Embed Size (px)

Citation preview

1

Recommended shares and cash acquisition

of Alfred McAlpine plc

Recommended shares and cash acquisition

of Alfred McAlpine plc

MAKING TOMORROW A BETTER PLACE

James Cooke Hospital, Cleveland

10 December 200710 December 2007

2

AgendaPhilip RogersonChairman

MAKING TOMORROW A BETTER PLACE

Tower Place

3

The presentation which follows is directed only at persons who (i) are persons falling within the definition of “investment professionals” under Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (ii) any other persons to whom it may otherwise lawfully be communicated pursuant to the Order or otherwise (all such persons being “relevant persons”). Any person who is not a relevant person should not act or rely on this presentation or any of its comments.

• This document does not constitute a prospectus or a prospectus equivalent document.

• This presentation does not constitute an offer to sell or invitation to purchase any securities or the solicitation of any vote for approval in any jurisdiction.

• The information in this presentation including, without limitation, references to the anticipated effect of the acquisition by the Company of Alfred McAlpine plc on the Company’s future earnings per share should not be interpreted as a profit forecast nor should any information contained herein be interpreted to mean that the future earnings per share of Carillion plc following the acquisition of Alfred McAlpine plc will necessarily match or exceed the historical published earnings per share.

• This presentation includes “forward-looking statements”. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding the Company’s financial position, business strategy, plans and objectives of management for future operations (including development plans and objectives relating to the Company’s services) are forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of the Company or those markets and economies to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future and such assumptions may or may not prove to be correct. These forward-looking statements speak only as at the date of this presentation. The Company expressly disclaims any obligation (other than pursuant to the Listing Rules of the UKLA) or undertaking to disseminate any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company’s expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

• The release, publication or distribution of this presentation in certain jurisdictions may be restricted by law. Persons who are not resident in the United Kingdom or who are subject to other jurisdictions who receive this document should inform themselves of and observe any applicable requirements.

• The expected operational cost savings have been calculated on the basis of the existing cost and operating structures of the companies. These statements of estimated cost savings and one-off costs for achieving them relate to future actions and circumstances which, by their nature, involve risks, uncertainties and other factors. Because of this, the cost savings referred to may not be achieved, or those achieved could be materially different from those estimated. The statements should not be interpreted to mean that the earnings per share in 2008, or in any subsequent period, would necessarily match or be greater than those for the relevant preceding financial period.

Important legal notice

4

• Creation of leading support service business

• Carillion’s strategy and strong track record

• Carillion and Alfred McAlpine - strong strategic and financial rationale- clear integration plan

John McDonoughGroup Chief Executive

Richard AdamGroup Finance Director

John McDonoughGroup Chief Executive

• Financial overview- offer terms and structure- strong synergies and returns- robust capital structure- fair value and pensions- expected timetable

• Carillion 2007 trading update

• Summary

Agenda

5

Norwich Union Call Centre

Overview Overview John McDonoughGroup Chief ExecutiveJohn McDonoughGroup Chief Executive

MAKING TOMORROW A BETTER PLACE

6

Creation of leadingsupport services business

• Recommended cash and share acquisition valuing Alfred McAlpine at 558p(1) per share

• Carillion and Alfred McAlpine are an excellent strategic fit

• Creates a Group with - combined revenues of £5.3bn(2)

- leading position in UK support services with revenues of £2.6bn(2)

- enhanced positions in a wide range of growth market sectors- increased capability in providing integrated solutions- increased project management resources

(1) Based on Carillion’s share price at close of business on 7 December 2007 of 363.25 pence and Carillion share exchange ratio of 1.08(2) 2007 forecast revenues – Citigroup for Alfred McAlpine, Oriel Securities for Carillion

7

Creation of leadingsupport services business

• Opportunities for substantial synergy cost savings - £30m by end 2009

• Carillion’s strong cash and risk management processes and selectivity criteria will continue to be applied to the enlarged Group

• Potential to deliver significant value for Carillion and Alfred McAlpine shareholders

- financial returns ahead of Carillion’s WACC - materially enhanced earnings in 2009, the first full year after

acquisition

• Carillion trading update in 2007- continuing strong growth with underlying earnings per share up by

at least 20%

8

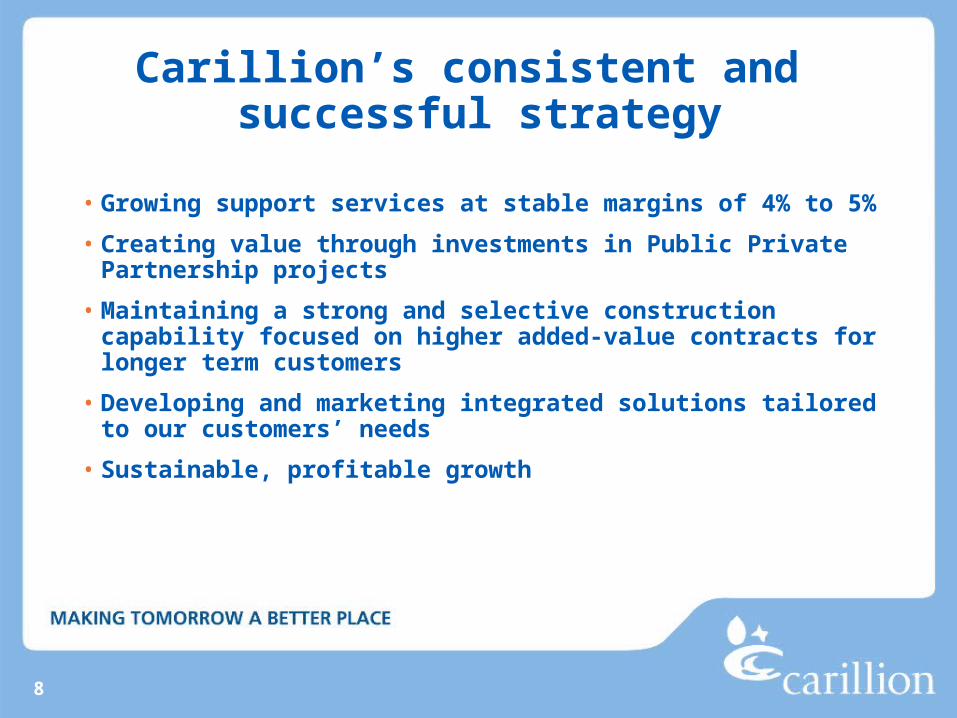

Carillion’s consistent and successful strategy

• Growing support services at stable margins of 4% to 5%

• Creating value through investments in Public Private Partnership projects

• Maintaining a strong and selective construction capability focused on higher added-value contracts for longer term customers

• Developing and marketing integrated solutions tailored to our customers’ needs

• Sustainable, profitable growth

9

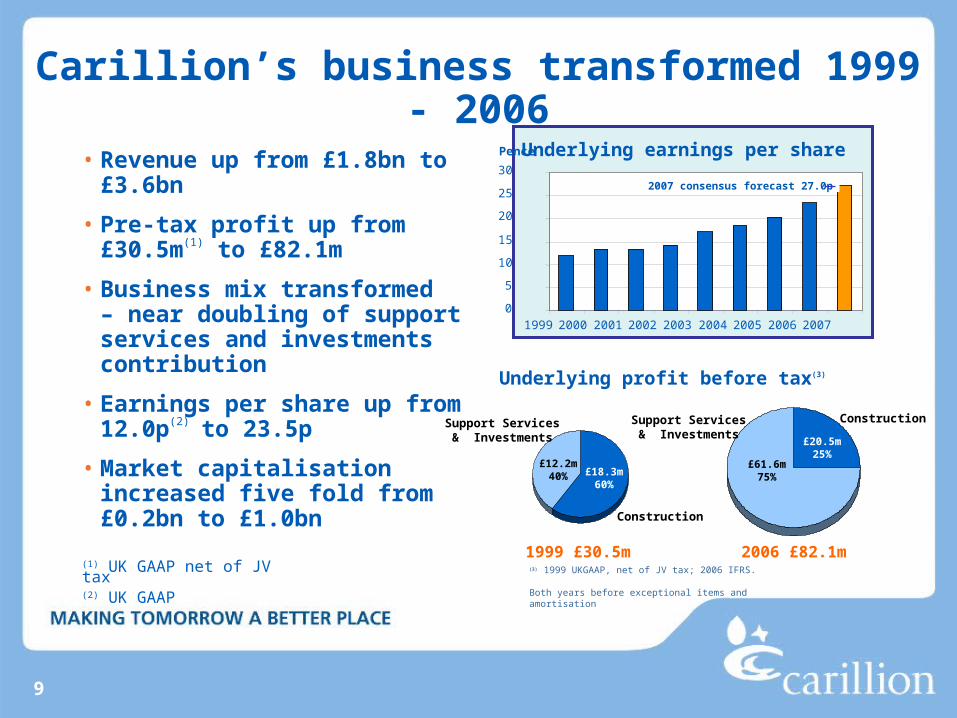

Carillion’s business transformed 1999 - 2006

• Revenue up from £1.8bn to £3.6bn

• Pre-tax profit up from £30.5m(1) to £82.1m

• Business mix transformed – near doubling of support services and investments contribution

• Earnings per share up from 12.0p(2)

to 23.5p

• Market capitalisation increased five fold from £0.2bn to £1.0bn

Underlying earnings per share

(1) UK GAAP net of JV tax(2) UK GAAP

£12.2m40% £18.3m

60%

1999 £30.5m(3) 1999 UKGAAP, net of JV tax; 2006 IFRS. Both years before exceptional items and amortisation

£61.6m75%

£20.5m25%

2006 £82.1m

Underlying profit before tax(3)

Support Services& Investments

Construction

ConstructionSupport Services& Investments

0

5

10

15

20

25

30

1999 2000 2001 2002 2003 2004 2005 2006 2007

Pence

2007 consensus forecast 27.0p

10

Strong acquisition track record

• Acquired Mowlem in February 2006 for £350m plus debt of £120m

• Step change in Carillion’s development, consistent with strategy for growth

• Doubled annual revenue to c£4bn

• Successfully integrated Mowlem ahead of schedule and implemented

- Carillion’s policies and risk management processes - Carillion’s strong focus on cash management

• Acquisition benefits exceeding expectations

• Carillion (excluding Mowlem) also delivered strong organic growth - c18% increase in profit(1) in 2006

(1) Before Group and JV tax, all exceptional items, amortisation and goodwill impairment

11

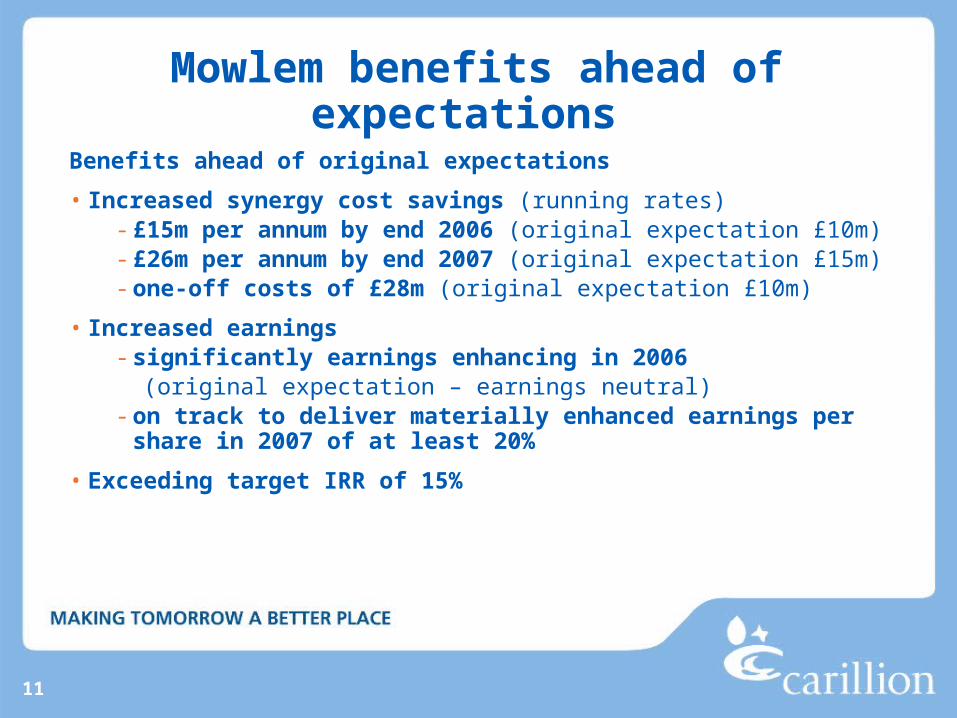

Mowlem benefits ahead of expectations

Benefits ahead of original expectations

• Increased synergy cost savings (running rates)- £15m per annum by end 2006 (original expectation £10m) - £26m per annum by end 2007 (original expectation £15m) - one-off costs of £28m (original expectation £10m)

• Increased earnings- significantly earnings enhancing in 2006 (original expectation – earnings neutral)- on track to deliver materially enhanced earnings per share in 2007

of at least 20%

• Exceeding target IRR of 15%

12

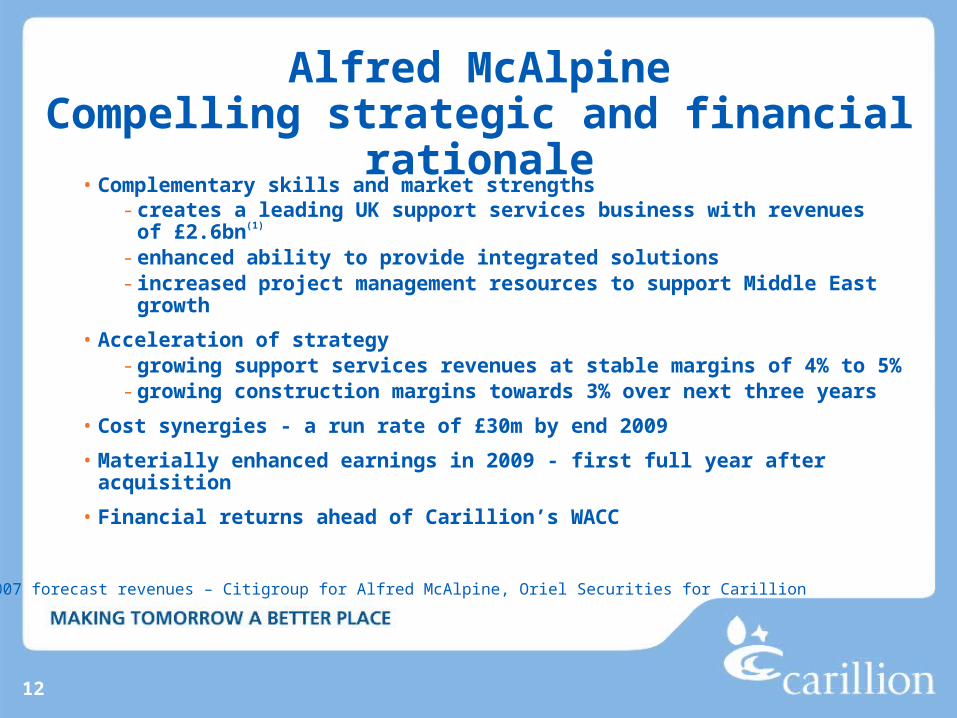

• Complementary skills and market strengths- creates a leading UK support services business with revenues

of £2.6bn(1)

- enhanced ability to provide integrated solutions- increased project management resources to support Middle East

growth

• Acceleration of strategy- growing support services revenues at stable margins of 4% to 5%- growing construction margins towards 3% over next three years

• Cost synergies - a run rate of £30m by end 2009

• Materially enhanced earnings in 2009 - first full year after acquisition

• Financial returns ahead of Carillion’s WACC

Alfred McAlpineCompelling strategic and financial rationale

(1) 2007 forecast revenues – Citigroup for Alfred McAlpine, Oriel Securities for Carillion

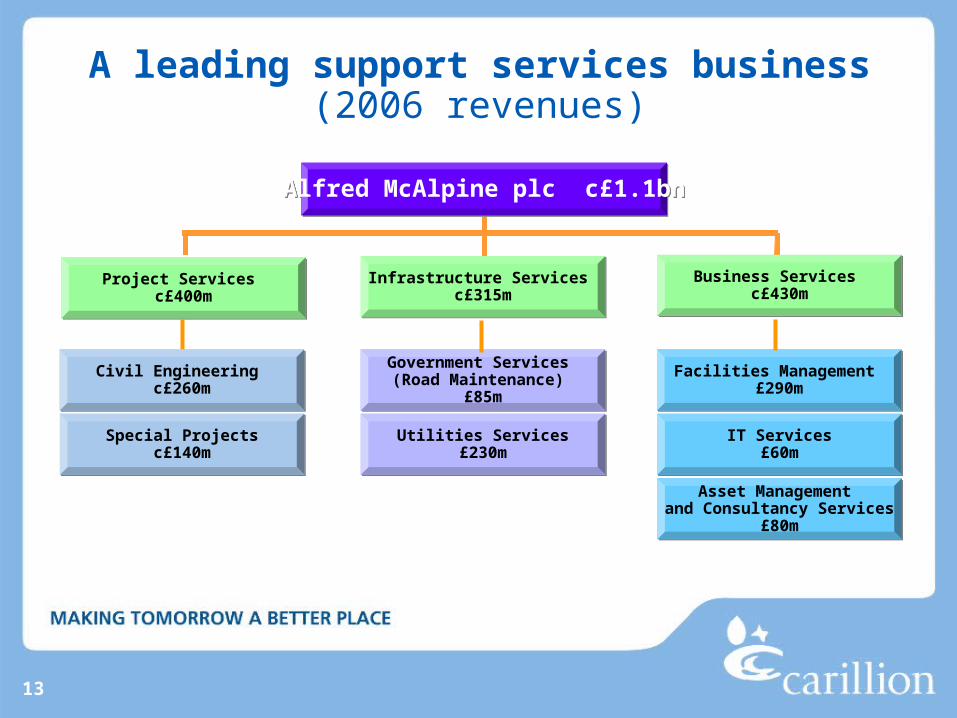

13

Project Services c£400m

Project Services c£400m

Alfred McAlpine plc c£1.1bnAlfred McAlpine plc c£1.1bn

Infrastructure Services c£315m

Infrastructure Services c£315m

Government Services (Road Maintenance)

£85m

Government Services (Road Maintenance)

£85m

Utilities Services£230m

Utilities Services£230m

Business Services c£430m

Business Services c£430m

Facilities Management £290m

Facilities Management £290m

IT Services£60m

IT Services£60m

Asset Management and Consultancy Services

£80m

Asset Management and Consultancy Services

£80m

A leading support services business(2006 revenues)

Civil Engineering c£260m

Civil Engineering c£260m

Special Projectsc£140m

Special Projectsc£140m

14

Carillion plc c£3.6bnCarillion plc c£3.6bn

A leading support services andconstruction business (2006 revenues)

Defence £232m

Defence £232m

Construction£268m

Construction£268m

Education£151m

Education£151m

Facilities Management& Services £6m

Facilities Management& Services £6m

Public Private Partnership Projectsand other Construction £117m

Public Private Partnership Projectsand other Construction £117m

Road maintenance and otherFacilities Management £46mRoad maintenance and otherFacilities Management £46m

Health £229mHealth £229m

Facilities Management& Services £697m

Facilities Management& Services £697m

Rail£368mRail

£368m

Roads£224mRoads£224m

Building£863m

Building£863m

Civil Engineering £241m

Civil Engineering £241m

PPP Equity returns£148m

PPP Equity returns£148m

UK£3,153m

UK£3,153m

Middle East£274m

Middle East£274m

Canada and Caribbean c£163m

Canada and Caribbean c£163m

15

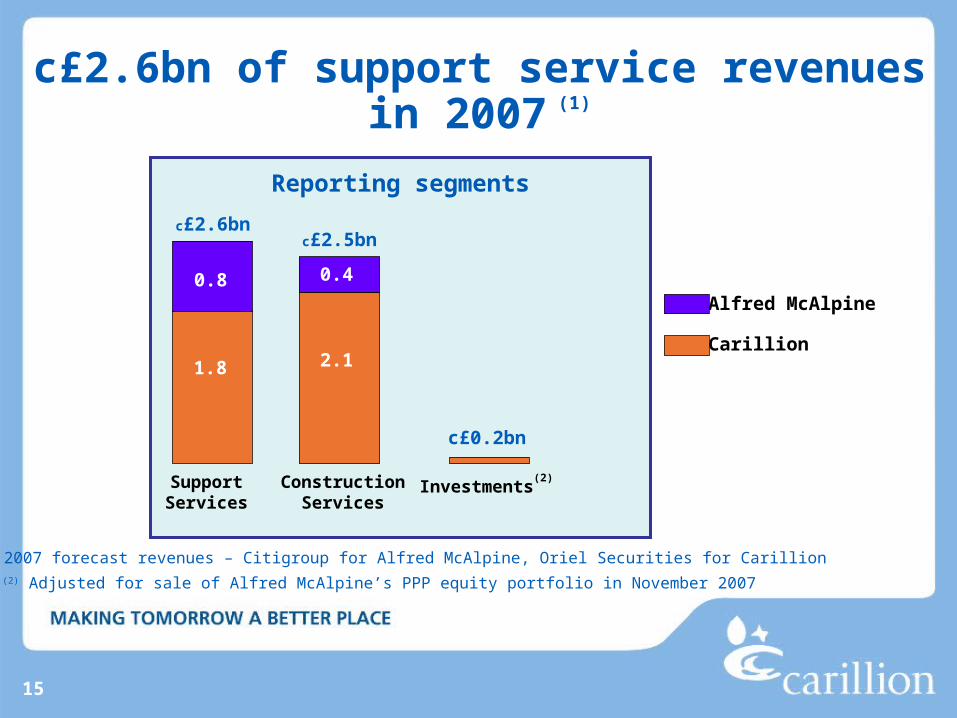

c£2.6bn of support service revenuesin 2007 (1)

(2) Adjusted for sale of Alfred McAlpine’s PPP equity portfolio in November 2007

SupportServices

ConstructionServices

c£2.6bnc£2.5bn

c£0.2bn

Investments(2)

Reporting segments

0.8

2.11.8

0.4

Alfred McAlpine

Carillion

(1) 2007 forecast revenues – Citigroup for Alfred McAlpine, Oriel Securities for Carillion

16

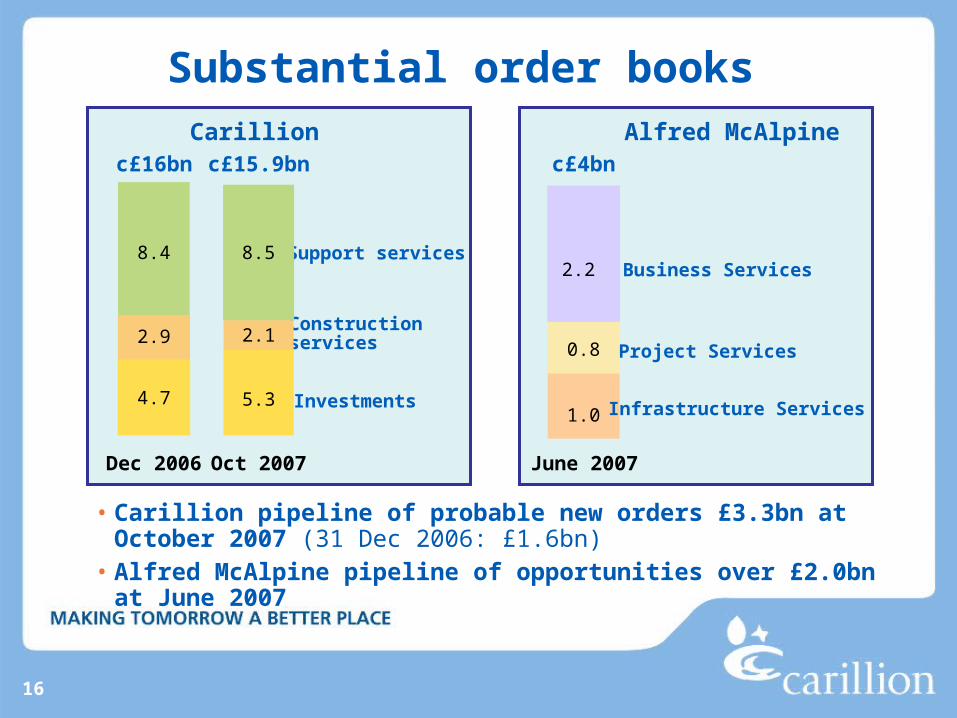

Substantial order books

• Carillion pipeline of probable new orders £3.3bn at October 2007 (31 Dec 2006: £1.6bn)

• Alfred McAlpine pipeline of opportunities over £2.0bn at June 2007

Construction services

Support services

Investments

Dec 2006 Oct 2007

4.7

8.4

2.9

c£16bn c£15.9bn

5.3

8.5

2.1

June 2007

Business Services

Project Services

Infrastructure Services1.0

2.2

c£4bn

0.8

Carillion Alfred McAlpine

17

Leading support services business

• Creates one of the UK’s leading support services businesses with c£2.6bn(1) of revenues

• Enhanced skills and capabilities in existing and new growth market sectors

• Strengthens integrated service offering

• Entry into higher margin IT services sector

• Cross-selling opportunities- Enviros/Consultancy- IT Services- M&E

(1) 2007 forecast revenues – Citigroup for Alfred McAlpine, Oriel Securities for Carillion

18

Enhanced construction resource

• Complementary positions in UK building and infrastructure

• Combined strengths in key sectors - education, defence, industrial, offices, mixed use

developments, leisure and transport infrastructure- strong relationships with Local Authorities

• Increased project management resources to support strong growth opportunities in Middle East

• Significant margin opportunities from integration through applying- selectivity and risk management- strong focus on cash management

19

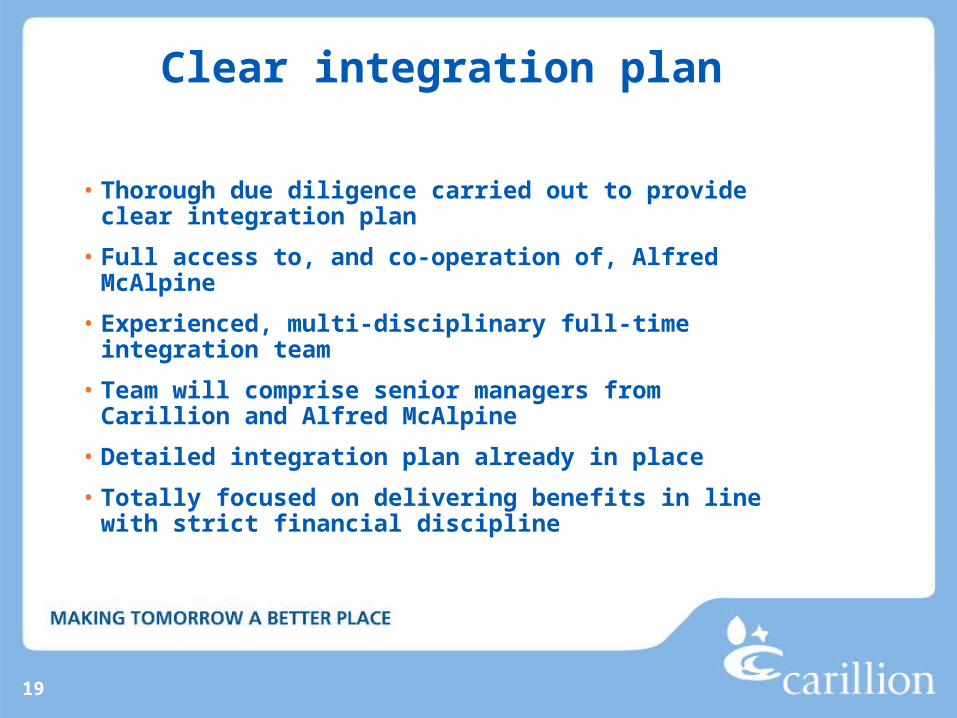

Clear integration plan

• Thorough due diligence carried out to provide clear integration plan

• Full access to, and co-operation of, Alfred McAlpine

• Experienced, multi-disciplinary full-time integration team

• Team will comprise senior managers from Carillion and Alfred McAlpine

• Detailed integration plan already in place

• Totally focused on delivering benefits in line with strict financial discipline

20

Richard AdamGroup Finance DirectorRichard AdamGroup Finance Director

Financial overview

MAKING TOMORROW A BETTER PLACE

Alfred McAlpine Government Services

21

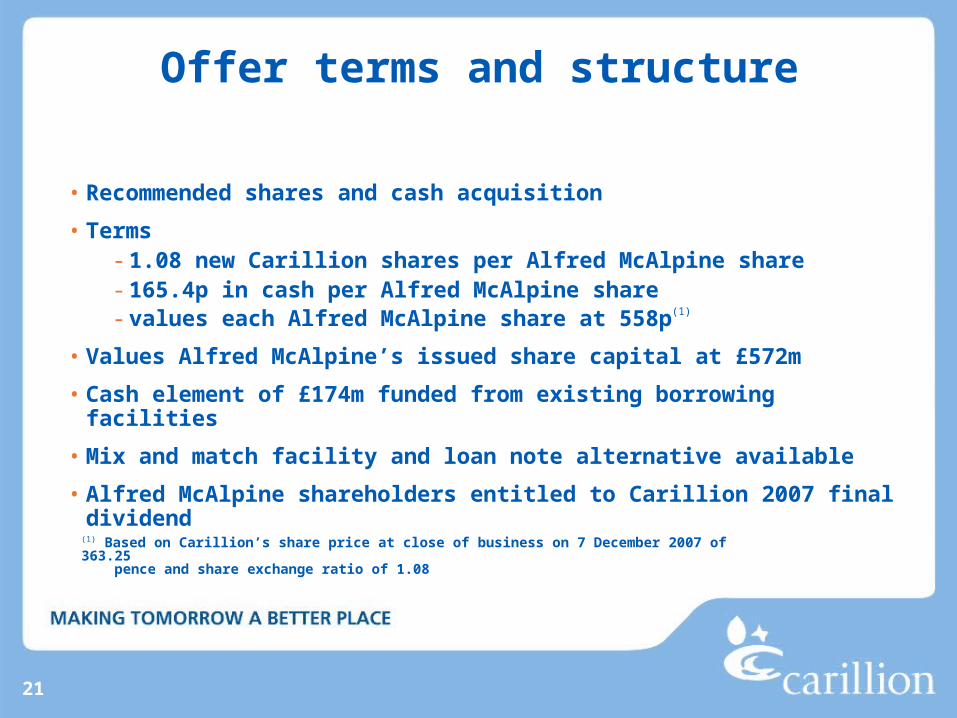

Offer terms and structure

• Recommended shares and cash acquisition

• Terms- 1.08 new Carillion shares per Alfred McAlpine share- 165.4p in cash per Alfred McAlpine share- values each Alfred McAlpine share at 558p(1)

• Values Alfred McAlpine’s issued share capital at £572m

• Cash element of £174m funded from existing borrowing facilities

• Mix and match facility and loan note alternative available

• Alfred McAlpine shareholders entitled to Carillion 2007 final dividend

(1) Based on Carillion’s share price at close of business on 7 December 2007 of 363.25 pence and share exchange ratio of 1.08

22

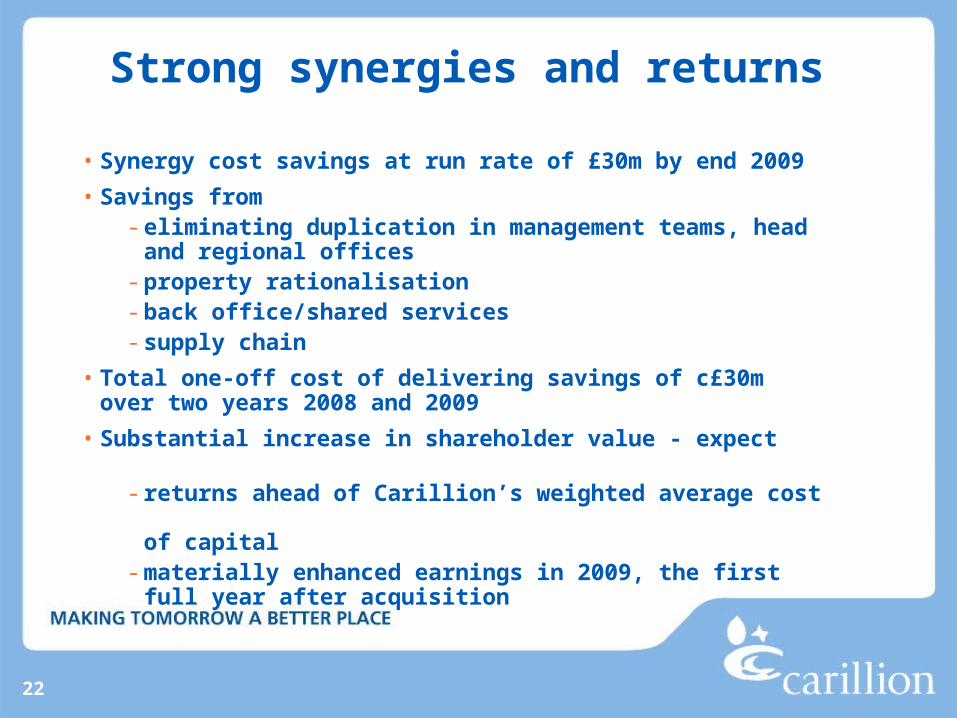

Strong synergies and returns

• Synergy cost savings at run rate of £30m by end 2009

• Savings from - eliminating duplication in management teams, head and

regional offices- property rationalisation- back office/shared services- supply chain

• Total one-off cost of delivering savings of c£30m over two years 2008 and 2009

• Substantial increase in shareholder value - expect - returns ahead of Carillion’s weighted average cost

of capital- materially enhanced earnings in 2009, the first full year

after acquisition

23

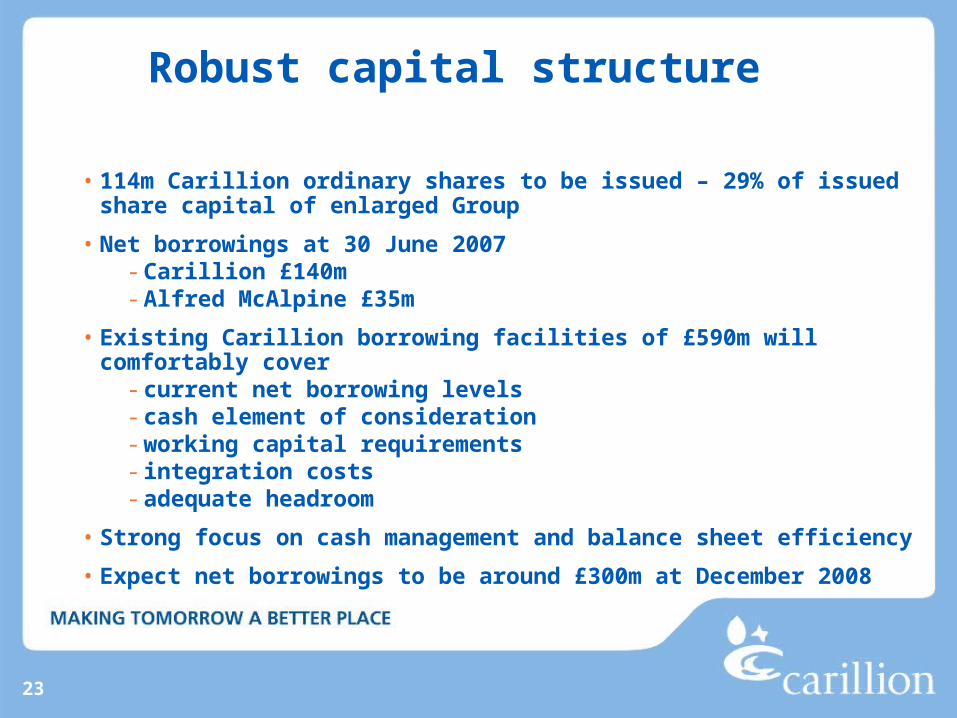

Robust capital structure

• 114m Carillion ordinary shares to be issued – 29% of issued share capital of enlarged Group

• Net borrowings at 30 June 2007- Carillion £140m - Alfred McAlpine £35m

• Existing Carillion borrowing facilities of £590m will comfortably cover- current net borrowing levels - cash element of consideration- working capital requirements- integration costs- adequate headroom

• Strong focus on cash management and balance sheet efficiency

• Expect net borrowings to be around £300m at December 2008

24

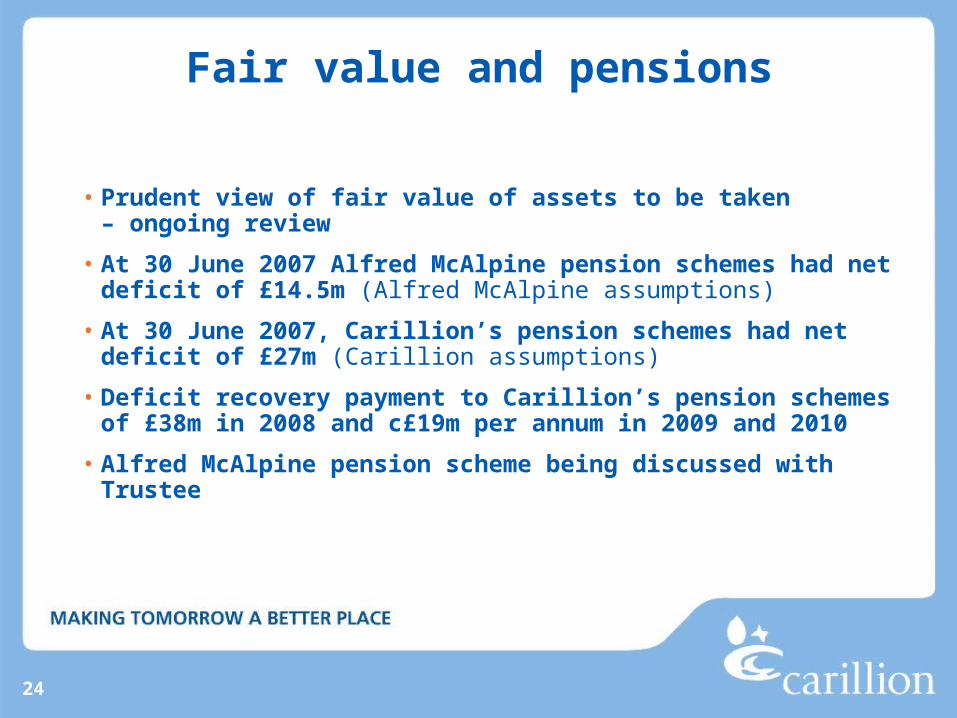

Fair value and pensions

• Prudent view of fair value of assets to be taken – ongoing review

• At 30 June 2007 Alfred McAlpine pension schemes had net deficit of £14.5m (Alfred McAlpine assumptions)

• At 30 June 2007, Carillion’s pension schemes had net deficit of £27m (Carillion assumptions)

• Deficit recovery payment to Carillion’s pension schemes of £38m in 2008 and c£19m per annum in 2009 and 2010

• Alfred McAlpine pension scheme being discussed with Trustee

25

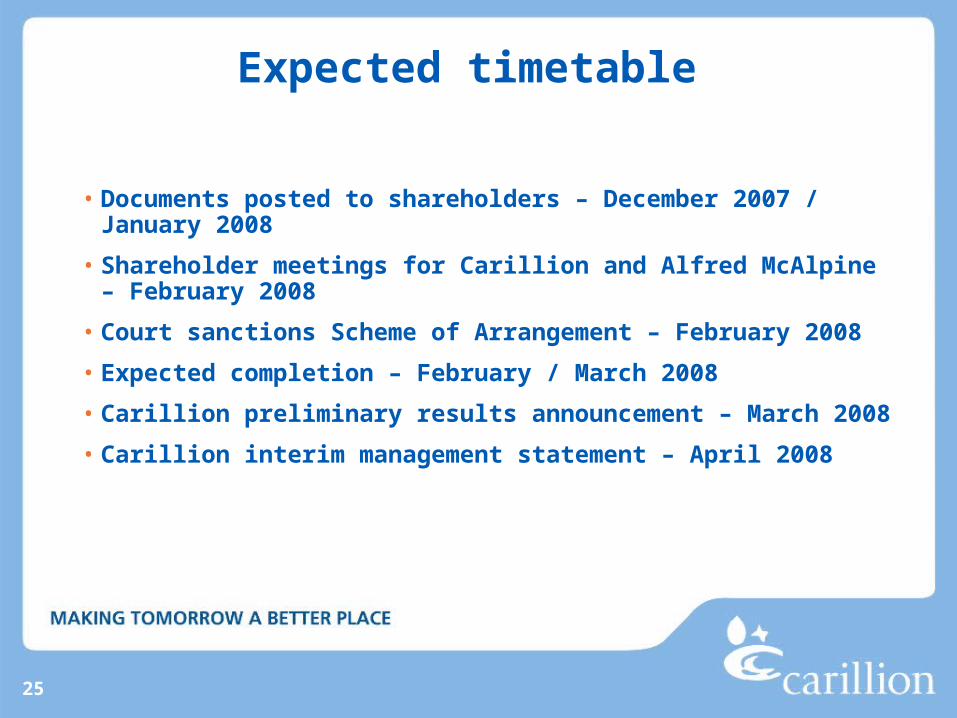

Expected timetable

• Documents posted to shareholders – December 2007 / January 2008

• Shareholder meetings for Carillion and Alfred McAlpine – February 2008

• Court sanctions Scheme of Arrangement – February 2008

• Expected completion – February / March 2008

• Carillion preliminary results announcement – March 2008

• Carillion interim management statement – April 2008

26

Carillion 2007 trading update Carillion 2007 trading update

News International, Broxbourne

27

20% growth in underlying earnings per share

• Expect to deliver underlying earnings per share growth of at least 20% in 2007

• Effective tax rate expected to reduce to 25%

• Mowlem synergy cost savings at run rate of £26m per annum by end 2007

• Average net borrowings in 2007 on target to be below £150m

• Net debt at 31 December now expected to be below £80m

• Order book at 31 December expected to be £15.7bn and pipeline of probable new orders of £3.3bn

• Positive trading conditions in the Group’s UK and international markets

• Middle East revenues now expected to more than double to over £600m within 3 years instead of 5

• Board expects outlook to remain positive and Carillion to continue its strong momentum in 2008 and over the medium term

28

Summary John McDonoughGroup Chief Executive

MAKING TOMORROW A BETTER PLACE

Alfred McAlpine Business Services

29

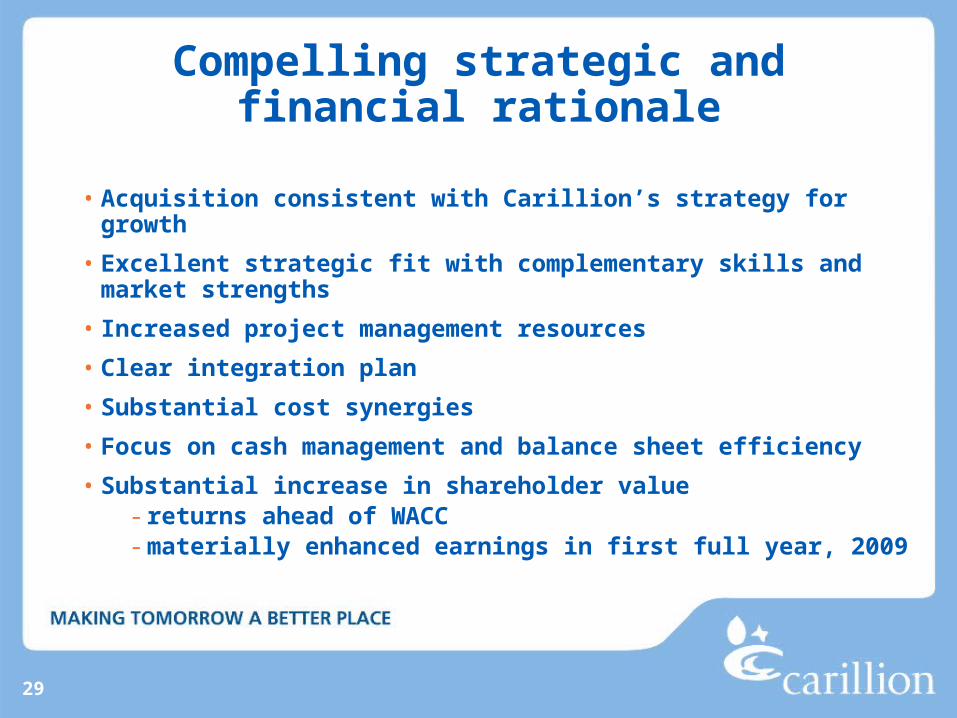

Compelling strategic andfinancial rationale

• Acquisition consistent with Carillion’s strategy for growth

• Excellent strategic fit with complementary skills and market strengths

• Increased project management resources

• Clear integration plan

• Substantial cost synergies

• Focus on cash management and balance sheet efficiency

• Substantial increase in shareholder value- returns ahead of WACC- materially enhanced earnings in first full year, 2009

30

Appendices

Alfred McAlpine Business Services

MAKING TOMORROW A BETTER PLACE

31

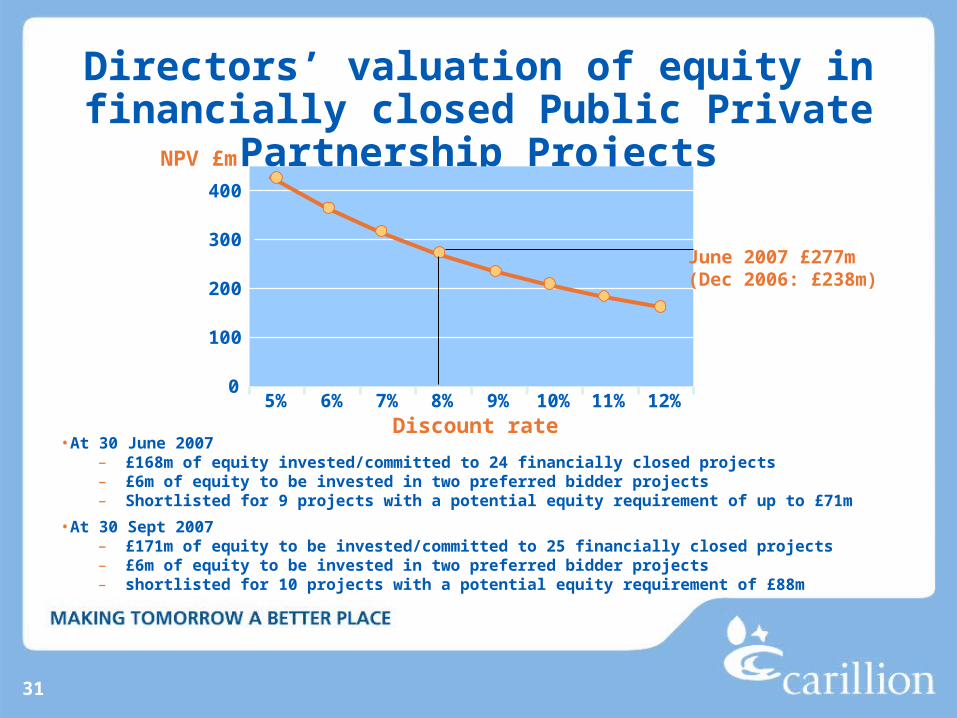

Directors’ valuation of equity in financially closed Public Private Partnership Projects

• At 30 June 2007– £168m of equity invested/committed to 24 financially closed projects – £6m of equity to be invested in two preferred bidder projects– Shortlisted for 9 projects with a potential equity requirement of up to £71m

• At 30 Sept 2007– £171m of equity to be invested/committed to 25 financially closed projects– £6m of equity to be invested in two preferred bidder projects – shortlisted for 10 projects with a potential equity requirement of £88m

0

100

200

300

400

5% 6% 7% 8% 9% 10% 11% 12%Discount rate

NPV £m

June 2007 £277m(Dec 2006: £238m)

32

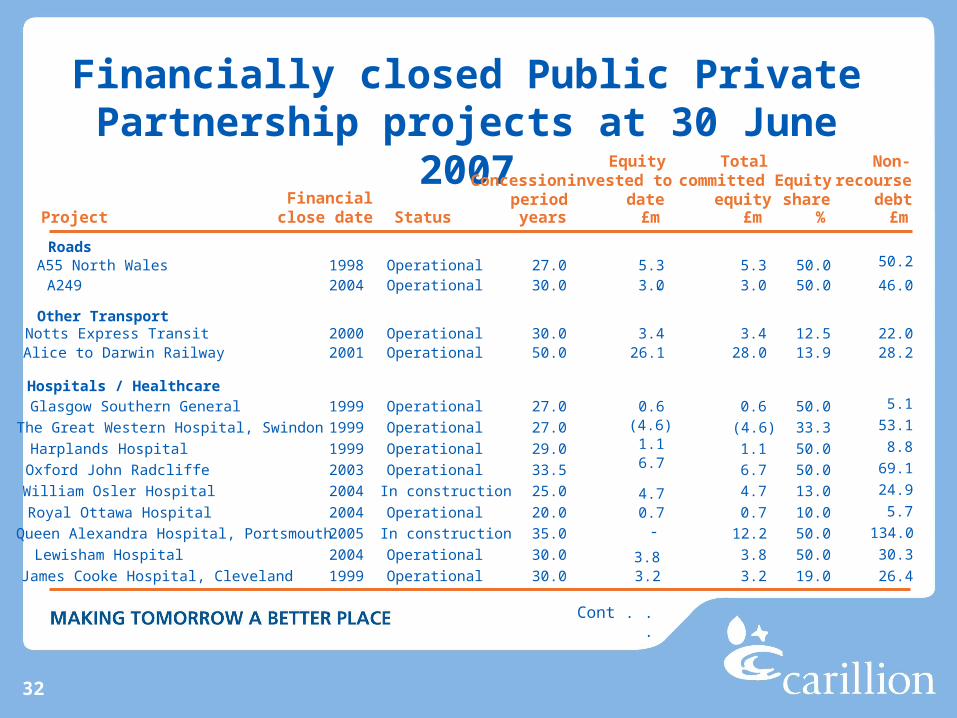

Financially closed Public Private Partnership projects at 30 June 2007

1998 Operational 27.0 5.3 5.3 50.0 50.2

2004 Operational 30.0 -3.0 3.0 50.0 46.0

2000 Operational 30.0 3.4 3.4 12.5 22.0

1999 Operational 27.0 0.6 0.6 50.0 5.1

1999 Operational 27.0 (4.6) (4.6) 33.3 53.1

1999 Operational 29.0 1.1 1.1 50.0 8.8

2003 Operational 33.5 6.7 6.7 50.0 69.1

4.7 24.92004 In construction 25.0 4.7 13.0

2004 Operational 20.0 0.7 0.7 10.0 5.7

2005 In construction 35.0 -

3.2

50.0

26.4

2001 Operational 50.0 26.1 28.0 13.9 28.2

2004 Operational 30.0 50.0

1999 Operational 30.0 19.03.2 3.8

RoadsA55 North WalesA249

Other TransportNotts Express Transit

Hospitals / HealthcareGlasgow Southern General

The Great Western Hospital, Swindon

Harplands Hospital

Oxford John Radcliffe

William Osler Hospital

Royal Ottawa Hospital

Queen Alexandra Hospital, Portsmouth

Alice to Darwin Railway

Lewisham Hospital

James Cooke Hospital, Cleveland

3.8

12.2

30.3

134.0

Cont . . .

ProjectFinancial

close date Status

Concessionperiod

Equityinvested to

date

Total committed

equityEquityshare

Non-recourse

debtyears £m £m % £m

33

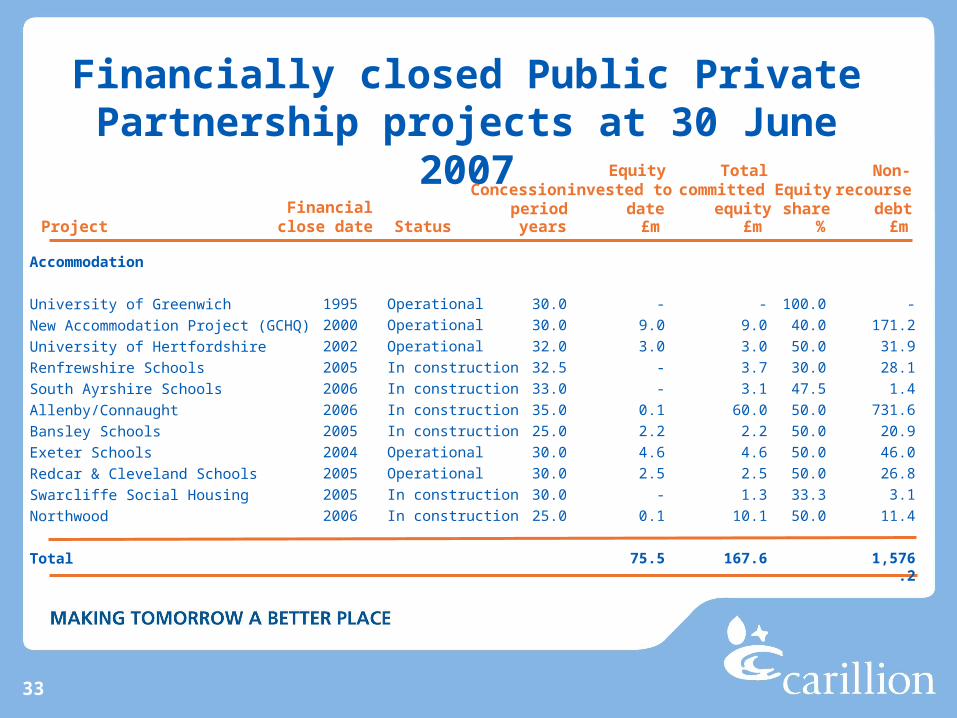

100.0

40.0

50.0

30.0

47.5

50.0

50.0

50.0

50.0

33.3

50.0

-

171.2

31.9

28.1

1.4

731.6

20.9

46.0

26.8

3.1

11.4

1,576.2

-

9.0

3.0

3.7

3.1

60.0

2.2

4.6

2.5

1.3

10.1

167.6

Financially closed Public Private Partnership projects at 30 June 2007

-

9.0

3.0

-

-

0.1

2.2

4.6

2.5

-

0.1

75.5

30.0

30.0

32.0

32.5

33.0

35.0

25.0

30.0

30.0

30.0

25.0

Operational

Operational

Operational

In construction

In construction

In construction

In construction

Operational

Operational

In construction

In construction

1995

2000

2002

2005

2006

2006

2005

2004

2005

2005

2006

Accommodation

University of Greenwich

New Accommodation Project (GCHQ)

University of Hertfordshire

Renfrewshire Schools

South Ayrshire Schools

Allenby/Connaught

Bansley Schools

Exeter Schools

Redcar & Cleveland Schools

Swarcliffe Social Housing

Northwood

Total

ProjectFinancial

close date Status

Concessionperiod

Equityinvested to

date

Total committed

equityEquityshare

Non-recourse

debtyears £m £m % £m

34

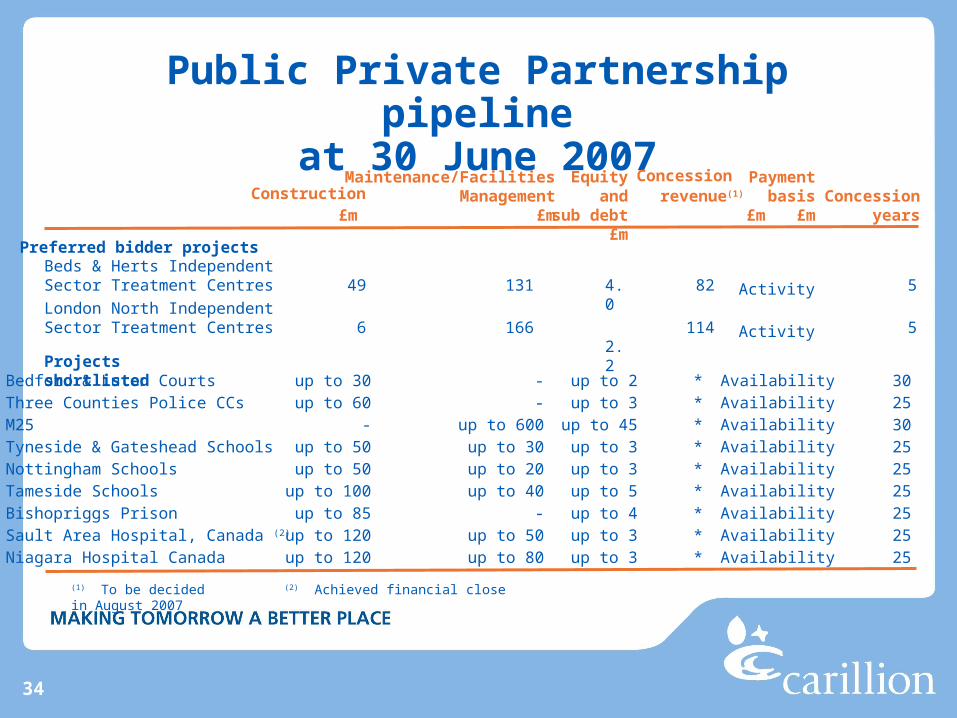

Public Private Partnership pipelineat 30 June 2007

Construction £m

Maintenance/FacilitiesManagement

£m

Equity andsub debt

£m

Concession revenue(1)

£m

Paymentbasis

£mConcession

years

Preferred bidder projectsBeds & Herts Independent Sector Treatment Centres

London North Independent Sector Treatment Centres

49

6

131

166

4.0

2.2

82

114

Activity

Activity

5

5

Projects shortlistedBedford & Luton CourtsThree Counties Police CCsM25Tyneside & Gateshead SchoolsNottingham Schools Tameside Schools Bishopriggs PrisonSault Area Hospital, Canada (2) Niagara Hospital Canada

up to 30up to 60

-up to 50up to 50

up to 100up to 85

up to 120up to 120

--

up to 600up to 30up to 20up to 40

-up to 50up to 80

up to 2up to 3

up to 45up to 3up to 3up to 5up to 4up to 3up to 3

*********

302530252525252525

AvailabilityAvailabilityAvailabilityAvailabilityAvailabilityAvailabilityAvailabilityAvailabilityAvailability

(1) To be decided (2) Achieved financial close in August 2007

35

THIS DOCUMENT IS NOT A PROSPECTUS. IT DOES NOT CONSTITUTE OR FORM PART OF ANY OFFER OF SECURITIES, OR CONSTITUTE SOLICITATION OF ANY OFFER OF SECURITIES. ANY ACCEPTANCE OR RESPONSE TO THE ACQUISITION SHOULD BE MADE ONLY ON THE BASIS OF THE INFORMATION REFERRED TO IN THE SCHEME DOCUMENT AND THE PROSPECTUS.

• Copies of the prospectus, the Carillion shareholder circular and the scheme document will, from the date of posting to Alfred McAlpine shareholders or Carillion shareholders (as appropriate), be available for inspection at the Document Viewing Facility which is situated at The Financial Services Authority, 25 The North Colonnade, Canary Wharf, London E14 5HS.

• Copies of the Carillion shareholder circular, the scheme document and the prospectus will, from the date of posting to Alfred McAlpine shareholders or Carillion shareholders (as appropriate), be available for inspection by Carillion shareholders at the offices of Carillion plc, Birch Street, Wolverhampton, WV1 4HY during normal business hours on any weekday (Saturdays, Sundays and public holidays excepted) and at the offices of Slaughter and May, One Bunhill Row, London, EC1Y 8YY during normal business hours on any weekday (Saturdays, Sundays and public holidays excepted).

• Copies of the scheme document and the prospectus will, from the date of posting to Alfred McAlpine shareholders or Comet shareholders (as appropriate), be available for inspection by Alfred McAlpine shareholders at the offices of Alfred McAlpine plc, Kinnaird House, 1 Pall Mall East, London, SW1Y 5AZ during normal business hours on any weekday (Saturdays, Sundays and public holidays excepted) and at the offices of CMS Cameron McKenna LLP, Mitre House, 160 Aldersgate Street, London, EC1A 4DD during normal business hours on any weekday (Saturdays, Sundays and public holidays excepted).

Important legal notice

36

MAKING TOMORROW A BETTER PLACE

James Cooke Hospital, Cleveland

Recommended shares and cash acquisition

of Alfred McAlpine plc

Recommended shares and cash acquisition

of Alfred McAlpine plc