Embed Size (px)

Citation preview

1

Rules of Thumb in Real Options Applications

George Y. WangGeorge Y. WangNational Dong-Hwa University

2004 NTU Conference on FinanceDecember 20, 2004

2

Capital Budgeting Practices

0%

20%

40%

60%

80%

Klammer (1972) 29% 30% 39% 35% 3%

Brigham (1975) 70% 78% 48% 74% 18%

Gitman and Forrester (1977) 10% 54% 25% 9% 3%

Oblak and Helm (1980) 14% 60% 14% 10% 2%

Klammer and Walker (1984) 54% 8% 4% 17%

Gilbert and Reichert (1995) 85% 82% 46% 63%

Jog and Srirastava (1995) 85% 82% 46% 63%

Arnold & Hatzopoulos (2000) 80% 81% 56% 70% 31%

Graham and Harvey (2001) 75% 76% 20% 86% 12%

NPVIRR (or Hurdle

Rate)ARR Payback PI Others

3

Capital Budgeting Practices

The literature indicates that NPV, IRR, and payback are top-three frequently used valuation techniques.

Busby and Pitts (1997) and Graham and Harvey (2001) reveal that only a small percentage of firms have formal procedures to appraise real options.

4

MotivationCapital budgeting literature suggests two important facts: first, conventional capital budgeting techniques are shown to have various theoretical shortcomings, yet still have widespread applications in practice; second, real options techniques are considered as relatively sophisticated analysis tools, yet most firms do not make explicit use of real options techniques to evaluate capital investments. This paper aims to bridge the theory-practice gap by translating real options theory into existing capital budgeting practices.

5

Research Purposes

Explore how real options decision criteria can be transformed into equivalent capital budgeting criteria such as NPV, profitability index, hurdle rate, and (discounted) payback. Propose heuristic investment rules in terms of capital budgeting practices to proxy for the inclusion of real options valuation.

6

Modified Capital Budgeting Rules under Real Options (Generalized

Expressions)

NPV

Profitability Index

Payback

Hurdle Rate

Cash Flow Trigger

Discounted Payback

( )NPV V I F V

V

I

V I

ln 1( )

, 0

1 , 0

P

1ln 1

1DP

7

The Comparison between the Modified Investment Rules and

Conventional Rules

8

Stochastic Processes of Interest

0

20

40

60

80

100

120

140

1 11 21 31 41 51 61 71 81 91 101 111 121 131 141 151 161 171 181 191 201

Week

$

GBM Mean Reversion

0

20

40

60

80

100

120

140

1 11 21 31 41 51 61 71 81 91 101 111 121 131 141 151 161 171 181 191 201

Week

$

GBM Mixed1 Mixed2

9

Options, F(V*), and Investment Triggers, V*

GBM

Mixed Diffusion-Jump

Mean Reversion

1( ; ) bF V V AV

1bA V I V

2

1 2 2 2

1 ( ) ( ) 1 2

2 2

r r rb

( ; ) ; ,MRF V V BV G x g

2

2 2 2

1 ( ) 1 2

2 2

r V r V r

2

2x V

2

22

r Vg

2 3( 1) ( 1)( 2)

; , 1( 1) 2! ( 1)( 2) 3!

x xG x g x

g g g g g g

2

2 2 2 2

1 ( ) ( ) 1 2( )

2 2

r r rb

where

2( ; ) bF V V AV

where

where

Pyndick (1991) and Dixit and Pindyck (1994)Pyndick (1991) and Dixit and Pindyck (1994)

10

Real Options in Capital Budgeting (GBM and Mixed Diffusion-Jump)

Profitability Index

Cash Flow Trigger

Hurdle Rate

Payback

Discounted Payback

1

11

1GBM b

1

1

1GBM I Ib

1

1

1GBM b

1

1

1

ln 1( 1)( )

, 0

1 1 , 0

GBM

bb

P

b

1lnDGBM

bP

11

The Option Impact

±=

Modified Rules = Conventional Rules + Option Impact(for PI, Hurdle Rate, and Cash Flow Rules)(for PI, Hurdle Rate, and Cash Flow Rules)

Modified Rules = Conventional Rules – Option Impact(for Payback Rules)(for Payback Rules)

12

Numerical Analysis of the Optimal Triggers under Alternative Processes

100

150

200

250

300

350

0 5% 10% 15% 20% 25% 30% 35% 40%

Volatility

Trig

ger V

alue

GBM or Mixe(λ = 0)

Mixed (λ = 10%)

Mixed (λ = 20%)

Mixed (λ = 30%)

MR (η = 0.02)

MR (η = 0.03)

MR (η = 0.04)

GBM Model

Mixed Diffusion-Jump

Mean Reversion

100, 5%, r 5%I V

13

Findings

The graph suggests that for a set of reasonable parameter values, both mean reversion and competitive arrivals have a significant influence on lowering optimal triggers, indicating that investment in both cases should be launched sooner than the normal GBM case. It seems that mean reversion has a stronger power to induce investment than the competitive arrival effect.

14

The Comparison between the Modified Investment Rules and

Conventional Rules

15

The Cost of Suboptimal Investment Rules under a GBM

0

4

8

12

16

100 120 140 160 180 200 220 240 260 280 300

Arbitrary Trigger ($)

Opt

ion

Val

ue ($

)

ρ =20%, σ =20% ρ =30%, σ =20% ρ =20%, σ =40% ρ =30%, σ =40%

L

H100, 5%, 5%V I r

16

The Cost of Suboptimal Investment Rules under a Mixed Diffusion-Jump

0

4

8

12

16

100 120 140 160 180 200 220 240 260 280 300

Arbitrary Trigger ($)

Opt

ion

Val

ue ($

)

ρ =20%, σ =20%, λ =0.2 ρ =30%, σ =20%, λ =0.2 ρ =20%, σ =40%, λ =0.2

ρ =30%, σ =40%, λ =0.2 ρ =20%, σ =40%, λ =0.4 ρ =20%, σ =40%, λ =0.4

H

L

100, 5%, 5%V I r

17

0

5

10

15

20

25

30

35

100 110 120 130 140 150 160 170 180 190 200

Arbitrary Trigger ($)

Opt

ion

Val

ue ($

)

η =0.03, σ =20% η =0.05, σ =20% η =0.03, σ =40% η =0.05, σ =40%

L H

100, 5%, r 5%V I V

The Cost of Suboptimal Investment Rules under a Mean Reversion

18

Findings

The best investment rule under uncertainty is the optimal investment rule itself.

However, if a simple heuristic decision rule is used to approximate V*, the rule should be as near as possible in order to minimize the opportunity cost of adopting the suboptimal investment policy.

19

The Process of Developing Heuristics

Identify a proper stochastic processConduct base-case analysis to determine target investment ruleConduct regression analysis and sensitivity analysis to identify key determinants and weightsFine-tuning the weightsDetermine heuristic rules

Model Formulation

Regression Analysis

Base Case Analysis

Sensitivity Analysis

Monte Carlo Simulation

3-9 Rule2-10 Rule or

2-10-(-2) Rule

GBM ModelDiffusion-Jump

ModelMean Reversion

Model

4-8 Rule

Adjusting the Weights

20

Optimal Hurdle Rate as a Function of σ and μ under a GBM

17%18%

21%

25%

30%

21%24%

28%

32%

37%

31%33%

36%

41%

46%

41%43%

46%

50%

55%

0%

10%

20%

30%

40%

50%

60%

10% 20% 30% 40% 50%

Volatility

The

Opt

imal

Hur

dle

Rat

e

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(γ*

)

8%

21

Optimal Hurdle Rate as a Function of σ and μ under a Mixed Diffusion-

Jump

29%31%

33%35%

38%

42%41%42%

45%

49%

53%

27%25%

23%21%

0%

10%

20%

30%

40%

50%

60%

10% 20% 30% 40% 50%

Volatility

The

Opt

imal

Hur

dle

Rat

e

Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(γ*

)

8%, 20%

22

Optimal Hurdle Rate as a Function of σ and μ under a

Mean Reversion

21%23%

25%28%

30%31%34%

37%

40%

43%41%

44%

47%

51%

56%

0%

10%

20%

30%

40%

50%

60%

10% 20% 30% 40% 50%

Volatility

The

Opt

imal

Hur

dle

Rat

e

Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(γ*

)

100, 0.02V

23

The Sensitivity of Other Capital Budgeting Criteria to σ and μ under

a GBM

4.33

5.24

6.65

8.53

10.88

2.43

1.111.63

1.33

2.001.72

1.04

1.481.291.13

1.02 1.08 1.18 1.311.47

0

2

4

6

8

10

12

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Pro

fitab

ility

Ind

ex T

rigge

r

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(Π*

)

10.47

13.30

17.06

21.76

8.65

29.21

13.26

19.60

16.00

24.00

37.85

22.77

32.60

28.28

24.94

47.06

41.89

37.71

34.6032.66

0

5

10

15

20

25

30

35

40

45

50

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Cas

h F

low

Trig

ger

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(π*

)

7.09

5.89

4.81

3.91

8.19

3.03

5.90

4.28

5.07

3.60

2.40

3.76

2.743.11

3.48

1.962.18

2.402.602.74

0

1

2

3

4

5

6

7

8

9

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Pya

back

Trig

ger

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(P*

)

10.60

8.15

6.23

4.82

13.15

4.41

19.61

7.89

11.55

5.78

3.96

15.39

5.11

6.84

9.71

3.564.51

5.90

8.09

12.18

0

5

10

15

20

25

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Dis

coun

edt

Pay

back

Trig

ger

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

()

DP

24

The Sensitivity of Other Capital Budgeting Criteria to σ and μ under

a MX Process

1.36

1.53

1.75

2.00

2.28

1.77

1.08

1.38

1.22

1.571.53

1.03

1.37

1.231.12

1.021.08

1.161.27

1.39

0

1

1

2

2

3

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Pro

fitab

ility

Ind

ex T

rigge

r

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(Π*

)

3.07 3.50 4.00 4.57

2.72

21.26

12.98

16.5914.65

18.80

33.62

22.74

30.16

27.13

24.60

44.54

40.56

37.16

34.4632.65

0

5

10

15

20

25

30

35

40

45

50

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Cas

h F

low

Trig

ger

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(π*

)

16.04

14.87

13.73

12.65

17.15

3.99

6.00

4.925.45

4.43

2.67

3.77

2.943.233.52

2.062.252.442.612.74

0

2

4

6

8

10

12

14

16

18

20

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Pay

back

Trig

ger

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

(σ )

(P*

)

52.77

42.36

34.66

28.80

66.58

6.93

21.52

10.7014.25

8.48

4.83

15.58

5.947.57

10.22

3.964.866.178.25

12.23

0

10

20

30

40

50

60

70

10% 20% 30% 40% 50%

Volatility

Equ

ival

ent

Dis

coun

ted

Pay

back

Trig

ger

Discount Rate = 10% Discount Rate = 20% Discount Rate = 30% Discount Rate = 40%

()

DP

(σ )

25

Monte Carlo Simulation

26

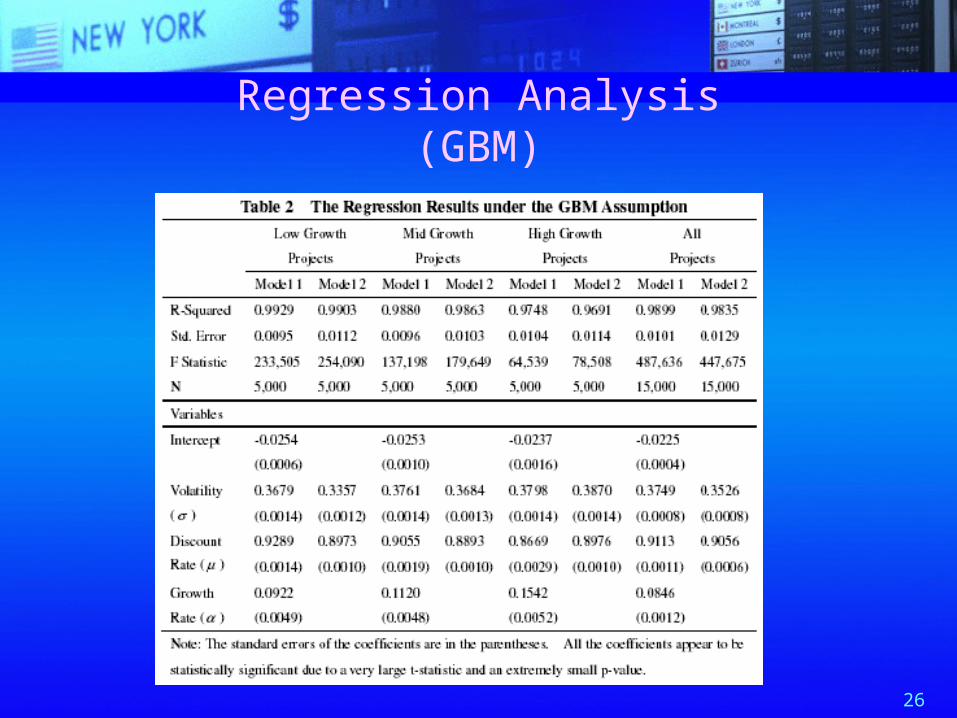

Regression Analysis(GBM)

27

Regression Analysis(Mixed Diffusion-Jump)

28

Regression Analysis(Mean Reversion)

29

Heuristic Investment Rules

Model Formulation

Regression Analysis

Base Case Analysis

Sensitivity Analysis

Monte Carlo Simulation

3-9 Rule2-10 Rule or

2-10-(-2) Rule

GBM ModelDiffusion-Jump

ModelMean Reversion

Model

4-8 Rule

Adjusting the Weights

30

Sensitivity to Growth Rate

Classify five types of projects Project A: high discount rate (μ=35%) and

high volatility (σ=40%) Project B: high discount rate (μ=35%) and

low volatility (σ=10%) Project C: middle discount rate (μ=25%)

and middle volatility (σ=25%) Project D: low discount rate (μ=15%) and

high volatility (σ=10%) Project E: low discount rate (μ=15%) and

low volatility (σ=10%)

31

Sensitivity to Growth RateGBM Model

0%

10%

20%

30%

40%

50%

60%

Growth Rate

Opt

imal

Hur

dle

Rat

e

Project A 44.74% 44.79% 44.84% 44.89% 44.94% 45.00% 45.06% 45.12% 45.19% 45.26% 45.34% 45.42% 45.51% 45.60% 45.70%

Project B 35.64% 35.65% 35.66% 35.66% 35.67% 35.68% 35.68% 35.69% 35.70% 35.71% 35.73% 35.74% 35.75% 35.77% 35.79%

Project C 29.30% 29.35% 29.41% 29.48% 29.55% 29.63% 29.72% 29.81% 29.92% 30.04% 30.18% 30.33% 30.50% 30.70% 30.93%

Project D 26.47% 26.63% 26.81% 27.00% 27.21% 27.43% 27.68% 27.94% 28.23% 28.54% 28.88% 29.25% 29.64% 30.06% 30.52%

Project E 16.00% 16.07% 16.15% 16.26% 16.41% 16.61% 16.89% 17.27% 17.77% 18.39% 19.11% 19.91% 20.76% 21.65% 22.57%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14%

( )

()

32

Sensitivity to Growth RateMixed Diffusion-Jump Model (λ= 20%)

0%

10%

20%

30%

40%

50%

60%

Growth Rate

Opt

imal

Hur

dle

Rat

e

Project A 43.61% 43.59% 43.58% 43.56% 43.54% 43.51% 43.49% 43.45% 43.42% 43.38% 43.33% 43.28% 43.22% 43.16% 43.08%

Project B 35.64% 35.64% 35.65% 35.65% 35.66% 35.66% 35.67% 35.68% 35.69% 35.69% 35.70% 35.71% 35.73% 35.74% 35.75%

Project C 28.78% 28.79% 28.79% 28.79% 28.80% 28.80% 28.79% 28.78% 28.77% 28.75% 28.73% 28.69% 28.65% 28.59% 28.51%

Project D 22.39% 22.22% 22.02% 21.80% 21.55% 21.26% 20.94% 20.57% 20.15% 19.68% 19.13% 18.52% 17.81% 17.00% 16.07%

Project E 15.88% 15.91% 15.94% 15.98% 16.02% 16.06% 16.11% 16.14% 16.17% 16.17% 16.14% 16.06% 15.93% 15.72% 15.41%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14%

()

( )

33

Sensitivity to Growth RateMean Reversion Model

0%

10%

20%

30%

40%

50%

60%

Growth Rate

Opt

imal

Hur

dle

Rat

e

Project A 44.40%44.51%44.62%45.09%45.41%45.45%45.30%45.03%44.69%44.30%43.89%43.48%43.06%42.64%42.22%41.81%

Project B 36.08%36.12%36.14%36.15%36.14%

Project C 29.00%29.29%29.51%29.72%29.75%29.65%29.48%29.26%29.01%28.76%28.50%28.25%27.99%27.74%27.49%27.24%

Project D 26.47%23.93%22.86%21.93%21.08%20.31%19.60%18.96%18.36%17.79%17.27%16.77%16.30%15.85%15.41%15.00%

Project E 16.00%16.07%16.20%16.23%16.19%16.12%16.02%15.91%15.80%15.69%15.57%15.46%15.34%15.23%15.11%15.00%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10% 11% 12% 13% 14% 15%

( )

()

34

4-8 Rule under a GBM

0%

20%

40%

60%

80%

0% 20% 40% 60% 80%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

ρ = 0.9925

0%

20%

40%

60%

80%

0% 20% 40% 60% 80%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

ρ = 0.9900

0%

20%

40%

60%

80%

0% 20% 40% 60% 80%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

ρ = 0.9830

Low-Growth Projects Mid-Growth Projects

High-Growth Projects

35

3-9 Rule under a Mixed Diffusion-Jump

0%

20%

40%

60%

80%

0% 20% 40% 60% 80%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

ρ = 0.9955

0%

20%

40%

60%

80%

0% 20% 40% 60% 80%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

ρ = 0.9909

0%

20%

40%

60%

80%

0% 20% 40% 60% 80%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

ρ = 0.9762

Low-Growth Projects Mid-Growth Projects

High-Growth Projects

36

2-10 Rule and 2-10-(-2) Rule under a Mean Reversion

0%

10%

20%

30%

40%

50%

0% 10% 20% 30% 40% 50%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

ρ = 0.9953

0%

20%

40%

60%

80%

0% 20% 40% 60% 80%

The Heuristic Hurdle Rate

The

Opt

imal

Hur

dle

Rat

e

0.9271

3.76%

( ) 3.37%

0.0023

SD

MSE

2-10 RuleZero-Growth Projects

2-10-(-2) RuleAll Projects

37

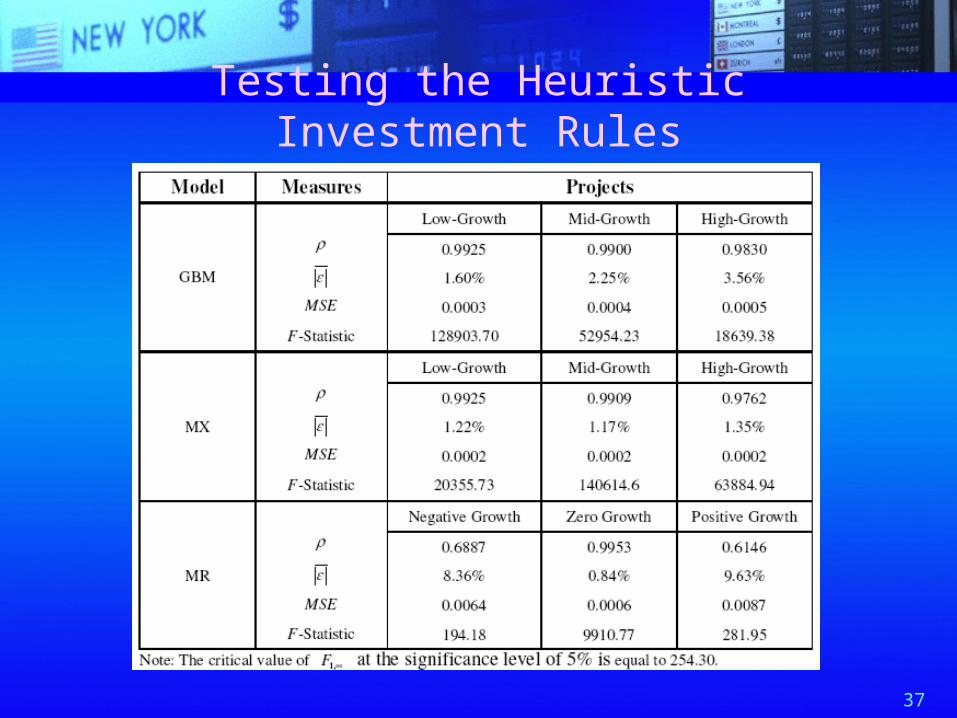

Testing the Heuristic Investment Rules

38

Implications

The heuristic investment rules provide a seemingly accurate approximation to the optimal investment rules by a set of two parameters, volatility and discount rate, under managerial flexibility and uncertainty. Corporate practitioners can apply real options techniques without always carrying out complicated analysis.