Embed Size (px)

Citation preview

Know Your Benefits2014-2015Plan Year

How did we get here?

2

April 2013 – Health Care Forum May/June 2013 – Two All-Day Benefits Planning Meetings July 2013 – RFP Preparation Oct./Nov. 2013 – Request for Proposal Nov 2013 – RFP Information Compiled by Hub International Dec. 2013 – Faculty & Staff Survey Dec. 2013/Feb. 2014 – Committee Review of Proposals

◦ Six, four-hour meetings Jan. 2014 – Final Vendor Presentations Feb. 2014 – Vendor Recommendations to President’s

Council Feb 2014 – HR Matters sent to employees April 2014 – Health Care Forum II

Employee survey sought to discover the number one issue for employees in regards to our health plan.

Employees were asked to rank three criteria from lowest to highest priority.◦ Cost: total yearly out-of-pocket costs including monthly

premiums, co-pays, and deductibles◦ Access: Ability to be seen by a member of the provider network

in the nearby vicinity◦ Choice: Ability to visit your preferred hospital, clinic, or health

professional Survey collected 559 responses 370 ranked cost as their highest priority (66%) 141 ranked choice as their highest (25%) 48 ranked access as their highest priority (9%)

Employee Survey Results

3

Where are our employees?

4

Nationwide network, with in-network coverage outside of UT.

85% of employees live in UT county UMR covers 96% of UVU’s top 200 providers Out-of-network coverage leased through

First Health Network

Employee Access

5

Two network offerings◦ United Healthcare Choice Plus and Options PPO

Choice Plus network mirrors our current network facilities with EMI ◦ Intermountain Health Care Facilities

Options PPO covers IHC as well as the University of Utah Hospital and IASIS facilities◦ Jordan Valley, Davis Hospital, Pioneer Valley, and

Salt Lake Regional◦ Mountain Star hospitals only offered as an out-of-

network facility

Employee Choice

6

Network Facilities

7

UHC Choice Plus UHC Options PPO Out-of-network

UVRMCAll UHC Choice Plus

FacilitiesHCA Facilities

American Fork University of Utah HospitalMountain View

HospitalIntermountain Medical Center Huntsman Cancer Center St. Mark's Hospital

Orem Community Hospital Jordan ValleyTimpanogos Regional

Hospital

Primary Children's Davis HospitalBrigham City

Community Hospital

Riverton Hospital Pioneer ValleyLone Peak Medical

Campus

Alta View Hospital Salt Lake RegionalOgden Regional Medical Center

Heber Valley MedicalCentral Utah Clinic of

American Fork Surgery Center

Central Utah Surgery Center (Provo)

Orthopedic Specialty Hospital Park City Medical

Dixie Regional LDS Hospital

No increase in premiums, deductibles, co-pays, or co-insurance coverage for 2014-15 plan year

Consumerism tools available through UMR◦ Healthcare Cost Estimator calculator◦ Teladoc◦ NurseLine◦ Maternity Management◦ Wellness◦ Disease and Case Management◦ Doc GPS app

Employee Cost

8

Unbundled Plan Elements

9

Medical Claims Administration – UMR◦ Best overall savings. Limited disruption for employees

Dental Claims Administration – EMI◦ Deepest savings on network claims. Best overall savings. ◦ No disruption to employees.

Vision – United Healthcare◦ Employee paid benefit◦ Co-pays for glasses and contacts vs. current plan with reimbursement

limits.◦ Lower premiums than current plan offerings, with richer benefit for

employees. Pharmacy Benefit Manager – Envision RX

◦ Best overall savings.◦ Large network offering (Walgreens, Walmart, Smiths, Costco, and more).◦ Specialized care covering 7 million lives.

What Does This Mean in Terms of Monthly Cost?

10

Choice Plus Network Options PPO Network

White Single

Two-Party Family Single

Two-Party Family

Employee Premium $45.38 $104.86 $151.42 $61.48 $142.05 $205.13

University Contribution $408.48 $943.68 $1,362.90 $408.48 $943.68 $1,362.90

Green Single

Two-Party Family Single

Two-Party Family

Employee Premium $73.90 $170.74 $246.58 $91.01 $210.27 $303.67

University Contribution $408.48 $943.68 $1,362.90 $408.48 $943.68 $1,362.90

High Deductible SingleTwo-Party Family Single

Two-Party Family

Employee Premium $0.00 $0.00 $0.00 $14.49 $33.47 $48.34

University Contribution $408.48 $943.68 $1,362.90 $408.48 $943.68 $1,362.90

White and Green Plan

Some services are covered outside the deductible through a co-pay system (office visits, lab work, emergency room, prescriptions, etc.) All preventative care is covered 100% by the plan.

Once the deductible is met, insurance pays 80% of most services and employee pays 20% up to the co-insurance maximum.

Separate deductible and co-insurance maximum for prescriptions.

HDHP:

Every medical/prescription expense is subject to the deductible before insurance payments begin, except for preventative care services, which is covered at 100%

Once the deductible is met, insurance pays 80% of most services and employee pays either a co-pay or co-insurance of 20%.

Two-party and family coverage all subject to $4,000 deductible.

Medical Plan Designs for UVU 2014-2015

11

Medical Plan Designs for UVU 2014-2015

12

White Plan Green Plan High Deductible

Medical Deductible

$1,000 - Individual $2,000 - Family

$500 - Individual $1,000 – Family

$2,000 - Single only coverage $4,000 - Family

Medical Out-of-Pocket Maximum

$5,000 - Individual $10,000 - Family

$4,500 - Individual $9,000 - Family

$3,000 - Single only coverage $6,000 - Family

RX Deductible

$100 - Individual $200 - Family

$100 - Individual $200 - Family Subject to Medical

RX Co-Insurance

$2,000 - Individual $4,000 - Family

$2,000 - Individual $4,000 - Family Subject to Medical

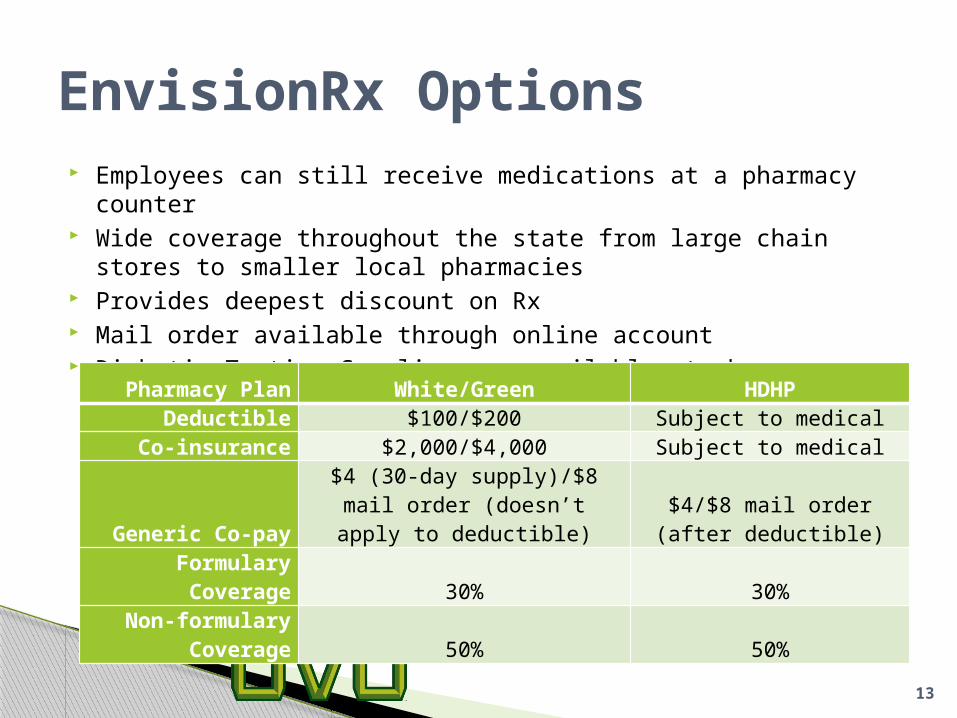

Employees can still receive medications at a pharmacy counter Wide coverage throughout the state from large chain stores to

smaller local pharmacies Provides deepest discount on Rx Mail order available through online account Diabetic Testing Supplies now available at pharmacy

EnvisionRx Options

13

Pharmacy Plan White/Green HDHPDeductible $100/$200 Subject to medical

Co-insurance $2,000/$4,000 Subject to medical

Generic Co-pay

$4 (30-day supply)/$8 mail order (doesn’t apply to

deductible)$4/$8 mail order (after

deductible)Formulary Coverage 30% 30%

Non-formulary Coverage 50% 50%

Plan will remain with EMI Health No disruption for employees Same premiums and plan design as 2013 -

14 $50 deductible per person up to $150 per

family $1500 calendar year limit per person

Dental Administration

14

Dental Plan Single Two-PartyFamil

yEmployee Premium $12.48 $15.96 $23.22

University Contribution $49.94 $63.86 $92.94

New benefit plan Lower premiums with richer benefit! $30 copay for materials (glasses, contacts, etc.) $100 frame benefit Lenses, frames, and contacts (in lieu of glasses) every 24

months

United Healthcare Vision

15

Vision Plan Single Two-Party FamilyEmployee Premium $2.98 $5.96 $9.69

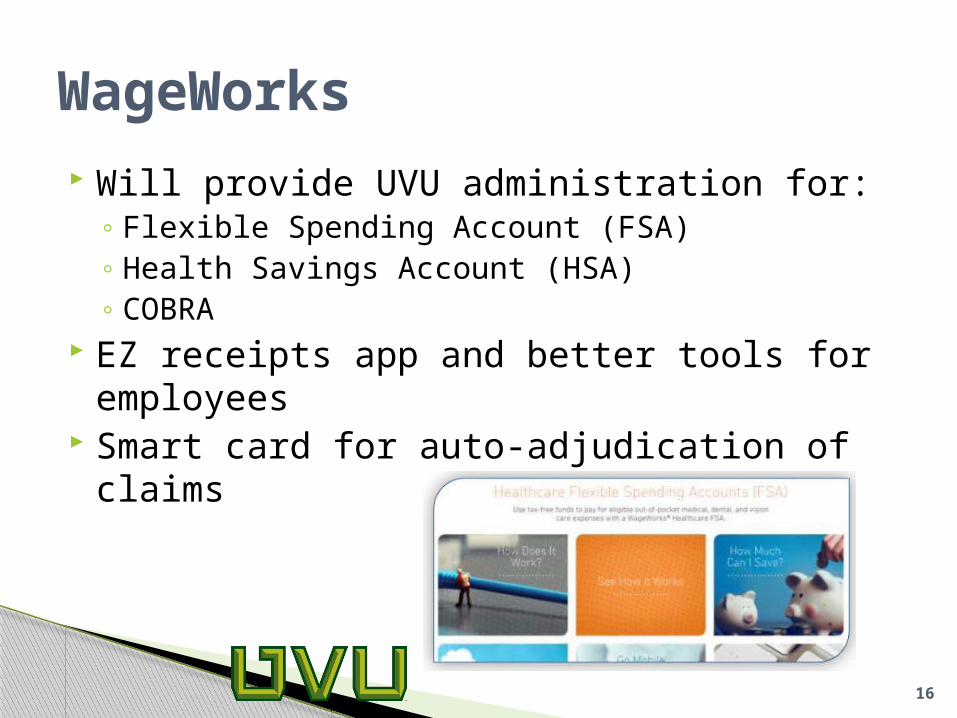

Will provide UVU administration for:◦ Flexible Spending Account (FSA)◦ Health Savings Account (HSA)◦ COBRA

EZ receipts app and better tools for employees

Smart card for auto-adjudication of claims

WageWorks

16

A medical plan that must meet certain IRS annual deductible minimums and maximum out-of-pocket limits.

All covered benefits, with the exception of preventive benefits, apply to the plan deductible, including prescriptions drugs.

Plan covers either Employee Only coverage or Family coverage. ◦ Family coverage - one family member or a combination

of all family members’ claims must meet the deductible amount before the plan will pay towards covered health care services.

What is a High Deductible Health Plan (HDHP)

17

An employee owned tax-free savings account (triple tax savings).1. Payroll contributions to account are on a pre-

tax basis and reduce employee’s annual taxable income.

2. Tax-free withdrawals if used to help pay for qualified out-of-pocket medical, dental, and vision expenses, such as co-pays, deductibles, and coinsurance.

3. Earns interest tax-free. Investment threshold of $1,000 with BNY Mellon

What is a Health Savings Account (HSA)

18

To be eligible for an HSA, an individual has to:• Be covered by a Qualified *HDHP• Not covered by a “*traditional” health insurance plan• Not enrolled in Medicare nor Tricare• Not claimed as a dependent on someone else’s tax return

*Traditional plan – Insurance plan helps pay from the first day*HDHP plan – Deductible must be met before insurance payments begin

What is a Health Savings Account (HSA) Cont.

19

Since the account is owned by the employee, not the employer, the employee decides:◦ Whether he or she will contribute and how much to

contribute;◦ How much to use for qualified expenses;◦ Which expenses to pay for from the account;◦ Whether to pay from the account or save for future use;◦ Which company will hold the account;◦ What type of investments to grow the account (when

qualified). Employer cannot restrict use of HSA distributions.

Employee Owns and Controls the HSA

20

No “use it or lose it” rules like Flexible Spending Accounts.◦ All amounts are fully vested.◦ Unspent balance in account remains in account until spent

(rollover). Encourages consumerism

◦ Encourages account holders to spend their funds more wisely.

◦ Encourages account holders to shop around for the best value for their health care dollars.

Accounts can grow through investment earnings.◦ Same investment options and investment limitations as

IRAs.◦ Same restrictions on self-dealing as with IRAs.

Benefits of an HSA

21

Contribution made by the employee reduces their annual taxable income and the contribution is not taxable to the HSA.

Contributions from all sources count toward the annual contribution limit. The contribution limits are: 2014 - $3,300 employee only: $6,550 family.

Catch-up $1,000 – age 55 by end of tax year. Employee can make a one-time transfer from

their IRA to an HSA (subject to annual contribution limits).

HSA Contribution Rules

22

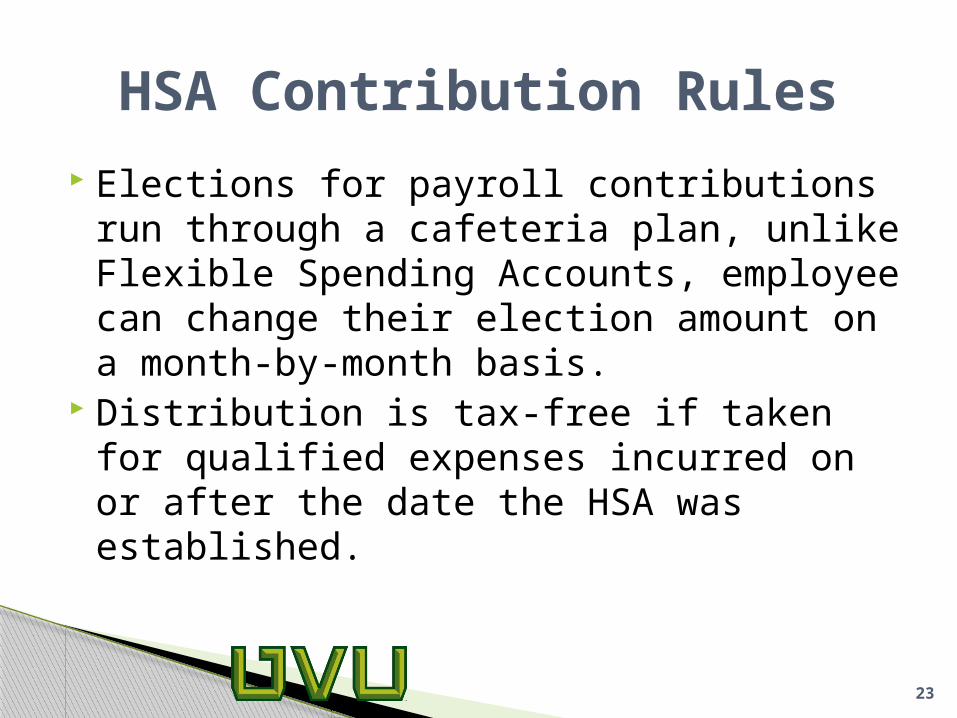

Elections for payroll contributions run through a cafeteria plan, unlike Flexible Spending Accounts, employee can change their election amount on a month-by-month basis.

Distribution is tax-free if taken for qualified expenses incurred on or after the date the HSA was established.

HSA Contribution Rules

23

Distributions can be taken for the employee, the spouse of the employee, and generally any tax dependent of the employee.

Distributions can be taken for non-qualified expenses. Distribution will be subject to:◦Income tax; and◦20% additional tax penalty.

HSA Contribution Rules

24

HSA v. FSA. What’s the difference?

25

Health Savings Account (HSA)

Flexible Spending Account (FSA)

Availability of funds Funds available as employees make payroll contributions

Full funding amounts available on the first day of the plan year.

Who may fund the account

Employee, employer, or any third party

Typically the employee

Who owns the account?

The employee/account holder Employer

Is there an annual contribution limit?

For 2014, $3,300 employee only; $6,550 family.Catch up $1,000 – age 55 by end of tax year.

$2,500.

Can unused fund rollover from year to year?

Yes No

Do claims have to be substantiated for reimbursement?

No Yes

Ineligible Medical Expenses Include: Insurance premiums (other than the ones

listed under the qualified medical expenses) Over-the-counter drugs (unless a

prescription is obtained from a physician or if the drug is insulin)

Cosmetic surgery Expenses covered by another insurance

plan General health items such as tissues,

toiletries, hand sanitizer, etc

What Can’t I Use My HSA/FSA For?

26

UVU will organize a mass transfer of accounts

Account holders have three options:◦ Spend down funds to $0◦ Transfer money from Optum Bank to BNY Mellon

account◦ Keep both accounts open

Account holders will be charged a fee for Optum Bank/Tango account

$4 to keep Tango functionality $1 for Optum Bank

HSA Transition

27

For employees who had an FSA during 2013-14 Grace period in effect until 09/15/2014

Will be administered by National Benefit ServiceDebit cards will not work after 06/30/2014Employees wishing to open an HSA with a

remaining FSA balance as of 7/1/14 will have to wait until 10/1/14 to contribute to an HSA

FSA Transition

28

All enrollments entered online through UVLINK

No paper forms for Medical, Dental, Vision, and Flex-Spending

Remember to check coverage boxes for dependents

Verify coverage level

Benefit Online Enrollment System

29

Will need to fill out UMR survey and inform them of other coverage

All employees must complete, even if they have no other insurance plans

Form can be completed by:◦ Returning form included in mailer with ID cards◦ Calling UMR and verifying coverage◦ Logging into UMR member portal and entering

other coverage information

Double Coverage?

30

UMR Medical Benefit Training: Facilitated by UMR Wednesday, April 23, 2014, 11:00am – 12:00 pm, SC 213 AB Wednesday, May 14, 2014, 1:00 pm – 2:00 pm, BA 207 (Webinar)

WageWorks HSA and FSA Training: Facilitated by WageWorks Wednesday, April 23, 2014, 1:00 pm – 2:00 pm, SC 213 AB Tuesday, April 29, 3014, 1:00 pm – 2:00 pm, BA 207 (Webinar) Tuesday, May 6, 2014, 11:00 am – 12:00 pm. SB 134

EnvisionRx Pharmacy Benefit Training: Facilitated by EnvisionRx Wednesday, April 23, 2014, 12:00 pm – 1:00 pm, SC 213 AB Tuesday, May 13, 2014, 2:00 pm – 3:00 pm, SB 134

Benefit Fair trainings are available on the Open Enrollment site.

Training Opportunities

31

Supplemental Benefit Options◦ Minnesota Life◦ AFLAC◦ Hyatt Legal◦ Met-Life◦ MedAmerica

Re-enroll in FSA◦ Must make new election each plan year

Open Enrollment◦ April 21 – May 16

Items to Remember

32

Thank you and questions!