Embed Size (px)

Citation preview

2007 Annual Report

2 Mission Statement

R E V E L S T O K E C R E D I T U N I O N

Table of Contents 3

A N N U A L R E P O R T 2 0 0 7

� Member Rewards and Community Contributions 4 � Board of Directors 5 � Our Staff 6 � CEO’s Report 7 � President’s Report 8 � Auditor’s Report 9 � Consolidated Balance Sheet 10 � Consolidated Statement of Earnings & Retained Earnings 11 � Consolidated Statement of Cash Flow 12 � Consolidated Schedule of Operating Expenses 13 � Notes to the Consolidated Financial Statements 14 - 18

Additional copies of the annual report can be obtained from our office or online at www.revcu.com

4 Member Rewards & Community Contributions

R E V E L S T O K E C R E D I T U N I O N

2007 was a successful year for Revelstoke Credit Union and RCU Insurance Services. In appreciation we have contributed back to our members in significant ways.

Member Rewards $ 220,000.00 December 19, 2007 Qualified accounts earn rebate credits which are paid by way of deposits to members’ accounts.

Member Share Dividends $ 62,000.00 January 1, 2007 Membership Class A Shares = 6.75% Equity Class B Shares = 9.00% Expired Class D Shares = 4.50%

Community Contributions A few of the community groups and organizations that we supported financially or in other ways:

• Community Connections • Community Recycling Initiatives • Crime Stoppers • Ducks Unlimited • Girl Guides of Canada • Golf Charity Pro Am • Kodiak Ladies Hockey • Miss Revelstoke Ambassador • Relay for Life • Revelstoke Aquaducks • Revelstoke Community Foundation • Revelstoke Grizzlies Jr B Hockey • Revelstoke Minor Hockey • Revelstoke Minor Lacrosse • Revelstoke Minor Soccer • Revelstoke Mountain Culture Society • Revelstoke Rod and Gun Club

• Revelstoke Skating Club • Revelstoke Ski Club • Revelstoke Theatre Company • Rocky Mountain Ranger Cadets • Royal Canadian Legion • RSS Dry Grad • RSS Parents Advisory Council • RSS Senior Girls Volleyball • Snowmobile Revelstoke Society • Teen Life Choices • The Eggstravaganza • The Yes Camp (Youth) • Timber Days • Time Capsule • Trees for Tots • Welcome Wagon • Youth Soccer

Board of Directors 5

A N N U A L R E P O R T 2 0 0 7

Dave Raven - President Bob Holland - Vice President

Chris Swayze - Director MaryJean LeBuke - Director Bill MacFarlane - Director

Bryan Dubasov - Director Malcolm Bott - Director Pat McKee - Director

6 Our Staff

R E V E L S T O K E C R E D I T U N I O N

Management Team Roberta Bobicki CEO Randy Driediger GM, RCU Insurance Services Martin Ralph Manager I/T, Security & Risk Todd Webber Manager Member Services

Commercial Lending Team Cailleih Beerling Commercial Loan Assistant Kashmir Dhillon Commercial Loan Officer Debbie Morabito Commercial Loan Officer

Consumer Lending Team Sharon Kohlman Consumer Loan Officer Kim McKinnon Consumer Loan Officer Katherine Parkhill Consumer Loan Officer

Account Services Team Kelly Degerness Account Services Rep Bobbi Doebert Account Clearing Officer Shelly Fifield Account Services Rep Wendy Fischer Account Services Rep

Member Services Team Amanda Brown Member Services Rep Dawn Cowley Cash Control Officer Leah Dillman Member Services Rep Danielle Fenrich Member Services Rep Laura Gursky Member Services Rep Renee Howe Member Services Rep Tracey McKinney MSR Supervisor Tracey Peluso Member Services Rep Gisela Rota Member Services Rep Eliisa Tennant Member Services Rep

Wealth Management Team Margie Dean Investment Assistant Kristine Howe Investment Assistant Melodie Kindret CFP, Insurance Advisor Jan Morehouse CFP, Insurance Advisor Donna Smit Investment Assistant

ICBC & General Insurance Team Angela Bergman Insurance Broker Sandy Blake Insurance Broker Bob Devlin Insurance Broker Tanya Roche Insurance Broker

Tannis Curila General Reception Michelle Hardy Accounting Officer Miya Hayman Systems Administrator

Tara Schneider General Reception Barb Tetrault Loan Reception Clerk Sandra Wallach Loan Administration

Administration & Support Team

CEO’s Report 7

A N N U A L R E P O R T 2 0 0 7

It is my great pleasure to be submitting this report as your new CEO. 2008 marks my 30th year in the Credit Union system and I feel very proud and fortunate to have worked my whole career influenced by the Credit Union philosophy. 2007 was an interesting year. Under the guidance of our Board of Directors we researched options for the future of Revelstoke Credit Union in the ever changing economic environ-ment. It was a very valuable process and provided clarity to the Board and Staff as to what role and direction the Revelstoke Credit Union should take moving forward. It was deter-mined that at the present time the Community, Staff and Members would most benefit from us remaining a strong Community Credit Union. We ended 2007 with exceptional financial results. We were able to pay Member Rewards, maximize the staff Profit Share Program and still make a substantial contribution to Retained Earnings. We are experiencing incredible growth in our deposit portfolio and this is ade-quately providing liquidity to fund our loan requests. The focus for 2008 is to offer as many career and educational opportunities to our staff as possible. We have a long history of our employees starting as tellers and moving into more senior positions over time. We take pride in providing “Careers” rather than “Jobs”. The loy-alty and integrity of our staff is unsurpassed and I appreciate the work done by each and every employee. They are the strength of Revelstoke Credit Union. A well educated staff translates to the best possible service being provided to our members. I look forward to the days ahead. We will be ready and well-positioned for whatever chal-lenges and accomplishments come our way!! Best Regards,

Roberta Bobicki CEO

8 President’s Report

R E V E L S T O K E C R E D I T U N I O N

On behalf of the Board of Directors, I am pleased to present the Revelstoke Credit Union’s annual report for 2007. The Revelstoke Credit Union exceeded our budget projections for 2007. Accordingly we were able to provide a profit sharing with the staff, a Member Rewards program and a sub-stantial increase in our retained earnings. Retained Earnings are now $6,806,000 and the total asset base is $ 136,973,000 (a 34% increase over 2006). Net Earnings after tax, Mem-ber Rewards and profit share are $573,311 and was all contributed to Retained Earnings. The Board of Directors addressed a number of challenges during 2007 starting with a signifi-cant drain on our liquidity which forced the Board to consider several actions to ensure the continued health of the Credit Union. One option was the pursuit of a merger with a larger institution which would have provided the resources and organizational depth necessary to address the challenges facing the Credit Union. Through the spring the Board pursued the merger option with many meetings, staff input, financial and operations reviews and draft le-gal agreements; although ultimately the Board came to the decision that the Revelstoke Credit Union could best serve what we understood to be the interests of our members and the community by remaining an independent and local institution. This decision precipitated a number of actions which lead to the separation of the Chief Executive Officer and the re-cruitment of a replacement through the fall months. It is with pride that the Board appointed Roberta Bobicki to the position of Chief Executive Officer early in the new year. The Board would like to again recognize the dedication of the staff throughout this period, for both the performance of the Credit Union and the acceptance of the changes necessary to ensure its future health. Indeed much of the growth and extraordinary achievements in addressing the operational challenges and eventual profit margins occurred in the latter half of the year. On behalf of the Board I would like to express our appreciation to the management and staff of the Credit Union and the Insurance agency for their dedication and exemplary work. All of the members truly appreciate the professionalism and friendly atmosphere that we experi-ence throughout the year. I would also like to express my sincere appreciation for the hard work, dedication and sup-port of the Board of Directors throughout this very challenging year for the Credit Union. It has been a true honor to work with such a dedicated group of staff and Board members this past year. Respectfully Submitted, David Raven Chairperson, Board of Directors

Auditor’s Report 9

A N N U A L R E P O R T 2 0 0 7

To the Members We have audited the Consolidated Balance Sheet of the Revelstoke Credit Union as at December 31, 2007 and the Consolidated Statements of Earnings and Retained Earnings and Cash Flows for the year then ended. These financial statements are the responsibility of the Credit Union's management. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we plan and perform an audit to obtain reasonable assurance whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. In our opinion, these consolidated financial statements present fairly, in all material respects, the financial position of the Revelstoke Credit Union as at December 31, 2007 and the results of its operations for the year then ended in accordance with Canadian generally accepted accounting principles applied on a basis consistent with the preceding year.

ADAMS REDDING WOOLEY Certified General Accountants Cranbrook, B.C. January 31, 2008

Adams Redding Wooley 824 - 1st Street South

Cranbrook, BC V1C 7H5

T (250) 426-8277 F (250) 426-4109 www.cgafirm.com

10 Consolidated Balance Sheet

R E V E L S T O K E C R E D I T U N I O N

STATEMENT I REVELSTOKE CREDIT UNION

Consolidated Balance Sheet

December 31, 2007

2007 2006

ASSETS CASH AND TERM DEPOSITS $ 21,454,387 $ 7,971,848

MEMBERS’ LOANS (Note 2) 110,349,223 90,178,882

OTHER (Note 3) 213,061 138,021

INVESTMENTS (Note 4) 687,559 688,590

PROPERTY, PLANT AND EQUIPMENT (Note 5) 3,268,929 3,420,341 $ 135,973,159 $ 102,397,682

LIABILITIES AND MEMBERS' ACCOUNTS

MEMBERS’ DEPOSITS (Note 6) $ 127,702,460 $ 89,197,393

MEMBERS’ SHARES (Note 7) 820,528 762,853

ACCOUNTS PAYABLE AND ACCRUED LIABILITIES 635,270 6,204,320

RETAINED EARNINGS 6,814,901 6,233,116

$ 135,973,159 $ 102,397,682 APPROVED ON BEHALF OF THE BOARD: David Raven Chairperson Malcolm Bott Director

The attached notes are an integral part of these financial statements.

Consolidated Statement of Earnings & Retained Earnings 11

A N N U A L R E P O R T 2 0 0 7

STATEMENT II REVELSTOKE CREDIT UNION

Consolidated Statement of Earnings and Retained Earnings

For the Year Ended December 31, 2007

2007 2006

FINANCIAL INCOME

Interest from Loans $ 6,314,568 $ 4,890,936 Interest from Investments 483,292 467,400

6,797,860 5,358,336

FINANCIAL EXPENSES

Interest on Deposits 3,506,193 2,780,418 Interest on Borrowed Funds 286,269 178,082

3,792,462 2,958,500 FINANCIAL MARGIN 3,005,398 2,399,836 OTHER REVENUES (EXPENSES) Service Fees and Commissions 1,490,800 1,163,267 Processing and Handling Fees (153,891) (147,502) Losses on Loans Expense (71,758) (532) 1,265,151 1,015,233 OPERATING MARGIN 4,270,549 3,415,069 OPERATING EXPENSES (Schedule A) (3,276,093) (2,811,701) EARNINGS BEFORE DISTRIBUTIONS AND TAXES 994,456 603,368

REWARDS TO MEMBERS (Note 9) (281,343) (62,081)

INCOME AND CAPITAL TAXES (Note 10) (139,802) (75,435) NET EARNINGS FOR THE YEAR 573,311 465,852RETAINED EARNINGS - BEGINNING OF YEAR 6,233,116 5,767,264

RETAINED EARNINGS - END OF YEAR $ 6,806,427 $ 6,233,116

The attached notes are an integral part of these financial statements.

12 Consolidated Statement of Cash Flows

R E V E L S T O K E C R E D I T U N I O N

STATEMENT III REVELSTOKE CREDIT UNION

Consolidated Statement of Cash Flows

For the Year Ended December 31, 2007

2007 2006 CASH PROVIDED (USED) BY:

OPERATING ACTIVITIES

Net Earnings for the Year $ 573,311 $ 465,852 Items Not Involving Cash Amortization 217,325 140,990 Change In Non-Cash Working Capital Items Decrease (Increase) in Other Assets (75,040) (52,010) (Decrease) Increase in Accounts Payable (5,560,576) 4,530,905 (4,844,980) 5,085,737 FINANCING ACTIVITIES Increase in Members’ Deposits 38,505,067 3,970,380 Increase in Members’ Shares 57,675 52,143 38,562,742 4,022,523 INVESTING ACTIVITIES (Increase) in Members’ Loans (20,170,341) (16,396,092) Decrease (Increase) in Investments 1,031 (11,542) Additions to Property, Plant and Equipment – Net (65,913) (766,213) (20,235,223) (17,173,847) INCREASE IN CASH 13,482,539 (8,065,587) CASH - BEGINNING OF YEAR 7,971,848 16,037,435 CASH - END OF YEAR $ 21,454,387 $ 7,971,848 CASH IS DEFINED AS: Cash $ 5,180,945 $ 548,256 Deposits – Special and Term 16,091,000 7,281,000 Accrued Interest 182,442 142,592 $ 21,454,387 $ 7,971,848

The attached notes are an integral part of these financial statements.

Consolidated Schedule of Operating Expenses 13

A N N U A L R E P O R T 2 0 0 7

SCHEDULE A REVELSTOKE CREDIT UNION

Consolidated Schedule of Operating Expenses

For the Year Ended December 31, 2007

2007 2006

ADMINISTRATIVE

Director and Committee Costs $ 48,862 $ 40,252 Staff Salaries 1,828,262 1,446,141 Staff Benefits 272,748 272,533 Staff Travel and Training 25,986 36,325 Data Processing and Accounting 229,408 275,885 Stationery and Supplies 72,817 75,971 Postage 35,048 28,398 Telephone 35,862 31,151 Insurance - Bonding 20,684 7,481 2,569,677 2,214,137

BUILDING AND OCCUPANCY

Insurance 19,880 24,499 Repairs and Maintenance 29,151 10,007 Amortization 77,129 26,077 Property Taxes 29,485 32,840 Janitor 58,165 39,370 Utilities 28,380 26,950

242,190 159,743

OTHER

Legal and Collection 20,966 26,392Audit 38,001 33,301Consulting 26,420 43,428Stabilization and Inspection Assessments 37,367 52,601Dues 35,605 31,415Promotion, Advertising and Donations 85,688 92,680Equipment Rental and Maintenance 37,697 28,109Computer Licenses and Subscriptions 13,162 5,016Amortization 140,196 114,913Annual Meeting 1,721 1,929Miscellaneous 27,403 8,037

464,226 437,821 TOTAL OPERATING EXPENSES - To Statement II $ 3,276,093 $ 2,811,701

14 Notes to the Consolidated Financial Statements

R E V E L S T O K E C R E D I T U N I O N

REVELSTOKE CREDIT UNION

Notes to the Consolidated Financial Statements

December 31, 2007

NOTE 1 SIGNIFICANT ACCOUNTING POLICIES

a) Allowance for Impaired Loans

Loans which in management's opinion may not be fully collectible, are provided for by charges to earnings for the year.

b) Amortization

Amortization of premises and equipment is provided as follows:

Building - 2 1/2% per annum on the straight-line basis.

Furniture, Equipment and Computer Software - from 1 to 10 years, depending upon nature of the asset Parking Lot - 5% per annum on the straight-line basis

As the major building renovation was completed during 2006, no amortization of the renovation and attendant furnishings was claimed during 2006. Amortization began at the above rates in 2007.

c) Provision for Dividends on Shares and Member Rewards

Dividends payable on shares and Member Rewards (Patronage Rebates) are charged to earnings for the year.

d) Property Held for Resale

Properties held for resale are carried at the lower of estimated realizable value or the balance of the loan.

e) Interest Rate Swaps

Derivative financial instruments are used by the Credit Union to hedge risk from changes in interest rates. The notional principals related to these contracts are not included in the Balance Sheet. Revenues and expenses from these contracts are recognized over the life of the hedge items and are recorded as interest income or expense accordingly. At December 31, 2007, the Credit Union had outstanding interest rate swap contracts in the notional principal amount of $5,000,000 (2006 – $5,000,000). The Credit Union has agreed to pay a floating rate, in return for the agreement to receive a fixed rate. Interest rate swaps are transactions in which two parties exchange interest flows on a specified notional principal amount for a pre-determined period based on agreed interest rate formulae. Principal amounts are not exchanged and are not indicative of a credit exposure.

f) Measurement Uncertainty

The preparation of financial statements in conformity with Canadian generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Significant areas requiring the use of management estimates relates to the determination of potential loan losses and the useful life of capital assets. Actual results could differ from those estimates.

g) Consolidation

The Consolidated financial Statements include the accounts of the Credit Union and its wholly owned subsidiary RCU Insurance Services Ltd. Segmented information of RCU Insurance Services Ltd. for the year ended December 31, 2007 is not required to be disclosed in accordance with Section 1701 of the CICA Handbook.

Notes to the Consolidated Financial Statements 15

A N N U A L R E P O R T 2 0 0 7

REVELSTOKE CREDIT UNION

Notes to the Consolidated Financial Statements

December 31, 2007

NOTE 2 MEMBERS’ LOANS a) 2007 2006

Residential Mortgages $ 61,430,437 $ 50,766,759 Commercial Mortgages and Loans 26,278,844 25,059,024 Personal Loans 14,596,000 9,905,714 Commercial Revolving Credits 7,923,607 4,340,722 Accrued Interest Receivable 340,335 271,663 110,569,223 90,343,882 Deduct: Allowance for Impaired Loans (220,000) (165,000)

$ 110,349,223 $ 90,178,882

b) The activity in the allowance for impaired loans has been: 2007 2006 Balance – Opening $ 165,000 $ 215,000 Provision (Reduction) Charged to Operations 64,156 1,100

229,156 216,100Loans Written Off (9,156) (51,100) Balance – Ending $ 220,000 $ 165,000

c) Loans totalling $7,283,802 to related parties and staff are included in members’ loans (2006 $5,618,159.

As part of its remuneration and benefit package the Credit Union offers staff members a reduction from current interest rates subject to specific maximum amounts as approved by the Financial Institutions Commission.

d) In the normal course of business, the credit union issues Letters of Credit on behalf of its members, with

deposits or other property pledged as security. These undrawn amounts of $1,181,101 at December 31, 2007 (2006 - $783,457) are not included in the Balance Sheet.

NOTE 3 OTHER 2007 2006 Accrued Interest on Swaps $ (1,166) $ 8,212 Prepaid Expenses and Accounts Receivable 214,227 129,809 $ 213,061 $ 138,021

NOTE 4 INVESTMENTS

2007 2006

Credit Union Central of B.C. Shares $ 298,198 $ 293,986Accrued Dividends 24,699 24,039CUPP Services Ltd. Shares 34,501 30,404Stabilization Central Shares 161 161ICBC Licence 330,000 330,000Venture Capital Fund - 10,000 $ 687,559 $ 688,590 The shares in Credit Union Central of British Columbia and Stabilization Central Credit Union are held pursuant to the Financial Institutions Act and the Credit Union Incorporation Act.

16 Notes to the Consolidated Financial Statements

R E V E L S T O K E C R E D I T U N I O N

REVELSTOKE CREDIT UNION

Notes to the Consolidated Financial Statements

December 31, 2007

NOTE 5 PROPERTY, PLANT AND EQUIPMENT Accumulated Net BookValue Cost Amortization 2007 2006 Building $ 3,527,875 $ 577,477 $ 2,950,398 $ 3,026,049Parking Lot 38,457 10,379 28,078 29,557Furniture and Equipment 1,500,878 1,262,666 238,212 312,494 5,067,210 1,850,522 3,216,688 3,368,100Land 52,241 - 52,241 52,241

$ 5,119,451 $ 1,850,522 $ 3,268,929 $ 3,420,341 NOTE 6 MEMBERS’ DEPOSITS

2007 2006Demand Deposits Chequing $ 41,396,907 $ 20,755,702 Plan 24 8,816,211 9,052,977 Special Savings 1,780,637 1,997,465 51,993,755 31,806,144Term Deposits 53,822,546 36,512,052Registered Savings Plans 20,413,025 19,820,376Accrued Interest Payable 1,473,134 1,058,821 $ 127,702,460 $ 89,197,393

NOTE 7 MEMBERS' SHARES

As at December 31, the three classes of shares consisted of the following issued and fully paid shares: 2007 2006

"A" $ 177,773 $ 168,435 "B" 595,413 548,899 "D" 47,342 45,519 $ 820,528 $ 762,853 The “A” and “B” equity shares are not guaranteed by the Credit Union Deposit Insurance Corporation of British Columbia.

NOTE 8 DIRECTORS’ REMUNERATION

During the current year, the directors, in their capacity as directors, received remuneration of $17,290 (2006 -$11,635).

NOTE 9 REWARDS TO MEMBERS

During the year dividends on shares and Patronage Refunds were paid as follows:

2007 2006

Equity Share Dividends $ 64,578 $ 59,789Non Equity Share Dividends 2,117 2,063Patronage Refunds 214,648 229 $ 281,343 $ 62,081

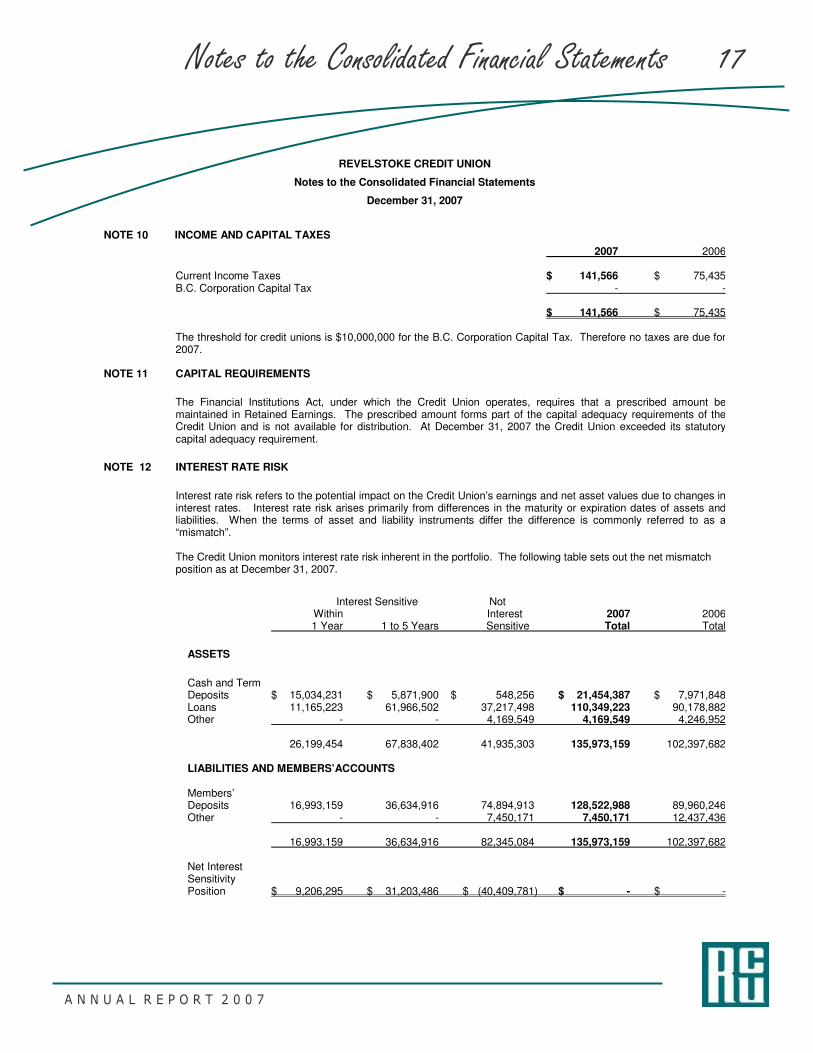

Notes to the Consolidated Financial Statements 17

A N N U A L R E P O R T 2 0 0 7

REVELSTOKE CREDIT UNION

Notes to the Consolidated Financial Statements

December 31, 2007

NOTE 10 INCOME AND CAPITAL TAXES

2007 2006 Current Income Taxes $ 141,566 $ 75,435 B.C. Corporation Capital Tax - - $ 141,566 $ 75,435

The threshold for credit unions is $10,000,000 for the B.C. Corporation Capital Tax. Therefore no taxes are due for 2007.

NOTE 11 CAPITAL REQUIREMENTS

The Financial Institutions Act, under which the Credit Union operates, requires that a prescribed amount be maintained in Retained Earnings. The prescribed amount forms part of the capital adequacy requirements of the Credit Union and is not available for distribution. At December 31, 2007 the Credit Union exceeded its statutory capital adequacy requirement.

NOTE 12 INTEREST RATE RISK

Interest rate risk refers to the potential impact on the Credit Union’s earnings and net asset values due to changes in interest rates. Interest rate risk arises primarily from differences in the maturity or expiration dates of assets and liabilities. When the terms of asset and liability instruments differ the difference is commonly referred to as a “mismatch”.

The Credit Union monitors interest rate risk inherent in the portfolio. The following table sets out the net mismatch position as at December 31, 2007.

Interest Sensitive Not Within Interest 2007 2006 1 Year 1 to 5 Years Sensitive Total Total

ASSETS

Cash and Term Deposits $ 15,034,231 $ 5,871,900 $ 548,256 $ 21,454,387 $ 7,971,848 Loans 11,165,223 61,966,502 37,217,498 110,349,223 90,178,882 Other - - 4,169,549 4,169,549 4,246,952 26,199,454 67,838,402 41,935,303 135,973,159 102,397,682 LIABILITIES AND MEMBERS’ACCOUNTS Members’ Deposits 16,993,159 36,634,916 74,894,913 128,522,988 89,960,246 Other - - 7,450,171 7,450,171 12,437,436 16,993,159 36,634,916 82,345,084 135,973,159 102,397,682 Net Interest Sensitivity Position $ 9,206,295 $ 31,203,486 $ (40,409,781) $ - $ -

18 Notes to the Consolidated Financial Statements

R E V E L S T O K E C R E D I T U N I O N

REVELSTOKE CREDIT UNION

Notes to the Consolidated Financial Statements

December 31, 2007

NOTE 13 FAIR VALUE OF FINANCIAL INSTRUMENTS

Estimated fair values of the financial instruments are set out below. Fair values have been assumed for premises and equipment or any other asset and liability that is not a financial instrument to be book value. 2007 2006 Book Value Fair Value Book Value Fair Value

ASSETS

Cash and Term Deposits $ 21,454,387 $ 21,552,399 $ 7,971,848 $ 7,939,414 Members' Loans 110,349,223 107,038,920 90,178,882 88,100,221 Other and Investments 4,169,549 4,169,549 4,246,952 4,246,952 $ 135,973,159 $ 132,760,868 $ 102,397,682 $ 100,286,587 LIABILITIES Members' Deposits and Shares 128,522,988 128,791,598 89,960,246 90,171,456 Accounts Payable and Retained Earnings 7,450,171 7,450,171 12,437,436 12,437,436

$ 135,973,159 $ 136,241,769 $ 102,397,682 $ 102,608,892 The fair value of items which are highly liquid or short-term in nature approximates their carrying value (such items consist of cash, investments and other assets and liabilities that are considered current). The fair value of loans and member deposits with fixed rates is estimated using present value calculations based on the differences between actual and market rates for similar types of instruments. The fair value of loans and member deposits with variable rates of interest is assumed to be their carrying value.

NOTE 14 FAIR VALUE OF SWAPS

The fair value of interest rate swaps held by Revelstoke Credit Union and as set out in Note 1(e) has been calculated at December 31, 2007 as $5,060,667 (2006 - $5,053,560).

P.O. Box 989 110 Second Street West

Revelstoke, BC Canada V0E 2S0

Telephone: (250) 837-6291 Toll Free: (888) 851-5715

Telebanking: (250) 837-7777 Fax: (250) 837-2431

www.revcu.com

Office Hours

Tuesday to Thursday: 9:30 a.m. to 5:00 p.m. Friday 9:30 a.m. to 6:00 p.m.

Saturday 9:30 a.m. to 1:00 p.m. Sunday / Monday CLOSED

![Surviving Value Based Purchasing - Bobbi Brown · Iwill!now!turn!the!time!over!to!Bobbi!Brown.!! Bobbi…!!! [BobbiBrown]! Okay.!!Thanks,!Tyler.!!We!wantto!welcome!you!all!this!morning!and!Ireally!thank!you!for](https://img.pdfslide.us/doc/110x75/5f3c289f81fdd528a334743a/surviving-value-based-purchasing-bobbi-brown-iwillnowturnthetimeovertobobbibrown.jpg)