Embed Size (px)

DESCRIPTION

2001 CAS ANNUAL MEETING. The Rating Agency’s View Eric Simpson, Moderator (SVP & CFO – DICO, American Re) Matt Mosher, Panelist (GVP – P/C, A.M. Best Company) Karen Davies, Panelist (Senior Analyst, Moody’s Investors Service). Post – WTC Issues for the P/C Insurance Industry. - PowerPoint PPT Presentation

Citation preview

2001 CAS ANNUAL 2001 CAS ANNUAL MEETINGMEETING

The Rating Agency’s View

Eric Simpson, Moderator (SVP & CFO – DICO, American Re)Matt Mosher, Panelist (GVP – P/C, A.M. Best Company)Karen Davies, Panelist (Senior Analyst, Moody’s Investors Service)

Post – WTC Issues for the Post – WTC Issues for the P/C Insurance Industry P/C Insurance Industry

Industry Capacity to Absorb Mega Terrorist Losses and Ongoing Cat, Reserve, & Investment Risks

Ultimate WTC Losses & Likely Market Implications

Analytical Approach for Identifying & Downgrading Weakened (Re) insurers

Market Outlooks for Product Lines/Sectors Most Affected by WTC Disaster

Post – WTC Issues for Post – WTC Issues for the the

P/C Insurance IndustryP/C Insurance Industry Key Drivers of a Company’s Rating;

Significant Changes in Rating Criteria Impact on Rating Agency Capital Adequacy &

Earnings Analysis Additional Risk Management Considerations

Posed By Rating Agencies Implications to VAR & DFA Modeling

CASUALTY ACTUARIAL SOCIETYCASUALTY ACTUARIAL SOCIETY

The Rating Agency’s View

Annual Meeting Annual Meeting

Matthew C. MosherGroup Vice PresidentA.M. Best Company

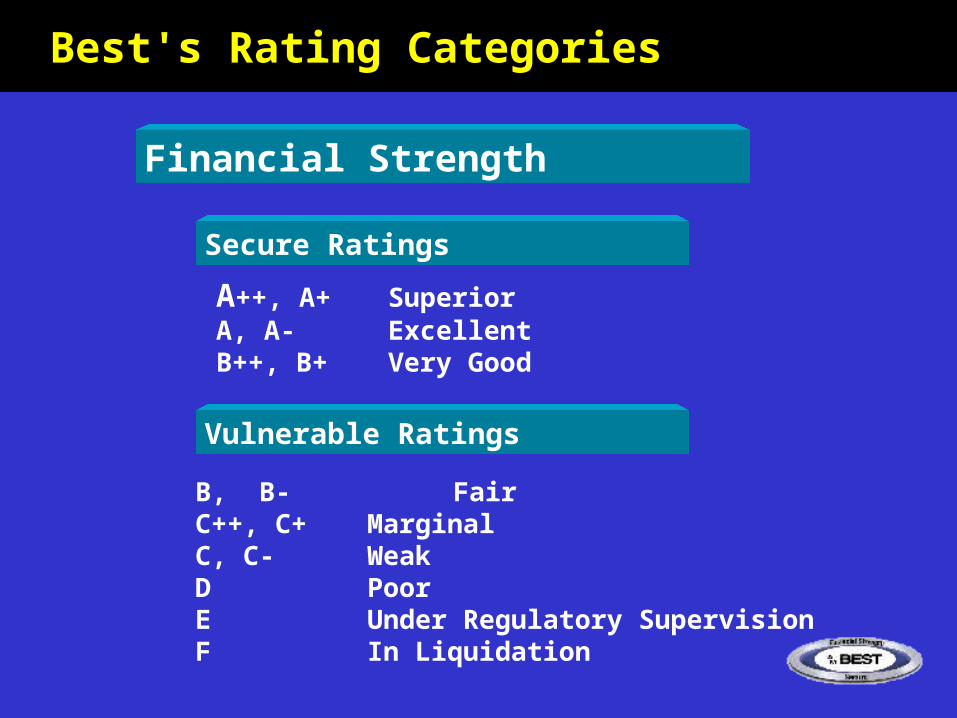

Vulnerable Ratings

Secure Ratings

B, B- FairC++, C+ MarginalC, C- WeakD PoorE Under Regulatory SupervisionF In Liquidation

A++, A+ SuperiorA, A- ExcellentB++, B+ Very Good

Best's Rating CategoriesBest's Rating Categories

Financial Strength

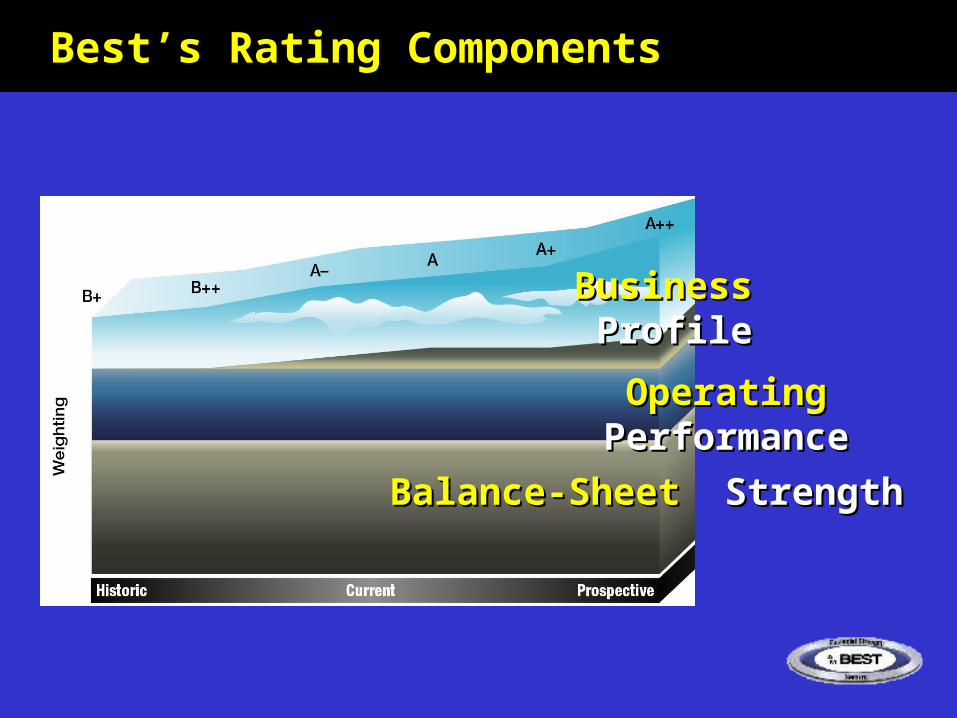

Best’s Rating ComponentsBest’s Rating Components

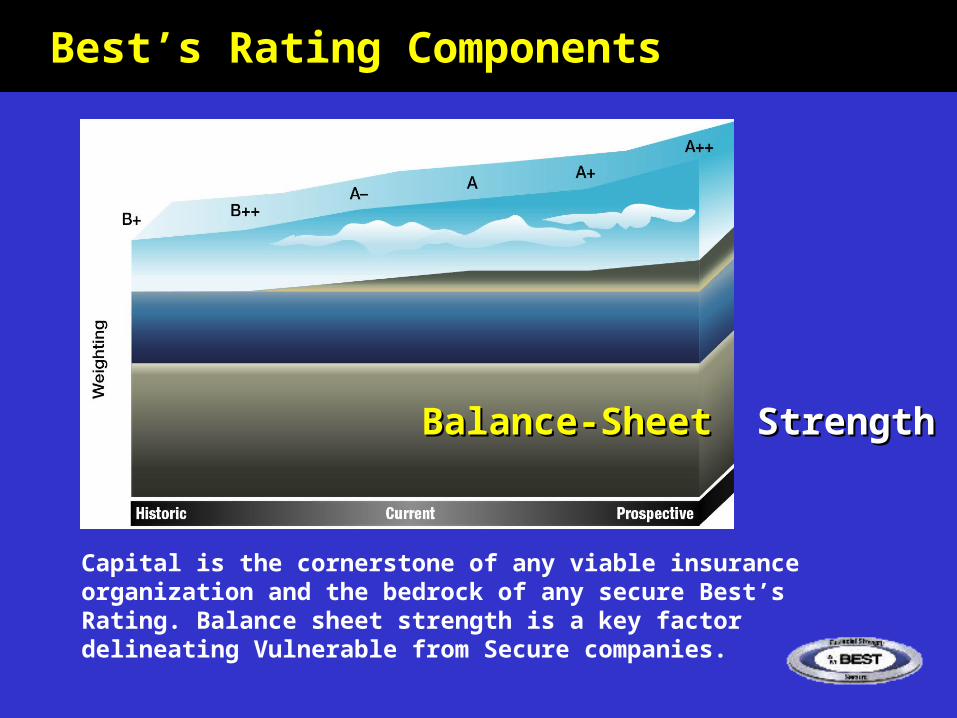

Balance-SheetBalance-Sheet StrengthStrength

OperatingOperating PerformancePerformance

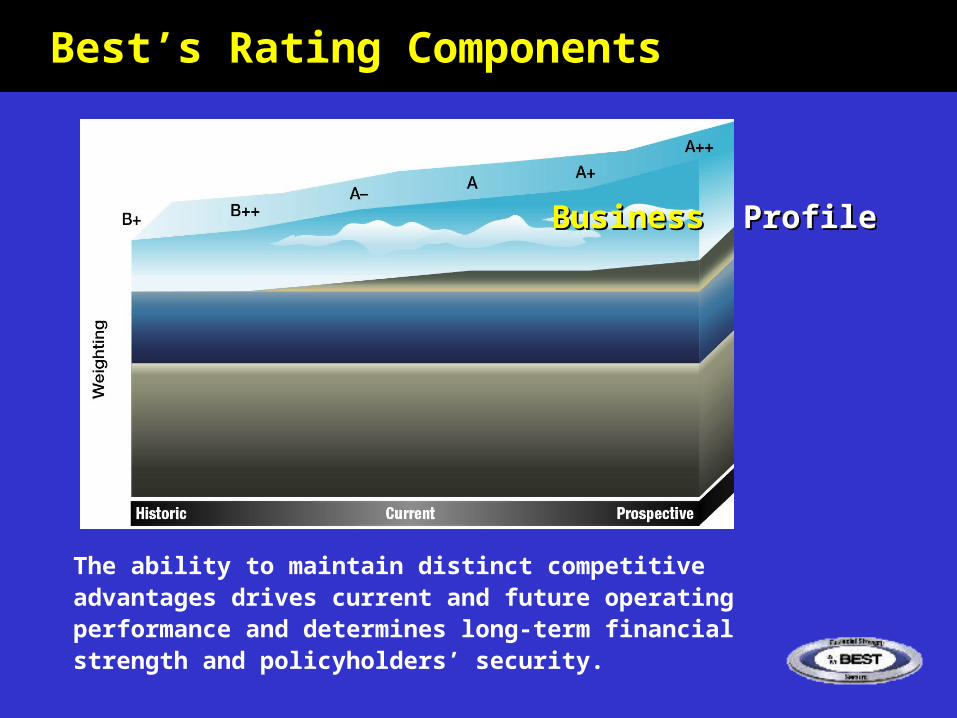

BusinessBusiness ProfileProfile

Best’s Rating ComponentsBest’s Rating Components

Capital is the cornerstone of any viable insurance organization and the bedrock of any secure Best’s Rating. Balance sheet strength is a key factor delineating Vulnerable from Secure companies.

Balance-SheetBalance-Sheet StrengthStrength

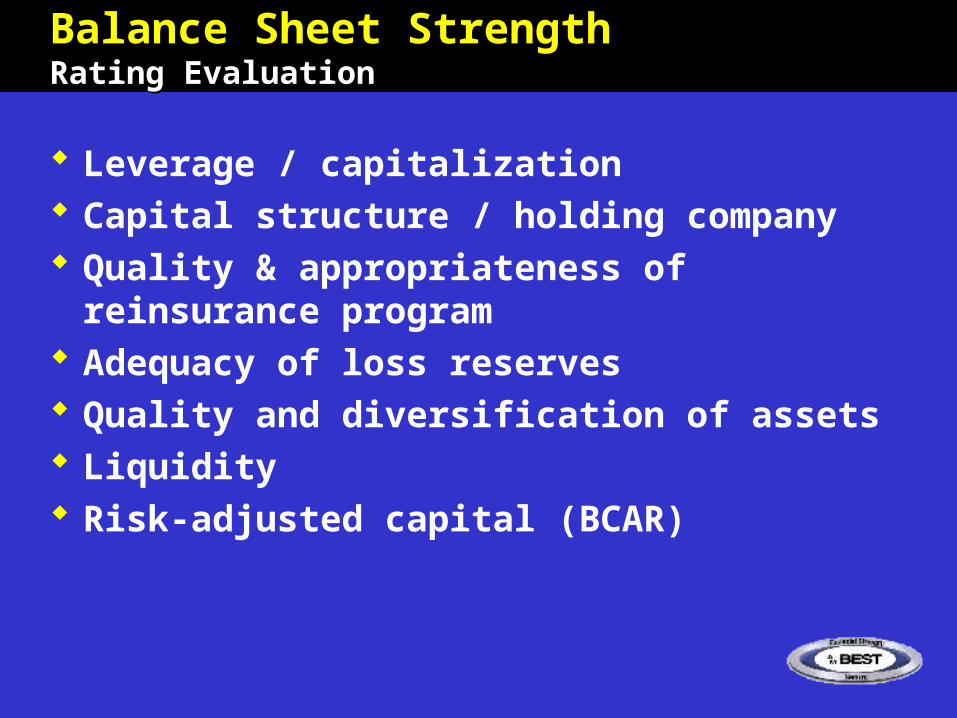

Balance Sheet StrengthBalance Sheet StrengthRating EvaluationRating Evaluation

Leverage / capitalization Capital structure / holding company Quality & appropriateness of reinsurance

program Adequacy of loss reserves Quality and diversification of assets Liquidity Risk-adjusted capital (BCAR)

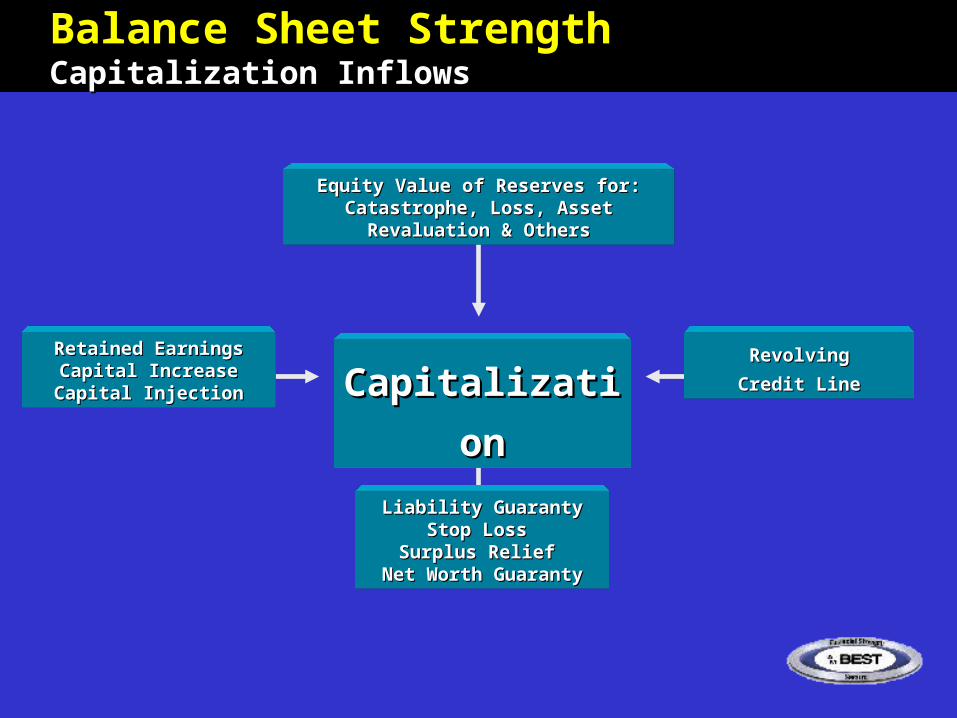

CapitalizatioCapitalizationn

Equity Value of Reserves for: Equity Value of Reserves for: Catastrophe, Loss, Asset Catastrophe, Loss, Asset

Revaluation & OthersRevaluation & Others

Retained EarningsRetained EarningsCapital IncreaseCapital IncreaseCapital InjectionCapital Injection

Liability GuarantyLiability GuarantyStop Loss Stop Loss

Surplus Relief Surplus Relief Net Worth GuarantyNet Worth Guaranty

RevolvingRevolvingCredit LineCredit Line

Balance Sheet StrengthBalance Sheet StrengthCapitalization InflowsCapitalization Inflows

Best’s Rating ComponentsBest’s Rating Components

Demonstrated profitability combined with capital strength are fundamental to long-term financial strength, and therefore to policyholder security.

OperatingOperating PerformancePerformance

Operating PerformanceOperating PerformanceRating EvaluationRating Evaluation

Profitability Revenue composition Management experience & objectives Ability to meet plan

Best’s Rating ComponentsBest’s Rating Components

The ability to maintain distinct competitive advantages drives current and future operating performance and determines long-term financial strength and policyholders’ security.

BusinessBusiness ProfileProfile

Business ProfileBusiness ProfileRating EvaluationRating Evaluation

Market risk Competitive market position Spread of risk Event risk Regulatory risk

Business ProfileBusiness ProfileCompetitive PositionCompetitive Position

Position in its chosen markets relative to direct competitors Advantage or barrier to continued growth Influences ability to respond to:

Market challenges Economic volatility Regulatory change

Influences ability to compete effectively long term Relationship with distributors Diversity of business among different distributors

A.M. Best Rating PerspectiveA.M. Best Rating Perspective

Balance-sheet strength holds the highest weight across all rating levels; however, as the rating levels increase so does the emphasis on operating performance and business profile.

Balance SheetBalance Sheet StrengthStrength

OperatingOperating PerformancePerformance

BusinessBusiness ProfileProfile

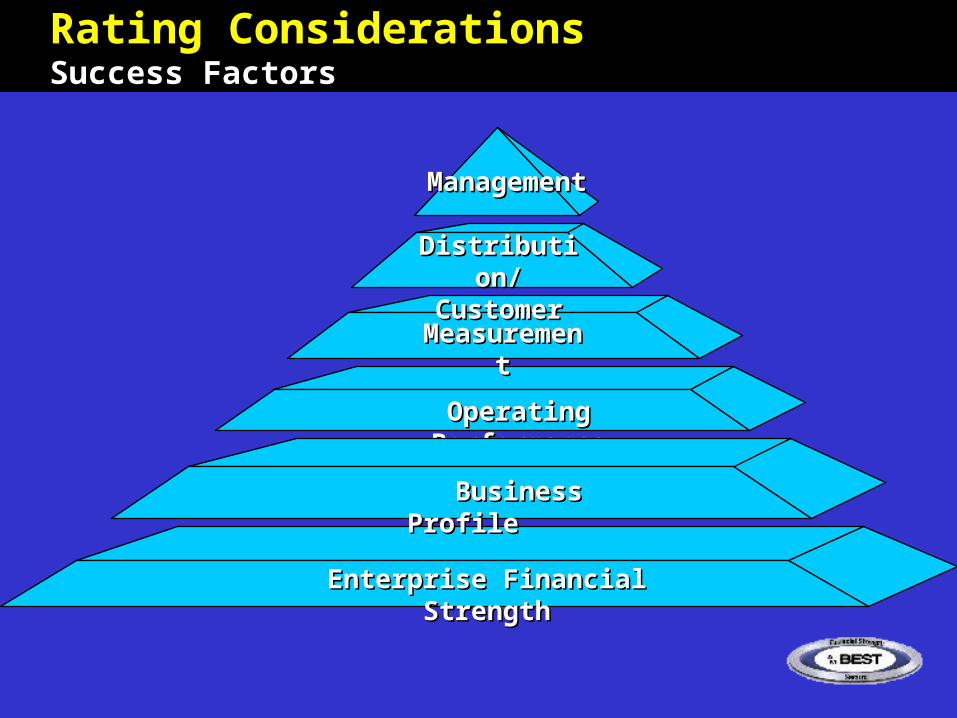

Enterprise Financial StrengthEnterprise Financial Strength

Operating PerformanceOperating Performance

Distribution/Distribution/CustomerCustomer

MeasurementMeasurement

ManagementManagement

Business Profile Business Profile

Rating ConsiderationsRating ConsiderationsSuccess FactorsSuccess Factors

Best’s WTC Rating PerspectiveBest’s WTC Rating Perspective

Rating actions to date mostly one notch adjustments. Phase one—stress test.

Emphasis on capital. Beyond phase one.

Continue to assess companies with direct & indirect exposure. Identify those companies with less obvious exposures. Emphasis on additional factors.

E.G., liquidity, cash flow, earnings capacity. Assess impact of deepening economic crisis on individual companies’ balance

sheet.

Best’s WTC Rating PerspectiveBest’s WTC Rating Perspective

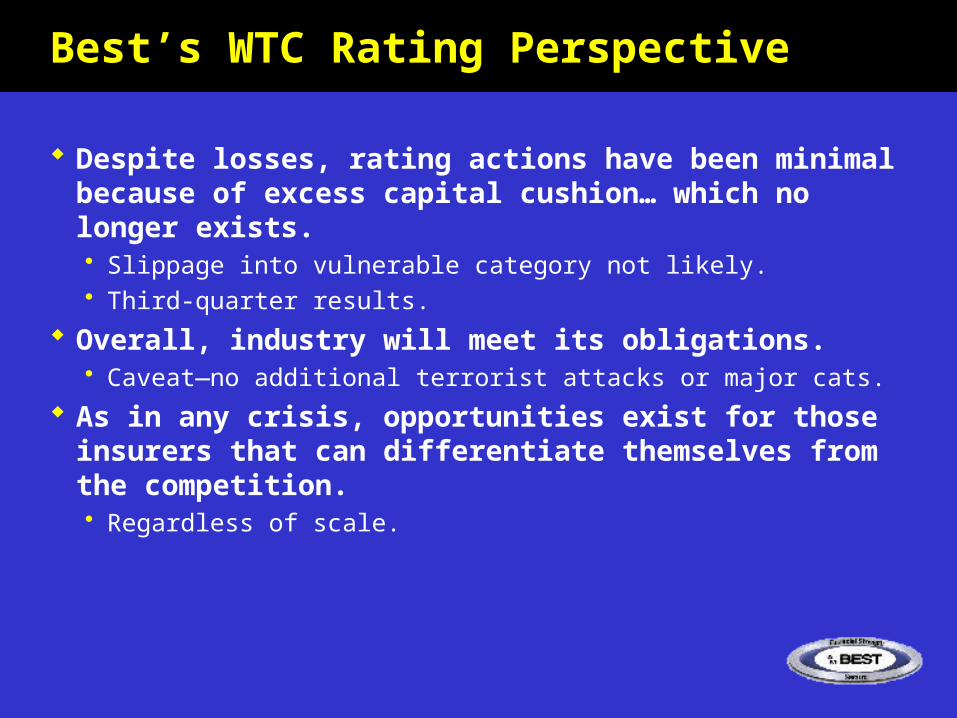

Despite losses, rating actions have been minimal because of excess capital cushion… which no longer exists. Slippage into vulnerable category not likely. Third-quarter results.

Overall, industry will meet its obligations. Caveat—no additional terrorist attacks or major cats.

As in any crisis, opportunities exist for those insurers that can differentiate themselves from the competition. Regardless of scale.

Additional ObservationsAdditional Observations

Events of September 11 changed the insurance industry fundamentally.

Many industry trends accelerated, others altered: Market hardening significantly and rapidly, but prospects for

adequate margins unlikely until 2003. Operating performance adversely effected by volatile and

declining financial markets. Commercial Lines’ excess capital cushion is gone. Pace of industry consolidation and global financial services

convergence will slow.

Additional ObservationsAdditional Observations

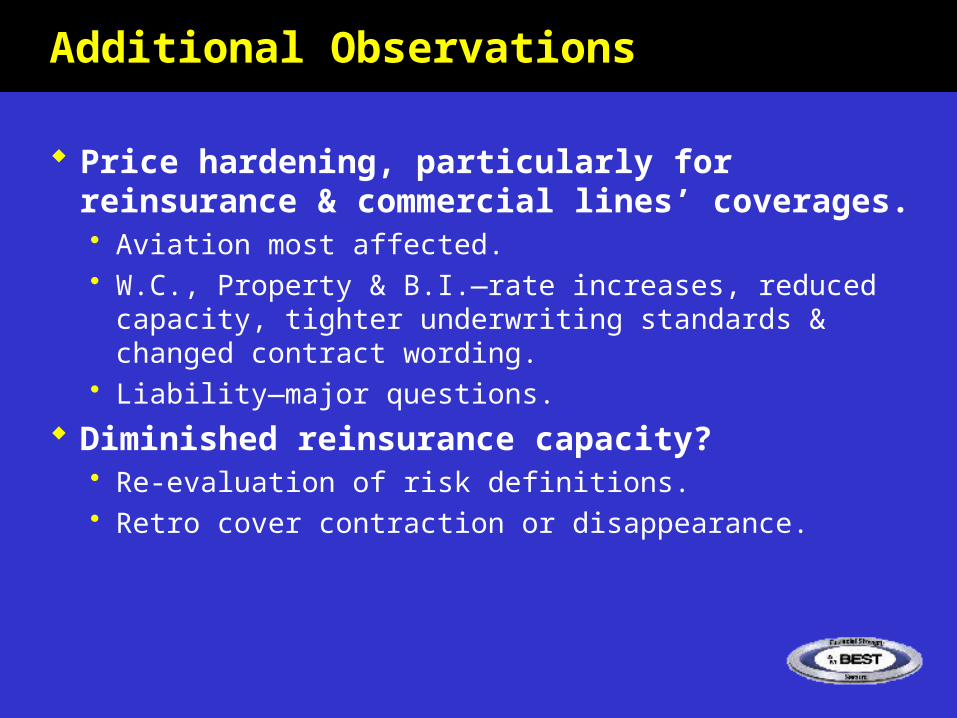

Price hardening, particularly for reinsurance & commercial lines’ coverages. Aviation most affected. W.C., Property & B.I.—rate increases, reduced capacity,

tighter underwriting standards & changed contract wording. Liability—major questions.

Diminished reinsurance capacity? Re-evaluation of risk definitions. Retro cover contraction or disappearance.

Additional ObservationsAdditional Observations

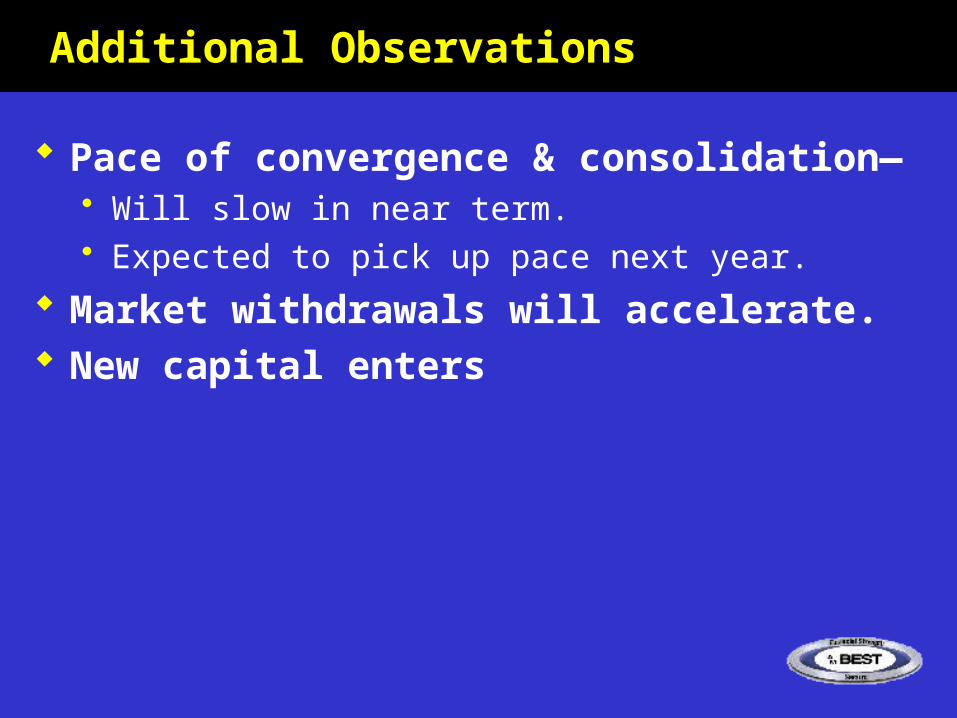

Pace of convergence & consolidation— Will slow in near term. Expected to pick up pace next year.

Market withdrawals will accelerate. New capital enters

Rating Agency’s ViewRating Agency’s View

CAS Annual MeetingCAS Annual Meeting

November 12, 2001November 12, 2001

Karen DaviesKaren DaviesVP/Senior AnalystVP/Senior Analyst

TopicsTopics

Introduction

Moody’s P&C Insurance Ratings

Credit Risk in P&C Insurance

Update on Impact of Terrorist Attacks

Outlook for Ratings of P&C Insurers

IntroductionIntroduction

Recent events have insurers and reinsurers under a spotlight and under a microscope

Against backdrop of past few years’ market turmoil

Pre Sept 11th issues: industry structure and cycle

Post Sept 11th: PV of opportunity vs. risk state

Power of ratings is growing in all markets

TopicsTopics

Introduction

Moody’s P&C Insurance Ratings

Credit Risk in P&C Insurance

Update on Impact of Terrorist Attacks

Outlook for Ratings of P&C Insurers

Moody’s P&C Insurance Moody’s P&C Insurance RatingsRatings

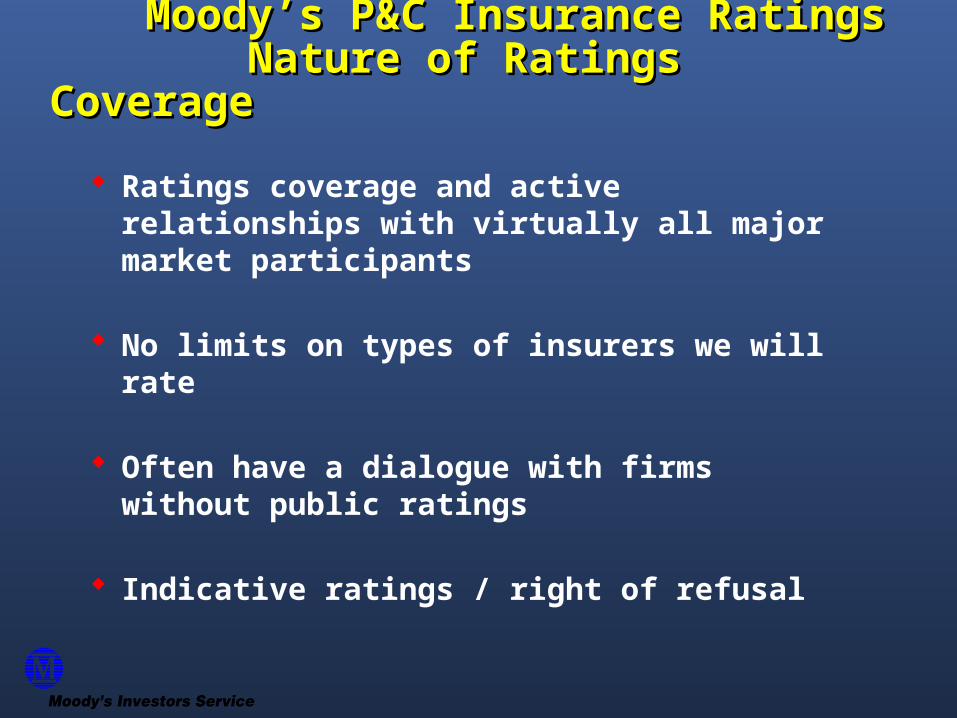

Nature of Ratings Coverage Nature of Ratings Coverage

Ratings coverage and active relationships with virtually all major market participants

No limits on types of insurers we will rate

Often have a dialogue with firms without public ratings

Indicative ratings / right of refusal

Moody’s P&C Insurance Moody’s P&C Insurance RatingsRatings

Meaning of the Ratings Meaning of the Ratings

Debt and preferred: investor orientation - speak to both default frequency and loss-given-default

Financial strength: policyholder orientation - speak to ability to pay, considering recovery value

Rating horizon, long-term (3-5 years)

Financial strength ratings do not speak directly to likelihood or timing of claim payments

Ability Vs. Willingness

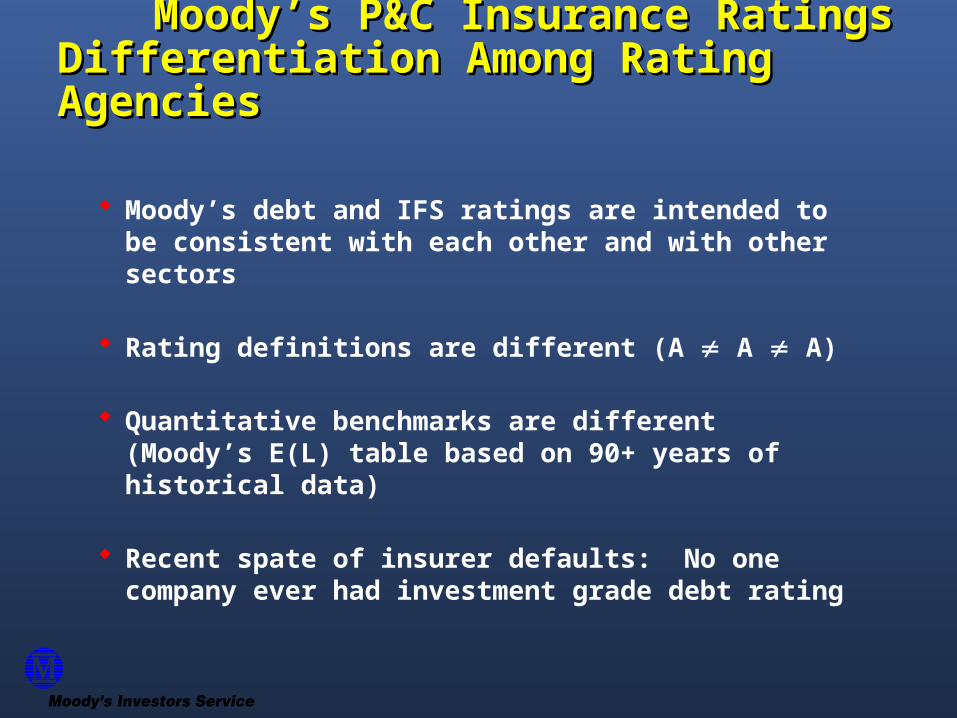

Moody’s P&C Insurance Moody’s P&C Insurance RatingsRatingsDifferentiation Among Rating Differentiation Among Rating AgenciesAgencies

Moody’s debt and IFS ratings are intended to be consistent with each other and with other sectors

Rating definitions are different (A A A)

Quantitative benchmarks are different (Moody’s E(L) table based on 90+ years of historical data)

Recent spate of insurer defaults: No one company ever had investment grade debt rating

TopicsTopics

Introduction

Moody’s P&C Insurance Ratings

Credit Risk in P&C Insurance

Update on Impact of Terrorist Attacks

Outlook for Ratings of P&C Insurers

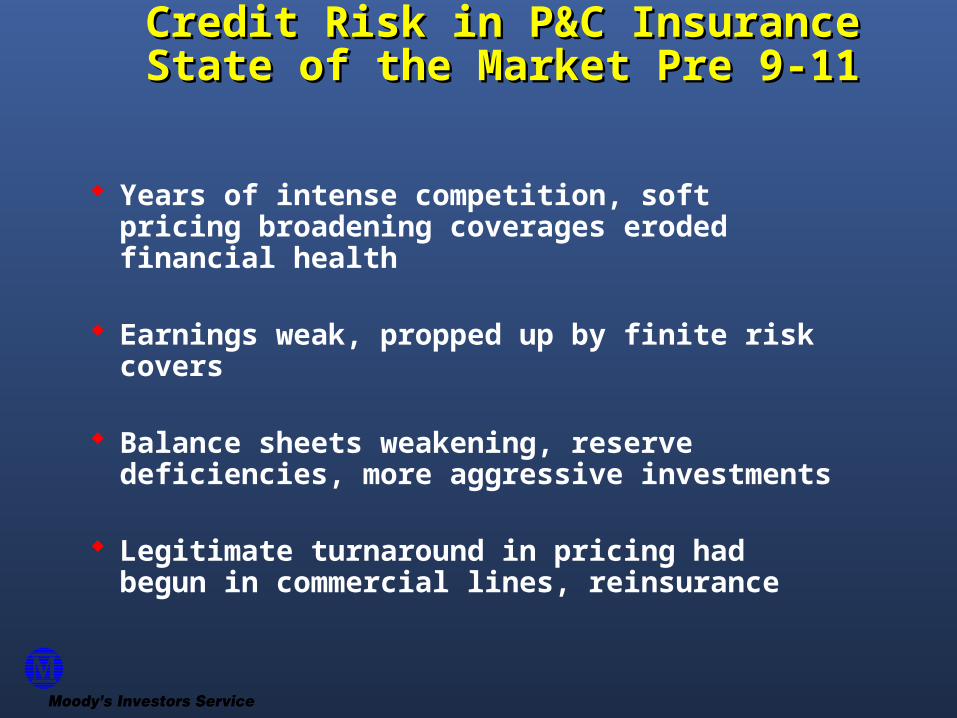

Credit Risk in P&C InsuranceCredit Risk in P&C InsuranceState of the Market Pre 9-11State of the Market Pre 9-11

Years of intense competition, soft pricing broadening coverages eroded financial health

Earnings weak, propped up by finite risk covers

Balance sheets weakening, reserve deficiencies, more aggressive investments

Legitimate turnaround in pricing had begun in commercial lines, reinsurance

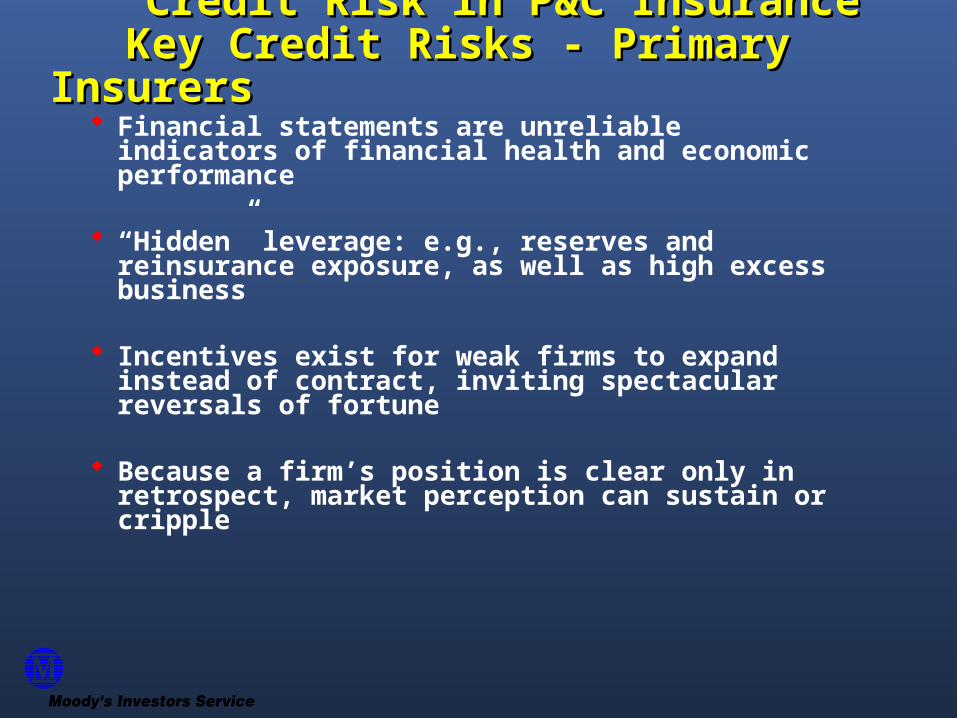

Credit Risk in P&C InsuranceCredit Risk in P&C Insurance Key Credit Risks - Primary Insurers Key Credit Risks - Primary Insurers

Financial statements are unreliable indicators of financial health and economic performance

“Hidden” leverage: e.g., reserves and reinsurance exposure, as well as high excess business

Incentives exist for weak firms to expand instead of contract, inviting spectacular reversals of fortune

Because a firm’s position is clear only in retrospect, market perception can sustain or cripple

Credit Risk in P&C InsuranceCredit Risk in P&C InsuranceKey Credit Risks - ReinsurersKey Credit Risks - Reinsurers

All comments about primary insurers apply, but to a greater degree

As a derivative market, reinsurers face less stable demand function, more capital market competition

Credit Risk in P&C InsuranceCredit Risk in P&C Insurance Recent Reversals of Fortune Recent Reversals of Fortune

New Cap Re

ReAC

Reliance

Frontier

Superior National

HIH

Independent

TopicsTopics

Introduction

Moody’s P&C Insurance Ratings

Credit Risk in P&C Insurance

Update on Impact of Terrorist Attacks

Outlook for Ratings of P&C Insurers

Update: Impact of Terrorist Update: Impact of Terrorist AttacksAttacks

General ObservationsGeneral Observations Unprecedented event in terms of coverages that will

respond and total size of the loss

Magnitude of the industry loss will vary depending on resolution of a number of uncertainties

Huge gap between estimates of industry loss and aggregation of ground-up company reports (2-3x)

Large gap between gross and net loss estimates raise issues of reinsurance recoverable, liquidity

Update: Impact of Terrorist Update: Impact of Terrorist AttacksAttacks

Ratings Placed Under Review Ratings Placed Under Review ACE American Re Chubb Copenhagen Re CNA Hartford (debt) Hannover Re Legion Liberty Mutual

Syn #2488 Syn #2020 Syn #2001 Syn #1007 Syn #1212 Markel Munich Re Partner Re PMA

PXRE Royal & Sun St.. Paul Swiss Re Trenwick XL Zurich Zurich Re

Update: Impact of Terrorist Update: Impact of Terrorist AttacksAttacks

Focus of Rating Reviews Focus of Rating Reviews Magnitude of losses reported, both gross and net, relative

to capitalization, fixed charges, cash flows, and core earnings.

Uncertainty surrounding current estimates of loss, including the prospect for disputes about the extent to which reinsurance will respond.

The extent to which, following the recent attacks, the profile of risk within the insurance industry has changed, at least for some period of time.

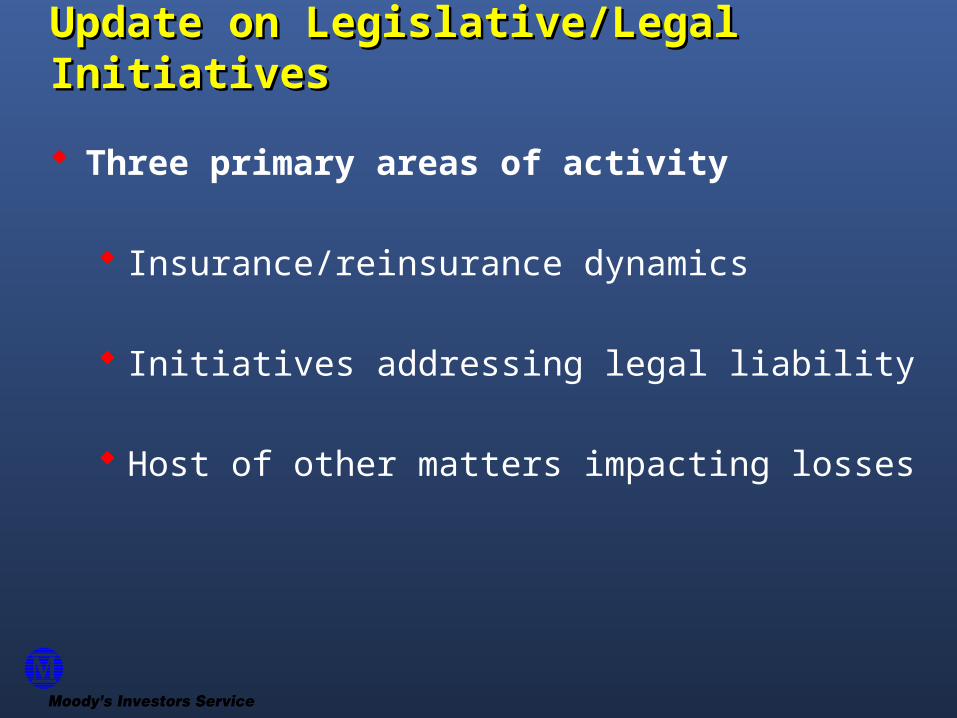

Update on Legislative/Legal Update on Legislative/Legal InitiativesInitiatives Three primary areas of activity

Insurance/reinsurance dynamics

Initiatives addressing legal liability

Host of other matters impacting losses

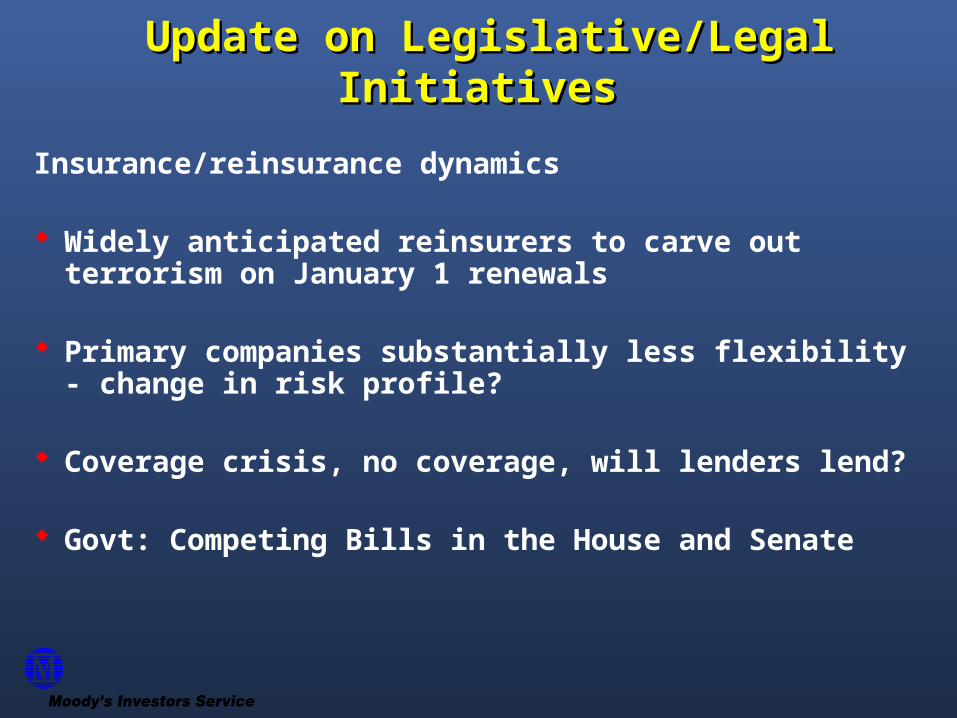

Update on Legislative/Legal Update on Legislative/Legal InitiativesInitiatives

Insurance/reinsurance dynamics

Widely anticipated reinsurers to carve out terrorism on January 1 renewals

Primary companies substantially less flexibility - change in risk profile?

Coverage crisis, no coverage, will lenders lend?

Govt: Competing Bills in the House and Senate

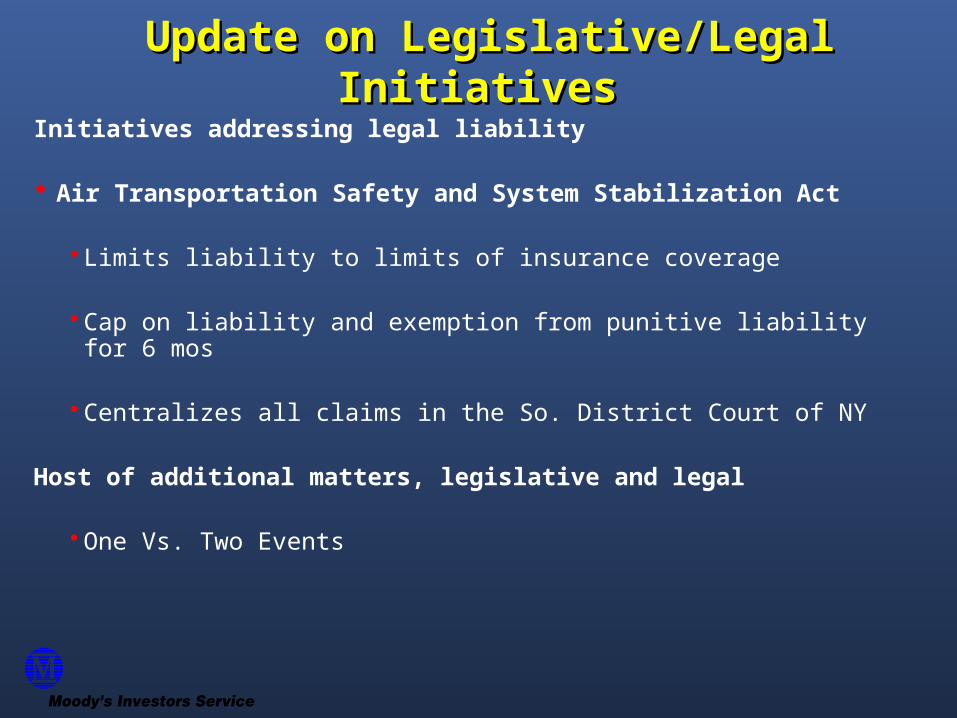

Update on Legislative/Legal Update on Legislative/Legal InitiativesInitiatives

Initiatives addressing legal liability

Air Transportation Safety and System Stabilization Act

Limits liability to limits of insurance coverage

Cap on liability and exemption from punitive liability for 6 mos

Centralizes all claims in the So. District Court of NY

Host of additional matters, legislative and legal

One Vs. Two Events

TopicsTopics

Introduction

Moody’s P&C Insurance Ratings

Credit Risk in P&C Insurance

Update on Impact of Terrorist Attacks

Outlook for Ratings of P&C Insurers

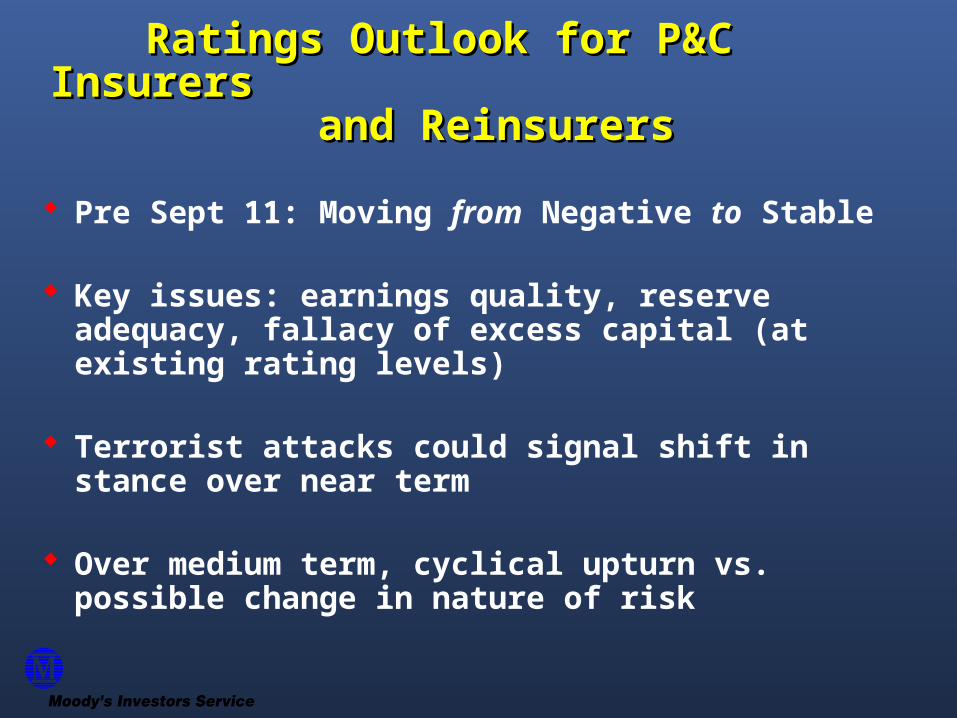

Ratings Outlook for P&C Insurers Ratings Outlook for P&C Insurers

and Reinsurers and Reinsurers Pre Sept 11: Moving from Negative to Stable

Key issues: earnings quality, reserve adequacy, fallacy of excess capital (at existing rating levels)

Terrorist attacks could signal shift in stance over near term

Over medium term, cyclical upturn vs. possible change in nature of risk