Embed Size (px)

Citation preview

Department ofAgriculture and Food

norTh-easT asia

Bulletin no. 4793 issn 1833-7236 February 2010

Market Outlook 2010 North Asia.indd 2 24/2/10 4:13:59 PM

Bulletin 4793 ISSN 1833-7236

February 2010

NORTH-EAST ASIA Western Australia's Exports

2008–09 and

Business Development Strategy to 2011–12

Disclaimer

While all reasonable care has been taken in the preparation of the material in this document, the Western Australian Government and its officers accept no responsibility for any errors it may contain, whether caused by negligence or otherwise, or for any loss, however caused, sustained by any person who relied on it.

Copyright © Western Australian Agriculture Authority, 2010

Copies of this document are available in alternative formats upon request. 3 Baron-Hay Court, South Perth WA 6151 Tel: (08) 9368 3333 Email: [email protected] www.agric.wa.gov.au

For further information about this document, contact: Matt Yamamoto Tel: +61 8 9368 3469

i

Contents Page

JAPAN ........................................................................................................................................... 1

Market overview ...................................................................................................................... 1 Economic outlook ................................................................................................................. 1 Consumer trends .................................................................................................................. 3 Marketing channels .............................................................................................................. 7 Online sales getting serious ................................................................................................. 9 Realignment and consolidation in the retail markets ........................................................... 9 Merger puts food companies on global path ........................................................................ 12

Japan’s agrifood, fibre and fisheries imports ...................................................................... 15 Wheat and barley ................................................................................................................. 18 Baled hay and cereal straw .................................................................................................. 25 Canola .................................................................................................................................. 27 Red-fleshed grapefruit .......................................................................................................... 28 Health food ingredients ........................................................................................................ 30 Investment attraction opportunities ...................................................................................... 30 Developing a Western Australian green tea industry ........................................................... 35 Cultivation of Pink Lady™ apple in Japan ........................................................................... 36

Major projects and upcoming events .................................................................................... 37

Contacts ................................................................................................................................... 38

SOUTH KOREA ............................................................................................................................. 39

Market overview ...................................................................................................................... 39 Grain exports (feed grains, seeds, wheat flour) ................................................................... 43 Meat and animal products .................................................................................................... 44 Dairy products ...................................................................................................................... 47 Horticulture ........................................................................................................................... 49 Fisheries ............................................................................................................................... 50 Wine ..................................................................................................................................... 52 Organic and ‘wellbeing’ products ......................................................................................... 54 Retail products ..................................................................................................................... 55 Pet food ................................................................................................................................ 57

Major projects and coming events ........................................................................................ 58 7th Seoul International Wines and Spirits Expo 2010 .......................................................... 58 Seoul Food and Hotel 2010 ................................................................................................. 58 Busan International Seafood and Fishery Expo 2010 ......................................................... 58

Further resources .................................................................................................................... 59

Contacts ................................................................................................................................... 60

Western Australian Agrifood and Fibre Market Outlook–Japan

1

JAPAN

A market overview for Western Australian agribusinesses Japan is a very important market for Western Australian agrifood businesses. This Market Outlook for Japan provides a market overview and discusses Western Australian agrifood export performance and business opportunities.

Economic outlook

Japan slips into deflationary spiral The Bank of Japan (BOJ) estimated that the Japanese economy is likely to plateau or shrink early next fiscal year, which begins April 2010. The BOJ’s basic economic outlook predicted that the economy would gradually recover although the consumer price index would continue to decline for three years through fiscal 2011. The report warned of a possible weakening in gross domestic product early that fiscal year.

Behind this pessimism is the likelihood that public spending and durable goods consumption will slow as the government's economic stimulus measures run out of steam. Falling prices may be desirable for consumers, but the phenomenon risks pushing down corporate earnings, thereby putting downward pressure on the economy.

Since October 2009 when the Bank of Japan forecast three straight years of negative inflation, the sustained decline in prices has become a more palpable threat to the fragile economy. Outlook for Economic Activity and Prices (a biannual benchmark report by the central bank) forecast a 1.5 per cent decrease in the core consumer price index in the current fiscal year, followed by a 0.8 per cent decline in 2010 and 0.4 per cent decline for 2011. The weak economic recovery is prolonging the glut of labour and fixed capital, according to the bank.

The core CPI, which excludes perishable food, logged a record decline of 2.4 per cent on the year (2009) in August, followed by a 2.3 per cent dip in September, according to the Internal Affairs Ministry. The core CPI dropped for a seventh straight month. Demand undershot supply by a record annualised 40 trillion yen (A$500 billion) in the April–June quarter, putting prices under continued strong downward pressure.

Pay cuts are also depressing prices by weakening consumer spending.

Western Australian Agrifood and Fibre Market Outlook–Japan

2

The BOJ fears that households and companies will put off purchases and investment in expectation of further price drops. Japan may slip into a deflationary spiral of recession and declining prices.

War of attrition Financial conditions for consumers are worsening, as indicated by a 20 per cent year-on-year drop in this year's summer bonuses at large companies, as well as the 2.6 per cent decrease in workers' net income in September 2009. Under the circumstances, retailers are scrambling to join a price battle over a shrinking consumer-spending pie, with the race showing little sign of ending soon.

Some economists noted that actual store prices are even lower than the levels indicated by the CPI. The extremely cheap 880 yen (approx. A$11) jeans that major supermarket operator Aeon Co. began selling in August at its Jusco chain as a private-brand product sold 250 000 pairs within 10 days of their release. Seven and I Holdings (the biggest retailer group) started selling private-brand wine from California at 598 yen (approx. A$7) in 750 ml bottles.

Prices in the market are trending south and may fall further in the future. There are two main reasons for falling prices. One is technological innovation. With digital home appliances, for example, mass production lowers costs, enabling consumers to buy high-performance products at lower prices while boosting company sales and profits. The development can be described as a 'benign price fall' because it energises economic activity.

However, what is happening now is a price decline resulting from intensifying competition among retailers and manufacturers. The financial and economic crises have heavily depressed demand, unleashing the 40 trillion yen a year supply glut, the worst on record, according to the Japanese Government Cabinet Office. The high level of surplus products and facilities is prompting manufacturers and retailers to increase sales volume at almost any cost. The BOJ estimates that closing the gap between supply and demand will take until fiscal 2012 at the earliest.

As a result, Aeon, for example, suffered 14.6 billion yen in group net loss in the half year through August 2009, despite the strong sales of its private-brand goods including the 880 yen jeans. That was the second straight net loss the company has posted for the first half of a fiscal year. Aeon spilled 16 billion yen in red ink in the same term last year. Many of its rival supermarket chains are also faring poorly amid the harsh price battle, underscoring the fact that retailers are mired in a war of attrition.

Profit fall or loss leads to even lower wages and possibly higher unemployment. As a result, consumption could weaken further, which in turn forces producers and retailers to cut prices further, triggering a deflationary spiral.

Meanwhile, department stores are increasingly losing ground to low price retailers such as Fast Retailing Co., the operator of the Uniqlo clothing chain, saw a 7.8 per cent year-on-year decline in September nationwide sales on the poor performance of high-end products. Regional department stores have put up the shutters in quick succession, while major department store Mitsukoshi Ltd is considering a substantial payroll cut. When households can secure stable income, falling prices should be favourable for consumers by heightening their purchasing power. However, recent circumstances do not allow people to bask in such affluence.

Western Australian Agrifood and Fibre Market Outlook — Japan

3

Australia is the only major economy to avoid recession during the global financial crisis and the Reserve Bank of Australia is among a handful of central banks to start tightening policy settings.

In response to the quicker recovery of Australian economy from financial crisis, the Australian dollar is expected to get stronger in relation to other currencies. This is not favourable for Australian exporters.

40

60

80

100

120

140

160

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Yen

USD/JPY AUD/JPY

Figure 1 Exchange Rate USD/JPY and AUD/JPY Source: Bank of Tokyo—Mitsubishi UFJ Exchange Quotations

Consumer trends

Population declining The natural attrition of Japan's population hit a record in the year through 31 March 2009, while the ranks of the working generation continued to plumb new lows.

The results show that the total number of births dropped for the first time in three years to 1.08 million in 2008. The aggregate number of deaths reached a record 1.13 million. The resulting net decrease of 45 914 far surpasses the decline of 29 119 in fiscal 2007.

Western Australian Agrifood and Fibre Market Outlook–Japan

4

By age group, those 14 or younger totalled just 17.2 million, the lowest ever. People in the productive ages from 15 to 64 totalled a record low of 81.65 million. This figure has been on a steady downtrend since the first survey in 1994. The number of people 65 or older rose to a record 28.21 million.

As a result, working age people accounted for just 64.25 per cent of the total population, the lowest among industrialised nations. In 1994, the figure stood at nearly 70 per cent. The continuing decline is a major concern because it will increasingly put pressure on the national pension and medical insurance programs.

Fifty-six per cent of Japan's total population now belong to the 40-and-older crowd. Not surprisingly, these 71.6 million people are swaying market trends. Moreover, their ranks are growing, having expanded by 2.5 million from 2005.

Clearly, at a time when the domestic market is shrinking, the senior segment is fast becoming fertile ground for firms in a wide variety of areas.

Key consumers The domestic market for eyeglasses is a good place to look at the growing influence of older people. In 2008, the eyewear market shrank more than 20 per cent to slightly over 420 billion yen (A$5.25 billion). Purchases of reading glasses, however, have been surging among people aged 45 and up. Since 2007, the demographic has been outstripping younger consumers in terms of total glasses purchases. On a unit basis, people in the 45 or older bracket purchase glasses more than do those under 45, according to eyewear industry sources.

Western Australian Agrifood and Fibre Market Outlook — Japan

5

According to an estimate by the Japan Research Institute, senior households—where the head of the house is 60 or older—will be responsible for 40 per cent of all consumption in Japan in 2009. What is more, the senior market will jump 30 per cent by 2025 compared to 2000.

Overall, seniors are satisfied with their material wealth but are looking for something deeper connections. An opinion poll conducted by the Cabinet Office found that 44 per cent of people in their 20s are seeking material wealth, in sharp contrast with 66 per cent of seniors in their 60s searching for emotional happiness.

Added convenience Gone are the days of convenience stores catering especially to young people. For Seven-Eleven Japan Co., customers in the 50-plus age bracket accounted for 26 per cent in fiscal 2008. That percentage is more than double the 10 per cent seen in fiscal 1993.

In sharp contrast, the proportion of young customers in their 20s has declined to just 25 per cent, a 12 point drop from fiscal 1993.

To meet the needs of older customers, Seven-Eleven Japan Co. (Japan's largest convenience store chain) started making price tags larger and shopping baskets lighter. Rival convenience store chain Lawson Inc., meanwhile, began expanding aisles and setting shelves lower.

The attempts by stores to lure older customers do not stop there. Many convenience store chains are rushing to develop prepared meals for seniors, especially bento box lunches. Wagashi, or Japanese-style sweets, are also occupying more shelf space.

As the number of working families in Japan increases, the demand for convenient foods such as ready-to-eat meals is growing.

Smaller packages Prepared rice packs are gaining popularity among seniors thanks to their ease of use—you just pop them into an electric oven for a few minutes. Frozen food maker Katokichi Co. boosted production of the packs by 20 per cent in August and started to sell prepared rice in 150-gram packs, 50 g smaller than ordinary ones. Most buyers are in the 50-plus bracket.

Western Australian Agrifood and Fibre Market Outlook–Japan

6

With an eye on elderly people as well as singles, many food manufacturers and retailers are making their offerings smaller and are selling some products individually. Ajinomoto Co., for example, began selling three instant soup powders in individual packs.

Food safety On the other hand, the Japanese are a health-conscious race, and food safety is becoming as important as food quality in purchasing decisions. Over the past five years, many new regulations aimed at increasing food safety have been introduced. Even local food processors struggle to keep pace with the changes imposed by the new regulations.

Health scares caused by cases of Escherichia coli 0–157, spoiled dairy products, bovine spongiform encephalopathy (BSE), more recent cases of pesticide-contaminated frozen dumplings imported from China and melamine contamination in Chinese dairy products have heightened consumer awareness in relation to food products. Consumers are paying much more attention to food safety.

0

10

20

30

40

50

60

Safetyconscious

Low price Products madeonly fromdomesticproduces

Healthconscious

Convenienceconscious

%2008 Jan2008 MayFuture

Figure 2 Food production aims of companies for food production (survey May 2008) Source: Agriculture Forestry and Fisheries Finance Corporation

0

10

20

30

40

50

60

Safety Economic Preferdomesticproduces

Healthconscious

Easy-to-use Home made

%

2008 Jan2008 MayFuture

Figure 3 Consumer preferences when making food choices (survey May 2008) Source: Agriculture Forestry and Fisheries Finance Corporation

Western Australian Agrifood and Fibre Market Outlook — Japan

7

Marketing channels

Nakashoku vs Gaishoku The Japanese meals market can be divided into three categories:

• Nakashoku (retail): prepared meals sold at retail outlets including supermarkets, convenience stores and specialised food outlets

• Gaishoku (food service): meals eaten away from home (fast food, restaurants)

• Naishoku (retail): meals cooked at home from ingredients purchased at supermarkets

Fully cooked home meal replacement (called ‘nakashoku’) is positioned between food service (gaishoku) and home cooking (naishoku). Meals such as packed lunch/dinner boxes and everyday household dishes are sold at prepared food specialty shops, supermarkets and convenience stores, which are often open 24 hours a day.

8

8.1

8.2

8.3

8.4

8.5

8.6

2004 2005 2006 2007 2008 2009(E) 2010(E)

Year

Yen

(x tr

illio

n)

Figure 4 Nakashoku (prepared meal) market Source: Business Media Makoto

01,0002,0003,0004,0005,0006,0007,0008,0009,000

04 05 06 07 08(E)

Year

Yen

(bill

ion)

Convenience storesFood supermarketGeneral Merchadise StoreDepartment storeSpecialised shop

Figure 5 Prepared meal sales by outlet type Source: Japan Meal Replacement Association

Under the depressed economy in Japan for the past decade, eating out has levelled off or decreased slightly, whilst outsourcing food has increased. With social advancement of women and the increase in single-person households, home cooking will decrease and outsourcing for food, such as take out and meal delivery service, will increase.

Western Australian Agrifood and Fibre Market Outlook–Japan

8

The growth of nakashoku market has slowed down, but it still had some growth with consumers who are keen to get by on less, rather than eating out. The gaishoku (food service) market declined by 0.5 per cent in 2008 compared to 2007. The nakashoku market has grown because of a trend towards nuclear families, the ease of home meal cooking and relative cheapness. Since the burst of the economic bubble in the early 1990s, the food service market has been affected by the economic downturn. In recent years, diversification of consumer needs has given that market more impact, indicating that the food service market has reached further maturity and saturation.

Facing the severe slump in consumer spending, the biggest family restaurant chain operator Skylark Co. decided to delay the opening of new locations by one year and instead turn existing eateries into lower-priced restaurants.

The company concluded that it would not be able to generate sufficient profits by opening new locations when consumers are increasingly tightening their belts. Additionally, rivals have staked out prime locations near train stations to take advantage of falling rents, further intensifying competition.

8626

14634

19277

25676

2786728650 29070 28496

27388 2699225854 25448

24568 24483 24390 24552 24558 24432

5,000

10,000

15,000

20,000

25,000

30,000

75 80 85 90 95 96 97 98 99 00 01 02 03 04 05 06 07 08

Year

Yen

(x tr

illio

n)

Figure 6 Total value of Japanese food service market 1975–2008 Source: Japan Food Service Association

Western Australian Agrifood and Fibre Market Outlook — Japan

9

Online sales getting serious Japan's online population of more than 90 million gives the internet a penetration rate approaching 75 per cent. If this massive consumer class moves, merchandise, services and money move as well. The trick is to be there when it does.

Shifting online In August, a major supermarket chain, Summit Inc., closed a store in Chofu, Tokyo. Sluggish sales were not the reason. Rather, the supermarket operator is converting the location into a merchandise-processing and shipping centre for its online store. The centre is to reopen in October 2010.

‘A major share holder company of Summit Inc is aiming to develop the online business to 100 billion yen (A$1.25 billion) in sales in 2019..

Other companies have also begun working to build online businesses. Before the end of the year, Seven and I Holdings Co. will consolidate its Ito-Yokado Co. and Seven-Eleven Japan Co. websites, which until now have been independently developed. The huge retail conglomerate will build a new distribution location in Saitama Prefecture, and the site will list 5 million products. Customers will be able to pick up orders at Seven-Eleven stores, if they choose to.

Seven and I is positioning online shopping as a new pillar of earnings, alongside overseas store openings. It ‘will continue to pursue partnerships and merger-and-acquisition opportunities with companies having expertise in this area,’ an official said.

Japan's old-line retailers all aspire to build portals that perform like Rakuten Ichiba, Japan's largest shopping site. Rakuten Inc. enjoyed a record operating profit for the first six months of 2009, up 28 per cent from the same period a year earlier. On its busiest days, its transactions exceed three billion yen (A$37.5 million), the equivalent of three large department stores the size of Mitsukoshi Ltd's main emporium in Nihombashi, Tokyo. ‘Even with the poor economy, online sales are growing well,’ company President Hiroshi Mikitani said. Department store and supermarket chains, on the other hand, are under duress due to the recession and are being forced to close stores, pare staff and reduce operating hours. The more this trend takes root, the more attractive online sales will be. The internet is effectively open 24 hours a day.

Online sales in Japan have been climbing at more than 20 per cent, topping 6 trillion yen (A$75 billion) in fiscal 2008. Conversely, department stores and supermarkets have seen sales fall by around 20 per cent over the past decade.

Online as well as mail-order catalogue sales seem to have exceeded 8 trillion yen (A$8 billion) in fiscal 2008, surpassing convenience stores (nearly 8 trillion yen) and department stores (over 7 trillion yen).

Realignment and consolidation in the retail markets General retail trends indicate that there has been, and will continue to be, increased consolidation among companies. Many retailers seem to be looking to purchase direct from producers rather than through import agents and wholesale distributors.

Western Australian Agrifood and Fibre Market Outlook–Japan

10

Japan's top three convenience store operators—Seven-Eleven Japan, Lawson and FamilyMart—are battling for market share through alliances and acquisitions.

Convenience stores are one of the major food outlets in Japan, especially for prepared meals, lunch box catering, sandwiches and drinks. There has been remarkable growth in this outlet type over the years. However, the market may now be reaching maturity. Department store companies have been in dark tunnel for a long time and supermarket chain operators are also struggling.

An emerging trend across all sectors of the Japanese food industry is to invest in China and other Asian countries to expand sales growth as well as to secure food product and ingredient supplies.

Japanese firms looking for global scale need to strategically handle more than one type of product. Becoming more comprehensive is a way to survive and thrive, as demonstrated by Nestle SA, the world's largest food company. The merger between Kirin Holdings Co. and Suntory Holdings Ltd is likely to fuel further realignments in Japan's food industry.

Realignments ongoing in retailing As the global economic downturn increasingly weighs on consumers, Japan's retail chains are being forced to adapt to ever fiercer competition.

Convenience store chains, department store operators and large specialty retail groups are reaching out to their adversaries and even beyond traditional boundaries as they search for partners—and survival.

Japan is saturated with more than 40 000 convenience stores. Through 2007, sales declined at every chain for eight years in a row.

Third-ranked convenience store operator FamilyMart Co. and its top shareholder Itochu Corp. are finalising plans to purchase their smaller rival company, am/pm Japan Co.

Western Australian Agrifood and Fibre Market Outlook — Japan

11

FamilyMart, which has around 7600 locations throughout Japan, sees the acquisition boosting its competitiveness. Post takeover, FamilyMart will close in on No. 2 rival Lawson Inc. , which has a nationwide network of some 9700 locations, and overtake top-ranked Seven-Eleven Japan Co. in Tokyo, which is the biggest market.

Itochu, which owns a 31 per cent stake in FamilyMart, will be able to secure a customer for new products by sweeping am/pm under its umbrella.

Convenience store major FamilyMart Co. this summer became the first Japanese retailer to run more stores outside Japan than in its home market, with the exception of Seven-Eleven Japan Co., another popular convenience store chain that originated, however, in the USA.

While the retail sector is typically a domestic demand-oriented industry, FamilyMart's successful expansion into Taiwan and South Korea has been driven by a localisation strategy. This combines the parent firm's operating expertise with each country's eating habits and other traditions.

Now the company expects to use the expertise it has obtained in Taiwan and elsewhere to move into other key areas.

The Japanese convenience store industry is unlikely to grow due to the country's falling birth rate and rapidly aging population, as well as the saturation of convenience stores across the country.

‘We will look abroad for growth,’ FamilyMart President Junji Ueda said.

Tie-ups between major supermarket and trading companies

Major trading house Itochu Corp. is to obtain a 3 per cent interest in Uny Co., moving in to help the No. 4 Japanese supermarket operator develop a supermarket chain in China.

The alliance caps a recent string of tie-ups between trading houses and major supermarket chain operators, underscoring the potential benefits for partnering companies in both industries.

Western Australian Agrifood and Fibre Market Outlook–Japan

12

Uny intends to launch 10 to 20 Chinese stores starting in 2011. In addition, Itochu aims to help these stores by leveraging the nationwide procurement and distribution network of the Ting Hsin group, which holds the largest share of China's processed food market and in which Itochu holds a stake.

In Japan, Itochu and Uny will cooperate in the contract farming business, riding growing interest in food safety. Itochu has developed ties with various agricultural corporations and farmers through its contract farming business. Their crops will be sold through Uny, as well as regional supermarket allies Izumiya Co. and Fuji Co. The resulting increase in volume is expected to drive prices down.

In addition, the two firms plan to cooperate in the convenience store business. Itochu holds a roughly 31 per cent interest in No. 3 convenience store operator FamilyMart Co., while Uny owns a stake of about 47 per cent in fourth-ranked Circle K Sunkus Co. If these two major operators join forces in product procurement and other areas, they will likely be able to achieve significant cost reductions.

Itochu and Uny are expected to invite regional supermarkets to tie up with them as well, with an eye toward creating an alliance capable of competing with leading players like Seven and I Holdings Co. and Aeon Co.

Aeon, the No. 1 supermarket operator, formed capital ties with Mitsubishi Corp. in December 2008, when the trading company acquired a 5 per cent interest. In addition to investing in Aeon's distribution unit, Mitsubishi has been cooperating in the development of Aeon's private-brand products.

At Daiei Inc., product procurement from its top shareholder, Marubeni Corp., is forecast to increase 10 per cent to be worth more than 80 billion yen (A$1 billion) in the year ending February 2010.

Supermarkets are turning to trading houses to drive streamlining forward and beef up profitability as their struggles continue.

Aeon sustained a group net loss of 14.6 billion yen in the March–August half. Seven and I Holdings supermarket unit Ito-Yokado Co. sank into the red on an operating basis for that period as well.

Information held by trading houses on the real estate market and locations in China and other Asian countries is also of great interest to supermarket operators looking to expand into these growth markets.

Merger puts food companies on global path The envisaged merger between beer giants Kirin Holdings Co. and Suntory Holdings Ltd would create an entity capable of competing overseas with major Western players. It could also serve as a growth model for other domestic demand-focused firms struggling amid Japan's shrinking population.

Both Kirin and Suntory posted record profits in the fiscal year ended December 2008, thanks to strong sales of low priced, beerlike beverages as well as high-grade beers.

Western Australian Agrifood and Fibre Market Outlook — Japan

13

Despite being at the top of their game, the two companies nevertheless began considering a merger for one reason—Japan's falling birth rate and aging society. The population trend means there is a strong prospect that the domestic food and beverage market will contract over the long term.

Kirin has been on something of a merger and acquisition spending spree in recent years, having purchased National Foods Ltd of Australia, San Miguel Brewery Inc. of the Philippines and Australian brewery Lion Nathan Ltd. Suntory bought Cerebos Pacific Ltd, a major Singaporean health-food maker, and Frucor Beverages Group Ltd, a New Zealand energy drink maker. The resulting company should have more funds at its disposal to pursue more overseas M&As.

Kirin President Kazuyasu Kato said that the company to emerge from the merger between Kirin Holdings Co. and Suntory Holdings Ltd will strive to become a leading food purveyor in the Asia and Oceania regions.

Major beer brewer Sapporo Holdings Ltd will acquire a 21.65 per cent stake in unlisted beverage producer Pokka Corporation, creating a food-and-drink triumvirate with Meiji Holdings Co., which owns 22 per cent of Pokka.

Foreign operations will be a key consideration for the three-way alliance. More than 20 per cent of Pokka's revenue comes from abroad, including foreign markets where it boasts high market share such as Singapore. Meanwhile, Sapporo's beer operations have a strong base in North America, though the company is lagging in Asia. Meiji Holdings has been slow to expand overseas.

Aeon speeding into Asia The Aeon Co. group is hastening its expansion into Asia, looking to establish new foundations for growth outside Japan in preparation for the inevitable time when domestic growth potential wanes.

As part of this strategy, Aeon Mall Co. will open shopping centres in Vietnam, adding that nation to a list that already includes supermarkets in China, Thailand and Malaysia. The first shopping centre will be located in Ho Chi Minh City and is expected to open by 2012. The facility will have dozens of tenants, anchored by a Jusco supermarket.

Western Australian Agrifood and Fibre Market Outlook–Japan

14

Seven and I aims to boost its Chinese sales Seven and I Holdings Co. plans to boost its Chinese sales to an annual 400 billion yen or so in fiscal year 2014, five times the fiscal 2008 figure, through rapid openings of convenience stores, supermarkets and restaurants.

With domestic retailers struggling amid deflation and the greying of Japanese society, Seven and I has set its sights on the Chinese market. It plans to increase its convenience stores there to more than 500 in three years and to accelerate supermarket and restaurant openings.

The retailer now operates 100 convenience stores in China. Seven-Eleven Japan Co. opened its first Chinese outlet in Beijing in 2004. The chain expanded into Shanghai in April 2009 under a franchise contract with a Taiwanese retailer and into Tianjin in September 2009. The goal is to have 500 stores in these three metropolises and to move into other cities, such as Chengdu.

A subsidiary, Ito-Yokado Co., has nine stores in Beijing and four in Chengdu. The Chengdu operations saw their sales grow 30 per cent on the year in fiscal 2008. The general supermarket operator plans to open two more in each city within three years and is considering openings in other inland cities and north-eastern locations.

Seven and I opened its first family restaurant in Beijing in July 209, with plans to expand to 30 locations in the nation's capital in three years.

The retail giant's convenience store, supermarket and restaurant businesses will deepen their cooperation in such areas as product procurement.

Western Australian Agrifood and Fibre Market Outlook — Japan

15

Japan’s agrifood, fibre and fisheries imports Japan is the second biggest economy after the USA. It is also the world's largest net importer of agrifood products with a population of 128 million people. A shortage of arable land and increasing labour and production costs have led to Japan’s growing dependency on agrifood imports. Japan’s food self-sufficiency ratio is declining as consumer eating habits change. Japan now imports 60 per cent of its food.

Japan imported A$79 billion of agrifood and fibre products from all over the world in 2008. It is important to note that imports have increased by 20 per cent from 2007. Imported food is in very tough competition with the food products from other countries and local production.

Table 1 Japan’s agrifood, fibre and fisheries imports 2008

Product Value (A$M) Suppliers

1 Fish and crustaceans 13 993 USA, Russia, China

2 Cereals 12 270 USA, Australia, Canada

3 Meat and edible offal 10 034 USA, Australia, Brazil

4 Edible preparations: meat, fish 5 605 China, Thailand, USA

5 Beverages 3 542 France, USA, Italy

6 Fruit, nuts and peel 2 929 Philippines, USA, New Zealand

7 Vegetables, roots and tubers 2 028 China, USA, New Zealand

8 Coffee, tea and spices 1 969 Brazil, Colombia, China

9 Dairy, eggs and honey 1 817 Australia, New Zealand, USA

10 Sugar and sugar confectionary 907 Thailand, Australia, USA

Source: Global Trade Information Service 2009

The top suppliers of agrifood and fibre products to Japan were the United States (28 per cent), China (12 per cent), Australia (8 per cent), Canada (7 per cent) and Thailand (5 per cent).

Western Australian Agrifood and Fibre Market Outlook–Japan

16

Australian and Western Australian agrifood export performance Japan is one of Australia’s largest agrifood markets and was valued at A$5265 million in 2008–09. Western Australia’s agrifood exports to Japan were valued at A$769 million in 2008–09, making Japan the state’s second biggest export market after Indonesia. Western Australia contributed approximately 15 per cent of Australia’s agrifood exports to Japan in the last fiscal year.

Western Australia exports a variety of produces to Japan, but the main exports are wheat, barley, cereal hay, canola and crayfish, which together constituted 84 per cent of Western Australia’s total value of exports to Japan. Unfortunately, wheat and crayfish showed a relatively big decline in the export value in 2008–09 from 2007–08. Japan was Western Australia’s largest export market on beef, cereal hay and prawn in 2008–09.

Japan has been a very important market for Western Australia’s grain industry for a long time. In 2008–09, Japan was Western Australia’s fourth largest wheat export market (A$288 million) accounting for about 11 per cent of Western Australia’s total wheat exports. Japan is also the second largest export market for Western Australian barley, valued at A$158 million in 2008–09 and accounting for about 31 per cent of Western Australia’s total barley exports.

In 2008–09, Western Australia exported A$60 million of canola, A$23 million of malt and A$8 million of lupins to Japan accounting for 11 per cent, 13 per cent and 19 per cent of total Western Australia’s exports respectively.

Japan was Western Australia’s largest cereal hay export market, valued at A$104 million about 75 per cent of Western Australia’s total cereal hay exports in 2008–09. Western Australia’s cereal hay exports to Japan have been growing steadily for last five years. The export value in 2008–09 increased by around 50 per cent from 2004–05.

Japan is also an important market for Western Australia’s seafood industry. In 2008–09, Japan was Western Australia’s largest prawn export market (A$12 million) accounting for 63 per cent of Western Australia’s total prawn exports. Western Australia’s prawn export showed more than 70 per cent increase in value as compared to the last two years. Although there has been a gradual decline in Western Australia’s crayfish export to Japan over the past five years, it is still about 14 per cent of Western Australia’s total crayfish export in 2008–09.

In 2008–09 Japan was Western Australia’s largest beef export market, valued at A$34 million accounting for 23 per cent of Western Australia’s total beef export. Western Australia exported A$6 million of lamb to Japan in the same fiscal year.

Japan was a major importer for Western Australian dairy industry for a long time since Western Australia was the largest ice cream exporter for Japan in Australia. Western Australia’s ice cream export to Japan declined by more than 80 per cent in 2008–09 compared to 2004–05 because a major exporter has almost pulled out of this business.

Western Australian Agrifood and Fibre Market Outlook — Japan

17

Table 2 Western Australia’s top 10 export value agrifood products to Japan 2008–09

Product Value (A$m) Proportion of total (%) Japan's ranking Change from 2007–08 (%)

1 Wheat 288 37.40 4th -23.60

2 Barley 157.9 20.50 2nd 28.40

3 Cereal Hay 103.8 13.50 1st 29.20

4 Canola 59.5 7.70 4th 12.50

5 Crayfish 35.7 4.60 3rd -20.20

6 Beef 33.5 4.40 1st 15.30

7 Malt 22.7 3.00 4th 2.40

8 Prawns 12.4 1.60 1st 73.30

9 Lupins 8.3 1.10 2nd 178.30

10 Lamb 6.2 0.80 7th 38.20

Others 40.77 5.30 -2.20

Total 769.1 100.00 -5.30

Source: ABS and DAFWA estimates

0

1,000

2,000

3,000

4,000

5,000

6,000

2004

/2005

2005

/2006

2006

/2007

2007

/2008

2008

/2009

Year

A$M

Rest of Australia

WA

Figure 7 Western Australian share of total Australian agrifood exports to Japan 2004–05 to 2008–09 Source: ABS and DAFWA estimates

Western Australian Agrifood and Fibre Market Outlook–Japan

18

Market opportunities and future outlook for Western Australian agrifood products

Wheat and barley

Wheat and barley import system Wheat and barley imports are still fully controlled by Japan MAFF (Ministry of Agriculture, Forestry and Fisheries) and very high tariffs are imposed on wheat, barley and wheat flour not imported through MAFF’s tender system.

From 2006 all barley (1 to 1.1 million tonnes) and wheat (50 000 to 100 000 tonnes) imported for feed purposes have to be imported under the SBS (Simultaneous Buying and Selling) tender system. From April 2007 barley for feed and food and some wheat for food commenced being imported though the SBS system. Under the SBS system, a Japanese importer and Japanese end user work together to bid their two prices simultaneously. The importer gives its selling price to MAFF and the user gives its buying price to MAFF. Basically, the combination with the biggest mark-up wins the bid for the tender and the planned import quantity of each tender set by MAFF is filled.

Most imports of wheat for food including ASW from Western Australia, however, are still conducted under the original MAFF tender system where the importer who bids at the lowest price to MAFF wins the tender. Under the current MAFF Weekly Tender system, the quality aspects of different varieties are not taken into account. As long as the shipper offers the correct specification for the ASW grade, they win or lose the tender on price alone.

Under the current import system, MAFF is responsible for storage risk, as opposed to the SBS system where the user is responsible for any storage risk in Japan. There are more than 90 wheat flour milling companies that mill less than 30 000 tonnes of annual flour production. Those small and medium sized companies are against shifting to the SBS system because they might lose their business. They may be the main reason why the wheat flour industry in Japan is reluctant to support shifting ASW trade to the SBS system.

The general view is that imports of wheat for food will be shifted to the SBS system within three years. In the meantime, MAFF is trying to shift to a temporal import system (so called 'Immediate Selling system') which passes most of the responsibilities in the management of inventory and shipment/vessel (18 ports for wheat and 25 ports in Japan) to the private sector (trading companies and wheat flour companies). The structure of MAFF that earns the mark up will be retained even if it is completely shifted to the SBS system.

The top four wheat flour milling companies (Nisshin, Nippon, Showa, Nitto Fuji) almost dominate the market at 74 per cent. With changes in the import system, the shakeout of firms will continue further.

Wheat Total wheat flour consumption in Japan has levelled off at about 4.6 million tonnes, with some decline in recent years.

From April 2007, a limited tonnage of wheat (Prime Hard from Australia and Durum from Canada) for food purposes was planned to be imported via the SBS tender system. However, due to a drought in Queensland, supply of Prime Hard was inadequate to meet the tender and a much smaller tonnage has been exported in containers. Approximately 400 000

Western Australian Agrifood and Fibre Market Outlook — Japan

19

tonnes of wheat are expected as imports to Japan via the SBS system in 2009, similar to 2008.

Prime Hard (PH) from Queensland is the preferred wheat for Chinese noodles and sheets for dumplings. However, there has been a shortage of PH and Dark Northern Spring (DNS) from the United States has made up the shortfall.

As for the quality of ASW wheat imported in 2009, a major user advised that the quality on the first few shipments was not as good as before. Some companies rejected to receive the wheat. Their complaints included the fact that

● unable to make udon noodle with usual good 'creamy golden' colour; it was dull and a bit too white.

● the texture did not have good viscosity; they had to feel some hardness in the udon noodle. shrine

Since then, there has not been a major issue in quality for the rest of the season.

Table 3 Japanese Government’s wheat imports by type (wheat grade) (unit: 1000 tonnes)

FY Type (Grade) 2003 2004 2005 2006 2007 2008

World total 5 061 4 979 4 787 4 960 4 896 4 863

USA WW 571 646 425 426 773 710

HRW (11.5) 921 885 704 823 908 791

HRW (13.0) 200 161 144 62 – –

DNS 1 168 1 066 1 304 1 414 1 264 1 441

S. total 2 860 2 758 2 577 2 726 2 945 2 942

Canada CW 798 896 919 860 878 826

DRM 205 196 223 226 217 293

S. total 1 004 1 092 1 142 1 086 1 095 1 119

Australia ASW 971 881 815 872 761 727

PH 226 249 253 275 92 72

S. total 1 198 1 129 1 068 1 148 853 799

Source: MAFF

Japanese domestic noodle wheat production, which is in direct competition with Western Australian noodle wheat, deceased 3 per cent (28 900 tonnes) to 881 200 tonnes in 2008 from the previous year due to unfavourable weather in growing season in Hokkaido. It is expected that this level of production will be maintained.

Rice flour production has been promoted by the government and the production of rice flour has been increased to 9500 tonnes in 2008 from 1000 tonnes in 2003. The rice flour is mainly used for bread, noodle and cake.

Western Australian Agrifood and Fibre Market Outlook–Japan

20

0

20

40

60

80

100

2000 2001 2002 2003 2004 2005 2006 2007 2008

Fiscal Year

Production Area

Figure 8 Domestic wheat production (unit: 10 000 tonnes, 10 000 ha) Source: MAFF

Flour production for noodles (fresh, frozen, dry and instant)

Total flour consumption for noodles has steadily declined since 1996 from 1.46 million tonnes to 1.28 million tonnes in 2008. Some increase in flour consumption has been seen for dry and frozen noodle at the expense of the fresh noodles.

2008 flour consumption by end use (previous year)

● Fresh and frozen noodles—586 778 tonnes (596 006)

● Dry noodles—202 139 tonnes (199 154)

● Instant noodles—323 326 tonnes (353 931)

Western Australian Agrifood and Fibre Market Outlook—Japan

21

Table 4 Wheat flour production (tonnes) by noodle type Udon Chinese noodle Japanese noodle (soba) Production Change (%) Fresh noodles

Fresh Cooked Fresh Cooked Steamed Dumpling wrap Fresh Cooked 2000 1 420 768 -0.9 686 719 33 319 216 747 187 681 60 506 97 414 23 333 25 387 42 332 2001 1 440 843 1.4 696 464 35 129 218 410 194 449 59 575 97 708 22 468 24 316 44 410 2002 1421 473 -1.3 684 968 34 289 215 399 193 994 54 792 96 059 22 411 23 978 44 045 2003 1 424 719 0.2 675 212 35 303 218 834 184 847 52 062 100 041 20 266 22 978 40 882 2004 1 413 555 -0.8 660 619 35 420 210 675 178 204 53 621 99 929 20 162 20 808 41 801 2005 1 367 960 -3.2 631 161 33 201 206 412 168 149 49 916 97 925 18 321 19 224 38 012 2006 1 323 601 -3.2 602 810 31 536 202 040 155 084 50 786 93 792 15 800 18 055 35 716 2006 1 323 601 -3.2 602 810 31 536 202 040 155 084 50 786 93 792 15 800 18 055 35 716 2007 1 319 118 -0.3 596 006 32 683 197 138 155 658 47 702 95 450 15 286 17 593 34 496 2008 1 277 165 -3.2 586 778 32 970 196 217 158 081 43 737 93 800 14 208 15 607 32 157

Tenobe Dry noodle Udon Hiramen Hiyamugi Somen

Udon Hiyamugi Somen Chinese Japanese Instant

noodle Pasta

242 047 51 730 5 184 27 225 40 153 67 691 5 611 44 453 336 684 168 314 235 072 50 205 5 125 25 834 39 619 65 331 6 143 42 815 342 933 156 044 238 512 47 869 5 063 26 099 41 543 70 006 5 660 42 269 356 377 149 490 226 373 45 653 4 116 22 552 37 145 67 830 5 423 43 654 356 375 153 757 230 295 49 338 3 920 20 951 38 763 66 762 6 564 43 998 364 836 154 376 228 428 48 779 3 421 21 123 41 496 4 737 3 992 52 826 6 900 45 153 368 003 156 505 220 257 45 761 3 050 18 658 41 728 4 638 4 010 54 137 7 023 41 253 355 606 160 936 203 264 44 925 2 786 17 918 42 193 3 222 3 379 44 036 7 127 37 718 350 007 167 521 199 154 43 064 2 632 17 380 38 656 3 828 3 642 44 490 7 762 37 700 353 931 170 027 202 139 44 079 2 806 18 024 39 842 3 535 3 199 45 537 9 061 36 055 323 326 164 925

Source: General FMAMAFF Note: Tenobe: Manual stretching process with two sticks is required. Hiyamugi and Somen are thinner than Udon or Hiramen. Somen is thinner than Hiyamugi.

Table 5 MAFF's sales of barley by food use

2002 2003 2004 2005 2006 2007 2008 Shochu 188 209 250 214 372 87 220 Barley tea 33 23 25 24 40 26 26 Beer 27 15 32 16 18 20 45

Source: MAFF

Western Australian Agrifood and Fibre Market Outlook — Japan

22

The Japanese import of wheat flour-based premix was growing steadily as a cheap substitute for wheat until the mid-1990s. However, the import has been decreasing after 2006 due to the price rise caused by recent rise of international wheat price. The import quantity in 2008 dropped by 14.4 per cent from previous year to 100 000 tonnes. Australia was the fifth biggest exporter with 8.5 per cent of share in 2008.

Barley Of the 1.3 to 1.4 million tonnes of barley imported by Japan per annum, approximately 1.0 million tonnes is used for animal feed and 0.3 million tonnes is used for human consumption, including the alcoholic beverage shochu. Barley is used for animal feed after steaming and rolling. Barley for shochu is processed by barley refining processors before distributing to shochu makers.

0

50

100

150

200

250

300

350

400

‘02 ‘03 ‘04 ‘05 ‘06 ‘07 ‘08

Year

'000

T ShochuBarley TeaBeer

Figure 9 MAFF’s sales of barley by food use Source: MAFF

Table 6 MAFF’s sales of barley (tonnes) by use

FY 2002 2003 2004 2005 2006 2007 2008 USA Two 2 USA naked 0.3 Canada Two raw 5 10 5 11 Canada Six raw 4 15 2 1 Canada naked 1 Australia Two raw 188 209 250 205 347 77 208

Shochu

S. total 188 209 250 214 372 87 220 Canada Six 26 18 20 20 35 25 25 Australia Two 7 5 5 4 5 1 1

Barley Tea

S. total 33 23 25 24 40 26 26 Canada Two 7 7 7 21 Australia Two 24 8 22 9 16 13 24 USA Two 3 7 3 2

Beer

S. total 27 15 32 16 18 20 45 G. Total 248 247 307 254 431 133 291

Source: MAFF

Western Australian Agrifood and Fibre Market Outlook — Japan

23

Barley for human consumption (beer and shochu alcohol) Regular beer consumption has been gradually declining after peaking in 1994. Alcoholic beverage consumption is declining in Japan due to fewer drinkers among young people and the ageing of the generation of big drinkers. Consumer preferences are moving away from consumption of beer due to the trend towards healthy lifestyles.

Table 7 Volume of sales of alcoholic beverages in Japan (1000 kL)

2003 2004 2005 2006 2007

Sake 826 746 719 688 664

Shochu 921 983 999 1 000 1 005

Beer 3 783 3 617 3 408 3 304 3 215

Whiskeys 112 100 94 90 85

Fruit wine 247 234 247 238 239

Low malt beer 2 403 2 213 1 679 1 516 1 473

Total 8 292 7 893 7 146 6 836 7 836

Source: National Tax Office

Major breweries are stepping up production of no-malt beer to quench the thirst of increasingly thrifty consumers who favour those low priced varieties over pricier regular beer. A 350 ml can of no-malt beer sells for around 140 yen, which is roughly 30 per cent less than regular beer. Many consumers have switched from regular to no-malt beer ever since the economic downturn became pronounced last fall. No-malt beer shipments for the January-June period jumped 27.4 per cent on the year, while shipments of regular beer dipped 5.5 per cent.

No-malt beer now accounts for almost 30 per cent of the overall beer market. By 2008, the country's beer market had shrunk 16 per cent from its 1994 peak, reflecting the falling birth rate and a shift among young consumers away from beer. Kirin Brewery Co.'s beer-flavoured beverage containing no alcohol has been boosting the market for such drinks and prompting other major brewers to come up with new products for the emerging segment.

Shochu (a distilled spirit made from raw materials such as barley, sweet potato, rice or buckwheat) and chuhai (shochu mixed with soda water and flavoured syrup), which have a lower alcohol content, are becoming more popular. Australia is the dominant supplier of barley to Japan for the shochu market. The shochu market as a whole has entered a period of maturity and further increases in the market are not anticipated. With regard to Japanese malting barley (for shochu) import from Australia, it is estimated that Japan purchases 160 000 tonnes from Western Australia and 40 000 tonnes from the eastern states each year.

In Japan most of the two row barley crop is used for shochu production. Barley with high starch content that delivers high alcohol production is appreciated for shochu production. Australian barley has an advantage on this point and is highly rated by users. The users want hard barley because high yield percentage is obtained at the time of barley processing (pearling). Western Australian Starling barley is also highly rated on the hardness. However, the current main varieties such as Starling from Western Australia and Schooner from South Australia are getting old and good varieties to take the place of the old varieties are expected. A major barley refiner (processor) for shochu has advised that Western Australian Bauden is very similar to Starling in quality characteristic and should be acceptable as its successor. However, they are concerned that Bauden has a bit higher broken grain at the time of pearling and tends to be a bit thinner in grain size (under 2 mm).

Western Australian Agrifood and Fibre Market Outlook — Japan

24

A barley processing association advised that the colour of 2008–2009 WA barley was not so attractive–rather they were dull in colour and the broken barley ratio after pearling process was higher than usual. This result could be caused by unfavourable climate during growing season and harvest time last year.

Table 8 MAFF’s import of barley for food (1000 tonnes)

2003 2004 2005 2006 2007 2008 Australia 216 286 216 324 91 257 Canada 20 20 43 49 38 74 USA 4 3 2 2 0.3 Total for year 240 309 259 375 131 331

Source: MAFF

Barley for feed Of the 1.0 to 1.1 million tonnes of barley imported for feed, about 70 per cent is used as an ingredient of stockfeed (compound mixed feed) after steaming and rolling. The remaining 30 per cent of barley for feed purposes is distributed to livestock farmers as a single component feed (direct feed) after either steaming and rolling or grinding roughly (less than 2.5 mm mesh). Barley for compound mixed-feed use is increasing, but it is difficult for Japanese beef consumption per capita to be expanded greatly. The increasingly ageing population and decline of the total population will affect the feed requirements for the livestock industry in the long term.

Under the SBS system, MAFF has increased the list of preferred suppliers to meet the diversified range of needs from users. Traditionally, feed barley was sourced from only three countries, the USA, Canada and Australia but there have been imports from other countries such as Russia and Ukraine. Toyota Tsusho Corp. plans to import milling wheat from Kazakhstan to Japan for the first time to diversify its supply sources as food demand increases in Asia. The company studied routes from Kazakhstan after a trial delivery of 3800 metric tonnes of feed barley from the central Asian nation in October 2009 while grain exporters in Kazakhstan as well as Russia and Ukraine restricted shipments in 2008 to secure the supply for local consumption or to curb food inflation.

Western Australian Agrifood and Fibre Market Outlook — Japan

25

It is estimated that Japan purchases 300 000 to 400 000 tonnes of feed barley from Western Australia each year.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2003 2004 2005 2006 2007 2008

Year

Tonn

es

United States Australia CanadaOthers

Figure 10 Barley imports by Japanese government for feed purposes Source: Global Trade Information Service 2009

Baled hay and cereal straw Japan has been a consistent importer of baled hay and straw which is used as a good roughage feed for dairy and beef cattle. In 2008 Japan imported 2.10 million tonnes of baled hay.

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Year

tonn

e

Beet pulp pelletsAlfalfa Hay cubesStraw Baled hay

Figure 11 Japan’s roughage feed imports (includes baled hay, straw, hay cubes and BPP) imports Source: Global Trade Information Service

The market has been growing very rapidly for the past 20 years but in 2008 baled hay imports decreased by 139 004 tonnes, down 6 per cent from the previous year. Japan’s total roughage feed imports have been declining for the last five years (Figure 1).

Western Australian Agrifood and Fibre Market Outlook — Japan

26

This was mainly due to increased commodity prices and stock feed prices last year and Japanese livestock farmers have been in a difficult situation from various reasons. Japanese agricultural cooperative organisation has analysed that the dairy industry couldn’t cover their production costs in their operation due to a low milk price last year, but due to a revised milk price that have provided this year, the dairy farmers have just taken a pause. On the other hand, consumers tend to buy cheaper meat such as chicken and pork and beef farmers have been in the most difficult situation at present in the livestock industry due to the poor beef market

Other remarkable points shown in 2008 are that rice straw imports from China were very much increased to 161 562 tonnes because the price is attractive. The imports in 2008 were seven times higher than the previous year. Australian oat hay imports to Japan also increased to 434 099 tonnes in 2008 which is 8 per cent up from 2007; Western Australia captured the highest share of this increase. This was mainly due to increased price of USA sudan hay which competes with oat hay. The price of USA alfalfa hay (another main import in the baled hay category) is expected to go up due to the recovery of the USA market.

It is difficult to see how the hay and straw market will expand further given the decline in Japanese livestock production.

0

100,000

200,000

300,000

400,000

500,000

600,000

2004/2005 2005/2006 2006/2007 2007/2008 2008/2009

Year

tonn

e

WA Rest of Aust

Figure 12 Australian and Western Australian cereal hay exports to Japan Source: ABS and DAFWA estimates

Table 9 Japan’s baled hay and straw imports

Import (tonnes)

2005 2006 2007 2008 2008/07 (%)

Alfalfa hay 469 261 456 968 423 715 430 488 102 Sudan hay 318 216 309 477 370 536 358 855 97 Timothy 504 052 289 831 508 320 436 948 86 Rye straw 254 130 281 081 215 619 182 217 85 Fescue straw 111 934 106 303 90 206 81 109 90 Bermuda 101 622 106 927 139 573 95 253 68 Australian oat hay 539 077 538 300 400 899 434 099 108 Others 87 116 2 439 629 90 447 81 342 90 Total 2 385 408 2 439 629 2 239 315 2 100 311 94

Source: Feed Industry Newspaper

Western Australian Agrifood and Fibre Market Outlook — Japan

27

Canola Since Japan has been dependent on Canada for its canola supply (96 per cent of canola supplied by Canada in 2008), Australian canola exports to Japan have been developed as an alternative source. The Australian share of the canola supply to Japan has averaged 19 per cent from 2002 to 2008 in volume.

Between 2003–04 to 2007–08, Japan was Western Australia’s largest market for canola. In 2008–09 Japan imported 90 702 tonnes of canola from Western Australia, valued at A$60 million, making Japan the fourth largest market for Western Australia’s canola exports after the Netherlands, France and Pakistan. Western Australia has been dominant in Australian canola exports to Japan.

Non-GM and GM canola market in Japan In 2007, 86 per cent of the Canadian area sown to canola was sown to GM canola. Estimates of the current market size of non-GM canola in Japan vary from 30 000 to 80 000 tonnes. These estimates include approximately 15 000 tonnes of requirements from Consumers’ Co-ops and 8–9000 tonnes of a small oil crusher which specialises in non-GM canola oil. It is most likely that a minimum of 23 000–25 000 tonnes of non-GM canola will stay, if the price of non-GM canola doesn’t get too high.

J-Oils Mills and Nisshin Oillio are the two major Japanese users of Australian canola. A rough market share of vegetable oil in Japan is Nisshin Oillio: 35 per cent; J-Oil: 35 per cent; and Showa: 10 per cent.

At the February 2009 opening of Grain Pool’s Japanese office, representatives from J-Oils answered questions from the Western Australian Farm Weekly as follows:

● J-Oils is prepared to pay a premium for Australian canola to ensure canola supply if there are problems with supply of Canadian canola.

● Over the past five years there has been a premium for non-GM canola but the market for non-GM canola is small and diminishing. Only small non-GM niche markets are prepared to pay a premium for non-GM canola.

● The demand for non-GM canola oil is only 3–5 per cent of the total canola oil market in Japan. Japanese demand for non-GM foods is not in the oil market but in the processed food market, for example, tofu which must be labelled as GM. Oil derived from GM canola is not required to be labelled as GM in Japan.

If the Australian Government allowed cultivation of GM canola this would not affect J-Oils purchase of Australian canola.

Western Australian Agrifood and Fibre Market Outlook — Japan

28

0

500

1,000

1,500

2,000

2,500

'000

T

2002 2003 2004 2005 2006 2007 2008

Year

Canada AustraliaOthers

Figure 13 Japan’s canola imports Source: Global Trade Information Service

201.304982

140.31157

86.4108969.808728 65.189486

82.434569 67.171548 71.00624852.903812 59.510859

0

50

100

150

200

250

04/05 05/06 06/07 07/08 08/09

Year

A$M

WA Australia

Figure 14 Western Australian canola export trends for Japan Sources: ABS and DAFWA estimates

Red-fleshed grapefruit Grapefruit is the second largest (by volume) imported fruit into Japan, behind bananas. However, Japanese total imports of grapefruit have shrunk to 184 022 tonnes in 2008 from the peak of 554 841 tonnes in 1995 mainly due to a decrease of exports from the USA.

Research by Department of Agriculture and Food, Western Australia senior research officer Francis De Lima made a significant impact on international market access for citrus fruit from Australia. Japan accepted new cold treatment protocols for fruit fly, based on years of groundbreaking research led by Dr De Lima.

The department’s Kununurra office advised at the beginning of 2010 that verification for Red-fleshed grapefruit has been completed and sent to MAFF in Japan. If all goes well, exports will commence to Japan in 2010. We understand that the anticipated annual tonnage will be 10–12,000 tonnes of which approximately 50 per cent will be shipped to Japan. Other markets include Hong Kong, Taiwan and the EU.

Western Australian Agrifood and Fibre Market Outlook — Japan

29

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2003 2004 2005 2006 2007 2008

Year

tonn

e

United States South Africa Swaziland Israel Others

Figure 15 Japan’s import of grapefruit including pomelos, fresh or dried (tonne) Source: Global Trade Information Service

50

100

150

200

250

J F M A M J J A S O N D

Month

Yen/

kg

2005 2006 2007 2008 2009

Figure 16 USA grapefruit wholesale price in Tokyo wholesale markets Source: Tokyo Wholesale Markets

Western Australian Agrifood and Fibre Market Outlook — Japan

30

2008

0

200

400

600

800

1000

1200

1400

J F M A M J J A S O N D

Month

Tonn

es

USA South Africa Israel Others

Figure 17 Quantity by origin at Tokyo wholesale markets 2008 Source: Tokyo Wholesale Markets

Health food ingredients The Japanese Government is encouraging people to stay healthy, eat correctly and use health foods and supplements, rather than rely on government-sponsored prescriptions. As a result, imports of health food production ingredients are expected to increase rapidly. Trade and Market Services aims to create business opportunities for Western Australian producers in this area.

Western Australia’s clean, green image provides an opportunity for Western Australian exporters to exploit the Japanese organic and healthy food market. Suppliers who can verify that their products come from a clean, green environment with an ecologically friendly production system and who can differentiate their own products from others are well placed to take advantage of this market.

Investment attraction opportunities Agricultural production in Japan is declining at an alarming rate. The country’s food self-sufficiency ratio is also declining as consumer eating habits change. Japan now imports 60 per cent of her food from overseas, which is a massive amount. This structure is expected to continue. The Japanese Government is now thinking that it is necessary to promote agricultural investment in overseas countries as a way to ensure food imports, to diversify the origin countries and to improve its food security.

There are many examples of Japanese trading houses, food and beverage manufacturers and retailers who have invested their capital in agrifood and retail businesses in overseas countries. These movements have recently increased and are expected to continue as those domestic industries are realigned. Australia has been a good destination for investment in agrifood business.

Western Australian Agrifood and Fibre Market Outlook — Japan

31

These companies need overseas markets for their business growth. The domestic market and market size is predicted to decline, due to rapid aging of the population and decline in the birth rate.

Naturally all the eyes of the companies are on Asia which holds approximately 60 per cent of world population. As income rises in that market, especially in China, the importance as a consumption area will arise more and more.

Japanese companies also have to cultivate a more global view to develop off-shore trade and secure business expansion. Western Australia needs to attract those companies that will bring special value-adding technology in food processing to the State for increased trade development and investment.

Nation low in food self-sufficiency Food self-sufficiency refers to the ratio of domestically produced food to the nation's total food consumption in terms of calories. In fiscal 2007, Japan's figure was 40 per cent, down from over 70 per cent in the first half of the 1960s due to dietary changes—mainly from rice to bread as a staple food and fish to meat dishes—and increasing imports. The figure first fell below half to 49 per cent in fiscal 1989.

Looking overseas, in 2003 Australia's self-sufficiency rate was 237 per cent, followed by the USA, France and Canada (all over 100 per cent), Germany (84 per cent) and the UK (70 per cent). Japan's figure is exceptionally low among developed nations.

As population growth in emerging nations tightens food supplies worldwide, anxiety is justifiably growing in Japan over food security.

Japanese agriculture declining rapidly The proportion of Japan's agricultural land is shrinking, and fewer and fewer people are working the nation's remaining fields. Arable land is sitting idle, as if the growing global concerns about imminent food shortages are someone else's problem.

Land and labour are essential factors in agricultural production. Since its 1960 peak at 14.54 million people, Japan's agricultural population has been trending steadily downward. At just 2.98 million, the 2008 figure is down by nearly 80 per cent compared to the high.

Western Australian Agrifood and Fibre Market Outlook — Japan

32

From 1960 to 2008, the number of agricultural households fell by 58 per cent to 2.52 million, and it is less than 2 million if one leaves out small operations producing mostly for their own consumption.

Aging and dwindling workforce in the agricultural sector Along with the falling numbers of farming people and households, farmers are getting older. In 1983, about 40 per cent of the people in agriculture were 60 years old and older; today the percentage is over 70 per cent, and 60 per cent of them are over 65.

In the same period, the number of those in their 40s and 50s has fallen by half. Although the Japanese population as a whole is aging, but still less than 30 per cent are 60 and older.

‘If this continues, 60 per cent of Japan's agricultural workers will be over 75 in 10 years, making agriculture a sub industry,’ warned a former official of the Ministry of Agriculture, Forestry and Fisheries.

The decrease and aging of the agricultural population have led to a reduction in agricultural land. In 1961, agricultural concerns reached a peak with 6.09 million hectares (15.04 million acres) of land in production; by 2008 that had fallen to 4.63 million hectares.

Japan changes tack to fix food shortage In response to rises in the price of food, the number of starving people has increased in many developing countries (1 billion people in 2009). World population is expected to grow, especially in Asian and African countries, from 6.6 billion people in 2006 to 7.6 billion people in 2018. Furthermore, GDP per capita is also expected to increase from $7234 to $9303 in 2009. Under those circumstances, world demand for grains is predicted to grow by 500 million tonnes to 2.6 billion tonnes in the 12 years from 2006 to 2018. As it is difficult to catch up with the growth of the demand through breed improvement or increase of planted area, the total stock of world grains is expected to shrink over that period.

Western Australian Agrifood and Fibre Market Outlook — Japan

33

The Japanese Government thinks that it is important to increase the food production in the world and to expand agricultural investment while the supply and demand situation in food tends to be tight in medium and long term. They now believe that it is necessary to promote agricultural investment in overseas countries and to diversify the origin countries from food security point of view.

The Japanese Government has already set up special desks at the two Ministries in Japan, Ministry of Agriculture and Ministry of Foreign Affairs, to deal with proposals of overseas agricultural investment from private companies. The government is prepared to support them with several programs including diplomatic and financial assistance. Overseas Development Administration (ODA) should be promoted to increase the food production in developing countries.

After focusing for decades on oil, metals and minerals, Japan's huge trading houses are turning to agricultural commodities. They are enthusiastically supporting the shift amid concerns about local and global food security.

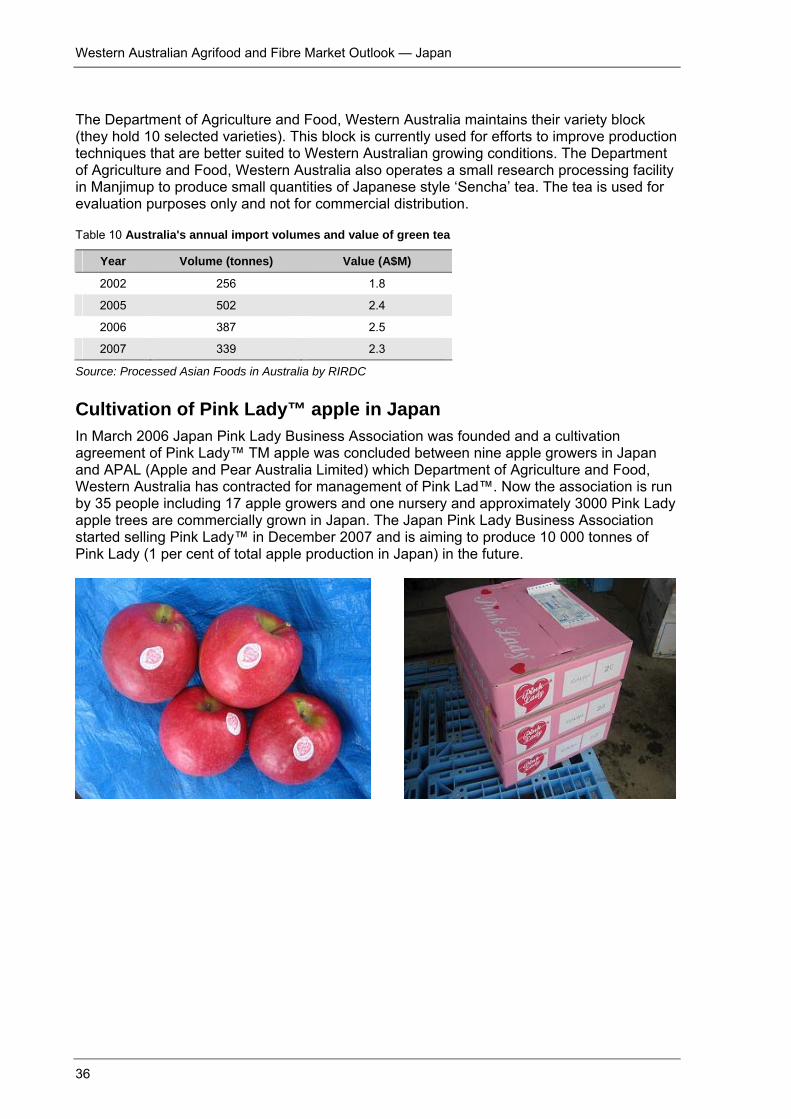

The move by general trading houses came as the Japanese Government prepared to launch plans last August to finance investment in food production overseas. Japan is the world's largest net importer of food, buying in more than $79 billion.

Among Japan's five mammoth trading houses, Mitsui and Co, Itochu and Marubeni are expanding into food commodities such as soybean, palm oil, wheat and corn.

‘The Japanese trading houses are … particularly investing in assets such as grain elevators and export terminals,’ says Philippe de Lapérouse, from USA-based agribusiness consultants HighQuest Partners.

The Japanese approach differs from countries such as South Korea and Saudi Arabia, which want to secure resources to feed their own populations. Rather, the trading houses want to increase global supplies by seeking opportunities abroad. Amid the global food crisis, having money does not necessarily guarantee the ability to obtain food. No matter how well developed domestic agriculture becomes, Japan simply will never be fully self-sufficient. However, the country can take steps to ensure a more stable food supply. One way is to take a ‘made by Japanese’ approach, in which domestic firms produce food products abroad for shipment to Japan. The recent overseas investments by Japanese food companies have other objectives. At a time when the Japanese market is shrinking because of a decline in population due to the falling birth rate and the ageing population, companies are more aggressively seeking overseas markets.

In August 2008 Japanese company Kirin Holdings Co. agreed to buy Australia’s second-ranked milk processor, Dairy Farmers, building on its purchases in the previous year of that country’s premier dairy firm, National Foods Ltd. Kirin aims to boost exports of dairy products to South-East Asia after expanding operations in Australia. The acquisition of Dairy Farmers will raise Kirin’s share of the Australian milk market from 37 per cent to 63 per cent and in the country’s yogurt market from 27 per cent to 55 per cent.

Itochu buys stake in Aussie dairy firm Itochu Corp. has acquired a 45 per cent interest in a mid-tier dairy company in Australia to produce milk powders for export to Japan, China and South-East Asia.

Western Australian Agrifood and Fibre Market Outlook — Japan

34

Figure 18 Itochu and Burra Foods will build a powdered milk factory in Australia.

Demand for dairy products is growing, particularly in China and other emerging nations as income levels rise. In anticipation of tighter market conditions, the trading house sought to secure a production base.

Itochu invested about 2.4 billion yen (A$30 million) in the holding company of dairy firm Burra Foods Australia Pty Ltd, becoming the second-largest shareholder after the founding family. Itochu also extended about 500 million yen (A$6.3 million) in loans to the holding company.

Burra Foods plans to build a powdered milk factory with an output capacity of 24 000 tons a year. Scheduled to go into operation in July 2010. the facility will make mainly powdered skim milk to be supplied to manufacturers of dairy products and foods. The ingredient is used in such items as ice cream, processed milk and yogurt.

Itochu poised to buy into leading China food firm In a bid to tap the strong growth potential of the Chinese food market, Itochu Corp. announced last November 2009 that it will acquire a 20 per cent stake in Ting Hsin group for 70 billion yen (A$875 million).

The leading Chinese processed food firm in terms of market share controls major food-related companies, including No. 1 Chinese instant noodle maker Tingyi (Cayman Islands) Holding Corp. and the operator of the FamilyMart chain of convenience stores.

Itochu will take the stake in Ting Hsin group through its holding company, Ting Hsin (Cayman Islands) Holding Corp.

Helped by its close relationship with Itochu, Ting Hsin has already established various local joint ventures with such Japanese firms as Asahi Breweries Ltd, Kagome Co., Nippon Flour Mills Co. and Shikishima Baking Co. Leveraging its capital ties with Itochu, Ting Hsin plans to bolster its partnerships with Japanese companies further across a wide range of areas, including sweets and spices.

Following a series of food scares, public interest in food safety has been growing in China. Demand for high-quality processed food has also been growing as the middle class continues to expand. By teaming up with Japanese companies and tapping their product development and manufacturing expertise, Ting Hsin aims to bolster its competitiveness.

Western Australian Agrifood and Fibre Market Outlook — Japan

35

In August, Itochu also formed a comprehensive business tie-up with major Chinese food company Cofco Ltd. The two firms are now holding talks to start joint procurement of wheat and dairy products. They are also looking to work together in the edible oil and meat processing businesses.

Mitsui inks feed materials tie-up with China's New Hope Group Last September 2009, Mitsui and Co. said that it has formed an alliance with Chinese agribusiness giant, New Hope Group, that will focus on such operations as importing feed ingredients into China.

Their cooperation will also extend to joint procurement and sales of feed in China, with Mitsui supplying compound feed technologies as well as access to distribution networks. Demand for dairy products and meats have grown in China alongside an improving standard of living, spurring the need for stable feed supplies.