Embed Size (px)

Citation preview

1

REFORMING SOCIAL SECURITY: WHAT CAN

INDONESIA LEARN FROM OTHER COUNTRIES?

by Estelle JamesPrepared for USAID workshop on social

security, Jakarta

2

Population aging and its impact on public spending

• Proportion of world’s people > 60 will increase from 9% to 16% by 2030

• Indonesia’s elderly will increase: from 7% to 16% • Public spending on health and pensions increases as

population ages, so spending on health and pensions will > 10% of GDP in Indonesia by 2030

• Young workers today will be 60+ in 2030, so important to set good old age security system now

• This will have a major impact on economy—quantity and productivity of labor and capital

• Many countries are reforming their social security systems to get better economic and equity effects

3

Public Health and Pension Spending versus Population Aging

Spending as a percentage of GDP

Percentage of population over 60 years old

0 5 10 15 20 250

5

10

15

20

Spending on health and pension

Spending on health

U.K.

Poland

Sweden

Austria

Czechoslovakia

Iceland

Australia

Cyprus

Switzerland

Japan

Brazil Trinidad & Tobago

ChinaJamaica

IndonesiaS. Korea

SwazilandZambia

Canada

New Zealand

4

Major lessons

• Don’t rush into DB scheme without careful actuarial analysis of long term costs—otherwise Finance Ministry will be faced with huge pension debt (already the case for civil service)

• Pre-funding important but don’t increase it until you have a competitive structure that will: – earn a high rate of return with low administrative costs– Diversify your investment portfolio to raise return and

reduce risk

• Informal sector cannot be covered by contributory scheme—requires finance from general treasury

5

Traditional schemes • In past, many countries had pay-as-you-go (PAYG)

defined benefit (DB) schemes – DB—pension based on worker’s wage and years of

contributions – PAYG—contributions by workers (or govt) today used to pay

pensions of retirees today, no investments– Indonesia has this in civil service but not private sector

• Some countries had defined contribution (DC) plans—workers get back contributions + interest (no DB). Funds accumulate but invested by public agency (Jamsostek)—political control, low returns

• Both these plans had big problems. Recently, many countries have switched to DC plans with funds under private competitive management

6

PAYG schemes worked well when systems were new and no retirees, but require large

contribution rate increases now• Why higher contribution rate?

– Workers evade contributions so less revenue

– Workers retire early so collect benefits for more years

– Population ages so fewer workers, more pensioners

• Problems caused by high contribution rate– Less take-home pay if worker pays

– Higher labor costs, less employment if employer pays

– Fewer workers in formal labor force (evasion, early retirement) so less economic growth

7

Other problems caused by PAYG DB schemes

• Redistributes to high earners (who live longer) and first covered generations (high benefits, low contributions)—these are better-off groups, not poorest groups

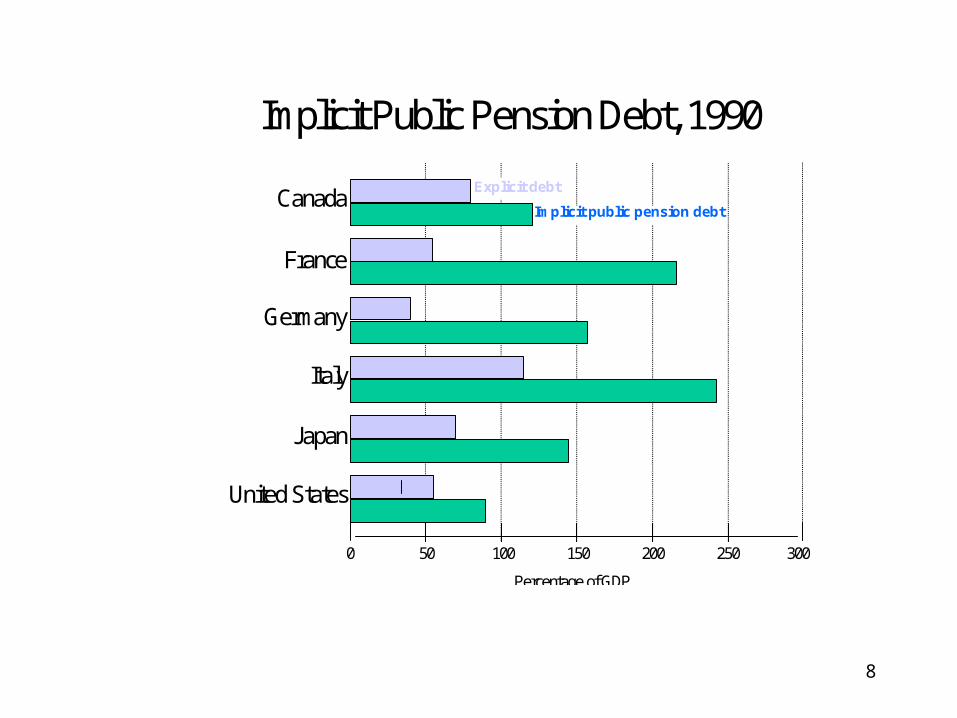

• Government owes workers large unfunded pension debt in return for contributions (>100% GDP)--paying this debt may reduce public spending on health and education

• May discourage saving, investment, economic growth

8

Percentage of GDP

0 50 100 150 200 250 300

France

Germany

Italy

Canada

United States

Japan

Explicit debt

Implicit public pension debt

Implicit Public Pension Debt, 1990

9

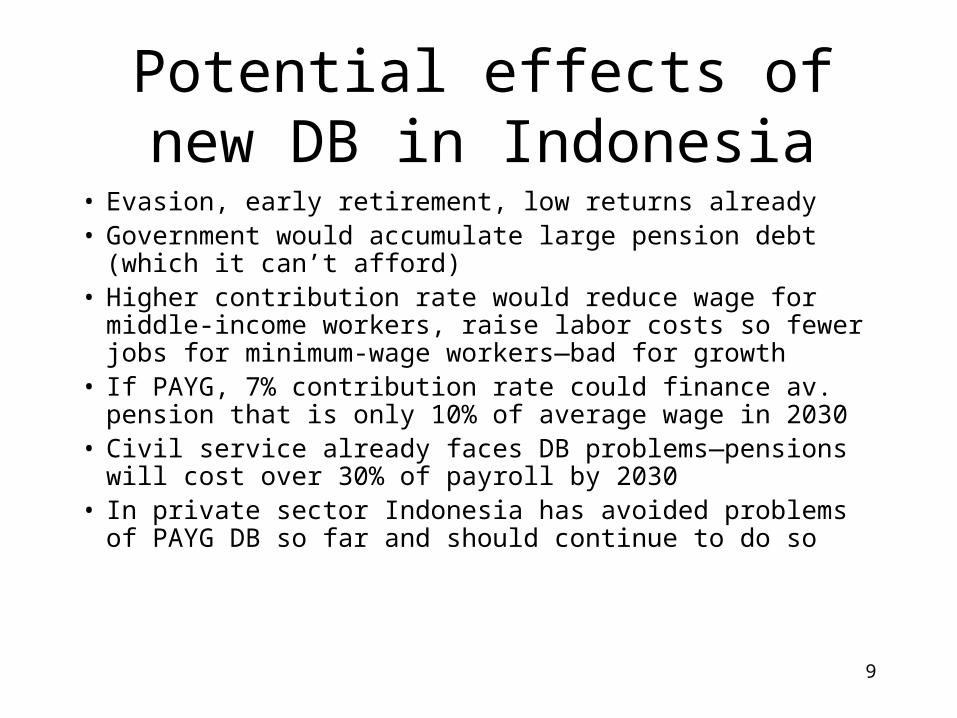

Potential effects of new DB in Indonesia

• Evasion, early retirement, low returns already• Government would accumulate large pension debt (which

it can’t afford)• Higher contribution rate would reduce wage for middle-

income workers, raise labor costs so fewer jobs for minimum-wage workers—bad for growth

• If PAYG, 7% contribution rate could finance av. pension that is only 10% of average wage in 2030

• Civil service already faces DB problems—pensions will cost over 30% of payroll by 2030

• In private sector Indonesia has avoided problems of PAYG DB so far and should continue to do so

10

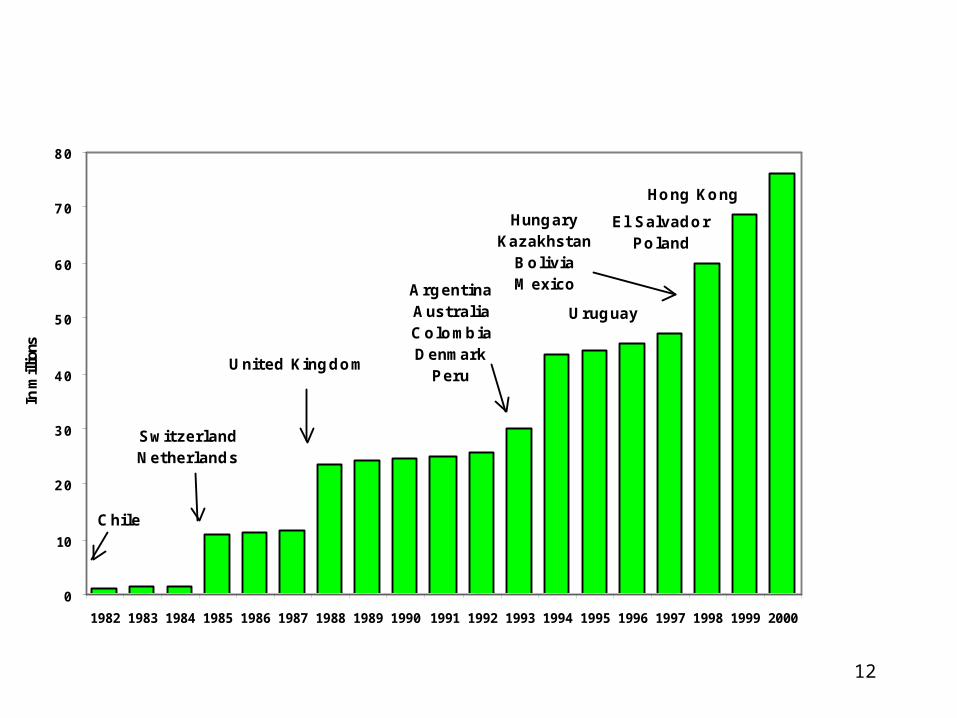

How have countries reformed?• Over 30 countries in Latin America, Europe, Asia-

Pacific have adopted multi-pillar system to avoid these problems

• One pillar handles peoples retirement savings– Shift to DC plan (not primarily DB)– Shift to pre-funding rather than PAYG– Funds are privately managed to avoid political control

• Another pillar provides safety net (redistribution)• A third pillar is voluntary retirement savings• Chile was first country to reform in 1981. So far: large

assets, increased saving, greater formal labor supply, financial market development, economic growth, poor are protected

11

The Pillars of Old Age Income Security

Mandatory publicly-

managed pillar

Voluntary pillar

Objectives

Form

Financing

Redistributionplus

Co-insurance

Savings plus

Co-insurance

Savings plus

Co-insurance

Flat or Means-tested

orMinimum pension

guarantee

Personal savings plan

orOccupational

plan

Personal savings plan

orOccupational

plan

Tax financedRegulated

Fully funded Fully funded

Mandatory privately-

managed pillar

12

0

10

20

30

40

50

60

70

80

1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

In m

illio

ns

Chile

SwitzerlandNetherlands

United Kingdom

ArgentinaAustraliaColombiaDenmark

Peru

Uruguay

HungaryKazakhstan

Bolivia Mexico

El SalvadorPoland

Hong Kong

13

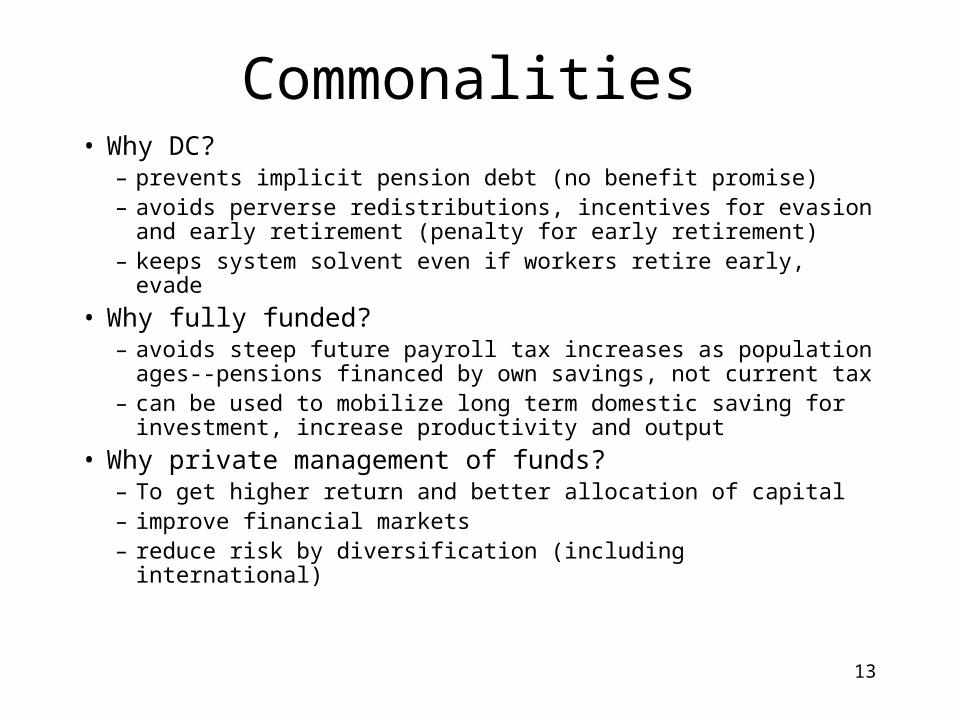

Commonalities • Why DC?

– prevents implicit pension debt (no benefit promise)– avoids perverse redistributions, incentives for evasion and early

retirement (penalty for early retirement) – keeps system solvent even if workers retire early, evade

• Why fully funded? – avoids steep future payroll tax increases as population ages--

pensions financed by own savings, not current tax– can be used to mobilize long term domestic saving for

investment, increase productivity and output

• Why private management of funds? – To get higher return and better allocation of capital– improve financial markets – reduce risk by diversification (including international)

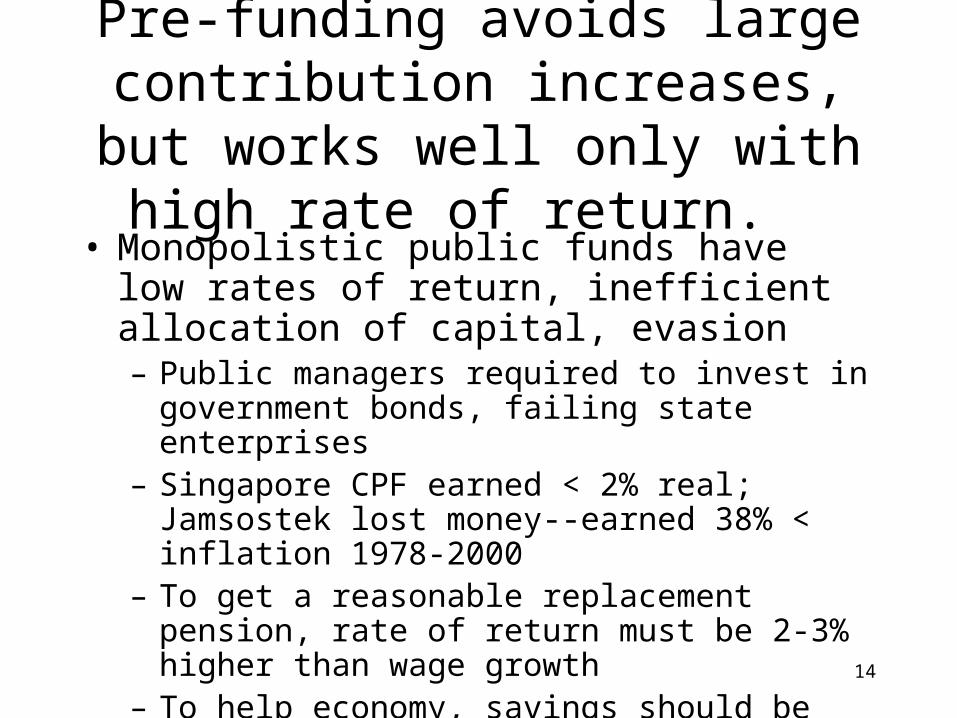

14

Pre-funding avoids large contribution increases, but works

well only with high rate of return. • Monopolistic public funds have low rates of

return, inefficient allocation of capital, evasion – Public managers required to invest in government

bonds, failing state enterprises– Singapore CPF earned < 2% real; Jamsostek lost

money--earned 38% < inflation 1978-2000– To get a reasonable replacement pension, rate of return

must be 2-3% higher than wage growth– To help economy, savings should be used productively

• So reforming countries are using private competitive markets, diversified portfolios (including international diversification)

15

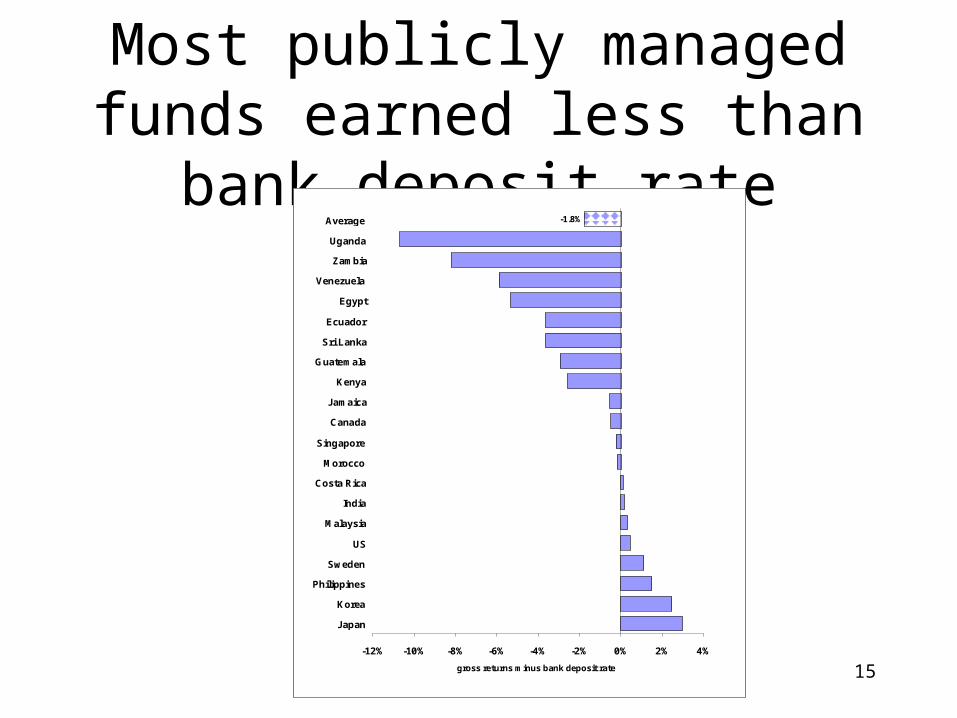

Most publicly managed funds earned less than bank deposit rate

-1.8%

-12% -10% -8% -6% -4% -2% 0% 2% 4%

Japan Korea

Philippines Sweden

US

Malaysia India

Costa Rica Morocco

Singapore

Canada Jamaica

Kenya Guatemala

Sri Lanka Ecuador

Egypt Venezuela

Zambia Uganda

Average

gross returns minus bank deposit rate

16

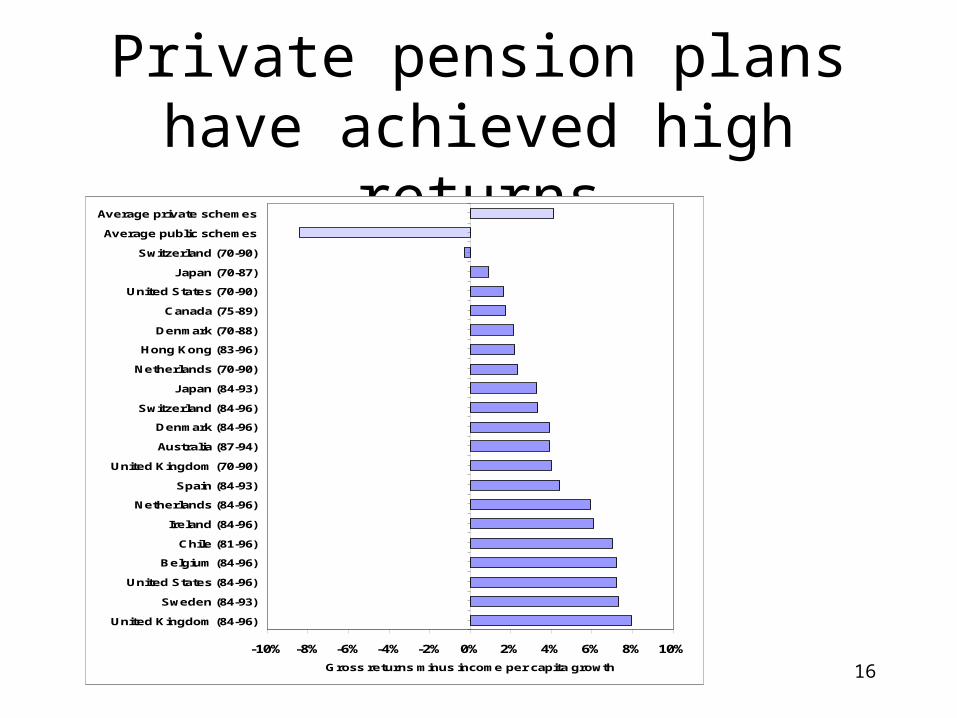

Private pension plans have achieved high returns

-10% -8% -6% -4% -2% 0% 2% 4% 6% 8% 10%

United Kingdom (84-96)

Sweden (84-93)

United States (84-96)

Belgium (84-96)

Chile (81-96)

Ireland (84-96)

Netherlands (84-96)

Spain (84-93)

United Kingdom (70-90)

Australia (87-94)

Denmark (84-96)

Switzerland (84-96)

Japan (84-93)

Netherlands (70-90)

Hong Kong (83-96)

Denmark (70-88)

Canada (75-89)

United States (70-90)

Japan (70-87)

Switzerland (70-90)

Average public schemes

Average private schemes

Gross returns minus income per capita growth

17

Importance of high rate of return: pension/final wage from 7% contribution

(also important to raise retirement age)(real wages assumed to grow 3% yearly)

Real rate of return

Retirement age r=2% r=5%

55 (contribute 35 years) 13% replacement rate 28% replacement rate

65 (contribute 45 years) 29% replacement rate 64% replacement rate

18

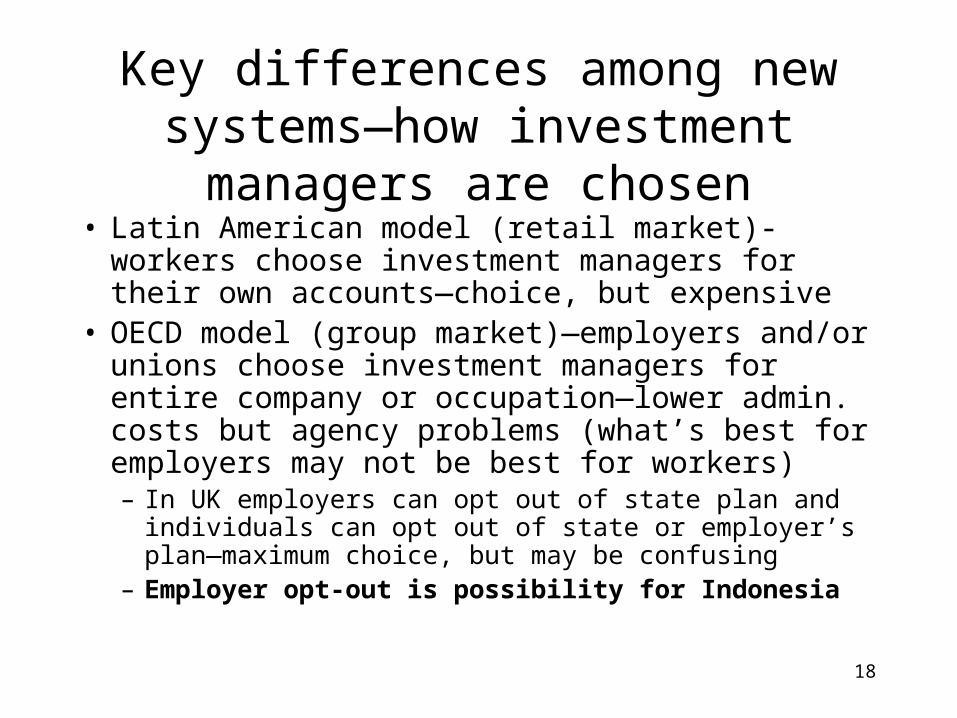

Key differences among new systems—how investment managers are chosen

• Latin American model (retail market)-workers choose investment managers for their own accounts—choice, but expensive

• OECD model (group market)—employers and/or unions choose investment managers for entire company or occupation—lower admin. costs but agency problems (what’s best for employers may not be best for workers) – In UK employers can opt out of state plan and individuals can

opt out of state or employer’s plan—maximum choice, but may be confusing

– Employer opt-out is possibility for Indonesia

19

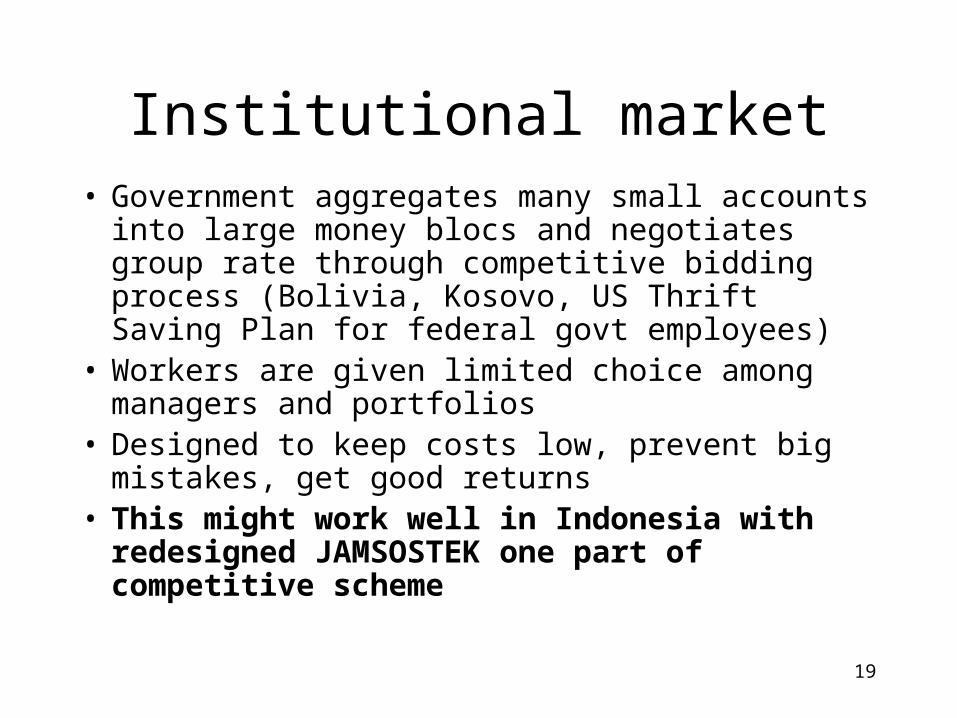

Institutional market• Government aggregates many small accounts into

large money blocs and negotiates group rate through competitive bidding process (Bolivia, Kosovo, US Thrift Saving Plan for federal govt employees)

• Workers are given limited choice among managers and portfolios

• Designed to keep costs low, prevent big mistakes, get good returns

• This might work well in Indonesia with redesigned JAMSOSTEK one part of competitive scheme

20

What are other countries in Asia-Pacific region doing?

• Singapore is allowing workers to opt out of CPF into personal accounts (retail)

• Australia and Hong Kong require employer to choose investment manager (group plan)

• India is requiring all new civil servants to enter DC plan; workers choose among small group of investment managers selected in competitive bidding process (institutional model); existing workers are grandfathered into old scheme. – This could be the basis for civil service pension reform

in Indonesia.

21

New experiments with centrally managed funds

• Canada, Ireland, New Zealand—keep DB but fund• Most portfolios managed externally with competitive

bidding, explicit selection and monitoring criteria, strict disclosure

• Board chosen on basis of professional competence, not as representatives

• Object is to maximize returns with moderate risk; no social or targeted investments (ltd govt bonds);

• Foreign investments and passive investments dominate (reduce risk and costs)

• This would not work here, because Indonesia would probably not adopt such strict restrictions.

22

What to do about poor workers and informal sector?

• Can’t collect contribution from informal sector, need non-contributory plan

• Almost all reforming countries include a safety net financed out of public treasury—could be minimum pension guarantee (MPG), means-tested benefit, flat benefit or compressed earnings-related benefit

23

The safety net

• Minimum pension guarantee (Latin America)– pension topped up if < 25% average wage – only for contributors (20-25 years)– Chile has social protection for non-contributors

• Means-and asset-tested benefits (Australia, Hong Kong, South Africa)—non-contributory– takes account of all income – may discourage work and saving – high transactions costs, mistargeting and bribery—leakage– hard to apply in extended family context– probably means-tested safety net is not a good plan for

Indonesia

24

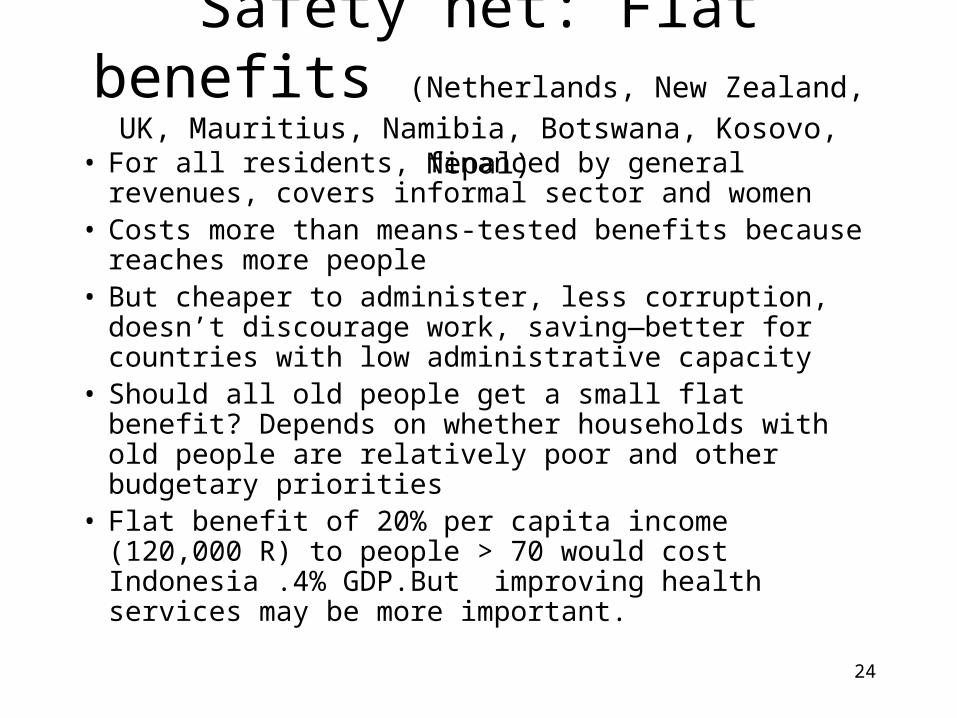

Safety net: Flat benefits (Netherlands, New

Zealand, UK, Mauritius, Namibia, Botswana, Kosovo, Nepal)

• For all residents, financed by general revenues, covers informal sector and women

• Costs more than means-tested benefits because reaches more people

• But cheaper to administer, less corruption, doesn’t discourage work, saving—better for countries with low administrative capacity

• Should all old people get a small flat benefit? Depends on whether households with old people are relatively poor and other budgetary priorities

• Flat benefit of 20% per capita income (120,000 R) to people > 70 would cost Indonesia .4% GDP.But improving health services may be more important.

25

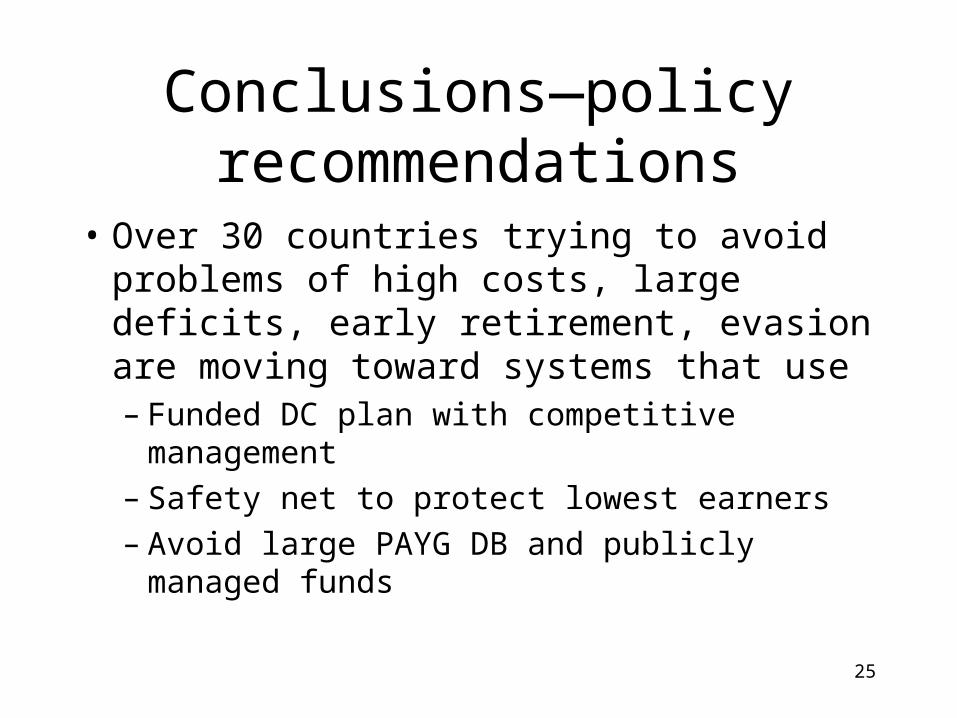

Conclusions—policy recommendations

• Over 30 countries trying to avoid problems of high costs, large deficits, early retirement, evasion are moving toward systems that use– Funded DC plan with competitive management– Safety net to protect lowest earners– Avoid large PAYG DB and publicly managed

funds

26

Key questions for Indonesia• Should new DB plan be introduced? (risky for

government, expensive for workers and employers. If DB is used it should be small, compressed, contain penalty for early retirement)

• What is best way to manage investment of funds? How to avoid past problems in Jamsostek and Taspen? (competitive management with limited choice and diversified portfolios?)

• What kind of safety net? If wish to cover informal sector must be financed by public treasury, not be contributory scheme. Small flat benefit for very old possible but depends on budgetary priorities and whether hh with old members are poor hh. (Health services may be more important).

27

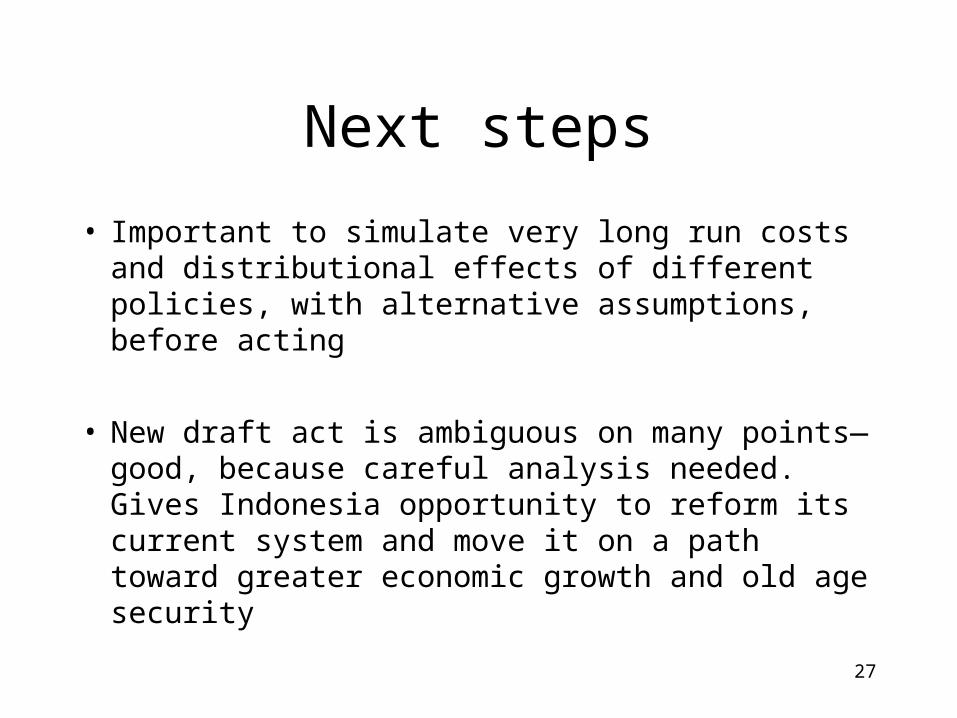

Next steps

• Important to simulate very long run costs and distributional effects of different policies, with alternative assumptions, before acting

• New draft act is ambiguous on many points—good, because careful analysis needed. Gives Indonesia opportunity to reform its current system and move it on a path toward greater economic growth and old age security