Embed Size (px)

Citation preview

11

Volatility Smiles Volatility Smiles

Chapter 18Chapter 18

22

Put-Call Parity ArgumentsPut-Call Parity Arguments Put-call parity Put-call parity p +Sp +S00ee-qT-qT = = c +X ec +X e–r T–r T

holds regardless of the holds regardless of the assumptions made about the stock assumptions made about the stock price distributionprice distribution

It follows thatIt follows that

ppmktmkt--ppbsbs==ccmktmkt--ccbsbs

33

Implied VolatilitiesImplied Volatilities

The implied volatility calculated from The implied volatility calculated from a European call option should be the a European call option should be the same as that calculated from a same as that calculated from a European put option when both have European put option when both have the same strike price and maturitythe same strike price and maturity

The same is approximately true of The same is approximately true of American optionsAmerican options

44

Volatility SmileVolatility Smile

A volatility smile shows the A volatility smile shows the variation of the implied volatility variation of the implied volatility with the strike pricewith the strike price

The volatility smile should be the The volatility smile should be the same whether calculated from call same whether calculated from call options or put options options or put options

55

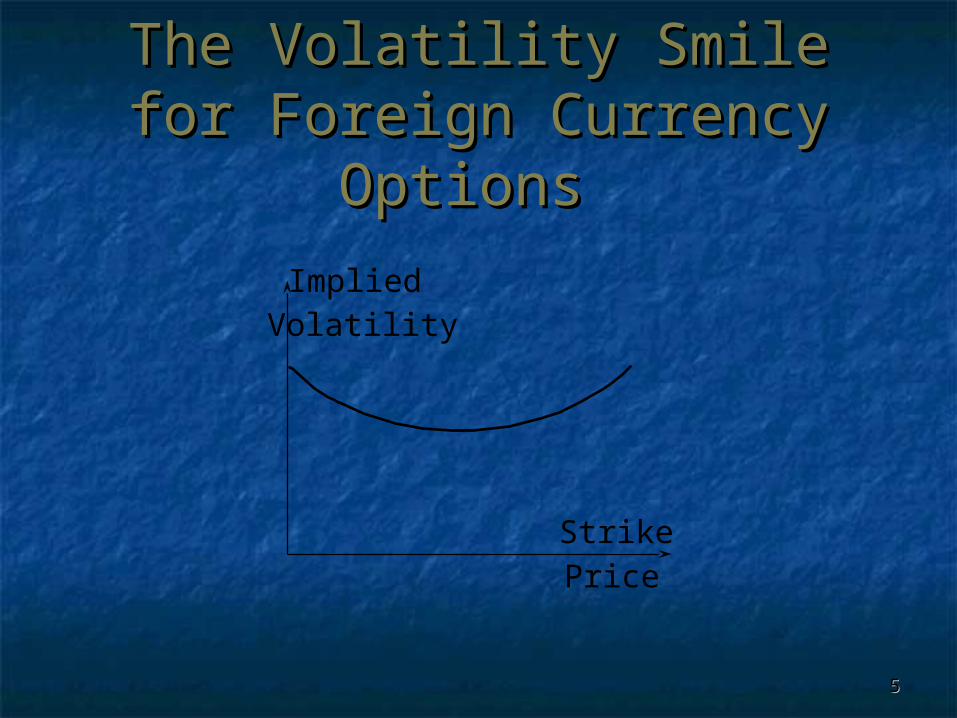

The Volatility Smile for The Volatility Smile for Foreign Currency Options Foreign Currency Options

ImpliedVolatility

StrikePrice

66

Implied Distribution for Implied Distribution for Foreign Currency OptionsForeign Currency Options

The implied distribution is heavier in The implied distribution is heavier in both tails than for the lognormal both tails than for the lognormal distribution.distribution.

It is also “more peaked” than the It is also “more peaked” than the lognormal distribution lognormal distribution

77

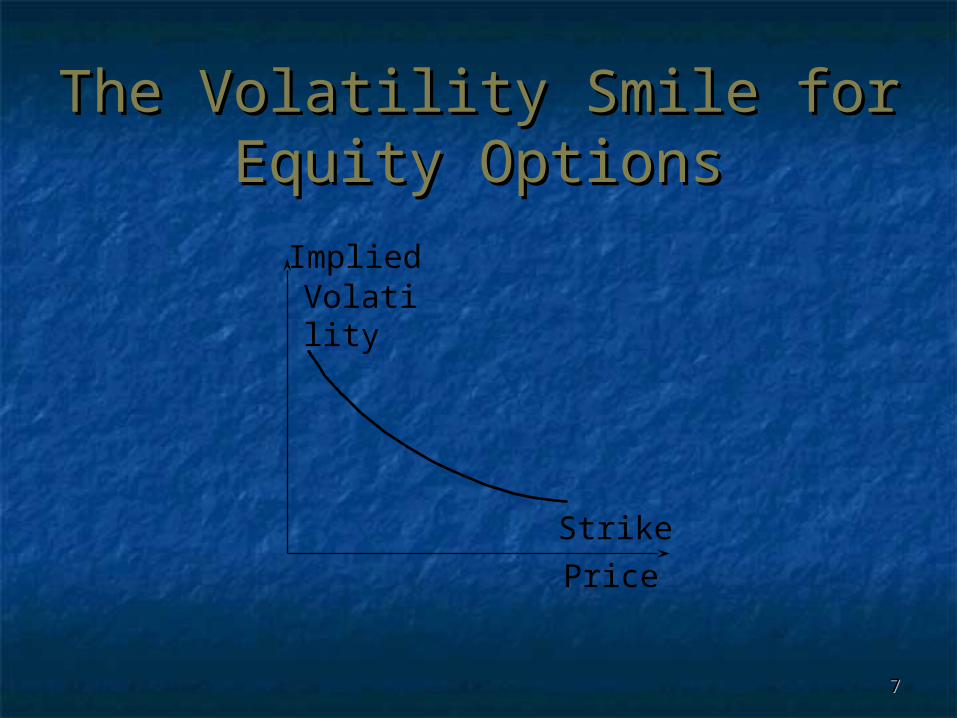

The Volatility Smile for The Volatility Smile for Equity OptionsEquity Options

ImpliedVolatility

Strike

Price

88

Implied Distribution for Implied Distribution for Equity OptionsEquity Options

The right tail is less heavy and the left tail is heavier than the lognormal distribution

99

Other Volatility Smiles?Other Volatility Smiles?

What is the volatility smile ifWhat is the volatility smile if True distribution has a less heavy left True distribution has a less heavy left

tail and heavier right tailtail and heavier right tail True distribution has both a less True distribution has both a less

heavy left tail and a less heavy right heavy left tail and a less heavy right tailtail

1010

Possible Causes of Volatility Possible Causes of Volatility SmileSmile

Asset price exhibiting jumps rather Asset price exhibiting jumps rather than continuous changethan continuous change

Volatility for asset price being Volatility for asset price being stochasticstochastic

(One reason for a stochastic (One reason for a stochastic volatility in the case of equities is volatility in the case of equities is the relationship between volatility the relationship between volatility and leverage)and leverage)

1111

Volatility Term StructureVolatility Term Structure

In addition to calculating a volatility In addition to calculating a volatility smile, traders also calculate a smile, traders also calculate a volatility term structurevolatility term structure

This shows the variation of implied This shows the variation of implied volatility with the time to maturity of volatility with the time to maturity of the optionthe option

1212

Volatility Term StructureVolatility Term Structure

The volatility term structure tends to The volatility term structure tends to be downward sloping when volatility be downward sloping when volatility is high and upward sloping when it is is high and upward sloping when it is low (mean reversion)low (mean reversion)

1313

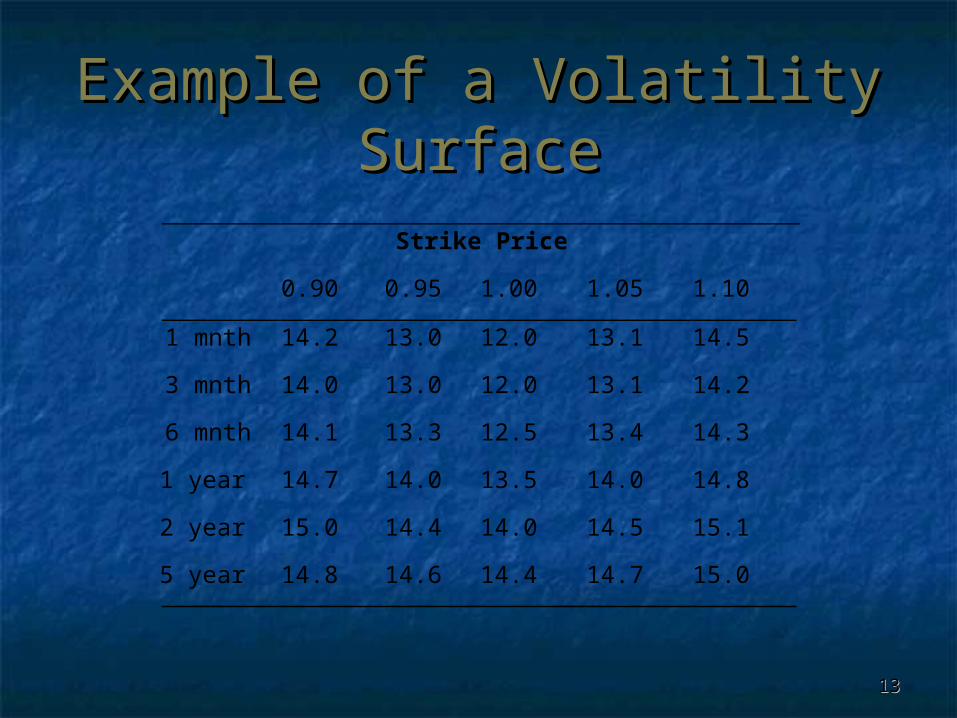

Example of a Volatility Example of a Volatility SurfaceSurface

Strike Price

0.90 0.95 1.00 1.05 1.10

1 mnth 14.2 13.0 12.0 13.1 14.5

3 mnth 14.0 13.0 12.0 13.1 14.2

6 mnth 14.1 13.3 12.5 13.4 14.3

1 year 14.7 14.0 13.5 14.0 14.8

2 year 15.0 14.4 14.0 14.5 15.1

5 year 14.8 14.6 14.4 14.7 15.0

1414

Brief ReviewBrief Review

1515

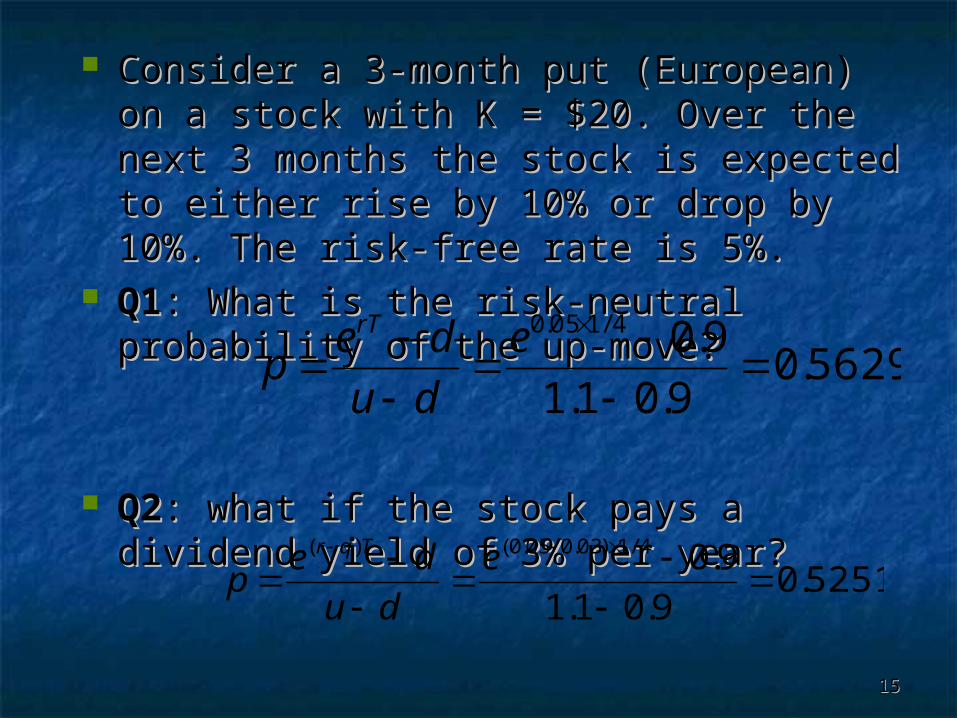

Consider a 3-month put (European) on a Consider a 3-month put (European) on a stock with K = $20. Over the next 3 stock with K = $20. Over the next 3 months the stock is expected to either months the stock is expected to either rise by 10% or drop by 10%. The risk-free rise by 10% or drop by 10%. The risk-free rate is 5%.rate is 5%.

Q1Q1: What is the risk-neutral probability of : What is the risk-neutral probability of the up-move?the up-move?

Q2Q2: what if the stock pays a dividend : what if the stock pays a dividend yield of 3% per year?yield of 3% per year?

5629.09.01.1

9.04/105.0

e

du

dep

rT

5251.09.01.1

9.04/1)03.005.0()(

e

du

dep

Tqr

1616

Q3Q3: What position in the stock is : What position in the stock is necessary to hedge a long position in 1 necessary to hedge a long position in 1 put option (assume no dividends)?put option (assume no dividends)?

Buy 0.5 sharesBuy 0.5 shares Q4Q4: How would the answer to Q3 change : How would the answer to Q3 change

if the stock paid a dividend yield of 3%?if the stock paid a dividend yield of 3%? Q5Q5: What is the value of the put?: What is the value of the put?

5.01822

20

du

du

SS

pp

1717

Assume now that the put has 6 months to Assume now that the put has 6 months to maturity and there are 2 periods on the maturity and there are 2 periods on the tree (each period is 3-moths long). tree (each period is 3-moths long). Everything else is the same.Everything else is the same.

Q6Q6: Compute the value of the put option.: Compute the value of the put option.

Q7Q7: Answer question 6 for an American : Answer question 6 for an American put.put.

Q8Q8: The cost of hedging which option is : The cost of hedging which option is higher – American or European put? higher – American or European put? Compute it for both. Compute Gamma of Compute it for both. Compute Gamma of the European put option. Can you hedge the European put option. Can you hedge your Gamma-exposure by trading futures?your Gamma-exposure by trading futures?

1818

Consider a European call option on FX. The Consider a European call option on FX. The exchange rate is 1.0000 $/FX, the strike exchange rate is 1.0000 $/FX, the strike price is 0.9100, the T is 1 year, the price is 0.9100, the T is 1 year, the domestic risk-free rate is 5% the foreign domestic risk-free rate is 5% the foreign risk-free rate is 3%. If the call is selling for risk-free rate is 3%. If the call is selling for 0.05 $/FX, is there arbitrage and, if so, how 0.05 $/FX, is there arbitrage and, if so, how would you exploit it?would you exploit it?

Hence, borrow and sellHence, borrow and sell units of FX, units of FX, invest the PV of K and buy the call today.invest the PV of K and buy the call today.

At maturity, you have $K which is more At maturity, you have $K which is more than enough to buy the currency.than enough to buy the currency.

1048.005.0 rTTr KeSec f

Trfe

1919

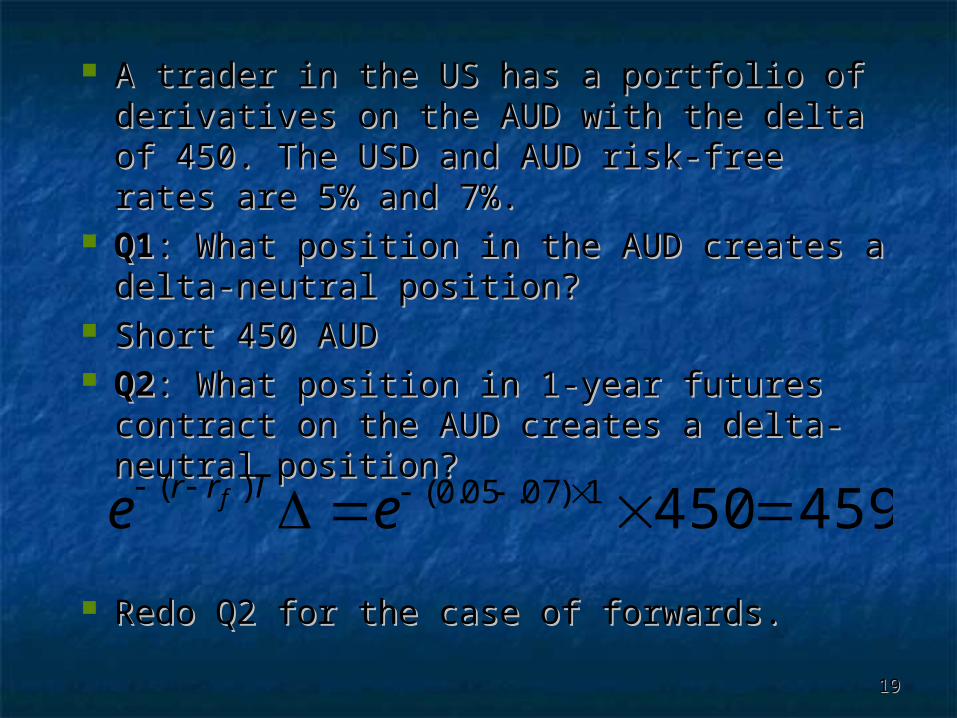

A trader in the US has a portfolio of A trader in the US has a portfolio of derivatives on the AUD with the delta of derivatives on the AUD with the delta of 450. The USD and AUD risk-free rates are 450. The USD and AUD risk-free rates are 5% and 7%.5% and 7%.

Q1Q1: What position in the AUD creates a : What position in the AUD creates a delta-neutral position?delta-neutral position?

Short 450 AUDShort 450 AUD Q2Q2: What position in 1-year futures contract : What position in 1-year futures contract

on the AUD creates a delta-neutral position?on the AUD creates a delta-neutral position?

Redo Q2 for the case of forwards.Redo Q2 for the case of forwards.

4594501)07.05.0()( ee Trr f

2020

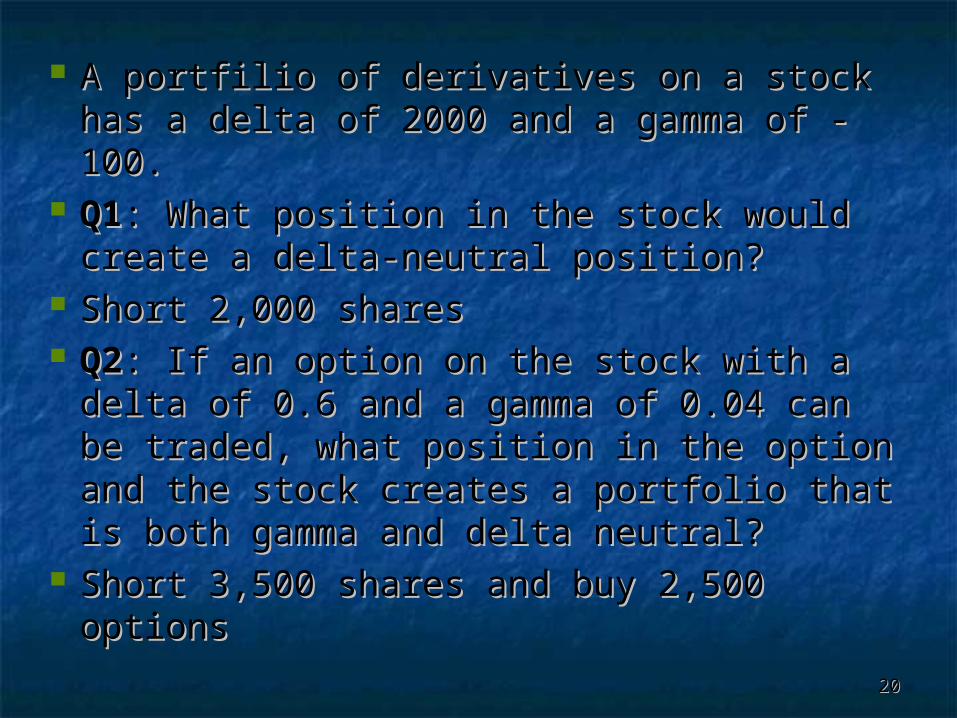

A portfilio of derivatives on a stock has a A portfilio of derivatives on a stock has a delta of 2000 and a gamma of -100.delta of 2000 and a gamma of -100.

Q1Q1: What position in the stock would : What position in the stock would create a delta-neutral position?create a delta-neutral position?

Short 2,000 sharesShort 2,000 shares Q2Q2: If an option on the stock with a delta : If an option on the stock with a delta

of 0.6 and a gamma of 0.04 can be of 0.6 and a gamma of 0.04 can be traded, what position in the option and traded, what position in the option and the stock creates a portfolio that is both the stock creates a portfolio that is both gamma and delta neutral?gamma and delta neutral?

Short 3,500 shares and buy 2,500 Short 3,500 shares and buy 2,500 optionsoptions