Embed Size (px)

Citation preview

2009 Full-year results presentation

Analysts’ & Media Conference CallBasel, 16 February 2010

2STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

Disclaimer

This presentation contains certain “forward-looking statements”, which can be identified by use of terminology such as “expect”, “expectation”, “intend”, “continue”, “achieve”, “maintain”, “improve”, “foresee”, “anticipate”, “product introductions”, “outlook”, “forecast”, or similar wording. Such forward-looking statements reflect the current views of management and are subject to known and unknown risks, uncertainties, assumptions and other factors that may cause actual results, performance or achievements of the Group to differ materially from those expressed or implied herein. Should such risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those described in this presentation. Straumann is providing the information in this presentation as of this date and does not undertake any obligation to update any forward-looking statements contained in it as a result of new information, future events or otherwise.

3STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

Full-year highlights

Business performance

Product highlights and milestones

Outlook

Questions & answers

Agenda

Full-year highlights

Gilbert AchermannPresident & CEO

5STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

-15%

-5%

5%

15%

25%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Straumann Other leading implant companies*

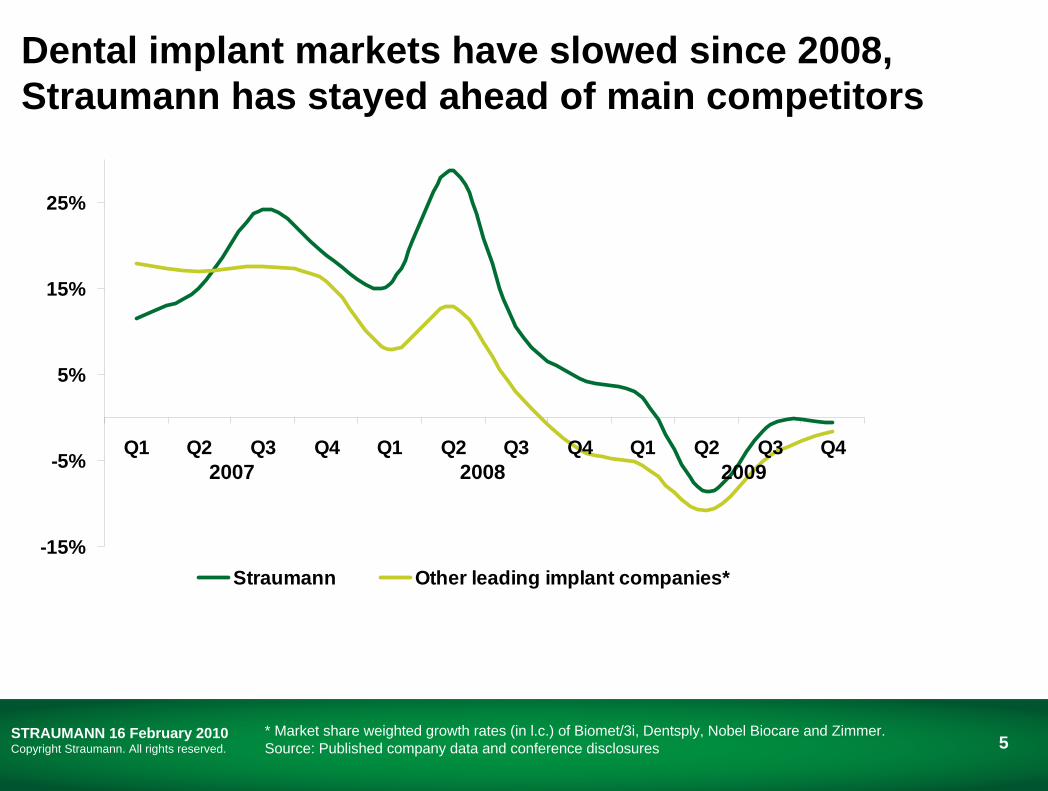

Dental implant markets have slowed since 2008, Straumann has stayed ahead of main competitors

* Market share weighted growth rates (in l.c.) of Biomet/3i, Dentsply, Nobel Biocare and Zimmer. Source: Published company data and conference disclosures

2007 2008 2009

6STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

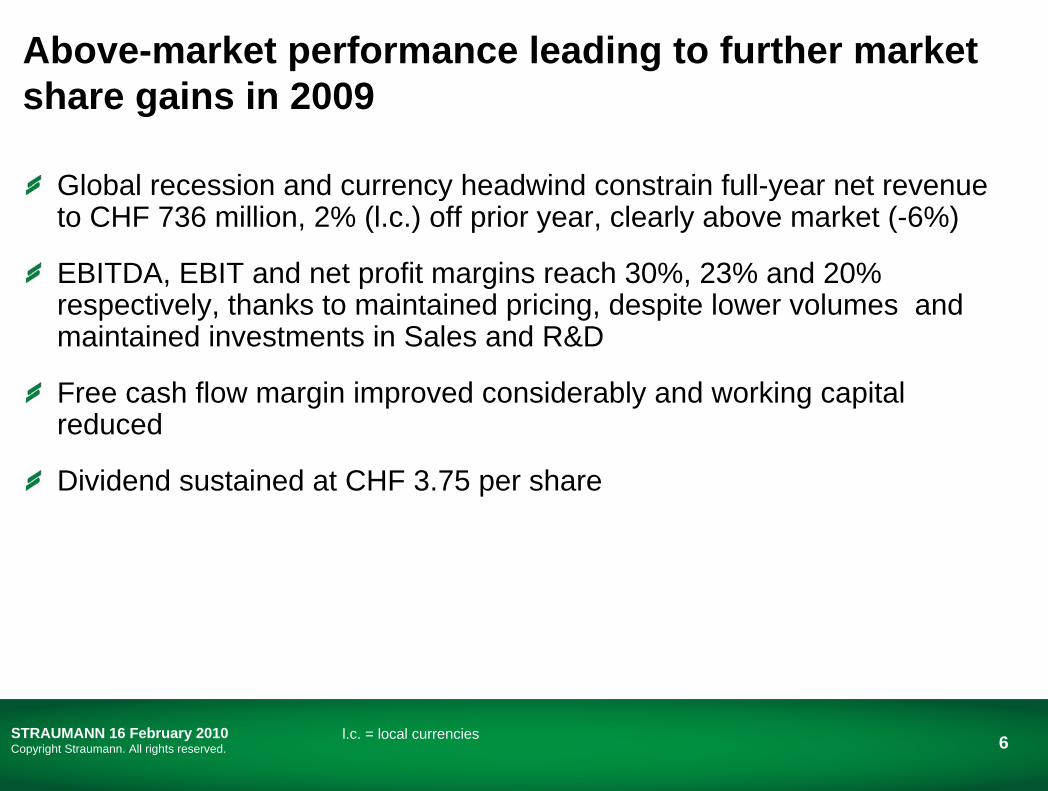

Above-market performance leading to further market share gains in 2009

Global recession and currency headwind constrain full-year net revenue to CHF 736 million, 2% (l.c.) off prior year, clearly above market (-6%)

EBITDA, EBIT and net profit margins reach 30%, 23% and 20% respectively, thanks to maintained pricing, despite lower volumes and maintained investments in Sales and R&D

Free cash flow margin improved considerably and working capital reduced

Dividend sustained at CHF 3.75 per share

l.c. = local currencies

7STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

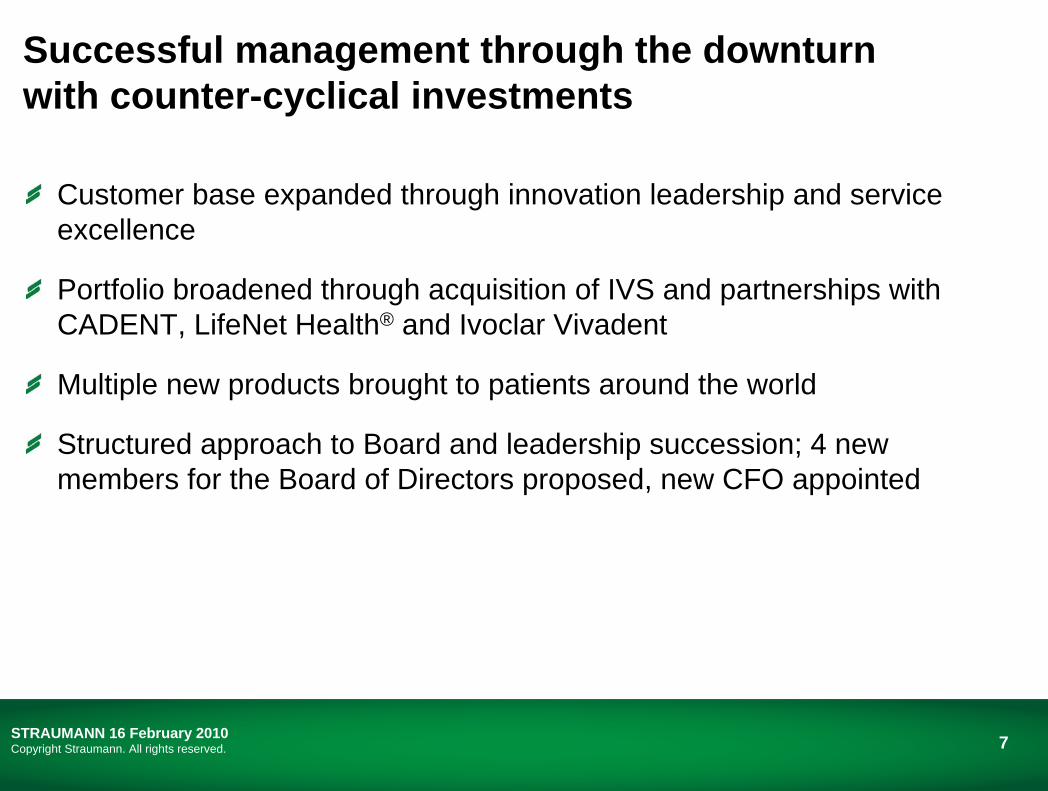

Customer base expanded through innovation leadership and serviceexcellence

Portfolio broadened through acquisition of IVS and partnerships with CADENT, LifeNet Health® and Ivoclar Vivadent

Multiple new products brought to patients around the world

Structured approach to Board and leadership succession; 4 new members for the Board of Directors proposed, new CFO appointed

Successful management through the downturn with counter-cyclical investments

Business performance

Beat SpalingerChief Financial Officer

9STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

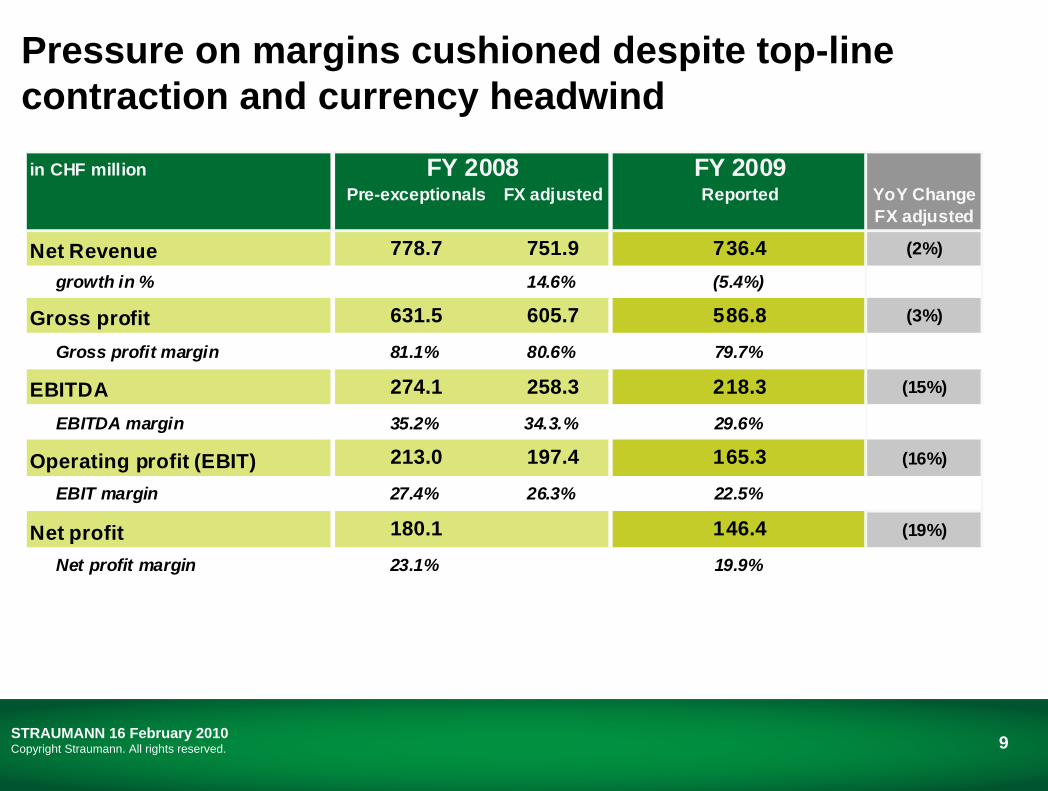

Pressure on margins cushioned despite top-line contraction and currency headwind

in CHF million FY 2009Pre-exceptionals FX adjusted Reported YoY Change

FX adjusted

Net Revenue 778.7 751.9 736.4 (2%)

growth in % 14.6% (5.4%)

Gross profit 631.5 605.7 586.8 (3%)

Gross profit margin 81.1% 80.6% 79.7%

EBITDA 274.1 258.3 218.3 (15%)

EBITDA margin 35.2% 34.3.% 29.6%

Operating profit (EBIT) 213.0 197.4 165.3 (16%)

EBIT margin 27.4% 26.3% 22.5%

Net profit 180.1 146.4 (19%)

Net profit margin 23.1% 19.9%

FY 2008

10STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

13%

20%

9%

4%

-1%

15%

29%

11%

5%2%

-8%-8%

2%

-1% -1%-1%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

Organic growth1 (l.c.)Local currency growth

2008 2009

Change in local

currencies

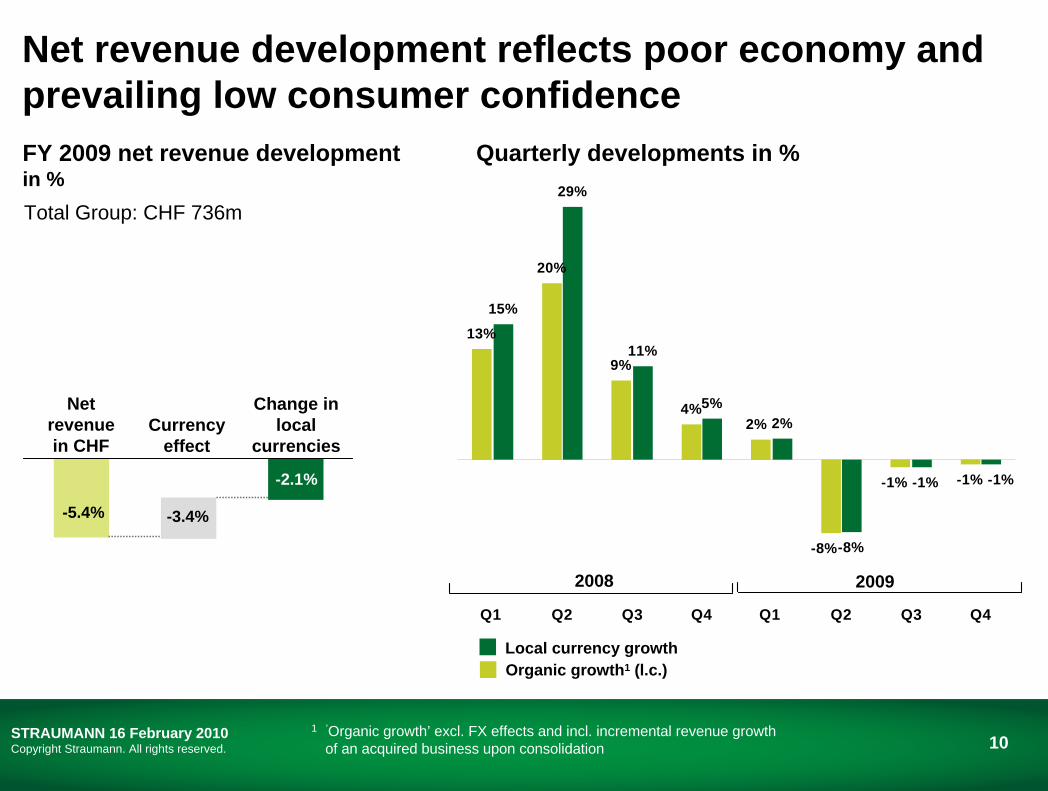

Net revenue in CHF

Currency effect

-5.4% -3.4%

-2.1%

FY 2009 net revenue developmentin %

Quarterly developments in %

Total Group: CHF 736m

1 ’Organic growth’ excl. FX effects and incl. incremental revenue growthof an acquired business upon consolidation

Net revenue development reflects poor economy and prevailing low consumer confidence

11STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

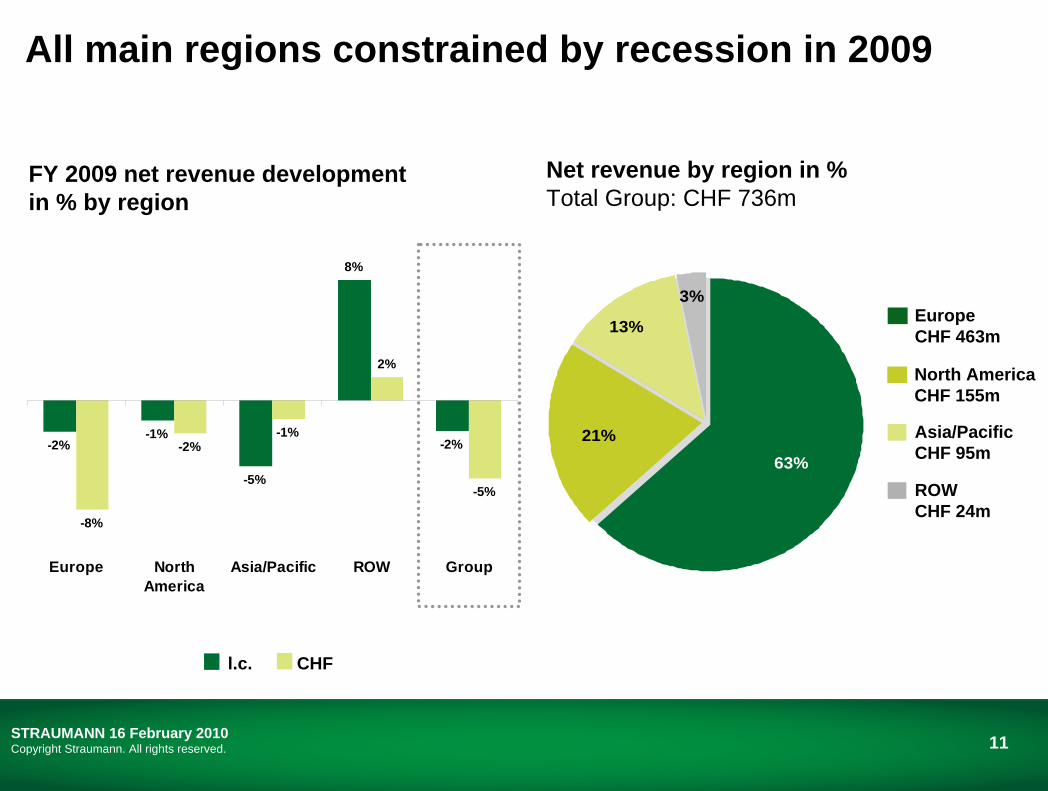

-2%-1%

-5%

8%

-2%

-8%

-2%-1%

2%

-5%

Europe NorthAmerica

Asia/Pacific ROW Group

All main regions constrained by recession in 2009

21%

13%

63%

3%EuropeCHF 463m

North AmericaCHF 155m

Asia/PacificCHF 95m

ROWCHF 24m

Net revenue by region in % Total Group: CHF 736m

FY 2009 net revenue developmentin % by region

l.c. CHF

12STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

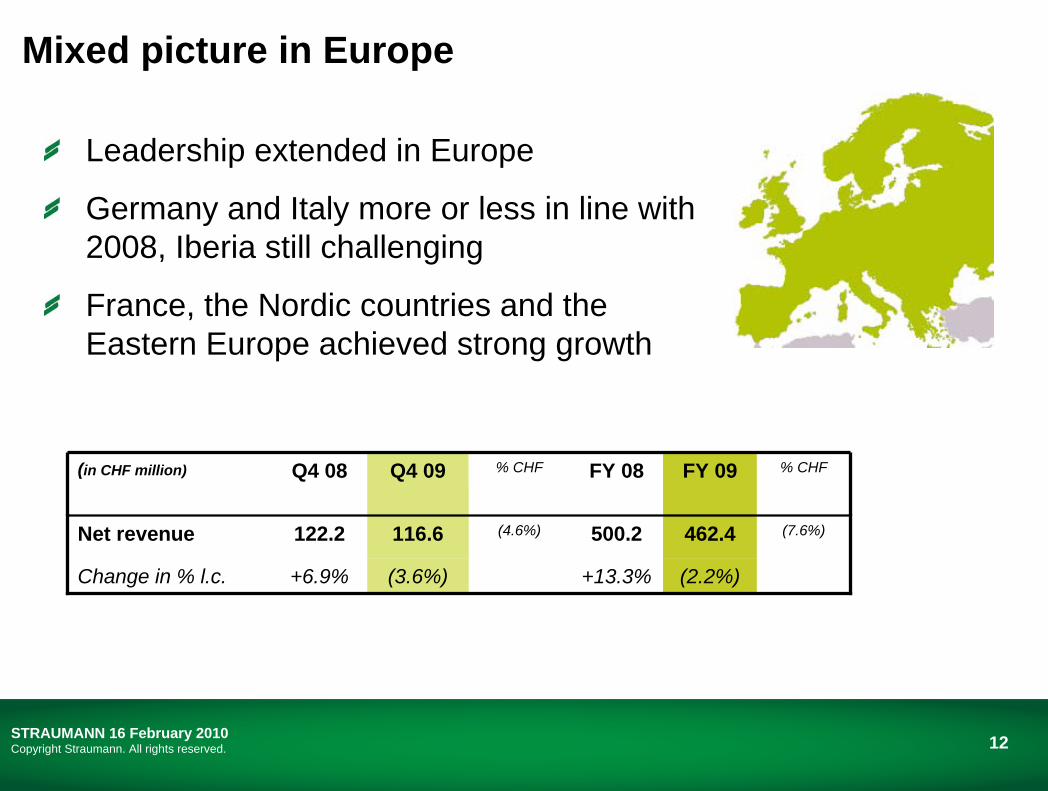

Mixed picture in Europe

Leadership extended in Europe

Germany and Italy more or less in line with 2008, Iberia still challenging

France, the Nordic countries and the Eastern Europe achieved strong growth

(2.2%)

462.4

FY 09

(3.6%)

116.6

Q4 09

+13.3%

(4.6%)

% CHF

+6.9%

122.2

Q4 08

Change in % l.c.

(7.6%)500.2Net revenue

% CHFFY 08(in CHF million)

13STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

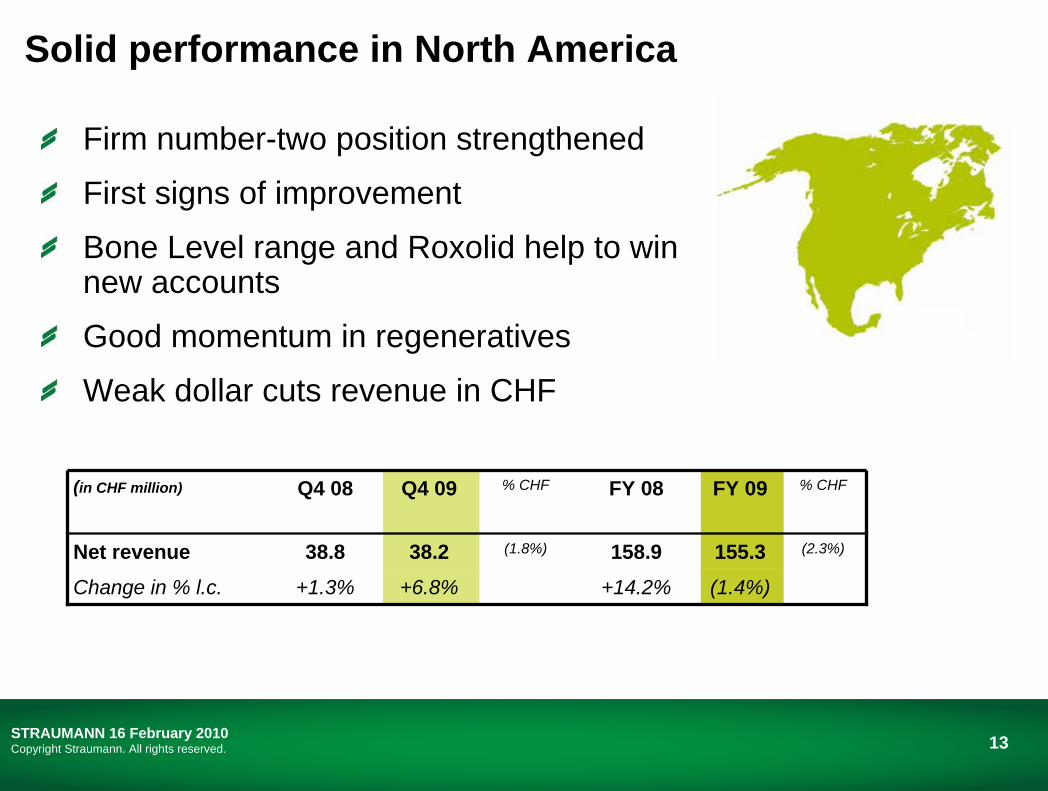

Solid performance in North America

Firm number-two position strengthened

First signs of improvement

Bone Level range and Roxolid help to win new accounts

Good momentum in regeneratives

Weak dollar cuts revenue in CHF

(1.4%)

155.3

FY 09

+6.8%

38.2

Q4 09

+14.2%

(1.8%)

% CHF

+1.3%

38.8

Q4 08

Change in % l.c.

(2.3%)158.9Net revenue

% CHFFY 08(in CHF million)

14STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

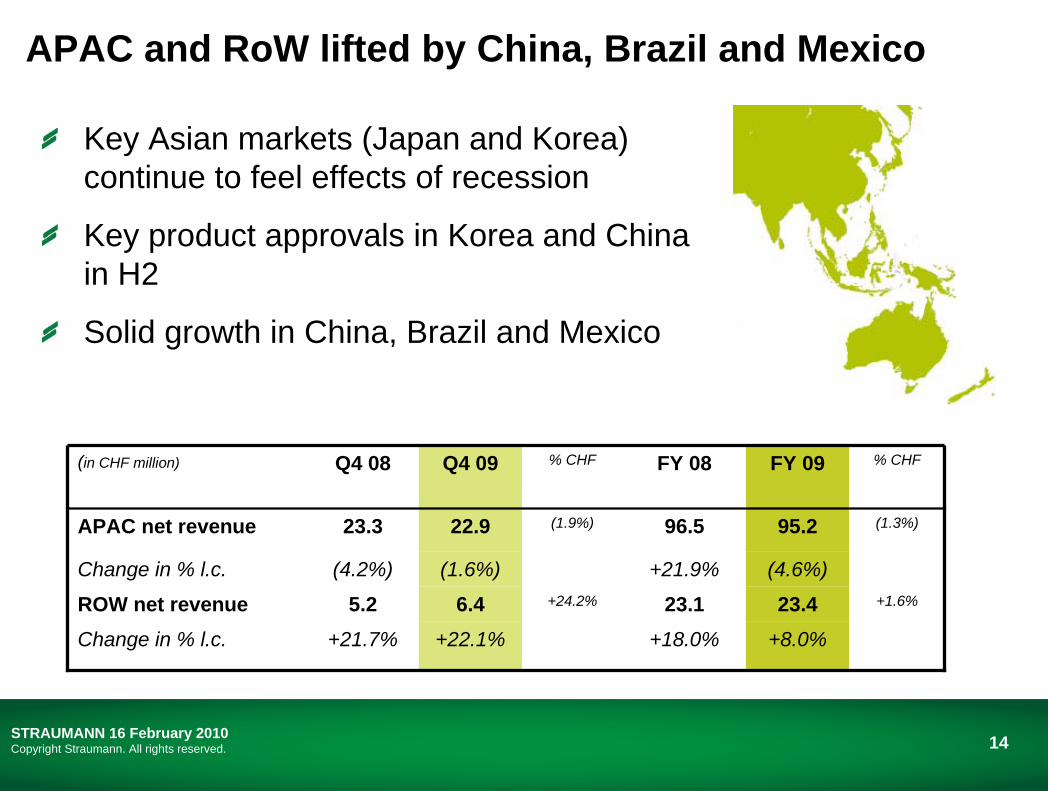

APAC and RoW lifted by China, Brazil and Mexico

Key Asian markets (Japan and Korea) continue to feel effects of recession

Key product approvals in Korea and Chinain H2

Solid growth in China, Brazil and Mexico

+8.0%

23.4(4.6%)

95.2

FY 09

+22.1%

6.4(1.6%)

22.9

Q4 09

+18.0%

23.1+21.9%

96.5

FY 08

+24.2%

(1.9%)

% CHF

+1.6%5.2ROW net revenue+21.7%Change in % l.c.

(4.2%)

23.3

Q4 08

Change in % l.c.

(1.3%)APAC net revenue

% CHF(in CHF million)

15STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

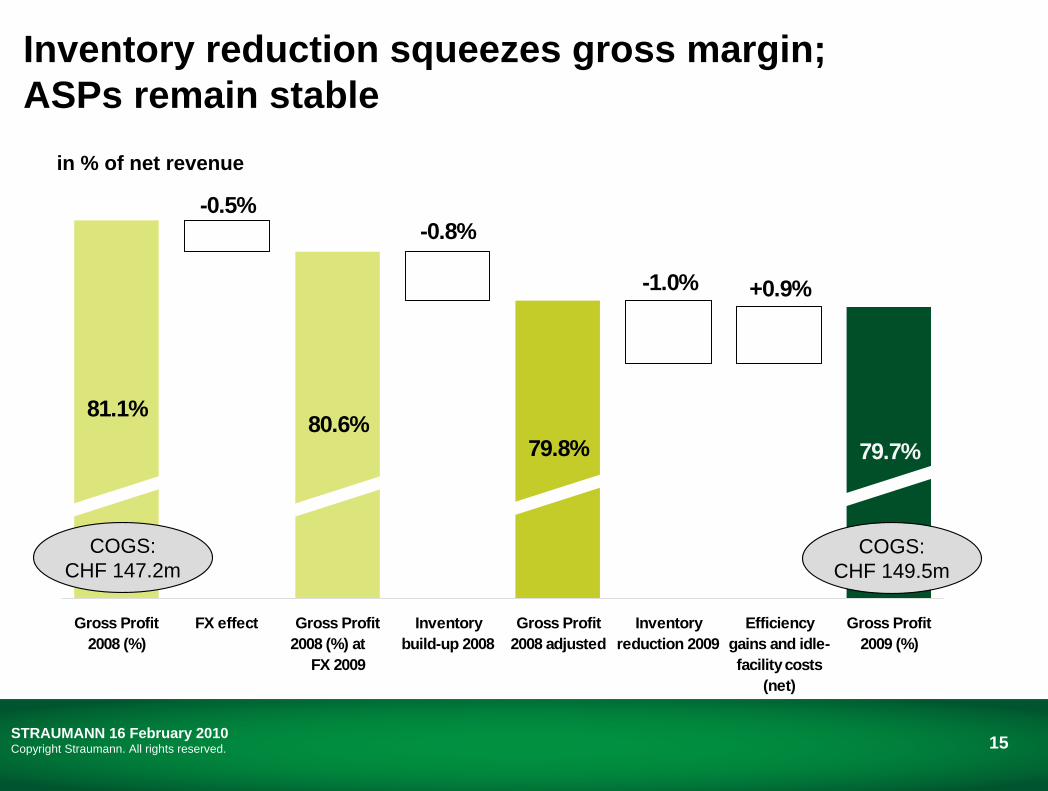

81.1% 80.6%79.8%

+0.9%-1.0%

-0.8%-0.5%

79.7%

Gross Profit2008 (%)

FX effect Gross Profit2008 (%) at

FX 2009

Inventorybuild-up 2008

Gross Profit2008 adjusted

Inventoryreduction 2009

Efficiencygains and idle-facility costs

(net)

Gross Profit2009 (%)

Inventory reduction squeezes gross margin; ASPs remain stable

in % of net revenue

COGS:CHF 149.5m

COGS:CHF 147.2m

16STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

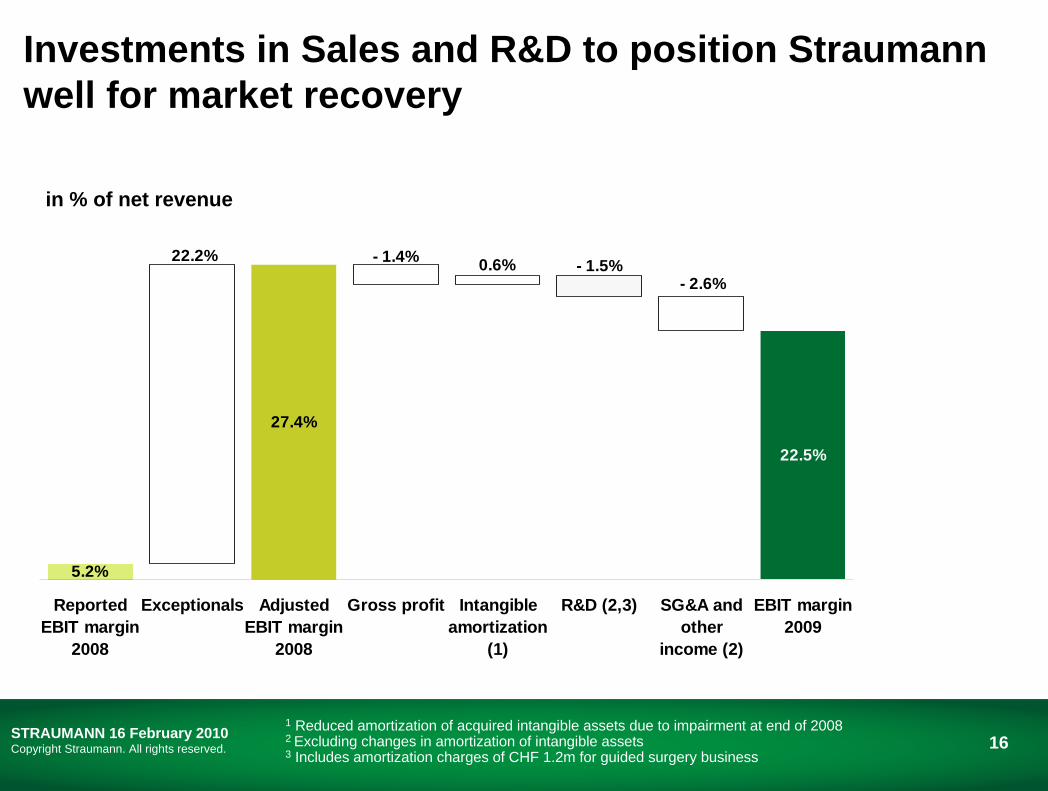

5.2%

27.4%

22.5%

- 2.6%- 1.5%0.6%- 1.4%22.2%

ReportedEBIT margin

2008

Exceptionals AdjustedEBIT margin

2008

Gross profit Intangibleamortization

(1)

R&D (2,3) SG&A andother

income (2)

EBIT margin2009

Investments in Sales and R&D to position Straumann well for market recovery

1 Reduced amortization of acquired intangible assets due to impairment at end of 20082 Excluding changes in amortization of intangible assets3 Includes amortization charges of CHF 1.2m for guided surgery business

in % of net revenue

17STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

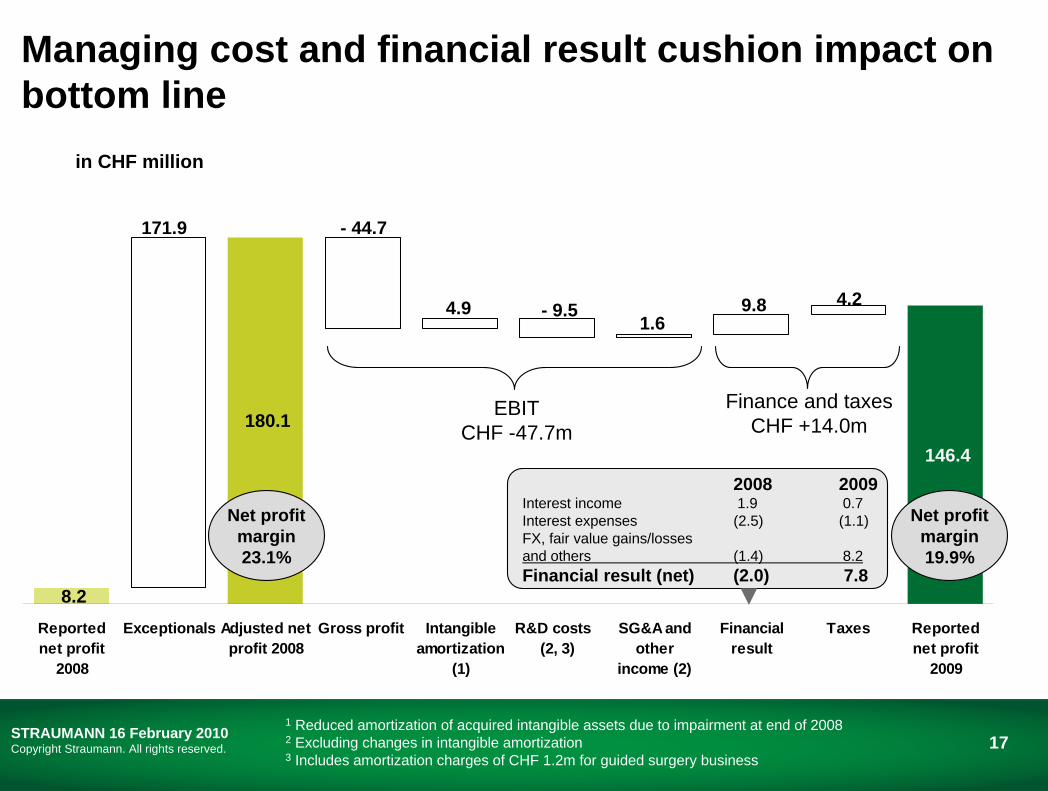

8.2

180.1

171.9

4.29.81.6

- 9.5 4.9

- 44.7

146.4

Reportednet profit

2008

Exceptionals Adjusted netprofit 2008

Gross profit Intangibleamortization

(1)

R&D costs (2, 3)

SG&A andother

income (2)

Financialresult

Taxes Reportednet profit

2009

Managing cost and financial result cushion impact on bottom line

in CHF million

EBIT CHF -47.7m

Net profitmargin23.1%

Finance and taxes CHF +14.0m

Net profitmargin19.9%

2008 2009Interest income 1.9 0.7Interest expenses (2.5) (1.1)FX, fair value gains/lossesand others (1.4) 8.2 Financial result (net) (2.0) 7.8

1 Reduced amortization of acquired intangible assets due to impairment at end of 20082 Excluding changes in intangible amortization3 Includes amortization charges of CHF 1.2m for guided surgery business

18STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

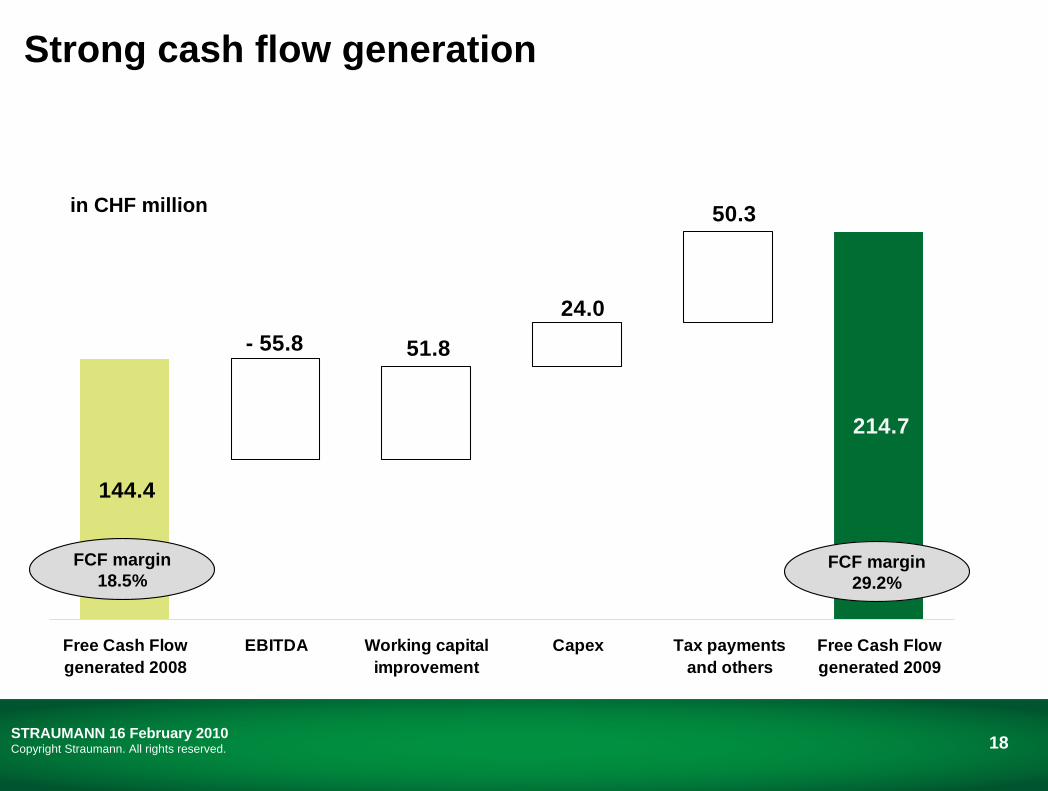

144.4

214.7

- 55.8 51.8

24.0

50.3

Free Cash Flowgenerated 2008

EBITDA Working capitalimprovement

Capex Tax paymentsand others

Free Cash Flowgenerated 2009

Strong cash flow generation

in CHF million

FCF margin29.2%

FCF margin18.5%

Achievements in 2009 and Outlook

Gilbert AchermannPresident & CEO

20STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

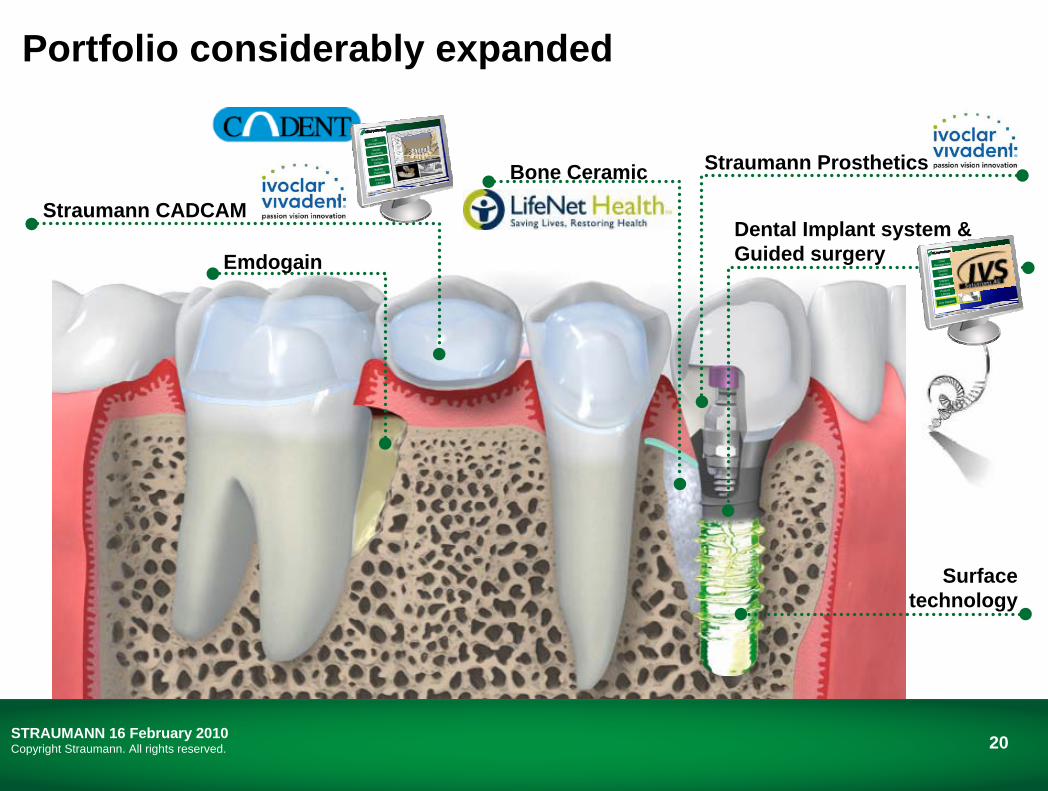

Portfolio considerably expanded

Surface technology

Straumann CADCAM

Emdogain

Bone Ceramic

Dental Implant system & Guided surgery

Straumann ProstheticsImplant

Planning

ProductLibrary

Model

Scanning

Prosthetic

Design

Lab

Management

Implant

Planning

ProductLibrary

Model

Scanning

Prosthetic

Design

Lab

Management

ProductLibrary

DICOMImport

Implant

Planning

CaseManagement

Live Support

ProductLibrary

DICOMImport

Implant

Planning

CaseManagement

Live Support

21STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

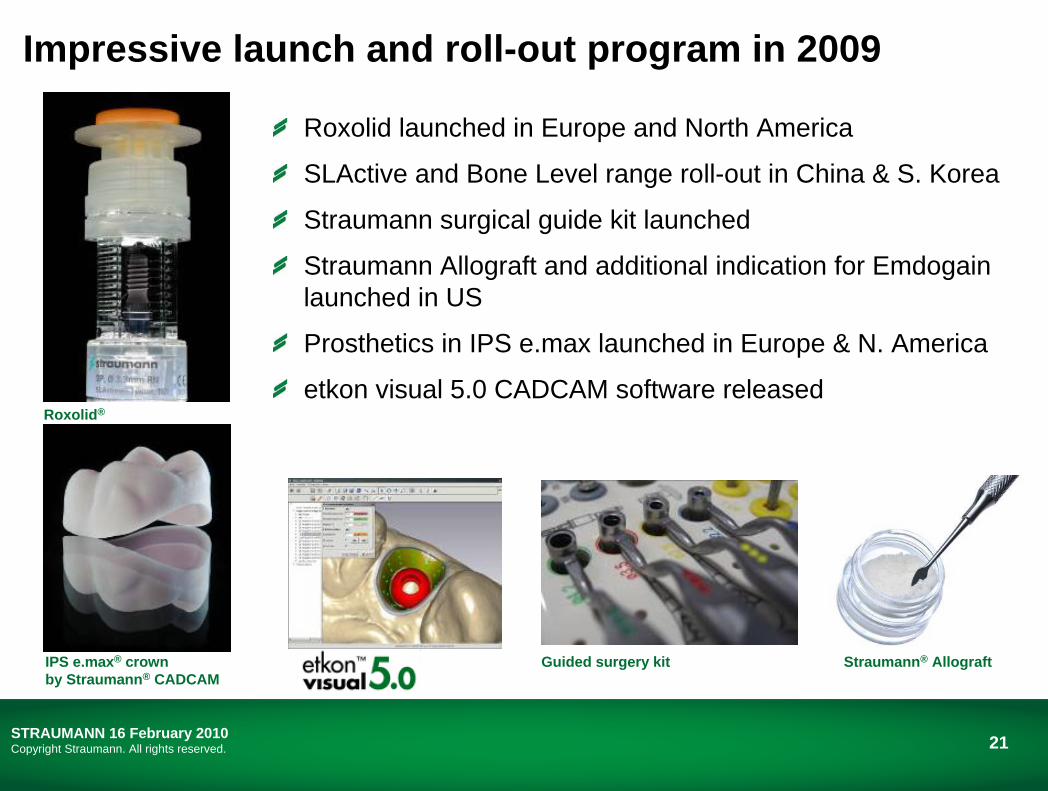

Roxolid launched in Europe and North America

SLActive and Bone Level range roll-out in China & S. Korea

Straumann surgical guide kit launched

Straumann Allograft and additional indication for Emdogain launched in US

Prosthetics in IPS e.max launched in Europe & N. America

etkon visual 5.0 CADCAM software released

Impressive launch and roll-out program in 2009

IPS e.max® crown by Straumann® CADCAM

Guided surgery kit Straumann® Allograft

Roxolid®

22STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

Output adapted to market downturn early ‘09; no compromise in skills or ability to supply despite 5% production staff reduction

Sales force increased and new jobs created in R&D bringing overall year on year reduction in Group headcount to just 1%

Return to normal working hours in implant production beginning of 2010

Early, structured approach to Board and leadership succession; 4 high-caliber candidates proposed for election

New CFO & EVP Operations engaged

New skills added in specific areas

23STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

Executive Management Board as of 1 April 2010

F. MaierSales

S. MatterProducts

B. Spalinger President & CEO

W. DaetzFinance & Operations

24STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

S. Burckhardt

U. Looser B. Lüthi S. MeisterR. Hess

Th. StraumannG. Achermann D. Ellenrieder

Proposals for election to the Board of Directors

25STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

Academic partnership further strengthened

Highly successful events in Iberia, Japan, Italy and the US

Membership increased to >7000 (+16% yoy)

Sections added in Finland and the Middle East

Seven Centers of Excellence in Implant Education approved worldwide

2010 World Symposium in Geneva in April promises to be one of the most prestigious scientific events in implant dentistry

26STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

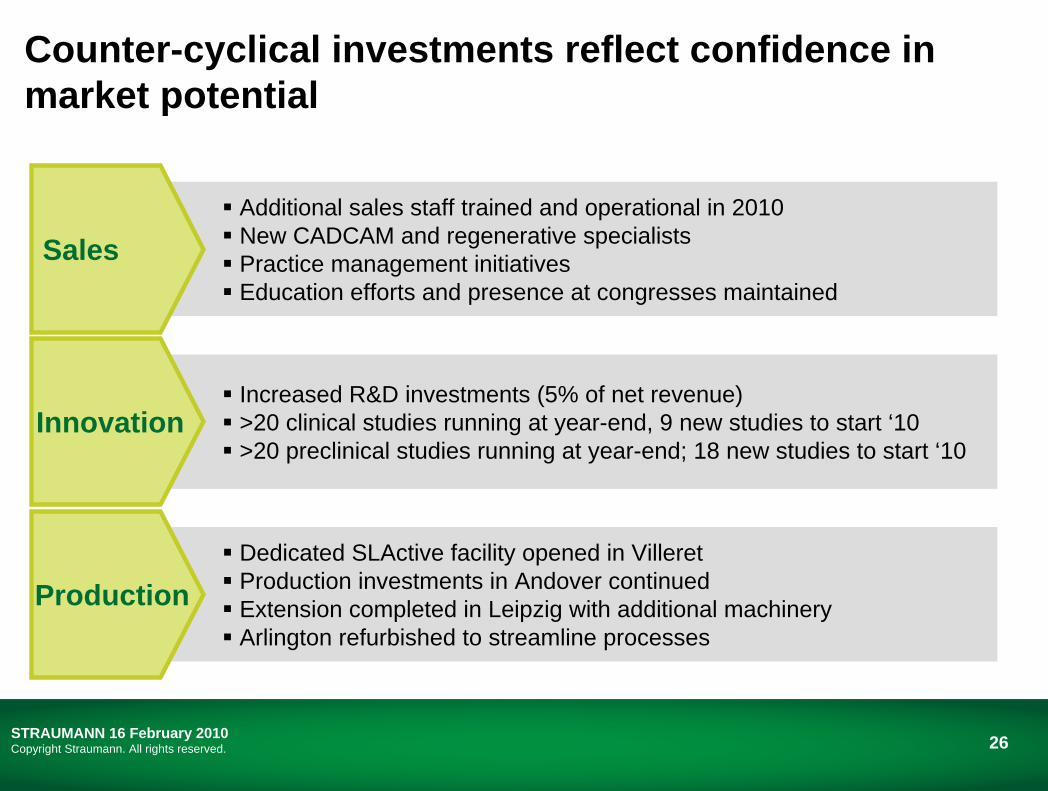

Additional sales staff trained and operational in 2010New CADCAM and regenerative specialistsPractice management initiatives Education efforts and presence at congresses maintained

Counter-cyclical investments reflect confidence in market potential

Increased R&D investments (5% of net revenue)>20 clinical studies running at year-end, 9 new studies to start ‘10>20 preclinical studies running at year-end; 18 new studies to start ‘10

Dedicated SLActive facility opened in VilleretProduction investments in Andover continued Extension completed in Leipzig with additional machineryArlington refurbished to streamline processes

Production

Innovation

Sales

27STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

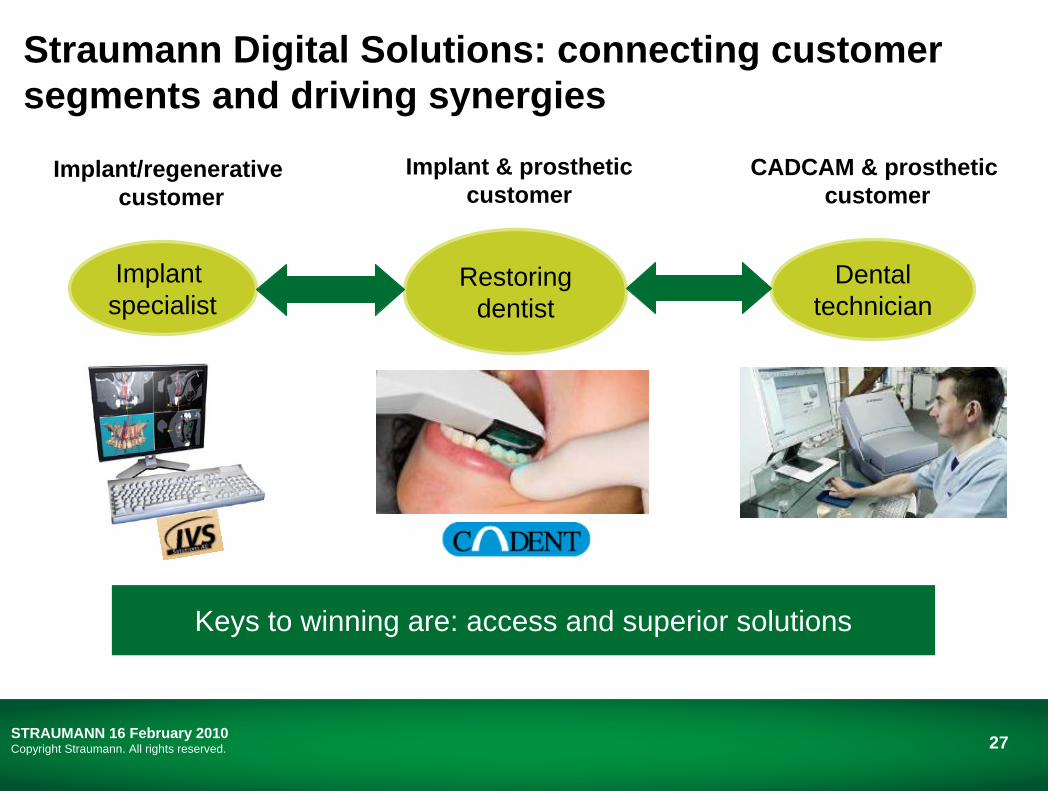

Straumann Digital Solutions: connecting customer segments and driving synergies

Restoringdentist

Dental technician

Implant specialist

Implant/regenerative customer

Implant & prostheticcustomer

CADCAM & prosthetic customer

Keys to winning are: access and superior solutions

28STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

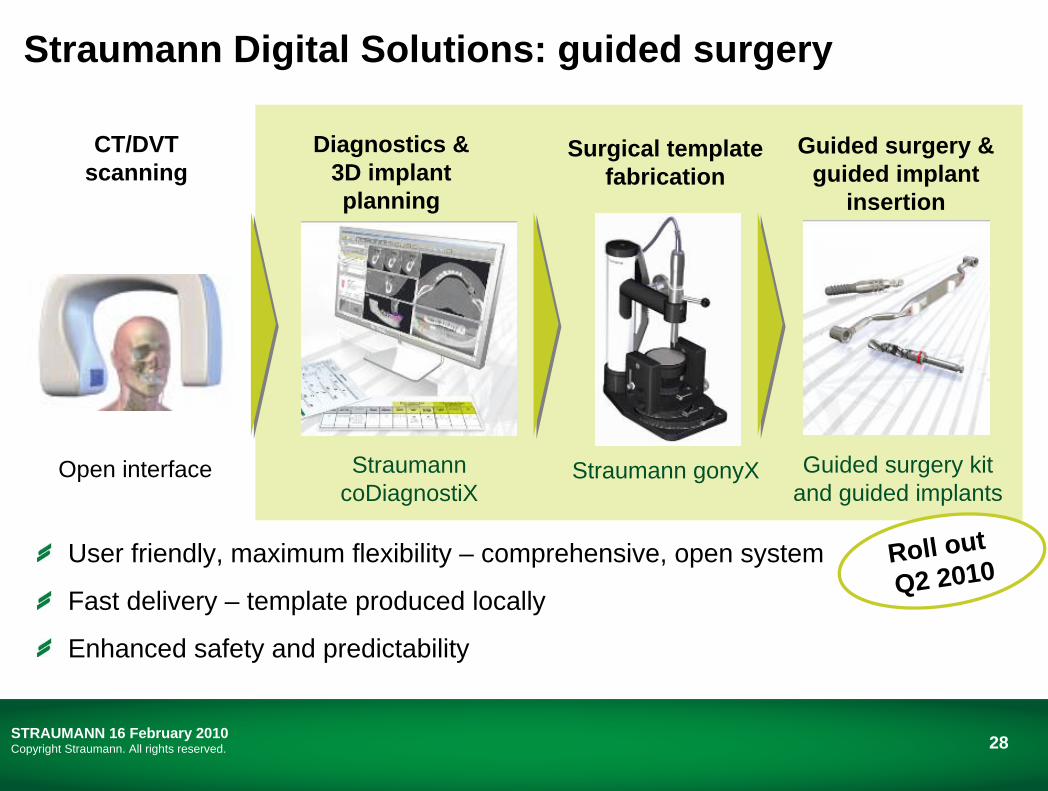

Straumann Digital Solutions: guided surgery

Open interface Straumann coDiagnostiX

Straumann gonyX Guided surgery kit and guided implants

CT/DVT scanning

Diagnostics & 3D implant planning

Surgical template fabrication

Guided surgery & guided implant

insertion

Roll out Q2 2010

User friendly, maximum flexibility – comprehensive, open system

Fast delivery – template produced locally

Enhanced safety and predictability

29STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

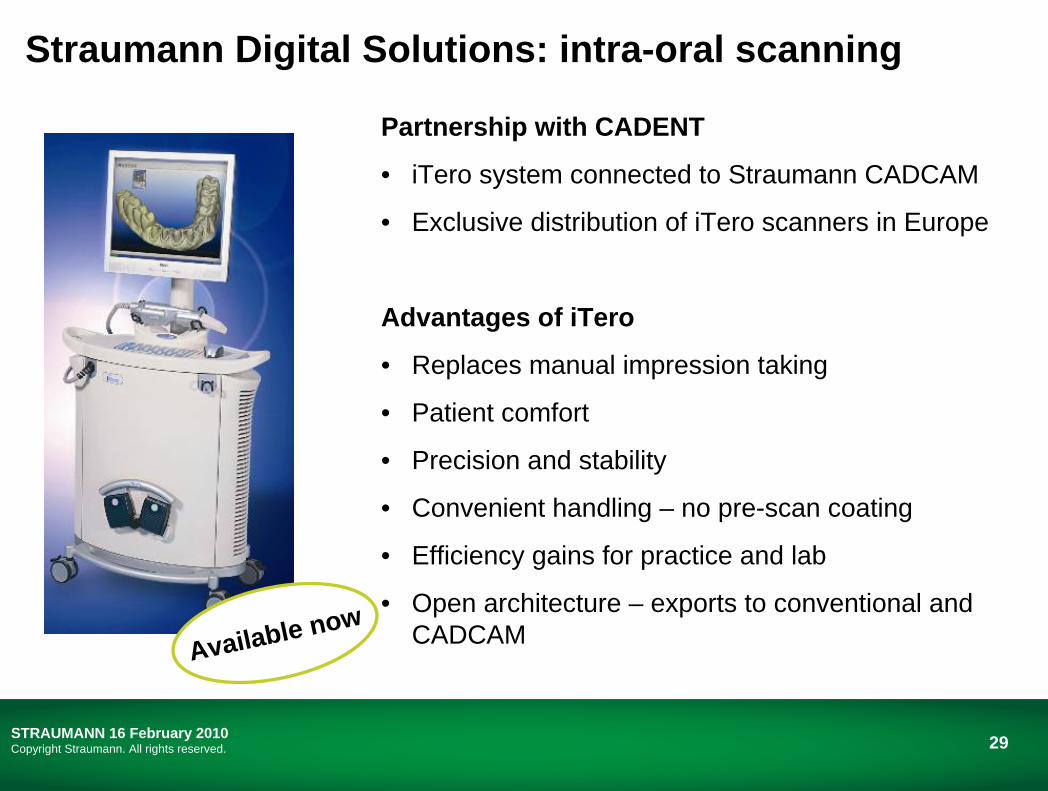

Straumann Digital Solutions: intra-oral scanning

Partnership with CADENT

• iTero system connected to Straumann CADCAM

• Exclusive distribution of iTero scanners in Europe

Advantages of iTero

• Replaces manual impression taking

• Patient comfort

• Precision and stability

• Convenient handling – no pre-scan coating

• Efficiency gains for practice and lab

• Open architecture – exports to conventional and CADCAMAvailable now

30STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

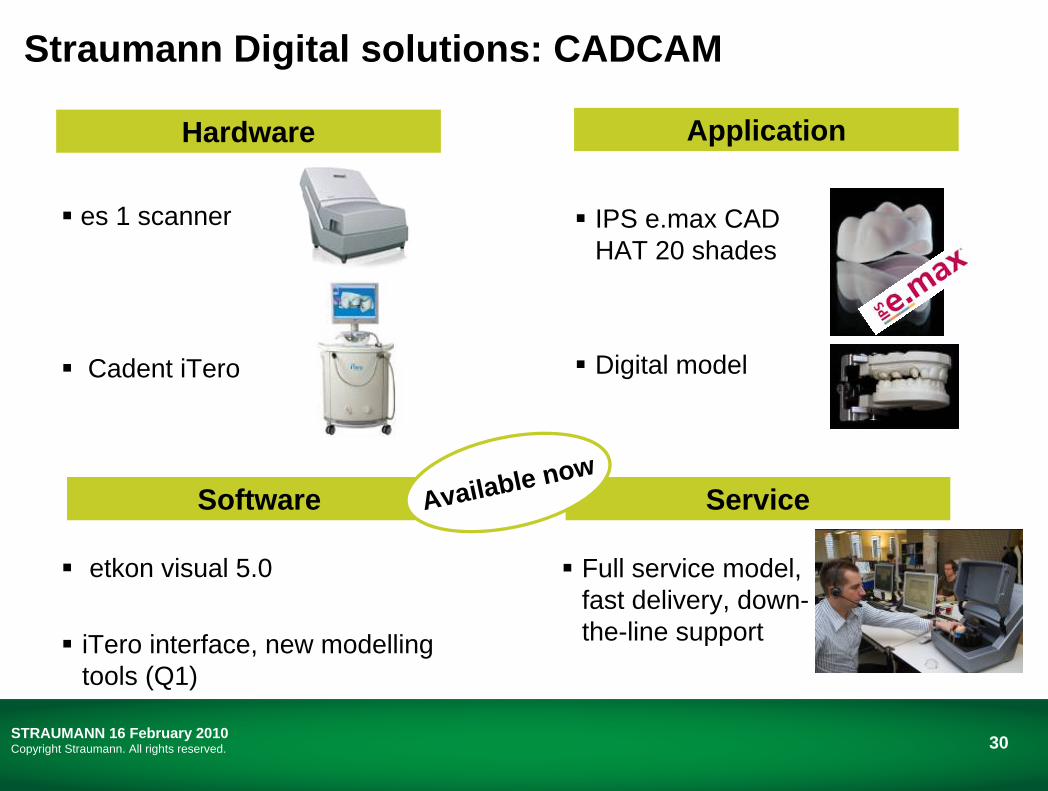

IPS e.max CAD HAT 20 shades

Digital model

Full service model, fast delivery, down-the-line support

Hardware

etkon visual 5.0

iTero interface, new modellingtools (Q1)

es 1 scanner

Cadent iTero

Straumann Digital solutions: CADCAM

Application

Software ServiceAvailable now

31STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

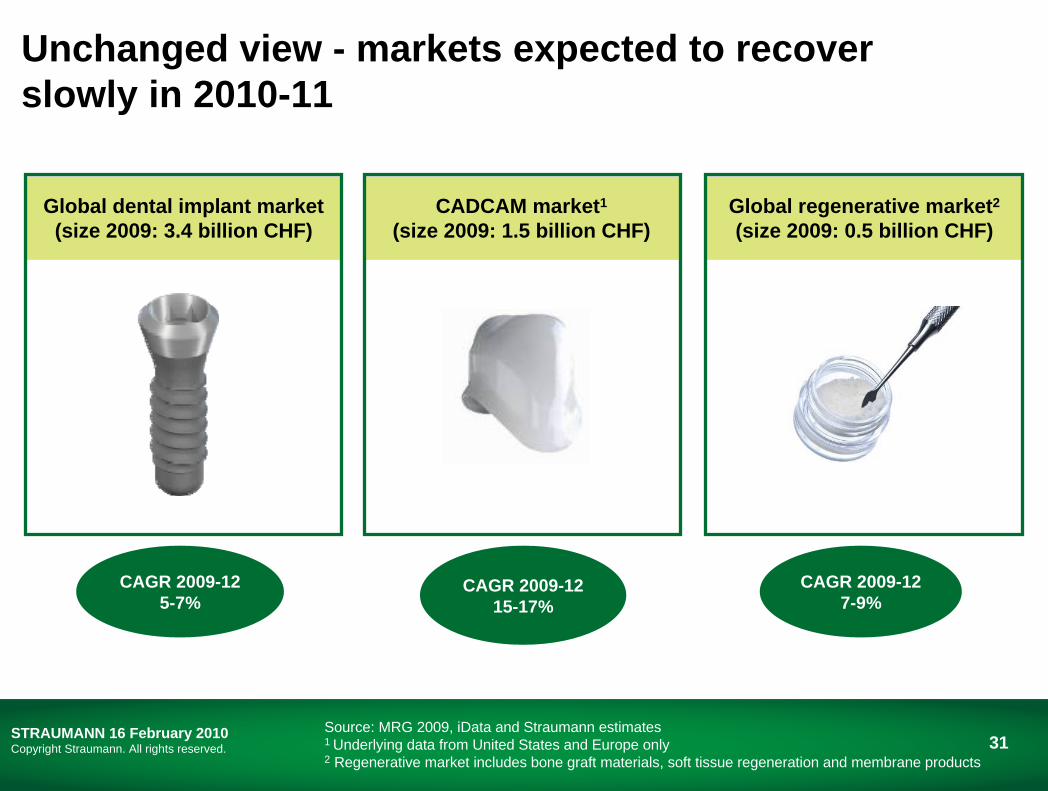

Unchanged view - markets expected to recover slowly in 2010-11

Global dental implant market (size 2009: 3.4 billion CHF)

CAGR 2009-125-7%

Source: MRG 2009, iData and Straumann estimates 1 Underlying data from United States and Europe only2 Regenerative market includes bone graft materials, soft tissue regeneration and membrane products

CADCAM market1

(size 2009: 1.5 billion CHF)

CAGR 2009-1215-17%

Global regenerative market2

(size 2009: 0.5 billion CHF)

CAGR 2009-127-9%

32STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

2010 Guidance(barring unforeseen circumstances)

With consumer spending, access to credit and unemployment far from returning to pre-recession levels, Straumann considers it premature to speak of a lasting recovery and remains cautious about forecasting when underlying, sustainable growth will return to the market in which it operates. The Group assumes that this market will be flat or grow in the low-single-digit range in 2010.

Based on its clinically-proven innovative products, organizational strength, market presence and differentiated services, the Group is convinced that it can deliver above-market performance. With the goal of simply doing more for customers and patients in 2010, it will continue to invest in all its business franchises, its innovation pipeline, and its marketing and sales organizations to create superior treatment solutions and services.

Taking this into account and assuming that there will be currency headwind in 2010, the Group expects to achieve net revenue in Swiss francs and an operating margin at least in line with the 2009 levels.

33STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

2009 Annual Report – pre-print version available

Comprehensive value reporting

Independent expert opinions, executive interviews, corporate governance, compensation report, outlooks, etc.

Follows GRI guidelines for sustainability reporting

Quality of Straumann’s reporting recognized in Swiss Annual Report awards

Questions & Answers

35STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

Calendar of upcoming events

Detailed calendar on www.straumann.com

1 March 2010 Investor Roadshow Toronto, London

2 March 2010 Investor Roadshow New York

2 March 2010 Credit Suisse HC Conference London

3 March 2010 Investor Roadshow Boston, Frankfurt

4 March 2010 Investor Roadshow Zurich

26 March 2010 Annual General Meeting Messe Basel

27 April 2010 First quarter results Basel (Audio webcast)

Appendix

37STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

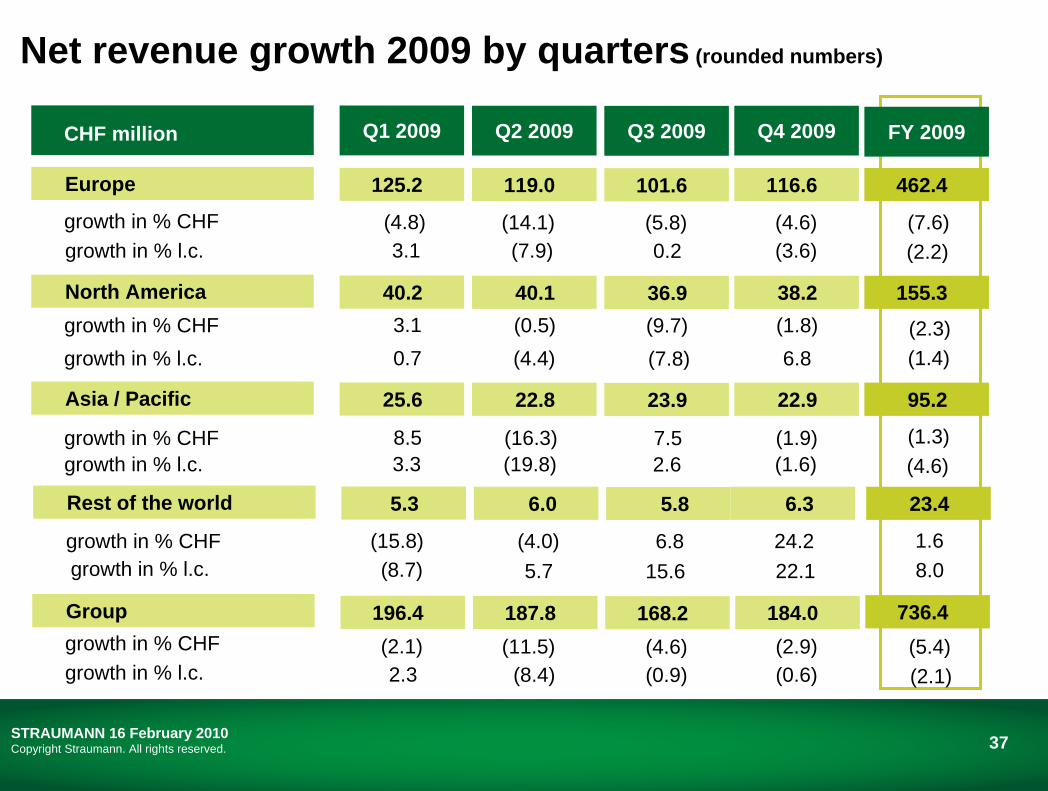

Rest of the world

North America

Europe

CHF million

Asia / Pacific

growth in % CHFgrowth in % l.c.

growth in % CHFgrowth in % l.c.

growth in % CHF

growth in % CHF

Groupgrowth in % CHFgrowth in % l.c.

Net revenue growth 2009 by quarters (rounded numbers)

growth in % l.c.

growth in % l.c.

FY 2009

736.4

23.4

95.2

155.3

462.4

(7.6)(2.2)

Q1 2009

196.4

5.3

25.6

40.2

125.2

2.3

(4.8)3.1

3.10.7

8.5

(15.8)

(2.1)

(8.7)

3.3

Q2 2009

187.8

6.0

22.8

40.1

119.0

(8.4)

(14.1)(7.9)

(0.5)(4.4)

(16.3)

(4.0)

(11.5)

5.7

(19.8)

Q3 2009

168.2

5.8

23.9

36.9

101.6

(0.9)

(5.8)0.2

(9.7)(7.8)

7.5

6.8

(4.6)

15.6

2.6

Q4 2009

184.0

6.3

22.9

38.2

116.6

(0.6)

(4.6)(3.6)

(1.8)6.8

(1.9)

24.2

(2.9)

22.1

(1.6)

(2.3)(1.4)

(1.3)(4.6)

1.68.0

(5.4)(2.1)

38STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

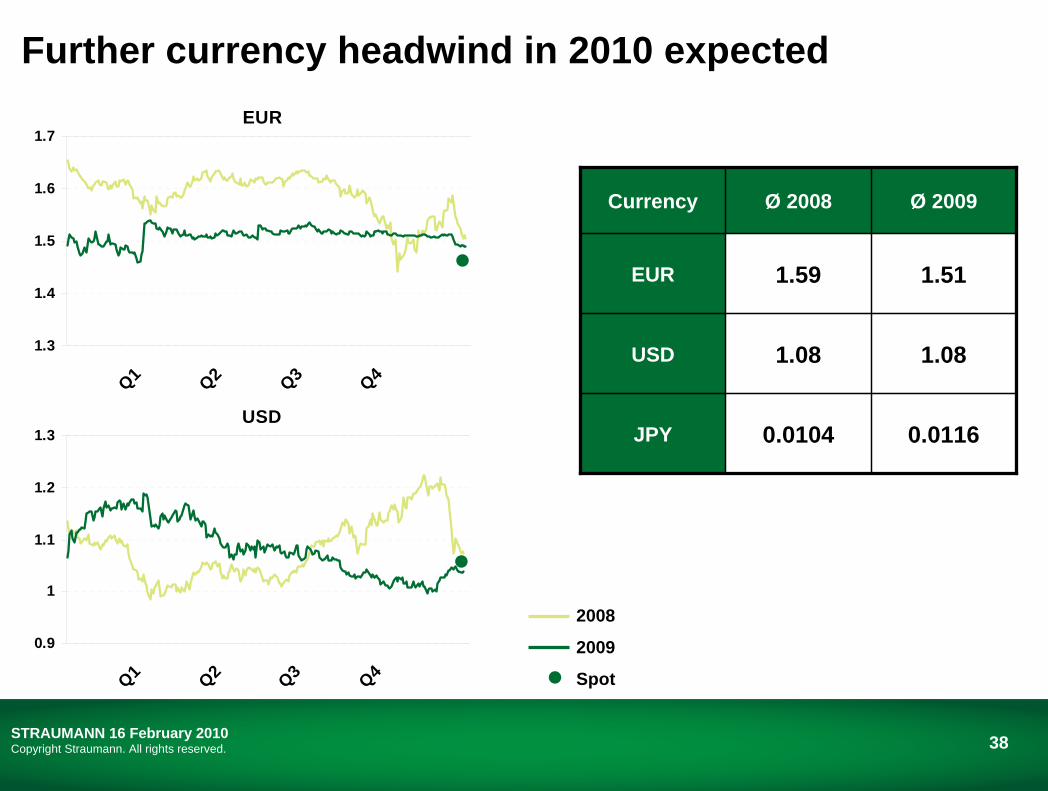

Further currency headwind in 2010 expected

0.01160.0104JPY

1.081.08USD

1.511.59EUR

Ø 2009 Ø 2008Currency

2008

2009

Spot

USD

0.9

1

1.1

1.2

1.3

Q1 Q2 Q3 Q4

EUR

1.3

1.4

1.5

1.6

1.7

Q1 Q2 Q3 Q4

39STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

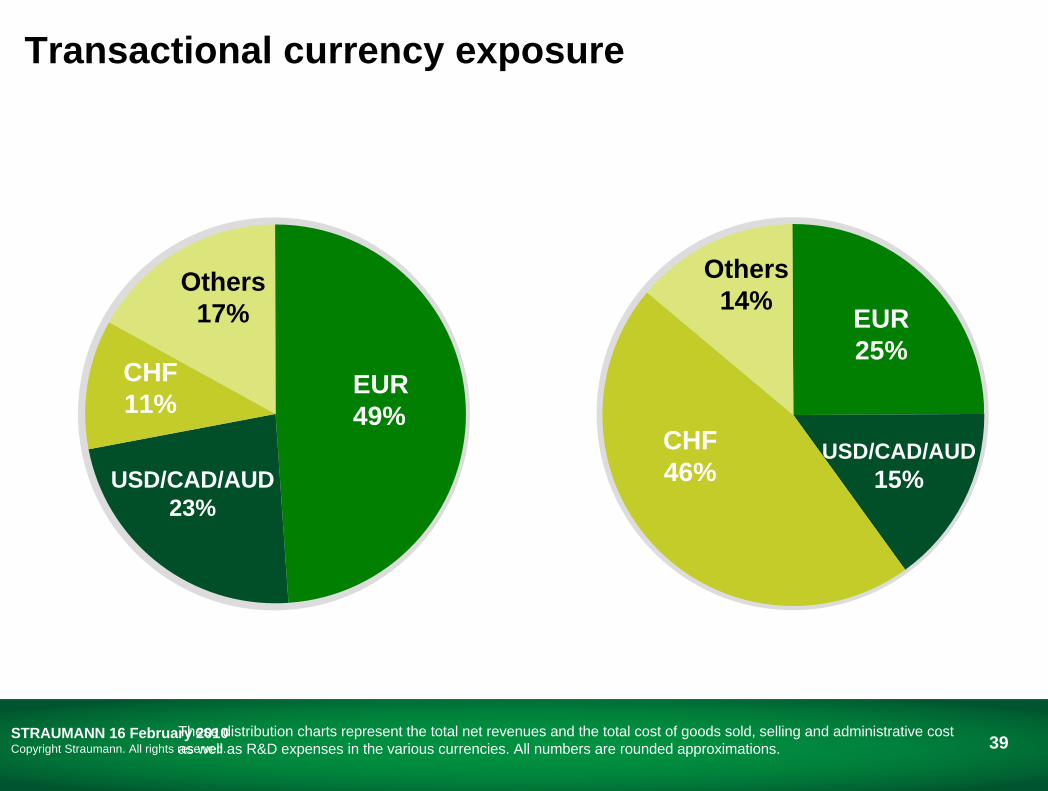

Transactional currency exposure

These distribution charts represent the total net revenues and the total cost of goods sold, selling and administrative cost as well as R&D expenses in the various currencies. All numbers are rounded approximations.

Others 17%

USD/CAD/AUD 23%

CHF 11%

EUR 49%

EUR 25%

USD/CAD/AUD 15%

CHF 46%

Others 14%

40STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

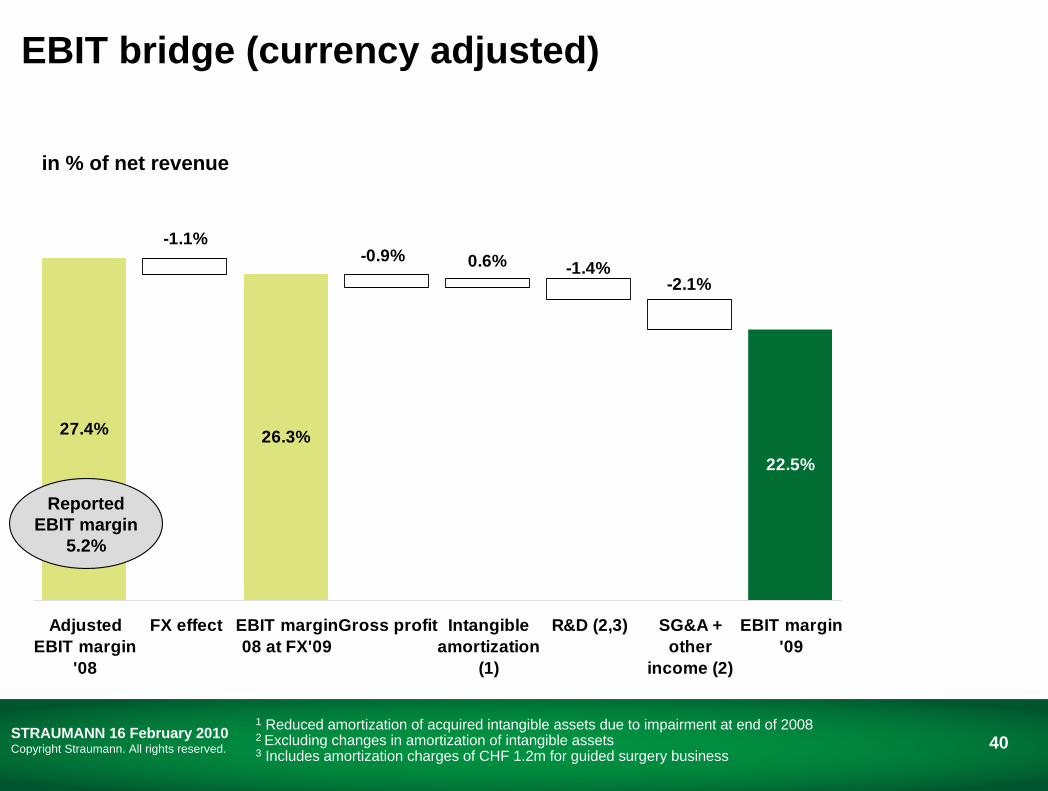

27.4% 26.3%

-2.1%-1.4%0.6%-0.9%

-1.1%

22.5%

AdjustedEBIT margin

'08

FX effect EBIT margin08 at FX'09

Gross profit Intangibleamortization

(1)

R&D (2,3) SG&A +other

income (2)

EBIT margin'09

EBIT bridge (currency adjusted)

1 Reduced amortization of acquired intangible assets due to impairment at end of 20082 Excluding changes in amortization of intangible assets3 Includes amortization charges of CHF 1.2m for guided surgery business

ReportedEBIT margin

5.2%

in % of net revenue

41STRAUMANN 16 February 2010Copyright Straumann. All rights reserved.

Your investor relations & media contacts

Fabian HildbrandCorporate Investor RelationsPhone +41 (0)61 965 13 27Mobile +41 (0)79 392 80 32Email [email protected]

Mark Hill & Thomas KonradCorporate CommunicationsPhone +41 (0)61 965 13 21Mobile +41 (0)79 320 24 77Email [email protected]