Embed Size (px)

Citation preview

S P O N S O R E D B Y

2012 CP CHANGES (APPROVED FOR USE 2013)

- PART 2

10/28/2013

1

2012 ISO CP Changes – Part 2Endorsements – changes and new

offeringswith

Irene Morrill, CPCU, CIC, ARM, CRM, LIA, CRIS, CPIWVice President of Technical Affairs

Massachusetts Association of Insurance Agents

This program is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

With special thanks to the Insurance Services Office, Inc. for advance information, continued support, and permission to use their forms and information.

1

Coverage form optionsCP 04 04 Specified Property Away from PremisesCP 04 08 Higher LimitsCP 04 11 Protective Safeguards

Cause of loss options CP 10 46 Equipment BreakdownCP 10 38 Discharge from Sewer, Drain or SumpCP 10 44 Theft of Building Materials and Supplies (Other Than Builders Risk) CP 10 34 Exclusion of Loss due to By-Products of Production or Processing Operation

2

contents

10/28/2013

2

Endorsement affecting loss settlementCP 14 70 Deductibles by Location

CP 04 09 Increase in Rebuilding Expenses Following Disaster

CP 10 36 Limitations on Coverage for Roof Surfacing

Business Income endorsementsCP 15 05 Food Contamination (BI and EE)CP 15 45 Utility Services – Wastewater Removal (Time Element)

3

contents

Your client has off premises operations where

expensive computer and diagnostic equipment

are utilized. The value off premises possession

of an employee could be upwards of $20,000.

4

Coverage Form Options – Specified property away from Premises

10/28/2013

3

1) While driving to a location the employee had an auto accident. This equipment was “totaled” as well as the auto the employee was driving.

2) The employee brought this equipment into the hotel room where staying while working at a client’s business location. The equipment was stolen from the hotel room.

5

Coverage Form Options – Specified property away from Premises

Prior editions … a problem

The full BPP limit only applies 100 ft from premises

6

Coverage Form Options – Specified property away from Premises

10/28/2013

4

There is a limit for BPP off premises but only

$10,000.

Loss in vehicle NOT covered7

Coverage Form Options – Specified property away from Premises

CP 2012 new endorsement CP 04 04

8

Coverage Form Options – Specified property away from Premises

10/28/2013

5

Temporarily off

premises

Certain types of

BPP NOT apply

to

9

Coverage Form Options – Specified property away from Premises

If other parts of

policy apply –

not duplicate

coverage

10

Coverage Form Options – Specified property away from Premises

10/28/2013

6

Do you use “additional coverages” or coverage extensions as

SALES TOOLS….sometimes for endorsements

sometimes for other policies

sometimes …just higher limits – more of what they already have

11

Coverage Form Options – Higher limit options

CP 2012 new

endorsement

CP 04 08

CLM CP section

Rule 27

Describes when

Can be used

12

Coverage Form Options – Higher limit options

10/28/2013

7

27. HIGHER LIMITS ENDORSEMENT

1. Fire Department Service Charge

2. Electronic Data

3. Interruption In Computer Operations

4. Valuable Papers And Records - Other Than Electronic Data

5. Non-owned Trailers

13

Coverage Form Options – Higher limit options

6. Builders Risk - Building Materials And Supplies Of Others

7. Newly Acquired Locations - Time ElementFor a limit in excess of $100,000 at each location

8. Special Causes Of Loss Theft LimitationsDifferent sub-limits apply to different types of property.

9. Business Personal Property Temporarily In Portable Storage Units 14

Coverage Form Options – Higher limit options

10/28/2013

8

Can endorsements …create problems?

Can endorsements create warrantees?

ABSOLUTELY ….

Protective safeguards …not what the company does for the client but what the client does for the company

15

Coverage Form Options – Protective safeguards CP 04 11

Good news …get credit – inherent in published rate

Bad news …those “safeguards” must ALWAYS be up and running

16

Coverage Form Options – Protective safeguards CP 04 11

10/28/2013

9

The endorsement mentions the following:

17

Coverage Form Options – Protective safeguards CP 04 11

One is REQUIRED to maintain the safeguard

18

Coverage Form Options – Protective safeguards CP 04 11

10/28/2013

10

The endorsement requires company identify building and safeguard

19

Coverage Form Options – Protective safeguards CP 04 11

The BACK of the endorsement is where the “gotcha” is ..

An EXCLUSION is added to the policy

20

Coverage Form Options – Protective safeguards CP 04 11

10/28/2013

11

MUST notify carrier of suspension or impairment of listed protective safeguard –or exclusion applies

21

Coverage Form Options – Protective safeguards CP 04 11

Exclusion applies if fail to MAINTAIN protective safeguard in good working order

22

Coverage Form Options – Protective safeguards CP 04 11

10/28/2013

12

A fan blade within a central air-conditioning unit breaks off and damage other components of the air-conditioning unit, causing it to stop working.

Is this covered under Special Form Cause of Loss

23

Cause of loss Options –

The heating boiler explodes and causes damage to the insured's business inventory and the building. This is a CPP … with business income.

Will damage to the building/contents/boiler and resulting BII be covered under Special Form Cause of Loss?

24

Cause of loss Options –

10/28/2013

13

Special form …any addition not cover either losses

25

Cause of loss Options –

Special form also excludes

26

Cause of loss Options –

10/28/2013

14

CPP …special form …is NOT special enough

Power surge, electric arcing, mechanical breakdown including any resulting damage are NOT covered …

We “think” equipment breakdown coverage formerly called “boiler and machinery”.

Now ISO offers an “endorsement”

27

Cause of loss Options – Equipment Breakdown CP 10 46

Can’t be used with Basic or Broad Cause of Loss form – only “special” cause of loss

Makes “equipment breakdown” a cause of loss - deletes or revises exclusions in special form that would preclude coverage for loss by an equipment breakdown event

28

Cause of loss Options – Equipment Breakdown CP 10 46

10/28/2013

15

Exclusions “revised” or deleted:

The exclusion of loss due to artificially generated electrical and magnetic energy (exclusion B.2.a) does not apply, except that loss or damage from a high altitude release of electromagnetic energy is not covered.

The exclusion of loss due to mechanical breakdown (exclusion b.2.d.(6)) does not apply.

The exclusion of loss due to explosion of steam boilers and other steam equipment (exclusion b.2.e) does not apply.

29

Cause of loss Options – Equipment Breakdown CP 10 46

Exclusions “revised” or deleted:

The exclusion of loss due to wear and tear (exclusion 2.d.(1)) is replaced with one that grants coverage for loss or damage from a resulting breakdown.

The exclusion of loss due to rust or other corrosion, decay, deterioration, hidden or latent defect, or any quality in property that caused it to damage or destroy itself is replaced with one that grants coverage for loss or damage from a resulting breakdown.

30

Cause of loss Options – Equipment Breakdown CP 10 46

10/28/2013

16

Exclusions “revised” or deleted:

The limitation that excludes loss to steam boilers and other steam equipment resulting from a condition or event inside the equipment does not apply.

The limitation that excludes loss to hot water boilers and other water heating equipment resulting from a condition or event inside the equipment does not apply.

31

Cause of loss Options – Equipment Breakdown CP 10 46

One exclusion is added:

there is no coverage for loss or damage to covered equipment undergoing a pressure or electrical test. However, loss or damage from a resulting fire or explosion is covered.

Equipment breakdown policies …generally restrict and/or allow endorsement for testing

32

Cause of loss Options – Equipment Breakdown CP 10 46

10/28/2013

17

Definition of covered equipment:

Equipment built to operate under internal pressure of vacuum other than weight of contents

Electrical or mechanical equipment that is used in the generation, transmission, or utilization of energy

Communication equipment

Computer equipment

33

Cause of loss Options – Equipment Breakdown CP 10 46

3 page endorsement

Is it as broad as the ISO Equipment breakdown policy …no

Is it as good as company specific equipment breakdown policies …probably not

Is it better than …nothing…. ABSOLUTELY 34

Cause of loss Options – Equipment Breakdown CP 10 46

10/28/2013

18

Your client has a special form policy. Very rainy week and sumps can’t keep up with extent of water in the ground. Sump overflows and causes damage to stock in basement.

OrCity sewer backs up causing damage to store bathrooms.

35

Cause of loss Options –

Sump overflow

Sewer back up

NOT covered

36

Cause of loss Options –

10/28/2013

19

New offeringAdds coverage for direct damage loss, business income and extra expense loss,or both, for loss to covered property caused by discharge or water or waterborne material from a sewer, drain (including a roof drain and related fixtures), or sump located on the described premises, "provided that such discharge is not caused by flood or flood-related conditions

37

Cause of loss Options – Discharge from Sewer, Drain, Sump CP 10 38

Buy a limit for direct physical damage andBII

38

Cause of loss Options – Discharge from Sewer, Drain, Sump CP 10 38

10/28/2013

20

39

Cause of loss Options – Discharge from Sewer, Drain, Sump CP 10 38

No coverage if NOT keep sump maintained

40

Cause of loss Options – Discharge from Sewer, Drain, Sump CP 10 38

Not pay to repair system - just resulting water loss and BII

10/28/2013

21

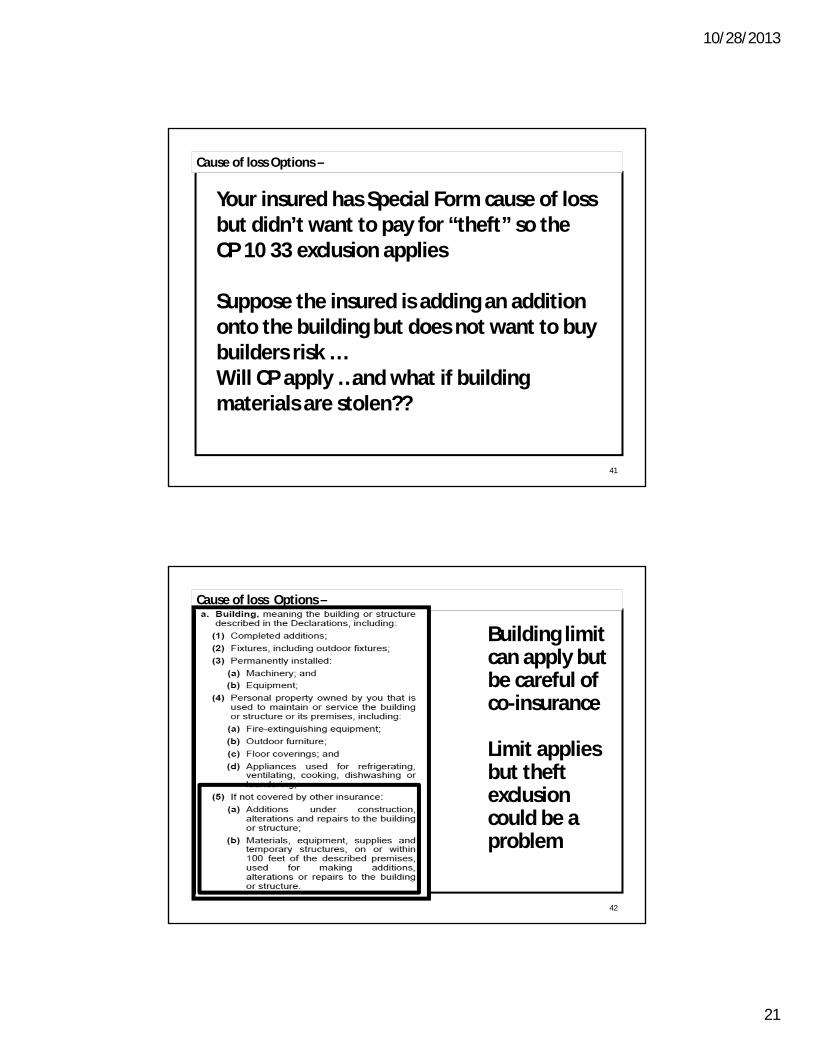

Your insured has Special Form cause of loss but didn’t want to pay for “theft” so the CP 10 33 exclusion applies

Suppose the insured is adding an addition onto the building but does not want to buy builders risk …Will CP apply …and what if building materials are stolen??

41

Cause of loss Options –

Building limit can apply but be careful of co-insurance

Limit applies but theft exclusion could be a problem

42

Cause of loss Options –

10/28/2013

22

Perhaps theft exclusion should be removed during building process

43

Cause of loss Options –

NOT apply to builders risk policy

44

Cause of loss Options – Theft of building materials and supplies (other than builders risk) CP 10 44

10/28/2013

23

Or …under CP 2012 – can add endorsement for this particular theft exposure

Show specified limit

45

Cause of loss Options – Theft of building materials and supplies (other than builders risk) CP 10 44

Your insured owns a strip mall and rents area to various business. One business just closed after a 10 year lease. They business was a take-out seafood restaurant offering the best fried claims, onion rings and french fries in the town.

The grease from the fried food operation damaged the ceilings and walls in the kitchen area. Is this covered under the landlord’s special form policy?

46

Cause of loss Options –

10/28/2013

24

Another of your insured’s owns a small commercial building that was rented out to a consignment store. One night the building blew up. It appears this “consignment store” was a meth lab in disguise and something went “awry”.

Is this covered under the special form policy?

47

Cause of loss Options –

These are true claims. The company in both situations invoked the “pollution” exclusion. Did it hold?

Special form covers EVERYTHING that isn’t excluded

48

Cause of loss Options –

10/28/2013

25

Graff v. Allstate Insurance Company, 113 Wash. App. 799; 54 P.3d 1266 (Wash, Ct. App. 2002), Insured filed a claim for cleanup expenses after a tenant's methamphetamine laboratory damaged his rental house. The insurer denied the claim, citing the policy's contamination exclusion.

The insured sued for breach of contract, and the trial court held in favor of the insured, finding that his insurance policy covered the cleanup expenses. 49

Cause of loss Options –

The appellate court affirmed the trial court and stated that operation of a methamphetamine laboratory is vandalism, a covered event under the policy at issue. This decision runs counter to the general understanding of what constitutes vandalism, regardless of the nature of the premises or operations at issue

50

Cause of loss Options –

10/28/2013

26

51

Cause of loss Options –

52

Cause of loss Options –

The loss by grease … well …pollution exclusion can work …

ISO has created an endorsement to make it EASIER to deny claims.

Regarding grease or damage by LEGAL business …this should be a contractual issue and expense …not insurance maintenance

10/28/2013

27

53

Cause of loss Options – CP 10 34 Exclusion of Loss due to By-Products of Production

To be added to owners and tenants of rental property

ISO states NOchange in “intended” coverage

54

Cause of loss Options – CP 10 34 Exclusion of Loss due to By-Products of Production

Reinforces no coverage for damage to rented premises due to operations of tenant … legal or not

10/28/2013

28

55

Cause of loss Options – CP 10 34 Exclusion of Loss due to By-Products of Production

Landlord needs to recoup coverage through contractual arrangement or court

56

Cause of loss Options – CP 10 34 Exclusion of Loss due to By-Products of Production

P.S. .. Don’t even TRY the vandalism route!

10/28/2013

29

57

Loss Settlement option- deductibles

Deductibles … when a CPP covers multiple locations … and one wants different deductibles for different locations …what to do?

58

Loss Settlement option- deductibles

The CP 00 10 – any edition – talks about THE deductible …

If want various deductibles …the only current option is … CP 03 20 Multiple Deductible Form

10/28/2013

30

59

If multiple building locations damaged by same occurrence then only the highest deductible will be taken

Loss Settlement option- deductibles

60

Loss Settlement option- deductibles by location CP 03 29

Show separate locations and deductibles for each location

10/28/2013

31

61

Loss Settlement option- deductibles by location CP 03 29

deductible amountcould be the same for each location, or different amounts could be selected

62

Loss Settlement option- deductibles by location CP 03 29

A location could be described in terms of aparticular site (on a risk with multiple sites) ora particular building (on a riskwith multiple buildings, or a risk with multiple buildings at multiple sites),maximum flexibility

10/28/2013

32

63

Loss Settlement option – replacement cost

When roof is damaged by hail or windstorm …how often does the insured want the WHOLE roof …reroofed …

And the carrier JUST wants to repair that portion that was damaged …

Insured worries about “aesthetics” … and devaluation …And …argues … “replacement value”

64

Loss Settlement option- Limitations on coverage for Roof Surfacing CP 10 36

Paragraph “A”Policy can provide replacement cost on all other parts of the building but roof losses can be subject to ACV

10/28/2013

33

65

Loss Settlement option- Limitations on coverage for Roof Surfacing CP 10 36

Two different options availableParagraph “A”Paragraph “B”

Can make either or both limitations apply to the roof

66

Loss Settlement option- Limitations on coverage for Roof Surfacing CP 10 36

Paragraph “B”Roof losses are NOT covered for cosmetic damageDue to wind/hail

Means “marring, pitting or other superficial damage

10/28/2013

34

67

Loss Settlement option-Increase in rebuilding expenses following disaster

Good ole’ American GREED …

Which economists call

Supply and demand

After Katrina …housing costs quadrupled in first 6 months after disaster

68

Loss Settlement option-Increase in rebuilding expenses following disaster

Widespread disaster … increases demand for labor and materials which then increases cost of rebuilding

HO policy utilizes the Specified Additional Limit endorsement – giving specified % increase for Dwelling value if necessary at loss

Or Additional limits of liability – which gives you what you need …

10/28/2013

35

69

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

New commercial offering – allows % increases after widespread disaster loss

70

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Get add’l limit shown if ALL Conditions met

10/28/2013

36

71

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Federal or state disaster declaration

Covered loss due to this disaster declaration

72

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Expenses over policy limit due to this disaster

You actually to repairs

10/28/2013

37

73

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

You notify us within 30 days of repairs which increase building replacement value over 5% - and then we adjust building limit if we see fit

74

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Formula for determining maximum amount of Add’l Expense Coverage allowed

Apply specified % to limit of insurance

10/28/2013

38

75

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Can use 20% of Add’lExpense Coverage for debris Removal –does NOT increase Additional Expense Coverage

76

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Can use 20% of Add’lExpense Coverage for Ordinance or Law expenses – again NOT increase Add’lCoverage Limit

10/28/2013

39

77

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Coverage on an Annual Aggregate basis

78

Loss Settlement option-Increase in rebuilding expenses following disaster CP 04 09

Any expenses payable under this endorsement are reduced by expensesrecovered under any Business Income or Extra Expense Coverage Formincluded in the policy.

10/28/2013

40

79

Business Income endorsements – utility services

What if there is damage to waste water treatment plant or the sewer lines and systems due to hurricane or explosion or other covered situation …and your insured has to close down because no waste can be removed …so whether operations require add’l waste removal …or just plain human needs …

No operations …no income ….

80

Business Income endorsements – utility services Time Element CP 15 45

Same old endorsement …but NEW option

10/28/2013

41

81

Business Income endorsements – utility services Time Element CP 15 45

Again … BII interruption must be due to covered Cause of Loss

Reinforce –NOT due to flooding

82

Business Income endorsements – food contamination

What if you insure a café that had purchased and prepared food such as salads and dinners that were contaminated by salmonella and the Board of Health closes it down due to discovery or suspicion of food contamination

Or …Employee playing with food …has hepatitis and potentially passed it along to customers

10/28/2013

42

83

Business Income endorsements – food contamination

What about the cost to advertise

so that you don’t lose customersyou let customers know your status

expensesTo clean the insured's equipment as required by governmental authority

Cost to replace the food

84

Business Income endorsements – food contamination CP 15 05

Coverage on annual aggregate basisFor two different types of expenses1) Food contamination

2) Advertizing expense

10/28/2013

43

85

Business Income endorsements – food contamination CP 15 05

Food contaminationExpenses paid

1) clean equip2) replace food3) Cost to test

employees not paid by W/C

4) BII loss after 24 hrs – closed by gov’t agency

86

Business Income endorsements – food contamination CP 15 05

Can buy additional advertizing expense to restore reputation

Either limit is annual aggregate

10/28/2013

44

87

Business Income endorsements – food contamination CP 15 05

Defines food contamination

Tainted food distribute or buy

Food improperly processed/stored during operations

Food contaminated by employees

88

Thank you for attending…

2012 ISO CP Changes – Part 2changes to existing coverage forms and

endorsements