Embed Size (px)

Citation preview

11-1

Option Models: Chapter 11 Part F

Employ option pricing methods to evaluate the option to default.

Used by many of the largest banks to monitor credit risk.

Theory developed by Bob Merton in 1974 Only implemented recently KMV Corporation markets this model quite

widely.

11-2

Key Factors

Capital Structure How much equity “cushion” ? Equity at market value

Incorporates the market’s evaluation of many factors

Volatility of the business (Assets) High volatility increases chances that the equity

cushion will be violated

11-3

11-4

11-5

11-6

-100

-75

-50

-25

0

25

50

75

100

Dec-97 Mar-98 Jun-98 Sep-98 Dec-98 Mar-99 Jun-99 Sep-99 Dec-99 Mar-00 Jun-00 Sep-00

Credit Risk Adjusted Spread

Xerox CorporationHistorical Credit Risk Adjusted Spread to Agencies

December 1997 – June 2000

Spread source: Goldman, Sachs & Co.

Spread (Basis Points)

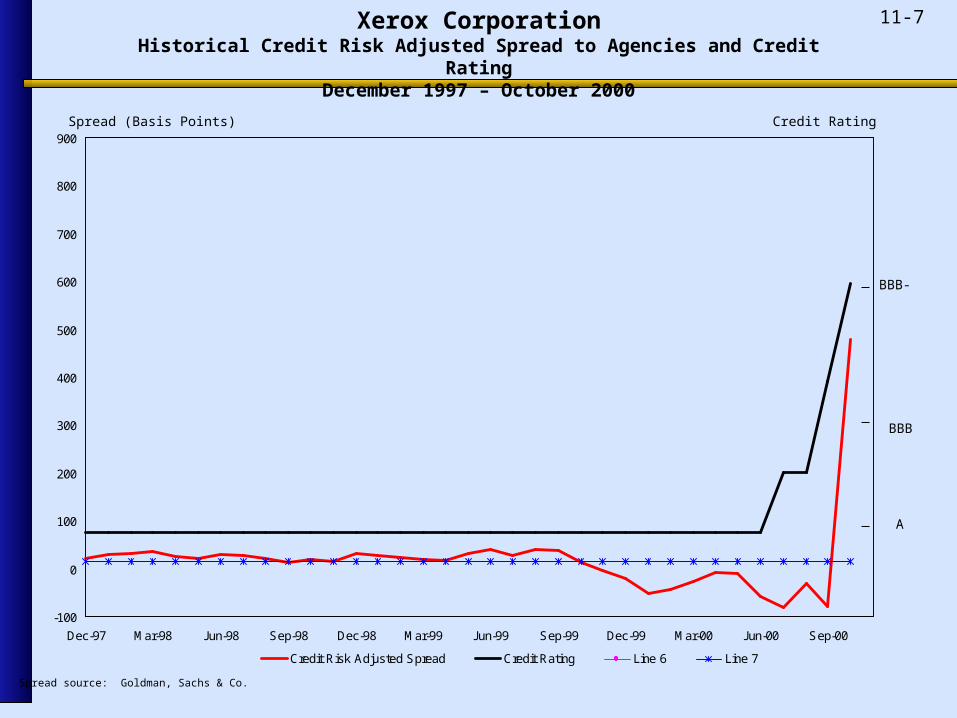

11-7

-100

0

100

200

300

400

500

600

700

800

900

Dec-97 Mar-98 Jun-98 Sep-98 Dec-98 Mar-99 Jun-99 Sep-99 Dec-99 Mar-00 Jun-00 Sep-00

Credit Risk Adjusted Spread Credit Rating Line 6 Line 7

Xerox CorporationHistorical Credit Risk Adjusted Spread to Agencies and Credit Rating

December 1997 – October 2000

Spread source: Goldman, Sachs & Co.

Spread (Basis Points) Credit Rating

BBB-

BBB

A