Embed Size (px)

Citation preview

1

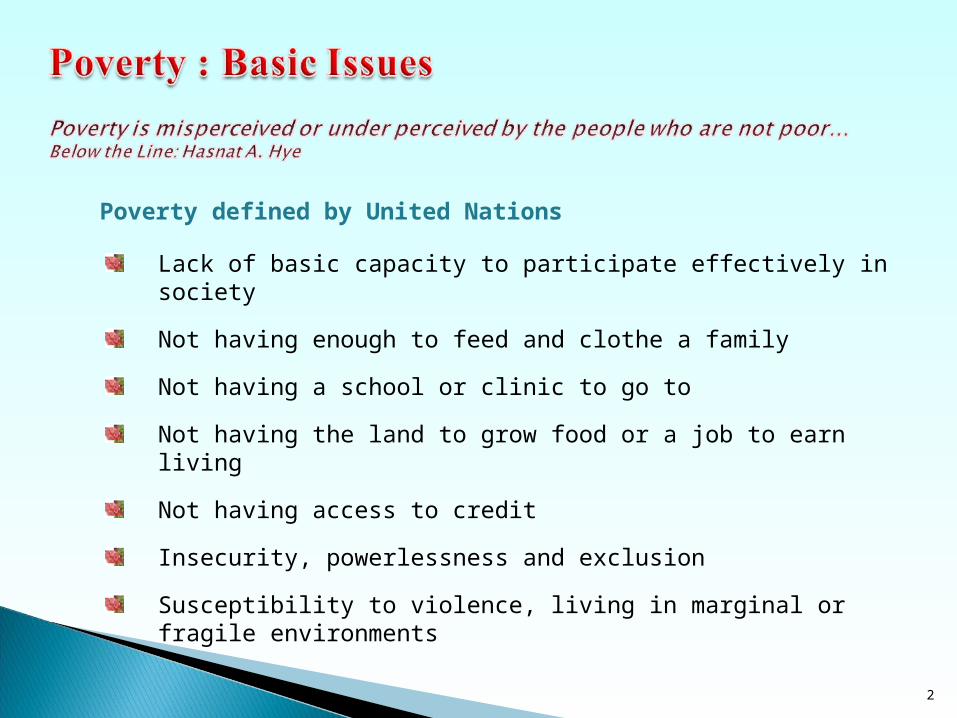

Poverty defined by United Nations

Lack of basic capacity to participate effectively in society

Not having enough to feed and clothe a family

Not having a school or clinic to go to

Not having the land to grow food or a job to earn living

Not having access to credit

Insecurity, powerlessness and exclusion

Susceptibility to violence, living in marginal or fragile environments

2

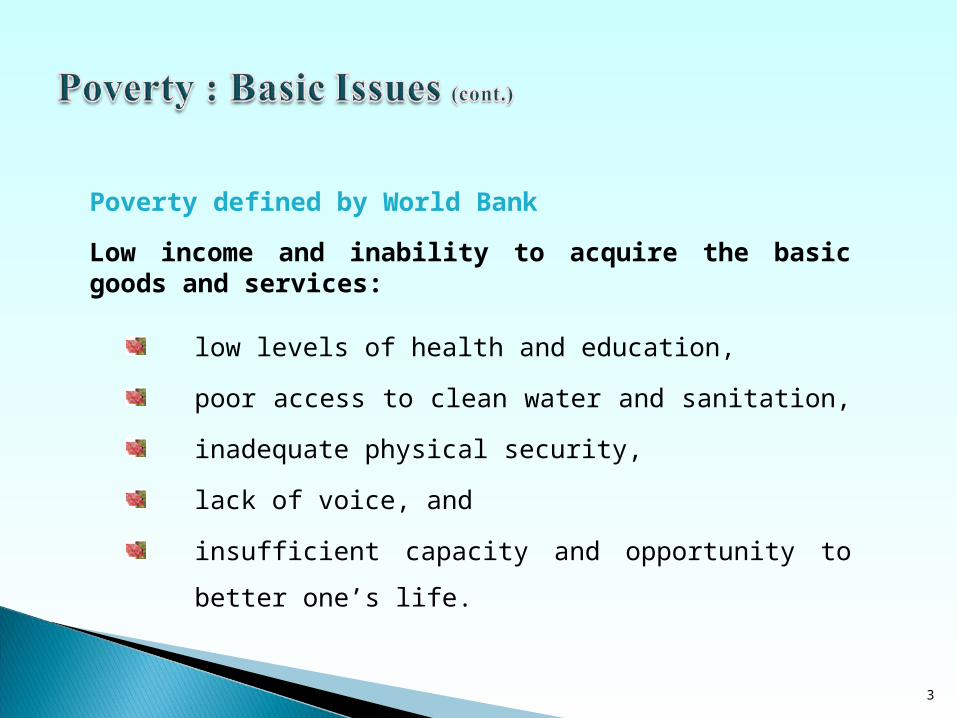

Poverty defined by World Bank

Low income and inability to acquire the basic goods and services:

low levels of health and education,

poor access to clean water and sanitation,

inadequate physical security,

lack of voice, and

insufficient capacity and opportunity to better one’s life.

3

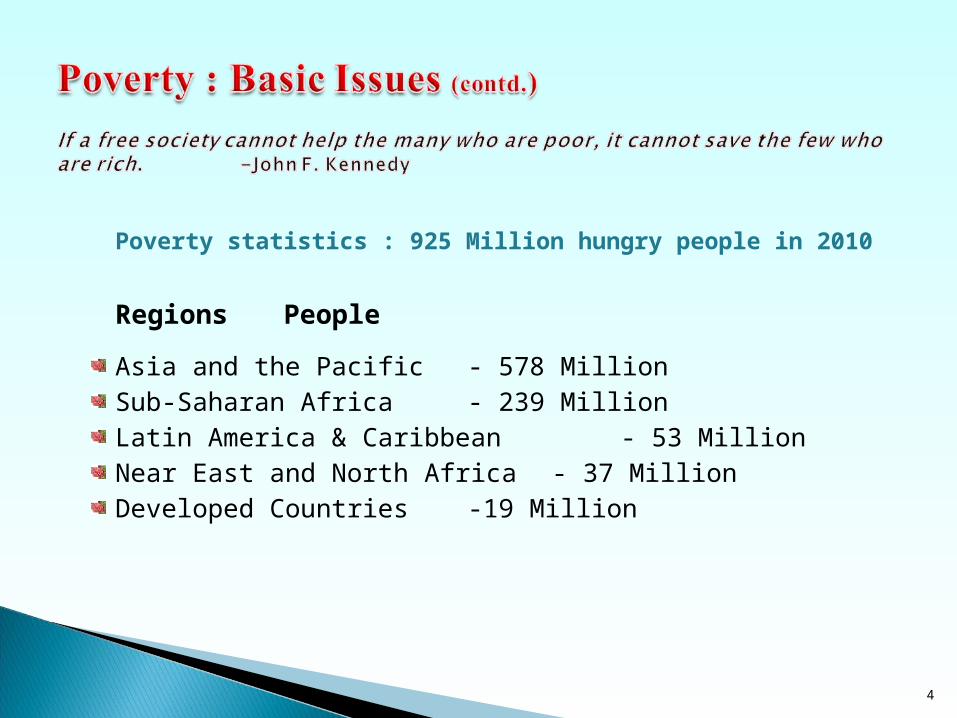

Poverty statistics : 925 Million hungry people in 2010

Regions People

Asia and the Pacific - 578 MillionSub-Saharan Africa - 239 MillionLatin America & Caribbean - 53 MillionNear East and North Africa - 37 MillionDeveloped Countries -19 Million

4

Banks

5

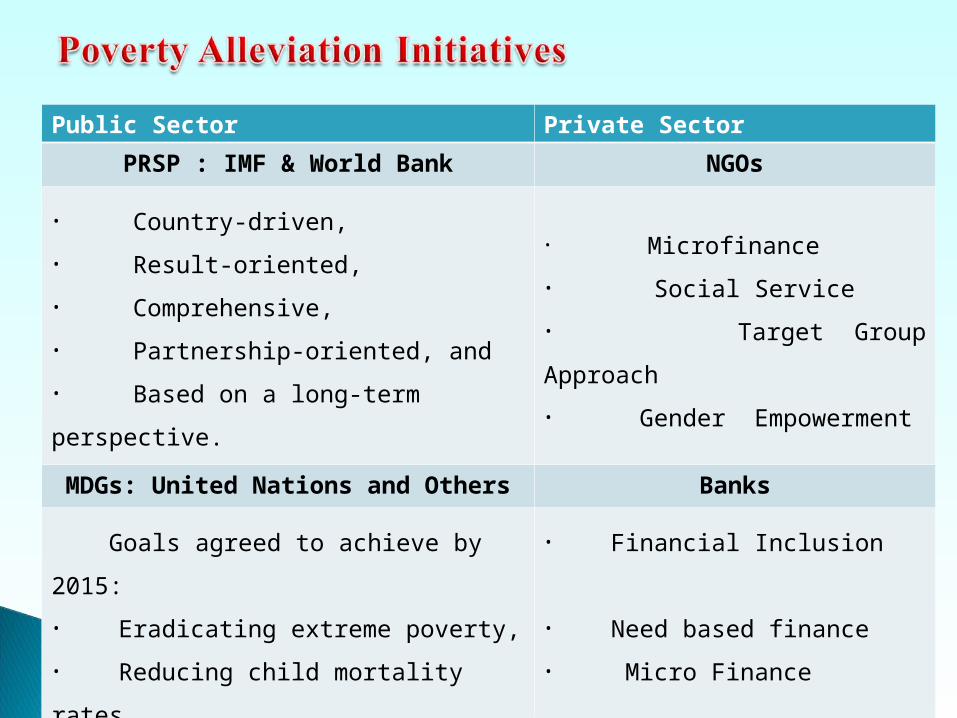

Public Sector Private Sector

PRSP : IMF & World Bank NGOs

• Country-driven,

• Result-oriented,

• Comprehensive,

• Partnership-oriented, and

• Based on a long-term perspective.

• Microfinance

• Social Service

• Target Group Approach

• Gender Empowerment

MDGs: United Nations and Others Banks

Goals agreed to achieve by 2015:

• Eradicating extreme poverty,

• Reducing child mortality rates,

• Fighting disease epidemics

• Partnership for development

• Financial Inclusion

• Need based finance

• Micro Finance

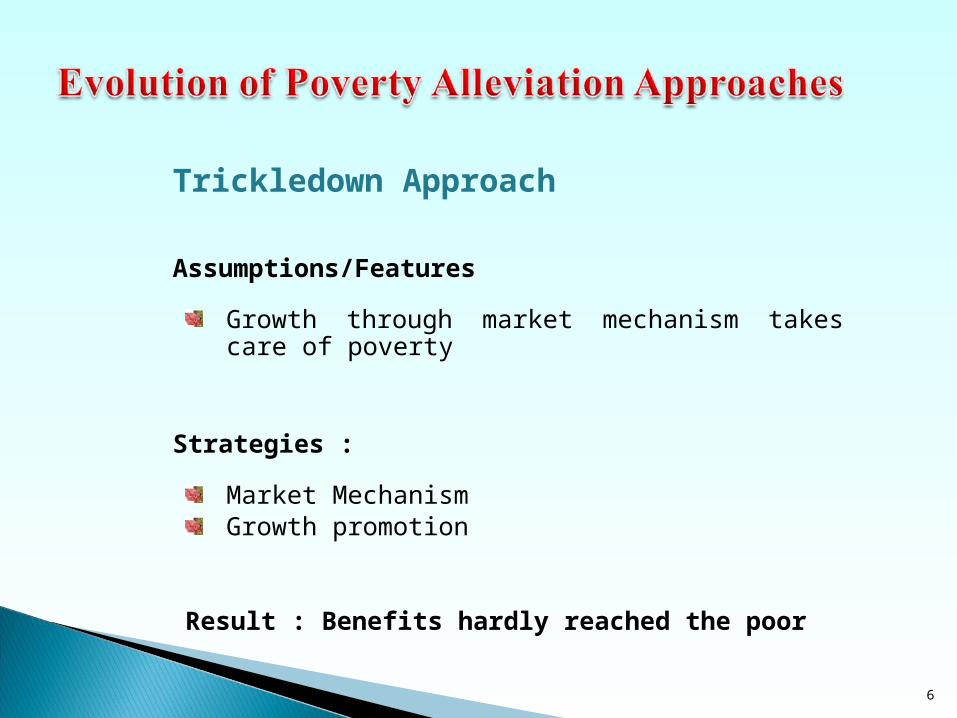

Trickledown Approach

Assumptions/Features

Growth through market mechanism takes care of poverty

Strategies :

Market MechanismGrowth promotion

Result : Benefits hardly reached the poor

6

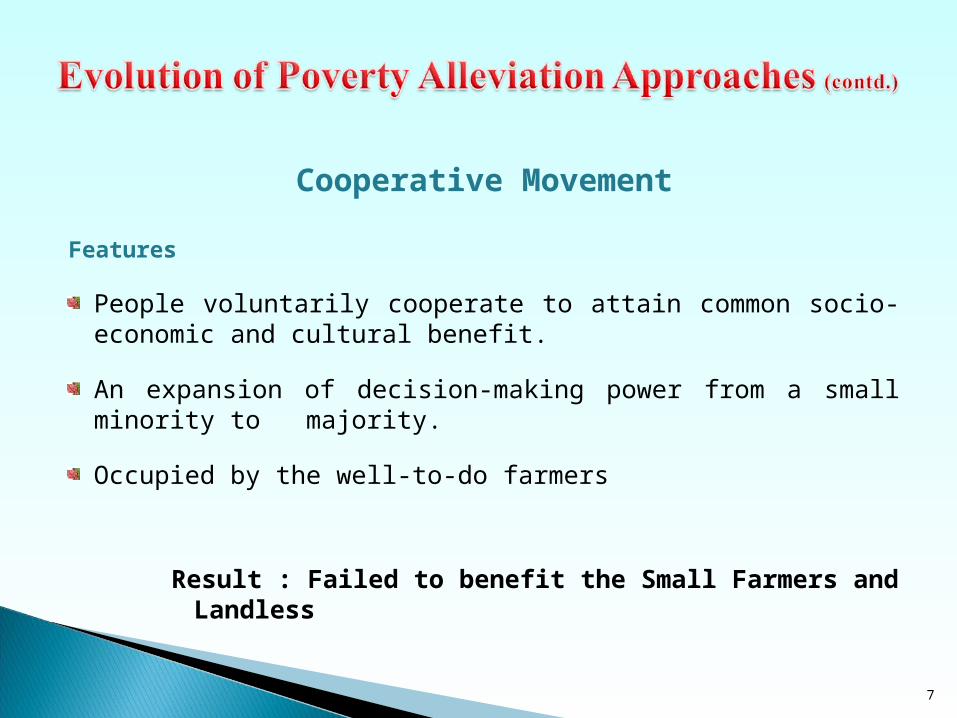

Cooperative Movement

Features

People voluntarily cooperate to attain common socio-economic and cultural benefit.

An expansion of decision-making power from a small minority to majority.

Occupied by the well-to-do farmers

Result : Failed to benefit the Small Farmers and Landless

7

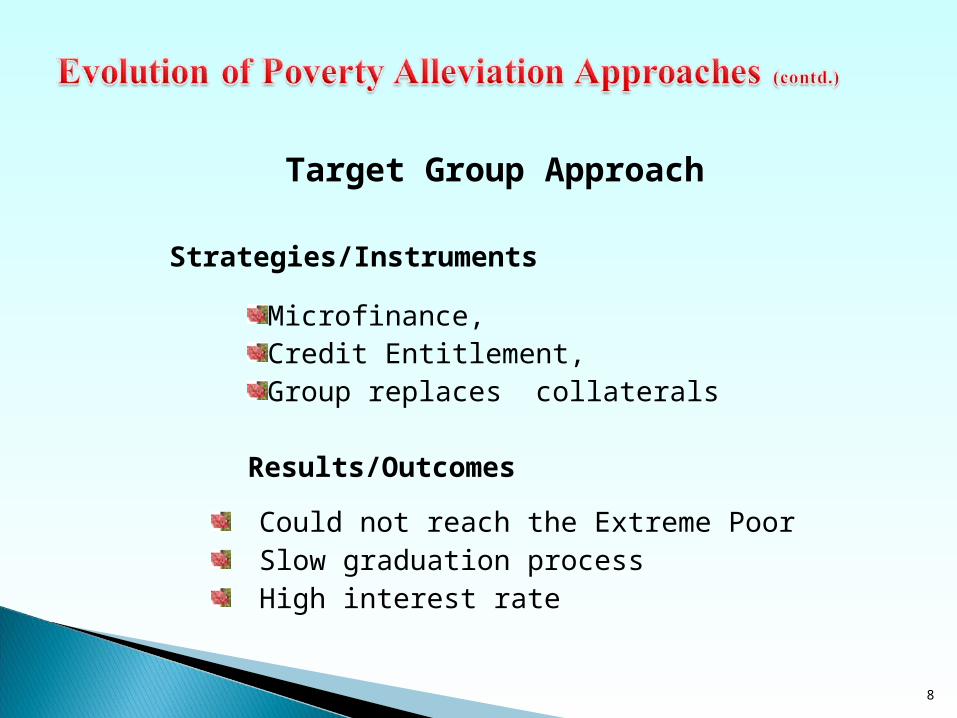

Target Group Approach

Strategies/Instruments

Microfinance, Credit Entitlement, Group replaces collaterals

Results/Outcomes

Could not reach the Extreme PoorSlow graduation process High interest rate

8

9

Ultra poor could not be targeted

Higher rate / pricing

Very basis of interest is exploitative

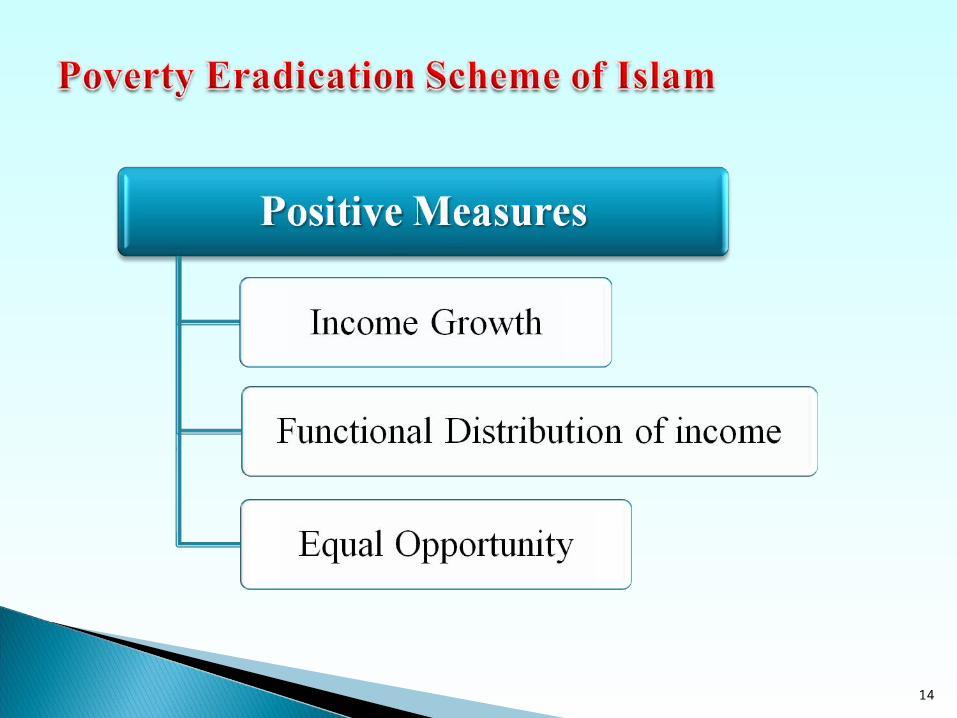

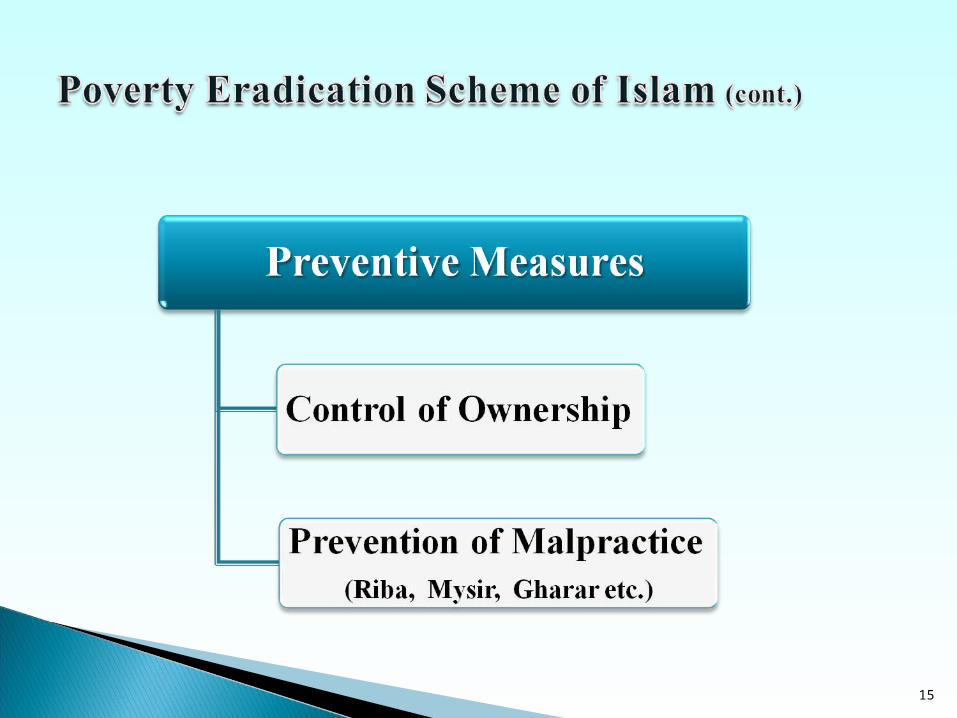

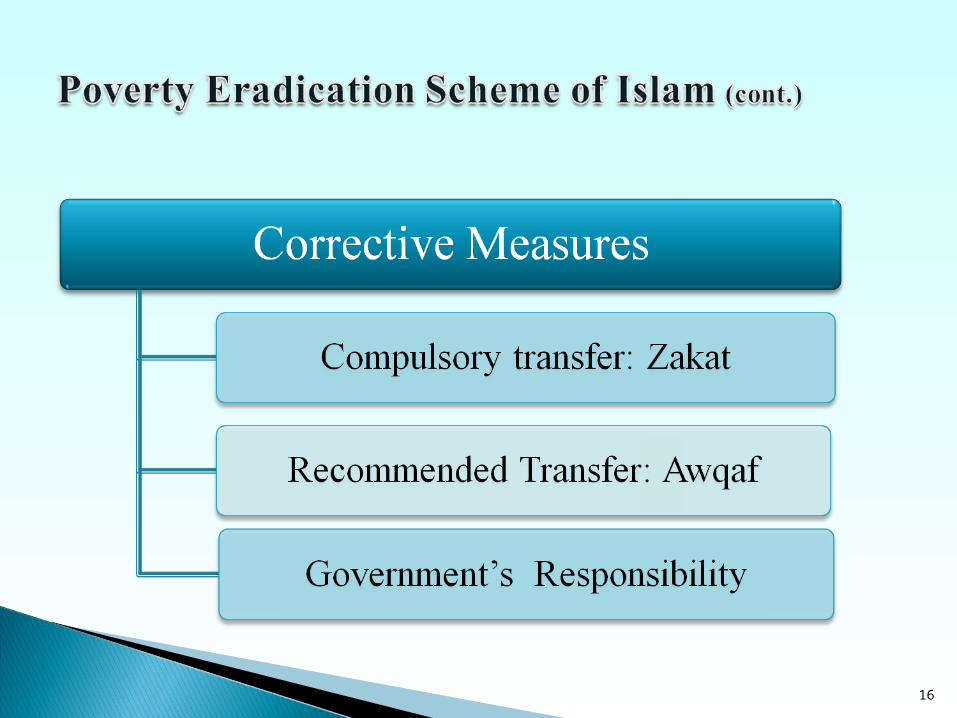

Islamic principles of poverty alleviation are based on:

10

Universal brotherhood

Distributive justice

Circulation of wealth

Transfer payment

Financial inclusion

Filter Mechanism ( Moral & Market)

Fellow feelings

I was hungry but you didn’t feed me. But how I would be able to feed you as you are ever exalted and the Lord of the worlds! O my servant, if you be at the side of my ailing servant and soothe him, you can reach me there. Hadith al Qudsi.

11

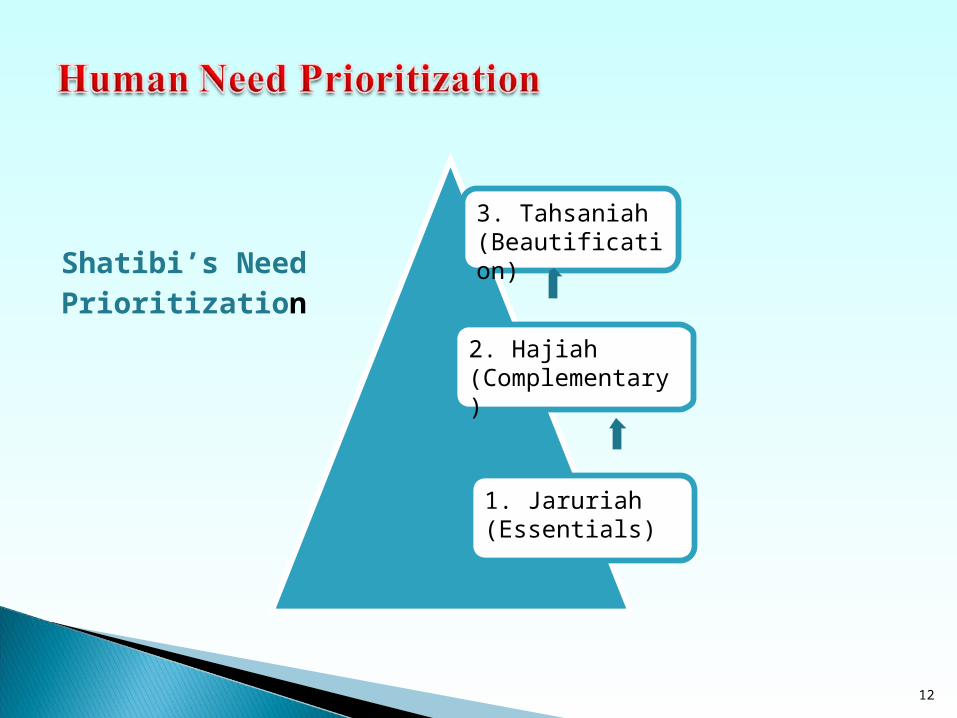

Shatibi’s Need Prioritization

12

1. Jaruriah(Essentials)

2. Hajiah (Complementary)

3. Tahsaniah (Beautification)

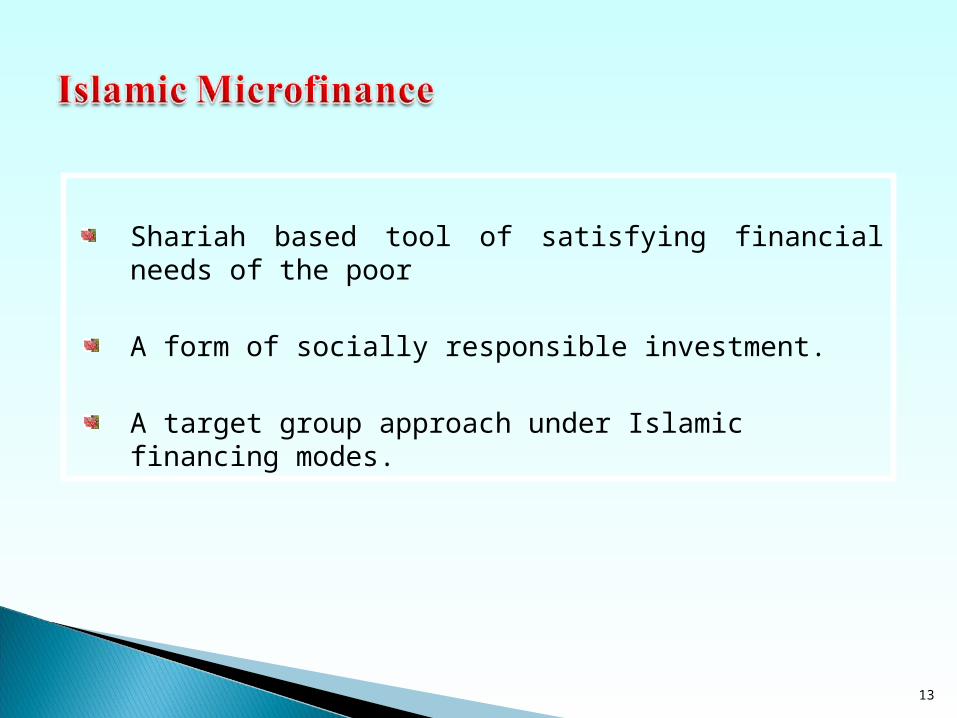

Shariah based tool of satisfying financial needs of the poor

A form of socially responsible investment.

A target group approach under Islamic financing modes.

13

14

15

16

17

Special Features of RDSSpecial Features of RDS

Shariah based micro-finance

Collateral free

Farming and off-farming activities

Job Creation

Welfare and ethical services

Quard facilitates for sanitation

18

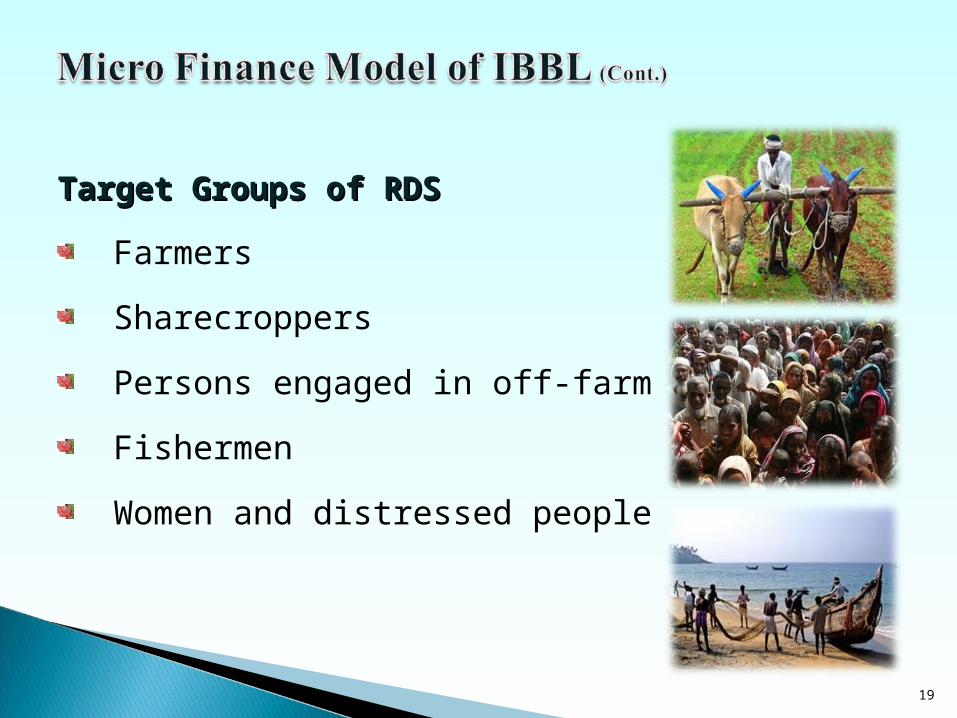

Target Groups of RDSTarget Groups of RDS

Farmers

Sharecroppers

Persons engaged in off-farm activities

Fishermen

Women and distressed people

19

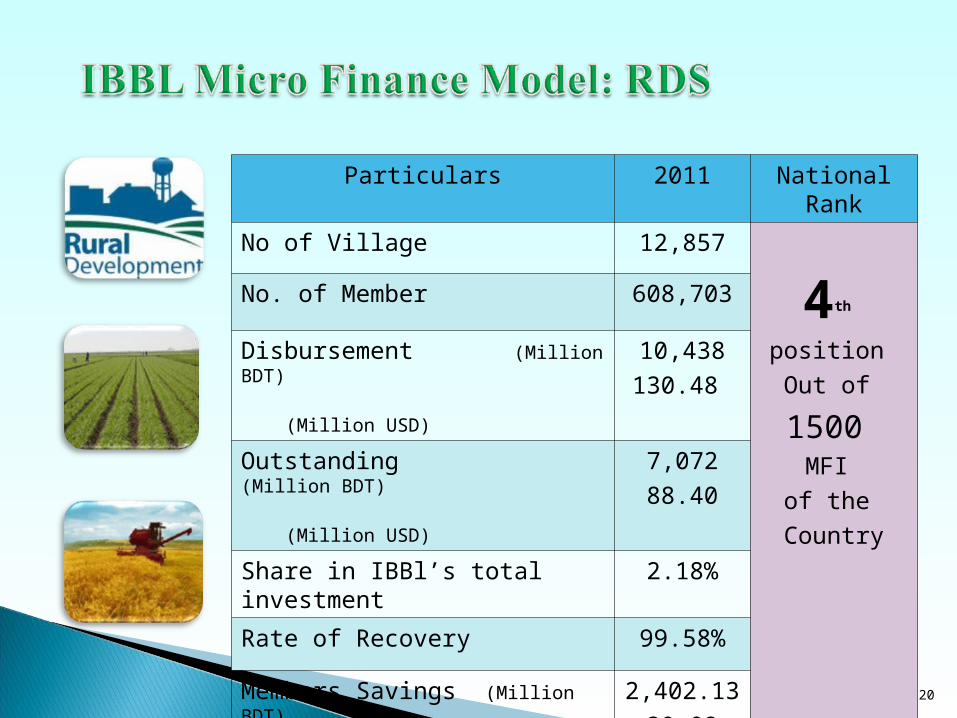

Particulars 2011 National Rank

No of Village 12,857

4th

position Out of

1500 MFI

of the Country

No. of Member 608,703

Disbursement (Million BDT)

(Million USD)

10,438130.48

Outstanding (Million BDT)

(Million USD)

7,07288.40

Share in IBBl’s total investment

2.18%

Rate of Recovery 99.58%

Members Savings (Million BDT)

(Million USD)

2,402.1330.02

20

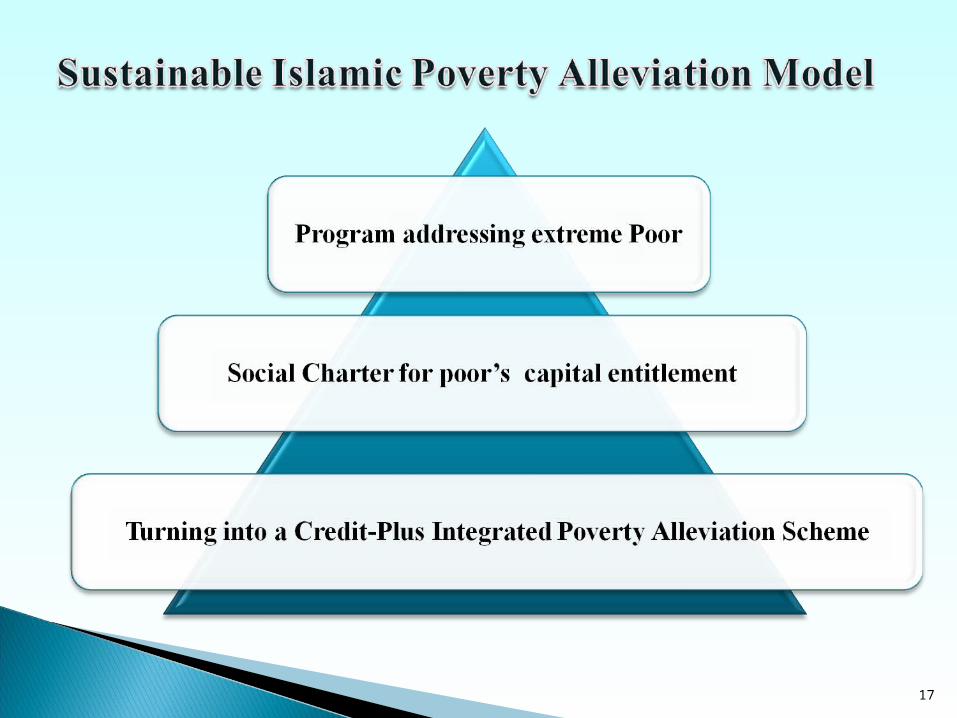

Go for an Integrated Poverty Eradication Model

(Microfinance, Zakah and Awqaf)

Target the extreme poor

Ensure Financial Inclusion

21

22

![[Slideshare] tafaqqahu-(2014)-#2 c -going-to-toilet-and- clothe-(13-september-2014)](https://img.pdfslide.us/doc/110x75/5537e3fe4a7959016b8b467f/slideshare-tafaqqahu-2014-2-c-going-to-toilet-and-clothe-13-september-2014.jpg)