Embed Size (px)

Citation preview

1

The Business Case The Business Case of Broadband Wireless Access of Broadband Wireless Access

February 2001February 2001

Rudy Leser

Vice President Business Development

e- mail: [email protected]

2

Early 2001 – New EnvironmentEarly 2001 – New Environment

Equity market - on hold

Vendor financing – very selective

Slow-down in the Telecom market

Growth of broadband – slower than expected

BWA CLECs business case – yet to be proven

3

Strategic Focus is ShiftingStrategic Focus is Shifting

Cash-flow

Better cost model

Slower broadband growth

Differentiation

4

Trends In The Telecom MarketTrends In The Telecom Market

Financing squeeze

Review plans to improve ROI

Some CLECs’s business plans are faulty

The strong ones will survive

5

Business Plan is RevisitedBusiness Plan is Revisited

Capture quality customer base quickly

Generate revenues

Reach profitability faster

6

BWA New Strategies – BWA New Strategies – From Survival to SuccessFrom Survival to Success

Focus on high density areas

Re-assess marketing strategy:

Leave behind buzzwords and hype

Strong focus on specific segments

Find stronger differentiating factors

Offer your segment what is really needed

Reduce initial investment and expand as you grow (Not a Slogan!!!)

7

Focus on Your Segment Focus on Your Segment

SME

Small business/soho

MTU

Residential

8

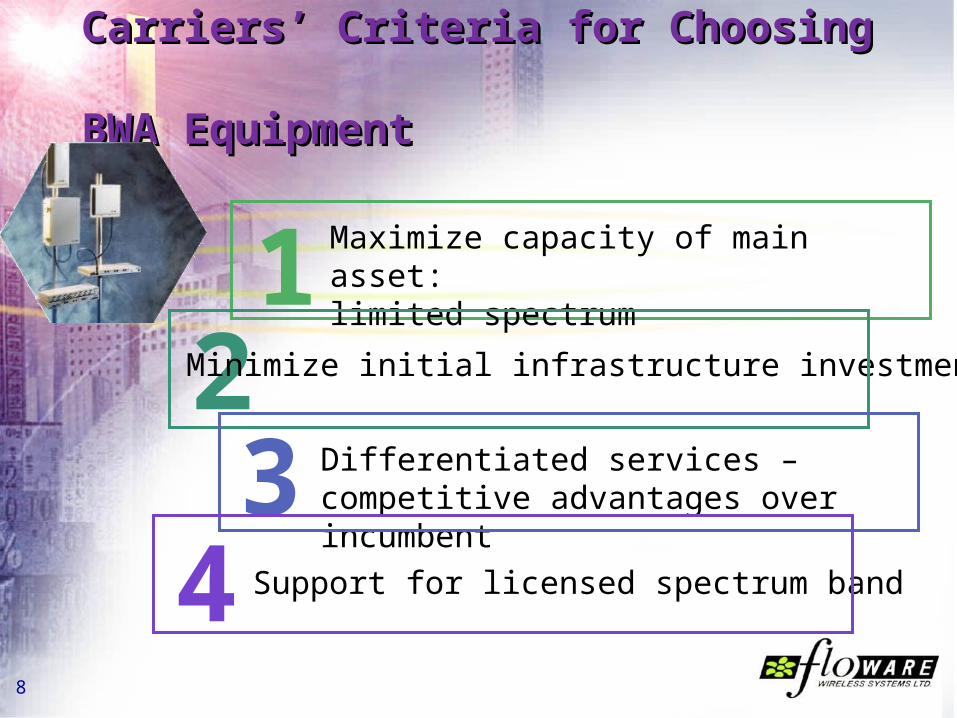

Carriers’ Criteria for Choosing Carriers’ Criteria for Choosing BWA EquipmentBWA Equipment

Support for licensed spectrum band

123

Maximize capacity of main asset: limited spectrum

Minimize initial infrastructure investment

Differentiated services – competitive advantages over incumbent

4

9

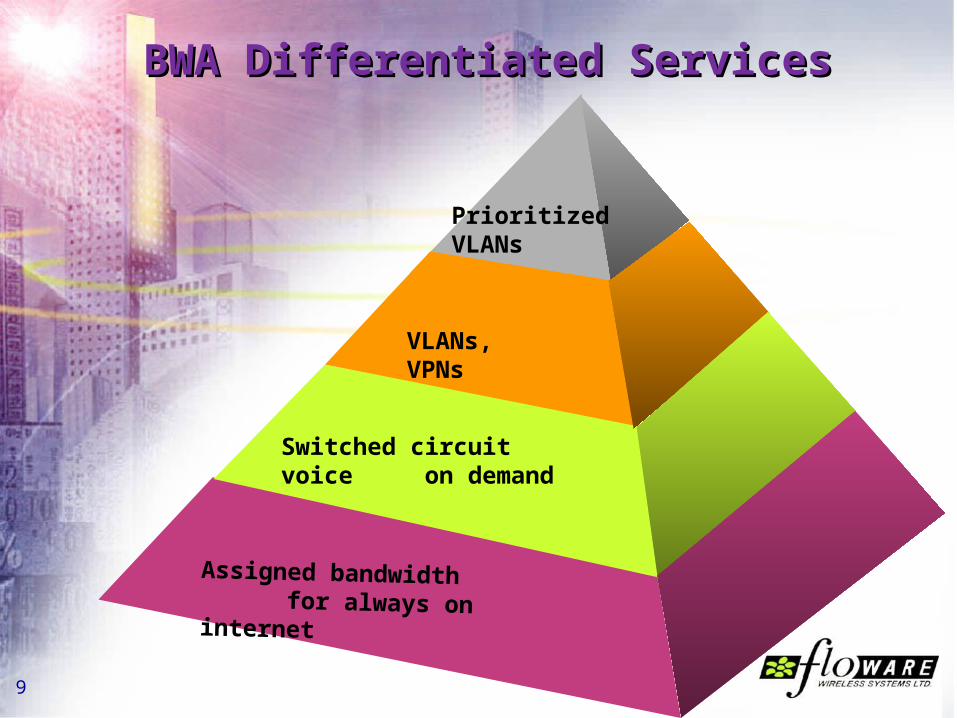

BWA Differentiated Services BWA Differentiated Services

Prioritized VLANs

VLANs, VPNs

Switched circuit voice on demand

Assigned bandwidth for always on internet

10

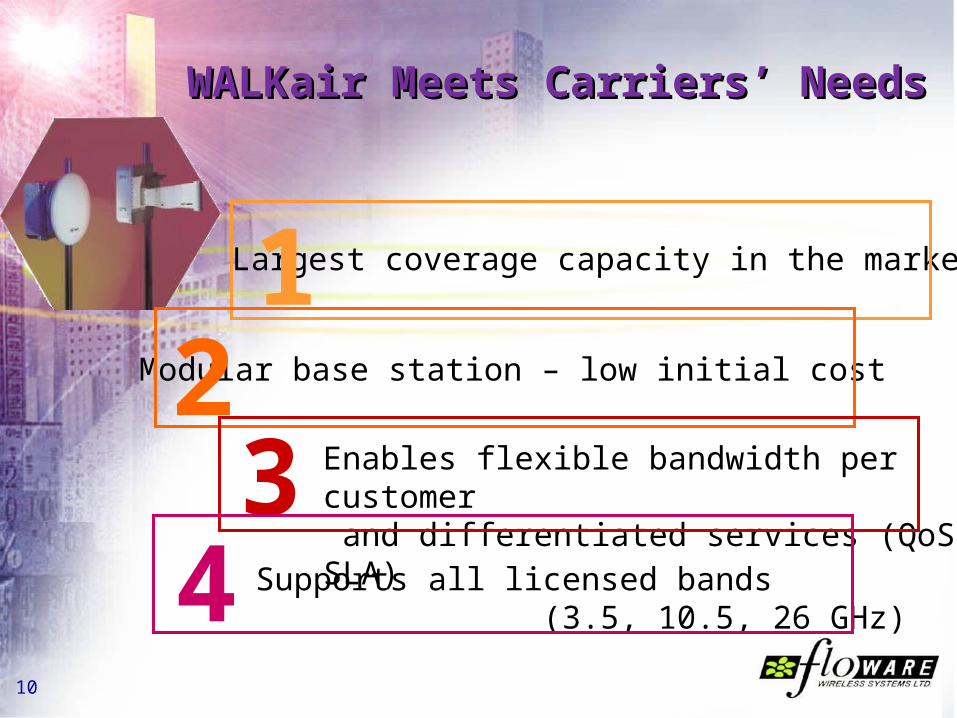

WALKair Meets Carriers’ NeedsWALKair Meets Carriers’ Needs

Supports all licensed bands (3.5, 10.5, 26 GHz)

Largest coverage capacity in the market

Modular base station – low initial cost

Enables flexible bandwidth per customer and differentiated services (QoS, SLA)

12

34

11

Commerical DeploymentsCommerical Deployments

Norway

Czech Rep.

Finland

Spain

Russia

Germany

Portugal

Slovenia

Luxembourg Poland

Europe: Cameron - Sakon

Czech Rep. – CRA, GlobalOne

Finland - Finnet

Germany - Arctel, FirstMark, Star 21

Luxembourg - FirstMark.

Norway - UPC

Poland – El Net, TPSA, TPZ, Czeptel, Elterix.

Portugal – Teleweb, Novis

Russia - Sovintel

Slovenia – Telekom Slovenia

Spain – Abrared, FirstMark

12

Argentina - Telefonica

Honduras - GlobalOne

Mexico – G-Tel

Uruguay – Rivizul

China

India – Gateway, STPI

Philippines - Beltel, Digitel

Commerical Deployments, CONT’DCommerical Deployments, CONT’D

Asia

Latin America

Cameron – Sakon

Gahna - SITA

Nigeria - SITA

Zimbabwe - Africom

Africa

PhilippinesIndia

China

Zimbabwe

Nigeria

Uruguay

Argentina

Honduras

Mexico

Cameron

Gahana

13

The BWA ExperienceThe BWA Experience

Germany – major allocation in Q3/1999

Hundreds of Base Stations

Very few end-user connected

Spain – allocation in Q1/ 2000

Hundreds of Base Stations

Very few end-user connected

Portugal – Allocation in Q4/1999

Tens of Base Station

Just started to connect customers

14

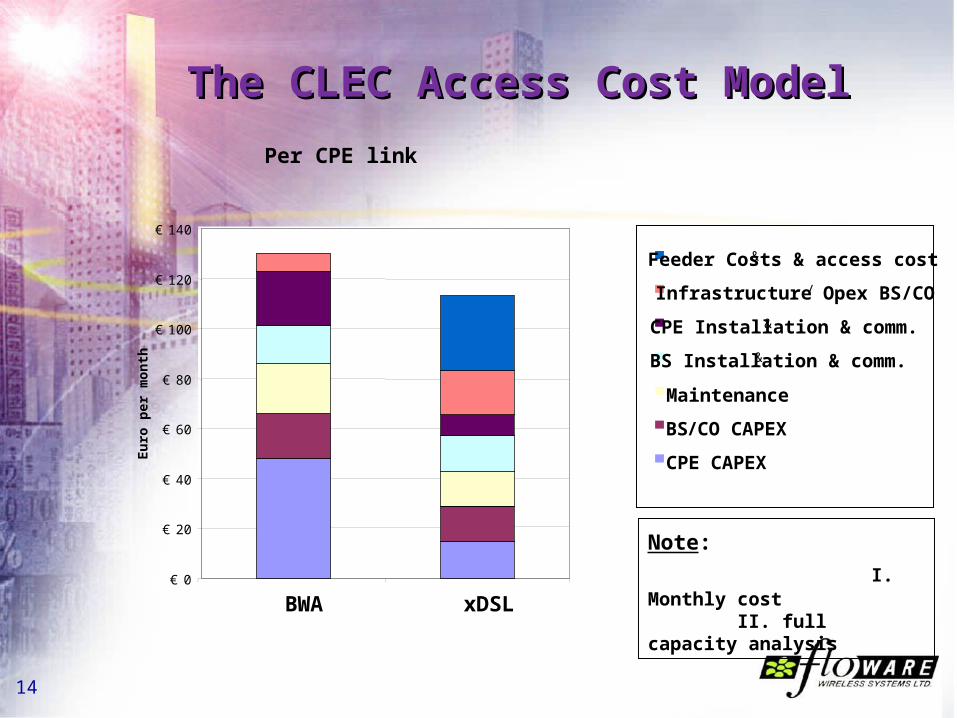

The CLEC Access Cost ModelThe CLEC Access Cost Model

Per CPE link

€ 0

€ 20

€ 40

€ 60

€ 80

€ 100

€ 120

€ 140

BWA xDSL

Eu

ro p

er m

on

th

Feeder Costs & access cost&

Infrastructure Opex BS/CO/

CPE Installation & comm. & .

BS Installation & comm. & .

Maintenance

BS / CO CAPEX

CPE CAPEX

Note: I. Monthly cost II. full capacity analysis

15

BWA Versus xDSL/ Unbundled AccessBWA Versus xDSL/ Unbundled Access

Various cost comparisons show that BWA may cost from 5% to 25% higher than xDSL using unbundled access.

16

CLEC: xDSL/Unbundling CLEC: xDSL/Unbundling AdvantagesAdvantages

Quick penetration with minimal investment

Lower cost mainly for basic services at high penetration

17

Incumbent is owner of the infrastructureNo control of line quality , response time, maintenance, competition ...

Poor qualitywhen binder fill more than 20% ...

Limited service capacityonly up to E1, no symmetric traffic ...

CLEC: xDSL/Unbundling CLEC: xDSL/Unbundling DisadvantagesDisadvantages

18

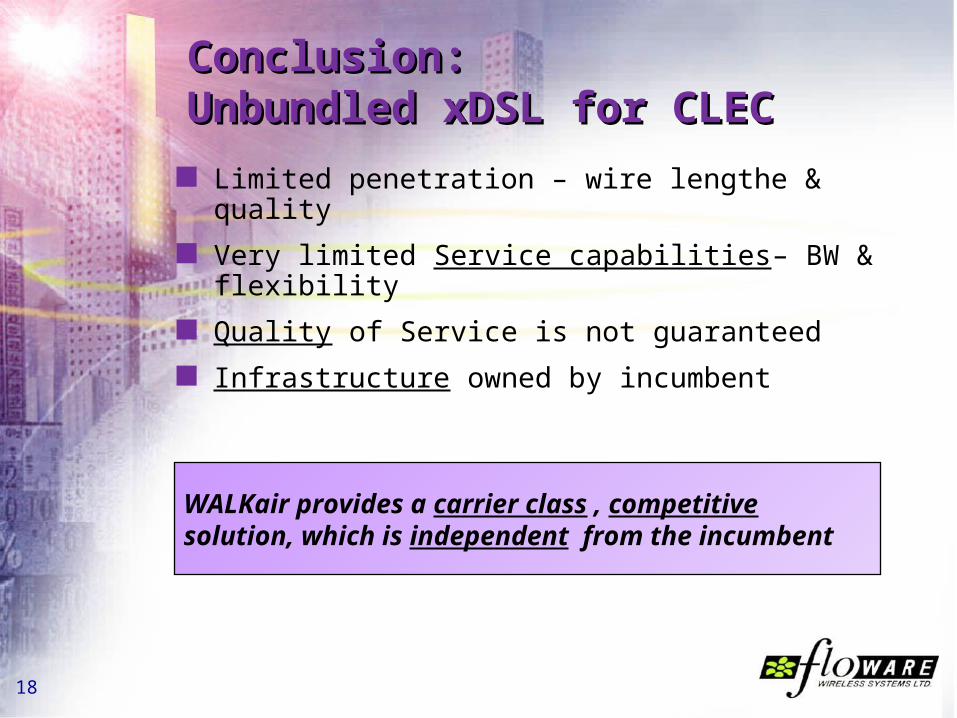

WALKair provides a carrier class , competitive solution, which is independent from the incumbent

Conclusion: Conclusion: Unbundled xDSL for CLECUnbundled xDSL for CLEC

Limited penetration – wire lengthe & quality

Very limited Service capabilities– BW & flexibility

Quality of Service is not guaranteed

Infrastructure owned by incumbent

19

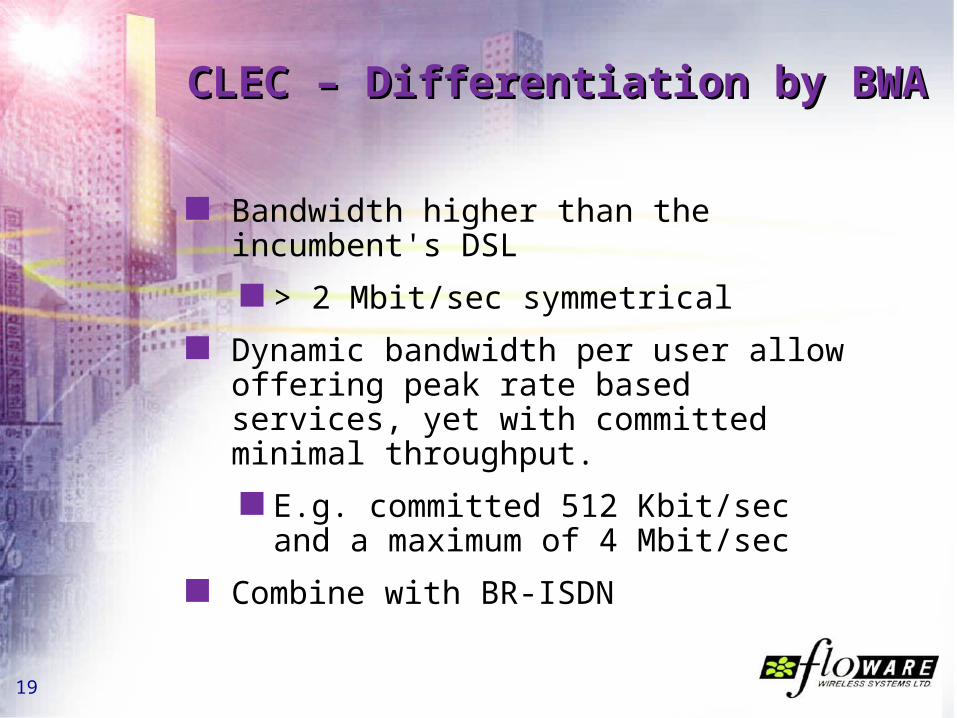

CLEC – Differentiation by BWA CLEC – Differentiation by BWA

Bandwidth higher than the incumbent's DSL

> 2 Mbit/sec symmetrical

Dynamic bandwidth per user allow offering peak rate based services, yet with committed minimal throughput.

E.g. committed 512 Kbit/sec and a maximum of 4 Mbit/sec

Combine with BR-ISDN

20

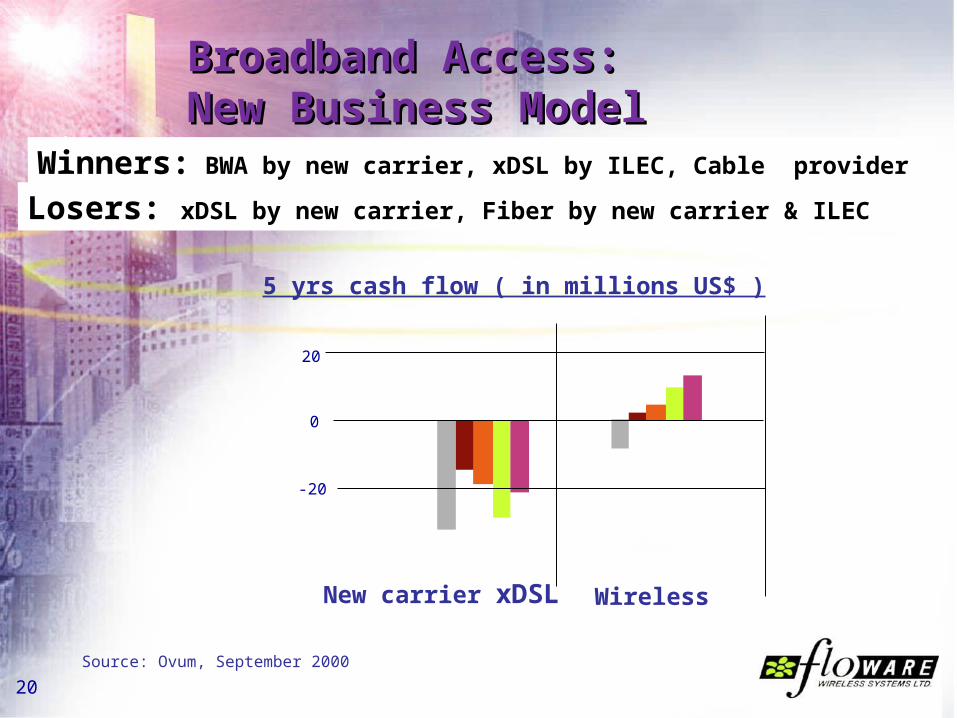

Broadband Access:Broadband Access:New Business ModelNew Business Model

New carrier xDSL

0

-20

20

Wireless

Winners: BWA by new carrier, xDSL by ILEC, Cable provider

Losers: xDSL by new carrier, Fiber by new carrier & ILEC

Source: Ovum, September 2000

5 yrs cash flow ( in millions US$ )

21

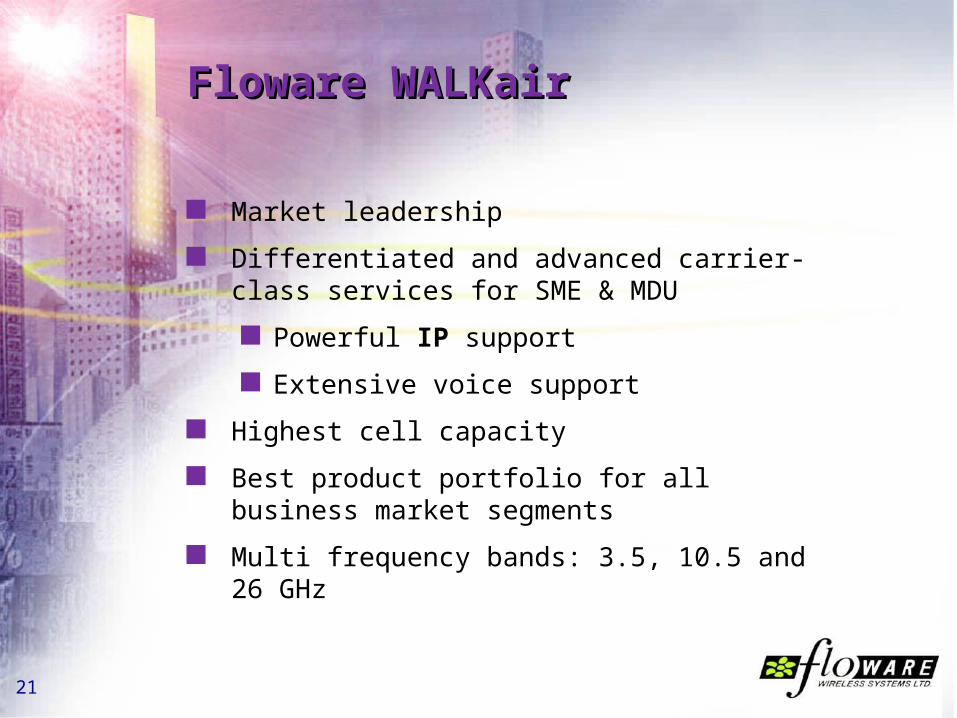

Floware WALKairFloware WALKair

Market leadership

Differentiated and advanced carrier-class services for SME & MDU

Powerful IP support

Extensive voice support

Highest cell capacity

Best product portfolio for all business market segments

Multi frequency bands: 3.5, 10.5 and 26 GHz

22

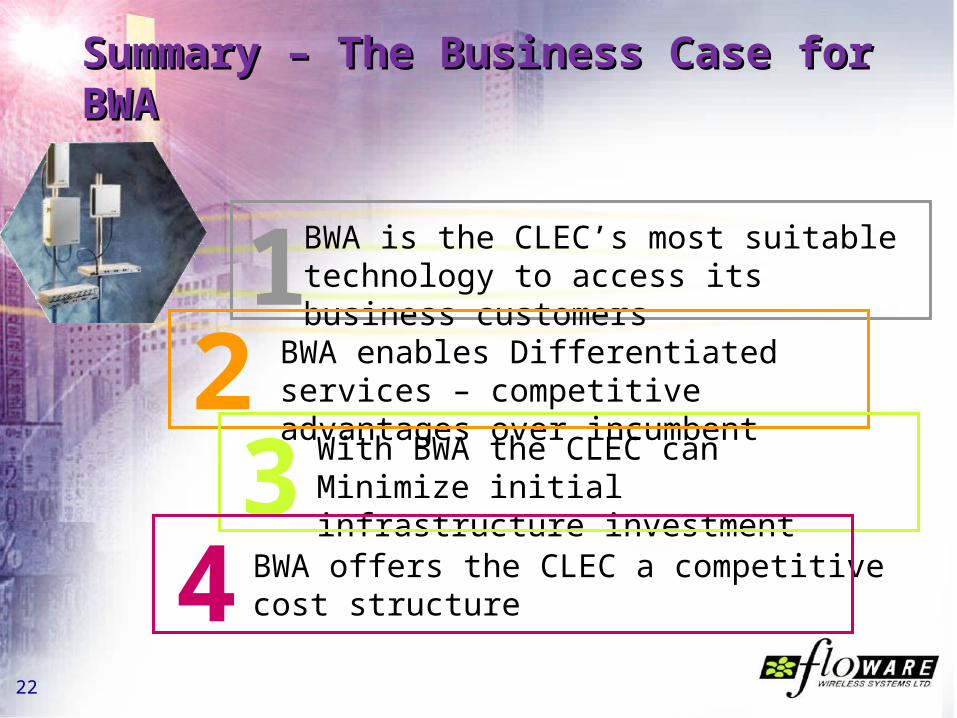

Summary – The BSummary – The Buusiness Case for siness Case for BWABWA

BWA offers the CLEC a competitive cost structure

123

BWA is the CLEC’s most suitable technology to access its business customers

With BWA the CLEC can Minimize initial infrastructure investment

BWA enables Differentiated services – competitive advantages over incumbent

4

23

““Broadbanding the last Broadbanding the last mile”mile”

Thank You Thank You

www.floware.com