Embed Size (px)

Citation preview

1

The UK BSE/FMD Experience and Challenges of Re-Establishing Domestic Markets

David A. BesslerTexas A&M University

September 22, 2008

The research described herein was supported by FAZD Center at Texas A&M and Bruce McCarl, Yanhong Jin, Levan Elbakidze and Aviral Chopra.

All errors are the author’s responsibility.

2

Outline of Presentation

(I) Econ 101: Demand and Supply.

a. Reduction in International Trade.

b. Changes in Domestic Supply and Demand.

(II) Questions On Substitution in Demand for Meat Products.

(III) BSE 1989, BSE 1996 and FMD 2001– Empirical Evidence on

Behavior of Prices.

(IV) Aggregate Effects – Agriculture, Agribusiness, Consumers,

Government.

3

Retail Level Supply and Demand Before and After Loss of International Markets with No Mandatory Slaughter

Ex Ante Demand

Ex Post Demand

Quantity

Price

P2

Ex Post Supply

P1

Ex Ante Supply

Q1 Q2

4

Interpretation of the Previous Slide

With no mandatory supply reduction a loss in markets due to health event (like FMD or BSE) in the domestic herd will result in lower prices domestically.

5

Post-Event Retail Supply and Demand if International Export Trade is Prohibited And Supply is Reduced by

Animal Slaughter

Total Demand Before Event

Supply Before Event

Q1

P1

Quantity

Price

P2

Q2

Reduced Supply

Demand After the Event

6

Interpretation of the Previous Slide

• If international export trade is prohibited and supply is reduced by animal slaughter, price and quantity changes depend on how large the slaughter is relative to loss in demand.

• Without looking at the data, we cannot say, a priori, whether prices will increase or decrease from prohibition of exports and animal slaughter.

• The relevant question is: which is larger, decrease in demand or size of animal slaughter?

7

Post-Event Retail Supply and Demand If Shifts in Supply are Larger than Shifts in Demand

Total Demand Before Event

Supply Before Event

Q1

P1

Quantity

Price

Q2

Post-Event Supply

Post-Event Demand

P2

8

Post-Event Retail Supply and Demand If Shifts in Demand are Much Larger than Shifts in Supply

Total Demand Before Event

Supply Before Event

Q1

P1

Quantity

Price

Q2

Post-Event Supply

Post-Event Demand

P2

9

Interpretation of the Previous Two Slides

• Without looking at the data, Econ 101 doesn’t give precise predictions about how market price will respond to discovery to an animal health event.

• Of course common sense may tell us that shifts in demand will be large relative to shifts in supply, but perhaps not!

10

Farm-Level Demand

• Consumers rarely buy directly from farmers/producers.

• Farmers/Producers sell to marketing service providers (“middlemen”), who process, store, transport, and otherwise add utility, and who sell to the consumer.

• Farm-Level demand is thus “derived” from retail-level demand.

• Without re-doing each of the previous graphs, but now at the farm (producer) level, let me just say a similar set of graphs apply at the producer level.

11

Relative Shifts and Slopes of Curves (Lines) are Fundamental to Assessments of

Ultimate Effects

• The graphs given above are merely indicative of effects.

• Slopes on each of the demand and supply lines may not be constant through time.

• Shifts in lines determine relative size of changes in price and quantity.

12

Substitution in Demand

• The previous analysis has been with respect to one commodity (say beef or pork) or its farm level component (cattle or pigs).

• When we moved (shifted) the demand curve in toward the origin due to health concerns, we are implicitly saying consumers will substitute other products.

• That is, if demand for beef falls, presumably consumers are substituting out of beef and into other products; e.g. poultry, non-meat protein, or non-UK beef (imports of non-UK meat protein), etc.

13

Indictors of How Big These Shifts in Supply and Demand Might Be

• Relative size of animal slaughter.

• Size of export markets for alternative products.

• Size of imports of meat products.

14

2001 Number of Animals Slaughtered for FMD Control by Type and Percentage of Herd-Type

(Source: Thompson, D. et.al. DEFRA, Whithall Place, London, UK)

Animal Type Slaughtered for Disease Control

Slaughtered for Welfare

Total Slaughtered

Approximate Percent

Slaughtered

Cattle 594,000 169,000 763,000 6.8%

Sheep 3,334,000 1,586,000 4,920,000 11.6%

Pigs 145,000 287,000 432,000 6.7%

15

Previous Slide: What Did We See?

Sheep slaughter due to the FMD event was proportionately larger (11.6%) than was slaughter on cattle and pigs (6.8% and 6.7% respectively).

Why might this fact be important? It may predict that prices for sheep may not fall as fast

as those for pigs and cattle because of greater proportional slaughter for sheep.

But wait! What about demand?

16

UK Animal and Animal Products Exported to European Union 1999-2000

(Source Peter Midmore, Institute of Rural Studies, University of Wales, Aberystwyth)

Animal Type

1999

Exports to EU

(‘000 tonnes)

1999

% of UK Animal Output

1999

Farm

Gate Value

(£ Million)

2000

Exports to EU

(‘000 tonnes)

2000

% of UK Animal Output

2000

Farm

Gate Value

(£ Million)

Cattle and calves

10 1.5% 30.3 9 1.3% 25.6

Sheep and Lambs

153 38.0% 380.0 124 31.8% 249.8

Pigs and Pig Meat

6 2.6% 20.3 9 4.2% 34.9

Milk, Butter and Cheese Not Included

17

What Did We See in the Previous Slide?

Sheep exports from the UK to Europe are proportionately larger (~35% of quantity produced) than cattle and pig exports to the UK (~ 1.4% of production and ~3.4%, respectively).

Why might this fact be important? While sheep slaughter due to the event was greater, proportionately

than that for cattle and pigs, the sheep industry also (presumably) lost greater share of the market. So the ultimate effects of controls on supply (slaughter) and demand (loss in exports markets) may not be clear.

But wait again!

What about substitution among meat products?

18

Ceteris Paribus

All of the previous graphs are constructed under the assumption of Ceteris Paribus (all other things held constant).

Of course the world doesn’t stop for anyone or at least any academic.

19

To investigate how actual prices behaved in the United Kingdom we investigate price declines in a neighborhood of three real events:

-- The 1989 discovery of BSE in the UK cattle herd. This was not linked to human health.

-- The 1996 discovery of BSE and the association of BSE with human health.

-- The 2001 discovery of FMD in the British pig crop and subsequent transfer to lamb and cattle.

20

• We fit a vector auto-regression on farm-level, wholesale level and retail–level price data measured weekly on cattle, sheep, pigs and poultry.

• We forecasted future prices using only information known before the event was known to the market and contrast these forecasted prices with actual prices over the subsequent 24 months.

• Our interest is in assessing the differential effect (if any) the three major meat events had on prices.

21

DATA

• Data provided by Department of Environmental Food and Rural Affairs (DEFRA), United Kingdom (UK).

• Consists of Real Daily prices at the Producer Level– Cattle – Lamb – Pigs– Poultry

• Period : January 1985 to December 2002.

22

Compare Actual Prices with Forecasted Prices

Build a VAR Model on Prices of Cattle, Pigs, Sheep and Poultry.

Forecast depends on only information known before discovery.

Out interest is observing whether the forecast lies above or below what actually occurred.

23

Cattle Price

1991 199285

90

95

100

105

110

115

Sheep Price

1991 1992100

125

150

175

200

225

250

Pig Price

1991 199280

90

100

110

120

130

Poultry Price

1991 199254

55

56

57

58

59

60

61

62

63

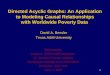

Figure 4. Forecasted Prices and Realized Prices (pence per kilogram) of Livestock Products over the Period November 1989 – October 1991.

Key: ------ Forecasted Prices based on information known before November 1989 _____ Realized (Actual) Prices

24

What Did We See in the Previous Slide?

For the 1989 BSE event cattle prices actually were above what they were forecast4ed to be based on information known just before the BSE event was known to the public.

Sheep and Poultry were actually below what they were forecasted to be before the event.

Generally the 1989 BSE event had no lasting affect on cattle market prices.

25

Cattle Price

1996 199785

90

95

100

105

110

115

120

125

Sheep Price

1996 1997150

200

250

300

350

400

450

Pig Price

1996 199780

90

100

110

120

130

140

150

160

Poultry Price

1996 199752

54

56

58

60

62

64

66

Figure 5. Forecasted Prices and Realized Prices (pence per kilogram) of Livestock Products over the Period March 1996 – March 1998.

Key: ------ Forecasted Prices based on information known before February 2001 _____ Realized (Actual) Prices

26

What Did We See in the Previous Slide?

For the BSE event cattle prices declined and never recovered.

Other prices were generally above their pre-event forecasted levels.

27

Cattle Price

2001 200282.5

85.0

87.5

90.0

92.5

95.0

97.5

100.0

Sheep Price

2001 2002150

175

200

225

250

275

300

Pig Price

2001 200270

75

80

85

90

95

100

105

110

Poultry Price

2001 200245.5

46.0

46.5

47.0

47.5

48.0

48.5

49.0

49.5

Figure 6. Forecasted Prices and Realized Prices (pence per kilogram) of Livestock Products over the Period February 2001 – February 2003.

Key: ------ Forecasted Prices based on information known before February 2001 _____ Realized (Actual) Prices

28

What Did We See in the Previous Slide?

.

For the FMD event when markets re-opened prices were above their pre-event forecasted levels.

Speaking colloquially, one might initially think poultry producers and retailers had “no dog in either the BSE or FMD fight.” Poultry is not affected directly by FMD, or BSE for that matter, but we see (through, perhaps, protein substitutions) that prices are not un-touched by these events.

29

Summary

• We see market prices actually did adjust to lost markets. These adjustments occurred almost immediately.

• Consumers did not move away from affected meat products in the 1989 BSE and the 2001 FMD events (evidence the poultry results – retail poultry prices fell to compete with increased quantities of beef, lamb and pork).

• When compared to 1996 BSE event, the 2001FMD and 1989 BSE events losses for commodity producers seem transitory rather than permanent.

• Perhaps the linking the 1996 BSE event to human health and death was the reason cattle prices never recovered after the 1996 BSE event.

30

Some Additional Thoughts

• Markets can and do take care of adjustments once the public is assured of the safety of the food product.

• Deeper analysis of welfare gains and losses requires more detailed information.

• I’ve not covered the additional consideration of tourism. Arguably, the short-run effects of FMD on tourism may have been greater than the above mentioned effects on agriculture (see Scott, et,al Jo. Rural Studies 2004).

31

Thank You