Embed Size (px)

Citation preview

NEW ISSUE NO RATING Book-Entry Only

In the opinion of Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, subject, however

to certain qualifications described herein, under existing law, the interest on the Bonds is excluded from gross income for federal income tax purposes, such interest is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations, although for the purpose of computing the alternative minimum tax imposed on certain corporations, such interest is taken into account in determining certain income and earnings. In the further opinion of Bond Counsel, such interest is exempt from California personal income taxes. See “OTHER MATTERS - Tax Matters”.

$16,085,000 Redevelopment Agency For the City of Goleta

Goleta Old Town Redevelopment Project 2011 Tax Allocation Bonds

Dated: Date of Delivery Due: December 1 and June 1,, as shown on inside cover

The captioned 2011 Tax Allocation Bonds (the “Bonds”) are being issued by the Redevelopment Agency For the City of Goleta (the “Agency”) pursuant to the California Community Redevelopment Law, constituting Part 1, Division 24 (commencing with Section 33000) of the California Health and Safety Code (the “Redevelopment Law”) and an Indenture of Trust dated as of March 1, 2011 (the “Indenture”), by and between the Agency and The Bank of New York Mellon Trust Company, N.A., as trustee (the “Trustee”). The Bonds are being issued to finance redevelopment activities with respect to the Agency’s Goleta Old Town Redevelopment Project (the ”Project Area”). The Bonds are special obligations of the Agency and are payable from Tax Revenues, consisting primarily of tax increment derived from property in the Project Area and allocated and paid to the Agency pursuant to the Redevelopment Law. No funds or properties of the Agency, other than the Tax Revenues, are pledged to secure the Bonds.

The Bonds are being issued in fully registered form, and when issued, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company (“DTC”), New York, New York. DTC will act as securities depository for the Bonds. Individual purchases of the Bonds may be made in book-entry form only, in denominations of $5,000. Purchasers of interests in the Bonds will not receive certificates representing their interest in the Bonds purchased.

Interest on the Bonds will be payable semiannually on June 1 and December 1 of each year, commencing December 1, 2011. Payments of principal, and interest on the Bonds will be payable by the Trustee to DTC, which is obligated in turn to remit such principal, and interest to the DTC Participants for subsequent disbursement to the Beneficial Owners of the Bonds, as more fully described herein.

The Bonds are subject to optional and mandatory redemption prior to maturity. See “THE BONDS — Redemption of the Bonds”.

The Bonds are not a debt, liability or obligation of the City of Goleta, the County of Santa Barbara, the State of California, or any of its political subdivisions other than the Agency, and neither the City, the County, the State nor any of its political subdivisions, other than the Agency, is therefore liable to pay the principal of, and interest on the Bonds . The principal of, and interest on the Bonds are payable solely from Tax Revenues allocated and paid to the Agency from the Project Area and amounts in certain funds and accounts held under the Indenture. Neither the Agency, the City nor any persons executing the Bonds are liable personally on the Bonds by reason of their issuance.

This cover page contains certain information for general reference only. It is not intended to be a summary of the security or terms of this issue. Investors are advised to read the entire Official Statement to obtain information essential to the making of an informed investment decision. Capitalized terms used and not defined on this cover page shall have the meanings set forth in this Official Statement. For a discussion of some of the risks associated with a purchase of the Bonds, including certain State of California proposals regarding the elimination of redevelopment agencies, see “RISK FACTORS”.

MATURITY SCHEDULE (See inside cover)

The Bonds are offered, when, as and if issued by the Underwriter, subject to approval as to their legality by Jones Hall, A Professional Law Corporation, San Francisco, California, Bond Counsel, and to certain other conditions. Jones Hall will also serve as Disclosure Counsel to the Agency. Certain matters will be passed on for the Agency by Tim W. Giles, City Attorney. It is anticipated that the Bonds in book-entry form will be available for delivery through the DTC book-entry system in New York, New York on or about March 8, 2011.

Dated: March 3, 2011

MATURITY SCHEDULE

BASE CUSIP : 381589

$2,155,000 Serial Bonds

Maturity Date (December 1)

Principal Amount

Interest Rate

Yield

Price

CUSIP†

2011 $ 420,000 2.500% 2.500% 100.000 AD2 2012 140,000 3.000 3.000 100.000 AE0 2013 145,000 4.000 4.000 100.000 AF7 2014 150,000 4.500 4.750 99.147 AG5 2015 155,000 5.250 5.500 98.962 AH3 2016 165,000 5.500 5.750 98.784 AJ9 2017 175,000 5.750 6.000 98.621 AK6 2018 185,000 6.000 6.250 98.474 AL4 2019 195,000 6.250 6.500 98.341 AM2 2020 205,000 6.500 6.750 98.224 AN0 2021 220,000 6.750 7.000 98.121 AP5

$1,365,000 7.500% Term Bonds due December 1, 2026; Yield: 7.650%; CUSIP†: AQ3

$1,970,000 7.750% Term Bonds due December 1, 2031; Yield: 7.900%; CUSIP†: AR1

$10,595,000 8.000% Term Bonds due June 1, 2044; Yield: 8.150%; CUSIP†: AT7

† Copyright 2011, American Bankers Association. CUSIP data are provided by Standard & Poor's CUSIP Service

Bureau, a division of The McGraw-Hill Companies, Inc., and are provided for convenience of reference only. Neither the Agency nor the Underwriter assumes any responsibility for the accuracy of these CUSIP data.

THE REDEVELOPMENT AGENCY FOR THE CITY OF GOLETA

AGENCY BOARD AND CITY COUNCIL

Margaret Connell, Agency Chair and Mayor Ed Easton, Agency Vice Chair and Mayor Pro Tem

Roger S. Aceves, Agency Member and Councilmember Michael T. Bennett, Agency Member and Councilmember

Paula Perotte, Agency Member and Councilmember

AGENCY AND/OR CITY STAFF

Daniel Singer, Agency Executive Director/City Manager Vyto Adomaitis, Director of Redevelopment and Neighborhood Services

Alvertina “Tina” Rivera, Agency Treasurer/City Director of Finance Steve Wagner, Community Services Director and City Engineer

SPECIAL SERVICES

Bond Counsel and Disclosure Counsel

Jones Hall, A Professional Law Corporation

San Francisco, California

Agency Counsel

Tim W. Giles, City Attorney/ Agency Counsel Goleta, California

Fiscal Consultant

Rosenow Spevacek Group, Inc. Santa Ana, California

Trustee

The Bank of New York Mellon Trust Company, N.A.

Los Angeles, California

GENERAL INFORMATION ABOUT THIS OFFICIAL STATEMENT

Use of Official Statement. This Official Statement is submitted in connection with the offer and sale of the Bonds referred to in this Official Statement and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not to be construed as a contract with the purchasers of the Bonds.

Estimates and Forecasts. When used in this Official Statement and in any continuing disclosure by the Agency in any press release and in any oral statement made with the approval of an authorized officer of the Agency or any other entity described or referenced herein, the words or phrases “will likely result,” “are expected to”, “will continue”, “is anticipated”, “estimate”, “project,” “forecast”, “expect”, “intend” and similar expressions identify “forward looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results, and those differences may be material. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, give rise to any implication that there has been no change in the affairs of the Agency or any other entity described or referenced herein since the date hereof.

Limit of Offering. No dealer, broker, salesperson or other person has been authorized by the Agency to give any information or to make any representations in connection with the offer or sale of the Bonds other than those contained herein and if given or made, such other information or representation must not be relied upon as having been authorized by the Agency or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

Involvement of Underwriter. The Underwriter has provided the following sentence for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with and as part of its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information.

Stabilization of Prices. In connection with this offering, the Underwriter may overallot or effect transactions which stabilize or maintain the market price of the Bonds at a level above that which might otherwise prevail in the open market. Such stabilizing, if commenced, may be discontinued at any time. The Underwriter may offer and sell the Bonds to certain dealers and others at prices lower than the public offering prices set forth on the cover page hereof and said public offering prices may be changed from time to time by the Underwriter.

THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXCEPTION FROM THE REGISTRATION REQUIREMENTS CONTAINED IN SUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE.

-i-

TABLE OF CONTENTS

INTRODUCTION.......................................................1 PLAN OF FINANCE ..................................................3 Proposed Projects ...................................................3 Estimated Sources and Used of Funds ...................4 Annual Debt Service Requirements of the Bonds ...5

THE BONDS .............................................................6 General ....................................................................6 Redemption of the Bonds ........................................6

SECURITY FOR THE BONDS..................................9 Tax Allocation Financing..........................................9 Allocation of Taxes ..................................................9 Pledge Under the Indenture...................................10 Funds Under the Indenture....................................11 Issuance of Additional Parity Debt.........................13 Issuance of Subordinate Debt ...............................14 Certain Limitations in the Redevelopment Plan.....14

Tax Sharing Statutes...............................................14 THE REDEVELOPMENT AGENCY .................................................................15 General ..................................................................15 Management of the Agency...................................16

THE PROJECT AREA.............................................18 Land Use ...............................................................18 Assessed Value Information ..................................20 New Development .................................................23 Property Transfers .................................................23 Appeals to Assessed Value...................................23 Outstanding Indebtedness of the Agency..............24 Projected Tax Revenues .......................................24 Projected Debt Service Coverage .........................26

RISK FACTORS......................................................28 Reduction in Taxable Value - Economic Factors and Property Damage............................................28 Recent Downturn in Residential and Other Values28

Reduction in Inflation Rate .................................... 28 Concentration of Ownership.................................. 29 Real Estate and Development Risks..................... 29 Levy and Collection of Taxes ................................ 30 State Budget Deficit; ERAF; SERAF..................... 30 Investment Risk..................................................... 37 Bankruptcy ............................................................ 37 Change in Law ...................................................... 38 Assumptions and Projections................................ 38 Risk of Earthquake and other Hazards ................. 38

STATUTORY LIMITATIONS ON TAX REVENUES ............................................................ 39 Property Tax Limitations: Article XIII A of the California Constitution ........................................... 39 Implementing Legislation ...................................... 39 Challenges to Article XIII ....................................... 40 Property Tax Collection Procedures ..................... 40 Teeter Plan............................................................ 41 Unitary Property .................................................... 42 Exclusion of Tax Revenues for General Obligation Bonds Debt Service .............................................. 42 Certification of Agency Indebtedness.................... 42 Appropriations Limitations: Article XIII B of the California Constitution ........................................... 43

OTHER MATTERS ................................................. 44 Litigation................................................................ 44 Rating.................................................................... 44 Tax Matters ........................................................... 44 Certain Legal Matters ............................................ 45 Underwriting .......................................................... 45 The Goleta Financing Authority............................. 45 Professionals Involved in the Offering................... 45 Miscellaneous ....................................................... 46

APPENDIX A Fiscal Consultant’s Report APPENDIX B Audited Financial Statements of the Agency For Fiscal Year Ended June 30, 2010 APPENDIX C General Information About the City of Goleta and Santa Barbara County APPENDIX D Summary of Certain Provisions of the Indenture APPENDIX E The Book-Entry System APPENDIX F Form of Opinion of Bond Counsel APPENDIX G Form of Continuing Disclosure Certificate

[THIS PAGE INTENTIONALLY LEFT BLANK]

-1-

$16,085,000 Redevelopment Agency For the City of Goleta

Goleta Old Town Redevelopment Project 2011 Tax Allocation Bonds

INTRODUCTION

This Introduction contains a brief summary of information contained in this Official Statement. It is not intended to be complete and is qualified by the more detailed information contained elsewhere in this Official Statement. Definitions of certain terms used in this Official Statement are set forth in “APPENDIX D SUMMARY OF CERTAIN PROVISIONS OF THE INDENTURE”.

Authority for Issuance. The Agency is a redevelopment agency existing under the

Community Redevelopment Law of the State of California (the “State”), constituting Part 1 of Division 24 (commencing with Section 33000) of the California Health and Safety Code, as amended (the “Redevelopment Law”). The Bonds are being issued under the Redevelopment Law and pursuant to an Indenture of Trust (the “Indenture”), dated as of March 1, 2011, by and between the Agency and The Bank of New York Mellon Trust Company, N.A., as trustee (the “Trustee”). The Bonds are being issued for sale to the Goleta Financing Authority (the “Authority”) pursuant to the Marks-Roos Local Bond Pooling Act of 1985, constituting Article 4 of Chapter 5 of Division 7 of Title 1 (commencing with Section 6584) of the California Government Code (the “JPA Law”). The Bonds purchased by the Authority will be resold concurrently to Stone & Youngberg LLC, the Underwriter.

Use of Proceeds. The proceeds of the Bonds will be applied by the Agency to (i)

construct and acquire certain capital improvements of benefit to the Agency’s Project Area, (ii) fund a reserve fund for the Bonds and (iii) pay costs of issuance. See “PLAN OF FINANCE.”

Security for the Bonds. The Bonds will be payable from and secured by Tax Revenues

allocated and paid to the Agency from the Project Area, as described below. In California, the financing and refinancing of redevelopment projects may be provided

by the issuance of tax allocation bonds. Such bonds are payable from property taxes collected within a redevelopment project area attributable to the increase in assessed valuation of property therein, as explained in greater detail below. The Bonds are payable from and secured by tax increment revenues of the Agency constituting Tax Revenues generated from property in the Project Area. The term Tax Revenues is defined in the Indenture and generally includes a portion of ad valorem property taxes attributable to increases in the assessed valuation of property (except public property and property exempt from taxation) in the Project Area over that shown on the assessment rolls for the adjusted base year assessment roll. Such taxes are eligible for allocation to the Agency pursuant to the Redevelopment Law to repay loans, advances and indebtedness incurred in connection with the Project Area. Tax Revenues are more fully described under the caption “SECURITY FOR THE BONDS – Allocation of Taxes”.

Pursuant to the Redevelopment Law, other taxing agencies receive statutory tax sharing

-2-

payments aggregating approximately 20% of the tax increment revenues from the Project Area. Such amounts are paid to the taxing agencies on a basis senior to the payment of debt service on the Bonds. See “ SECURITY FOR THE BONDS - Tax Sharing Statutes.”

On the date of issuance of the Bonds, the Agency is required under the Indenture to

deposit the amount of $1,340,400.00 (the “Reserve Requirement”) into the Reserve Account held under the Indenture. See “SECURITY FOR THE BONDS – Funds Held Under the Indenture - Reserve Account”.

Risk Factors. Any future decrease in the taxable valuation in the Project Area or in the

applicable tax rates could reduce the Tax Revenues allocated to the Agency and correspondingly could have an adverse impact on the ability of the Agency to pay debt service on the Bonds. See “RISK FACTORS”. In addition, certain State of California budget proposals regarding the elimination of redevelopment agencies could adversely impact the Agency and its projects, See “RISK FACTORS - State Budget Deficit; ERAF; SERAF”.

The Agency and the Project Area. The Agency was activated on February 1, 2002, by

the City Council of the City of Goleta (the “City”) pursuant to the Redevelopment Law. For further information with respect to the Agency, see “THE REDEVELOPMENT AGENCY”.

The Redevelopment Plan for the Goleta Old Town Redevelopment Project (the “Project

Area”) was originally adopted by the County of Santa Barbara (the “County”) on June 16, 1998. The City assumed control of the Redevelopment Plan of the Project Area after the City incorporated in 2002. The Project Area encompasses approximately 595 acres and consists of industrial, residential, commercial, and agricultural lands. For information concerning the Agency’s Project Area, see “THE PROJECT AREA”.

In connection with the issuance of the Bonds, the Agency has engaged Rosenow

Spevacek Group, Inc., Santa Ana, California (the “Fiscal Consultant”) to prepare a Fiscal Consultant Report dated February 22, 2011. See “APPENDIX A – Fiscal Consultant’s Report”.

Continuing Disclosure. The Agency will undertake all responsibilities for continuing

disclosure to Owners of the Bonds as described below. The Agency has covenanted in the Indenture and in a Continuing Disclosure Certificate to prepare and deliver an annual report to the Municipal Securities Rule-making Board, and to provide certain other information. The specific nature of the information to be contained in the Annual Report or the notices of listed events is described in “APPENDIX G – Form of Continuing Disclosure Certificate.” These covenants have been made in order to assist the Underwriter in complying with S.E.C. Rule 15c2-12(b)(5). The Bonds are the first obligations of the Agency subject to such Rule.

Miscellaneous. There follows in this Official Statement, which includes the cover page

and Appendices hereto, a brief description of the Bonds, the Agency, Tax Revenues, the Project Area, security for the Bonds, risk factors and limitations on Tax Revenues and certain other information relevant to the issuance of the Bonds. All references to the Indenture are qualified n their entirety by reference to the definitive form thereof, all references to the Bonds are further qualified by references to the information with respect thereto contained in the Indenture. A summary of certain provisions of the Indenture is included in APPENDIX D. The audited financial statements of the Agency for fiscal year 2009-10 are included in APPENDIX B. The information set forth in this Official Statement and in the Appendices has been furnished by the Agency and includes information which has been obtained from other sources which are believed to be reliable but is not guaranteed as to accuracy or completeness and is not to be

-3-

construed as a representation by the Underwriter. All capitalized terms used and not normally capitalized have the meanings assigned in the Indenture, unless otherwise stated in this Official Statement.

The information and expressions of opinion in this Official Statement speak only as of

the date of this Official Statement and are subject to change without notice. Neither delivery of this Official Statement nor any sale made hereunder nor any future use of this Official Statement shall, under any circumstances, create any implication that there has been no change in the affairs of the Agency since the date of this Official Statement.

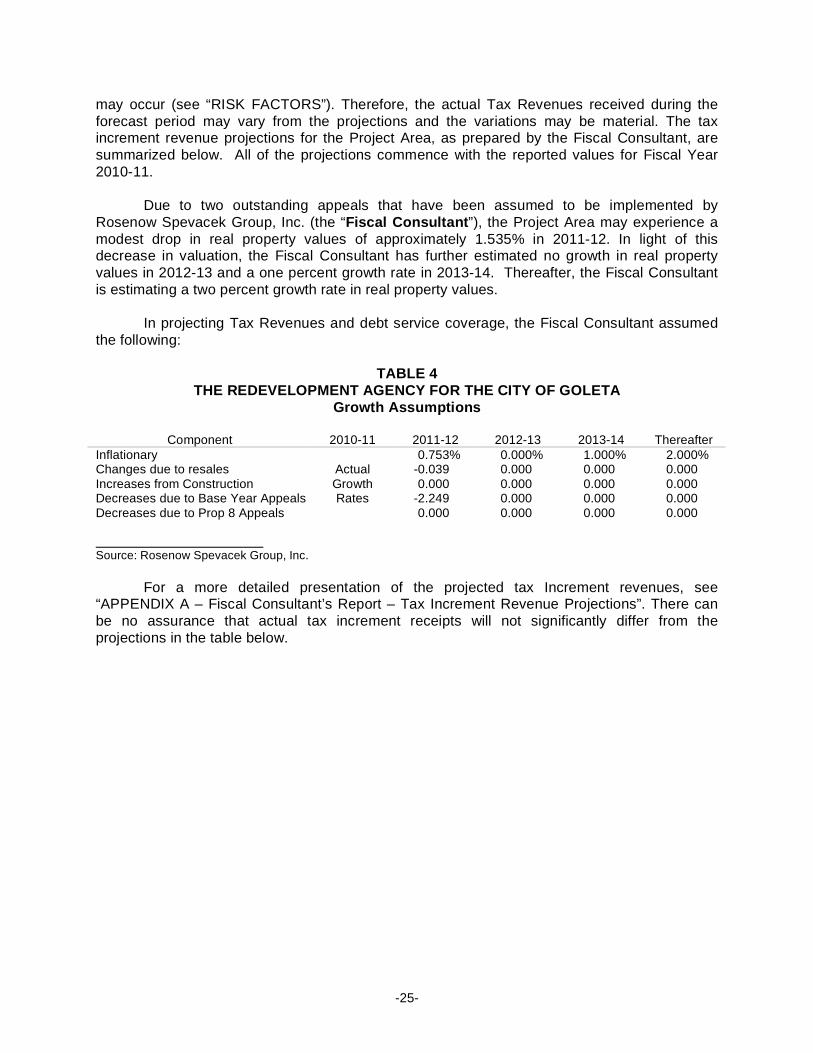

PLAN OF FINANCE

The Bonds are being issued to provide a portion of the funds needed to (i) provide

moneys to finance redevelopment activities of the Agency relating to the Project Area, (ii) fund a reserve fund for the Bonds, and (iii) pay costs of issuance of the Bonds.

Proposed Projects

The net proceeds of the Bonds will be used for some or all of the following projects. The actual timing and scope of the projects are in the planning stages and cannot be guaranteed. It is possible that one or more of the projects described below may not occur. The Agency, consistent with the Redevelopment Law, may substitute other projects for the projects described below.

San Jose Creek Channel Improvement. The San Jose Creek Capacity Improvement

Project will increase the capacity of the channel and decrease the likelihood of flooding in the downtown Goleta area along Hollister Avenue. The current capacity of San Jose Creek Channel is insufficient to accommodate a 100 year flood storm event. As a result, during lesser events, flood waters have traditionally broken out at Hollister Bridge and caused significant flooding damage in Goleta Old Town. The project includes replacing the existing Hollister Avenue Bridge over San Jose Creek, and replacing the existing 4,250 foot long channel with a wider channel with an articulated concrete revetment bottom with an internal fish passage channel.

Ekwill/Fowler Road Extension. The Ekwill/Fowler Road Extension Project is designed

to decrease traffic in downtown Goleta by creating alternative routes to the South of Hollister Avenue. The new streets will span from Kellogg Avenue to Fairview Avenue, contain two lanes with left turn pockets, Class II bikeways, and sidewalks. The project will also install two roundabouts on Hollister Avenue east and west of SR 217. This project will relieve regional congestion, improve traffic circulation in Goleta Old Town, and improve access within Goleta Old Town and to the airport.

Hollister Avenue Reconstruction. The purpose of the Hollister Avenue Reconstruction

Project is to create a more efficient flow of traffic, improve drainage, make sidewalk and parking improvements, accommodation of alternative transportation, enhance safety lighting and add visual appeal to the area with the addition of landscaped medians, sidewalk amenities and other landscaping which will increase the overall appeal of the area and draw new customers to local businesses. The Hollister Corridor experiences major traffic congestion due to a number of factors: local and regional through traffic, driveways along Hollister Avenue that have poor visibility, and on-street parking that slows drivers in the right lane due to safety concerns for

-4-

persons exiting parking vehicles.

Estimated Sources and Used of Funds

Set forth below are the estimated sources and uses of proceeds of the Bonds.

Sources: Par Amount of Bonds $16,085,000.00 Original Issue Discount (253,615.20) TOTAL SOURCES: $15,831,384.80 Uses: Deposit to Redevelopment Fund $14,082,472.30 Deposit to Reserve Account 1,340,400.00 Underwriter’s Discount 262,512.50 Costs of Issuance (1) 146,000.00 TOTAL USES: $15,831,384.80

_____________________

(1) Includes legal fees, fiscal consultant fees, printing, expenses, and other issuance costs.

-5-

Annual Debt Service Requirements of the Bonds

The following table provides the annual debt service requirements of the Bonds.

Year (Ending December 1)

Principal

Interest

Total

2011 $ 420,000 $ 882,976.84 $ 1,302,976.84 2012 140,000 1,198,137.50 1,338,137.50 2013 145,000 1,193,937.50 1,338,937.50 2014 150,000 1,188,137.50 1,338,137.50 2015 155,000 1,181,387.50 1,336,387.50 2016 165,000 1,173,250.00 1,338,250.00 2017 175,000 1,164,175.00 1,339,175.00 2018 185,000 1,154,112.50 1,339,112.50 2019 195,000 1,143,012.50 1,338,012.50 2020 205,000 1,130,825.00 1,335,825.00 2021 220,000 1,117,500.00 1,337,500.00 2022 235,000 1,102,650.00 1,337,650.00 2023 255,000 1,085,025.00 1,340,025.00 2024 270,000 1,065,900.00 1,335,900.00 2025 290,000 1,045,650.00 1,335,650.00 2026 315,000 1,023,900.00 1,338,900.00 2027 340,000 1,000,275.00 1,340,275.00 2028 365,000 973,925.00 1,338,925.00 2029 390,000 945,637.50 1,335,637.50 2030 420,000 915,412.50 1,335,412.50 2031 455,000 882,862.50 1,337,862.50 2032 490,000 847,600.00 1,337,600.00 2033 530,000 808,400.00 1,338,400.00 2034 570,000 766,000.00 1,336,000.00 2035 620,000 720,400.00 1,340,400.00 2036 665,000 670,800.00 1,335,800.00 2037 720,000 617,600.00 1,337,600.00 2038 780,000 560,000.00 1,340,000.00 2039 840,000 497,600.00 1,337,600.00 2040 910,000 430,400.00 1,340,400.00 2041 980,000 357,600.00 1,337,600.00 2042 1,060,000 279,200.00 1,339,200.00 2043 1,145,000 194,400.00 1,339,400.00 2044* 1,285,000 51,400.00 1,336,400.00 Total $16,085,000 $29,370,089.34 $45,455,089.34

* Final Sinking Fund Payment / Maturity will be on June 1, 2044

-6-

THE BONDS General

The Bonds will be issued as fully registered bonds, and when issued, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”), as securities depository for the Bonds. Individual purchases of the Bonds will be made in book-entry form only. The Bonds will be issued in denominations of $5,000. The Bonds will be issued in the principal amounts, will be dated and will bear interest at the rates and mature on the dates and in the amounts set forth on the inside cover page of this Official Statement.

Interest on the Bonds is payable commencing December 1, 2011, and semiannually

thereafter on each June 1 and December 1 (each an “Interest Payment Date”). Interest will be calculated on the basis of a 360-day year composed of twelve 30-day months. Principal, and interest on the Bonds are payable by the Trustee to DTC, which is obligated in turn to remit such amounts to DTC Participants for subsequent disbursement to Beneficial Owners of the Bonds. See APPENDIX E - “The Book-Entry System”.

Redemption of the Bonds*

Optional Redemption. The Bonds maturing on or before December 1, 2016 are not subject to optional redemption. The Bonds maturing on and after December 1, 2017, are subject to redemption, at the option of the Agency on any date on or after December 1, 2016, as a whole or in part, by such maturities as shall be determined by the Agency, and by lot within a maturity, from any available source of funds, at a redemption price equal to the par amount of the Bonds being so redeemed, without premium, together with accrued interest to the date fixed for redemption.

Mandatory Sinking Account Redemption. The Bonds maturing on December 1,

2026, December 1, 2031 and on June 1, 2044 are also subject to mandatory redemption in part by lot on December 1 (or June 1, if applicable) in each year, as shown below from Sinking Account payments made by the Agency at a redemption price equal to the principal amount thereof to be redeemed together with accrued interest thereon to the redemption date, without premium, or in lieu thereof shall be purchased in whole or in part as described below, in the aggregate respective principal amounts and on the respective dates as set forth in the following table; provided, however, that if some but not all of the Bonds have been redeemed pursuant to optional redemption as described above, the total amount of all future Sinking Account payments shall be reduced by the aggregate principal amount of Bonds so redeemed, to be allocated among the applicable Sinking Account payments as are thereafter payable on a pro rata basis in integral multiples of $5,000 as determined by the Agency (notice of which determination shall be given by the Agency to the Trustee).

-7-

$1,365,000 Bonds Maturing December 1, 2026

Sinking Account Redemption Date

Principal Amount To Be Redeemed or Purchased

12/01/2022 $235,000 12/01/2023 255,000 12/01/2024 270,000 12/01/2025 290,000 12/01/2026 (Maturity) 315,000

$1,970,000 Bonds Maturing December 1, 2031

Sinking Account

Redemption Date Principal Amount To Be

Redeemed or Purchased

12/01/2027 $340,000 12/01/2028 365,000 12/01/2029 390,000 12/01/2030 420,000 12/01/2031 (Maturity) 455,000

$10,595,000 Bonds Maturing June 1, 2044

Sinking Account

Redemption Date Principal Amount To Be

Redeemed or Purchased

12/01/2032 $ 490,000 12/01/2033 530,000 12/01/2034 570,000 12/01/2035 620,000 12/01/2036 665,000 12/01/2037 720,000 12/01/2038 780,000 12/01/2039 840,000 12/01/2040 910,000 12/01/2041 980,000 12/01/2042 1,060,000 12/01/2043 1,145,000 6/01/2044 (Maturity) 1,285,000

In lieu of mandatory Sinking Account redemption of Bonds as described above, amounts

on deposit as Sinking Account payments may also be used and withdrawn by the Trustee, at the written direction of the Agency, at any time for the purchase of Bonds otherwise required to be redeemed on the following December 1 (or June 1, if applicable) at public or private sale as and when and at such prices (including brokerage and other charges and including accrued interest) as the Agency may in its discretion determine. The par amount of any of the Bonds so purchased by the Agency and surrendered to the Trustee for cancellation in any twelve-month period ending on July 1 in any year shall be credited towards and shall reduce the par amount of the Bonds otherwise required to be redeemed on the following December 1 (or June 1, if applicable) pursuant to mandatory Sinking Account redemption.

-8-

Notice of Redemption; Rescission. The Trustee on behalf and at the expense of the Agency will mail (by first class mail, postage prepaid) notice of any redemption at least 30 but not more than 60 days prior to the redemption date, to (i) to the Owners of any Bonds designated for redemption at their respective addresses appearing on the Registration Books, and (ii) the Securities Depositories and to one or more Information Services designated in a Written Request of the Agency filed with the Trustee; but such mailing is a condition precedent to such redemption and neither failure to receive any such notice nor any defect therein will affect the validity of the proceedings for the redemption of such Bonds or the cessation of the accrual of interest thereon. Such notice will state the redemption date and the redemption price, will state that such redemption is conditioned upon the timely delivery of the redemption price by the Agency to the Trustee for deposit in the Redemption Account, will designate the CUSIP number of the Bonds to be redeemed, shall state the individual number of each Bond to be redeemed or will state that all Bonds between two stated numbers (both inclusive) or all of the Bonds Outstanding are to be redeemed, and shall require that such Bonds be then surrendered at the Principal Corporate Trust Office of the Trustee for redemption at the redemption price, giving notice also that further interest on such Bonds will not accrue from and after the redemption date.

The Agency has the right to rescind any optional redemption by written notice to the

Trustee on or prior to the date fixed for redemption. Any such notice of optional redemption will be canceled and annulled if for any reason funds will not be or are not available on the date fixed for redemption for the payment in full of the Bonds then called for redemption, and such cancellation will not constitute an Event of Default under the Indenture. The Agency and the Trustee will have no liability to the Owners or any other party related to or arising from such rescission of redemption. The Trustee will mail notice of such rescission of redemption in the same manner as the original notice of redemption was sent.

From and after the date fixed for redemption, if funds available for the payment of the

redemption price of and interest on the Bonds so called for redemption have been duly deposited with the Trustee, such Bonds so called will cease to be entitled to any benefit under the Indenture other than the right to receive payment of the redemption price and accrued interest to the redemption date, and no interest will accrue on the Bonds from and after the redemption date specified in such notice.

Manner of Redemption. Whenever all or any portion of the Bonds are to be selected

for redemption by lot, the Trustee will make such selection, in such manner as the Trustee deems appropriate, and shall notify the Agency thereof to the extent Bonds are no longer held in book-entry form. In the event of redemption by lot of Bonds, the Trustee will assign to each Bond then Outstanding a distinctive number for each $5,000 of the principal amount of each such Bond. The Bonds to be redeemed will be the Bonds to which were assigned numbers so selected, but only so much of the principal amount of each such Bond of a denomination of more than $5,000 will be redeemed as equals $5,000 for each number assigned to it and so selected.

-9-

SECURITY FOR THE BONDS

Tax Allocation Financing

The Redevelopment Law generally provides a means for financing redevelopment projects based upon an allocation of taxes collected within a redevelopment project area. The taxable valuation of a project area last equalized prior to adoption of the redevelopment plan, or base roll, is established and, except for any period during which the taxable valuation drops below the base year level, the taxing agencies within a project area, which generally includes any city, county, district or other public corporation for whose benefit taxes are levied (the “Taxing Agencies”), thereafter receive only the taxes produced by the levy of the then current tax rate upon the base roll. Taxes collected upon any increase in taxable valuation over the base roll (the “Tax Increment”) are allocated to a redevelopment agency and may be pledged by a redevelopment agency to the repayment of any indebtedness incurred in financing or refinancing a redevelopment project. The Tax Increment, however, is subject to a number of claims and reductions which are prior to the pledge of the repayment of redevelopment agency indebtedness, including among others, statutory pass-through agreements to Taxing Agencies and administrative charges by the County, as further described herein. Redevelopment agencies themselves have no authority to levy property taxes and must look specifically to the allocation of taxes produced as above described.

Since the Agency has no power to levy and collect property taxes, any property tax

limitation, legislative measure, voter initiative or diversion of Tax Increment to Taxing Agencies may have the effect of reducing the amount of Tax Revenues that would otherwise be available to pay the Bonds and any Parity Debt (as hereinafter defined). Likewise, the reduction of assessed valuations of taxable property in the Project Area, any reduction in tax rates or tax collection rates and broadened property tax exemptions would have a similar effect. See “RISK FACTORS” and “STATUTORY LIMITATIONS ON TAX REVENUES”.

The Bonds are not a debt of the City of Goleta, the County of Santa Barbara, the

State of California, or any of its political subdivisions, and neither the City, the County, the State, nor any of its political subdivisions is therefore liable to pay the Bonds, nor in any event shall the Bonds be payable out of any funds or properties other than those of the Agency. The Bonds do not constitute an indebtedness in contravention of any constitutional or statutory debt limitation or restriction.

Allocation of Taxes

As provided in the Redevelopment Plan for the Project Area originally approved by the County on June 16, 1998, pursuant to Ordinance No. 4326 (the “Redevelopment Plan”), and pursuant to Article 6 of Chapter 6 of the Redevelopment Law (commencing with Section 33670 of the California Health and Safety Code) and Section 16 of Article XVI of the Constitution of the State, taxes levied upon taxable property in the Project Area each year by or for the benefit of the Taxing Agencies, for fiscal years beginning after July 1 subsequent to the effective date of the ordinance adopting the Redevelopment Plan for the Project Area, or any amendment thereof, are divided as follows:

1. To the Taxing Agencies: That portion of the taxes which would be produced by

the rate upon which the tax is levied each year by or for each of said Taxing Agencies upon the total sum of the assessed value of the taxable property in the Project Area as shown upon the assessment roll used in connection with the

-10-

taxation of such property by such Taxing Agency last equalized prior to the ordinance approving the Redevelopment Plan, shall be allocated to, and when collected shall be paid into the funds of the respective Taxing Agencies as taxes by or for said Taxing Agencies on all other property are paid;

2. To the Agency: Except for taxes which are attributable to a tax rate levied by a

Taxing Agency for the purpose of producing revenues to repay bonded indebtedness approved by the voters of the Taxing Agency on or after January 1, 1989, which shall be allocated to and when collected shall be paid to the respective Taxing Agency, that portion of said levied taxes each year in excess of such amount (the Tax Increment) shall be allocated to, and when collected, shall be paid to the Agency to pay principal of and interest on loans, moneys advanced to, or indebtedness (whether funded, refunded, assumed or otherwise) incurred by the Agency to finance or refinance, in whole or in part, the redevelopment project.

Housing Set-Aside Amounts. The Redevelopment Law requires that, except under

certain circumstances, redevelopment agencies set-aside 20% of all gross Tax Increment (as described above) derived from redevelopment project areas into a low and moderate income housing fund, to be used for the purpose of increasing, improving and/or preserving the community’s supply of low and moderate income housing. This 20% set-aside requirement is referred to as the “Housing Set-Aside Amounts.” The Housing Set-Aside Amounts are not pledged to any portion of the debt service on the Bonds.

Pledge Under the Indenture

Pursuant to the Indenture, the Tax Revenues are pledged to the payment of the debt service on the Bonds and Parity Debt. See “Issuance of Additional Parity Debt” below.

The Indenture defines “Tax Revenues” to mean (a) moneys allocated within the Plan Limit and paid to the Agency derived from that

portion of taxes levied upon assessable property within the Project Area allocated to the Agency pursuant to Article 6 of Chapter 6 of the Law and Section 16 of Article XVI of the Constitution of the State of California, or pursuant to other applicable State laws, and

(b) reimbursements, subventions, or other payments made by the State with respect to

any property taxes that would otherwise be due on real or personal property but for an exemption of such property from such taxes.

“Tax Revenues” shall not include: (a) payments made to the Agency with respect to personal property within the Project

Area pursuant to Section 16110, et seq., of the Government Code of the State; (b) that portion of taxes paid to the Agency which are required by Section 33334.3 of the

Law to be deposited in the Low and Moderate Income Housing Fund to increase, improve or preserve the supply of low and moderate income housing within or of benefit to the Project Area; and

-11-

(c) all amounts payable by the Agency pursuant to Section 33607.5 or Section 33607.7 of the Law, unless the payment of such amounts has been subordinated to the payment of Debt Service on the Bonds or on any Parity Debt, as applicable.

The Indenture establishes a special fund known as the “Special Fund”, which is held by

the Agency. The Agency is required to deposit all of the Tax Revenues received in any Bond Year promptly upon receipt by the Agency, until such time during such Bond Year as the amounts on deposit in the Special Fund equal the aggregate amounts required to be transferred by the Trustee for deposit in such Bond Year with respect to any additional Parity Debt pursuant to the applicable Parity Debt Instrument and for deposit into the Debt Service Fund for transfer to the Interest Account, the Principal Account, the Sinking Account, the Reserve Account and the Redemption Account in such Bond Year to pay debt service on the Bonds.

All Tax Revenues received by the Agency during any Bond Year in excess of the

amount required to be deposited in the Special Fund for transfer to the Trustee during such Bond Year are released from the pledge under the Indenture for the security of the Bonds and any additional Parity Debt and may be applied by the Agency for any lawful purpose of the Agency.

Funds Under the Indenture

Moneys in the Debt Service Fund are transferred by the Trustee in the following

amounts, at the following times, and deposited by the Trustee in the following respective special accounts, which are established in the Debt Service Fund, and in the following order of priority:

Interest Account. On or before the Business Day preceding each Interest Payment

Date, the Trustee will withdraw from the Debt Service Fund and deposit in the Interest Account an amount which when added to the amount contained in the Interest Account on that date, will be equal to the aggregate amount of the interest becoming due and payable on the Outstanding Bonds on such Interest Payment Date. All moneys in the Interest Account will be used and withdrawn by the Trustee solely for the purpose of paying the interest on the Bonds as it shall become due and payable (including accrued interest on any Bonds redeemed prior to maturity pursuant to the Indenture).

Principal Account. On or before the Business Day preceding December 1 in each year

in which principal amounts of the Bonds is due, the Trustee will withdraw from the Special Fund and deposit in the Principal Account an amount which, when added to the amount then contained in the Principal Account, will be equal to the principal becoming due and payable on the Outstanding Serial Bonds on the next December 1. All moneys in the Principal Account shall be used and withdrawn by the Trustee solely for the purpose of paying the principal of the Serial Bonds and maturing Term Bonds as it will become due and payable.

Sinking Account. No later than the Business Day preceding each December 1 or June

1, as applicable, on which any Outstanding Term Bonds, issued as Parity Debt pursuant to a Parity Debt Instrument, are subject to mandatory Sinking Account redemption, or otherwise for purchases of Term Bonds, the Trustee will withdraw from the Special Fund and deposit in the Sinking Account an amount which, when added to the amount then contained in the Sinking Account, will be equal to the aggregate principal amount of the Term Bonds required to be redeemed on such December 1 (or June 1, if applicable). All moneys on deposit in the Sinking Account will be used and withdrawn by the Trustee for the sole purpose of paying the principal of the Term Bonds as it shall become due and payable upon redemption or purchase.

-12-

Reserve Account. The Indenture requires the establishment of a Reserve Account in an

amount equal to the Reserve Requirement. The Indenture defines the term “Reserve Requirement” to mean, as of the date of calculation, lesser of: (i) Maximum Annual Debt Service on the Bonds; (ii) ten percent (10%) of the original principal amount of the Bonds; or (iii) 125% of Average Annual Debt Service on the Bonds. The term “Reserve Requirement”, for Parity Debt, means as of the date of calculation, an amount equal to the lesser of: (i) Maximum Annual Debt Service on the Parity Debt; (ii) ten percent (10%) of the original principal amount of the Parity Debt; or (iii) 125% of Average Annual Debt Service on the Parity Debt. The Indenture defines the term “Maximum Annual Debt Service” to mean, as of the date of calculation, the largest Annual Debt Service for the current or any future Bond Year, including payments on any additional Parity Debt, as certified in writing by the Agency to the Trustee. For purposes of such calculation, there shall be excluded the principal of any Parity Debt, together with the interest to accrue thereon, in the event and to the extent that the proceeds of such Parity Debt are deposited in an escrow fund are then held in cash or are invested solely in Permitted Investments and from which amounts may not be released to the Agency unless the amount of Tax Revenues for the current Fiscal Year (as evidenced in the written records of the County), at least equal the requirements for issuance of Parity Debt under the Indenture. Initially, the Reserve Account will be funded in the amount of $1,340,400.

In the event that on the Business Day preceding an Interest Payment Date the amount

on deposit in the Reserve Account at any time becomes less than the Reserve Requirement, the Trustee shall promptly notify the Agency of such fact. Promptly upon receipt of any such notice, the Agency will transfer to the Trustee an amount sufficient to maintain the Reserve Requirement on deposit in the Reserve Account. If there shall then not be sufficient Tax Revenues to transfer an amount sufficient to maintain the Reserve Requirement on deposit in the Reserve Account, the Agency is obligated to continue making transfers as Tax Revenues become available until there is an amount sufficient to maintain the Reserve Requirement on deposit in the Reserve Account. All money in the Reserve Account will be used and withdrawn by the Trustee solely for the purpose of making transfers to the Interest Account, the Principal Account and the Sinking Account in such order of priority, in the event of any deficiency at any time in any of such accounts or for the retirement of all the Bonds then Outstanding, except that so long as the Agency is not in default under the Indenture, any amount in the Reserve Account in excess of the Reserve Requirement shall be withdrawn from the Reserve Account semiannually on or before four Business Days preceding each June 1 and December 1 by the Trustee and deposited in the Interest Account.

The Reserve Account may be maintained in the form of one or more separate sub-

accounts which are established for the purpose of holding the proceeds of separate issues of the Bonds and any Parity Debt in conformity with applicable provisions of the Code to the extent directed by the Agency in writing to the Trustee.

Redemption Account. On or before the Business Day preceding any date on which

Bonds are to be optionally redeemed, the Trustee will withdraw from the Debt Service Fund any amount transferred by the Agency for optional redemption of Bonds, for deposit in the Redemption Account, such amount being the amount required to pay the principal of and premium, if any, on the Bonds to be redeemed on such date. All moneys in the Redemption Account will be used and withdrawn by the Trustee solely for the purpose of paying the principal of and premium, if any, on the Bonds to be redeemed on the date set for such redemption. Interest due on Bonds to be redeemed on the date set for redemption will, if applicable, be paid from funds available therefor in the Interest Account.

-13-

Issuance of Additional Parity Debt

In addition to the Bonds, the Indenture permits the Agency to issue or incur other loans, advances or indebtedness payable from Tax Revenues on a parity with the Bonds (“Parity Debt”), to finance or refinance the Redevelopment Project in such principal amount as shall be determined by the Agency. The Agency may issue and deliver any such Parity Debt subject to the following specific conditions:

(a) The Agency shall be in compliance with all covenants set forth in the Indenture.

(b) The Tax Revenues for the then current Fiscal Year based on assessed valuation of property in the Project Area as evidenced in a written document from an appropriate official of the County, plus, at the option of the Agency, the Additional Allowance (as defined below) shall be at least equal to the Parity Debt Test Percentage of Maximum Annual Debt Service on all Bonds and Parity Debt which will be Outstanding following the issuance of such Parity Debt; provided, however:

(i) for purposes of calculating Tax Revenues, an assumed tax rate of $1.00 per

$100 assessed value shall be used; and (ii) the amount of Tax Revenues used in calculating the foregoing coverage test

will be the amount received or to be received in the most recent Fiscal Year (which may be the current Fiscal Year) for which records are available from the County of Santa Barbara establishing the assessed valuations of property in the Project Area.

(c) The Parity Debt Instrument or other document providing for the issuance of such

Parity Debt shall provide that:

(i) Interest on said Parity Debt shall be payable on June 1 and December 1 in each year of the term of such Parity Debt except the first twelve month period, during which interest may be payable on any June 1 or December 1;

(ii) The principal of such Parity Debt shall be payable on December 1 in any year

in which principal is payable; and (iii) Money shall be deposited in a reserve account in an amount equal to the

Reserve Requirement following the issuance of incurrence of such Parity Debt.

(d) The Parity Debt Instrument or other document providing for the issuance of such Parity Debt may provide for the establishment of separate funds, accounts or subaccounts.

(e) The proceeds of such Parity Debt may be deposited into an escrow fund from which

amounts may not be released to the Agency unless and until the Tax Revenues (as evidenced in the written records of the County) at least equal the Parity Debt Test Percentage of the amount of Maximum Annual Debt Service.

The Indenture defines the term “Additional Allowance” to mean, as of the date of

calculation, the amount of Tax Revenues which, as shown in the report of an Independent Redevelopment Consultant, are estimated to be receivable by the Agency in the next Fiscal Year as a result of increases in the assessed valuation of taxable property in the Project Area

-14-

due to either (i) construction which has been completed but has not yet been reflected on the tax roll, or (ii) transfer of ownership or any other interest in real property, which is not then reflected on the tax rolls.

The Indenture defines “Parity Debt Test Percentage” to mean initially, 150%, unless and

until the total value of taxable property in the Project Area, as set forth in a Tax Revenues Certificate, is at least equal to 200% of the value of the taxable property in the Project Area as of the Base Year for the Project Area established in the Redevelopment Plan; and thereafter, the Parity Debt Test Percentage shall be equal to 135%.

Issuance of Subordinate Debt

In addition to the Bonds, the Agency may issue or incur debt subordinate to the payment

of debt service on the Bonds.

Certain Limitations in the Redevelopment Plan

The Redevelopment Law requires that the Redevelopment Plan contain certain limitations on the redevelopment activities of the Agency and related matters. In compliance with AB 1290 adopted by the California Legislature as Chapter 942, Statutes 1993 (“AB 1290”), the Redevelopment Plan established a time limit on the establishing of loans, advances, and indebtedness as June 16, 2018, and the date after which the Agency may not pay indebtedness or receive property taxes as June 16, 2044.

The California Legislature enacted Senate Bill 1045, Chapter 260, Statutes 2003,

effective September 1, 2003 (“SB 1045”). SB 1045 provides, among other things, that the Redevelopment Plan for the Project Area may be amended to add one year to the effectiveness of the Redevelopment Plan and on to the period for collection of tax increment revenues and the repayment of indebtedness. As permitted by SB 1045, the City Council on May 21, 2007, adopted Ordinance No. 07-05, adding one year on to the effectiveness of the Redevelopment Plan and on to the period for collection of tax increment revenues and the repayment of indebtedness. The Redevelopment Plan establishes June 16, 2029, as the termination date for the effectiveness of the Redevelopment Plan, as a result of Ordinance No. 07-05.

The Redevelopment Plan also contains a limitation on bonded indebtedness of the

Agency which can be outstanding at any one time of not exceed $45,956,884, as required by the Redevelopment Law. Although the Redevelopment Law does not require that there be a limit on the aggregate amount of tax increment revenues, with respect to project areas formed after the adoption of AB 1290, the Redevelopment Plan does contain a limit of $363,339,006 on the amount of tax increment the Agency may receive. Through fiscal year 2009-10, the Agency has reported total receipts of $19,421,236, leaving almost $344 million of gross tax increment revenue remaining to be collected under the current limitation. The Agency does not foresee that the Agency will reach its tax increment collection limit throughout the duration of the Redevelopment Plan and the period thereafter for repayment of indebtedness. The Fiscal Consultant has reviewed these limitations and has determined that the Bonds would not be negatively impacted by these limitations. See “APPENDIX A - Fiscal Consultant’s Report – Time Limitations.”

Tax Sharing Statutes

AB 1290 eliminated the statutory authority to negotiate tax sharing agreements with

-15-

Taxing Agencies and provided a formula for mandatory tax sharing, applicable to projects adopted after January 1, 1994 or amended after that date to add territory. The formula thus applies to the Project Area.

The AB 1290 formula is set forth in Section 33607.5 of the Redevelopment Law. Generally speaking, under the Tax Sharing Statutes, the Agency is to pay to the affected

taxing entities percentages of tax increment generated in the Project Area as follows: 1. Throughout the term of the Project Area’s eligibility to receive tax increment

commencing with a base year determined as of the year the formula first becomes effective (Fiscal Year 1997-98), 25% of post Housing Set-Aside Amounts; plus,

2. For the eleventh year of the receipt of tax increment and thereafter, 21% of

revenues in excess of tenth year revenue; plus, 3. For the thirty-first year of receipt of tax increment and thereafter, 14% of revenues

in excess of thirtieth year revenues. As indicated, amounts specified as payable to taxing agencies under the AB 1290

formula contained in the Tax Sharing Statutes are to be computed after deducting the Housing Set-Aside amounts.

The Agency is treating all payments to taxing entities under the Tax Sharing Statutes to

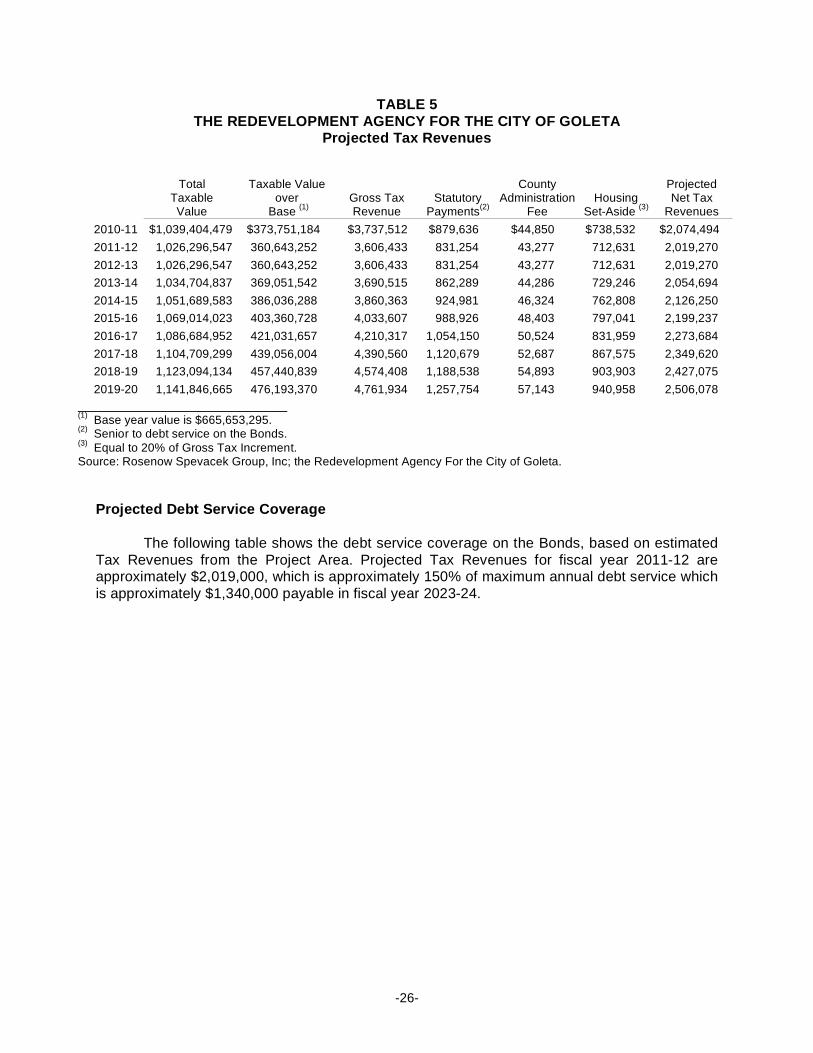

be superior to the payment of debt service on the Bonds. See Table 6 “Redevelopment Agency For the City of Goleta – Goleta Old Town Redevelopment Project – Projected Tax Revenues”.

THE REDEVELOPMENT AGENCY

General

The County originally adopted the Redevelopment Plan on June 16, 1998 by County Ordinance No. 4326. The Redevelopment Plan was administered as part of the County’s unincorporated territory until the City Council assumed control of redevelopment activities for the Project Area under the Redevelopment Plan after the City incorporated in 2002. The City of Goleta activated the Redevelopment Agency on February 1, 2002 by Ordinance No. 02-08 and assumed control of the Redevelopment Plan for the Project Area on April 15, 2002 by Ordinance No. 02-19. The Redevelopment Plan enables the Agency to collect tax increment to implement and finance revitalization projects in the 595-acre Project Area, which is approximately 12% of the total area of the City.

All powers of the Agency are vested in its governing body. Pursuant to the

Redevelopment Law, the Agency may exercise broad governmental functions and authority to accomplish its purposes, including, but not limited to, the right to issue bonds, notes and other obligations and expend their proceeds and the right to acquire, sell, develop, administer or lease property (the Agency is not authorized to exercise eminent domain under its Redevelopment Plan). The Agency may clear or move buildings, structures, or other improvements form real property as necessary to carry out the purposes of the Redevelopment Plan. .

-16-

To the extent permitted and in the manner required by law, the Agency is authorized to install and construct or cause to be installed and constructed the public improvements and public utilities (within or outside the Project Area) necessary to carry out the Redevelopment Plan. Such public improvements include, but are not limited to, parking lots or structures, over or underpasses, bridges, streets, curbs, gutters, sidewalks, streetlights, sewers, storm drains, traffic signals, electrical distribution systems, flood control facilities, natural gas distribution systems, water distribution systems, landscaping, parks, playgrounds, and any buildings, structures or improvements necessary and convenient to the full development of any of the above.

With certain exceptions, the Agency may not construct or develop buildings, with the

exception of public facilities, but must sell or lease cleared property to redevelopers for construction and development in accordance with the Redevelopment Plan. The Agency may, out of any funds available to it for such purposes, pay for all or part of the value of the land and the cost of buildings, facilities, structures or other improvements to be publicly owned and operated, to the extent that such improvements are of benefit to a project area and no other reasonable means of financing is available.

Certain State of California budget proposals regarding the elimination of redevelopment

agencies could adversely impact the Agency and its projects. See “RISK FACTORS - State Budget Deficit; ERAF; SERAF” herein for a description of recent State proposals to eliminate redevelopment agencies.

Management of the Agency

Margaret Connell currently serves as Chair of the Agency. The current members of the Council and term expiration are as follows:

Name City and Agency Title Term Expires

Margaret Connell Agency Chair/Mayor November 2012 Ed Easton Agency Vice Chair/Mayor Pro Tem November 2012 Roger S. Aceves Agency Member/Councilmember November 2014 Michael T. Bennett Agency Member/Councilmember November 2014 Paula Perotte Agency Member/Councilmember November 2014

Agency staff services are provided by City staff. Such support includes project

management, real estate acquisition and disposition, relocation, engineering and planning, legal, financing and fiscal services. See “THE PROJECT AREA - Outstanding Indebtedness of the Agency - Arrangement with City for Administrative Services”.

The City Manager also serves as the Executive Director of the Agency. Daniel Singer is currently the City Manager of the City, and has served in that capacity

since September 2005. He came to the City of Goleta with 14 years of local government experience including service as City Manager for the City of Ojai in Ventura County. Mr. Singer’s municipal background includes extensive experience in redevelopment, grant management, finance, risk management, transportation, and community relations and he has also served on numerous non-profit and civic organization boards. Mr. Singer received a master’s degree in Political Science and a master’s degree in Public Administration from the

-17-

Maxwell School of Citizenship at Syracuse University. He also holds a certificate in Conflict Resolution and was a former mediator in both California and New York.

Vytautas "Vyto" Adomaitis has served the City of Goleta since July, 2002. He is

currently the Director of the Redevelopment & Neighborhood Services Department. Mr. Adomaitis has 20 years of broad local government and private sector experience including economic development, redevelopment, planning, city administration, grant administration, public safety and inspection services. Mr. Adomaitis has also served as an advisory board member for Habitat for Humanity and other non-profit organizations. He received a Master's Degree in Public Administration and a Bachelor's Degree in Political Science from California State University, Northridge.

Alvertina Rivera, the City Finance Director, joined the City of Goleta’s management

team in November 2006. Prior to her work with the City she served for 7 1/2 years as Finance Director for the cities of Santa Paula and Orange Cove. Ms. Rivera received a Bachelor of Science degree in Business Administration with an emphasis in Accounting from California State University Fresno. She has experience in finance, risk management, financial reporting, investments, labor negotiations, grant management, redevelopment, and bond issuances.

Steve Wagner has served as the City’s Community Services Director and City Engineer

since February 2003. He has over 20 years of local government experience in public works capital project management. Prior to coming to the City Mr. Wagner served as Public Works Director/City Engineer for the City of Carpinteria and Deputy Director of Public Works for the County of Santa Barbara. He obtained his Bachelor of Science degree in Civil Engineering from Cal Poly San Luis Obispo. He is a registered Civil Engineer and Certified Flood Plain Manager in the State of California.

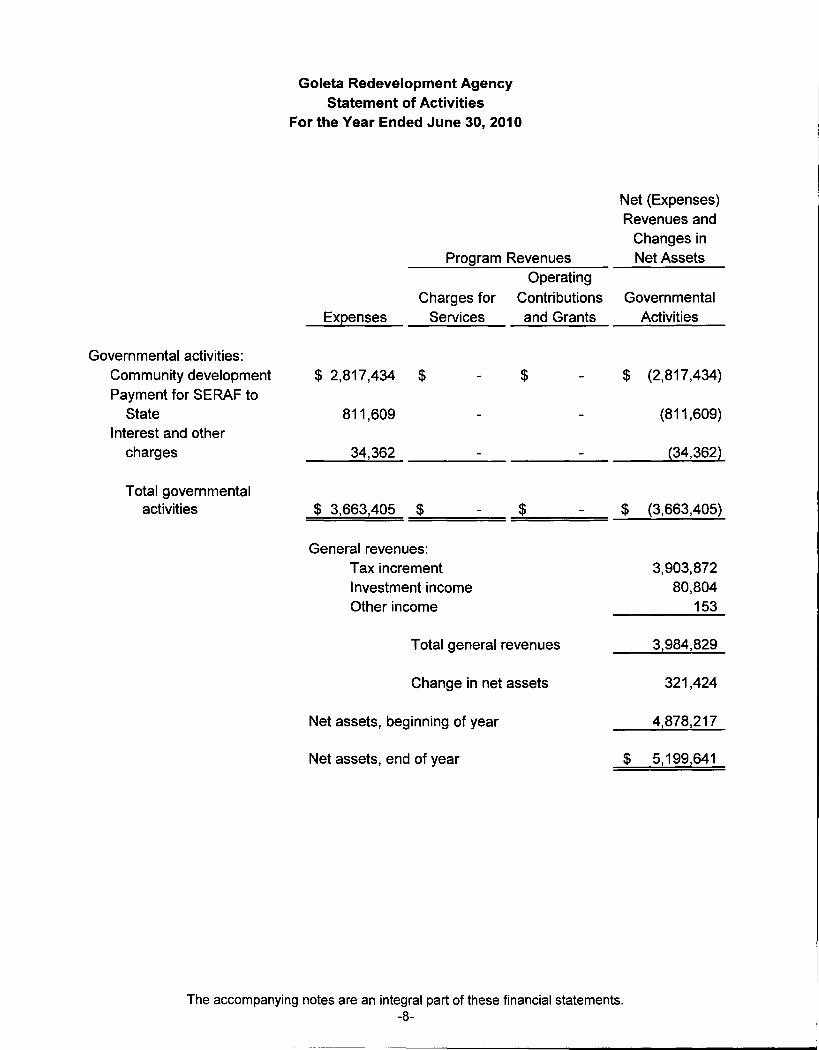

See APPENDIX B for the Agency’s audited financial statement for the Fiscal Year ended

June 30, 2010. The auditor has not reviewed such statements in connection with their inclusion in this Official Statement, nor has the Agency requested such a review. See also “RISK FACTORS – State Budget Deficit; ERAF; SERAF” herein for a discussion of recent proposals to eliminate redevelopment agencies.

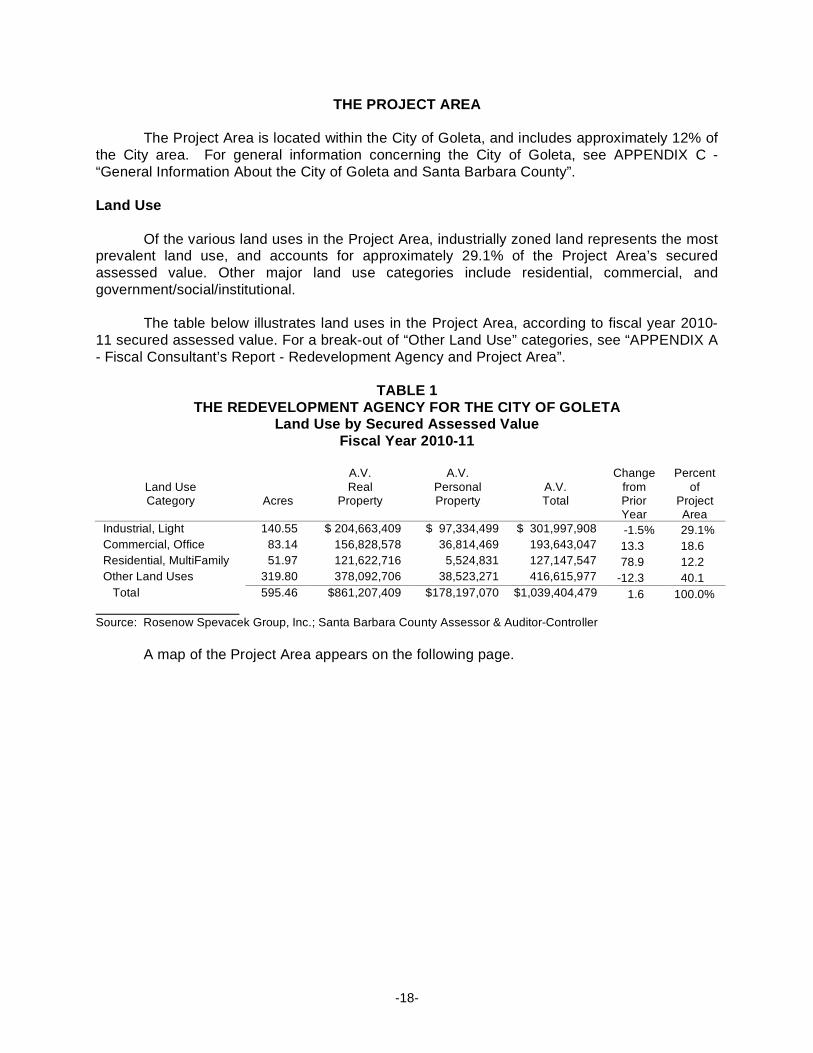

-18-

THE PROJECT AREA The Project Area is located within the City of Goleta, and includes approximately 12% of

the City area. For general information concerning the City of Goleta, see APPENDIX C - “General Information About the City of Goleta and Santa Barbara County”.

Land Use

Of the various land uses in the Project Area, industrially zoned land represents the most prevalent land use, and accounts for approximately 29.1% of the Project Area’s secured assessed value. Other major land use categories include residential, commercial, and government/social/institutional.

The table below illustrates land uses in the Project Area, according to fiscal year 2010-

11 secured assessed value. For a break-out of “Other Land Use” categories, see “APPENDIX A - Fiscal Consultant’s Report - Redevelopment Agency and Project Area”.

TABLE 1

THE REDEVELOPMENT AGENCY FOR THE CITY OF GOLETA Land Use by Secured Assessed Value

Fiscal Year 2010-11

Land Use Category

Acres

A.V. Real

Property

A.V. Personal Property

A.V. Total

Change from Prior Year

Percent of

Project Area

Industrial, Light 140.55 $ 204,663,409 $ 97,334,499 $ 301,997,908 -1.5% 29.1% Commercial, Office 83.14 156,828,578 36,814,469 193,643,047 13.3 18.6 Residential, MultiFamily 51.97 121,622,716 5,524,831 127,147,547 78.9 12.2 Other Land Uses 319.80 378,092,706 38,523,271 416,615,977 -12.3 40.1 Total 595.46 $861,207,409 $178,197,070 $1,039,404,479 1.6 100.0%

Source: Rosenow Spevacek Group, Inc.; Santa Barbara County Assessor & Auditor-Controller

A map of the Project Area appears on the following page.

Goleta Old Town . Redevelopment :Project Area .Boundary

{

1_: .. OCH2 ..

'-~

City of Santa·. Borbara

-20-

Assessed Value Information

Assessed Valuations. Taxable values are prepared and reported by the County Auditor-Controller each fiscal year and represent the aggregation of all locally assessed properties, which are part of the Project Area. The assessments are assigned to Tax Rate Areas (TRA) that are coterminous to the boundaries of the Project Area.

The current (fiscal year 2010-11) total assessed value of the Project Area is

$1,039,603,877, of which tax increment revenue is generated from the incremental assessed value in excess of the Project Area’s 1997-98 base year value of $665,653,295. The 2010-11 incremental assessed value for the Project Area, equal to the difference between the current assessed value and base year value, is $373,751,184.

The following table presents the assessed values, base year values, and incremental

assessed values for the past five years. For a ten-year history of assessed value in the Project Area, see “APPENDIX A – Fiscal Consultant’s Report – Assessed Valuation”. See also “Appeals to Assessed Valuation” below.

TABLE 2

THE REDEVELOPMENT AGENCY FOR THE CITY OF GOLETA Historical Assessed Valuation Growth

Year Real Property Personal Property Total AV % Change Incremental AV

2010-11 $853,936,906 $185,467,573 $1,039,404,479 1.6% $373,751,184

2009-10 833,984,780 189,426,507 1,023,411,287 6.3 357,757,992

2008-09 759,059,796 204,149,879 963,209,675 5.1 297,556,380

2007-08 713,908,786 202,613,471 916,522,257 5.3 250,868,962

2006-07 674,111,291 196,046,092 870,157,383 7.4 204,504,088

1997-98 (Base Year)

476,922,697 188,730,598 665,653,295

Source: Rosenow Spevacek Group, Inc.; Santa Barbara County Auditor Controller Reports.

-21-

Largest Taxpayers. The following table lists the ten largest payers of property taxes in the Project Area for fiscal year 2010-11. The top ten taxpayers account for $259,507,562 account for 25.0% of the Project Area’s 2010-11 total assessed value and 69.4% of its total incremental value. See “RISK FACTORS – Concentration of Ownership”.

TABLE 3

THE REDEVELOPMENT AGENCY FOR THE CITY OF GOLETA Total Project Area

Largest Fiscal Year 2010-11 Taxpayers

Property Owner

Bills (1) Assessed Value Real Property

Assessed Value Personal Prop.

Assessed Value Total

% Change

from Prior Year (5)

% of Project Area

% of

Increment Value

Sumida Gardens LP (2) 1 $ 55,342,473 $ 648,080 $55,990,553 143.7% 5.4% 15.0% Raytheon Company (3) 2 22,853,007 20,083,460 42,936,467 (7.9) 4.1 11.5 Torridon LLC 2 28,524,666 -- 28,524,666 (0.2) 2.7 7.6 SB Corporate Center 2 24,056,853 -- 24,056,853 (0.2) 2.3 6.4 Fairview Business Center(4) 1 20,691,442 -- 20,691,442 5.9 2.0 5.5 Cox Enterprises, Inc. 5 6,063,517 13,358,200 19,421,717 (1.1) 1.9 5.2 Ocean Park Hotels, LLC 1 16,259,253 1,421,000 17,680,253 (0.2) 1.7 4.7 Ampersand Publishing LLC 2 9,922,533 7,248,310 17,170,843 (2.1) 1.7 4.6 Dupont Displays Inc. 1 3,882,570 12,789,040 16,671,610 0.0 1.6 4.5 Ekwill Partners LTD 1 16,363,158 -- 16,363,158 (0.2) 1.6 4.4 Total Top Ten 18 $203,959,472 $55,548,090 259,507,562 12.9% Total Project Area 1,039,404,469 25.0%

Total Project Area Incremental $373,751,184 69.4%

(1) Bills consist of the number of secured parcels and unsecured bill records. (2) Sumida Gardens LP filed a base year appeal with the County in 2010 to reduce assessed value to $36

million. Potential reduction could decrease 2011-12 personal property value by approximately $20 million. (3) Raytheon Co. filed an appeal in 2009 to reduce personal property value from $13.2 million to $1.3 million.

The appeal was withdrawn. Raytheon Co. has no appeals in 2010. (4) Fairview Business Center filed a base year appeal in 2009 to reduce assessed value to $15.3 million; the

appeal is still open. Potential reduction could reduce the 2011-12 assessed value by approximately $4 million.

(5) Represents the change in assessed value from fiscal year 2009-10 Source: Rosenow Spevacek Group, Inc.; Santa Barbara County Assessor and City of Goleta

The following provides brief descriptions of the ten largest taxpayers in the Project Area: Sumida Gardens LP owns one parcel which is located at 100 Sumida Gardens Lane

occupied by a multifamily residential development constructed in 2007. Sumida Gardens is a 200-unit apartment complex, which includes 34 apartments for low- and very low-income households. The parcel was purchased from the Sumida Limited Partnership in 2002. Sumida Gardens filed an appeal in 2010 to reduce the base year value (reassessed due to construction) to $36 million.

Raytheon Company, a defense and aerosystems supplier has two industrial owner-

occupied research parks located at 6380 Hollister Avenue and 115 Robin Hill Road. The Raytheon Company appealed its personal property assessed values in 2009, but the appeal was withdrawn. There have been no other appeals within the last five years. The parcels were last transferred on December 5, 1980 (APN 073050027) and March 14, 1979 (APN 073050044).

Torridon LLC owns two commercial parcels located at 430 S. Fairview Avenue and 490

S. Fairview Avenue #100. There have been no assessment appeals filed by this property owner

-22-

within the last five years. The parcels were last transferred on April 22, 2004 (APN 071130057) and August 10, 2007 (APN 07113062).

Santa Barbara Corporate Center LLC has two multi-story offices located at 5383

Hollister Avenue #150, and 201 Mentor Drive. There have been no assessment appeals filed by this property owner within the last five years. The 5383 Hollister Avenue (APN 071140074) property, or the GRCI Founders Building, is a two-story, steel frame, stucco-faced commercial Class A office building built in 1995. Major tenants include GRC International, Time-Warner Telecom, Somera Communications, and Bermant Development Co. The property(APN 071140074) was last transferred on February 16, 1996. The 201 Mentor Drive property (APN 071140078), or Mentor Corporation Building One, is a two-story office building built in 1991. It is designed for technology and office uses. The property was last transferred on February 13, 2006.

Fairview Business Center owns one parcel which is located at 420 Fairview Avenue.

Fairview Business Center has filed two appeals within the past five years. In 2009, a base year appeal was filed to reduce its assessed value to $15.3 million, and this appeal is still open. They appealed their 2008 personal property value assessed value and the case was stipulated in August 2003 to reduce the unsecured value from $5.9 million to $5.7 million.

Cox Enterprises, a cable service provider, owns two commercial parcels in the project

area and has additional unsecured value reported worth $13,565,150. The parcels are located at 22 S. Fairview Avenue. There have been no assessment appeals filed by this property owner within the last five years. Both parcels (APN 07102101 and APN 071021044) were last transferred on November 30, 1993.

Ocean Park Hotels has one motel located at 5665 Hollister Avenue. There have been

no assessment appeals filed by this property owner within the last five years. The property was last transferred on December 29, 2005(071130060).

Ampersand Publishing LLC, a publisher of electronic newspapers, has two light

industrial properties located at 725 S. Kellogg Avenue. There have been no assessment appeals filed by this property owner within the last five years. The parcels were last transferred on October 19, 2000 (APN 071170005 and APN 07117011).

Dupont Displays, a manufacturer of electronic displays, has one unsecured value

reported worth $16,671,610. The site address is 600 Ward Drive (APN 071140015), which is an industrial research park. There have been no assessment appeals filed by this property owner within the last five years.

Ekwill Partners Ltd has one light manufacturing property at 5540 Ekwill Street (APN

071230009). There have been no assessment appeals filed by this property owner within the last five years. The property was last transferred on December 29, 1988.

Tax Rates. The Agency collects tax increment revenues generated by the general

(1.00%) tax levy in the Project Area. There is no levy in excess of the 1.00% rate, otherwise known as override or debt service, in the Project Area from which the Agency receives revenue.

-23-

New Development

The Revenue and Taxation Code provides for reassessment of properties upon the completion of new construction. The County Assessor determines the construction value in place as of January 1 each year and that amount is reflected on the next equalized assessment roll. Construction in process or completed as of January 1, 2011 is assessed on the 2011-12 roll; construction in place after this date will be reflected on future tax rolls.

Based on a review of building permit records provided by the City’s Building and Safety

Department, it is unlikely that any material changes in assessed values will occur on the 2011-12 assessment roll due to the low level of construction activity in the past year. While owners are investing in their properties, most of this reinvestment appears to be repairs and replacement in nature, and therefore less likely to result in a reassessment.

The Fiscal Consultant has made no attempt to estimate the level of new construction in

the Project Area in future years, although there is ample land available in the Project Area to do so. The Fiscal Consultant believes this assumption is reasonable given the current local, regional and national real estate climate, even though it may result in some understating in potential future tax increment revenues for the Agency.

Property Transfers

The Fiscal Consultant compiled statistics of sales transactions based on data from the County Recorder, via a private property vendor. Sales closed and recorded between January 1, 2010 and January 1, 2011 would be reassessed on the 2011-12 assessment roll, while sales after this date would be reflected on subsequent assessment rolls. During 2009, a total of 39 transactions occurred in the Project Area, dropping to 24 sales for the same 12-month period in 2010. In 2009, sales prices were somewhat lower than assessed values, resulting in an aggregate decrease in Project Area real property values of $866,227, or 0.104 percent of the 2009-10 assessment roll. Condominium residential property sales were the dominant cause of this decrease in the Project Area.

The Fiscal Consultant’s projections shown on Table 5 incorporate a 0.039% decrease in

2011-12 assessed value due to resales. The projections do not include supplemental roll revenues that may be generated from resale activity. See “THE PROJECT AREA - Projected Debt Service Coverage”. See also “APPENDIX A – Fiscal Consultant’s Report – General Assumptions in the Revenue Projections - Resales.”

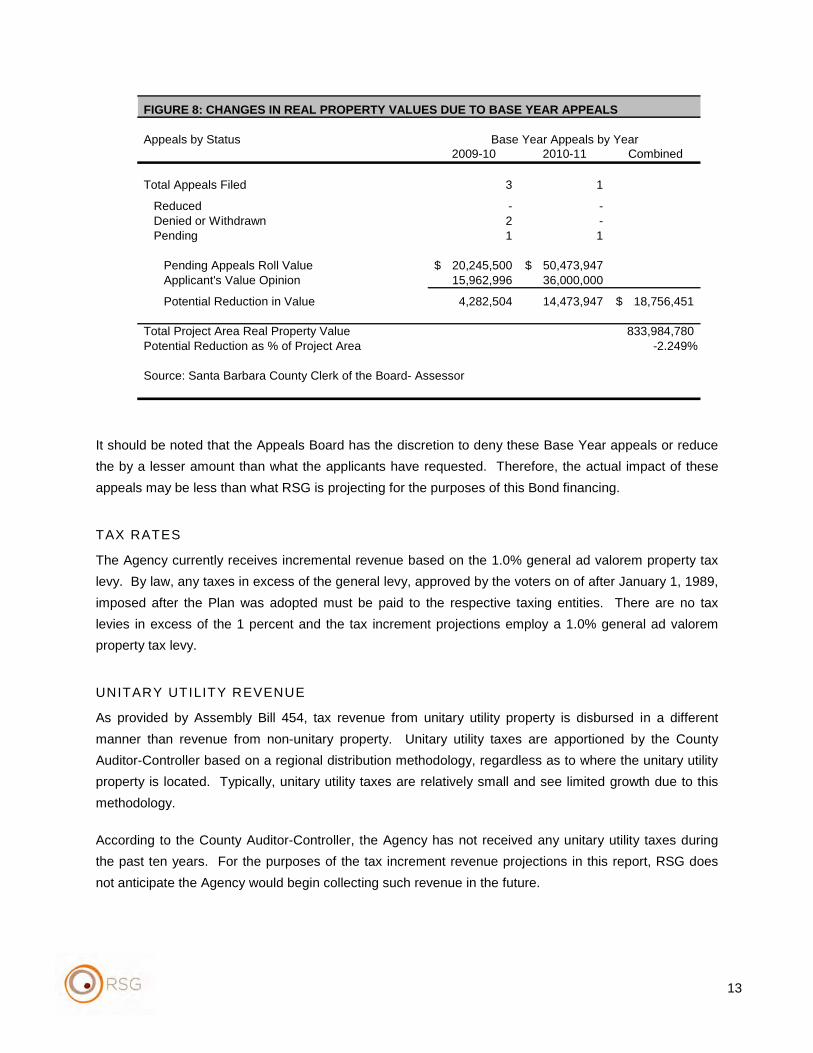

Appeals to Assessed Value