Embed Size (px)

Citation preview

1

Retirement Plans Overview and Regulatory Update for 2012

Presented by:

Mary Scott, CFP®, CRPS®

Vice President, Retirement Plan Specialist

2

Today’s Agenda

• Overview of Employer Sponsored Plans– Defined contribution and defined benefit plans

• Fee Disclosure Rules for 2012– Service provider fee disclosures– Participant level fee disclosures

3

MANDATORYMANDATORY VOLUNTARYVOLUNTARYSocial SecuritySocial SecurityUnemployment TaxUnemployment Tax

Health, Medical & Health, Medical & Retirement PlansRetirement Plans

TAX FAVOREDTAX FAVOREDSEP/SAR-SEPSEP/SAR-SEPSIMPLE-IRASIMPLE-IRA

QUALIFIEDQUALIFIED NONQUALIFIEDNONQUALIFIED457457

Deferred CompensationDeferred CompensationTop Hat (SERP)Top Hat (SERP)Excess BenefitExcess Benefit

DEFINED CONTRIBUTIONDEFINED CONTRIBUTIONProfit SharingProfit SharingAge Weighted/Cross Tested P/SAge Weighted/Cross Tested P/S401(k)/SIMPLE 401(k)401(k)/SIMPLE 401(k)Money Purchase PensionMoney Purchase PensionESOPESOP

DEFINED BENEFITDEFINED BENEFITPensionPension

403(b)403(b) 457(b)457(b)

Employer Benefit Plans

4

Retirement Plan Options

• SEP-IRA• SIMPLE-IRA• Profit Sharing• 401(k) Profit Sharing• Defined Benefit• 403(b)

5

SEP-IRA

• Flexible, employer-only contributions are made to individual IRAs on behalf of employees

• Limited fiduciary liability as employees direct their own IRA investments

• Simple to establish and maintain with minimal administration costs

6

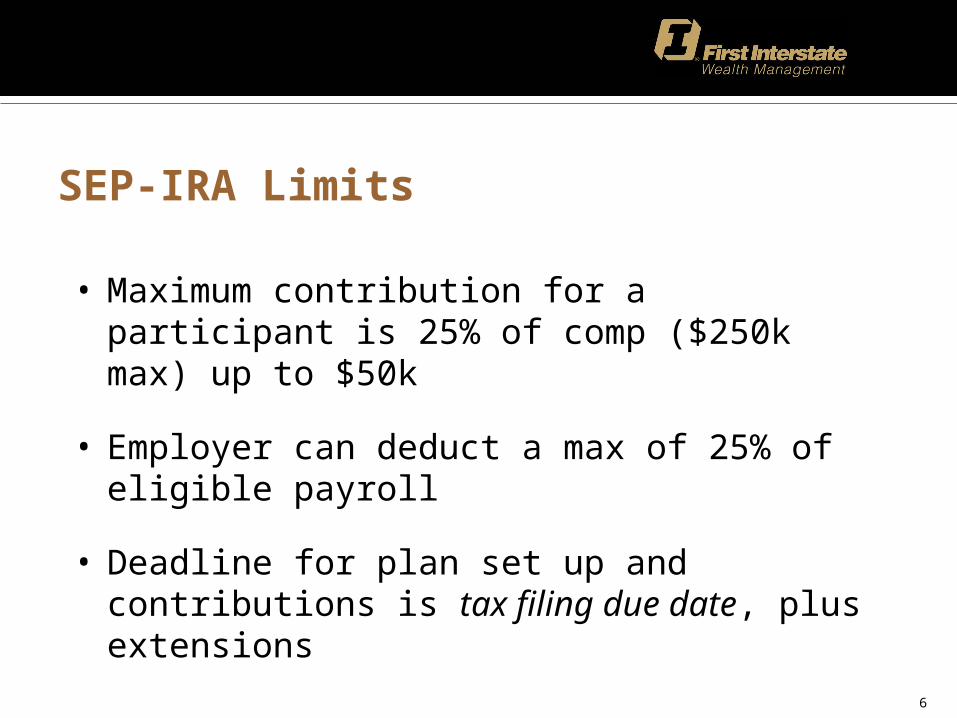

SEP-IRA Limits

• Maximum contribution for a participant is 25% of comp ($250k max) up to $50k

• Employer can deduct a max of 25% of eligible payroll

• Deadline for plan set up and contributions is tax filing due date, plus extensions

7

SIMPLE-IRA

• For business owners who want employees to share responsibility for their retirement

• Funding to SIMPLE IRAs, where employees direct investments, minimizes employer fiduciary issues

• Plan administration costs are minimal

8

SIMPLE-IRA Limits

• Employee deferral limit for 2012 is $11,500 with a $2,500 catch up for participants over age 50

• Mandatory employer contribution– 3% match or – 2% non-elective contribution

9

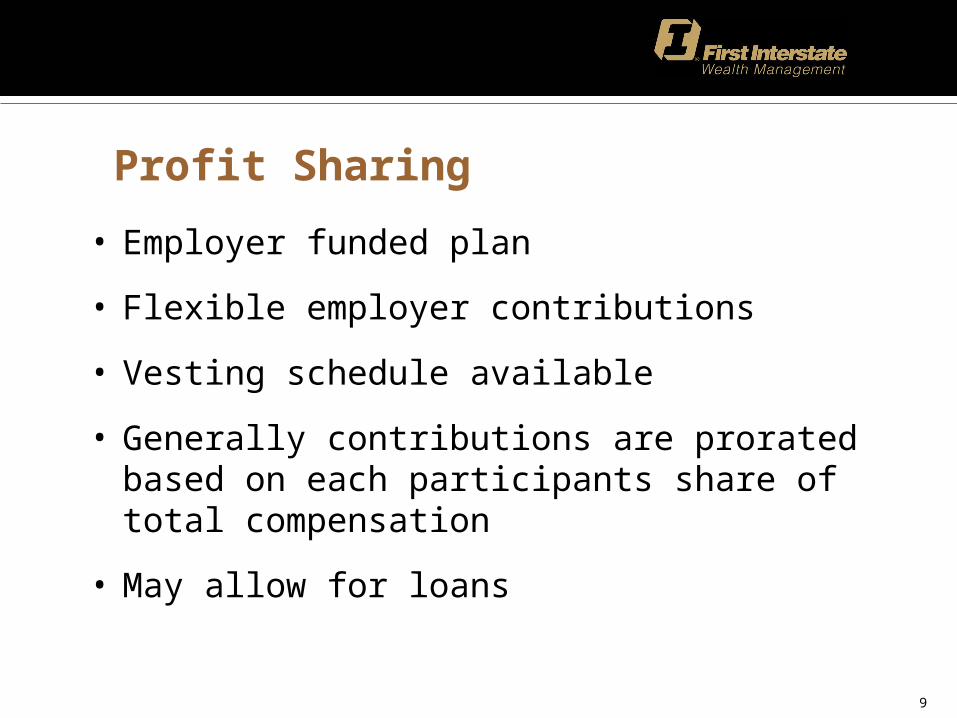

Profit Sharing

• Employer funded plan

• Flexible employer contributions

• Vesting schedule available

• Generally contributions are prorated based on each participants share of total compensation

• May allow for loans

10

Profit Sharing Limits

• Maximum contribution for participant is 100% of compensation up to $50k (2012)

• Employer can deduct a max of 25% of eligible payroll

• Plan must be established by end of taxable year

• Contributions must be made by tax filing deadline

11

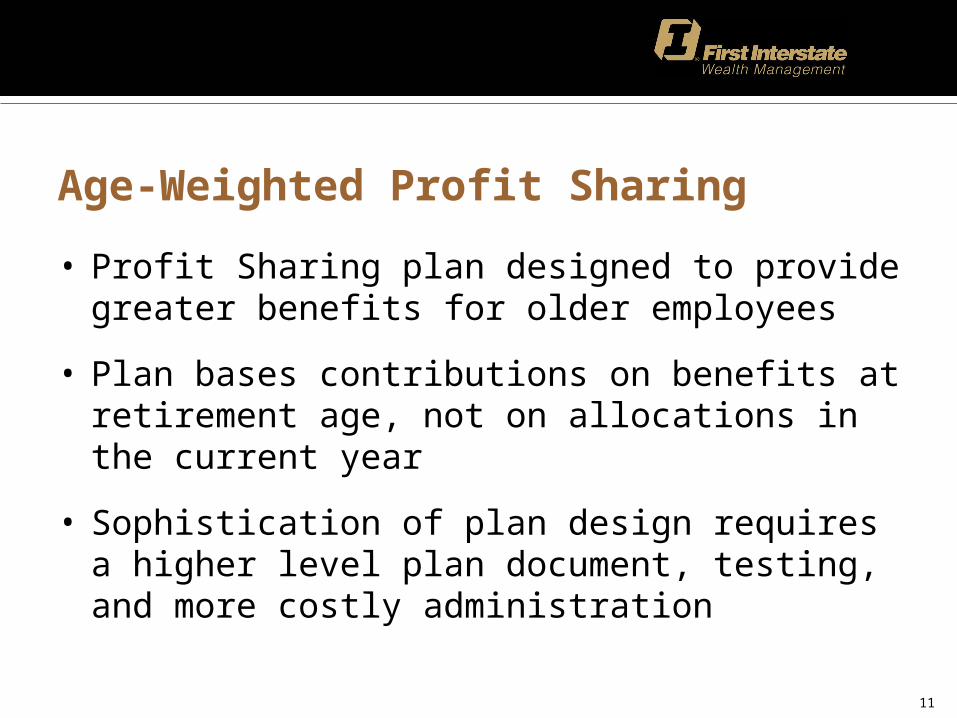

Age-Weighted Profit Sharing

• Profit Sharing plan designed to provide greater benefits for older employees

• Plan bases contributions on benefits at retirement age, not on allocations in the current year

• Sophistication of plan design requires a higher level plan document, testing, and more costly administration

12

New Comparability Profit Sharing

• Profit Sharing plan designed to vary the benefits by different employee groups

• Plan measures benefits at retirement, not on contribution in current year - similar to Age Weighted plan

• Plan appeals to businesses interested in favoring specific employees

13

Employees Age Compensation Standard Integrated Age-Weighted New Comp Doctor, B* 44 $250,000.00 $50,000.00 $50,000.00 $50,000.00 $50,000.00

Doctor, A* 53 $250,000.00 $50,000.00 $50,000.00 $50,000.00 $50,000.00

Group A $500,000.00 $100,000.00 $100,000.00 $100,000.00 $100,000.00

Asst, C 23 $26,000.00 $5,200.00 $4,370.67 $1,138.74 $1,300.00

Asst, B 26 $26,000.00 $5,200.00 $4,370.67 $1,414.66 $1,300.00

Asst, A 46 $30,000.00 $6,000.00 $5,043.08 $6,933.75 $1,500.00

Nurse, B 29 $40,000.00 $8,000.00 $6,724.11 $2,703.73 $2,000.00

Nurse, A 40 $60,000.00 $12,000.00 $10,086.17 $8,985.61 $3,000.00

Receptionist, A 24 $24,000.00 $4,800.00 $4,034.47 $1,129.98 $1,200.00

Group B $206,000.00 $41,200.00 $34,629.18 $22,306.47 $10,300.00

Total $706,000.00 $141,200.00 $134,629.18 $122,306.47 $110,300.00

Group A % 70.82% 70.82% 74.28% 81.76% 90.66%

Group B % 29.18% 29.18% 25.72% 18.24% 9.34%

14

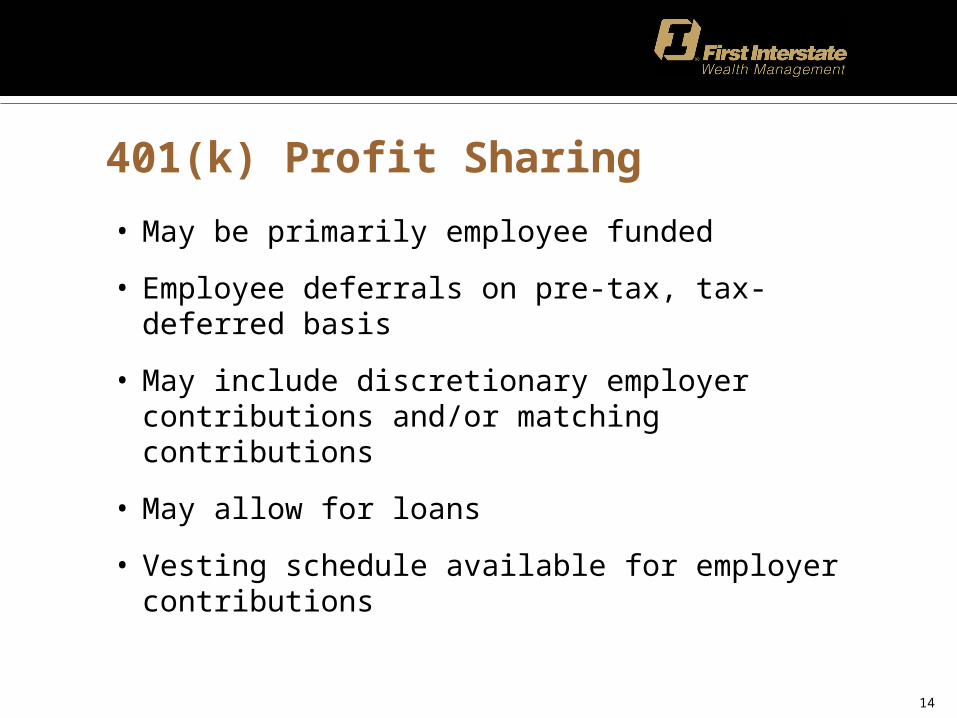

401(k) Profit Sharing

• May be primarily employee funded

• Employee deferrals on pre-tax, tax-deferred basis

• May include discretionary employer contributions and/or matching contributions

• May allow for loans

• Vesting schedule available for employer contributions

15

401(k) P/S Limits

• Employee contributions up to $17,000 with a $5,500 catch up for participants age 50+

• Employer contribution cannot exceed 25% of eligible payroll

• Maximum benefit an employee can receive in the plan $50k or 100% of comp

16

Safe Harbor 401(k) P/S

• Suitable for businesses where owners/ highly compensated employees are limited in their contributions

• Plan eliminates the need for some nondiscrimination tests

• Mandatory employer contribution must be made to plan

• No vesting schedule on the S/H contribution

17

Safe Harbor 401(k) Contributions

• Non-elective contribution of 3%, or a

• Matching contribution

– Basic match formula matches 100% of the first 3% of deferrals, then 50% between 3%-5% of deferrals

• Enhanced match available

18

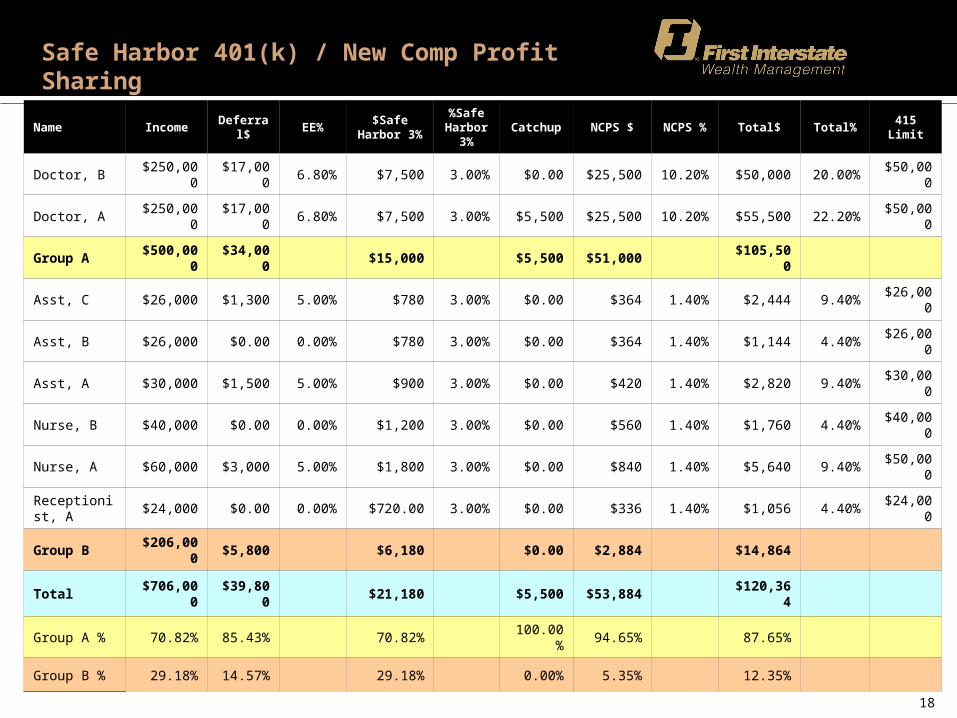

Name Income Deferral$ EE%$Safe

Harbor 3%

%Safe Harbor

3%Catchup NCPS $ NCPS % Total$ Total% 415 Limit

Doctor, B $250,000 $17,000 6.80% $7,500 3.00% $0.00 $25,500 10.20% $50,000 20.00% $50,000

Doctor, A $250,000 $17,000 6.80% $7,500 3.00% $5,500 $25,500 10.20% $55,500 22.20% $50,000

Group A $500,000 $34,000 $15,000 $5,500 $51,000 $105,500

Asst, C $26,000 $1,300 5.00% $780 3.00% $0.00 $364 1.40% $2,444 9.40% $26,000

Asst, B $26,000 $0.00 0.00% $780 3.00% $0.00 $364 1.40% $1,144 4.40% $26,000

Asst, A $30,000 $1,500 5.00% $900 3.00% $0.00 $420 1.40% $2,820 9.40% $30,000

Nurse, B $40,000 $0.00 0.00% $1,200 3.00% $0.00 $560 1.40% $1,760 4.40% $40,000

Nurse, A $60,000 $3,000 5.00% $1,800 3.00% $0.00 $840 1.40% $5,640 9.40% $50,000

Receptionist, A

$24,000 $0.00 0.00% $720.00 3.00% $0.00 $336 1.40% $1,056 4.40% $24,000

Group B $206,000 $5,800 $6,180 $0.00 $2,884 $14,864

Total $706,000 $39,800 $21,180 $5,500 $53,884 $120,364

Group A % 70.82% 85.43% 70.82% 100.00% 94.65% 87.65%

Group B % 29.18% 14.57% 29.18% 0.00% 5.35% 12.35%

Safe Harbor 401(k) / New Comp Profit Sharing

19

Defined Benefit Pension Plan

• Provides a determinable annual benefit at retirement

• Plan contribution formulas are based on a specific retirement benefit– Max benefit to fund for in 2012 is $200,000

• Contribution is actuarially determined and is usually made quarterly

• No loans or in-service withdrawals allowed

20

403(b) Plans

• Non-profit 501(c)(3) organizations and public schools, college or university

• ERISA and non-ERISA plans• Limits same as 401(k)s• Document required for all types (2009)• Information sharing arrangements required with

providers allowed under the plan

21

DOL’s Fee Disclosure Initiatives

• Part 1: Schedule C of the form 5500 (2009)• Part 2: Covered service provider disclosure

under ERISA 408(b)(2) (July 1, 2012)• Part 3: Plan fiduciary disclosure to participants

who direct their own investments DOL 404a-5 (August 30, 2012)

22

Purpose of the new rules

• Help plan fiduciaries to determine if contracts are “reasonable”

• Provide transparency with regards to plan fees• Inform participants of the fees they pay inside of

the plan

23

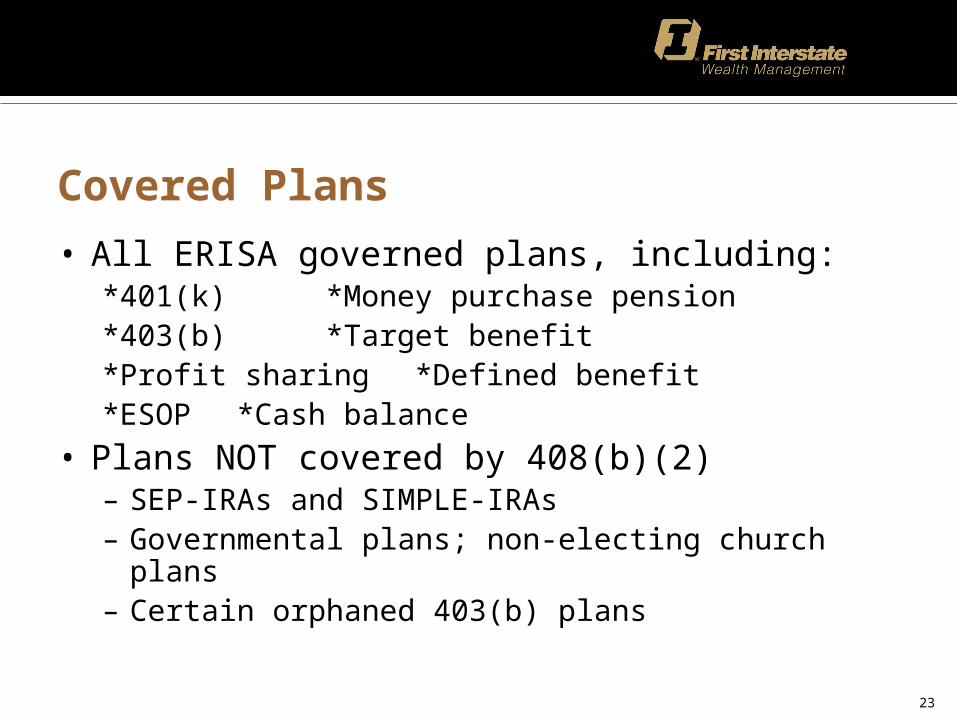

Covered Plans

• All ERISA governed plans, including: *401(k) *Money purchase pension*403(b) *Target benefit*Profit sharing *Defined benefit*ESOP *Cash balance

• Plans NOT covered by 408(b)(2)– SEP-IRAs and SIMPLE-IRAs– Governmental plans; non-electing church plans– Certain orphaned 403(b) plans

24

Covered Service Providers

• Broker-Dealers• Registered Investment Advisers (RIAs)• Recordkeepers• Third Party Administrators (TPAs)• Banks and trust companies• Only if expected to receive $1000 over life of

contract

25

Plan Sponsor Obligations

• Determine “covered” service providers• Make sure each has disclosed by July 1, 2012

– All required information been disclosed?– Non-compliant service providers must be reported to

the DOL and terminated (90 days)

• Determine whether each service arrangement is “reasonable”

26

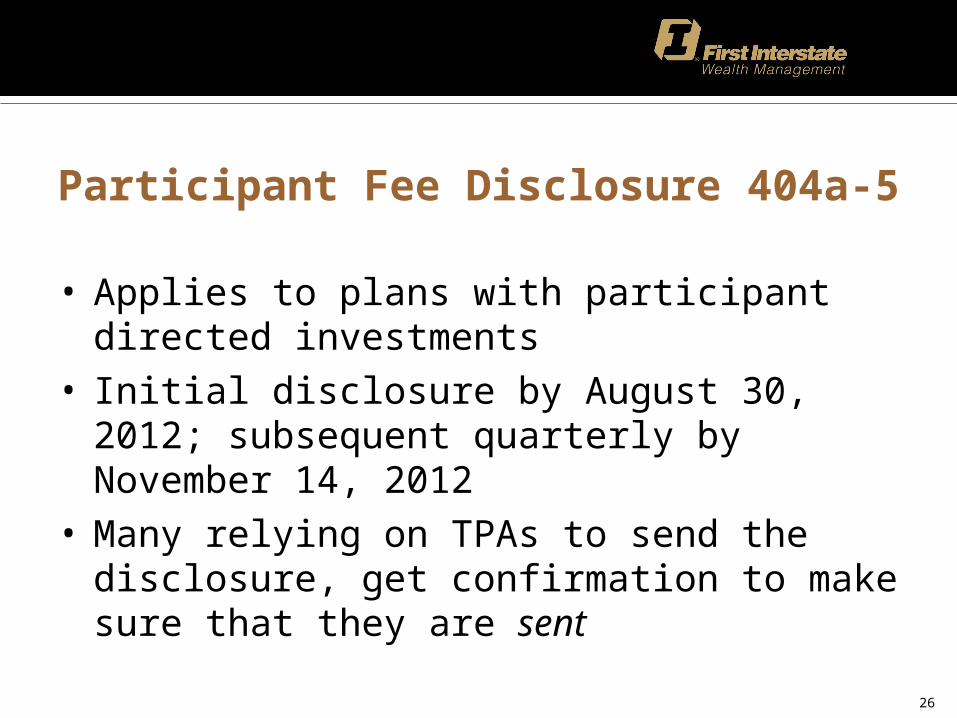

Participant Fee Disclosure 404a-5

• Applies to plans with participant directed investments

• Initial disclosure by August 30, 2012; subsequent quarterly by November 14, 2012

• Many relying on TPAs to send the disclosure, get confirmation to make sure that they are sent

27

Participant Fee Disclosure Contents

• Disclosure must contain:– Plan related information– Information regarding plan administrative and

individual expenses– Investment information about designated investment

alternatives• Performance data, benchmarks, fees, website, etc.• Comparative chart format

28

Preparing Your Participants

• Communicate, communicate, communicate!• The fees are not new, nothing has changed but

the disclosure• Don’t let fee disclosure overshadow the many

benefits of the plan– Tax savings – Matching contributions

– Higher contribution limits