Embed Size (px)

Citation preview

20/04/23 by: Elena Dilara 1

CMBS and ServicingCMBS and Servicing

Hatfield Philips InternationalHatfield Philips InternationalAn LNR companyAn LNR company

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 22

What is CMBS ?What is CMBS ?

CMBS are bonds sold through the capital CMBS are bonds sold through the capital markets, whose payments are backed by markets, whose payments are backed by commercial loanscommercial loans

CMBS are a segment of structured finance CMBS are a segment of structured finance markets (or securitised markets)markets (or securitised markets)

Other segments: ABS, RMBS, CDO etc.Other segments: ABS, RMBS, CDO etc. CMBS are typically rated by one or more CMBS are typically rated by one or more

rating agencyrating agency

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 33

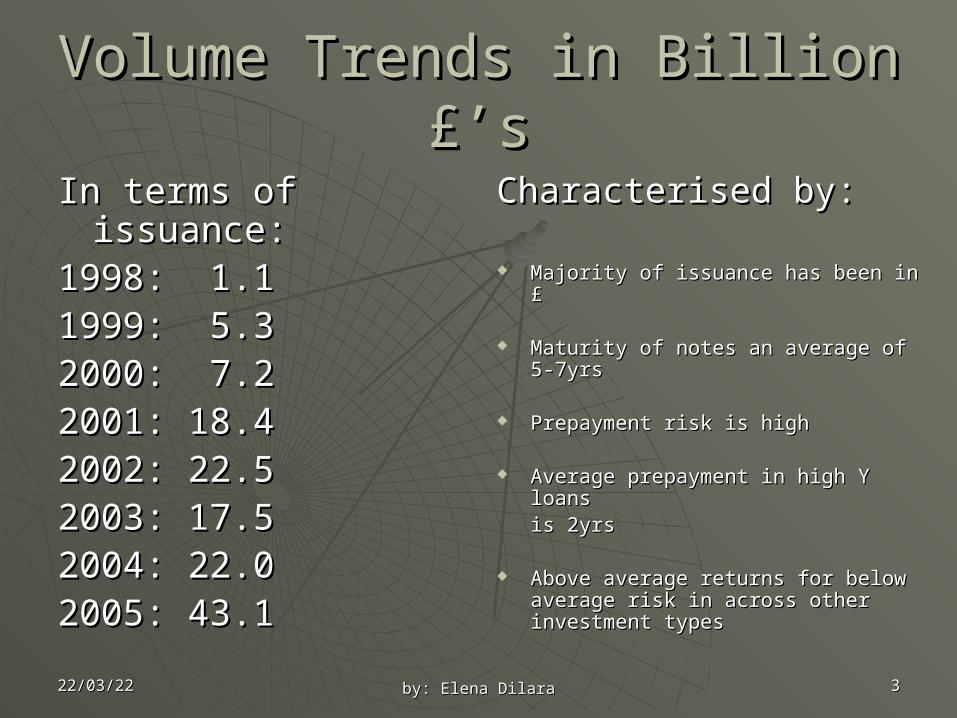

Volume Trends in Billion £’sVolume Trends in Billion £’s

In terms of issuance:In terms of issuance:1998: 1.11998: 1.11999: 5.31999: 5.32000: 7.22000: 7.22001: 18.42001: 18.42002: 22.52002: 22.52003: 17.52003: 17.52004: 22.02004: 22.02005: 43.12005: 43.1

Characterised by:Characterised by:

Majority of issuance has been in £Majority of issuance has been in £

Maturity of notes an average of 5-Maturity of notes an average of 5-7yrs7yrs

Prepayment risk is highPrepayment risk is high

Average prepayment in high Y loans Average prepayment in high Y loans is 2yrsis 2yrs

Above average returns for below Above average returns for below average risk in across other average risk in across other investment typesinvestment types

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 44

CMBS and un-Securitised Deal CMBS and un-Securitised Deal Volumes in U.S., U.K. and E.U.Volumes in U.S., U.K. and E.U.

U.S.A.U.S.A.40% - 60%40% - 60%

U.K.U.K.

25% -75%25% -75%

E.U.E.U.11% - 89%11% - 89%

More Growth in years to come !!!!!!!!!!!!!More Growth in years to come !!!!!!!!!!!!!

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 55

European 2005 Securitisation European 2005 Securitisation PlatformPlatform

CMBS:CMBS: 13.4%13.4% CDO’s: CDO’s: 14.4%14.4% ABS: ABS: 26.2%26.2% RMBS: RMBS: 46.0%46.0%

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 66

How does it work? How does it work?

Loan

Loan

Loan

Loan

TrustBonds

Pooled and transferred Issues bonds

Rated Bonds AAA to B-/B3

Rating Agenc’s

CMBS bonds bought by investors

Investors

Investors

Investors

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 77

The parties involvedThe parties involved OriginatorsOriginators Rating AgenciesRating Agencies Trustees Trustees (Note and Security)(Note and Security)

IssuerIssuer Swap Counter-partiesSwap Counter-parties InvestorsInvestors ServicersServicers Liquidity ProvidersLiquidity Providers Information Sources Information Sources (Bloomberg and TREPP)(Bloomberg and TREPP) Associations and FederationsAssociations and Federations

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 88

Rating agenciesRating agencies There will be a few as one and as many as four rating agenciesThere will be a few as one and as many as four rating agencies

They provide an OPINION onThey provide an OPINION onFULL and timely receipt of INTERESTFULL and timely receipt of INTERESTUltimate receipt of PRINCIPAL to Noteholders for each classUltimate receipt of PRINCIPAL to Noteholders for each class

Each have different methodologiesEach have different methodologies

Each use different modelsEach use different models

Assessment of RiskAssessment of RiskPROPERTY AS LOAN SECURITYPROPERTY AS LOAN SECURITYLOANLOANLOAN POOLLOAN POOLSTRUCTURE of NOTESSTRUCTURE of NOTES

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 99

Rating agencies Rating agencies DO NOT PROVIDE RECOMMENDATION to:DO NOT PROVIDE RECOMMENDATION to:

BuyBuy

SellSell

Hold securities or TradeHold securities or Trade

OnlyOnly Address CREDIT RISK Address CREDIT RISK

Not marketability / liquidity of NotesNot marketability / liquidity of Notes

Not advise on Prepayment risk and potential impact on Not advise on Prepayment risk and potential impact on Yield Yield to investorsto investors

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1010

Trustee and ServicerTrustee and Servicer Trustee

The trustee’s primary role is to hold all the loan documents and distribute The trustee’s primary role is to hold all the loan documents and distribute payments received from the master servicer to the bondholders. The payments received from the master servicer to the bondholders. The trustee typically delegates its authority to either the loan Servicer or the trustee typically delegates its authority to either the loan Servicer or the Master servicerMaster servicer

Master Servicer’s responsibilitiesservice the loan, service the loan, collect the payments from the borrower collect the payments from the borrower report on the performance of the loanreport on the performance of the loanmaintain all of the responsibilities and duties to the trust under maintain all of the responsibilities and duties to the trust under the PSA (Pooling and Servicing Agreement)the PSA (Pooling and Servicing Agreement)

Primary or Sub-servicerIn some cases the borrower may deal with the primary In some cases the borrower may deal with the primary

servicer that may also be the Originator / Mortgage Bankservicer that may also be the Originator / Mortgage Bank

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1111

ServicingServicing B-Piece buyer

The investor in the most subordinate bond classes is commonly The investor in the most subordinate bond classes is commonly referred to as “B piece buyer”. Given that losses come out from referred to as “B piece buyer”. Given that losses come out from lowest rated bonds, the PSA provides the Directing Certificate-holder lowest rated bonds, the PSA provides the Directing Certificate-holder the opportunity to play an active role in monitoring the performance the opportunity to play an active role in monitoring the performance of each loan, make decisions on key asset issues of each loan, make decisions on key asset issues and appoint and/or terminate the Special Servicerand appoint and/or terminate the Special Servicer..

Special ServicerUpon occurrence of certain specified events, primarily a default, Upon occurrence of certain specified events, primarily a default, the administration of the loan is transferred to special servicing. the administration of the loan is transferred to special servicing. The Borrower receives notification from the master or special The Borrower receives notification from the master or special servicer if its loan has been transferred to special servicing. servicer if its loan has been transferred to special servicing. The special servicer The special servicer must act to maximise the recovery of the must act to maximise the recovery of the loan to the bondholders by analysis of collection alternativesloan to the bondholders by analysis of collection alternatives, i.e. , i.e.

(loan modification, foreclosure, deed in lieu, negotiated payoff or (loan modification, foreclosure, deed in lieu, negotiated payoff or sale of the default loan) using NPV methodology.sale of the default loan) using NPV methodology.

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1212

Payment DistributionPayment Distribution

The master servicer is responsible for collecting payments from the borrower

Borrower

Bondholders

Special Servicer

Master Servicer

TrustThe trustee distributes payment received from the Master servicer. The trustee acts by and through either the Master servicer or the special servicer

Each month the interest received from all the pools loans is paid to investors

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1313

Types of CMBS TransactionsTypes of CMBS Transactions

Credit Tenant Lease TransactionsCredit Tenant Lease Transactions Single Borrower – Single PropertySingle Borrower – Single Property Single Borrower – Multiple PropertiesSingle Borrower – Multiple Properties Multiple Borrowers – Multiple Multiple Borrowers – Multiple

PropertiesProperties Synthetic CMBS TransactionsSynthetic CMBS Transactions Whole Business SecuritisationsWhole Business Securitisations

20/04/23 by: Elena Dilara 14

LEI and HPLEI and HP

LNR and Hatfield PhilipsLNR and Hatfield Philips

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1515

LEI LEI

LEI is a pan-European real estate private equity investment vehicle, whose primary purpose is to evaluate, make and actively manage investments in real estate related debt instruments and securities.

Who’s Who? Equity InvestmentLNR Holdings £180,000,000 50%PSP £ 75,000,000 21%Teachers Insurance £ 15,000,000 4%Bank of America £ 15,000,000 4%ABP £ 75,000,000 21%

Total equity investment is £360,000,000

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1616

BREAKDOWN OF INVESTABLE FUNDS

Investor Equity £360,000,000

Fund Leverage 55%

Investable Funds £800,000,000

WHAT DOES LEI INVEST IN CMBS, Subordinate Notes, Mezzanine Debt, NPLs, R/E Equity

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1717

LEI Investment Breakdown by Deal TypeLEI Investment Breakdown by Deal Type

LEI Fund Investments by Deal Type

CMBS47%

B Notes34%

Mezzanine Loans19%

CMBS B Notes Mezzanine Loans

CMBS 47%CMBS 47%Bonds collateralised by a pool of 1Bonds collateralised by a pool of 1stst charge charge mortgages on commercial real estatemortgages on commercial real estate

Subordinate Notes 34%Subordinate Notes 34%Secured note collateralised by a Secured note collateralised by a subordinate position in a 1subordinate position in a 1stst charge charge mortgage on commercial real estatemortgage on commercial real estate

Mezzanine Debt 19%Mezzanine Debt 19%Loan to a real estate holding company Loan to a real estate holding company secured by a second mortgage or a pledge secured by a second mortgage or a pledge of the shares of the holding companyof the shares of the holding company

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1818

Deal Breakdown by Property Type Deal Breakdown by Property Type and Jurisdictionand Jurisdiction

LEI Fund Investments by Jurisdiction

UK43%

Germany19%

Sw itzerland16%

France3%

Netherlands19%

UK Germany Sw itzerland France Netherlands

LEI Fund Investments by Property Type

Office/Industrial6%

Office31%

Retail21%

Mixed Use24%

Multifamily15%

Hotel3%

Office/Industrial Off ice Retail Mixed Use Multifamily Hotel

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 1919

Hatfield Philips historyHatfield Philips history

PTG - LehmanPTG - Lehman Securitisation - other OriginatorsSecuritisation - other Originators Investor Reporting Investor Reporting Special ServicingSpecial Servicing

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 2020

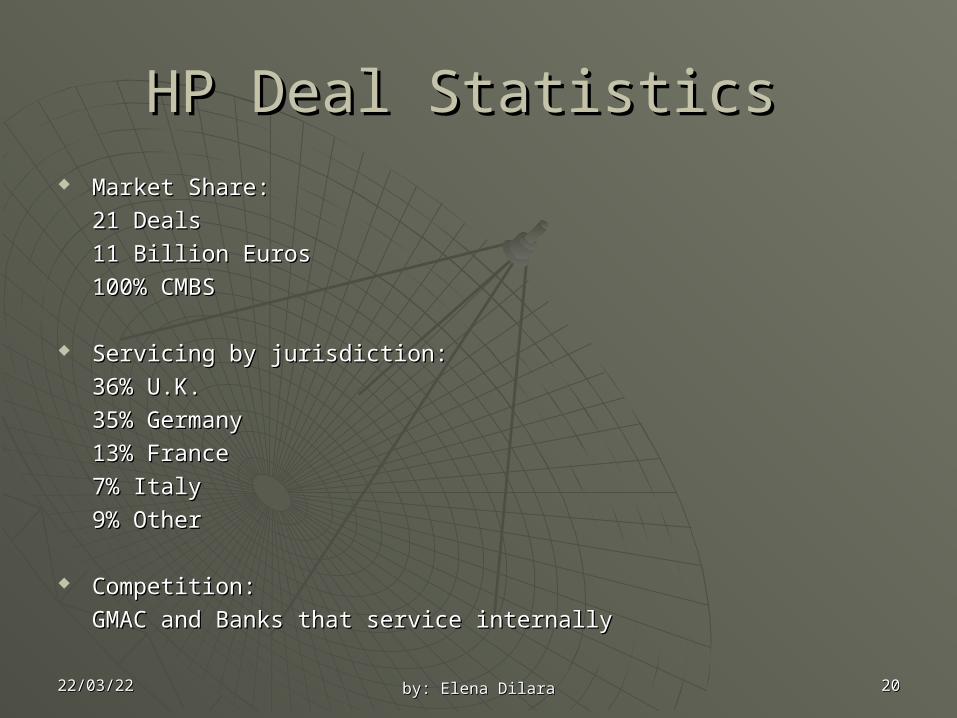

HP Deal Statistics HP Deal Statistics Market Share:Market Share:

21 Deals21 Deals

11 Billion Euros11 Billion Euros

100% CMBS100% CMBS

Servicing by jurisdiction: Servicing by jurisdiction:

36% U.K.36% U.K.

35% Germany35% Germany

13% France13% France

7% Italy7% Italy

9% Other9% Other

Competition:Competition:

GMAC and Banks that service internallyGMAC and Banks that service internally

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 2121

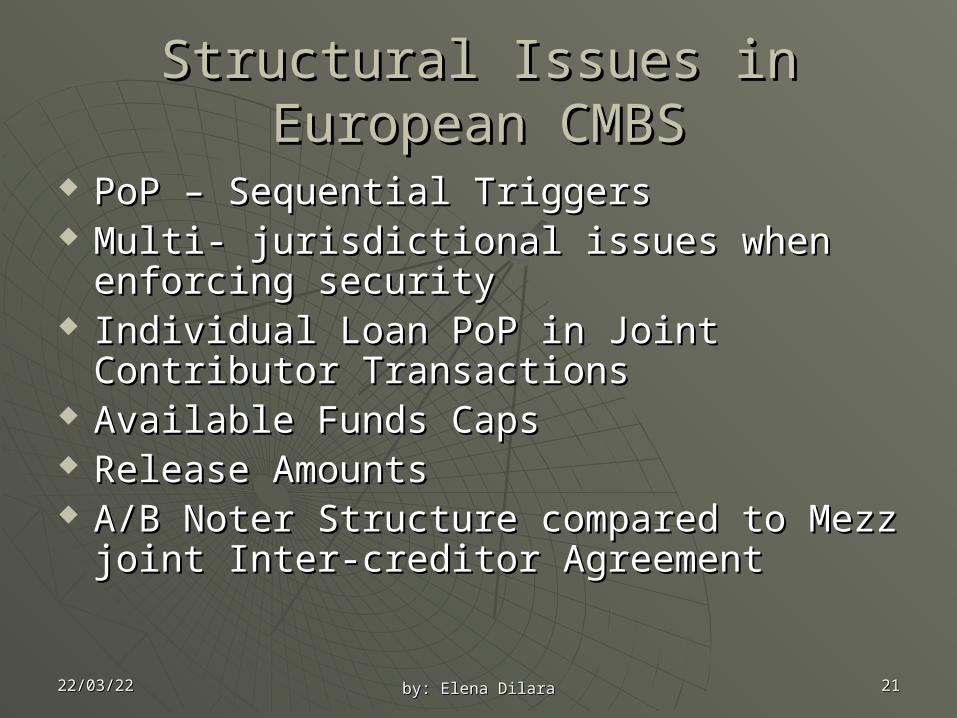

Structural Issues in European Structural Issues in European CMBSCMBS

PoP – Sequential TriggersPoP – Sequential Triggers Multi- jurisdictional issues when enforcing Multi- jurisdictional issues when enforcing

securitysecurity Individual Loan PoP in Joint Contributor Individual Loan PoP in Joint Contributor

TransactionsTransactions Available Funds CapsAvailable Funds Caps Release AmountsRelease Amounts A/B Noter Structure compared to Mezz A/B Noter Structure compared to Mezz

joint Inter-creditor Agreementjoint Inter-creditor Agreement

20/04/2320/04/23 by: Elena Dilaraby: Elena Dilara 2222

Servicing IssuesServicing Issues

Transparency Transparency timely presentation of information so it can be timely presentation of information so it can be communicated evenly across the market as is super sensitive when it communicated evenly across the market as is super sensitive when it comes to pricingcomes to pricing

Originator - Servicer- B piece holder Originator - Servicer- B piece holder underwriting models, servicer reports, special servicingunderwriting models, servicer reports, special servicing

Guidelines in Reporting CMSA Guidelines in Reporting CMSA Value added reporting Value added reporting Covenant complianceCovenant compliance Notification periodsNotification periods for Prepayments or Watchlistsfor Prepayments or Watchlists Special ServicingSpecial Servicing