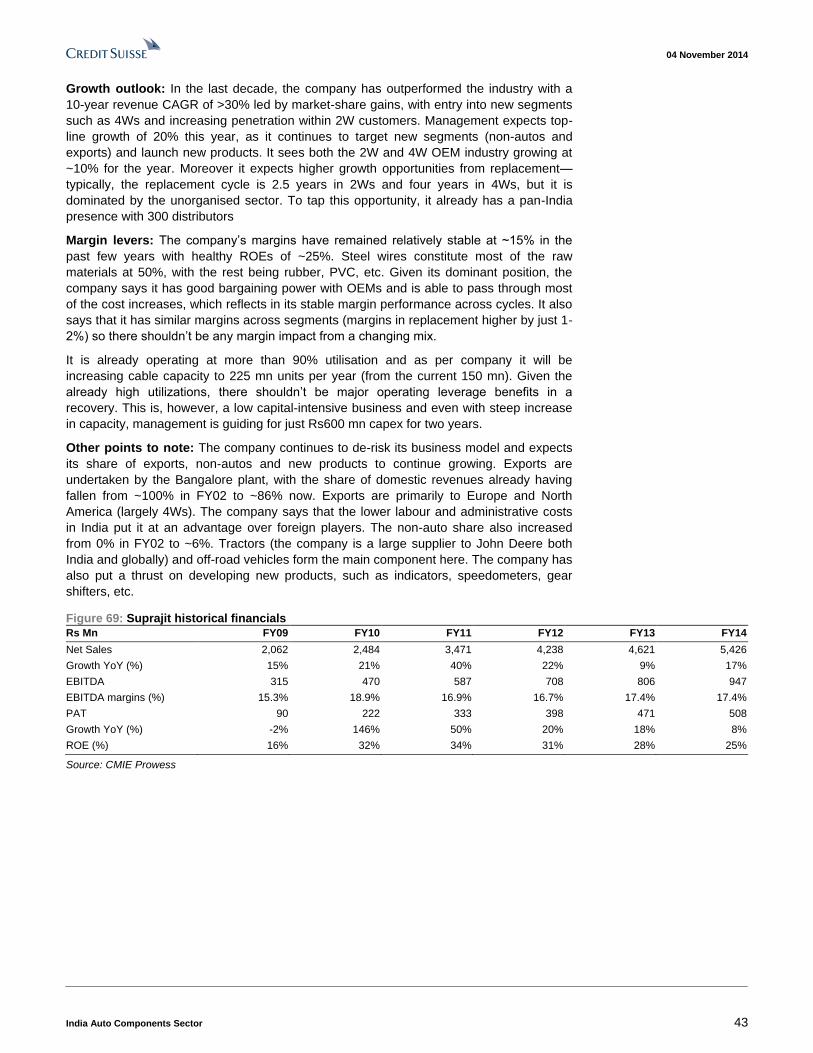

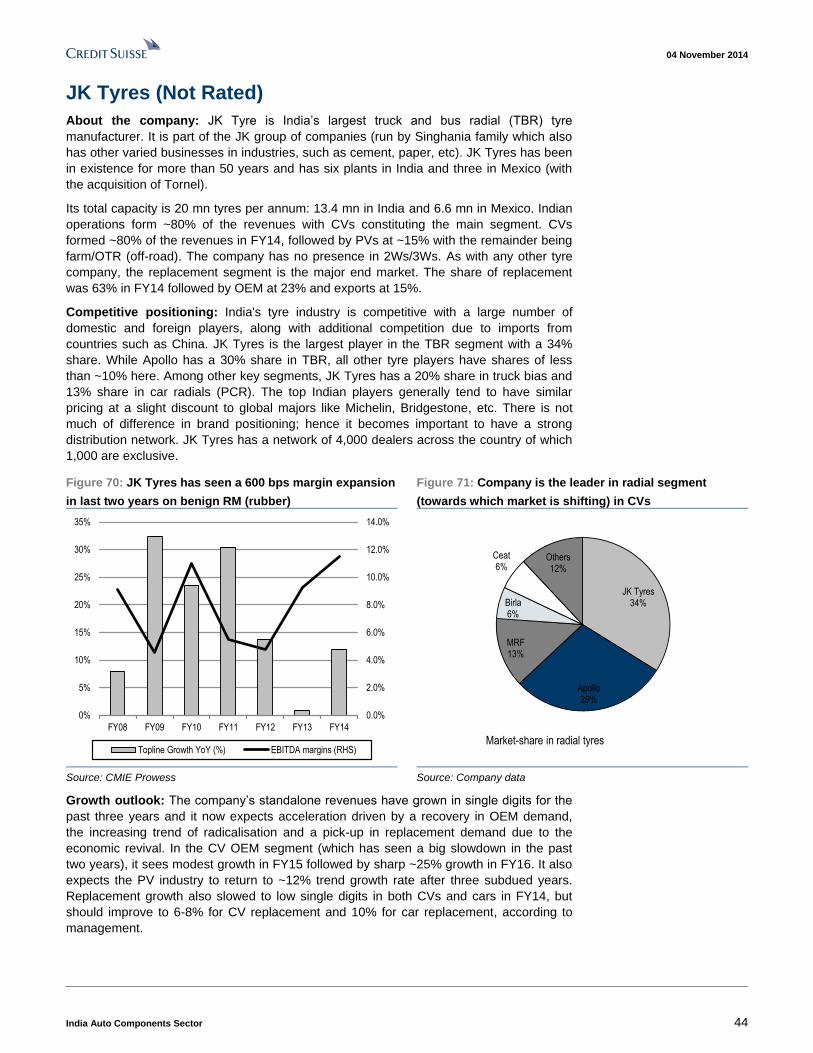

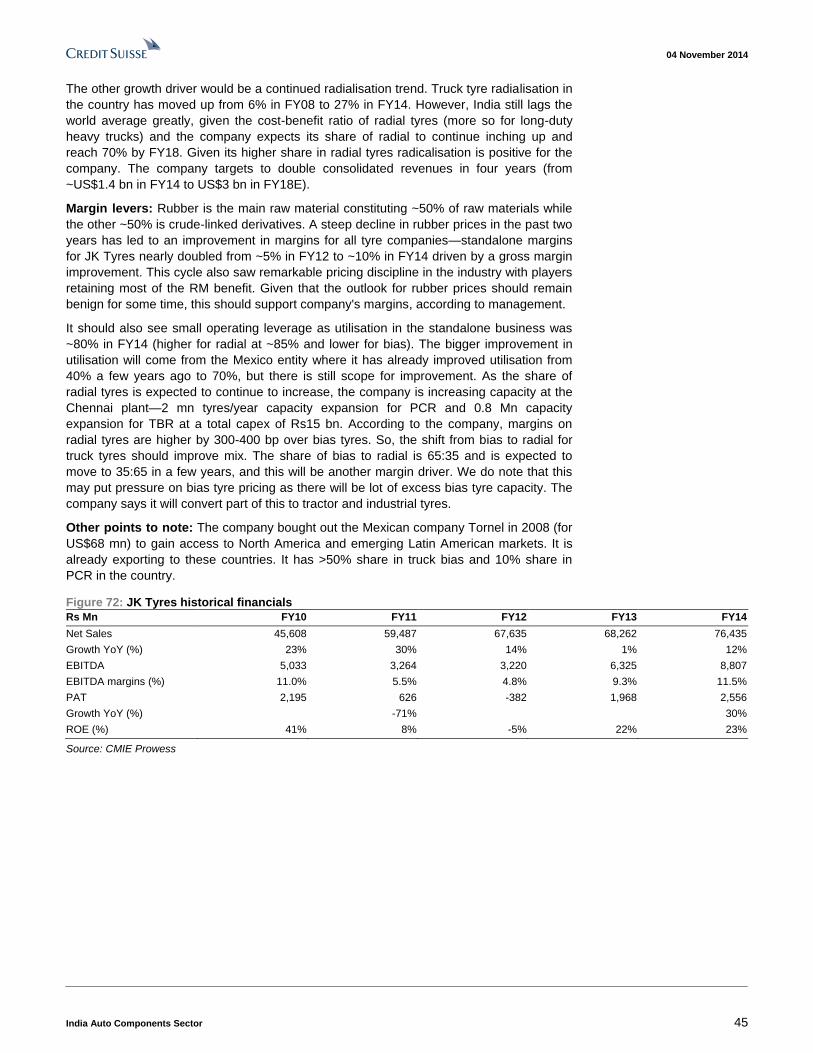

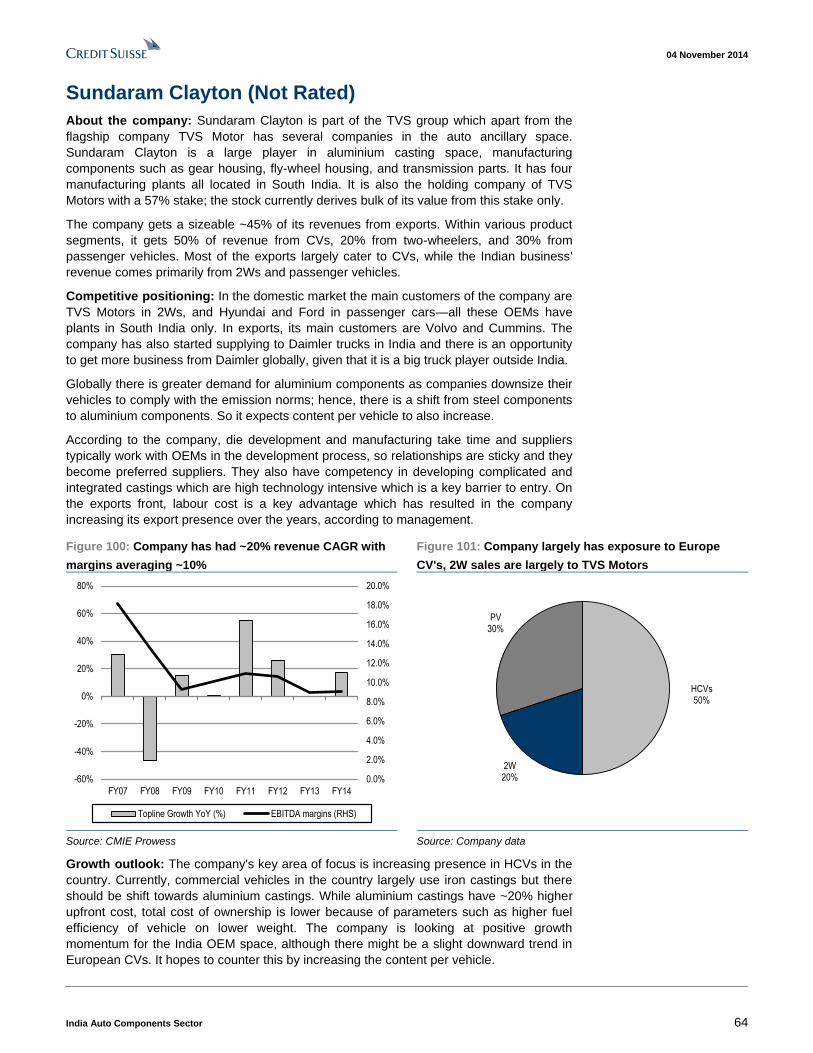

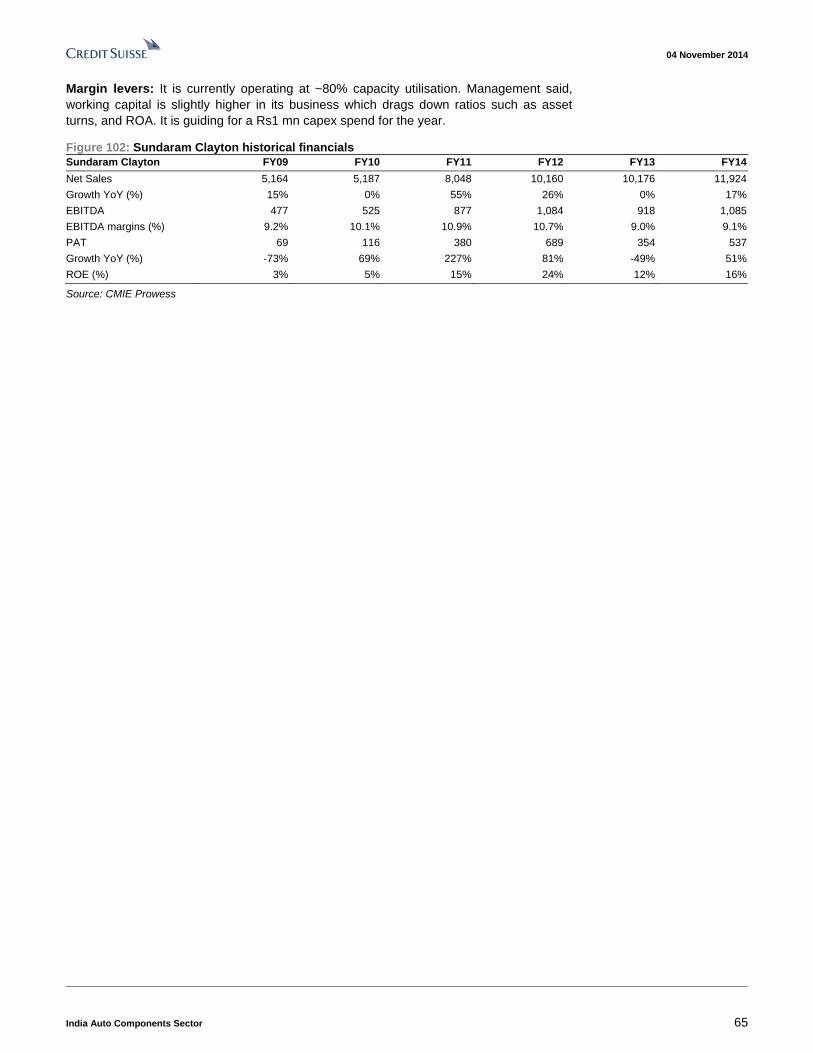

Embed Size (px)

Citation preview

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

04 November 2014

Asia Pacific/India

Equity Research

Auto Parts & Equipment (Automobiles & Components IN (Asia)/Media IN (Asia))

India Auto Components Sector THEME

On the fast track

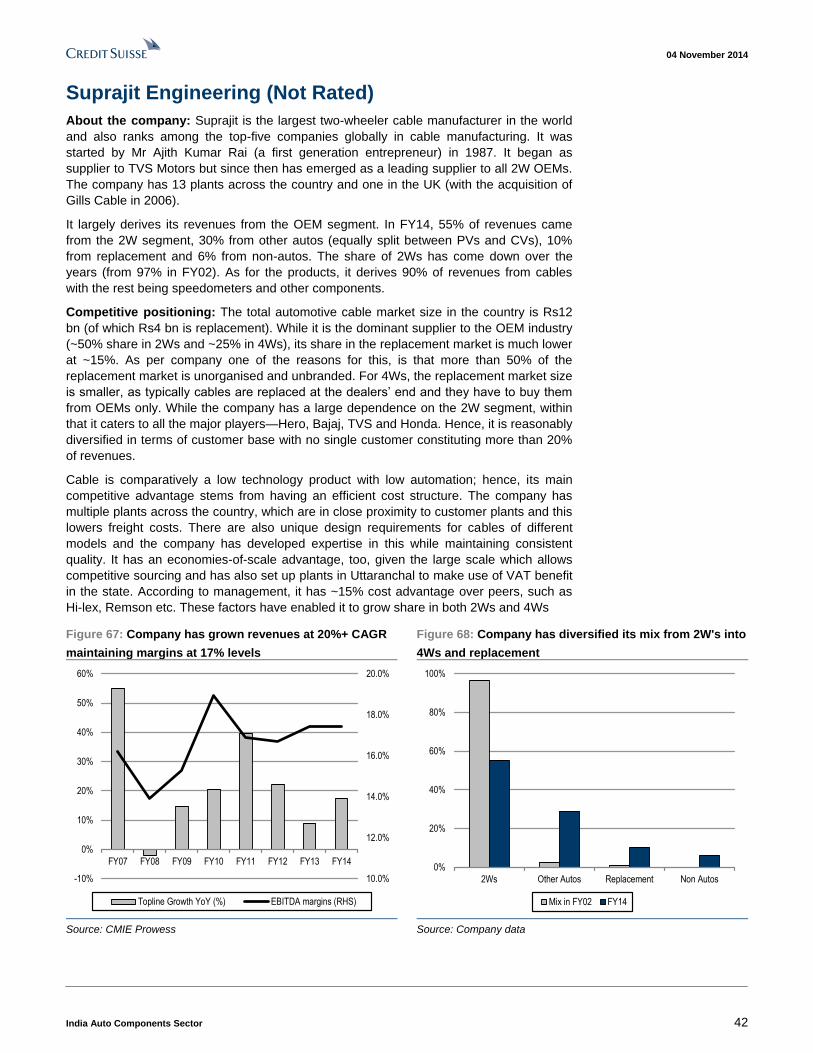

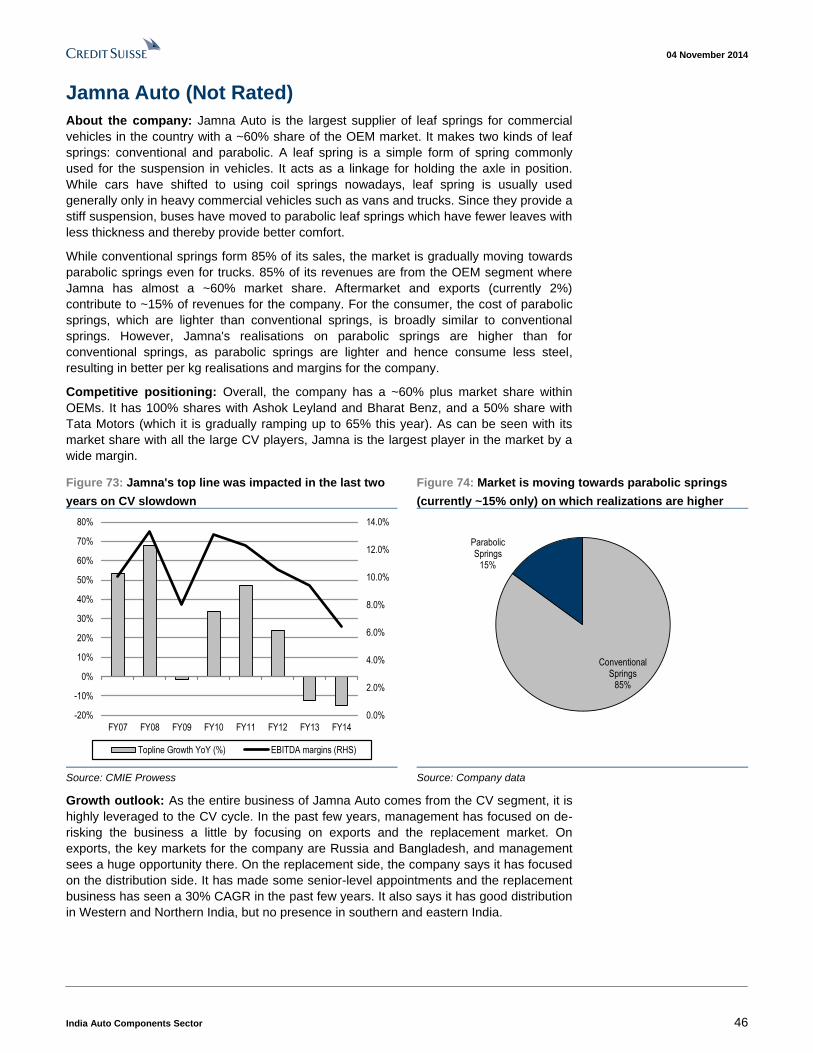

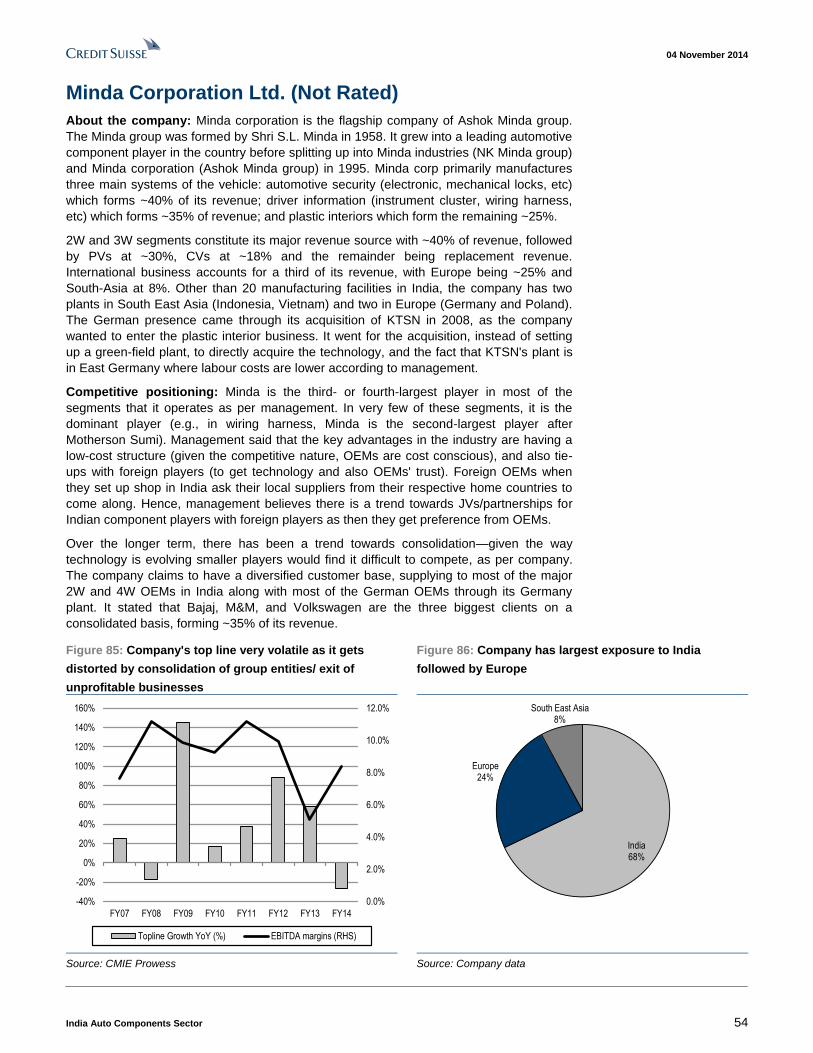

Figure 1: Auto components industry has grown faster than OEMs in the past

ten years and better maintained profitability and return ratios

-10.0%

0.0%

10.0%

20.0%

Revenue growth Change in Gross margins Change in EBITDA margins Change in ROEs

Auto OEMs Auto Parts

Trend in last 10 years

Source: Company data, Credit Suisse estimates, CMIE Prowess

■ Auto components industry may grow faster than OEMs. In the past ten

years, the top 100 auto component companies' revenue growth has

outpaced that of original equipment manufacturers (OEM) by >500 bp. We

expect this trend to accelerate on: (1) OEMs' efforts to consolidate vendors;

(2) higher localisation; (3) faster export growth; (4) rising content per vehicle;

and (5) faster replacement market growth.

■ Mapping the small-cap auto component companies. As all the large

Indian auto component companies have a very high exposure to global

markets, and thus are not plays on an Indian recovery, we met

managements of 15 small-cap Indian auto component companies over the

past month. Within our coverage of the auto component sector, we prefer

companies having: (1) exposure to passenger and commercial vehicles; (2)

products with technological edge; (3) dominant share in key products; (4)

diversified customer base; (5) opportunity to expand into new products; (6)

improving product mix; and (7) low margin volatility.

■ Prefer CV component plays; initiating coverage on Wabco; raise TP on

Apollo, and Bharat Forge. We have a positive view on the CV cycle;

however, Ashok Leyland (an OEM play) is now pricing in best-case earnings;

we downgrade it to NEUTRAL. We prefer a basket of CV component stocks.

We initiate coverage on Wabco with an OUTPERFORM rating and a TP of

Rs4,820 (34.5% potential upside), and upgrade our TPs on Apollo Tyres and

Bharat Forge. Wabco has an ~80% market share in the CV braking industry in

India and is a good structural play on CVs, with safety and emission content

per truck in India being a tenth that of European markets. A CV cycle recovery

and mandatory ABS implementation are near-term stock triggers, in our view.

Research Analysts

Jatin Chawla

91 22 6777 3719

Akshay Saxena

91 22 6777 3825

04 November 2014

India Auto Components Sector 2

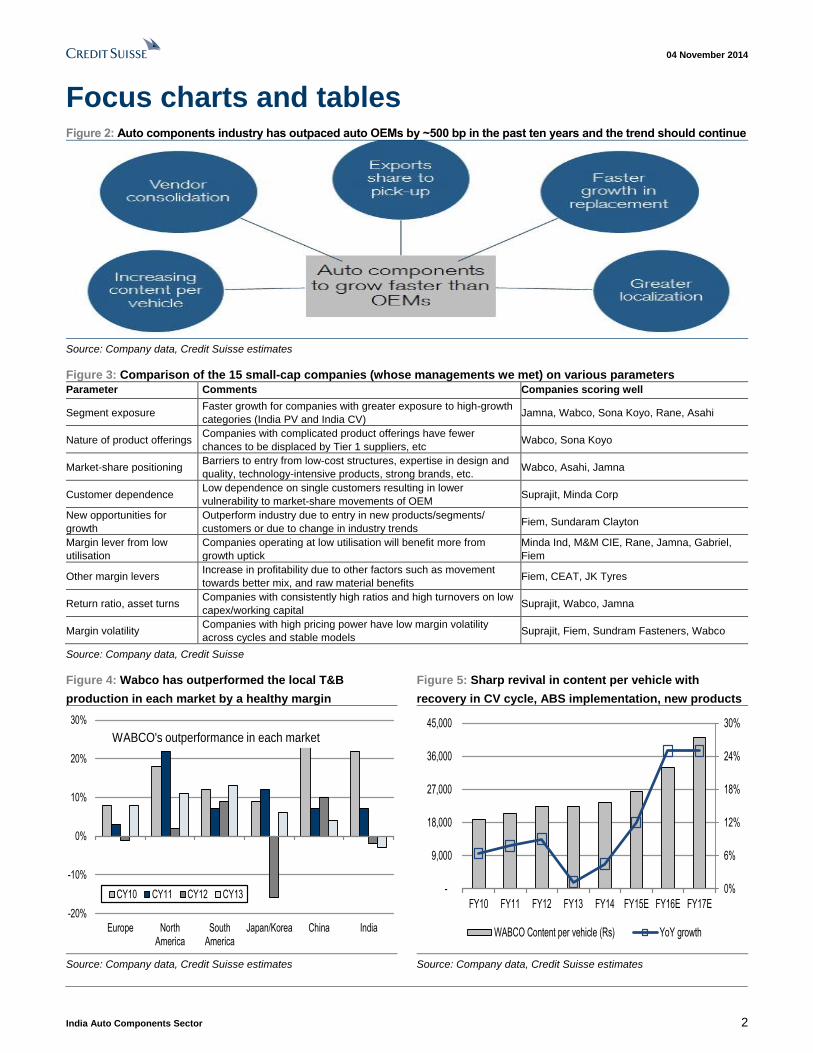

Focus charts and tables Figure 2: Auto components industry has outpaced auto OEMs by ~500 bp in the past ten years and the trend should continue

Source: Company data, Credit Suisse estimates

Figure 3: Comparison of the 15 small-cap companies (whose managements we met) on various parameters

Parameter Comments Companies scoring well

Segment exposure Faster growth for companies with greater exposure to high-growth

categories (India PV and India CV) Jamna, Wabco, Sona Koyo, Rane, Asahi

Nature of product offerings Companies with complicated product offerings have fewer

chances to be displaced by Tier 1 suppliers, etc Wabco, Sona Koyo

Market-share positioning Barriers to entry from low-cost structures, expertise in design and

quality, technology-intensive products, strong brands, etc. Wabco, Asahi, Jamna

Customer dependence Low dependence on single customers resulting in lower

vulnerability to market-share movements of OEM Suprajit, Minda Corp

New opportunities for

growth

Outperform industry due to entry in new products/segments/

customers or due to change in industry trends Fiem, Sundaram Clayton

Margin lever from low

utilisation

Companies operating at low utilisation will benefit more from

growth uptick

Minda Ind, M&M CIE, Rane, Jamna, Gabriel,

Fiem

Other margin levers Increase in profitability due to other factors such as movement

towards better mix, and raw material benefits Fiem, CEAT, JK Tyres

Return ratio, asset turns Companies with consistently high ratios and high turnovers on low

capex/working capital Suprajit, Wabco, Jamna

Margin volatility Companies with high pricing power have low margin volatility

across cycles and stable models Suprajit, Fiem, Sundram Fasteners, Wabco

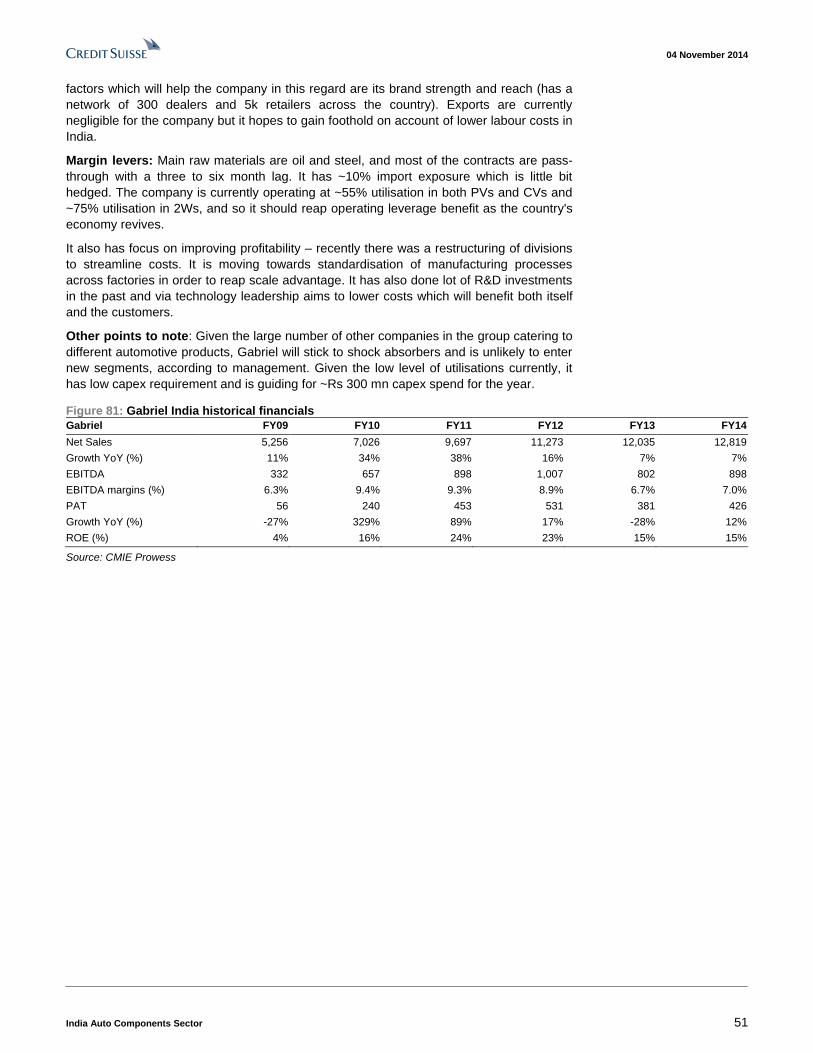

Source: Company data, Credit Suisse

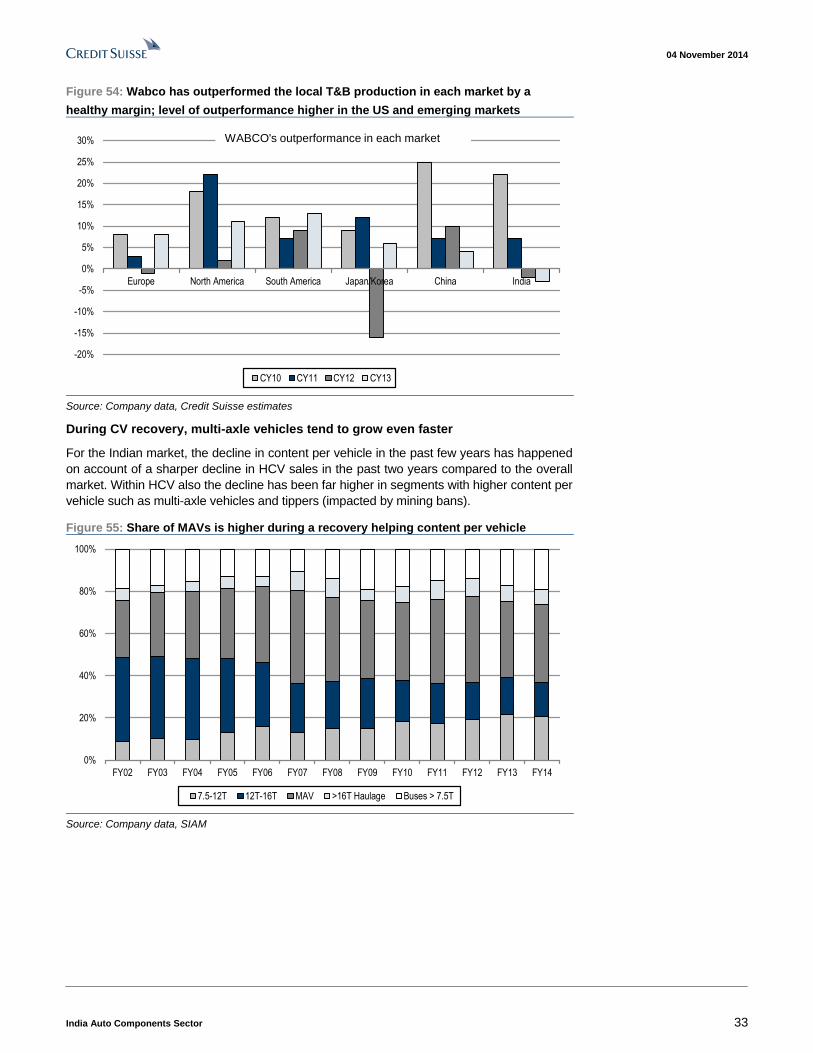

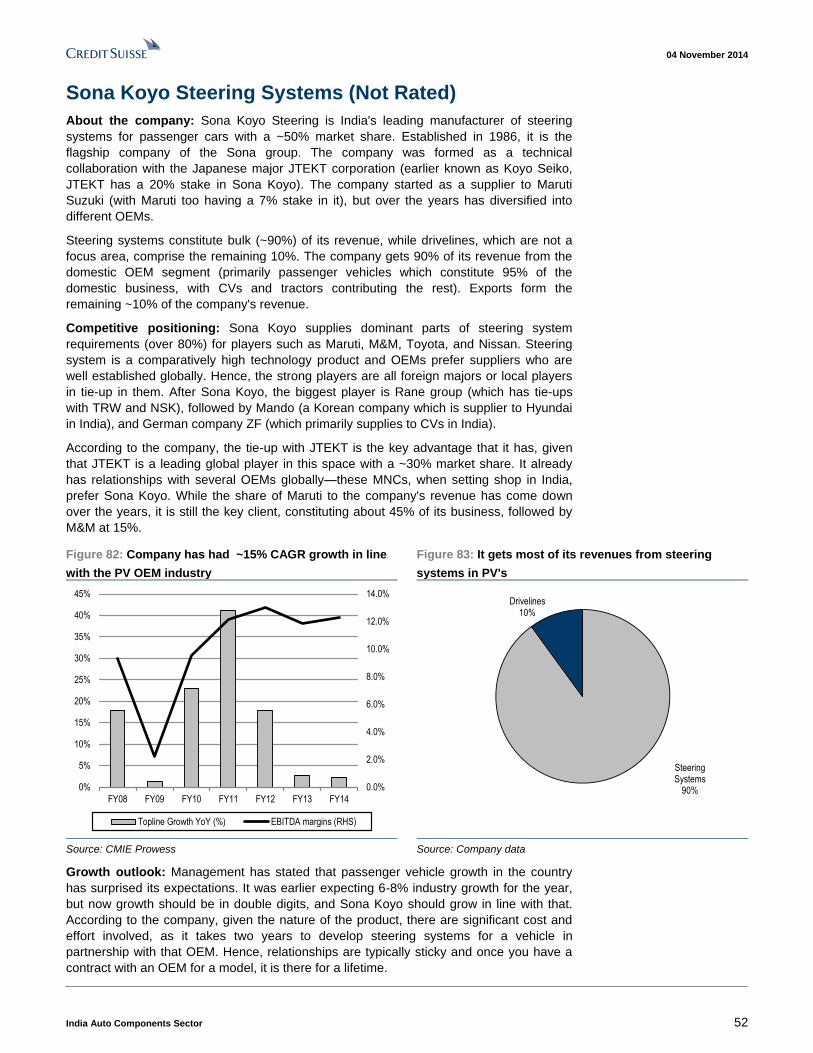

Figure 4: Wabco has outperformed the local T&B

production in each market by a healthy margin

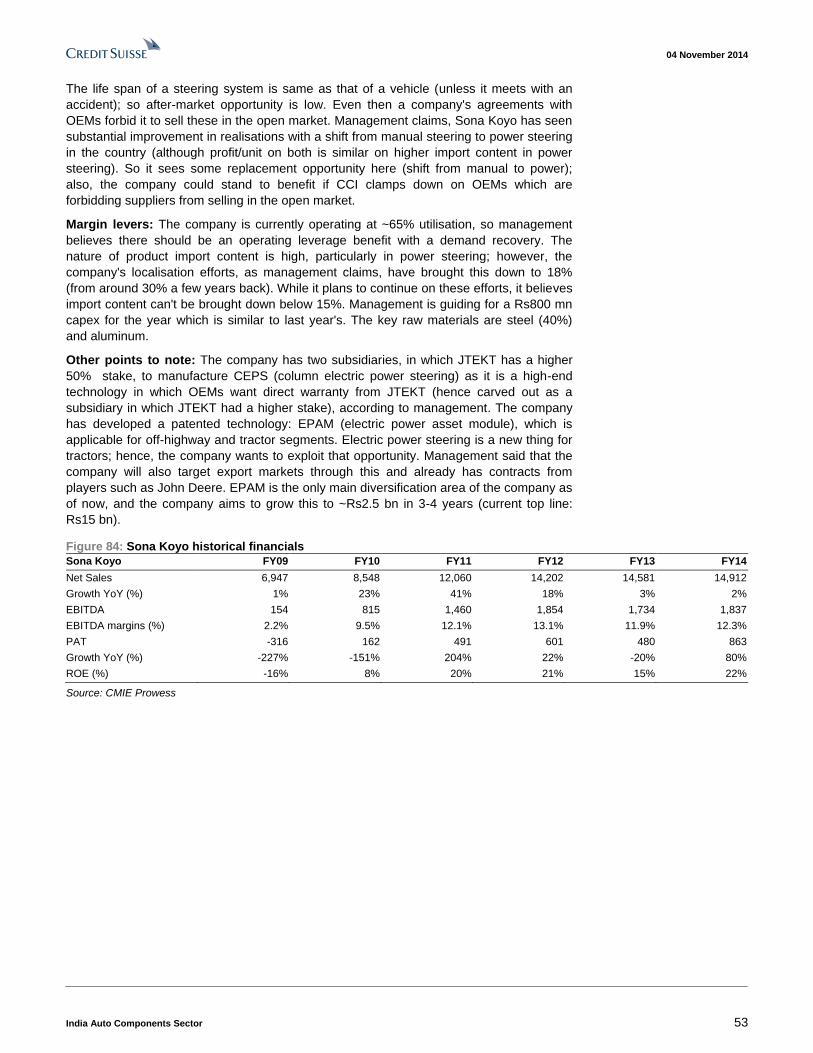

Figure 5: Sharp revival in content per vehicle with

recovery in CV cycle, ABS implementation, new products

-20%

-10%

0%

10%

20%

30%

Europe NorthAmerica

SouthAmerica

Japan/Korea China India

CY10 CY11 CY12 CY13

WABCO's outperformance in each market

0%

6%

12%

18%

24%

30%

-

9,000

18,000

27,000

36,000

45,000

FY10 FY11 FY12 FY13 FY14 FY15E FY16E FY17E

WABCO Content per vehicle (Rs) YoY growth

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

04 November 2014

India Auto Components Sector 3

On the fast track Geared for growth In the past ten years, the top-line CAGR of auto components industry has outpaced that of

auto OEMs by >500 bp, and we expect this gap to widen further on: (1) a consolidation of

the industry as OEMs increasingly move towards a single/lesser supplier model—share of

top ten players is up >500 bp in the past five years; (2) the rising share of exports as

foreign-based OEMs look to source greater components from India—exports have

increased from US$3.5 bn in FY07 to US$10 bn in FY14; (3) sizeable growth opportunity

in the replacement segment (margins are 300-400 bp higher than the OEM segment) as

consumers up-trade from the unorganised segment; GST implementation can reduce the

pricing gap (~40%) between organised and unorganised, and CCI clampdown on OEMs

regarding spares' availability could expand the market; (4) Indian arms of foreign OEMs

increasing localisation in the wake of rising costs in a competitive environment (gap of

almost ~15% between Maruti and other MNCs); and (5) increasing content per vehicle,

driven by regulation and consumer aspirations.

Our analysis of the consolidated industry financials indicates that the components sector

is well placed to tap into this future growth; utilisation rates remain low (~70%),

indicating margin expansion from operating leverage as the cycle recovers. Despite

slowing top-line growth, components companies managed to improve gross margins,

driven by export profitability and some raw material benefit (which could increase further

if commodity prices remain benign). PAT margins are though only steady because of

negative operating leverage.

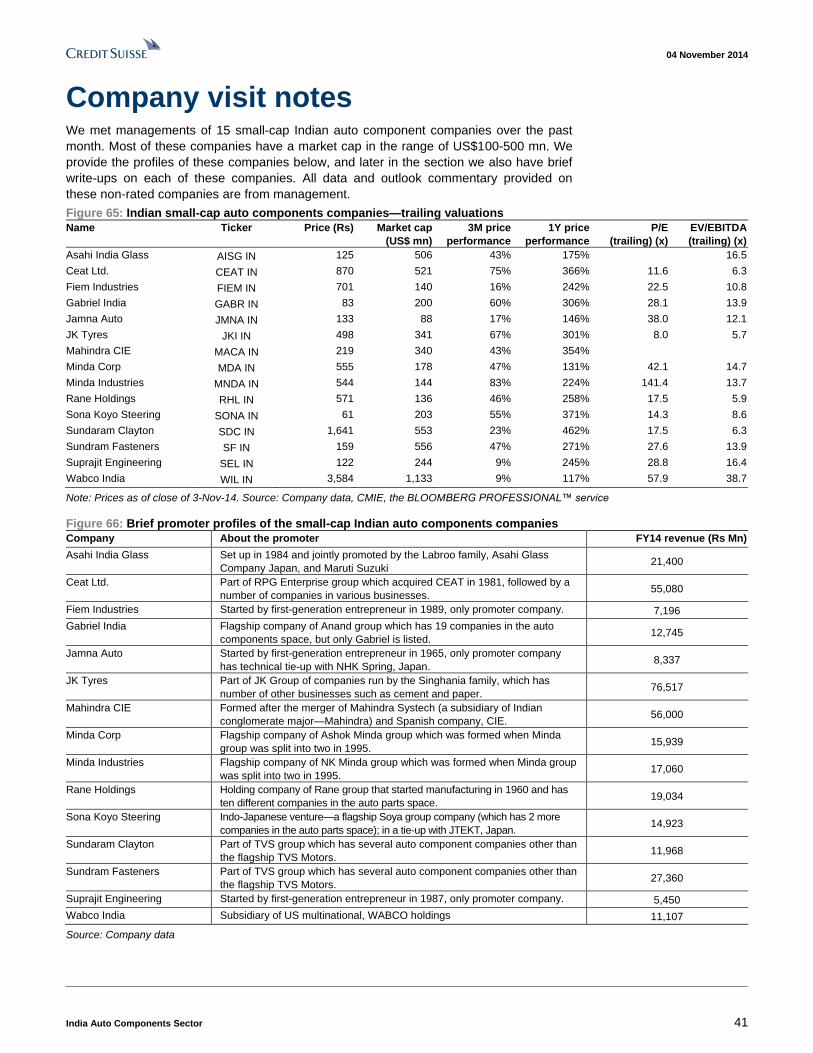

Conversations with small-cap companies We met managements of 15 small-cap Indian auto component companies (US$100-500

mn market cap) over the past month (short write-ups on each company are provided later).

Our discussions with them indicate that while demand is improving with suppliers across

segments, they are still not outright bullish.

We believe the auto component sector can be assessed on the following parameters:

On growth parameters, we like companies having: (1) larger exposure to the India OEM

space (particularly PVs and CVs), (2) product offerings with a technological edge, (3)

dominant market share positioning in key segments with entry barriers, (4) a diversified

customer base with low exposure to a single customer, and (5) the potential to outperform

market growth from untapped opportunities such as new product, and new segment.

Based on margin lever parameters, we like companies that can improve margins in the near

term on: (1) operating leverage benefit from an uptick in utilisation, as growth returns and (2)

other margin levers such as movement towards better mix, and benign raw materials. On

financial parameters we like companies that have: (1) high return ratios and higher asset turns,

and (2) low margin volatility across cycles, denoting stable model and high pricing power.

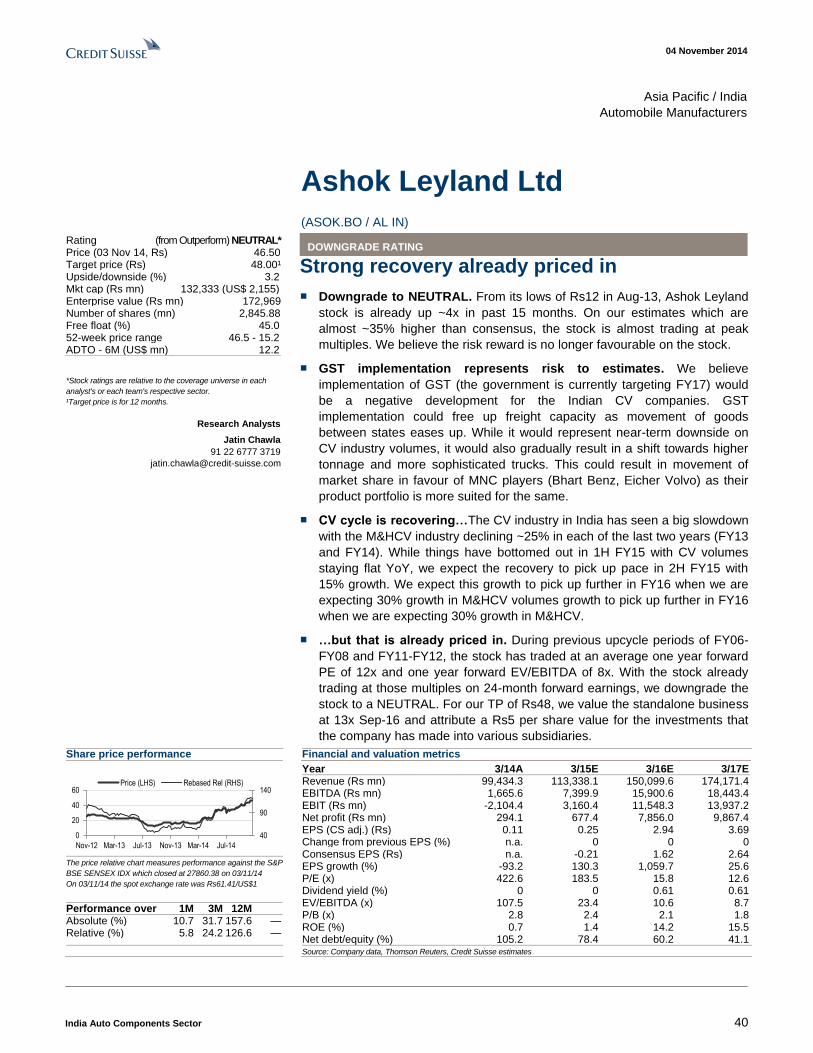

A basket of component stocks to play the CV cycle We remain very constructive on the CV cycle but our preferred play on this theme, Ashok

Leyland, is now already pricing in the best-case scenario; hence, we are downgrading it to

NEUTRAL. We think investors should instead switch to a basket of component names that

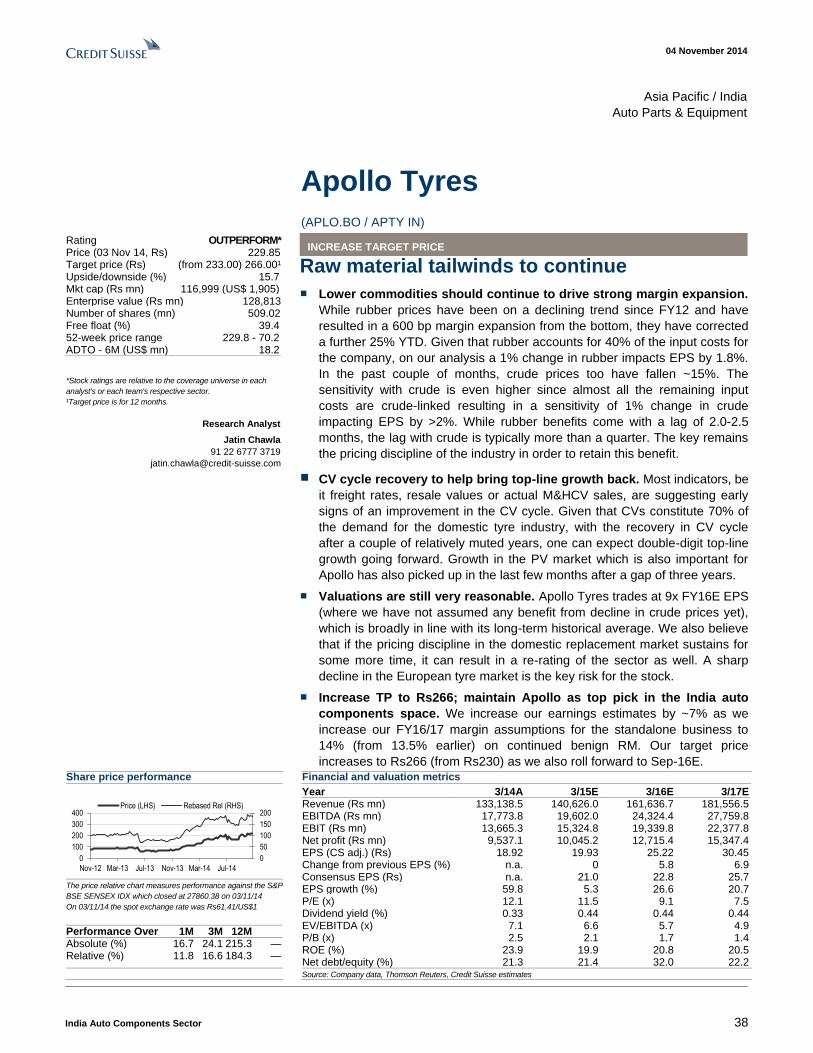

are supplying to the CV industry. We are increasing our target price for Apollo Tyres

(OUTPERFORM) to Rs266 and for Bharat Forge (NEUTRAL) to Rs830. Apollo Tyres

remains our preferred pick in the components space, and we initiate on Wabco as well.

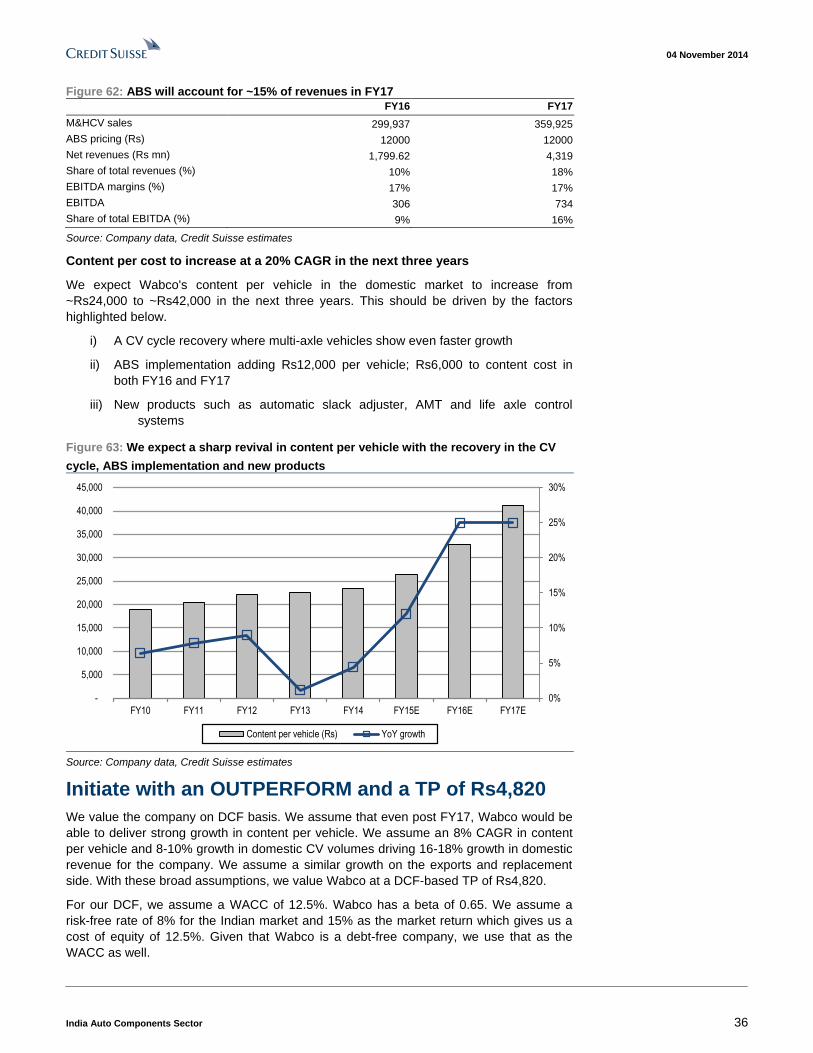

We initiate coverage on Wabco with an OUTPERFORM rating and a TP of Rs4,820:

Wabco is the largest player in the CV braking industry in India with a >80% market share.

We believe Wabco is one of the best structural plays in the Indian auto components space,

with safety and emission content per vehicle in India being a tenth of European markets.

Wabco India also has a prominent position in Wabco's global scheme of things as its hub

for adapting products for emerging markets as well as being a critical country in its plans

to increase sourcing from low-cost countries. CV cycle recovery and mandatory ABS

implementation are near-term triggers for the stock, in our view.

Auto components industry

has grown 500 bp higher

than OEMs…

…structural factors which

will increase the gap

Components industry well

placed for an upcycle

Downgrade Ashok Leyland

to NEUTRAL

Prefer Wabco, Apollo Tyres

to play the CV cycle

04 November 2014

India Auto Components Sector 4

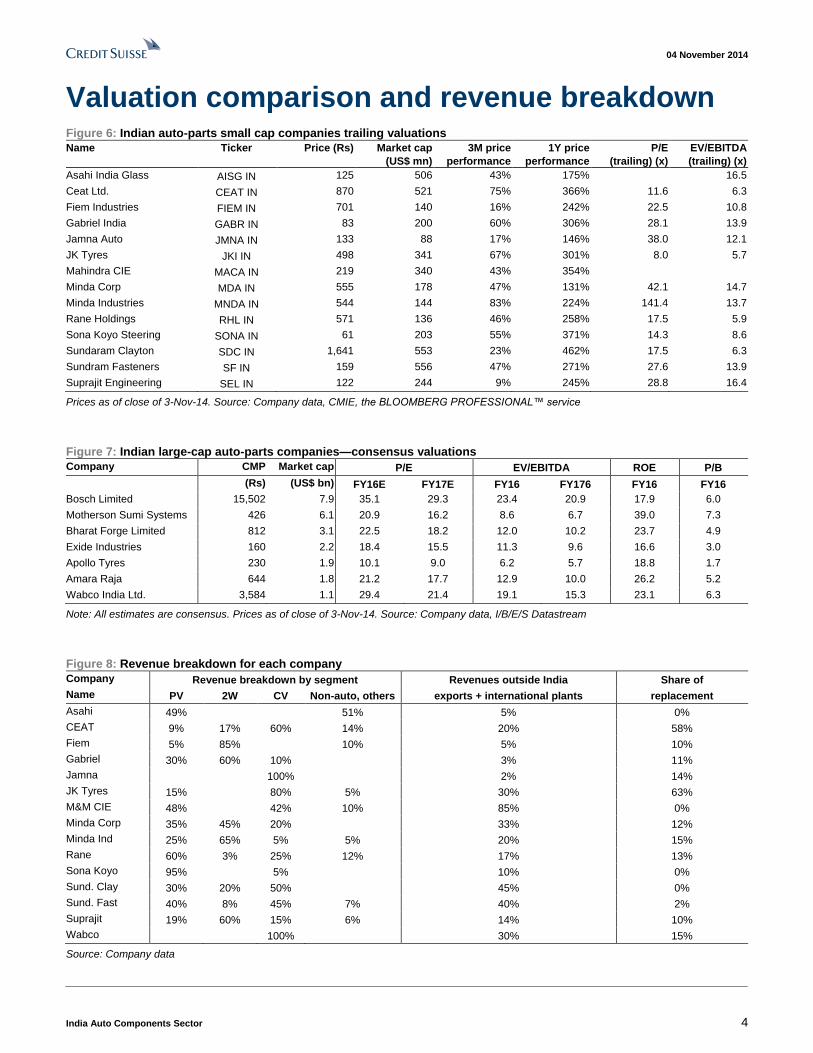

Valuation comparison and revenue breakdown Figure 6: Indian auto-parts small cap companies trailing valuations

Name Ticker Price (Rs) Market cap

(US$ mn)

3M price

performance

1Y price

performance

P/E

(trailing) (x)

EV/EBITDA

(trailing) (x)

Asahi India Glass AISG IN 125 506 43% 175% 16.5

Ceat Ltd. CEAT IN 870 521 75% 366% 11.6 6.3

Fiem Industries FIEM IN 701 140 16% 242% 22.5 10.8

Gabriel India GABR IN 83 200 60% 306% 28.1 13.9

Jamna Auto JMNA IN 133 88 17% 146% 38.0 12.1

JK Tyres JKI IN 498 341 67% 301% 8.0 5.7

Mahindra CIE MACA IN 219 340 43% 354%

Minda Corp MDA IN 555 178 47% 131% 42.1 14.7

Minda Industries MNDA IN 544 144 83% 224% 141.4 13.7

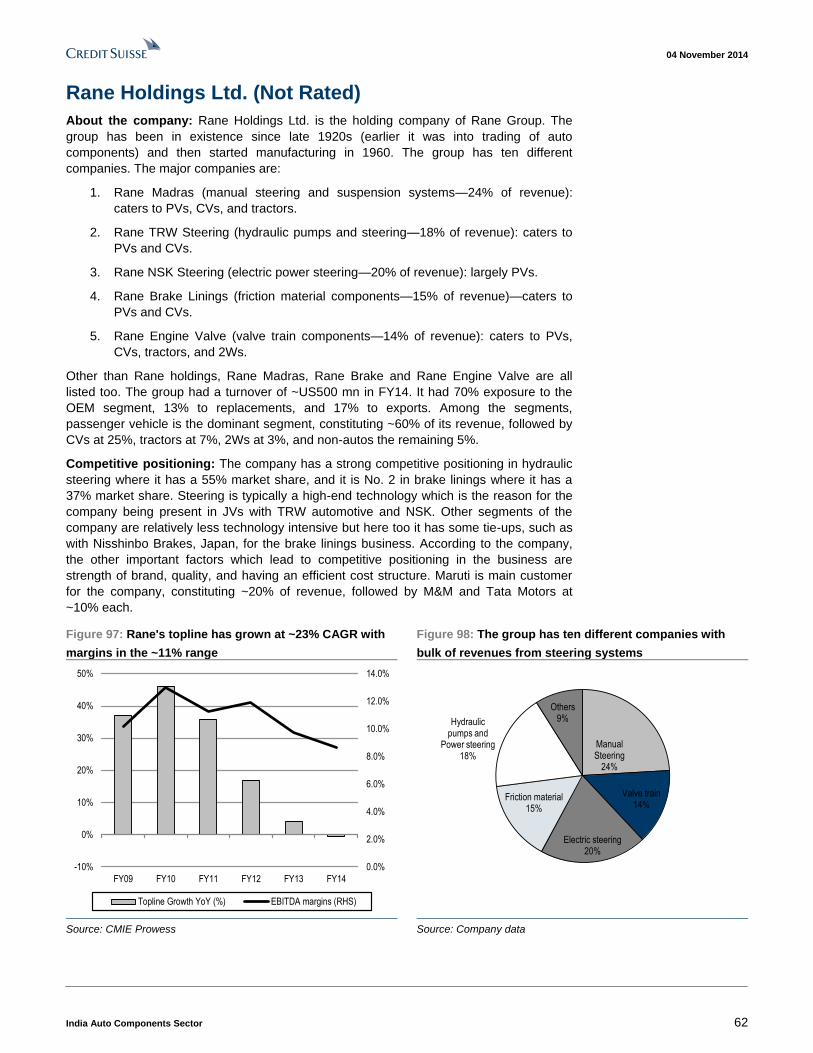

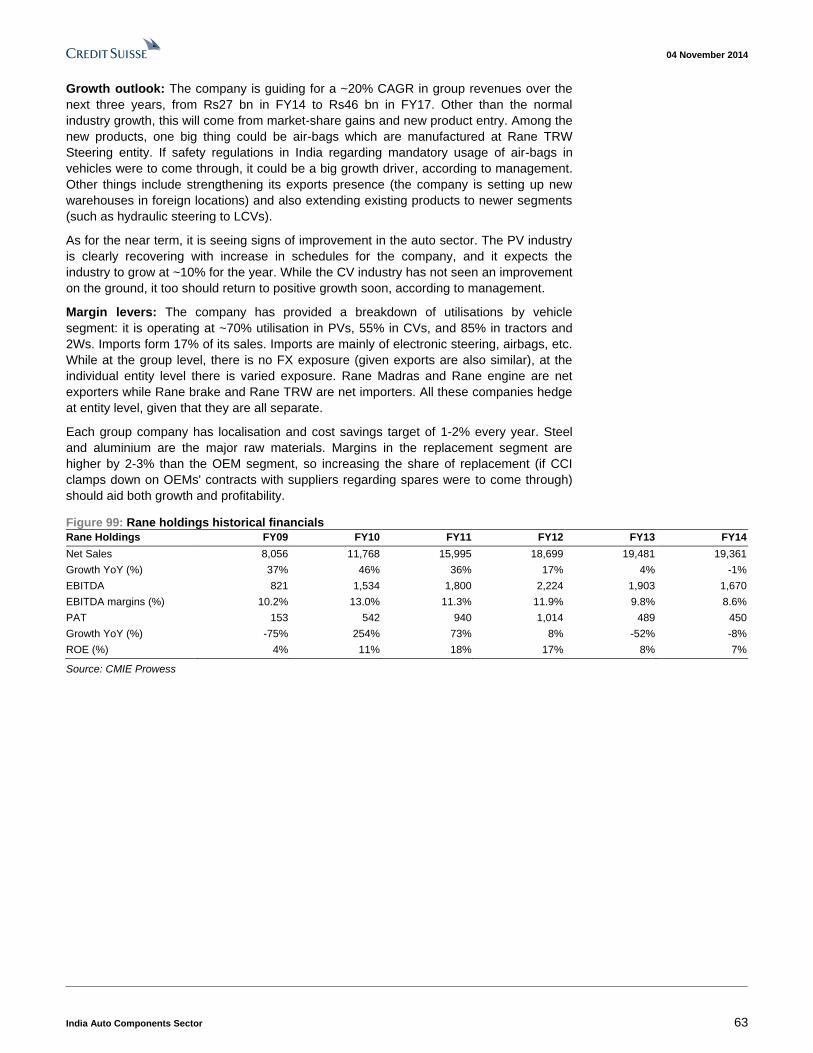

Rane Holdings RHL IN 571 136 46% 258% 17.5 5.9

Sona Koyo Steering SONA IN 61 203 55% 371% 14.3 8.6

Sundaram Clayton SDC IN 1,641 553 23% 462% 17.5 6.3

Sundram Fasteners SF IN 159 556 47% 271% 27.6 13.9

Suprajit Engineering SEL IN 122 244 9% 245% 28.8 16.4

Prices as of close of 3-Nov-14. Source: Company data, CMIE, the BLOOMBERG PROFESSIONAL™ service

Figure 7: Indian large-cap auto-parts companies—consensus valuations

Company CMP Market cap P/E EV/EBITDA ROE P/B

(Rs) (US$ bn) FY16E FY17E FY16 FY176 FY16 FY16

Bosch Limited 15,502 7.9 35.1 29.3 23.4 20.9 17.9 6.0

Motherson Sumi Systems 426 6.1 20.9 16.2 8.6 6.7 39.0 7.3

Bharat Forge Limited 812 3.1 22.5 18.2 12.0 10.2 23.7 4.9

Exide Industries 160 2.2 18.4 15.5 11.3 9.6 16.6 3.0

Apollo Tyres 230 1.9 10.1 9.0 6.2 5.7 18.8 1.7

Amara Raja 644 1.8 21.2 17.7 12.9 10.0 26.2 5.2

Wabco India Ltd. 3,584 1.1 29.4 21.4 19.1 15.3 23.1 6.3

Note: All estimates are consensus. Prices as of close of 3-Nov-14. Source: Company data, I/B/E/S Datastream

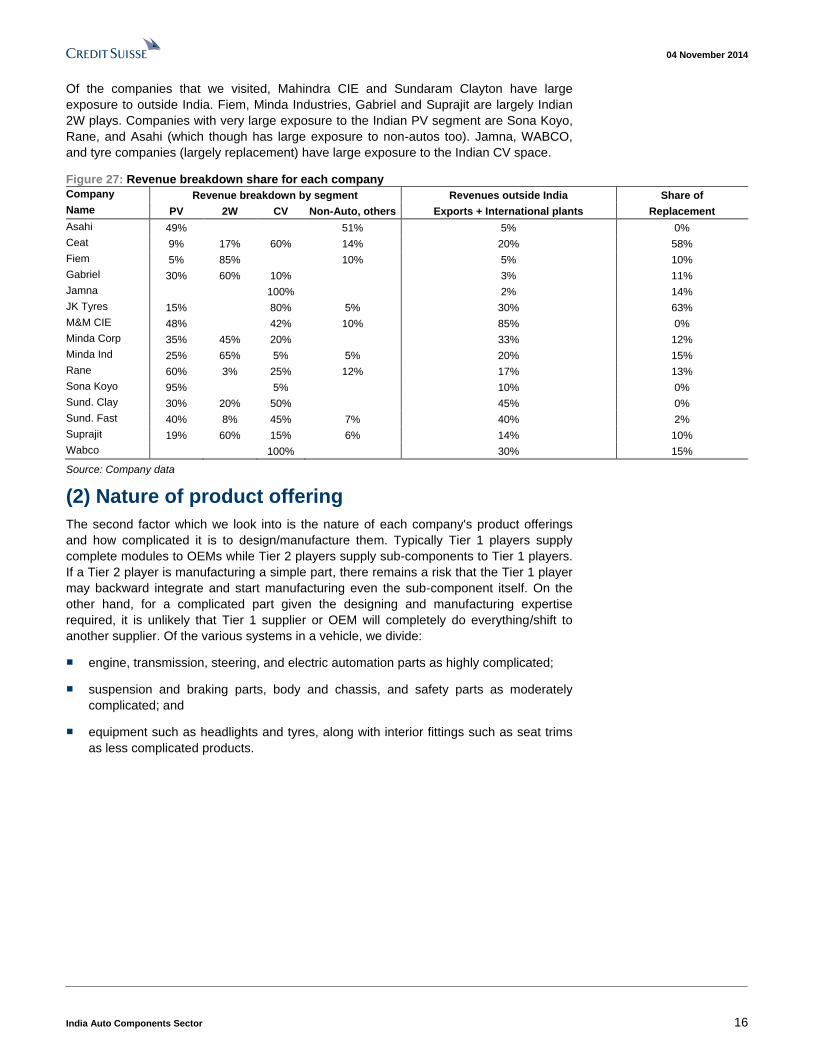

Figure 8: Revenue breakdown for each company

Company Revenue breakdown by segment Revenues outside India Share of

Name PV 2W CV Non-auto, others exports + international plants replacement

Asahi 49% 51% 5% 0%

CEAT 9% 17% 60% 14% 20% 58%

Fiem 5% 85% 10% 5% 10%

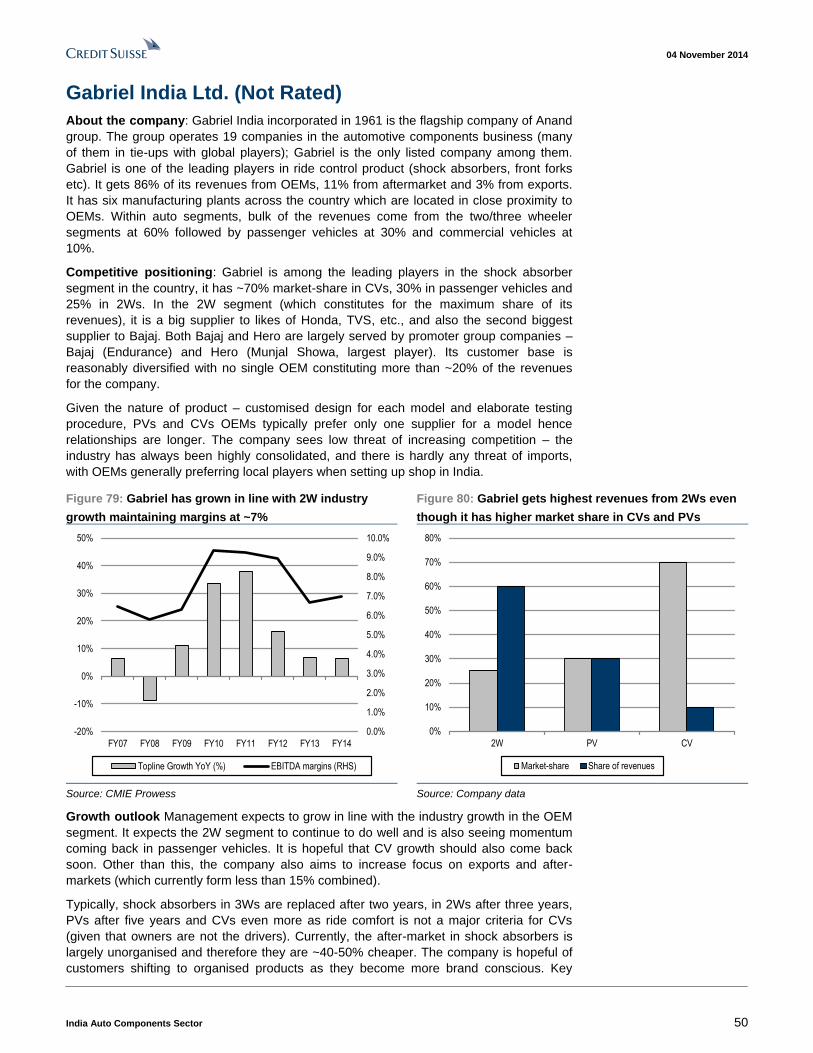

Gabriel 30% 60% 10% 3% 11%

Jamna 100% 2% 14%

JK Tyres 15% 80% 5% 30% 63%

M&M CIE 48% 42% 10% 85% 0%

Minda Corp 35% 45% 20% 33% 12%

Minda Ind 25% 65% 5% 5% 20% 15%

Rane 60% 3% 25% 12% 17% 13%

Sona Koyo 95% 5% 10% 0%

Sund. Clay 30% 20% 50% 45% 0%

Sund. Fast 40% 8% 45% 7% 40% 2%

Suprajit 19% 60% 15% 6% 14% 10%

Wabco 100% 30% 15%

Source: Company data

04 November 2014

India Auto Components Sector 5

Table of contents Geared for growth 6

Auto-parts to continue growing faster than OEMs 6 Auto OEMs entering an upcycle… 10 …parts companies well positioned to capitalise 11

Conversations with small-cap companies 14 Growth outlook improving but a full-blown recovery still some time away 14 Framework to assess auto-component plays 15 (1) Segment exposure 15 (2) Nature of product offering 16 (3) Market-share positioning 17 (4) Customer dependence 18 (5) Potential to outperform from new opportunities 19 (6) Operating leverage lever from utilisation pick-up 19 (7) Other margin levers such as mix, raw materials 20 (8) Higher return ratios and higher asset turns 20 (9) Lower margin volatility 22

A basket of component stocks to play CV cycle 23 CV cycle is recovering… 23 ..but OEM Valuations already reflect that 25 Prefer basket of CV focused auto-component plays 26

Companies 27 Wabco India Ltd. (WABC.BO / WIL IN) 28

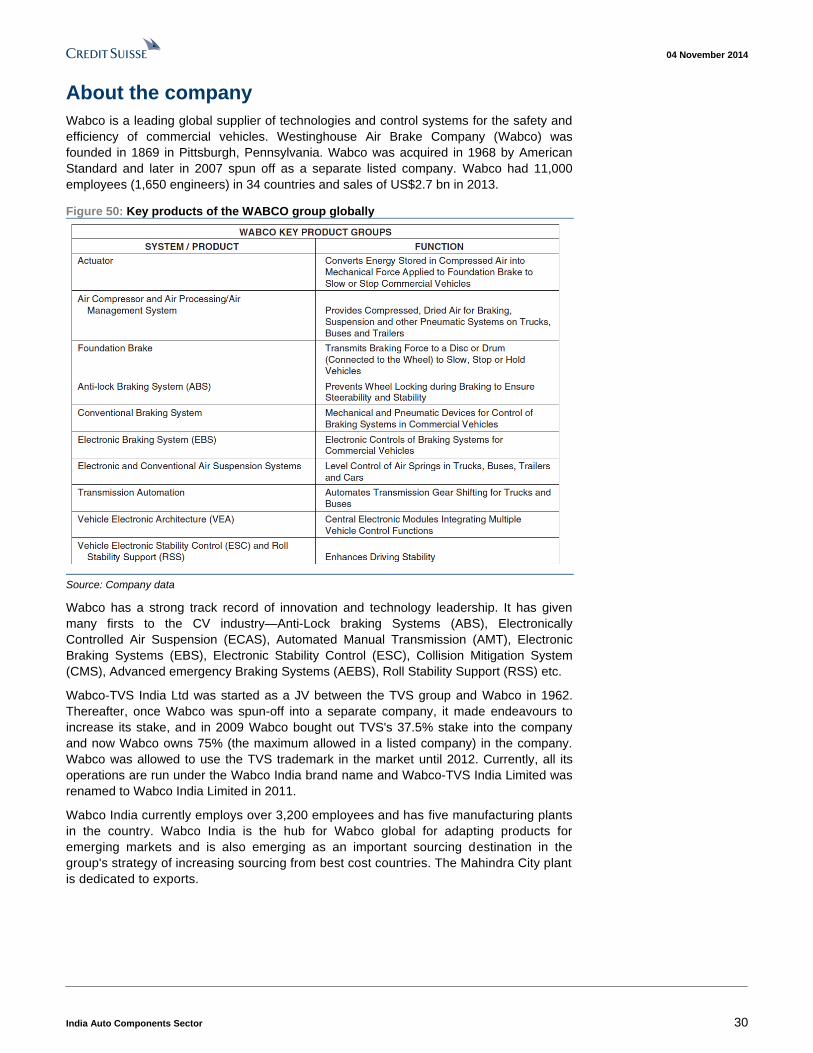

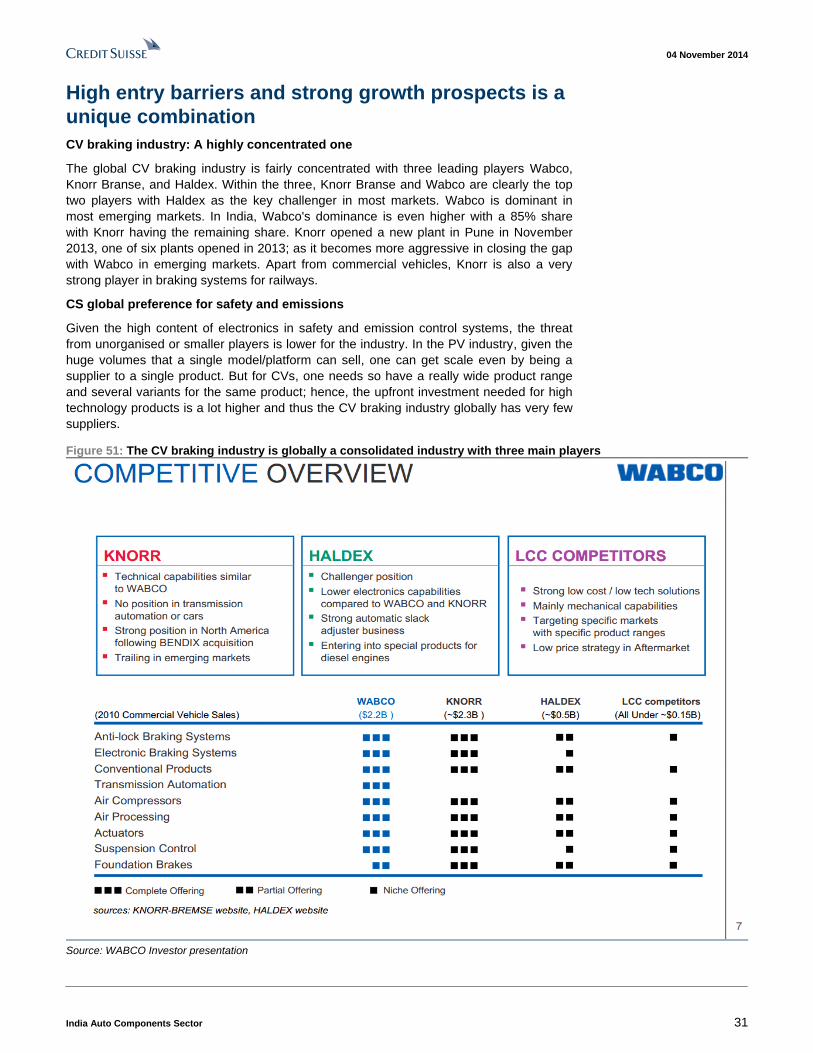

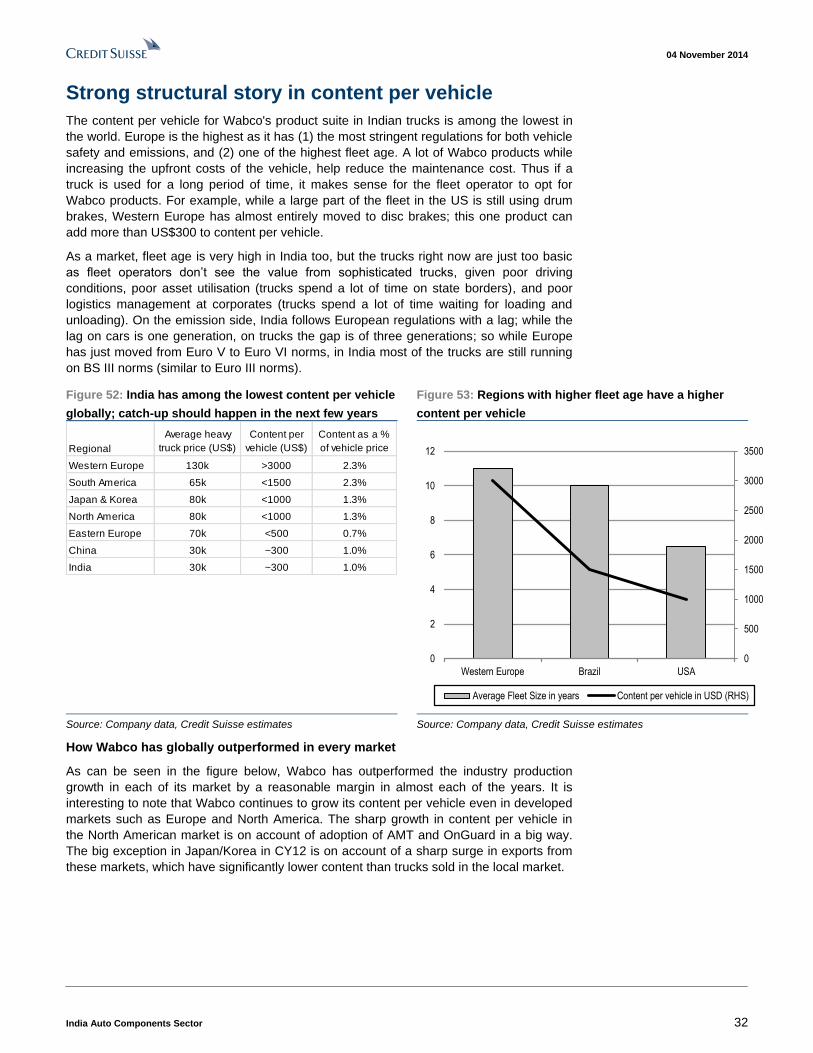

Structural play in a cyclical industry 28 Wabco India Ltd. WABC.BO / WIL IN 29 About the company 30 High entry barriers and strong growth prospects is a unique combination 31 Strong structural story in content per vehicle 32 Initiate with an OUTPERFORM and a TP of Rs4,820 36 Investment risks 37

Apollo Tyres (APLO.BO / APTY IN) 38 Raw material tailwinds to continue 38

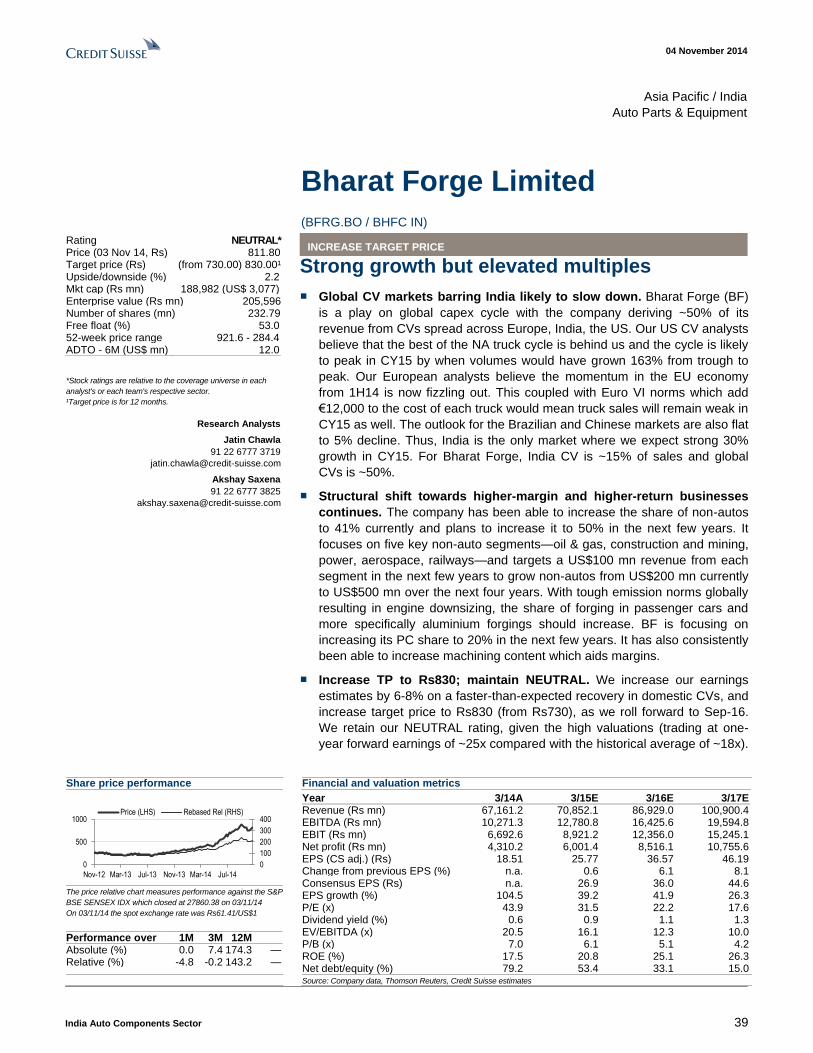

Bharat Forge Limited (BFRG.BO / BHFC IN) 39 Strong growth but elevated multiples 39

Ashok Leyland Ltd (ASOK.BO / AL IN) 40 Strong recovery already priced in 40

Company visit notes 41 Suprajit Engineering (Not Rated) 42 JK Tyres (Not Rated) 44 Jamna Auto (Not Rated) 46 Fiem Industries (Not Rated) 48 Gabriel India Ltd. (Not Rated) 50 Sona Koyo Steering Systems (Not Rated) 52 Minda Corporation Ltd. (Not Rated) 54 CEAT Ltd. (Not Rated) 56 Minda Industries Ltd. (Not Rated) 58 Sundram Fasteners (Not Rated) 60 Rane Holdings Ltd. (Not Rated) 62 Sundaram Clayton (Not Rated) 64 Asahi India Glass (Not Rated) 66 Mahindra CIE (Not Rated) 67

04 November 2014

India Auto Components Sector 6

Geared for growth In the past ten years, top-line CAGR of auto components industry outpaced that of auto

OEMs by >500 bp, and we expect this gap to widen further on: (1) a consolidation of the

industry as OEMs increasingly move towards a single/lesser supplier model—the share of

the top ten players is up >500 bp in the past five years; (2) the rising share of exports as

foreign-based OEMs look to source greater components from India—exports have

increased from US$3.5 bn in FY07 to US$10 bn in FY14; (3) sizeable growth opportunity

in the replacement segment (margins are 300-400 bp higher than the OEM segment) as

consumers up-trade from the unorganised segment; GST implementation could reduce

pricing gap (~40%) between organised and unorganised players and CCI clampdown on

OEMs regarding spares' availability can expand the market; (4) Indian arms of foreign

OEMs increasing localisation in the wake of rising costs in a competitive environment (gap

of almost ~15% between Maruti and other MNCs); and (5) the increasing content per

vehicle, driven by regulation and consumer aspirations.

Our analysis of the consolidated industry financials indicates that the components sector is well

placed to tap into this future growth; utilisation rates remain low (~70%), indicating margin

expansion from operating leverage as the cycle recovers. Despite slowing top-line growth,

components companies manage to improve gross margins, driven by export profitability and

some raw material benefits (which could increase further if commodity prices remain benign).

PAT margins are though only steady because of negative operating leverage.

Auto-parts to continue growing faster than OEMs

Over the past ten years, the top 100 auto-components companies have witnessed a

CAGR of 17% compared with a ~12% CAGR for the auto OEM industry, thus

outperforming the industry by ~500 bp. While doing so these companies have managed to

maintain their profitability, with EBITDA margins remaining stable at 13% and PAT

margins at 5%. In our view, the outperformance of the auto parts industry could increase

further in the next few years on account of the following factors

#1 Industry consolidation

The Indian auto components industry is highly fragmented, consisting of ~500 players in

the organised sector and many more in the unorganised sector. The top 50 companies

contribute 85% to the total revenue. Industry consolidation is a global phenomenon and

the trend is now catching up in India as well. As per a McKinsey report of March 2012, The

share of revenues of top 150 suppliers globally has climbed up from 34% to 45% over the

last decade. In India, the share of the top 10 companies (excluding tyres) has increased by

more than 500 bp in the past five years.

Figure 9: The automotive industry in India is highly

fragmented with over 500 players in the organised sector

Figure 10: Just like globally, India's auto parts industry

consolidating with the share of top players rising

0 50 100 150 200 250 300

Revenue>USD 100 Mn

Between USD 50 Mn and 100Mn

Between USD 25Mn and 50Mn

Between USD 5Mn and 25Mn

Less than USD 5 Mn

Number of auto parts companies split by revenues

44.0%

46.0%

48.0%

50.0%

52.0%

FY10 FY11 FY12 FY13 FY14

Share of revenues of 10 largest companies (excluding Tyre)

Source: Company data, ACMA Note: Aggregate of ~100 auto parts companies. Source: CMIE

04 November 2014

India Auto Components Sector 7

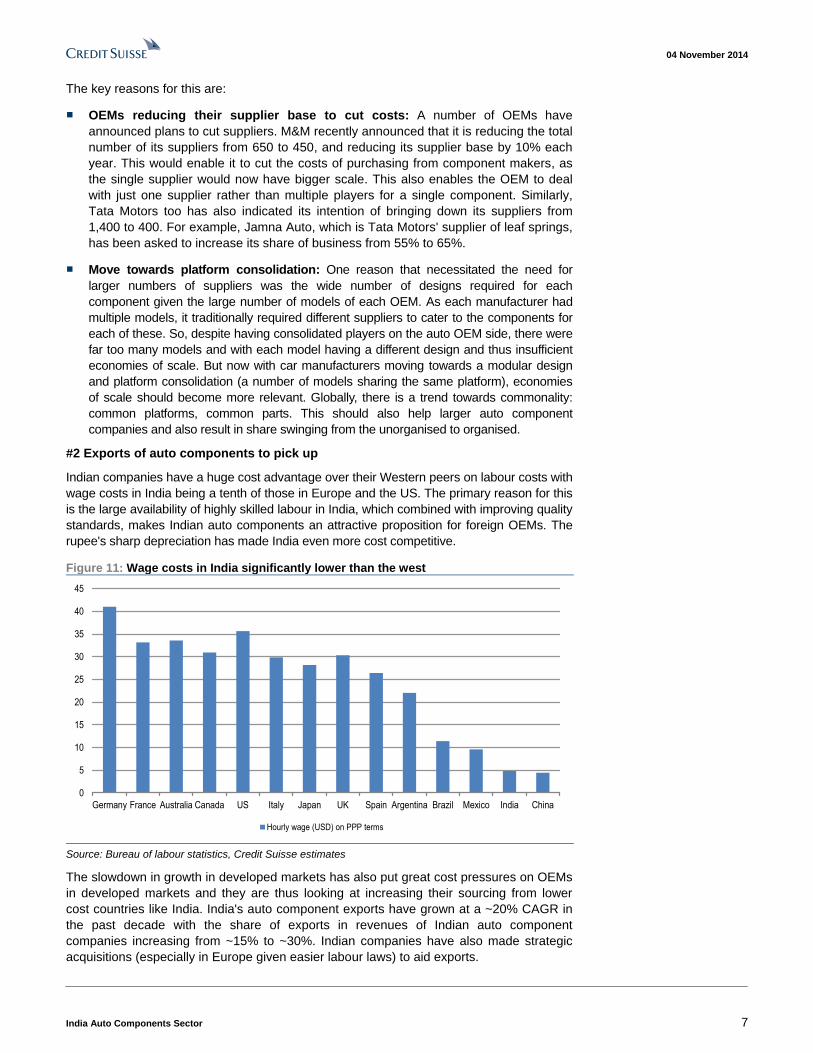

The key reasons for this are:

■ OEMs reducing their supplier base to cut costs: A number of OEMs have

announced plans to cut suppliers. M&M recently announced that it is reducing the total

number of its suppliers from 650 to 450, and reducing its supplier base by 10% each

year. This would enable it to cut the costs of purchasing from component makers, as

the single supplier would now have bigger scale. This also enables the OEM to deal

with just one supplier rather than multiple players for a single component. Similarly,

Tata Motors too has also indicated its intention of bringing down its suppliers from

1,400 to 400. For example, Jamna Auto, which is Tata Motors' supplier of leaf springs,

has been asked to increase its share of business from 55% to 65%.

■ Move towards platform consolidation: One reason that necessitated the need for

larger numbers of suppliers was the wide number of designs required for each

component given the large number of models of each OEM. As each manufacturer had

multiple models, it traditionally required different suppliers to cater to the components for

each of these. So, despite having consolidated players on the auto OEM side, there were

far too many models and with each model having a different design and thus insufficient

economies of scale. But now with car manufacturers moving towards a modular design

and platform consolidation (a number of models sharing the same platform), economies

of scale should become more relevant. Globally, there is a trend towards commonality:

common platforms, common parts. This should also help larger auto component

companies and also result in share swinging from the unorganised to organised.

#2 Exports of auto components to pick up

Indian companies have a huge cost advantage over their Western peers on labour costs with

wage costs in India being a tenth of those in Europe and the US. The primary reason for this

is the large availability of highly skilled labour in India, which combined with improving quality

standards, makes Indian auto components an attractive proposition for foreign OEMs. The

rupee's sharp depreciation has made India even more cost competitive.

Figure 11: Wage costs in India significantly lower than the west

0

5

10

15

20

25

30

35

40

45

Germany France Australia Canada US Italy Japan UK Spain Argentina Brazil Mexico India China

Hourly wage (USD) on PPP terms

Source: Bureau of labour statistics, Credit Suisse estimates

The slowdown in growth in developed markets has also put great cost pressures on OEMs

in developed markets and they are thus looking at increasing their sourcing from lower

cost countries like India. India's auto component exports have grown at a ~20% CAGR in

the past decade with the share of exports in revenues of Indian auto component

companies increasing from ~15% to ~30%. Indian companies have also made strategic

acquisitions (especially in Europe given easier labour laws) to aid exports.

04 November 2014

India Auto Components Sector 8

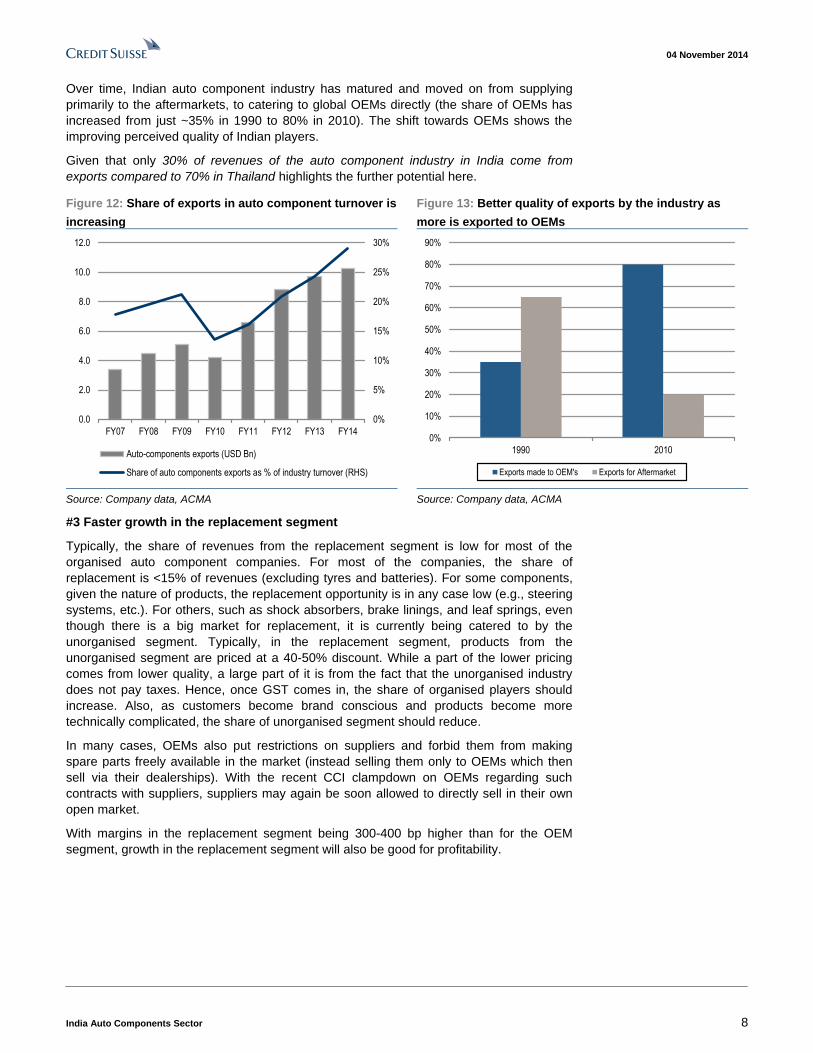

Over time, Indian auto component industry has matured and moved on from supplying

primarily to the aftermarkets, to catering to global OEMs directly (the share of OEMs has

increased from just ~35% in 1990 to 80% in 2010). The shift towards OEMs shows the

improving perceived quality of Indian players.

Given that only 30% of revenues of the auto component industry in India come from

exports compared to 70% in Thailand highlights the further potential here.

Figure 12: Share of exports in auto component turnover is

increasing

Figure 13: Better quality of exports by the industry as

more is exported to OEMs

0%

5%

10%

15%

20%

25%

30%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Auto-components exports (USD Bn)

Share of auto components exports as % of industry turnover (RHS)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1990 2010

Exports made to OEM's Exports for Aftermarket

Source: Company data, ACMA Source: Company data, ACMA

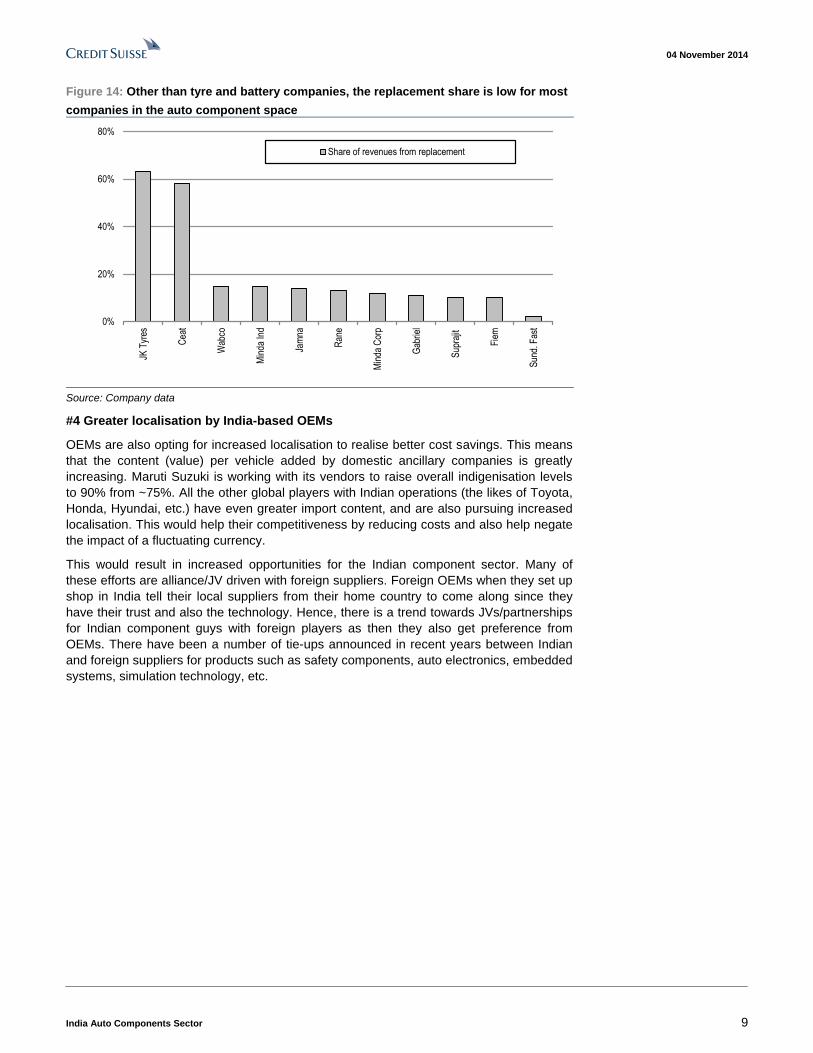

#3 Faster growth in the replacement segment

Typically, the share of revenues from the replacement segment is low for most of the

organised auto component companies. For most of the companies, the share of

replacement is <15% of revenues (excluding tyres and batteries). For some components,

given the nature of products, the replacement opportunity is in any case low (e.g., steering

systems, etc.). For others, such as shock absorbers, brake linings, and leaf springs, even

though there is a big market for replacement, it is currently being catered to by the

unorganised segment. Typically, in the replacement segment, products from the

unorganised segment are priced at a 40-50% discount. While a part of the lower pricing

comes from lower quality, a large part of it is from the fact that the unorganised industry

does not pay taxes. Hence, once GST comes in, the share of organised players should

increase. Also, as customers become brand conscious and products become more

technically complicated, the share of unorganised segment should reduce.

In many cases, OEMs also put restrictions on suppliers and forbid them from making

spare parts freely available in the market (instead selling them only to OEMs which then

sell via their dealerships). With the recent CCI clampdown on OEMs regarding such

contracts with suppliers, suppliers may again be soon allowed to directly sell in their own

open market.

With margins in the replacement segment being 300-400 bp higher than for the OEM

segment, growth in the replacement segment will also be good for profitability.

04 November 2014

India Auto Components Sector 9

Figure 14: Other than tyre and battery companies, the replacement share is low for most

companies in the auto component space

0%

20%

40%

60%

80%JK

Tyr

es

Cea

t

Wab

co

Min

da In

d

Jam

na

Ran

e

Min

da C

orp

Gab

riel

Sup

rajit

Fie

m

Sun

d. F

ast

Share of revenues from replacement

Source: Company data

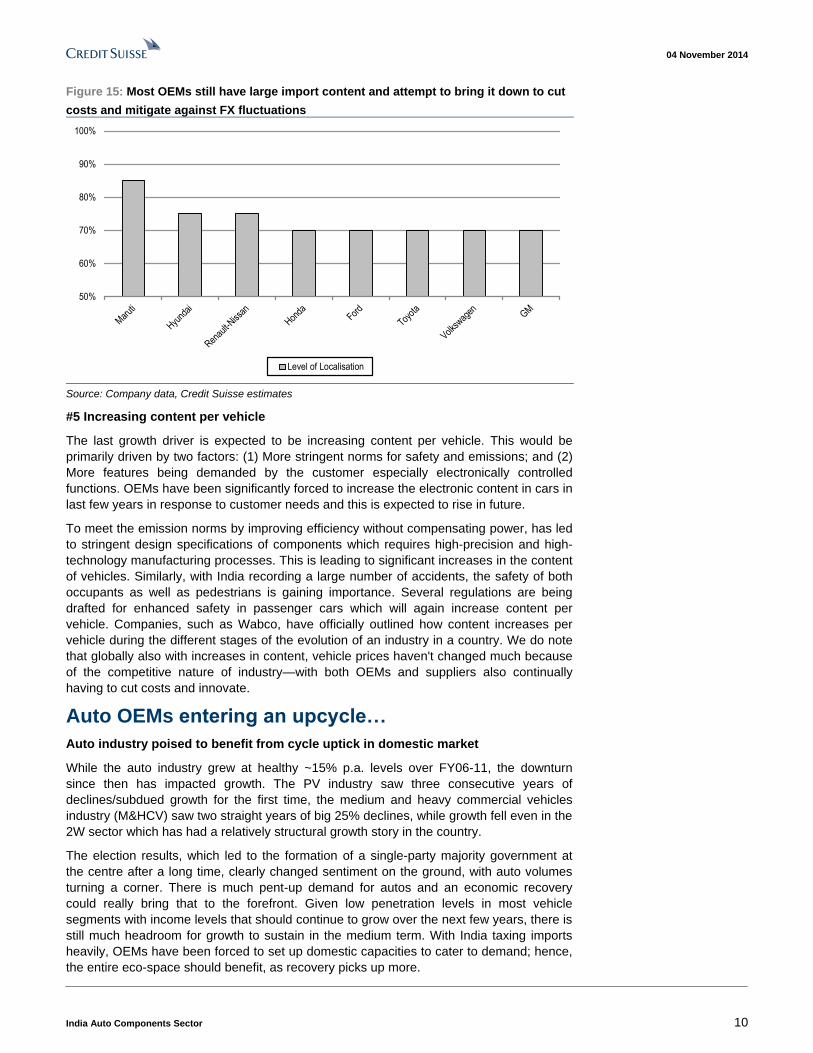

#4 Greater localisation by India-based OEMs

OEMs are also opting for increased localisation to realise better cost savings. This means

that the content (value) per vehicle added by domestic ancillary companies is greatly

increasing. Maruti Suzuki is working with its vendors to raise overall indigenisation levels

to 90% from ~75%. All the other global players with Indian operations (the likes of Toyota,

Honda, Hyundai, etc.) have even greater import content, and are also pursuing increased

localisation. This would help their competitiveness by reducing costs and also help negate

the impact of a fluctuating currency.

This would result in increased opportunities for the Indian component sector. Many of

these efforts are alliance/JV driven with foreign suppliers. Foreign OEMs when they set up

shop in India tell their local suppliers from their home country to come along since they

have their trust and also the technology. Hence, there is a trend towards JVs/partnerships

for Indian component guys with foreign players as then they also get preference from

OEMs. There have been a number of tie-ups announced in recent years between Indian

and foreign suppliers for products such as safety components, auto electronics, embedded

systems, simulation technology, etc.

04 November 2014

India Auto Components Sector 10

Figure 15: Most OEMs still have large import content and attempt to bring it down to cut

costs and mitigate against FX fluctuations

50%

60%

70%

80%

90%

100%

Level of Localisation

Source: Company data, Credit Suisse estimates

#5 Increasing content per vehicle

The last growth driver is expected to be increasing content per vehicle. This would be

primarily driven by two factors: (1) More stringent norms for safety and emissions; and (2)

More features being demanded by the customer especially electronically controlled

functions. OEMs have been significantly forced to increase the electronic content in cars in

last few years in response to customer needs and this is expected to rise in future.

To meet the emission norms by improving efficiency without compensating power, has led

to stringent design specifications of components which requires high-precision and high-

technology manufacturing processes. This is leading to significant increases in the content

of vehicles. Similarly, with India recording a large number of accidents, the safety of both

occupants as well as pedestrians is gaining importance. Several regulations are being

drafted for enhanced safety in passenger cars which will again increase content per

vehicle. Companies, such as Wabco, have officially outlined how content increases per

vehicle during the different stages of the evolution of an industry in a country. We do note

that globally also with increases in content, vehicle prices haven't changed much because

of the competitive nature of industry—with both OEMs and suppliers also continually

having to cut costs and innovate.

Auto OEMs entering an upcycle…

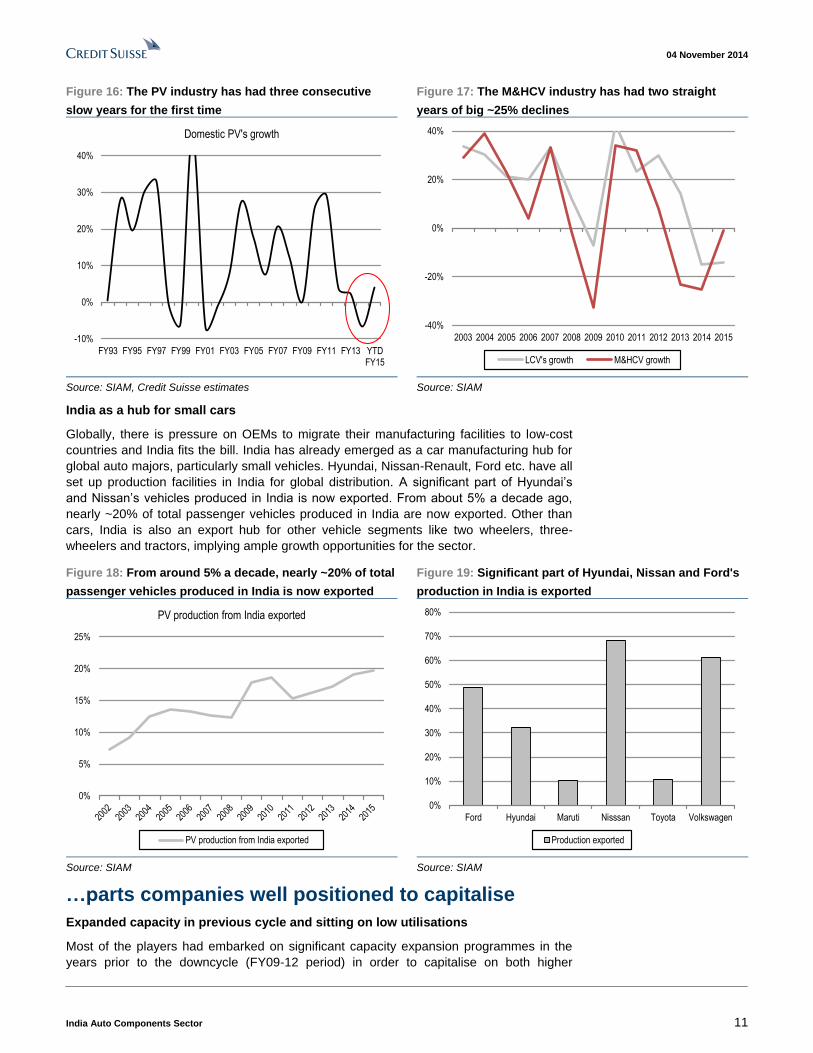

Auto industry poised to benefit from cycle uptick in domestic market

While the auto industry grew at healthy ~15% p.a. levels over FY06-11, the downturn

since then has impacted growth. The PV industry saw three consecutive years of

declines/subdued growth for the first time, the medium and heavy commercial vehicles

industry (M&HCV) saw two straight years of big 25% declines, while growth fell even in the

2W sector which has had a relatively structural growth story in the country.

The election results, which led to the formation of a single-party majority government at

the centre after a long time, clearly changed sentiment on the ground, with auto volumes

turning a corner. There is much pent-up demand for autos and an economic recovery

could really bring that to the forefront. Given low penetration levels in most vehicle

segments with income levels that should continue to grow over the next few years, there is

still much headroom for growth to sustain in the medium term. With India taxing imports

heavily, OEMs have been forced to set up domestic capacities to cater to demand; hence,

the entire eco-space should benefit, as recovery picks up more.

04 November 2014

India Auto Components Sector 11

Figure 16: The PV industry has had three consecutive

slow years for the first time

Figure 17: The M&HCV industry has had two straight

years of big ~25% declines

-10%

0%

10%

20%

30%

40%

FY93 FY95 FY97 FY99 FY01 FY03 FY05 FY07 FY09 FY11 FY13 YTDFY15

Domestic PV's growth

-40%

-20%

0%

20%

40%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

LCV's growth M&HCV growth

Source: SIAM, Credit Suisse estimates Source: SIAM

India as a hub for small cars

Globally, there is pressure on OEMs to migrate their manufacturing facilities to low-cost

countries and India fits the bill. India has already emerged as a car manufacturing hub for

global auto majors, particularly small vehicles. Hyundai, Nissan-Renault, Ford etc. have all

set up production facilities in India for global distribution. A significant part of Hyundai’s

and Nissan’s vehicles produced in India is now exported. From about 5% a decade ago,

nearly ~20% of total passenger vehicles produced in India are now exported. Other than

cars, India is also an export hub for other vehicle segments like two wheelers, three-

wheelers and tractors, implying ample growth opportunities for the sector.

Figure 18: From around 5% a decade, nearly ~20% of total

passenger vehicles produced in India is now exported

Figure 19: Significant part of Hyundai, Nissan and Ford's

production in India is exported

0%

5%

10%

15%

20%

25%

PV production from India exported

PV production from India exported

0%

10%

20%

30%

40%

50%

60%

70%

80%

Ford Hyundai Maruti Nisssan Toyota Volkswagen

Production exported

Source: SIAM Source: SIAM

…parts companies well positioned to capitalise

Expanded capacity in previous cycle and sitting on low utilisations

Most of the players had embarked on significant capacity expansion programmes in the

years prior to the downcycle (FY09-12 period) in order to capitalise on both higher

04 November 2014

India Auto Components Sector 12

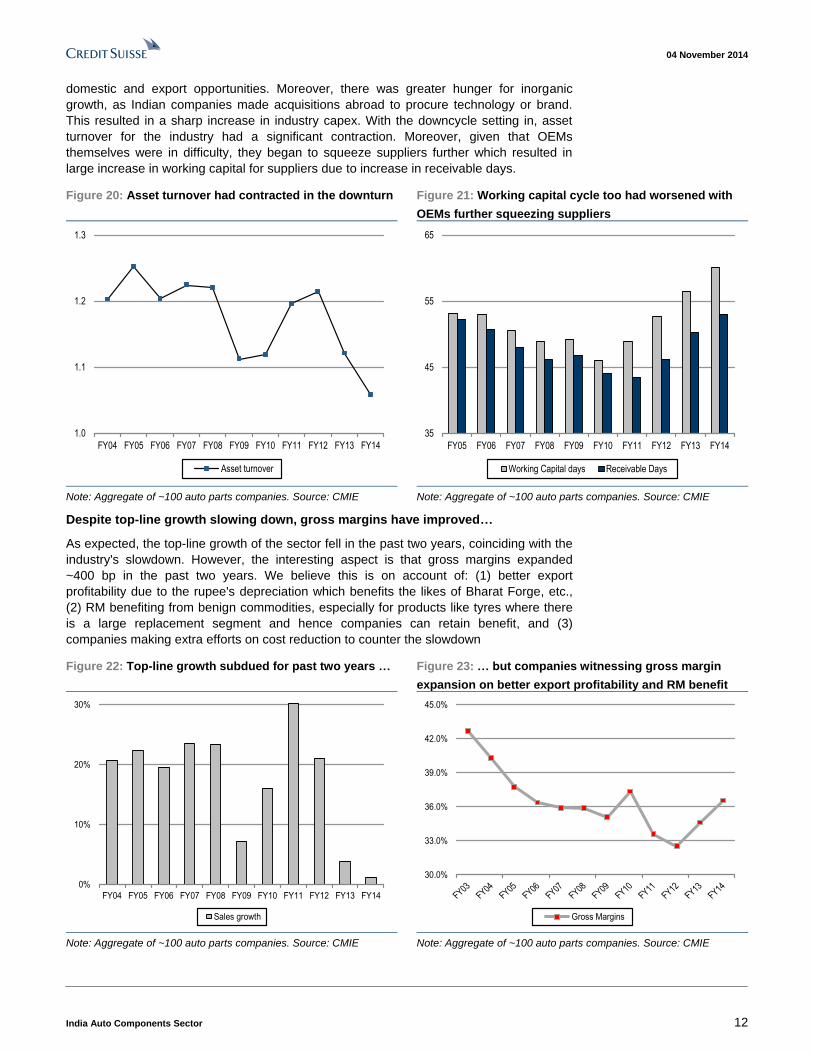

domestic and export opportunities. Moreover, there was greater hunger for inorganic

growth, as Indian companies made acquisitions abroad to procure technology or brand.

This resulted in a sharp increase in industry capex. With the downcycle setting in, asset

turnover for the industry had a significant contraction. Moreover, given that OEMs

themselves were in difficulty, they began to squeeze suppliers further which resulted in

large increase in working capital for suppliers due to increase in receivable days.

Figure 20: Asset turnover had contracted in the downturn Figure 21: Working capital cycle too had worsened with

OEMs further squeezing suppliers

1.0

1.1

1.2

1.3

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Asset turnover

35

45

55

65

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Working Capital days Receivable Days

Note: Aggregate of ~100 auto parts companies. Source: CMIE Note: Aggregate of ~100 auto parts companies. Source: CMIE

Despite top-line growth slowing down, gross margins have improved…

As expected, the top-line growth of the sector fell in the past two years, coinciding with the

industry's slowdown. However, the interesting aspect is that gross margins expanded

~400 bp in the past two years. We believe this is on account of: (1) better export

profitability due to the rupee's depreciation which benefits the likes of Bharat Forge, etc.,

(2) RM benefiting from benign commodities, especially for products like tyres where there

is a large replacement segment and hence companies can retain benefit, and (3)

companies making extra efforts on cost reduction to counter the slowdown

Figure 22: Top-line growth subdued for past two years … Figure 23: … but companies witnessing gross margin

expansion on better export profitability and RM benefit

0%

10%

20%

30%

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Sales growth

30.0%

33.0%

36.0%

39.0%

42.0%

45.0%

Gross Margins

Note: Aggregate of ~100 auto parts companies. Source: CMIE Note: Aggregate of ~100 auto parts companies. Source: CMIE

04 November 2014

India Auto Components Sector 13

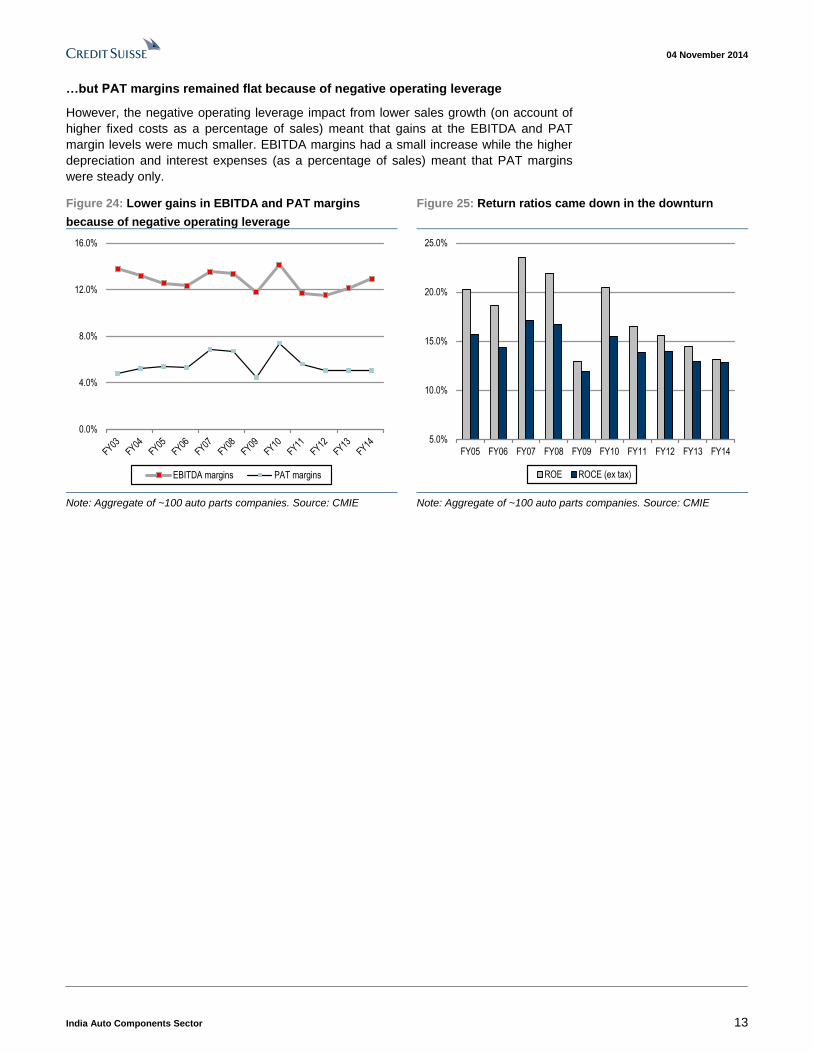

…but PAT margins remained flat because of negative operating leverage

However, the negative operating leverage impact from lower sales growth (on account of

higher fixed costs as a percentage of sales) meant that gains at the EBITDA and PAT

margin levels were much smaller. EBITDA margins had a small increase while the higher

depreciation and interest expenses (as a percentage of sales) meant that PAT margins

were steady only.

Figure 24: Lower gains in EBITDA and PAT margins

because of negative operating leverage

Figure 25: Return ratios came down in the downturn

0.0%

4.0%

8.0%

12.0%

16.0%

EBITDA margins PAT margins

5.0%

10.0%

15.0%

20.0%

25.0%

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

ROE ROCE (ex tax)

Note: Aggregate of ~100 auto parts companies. Source: CMIE Note: Aggregate of ~100 auto parts companies. Source: CMIE

04 November 2014

India Auto Components Sector 14

Conversations with small-cap companies We met managements of 15 small-cap Indian auto component companies (US$100-500

mn market cap) over the past month (short write-ups on each company are provided later).

Our discussions indicate that demand is improving with suppliers across segments seeing

improving growth outlook but they are still not outright bullish.

We believe the auto component sector can be assessed on the following parameters:

On growth parameters, we like companies having: (1) larger exposure to the India OEM

space (particularly PV and CV), (2) product offerings with a technological edge, (3)

dominant market share positioning in key segments with entry barriers, (4) a diversified

customer base with low exposure to a single customer, and (5) potential to outperform

market growth from untapped opportunities such as new product, and new segment.

On margin lever parameters, we like the companies which can improve margins in the

near term on: (1) operating leverage benefit from an uptick in utilisation as growth returns

and (2) other margin levers such as movement towards a better mix, and benign raw

material prices. On financial parameters, we like companies which have: (1) high return

ratios and higher asset turns, and (2) low margin volatility across cycles, denoting stable

model and high pricing power.

Growth outlook improving but a full-blown recovery

still some time away

The Indian OEM industry has had a tough time of late with consecutive years of decline/

subdued industry growth across segments. In the past few months, especially after

elections results there have been signs of growth returning, though the festival season has

again been lukewarm. Our discussions with suppliers across segments indicate that they

are seeing positive growth momentum. They expect the gradual trend in growth

acceleration to sustain as they are clearly seeing uptick in schedules from OEMs.

The two-wheeler (2W) industry had recovered the first (and was anyways not much

impacted in the slowdown). Suppliers expect 10-15% growth in the near term for the 2W

industry and 10% in the long term. On the passenger vehicles side, they are expecting the

industry to grow at ~10% for the year and at ~15% in the long term given the large

headroom for growth. The CV segment should also continue on its positive growth

momentum with the extremely favourable base, though there has been little on the ground

improvement.

Figure 26: Suppliers across segments looking at growth uptick in the Indian OEM space

Company Comments on FY15/ short-term OEM industry growth

CEAT Ltd. Growth pick-up observed in all OEM segments, replacement has not yet recovered but should follow suit.

Fiem Industries Both 2W and 4W industry to grow at 10-12% in medium term

Gabriel India 2W segment to continue to do well, momentum coming back in PVs and CVs should recover soon.

Jamna Auto 8% CV industry growth in FY15.

JK Tyres Small growth in CV OEM in FY15 followed by 25% n FY16, 12% growth in FY15 in PV OEM, replacement to also

recover to ~10% from low single digit.

Mahindra CIE In near term: India PV market to grow at 10%, European PV in mid-single digits and small decline in Europe CVs.

Minda Corp In near term: 2W to grow at 15-20%, PVs at 10-15% and CVs too should start growing now.

Rane Holdings PV industry to grow at 10% in FY15, CV industry to return to positive growth soon.

Sona Koyo Steering PV industry recovery has surprised them and it may grow in double digits now.

Sundaram Clayton Positive growth momentum for India OEMs, slight downward trend in European CVs.

Sundram Fasteners Signs of recovery in the CV industry.

Suprajit Engineering Both 2W and 4W industries to grow at >10% hereon

Source: Company data

04 November 2014

India Auto Components Sector 15

Framework to assess auto-component plays

The Indian auto components sector is highly fragmented with nearly ~500 companies in

the organised sector. Barring select companies such as Bosch, Motherson Sumi, Bharat

Forge, all the other companies have market capitalisation that is less than US$500 mn.

Consequently, most of these companies have limited coverage and are not on investors'

radar. We provide a framework on possible ways to evaluate companies in our coverage

of the auto component sector, and also profiles of the 15 companies we had visited on

each of these factors based on the historical data. We believe auto component companies

should be assessed on the following growth parameters, margin levers parameters and

return ratios parameters.

Growth parameters: The factors which we consider here determine the top-line growth

opportunities of a company: these are potential of segments where a company is present,

core competitive advantages that will ensure a sustainable market share, possibility to

exploit untapped opportunities. We use the following five parameters to measure this:

1. Larger exposure to the Indian OEM space, particularly PV and CV.

2. Complicated product offering with technological edge.

3. Dominant market-share positioning in key segments with entry barriers.

4. Diversified customer base with low exposure to a single customer.

5. Poised to outperform the market either by entering into new segments/new

geographies or by introducing new products.

Margin lever parameters: The parameters which we consider here determine the trend in

profitability for the company and which have levers to expand margins in the near term:

6. Operating leverage benefit from pickup in capacity utilisation.

7. Other levers such as shift towards better mix, benign raw material prices etc.

Financial parameters: The parameters determine the free cash flow generation ability,

stability of business model and resilience in down-cycles and free cash. We use the

following parameters to measure this

8. Higher return ratios and asset turns.

9. Low margin volatility across cycles denoting stable model and high pricing power.

Below we explain why each of these parameters is important and also provide profiling of

the companies we had visited.

(1) Segment exposure The first factor which we look into is the segment exposure of the company. The Indian

auto industry has lot of structural drivers which will come to the fore as income levels rise

and customers' purchasing power increase. Vehicle penetration in the country still

significantly lags that of other countries—both developed and even emerging markets

such as Brazil, China, and South-East Asia. Hence, we expect companies which have

greater exposure to India's OEM sector to enjoy faster market growth.

Within the Indian OEM space, we expect PVs and CVs to grow faster over the longer run.

The gap in 2W penetration in the country (with respect to other countries) is smaller than

that for cars. Hence, India may reach the maturity stage in 2Ws by as early as 2020,

whereas on the cars front there is still a long way to go. Moreover, PV and CV growth was

impacted much more in the downturn as compared with the 2Ws; so even near-term

growth should be higher in PVs and CVs. Hence, we prefer companies which have greater

exposure to Indian PV and CV segments.

04 November 2014

India Auto Components Sector 16

Of the companies that we visited, Mahindra CIE and Sundaram Clayton have large

exposure to outside India. Fiem, Minda Industries, Gabriel and Suprajit are largely Indian

2W plays. Companies with very large exposure to the Indian PV segment are Sona Koyo,

Rane, and Asahi (which though has large exposure to non-autos too). Jamna, WABCO,

and tyre companies (largely replacement) have large exposure to the Indian CV space.

Figure 27: Revenue breakdown share for each company

Company Revenue breakdown by segment Revenues outside India Share of

Name PV 2W CV Non-Auto, others Exports + International plants Replacement

Asahi 49% 51% 5% 0%

Ceat 9% 17% 60% 14% 20% 58%

Fiem 5% 85% 10% 5% 10%

Gabriel 30% 60% 10% 3% 11%

Jamna 100% 2% 14%

JK Tyres 15% 80% 5% 30% 63%

M&M CIE 48% 42% 10% 85% 0%

Minda Corp 35% 45% 20% 33% 12%

Minda Ind 25% 65% 5% 5% 20% 15%

Rane 60% 3% 25% 12% 17% 13%

Sona Koyo 95% 5% 10% 0%

Sund. Clay 30% 20% 50% 45% 0%

Sund. Fast 40% 8% 45% 7% 40% 2%

Suprajit 19% 60% 15% 6% 14% 10%

Wabco 100% 30% 15%

Source: Company data

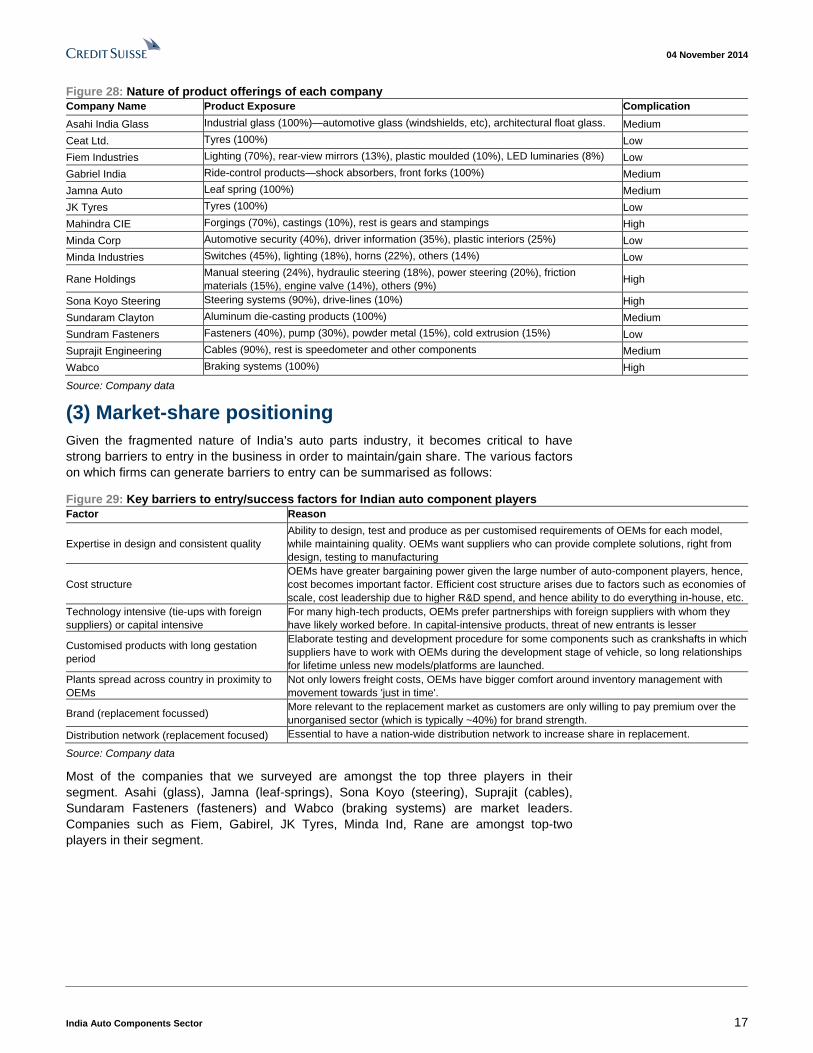

(2) Nature of product offering

The second factor which we look into is the nature of each company's product offerings

and how complicated it is to design/manufacture them. Typically Tier 1 players supply

complete modules to OEMs while Tier 2 players supply sub-components to Tier 1 players.

If a Tier 2 player is manufacturing a simple part, there remains a risk that the Tier 1 player

may backward integrate and start manufacturing even the sub-component itself. On the

other hand, for a complicated part given the designing and manufacturing expertise

required, it is unlikely that Tier 1 supplier or OEM will completely do everything/shift to

another supplier. Of the various systems in a vehicle, we divide:

■ engine, transmission, steering, and electric automation parts as highly complicated;

■ suspension and braking parts, body and chassis, and safety parts as moderately

complicated; and

■ equipment such as headlights and tyres, along with interior fittings such as seat trims

as less complicated products.

04 November 2014

India Auto Components Sector 17

Figure 28: Nature of product offerings of each company

Company Name Product Exposure Complication

Asahi India Glass Industrial glass (100%)—automotive glass (windshields, etc), architectural float glass. Medium

Ceat Ltd. Tyres (100%) Low

Fiem Industries Lighting (70%), rear-view mirrors (13%), plastic moulded (10%), LED luminaries (8%) Low

Gabriel India Ride-control products—shock absorbers, front forks (100%) Medium

Jamna Auto Leaf spring (100%) Medium

JK Tyres Tyres (100%) Low

Mahindra CIE Forgings (70%), castings (10%), rest is gears and stampings High

Minda Corp Automotive security (40%), driver information (35%), plastic interiors (25%) Low

Minda Industries Switches (45%), lighting (18%), horns (22%), others (14%) Low

Rane Holdings Manual steering (24%), hydraulic steering (18%), power steering (20%), friction

materials (15%), engine valve (14%), others (9%) High

Sona Koyo Steering Steering systems (90%), drive-lines (10%) High

Sundaram Clayton Aluminum die-casting products (100%) Medium

Sundram Fasteners Fasteners (40%), pump (30%), powder metal (15%), cold extrusion (15%) Low

Suprajit Engineering Cables (90%), rest is speedometer and other components Medium

Wabco Braking systems (100%) High

Source: Company data

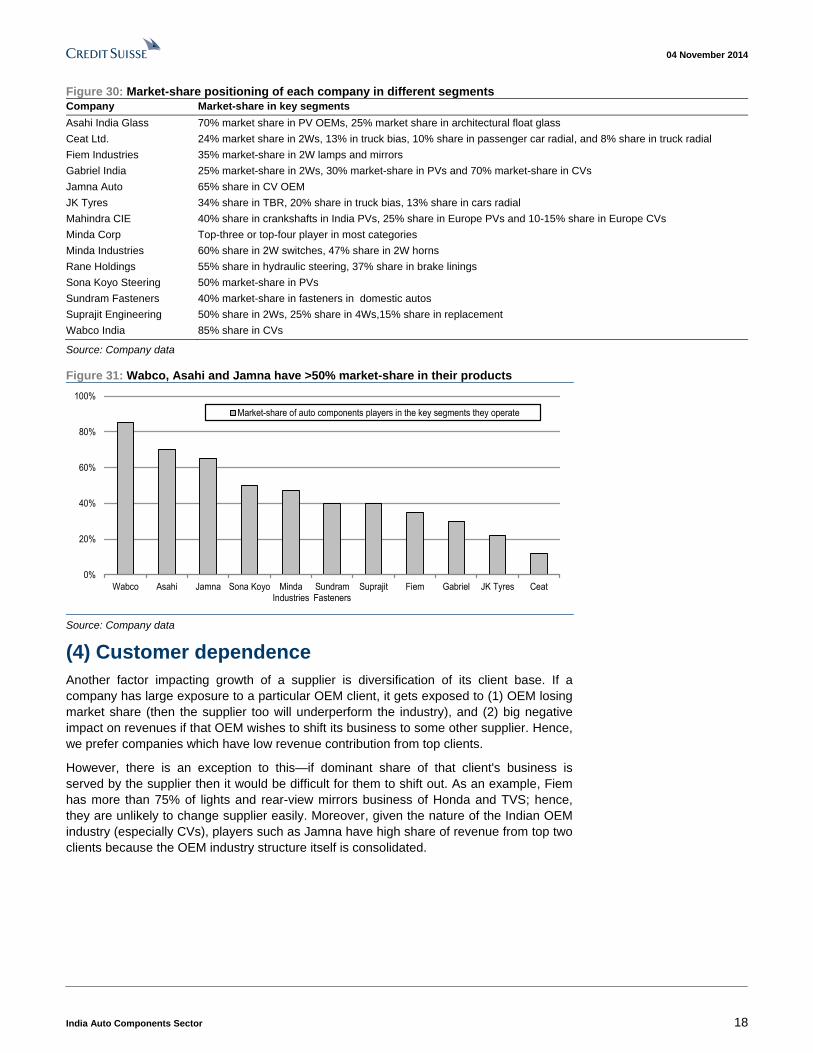

(3) Market-share positioning

Given the fragmented nature of India's auto parts industry, it becomes critical to have

strong barriers to entry in the business in order to maintain/gain share. The various factors

on which firms can generate barriers to entry can be summarised as follows:

Figure 29: Key barriers to entry/success factors for Indian auto component players

Factor Reason

Expertise in design and consistent quality

Ability to design, test and produce as per customised requirements of OEMs for each model,

while maintaining quality. OEMs want suppliers who can provide complete solutions, right from

design, testing to manufacturing

Cost structure

OEMs have greater bargaining power given the large number of auto-component players, hence,

cost becomes important factor. Efficient cost structure arises due to factors such as economies of

scale, cost leadership due to higher R&D spend, and hence ability to do everything in-house, etc.

Technology intensive (tie-ups with foreign

suppliers) or capital intensive

For many high-tech products, OEMs prefer partnerships with foreign suppliers with whom they

have likely worked before. In capital-intensive products, threat of new entrants is lesser

Customised products with long gestation

period

Elaborate testing and development procedure for some components such as crankshafts in which

suppliers have to work with OEMs during the development stage of vehicle, so long relationships

for lifetime unless new models/platforms are launched.

Plants spread across country in proximity to

OEMs

Not only lowers freight costs, OEMs have bigger comfort around inventory management with

movement towards 'just in time'.

Brand (replacement focussed) More relevant to the replacement market as customers are only willing to pay premium over the

unorganised sector (which is typically ~40%) for brand strength.

Distribution network (replacement focused) Essential to have a nation-wide distribution network to increase share in replacement.

Source: Company data

Most of the companies that we surveyed are amongst the top three players in their

segment. Asahi (glass), Jamna (leaf-springs), Sona Koyo (steering), Suprajit (cables),

Sundaram Fasteners (fasteners) and Wabco (braking systems) are market leaders.

Companies such as Fiem, Gabirel, JK Tyres, Minda Ind, Rane are amongst top-two

players in their segment.

04 November 2014

India Auto Components Sector 18

Figure 30: Market-share positioning of each company in different segments

Company Market-share in key segments

Asahi India Glass 70% market share in PV OEMs, 25% market share in architectural float glass

Ceat Ltd. 24% market share in 2Ws, 13% in truck bias, 10% share in passenger car radial, and 8% share in truck radial

Fiem Industries 35% market-share in 2W lamps and mirrors

Gabriel India 25% market-share in 2Ws, 30% market-share in PVs and 70% market-share in CVs

Jamna Auto 65% share in CV OEM

JK Tyres 34% share in TBR, 20% share in truck bias, 13% share in cars radial

Mahindra CIE 40% share in crankshafts in India PVs, 25% share in Europe PVs and 10-15% share in Europe CVs

Minda Corp Top-three or top-four player in most categories

Minda Industries 60% share in 2W switches, 47% share in 2W horns

Rane Holdings 55% share in hydraulic steering, 37% share in brake linings

Sona Koyo Steering 50% market-share in PVs

Sundram Fasteners 40% market-share in fasteners in domestic autos

Suprajit Engineering 50% share in 2Ws, 25% share in 4Ws,15% share in replacement

Wabco India 85% share in CVs

Source: Company data

Figure 31: Wabco, Asahi and Jamna have >50% market-share in their products

0%

20%

40%

60%

80%

100%

Wabco Asahi Jamna Sona Koyo MindaIndustries

SundramFasteners

Suprajit Fiem Gabriel JK Tyres Ceat

Market-share of auto components players in the key segments they operate

Source: Company data

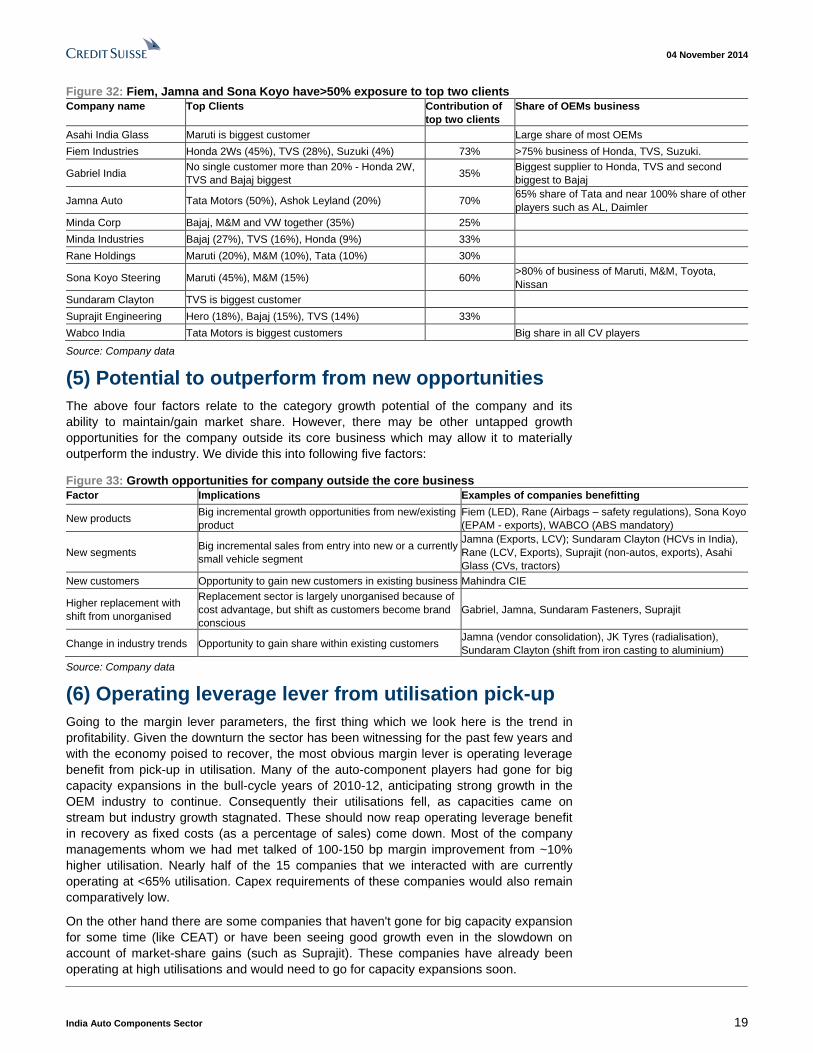

(4) Customer dependence

Another factor impacting growth of a supplier is diversification of its client base. If a

company has large exposure to a particular OEM client, it gets exposed to (1) OEM losing

market share (then the supplier too will underperform the industry), and (2) big negative

impact on revenues if that OEM wishes to shift its business to some other supplier. Hence,

we prefer companies which have low revenue contribution from top clients.

However, there is an exception to this—if dominant share of that client's business is

served by the supplier then it would be difficult for them to shift out. As an example, Fiem

has more than 75% of lights and rear-view mirrors business of Honda and TVS; hence,

they are unlikely to change supplier easily. Moreover, given the nature of the Indian OEM

industry (especially CVs), players such as Jamna have high share of revenue from top two

clients because the OEM industry structure itself is consolidated.

04 November 2014

India Auto Components Sector 19

Figure 32: Fiem, Jamna and Sona Koyo have>50% exposure to top two clients

Company name Top Clients Contribution of

top two clients

Share of OEMs business

Asahi India Glass Maruti is biggest customer Large share of most OEMs

Fiem Industries Honda 2Ws (45%), TVS (28%), Suzuki (4%) 73% >75% business of Honda, TVS, Suzuki.

Gabriel India No single customer more than 20% - Honda 2W,

TVS and Bajaj biggest 35%

Biggest supplier to Honda, TVS and second

biggest to Bajaj

Jamna Auto Tata Motors (50%), Ashok Leyland (20%) 70% 65% share of Tata and near 100% share of other

players such as AL, Daimler

Minda Corp Bajaj, M&M and VW together (35%) 25%

Minda Industries Bajaj (27%), TVS (16%), Honda (9%) 33%

Rane Holdings Maruti (20%), M&M (10%), Tata (10%) 30%

Sona Koyo Steering Maruti (45%), M&M (15%) 60% >80% of business of Maruti, M&M, Toyota,

Nissan

Sundaram Clayton TVS is biggest customer

Suprajit Engineering Hero (18%), Bajaj (15%), TVS (14%) 33%

Wabco India Tata Motors is biggest customers Big share in all CV players

Source: Company data

(5) Potential to outperform from new opportunities

The above four factors relate to the category growth potential of the company and its

ability to maintain/gain market share. However, there may be other untapped growth

opportunities for the company outside its core business which may allow it to materially

outperform the industry. We divide this into following five factors:

Figure 33: Growth opportunities for company outside the core business

Factor Implications Examples of companies benefitting

New products Big incremental growth opportunities from new/existing

product

Fiem (LED), Rane (Airbags – safety regulations), Sona Koyo

(EPAM - exports), WABCO (ABS mandatory)

New segments Big incremental sales from entry into new or a currently

small vehicle segment

Jamna (Exports, LCV); Sundaram Clayton (HCVs in India),

Rane (LCV, Exports), Suprajit (non-autos, exports), Asahi

Glass (CVs, tractors)

New customers Opportunity to gain new customers in existing business Mahindra CIE

Higher replacement with

shift from unorganised

Replacement sector is largely unorganised because of

cost advantage, but shift as customers become brand

conscious

Gabriel, Jamna, Sundaram Fasteners, Suprajit

Change in industry trends Opportunity to gain share within existing customers Jamna (vendor consolidation), JK Tyres (radialisation),

Sundaram Clayton (shift from iron casting to aluminium)

Source: Company data

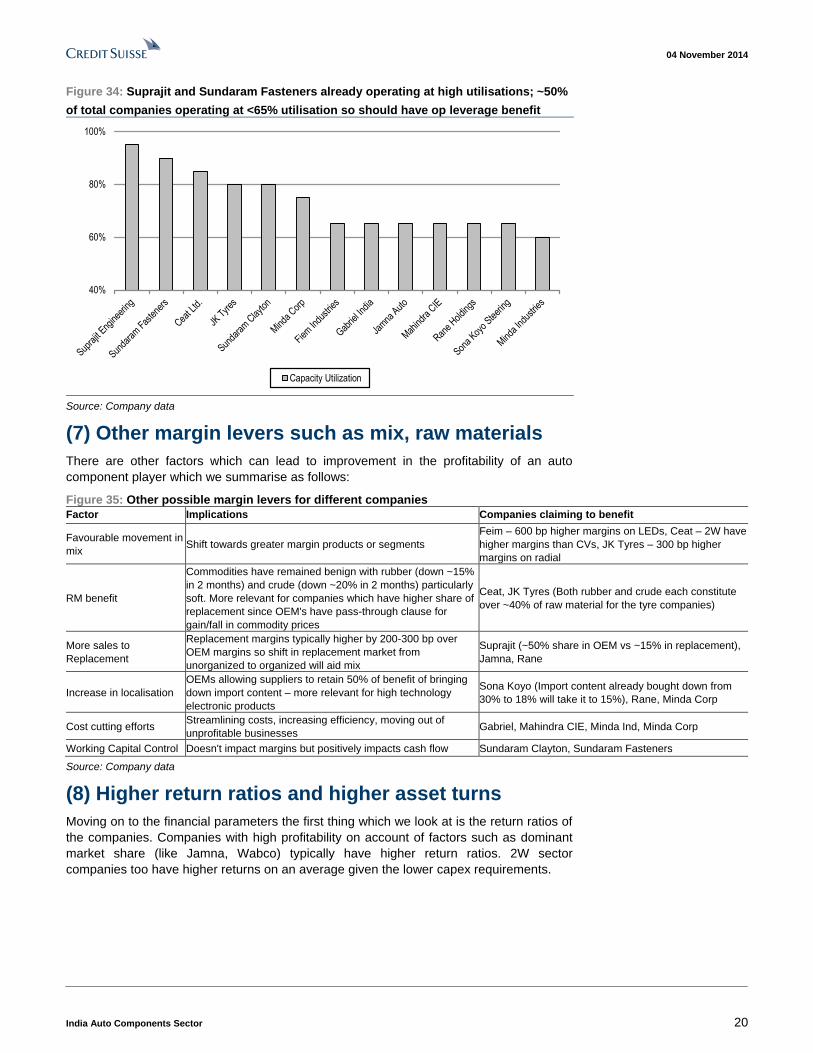

(6) Operating leverage lever from utilisation pick-up

Going to the margin lever parameters, the first thing which we look here is the trend in

profitability. Given the downturn the sector has been witnessing for the past few years and

with the economy poised to recover, the most obvious margin lever is operating leverage

benefit from pick-up in utilisation. Many of the auto-component players had gone for big

capacity expansions in the bull-cycle years of 2010-12, anticipating strong growth in the

OEM industry to continue. Consequently their utilisations fell, as capacities came on

stream but industry growth stagnated. These should now reap operating leverage benefit

in recovery as fixed costs (as a percentage of sales) come down. Most of the company

managements whom we had met talked of 100-150 bp margin improvement from ~10%

higher utilisation. Nearly half of the 15 companies that we interacted with are currently

operating at <65% utilisation. Capex requirements of these companies would also remain

comparatively low.

On the other hand there are some companies that haven't gone for big capacity expansion

for some time (like CEAT) or have been seeing good growth even in the slowdown on

account of market-share gains (such as Suprajit). These companies have already been

operating at high utilisations and would need to go for capacity expansions soon.

04 November 2014

India Auto Components Sector 20

Figure 34: Suprajit and Sundaram Fasteners already operating at high utilisations; ~50%

of total companies operating at <65% utilisation so should have op leverage benefit

40%

60%

80%

100%

Capacity Utilization

Source: Company data

(7) Other margin levers such as mix, raw materials

There are other factors which can lead to improvement in the profitability of an auto

component player which we summarise as follows:

Figure 35: Other possible margin levers for different companies

Factor Implications Companies claiming to benefit

Favourable movement in

mix Shift towards greater margin products or segments

Feim – 600 bp higher margins on LEDs, Ceat – 2W have

higher margins than CVs, JK Tyres – 300 bp higher

margins on radial

RM benefit

Commodities have remained benign with rubber (down ~15%

in 2 months) and crude (down ~20% in 2 months) particularly

soft. More relevant for companies which have higher share of

replacement since OEM's have pass-through clause for

gain/fall in commodity prices

Ceat, JK Tyres (Both rubber and crude each constitute

over ~40% of raw material for the tyre companies)

More sales to

Replacement

Replacement margins typically higher by 200-300 bp over

OEM margins so shift in replacement market from

unorganized to organized will aid mix

Suprajit (~50% share in OEM vs ~15% in replacement),

Jamna, Rane

Increase in localisation

OEMs allowing suppliers to retain 50% of benefit of bringing

down import content – more relevant for high technology

electronic products

Sona Koyo (Import content already bought down from

30% to 18% will take it to 15%), Rane, Minda Corp

Cost cutting efforts Streamlining costs, increasing efficiency, moving out of

unprofitable businesses Gabriel, Mahindra CIE, Minda Ind, Minda Corp

Working Capital Control Doesn't impact margins but positively impacts cash flow Sundaram Clayton, Sundaram Fasteners

Source: Company data

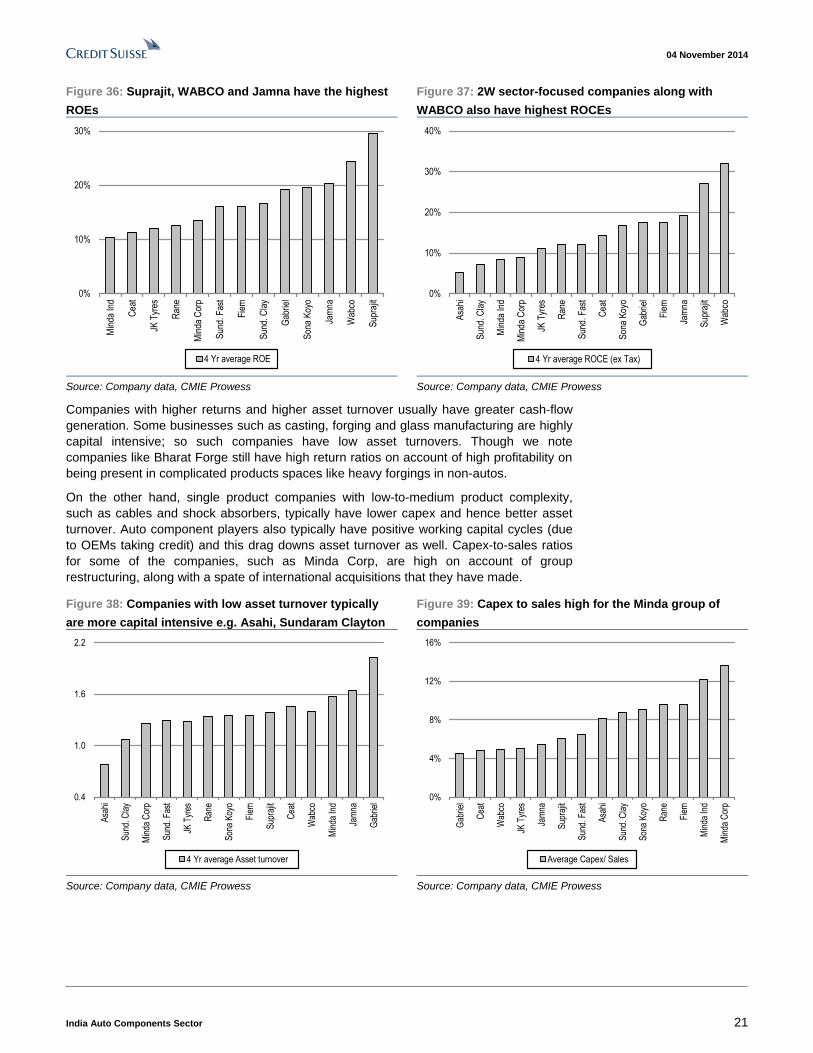

(8) Higher return ratios and higher asset turns

Moving on to the financial parameters the first thing which we look at is the return ratios of

the companies. Companies with high profitability on account of factors such as dominant

market share (like Jamna, Wabco) typically have higher return ratios. 2W sector

companies too have higher returns on an average given the lower capex requirements.

04 November 2014

India Auto Components Sector 21

Figure 36: Suprajit, WABCO and Jamna have the highest

ROEs

Figure 37: 2W sector-focused companies along with

WABCO also have highest ROCEs

0%

10%

20%

30%

Min

da In

d

Cea

t

JK T

yres

Ran

e

Min

da C

orp

Sun

d. F

ast

Fie

m

Sun

d. C

lay

Gab

riel

Son

a K

oyo

Jam

na

Wab

co

Sup

rajit

4 Yr average ROE

0%

10%

20%

30%

40%

Asa

hi

Sun

d. C

lay

Min

da In

d

Min

da C

orp

JK T

yres

Ran

e

Sun

d. F

ast

Cea

t

Son

a K

oyo

Gab

riel

Fie

m

Jam

na

Sup

rajit

Wab

co

4 Yr average ROCE (ex Tax)

Source: Company data, CMIE Prowess Source: Company data, CMIE Prowess

Companies with higher returns and higher asset turnover usually have greater cash-flow

generation. Some businesses such as casting, forging and glass manufacturing are highly

capital intensive; so such companies have low asset turnovers. Though we note

companies like Bharat Forge still have high return ratios on account of high profitability on

being present in complicated products spaces like heavy forgings in non-autos.

On the other hand, single product companies with low-to-medium product complexity,

such as cables and shock absorbers, typically have lower capex and hence better asset

turnover. Auto component players also typically have positive working capital cycles (due

to OEMs taking credit) and this drag downs asset turnover as well. Capex-to-sales ratios

for some of the companies, such as Minda Corp, are high on account of group

restructuring, along with a spate of international acquisitions that they have made.

Figure 38: Companies with low asset turnover typically

are more capital intensive e.g. Asahi, Sundaram Clayton

Figure 39: Capex to sales high for the Minda group of

companies

0.4

1.0

1.6

2.2

Asa

hi

Sun

d. C

lay

Min

da C

orp

Sun

d. F

ast

JK T

yres

Ran

e

Son

a K

oyo

Fiem

Sup

rajit

Cea

t

Wab

co

Min

da In

d

Jam

na

Gab

riel

4 Yr average Asset turnover

0%

4%

8%

12%

16%

Gab

riel

Cea

t

Wab

co

JK T

yres

Jam

na

Sup

rajit

Sun

d. F

ast

Asa

hi

Sun

d. C

lay

Son

a K

oyo

Ran

e

Fiem

Min

da In

d

Min

da C

orp

Average Capex/ Sales

Source: Company data, CMIE Prowess Source: Company data, CMIE Prowess

04 November 2014

India Auto Components Sector 22

(9) Lower margin volatility

Suppliers, such as Wabco, which have high bargaining power due to reasons such as

technology leadership have better pricing power and resilient margins across cycles. The

other suppliers with stable margins are 2W sector-focused companies, such as Suprajit

and Fiem, as the 2W OEM sector in India has seen relatively secular growth with very few

down-cycle years. On the other hand, tyre companies have very volatile margins

depending on the commodity cycle and consequently trade at lower multiples. The current

margins of tyre companies are already much higher than the historical average, given the

continued raw material benefits they have enjoyed from falling rubber prices.

Figure 40: 2W sector-focused companies and Wabco have

low margin volatility while for tyre companies it is high

Figure 41: Current margins of tyre companies are above

the historical average

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

Sup

rajit

Fie

m

Sun

d. F

ast

Ran

e

Wab

co

Gab

riel

Min

da C

orp

Asa

hi

Jam

na

Son

a K

oyo

Sun

d, C

lay

Min

da In

d

JK T

yres

Cea

t

Margin Volatility ((Peak margin less bottom margin)/ average margin))

-6%

-4%

-2%

0%

2%

4%

6%

Min

da In

d

Wab

co

Jam

na

Sun

d. C

lay

Ran

e

Asa

hi

Min

da C

orp

Gab

riel

Sun

d. F

ast

Fie

m

Sup

rajit

Son

a K

oyo

JK T

yres

Cea

t

Margin difference (Current vs historic average)

Source: Company data, CMIE Prowess Source: Company data, CMIE Prowess

04 November 2014

India Auto Components Sector 23

A basket of component stocks to play CV cycle We remain very constructive on the CV cycle but our preferred play on the same Ashok

Leyland is now already pricing in the best case scenario hence we are downgrading it to a

NEUTRAL. We think investors should instead switch to a basket of component stocks

supplying to the CV industry. We are also increasing our TP on Apollo Tyres (O) to Rs260

and on Bharat Forge (N) to Rs830. Our preferred pick in the component space remains

Apollo Tyres and we are now initiating coverage on WABCO as well.

Initiate on WABCO (OUTPEFROM) with a TP of Rs4,820: WABCO is the largest player in

the CV braking industry in India with a >80% market share. We believe WABCO is one of

the best structural plays in the Indian auto component space with safety and emission

content per vehicle in India being a tenth of European markets. WABCO India also has a

prominent position in WABCO's global scheme of things as its hub for adapting products

for emerging markets as well as being a critical country in its plans to increase sourcing

from low cost countries. CV cycle recovery and mandatory ABS implementation are near-

term triggers for the stock.

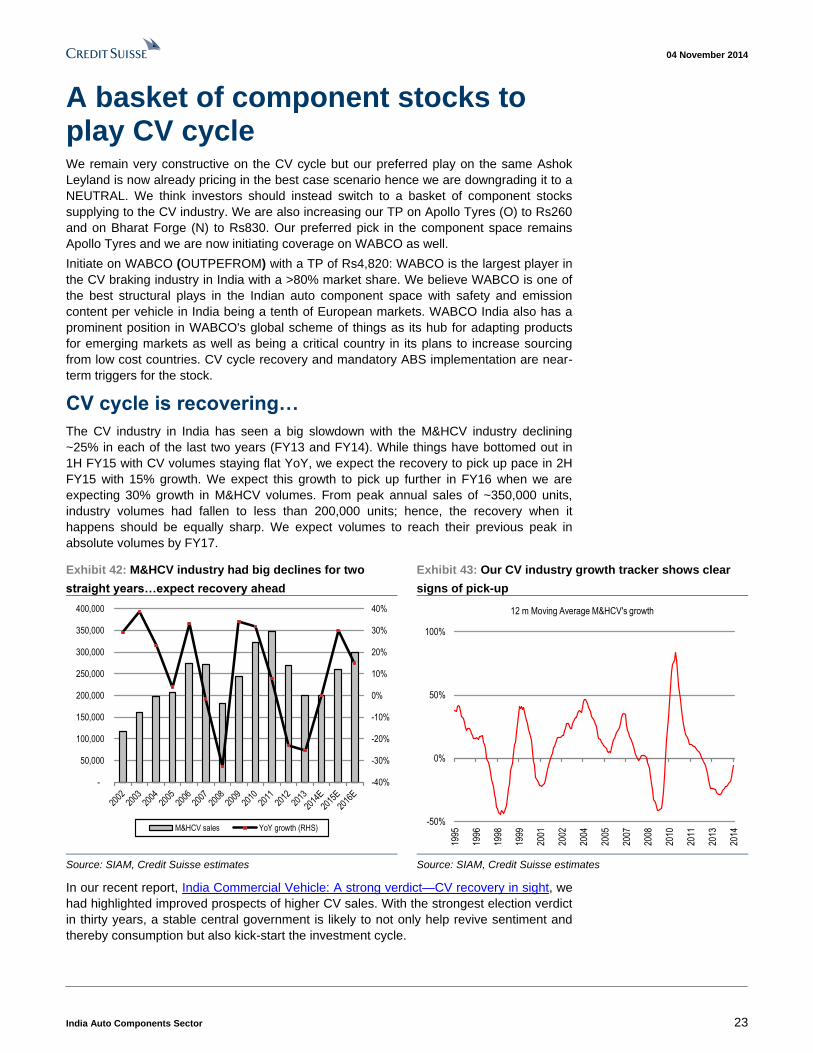

CV cycle is recovering…

The CV industry in India has seen a big slowdown with the M&HCV industry declining

~25% in each of the last two years (FY13 and FY14). While things have bottomed out in

1H FY15 with CV volumes staying flat YoY, we expect the recovery to pick up pace in 2H

FY15 with 15% growth. We expect this growth to pick up further in FY16 when we are

expecting 30% growth in M&HCV volumes. From peak annual sales of ~350,000 units,

industry volumes had fallen to less than 200,000 units; hence, the recovery when it

happens should be equally sharp. We expect volumes to reach their previous peak in

absolute volumes by FY17.

Exhibit 42: M&HCV industry had big declines for two

straight years…expect recovery ahead

Exhibit 43: Our CV industry growth tracker shows clear

signs of pick-up

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

M&HCV sales YoY growth (RHS)

-50%

0%

50%

100%

1995

1996

1998

1999

2001

2002

2004

2005

2007

2008

2010

2011

2013

2014

12 m Moving Average M&HCV's growth

Source: SIAM, Credit Suisse estimates Source: SIAM, Credit Suisse estimates

In our recent report, India Commercial Vehicle: A strong verdict—CV recovery in sight, we

had highlighted improved prospects of higher CV sales. With the strongest election verdict

in thirty years, a stable central government is likely to not only help revive sentiment and

thereby consumption but also kick-start the investment cycle.

04 November 2014

India Auto Components Sector 24

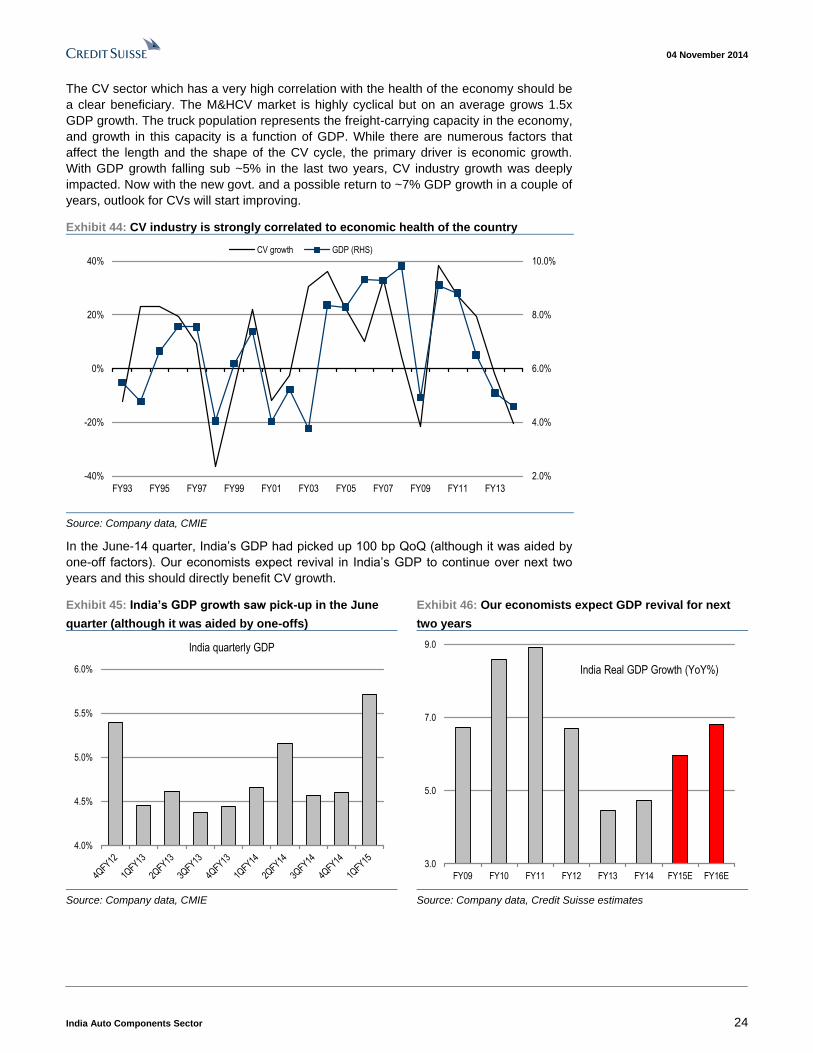

The CV sector which has a very high correlation with the health of the economy should be

a clear beneficiary. The M&HCV market is highly cyclical but on an average grows 1.5x

GDP growth. The truck population represents the freight-carrying capacity in the economy,

and growth in this capacity is a function of GDP. While there are numerous factors that

affect the length and the shape of the CV cycle, the primary driver is economic growth.

With GDP growth falling sub ~5% in the last two years, CV industry growth was deeply

impacted. Now with the new govt. and a possible return to ~7% GDP growth in a couple of

years, outlook for CVs will start improving.

Exhibit 44: CV industry is strongly correlated to economic health of the country

2.0%

4.0%

6.0%

8.0%

10.0%

-40%

-20%

0%

20%

40%

FY93 FY95 FY97 FY99 FY01 FY03 FY05 FY07 FY09 FY11 FY13

CV growth GDP (RHS)

Source: Company data, CMIE

In the June-14 quarter, India’s GDP had picked up 100 bp QoQ (although it was aided by

one-off factors). Our economists expect revival in India’s GDP to continue over next two

years and this should directly benefit CV growth.

Exhibit 45: India’s GDP growth saw pick-up in the June

quarter (although it was aided by one-offs)

Exhibit 46: Our economists expect GDP revival for next

two years

4.0%

4.5%

5.0%

5.5%

6.0%

India quarterly GDP

3.0

5.0

7.0

9.0

FY09 FY10 FY11 FY12 FY13 FY14 FY15E FY16E

India Real GDP Growth (YoY%)

Source: Company data, CMIE Source: Company data, Credit Suisse estimates

04 November 2014

India Auto Components Sector 25

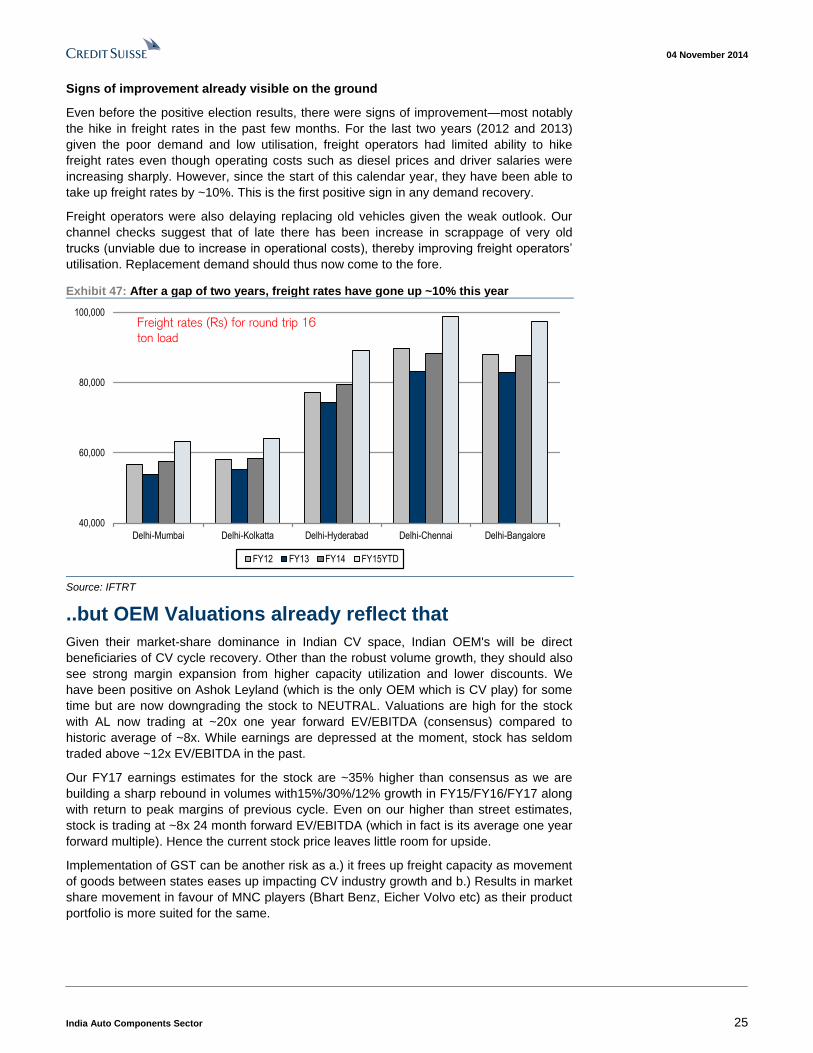

Signs of improvement already visible on the ground

Even before the positive election results, there were signs of improvement—most notably

the hike in freight rates in the past few months. For the last two years (2012 and 2013)

given the poor demand and low utilisation, freight operators had limited ability to hike

freight rates even though operating costs such as diesel prices and driver salaries were

increasing sharply. However, since the start of this calendar year, they have been able to

take up freight rates by ~10%. This is the first positive sign in any demand recovery.

Freight operators were also delaying replacing old vehicles given the weak outlook. Our

channel checks suggest that of late there has been increase in scrappage of very old

trucks (unviable due to increase in operational costs), thereby improving freight operators’

utilisation. Replacement demand should thus now come to the fore.

Exhibit 47: After a gap of two years, freight rates have gone up ~10% this year

40,000

60,000

80,000

100,000

Delhi-Mumbai Delhi-Kolkatta Delhi-Hyderabad Delhi-Chennai Delhi-Bangalore

FY12 FY13 FY14 FY15YTD

Freight rates (Rs) for round trip 16

ton load

Source: IFTRT

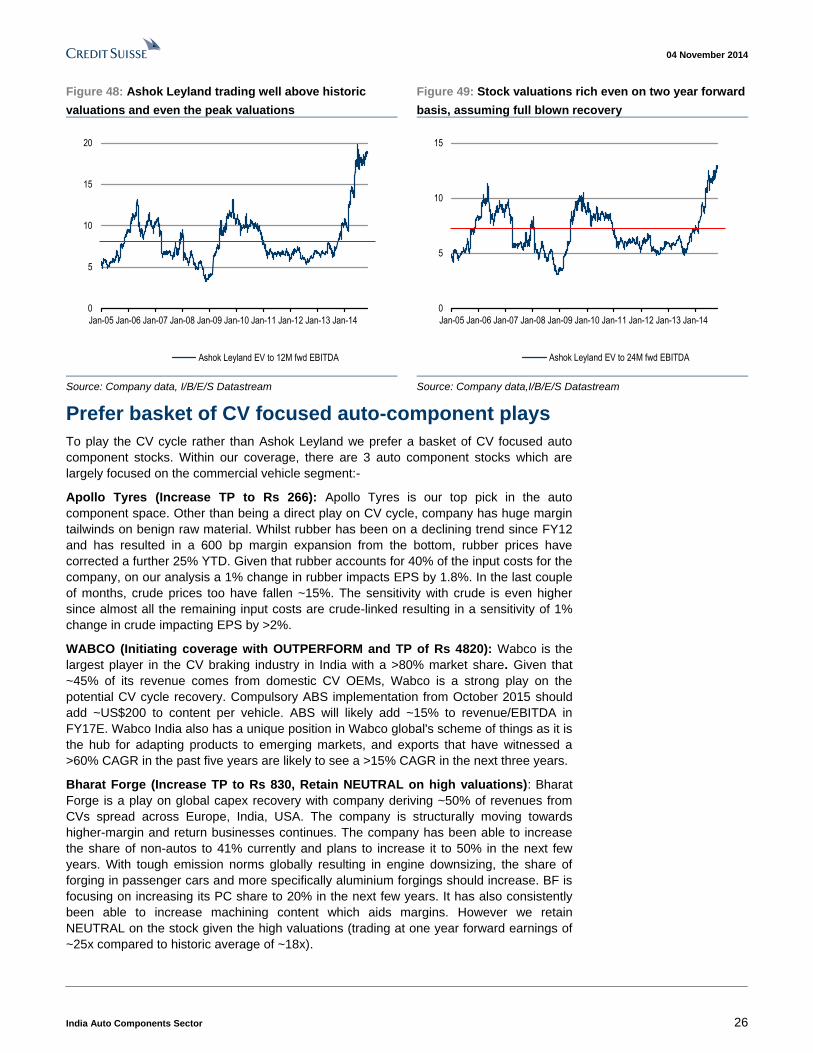

..but OEM Valuations already reflect that

Given their market-share dominance in Indian CV space, Indian OEM's will be direct

beneficiaries of CV cycle recovery. Other than the robust volume growth, they should also

see strong margin expansion from higher capacity utilization and lower discounts. We

have been positive on Ashok Leyland (which is the only OEM which is CV play) for some

time but are now downgrading the stock to NEUTRAL. Valuations are high for the stock

with AL now trading at ~20x one year forward EV/EBITDA (consensus) compared to

historic average of ~8x. While earnings are depressed at the moment, stock has seldom

traded above ~12x EV/EBITDA in the past.

Our FY17 earnings estimates for the stock are ~35% higher than consensus as we are

building a sharp rebound in volumes with15%/30%/12% growth in FY15/FY16/FY17 along

with return to peak margins of previous cycle. Even on our higher than street estimates,

stock is trading at ~8x 24 month forward EV/EBITDA (which in fact is its average one year

forward multiple). Hence the current stock price leaves little room for upside.

Implementation of GST can be another risk as a.) it frees up freight capacity as movement

of goods between states eases up impacting CV industry growth and b.) Results in market

share movement in favour of MNC players (Bhart Benz, Eicher Volvo etc) as their product

portfolio is more suited for the same.

04 November 2014

India Auto Components Sector 26

Figure 48: Ashok Leyland trading well above historic

valuations and even the peak valuations

Figure 49: Stock valuations rich even on two year forward

basis, assuming full blown recovery

0

5

10

15

20

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Ashok Leyland EV to 12M fwd EBITDA

0

5

10

15

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

Ashok Leyland EV to 24M fwd EBITDA

Source: Company data, I/B/E/S Datastream Source: Company data,I/B/E/S Datastream

Prefer basket of CV focused auto-component plays

To play the CV cycle rather than Ashok Leyland we prefer a basket of CV focused auto

component stocks. Within our coverage, there are 3 auto component stocks which are

largely focused on the commercial vehicle segment:-

Apollo Tyres (Increase TP to Rs 266): Apollo Tyres is our top pick in the auto

component space. Other than being a direct play on CV cycle, company has huge margin

tailwinds on benign raw material. Whilst rubber has been on a declining trend since FY12

and has resulted in a 600 bp margin expansion from the bottom, rubber prices have

corrected a further 25% YTD. Given that rubber accounts for 40% of the input costs for the

company, on our analysis a 1% change in rubber impacts EPS by 1.8%. In the last couple

of months, crude prices too have fallen ~15%. The sensitivity with crude is even higher

since almost all the remaining input costs are crude-linked resulting in a sensitivity of 1%

change in crude impacting EPS by >2%.

WABCO (Initiating coverage with OUTPERFORM and TP of Rs 4820): Wabco is the

largest player in the CV braking industry in India with a >80% market share. Given that

~45% of its revenue comes from domestic CV OEMs, Wabco is a strong play on the

potential CV cycle recovery. Compulsory ABS implementation from October 2015 should

add ~US$200 to content per vehicle. ABS will likely add ~15% to revenue/EBITDA in

FY17E. Wabco India also has a unique position in Wabco global's scheme of things as it is

the hub for adapting products to emerging markets, and exports that have witnessed a

>60% CAGR in the past five years are likely to see a >15% CAGR in the next three years.

Bharat Forge (Increase TP to Rs 830, Retain NEUTRAL on high valuations): Bharat

Forge is a play on global capex recovery with company deriving ~50% of revenues from

CVs spread across Europe, India, USA. The company is structurally moving towards

higher-margin and return businesses continues. The company has been able to increase

the share of non-autos to 41% currently and plans to increase it to 50% in the next few

years. With tough emission norms globally resulting in engine downsizing, the share of

forging in passenger cars and more specifically aluminium forgings should increase. BF is

focusing on increasing its PC share to 20% in the next few years. It has also consistently

been able to increase machining content which aids margins. However we retain

NEUTRAL on the stock given the high valuations (trading at one year forward earnings of

~25x compared to historic average of ~18x).

04 November 2014

India Auto Components Sector 27

Companies

04 November 2014

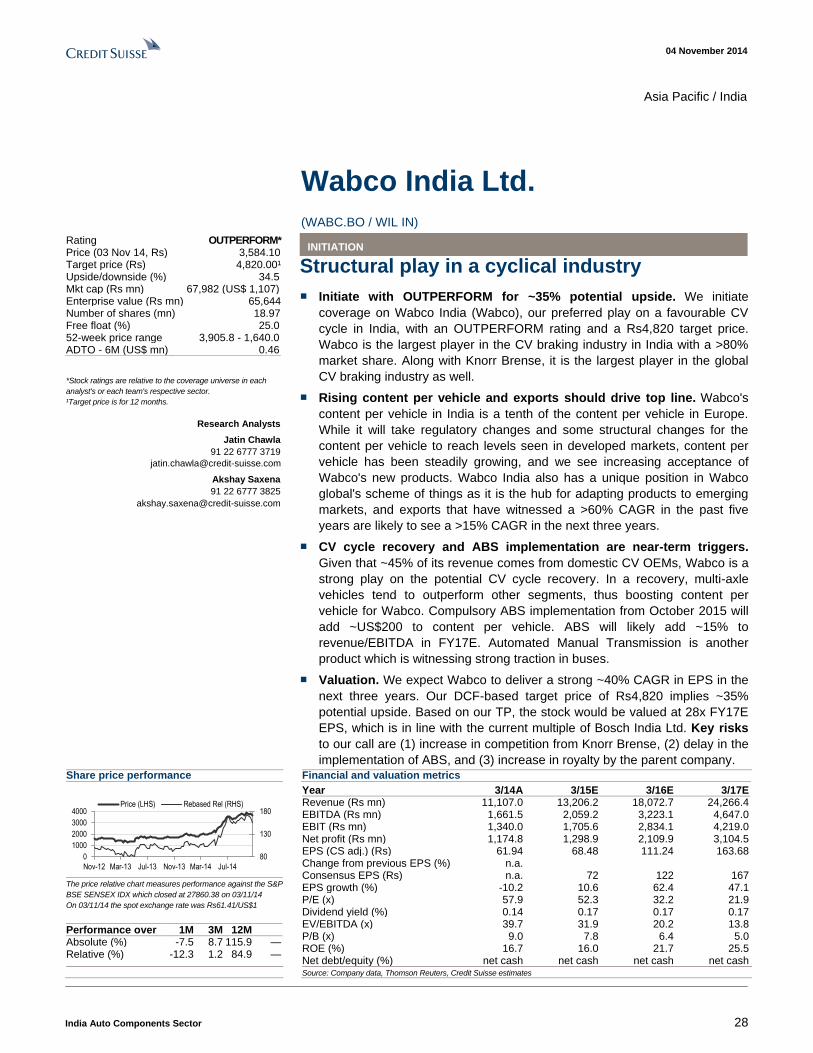

India Auto Components Sector 28

Asia Pacific / India

Wabco India Ltd.

(WABC.BO / WIL IN) INITIATION

Structural play in a cyclical industry

■ Initiate with OUTPERFORM for ~35% potential upside. We initiate

coverage on Wabco India (Wabco), our preferred play on a favourable CV

cycle in India, with an OUTPERFORM rating and a Rs4,820 target price.

Wabco is the largest player in the CV braking industry in India with a >80%

market share. Along with Knorr Brense, it is the largest player in the global

CV braking industry as well.

■ Rising content per vehicle and exports should drive top line. Wabco's

content per vehicle in India is a tenth of the content per vehicle in Europe.

While it will take regulatory changes and some structural changes for the

content per vehicle to reach levels seen in developed markets, content per

vehicle has been steadily growing, and we see increasing acceptance of

Wabco's new products. Wabco India also has a unique position in Wabco

global's scheme of things as it is the hub for adapting products to emerging

markets, and exports that have witnessed a >60% CAGR in the past five

years are likely to see a >15% CAGR in the next three years.

■ CV cycle recovery and ABS implementation are near-term triggers.

Given that ~45% of its revenue comes from domestic CV OEMs, Wabco is a

strong play on the potential CV cycle recovery. In a recovery, multi-axle

vehicles tend to outperform other segments, thus boosting content per

vehicle for Wabco. Compulsory ABS implementation from October 2015 will

add ~US$200 to content per vehicle. ABS will likely add ~15% to

revenue/EBITDA in FY17E. Automated Manual Transmission is another

product which is witnessing strong traction in buses.

■ Valuation. We expect Wabco to deliver a strong ~40% CAGR in EPS in the

next three years. Our DCF-based target price of Rs4,820 implies ~35%

potential upside. Based on our TP, the stock would be valued at 28x FY17E

EPS, which is in line with the current multiple of Bosch India Ltd. Key risks

to our call are (1) increase in competition from Knorr Brense, (2) delay in the

implementation of ABS, and (3) increase in royalty by the parent company. Share price performance

80

130

180

0

1000

2000

3000

4000

Nov-12 Mar-13 Jul-13 Nov-13 Mar-14 Jul-14

Price (LHS) Rebased Rel (RHS)

The price relative chart measures performance against the S&P

BSE SENSEX IDX which closed at 27860.38 on 03/11/14

On 03/11/14 the spot exchange rate was Rs61.41/US$1

Performance over 1M 3M 12M Absolute (%) -7.5 8.7 115.9 — Relative (%) -12.3 1.2 84.9 —

Financial and valuation metrics