Embed Size (px)

Citation preview

Real Estate Investment Research

National Apartment Report2011

SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY INCREASE SALES DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND REVENUES BUYER ACTIVITY INTEREST DECLINE CONCESSIONS BURN SELLER RECOVERY CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES QE2 RENT GROWTH VELOCITY MOMENTUM DISCOUNTS RATE REBOUND SUBMARKET RENT GROWTH PERCENT ABSORPTION EXPANSION PRICING PROPERTY AVERAGE BID ASK MAXIMIZE FOCUS HEADWINDS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH PROJECTED FREDDIE MAC LOCAL EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH ACQUISITIONS POTENTIAL UPTURN FORECLOSURE MODERATE JOB GROWTH SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY INCREASE SALES DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND REVENUES BUYER EMERGING INTEREST DECLINE CONCESSIONS BURN SELLER RECOVERY CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES QE2 RENT GROWTH VELOCITY MOMENTUM DISCOUNTS RATE VELOCITY SUBMARKET RENT GROWTH PERCENT ABSORPTION EXPANSION PRICING PROPERTY AVERAGE BID ASK MAXIMIZE FOCUS HEADWINDS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH PROJECTED FREDDIE MAC LOCAL EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH ACQUISITIONS POTENTIAL UPTURN FORECLOSURE MODERATE JOB GROWTH SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY INCREASE SALES DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND REVENUES BUYER EMERGING INTEREST DECLINE CONCESSIONS BURN SELLER RECOVERY CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES QE2 RENT GROWTH VELOCITY MOMENTUM DISCOUNTS RATE LEGISLATIVE GRIDLOCK SUBMARKET RENT GROWTH PERCENT ABSORPTION EXPANSION PRICING ECHO BOOMERS AVERAGE BID ASK MAXIMIZE FOCUS HEADWINDS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH PROJECTED FREDDIE MAC EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH LOCAL ACQUISITIONS POTENTIAL UPTURN APARTMENT FORECLOSURE MODERATE JOB GROWTH SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY SALES INCREASE DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND REVENUES BUYER EMERGING INTEREST CONCESSIONS BURN SELLER RECOVERY CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES QE2 RENT GROWTH HEADWINDS VELOCITY MOMENTUM SUBMARKET DISCOUNTS RATE RENT GROWTH MARKET PERCENT ABSORPTION EXPANSION PRICING PROPERTY AVERAGE BID ASK MAXIMIZE FOCUS REBOUND ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH PROJECTED FREDDIE MAC LOCAL QE2 EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH ACQUISITIONS POTENTIAL UPTURN FORECLOSURE MODERATE JOB GROWTH SUSTAINABLE FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SINGLE-FAMILY OVER-SUPPLY SALES DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND TRENDS REVENUES BUYER EMERGING INTEREST DECLINE CONCESSIONS BURN SELLER CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY FISCAL PROFORMA ECONOMY DELIVER CAP RATES VELOCITY MOMENTUM DISCOUNTS CONCESSIONS BURN SUBMARKET RECOVERY ABSORPTION EXPANSION PRICING PROPERTY AVERAGE SHADOW BID ASK MARKET MAXIMIZE FOCUS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT NATIONWIDE STRENGTH PROJECTED FREDDIE MAC LOCAL EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS HEADWINDS SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH ACQUISITIONS POTENTIAL UPTURN FORECLOSURE MODERATE JOB GROWTH HEADWINDS SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION ROLLOVER RESILIENCE SPENDING INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY INCREASE SALES DISTRESSED RANK POPULATION PENT-UP DEMAND REVENUES BUYER EMERGING LOW COMPLETIONS INTEREST DECLINE CONCESSIONS BURN SELLER SPENDING FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES DISTRESSED QE2 VELOCITY RENT GROWTH MOMENTUM DISCOUNTS RATE LEGISLATIVE GRIDLOCK SUBMARKET RENT GROWTH PERCENT ABSORPTION EXPANSION PRICING PROPERTY AVERAGE BID ASK MAXIMIZE FOCUS HEADWINDS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH PROJECTED FREDDIE MAC LOCAL EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH ACQUISITIONS POTENTIAL UPTURN FORECLOSURE MODERATE JOB GROWTH SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY SALES DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND REVENUES BUYER INTEREST DECLINE CONCESSIONS BURN SELLER RECOVERY CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES QE2 RENT GROWTH VELOCITY MOMENTUM DISCOUNTS RATE LEGISLATIVE GRIDLOCK SUBMARKET RENT GROWTH PERCENT ABSORPTION EXPANSION PRICING PROPERTY AVERAGE BID ASK MAXIMIZE FOCUS HEADWINDS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH ECHO BOOMERS FREDDIE MAC LOCAL EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH ACQUISITIONS POTENTIAL UPTURN FORECLOSURE MODERATE JOB GROWTH SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY INCREASE SALES DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND REVENUES BUYER EMERGING INTEREST DECLINE CONCESSIONS BURN SELLER RECOVERY CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES QE2 RENT GROWTH VELOCITY MOMENTUM DISCOUNTS RATE LEGISLATIVE GRIDLOCK SUBMARKET RENT GROWTH PERCENT ABSORPTION EXPANSION PRICING PROPERTY AVERAGE BID ASK MAXIMIZE FOCUS HEADWINDS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH PROJECTED FREDDIE MAC LOCAL EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION UNCERTAINTY RENT GROWTH ACQUISITIONS POTENTIAL UPTURN FORECLOSURE MODERATE JOB GROWTH SURGE SUSTAINABLE OPPORTUNITY FORECAST OUTLOOK SIGNS CAPITAL NEW CONSTRUCTION INFLATION TRENDS HIGH UNEMPLOYMENT GROWTH SPENDING STABILIZED INVESTMENT VACANCIES SHADOW MARKET SINGLE-FAMILY OVER-SUPPLY INCREASE SALES DISTRESSED RANK RESILIENCE INVENTORY POPULATION PENT-UP DEMAND REVENUES BUYER EMERGING INTEREST DECLINE CONCESSIONS BURN SELLER RECOVERY CONDOS FOR RENT FUTURE OF FANNIE MAE RETURNS YEAREND LOW COMPLETIONS QE2 STRATEGY LIMIT FISCAL PROFORMA ECONOMY DELIVER CAP RATES QE2 RENT GROWTH VELOCITY MOMENTUM DISCOUNTS RATE LEGISLATIVE GRIDLOCK SUBMARKET RENT GROWTH PERCENT ABSORPTION EXPANSION PRICING PROPERTY AVERAGE BID ASK MAXIMIZE FOCUS HEADWINDS ROLLOVER POTENTIAL FUNDAMENTALS URBAN DEVELOPMENT INCOME NATIONWIDE STRENGTH PROJECTED FREDDIE MAC LOCAL EXCEEDING CONDOS FOR RENT INVESTOR TRENDS EMERGING GAINS RISK SLUMP DRIVERS ASSETS CASH FLOW RECESSION

COVER – 2011 NATIONAL APARTMENT RESEARCH REPORT: 16” X 10¾” (8” X 10¾” FOLDED); PMS 540 SPOT + C M Y K

Research Services:2398 E. Camelback RoadSuite 550Phoenix, AZ 85016(602) 687-6700

Offices Throughout the United States

www.MarcusMillichap.com

2011

2011 National Apartment Report

To our valued clients:

The economy weathered numerous challenges and setbacks as it made slow progress toward recovery last year. Cautious consumers and cash-heavy, but guarded, U.S. companies refl ected a pervasive negative psychology, which hampered economic momentum. To be sure, profound concerns and economic risks will linger well into 2011, par-ticularly high unemployment, record private- and public-sector debt, and the potential for sovereign debt contagion. The gravity of these issues, however, should not overshadow key indicators that affi rm a solid footing for the U.S. economy, including the return of core retail sales and corporate earnings to pre-recession levels and the creation of more than 1.2 million private-sector jobs in 2010. While job creation last year was tepid, especially in light of the 8.4 mil-lion jobs cut during the Great Recession, it is a solid start and better than the early stages of the last two recovery cycles.

Consumers, though hampered by high unemployment and limited credit, will make positive contributions to the recovery this year, but they still lack the wherewithal to propel the economy forward as they have in previous recoveries. In this cycle, businesses must assume the lead, a trend that will slowly manifest over the course of 2011 as companies gain suffi cient confi dence to expand capital expenditures and long-term hiring. In the near term, they will continue to rely on temporary employment to keep expenses low and options open, though easing uncertainty and strengthening demand by midyear will encourage business spending and job creation in the second half.

The Fed’s latest round of quantitative easing signals a continued willingness by the government to mitigate defl a-tion and other near-term risks to the recovery. The extension of the Bush-era tax cuts, which were scheduled to sunset at the end of 2010, will stimulate the economy and bring badly needed clarity to the markets. Like many policy deci-sions developed along the learning curve of the Great Recession, the economic benefi t and effi cacy of these efforts in achieving the stated goals, and even unintended consequences, may not emerge for some time.

The apartment sector will continue to lead the recovery in commercial real estate fundamentals through 2011 as owners capitalize on lower vacancies to raise rents and scale back concessions. In addition, historically light construc-tion levels in most markets over the next two to three years will help owners more than recover the ground lost through the recession. These factors, along with broad-based, though limited, job growth, will propel all 44 markets covered in this report toward falling apartment vacancies in 2011, together with climbing rents. The unprecedented breadth of this strengthening in apartment fundamentals, coupled with low-cost debt, will continue to fuel higher apartment investment activity. REITs and institutional investors, who led the charge in the buying surge last year, will look be-yond top-tier assets in the best markets, which are now priced to perfection, in search of yield. Private and opportunity investors, frustrated by the limited inventory of distressed sales, are adjusting their yield expectations and appear poised to become more active.

To assist you in planning and executing a successful investment strategy, we are pleased to present our 2011 Na-tional Apartment Report. Included is our National Apartment Index (NAI), a forward-looking ranking of 44 markets based upon forecast economic, supply and demand conditions. We hope you will fi nd this report helpful, and our investment professionals look forward to assisting you in meeting your goals.

Sincerely,

John J. Kerin Hessam NadjiPresident and Managing DirectorChief Executive Offi cer Research and Advisory Services

2011 National Apartment Report

2011 Annual Report

NATIONAL PERSPECTIVE Executive Summary .......................................................................................... 3 National Apartment Index ................................................................................ 4-5 National Economy ............................................................................................ 6 National Apartment Overview .............................................................................. 7 Capital Markets ............................................................................................... 8 Apartment Investment Outlook ............................................................................ 9

MARKET OVERVIEWS Atlanta ........................................................................................................ 10 Austin ......................................................................................................... 11 Boston ......................................................................................................... 12 Charlotte ..................................................................................................... 13 Chicago ....................................................................................................... 14 Cincinnati..................................................................................................... 15 Cleveland ..................................................................................................... 16 Columbus ..................................................................................................... 17 Dallas/Fort Worth ........................................................................................... 18 Denver ........................................................................................................ 19 Detroit ........................................................................................................ 20 Fort Lauderdale ............................................................................................. 21 Houston ....................................................................................................... 22 Indianapolis .................................................................................................. 23 Jacksonville .................................................................................................. 24 Kansas City ................................................................................................... 25 Las Vegas ..................................................................................................... 26 Los Angeles ................................................................................................... 27 Louisville ..................................................................................................... 28 Miami .......................................................................................................... 29 Milwaukee .................................................................................................... 30 Minneapolis-St. Paul ........................................................................................ 31 Statistical Summary Table ............................................................................. 32-33 New Haven ................................................................................................... 34 New Jersey ................................................................................................... 35 New York City ................................................................................................ 36 Oakland ....................................................................................................... 37 Orange County ............................................................................................... 38 Orlando ....................................................................................................... 39 Philadelphia .................................................................................................. 40 Phoenix ....................................................................................................... 41 Portland ....................................................................................................... 42 Riverside-San Bernardino .................................................................................. 43 Sacramento .................................................................................................. 44 Salt Lake City ................................................................................................ 45 San Antonio ................................................................................................... 46 San Diego ..................................................................................................... 47 San Francisco ................................................................................................ 48 San Jose ...................................................................................................... 49 Seattle ........................................................................................................ 50 St. Louis ...................................................................................................... 51 Tampa ......................................................................................................... 52 Tucson ......................................................................................................... 53 Washington, D.C. ............................................................................................ 54 West Palm Beach ............................................................................................ 55

CLIENT SERVICES Research Services ........................................................................................... 56 Contacts, Sources and Defi nitions ........................................................................ 57 Offi ce Locations ......................................................................................... 58-59

Written by John Chang, Vice President, Research Services, and edited by Hessam Nadji, Managing Director. The Capital Markets section was co-authored by William E. Hughes, Managing Director, Marcus & Millichap Capital Corporation. Additional contributions were made by Marcus & Millichap market analysts and investment brokerage professionals nationwide.

Executive Summary

2011 Annual Report page 3

National Apartment Index (NAI)◆ Healthy employment growth expectations and tight vacancies advanced New York City two places to the #1 spot in the NAI,

bumping Washington, D.C., to #2. California markets also fared well in the index due to perennial supply constraints that will keep vacancy steady and generate some of the strongest effective rent gains.

◆ Tech-heavy markets led advances in the 2011 NAI, with Austin (#9), Denver (#14) and Seattle (#15) all climbing seven spots. Fellow tech titans Boston (#3) and San Jose (#4) gained fi ve and six positions, respectively. Other Texas markets achieved strong momentum due to healthy job gains, favorable demographics and revenue growth prospects; Dallas/Fort Worth (#18) and Houston (#24) rose fi ve and four spots, respectively.

◆ Midwestern markets remain stable but slipped in the NAI, as coastal and dynamic markets offer greater growth potential this year. Declines were led by Cleveland (#40) and Milwaukee (#25), both of which lost eight positions, while Detroit (#42) and Columbus (#37) each dropped six spots. Minneapolis-St. Paul (#8) slipped four places but maintained a top 10 ranking.

National Economy◆ The U.S. economy will add 2 million jobs in 2011, double the amount created in 2010. The extension of Bush-era tax cuts and

the addition of new incentives for businesses should stimulate hiring driven by export-related industries, a cyclical rebound in technology goods and services, and the business and professional services sector.

◆ Several trends suggest the recovery will gain more traction, including moderate private-sector job growth, improving consump-tion, stabilizing initial unemployment claims, robust temporary hiring, strong and sustained corporate profi tability, and easing bond spreads. Recent government actions signal a willingness to take strong, albeit controversial, steps to reinforce the recovery.

◆ The Fed will have to tread carefully to recalibrate monetary policy in response to stronger economic expansion to keep infl a-tion at bay. Many housing markets will also continue to struggle as foreclosures make their way through the pipeline, and concerns will loom over solvency and trade implications as risks of sovereign debt defaults roll across the eurozone.

National Apartment Overview◆ All 44 markets will post employment growth, vacancy declines and effective rent gains in 2011, confi rming a sweeping recov-

ery and expansion in the U.S. apartment sector above expectations. This year will mark the fi rst across-the-board reduction in vacancy since at least 1990. This is driven by the release of pent-up demand in the aftermath of the Great Recession, lower turnover rates, falling homeownership and job growth.

◆ Apartment completions will total 53,000 units this year, 46 percent fewer than delivered in 2010. New supply will again fall critically short of demand, which is expected to reach 158,000 units. U.S. apartment vacancy will decrease 110 basis points in 2011 to 5.8 percent as a result, matching the decline recorded in 2010.

◆ As vacancy in 2011 aligns closely to pre-recession levels, owners will regain pricing power. Asking rents will rise 3.5 percent to $1,067 per month, while effective rates will increase 4.5 percent to $1,002 per month.

Capital Markets◆ Fannie Mae and Freddie Mac provide apartments a fi nancing advantage relative to other property types, but more com-

mercial banks and life insurance companies are stepping up with competitive terms. The agencies registered a healthy delin-quency rate of 1 percent in their multifamily portfolios, a strong indication of their continued involvement in the sector.

◆ Debt availability increased dramatically from the trough two years ago, but the overall supply remains limited and selective. Sales of $5 million to $20 million in the Class B-minus to C-quality range face fewer fi nancing prospects than top-tier assets.

◆ Seller fi nancing and loan assumptions accounted for nearly 30 percent of all commercial real estate transactions last year and will remain common in 2011. Life insurance companies and CMBS are poised to extend recent gains in volume.

Apartment Investment Outlook◆ Dollar volume will rise further this year as the economy gains momentum, apartment fundamentals improve, debt markets

loosen, and REITs and institutions increase acquisitions. During 2010, apartment sales volume totaled an estimated $40 bil-lion, up nearly 65 percent from the cyclical low in 2009 but less than one-third of the 2006 peak.

◆ Institutional investors led the surge in sales in 2010, with dollar volume more than doubling in the $20 million-plus segment. Improving occupancy and rising rents, along with low-cost debt, will help assuage investors’ and lenders’ lingering trepida-tion about values. As the year progresses, investors will move down the quality chain in search of stronger yields, resulting in more sales in the Class B and B- categories.

◆ The average cap rate will decline in 2011 after slipping 20 basis points in 2010 to 7.2 percent, led by recompression of the most sought-after deals. Since peaking in 2009, cap rates for top-quality properties have fallen by as much as 100 basis points.

National Apartment Index

page 4 2011 Annual Report

Vaca

ncy

Rate

Markets with the LowestExpected 2011 Employment Growth

Nonfarm Employment (Y-O-Y Change)

Markets with the LowestExpected 2011 Vacancy Rates

New Yo

rk C

ity

San

Jose

Minne

apoli

s-St.

Paul

San

Diego

New Je

rsey

Phila

delph

ia

San

Fran

cisco

New H

aven

Portl

and

Washi

ngto

n, D

.C.

Unite

d Sta

tes

Markets with the HighestExpected 2011 Employment Growth

Nonfarm Employment (Y-O-Y Change)

0% 1% 2% 3% 4%United StatesNew York City

OrlandoWest Palm Beach

San AntonioSan JoseHouston

Orange CountyDallas/Fort WorthWashington, D.C.

Austin

0% 0.4% 0.8% 1.2% 1.6%United States

Fort LauderdaleKansas CityCincinnati

ChicagoLouisville

SacramentoCleveland

PhiladelphiaDetroit

New Jersey

2%

3%

4%

5%

6%

Vaca

ncy

Rate

Markets with the HighestExpected 2011 Vacancy Rates

Jack

sonv

ille

Housto

n

Las V

egas

Tucs

on

Phoe

nix

Atlan

ta

Orland

o

Colu

mbus

Kans

as C

ity

Char

lotte

Unite

d Sta

tes

4%

6%

8%

10%

12%

Markets with the HighestExpected 2011 Completions

Uni

ts (

thou

sand

s)

Dalla

s/For

t Wor

th

Housto

n

Washi

ngto

n, D

.C.

Austi

n

Phoe

nix

San A

nton

io

Seat

tle

New Yo

rk C

ity

Los A

ngele

s

New Je

rsey

0

1.5

3.0

4.5

6.0

2011 National Apartment Index

Strengthening Economy Fuels Tech Markets, Texas and Florida

A cyclical recovery of the technology sector will continue to lend strength to the national economy, benefi ting tech-heavy employment markets. These metros led advances in the 2011 National Apartment In-dex (NAI), with Austin (#9), Denver (#14) and Seattle (#15) rising seven places, supported by growing hardware companies, software publishing and commercial aircraft manufacturing. Fellow tech titans Boston (#3) and San Jose (#4) gained fi ve and six positions, respectively.

Texas markets achieved strong momentum, generally due to healthy job gains, population and migration trends, and revenue growth pros-pects. The four major Texas MSAs lead U.S. employment growth fore-casts for 2011, refl ecting the state’s linkages to global trade, energy, tech-nology, and business and professional services. Dallas/Fort Worth (#18) and Houston (#24) rose fi ve and four spots, respectively. San Antonio (#13) slipped one notch this year behind markets with tighter vacancies. If Texas holds true to form, the next few years will present a good window for superior performance before the hyper-supply cycle begins again.

While Florida markets rank near the bottom of the NAI, all refl ect a broad-based regional vacancy rate recovery. Both central and coastal Florida metro areas strengthened in the ranking; Orlando (#30) and Fort Lauderdale (#34) advanced fi ve positions, while Miami (#21) and Tampa (#36) improved four spots. Jacksonville ranked last in the index, unchanged from 2010. Despite a strong rebound in occupancies, Jack-sonville posts a vacancy rate in double digits, and its 2011 rent growth forecast falls well below the national average. Supported by trends simi-lar to those in the Florida markets, the Phoenix (#27) apartment recovery built momentum last year that will carry into 2011, advancing the market seven places in the 2011 ranking.

New York City Edges Out Washington, D.C., for Top Spot

With healthy employment expected for 2011, combined with already tight vacancies, New York City advanced two places in the NAI this year to claim the #1 spot, bumping Washington, D.C., to #2. Three other New England markets retreated, however; New Jersey (#12) and New Haven (#20) fell six places, while Philadelphia (#10) slipped fi ve spots, primar-ily on weak employment forecasts. Philadelphia and New Jersey’s lower ranking stems from other markets posting stronger recoveries, and each will likely improve as their lagging labor markets recover.

National Apartment Index

2011 Annual Report page 5

Growth Markets Bypass Stable Midwestern Metros; Coastal California Maintains Ranking in Top Quartile

Midwestern markets fell in the 2011 NAI, largely due to being sup-planted by core, coastal and dynamic markets with greater growth poten-tial. Cleveland (#40) and Milwaukee (#25) declined eight positions, while Detroit (#42) and Columbus (#37) dropped six spots. Minneapolis-St. Paul (#8) slipped four places but remained in the top one-third due to tight and declining vacancy and solid rent growth prospects. Chicago (#23) receded three spots in the ranking but should move up next year as employment gains momentum and vacancies tighter further.

Perennial supply constraints throughout much of California have kept vacancies among the tightest in the country while generating some of the highest-ranked effective rents. These factors drove most markets in the state toward the top of the NAI this year. Orange County (#5) and Los Angeles (#11) advanced two spots in the 2011 ranking, while San Fran-cisco (#7) also moved up two positions on a job growth projection above that of the nation and strong momentum in asking rents. San Diego (#6), however, dropped four notches as top employment growth markets sur-passed it.

Index Methodology

The NAI is a snapshot analysis that ranks 44 major apartment mar-kets based upon a series of 12-month forward-looking economic and sup-ply and demand variables. Markets are ranked based on their cumula-tive weighted-average scores for various indicators, including forecast employment growth, vacancy, construction, housing affordability and rents. Taking into account both the forecast level and incremental change over the next year, the index is designed to indicate relative supply and demand conditions at the metro level.

Users of the index are cautioned to keep several important points in mind. First, the NAI is not designed to predict the performance of indi-vidual investments. A carefully chosen property in the bottom-ranked market could easily outperform a poor choice in the top-ranked market. Second, the index ranking is a snapshot of a one-year time horizon. A market facing diffi culties in the near term may provide excellent long-term prospects, and vice versa. Third, a market’s ranking may fall from one year to the next even if its fundamentals are strengthening.

The NAI is an ordinal index, and differences in specifi c rankings should be carefully interpreted. A top-ranked market is not necessarily twice as good as the second-ranked market, for example, nor is it 10 times better than the 10th-ranked market.

Markets with the HighestExpected 2011 Absorption

Uni

ts (

thou

sand

s)

Dalla

s/For

t Wor

th

Housto

n

Atlan

ta

Washi

ngto

n, D

.C.

Los A

ngele

s

New Je

rsey

Phoe

nix

Austi

n

Phila

delph

ia

San A

nton

io2

4

6

8

10

Rank Rank 10-11MSA 2011 20101 Change

New York City 1 3 ▲ 2

Washington, D.C. 2 1 ▼ 1

Boston 3 8 ▲ 5

San Jose 4 10 ▲ 6

Orange County 5 7 ▲ 2

San Diego 6 2 ▼ 4

San Francisco 7 9 ▲ 2

Minneapolis-St. Paul 8 4 ▼ 4

Austin 9 16 ▲ 7

Philadelphia 10 5 ▼ 5

Los Angeles 11 13 ▲ 2

New Jersey 12 6 ▼ 6

San Antonio 13 12 ▼ 1

Denver 14 21 ▲ 7

Seattle 15 22 ▲ 7

Portland 16 19 ▲ 3

Oakland 17 18 ▲ 1

Dallas/Fort Worth 18 23 ▲ 5

Salt Lake City 19 11 ▼ 8

New Haven 20 14 ▼ 6

Miami 21 25 ▲ 4

Louisville 22 15 ▼ 7

Chicago 23 20 ▼ 3

Houston 24 28 ▲ 4

Milwaukee 25 17 ▼ 8

Kansas City 26 24 ▼ 2

Phoenix 27 34 ▲ 7

Charlotte 28 29 ▲ 1

St. Louis 29 26 ▼ 3

Orlando 30 35 ▲ 5

Indianapolis 31 27 ▼ 4

Riverside-San Bernardino 32 37 ▲ 5

Cincinnati 33 30 ▼ 3

Fort Lauderdale 34 39 ▲ 5

Sacramento 35 33 ▼ 2

Tampa 36 40 ▲ 4

Columbus 37 31 ▼ 6

West Palm Beach 38 41 ▲ 3

Atlanta 39 42 ▲ 3

Cleveland 40 32 ▼ 8

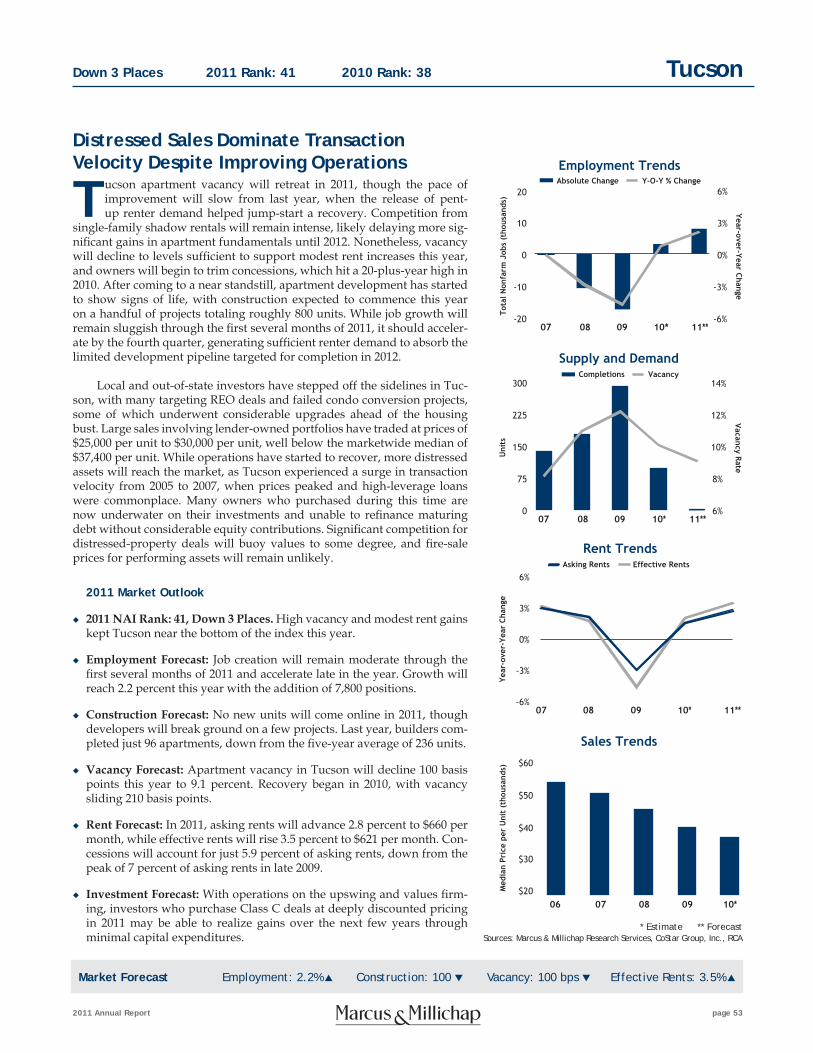

Tucson 41 38 ▼ 3

Detroit 42 36 ▼ 6

Las Vegas 43 43 ■ 0

Jacksonville 44 44 ■ 0

1 See National Apartment Index Note on page 57.

National Economy

page 6 2011 Annual Report

Ann

ualiz

ed Q

uart

erly

Cha

nge

in G

DP

-10%

-5%

0%

5%

10%

11**10*050095908580

U.S. GDP

Retail Sales and UnemploymentUnemployment RateRetail Sales, Excluding Auto & Gas

Une

mpl

oym

ent

Rate

Year-over-Year Change in Retail Sales-10%

-5%

0%

5%

10%

0%

3%

6%

9%

12%

10****09080706050403020100

Fallen Yield Curve Sign of Slow Growth;Level Still Above Recessionary Point

Tem

pora

ry E

mpl

oym

ent

(Y-O

-Y C

hg.) N

onfarm Em

ployment (Y-O

-Y Chg.)-30%

-15%

0%

15%

30%

10***09070503019997959391-6%

-3%

0%

3%

6%

Recessions

Temporary vs. Nonfarm EmploymentTemporary Employment Nonfarm Employment

Spre

ad B

etw

een

10-Y

ear

Not

e &

Thre

e-M

onth

Bill

-6

-3

0

3

6

10***050095908580757068

Recessions

The U.S. economic recovery has unfolded in anything but a linear fash-ion, as tenuous, and occasionally erratic, economic growth has tested the durability of the recovery and sparked concerns of a double-dip

recession. This scenario remains improbable, however, as today’s low in-terest rate and minimal infl ation environment differs from conditions 30 years ago, when the U.S. experienced its last double-dip recession. Further-more, recent government actions, such as the extension of Bush-era tax cuts and the resumption of quantitative easing by the Fed, signal a willingness to take strong, albeit controversial, measures to reinforce economic recov-ery. Several trends suggest the recovery will gain more traction, including moderate private-sector job growth, improving consumption, lower initial unemployment claims, robust temporary hiring, strong and sustained cor-porate profi tability, and easing bond spreads.

While overall employment growth disappointed through the lat-ter half of 2010, job creation among the prime renter age cohort of 20- to 34-year-olds signifi cantly outpaced the broader market. This trend helped jump-start a recovery in the apartment market, boosting absorption to lev-els unseen since 2000, when job growth and household formations boomed, a sharp contrast to current conditions. Both employment and household growth will accelerate in 2011, but the rate of gains depends on improving corporate confi dence, which is essential to increasing investment and hir-ing. The Fed’s ability to keep infl ation at bay by recalibrating monetary pol-icy in response to economic expansion may not be fully tested in 2011 but remains paramount to the recovery staying on course. The housing market, saddled with foreclosures, will not be a contributor to the expansion until 2012. Concerns about solvency and trade implications also loom as risks of sovereign debt defaults roll across the eurozone.

2011 National Economic Outlook

◆ Employment Growth to Accelerate. The U.S. economy will add 2 million jobs in 2011, double the amount created in 2010. The extension of Bush-era tax cuts and the addition of new incentives for businesses should stimulate hiring driven by export-related industries, a cyclical rebound in technology goods and services, and the business and professional ser-vices sector. Tax-cut extensions will add 50 basis points to 75 basis points to GDP.

◆ U.S. Economy Transitioning to Private Sector. GDP will rise by between 2.5 percent and 3.0 percent this year as growth shifts from government initiatives and inventory restocking to the still-wary private sector. Cor-porations will likely utilize a share of their cash stockpiles on new equip-ment and software, lending a boost to the headline rate of growth.

◆ Elevated Unemployment, Weak Housing Create Drag. While foreclo-sures will slow as irregularities in the process are examined, distress sales will remain an enduring theme, holding down prices in harder-hit markets. At the same time, unemployment will stay elevated, hovering in the high-9 percent range through at least the fi rst half of the year.

◆ Commercial Mortgage Maturities Pose Risk. Five-year loans made at the peak of the commercial real estate market in 2006 will ma-ture in 2011, creating risk for lenders holding high-leverage notes on underperforming assets. Banks hold approximately $1.5 trillion in com-mercial real estate loans, or roughly 45 percent of the total, while CMBS accounts for 20 percent.

Choppy Recovery Gradually Gains Steam as Private Sector Cautiously Takes Lead

* Estimate ** Forecast *** Through November**** Unemployment through Nov.; retail sales through Oct.

National Apartment Overview

2011 Annual Report page 7

Apartment Rent and Vacancy Trends

Aver

age

Effe

ctiv

e Re

nt

Vacancy Rate

Effective RentVacancy Rate

$700

$800

$900

$1,000

$1,100

11**10*0908070605040302012%

4%

6%

8%

10%

Completions vs. Units AbsorbedUnits CompletedNet Absorption

Employment in thePrime Renter Demographic

Vaca

ncy

Rate

Employm

ent Change (millions of jobs)

Employment Change - Ages 20-34Vacancy Rate

-1.0

-0.5

0

0.5

1.0

Apartment Revenue and Concessions

Reve

nue

per

Uni

t

Concessions as a % of Asking Rents

Revenue per UnitConcessions as a Percentageof Asking Rents

$750

$800

$850

$900

$950

10*0908070605040302010%

3%

6%

9%

12%

Uni

ts C

ompl

eted

(th

ousa

nds) U

nits Absorbed (thousands)

0

80

160

240

11**10*08060402009896949290-80

0

80

160

240

2%

4%

6%

8%

10%

10*090807060504030201

Apartments staged a strong recovery in 2010 well ahead of expecta-tions, despite modest job creation and stubbornly high unemploy-ment. Net absorption surged, with occupied stock rising by nearly

200,000 units, double the number of apartments constructed and the high-est level on record since 2000. Several factors contributed to high levels of absorption, including the release of pent-up renter demand as households de-bundled in the wake of the recession. In addition, apartments benefi ted from private-sector job growth in the critical 20- to 34-year-old cohort, ex-piration of the homebuyer tax credit, displaced foreclosed homeowners en-tering the renter pool, immigration and lower unit turnover. Renting also became a lifestyle and economic choice for many households as the effects of the housing collapse and recession persisted. Continued recovery in 2011 depends more heavily on improvements in the job market, which should gain momentum as the year progresses.

All 44 markets in the Marcus & Millichap National Apartment Index will post employment growth, vacancy declines and effective rent gains in 2011, confi rming a sweeping recovery and expansion in the U.S. apartment sector above expectations. This year will mark the fi rst across-the-board reduction in vacancy recorded since at least 1990; the strongest previous performance played out in 2005, when all but three apartment markets reg-istered declining vacancy rates. The last time all markets exhibited positive employment trends occurred in 1999, and not since 2006 have all markets posted effective rent growth. Further, new apartment supply will decline in all but six markets in 2011, the fi rst time such broad-based reductions have emerged in 20 years. At the national level, new supply dropped to sub-trend levels last year and completions will slip further in 2011, as tight cred-it conditions stalled construction projects and delayed new starts through much of the past few years.

2011 National Apartment Outlook

◆ Demand Outstrips New Supply. Apartment completions will total 53,000 units this year, 46 percent fewer than delivered in 2010. New sup-ply will again fall critically short of demand, which is expected to reach 158,000 units.

◆ Surging Demand Drives Vacancies Lower. U.S. apartment vacancy will decrease 110 basis points in 2011 to 5.8 percent, matching the decline recorded in 2010. Strong demand drivers and expectations for increased availability of debt this year, however, elevate the likelihood of a con-struction cycle ramping up in 2012.

◆ Rents Rise, Concession Ease. With vacancy in 2011 expected to align closely with pre-recession levels, owners will regain pricing power, par-ticularly in tight core markets. At the national level, asking rents will rise 3.5 percent to $1,067 per month, while effective rates will increase 4.5 percent to $1,002 per month. Last year, asking and effective rents gained 1.5 percent and 2.3 percent, respectively.

◆ Demographic Trends Support Positive Outlook. Stronger job growth will spur new household formation over the next few years, as will the progression of echo boomers into their prime renter years. Over the next fi ve years, the 20- to 34-year-old cohort will expand by 3.2 million in-dividuals. Rising interest rates, large downpayment requirements and tight lending standards will bias young households toward renting.

Apartment Recovery Surges Past Expectations; Strong Momentum for Coming Year

* Estimate ** Forecast

Capital Markets

page 8 2011 Annual Report

Commercial Mortgage Delinquency Rates

Del

inqu

ency

Rat

e

CMBS (30+ days and REO)Life Companies (60+ days)Fannie Mae (60+ days)Freddie Mac (60+ days)Banks & Thrifts (90+ days)

0%

2%

4%

6%

8%

10%

3Q10

4Q09

4Q08

4Q07

4Q06

4Q05

4Q04

4Q03

4Q02

4Q01

4Q00

4Q99

4Q98

CMBS, CDO & Other ABS, 13%

GSEs & Ginnie Mae, 36%

Other, 5%Life Insurance

Companies, 6%

SavingsInstitutions, 7%

State & Local Governments, 9%

Commercial Banks, 24%

Multifamily Mortgage Debt Outstanding

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Mat

urin

g Ba

lanc

e (b

illio

ns)

$0

$25

$50

$75

$100

Estimated Multifamily DebtMaturities by Vintage

Pre-20012001-2004

2005-20072008

All-in Rates Trend Lower, FollowDeclining 10-Year Treasury Yield

Rate

10-Year Treasury YieldFannie Mae All-in Rate (Tier 2)

0%

2%

4%

6%

8%

10090807

Debt availability has increased dramatically from the trough two years ago, but the overall supply remains limited and selective. Institutional debt sources share a preference for low-risk, higher-quality assets in

top-tier markets with strong sponsors. This mandate leaves the majority of the transaction bell-curve, which includes sales of $5 million to $20 million in the B-minus to C-quality range, with fewer fi nancing options. Transactions of this type can get funding, but the process and qualifi cations are more chal-lenging, with a signifi cant focus on sponsorship. A large number of proper-ties remain in limbo with respect to refi nancing without recapitalization or lender writedowns. An estimated $77 billion of maturing multifamily mort-gages will weigh on the market in 2011 as reduced market values in the B- to C- categories and higher loan-to-values (LTVs) create shortfalls for owners in need of refi nancing. This may result in more acquisition opportunities as many owners opt for a quick sale over additional equity contributions.

Fannie Mae and Freddie Mac provide apartments a fi nancing advan-tage relative to other property types, though more commercial banks and life insurance companies are stepping up with competitive terms. Lending by life insurance companies increased nearly 150 percent last year, while GSE volume declined 55 percent. In perspective, the GSEs currently hold 37 percent of the $843 billion in total multifamily mortgage debt outstanding, while life companies account for 6 percent. Multifamily delinquencies held in the GSEs’ portfolios remain below 1 percent, supporting expectations for the agencies to remain active, despite talk of reform in Washington, D.C. CMBS apartment loans continue to post high levels of distress, with delin-quency in this sector hovering around 8.5 percent. Economic growth and increases in apartment property values, particularly for high-quality assets, will relieve some pressure and lead to more sales and refi nancing. Some level of distress at the local- and regional-bank level with high exposure to lower-quality assets and construction loans will persist into 2013.

2011 Capital Markets Outlook

◆ 10-Year Treasury Yields Remain Low. The extension of quantitative eas-ing by the Fed will help restrain interest rates in the near term, holding the 10-year Treasury yield in the 3.4 percent to 4.0 percent range through most of 2011.

◆ All-in Rates Attractive; Lender Requirement Hurdles Remain. All-in rates for smaller apartment loans range from 3.75 percent to 4.5 percent for fi ve-year terms, with 10-year notes pricing 100 basis points higher. For larger, high-quality deals, the GSEs quote all-in rates of 3.75 percent to 4.6 percent, 100 basis points to 200 basis points lower than portfolio lenders. While rates are relatively low, stringent credit qualifi cations and higher LTVs will remain challenges for many potential borrowers.

◆ Seller Financing, Assumable Loans Prevalent. Seller fi nancing and loan as-sumptions accounted for nearly 30 percent of all commercial real estate transac-tions last year and will remain common in 2011. For more broad-based easing in traditional lending sources to occur, the economy will need to post several consecutive quarters of solid employment growth and overall expansion.

◆ Life Companies Ramp up; CMBS Re-Emerges. Motivated life insurance companies will offer low all-in rates on top-tier assets with good credit charac-teristics this year, regardless of asset size. CMBS issuance will continue to rise, but its next iteration will include new regulation, oversight of ratings’ agencies and more conservative underwriting than at the peak of CMBS dominance.

Access to Debt Capital DramaticallyImproving, Though Favoring Top-Tier Assets

Apartment Investment Outlook

2011 Annual Report page 9

Apartment Price and Cap Rate Trends

Aver

age

Pric

e pe

r U

nit

(tho

usan

ds)

Average Cap Rate

Average Price per UnitAverage Cap Rate

$0

$30

$60

$90

$120

10**090807060504030201005%

6%

7%

8%

9%

Tota

l Tra

nsac

tion

s (t

hous

ands

)

0

1

2

3

4

10**09080706

U.S. Apartment Transactions by Quarter

Yields in Primary Markets Recompress;Secondary, Tertiary Trends Stabilizing

Aver

age

Cap

Rate

Primary Secondary Tertiary

5%

6%

7%

8%

9%

10**090807060504

Apartment Cap Rate TrendsApartment Cap Rate 10-Year Treasury Rate

Sales $1M and above

Ave

rage

Rat

e

2%

4%

6%

8%

10%

10*08060402009896949290

380 bps

400 bps

430 bps

410 bps

Cap Rate Long-Term Avg.

10-Year TreasuryLong-Term Avg.

90 bps

400 bps

Pricing for quality apartment assets in primary markets turned aggres-sive in 2010, leapfrogging property fundamentals. As REIT and insti-tutional activity fueled momentum in the $20 million-plus category,

the average price per unit increased and cap rates fell, though both mea-sures are still down from levels achieved at the market’s peak. A prevailing fl ight to quality and attractive returns over other investment alternatives prompted buyers to compete more intensely for top-quality deals. Last year, the spread between the average cap rate in the apartment sector and the 10-year Treasury yield widened to the largest gap on record in at least 20 years before edging back to 400 basis points. For comparison, the differ-ence between the long-term average cap rate and 10-year Treasury yield is 290 basis points.

Improving occupancies and rising rents, along with stabilized cash fl ows and strong demand for quality income-producing properties, will continue to lend support to market pricing this year, helping assuage lin-gering trepidation about values. Yield compression and limited inventory in the upper end of the market will lead to more sales of Class B and B- properties in 2011, spurring greater activity among private and opportuni-ty investors. As the year progresses, more buyers will move down the qual-ity chain in search of stronger yields, encouraging price discovery in the lower tiers and in secondary/tertiary markets. At the end of 2010, cap rates for mid-tier assets in tertiary markets exceeded those in primary markets by approximately 200 basis points, with secondary markets falling in the middle. This arbitrage offers attractive return spreads when viewed with properly assessed risks and a longer, fi ve-plus-year investment horizon.

2011 Investment Outlook

◆ Sales Volume Rising, Still Well Below Peak Levels. Dollar volume will rise further this year as the economy gains momentum, apartment fun-damentals improve and debt markets loosen. During 2010, apartment sales volume totaled an estimated $40 billion, up nearly 65 percent from the cyclical low in 2009 but less than one-third of the 2006 peak.

◆ Apartment Buyer Composition Shifting. REITs and institutions will increase acquisitions in 2011. Last year, approximately 80 percent of all transactions fell below $10 million, refl ecting a highly active private-buyer segment; however, public and institutional investors nearly qua-drupled their share of transactions, while equity funds tripled their share.

◆ Cap Rates Recompress. The average cap rate will decline in 2011 after slipping 20 basis points in 2010 to 7.2 percent, led by recompression of the most sought-after deals. Since peaking in 2009, cap rates for top-quality properties have fallen by as much as 100 basis points. Additional sup-port for prices derives from historically light construction and emerging demographic shifts that favor rental housing.

◆ Distress Creating Opportunities — in Moderation. Distressed-property sales increased dramatically in recent quarters, led by gains in deals over $20 million, but distressed activity still accounts for just 12 percent of all apartment sales. While demand for high-quality distress deals will con-tinue to outpace supply, a shortage of apartment construction, combined with a positive demand-side outlook and fi rming values, may turn more investor attention to unfi nished multifamily developments.

Low-Cost Debt, Rent Growth toIncrease Sales, Broaden Buyer Demand

* Estimate ** Through 3QSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

page 10 2011 Annual Report

* Estimate ** ForecastSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

Demand Surge Sparks Performance Gains,Though Distress Lingers in Atlanta

-150

-100

-50

0

50

Tota

l Non

farm

Job

s (t

hous

ands

)

Absolute Change Y-O-Y % Change

Employment Trends

08 09 10* 11**07

Year-over-Year Change

Uni

ts (

thou

sand

s)

Completions Vacancy

Supply and Demand

Vacancy Rate

$30

$40

$50

$60

$70

Med

ian

Pric

e pe

r U

nit

(tho

usan

ds)

Sales Trends

07 08 09 10*06

Year

-ove

r-Ye

ar C

hang

e

Asking Rents Effective Rents

Rent Trends

08 09 10* 11**07

0

2

4

6

8

08 09 10* 11**076%

8%

10%

12%

14%

-6%

-4%

-2%

0%

2%

-6%

-3%

0%

3%

6%

Atlanta Up 3 Places 2011 Rank: 39 2010 Rank: 42

Market Forecast Employment: 1.6% ▲ Construction: 3,900 ▼ Vacancy: 150 bps ▼ Effective Rents: 3.1% ▲

Renter demand will continue to improve in Atlanta during 2011 as hiring accelerates, providing a foundation for property owners to raise rents more aggressively as the year progresses. Asking rents in the Class A

segment, especially, appear poised to grow faster than the 1 percent increase posted last year. Submarkets such as Buckhead, Marietta and South Gwin-nett County, each with a large stock of upper-tier rentals, will record some of the greatest rent gains as availability tightens in these established core areas . Asking rents at Class B/C complexes will also rise more signifi cantly as hiring in lower-paying sectors boosts demand for lower-tier rental s . In another posi-tive trend in the market, completions will decrease this year. As demand-side conditions strengthen, however, developers will advance projects through the pipeline, initiating a new building cycle after 2011. Potential supply growth remains greatest in the Midtown and Cherokee County submarkets, where planned projects equal 19 percent and 12 percent of existing stock, respectively.

Although property operations will gain ground this year, the improve-ments may arrive too late to avert distress for many owners who purchased assets at the peak of the market under aggressive rent growth and occu-pancy assumptions. Sales of lender-owned properties accounted for more than 75 percent of Atlanta-area deals last year and will command a sizable proportion again in the year ahead. Potential buyers include owners of sta-bilized assets who have met return objectives and can redeploy capital into properties with greater upside potential. In addition to distressed assets, stabilized complexes that can be obtained with agency debt will draw the greatest interest, with cap rates expected to vary from 8 percent to 9 per-cent. More intense competition for well-performing Class A complexes will compress cap rates to less than 6 percent as a result.

2011 Market Outlook

◆ 2011 NAI Rank: 39, Up 3 Places. Below-average rent gains limited At-lanta’s rise in the NAI to just three spots this year.

◆ Employment Forecast: Employers will create 37,000 positions in 2011, a 1.6 percent increase. Last year, 21,700 jobs were added.

◆ Construction Forecast: Deliveries will subside to 1,000 units this year, compared with 4,900 units in 2010 and the fi ve-year average completion of 5,700 rentals annually.

◆ Vacancy Forecast: Following a 140 basis point decline last year, vacancy will fall 150 basis points in 2011 to 8.8 percent. Stronger job creation in the service sectors will reduce the Class B/C vacancy rate by 140 basis points to 11.1 percent.

◆ Rent Forecast: Driven by a 3.4 percent increase in the Class A segment, marketwide average asking rents will rise 2.5 percent this year to $853 per month; Class B/C asking rents will advance 1.4 percent. Marketwide effective rents will jump 3.1 percent to $770 per month.

◆ Investment Forecast: Distressed lower-quality assets will continue to at-tract buyers able to take a considerable equity portion in deals. Prices of approximately $20,000 per unit remain an attractive entry point for investors seeking to expand local portfolios.

2011 Annual Report page 11

* Estimate ** ForecastSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

-30

-15

0

15

30

Tota

l Non

farm

Job

s (t

hous

ands

)

Absolute Change Y-O-Y % Change

Employment Trends

08 09 10* 11**07

Year-over-Year Change

Uni

ts (

thou

sand

s)

Completions Vacancy

Supply and Demand

Vacancy Rate

$40

$45

$50

$55

$60

Med

ian

Pric

e pe

r U

nit

(tho

usan

ds)

Sales Trends

07 08 09 10*06

Year

-ove

r-Ye

ar C

hang

e

Asking Rents Effective Rents

Rent Trends

08 09 10* 11**07

0

3

6

9

12

08 09 10* 11**074%

6%

8%

10%

12%

-4%

-2%

0%

2%

4%

-8%

-4%

0%

4%

8%

Market Forecast Employment: 3.6% ▲ Construction: 1,100 ▼ Vacancy: 140 bps ▼ Effective Rents: 5.6% ▲

Austin Apartment Demand to Outstrip New Supply, Driving Above-Average Rent Growth

Healthy job and population growth will combine with reduced con-struction to set the stage for a potential shortage of apartments by late 2011. Throughout the economic downturn, absorption remained

positive in Austin, with rising vacancy largely a product of surging con-struction as opposed to sagging demand. Many of the complexes brought online in 2009 have since stabilized, with vacancy declining substantially through 2010; however, construction has commenced on just a handful of projects. As vacancy slips to a 10-year low in 2011, supporting stronger rent gains and concession burn, some planned and postponed projects will move off the sidelines. This likely includes a few large master-planned commu-nities just outside the metro’s boundaries along Highway 130. It will take time for developers to fully reboot, though, and Austin property owners will benefi t from the lull in completions over the next 12 to 18 months.

Austin apartment prices declined to a lesser degree than anticipated during the downturn and even began to recover last year, rising 3 percent. Limited discounting has driven many local investors to other Texas metros, a trend likely to persist through 2011 as prices edge up, particularly for bet-ter-quality assets. Opportunities for local investors will center around small properties in some level of distress, while most larger deals will be targeted by REITs, syndicates and out-of-state, private investors. Strong competition has already driven down cap rates for best-of-class assets to the low-5 per-cent range, while fi rst-year returns on well-located Class B properties fall in the high-6 percent range. As a result of compression, cap rates today may be comparable to some coastal markets, but investors in Austin anticipate outsized rent gains over the next few years as new apartment supply falls short of demand.

2011 Market Outlook

◆ 2011 NAI Rank: 9, Up 7 Places. The strongest rate of job growth in the nation fueled Austin’s seven-place jump in the index into the top 10.

◆ Employment Forecast: Job growth will reach 3.6 percent, or 28,000 posi-tions, in 2011. Last year, local employment rose by 3 percent.

◆ Construction Forecast: Construction will continue to wind down this year, with 1,800 units slated for delivery. In 2009 and 2010, developers completed 10,400 units and 2,900 units, respectively.

◆ Vacancy Forecast: Vacancy in Austin will decline 140 basis points in 2011 to 6.2 percent, the lowest level since 2001. Last year, vacancy plummeted 250 basis points.

◆ Rent Forecast: This year, average asking rents will rise 4.2 percent to an average of $901 per month, and effective rents will climb 5.6 percent to $824 per month.

◆ Investment Forecast: More Class A product will likely become available this year as projects completed in 2009 and early 2010 achieve suffi cient occupancy to support a sale. Proceeds from these deals will likely be put toward new development as higher rents and occupancy justify con-struction costs.

AustinUp 7 Places 2011 Rank: 9 2010 Rank: 16

page 12 2011 Annual Report

* Estimate ** ForecastSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

Market Forecast Employment: 2.0% ▲ Construction: 410 ▼ Vacancy: 100 bps ▼ Effective Rents: 4.5% ▲

-90

-45

0

45

90

Tota

l Non

farm

Job

s (t

hous

ands

)

Absolute Change Y-O-Y % Change

Employment Trends

08 09 10* 11**07

Year-over-Year Change

Uni

ts (

thou

sand

s)

Completions Vacancy

Supply and Demand

Vacancy Rate

$60

$80

$100

$120

$140

Med

ian

Pric

e pe

r U

nit

(tho

usan

ds)

Sales Trends

07 08 09 10*06

Year

-ove

r-Ye

ar C

hang

e

Asking Rents Effective Rents

Rent Trends

08 09 10* 11**07

0

2

4

6

8

08 09 10* 11**073%

4%

5%

6%

7%

-4%

-2%

0%

2%

4%

-6%

-3%

0%

3%

6%

A faster pace of job growth, a decline in rental construction, and im-proving vacancy and rent trends will place Boston among the top performing apartment markets in the country in 2011. Following a

solid rebound in hiring last year, employers will step up the pace as de-mand for goods and services strengthens in the months ahead. Job gains will occur in most employment segments, with the professional and busi-ness services and education and health services sectors expected to each grow nearly 3 percent. Demand for rental housing will improve with the employment market. Vacancy will decrease to the low-3 percent range in core urban submarkets, down from more than 5 percent during the reces-sion. In the suburbs, where more than 60 percent of jobs in the metro exist, vacancy will dip below 6 percent, enabling operators to signifi cantly reduce concessions by the second half of 2011.

As Boston remains a large, primary market with diverse demand driv-ers, local apartments will generate considerable interest when listed. Gener-ally, cap rates ranged from about 6.2 percent to 7.0 percent at the end of last year. Low interest rates and intensifi ed bidding will maintain downward pressure on cap rates throughout the fi rst half of 2011, encouraging owners to explore sales. Local investors will leverage price adjustments to expand portfolios, focusing on small properties in the city of Boston and near-in suburbs. Institutions and REITs, which increased activity in the second half of 2010, will target large, high-quality properties in the suburbs. The prob-ability that more intense bidding for these assets will drive up prices as the year progresses may compel many of these investors to seek lower-priced opportunities in other markets.

2011 Market Outlook

◆ 2011 NAI Rank: 3, Up 5 Places. Low housing affordability and above-average employment growth pushed Boston to the third position in this year’s NAI.

◆ Employment Forecast: In 2011, employment will expand 2 percent, or by 49,000 positions, compared with a 1.5 percent increase nationwide. Last year, local employers created 37,500 jobs.

◆ Construction Forecast: Rental stock will grow only 0.3 percent in 2011 as 600 units are completed, one of the lowest totals in the past 10 years. Slightly more than 1,000 rentals were delivered in 2010.

◆ Vacancy Forecast: Waning construction and accelerated job growth will support a 100 basis point decline in vacancy this year to 4.5 percent. The release of pent-up demand generated a 90 basis point decrease in the vacancy rate during 2010.

◆ Rent Forecast: In 2011, asking rents will climb 3.5 percent to $1,777 per month, while concessions will burn as effective rents advance 4.5 percent to $1,697 per month.

◆ Investment Forecast: Additional loosening of the capital markets will support strong bids among local buyers for small properties in the city of Boston. Investors seeking stable suburban assets will focus on the Mass Pike and Route 9 corridors.

Vacancy Decline Persists, Rents to RiseFollowing Strong Rebound Last Year

Boston Up 5 Places 2011 Rank: 3 2010 Rank: 8

2011 Annual Report page 13

* Estimate ** ForecastSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

-50

-25

0

25

50

Tota

l Non

farm

Job

s (t

hous

ands

)

Absolute Change Y-O-Y % Change

Employment Trends

08 09 10* 11**07

Year-over-Year Change

Uni

ts (

thou

sand

s)

Completions Vacancy

Supply and Demand

Vacancy Rate

$30

$40

$50

$60

$70

Med

ian

Pric

e pe

r U

nit

(tho

usan

ds)

Sales Trends

07 08 09 10*06

Year

-ove

r-Ye

ar C

hang

e

Asking Rents Effective Rents

Rent Trends

08 09 10* 11**07

0

1

2

3

4

08 09 10* 11**074%

6%

8%

10%

12%

-6%

-3%

0%

3%

6%

-6%

-3%

0%

3%

6%

Market Forecast Employment: 2.1% ▲ Construction: 860 ▼ Vacancy: 100 bps ▼ Effective Rents: 3.6% ▲

A projected decrease in apartment completions this year will under-pin a further reduction in vacancy and enable Charlotte property operators to implement more signifi cant rent increases. In a market

characterized by periods of substantial development, the slowdown in construction and permitting constitute important trends that will infl u-ence apartment operations for the next several quarters. Beyond the effects of minimal completions during 2011, permitting fell to one of the lowest annual totals on record last year, assuring the construction cycle will not accelerate until late 2012. The gap in the cycle provides owners the oppor-tunity to leverage this year’s expected improvements in rental demand and tenant turnover into higher rents and reduced concessions on new leases. In areas where vacancy has already fallen well below the marketwide aver-age, such as the Carmel and North Pineville submarkets, rent growth will signifi cantly outpace the metrowide average.

After two years of subdued activity, improving fi nancing capacity, a large stock of new properties and prices below pre-recession levels will re-attract investors back to the metro in 2011. Initially, most buyers will con-centrate on assets located within the boundaries formed by interstates 85 and 485, along with areas with easy access to major employment nodes. As the year progresses, though, activity will shift gradually to more suburban areas as the recovery in property operations gains momentum. Assets in Gaston County and communities along the Interstate 77 and I-85 corridors north of the downtown area may offer considerable upside for investors skilled in operating suburban, garden-style properties.

2011 Market Outlook

◆ 2011 NAI Rank: 28, Up 1 Place. Charlotte remained near the middle of the index due to below-average rent growth and high vacancy.

◆ Employment Forecast: Employers will create 17,000 jobs in the metro this year, a 2.1 percent increase and up from 2010, when 10,300 new hires were made.

◆ Construction Forecast: Projects totaling 900 units will come online in 2011, down from 1,760 units last year.

◆ Vacancy Forecast: A decrease in construction and projected positive net absorption of 1,800 units will reduce the vacancy rate 100 basis points to 7.6 percent this year. Vacancy fell 270 basis points in 2010.

◆ Rent Forecast: Driven by signifi cant rent growth in low-vacancy areas such as the Harris Boulevard and East Charlotte submarkets, marketwide asking rents will rise 2.7 percent this year to $789 per month. Effective rents will increase 3.6 percent to $717 per month.

◆ Investment Forecast: Attractive investment opportunities will emerge in several potential high-growth areas of the metro as property operations strengthen. Complexes that serve the growing employment base at the North Carolina Research Park in Kannapolis, for example, will garner increased attention.

Reduced Construction Supports Operations,Draws Investors to Charlotte

CharlotteUp 1 Place 2011 Rank: 28 2010 Rank: 29

page 14 2011 Annual Report

* Estimate ** ForecastSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

Market Forecast Employment: 1.3% ▲ Construction: 1,720 ▼ Vacancy: 60 bps ▼ Effective Rents: 3.2% ▲

-240

-160

-80

0

80

Tota

l Non

farm

Job

s (t

hous

ands

)

Absolute Change Y-O-Y % Change

Employment Trends

08 09 10* 11**07

Year-over-Year Change

Uni

ts (

thou

sand

s)

Completions Vacancy

Supply and Demand

Vacancy Rate

$50

$60

$70

$80

$90

Med

ian

Pric

e pe

r U

nit

(tho

usan

ds)

Sales Trends

07 08 09 10*06

Year

-ove

r-Ye

ar C

hang

e

Asking Rents Effective Rents

Rent Trends

08 09 10* 11**07

0

1

2

3

4

08 09 10* 11**074%

5%

6%

7%

8%

-6%

-4%

-2%

0%

2%

-6%

-3%

0%

3%

6%

Operating conditions in the Chicago apartment market will strength-en considerably this year, building on improvements in vacancy and rents recorded in 2010. Apartment construction will sink to one of

the lowest levels in the past decade, minimizing competition for tenants at a time when renewed job growth will accelerate the formation of rental households. A 2 percent increase in fi nancial services and professional and business services employment will spur demand for apartments in higher-priced city submarkets such as the Gold Coast and the Loop. As vacancy in the city falls closer to the 5 percent threshold in 2011 , rent growth and a more rapid burn-off of concessions will commence in the second half. The performance of properties in inner-ring suburbs also will strengthen this year, as apartments in these areas draw both residents from outlying sections of the metro who desire housing closer to workplaces and those renters shut out of tighter in-city submarkets .

Driven by low interest rates and the expanded availability of acquisi-tion fi nancing, the investment market will gain momentum in 2011. Buyers will bid aggressively on high-quality properties in the city and fi rst-ring sub-urbs, encouraging an increasing number of owners to list assets. Cap rates fell across the market in 2010 but will likely remain near their current ranges through this year. High-quality assets in city locations often command fi rst-year returns of less than 6 percent, while noncore city assets and properties in the suburbs primarily trade from 6.5 percent to 8.0 percent based upon current operations. Distressed listings received considerable attention in 2010, but deals involving these assets will diminish as the year progresses and owners facing diffi culties begin to restore property operations.

2011 Market Outlook

◆ 2011 NAI Rank: 23, Down 3 Places. Chicago’s lagging employment mar-ket and modest rent growth dropped the metro three spots in the index.

◆ Employment Forecast: Expansion of the trade and professional and busi-ness services sectors will contribute signifi cantly to the creation of 52,500 jobs this year, a 1.3 percent increase in total employment. Approximately 20,000 positions were eliminated in 2010.

◆ Construction Forecast: Only 700 new rentals will come online in 2011, down considerably from the completion of 2,420 units last year.

◆ Vacancy Forecast: The metrowide vacancy rate will decrease 60 basis points this year to 5.5 percent on resurgent demand and minimal con-struction; vacancy also fell 60 basis points in 2010.

◆ Rent Forecast: Asking rents will rise 2.3 percent to $1,070 per month in 2011, following a 1.3 percent increase last year. Concessions will decline to 6.1 percent of asking rents as effective rents climb 3.2 percent to $1,005 per month; in 2010, effective rents advanced 2.4 percent.

◆ Investment Forecast: Investors seeking distressed assets will continue to fi nd opportunities on the southern and western sides of the city. Prospec-tive buyers will require a long-term outlook for rehabilitating properties, restoring stable operations and implementing rent increases.

Resurgent Demand BoostsOperations, Pressing Prices Upward

Chicago Down 3 Places 2011 Rank: 23 2010 Rank: 20

2011 Annual Report page 15

* Estimate ** ForecastSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

Major Development Projects GenerateJobs, Support Apartment Demand

CincinnatiDown 3 Places 2011 Rank: 33 2010 Rank: 30

Spurred by an economic recovery in the city core and marketwide job growth , apartment operations in Cincinnati will strengthen further in 2011. The fi rst phase of the mixed-use Banks development, located be-

tween the Great American Ballpark and Paul Brown Stadium on the Ohio River, will open in the second quarter of this year, expanding rental inven-tory in the Downtown submarket by 3 percent. Nevertheless, high-paying job growth in the area will outpace new supply. Metrowide, employers will add more than 5,600 positions in the professional and business services and education and health services sectors this year, boosting Class A demand near major employment centers. Operations at Class B/C complexes will also improve as employment gains rise in lower-paying industries. De-velopment of the Broadway Commons Casino, for instance, will generate 2,100 construction jobs during 2011 and 2,800 permanent positions by year-end 2012. As a result, vacancy will retreat to a 10-year low in Cincinnati.

Apartment sales activity in the metro will increase this year as local investors leave the sidelines and out-of-state syndicates explore new op-portunities. In the lower tiers, buyers will target older REO complexes with turnaround potential. Many of these properties were purchased by out-of-state investors at the height of the market and have since been foreclosed due to weakening operations and banks’ reluctance to refi nance. Two in-vestment strategies are emerging with these deals. Local buyers are pur-chasing at low per-door prices, addressing deferred maintenance issues and stabilizing the property for long-term revenue potential. Syndicates, however, are re-listing assets shortly after building and occupancy condi-tions improve. Top-tier investment activity remains focused on complexes in the Downtown and Blue Ash/Amberley submarkets due to their high barriers to entry and historically stable NOIs. Cap rates for assets in pre-mium locations currently average in the mid- to high-6 percent range and could compress further if institutions and REITs become active.

2011 Market Outlook

◆ 2011 NAI Rank: 33, Down 3 Places. Below-average job growth and high home affordability dropped Cincinnati three positions in this year’s NAI.

◆ Employment Forecast: Approximately 13,200 jobs will be added to the work force this year, a 1.3 percent increase. In 2010, employers created 700 positions.

◆ Construction Forecast: Following the completion of 350 units last year, developers will deliver 700 apartments in 2011.

◆ Vacancy Forecast: Vacancy will tick down 60 basis points this year to 6.3 percent. In 2010, the average vacancy rate retreated 110 basis points.

◆ Rent Forecast: Asking rents will increase 1.9 percent during 2011 to $715 per month, and effective rents will climb 2.4 percent to $683 per month.

◆ Investment Forecast: Financing standards in Cincinnati remain slightly more stringent than in some other markets , creating opportunities for cash-heavy investors to purchase quality assets in a relatively stable met-ro without competing with highly leveraged buyers.

-40

-20

0

20

40

Tota

l Non

farm

Job

s (t

hous

ands

)

Absolute Change Y-O-Y % Change

Employment Trends

08 09 10* 11**07

Year-over-Year Change

Uni

ts

Completions Vacancy

Supply and Demand

Vacancy Rate

$30

$32

$34

$36

$38

Med

ian

Pric

e pe

r U

nit

(tho

usan

ds)

Sales Trends

07 08 09 10*06

Year

-ove

r-Ye

ar C

hang

e

Asking Rents Effective Rents

Rent Trends

08 09 10* 11**07

0

250

500

750

1,000

08 09 10* 11**075%

6%

7%

8%

9%

-4%

-2%

0%

2%

4%

-4%

-2%

0%

2%

4%

Market Forecast Employment: 1.3% ▲ Construction: 350 ▲ Vacancy: 60 bps ▼ Effective Rents: 2.4% ▲

page 16 2011 Annual Report

* Estimate ** ForecastSources: Marcus & Millichap Research Services, CoStar Group, Inc., RCA

Market Forecast Employment: 1.1% ▲ Construction: 210 ▼ Vacancy: 40 bps ▼ Effective Rents: 2.2% ▲

-75

-50

-25

0

25

Tota

l Non

farm

Job

s (t

hous

ands

)

Absolute Change Y-O-Y % Change

Employment Trends

08 09 10* 11**07

Year-over-Year Change

Uni

ts

Completions Vacancy

Supply and Demand

Vacancy Rate