Embed Size (px)

Citation preview

1

THE NEWS-BASED APPROACH TO EXCHANGE RATES AND THE

ECONOMETRICS OF SHORT-TERM TRADING

University of Greenwich ECON1083 Global Macroeconomics - Module 5

Massimo Tivegna

University of Teramo, Italy

2

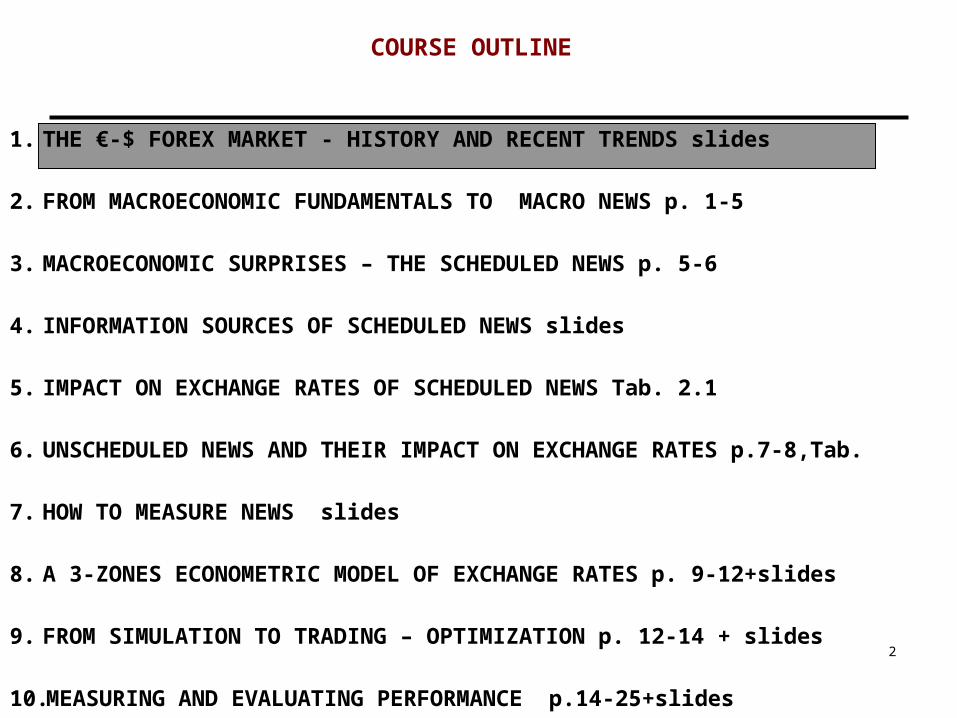

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS slides

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS p. 1-5

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS p. 5-6

4. INFORMATION SOURCES OF SCHEDULED NEWS slides

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS Tab. 2.1

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES p.7-8,Tab.

7. HOW TO MEASURE NEWS slides

8. A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES p. 9-12+slides

9. FROM SIMULATION TO TRADING – OPTIMIZATION p. 12-14 + slides

10.MEASURING AND EVALUATING PERFORMANCE p.14-25+slides

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

A CHECKLIST OF THE FOREX MARKET

• General Features • Instruments exchanged• Trading • Forecasting Techniques for trading• Forex Market Microstructure• The role of Central Banks and their operations

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

GENERAL FEATURES

• Open 24 hours a day • Quoting currency pairs• Number and ranking of currencies• Who trades, where, when, why, how• Postwar history at glance• Instruments exchanged

– Spot, Forward,Swaps,Futures, Options

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

FROM MEDIUM TERM TO DAY-TRADING• Position Trading with a Multicurrency Portfolio (several

days) • Hedging

– On Real and Financial Assets – On Payables and Receivables – For Offsetting Payments Flows – For Asset Management

• Day-trading as a separate asset class

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

Forecasting Techniques for Trading • Technical Analysis• Snooping “professional” Behaviours and Hints (herding

and insider trading) • Rumours and news trading• Econometric Models from Various Theories and

Frequencies• The LONG – SHORT terminology

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

Microstructure • Order flows• Payment and trading circuits (e.g.EBS,www.ebs.com) • Trading over the Internet(e.g.Oanda,IG Markets,

Saxobank, etc.)• High-frequency information (e.g. Bloomberg, Reuters,

Dow Jones, etc.)• Online consulting services, free and fee (e.g.

Forexfactory, Forexpros, RANsquawk, etc.)• Carry trades

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

Role and Operations of Central Banks • European Central Bank• The Federal Reserve System, Fed • Bank of England, The Old Lady• Bank of Japan• Reserve Bank of Australia

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

• Notation: €-$ (EUR-USD) £-$ (STG-USD)

• From the “Legacy Currencies” to the Euro: The Role of the DM and the Bundesbank

• The Dimension of the Currency Market

• The Euro and the British Pound

• Cross exchange rates

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

EUR-USD DailyAt 4PM EST (Source Reuters, WSJ) - From Jan. 4,1999 To Present

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

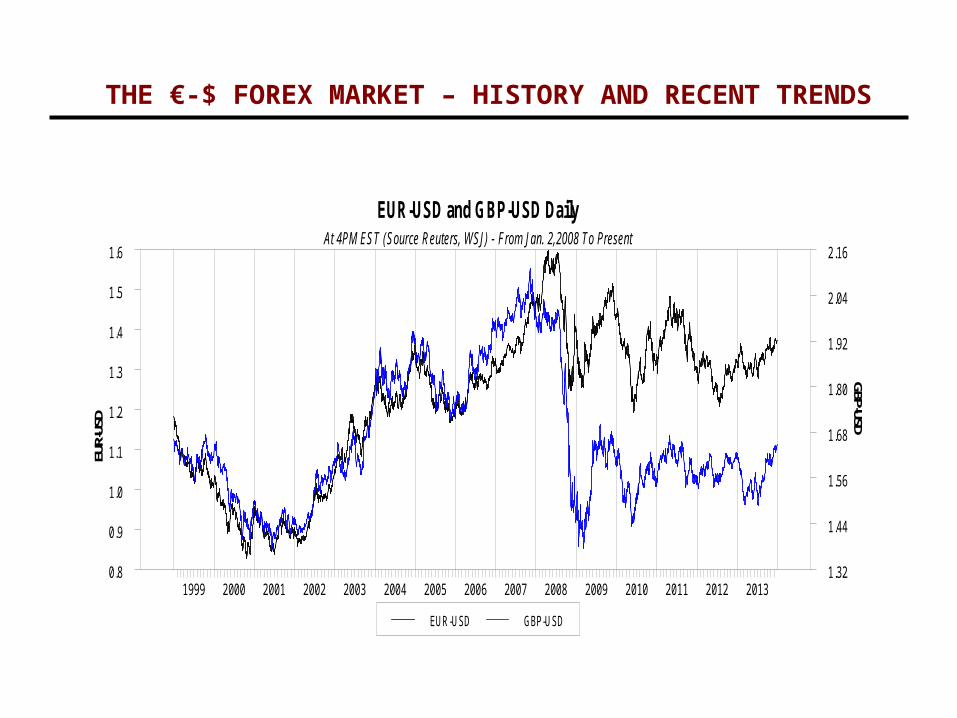

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

EUR-USD GBP-USD

EUR-USD and GBP-USD DailyAt 4PM EST (Source Reuters, WSJ) - From Jan. 2,2008 To Present

EUR-

USD

GBP-USD

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.32

1.44

1.56

1.68

1.80

1.92

2.04

2.16

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

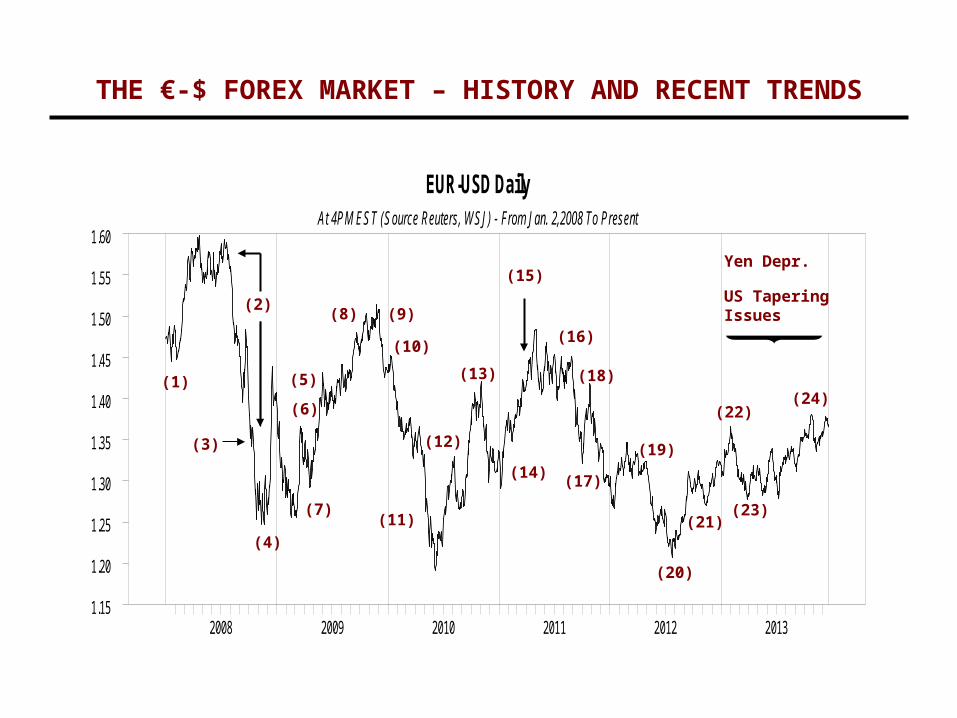

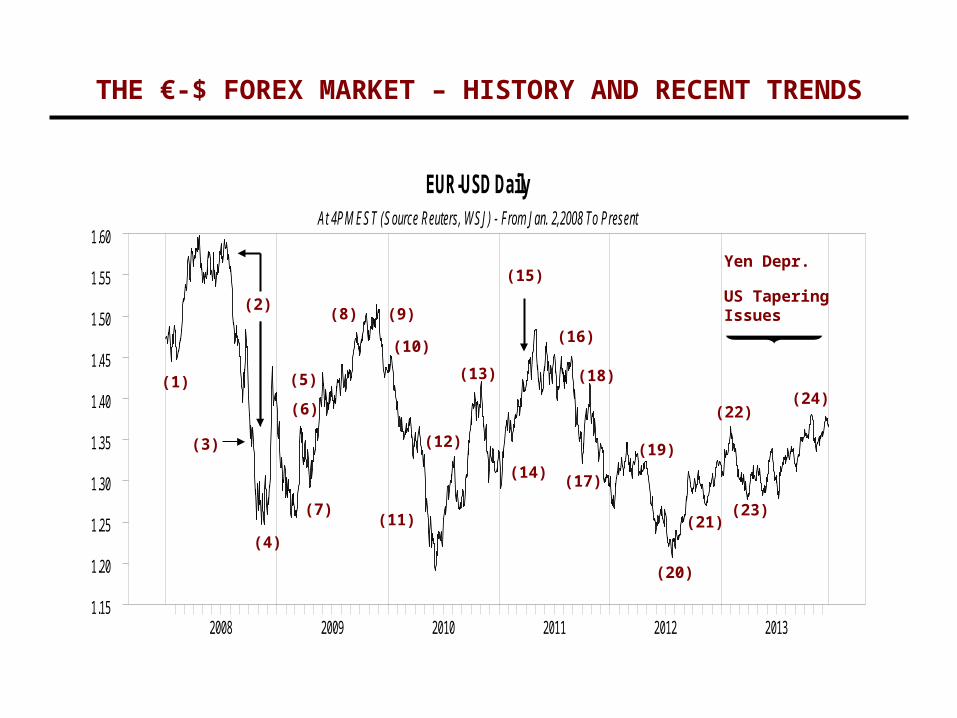

EUR-USD DailyAt 4PM EST (Source Reuters, WSJ) - From Jan. 2,2008 To Present

2008 2009 2010 2011 2012 20131.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

(1)

(2)

(3)

(4)

(6)

(5)

(7)

(8) (9)

(10)

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

(21)

(22)

(23)

(24)

Yen Depr.

US TaperingIssues

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

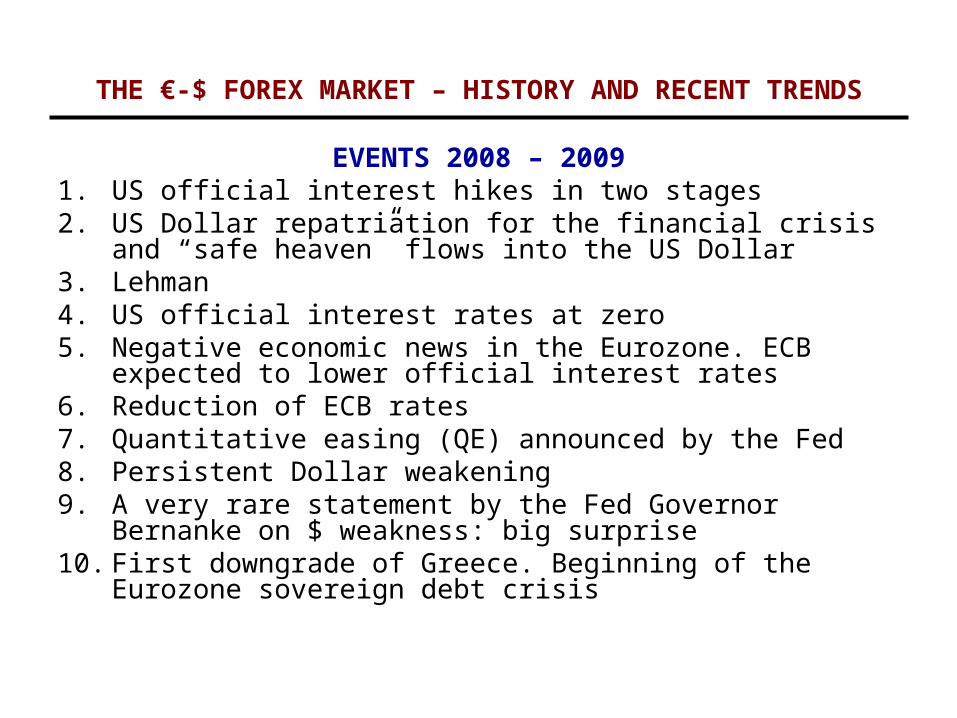

EVENTS 2008 – 20091. US official interest hikes in two stages2. US Dollar repatriation for the financial crisis and “safe

heaven” flows into the US Dollar3. Lehman4. US official interest rates at zero5. Negative economic news in the Eurozone. ECB expected to

lower official interest rates6. Reduction of ECB rates7. Quantitative easing (QE) announced by the Fed8. Persistent Dollar weakening 9. A very rare statement by the Fed Governor Bernanke on $

weakness: big surprise 10. First downgrade of Greece. Beginning of the Eurozone

sovereign debt crisis

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

EUR-USD DailyAt 4PM EST (Source Reuters, WSJ) - From Jan. 2,2008 To Present

2008 2009 2010 2011 2012 20131.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

(1)

(2)

(3)

(4)

(6)

(5)

(7)

(8) (9)

(10)

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

(21)

(22)

(23)

(24)

Yen Depr.

US TaperingIssues

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

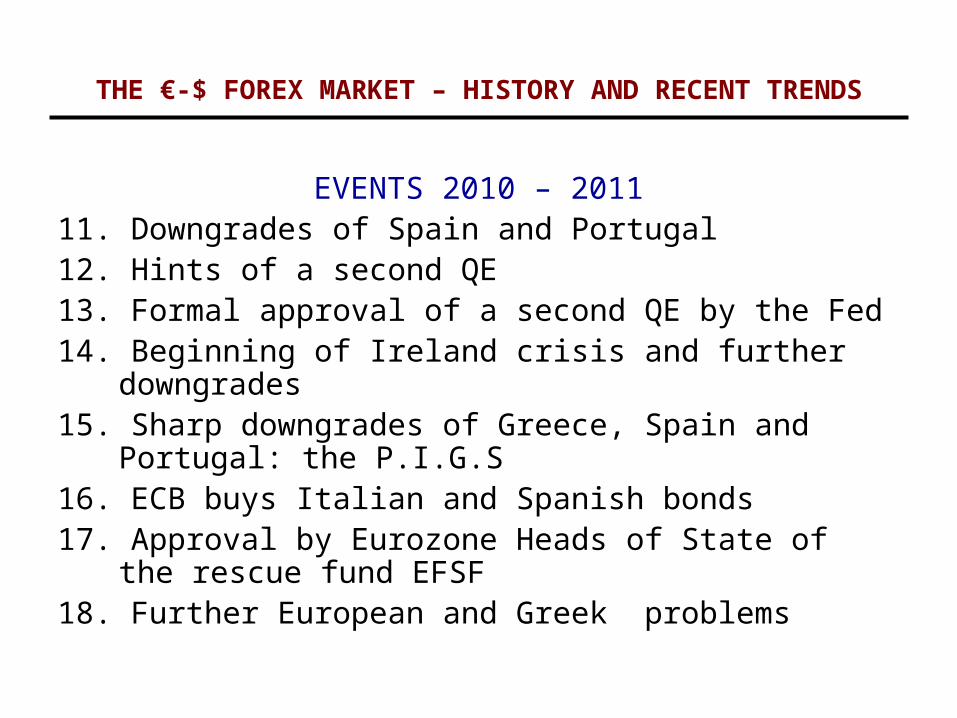

EVENTS 2010 – 201111. Downgrades of Spain and Portugal12. Hints of a second QE13. Formal approval of a second QE by the Fed14. Beginning of Ireland crisis and further downgrades15. Sharp downgrades of Greece, Spain and Portugal: the

P.I.G.S 16. ECB buys Italian and Spanish bonds17. Approval by Eurozone Heads of State of the rescue

fund EFSF18. Further European and Greek problems

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

EUR-USD DailyAt 4PM EST (Source Reuters, WSJ) - From Jan. 2,2008 To Present

2008 2009 2010 2011 2012 20131.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

(1)

(2)

(3)

(4)

(6)

(5)

(7)

(8) (9)

(10)

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

(20)

(21)

(22)

(23)

(24)

Yen Depr.

US TaperingIssues

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

EVENTS 2012 – 201319 .Hollande victory in France. Two Greek elections.

Further Eurozone difficulties20. ECB Governor Draghi’s “ECB will do whatever it takes

to preserve the Euro”21. Improvement in the Greek economic outlook22. A rare statement by Draghi on currencies23. Solution of the Cyprus banking crisis 24. ECB official interest rates cut

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

36

37

38

39

40

41

42

43

44

4546

47

48

49

50

51

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

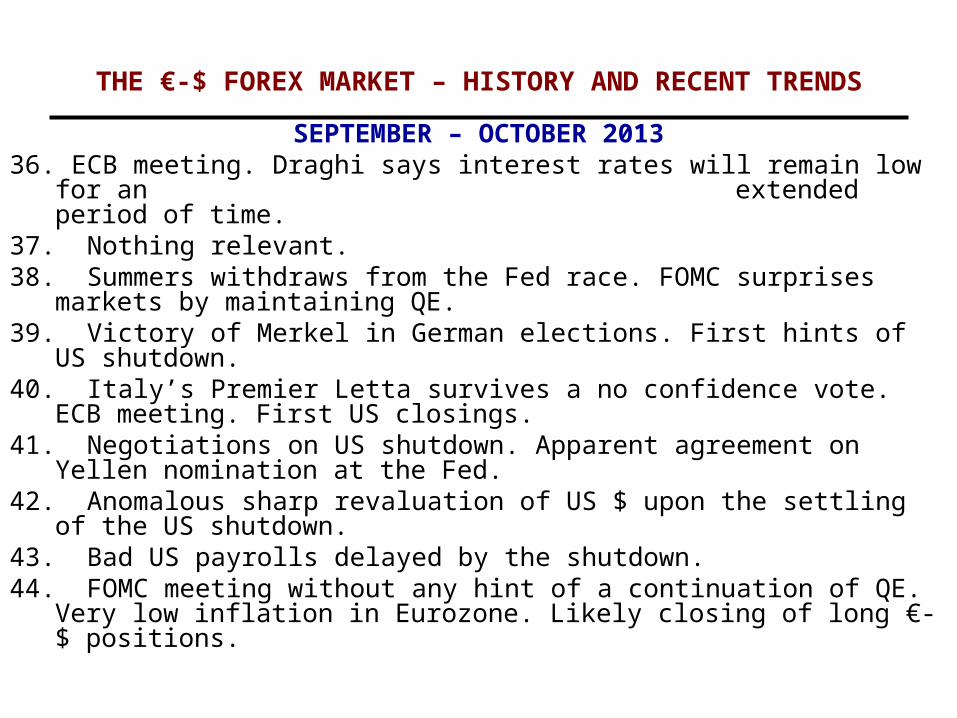

SEPTEMBER – OCTOBER 201336. ECB meeting. Draghi says interest rates will remain low for an

extended period of time.37. Nothing relevant.38. Summers withdraws from the Fed race. FOMC surprises markets

by maintaining QE.39. Victory of Merkel in German elections. First hints of US shutdown.40. Italy’s Premier Letta survives a no confidence vote. ECB meeting.

First US closings.41. Negotiations on US shutdown. Apparent agreement on Yellen

nomination at the Fed.42. Anomalous sharp revaluation of US $ upon the settling of the US

shutdown.43. Bad US payrolls delayed by the shutdown. 44. FOMC meeting without any hint of a continuation of QE. Very low

inflation in Eurozone. Likely closing of long €-$ positions.

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

36

37

38

39

40

41

42

43

44

4546

47

48

49

50

51

THE €-$ FOREX MARKET – HISTORY AND RECENT TRENDS

NOVEMBER – DECEMBER 201345. ECB cuts rates at regular meeting46. Nothing relevant47. Minutes of the of the FOMC with offsetting messages

on tapering QE48. Nothing relevant49. ECB meeting 50. Nothing relevant51. FOMC meeting: first steps away from QE. The Fed will

reduce its monthly buying of US bonds from 85 to 75 billions per month.

23

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS IMPACT ON EXCHANGE RATES

8. A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

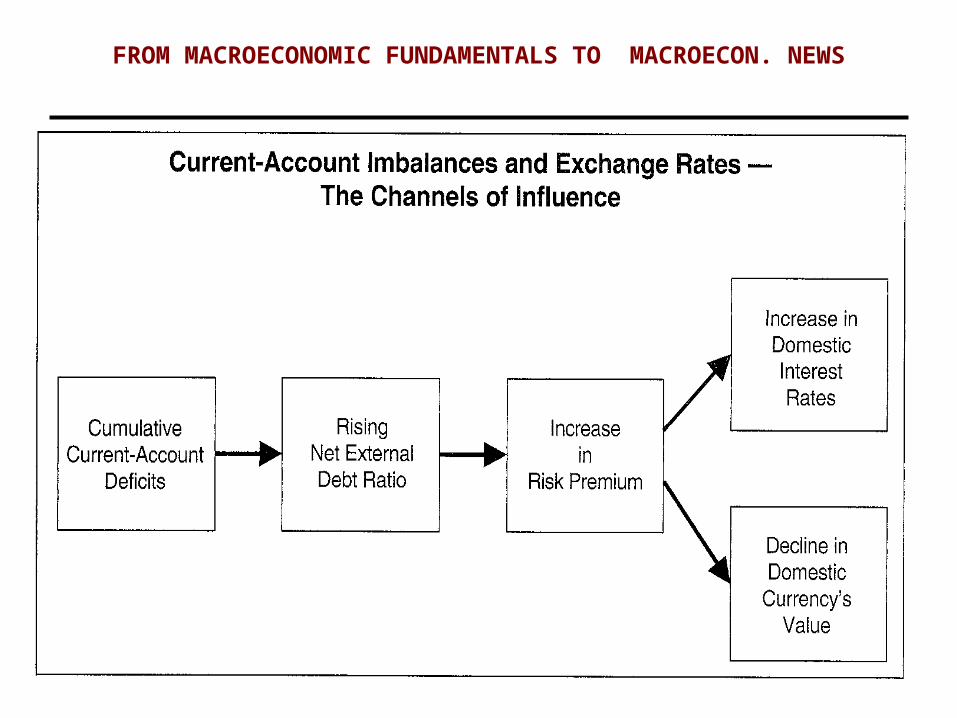

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

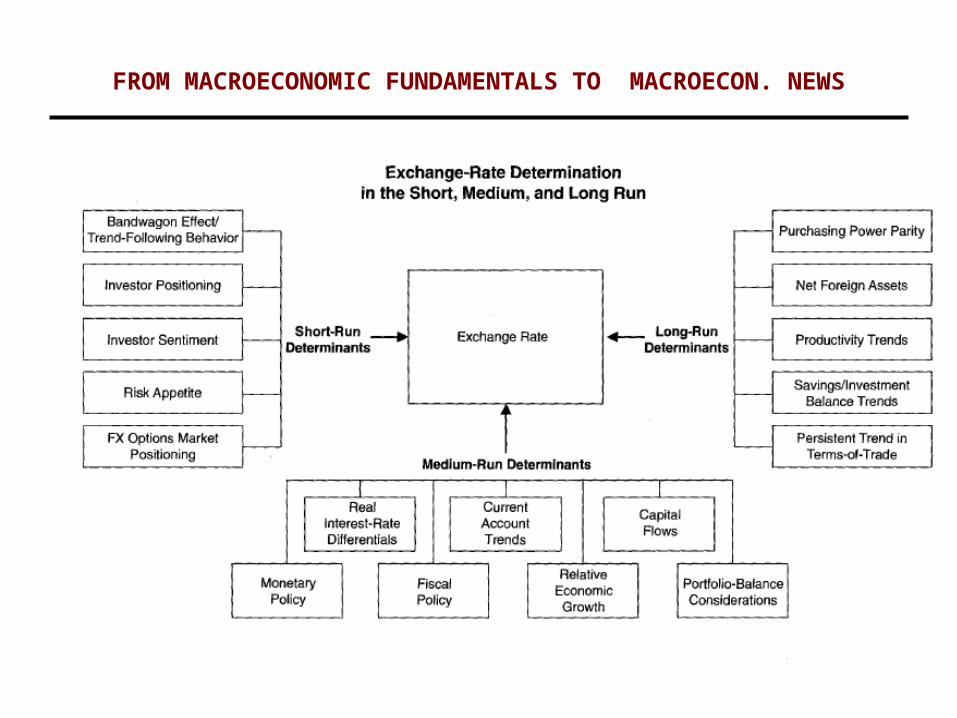

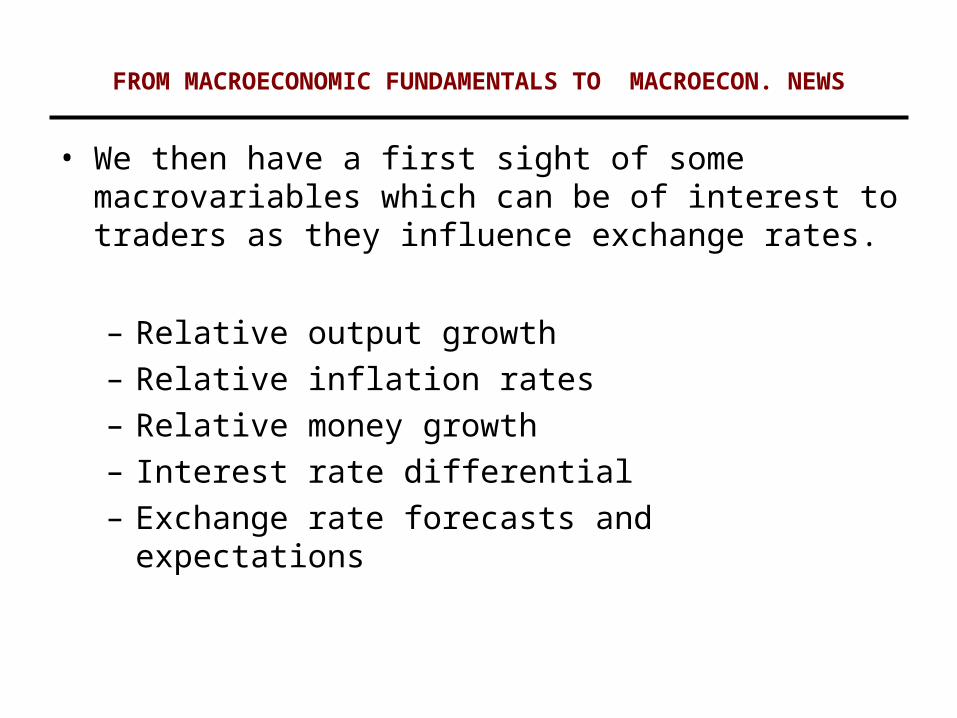

• We then have a first sight of some macrovariables which can be of interest to traders as they influence exchange rates.

– Relative output growth– Relative inflation rates– Relative money growth– Interest rate differential– Exchange rate forecasts and expectations

FROM MACROECONOMIC FUNDAMENTALS TO MACROECON. NEWS

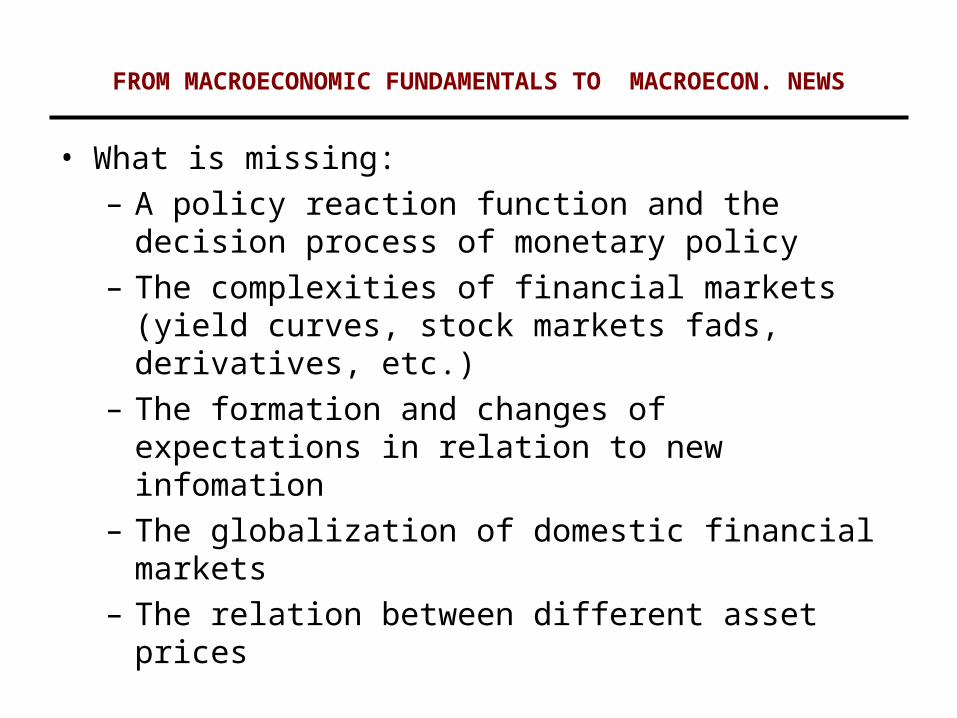

• What is missing:– A policy reaction function and the decision process of

monetary policy– The complexities of financial markets (yield curves,

stock markets fads, derivatives, etc.) – The formation and changes of expectations in relation

to new infomation – The globalization of domestic financial markets– The relation between different asset prices

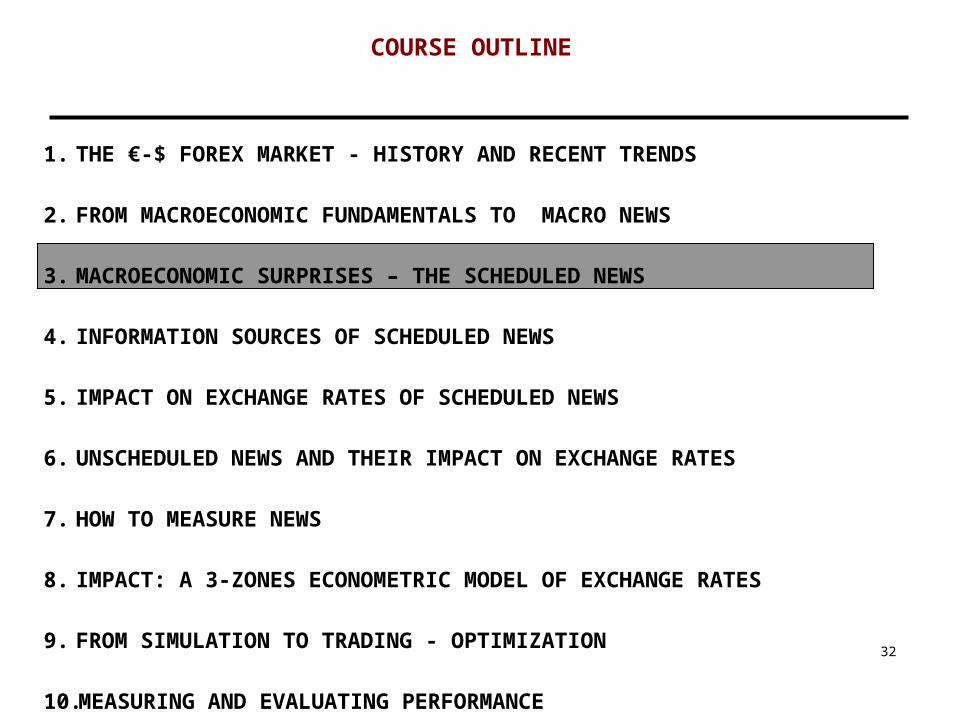

32

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. IMPACT: A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

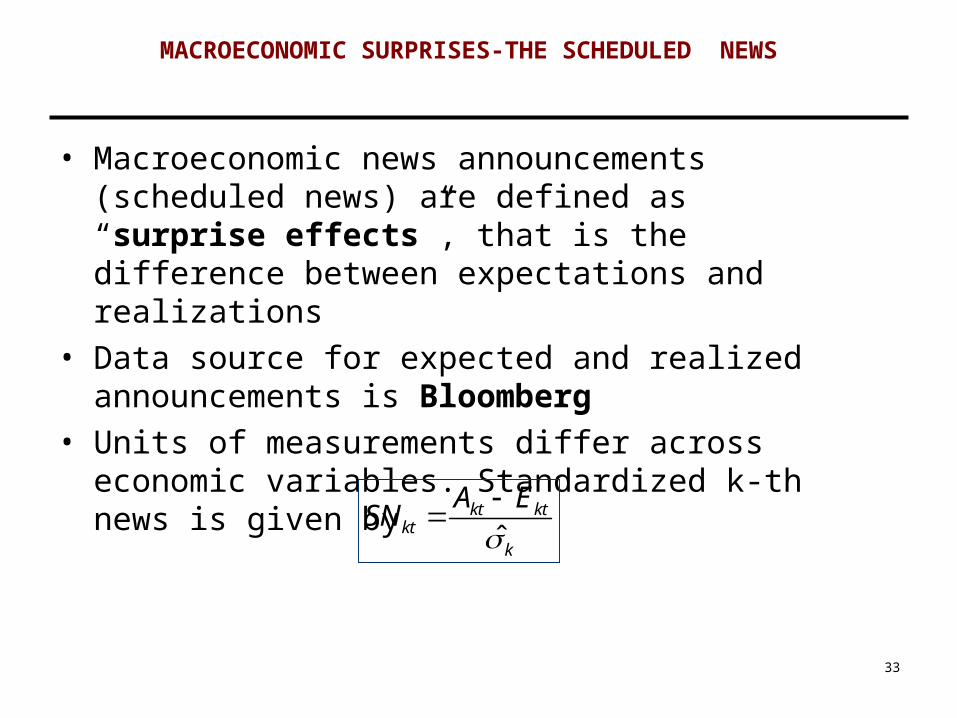

33

• Macroeconomic news announcements (scheduled news) are defined as “surprise effects”, that is the difference between expectations and realizations

• Data source for expected and realized announcements is Bloomberg

• Units of measurements differ across economic variables. Standardized k-th news is given by

ˆkt kt

ktk

A ESN

MACROECONOMIC SURPRISES-THE SCHEDULED NEWS

34

Scheduled News Frequency Measurement Unit Impact on €-$ Source

1 2 3 4

US Announcements

Forward-Looking Indicators

Non-farm Payrolls Monthly Units Negative Bloomberg

Initial Jobless Claims Monthly Units Negative Bloomberg

ISM (formerly NAPM) Manufatcture Index Monthly Diffusion Index Negative Bloomberg

ISM (formerly NAPM) Services Index Monthly Diffusion Index Negative Bloomberg

ISM (formerly NAPM) Chicago Monthly Diffusion Index Negative Bloomberg

Manufacture Index Philadelphia Fed Monthly Diffusion Index Negative Bloomberg

Consumer Confidence, Conference Board Monthly Weighted Index Negative Bloomberg

Consumer Confidence, Univ. of Michigan Monthly Weighted Index Negative Bloomberg

Leading Indicators Monthly % Var. Monthly Negative Bloomberg

MACROECONOMIC SURPRISES-THE SCHEDULED NEWS MAIN SCHEDULED NEWS IN ETZ ED ATZ

35

Scheduled News Frequency Measurement Unit Impact on €-$ Source

1 2 3 4

US Announcements

Other Indicators

Unemployment Rate Monthly Percentage Positive Bloomberg

Wage Rate, Non Farm Monthly % Var. Monthly Negative Bloomberg

Deflatore del GDP Monthly % Var. Quarterly Negative Bloomberg

Consumer Price Index Monthly % Var. Monthly Negative Bloomberg

Producer Price Index Monthly % Var. Monthly Negative Bloomberg

Producer Price Index,excl. Food&Energy Monthly % Var. Monthly Negative Bloomberg

GDP(advance,preliminary,final) Monthly % Var. Quarterly Negative Bloomberg

MACROECONOMIC SURPRISES-THE SCHEDULED NEWS MAIN SCHEDULED NEWS IN ETZ ED ATZ

36

Scheduled News Frequency Measurement Unit Impact on €-$ Source

1 2 3 4

US Announcements

Other Indicators

Retail Sales Monthly % Var. Monthly Negative Bloomberg

Retail Sales excl. Automobiles Monthly % Var. Monthly Negative Bloomberg

Industrial Production Monthly % Var. Monthly Negative Bloomberg

Durable Goods Monthly % Var. Monthly Negative Bloomberg

Factory Orders Monthly % Var. Monthly Negative Bloomberg

Personal Income Monthly % Var. Monthly Negative Bloomberg

Personal Consumption Monthly % Var. Monthly Negative Bloomberg

Trade Balance Monthly Billions di $ Negative Bloomberg

Current Account Balance Quarterly Billions di $ Negative Bloomberg

MACROECONOMIC SURPRISES-THE SCHEDULED NEWS MAIN SCHEDULED NEWS IN ETZ ED ATZ

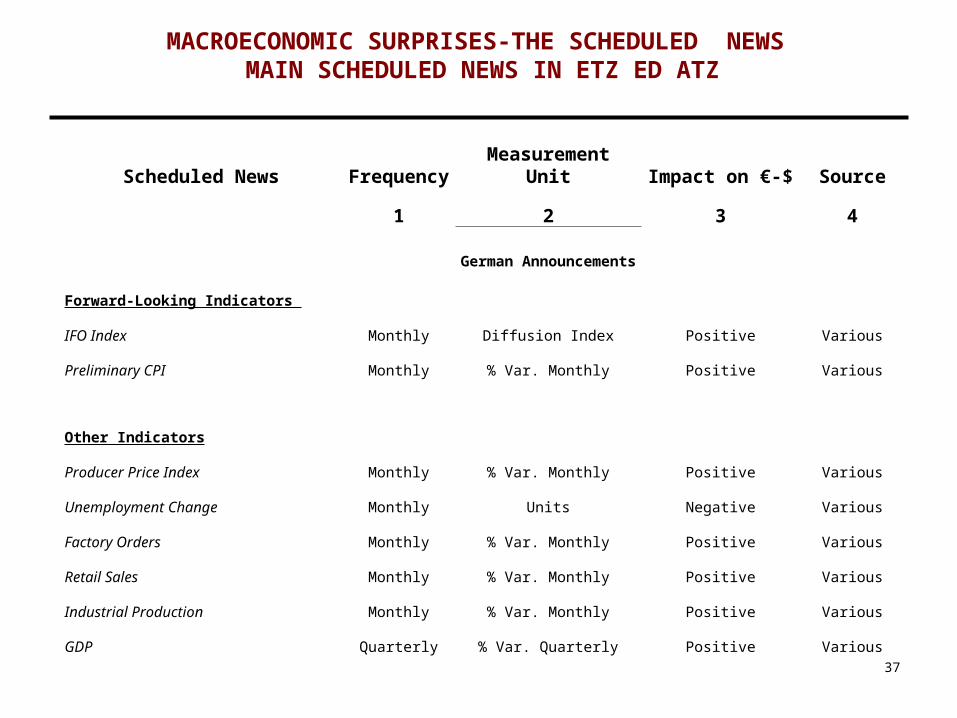

37

Scheduled News Frequency Measurement Unit Impact on €-$ Source

1 2 3 4

German Announcements

Forward-Looking Indicators

IFO Index Monthly Diffusion Index Positive Various

Preliminary CPI Monthly % Var. Monthly Positive Various

Other Indicators

Producer Price Index Monthly % Var. Monthly Positive Various

Unemployment Change Monthly Units Negative Various

Factory Orders Monthly % Var. Monthly Positive Various

Retail Sales Monthly % Var. Monthly Positive Various

Industrial Production Monthly % Var. Monthly Positive Various

GDP Quarterly % Var. Quarterly Positive Various

MACROECONOMIC SURPRISES-THE SCHEDULED NEWS MAIN SCHEDULED NEWS IN ETZ ED ATZ

38

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. IMPACT: A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

INFORMATION SOURCES OF SCHEDULED NEWS

• Bloomberg, Reuters. The most reliable and expensive.• ForexFactory has the best cost-quality ratio (but there

could be equivalent ones)• Find your favoured one and stick to it (but occasionally

checking elsewhere).• Establish (with experience) your metrics of the news

impact as trading is a highly personal business.

40

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. IMPACT: A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

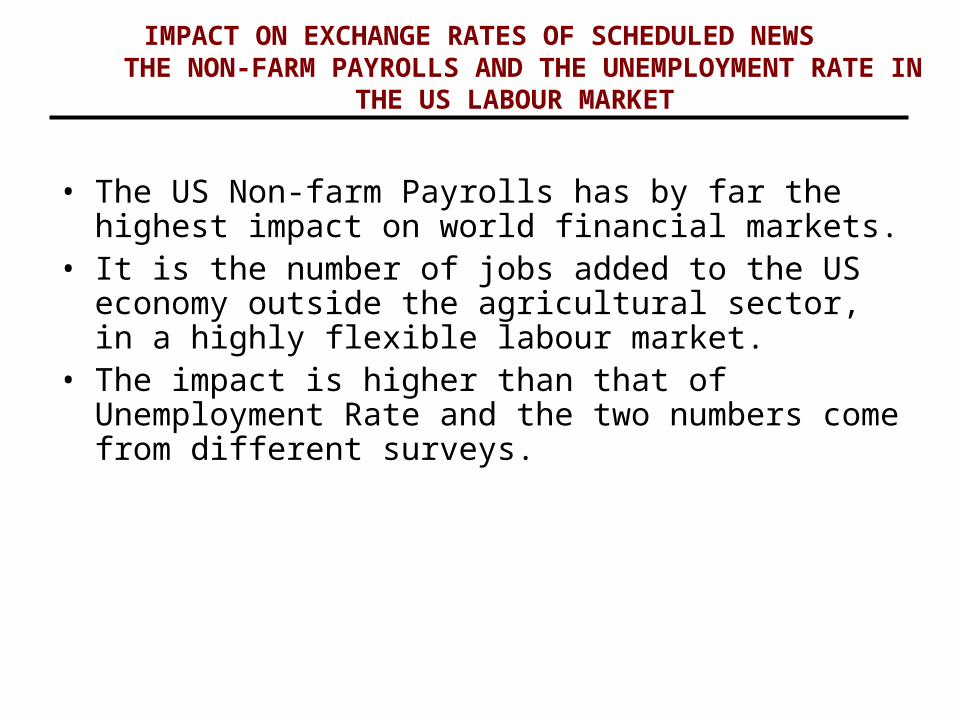

IMPACT ON EXCHANGE RATES OF SCHEDULED NEWSTHE NON-FARM PAYROLLS AND THE UNEMPLOYMENT RATE IN

THE US LABOUR MARKET

• The US Non-farm Payrolls has by far the highest impact on world financial markets.

• It is the number of jobs added to the US economy outside the agricultural sector, in a highly flexible labour market.

• The impact is higher than that of Unemployment Rate and the two numbers come from different surveys.

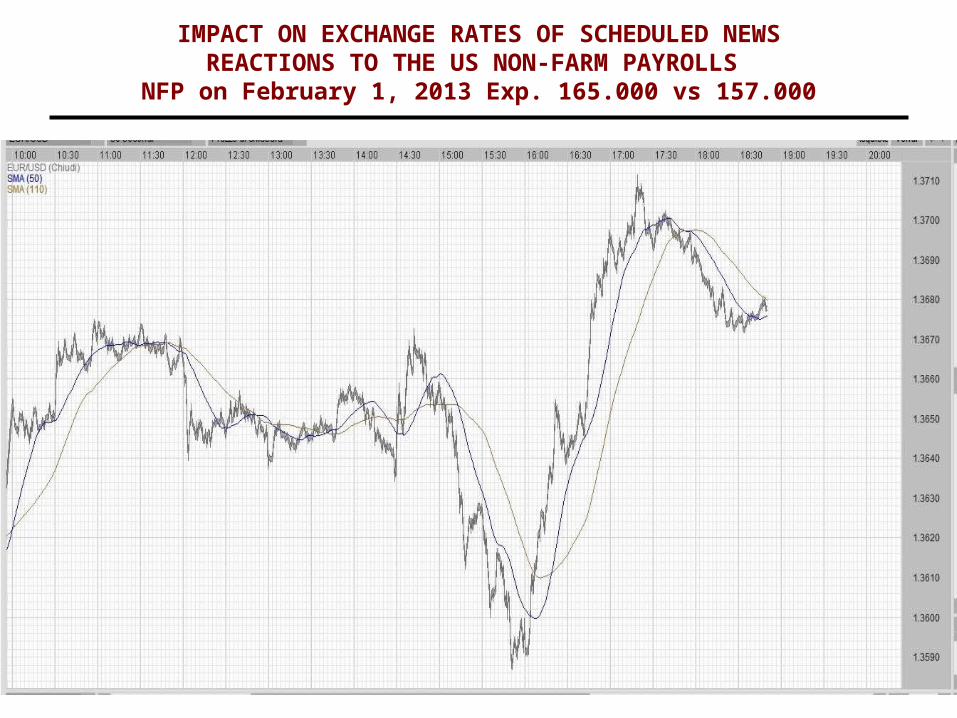

IMPACT ON EXCHANGE RATES OF SCHEDULED NEWSREACTIONS TO THE US NON-FARM PAYROLLS

• In the following two slides we have the €-$ reactions in the last two months:

• The first chart indicates a reaction to a 160.000 Expected and a 236.000 Actual with unemployment rate going down.

• The second chart indicates a reaction to a 165.000 Expected and a 157.000 actual, with unemployment rate going up.

IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

REACTIONS TO THE US NON-FARM PAYROLLS NFP on March 8: Exp. 160.000 vs 236.000

IMPACT ON EXCHANGE RATES OF SCHEDULED NEWSREACTIONS TO THE US NON-FARM PAYROLLS NFP on February 1, 2013 Exp. 165.000 vs 157.000

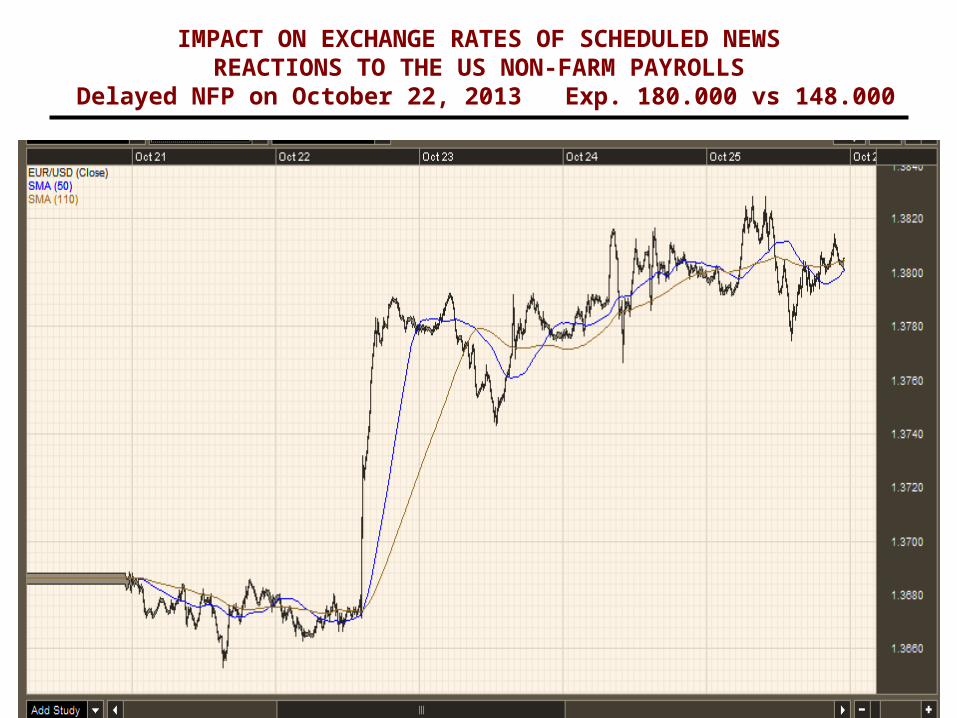

IMPACT ON EXCHANGE RATES OF SCHEDULED NEWSREACTIONS TO THE US NON-FARM PAYROLLS

Delayed NFP on October 22, 2013 Exp. 180.000 vs 148.000

IMPACT ON EXCHANGE RATES OF SCHEDULED NEWSREACTIONS TO THE US NON-FARM PAYROLLS

NFP on November 8, 2013 Exp. 120.000 vs 204.000

47

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

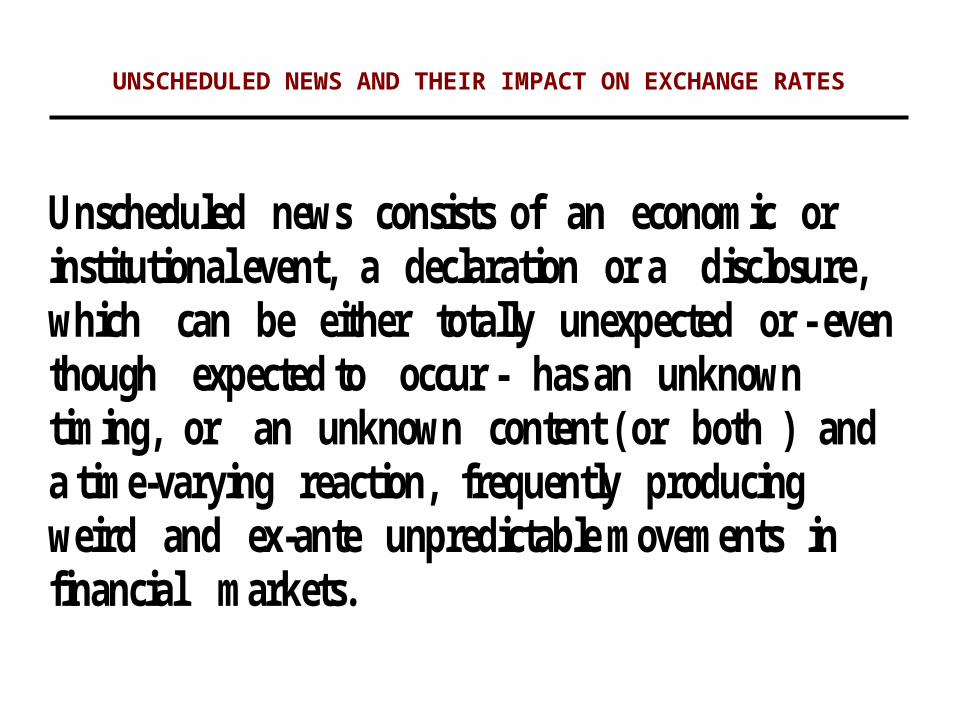

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

Unscheduled news consists of an economic or institutional event, a declaration or a disclosure, which can be either totally unexpected or - even though expected to occur - has an unknown timing, or an unknown content ( or both ) and a time-varying reaction, frequently producing weird and ex-ante unpredictable movements in financial markets.

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATESGRADUAL RESULTS OF THE ITALIAN ELECTIONS

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATESREACTION (MONDAY, JTZ) TO THE CRISIS OF THE MONTI GOVERNMENT

IN ITALY (ON FRIDAY, IN ATZ)

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

Public interventions by Central Banks in the foreign exchange market or statements by the same source announcing or threatening them ( Japanese Authorities is a good example).

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCH. RATESECB RATE SETTING AND PRESS CONFERENCE FEB.7,2013

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

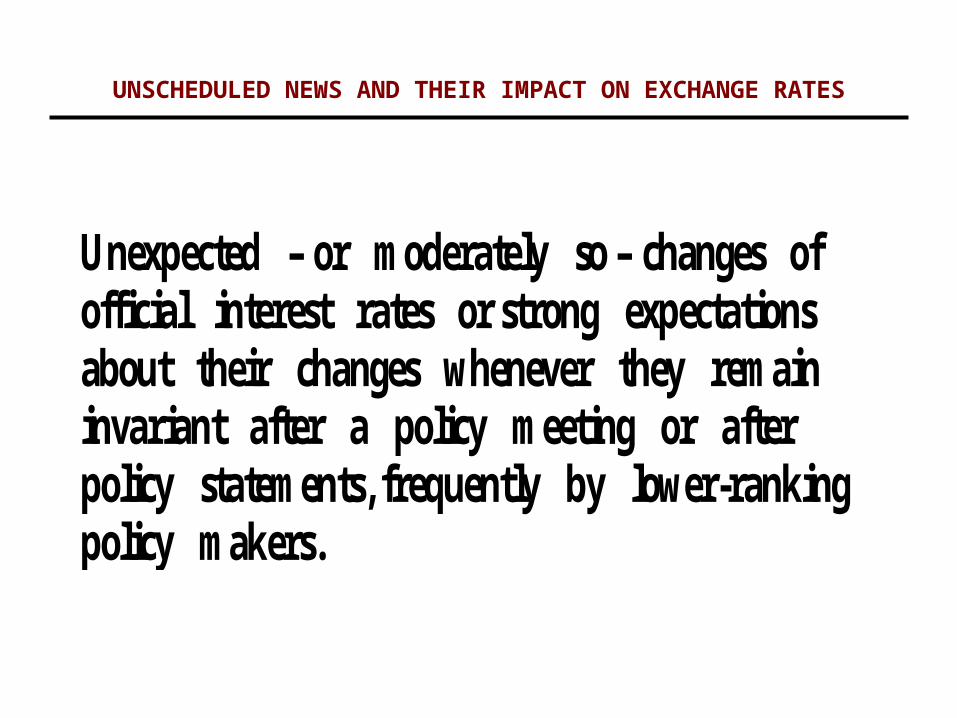

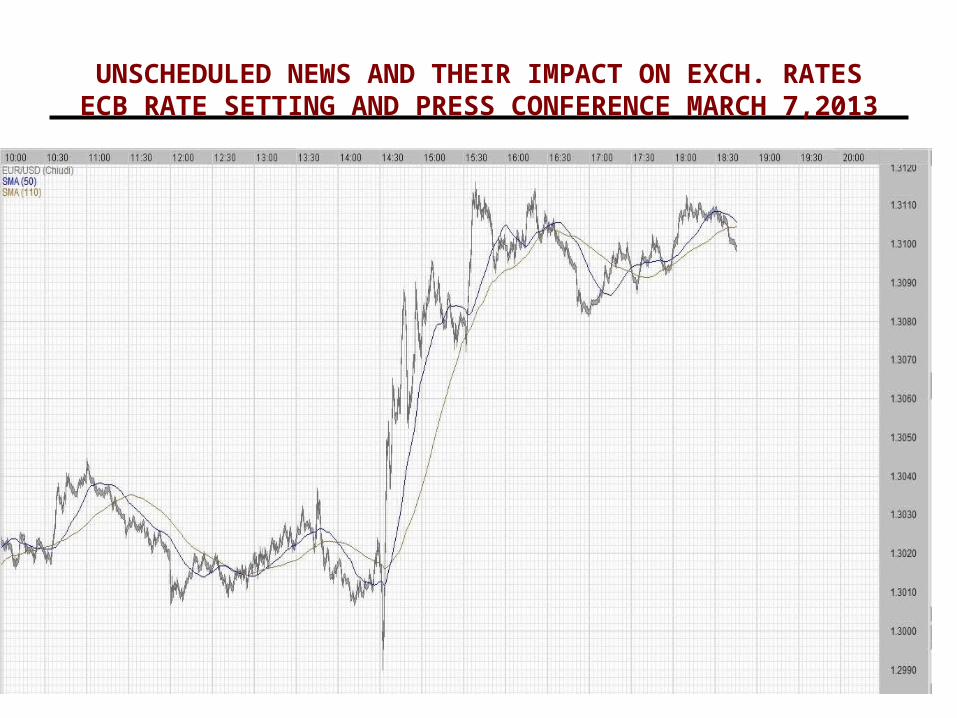

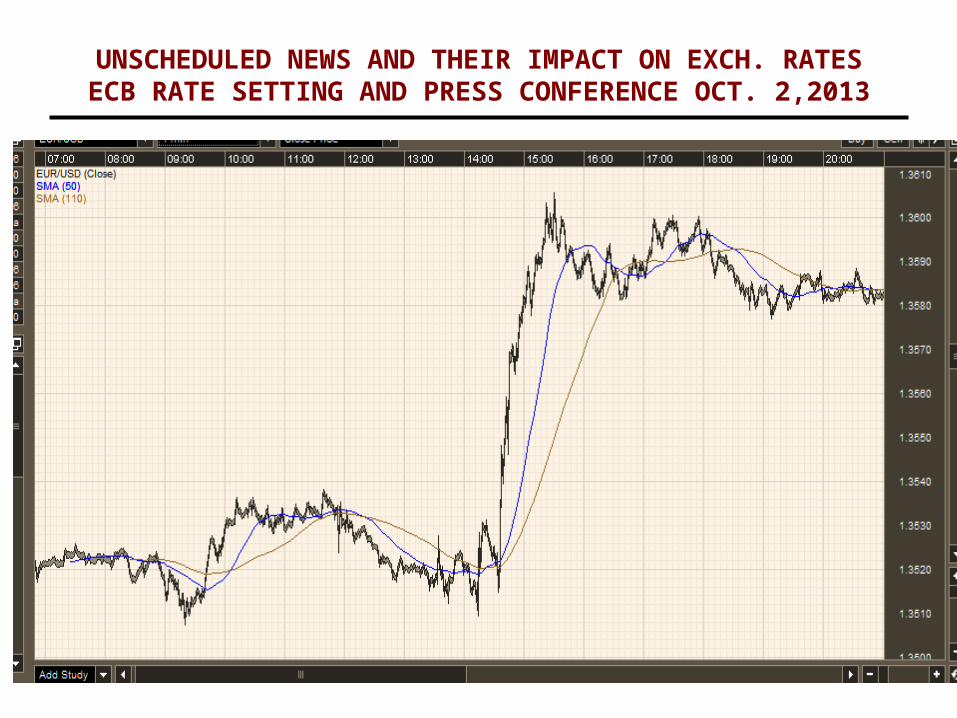

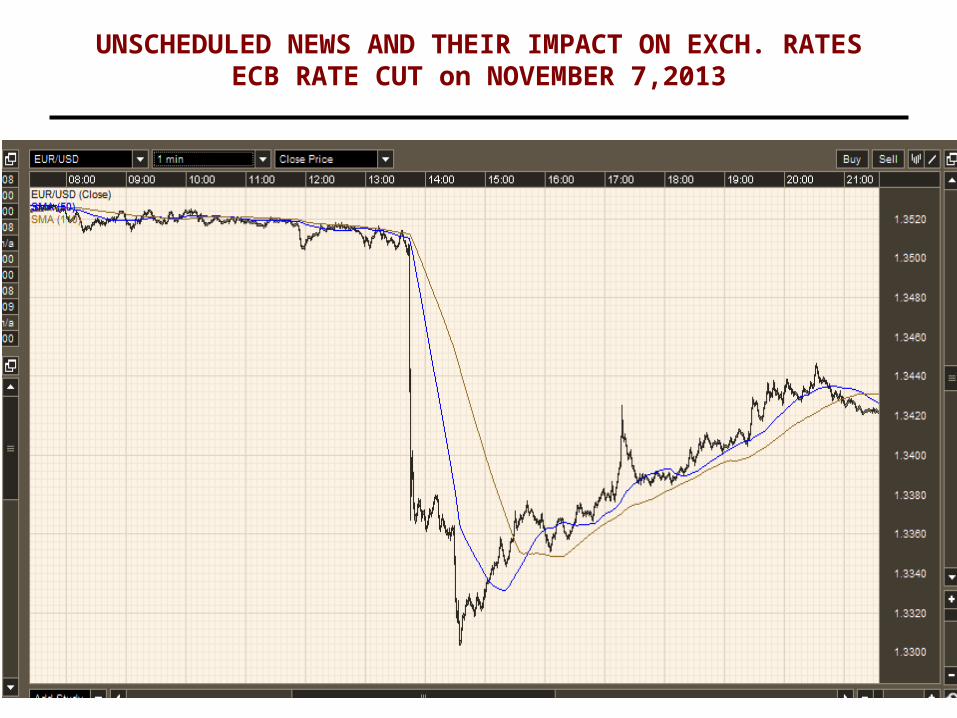

Unexpected – or moderately so – changes of official interest rates or strong expectations about their changes whenever they remain invariant after a policy meeting or after policy statements, frequently by lower-ranking policy makers.

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCH. RATESECB RATE SETTING AND PRESS CONFERENCE MARCH 7,2013

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCH. RATESECB RATE SETTING AND PRESS CONFERENCE OCT. 2,2013

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCH. RATESECB RATE CUT on NOVEMBER 7,2013

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCH. RATESECB RATE SETTING AND PRESS CONFERENCE DEC. 5,2013

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCH. RATESUS FOMC COMUNIQUE’ OCTOBER 30,2013

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

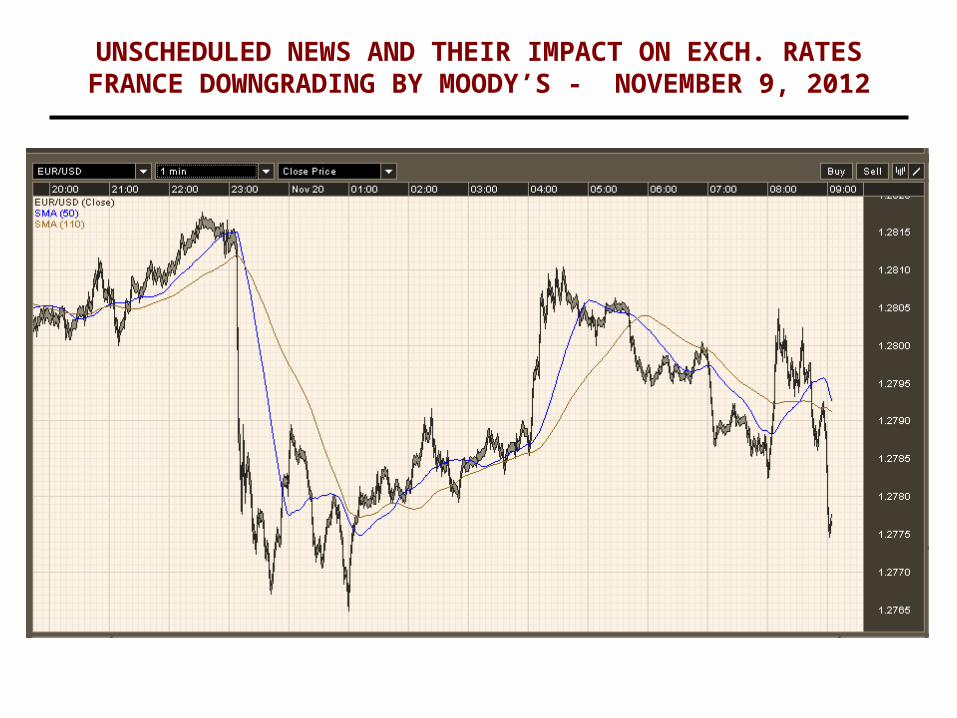

Unexpected – or moderately so - upgrading or downgrading by Rating Agencies or official Institutions of entire countries or important financial Institutions.

UNSCHEDULED NEWS AND THEIR IMPACT ON EXCH. RATESFRANCE DOWNGRADING BY MOODY’S - NOVEMBER 9, 2012

61

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. IMPACT: A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

HOW TO MEASURE NEWS SCHEDULED NEWS

• SCHEDULED NEWS can be measured in 2 metric scales.

• The news scale measured by the standardized difference between ACTUAL VALUE (A) published in the newswires and EXPECTED VALUE (E) as computed by specialized Agencies.

• The impact on exchange rate as measured by the standard. variation over the 3 Time Zones.

ˆkt kt

ktk

A ESN

(€-$)ATZ – (€-$)ETZ

Stand.Error(ATZ-ETZ)

HOW TO MEASURE NEWS – SCHEDULED NEWSACTUAL AND EXPECTED NON-FARM PAYROLLS (NFP)

Date Act.NFP Exp.NFP Act-Exp STAND.(Act-Exp)

2011.01.07 103 160 -57 -0.56272011.02.04 36 140 -104 -1.02672011.03.04 192 200 -8 -0.07892011.04.01 216 200 16 0.15792011.05.06 244 185 59 0.58242011.06.03 54 170 -116 -1.14522011.07.08 18 105 -87 -0.85892011.08.05 117 75 42 0.41462011.09.02 0 60 -60 -0.59232011.10.07 103 65 38 0.37512011.11.04 80 90 -10 -0.09872011.12.02 120 131 -11 -0.10852012.01.06 200 150 50 0.49362012.02.03 243 135 108 1.06622012.03.09 227 204 23 0.2272012.04.06 120 201 -81 -0.79962012.05.04 115 165 -50 -0.49362012.06.01 69 150 -81 -0.79962012.07.06 80 90 -10 -0.09872012.08.03 163 100 63 0.62192012.09.07 96 125 -29 -0.28632012.10.05 114 113 1 0.0098

STANDARD ERROR OF ACTUAL LESS EXPECTED: 101.29

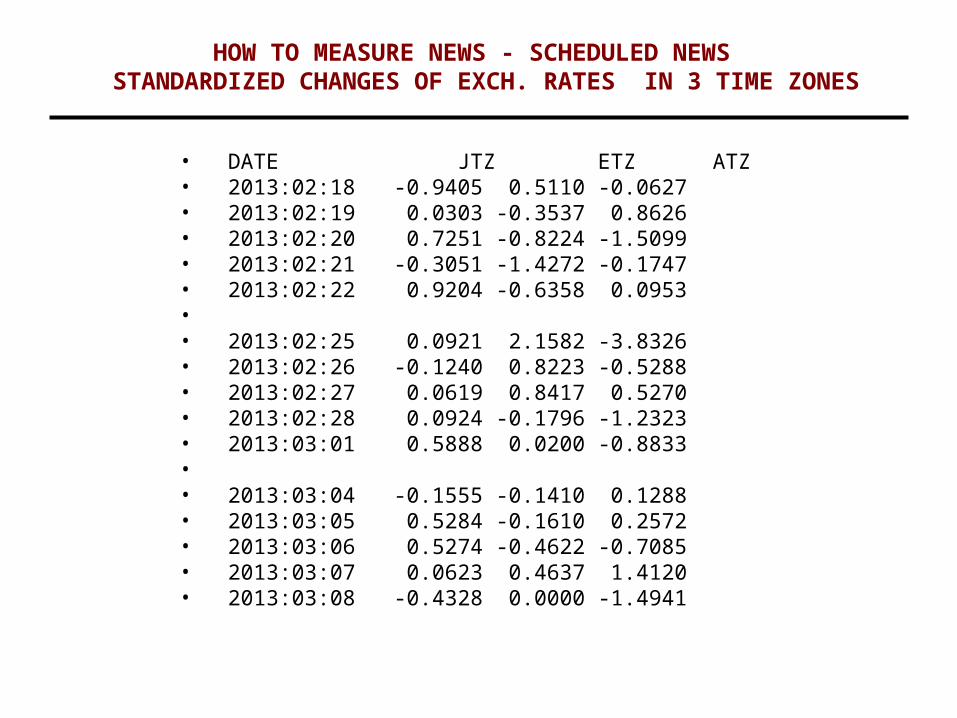

HOW TO MEASURE NEWS - SCHEDULED NEWS STANDARDIZED CHANGES OF EXCH. RATES IN 3 TIME ZONES

• DATE JTZ ETZ ATZ• 2013:02:18 -0.9405 0.5110 -0.0627• 2013:02:19 0.0303 -0.3537 0.8626• 2013:02:20 0.7251 -0.8224 -1.5099• 2013:02:21 -0.3051 -1.4272 -0.1747• 2013:02:22 0.9204 -0.6358 0.0953• • 2013:02:25 0.0921 2.1582 -3.8326• 2013:02:26 -0.1240 0.8223 -0.5288• 2013:02:27 0.0619 0.8417 0.5270• 2013:02:28 0.0924 -0.1796 -1.2323• 2013:03:01 0.5888 0.0200 -0.8833• • 2013:03:04 -0.1555 -0.1410 0.1288• 2013:03:05 0.5284 -0.1610 0.2572• 2013:03:06 0.5274 -0.4622 -0.7085• 2013:03:07 0.0623 0.4637 1.4120• 2013:03:08 -0.4328 0.0000 -1.4941

65

+1 €-$-Positive, $-¥-Negative, £-$-Positive News

- 1 €-$ or £-$ - Negative News, $-¥-Positive

0 No news

HOW TO MEASURE NEWS - UNSCHEDULED NEWS

66

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. IMPACT: A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

67

GT Day(t-1)

Global Trading Day

(t)

21:00 5:00 13:00 21:00

JAPANESETIME ZONE

EUROPEANTIME ZONE

AMERICANTIME ZONE

(t-1)

A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES3 TRADING ZONES IN THE GLOBAL TRADING DAY

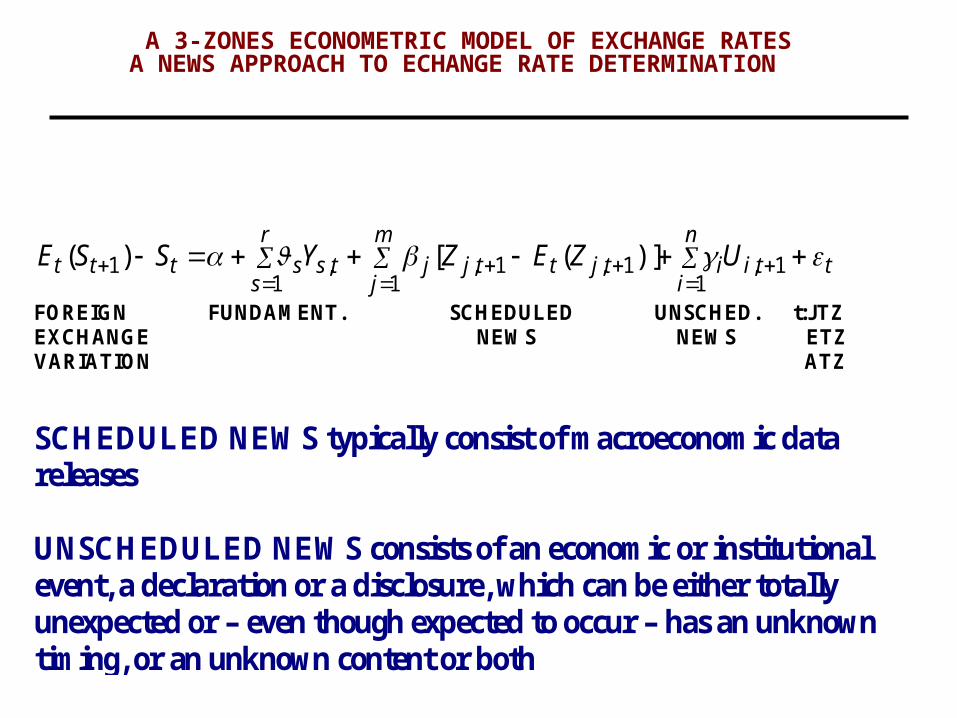

FOREIGN FUNDAMENT. SCHEDULED UNSCHED. t:JTZ EXCHANGE NEWS NEWS ETZ VARIATION ATZ

SCHEDULED NEWS typically consist of macroeconomic data releases UNSCHEDULED NEWS consists of an economic or institutional event, a declaration or a disclosure, which can be either totally unexpected or – even though expected to occur – has an unknown timing, or an unknown content or both

ttin

iitjttj

m

jjts

r

ssttt UZEZYSSE

1,

11,1,

1,

11 )]([)(

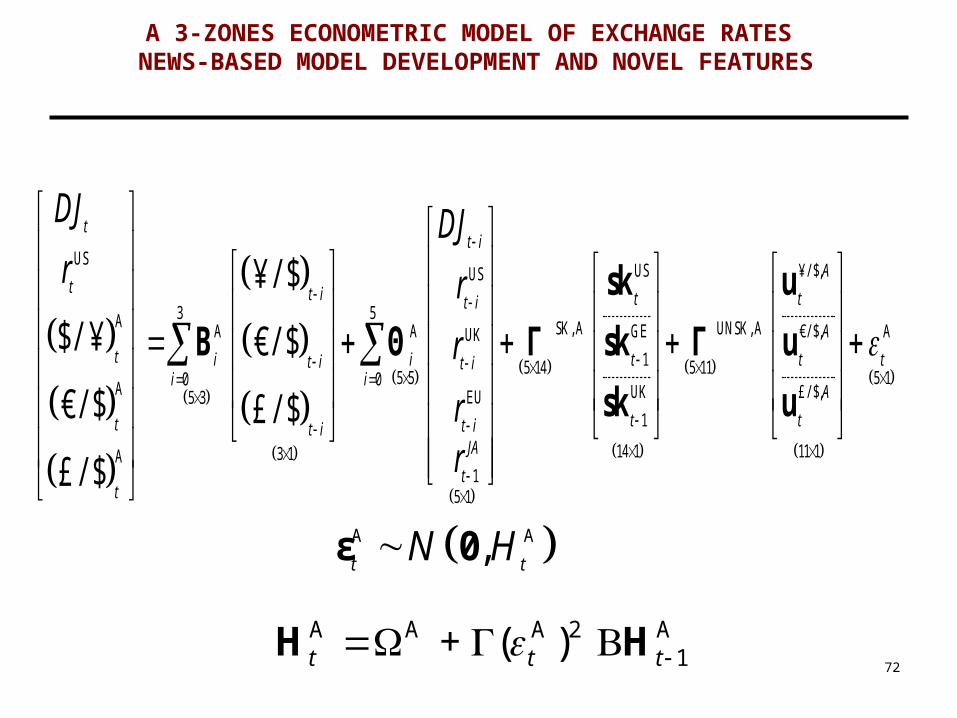

A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATESA NEWS APPROACH TO ECHANGE RATE DETERMINATION

A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

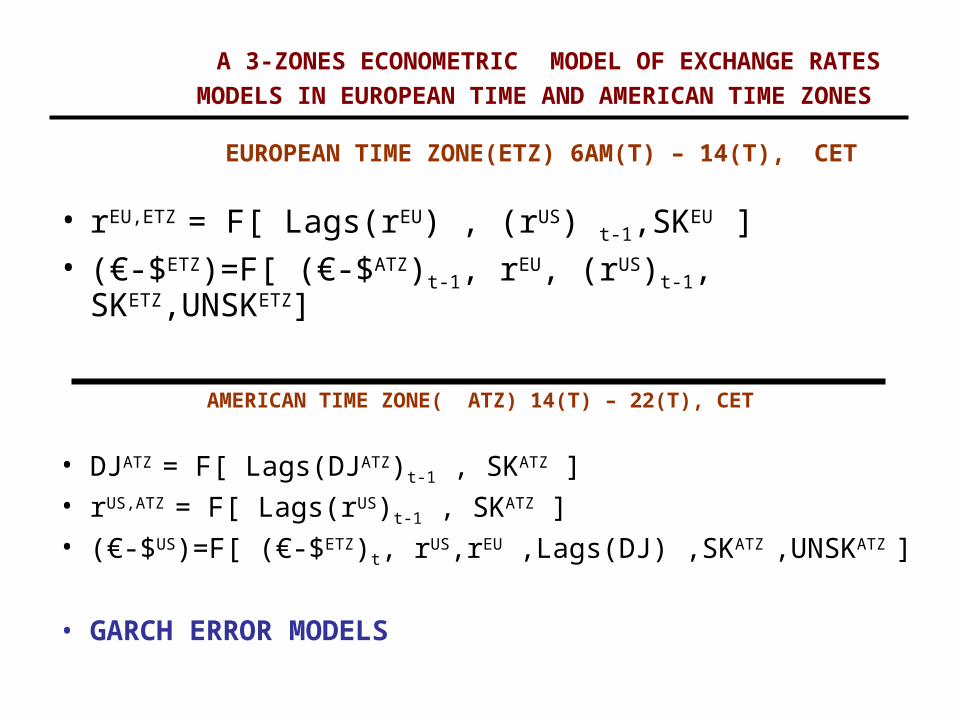

MODELS IN EUROPEAN TIME AND AMERICAN TIME ZONES

EUROPEAN TIME ZONE(ETZ) 6AM(T) – 14(T), CET

• rEU,ETZ = F[ Lags(rEU) , (rUS) t-1,SKEU ]• (€-$ETZ)=F[ (€-$ATZ)t-1, rEU, (rUS)t-1, SKETZ,UNSKETZ]

AMERICAN TIME ZONE( ATZ) 14(T) – 22(T), CET

• DJATZ = F[ Lags(DJATZ)t-1 , SKATZ ]• rUS,ATZ = F[ Lags(rUS)t-1 , SKATZ ]• (€-$US)=F[ (€-$ETZ)t, rUS,rEU ,Lags(DJ) ,SKATZ ,UNSKATZ ]

• GARCH ERROR MODELS

70

E E,t tN Hε 0

E E E 2 E1 + ( ) t t t H H

3

03 9 3 12

3 3 3 1

23 1 3 1 9 1 12 1

Β Γ

u

Γ u

u

sk

sk ε

sk

$/ ¥,

SK, E UNSK, EE €/ $,

£ / $,

( )

$/$/€/ $ €/ $£/ $ £/ $

i

t

t

t

UK EE

tt itE GE E E

i t tt t iE

US Et tt i

¥¥

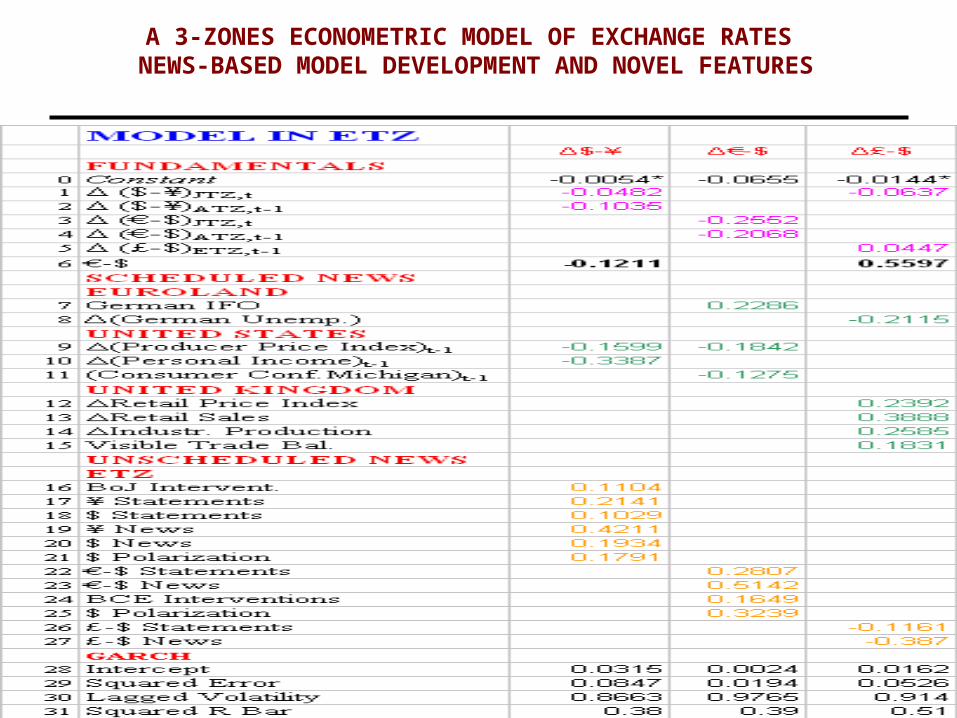

A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES NEWS-BASED MODEL DEVELOPMENT AND NOVEL FEATURES

71

A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES NEWS-BASED MODEL DEVELOPMENT AND NOVEL FEATURES

72

A A,t tN Hε 0

A A A 2 A1 + ( ) t t t H H

USUSUS

3 5A SK, AA A GEUK15 14 55 50 0A UKEU5 31

14 13 1A1

5 1

/ $

$/ €/ $

€/ $ £/ $

£/ $

tt i

t t i tt i

t i i tt i t ii i

tt t it iJA

tt

DJ DJr r

r

rr

¥

¥sk

Β Θ Γ sk Γ

sk

/ $,

UNSK, A €/ $, A

11 5 1£/ $,

11 1

A

t

A

t t

A

t

¥u

u

u

A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES NEWS-BASED MODEL DEVELOPMENT AND NOVEL FEATURES

73

A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES NEWS-BASED MODEL DEVELOPMENT AND NOVEL FEATURES

74

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. IMPACT: A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

FROM SIMULATION TO TRADING - OVERVIEW

• In this course we will examine four protocols which can be used with a short-term econometric model:

• Directional Trading

• Contrarian Trading, news-assisted mode

• Contrarian trading, automatic mode

• Mixed Trading: Directional plus “Contrarian” at Stop Loss

• Baseline (for a benchmark)

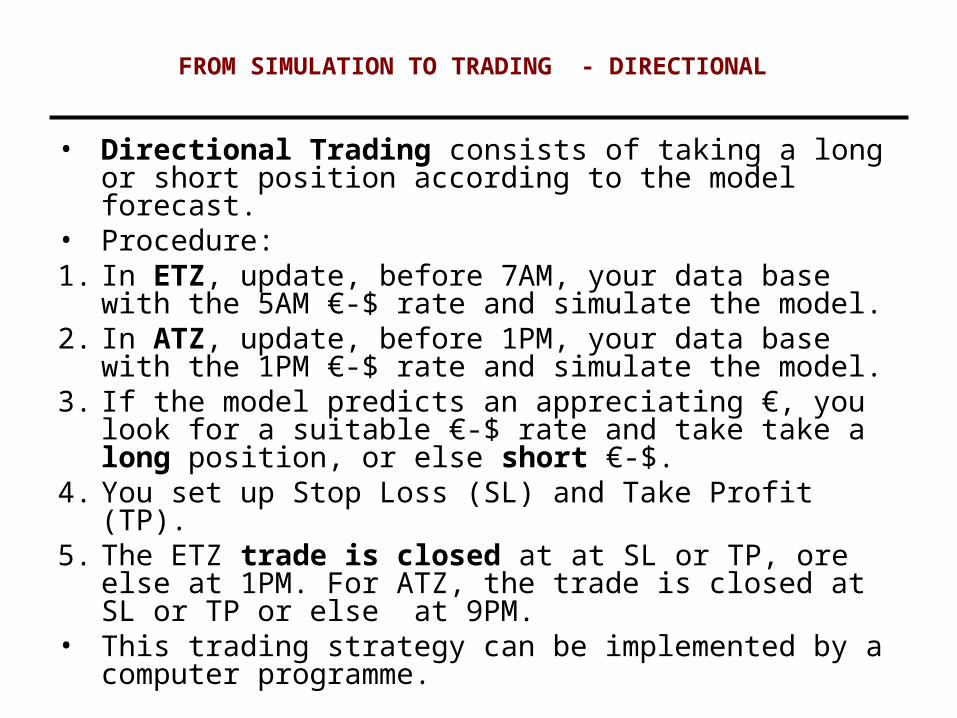

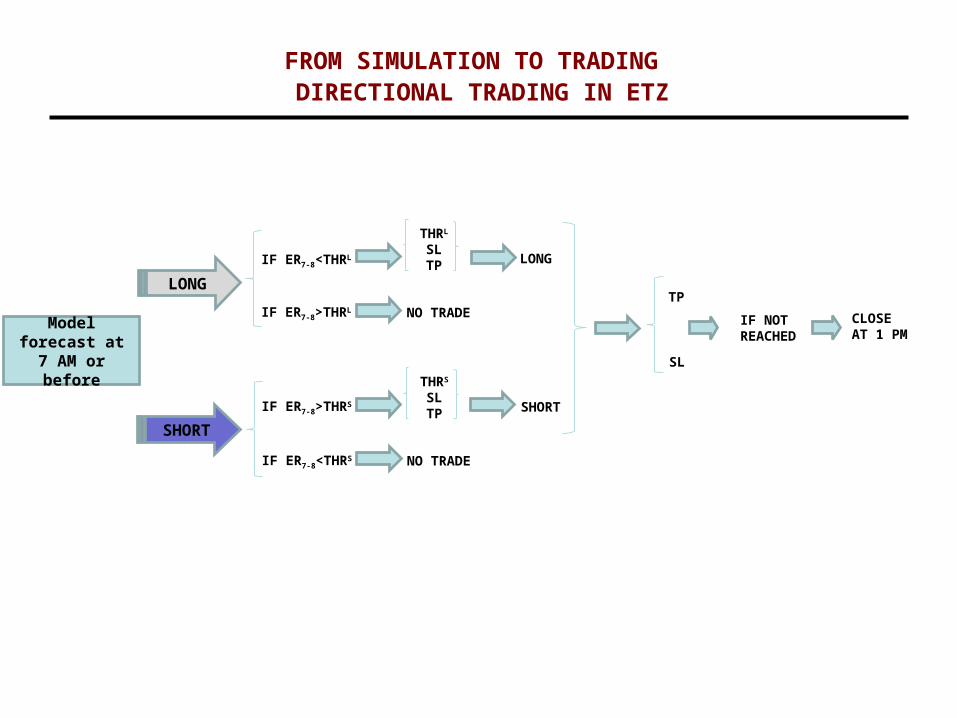

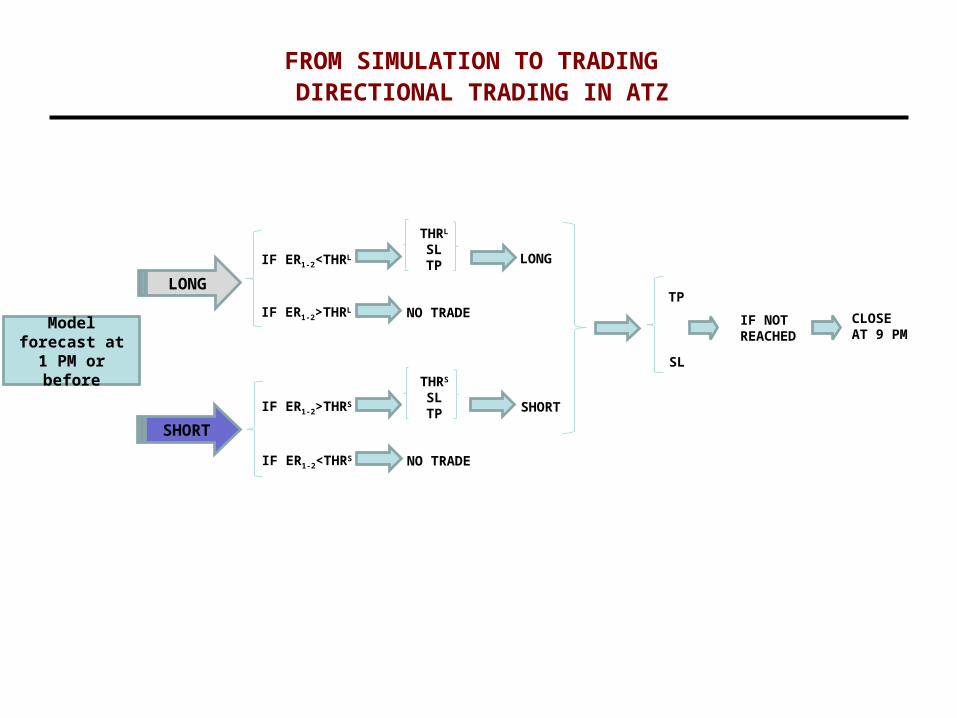

FROM SIMULATION TO TRADING - DIRECTIONAL

• Directional Trading consists of taking a long or short position according to the model forecast.

• Procedure:1. In ETZ, update, before 7AM, your data base with the

5AM €-$ rate and simulate the model.2. In ATZ, update, before 1PM, your data base with the

1PM €-$ rate and simulate the model.3. If the model predicts an appreciating €, you look for a

suitable €-$ rate and take take a long position, or else short €-$.

4. You set up Stop Loss (SL) and Take Profit (TP). 5. The ETZ trade is closed at at SL or TP, ore else at

1PM. For ATZ, the trade is closed at SL or TP or else at 9PM.

• This trading strategy can be implemented by a computer programme.

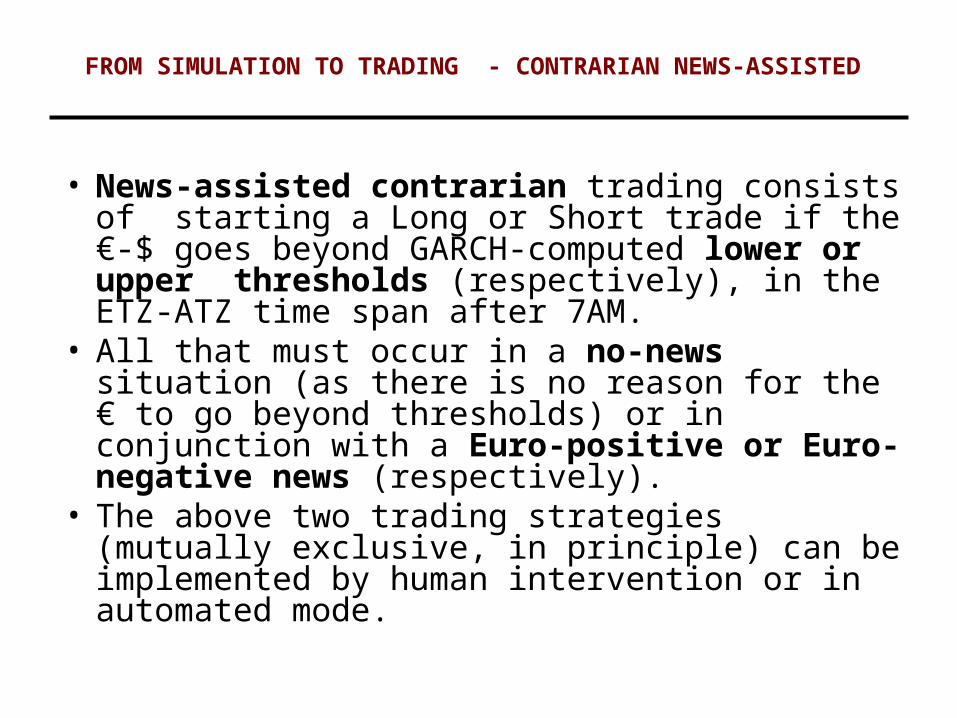

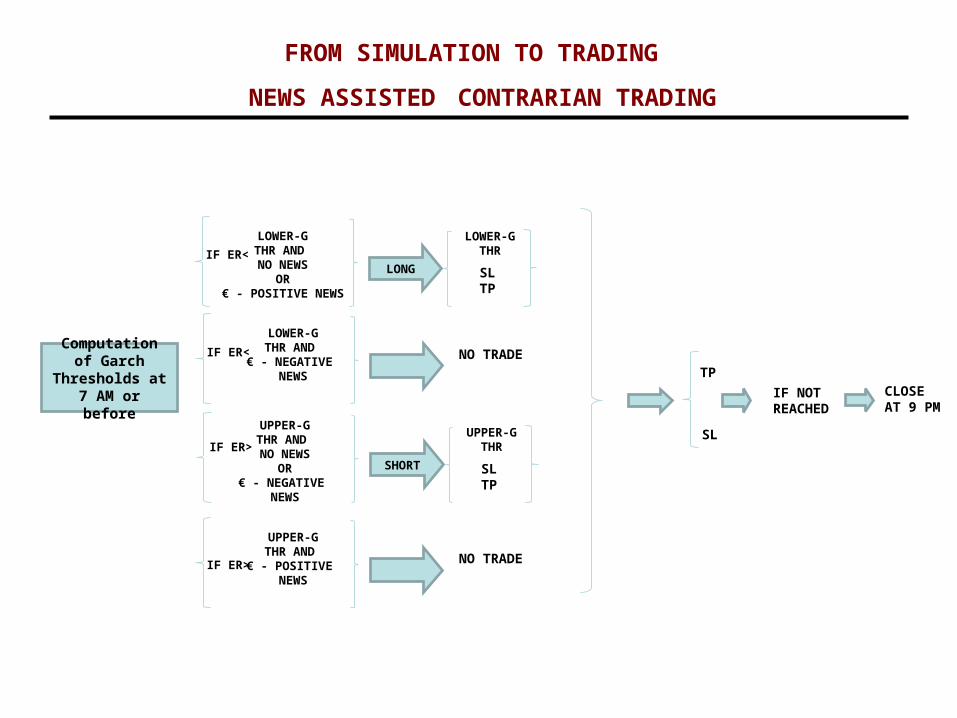

FROM SIMULATION TO TRADING - CONTRARIAN NEWS-ASSISTED

• News-assisted contrarian trading consists of starting a Long or Short trade if the €-$ goes beyond GARCH-computed lower or upper thresholds (respectively), in the ETZ-ATZ time span after 7AM.

• All that must occur in a no-news situation (as there is no reason for the € to go beyond thresholds) or in conjunction with a Euro-positive or Euro-negative news (respectively).

• The above two trading strategies (mutually exclusive, in principle) can be implemented by human intervention or in automated mode.

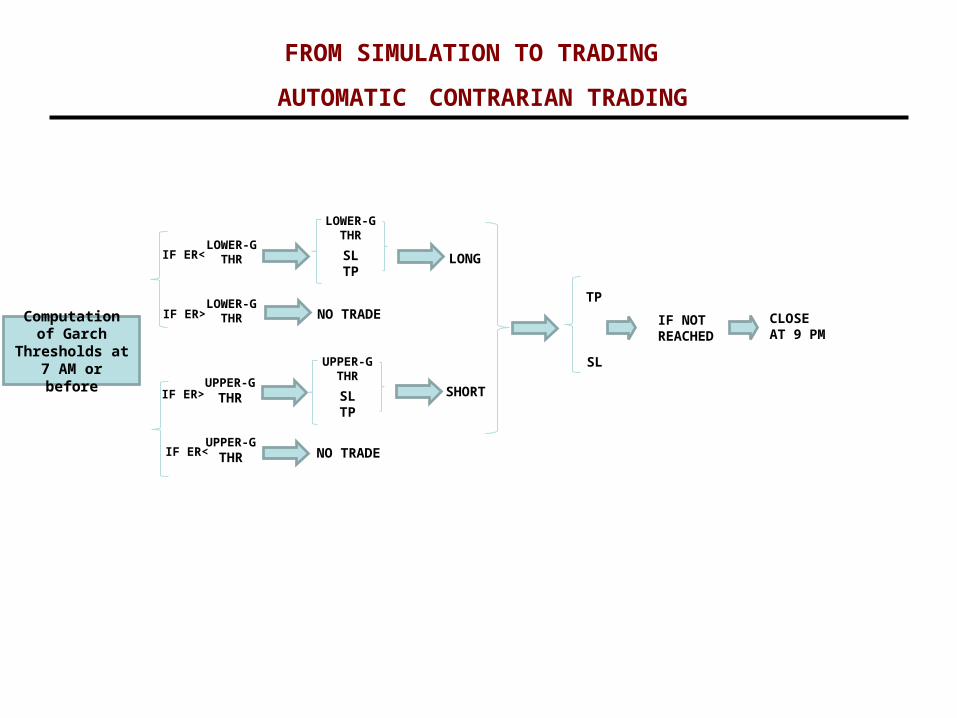

FROM SIMULATION TO TRADING - CONTRARIAN AUTOMATED

• Automated contrarian trading consists of starting a Long or Short trade whenever the €-$ goes beyond GARCH-computed lower or upper thresholds (respectively), in the ETZ-ATZ time span after 7AM.

• Contrary to the news-assisted protocol, the trade begins mechanically if the € goes beyond GARCH thresholds.

• This trading strategy can be implemented by a computer programme.

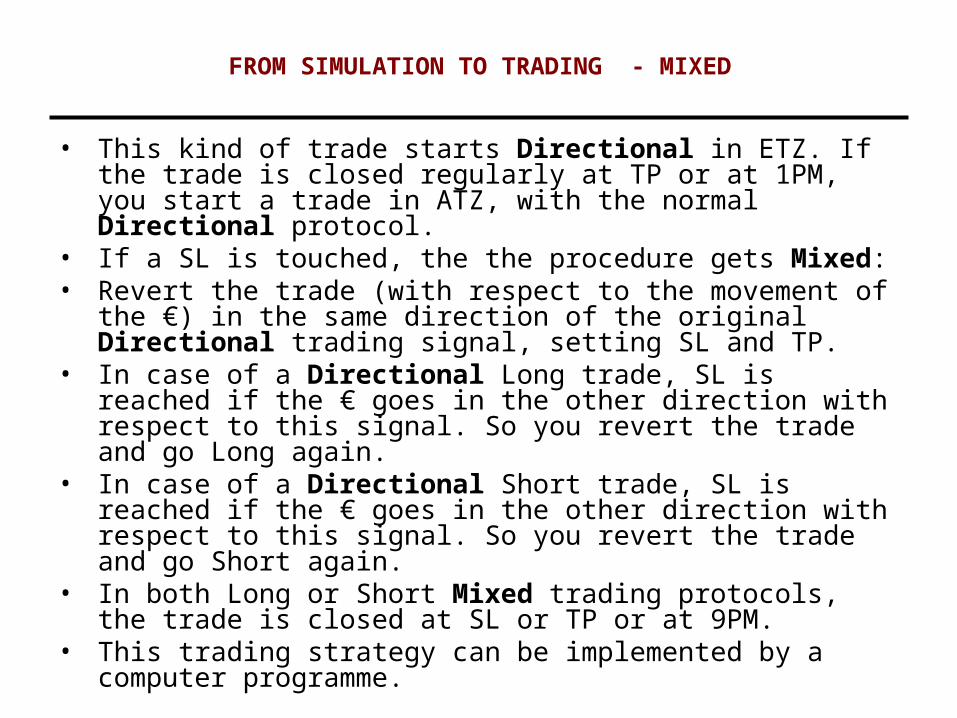

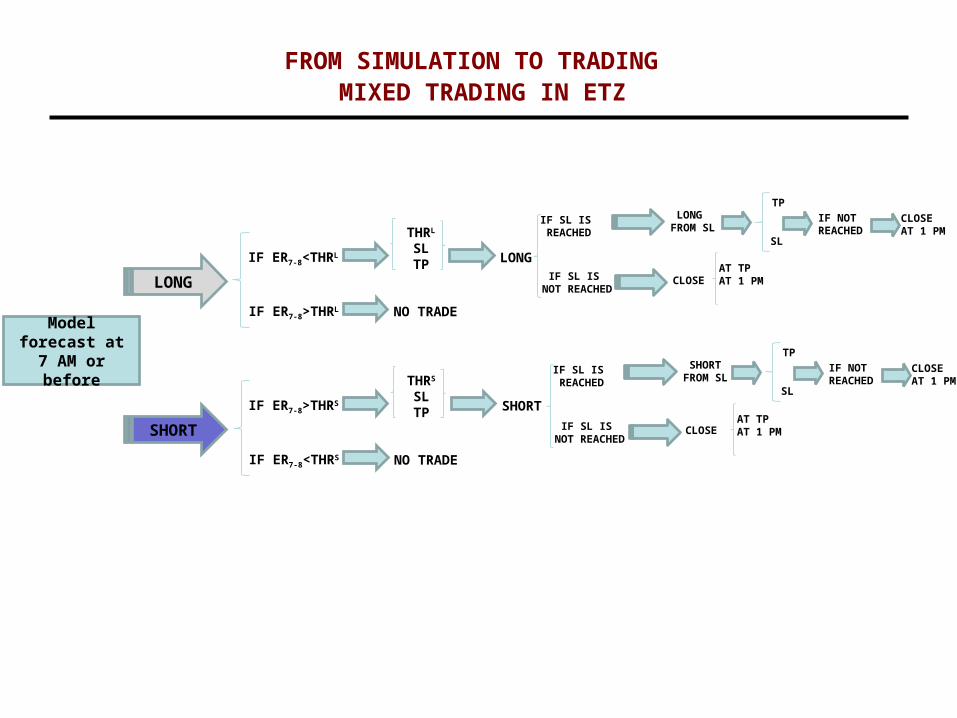

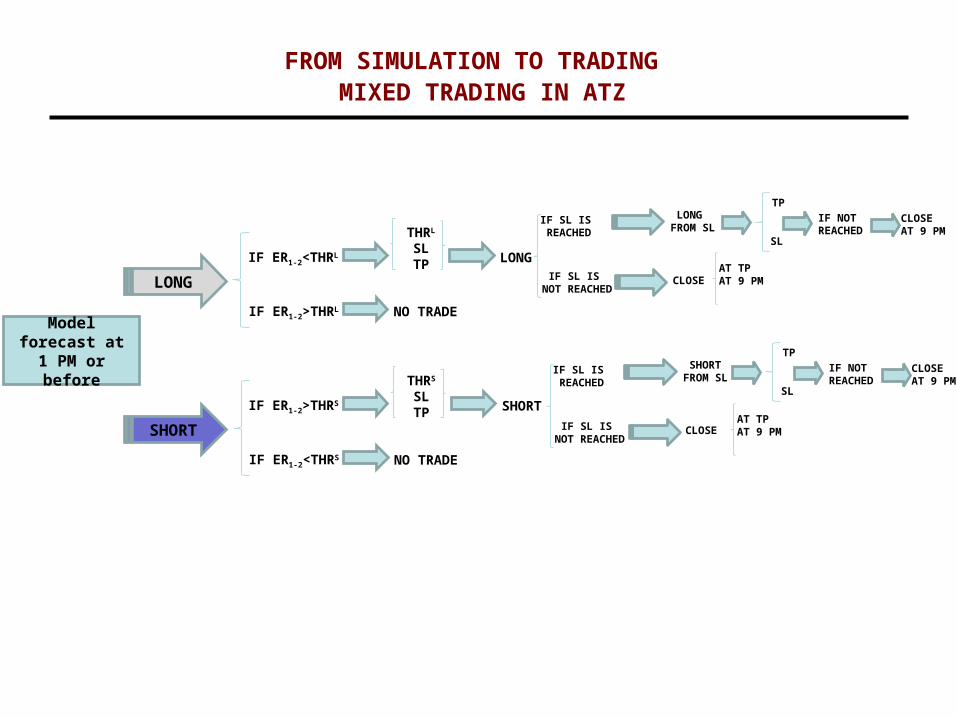

FROM SIMULATION TO TRADING - MIXED

• This kind of trade starts Directional in ETZ. If the trade is closed regularly at TP or at 1PM, you start a trade in ATZ, with the normal Directional protocol.

• If a SL is touched, the the procedure gets Mixed: • Revert the trade (with respect to the movement of the €)

in the same direction of the original Directional trading signal, setting SL and TP.

• In case of a Directional Long trade, SL is reached if the € goes in the other direction with respect to this signal. So you revert the trade and go Long again.

• In case of a Directional Short trade, SL is reached if the € goes in the other direction with respect to this signal. So you revert the trade and go Short again.

• In both Long or Short Mixed trading protocols, the trade is closed at SL or TP or at 9PM.

• This trading strategy can be implemented by a computer programme.

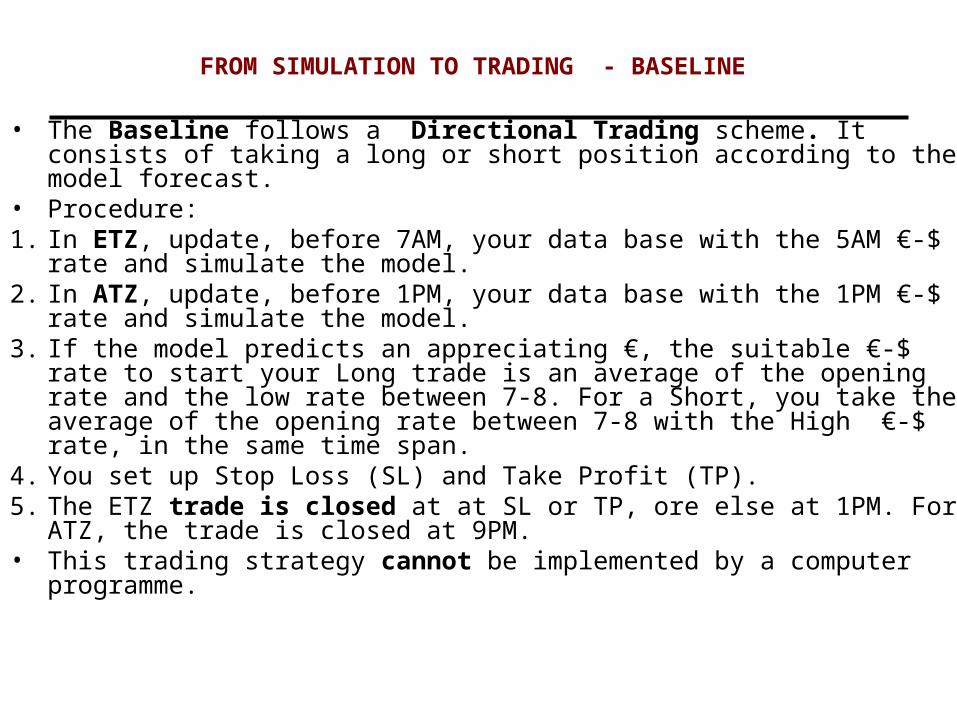

FROM SIMULATION TO TRADING - BASELINE

• The Baseline follows a Directional Trading scheme. It consists of taking a long or short position according to the model forecast.

• Procedure:1. In ETZ, update, before 7AM, your data base with the 5AM €-$ rate and

simulate the model.2. In ATZ, update, before 1PM, your data base with the 1PM €-$ rate and

simulate the model.3. If the model predicts an appreciating €, the suitable €-$ rate to start

your Long trade is an average of the opening rate and the low rate between 7-8. For a Short, you take the average of the opening rate between 7-8 with the High €-$ rate, in the same time span.

4. You set up Stop Loss (SL) and Take Profit (TP). 5. The ETZ trade is closed at at SL or TP, ore else at 1PM. For ATZ, the

trade is closed at 9PM.• This trading strategy cannot be implemented by a computer

programme.

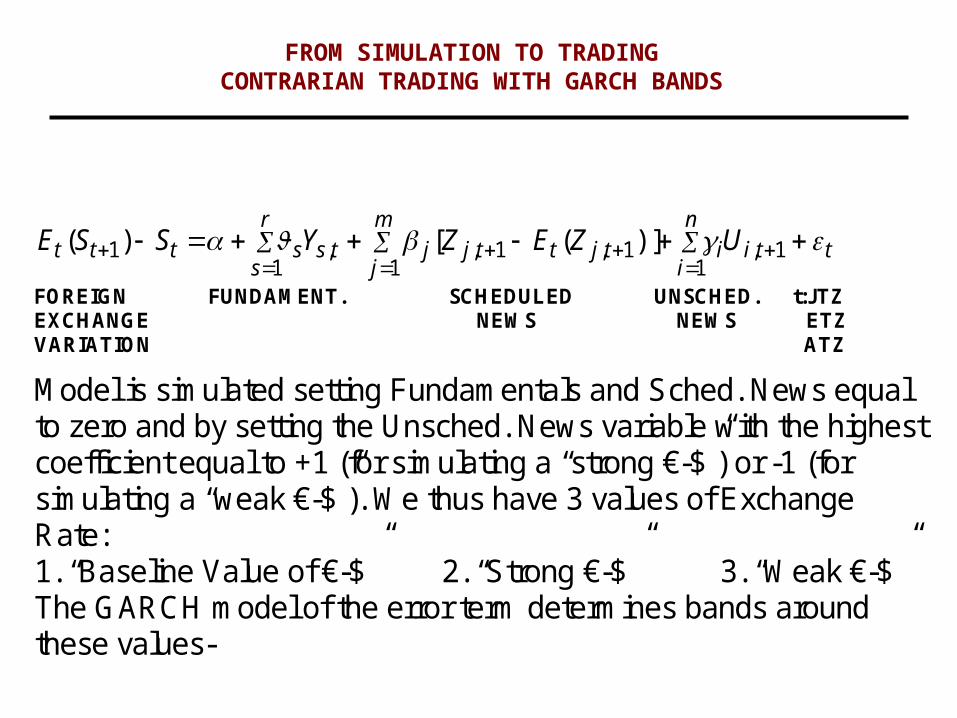

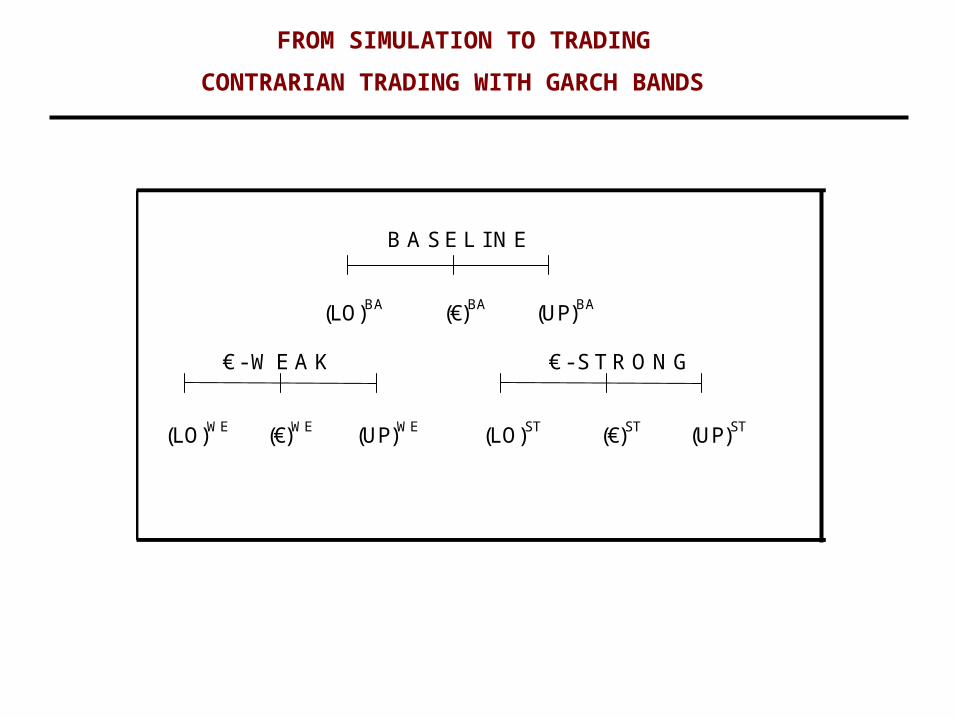

FROM SIMULATION TO TRADING CONTRARIAN TRADING WITH GARCH BANDS

FOREIGN FUNDAMENT. SCHEDULED UNSCHED. t:JTZ EXCHANGE NEWS NEWS ETZ VARIATION ATZ

Model is simulated setting Fundamentals and Sched. News equal to zero and by setting the Unsched. News variable with the highest coefficient equal to +1 (for simulating a “strong €-$”) or -1 (for simulating a “weak €-$”). We thus have 3 values of Exchange Rate: 1. “Baseline Value of €-$” 2. “Strong €-$” 3. “Weak €-$” The GARCH model of the error term determines bands around these values-

ttin

iitjttj

m

jjts

r

ssttt UZEZYSSE

1,

11,1,

1,

11 )]([)(

),0( ,2 it

it N

it

it

it

,21

,21

,2

FROM SIMULATION TO TRADINGCONTRARIAN TRADING WITH GARCH BANDS

i => ETZ ATZ

• GARCH structure of the error term

FROM SIMULATION TO TRADING

CONTRARIAN TRADING WITH GARCH BANDS

B A S E L I N E

(LO)BA (€)BA (UP)BA

€ - W E A K € - S T R O N G

(LO)WE (€)WE (UP)WE (LO)ST (€)ST (UP)ST

Model forecast at 7 AM or

before

LONG

SHORT

IF ER7-8<THRL

THRL

SLTP LONG

IF ER7-8>THRL NO TRADE

IF ER7-8>THRS

THRS

SLTP SHORT

IF ER7-8<THRS NO TRADE

FROM SIMULATION TO TRADING DIRECTIONAL TRADING IN ETZ

TP

SL

IF NOT REACHED

CLOSE AT 1 PM

Model forecast at 1 PM or

before

LONG

SHORT

IF ER1-2<THRL

THRL

SLTP LONG

IF ER1-2>THRL NO TRADE

IF ER1-2>THRS

THRS

SLTP SHORT

IF ER1-2<THRS NO TRADE

FROM SIMULATION TO TRADING DIRECTIONAL TRADING IN ATZ

TP

SL

IF NOT REACHED

CLOSE AT 9 PM

Model forecast at 7 AM or

before

SHORT

IF ER7-8<THRL

THRL

SLTP LONG

IF SL IS REACHED

LONG FROM SL

CLOSEAT TP AT 1 PM

IF ER7-8>THRL NO TRADE

IF ER7-8>THRS

THRS

SLTP SHORT

IF ER7-8<THRS NO TRADE

FROM SIMULATION TO TRADING MIXED TRADING IN ETZ

IF SL IS NOT REACHED

TP

SL

IF NOT REACHED

CLOSE AT 1 PM

LONG

IF SL IS REACHED

SHORTFROM SL

CLOSEAT TP AT 1 PMIF SL IS

NOT REACHED

TP

SL

IF NOT REACHED

CLOSE AT 1 PM

Model forecast at 1 PM or

before

SHORT

IF ER1-2<THRL

THRL

SLTP LONG

IF SL IS REACHED

LONG FROM SL

CLOSEAT TP AT 9 PM

IF ER1-2>THRL NO TRADE

IF ER1-2>THRS

THRS

SLTP SHORT

IF ER1-2<THRS NO TRADE

FROM SIMULATION TO TRADING MIXED TRADING IN ATZ

IF SL IS NOT REACHED

TP

SL

IF NOT REACHED

CLOSE AT 9 PM

LONG

IF SL IS REACHED

SHORTFROM SL

CLOSEAT TP AT 9 PMIF SL IS

NOT REACHED

TP

SL

IF NOT REACHED

CLOSE AT 9 PM

Computation of Garch

Thresholds at 7 AM or before

IF ER< SLTP

LONG

NO TRADE

SHORT

NO TRADE

FROM SIMULATION TO TRADING AUTOMATIC CONTRARIAN TRADING

LOWER-GTHR

LOWER-GTHR

IF ER>LOWER-G

THR

TP

SL

IF NOT REACHED

CLOSE AT 9 PM

IF ER>UPPER-G

THR

UPPER-GTHRIF ER<

SLTP

UPPER-GTHR

Computation of Garch

Thresholds at 7 AM or before

IF ER<

SLTP

LONG

FROM SIMULATION TO TRADING NEWS ASSISTED CONTRARIAN TRADING

LOWER-GTHR AND NO NEWS

OR€ - POSITIVE NEWS

LOWER-GTHR

TP

SL

IF NOT REACHED

CLOSE AT 9 PM

IF ER< NO TRADE

LOWER-GTHR AND

€ - NEGATIVE NEWS

SLTP

SHORT

UPPER-GTHR AND NO NEWS

OR€ - NEGATIVE

NEWS

UPPER-GTHRIF ER>

NO TRADE

UPPER-GTHR AND

€ - POSITIVE NEWS

IF ER>

FROM SIMULATION TO TRADING CUMULATIVE PROFITS IN THE 4 TRADING RULES

E-$ Contrarian-News Contr.Autom. Mixed Directional

Euro-$,Cumulative Total Profits in All Trading RulesJanuary 3, 2011 - November 29, 2013

Exch

ange

Rate

Cumulative Profits

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N2011 2012 2013

1.20

1.25

1.30

1.35

1.40

1.45

1.50

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

33.4%

22.6%

8.5%

6.1%

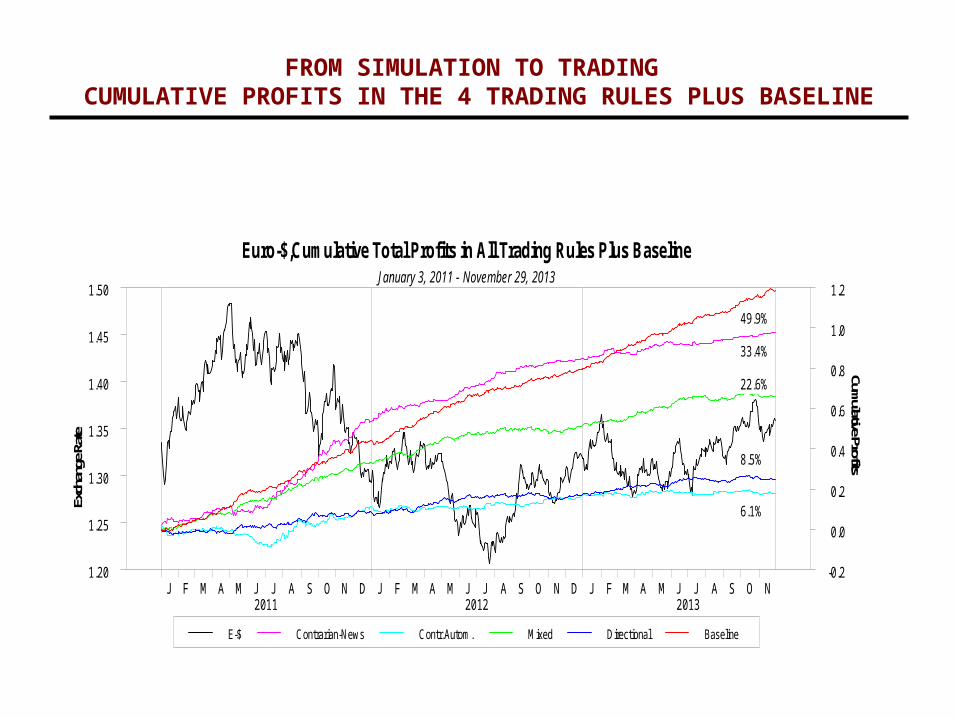

FROM SIMULATION TO TRADING CUMULATIVE PROFITS IN THE 4 TRADING RULES PLUS BASELINE

E-$ Contrarian-News Contr.Autom. Mixed Directional Baseline

Euro-$,Cumulative Total Profits in All Trading Rules Plus BaselineJanuary 3, 2011 - November 29, 2013

Exch

ange

Rat

e

Cumulative Profits

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N2011 2012 2013

1.20

1.25

1.30

1.35

1.40

1.45

1.50

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

49.9%

33.4%

22.6%

8.5%

6.1%

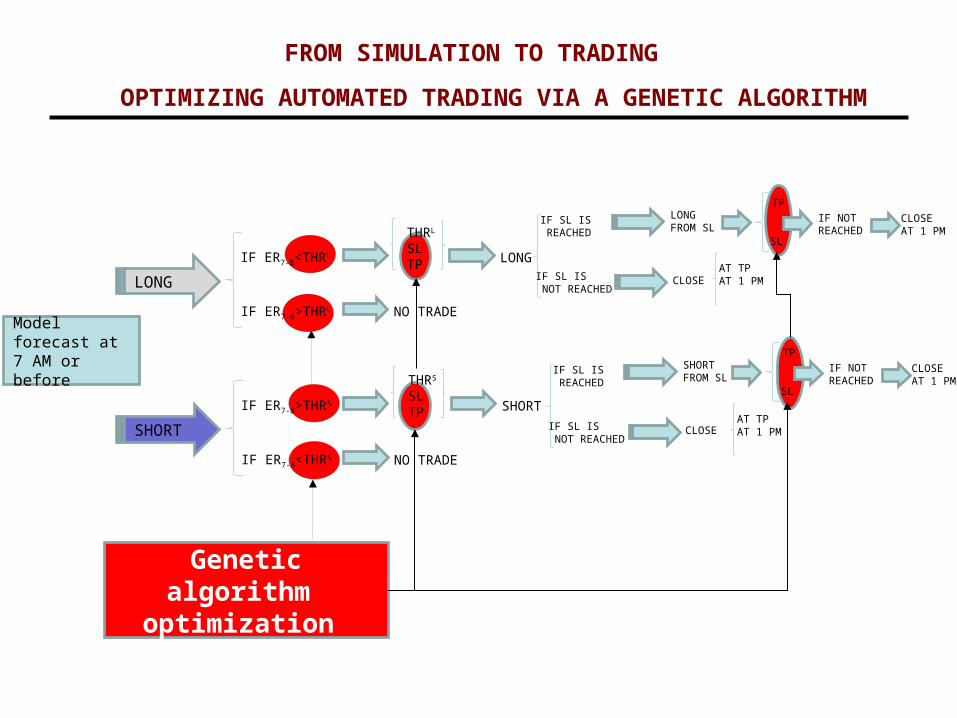

FROM SIMULATION TO TRADING OPTIMIZING AUTOMATED TRADING VIA A GENETIC ALGORITHM

• Once you are able to devise a protocol which can be automated and you build a computer program able to execute your trading instructions sequentially, you may try to optimize the parameters of our rule which condition the profit performance.

• A widely used optimization technique in finance is the Genetic Algorithm (GA), which is adapted from a “selection of the species” to a “selection of the profit-maximizing parameters”

FROM SIMULATION TO TRADING OPTIMIZING AUTOMATED TRADING VIA A GENETIC ALGORITHM

• It is basically a data mining program which iteratively finds the best set of parameters from a group of numbers within boundary conditions.

• In order to avoid “data snooping” (namely use the same set of numbers to optimize and compute trading results), you will need to split your data set into two parts.

FROM SIMULATION TO TRADING OPTIMIZING AUTOMATED TRADING VIA A GENETIC ALGORITHM

• A Training Set (TNS), made up by the first part of your data set, where you find the optimal parameters.

• A Trading Set (TRS), made up of the second part of your data set still within the sample, where you will compute the performance (generally in terms of cumulative profits, their volatility and their Drawdown)

FROM SIMULATION TO TRADING OPTIMIZING AUTOMATED TRADING VIA A GENETIC ALGORITHM

• Ideally the time series of exchange rate (ER) in the two Sets should have comparable time series properties (e.g mean, volatility, cyclical properties, outliers) and they should be usable in the trading environment of the immediate future.

• After some use of the optimized day-trading rule, the GA will have to be trained again, using the ER actually used for trading as a Training/Trading Set.

FROM SIMULATION TO TRADING OPTIMIZING AUTOMATED TRADING VIA A GENETIC ALGORITHM

• The following slide shows what to optimize in the Automated Rule shown before (slide 66). The parameters are thresholds and SL and TP, besides a time length to decide to “Close and Reverse” the trade.

• The subsequent two slides show a TNS and a TRS where charts of cumulative profits and of Drawdown features are depicted, together with the observed ER series

Model forecast at 7 AM or before

SHORT

IF ER7-8<THRL

THRL

SLTP LONG

IF SL IS REACHED

LONG FROM SL

CLOSEAT TP AT 1 PM

IF ER7-8>THRL NO TRADE

IF ER7-8>THRS

THRS

SLTP SHORT

IF ER7-8<THRS NO TRADE

FROM SIMULATION TO TRADING OPTIMIZING AUTOMATED TRADING VIA A GENETIC ALGORITHM

IF SL IS NOT REACHED

TP

SL

IF NOT REACHED

CLOSE AT 1 PM

LONG

IF SL IS REACHED

SHORTFROM SL

CLOSEAT TP AT 1 PMIF SL IS

NOT REACHED

TP

SL

IF NOT REACHED

CLOSE AT 1 PM

Genetic algorithm optimization

98

COURSE OUTLINE

1. THE €-$ FOREX MARKET - HISTORY AND RECENT TRENDS

2. FROM MACROECONOMIC FUNDAMENTALS TO MACRO NEWS

3. MACROECONOMIC SURPRISES – THE SCHEDULED NEWS

4. INFORMATION SOURCES OF SCHEDULED NEWS

5. IMPACT ON EXCHANGE RATES OF SCHEDULED NEWS

6. UNSCHEDULED NEWS AND THEIR IMPACT ON EXCHANGE RATES

7. HOW TO MEASURE NEWS

8. IMPACT: A 3-ZONES ECONOMETRIC MODEL OF EXCHANGE RATES

9. FROM SIMULATION TO TRADING - OPTIMIZATION

10.MEASURING AND EVALUATING PERFORMANCE

MEASURING AND EVALUATING PERFORMANCE

• The profitability of a day-trading rule is measured as any standard financial investment.

• Profit Rate over a given time horizon and its standard deviation for evaluating statistical significance and drawing confidence bands. A Sharpe Ratio (i.e. standardized excess return over the risk-free return) is also widely used.

MEASURING AND EVALUATING PERFORMANCE

• But a high-frequency trading rule (as a protocol replicating itself without any change) needs also monitoring indicators for checking the stability of profits and their volatility overtime and, in particular, in turbulent periods.

MEASURING AND EVALUATING PERFORMANCE

The monitoring indicators can be:

1. Equity Line (a Cumulative Profit Line)

2. Moving Standard Deviation of Profit along the Equity Line (Volatility)

3. Drawdown Analysis

4. Policy and event analysis from the perspective of an historical evaluation of quiet and turbulent periods and related policy measures and market sentiment.

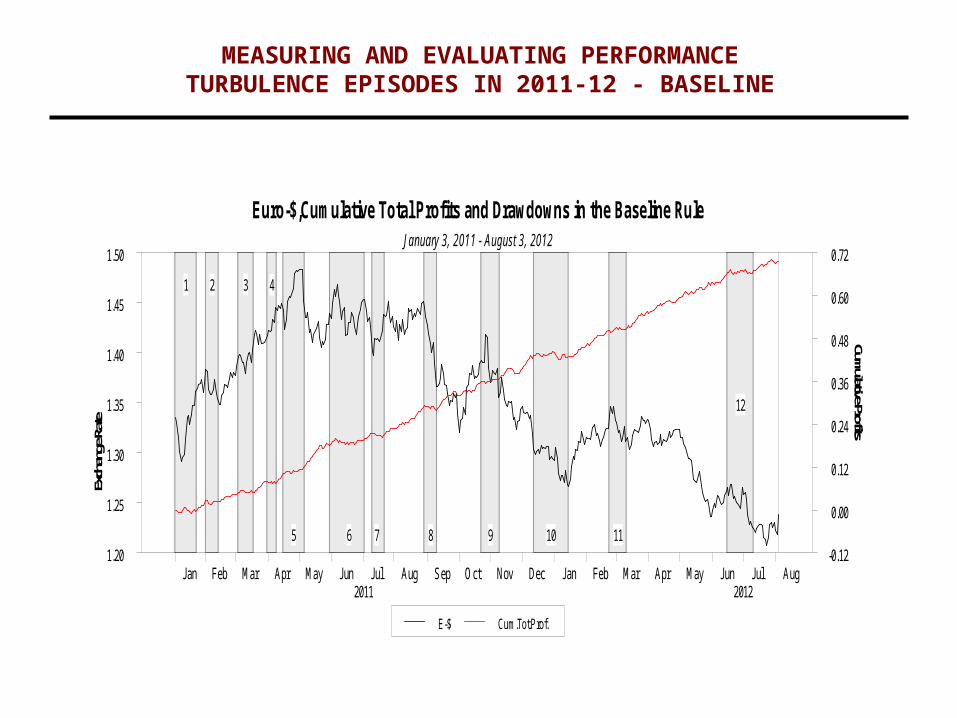

MEASURING AND EVALUATING PERFORMANCE

Turbulent periods follow:

1. Unexpected Policy measures (e.g. US ultra expansionary monetary policy after Lehman and QE later)

2. Ongoing financial distress from contagion (e.g. Greece=>Ireland=>Portugal=>Italy and Spain, PIIGS)

3. Rumors, Fads, Myths, Excuses

4. Irrational Exuberance or Irrational Pessimism

MEASURING AND EVALUATING PERFORMANCETURBULENCE POST-LEHMAN

E-$ Cum.Tot.Prof.

Fig. 3.1 - Euro-$,Cumulative Total Profits and Drawdowns2008 - 2010

Exch

ange

Rat

eCum

ulative Profits

J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J2008 2009 2010

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1 2 3

4 5 6 7 8

MEASURING AND EVALUATING PERFORMANCETURBULENCE EPISODES IN 2011-12 - BASELINE

E-$ Cum.Tot.Prof.

Euro-$,Cumulative Total Profits and Drawdowns in the Baseline RuleJanuary 3, 2011 - August 3, 2012

Exch

ange

Rate

Cumulative Profits

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug2011 2012

1.20

1.25

1.30

1.35

1.40

1.45

1.50

-0.12

0.00

0.12

0.24

0.36

0.48

0.60

0.72

1 2 3 4

5 6 7 8 9 10 11

12

MEASURING AND EVALUATING PERFORMANCETURBULENCE EPISODES IN 2011-12 – 4 TRADING RULES PLUS BASELINE

E-$ Contrarian-News Contr.Autom. Mixed Directional Baseline

Euro-$,Cumulative Total Profits and Drawdowns in All Trading Rules Plus BaselineJanuary 3, 2011 - August 3, 2012

Exch

ange

Rate

Cumulative Profits

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug2011 2012

1.20

1.25

1.30

1.35

1.40

1.45

1.50

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

1 2 3 4

5 6 7 8 9 10 11

12

MEASURING AND EVALUATING PERFORMANCETURBULENCE EPISODES IN 2012-13 – BASELINE

E-$ Cum.Tot.Prof.

Euro-$,Cumulative Total Profits and Drawdowns in the Baseline RuleJuly 30, 2012 - November 29, 2013

Exch

ange

Rate

Cumulative Profits

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov2013

1.20

1.25

1.30

1.35

1.40

-0.08

0.00

0.08

0.16

0.24

0.32

0.40

0.48

0.56

0.64

13 14 15 16 17 18 19 20 21 22 23 24

MEASURING AND EVALUATING PERFORMANCETURBULENCE EPISODES IN 2012-13 – 4 TRADING RULES PLUS BASELINE

E-$ Contrarian-News Contr.Autom. Mixed Directional Baseline

Euro-$,Cumulative Total Profits and Drawdowns in All Trading Rules Plus BaselineAugust 6, 2012 - November 29, 2013

Exch

ange

Rate

Cumulative Profits

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov2013

1.20

1.25

1.30

1.35

1.40

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

13 14 15 16 17 18 19 20 21 22 23 24

THE END

Goodnight

And Good Luck !

Shakespeare “Julius Caesar”

(Brutus)