Embed Size (px)

Citation preview

2011

Consolidated annual report

Transparency

Simplicity

Accessibility

Good design

73Independent Auditor’s Report

136Contact andbranches

03Consolidatedgroup

05Basic economic indicators

08Report of the Board of Directorsof Equa bank a.s.

14Board of Directors of Equa bank a.s.

17Report of the Supervisory Board of Equa bank a.s.

75Report on relations between related parties

19Supervisory Board of Equa bank a.s.

80Audited non-consolidated financial statements of Equa bank a.s.

22Consolidated financial statements

134Organizational structure of Equa bank a.s.

Contents

Consolidated group

back to the contents

03

04Con

solid

ated

gro

up

Shares of Equa bank a.s. are not listed on any stock exchange.

Consolidating entity Consolidated entity

Equa bank a. s. Equa Financial Services s. r. o.

The sole shareholder

The registered office:

Lazarská 1718/3111 21 Praha 1(until February 29, 2012)

Karolinská 661/4186 00 Praha 8(from March 1, 2012)

The registered office:

Sokolovská 394/17180 00 Praha 8(until February 29, 2012)

Karolinská 661/4186 00 Praha 8(from March 1, 2012)

The registered office:

Banco Popolare Societá CooperativaVerona, Piazza Nogara 2Republic of Italy (until June 26, 2011)

Equa Group LimitedValletta, St Paul Street 259, VLT 1213 Republic of Malta(from June 27, 2011)

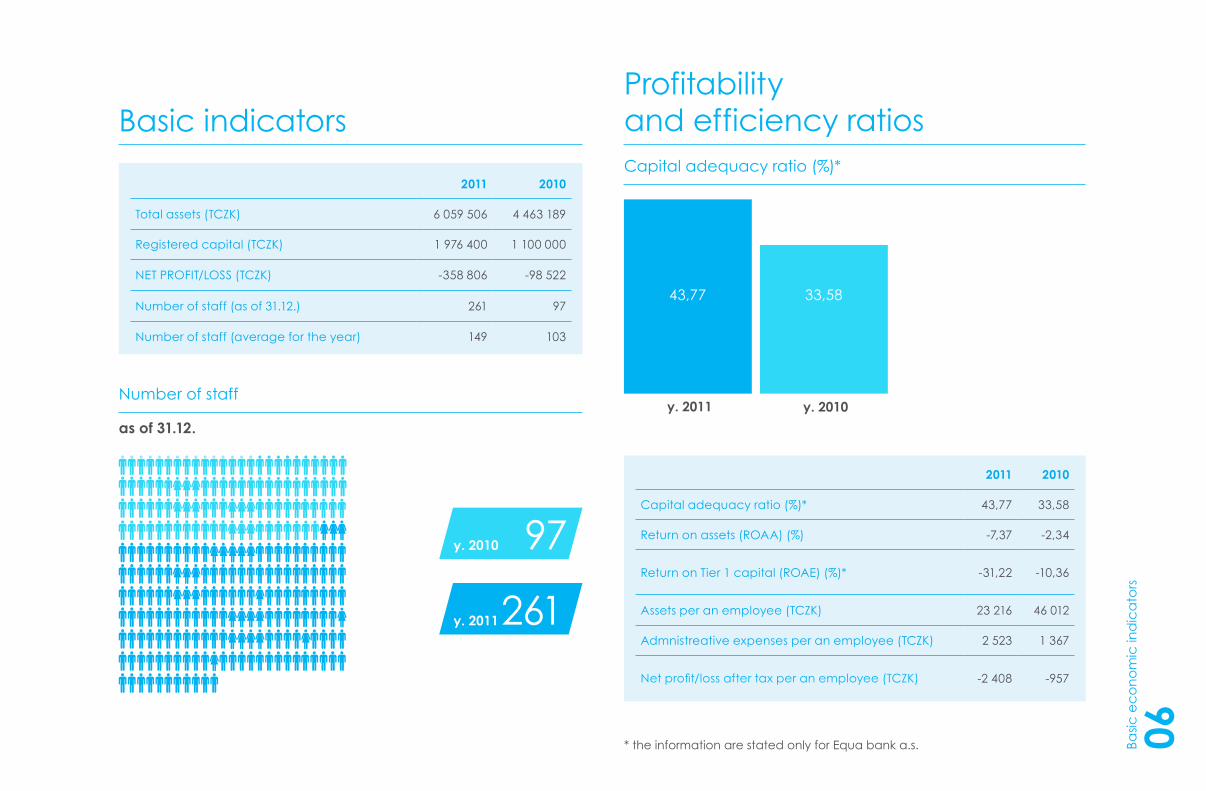

Basic economic indicators 05If not otherwise stated, the information are stated for consolidated group.

back to the contents

06Basic

eco

nom

ic in

dic

ator

s

Number of staff

Capital adequacy ratio (%)*

Basic indicators Profitabilityand efficiency ratios

as of 31.12.

2011 2010

Capital adequacy ratio (%)* 43,77 33,58

Return on assets (ROAA) (%) -7,37 -2,34

Return on Tier 1 capital (ROAE) (%)* -31,22 -10,36

Assets per an employee (TCZK) 23 216 46 012

Admnistreative expenses per an employee (TCZK) 2 523 1 367

Net profit/loss after tax per an employee (TCZK) -2 408 -957

y. 2011

261

97

y. 2011

y. 2010

y. 2010

43,77 33,58

* the information are stated only for Equa bank a.s.

2011 2010

Total assets (TCZK) 6 059 506 4 463 189

Registered capital (TCZK) 1 976 400 1 100 000

NET PROFIT/LOSS (TCZK) -358 806 -98 522

Number of staff (as of 31.12.) 261 97

Number of staff (average for the year) 149 103

07

Capital*

Capital requirements*

2011 2010

Total capital (TCZK) 1 456 511 935 652

out of which:

Tier 1 (TCZK) 1 456 511 935 652

2011 2010

Total capital requirements (TCZK) 266 190 222 933

out of which:

Capital requirement for credit risk according to the standardized approach (TCZK) 256 214 213 708

Capital requirement for operational risk (TCZK) 9 976 9 225

* the information are stated only for Equa bank a.s.

Basic

eco

nom

ic in

dic

ator

s

Report of the Board of Directors of Equa bank a.s. 08

back to the contents

09

Our vision Dear shareholders, associates, and valued clients,

We are very pleased with and proud of Equa bank, its staff and our accomplishments in 2011. On June 20th, 2011, our ownership changed and we became Equa bank. We immediately announced a new vision and rigorously transformed every aspect of the business to align to that vision – in 6 months, we took a small bank with limited products formerly owned by Banco Popolare, and transformed it into a complete retail bank with national reach and a vision for the future. Every element of the entire bank underwent some level of transformation, as I’ll explain in a moment.

All of our success we owe to our people. We started with 37 branch staff and a small central team, and added the best sales, service, and risk specialists we could find from over 10 different banks. With that said, what might make us the most proud is that we accom-plished our transformation without losing a single profitable client, or a critical employee, and without any operational failures or sys-tems issues.

This report explains our vision, our 2011 accomplishments, financial highlights, and articulates our key challenges for 2012.

We believe deeply in our motto of “simply better banking”. In fact, it is our vision. We strive to create a well-designed multi-channel retail bank which delivers both superior customer service and su-perior shareholder returns by levering best-in-class technologies and processes. This is as much as a vision as a necessity – customers demand unique propositions and efficiency, and they will only become clients of Equa bank if we deliver.

• For individuals, we offer an initial range of mortgages and everyday banking current and savings products. Each product has a strong unique proposition – for example, clients enjoy our ability to give an “honest offer” from our calculator during the 1st meeting and then stick to this offer upon confirming the client’s data. We can also re-finance client’s mortgages at another bank without a valuation in certain circumstances, among other innovations.

• For small and micro-businesses, our initial unique proposition is our flexibility. We have the tools to take into account all aspects of a borrower’s business and personal situation into our lending decisions, thus giving clients a greater ability to prudently borrow the capital they need for their businesses. Over time, our product offering will evolve as our systems evolve, and we look forward to revealing our new 2013 products later in 2012.

Repo

rt of

the

Boar

d o

f Dire

ctor

s of

Equ

a ba

nk a

.s.

10

We have a long-term goal to achieve 2% market share and become a top 10 bank in 5 years. In 2011, we took our 1st step with confidence and conviction, which is critical to execution in 2012 and beyond:

2011: Transform and launch “Equa bank” – completely new brand, system and products

2012: Expand capabilities and products, and prove the strategy2013: Achieve critical mass in all business lines2014: Achieve self-sustainability and accelerate growth

2011 - A Year of Transformation and Launch accomplishments On June 20th, 2011, change of control to new ownership was exe-cuted. Immediately, Equa bank rebranded all of its branches and materials within 3 working days.

Then on September 20th, the bank launched:

• new redesigned branches and modern mini-branches,

• new multi-currency and multi-lingual banking systems, based on proven international hardware and software solutions

• an innovative current account, with a multi-currency debit card

• a market-leading intuitive internet experience,

• smart phone application available on iPhone and Android, and call center channels

• a suite of savings and term deposit offerings

• a national marketing campaign, advertising our 2,3% p.a. savings product, free current account (for active clients) and simple fee structure

At the same time, Equa bank also acquired EUR 53.4 m of mort-gage receivables, selected carefully from the portfolio of Credit Funding a. s. a First Funding a. s. using the services of an inde-pendent 3rd party valuer. Then in late November, Equa’s new mortgage product was made available through our branches, and in early 2012, it was made available through brokers as well.

During any transformation, it is easy to allow people, processes and service to suffer. We avoided this trap. Our senior executives were particularly proud that:

Repo

rt of

the

Boar

d o

f Dire

ctor

s of

Equ

a ba

nk a

.s.

11

• Customer service was maintained or increased. Indeed, new systems can sometimes bring some inconvenience, but our overall net promoter score was 29, well above our target of 25 (net pro-moter score is a measure of propensity to recommend).

• Governance oversight, compliance and control increased dramatically. New AML monitoring processes were built into our systems and automated, and we grew both the size and quality of our compliance function and internal audit.

• Cost control was exemplary. Financial and regulatory reporting was implemented and integrated across both the legacy BankUp and the new FlexCube system.

• Risk oversight was very prudent. New and more strict policies were adopted at change of control, and against these policies, a post-acquisition review of the portfolio identified many oppor-tunities for improvements and better alignment of economic value generation and credit risk

• People were a priority. New organizational structures were adopted to align to the bank’s new priorities, affecting a large majority of employees. However, not a single key employee left during this time. In December, 91% of employees reported them-selves as being happy or very happy to work at Equa bank, which exceeded our expectations.

Our only blemish in 2011 was that we could not meet expectations to launch our new mortgage offering sooner, which may not be surprising considering the complexity of managing both a transfor-mation and the launch of a redesigned bank. We are pleased however that when the product was launched, we exceeded the expectations of our broker partners and clients with our speed of decision making and the transparency of our processes.

Financial Highlights Financial commentary is within this report, though it is worth high-lighting a few facts here:

• Our bank is sound and well-capitalized. We finished the year with a Tier 1 ratio of 44% and a liquidity ratio of 42%.

• We grew our deposits by 63% from June 20th to the end of year, and with the acquisition of mortgage receivables portfolios, we grew our loan portfolio by 44% during the same period.

• Investment levels were high in 2011, due to the need to invest

early in both a new and complete banking system, and to ensure full regulatory compliance and well-functioning controls. How-ever, capital expenditures were kept under plan.

Repo

rt of

the

Boar

d o

f Dire

ctor

s of

Equ

a ba

nk a

.s.

12

• Loss provisions were higher than expected, entirely due to the effect of changes in the bank’s risk and credit documentation policies to better align to higher standards of prudency. These changes affected provision levels related to the legacy portfolio of Banco Popolare. These provisions were prudently taken, and there is a potential that should performance of the portfolio im-prove, that these could be decreased at that time.

Challenges in 2012 Our priority in 2012 will be to complete our development and transformation work:

• New products will be launched, such as cash loans in Q3 and business products in Q4

• New functionality will be added, including but not limited to automated approval systems and more treasury functionality

• Customer migration from the old BankUp system to the new Flexcube system will continue, so that the BankUp system can be shut-down in mid-2013

At the same time, we face two external challenges:

1. Change in the competitive environment. There has been a steady downward trend in mortgage prices over the past several years.At the same time, new entrants and those banks seeking liquidity have raised deposit rates. Equa bank’s response to the margin squeeze is to skew our business mix more toward higher ROI mort-gages and business lending at the moment.

2. The sovereign debt crisis. The crisis generated a peak of anxiety in 2011, though this anxiety level is lower at the time of writing this letter. Despite the recent calm, the implementation of reforms have yet to be completed in several countries in addition to Greece, namely Spain and Italy, and the outcome of austerity strategies are not yet clear. Should the effect of the continuing sovereign debt crisis worsen or spread, the Czech banking market could be affected.

Repo

rt of

the

Boar

d o

f Dire

ctor

s of

Equ

a ba

nk a

.s.

13

In summary, we are proud to have accomplished so much in 2011. We are excited to have unique branding and propositions, modern systems and processes, and a growing customer base. We under-stand the challenges of the market and while these are substantial, we believe we can meet such challenges and execute in 2012 with confidence and a motivated team.

Closing comment

Repo

rt of

the

Boar

d o

f Dire

ctor

s of

Equ

a ba

nk a

.s.

Radek Pluhař Ondřej MoravecCRO COOMember of the Member of the Board Board of Directors Board of Directors

Leoš Pýtr David Putts CEO,Chairman of the Member of theof Directors Board of Directors

Board of Directors of Equa bank a.s. 14

back to the contents

15Boar

d o

f Dire

ctor

s of E

qua

bank

a.s.

Ing. Leoš PýtrChairman of the Board since November 3, 2008

(born on December 17, 1955,

29 years of practice in banking)

Ing. Radek PluhařMember of the Boardsince June 27, 2011, CRO(born on July 27, 1976,

13 years of practice in banking)

David PuttsMember of the Boardsince June 20, 2011, CEO

(born on February 23, 1966, 21 years of practice

in banking and advisory in financial sector)

Ondřej MoravecMember of the Boardsince August 25, 2011, COO

(born on November 10, 1975, 14 years of practice

in banking and advisory in financial sector)

Board of Directors As at 31 December 2011:

16

Sergio ResegottiMember of the Board since November 14, 2007 until June 20, 2011

Ing. Tomáš HalousekMember of the Board since August 29, 2008 until June 20, 2011

The Czech National Bank has assessed the competence, trustwor-thiness and experience of the above mentioned members of the Board of Directors and approved their appointment.

No member of the Board of Directors is a statutory body or a member of a statutory body or a member of a supervisory board of any other legal entity, except for Mr. Ondřej Moravec who is an executive of company Equa Financial Services s.r.o., which is a service com-pany for the Bank.

Changes during 2011

Boar

d o

f Dire

ctor

s of E

qua

bank

a.s.

Report of the SupervisoryBoard of Equa bank a. s. 17

back to the contents

18Repo

rt of

the

Supe

rviso

ry B

oard

of

Equ

a ba

nk a

. s.

The Supervisory Board has fulfilled in 2011 its task accordance with the valid laws of the Czech Republic, the Articles of Association of Equa bank a.s. (the "Bank") and its Rules of Procedure. The Board of Directors of the Bank has duly provided all data and information necessary for the task of verifying the Bank’s results in timely manner. In this way, the Supervisory Board was fully informed on all important activities undertaken by the Bank during 2011.

The Board of Directors submittes to the Supervisory Board the Bank’s financial statement as of December 31, 2011 verified by the audit company KPMG Česká republika Audit, s.r.o. Having reviewed it the Supervisory Board expressed its approval of the Bank’s annual financial statements for 2011 and recommended that the sole shareholder acting in the capacity of the Shareholders’ Meeting approves the same. Furthermore, the Supervisory Board stated that the Bank’s business activities were conducted in accordance with the applicable legal regulations and Bank’s statutes.

The Board of Directors submitted to the Supervisory Board written Report on relations between the related entities for the year ended December 31, 2011. The Supervisory Board reviewed the Report on relations in accordance with the Section 66a (9) of the Act No. 513/1991 Coll., Commercial Code.

Prague, April 25, 2012

Peter Bramwell Cartwright Chairman of the Suervisory Board

Supervisory Board of Equa bank a. s. 19

back to the contents

20Supe

rviso

ry B

oard

of E

qua

bank

a. s

.

Peter Bramwell CartwrightChairman of Supervisory Board since June 29, 2011, Member of the Supervisory Board since June 20, 2011 (born on December 16, 1965, 28 years of practice in banking and financial sector)

Stephen PulleyMember of the Supervisory Board since June 29, 2011, Chairman of Supervisory Board since June 20, 2011 till June 29, 2011 (born on March 29, 1982, 9 years of practice in banking and financial sector)

JUDr. Jan KittrichMember of the Supervisory Board since September 20, 2011 (born on May 7, 1976, 9 years of practice in banking and legal advisory)

Mr. Peter Bramwell Cartwright was appointed the Chairman of the Supervisory Board on June 29, 2011. This change will be filed in the Commercial Register in the second quarter of 2012.

Giuseppe MalerbiChairman of the Supervisory Board since July 28, 2009 until June 20, 2011

Lorenzo ChiappiniMember of the Supervisory Board since May 14, 2007 until Febru-ary 22, 2011

Ing. Martin HoudaMember of the Supervisory Board since August 4, 2009 until Septem-ber 7, 2011

As at Changes 31 December 2011 during 2011

21

Mr. Peter Bramwell Cartwright is further active in the following entities:

• Anacap Financial Partners LLP – Designated Member

• Base Commercial Mortgages Holdings Limited – Director

• Apex Credit Management Holdings Limited – Director

• AC Acquisitions Limited – Director

• Aldermore Bank Nominees Limited – Director

• Aldermore Bank plc – Director

• Aldermore Holdings Limited – Director

• Cabot Financial Group Limited – Director

• Equa Group Limited – Director

• Equa Holdings Limited – Director

• Medifin Holding Limited – Director

• Mediterranean Bank plc – Director

• Pall Mall Finance Limited – Director

Mr. Stephen Pulley is further active in the following entities:

• Anacap Financial Partners LLP – Member

Supe

rviso

ry B

oard

of E

qua

bank

a. s

.

Consolidated financial statements 22

back to the contents

23Con

solid

ated

fina

ncia

l sta

tem

ents

Consolidated balance sheet As at 31.12.2011

The data is stated in TCZKItem No ASSETS Note Current period Past period

31.12.2011 31.12.20101 Cash in hand and balances with central banks 142 073 481 1123 Receivables from banks and cooperative savings associations 10 2 476 955 1 875 874 of which: a) repayable on demand 330 024 1 192 807 b) other receivables 2 146 931 683 0674 Receivables from customers – cooperative savings association's members 11 2 846 622 2 070 012 of which: a) repayable on demand 111 225 239 742 b) other receivables 2 735 397 1 830 2709 Intangible fixed assets 12 321 531 2 930 of which: b) goodwill -5 966 010 Tangible fixed assets 13 106 488 21 169 of which: land and buildings for operating activities 42 794 12 43111 Other assets 14 148 152 7 69313 Prepaid expenses and accrued income 17 685 4 399 TOTAL ASSETS 6 059 506 4 463 189

Company name: Equa bank a.s.Registered office: Lazarská 1718/3, Praha 1 Identification number: 47116102 Date of preparation of financial statements: 25/4/2012

24

Consolidated balance sheet As at 31.12.2011

The data is stated in TCZKItem No. LIABILITIES Note Current period Past period

31.12.2011 31.12.20101 Due to banks and cooperative savings associations 15 0 120 376 of which: b) ostatní závazky 0 120 3762 Due to customers – cooperative savings association´s members 16 4 475 707 3 380 220 of which: a) repayable on demand 1 715 935 647 542 b) other payables 2 759 772 2 732 6784 Other liabilities 17 118 648 22 7035 Deferred income and accrued expenses 2 513 06 Provisions 19 6 446 1 308 of which: c) other 6 446 1 3088 Registered capital 20 1 976 400 1 100 000 of which: a) registered paid up capital 1 976 400 1 100 0009 Share premium 16 010 Reserve funds and other funds from profit 25 805 25 805 of which: a) statutory reserve funds and risk funds 25 805 25 80514 Retained earnings (or accumulated losses) from previous years -187 223 -88 70115 Profit (loss) for the accounting period -358 806 -98 522

TOTAL LIABILITIES 58 6 059 506 4 463 189

Con

solid

ated

fina

ncia

l sta

tem

ents

25Con

solid

ated

fina

ncia

l sta

tem

ents

Company name: Equa bank a.s.Registered office: Lazarská 1718/3, Praha 1 Identification number: 47116102 Date of preparation of financial statements: 25/4/2012

The data is stated in TCZKItem No. OFF-BALANCE SHEET ASSETS Note Current period Past period

31.12.2011 31.12.20101 Commitments and guarantees granted 22 277 453 407 4072 Collaterals granted 0 29 1103 Receivables from spot transactions 22b 1 170 3 8894 Receivables from fixed term transactions 22b 179 986 06 Receivables written-off 2 324 2 362

TOTAL OFF-BALANCE SHEET ASSETS 460 933 442 768

The data is stated in TCZKItem No. OFF-BALANCE SHEET LIABILITIES Note Current period Past period

31.12.2011 31.12.20109 Commitments and guarantees received 16 171 519 93610 Collaterals and pledges received 4 356 635 1 794 57911 Payables from spot transactions 22b 1 177 3 88412 Payables from fixed term transactions 22b 180 664 014 Values taken into custody, administration and deposit 23 6 208 4 206 TOTAL OFF-BALANCE SHEET LIABILITIES 4 560 855 2 322 605

Consolidated off-balance sheet As at 31.12.2011

26Con

solid

ated

fina

ncia

l sta

tem

ents

Company name: Equa bank a.s.Registered office: Lazarská 1718/3, Praha 1 Identification number: 47116102 Date of preparation of financial statements: 25/4/2012 Consolidated income statement

for the year 2011

The data is stated in TCZKItem No. Note Current period Past period

31.12.2011 31.12.20101 Interest income and similar income 3 118 387 109 8422 Interest expense and similar expense 3 -68 411 -63 1754 Commission and fee income 4 10 173 7 2105 Commission and fee expense 4 -4 288 -4 4236 Gain or loss from financial operations 5 3 088 5 5077 Other operating income 6 2 453 6158 Other operating expenses 6 -7 962 -4 3529 Administrative expenses 7 -375 883 -140 783 of which: a) employee expenses -171 640 -81 483 of which: aa) social and health insurance -37 675 -17 290 b) other administrative expenses -204 243 -59 300

11 Depreciation, creation and use of reserves and adjustments to tangible and intangible fixed assets -23 035 -7 049

12 Release of adjustments and provisions for receivables and guarantees,income from written-off receivables 18b 9 501 63

13 Write-offs, creation and use of adjustments and provisions for receivable and guarantees 18c -121 214 -2 189

17 Creation and use of other provisions -5 138 21219 Current year profit (loss) from ordinary activities before tax -462 329 -98 52223 Income tax 21 103 523 024 Net profit (loss) for the accounting period -358 806 -98 522

27

Consolidated statement of changes in equity for the year 2011

Company name: Equa bank a.s.Registered office: Lazarská 1718/3, Praha 1 Identification number: 47116102 Date of preparation of financial statements: 25/4/2012

Con

solid

ated

fina

ncia

l sta

tem

ents

The data is stated in TCZK

Registered capital Share premium Reserve Profit (loss) Total

Balance as at 1/1/2010 1 000 000 0 25 805 -88 701 937 104

Net profit (loss) for accounting period 0 0 0 -98 522 -98 522

Increase in registered capital 100 000 0 0 0 100 000

Balance as at 31/12/2010 1 100 000 0 25 805 -187 223 938 582

Balance as at 1/1/2011 1 100 000 0 25 805 -187 223 938 582

Net profit (loss) for accounting period 0 0 0 -358 806 -358 806

Increase in registered capital 876 400 16 0 0 876 416

Balance as at 31/12/2011 1 976 400 16 25 805 -546 029 1 456 192

28

1. Basic information (a) Description and principal activities of the Bank as the consoli-dating entity

Establishment and description of the Bank

The consolidating entity Equa bank a.s. (“the Bank” or “the consolidating entity”) was incorporated and registered in the Commercial Register on 6 January 1993 as IC Banka, a.s., which initiated its business activity in April 1994.

In May 2007 IC Banka, a.s. was taken over by the Italian banking group Banco Popolare, and on 10 September 2007 was renamed to Banco Popolare Česká republika, a.s.

In June 2011 the Bank was taken over by Equa Group Limited, with its registered office at Valletta, St Paul Street 259, VLT 1213, Republic of Malta, which is the Bank’s sole shareholder. The Bank was sub-sequently renamed to Equa bank a.s. on 27 June 2011.

The principal activities of the Bank are retail and corporate banking.

Company name and registered office:

Equa bank a. s.Lazarská 1718/3111 21 Praha 1 Czech Republic

From 1 March 2012 the Bank’s registered office is Karolinská 661/4, 186 00 Prague 8.

Identification number:

47116102

Equa bank a.s.Notes to the Czech statutory financial statements (consolidated, translated from the Czech original)Year ended 31 December 2011

Con

solid

ated

fina

ncia

l sta

tem

ents

29

Members of the board of directors and supervisory board

Members of the board of directors

Members of the supervisory board

Changes in the board of directors and supervisory board in the accounting period

In 2011, the following changes were made:

Board of directors

● on 20 June 2011 Sergio Resegotti and Tomáš Halousek terminated their membership in the board of directors,

● on 20 June 2011 David Putts was appointed as a member of the board of directors,

● on 27 June 2011 Radek Pluhař was appointed as a member of the board of directors,

● on 25 August 2011 Ondřej Moravec was appointed as a member of the board of directors.

as at 31 December 2011

Con

solid

ated

fina

ncia

l sta

tem

ents

Peter Bramwell Cartwright (Chairman)

Stephen Pulley JUDr. Jan Kittrich

Ing. Leoš Pýtr(Chairman) David Putts

Ing. Radek Pluhař Ondřej Moravec

30

Basic information

(a) Description and principal activities of the Bank as the consolidating entity (continued)

Supervisory board

● on 22 February 2011 Lorenzo Chiappini was removed from the supervisory board,

● on 20 June 2011 Giuseppe Malerbi terminated his membership in the supervisory board,

● on 20 June 2011 Stephen Pulley was elected as the Chairman of the supervisory board and Peter Bramwell Cartwright as a mem-ber of the supervisory board,

● on 29 June 2011 Peter Bramwell Cartwright was elected as the Chairman of supervisory board and Stephen Pulley was elected as a member of the supervisory board. The change in the com-mercial register will be made in the second quarter of 2012 together with registration of new members of board of directors.

● on 7 September 2011 Ing. Martin Houda terminated his membership in the supervisory board,

● on 20 September 2011 Jan Kittrich was elected as a member of the supervisory board.

In 2012 the following changes were made:

Board of directors

● on 3 April 2012 Ing. Monika Kristková and Petr Řehák were appointed as members of the board of directors.

Organisational structure of the Bank

The internal organisational and management structure respects the regulatory requirements for segregation of duties. In the course of 2011, the Bank’s organisational and management structure was continuously adjusted to changes connected with the new goals and the new strategy of the Bank. All changes were considered and implemented taking into account compliance with the internal standards set by the internal management and control system, and taking into account regulatory requirements as stipulated by Decree No. 123/2007 Coll., on the prudential rules for banks, savings and credit unions, and security brokers, as amended.

continued

Con

solid

ated

fina

ncia

l sta

tem

ents

31

The Bank’s organisational structure consists of separate organisa-tional units arranged in a linear management structure. It comprises divisions managed by individual members of the board of directors; divisions are further divided into organisational units. The organi-sational structure includes bank branches, financial centres and “mini branches”.

Pursuant to Act No. 21/1992 Coll., on Banks, as amended, internal audit department has a special position within the Bank’s organisa-tional structure. Internal audit carries out its activity independently and reports directly to the Bank’s s board of directors.

(b) Description and principal activities of the Subsidiary as the consolidated entity

Establishment and description of the Subsidiary

Equa Financial Services s.r.o. (“EFS” or “the Subsidiary”) was incor-porated by registration in the Commercial Register as PLEIONE s.r.o. on 30 December 2008. Its principal activities are the development of banking infrastructure and provision out outsourcing services and banking infrastructure to the parent company.

The sole owner of EFS is Equa bank a.s., the consolidating entity.

Description and principal activities of the Subsidiary as the consolidated entity (continued)

Company name and registered office

Equa Financial Services s.r.o. Karolinská 661/4186 00 Praha 8Czech Republic

Identification number

28509099

Statutory body of the Subsidiary as at 31 December 2011

Ondřej Moravec (statutory representative)

Con

solid

ated

fina

ncia

l sta

tem

ents

32

(c) Description of the consolidated group

The consolidated group (“the Group”) as at 31 December 2011 comprises Equa bank a.s. together with Equa Financial services s.r.o.

The consolidated group came into being on 20 July 2011, when the Bank purchased a 100% share in EFS.

(d) Basis of preparation

The consolidated financial statements have been prepared on the basis of accounting maintained in accordance with:

● Act No. 563/1991 Coll. on Accounting, as amended,

● Decree No. 501/2002 Coll., implementing certain provisions of Act No. 563/1991 Coll., on Accounting, as amended, for banks and other financial institutions,

● Czech Accounting Standards for financial institutions.

These consolidated financial statements have been prepared using the full consolidation method, and include the balance sheet, profit and loss account, statement of changes in equity and notes to financial statements containing description of accounting policies adopted and explanatory comments.

The financial statements have been prepared on an accrual basis, meaning that transactions have been presented in the financial statements in the period to which they relate in terms of substance and time, and on a going concern basis.

The financial statements have been prepared under the historical cost convention, except for selected financial instruments that are stated at fair value.

All amounts are in thousands of Czech crowns (TCZK), unless otherwise stated. Numbers in brackets represent negative amounts.

As the consolidated group came into being in the course of the accounting period, some current period data of the financial statements are not comparable to those of the prior period. The prior period data in the balance sheet and the profit and loss account only concern the consolidating entity.

Con

solid

ated

fina

ncia

l sta

tem

ents

33

2. Significant accounting policies The significant accounting policies adopted in the preparation of the consolidated financial statements are set out below:

(a) Transaction date

Depending on the type of transaction, the transaction date is de-fined as the date of payment or collection of cash; the date of pur-chasing or selling of foreign currency or securities; date of payment or collection from a customer's account; date of order to a cor-respondent to make a payment, settlement date of the bank’s payment orders with the CNB clearing centre, the value date ac-cording to a statement received from a bank’s correspondent (statement means SWIFT statement, bank’s notice, received media, bank statement or other documents); the trade date and settlement date of transactions with securities, foreign currency, options or other derivatives; the date of issue or receipt of a guarantee or opening credit commitment; the date of acceptance of values into custody.

Accounting transactions involving the purchase or sale of financial assets with a usual term of delivery (spot transactions), as well as fixed term and option contracts, are recorded in off-balance sheet ac-counts from the trade date until the settlement date. Where financial assets that are classified in portfolios subsequently measured at fair value are involved, the financial assets are revaluated starting from the purchase trade date to the sale trade date.

A financial asset or its part is derecognised from the balance sheet if the entity loses control over the contractual rights to the asset in whole or in part. The entity loses this control if it exercises the rights to the benefits defined in the contract, if these rights expire, or if these rights are waived by the Bank.

Financial liabilities are recognised in the balance sheet at the mo-ment the entity becomes a party to a contractual arrangement regarding the financial instrument, and derecognised at the time the liability terminates, i.e. when the obligation defined by the con-tract is discharged or cancelled, or when it expires.

(b) Recognition of income and expenses

Interest income and expense on interest-bearing financial instru-ments are recognised in the profit and loss account on an accrual basis, in “Interest income and similar income” or “Interest expense and similar expense”.

Fees and commissions directly related to granting a loan are accrued over the term of the loan. Other fees and commissions are recognised as an income in the period when the services are provided. Fees and commissions are presented in “Commission and fee income”.

Con

solid

ated

fina

ncia

l sta

tem

ents

34

Realised and unrealised gains and losses from derivatives, FX transactions and translation of assets and liabilities in foreign cur-rencies are recognised in “Gain or loss from financial operations”.

(c) Reverse repo transactions Transactions where securities are purchased under a commitment to resell (resale commitment) are treated as collateralised lending transactions.

Securities (such as treasury bills) received as a collateral to loans provided within reverse repo transactions are recorded in the off-balance sheet as “Collaterals and pledges received” and are re-measured at fair value in the off-balance sheet. The amount of the loan provided is recognised as “Due to banks and cooperative savings associations”.

Income arising from resale commitments as the difference between the selling and purchase price is accrued over the period of the transaction and charged to the profit and loss account as “Interest income and similar income”.

(d) Receivables from banks and customers

Receivables are carried at cost reduced by any impairment loss. Accrued interest income is part of the carrying amount of receiv-ables.

Receivables are reviewed for recoverability, which is the basis for determining the impairment loss in respect of individual receivables. Unless the Bank writes off the portion of receivables corresponding to the impairment loss, an adjustment is created for that portion of receivables. The method of creating adjustments in the appro-priate accounting period is described in note 25. Adjustments created by debiting expenses are reported under “Write-offs, creation and use of adjustments and provisions for receivables and guarantees”.

The Bank also accrues interest income from risky receivables. Adjustments to accrued interest income are established, at 100% in accordance with Decree No. 123/2007 Coll., on the prudential rules of banks, savings and credit unions, and security brokers.

Con

solid

ated

fina

ncia

l sta

tem

ents

35

● a present obligation (legal or constructive) exists as a result of a past event,

● it is probable or certain that an outflow of economic benefits will be required to settle the obligation (“probable” means a prob-ability exceeding 50%), and

● the amount of the obligation can be estimated reliably.

(f) Tangible and intangible fixed assets

Tangible and intangible fixed assets are stated at historical cost and are depreciated on a straight-line basis over their estimated useful lives.

The depreciation period for each category of tangible and intan-gible fixed assets is as follows:

Software 4–8 years

Goodwill 5–6 years

Buildings and land 50 years

Fixtures and fittings 5–10 years

Equipment 3–5 years

The adjustments are recorded in sub-ledger accounts for the purpose of determining the income tax liability. The tax deductible portion of total adjustments created in the accounting period for credit losses is calculated in accordance with the requirements of Section 5 (“Banking reserves and adjustments”) and Section 8 (“Adjustments to receivables from debtors”) of Act No. 593/1992 Coll., on Reserves, as amended.

Receivables are written off based on an individual assessment and decision of the Credit Risk Committee, taking into account the number of days past due, the financial position and legal background.

The write-off of unrecoverable receivables is accounted for as “Write-offs, creation and use of adjustments and provisions for re-ceivables and guarantees” in the profit and loss account. If a fully adjusted receivable is written off, the adjustments are reduced by an amount equal to the amount written off in the same account in the profit and loss account. Recoveries of loans previously written off are included in the profit and loss account in “Release of adjust-ments and provisions for receivables and guarantees, income from written-off receivables”.

(e) Creation of provisions

A provision represents a probable cash outflow of uncertain timing or amount. Provisions are created if the following criteria are met:

Con

solid

ated

fina

ncia

l sta

tem

ents

36

Leasehold improvements are depreciated on a straight-line basis over the shorter of the lease term or their remaining useful lives.

The following low-value assets are recorded under fixed assets and depreciated in the period in which they are acquired:

● low-value intangible assets costing more than TCZK 20 and less then TCZK 60,

● low-value tangible assets costing more than TCZK 20 and less then TCZK 40, or

● low-value tangible and intangible assets of any acquisition cost with an expected useful life of more than one year.

Intangible fixed assets costing less than TCZK 20 and tangible fixed assets costing less than TCZK 20 with useful lives of less than one year are charged to the profit and loss account in the period in which they are acquired.

(g) Foreign currency translation

Upon initial recognition, transactions realised in foreign currencies are translated to Czech currency using the Czech National Bank (“CNB”) exchange rate for the respective foreign currency. As at the balance sheet date, items expressed in foreign currency are translated, depending on the nature of the item, as follows:

● monetary assets and liabilities in foreign currency are translated using the CNB exchange rate published on the balance sheet date;

● non-monetary assets and liabilities at historical cost expressed in foreign currency are translated to Czech currency using the historical CNB exchange rate published on the date of the transaction;

● non-monetary assets and liabilities at fair value expressed in foreign currency are translated to Czech currency using the current CNB exchange rate published on the date of fair value measurement.

Foreign exchange gains or losses arising from the translation of foreign currency assets and liabilities are recognised in the profit and loss account as “Gain or loss from financial operations”.

Con

solid

ated

fina

ncia

l sta

tem

ents

37

(h) Financial derivatives

A derivative as a financial instrument or other contract with the following three characteristics:

● its value changes in response to the change in a specified interest rate, financial instrument price, commodity price, foreign exchange rate, index of prices or rates, credit rating, market prices of securities or similar market parameters;

● it requires no initial investment or an initial investment that is smaller than would be required for other types of contracts that would be expected to have a similar response to changes in market factors, and

● it is settled at a future date.

Financial derivatives held for trading are initially recognised in the balance sheet at cost, and subsequently measured at fair value. Gains (losses) from changes in fair value are recorded in the profit and loss account in “Gain or loss from financial operations”.

Although the vast majority of the Bank’s financial derivatives are held for hedging purposes, they do not meet the conditions for hedge accounting; therefore all derivatives are classified as trading derivatives.

(i) Taxation

Tax non-deductible expenses are added to, and non-taxable income is deducted from, the profit for the period to arrive at the taxable income, which is further adjusted by tax allowances and relevant credits.

Deferred tax is provided on all temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes multiplied by the income tax rate expected to be valid for the next period. A deferred tax asset is recognised only if there are no doubts that it will be utilised in future accounting periods.

Con

solid

ated

fina

ncia

l sta

tem

ents

38

3. Net interest income

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010

Interest income and similar income

from loans 89 157 97 707

from deposits 28 330 12 135

From reverse repo transactions with the CNB 900 -

Total 118 387 109 842

Interest expense and similar income

from deposits 68 106 63 175

from loans 305 -

Total 68 411 63 175

Net interest income 49 976 46 667

39

4. Fees and commissions

5. Gain or lossfrom financial operations

TCZK 2011 2010

Gain/(loss) from derivatives transactions (5 492) -

Gain/(loss) from foreign exchange trans- (2 791) 5 831

Foreign exchange gain/(loss) 11 443 (324)

Other (72) -

Total 3 088 5 507

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010

Commission and fee income from

payments and account maintenance 4 555 4 017

foreign exchange operations 129 165

lending 5 368 2 529

other 121 499

Total 10 173 7 210

Commission and fee expense 4 288 4 423

Total 4 288 4 423

40

6. Other operating incomeand expenses

7. Administrative expenses

TCZK 2011 2010Wages and salaries paid to employees 132 521 64 055Social security and health insurance 37 675 17 290Other employee expenses 1 444 138of which:Wages and salaries paid to:

members of the board of directors and other executives 26 044 19 165

members of the supervisory board 2 885 2 003Total employee expenses 171 640 81 483

Other administrative expenses 204 243 59 300of which: expenses for audit, legal and tax advisory 15 383 2 438

Total 375 883 140 783

The average number of the Group’s employees was as follows:

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010Operating income

Income from sale of tangible fixed assets 522 239

Other income 1 931 376Total 2 453 615

Operating expensesContribution to the deposit insurance fund 5 048 3 686

Costs to sell tangible fixed assets 2 243 279Other expenses 671 387

Total 7 962 4 352

2011 2010Employees 141 96Members of the board of directors and other executives 5 4

Members of the supervisory board 3 3Total 149 103

41Con

solid

ated

fina

ncia

l sta

tem

ents

8. Income and expense by operating segment (a) Business segments

(b) Geographical segments

RetailBanking

Corporate Banking Other Total

TCZK 2011 2010 2011 2010 2011 2010 2011 2010Interest income and similar income 20 288 3 906 82 065 91 060 16 034 14 876 118 387 109 842Interest expense and similar expense (51 524) (46 417) (16 887) (16 758) - - (68 411) (63 175)Commission and fee income 5 210 3 692 4 935 3 498 28 20 10 173 7 210Commission and fee expense - - - - (4 288) (4 423) (4 288) (4 423)Gain or loss from financial operations - - - - 3 088 5 507 3 088 5 507

Czech Republic

EuropeanUnion Other Total

TCZK 2011 2010 2011 2010 2011 2010 2011 2010Interest income and similar income 117 468 108 989 919 853 - - 118 387 109 842Interest expense and similar expense (63 503) (58 643) (4 873) (4 500) (35) (32) (68 411) (63 175)Commission and fee income 10 111 7 166 60 42 2 2 10 173 7 210Commission and fee expense (3 460) (3 733) (828) (690) - - (4 288) (4 423)Gain or loss from financial operations 3 088 5 507 - - - - 3 088 5 507

42

9. Transactions with related parties

The table includes all transactions with related parties. Additional information on transactions with persons with a special relationship to the Group is disclosed in notes 11 (e), 16 (b).

TCZK 2011 2010

Receivables 700 459 864

Payables 61 527 82 626

Income 1 221 1 011

Expense 23 090 14 373

10. Receivables from banks Classification of receivables from banks

TCZK 2011 2010

Reverse repo transactions with the CNB 2 100 340 -

Term deposits 353 109 1 874 571

Nostro accounts 3 637 1 303

EFS’s current accounts 19 869 -

Receivables from banks 2 476 955 1 875 874

Con

solid

ated

fina

ncia

l sta

tem

ents

43

11. Receivables from customers (a) Classification of receivables from customers

In the second half of 2011 the Bank purchased mortgage loans from related parties in four tranches, costing a total of TCZK 1 357 865. The cost of individual loans purchased was determined based on expert appraisals. On the date of acquisition, individual loans purchased were recognised at cost, which might differ

from the nominal value of the loans purchased, by the respective discount or premium.

The increase in individual adjustments is related to the original port-folio of Banco Popolare Česká republika, a.s.

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010

Standard 2 257 738 1 942 334

Watch 143 548 90 269

Substandard 332 850 49 599

Doubtful 181 789 2

Loss 80 209 25 621

Individual adjustment to receivables from customers (146 868) (25 725)

Total 2 849 266 2 082 100

Portfolio adjustment to receivables from customers (2 644) (12 088)

Net receivables from customers 2 846 622 2 070 012

44

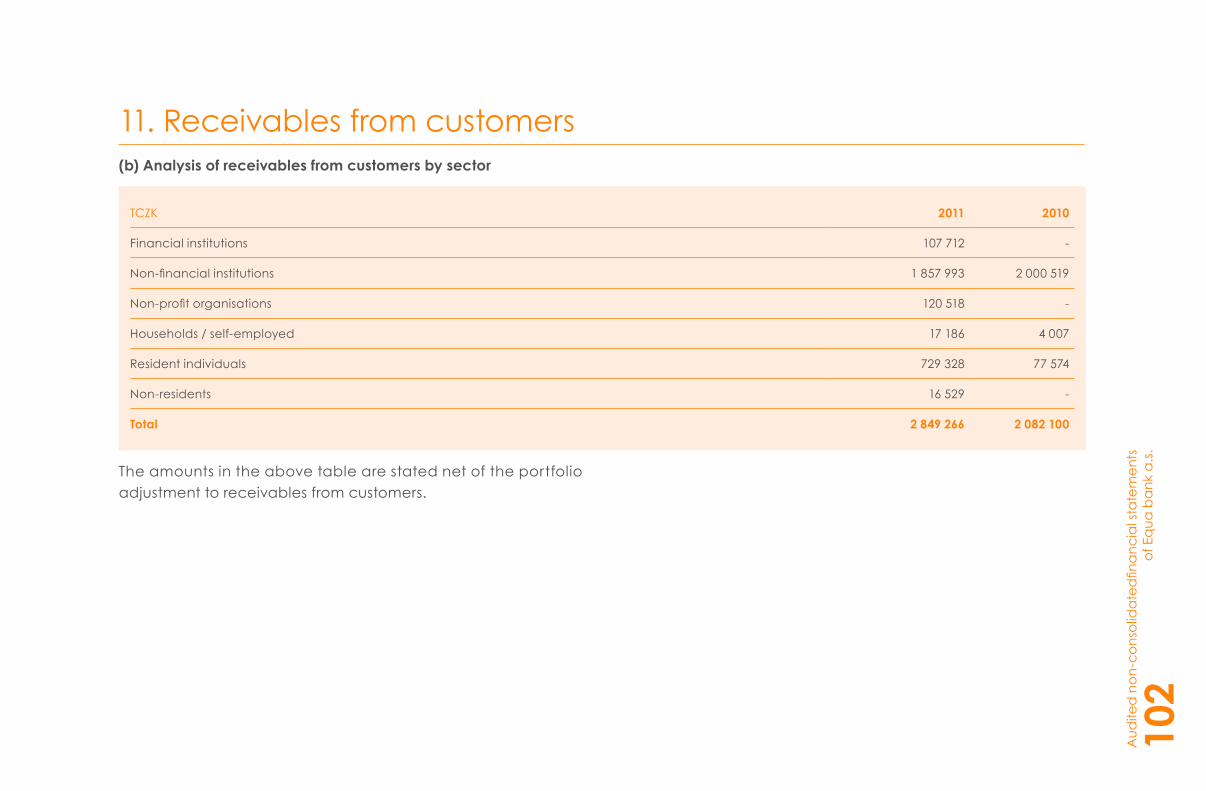

11. Receivables from customers (b) Analysis of receivables from customers by sector

The amounts in the above table are stated net of the portfolio adjustment to receivables from customers.

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010

Financial institutions 107 712 -

Non-financial institutions 1 857 993 2 000 519

Non-profit organisations 120 518 -

Households / self-employed 17 186 4 007

Resident individuals 729 328 77 574

Non-residents 16 529 -

Total 2 849 266 2 082 100

45

The amounts in the above table are stated net of the portfolio adjustment to receivables.

(c) Analysis of receivables from customers by sector and type of security received

11. Receivables from customers

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK Bank guarantee Mortgage Bank deposit Unsecured Total

At 31 December 2011

Financial institutions - 107 712 - - 107 712

Non-financial institutions 16 171 1 276 570 7 900 557 352 1 857 993

Non-profit organisations - 120 518 - - 120 518

Households / self-employed - 15 598 50 1 538 17 186

Resident individuals - 709 750 - 19 578 729 328

Non-residents - 14 465 129 1 935 16 529

Total 16 171 2 244 613 8 079 580 403 2 849 266

At 31 December 2010

Non-financial institutions 43 796 1 709 338 12 849 234 536 2 000 519

Households / self-employed - 1 536 50 2 421 4 007

Individuals - 67 213 - 10 361 77 574

Total 43 796 1 778 087 12 899 247 318 2 082 100

46

(d) Receivables from customers written-off

TCZK 2011 2010

Write-offs

Non-financial institutions 27 1 803

Households / self-employed 2 -

Individuals 42 31

Total 71 1 834

Receivables from persons with a special relationship to the Group

TCZK Supervisory bodies

At 31 December 2010 -

At 31 December 2011 313

11. Receivables from customers

Con

solid

ated

fina

ncia

l sta

tem

ents

47Con

solid

ated

fina

ncia

l sta

tem

ents

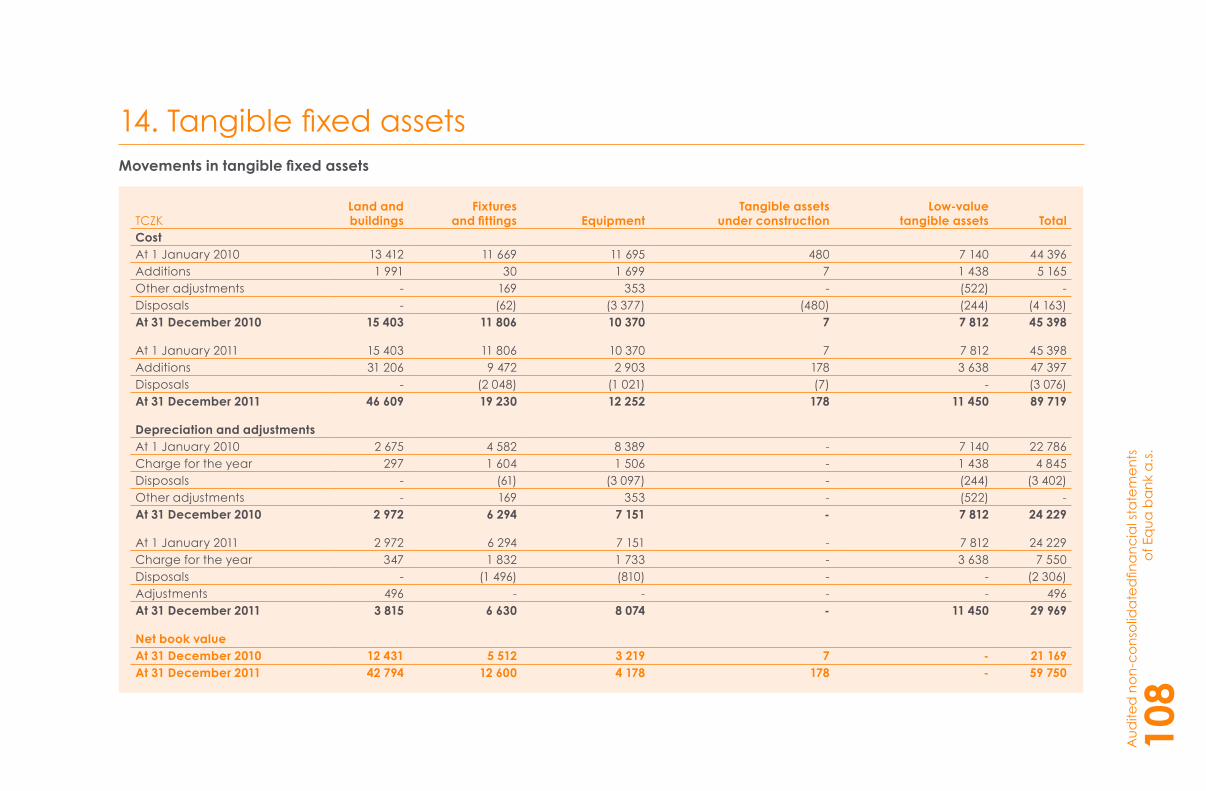

Movements in intangible fixed assets

Additions to software in 2011 comprised the banking software owned by EFS that is leased to the Bank.

“Goodwill” comprises the negative goodwill arising on the acquisition of the Subsidiary of TCZK -9 144, which is amortised over 5 years, and the goodwill of EFS arising on the purchase of a part of business

12. Intangible fixed assets

in 2010 of TCZK 2 620, which is amortised over 6 years. Amortisation of the negative goodwill of TCZK 760 for 2011 is recorded under “Other operating income”.

TCZK Software GoodwillOther

intangible assetsLow-value

intangible assets Intangible assets

under construction TotalCostAt 1 January 2010 3 744 - - 95 1 642 5 481Additions 606 - - 289 1 250 2 145At 31 December 2010 4 350 - - 384 2 892 7 626

At 1 January 2011 4 350 - - 384 2 892 7 626Additions 340 985 (6 524) 2 353 73 1 635 338 522Disposals (5 023) - - - (3 081) (8 104)At 31 December 2011 340 312 (6 524) 2 353 457 1 446 338 044

Amortisation and adjustmentsAt 1 January 2010 2 397 - - 95 - 2 492Charge for the year 665 - - 289 - 954Adjustments - - - - 1 250 1 250At 31 December 2010 3 062 - - 384 1 250 4 696

At 1 January 2011 3 062 - - 384 1 250 4 696Charge for the year 13 552 (558) - 73 - 13 067Adjustments - - - - (1 250) (1 250)At 31 December 2011 16 614 (558) - 457 - 16 513

Net book valueAt 31 December 2010 1 288 - - - 1 642 2 930At 31 December 2011 323 698 (5 966) 2 353 - 1 446 321 531

48Con

solid

ated

fina

ncia

l sta

tem

ents

Movements in tangible fixed assets

13. Tangible fixed assets

TCZKLand and buildings

Equipment,fixtures and fittings Hardware

Low-valuetangible assets

Tangible assetsnot yet in use Total

CostAt 1 January 2010 13 412 23 364 - 7 140 480 44 396Additions 1 991 1 729 - 1 438 7 5 165Other adjustments - 522 - (522) - -Disposals - (3 439) - (244) (480) (4 163)At 31 December 2010 15 403 22 176 - 7 812 7 45 398

At 1 January 2011 15 403 22 176 - 7 812 7 45 398Additions 31 206 12 375 49 400 3 638 178 96 797Disposals - (3 069) (803) - (7) (3 879)At 31 December 2011 46 609 31 482 48 597 11 450 178 138 316

Depreciation and adjustmentsAt 1 January 2010 2 675 12 971 - 7 140 - 22 786Charge for the year 297 3 110 - 1 438 - 4 845Disposals - (3 158) - (244) - (3 402)Other adjustments - 522 - (522) - -At 31 December 2010 2 972 13 445 - 7 812 - 24 229

At 1 January 2011 2 972 13 445 - 7 812 - 24 229Charge for the year 347 3 565 2 412 3 638 - 9 962Disposals - (2 306) (553) - - (2 859)Adjustments 496 - - - - 496At 31 December 2011 3 815 14 704 1 859 11 450 - 31 828

Net book valueAt 31 December 2010 12 431 8 731 - - 7 21 169At 31 December 2011 42 794 16 778 46 738 - 178 106 488

49

14. Other assets 15. Due to banks

TCZK 2011 2010Other debtors 44 562 7 693Positive fair value of derivatives 67 -Deferred tax asset 103 523 -Total 148 152 7 693

TCZK 2011 2010Term deposits with fixed maturity - 120 376Total - 120 376

Analysis of due to banks by residual maturity

(a) Analysis of due to customers by sector

16. Due to customers

TCZK Repayable on demand Term deposits with fixed maturity Other TotalAt 31 December 2011Financial institutions 235 121 465 - 121 700Non-financial institutions 531 243 591 485 20 1 122 748Non-profit organisations 2 309 64 207 - 66 516Households / self-employed - - 3 3Resident individuals 1 084 618 1 972 258 416 3 057 292Non-residents 96 941 10 357 150 107 448Total 1 715 346 2 759 772 589 4 475 707

Con

solid

ated

fina

ncia

l sta

tem

ents

50Con

solid

ated

fina

ncia

l sta

tem

ents

(a) Analysis of due to customers by sector (continued)

(b) Due to persons with a special relationship to the Group

16. Due to customers

TCZK Repayable on demand Term deposits with fixed maturity Other TotalAt 31 December 2010Financial institutions - 11 278 - 11 278Non-financial institutions 307 662 559 553 - 867 215Government sector - 85 - 85Non-profit organisations 3 071 71 723 - 74 794Households / self-employed 75 739 61 162 - 136 901Resident individuals 152 945 1 998 295 - 2 151 240Non-residents 107 868 30 582 - 138 450Unallocated - - 257 257Total 647 285 2 732 678 257 3 380 220

TCZK Members of the board of directors and other executives í

Supervisory bodies

At 31 December 2010 5 984 2 516At 31 December 2011 4 944 534

51

17. Other liabilities

TCZK 2011 2010

Negative fair values of derivatives 735 -

Liabilities from collection and payments clearing 7 905 2 223

Various creditors 26 525 10 489

Advances received 51 33

Liabilities to employees 10 549 3 024

Social security and health insurance 6 123 1 555

Tax liabilities 5 889 749

Estimated liabilities 60 871 4 630

Total 118 648 22 703

Con

solid

ated

fina

ncia

l sta

tem

ents

52Con

solid

ated

fina

ncia

l sta

tem

ents

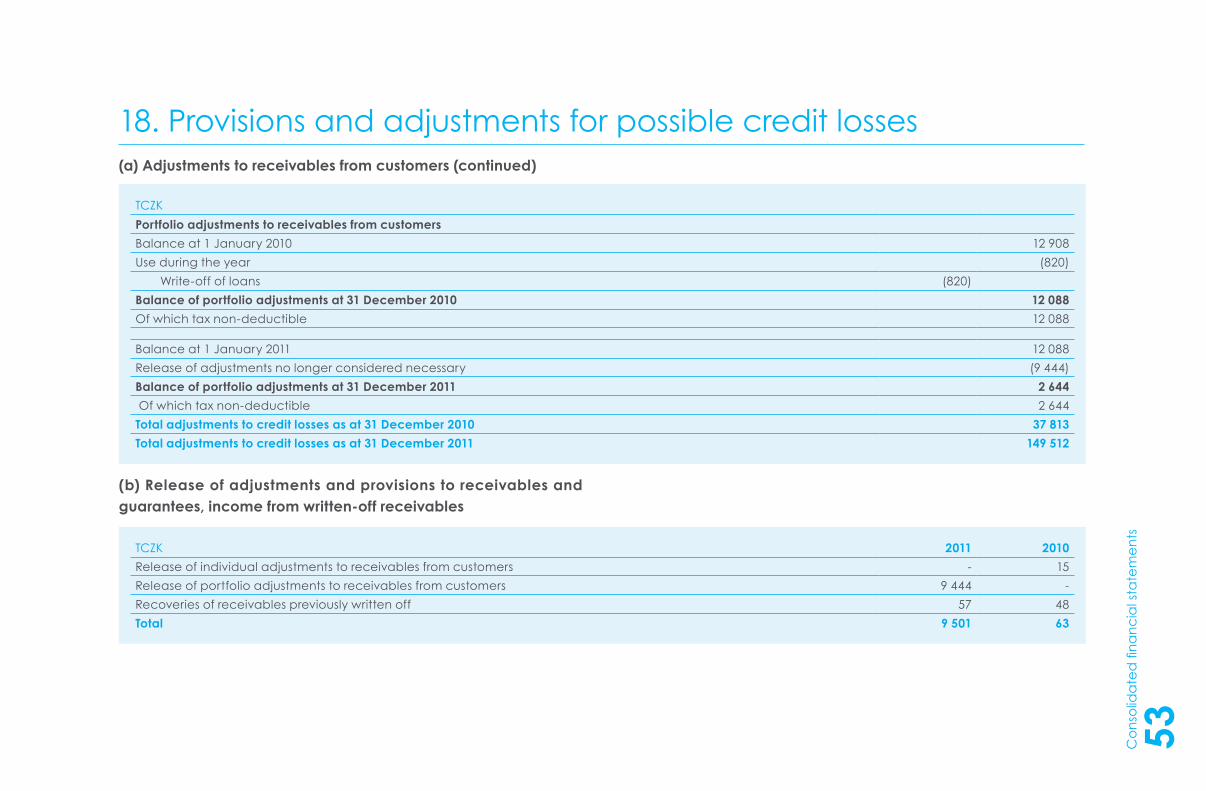

(a) Adjustments to receivables from customers

18. Provisions and adjustments for possible credit losses

TCZKBalance at 1 January 2010 24 565Creation during the year 2 929

Loss loans 2 929Use during the year (1 754)

Write-off of loans (1 754)Release of adjustments no longer considered necessary (15)Balance of individual adjustments at 31 December 2010 25 725 Of which tax non-deductible 9 967

TCZKBalance at 1 January 2011 25 725Creation during the year 121 143

Special mention loans 4 471Substandard loans 27 886Doubtful loans 36 839Loss loans 51 947

Balance of individual adjustments at 31 December 2011 146 868Of which tax non-deductible 86 359

53Con

solid

ated

fina

ncia

l sta

tem

ents

(a) Adjustments to receivables from customers (continued)

(b) Release of adjustments and provisions to receivables and guarantees, income from written-off receivables

TCZKPortfolio adjustments to receivables from customersBalance at 1 January 2010 12 908Use during the year (820)

Write-off of loans (820)Balance of portfolio adjustments at 31 December 2010 12 088Of which tax non-deductible 12 088

Balance at 1 January 2011 12 088Release of adjustments no longer considered necessary (9 444)Balance of portfolio adjustments at 31 December 2011 2 644 Of which tax non-deductible 2 644Total adjustments to credit losses as at 31 December 2010 37 813Total adjustments to credit losses as at 31 December 2011 149 512

TCZK 2011 2010Release of individual adjustments to receivables from customers - 15Release of portfolio adjustments to receivables from customers 9 444 -Recoveries of receivables previously written off 57 48Total 9 501 63

18. Provisions and adjustments for possible credit losses

54Con

solid

ated

fina

ncia

l sta

tem

ents

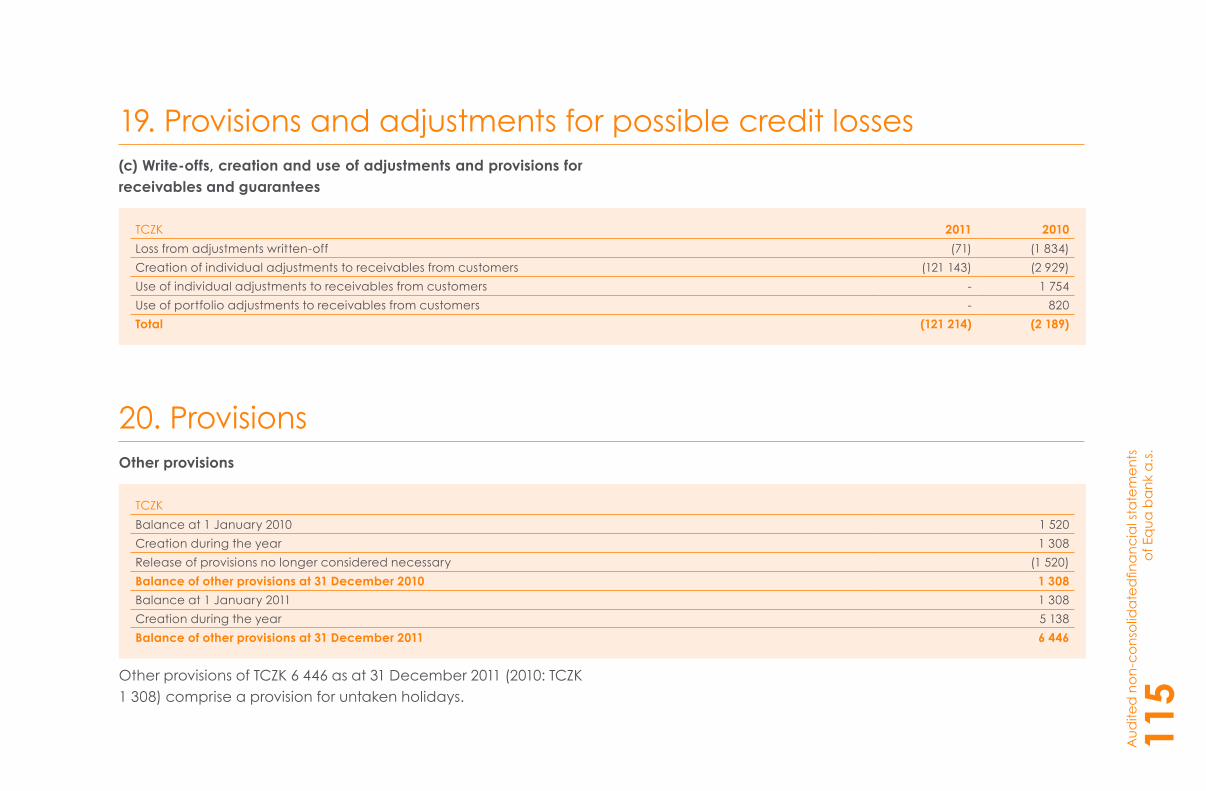

18. Provisions and adjustments for possible credit losses (c) Write-offs, creation and use of adjustments and provisions for receivables and guarantees

Other provisions

Other provisions of TCZK 6 446 as at 31 December 2011 (2010: TCZK 1 308) comprise a provision for untaken holidays.

19. Provisions

TCZK 2011 2010Loss from adjustments written-off (71) (1 834)Creation of individual adjustments to receivables from customers (121 143) (2 929)Use of individual adjustments to receivables from customers - 1 754Use of portfolio adjustments to receivables from customers - 820Total (121 214) (2 189)

TCZKBalance at 1 January 2010 1 520Creation during the year 1 308Release of provisions no longer considered necessary (1 520)Balance of other provisions at 31 December 2010 1 308Balance at 1 January 2011 1 308Creation during the year 5 138Balance of other provisions at 31 December 2011 6 446

55

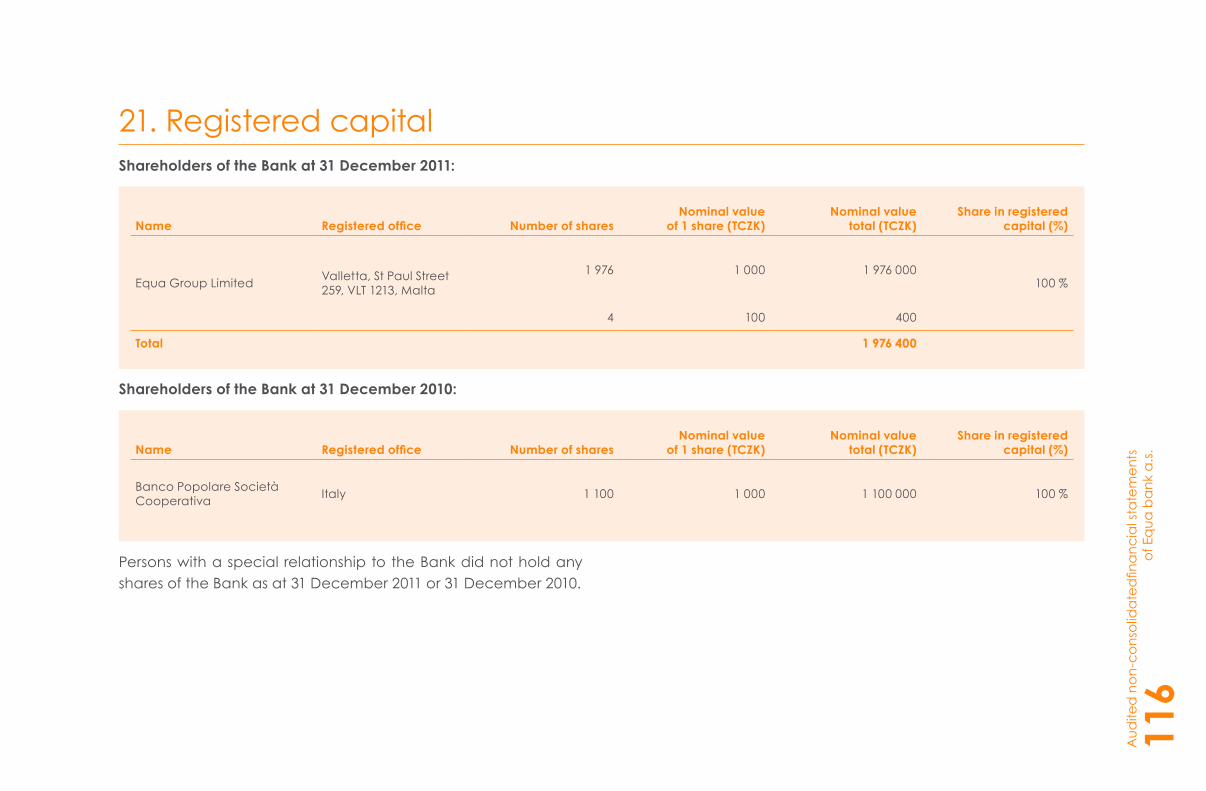

Shareholders of the Bank at 31 December 2011:

Shareholders of the Bank at 31 December 2010:

Persons with a special relationship to the Bank did not hold any shares of the Bank as at 31 December 2011 or 31 December 2010.

20. Registered capital

Con

solid

ated

fina

ncia

l sta

tem

ents

Name Registered office Number of sharesNominal value

of 1 share (TCZK)Nominal value

total (TCZK)Share in registered

capital (%)

Equa Group Limited Valletta, St Paul Street 259, VLT 1213, Malta

1 976 1 000 1 976 000100 %

4 100 400

Total 1 976 400

Name Registered office Number of sharesNominal value

of 1 share (TCZK)Nominal value

total (TCZK)Share in registered

capital (%)

Banco Popolare Società Cooperativa Italy 1 100 1 000 1 100 000 100 %

56

Income tax for 2011 of TCZK 103 523 comprises exclusively the year-on-year change in the recognised deferred tax asset/liability.

(a) Splatná daň z příjmů

21. Income tax and deferred tax asset/liability

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010

Current year profit (loss) before tax (462 329) (98 522)

Income not liable to tax (17 098) (6 291)

Tax non-deductible expenses 119 077 6 641

Other items - -

Taxable income (360 350) (98 172)

Tax rate 19 % 19 %

Current tax - -

57

(b) Deferred tax liability/asset

Deferred income tax is calculated on all temporary differences using the tax rates expected to be valid in the following period, i.e. 19% for 2011 and 2010. The table below shows deferred tax assets and liabilities calculated on individual temporary differences:

21. Income tax and deferred tax asset/liability

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010

Deferred tax assets 110 309 44 586

of which:

Tax loss from prior periods 91 094 40 146

Adjustments 15 702 4 191

Provision for untaken holidays 3 513 249

Deferred tax liabilities (5 619) (360)

of which:

Tangible and intangible fixed assets (5 123) (360)

Revaluation of participation interest with controlling influence (496) -

Net deferred tax asset/liability 104 690 44 226

58

continued

(b) Deferred tax liability/asset (continued)

A portion of the deferred tax asset was calculated on cumulated deferred losses of the Bank and its Subsidiary.

As at 31 December 2011 the Bank recognised a deferred tax asset arising on cumulated deferred loss of TCZK 85 102 (2010: TCZK 40 146); the deferred tax asset was calculated on cumulated tax losses for taxable periods 2010 and 2011 totalling TCZK 447 912. The Bank’s management believes that current and future taxable profits will be sufficient to claim the tax losses within 5 years from when the tax asset arose (i.e. until 2015 and 2016, respectively).

For reasons of prudence, the deferred tax asset as at 31 December 2010 was only recognised to the extent of the deferred tax liability of TCZK 360; the remaining portion of the calculated deferred tax asset of TCZK 44 226 was not recognised.

21. Income tax and deferred tax asset/liability

As at 31 December 2011 the Subsidiary recognised a deferred tax asset arising on cumulated deferred losses of TCZK 4 825; the deferred tax asset was calculated on cumulated tax losses for taxable periods 2010 and 2011 totalling TCZK 31 539. For reasons of prudence, the Subsidiary only used tax losses of TCZK 25 398 to calculate the deferred tax as at 31 December 2011. The deferred tax asset of TCZK 1 167 was not recognised.

Con

solid

ated

fina

ncia

l sta

tem

ents

59

(a) Irrevocable contingent liabilities arising from acceptances and endorsements, other written contingent liabilities and assets pledged as collateral

(b) Off-balance sheet financial instruments

All of the above instruments were contracted on interbank market (OTC).

(c) Residual maturity of financial derivativesAll FX swap contracts of nominal value of MCZK 180 as at 31 Decem-ber 2011 have maturities of up to 3 months.

22. Off-balance sheet items

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK 2011 2010Commitments granted 277 453 396 245

Payables from guarantees - 11 162

Assets pledged as collateral - 29 110

Total 277 453 436 517

TCZK Contractual amount Fair value2011 2010 2011 2010

purchase sale purchase sale

Trading instruments

FX spot transactions 1 170 (1 177) 3 889 (3 884) (7) (5)

FX swap contracts 179 986 (180 664) - - (678) -

Total 181 156 (181 841) 3 889 (3 884) (685) (5)

60

As at 31 December 2011 the Bank recorded values of TCZK 6 208 (31 December 2010: TCZK 4 206), which comprise promissory notes from documentary collections.

The Bank is exposed to market risks arising from the open positions of transactions with interest rate, equity and currency instruments that are sensitive to changes in financial market conditions.

(b) Trading

The Bank does not trade in options, forwards, swaps or other derivatives (except for derivatives held for hedging purposes), or commodities, including gold. The Bank does not actively trade in shares or bonds.

(b) Risk management

Liquidity riskLiquidity risk is the risk that the Bank will become unable to settle its liabilities as they fall due or to finance its assets. The liquidity risk of the Bank arises from the time and subject-matter mismatch

23. Values taken into custody, administration and deposit

24. Financial instruments –market risk

of balance sheet assets and liabilities and some off-balance sheet items. In managing liquidity and setting positions, the Bank considers the maturity of its financial liabilities as well as the possi-bility to realise its assets in the market without major losses.

The Bank has access to diversified sources of funding, which comprise funds in customers’ current and savings account, various term deposits and the Bank’s equity. The Bank regularly (on a daily basis) evaluates the liquidity risk, in particular by monitoring changes in the structure of its financing and comparing these changes with the Bank’s liquidity risk management strategy, which is approved by the Bank’s board of directors. The Bank also holds a portion of its assets in highly liquid funds, such as state treasury bills received in reverse repo transactions with the CNB, or overnight deposits with other banks.

To manage the liquidity risk, the Bank uses the following ratios:

● highly liquid assets to total assets (HLA/A), or to cover the stress scenario of expected cash outflow

● cumulative liquidity position in individual time bands

These ratios are reviewed on a daily basis and compared against limits set by the board of directors. If a breach of limits is detected, the board of directors is informed.

Con

solid

ated

fina

ncia

l sta

tem

ents

61Con

solid

ated

fina

ncia

l sta

tem

ents

continued

(b) Risk management (continued)

Residual maturity of assets and liabilities

24. Financial instruments – market risk

Unspecified receivables from customers include classified loans.

TCZK Up to 3 months 3 months to 1 year 1 to 5 years Over 5 years Unspecified TotalAt 31 December 2011Cash and balances with CB 142 073 - - - - 142 073Receivables from banks 2 476 451 504 - - - 2 476 955Receivables from customers 173 243 133 050 927 461 1 020 022 592 846 2 846 622Tangible and intangible fixed asset - - - - 428 019 428 019Other assets - - - - 148 152 148 152Prepaid expenses and accrued income - - - - 17 685 17 685Total 2 791 767 133 554 927 461 1 020 022 1 186 702 6 059 506

Due to customers 2 658 288 1 509 560 297 836 5 503 4 520 4 475 707Other liabilities - - - - 118 648 118 648Accrued expenses and deferred income - - - - 2 513 2 513Provisions - - - - 6 446 6 446Equity - - - - 1 456 192 1 456 192Total 2 658 288 1 509 560 297 836 5 503 1 588 319 6 059 506Gap 133 479 (1 376 006) 629 625 1 014 519 (401 617) -Cumulative gap 133 479 (1 242 527) (612 902) 401 617 - -

62Con

solid

ated

fina

ncia

l sta

tem

ents

continued

(b) Risk management (continued)

Residual maturity of assets and liabilities (continued)

24. Financial instruments – market risk

Unspecified receivables from customers include classified loans.

TCZK Up to 3 months 3 months to 1 year 1 to 5 years Over 5 years Unspecified TotalAt 31 December 2010Cash and balances with CB 481 112 - - - - 481 112Receivables from banks 1 875 370 504 - - - 1 875 874Receivables from customers 262 234 143 692 760 740 763 579 139 767 2 070 012Tangible and intangible fixed asset - - - - 24 099 24 099Other assets - - - - 7 693 7 693Prepaid expenses and accrued income - - - - 4 399 4 399Total 2 618 716 144 196 760 740 763 579 175 958 4 463 189

Due to banks 45 196 75 180 - - - 120 376Due to customers 2 259 796 870 836 248 488 - 1 100 3 380 220Other liabilities 257 - - - 22 446 22 703Provisions - - - - 1 308 1 308Equity - - - - 938 582 938 582Total 2 305 249 946 016 248 488 - 963 436 4 463 189Gap 313 467 (801 820) 512 252 763 579 (787 478) -Cumulative gap 313 467 (488 353) 23 899 787 478 - -

63

continued

(b) Risk management (continued)

Interest rate riskThe Bank is exposed to interest rate risk arising from the time mismatch of interest-rate sensitive assets and liabilities and some off-balance sheet items. The Bank’s interest rate risk management activities are aimed at optimising net interest income in accordance with the Bank’s strategy and interest rate risk limits approved by the board of directors.

To manage the interest rate risk, the Bank uses a gap analysis. The analysis is based on quantifying the mismatch between interest-rate sensitive assets and interest-rate sensitive liabilities in view of their repricing dates. Interest rate risk is measured on a daily basis.

In accordance with CNB requirements, the Bank also carries out stress testing of interest rate risk; the Bank simulates the impact on the net interest income, or the Bank’s financial results of movements or changes in the shape of the yield curve. Interest rate risk stress testing is carried out on a quarterly basis, taking into account various scenarios of developments in market interest rates.

Independent monitoring of the Bank’s interest rate exposure against set limits is carried out on a daily basis; excesses over the limits are reported to the board of directors.

24. Financial instruments – market risk

Con

solid

ated

fina

ncia

l sta

tem

ents

64

continued

Interest-rate sensitivity of assets and liabilities

24. Financial instruments – market risk

Receivables from customers in the category Non-interest-rate sensitive items include primarily portfolio adjustments.

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK Up to 3 months 3 months to 1 year 1 to 5 years Over 5 yearsNon-interest-rate

sensitive items Total

At 31 December 2011

Cash and balances with CB 106 211 - - - 35 862 142 073

Receivables from banks 2 476 451 504 - - - 2 476 955

Receivables from customers 1 261 105 1 574 802 12 799 - (2 084) 2 846 622

Total 3 843 767 1 575 306 12 799 - 33 778 5 465 650

Due to customers 2 192 545 1 161 032 265 792 5 503 850 835 4 475 707

Total 2 192 545 1 161 032 265 792 5 503 850 835 4 475 707

Gap 1 651 222 414 274 (252 993) (5 503) (817 057) 989 943

Cumulative gap 1 651 222 2 065 496 1 812 503 1 807 000 989 943 -

65

continued

(b) Risk management (continued)

Interest rate risk (continued)

Interest-rate sensitivity of assets and liabilities

24. Financial instruments – market risk

Receivables from customers in the category Non-interest-rate sensitive items include portfolio adjustments.

Con

solid

ated

fina

ncia

l sta

tem

ents

TCZK Up to 3 months 3 months to 1 year 1 to 5 years Over 5 yearsNon-interest-rate

sensitive items TotalAt 31 December 2010Cash and balances with CB 434 676 - - - 46 436 481 112Receivables from banks 1 875 374 500 - - - 1 875 874Receivables from customers 1 072 812 760 917 248 371 - (12 088) 2 070 012Total 3 382 862 761 417 248 371 - 34 348 4 426 998

Due to banks 120 376 - - - - 120 376Due to customers 2 229 780 940 108 210 332 - - 3 380 220Total 2 350 156 940 108 210 332 - - 3 500 596Gap 1 032 706 (178 691) 38 039 - 34 348 926 402Cumulative gap 1 032 706 854 015 892 054 892 054 926 402 -

66

continued

Currency risk

Currency risk management aims to eliminate potential losses from open currency positions as a result of economic and market changes.

The Bank has set currency risk limits based on its net currency exposure in individual currencies. Furthermore, the Bank has set a limit for its total net currency exposure in relation to the Bank’s capital, as well as an absolute limit for its net currency exposure.

Independent monitoring is carried out on a daily basis.

Independent monitoring of the Bank’s exposure against set limits is carried out on a daily basis; excesses over the limits are reported to the board of directors.

24. Financial instruments – market risk

Con

solid

ated

fina

ncia

l sta

tem

ents

67Con

solid

ated

fina

ncia

l sta

tem

ents

continued

(b) Risk management (continued)

Currency risk (continued)

Foreign currency position

24. Financial instruments – market risk

TCZK EUR USD CZK Other TotalAt 31 December 2011Cash and balances with CB 9 182 2 016 130 875 - 142 073Receivables from banks 134 951 4 617 2 318 275 19 112 2 476 955Receivables from customers 431 236 - 2 415 386 - 2 846 622Tangible and intangible fixed asset - - 428 019 - 428 019Other assets 11 064 17 228 119 860 - 148 152Prepaid expenses and accrued income 1 027 1 306 15 352 - 17 685Total 587 460 25 167 5 427 767 19 112 6 059 506

Due to customers 494 983 25 250 3 936 421 19 053 4 475 707Other liabilities 9 247 359 109 042 - 118 648Accrued expenses and deferred income - - 2 513 - 2 513Provisions - - 6 446 - 6 446Equity - - 1 456 192 - 1 456 192Total 504 230 25 609 5 510 614 19 053 6 059 506

Long positions of off-balance sheet instruments 51 600 - 128 386 - 179 986Short positions of off-balance sheet instruments 129 000 - 51 644 - 180 664Net currency exposure 5 830 (442) (6 105) 59 (678)

68Con

solid

ated

fina

ncia

l sta

tem

ents

continued

(b) Risk management (continued)

Currency risk (continued)

Foreign currency position (continued)

24. Financial instruments – market risk

TCZK EUR USD CZK Other TotalAt 31 December 2010Cash and balances with CB 14 861 1 179 465 072 - 481 112Receivables from banks 32 876 29 622 1 797 322 16 054 1 875 874Receivables from customers 669 347 - 1 400 665 - 2 070 012Tangible and intangible fixed asset - - 24 099 - 24 099Other assets 2 548 - 5 145 - 7 693Prepaid expenses and accrued income - - 4 399 - 4 399Total 719 632 30 801 3 696 702 16 054 4 463 189

Due to banks 120 376 - - - 120 376Due to customers 595 069 30 392 2 738 745 16 014 3 380 220Other liabilities 7 887 413 14 403 - 22 703Provisions - - 1 308 - 1 308Equity - - 938 582 - 938 582Total 723 332 30 805 3 693 038 16 014 4 463 189

Long positions of off-balance sheet instruments - - 3 889 - 3 889Short positions of off-balance sheet instruments 3 884 - - - 3 884Total (7 584) (4) 7 553 40 5

69

25. Financial instruments – credit risk The Bank has established standardised and independent credit risk management processes. In terms of organisation, credit risk management is centralised in the Credit Risk department, which is managed directly by the member of the board of directors in charge of risk management.

As a result of historical development, a major portion of the Bank’s loan assets are loans granted by Banco Popolare Česká repub-lika, a.s. (hereinafter “BPCR”). In line with its business plan, in the second half of 2011 the Bank gradually purchased a portfolio of receivables from mortgage loans originally granted by Credoma group companies.

At the end of 2011, the Bank started to provide mortgage loans to households. In this activity, the Bank uses newly developed or modi-fied systems and approval processes to manage the risks connected with these loans.

The portfolio of corporate loans comprises primarily loans granted by BPCR, as well as purchased loans originally provided by Credoma group companies. Corporate loans are mostly secured by real es-tate collateral.

The portfolio of loans to individuals comprises primarily purchased receivables from mortgage loans, which are secured by real estate.

Classification of receivables is one of the standard tasks of the Credit Risk department. The Bank follows the procedure stipulated by Decree No. 123/2007. Classification of receivables is carried out on a monthly basis, and covers all portfolios of the Bank. Receivables are classified into one of 5 categories (standard, special mention, substandard, doubtful, loss) at the level of the customer, or group of connected customers. The main parameters for classification of receivables are days past due, payment discipline, existence of restructuring, insolvency, result of borrowers’ financial analysis, and other relevant information.

Based on classification of receivables, the Bank creates adjustments, taking into account also the amount of security, using the coefficient as per Decree No. 123/2007.

A vast majority of loan receivables are secured by real estate collateral, the value of which the Bank reviews on a regular basis. In the second half of 2011, all collateral was revaluated. The Collat-eral Management department is responsible for the value of real estate collateral, and its head reports directly to the member of the board of directors in charge of risk management.

Con

solid

ated

fina

ncia

l sta

tem

ents

70

The Collection department is in charge of administration of overdue receivables (generally 60 days past due for receivables from loans to households). The Credit Risk department sets parameters for collection of receivables that are past due by a shorter time; these are then collected by a specialised department in the Operations division.

The quality and other significant aspects of the loan portfolio are reviewed on a monthly basis by the Credit Committee consisting of representatives of the board of directors and of the relevant departments in charge.

The Bank only writes off receivables after all attempts to recover them have been completed (e.g. after the insolvency or bankruptcy proceedings have closed). Because of the length of these pro-ceedings, the volume of receivables in Loss category remains rather high. We consider the Bank’s loan portfolio to be of a high quality, and the creation of adjustments to be adequate and prudent.

Specialised departments of the Bank are now working on imple-mentation of an information infrastructure, which is a prerequisite for further expansion of the range of loan products offered, in particular in the area of consumer loans and loans to small and medium-sized enterprises.

25. Financial instruments – credit risk

Con

solid

ated

fina

ncia

l sta

tem

ents

71