Keystone Chapter and a Chapter Member of the National Association of Surety Bond Producers Region 10. Ms. Mantle is also an Associate Member of the American Subcontractors Association of Central Pennsylvania, Associated Pennsylvania Constructors, Harrisburg, Pennsylvania, and the Construction Financial Management Association Local Chapter. Scott McManamon Fulton Bank Senior Vice President, Corporate Banking-Capital Division [email protected]

Scott McManamon is a relationship manager for Fulton Bank’s Corporate Banking Group in the Capital Region. He joined Fulton Bank in 1992, after receiving a Bachelor of Science Degree in Finance from King’s College in Wilkes-Barre, PA. Mr. McManamon later attended the Central Atlantic Advanced School of Banking at Bucknell University. He has served and is serving in voluntary leadership positions with the Rotary Club of Colonial Park, Rotary District 7390 Rotary Youth Leaders Conference and the Home Builders Association of Metropolitan Harrisburg. Tina Thompson Fulton Bank Regional Senior Commercial Credit Analyst [email protected]

Tina Thompson is a Regional Senior Commercial Credit Analyst with Fulton Financial Corporation. She reviews commercial

credit requests and completes the underwriting/analysis process and completes the package for formal approval for all

industries and dollar amounts. Ms. Thompson has been an active volunteer with the United Way of the Capital Region, leading

the work campaign for the Harrisburg Division for several years, along with teaching Small Business Lending to the retail staff of

Fulton Financial Corporation and is the current President of the South Central PA Chapter of RMA (Risk Management

Association).

1

2012 Spring Construction Seminar

May 18, 2012

Welcome!

hosted by:

Top 10 Contract Provisions Most Likely to Affect Your Right to Payment in this Tight

Economy

2012 Construction Industry Seminar

2

About Tim Woolford and Woolford Law

• Adjunct Professor, Dickinson School of Law of Penn State University: Construction & Surety Law

• Regularly drafts and negotiates contracts for his construction clients

• Devotes his practice exclusively to representing contractors, subcontractors, owners and design professionals in the construction industry

• Frequently contributes to regional and national publications, and regularly speaks on a variety of construction-related legal topics

• Holds seminars for construction companies on construction project documentation and other topics

• For more information and helpful articles, visit www.woolfordlaw.com

2

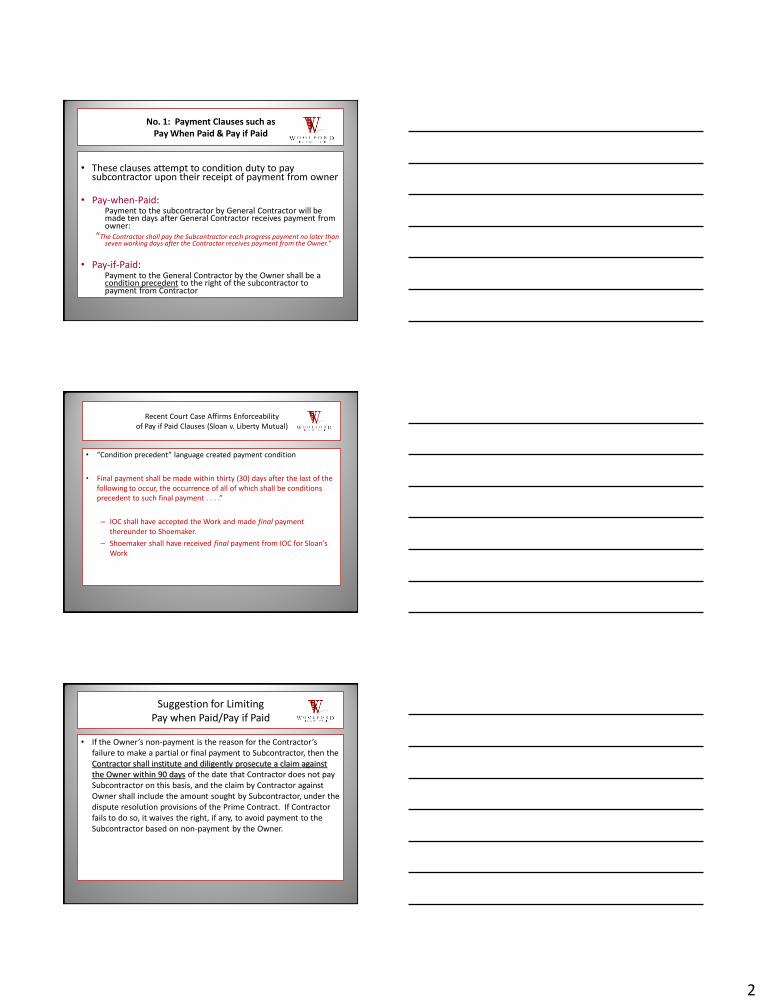

No. 1: Payment Clauses such as Pay When Paid & Pay if Paid

• These clauses attempt to condition duty to pay

subcontractor upon their receipt of payment from owner

• Pay-when-Paid: Payment to the subcontractor by General Contractor will be

made ten days after General Contractor receives payment from owner:

“The Contractor shall pay the Subcontractor each progress payment no later than seven working days after the Contractor receives payment from the Owner.”

• Pay-if-Paid:

Payment to the General Contractor by the Owner shall be a condition precedent to the right of the subcontractor to payment from Contractor

Recent Court Case Affirms Enforceability of Pay if Paid Clauses (Sloan v. Liberty Mutual)

• “Condition precedent” language created payment condition

• Final payment shall be made within thirty (30) days after the last of the following to occur, the occurrence of all of which shall be conditions precedent to such final payment . . . .”

– IOC shall have accepted the Work and made final payment thereunder to Shoemaker.

– Shoemaker shall have received final payment from IOC for Sloan’s Work

Suggestion for Limiting Pay when Paid/Pay if Paid

• If the Owner’s non-payment is the reason for the Contractor’s failure to make a partial or final payment to Subcontractor, then the Contractor shall institute and diligently prosecute a claim against the Owner within 90 days of the date that Contractor does not pay Subcontractor on this basis, and the claim by Contractor against Owner shall include the amount sought by Subcontractor, under the dispute resolution provisions of the Prime Contract. If Contractor fails to do so, it waives the right, if any, to avoid payment to the Subcontractor based on non-payment by the Owner.

3

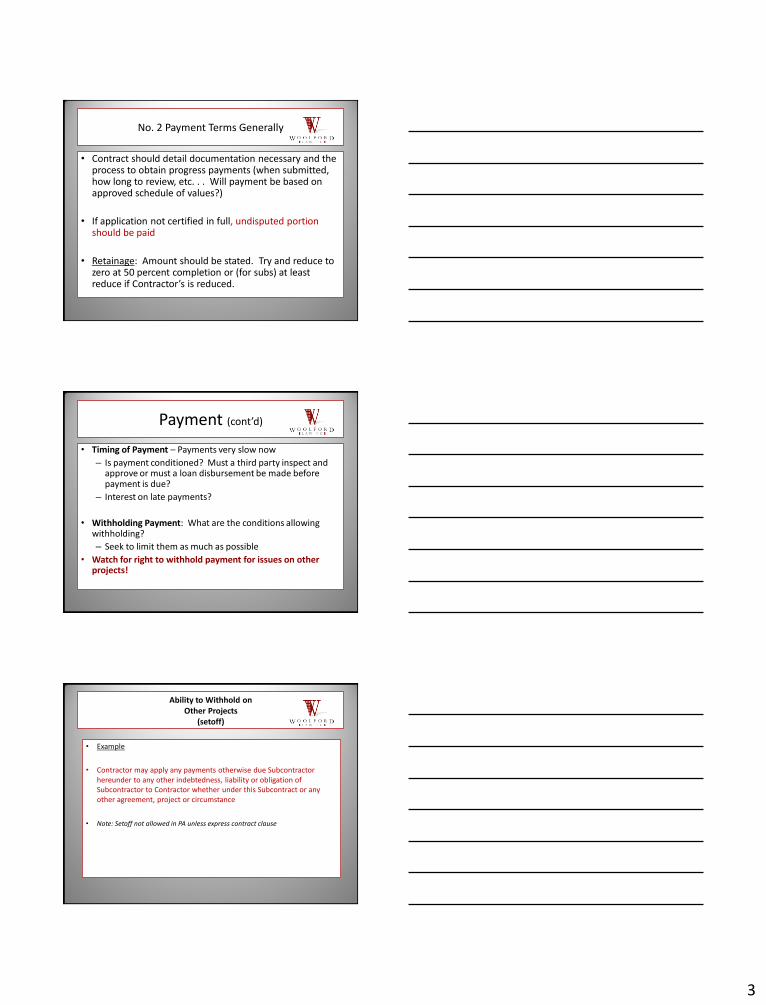

No. 2 Payment Terms Generally

• Contract should detail documentation necessary and the process to obtain progress payments (when submitted, how long to review, etc. . . Will payment be based on approved schedule of values?)

• If application not certified in full, undisputed portion should be paid

• Retainage: Amount should be stated. Try and reduce to zero at 50 percent completion or (for subs) at least reduce if Contractor’s is reduced.

Payment (cont’d)

• Timing of Payment – Payments very slow now

– Is payment conditioned? Must a third party inspect and approve or must a loan disbursement be made before payment is due?

– Interest on late payments?

• Withholding Payment: What are the conditions allowing withholding?

– Seek to limit them as much as possible

• Watch for right to withhold payment for issues on other projects!

Ability to Withhold on Other Projects

(setoff)

• Example

• Contractor may apply any payments otherwise due Subcontractor hereunder to any other indebtedness, liability or obligation of Subcontractor to Contractor whether under this Subcontract or any other agreement, project or circumstance

• Note: Setoff not allowed in PA unless express contract clause

4

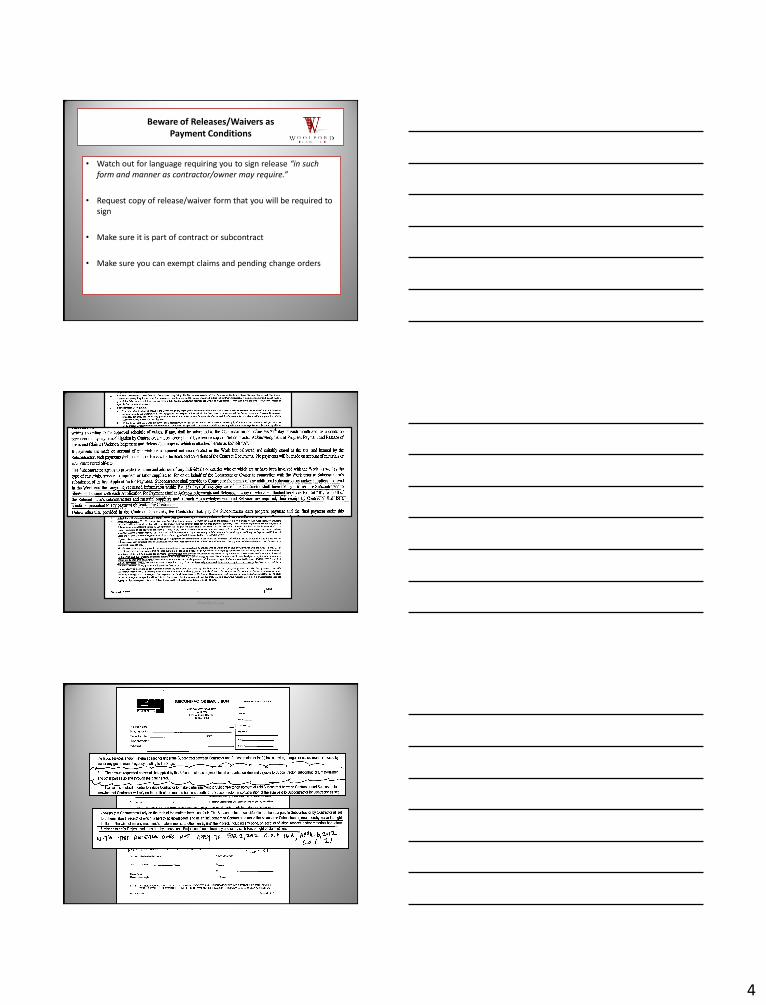

Beware of Releases/Waivers as Payment Conditions

• Watch out for language requiring you to sign release “in such form and manner as contractor/owner may require.”

• Request copy of release/waiver form that you will be required to sign

• Make sure it is part of contract or subcontract

• Make sure you can exempt claims and pending change orders

Woolford Law

Insert release

5

13 WOOLFORD LAW

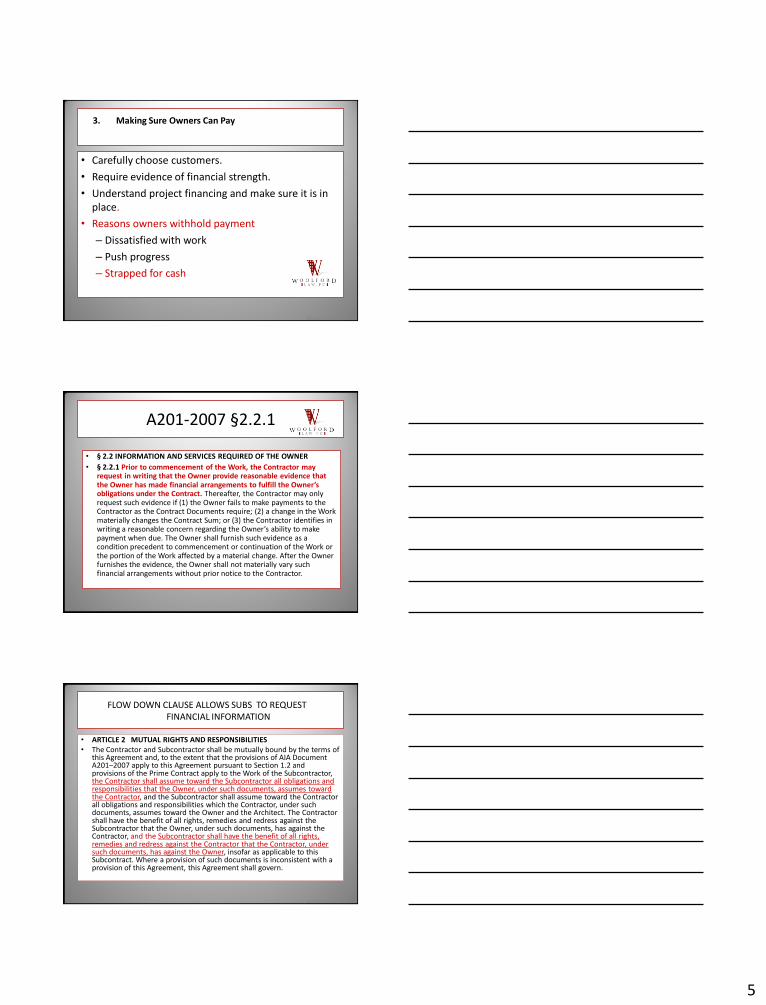

3. Making Sure Owners Can Pay

• Carefully choose customers.

• Require evidence of financial strength.

• Understand project financing and make sure it is in place.

• Reasons owners withhold payment

– Dissatisfied with work

– Push progress

– Strapped for cash

14

A201-2007 §2.2.1

• § 2.2 INFORMATION AND SERVICES REQUIRED OF THE OWNER

• § 2.2.1 Prior to commencement of the Work, the Contractor may request in writing that the Owner provide reasonable evidence that the Owner has made financial arrangements to fulfill the Owner’s obligations under the Contract. Thereafter, the Contractor may only request such evidence if (1) the Owner fails to make payments to the Contractor as the Contract Documents require; (2) a change in the Work materially changes the Contract Sum; or (3) the Contractor identifies in writing a reasonable concern regarding the Owner’s ability to make payment when due. The Owner shall furnish such evidence as a condition precedent to commencement or continuation of the Work or the portion of the Work affected by a material change. After the Owner furnishes the evidence, the Owner shall not materially vary such financial arrangements without prior notice to the Contractor.

15 WOOLFORD LAW

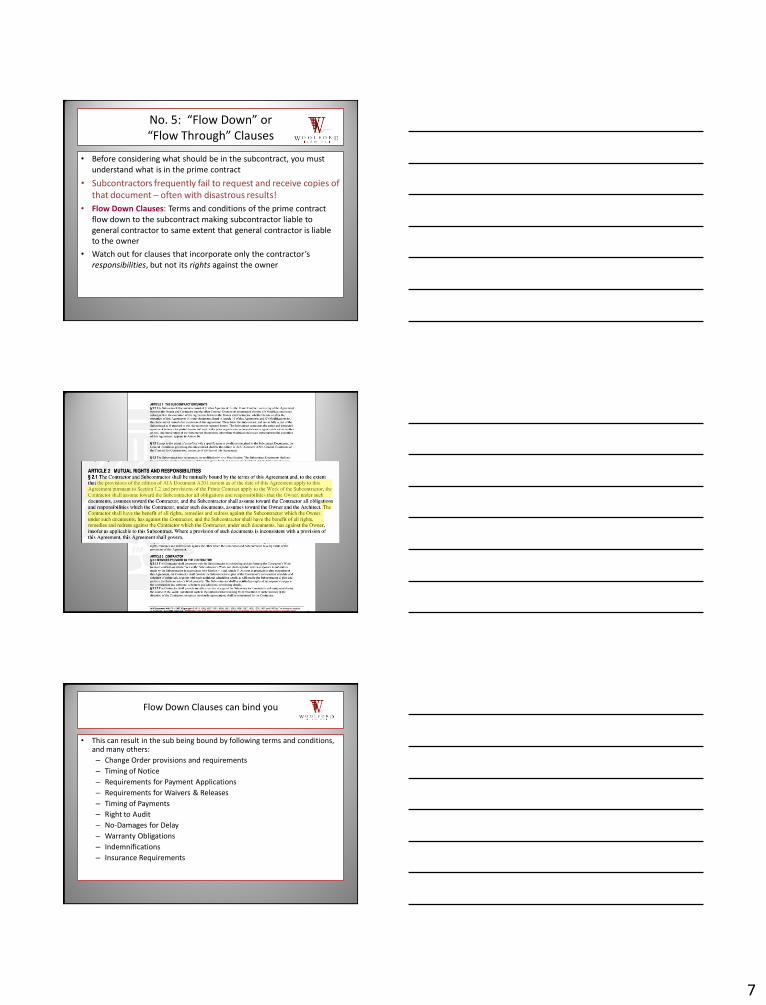

FLOW DOWN CLAUSE ALLOWS SUBS TO REQUEST FINANCIAL INFORMATION

• ARTICLE 2 MUTUAL RIGHTS AND RESPONSIBILITIES • The Contractor and Subcontractor shall be mutually bound by the terms of

this Agreement and, to the extent that the provisions of AIA Document A201–2007 apply to this Agreement pursuant to Section 1.2 and provisions of the Prime Contract apply to the Work of the Subcontractor, the Contractor shall assume toward the Subcontractor all obligations and responsibilities that the Owner, under such documents, assumes toward the Contractor, and the Subcontractor shall assume toward the Contractor all obligations and responsibilities which the Contractor, under such documents, assumes toward the Owner and the Architect. The Contractor shall have the benefit of all rights, remedies and redress against the Subcontractor that the Owner, under such documents, has against the Contractor, and the Subcontractor shall have the benefit of all rights, remedies and redress against the Contractor that the Contractor, under such documents, has against the Owner, insofar as applicable to this Subcontract. Where a provision of such documents is inconsistent with a provision of this Agreement, this Agreement shall govern.

6

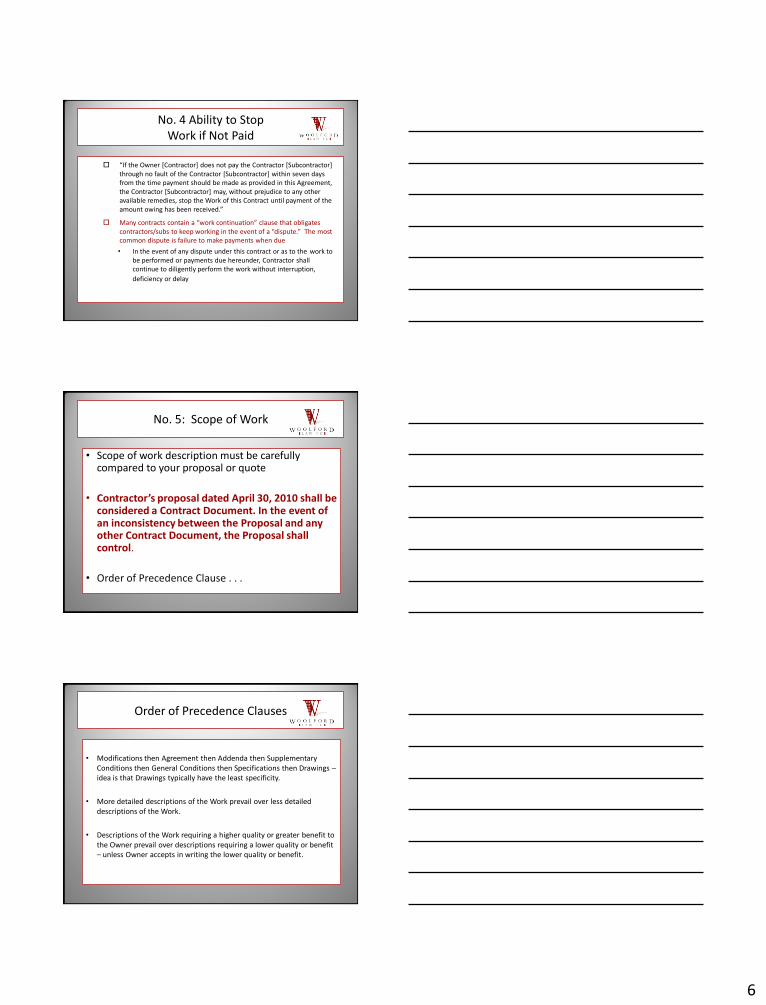

No. 4 Ability to Stop Work if Not Paid

“If the Owner *Contractor+ does not pay the Contractor *Subcontractor+ through no fault of the Contractor [Subcontractor] within seven days from the time payment should be made as provided in this Agreement, the Contractor [Subcontractor] may, without prejudice to any other available remedies, stop the Work of this Contract until payment of the amount owing has been received.”

Many contracts contain a “work continuation” clause that obligates contractors/subs to keep working in the event of a “dispute.” The most common dispute is failure to make payments when due

• In the event of any dispute under this contract or as to the work to be performed or payments due hereunder, Contractor shall

continue to diligently perform the work without interruption,

deficiency or delay

No. 5: Scope of Work

• Scope of work description must be carefully compared to your proposal or quote

• Contractor’s proposal dated April 30, 2010 shall be considered a Contract Document. In the event of an inconsistency between the Proposal and any other Contract Document, the Proposal shall control.

• Order of Precedence Clause . . .

Order of Precedence Clauses

• Modifications then Agreement then Addenda then Supplementary Conditions then General Conditions then Specifications then Drawings – idea is that Drawings typically have the least specificity.

• More detailed descriptions of the Work prevail over less detailed descriptions of the Work.

• Descriptions of the Work requiring a higher quality or greater benefit to the Owner prevail over descriptions requiring a lower quality or benefit – unless Owner accepts in writing the lower quality or benefit.

7

No. 5: “Flow Down” or “Flow Through” Clauses

• Before considering what should be in the subcontract, you must understand what is in the prime contract

• Subcontractors frequently fail to request and receive copies of that document – often with disastrous results!

• Flow Down Clauses: Terms and conditions of the prime contract flow down to the subcontract making subcontractor liable to general contractor to same extent that general contractor is liable to the owner

• Watch out for clauses that incorporate only the contractor’s responsibilities, but not its rights against the owner

Woolford Law

Flow Down Clauses can bind you

• This can result in the sub being bound by following terms and conditions,

and many others:

– Change Order provisions and requirements

– Timing of Notice

– Requirements for Payment Applications

– Requirements for Waivers & Releases

– Timing of Payments

– Right to Audit

– No-Damages for Delay

– Warranty Obligations

– Indemnifications

– Insurance Requirements

8

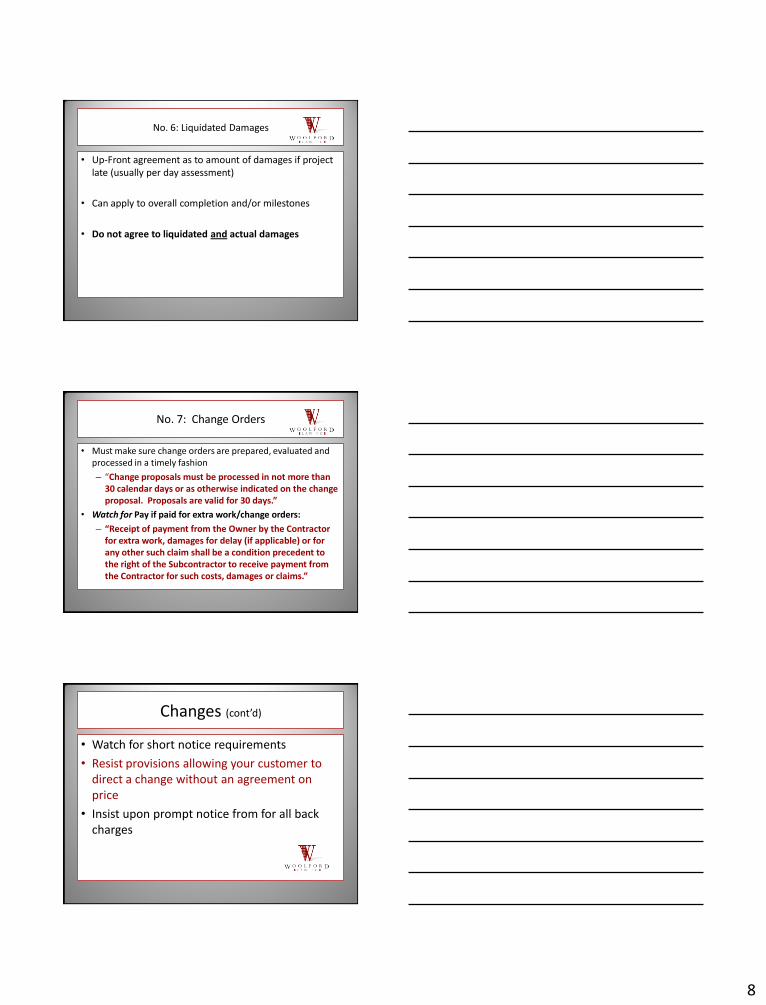

No. 6: Liquidated Damages

• Up-Front agreement as to amount of damages if project late (usually per day assessment)

• Can apply to overall completion and/or milestones

• Do not agree to liquidated and actual damages

No. 7: Change Orders

• Must make sure change orders are prepared, evaluated and processed in a timely fashion

– “Change proposals must be processed in not more than 30 calendar days or as otherwise indicated on the change proposal. Proposals are valid for 30 days.”

• Watch for Pay if paid for extra work/change orders:

– “Receipt of payment from the Owner by the Contractor for extra work, damages for delay (if applicable) or for any other such claim shall be a condition precedent to the right of the Subcontractor to receive payment from the Contractor for such costs, damages or claims.”

Changes (cont’d)

• Watch for short notice requirements

• Resist provisions allowing your customer to direct a change without an agreement on price

• Insist upon prompt notice from for all back charges

9

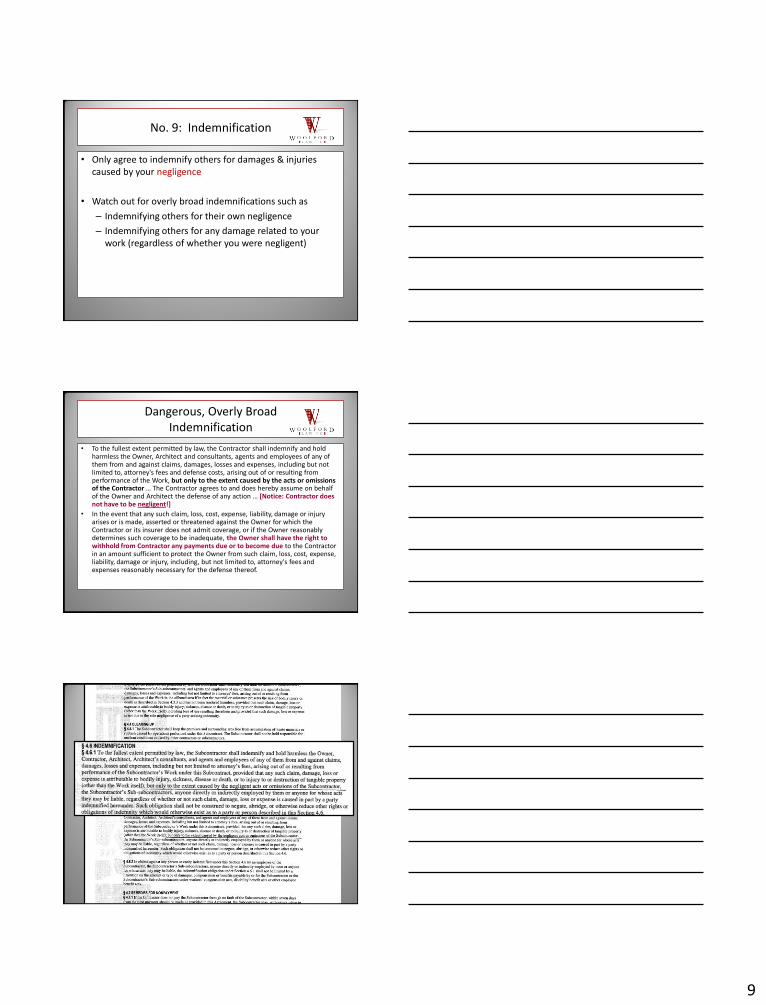

No. 9: Indemnification

• Only agree to indemnify others for damages & injuries caused by your negligence

• Watch out for overly broad indemnifications such as

– Indemnifying others for their own negligence

– Indemnifying others for any damage related to your work (regardless of whether you were negligent)

Dangerous, Overly Broad Indemnification

• To the fullest extent permitted by law, the Contractor shall indemnify and hold harmless the Owner, Architect and consultants, agents and employees of any of them from and against claims, damages, losses and expenses, including but not limited to, attorney's fees and defense costs, arising out of or resulting from performance of the Work, but only to the extent caused by the acts or omissions of the Contractor … The Contractor agrees to and does hereby assume on behalf of the Owner and Architect the defense of any action … [Notice: Contractor does not have to be negligent!]

• In the event that any such claim, loss, cost, expense, liability, damage or injury arises or is made, asserted or threatened against the Owner for which the Contractor or its insurer does not admit coverage, or if the Owner reasonably determines such coverage to be inadequate, the Owner shall have the right to withhold from Contractor any payments due or to become due to the Contractor in an amount sufficient to protect the Owner from such claim, loss, cost, expense, liability, damage or injury, including, but not limited to, attorney's fees and expenses reasonably necessary for the defense thereof.

Woolford Law

10

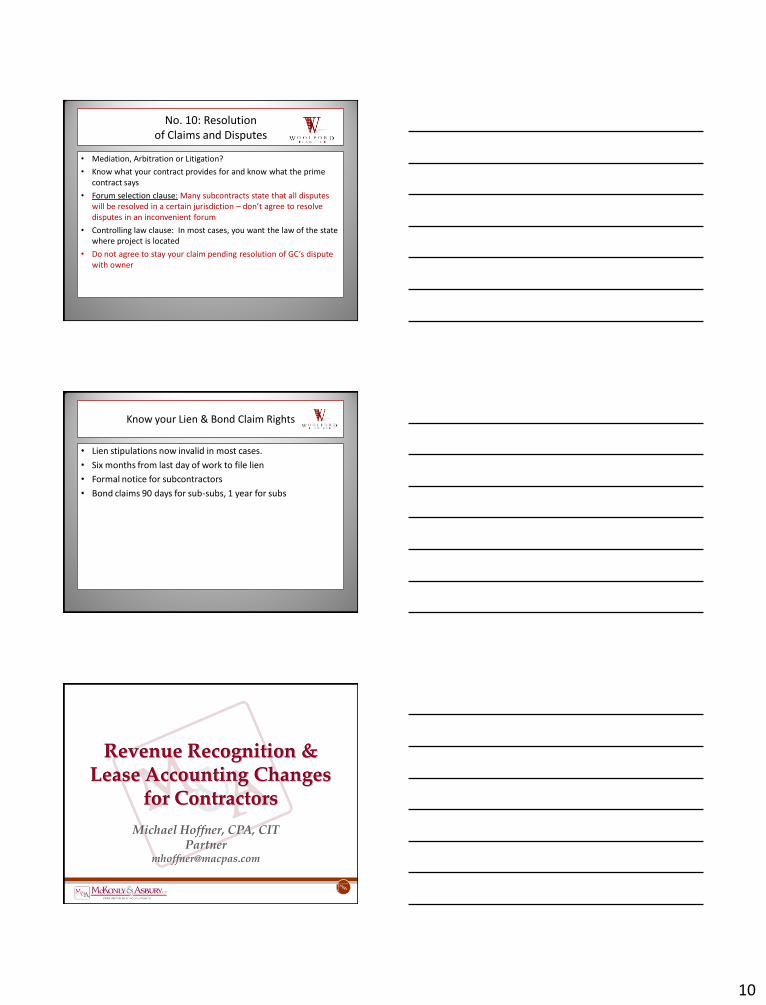

No. 10: Resolution of Claims and Disputes

• Mediation, Arbitration or Litigation?

• Know what your contract provides for and know what the prime contract says

• Forum selection clause: Many subcontracts state that all disputes will be resolved in a certain jurisdiction – don’t agree to resolve disputes in an inconvenient forum

• Controlling law clause: In most cases, you want the law of the state where project is located

• Do not agree to stay your claim pending resolution of GC’s dispute with owner

Know your Lien & Bond Claim Rights

• Lien stipulations now invalid in most cases.

• Six months from last day of work to file lien

• Formal notice for subcontractors

• Bond claims 90 days for sub-subs, 1 year for subs

Revenue Recognition & Lease Accounting Changes

for Contractors Michael Hoffner, CPA, CIT

Partner [email protected]

11

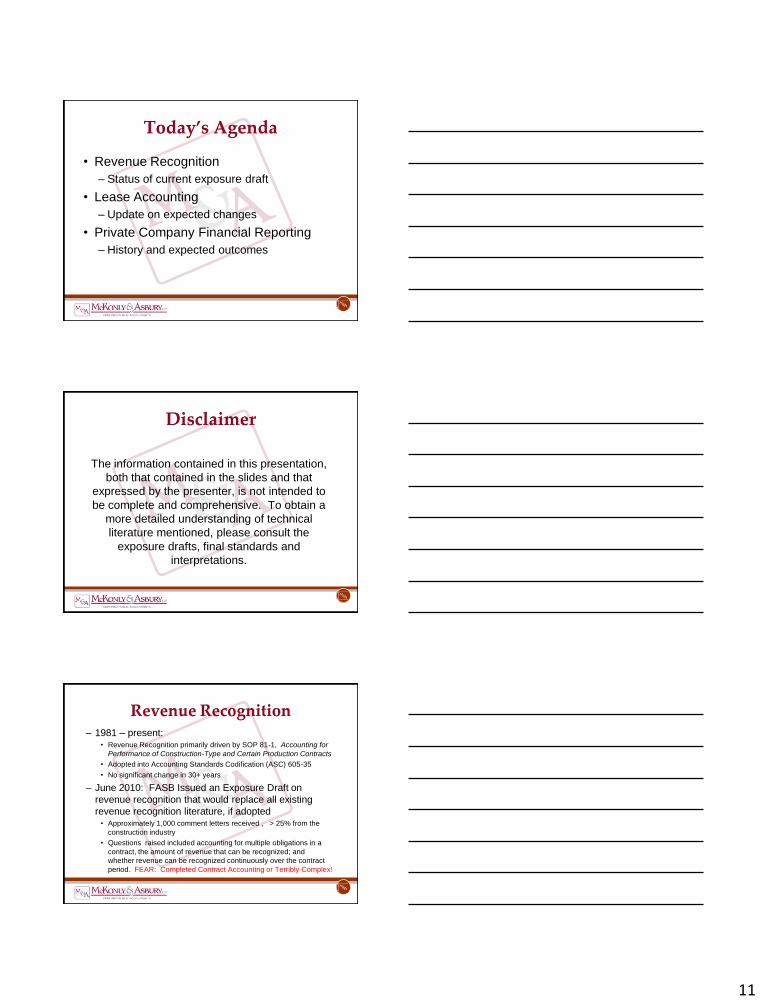

Today’s Agenda

• Revenue Recognition

– Status of current exposure draft

• Lease Accounting

– Update on expected changes

• Private Company Financial Reporting

– History and expected outcomes

Disclaimer

The information contained in this presentation,

both that contained in the slides and that

expressed by the presenter, is not intended to

be complete and comprehensive. To obtain a

more detailed understanding of technical

literature mentioned, please consult the

exposure drafts, final standards and

interpretations.

Revenue Recognition – 1981 – present:

• Revenue Recognition primarily driven by SOP 81-1, Accounting for

Performance of Construction-Type and Certain Production Contracts

• Adopted into Accounting Standards Codification (ASC) 605-35

• No significant change in 30+ years

– June 2010: FASB Issued an Exposure Draft on

revenue recognition that would replace all existing

revenue recognition literature, if adopted • Approximately 1,000 comment letters received , > 25% from the

construction industry

• Questions raised included accounting for multiple obligations in a

contract, the amount of revenue that can be recognized; and

whether revenue can be recognized continuously over the contract

period. FEAR: Completed Contract Accounting or Terribly Complex!

12

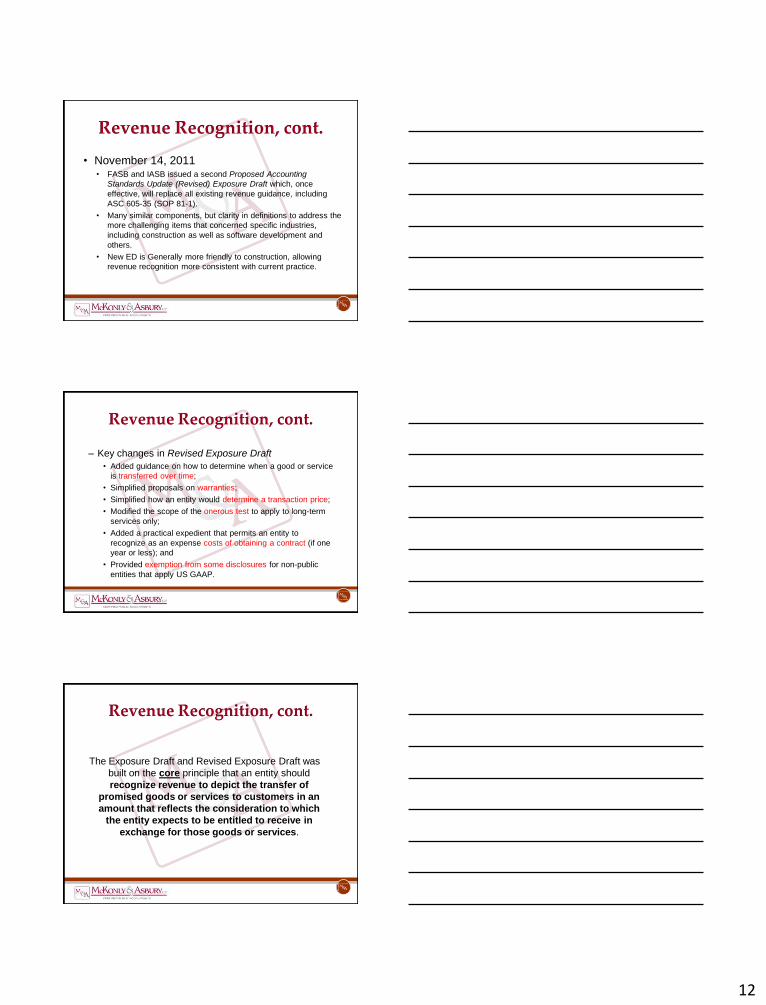

Revenue Recognition, cont.

• November 14, 2011 • FASB and IASB issued a second Proposed Accounting

Standards Update (Revised) Exposure Draft which, once

effective, will replace all existing revenue guidance, including

ASC 605-35 (SOP 81-1).

• Many similar components, but clarity in definitions to address the

more challenging items that concerned specific industries,

including construction as well as software development and

others.

• New ED is Generally more friendly to construction, allowing

revenue recognition more consistent with current practice.

Revenue Recognition, cont.

– Key changes in Revised Exposure Draft

• Added guidance on how to determine when a good or service

is transferred over time;

• Simplified proposals on warranties;

• Simplified how an entity would determine a transaction price;

• Modified the scope of the onerous test to apply to long-term

services only;

• Added a practical expedient that permits an entity to

recognize as an expense costs of obtaining a contract (if one

year or less); and

• Provided exemption from some disclosures for non-public

entities that apply US GAAP.

Revenue Recognition, cont.

The Exposure Draft and Revised Exposure Draft was

built on the core principle that an entity should

recognize revenue to depict the transfer of

promised goods or services to customers in an

amount that reflects the consideration to which

the entity expects to be entitled to receive in

exchange for those goods or services.

13

Revenue Recognition, cont.

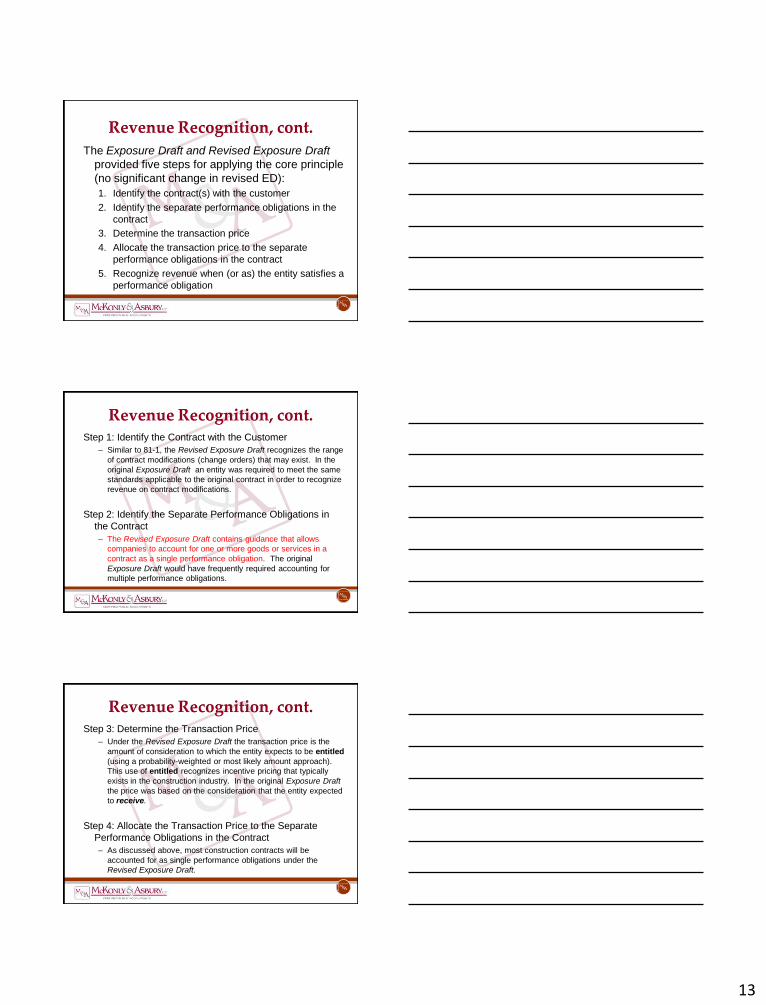

The Exposure Draft and Revised Exposure Draft

provided five steps for applying the core principle

(no significant change in revised ED):

1. Identify the contract(s) with the customer

2. Identify the separate performance obligations in the

contract

3. Determine the transaction price

4. Allocate the transaction price to the separate

performance obligations in the contract

5. Recognize revenue when (or as) the entity satisfies a

performance obligation

Revenue Recognition, cont. Step 1: Identify the Contract with the Customer

– Similar to 81-1, the Revised Exposure Draft recognizes the range

of contract modifications (change orders) that may exist. In the

original Exposure Draft an entity was required to meet the same

standards applicable to the original contract in order to recognize

revenue on contract modifications.

Step 2: Identify the Separate Performance Obligations in

the Contract

– The Revised Exposure Draft contains guidance that allows

companies to account for one or more goods or services in a

contract as a single performance obligation. The original

Exposure Draft would have frequently required accounting for

multiple performance obligations.

Revenue Recognition, cont. Step 3: Determine the Transaction Price

– Under the Revised Exposure Draft the transaction price is the

amount of consideration to which the entity expects to be entitled

(using a probability-weighted or most likely amount approach).

This use of entitled recognizes incentive pricing that typically

exists in the construction industry. In the original Exposure Draft

the price was based on the consideration that the entity expected

to receive.

Step 4: Allocate the Transaction Price to the Separate

Performance Obligations in the Contract

– As discussed above, most construction contracts will be

accounted for as single performance obligations under the

Revised Exposure Draft.

14

Revenue Recognition, cont. Step 5: Recognize revenue when (or as) the entity satisfies

a performance obligation

– Under the Revised ED an entity will recognize revenue by

measuring the progress toward complete satisfaction of that

performance obligation. In addition, the Revised ED requires that

an entity update its measure of progress to depict the

performance completed to date.

– Permitted to recognize revenue only to the extent to the

consideration that the entity is reasonably assured to be entitled.

– Revised ED provides considerable guidance on the use of input

and output methods in measuring progress towards completion.

Input methods (such as cost-to-cost) generally permissible,

particularly when output methods are difficult and costly to

measure.

Revenue Recognition, cont.

– Final standard expected in late 2012, with an

effective date of 2015 or later.

• Expected deferral of an additional year for

nonpublic entities

– FASB Project Updates and public comment

letters are available at www.fasb.org

Lease Accounting

Leases – Initial exposure draft August 2010 generated substantial

feedback on many key points (over 2,800 comment letters)

• General support for placing leases on balance sheet, but

concerns about complexities in calculations

• Concerns about Lessor-side accounting

– At their February 2012 meeting the FASB and IASB were

unable to agree on the proposed amortization method that

lessees would be required to apply to right-of-use assets after

initial recognition.

– FASB will likely issue a revised Exposure Draft in Q3 2012 at

the earliest.

– Standard will likely not be effective before 2016.

15

Lease Accounting

Leases

– Tentative changes include classifying leases as

either:

• Finance leases - includes a financing element,

similar to current capital lease treatment.

• Short-term leases – less than 12 months in length

(maximum possible term), do not need to recognize

lease assets or lease liabilities, recognize lease

payments in profit or loss on a straight-line (or other

systematic) basis over the lease term.

Lease Accounting

Leases – Other tentative changes related to Lease Term:

• Initial ED required inclusion of longest term that is more likely than

not to occur. Expected new ED will be non-cancelable term plus

any option period for which exercise is reasonably certain.

• Initial ED required consideration of lessee specific factors (history,

intentions, etc.) as well as economic factors in making

determination. New ED expected to include lease terms that

contain a “significant economic incentive to exercise”.

– Other tentative changes:

• Variable payments: Initial ED required projected rate or index, new

ED expected to require current rate or index.

• Lessor accounting issues expected to be addressed.

Lease Accounting

Leases: Lessee Accounting (Finance Leases)

– Balance Sheet Impact:

• A new asset is recorded representing the right to use the

leased item for the lease term.

• A liability is recorded representing the obligation to pay

rentals based on the present value of lease payments.

– Income Statement Impact:

• Straight-line rent expense would be replaced by

amortization and interest expense for lessees with current

operating lease treatment. This would result in acceleration

of expense recognition.

– More disclosures to be required for all leases.

16

Private Company Financial Reporting

• The Financial Accounting Foundation (FAF) trustees hope to vote

on a final structure and plan for private company financial reporting

at their meeting scheduled for May 22-23, 2012.

• FAF has proposed creating a Private Company Standards

Improvement Council (PCSIC) that would recommend deviations

from U.S. GAAP for private companies.

• The AICPA was disappointed with the proposal because the PCSIC

recommendations would be subject to FASB’s approval.

• The FASB is developing a decision-making framework that will

determine when differences in U.S. GAAP are appropriate for

private companies.

• FASB is working to develop a disclosure framework to identify which

information is most helpful to users of entities’ financial statements. Source: Journal of Accountancy, Private Company Reporting Decision Could Come in May, FASB Chairman Says

Questions?

Break

hosted by:

17

Individual Surety

Is This the Right Choice for You?

May 18, 2012

Lydia A. Mantle

Bond Account Executive

Murray Risk Management and Insurance

• Compare corporate surety and individual surety

• How to qualify/validate a bond

• State of the surety market

What is personal surety?

Also, known as individual surety and private surety

18

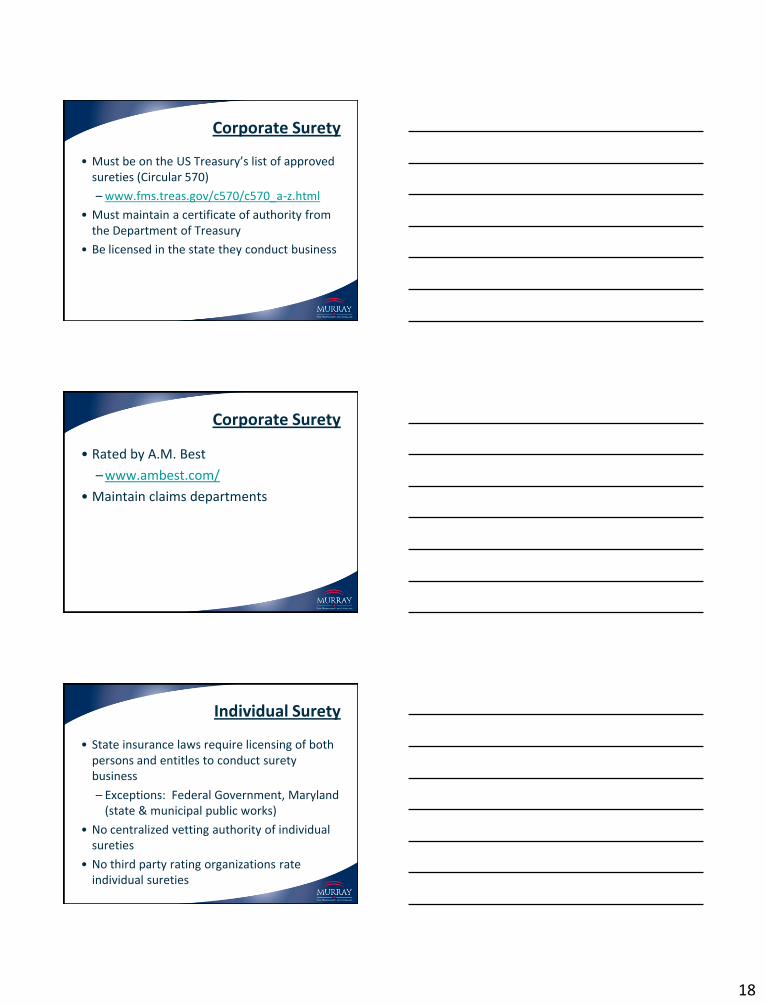

Corporate Surety

• Must be on the US Treasury’s list of approved sureties (Circular 570)

– www.fms.treas.gov/c570/c570_a-z.html

• Must maintain a certificate of authority from the Department of Treasury

• Be licensed in the state they conduct business

Corporate Surety

• Rated by A.M. Best

– www.ambest.com/

• Maintain claims departments

Individual Surety

• State insurance laws require licensing of both persons and entitles to conduct surety business

– Exceptions: Federal Government, Maryland (state & municipal public works)

• No centralized vetting authority of individual sureties

• No third party rating organizations rate individual sureties

19

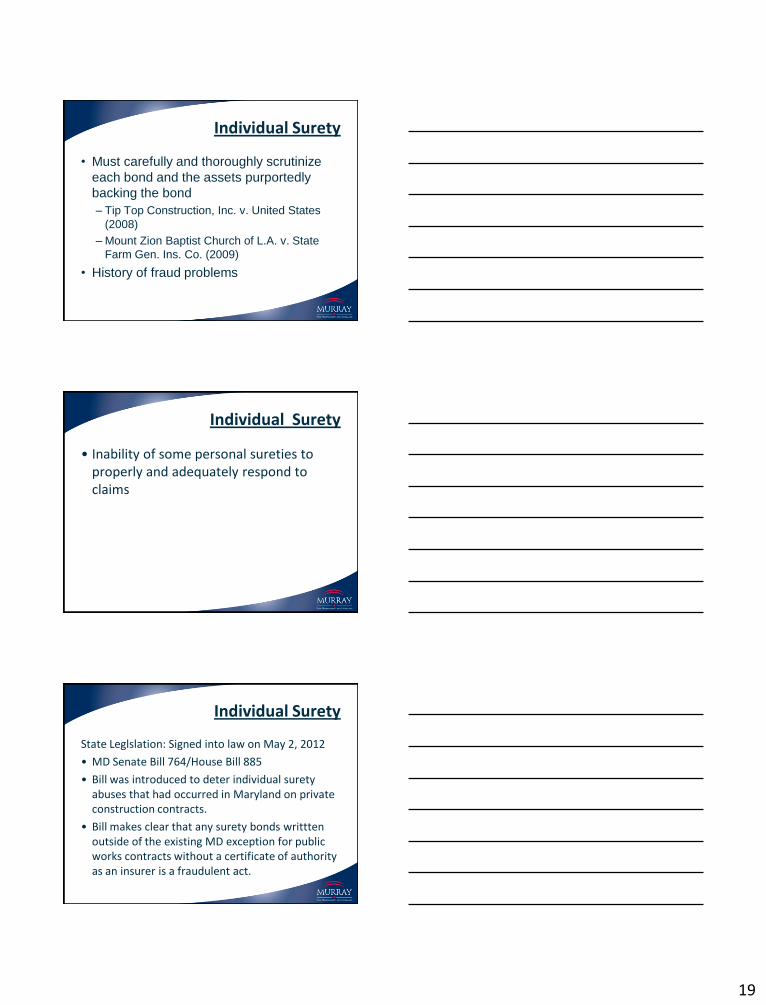

Individual Surety

• Must carefully and thoroughly scrutinize

each bond and the assets purportedly

backing the bond

– Tip Top Construction, Inc. v. United States

(2008)

– Mount Zion Baptist Church of L.A. v. State

Farm Gen. Ins. Co. (2009)

• History of fraud problems

Individual Surety

• Inability of some personal sureties to properly and adequately respond to claims

Individual Surety

State Leglslation: Signed into law on May 2, 2012

• MD Senate Bill 764/House Bill 885

• Bill was introduced to deter individual surety abuses that had occurred in Maryland on private construction contracts.

• Bill makes clear that any surety bonds writtten outside of the existing MD exception for public works contracts without a certificate of authority as an insurer is a fraudulent act.

20

Individual Surety

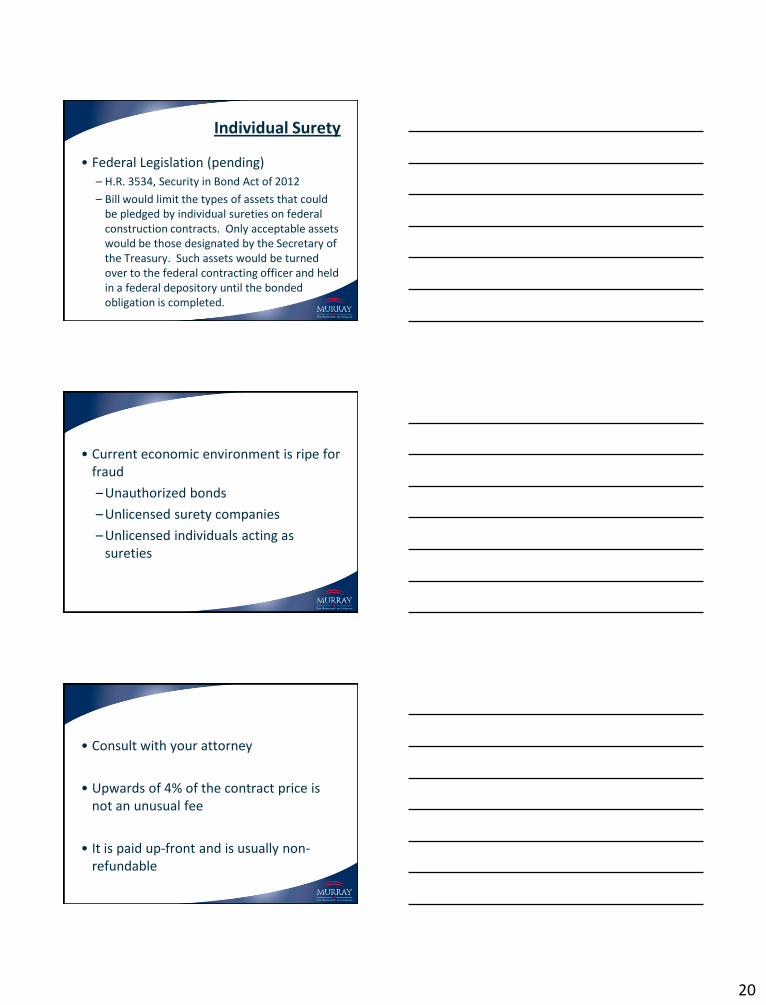

• Federal Legislation (pending) – H.R. 3534, Security in Bond Act of 2012

– Bill would limit the types of assets that could be pledged by individual sureties on federal construction contracts. Only acceptable assets would be those designated by the Secretary of the Treasury. Such assets would be turned over to the federal contracting officer and held in a federal depository until the bonded obligation is completed.

• Current economic environment is ripe for fraud

– Unauthorized bonds

– Unlicensed surety companies

– Unlicensed individuals acting as sureties

• Consult with your attorney

• Upwards of 4% of the contract price is not an unusual fee

• It is paid up-front and is usually non-refundable

21

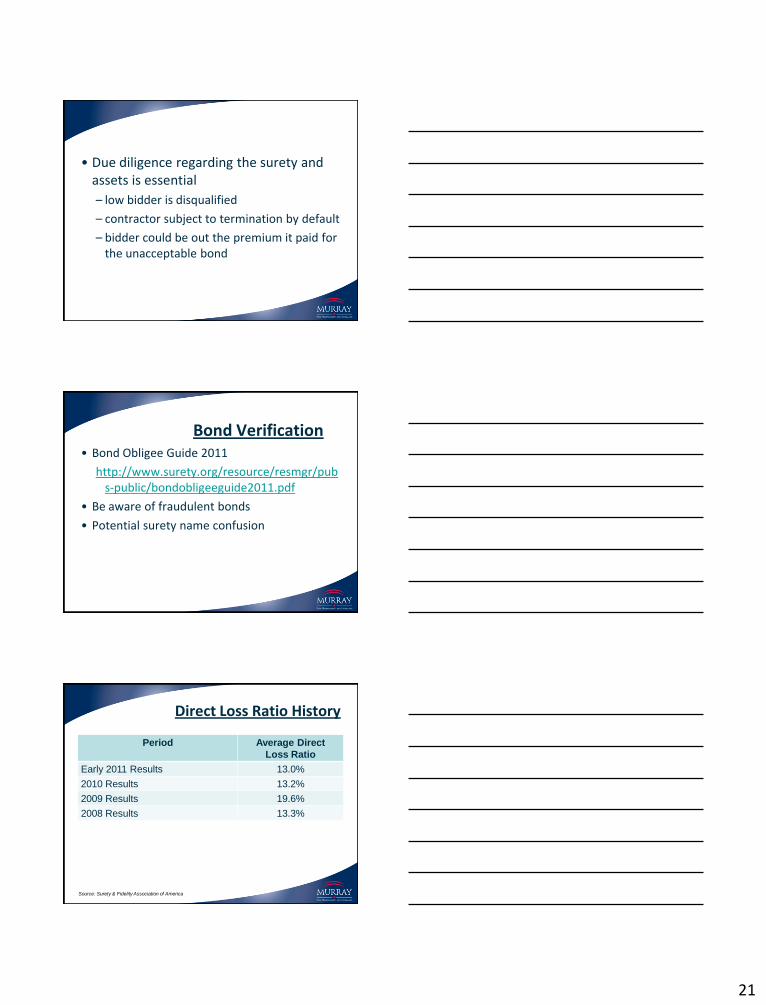

• Due diligence regarding the surety and assets is essential

– low bidder is disqualified

– contractor subject to termination by default

– bidder could be out the premium it paid for the unacceptable bond

Bond Verification

• Bond Obligee Guide 2011

http://www.surety.org/resource/resmgr/pubs-public/bondobligeeguide2011.pdf

• Be aware of fraudulent bonds

• Potential surety name confusion

Period Average Direct

Loss Ratio

Early 2011 Results 13.0%

2010 Results 13.2%

2009 Results 19.6%

2008 Results 13.3%

Direct Loss Ratio History

Source: Surety & Fidelity Association of America

22

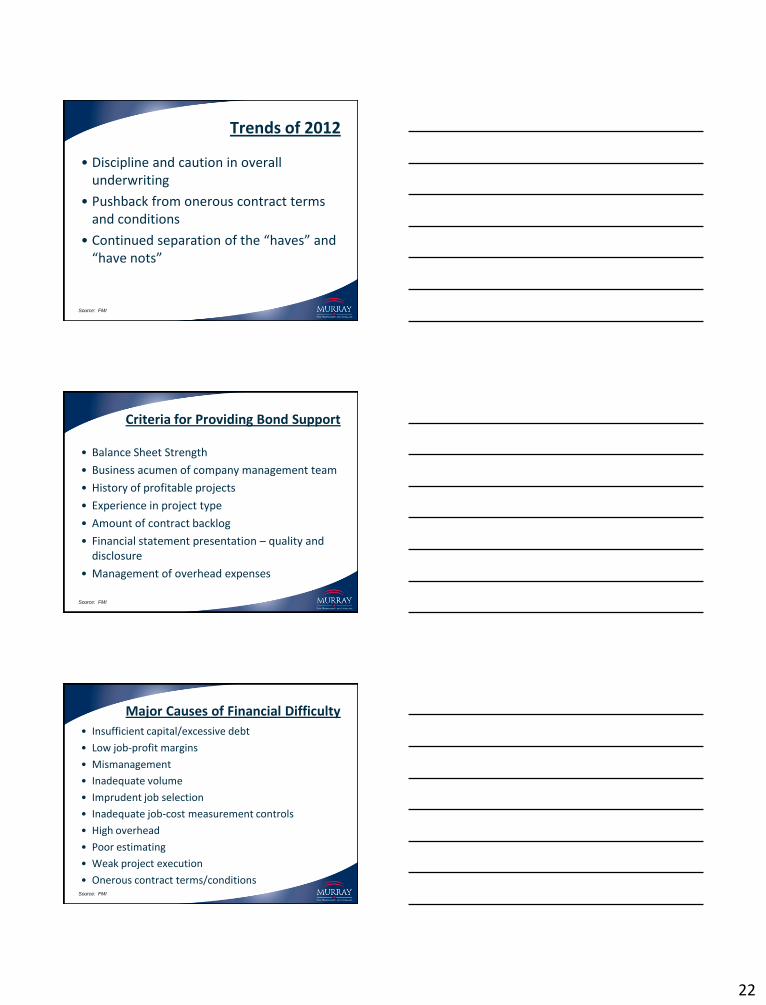

Trends of 2012

• Discipline and caution in overall underwriting

• Pushback from onerous contract terms and conditions

• Continued separation of the “haves” and “have nots”

Source: FMI

Criteria for Providing Bond Support

• Balance Sheet Strength

• Business acumen of company management team

• History of profitable projects

• Experience in project type

• Amount of contract backlog

• Financial statement presentation – quality and disclosure

• Management of overhead expenses

Source: FMI

Major Causes of Financial Difficulty

• Insufficient capital/excessive debt

• Low job-profit margins

• Mismanagement

• Inadequate volume

• Imprudent job selection

• Inadequate job-cost measurement controls

• High overhead

• Poor estimating

• Weak project execution

• Onerous contract terms/conditions

Source: FMI

23

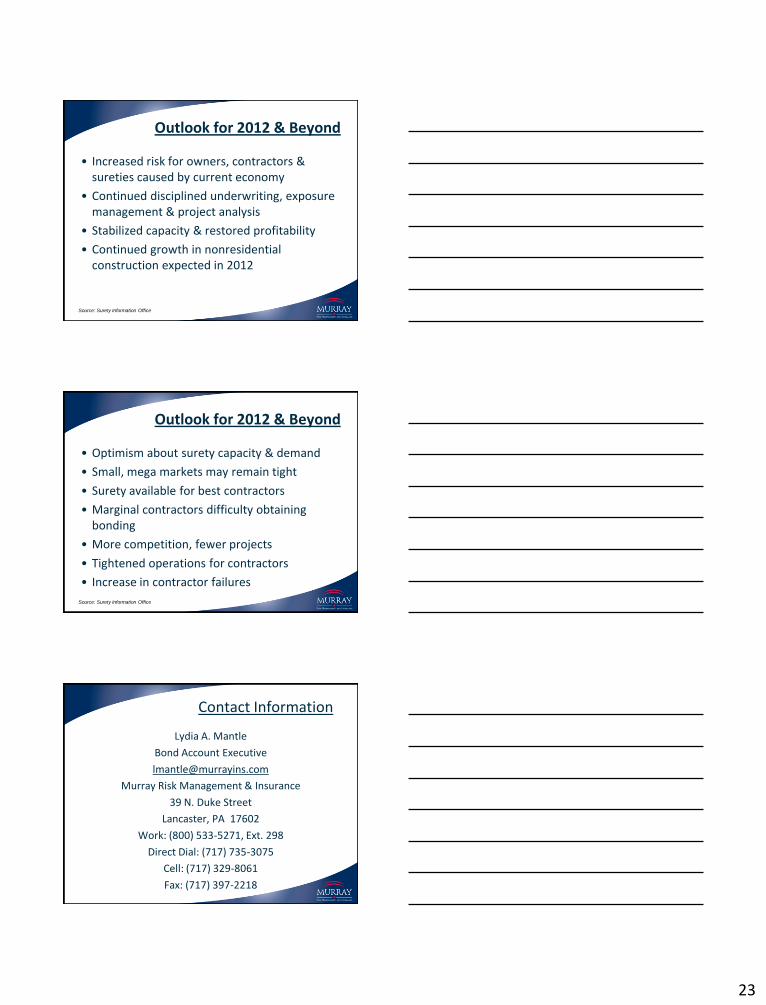

Outlook for 2012 & Beyond

• Increased risk for owners, contractors & sureties caused by current economy

• Continued disciplined underwriting, exposure management & project analysis

• Stabilized capacity & restored profitability

• Continued growth in nonresidential construction expected in 2012

Source: Surety Information Office

Outlook for 2012 & Beyond

• Optimism about surety capacity & demand

• Small, mega markets may remain tight

• Surety available for best contractors

• Marginal contractors difficulty obtaining bonding

• More competition, fewer projects

• Tightened operations for contractors

• Increase in contractor failures

Source: Surety Information Office

Contact Information

Lydia A. Mantle

Bond Account Executive

Murray Risk Management & Insurance

39 N. Duke Street

Lancaster, PA 17602

Work: (800) 533-5271, Ext. 298

Direct Dial: (717) 735-3075

Cell: (717) 329-8061

Fax: (717) 397-2218

24

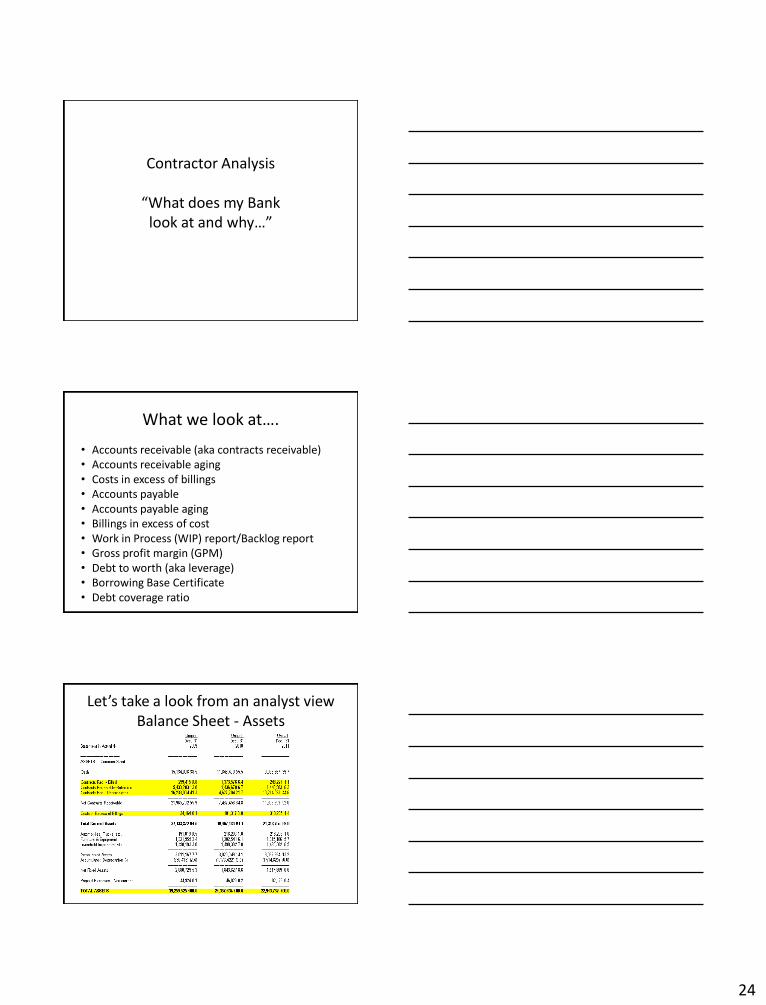

Contractor Analysis

“What does my Bank look at and why…”

What we look at….

• Accounts receivable (aka contracts receivable) • Accounts receivable aging • Costs in excess of billings • Accounts payable • Accounts payable aging • Billings in excess of cost • Work in Process (WIP) report/Backlog report • Gross profit margin (GPM) • Debt to worth (aka leverage) • Borrowing Base Certificate • Debt coverage ratio

Let’s take a look from an analyst view Balance Sheet - Assets

25

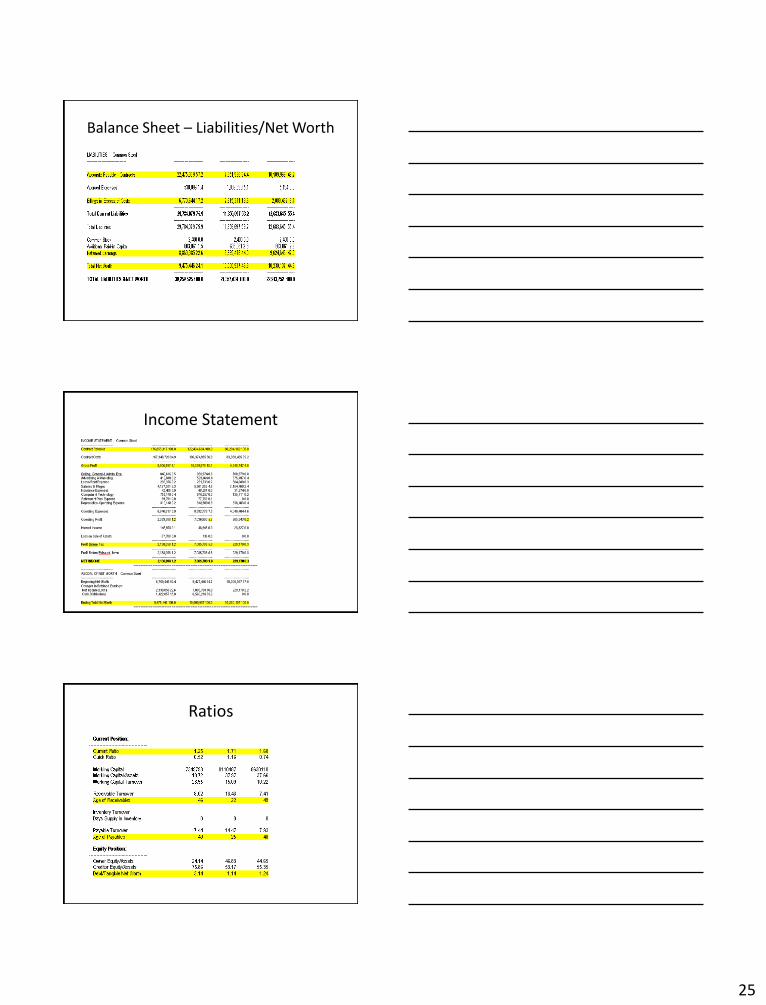

Balance Sheet – Liabilities/Net Worth

Income Statement

Ratios

26

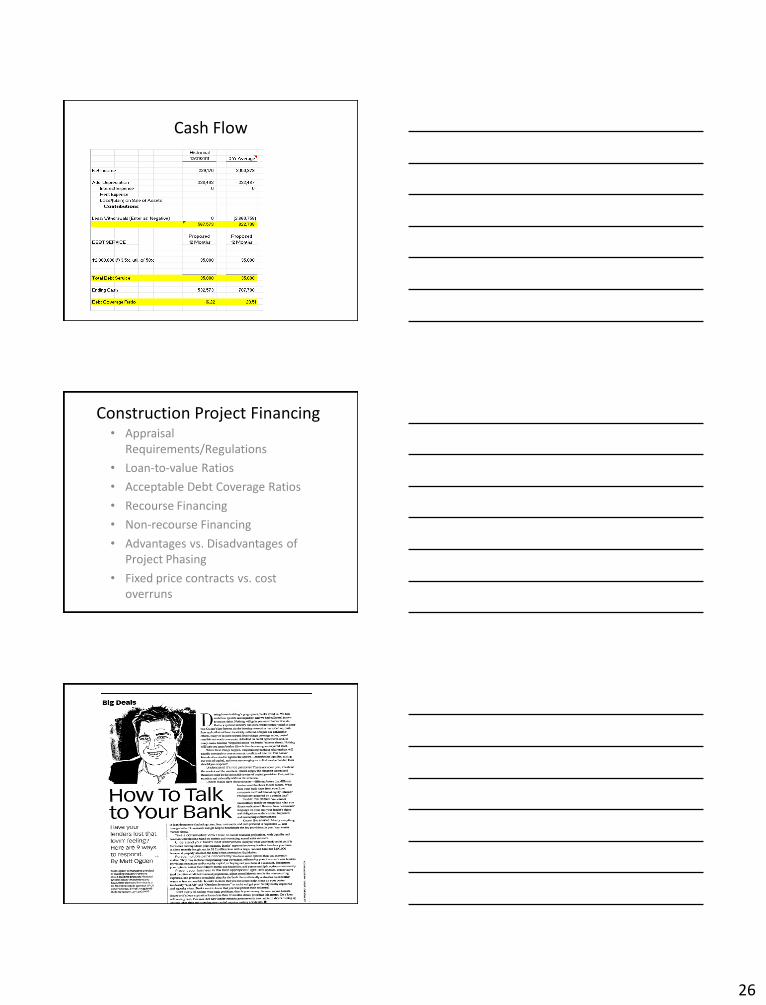

Cash Flow

Construction Project Financing • Appraisal

Requirements/Regulations

• Loan-to-value Ratios

• Acceptable Debt Coverage Ratios

• Recourse Financing

• Non-recourse Financing

• Advantages vs. Disadvantages of Project Phasing

• Fixed price contracts vs. cost overruns

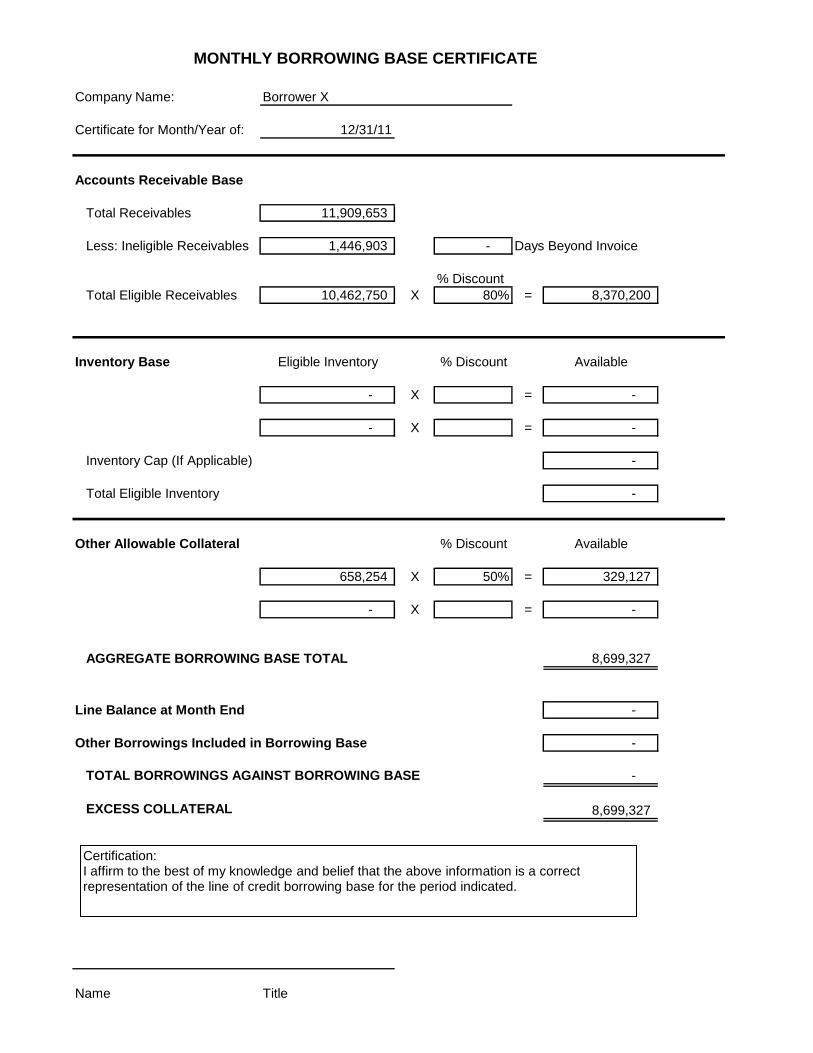

Company Name: Borrower X

Certificate for Month/Year of: 12/31/11

Accounts Receivable Base

Total Receivables 11,909,653

Less: Ineligible Receivables 1,446,903 - Days Beyond Invoice

% Discount

Total Eligible Receivables 10,462,750 X 80% = 8,370,200

Inventory Base Eligible Inventory % Discount Available

- X = -

- X = -

Inventory Cap (If Applicable) -

Total Eligible Inventory -

Other Allowable Collateral % Discount Available

658,254 X 50% = 329,127

- X = -

AGGREGATE BORROWING BASE TOTAL 8,699,327

Line Balance at Month End -

Other Borrowings Included in Borrowing Base -

TOTAL BORROWINGS AGAINST BORROWING BASE -

EXCESS COLLATERAL 8,699,327

Name Title

MONTHLY BORROWING BASE CERTIFICATE

Certification: I affirm to the best of my knowledge and belief that the above information is a correct representation of the line of credit borrowing base for the period indicated.

Glossary

Accounts receivable (aka contracts receivable) is money owed to your business by customers. Accounts

receivable aging is a report that lists open receivables, with details including customer name, length

open and total amount

• A/R and A/R agings – bulk of your company’s assets will more than likely be in A/R. They should be in line with sales trends (typically.) A/R aging will verify prompt collection of receivables, should breakout bonded receivables as well as retainage. The Bank cannot take bonded or retainage as collateral.

Costs in excess of billings represents cost of work that has not been billed.

• Costs in excess of billings –. if trend shows large costs in excess, or not in line with sales movement, your business may not be billing customers on a timely basis.

Accounts payable is money your business owes other vendors. Accounts payable aging is a report that

lists open payables, with details including customer name, length open and total amount.

• A/P and A/P aging - should be in line with sales trends typically and verify prompt payment of payables.

Billings in excess of cost is money received for work that has not been completed.

• Billings in excess of cost – because this is money you have received before spending on a specific project, be sure to have offsetting cash on hand, otherwise a cash shortage may occur causing a need to borrow funds.

Work in Process (WIP) report/Backlog report is a report that lists open/pending jobs, to include (but

not limited to)name of the job, estimated revenue and costs, estimated gross profit margin, and

estimated net profit.

• WIP/Backlog report – how has it changed year over, shrinkage/improvement, job profitability (correctly estimating projects), bidding for work in your skillset, ability to meet project needs. In addition, win rate on bidding jobs and type of work (negotiated versus hard bid)are beneficial for the Bank to know.

Gross profit margin (GPM) is revenues less the variable and fixed costs directly related to the sale (i.e.

materials, labor, shipping.)

• Gross profit margin – ratio that shows if your business is estimating and managing jobs properly. Downward trend (or shrinkage in the %) is not a good sign….larger margins allow for room to under bid if necessary on a rare case.

Debt to worth (aka leverage) is total debt divided by the net worth of your business.

• Debt to worth – we look for lower leverage, as it indicates less debt, retainage of profits, and the higher probability that your business will be able to weather a down turn.

Borrowing Base Certificate is a valuation method of your liquid assets (i.e. inventory, A/R) to the line of

credit usage.

• Borrowing base certificate – allows the financial institution to properly secure the line of credit as well as monitor the proper usage of the line, as it is tied directly to the working assets.

Debt coverage ratio is a ratio of cash available for debt service including interest, principal and lease

payments.

• Debt coverage ratio – 1.20:1 is our targeted benchmark. This indicates that for every dollar of debt, the company has $1.20 worth of cash flow.

![S 1 inO N /HS duality arXiv:1205.4117v1 [hep-th] 18 May 2012 · arXiv:1205.4117v1 [hep-th] 18 May 2012 BROWN-HET-1629 WITS-CTP-096 S=1 inO(N)/HS duality Robert de Mello Kocha, Antal](https://img.pdfslide.us/doc/110x75/5fc629159d1fb87b7c7629c7/s-1-ino-n-hs-duality-arxiv12054117v1-hep-th-18-may-2012-arxiv12054117v1-hep-th.jpg)