Embed Size (px)

Citation preview

1

The Research Perspective

I N F O C U S

Prime central London’s property market

Property, prices and predictions

1 0 N O V E M B E R 2 0 2 0

2

Where do we stand currently?

3

Tough times for the Prime Central London Market since 2014

4

A lack of urgency post covid

Travel restrictions

focusses overseas

buying on off-plan

investment

The discretionary

nature of demand means

fewer needs based buyers responding to

lifestyle drivers

Shut-down of amenities

removes the incentive to be in central

London

Falls in stocks and

commodities erodes global

wealth

Weaker global

economy curtails new

wealth generation

Attention shifts to the

amenity offering of

prime country property

Source: Savills 5

Rents and capital values over that period

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

PCL Capital Values PCL Rental Values

Since March

-1.4%Capital Values

-5.0%Rental Values

Annual

-0.5%Capital Values

-4.7%Rental Values

Since 2014 peak

-20.9%Capital Values

-20.6%Rental Values

Source: Twenty CI 6

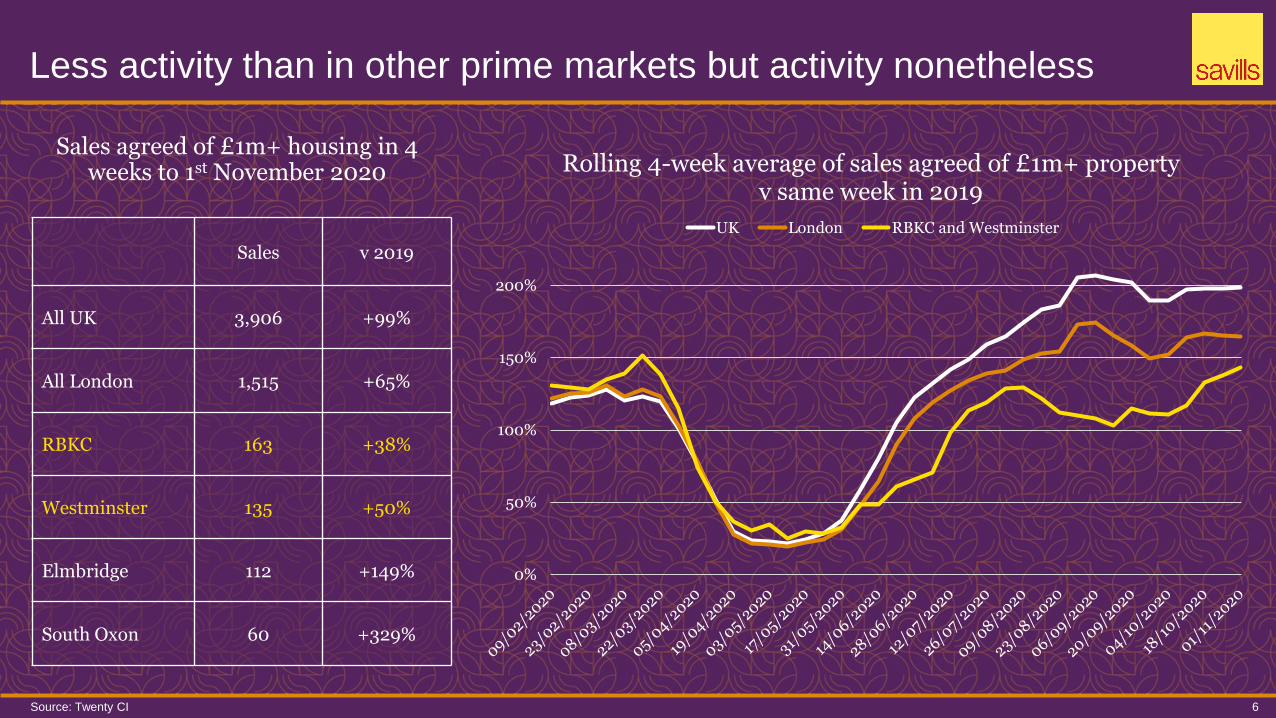

Less activity than in other prime markets but activity nonetheless

0%

50%

100%

150%

200%

Rolling 4-week average of sales agreed of £1m+ property v same week in 2019

UK London RBKC and Westminster

Sales v 2019

All UK 3,906 +99%

All London 1,515 +65%

RBKC 163 +38%

Westminster 135 +50%

Elmbridge 112 +149%

South Oxon 60 +329%

Sales agreed of £1m+ housing in 4 weeks to 1st November 2020

Source: Savills 7

With robust spend over £5m in Q3 this year

0

5

10

15

20

25

30

35

40

45

50

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20

£5m - £10m £10m - £15m £15m - £20m £20m+ £5m+ average in previous 4 years

Quarter 3

£876m

Quarter 2

£436m

Quarter 1

£944m

8

When will conditions be right

for a recovery?

Source: Savills 9

Putting the downturn in context

Late eighties / early nineties

In the preceding 5 years

+107% nominal price growth

+75% real price growth

3.75 years of falls

Prices fall by

-26% in nominal terms

-39% in real terms

-26% in US$ terms

Post credit crunch

In the preceding 5 years

+66% nominal price growth

+52% real price growth

1.50 years of falls

Prices fall by

-22% in nominal terms

-26% in real terms

-45% in US$ terms

Since Mid 2014

In the preceding 5 years

+71% nominal price growth

+54% real price growth

6.50 years of falls

Prices fall by

-21% in nominal terms

-27% in real terms

-39% in US$ terms

Source: Savills 10

Competitive on a world stage

US$ per sq ft June 2014 US$ per sq ft June 2020

London 5,631 Hong Kong 8,129

Hong Kong 5,557 Tokyo 3,986

Tokyo 3,300 London 3,310

New York 3,112 New York 3,012

Sydney 2,764 Sydney 2,799

Paris 2,747 Shanghai 2,657

Shanghai 2,485 Paris 2,623

San Francisco 1,988 Los Angeles 2,516

Singapore 1,897 San Francisco 2,367

Los Angeles 1,692 Shenzhen 2,125

Guangzhou 1,499 Singapore 1,804

Shenzhen 1,138 Guangzhou 1,779

Source: Savills 11

Not uncompetitive from a tax perspective (US$10m)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Vancouver Hong Kong Singapore New York Sydney Madrid Londonpost 31st

March2021

Paris Londonpre 31stMarch2021

Berlin Dubai Shanghai

Per

cen

tag

e o

f p

rop

ert

y p

rice

($

10M

)

Cost of Buying Cost of Holding Cost of Selling

Source: Yahoo Finance 12

Wealth drivers #1

21,000

22,500

24,000

25,500

27,000

28,500

30,000

5,000

5,500

6,000

6,500

7,000

7,500

8,000

04

/11/

20

19

02

/12

/20

19

30

/12

/20

19

27

/01/

20

20

24

/02

/20

20

23

/03

/20

20

20

/04

/20

20

18/0

5/2

02

0

15/0

6/2

02

0

13/0

7/2

02

0

10/0

8/2

02

0

07

/09

/20

20

05

/10

/20

20

02

/11/

20

20

Ha

ng

Sen

g

FT

SE

10

0

FTSE 100 HangSeng

FTSE 100

23%

below

peakHang

Seng 13%

below

peak

15,000

17,000

19,000

21,000

23,000

25,000

27,000

29,000

31,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

24,000

25,000

04

/11/

20

19

02

/12

/20

19

30

/12

/20

19

27

/01/

20

20

24

/02

/20

20

23

/03

/20

20

20

/04

/20

20

18/0

5/2

02

0

15/0

6/2

02

0

13/0

7/2

02

0

10/0

8/2

02

0

07

/09

/20

20

05

/10

/20

20

02

/11/

20

20

Do

w J

on

es

Nik

kei

Nikkei Dow Jones Industrial Average

Nikkei

At peak

Dow

Jones

3%

below

peak

Source: Yahoo Finance, Pitchbook 13

Wealth drivers #2

0

500

1,000

1,500

2,000

2,500

0

10

20

30

40

50

60

70

Go

ld (

US

$)

Oil

(U

S$

per

ba

rrel

)

Commodities (US$)

Oil Gold

Private equity and venture

capital raised globally

Life Sciences

£108bn

in 2019

£105bn

to end Oct 2020

TMT£336bn

in 2019

£343bn

to end Oct 2020

Source: Heathrow Airport Limited 14

The absence of international travel in context

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Heathrow Passenger NumbersExcludes Gatwick, Stansted, Edinburgh, Naples, Aberdeen, Glasgow and Southampton

UK EU Non-EU Europe Africa North America Latin America Middle East Asia / Pacific

Source: World Health Organisation 15

The search for a vaccine (as at 27th of October)

11Phase 3

Wider testing and

effectiveness assessed

Approval and

Distribution

12Phase 2

Expanded safety trials

154in pre clinical

trials

21Phase 1

Small-scale safety trials

Regulatory Review

16

What might that recovery look like?

Source: Savills 17

How has the market recovered in the past?

Late eighties / early nineties

During the downturn

prices fall by

-26% in nominal terms

-39% in real terms

In the next 5 years

prices rise by

+98% in nominal terms

+77% in real terms

Post credit crunch

During the downturn

prices fall by

-22% in nominal terms

-26% in real terms

In the next 5 years

prices rise by

+79% in nominal terms

+54% in real terms

18

A different environment for a recovery

The tax environment

is less welcoming

Despite low costs of funds

low income yields may

temper investor demand

It will face increased

competition as a global “tech city”

London has largely

matured as a global city

It will face challenges to maintain its position as a

global financial

sector

Sources of wealth will come under

greater scrutiny

Source: Savills 19

Prime Central London price forecasts

+4.0%2023

+17.5%5 year

+7.0%2022

-0.5%2020

+4.0%2021

+2.0%2024

Thank you

© Savills 2020

20

This presentation is for general informative purposes only. It may not be published, reproduced or quoted in part or in whole, nor may it be used as a basis for any contract, prospectus, agreement or other document

without prior consent. While all effort has been made to ensure its accuracy, Savills accepts no liability whatsoever for any direct or consequential loss arising from its use. The content is strictly copyright and

reproduction of the whole or part of it in any form is prohibited without written permission from Savills Research.