Embed Size (px)

Citation preview

1

Mortgage Defaults and Foreclosures: Recent Trends and Associated Economic and Market

Developments

Randy FasnachtU.S. Government Accountability Office

Financial Markets and Community [email protected]

Presentation at the National Community Development Association

2008 Winter ConferenceJanuary 23, 2008

2

Objectives

• Analyze the scope and magnitude of recent trends in home mortgage defaults and foreclosures, and how these trends compare with historical values.

• Evaluate developments in economic conditions and the primary and secondary mortgage markets associated with recent default and foreclosure trends.

3

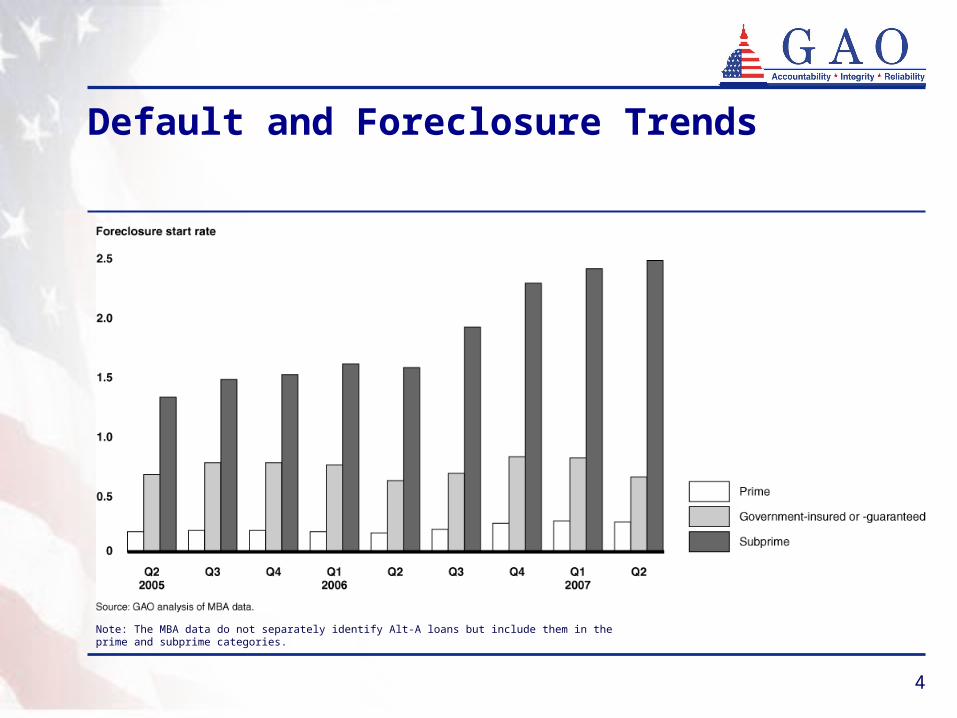

Default and Foreclosure Trends

4

Default and Foreclosure Trends

Note: The MBA data do not separately identify Alt-A loans but include them in the prime and subprime categories.

5

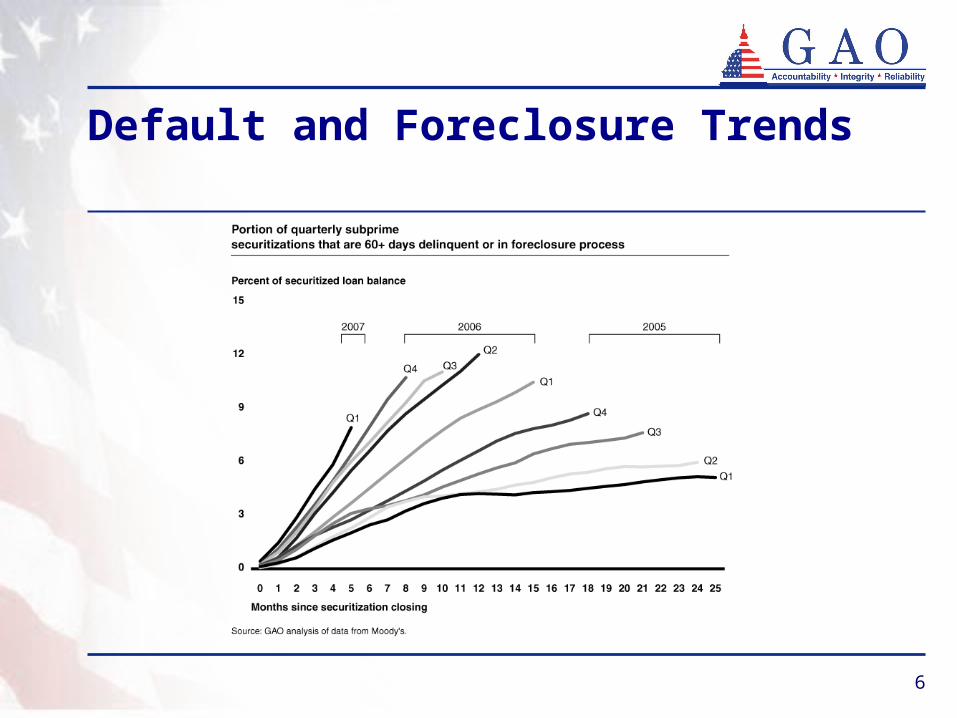

Default and Foreclosure Trends

6

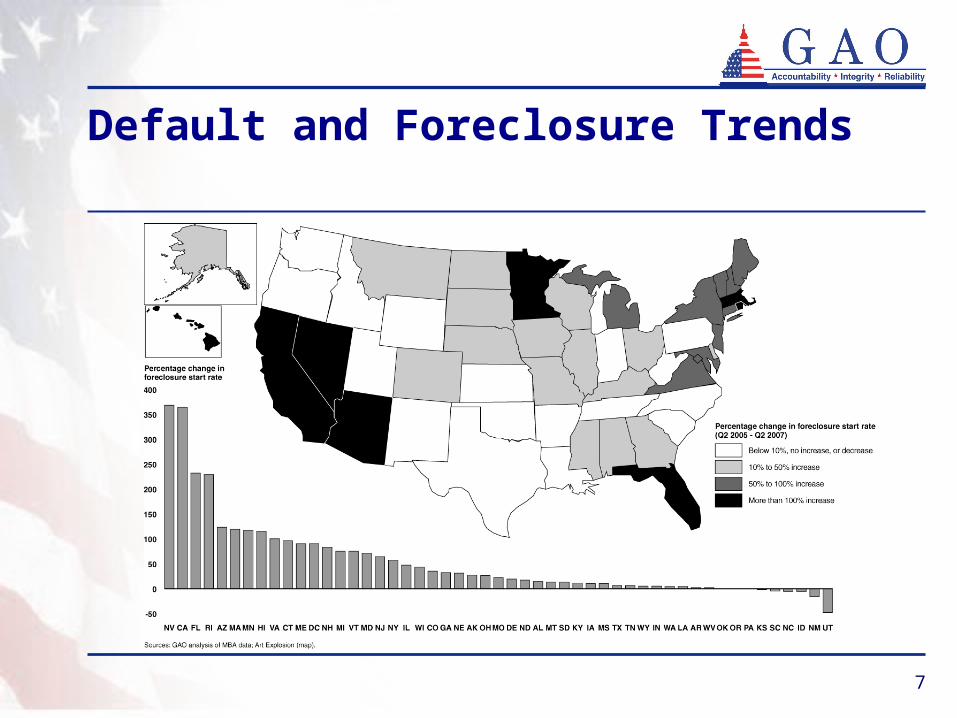

Default and Foreclosure Trends

7

Default and Foreclosure Trends

8

Developments Associated with Recent Trends

• A combination of economic and market developments contributed to recent default and foreclosure trends, including:

• the rapid decrease in home price appreciation throughout much of the nation beginning in 2005 and weak labor market conditions in certain states;

• aggressive lending practices that reduced the likelihood that some borrowers would be able to meet their mortgage obligations; and

• growth in the private mortgage-backed securities market, which provided liquidity to support these lending practices.

• Other developments may have played a role, but additional information would be needed to fully assess their impact.

9

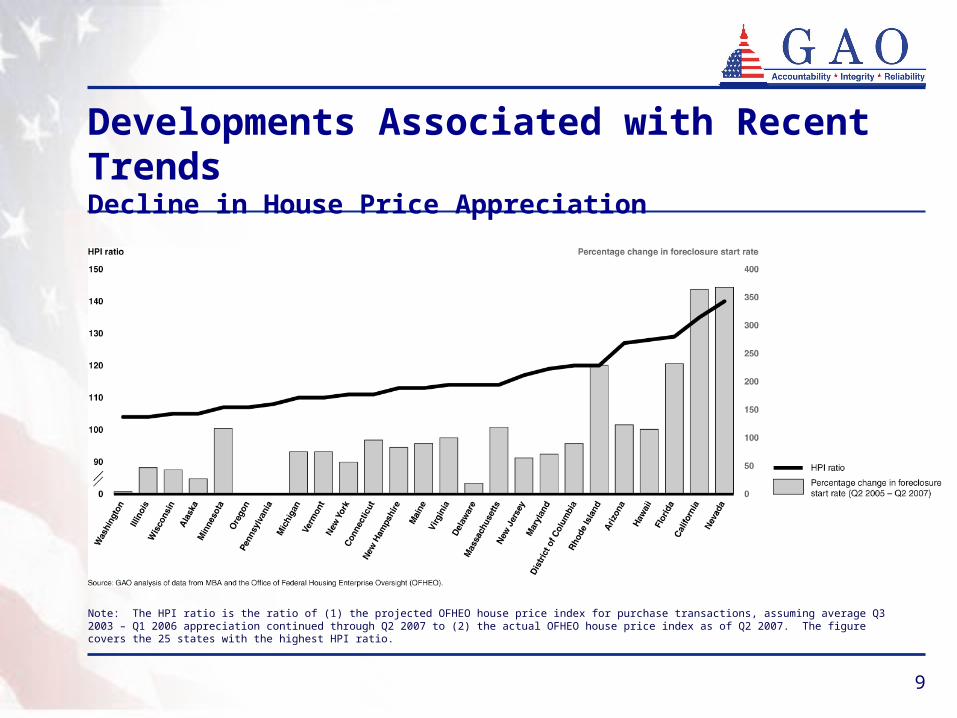

Developments Associated with Recent TrendsDecline in House Price Appreciation

Note: The HPI ratio is the ratio of (1) the projected OFHEO house price index for purchase transactions, assuming average Q3 2003 – Q1 2006 appreciation continued through Q2 2007 to (2) the actual OFHEO house price index as of Q2 2007. The figure covers the 25 states with the highest HPI ratio.

10

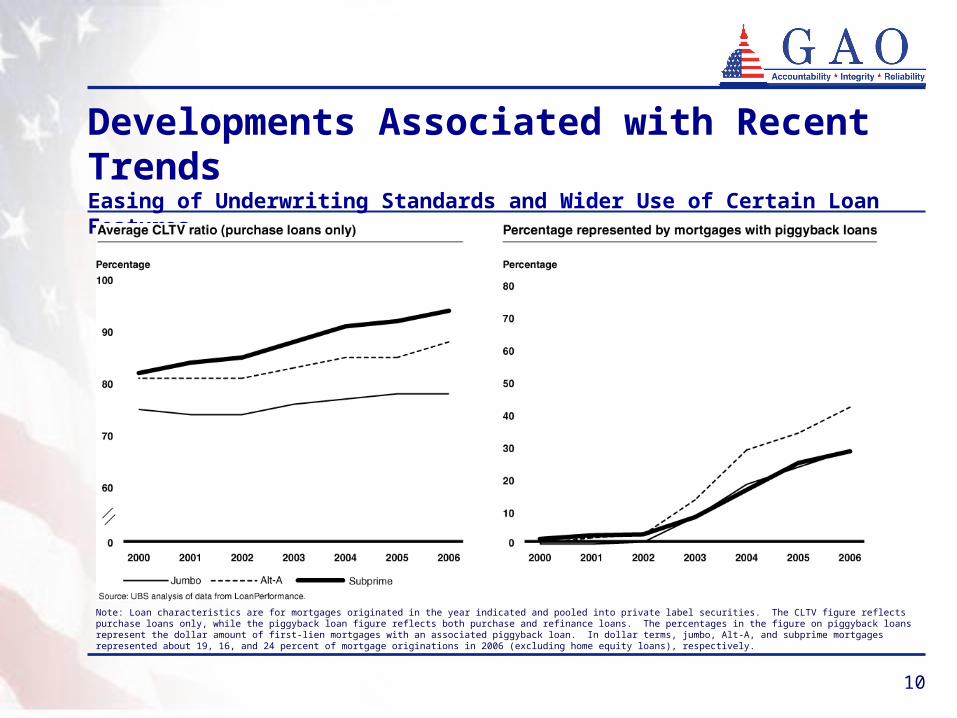

Developments Associated with Recent TrendsEasing of Underwriting Standards and Wider Use of Certain Loan Features

Note: Loan characteristics are for mortgages originated in the year indicated and pooled into private label securities. The CLTV figure reflects purchase loans only, while the piggyback loan figure reflects both purchase and refinance loans. The percentages in the figure on piggyback loans represent the dollar amount of first-lien mortgages with an associated piggyback loan. In dollar terms, jumbo, Alt-A, and subprime mortgages represented about 19, 16, and 24 percent of mortgage originations in 2006 (excluding home equity loans), respectively.

11

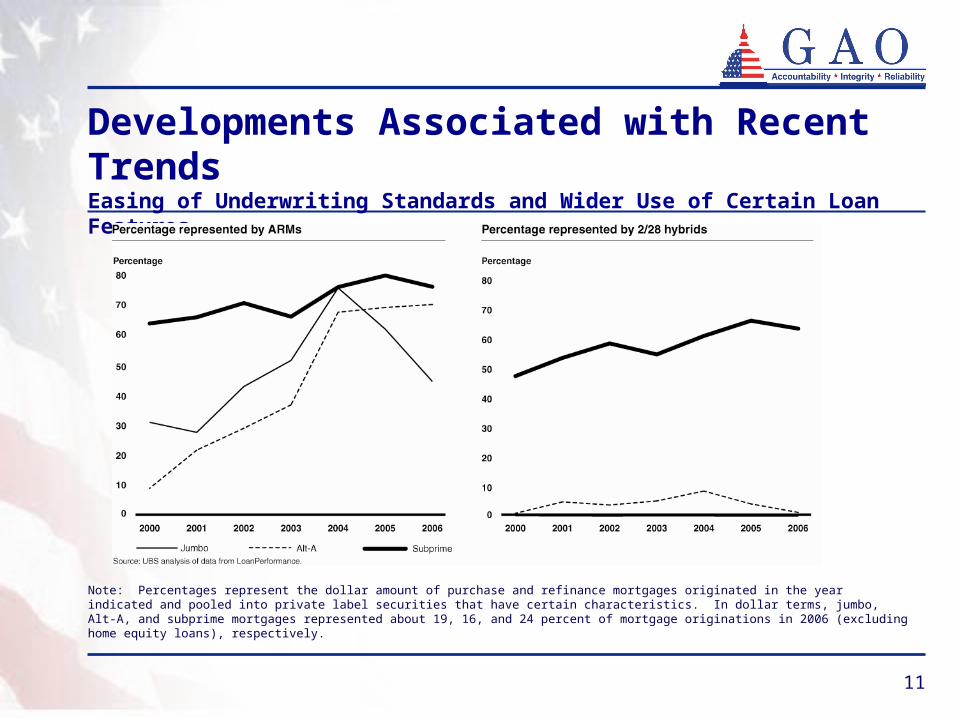

Developments Associated with Recent TrendsEasing of Underwriting Standards and Wider Use of Certain Loan Features

Note: Percentages represent the dollar amount of purchase and refinance mortgages originated in the year indicated and pooled into private label securities that have certain characteristics. In dollar terms, jumbo, Alt-A, and subprime mortgages represented about 19, 16, and 24 percent of mortgage originations in 2006 (excluding home equity loans), respectively.

12

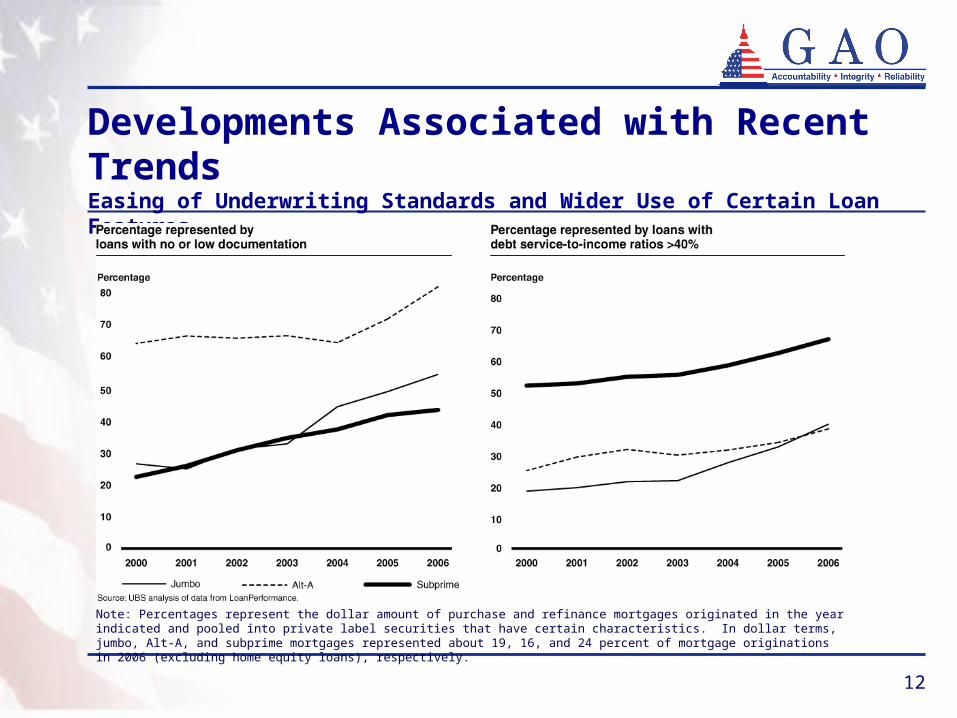

Developments Associated with Recent TrendsEasing of Underwriting Standards and Wider Use of Certain Loan Features

Note: Percentages represent the dollar amount of purchase and refinance mortgages originated in the year indicated and pooled into private label securities that have certain characteristics. In dollar terms, jumbo, Alt-A, and subprime mortgages represented about 19, 16, and 24 percent of mortgage originations in 2006 (excluding home equity loans), respectively.

13

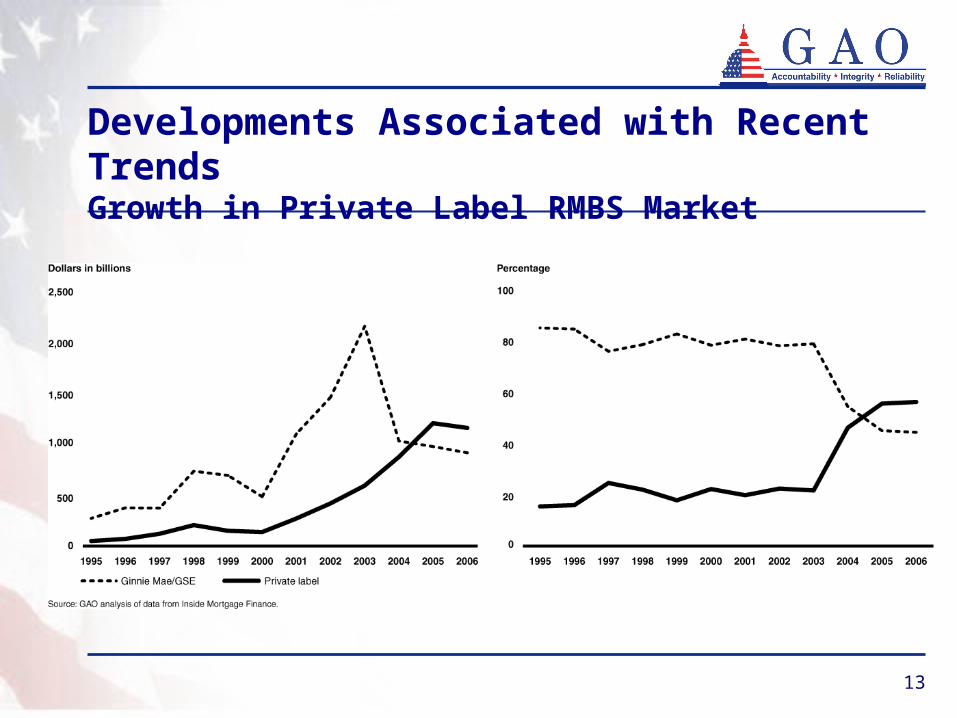

Developments Associated with Recent TrendsGrowth in Private Label RMBS Market

14

Developments Associated with Recent TrendsGrowth in Private Label RMBS Market

• Role of investment banks and credit rating agencies

• Surprised by the speed and severity of declines in house price appreciation and underestimated the risks of certain loan features such as low documentation and high LTV ratios.

• Credit rating agencies have made changes to their ratings methodologies to reflect worse-than-expected loan performance.

• Rating downgrades introduced uncertainty about the credit quality of subprime RMBS and other structured products, contributing to credit crunch.

15

Developments Associated with Recent TrendsOther Possible Factors

• Misaligned incentives and lack of accountability in the origination and distribution of mortgages

• Financial incentives to increase loan volume, potentially at the expense of loan quality.

• Some originators lacked sufficient capital to make good on representations and warranties.

• Federal regulation of non-bank lenders• Of the top 25 originators of subprime and Alt-A loans in 2006,

21 were nonbank lenders.• Mortgage fraud

• No and low documentation loans presented opportunities to misrepresent income and assets