Embed Size (px)

Citation preview

© 2011 Alvarez-Glasman & Colvinwww.agclawfirm.com

© 2012 Alvarez-Glasman & Colvin

THE CHANGING LEGALTHE CHANGING LEGAL LANDSCAPE OF LOCAL

TAXES AND FEESTAXES AND FEESREGIONAL CHAMBER OF COMMERCE –

SAN GABRIEL VALLEYPOWER LUNCHMAY 9, 2012

Alvarez-Glasman & ColvinDavid H. King, Esq. Teresa Chen, Esq., LEED AP

About us

Al Gl & C l i

About us

Al Gl & C l i i I d b d l

Alvarez-Glasman & Colvin

Alvarez-Glasman & Colvin is an Industry-based law firm specializing in representing public agency and private sector clients in the complex fields of real estate, l d d d l t i t l lland use and development, environmental law, employment and labor relations, and general liability and risk management.

Founded in 1985 by the Firm’s managing partner, Arnold M. Alvarez-Glasman

For more info: www.agclawfirm.com g

© 2012 Alvarez-Glasman & Colvin

About us

D id H Ki

About us

Education:

David H. KingEducation: Loyola Law School, Juris Doctor U.C.L.A., Bachelor of Arts

Practice Areas: Business Litigation Labor & Employment Municipal & Public Agency Law Municipal & Public Agency Law Civil Writs Election Law

© 2012 Alvarez-Glasman & Colvin

Disclaimer (we are attorneys, after all…)

This presentation is provided for general information only and is not offered or intended as legal advice.

Audience members should seek the advice of an attorney when confronted with legal issues and

attorne s sho ld perform an independent e al ation attorneys should perform an independent evaluation of the issues raised in this presentation.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Context

State of California is facing huge deficits

In January 2011, Governor Brown declared fiscal emergency in California

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Context cont.

State is increasingly taking revenue from local governments to balance its own budgets

Legislature adopted AB 1x 26 in 2011, eliminating redevelopment agencies

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Context cont.

As a result, local governments will be looking to increase local taxes and fees in the immediate future to overcome shortfalls

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Context cont.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Context cont.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Context cont.

Purpose of this presentation is to advise you, as a local businessperson or property owner, of the ever-changing law regarding local taxes and fees

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

A few definitions…

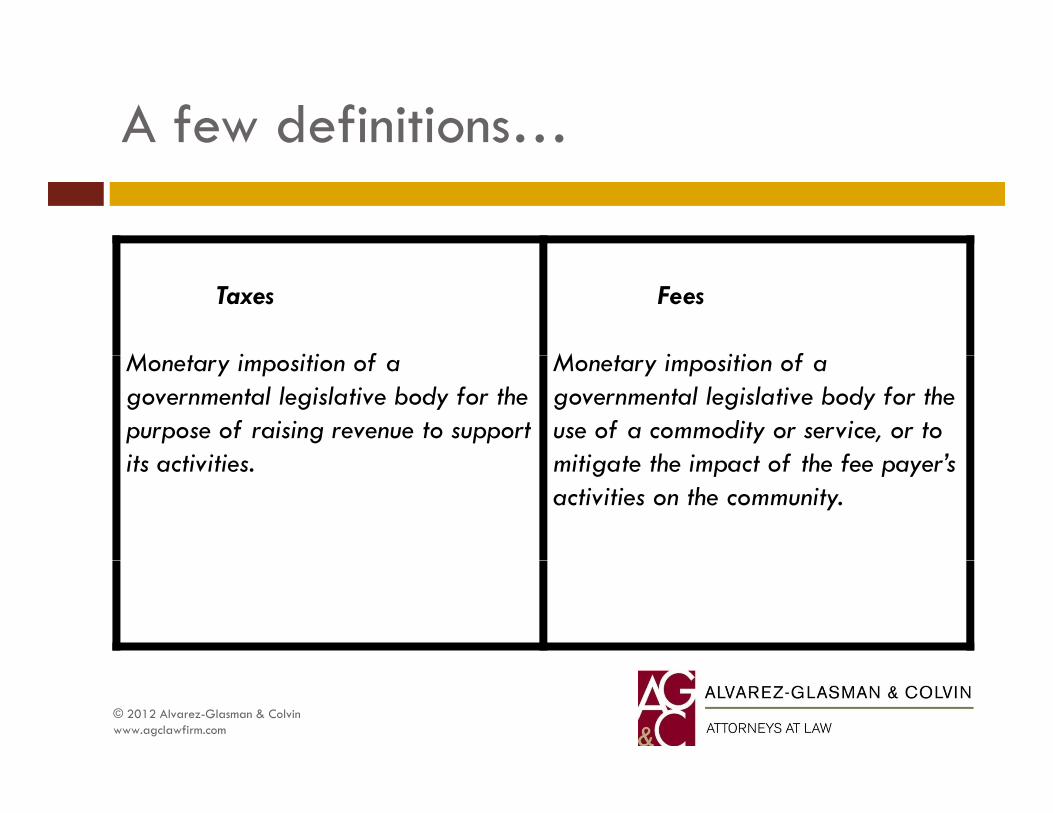

Taxes

M t i iti f

Fees

M t i iti f Monetary imposition of a governmental legislative body for the purpose of raising revenue to support it ti iti

Monetary imposition of a governmental legislative body for the use of a commodity or service, or to

iti t th i t f th f ’ its activities.

Mon

mitigate the impact of the fee payer’s activities on the community.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

A few definitions…

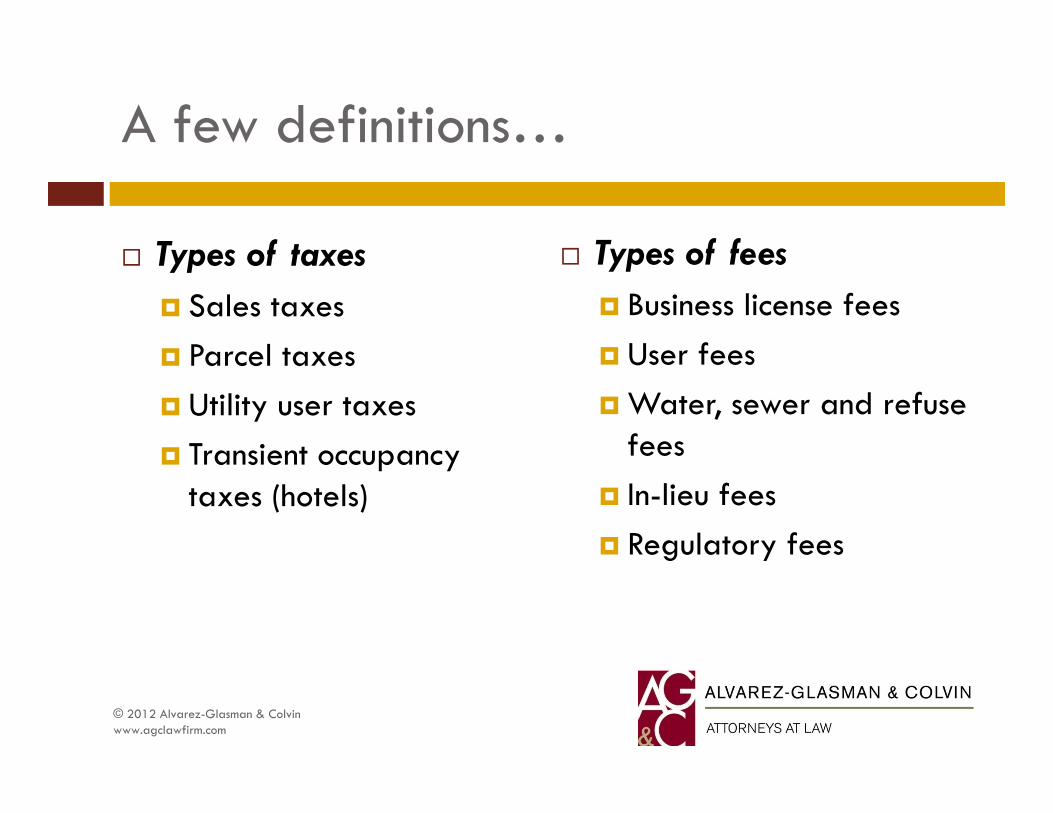

Types of taxes Types of fees Types of taxes Sales taxes Parcel taxes

Types of fees Business license fees User fees Parcel taxes

Utility user taxes Transient occupancy

User fees Water, sewer and refuse

fees Transient occupancy taxes (hotels) In-lieu fees

Regulatory feesg y

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Overview

Proposition 13 Proposition 62 Proposition 218 Proposition 26p Fee Mitigation Act

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Proposition 13p

Approved by voters in 1978 Set general-purpose property tax rate at 1% of assessed

value (Cut local property taxes by more than half)value (Cut local property taxes by more than half) Transferred control over property tax allocation to state Required voter approval of “special taxes” imposed by cities Required voter approval of special taxes imposed by cities,

counties and special districts

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

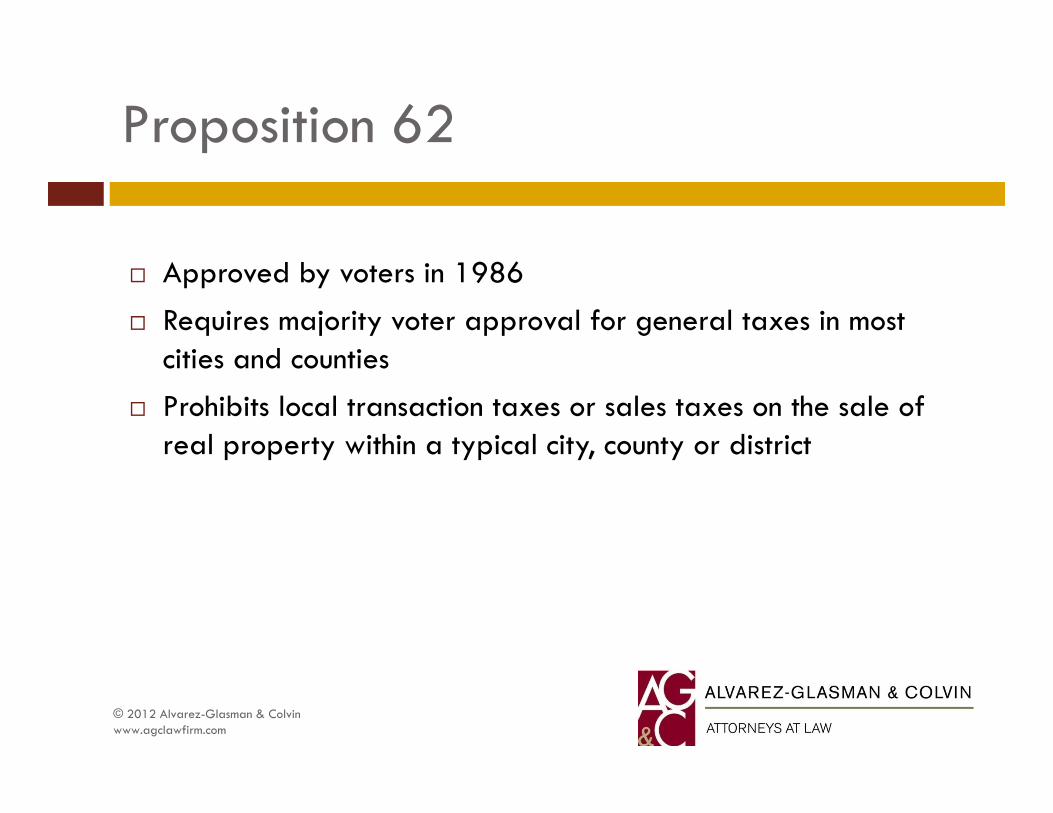

Proposition 62p

Approved by voters in 1986 Requires majority voter approval for general taxes in most

cities and countiescities and counties Prohibits local transaction taxes or sales taxes on the sale of

real property within a typical city, county or districtp p y yp y, y

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

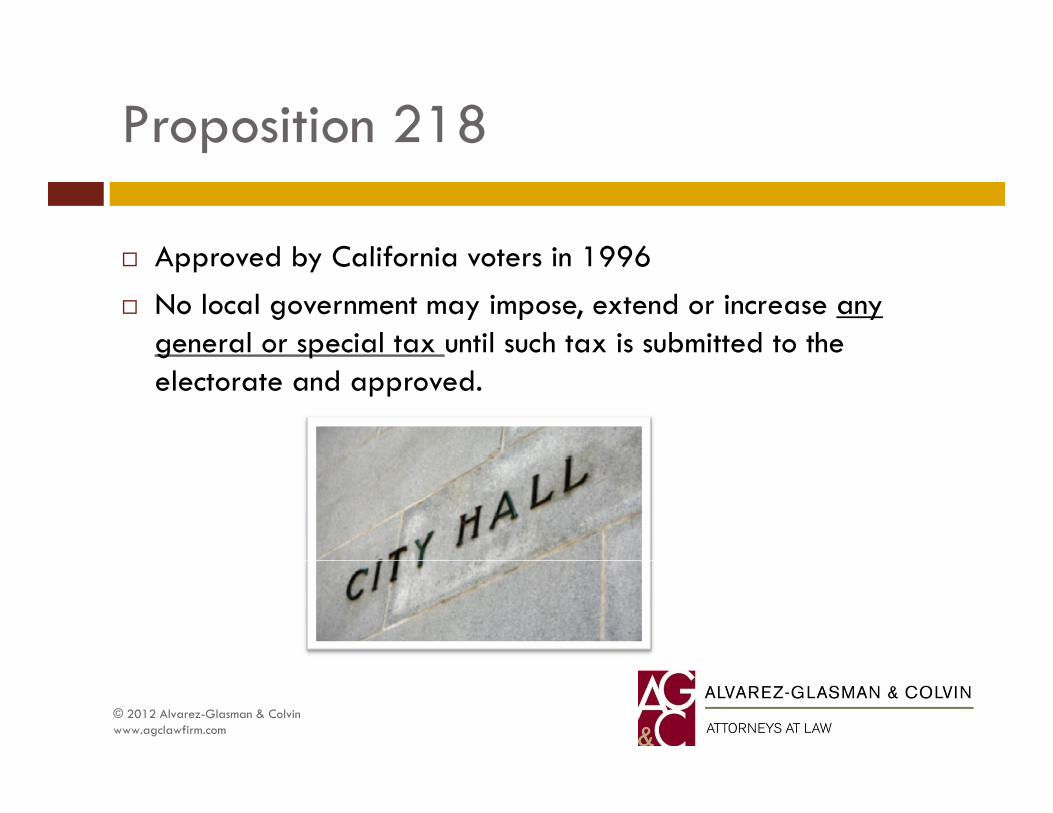

Proposition 218p

A d b C lif i t i 1996 Approved by California voters in 1996 No local government may impose, extend or increase any

general or special tax until such tax is submitted to the g pelectorate and approved.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

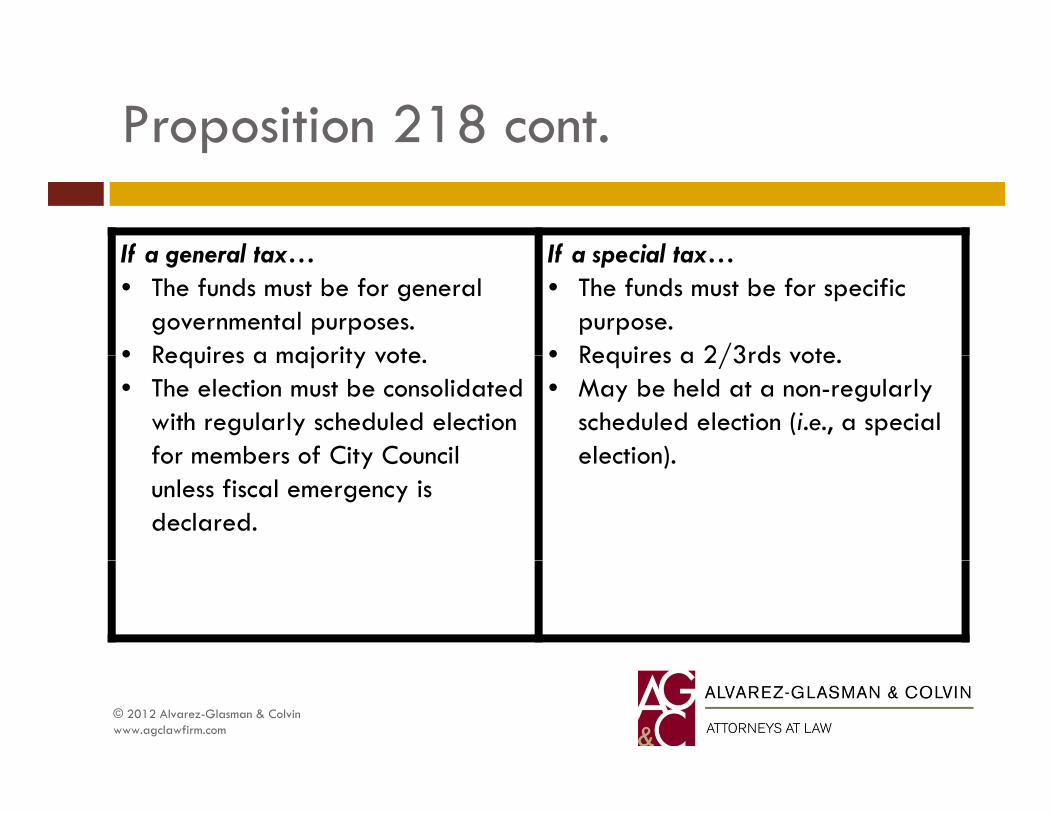

Proposition 218 cont. p

If a general tax If a special tax If a general tax…• The funds must be for general

governmental purposes. • Requires a majority vote

If a special tax… • The funds must be for specific

purpose.• Requires a 2/3rds vote • Requires a majority vote.

• The election must be consolidated with regularly scheduled election for members of City Council

• Requires a 2/3rds vote. • May be held at a non-regularly

scheduled election (i.e., a special election)for members of City Council

unless fiscal emergency is declared.

election).

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

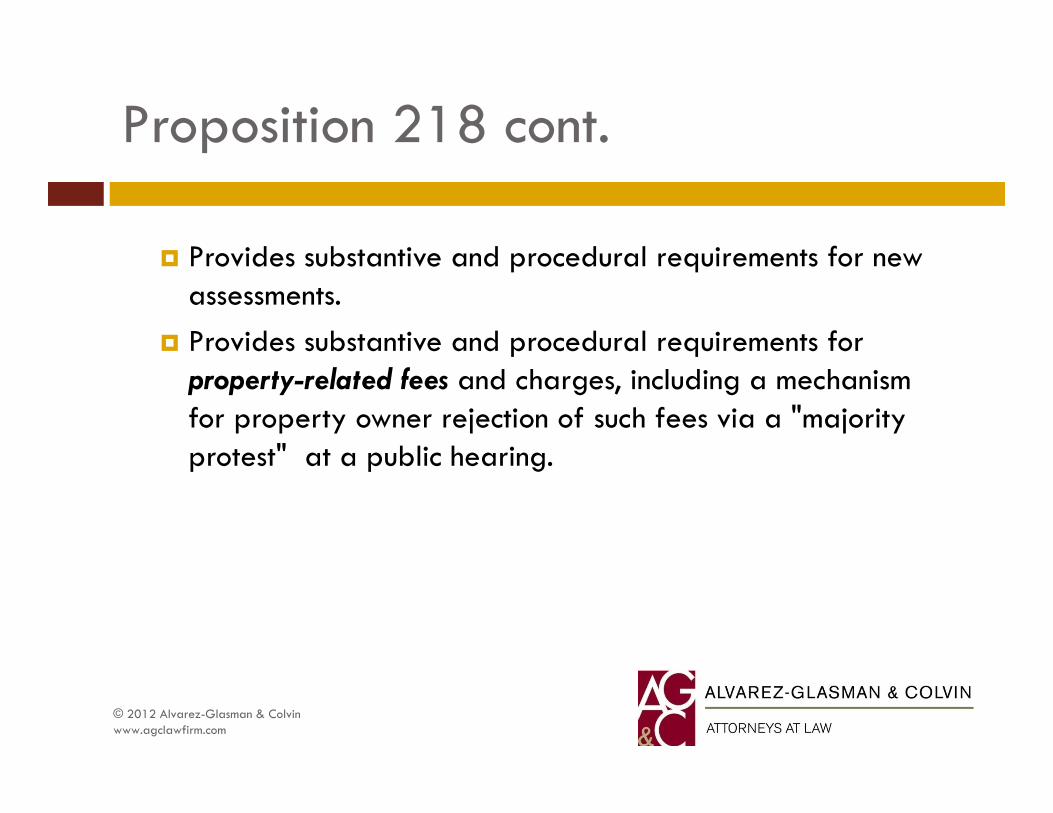

Proposition 218 cont. p

P id b t ti d d l i t f w Provides substantive and procedural requirements for new assessments.

Provides substantive and procedural requirements for p qproperty-related fees and charges, including a mechanism for property owner rejection of such fees via a "majority protest" at a public hearing protest at a public hearing.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

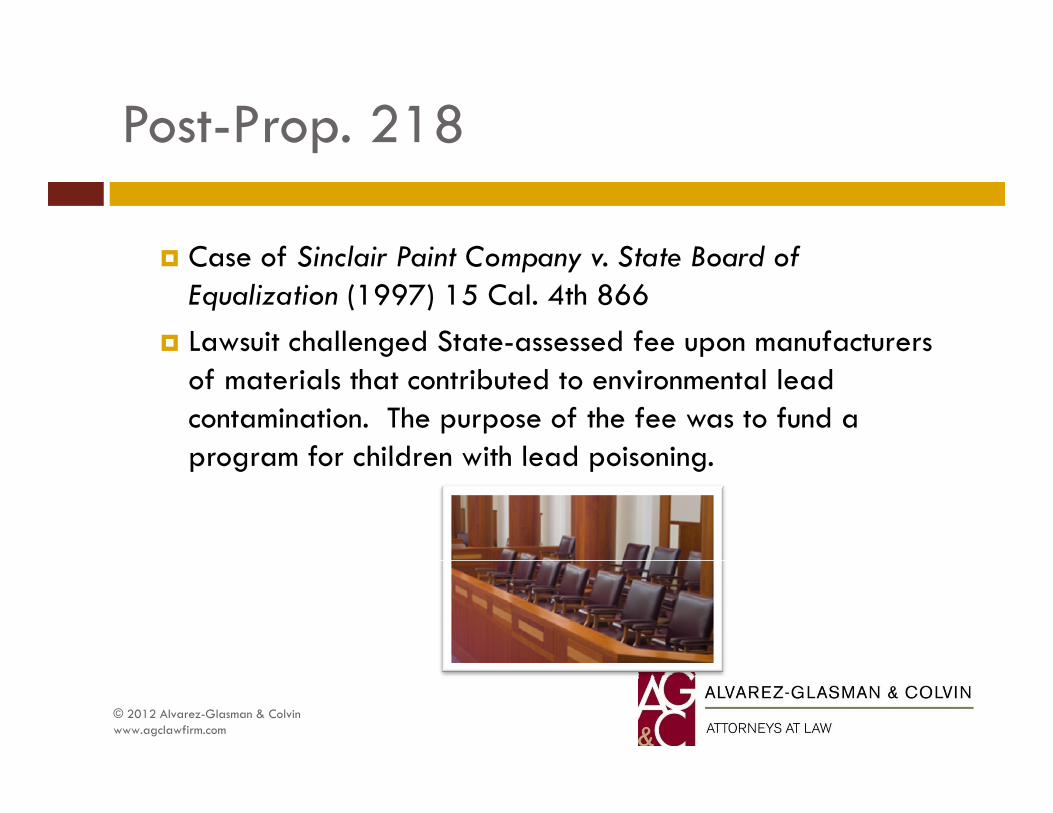

Post-Prop. 218 p

C f Si l i P i t C St t B d f Case of Sinclair Paint Company v. State Board of Equalization (1997) 15 Cal. 4th 866

Lawsuit challenged State-assessed fee upon manufacturers g pof materials that contributed to environmental lead contamination. The purpose of the fee was to fund a program for children with lead poisoningprogram for children with lead poisoning.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

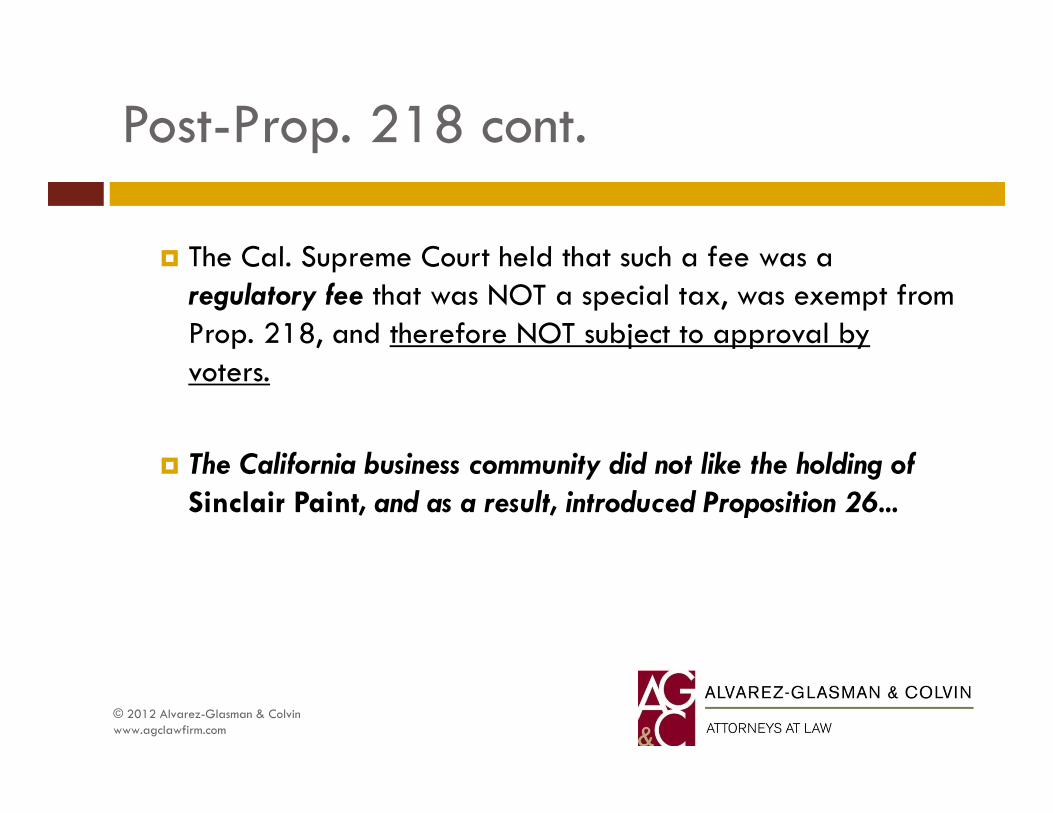

Post-Prop. 218 cont. p

Th C l S C t h ld th t h f w The Cal. Supreme Court held that such a fee was a regulatory fee that was NOT a special tax, was exempt from Prop. 218, and therefore NOT subject to approval by voters.

Th C lif i b i it did t lik th h ldi f The California business community did not like the holding of Sinclair Paint, and as a result, introduced Proposition 26...

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

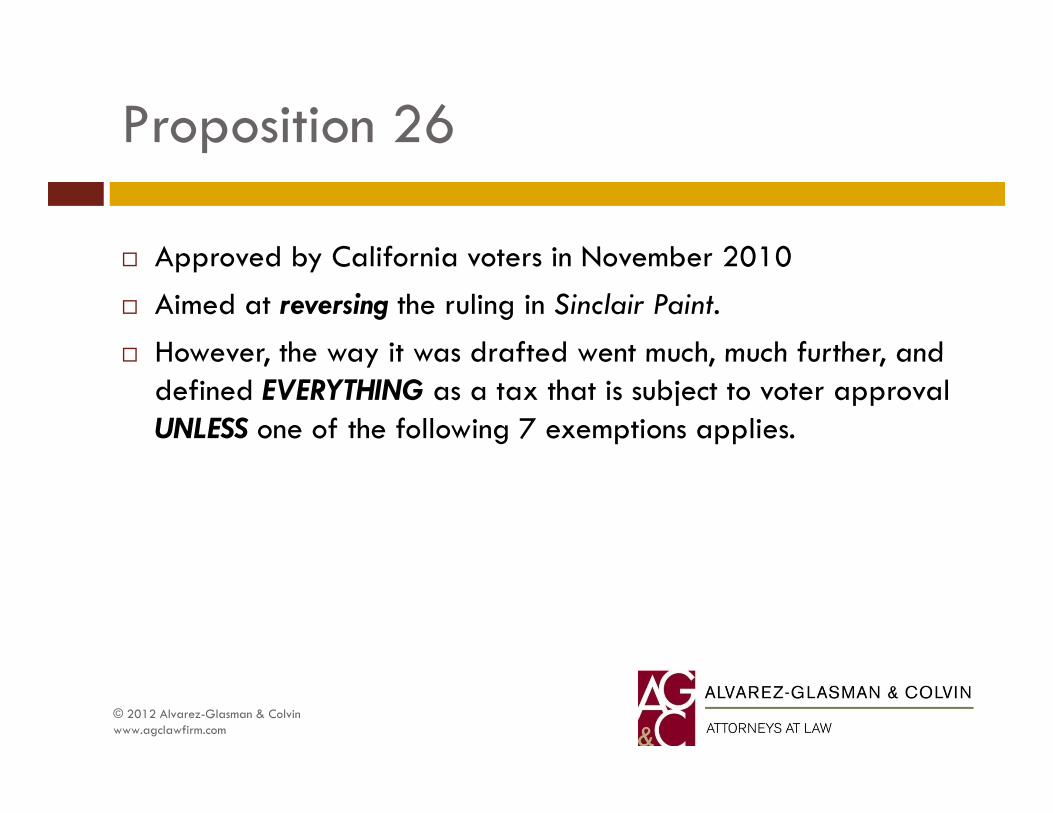

Proposition 26 p

A d b C lif i t i N b 2010 Approved by California voters in November 2010 Aimed at reversing the ruling in Sinclair Paint. However the way it was drafted went much much further and However, the way it was drafted went much, much further, and

defined EVERYTHING as a tax that is subject to voter approval UNLESS one of the following 7 exemptions applies.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

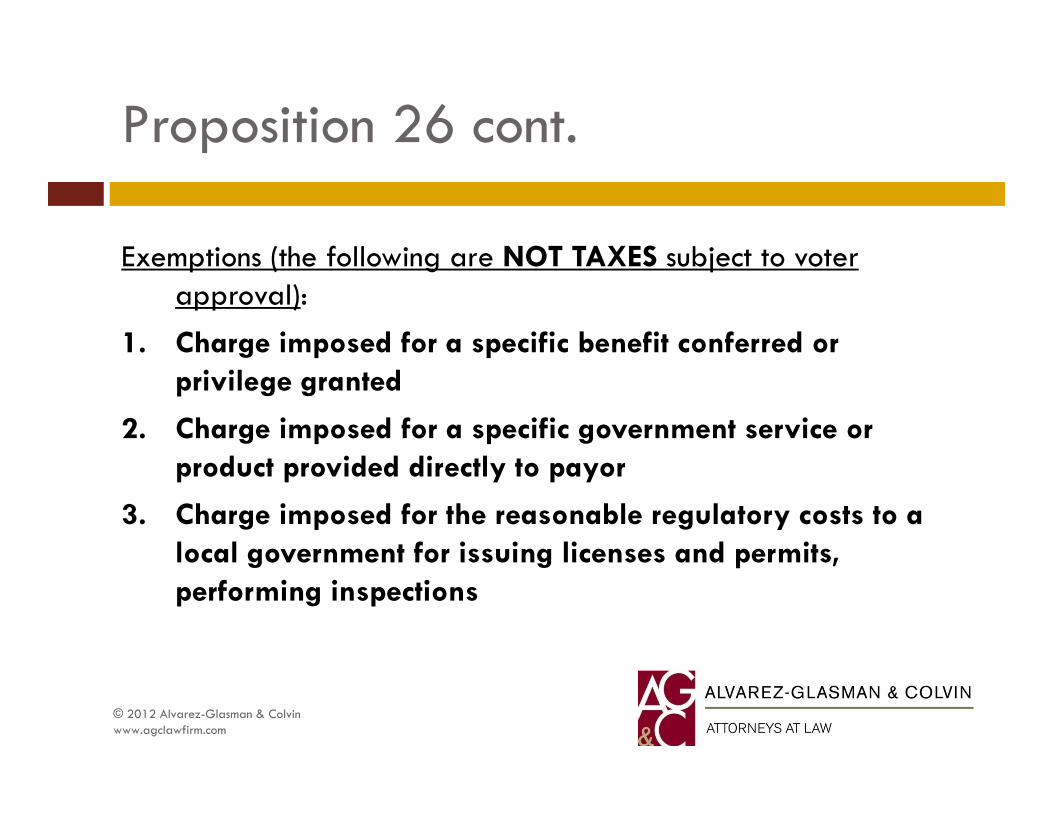

Proposition 26 cont. p

E ti (th f ll wi NOT TAXES bj t t t Exemptions (the following are NOT TAXES subject to voter approval):

1. Charge imposed for a specific benefit conferred or g p pprivilege granted

2. Charge imposed for a specific government service or d id d di l product provided directly to payor

3. Charge imposed for the reasonable regulatory costs to a local government for issuing licenses and permits, local government for issuing licenses and permits, performing inspections

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Proposition 26 cont. p

E ti (th f ll wi NOT TAXES bj t t t Exemptions (the following are NOT TAXES subject to voter approval):

4. Charge imposed for entrance to or use of local g pgovernment property, or purchase, rental or lease of government property

5 A fi l h h5. A fine, penalty or other monetary charge

6. A charge imposed as a condition of property development

7 Assessments and property related fees in accordance with 7. Assessments and property-related fees in accordance with Prop. 218

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

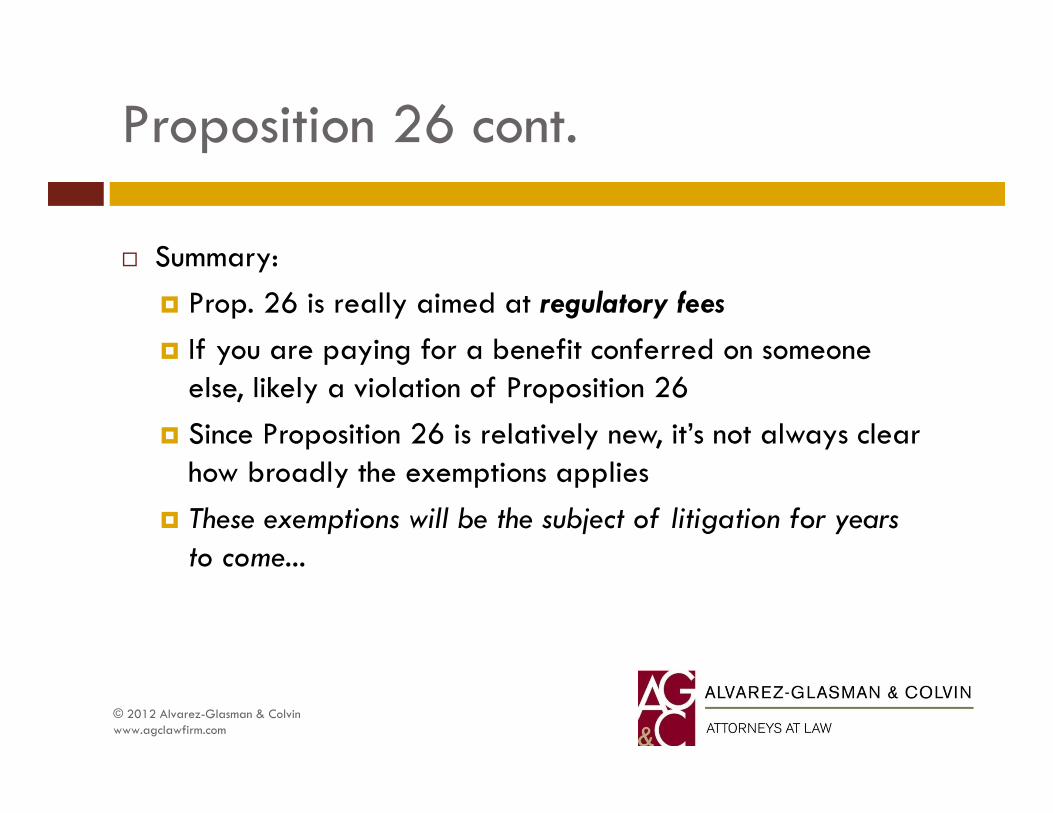

Proposition 26 cont. p

S Summary: Prop. 26 is really aimed at regulatory fees

If you are paying for a benefit conferred on someone If you are paying for a benefit conferred on someone else, likely a violation of Proposition 26

Since Proposition 26 is relatively new, it’s not always clear how broadly the exemptions applies

These exemptions will be the subject of litigation for years to come to come...

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Fee Mitigation Actg

N w w ’ll t lk b i fl b t f Now, we’ll talk briefly about fees What’s the difference?

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Fee Mitigation Act cont. g

I d t i i ti f dd w f iti t In order to increase existing fees, or add new fees, cities must hold public hearing, and a report / data supporting the fees be made available to the public.

Note that Mitigation Fee Act requirements apply to fees, not taxes or fines.

Fi b i d i h f h l ( h Fines may be increased without a vote of the people (they fall into Exemption # 5 under Prop. 26), and are not subject to public hearing or fee study requirements.

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

Conclusion

Closing Thoughts

Any questions?

Thank you!

© 2012 Alvarez-Glasman & Colvinwww.agclawfirm.com

![Web viewClaudette Colvin : twice toward justice [ Book ] B COLVIN Hoose, Phillip M., 1947- Published 2009](https://img.pdfslide.us/doc/110x75/5aaefeac7f8b9a190d8ccd5e/web-viewclaudette-colvin-twice-toward-justice-book-b-colvin-hoose-phillip.jpg)