Embed Size (px)

Citation preview

1

Managing Your CreditDr. HaysPersonal Finance – BKHS2-26-13

2

Objectives

• Provide a background on credit

• Explain the key characteristics of credit cards

• Offer tips on using credit cards

3

Background on Credit

• Credit: funds provided by a creditor to a borrower that will be repaid by the borrower in the future with interest

• Advantages of using credit– Ability to purchase when price exceeds

available cash• Purchase home, car, pay tuition

– Convenience

4

Background on Credit

• Disadvantages of using credit– Difficulty making payments– Temptation for impulse purchases– Hinders ability to save– Expensive

5

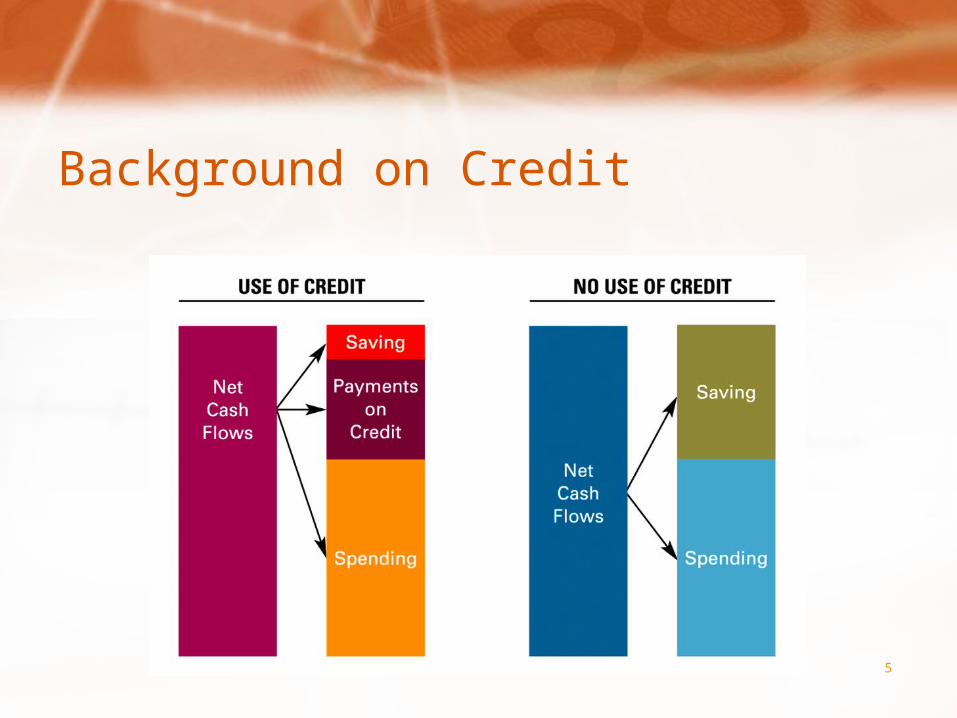

Background on Credit

Exhibit 7.1: Impact of Credit Payments on Saving

6

Background on Credit

• Establish a credit history– Often begins with timely payment

of utility bills

• Impact of the interest rate on credit payments– Simple interest rate: the percentage of credit

that must be paid as interest on an annual basis

7

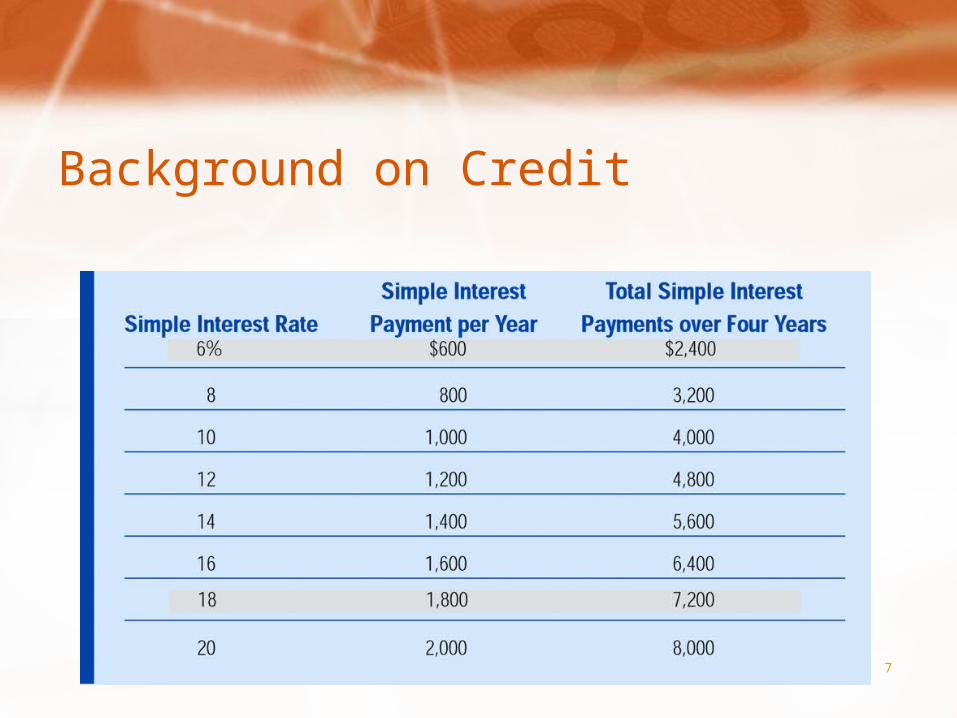

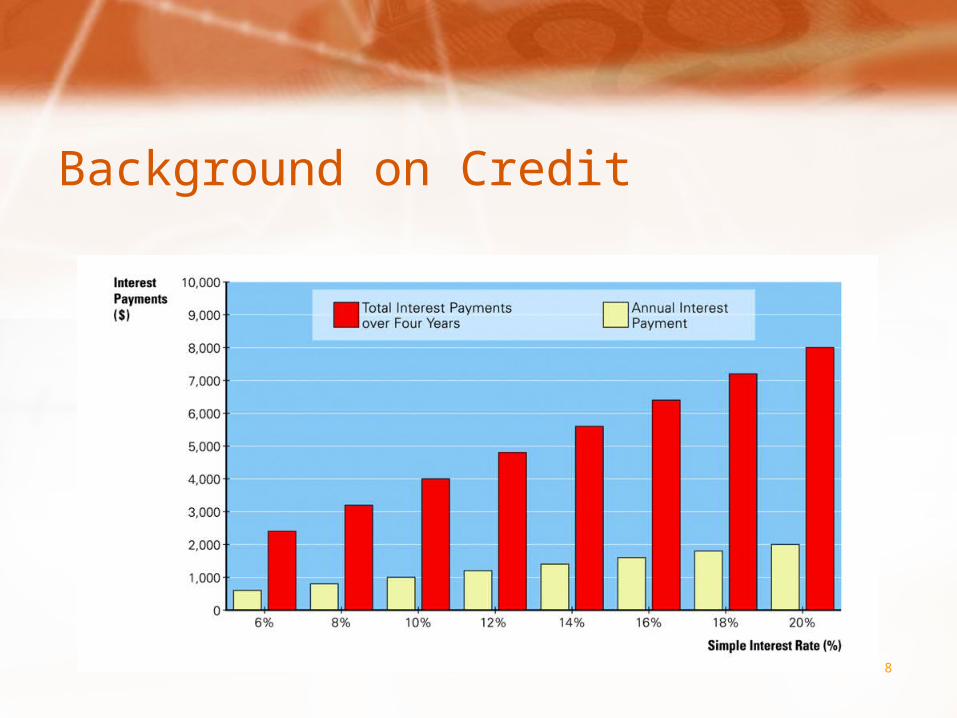

Background on Credit

Exhibit 7.2: How Interest Payments Are Influenced by Interest Rates

8

Background on Credit

Exhibit 7.2: How Interest Payments Are Influenced by Interest Rates

9

Background on Credit

– Annual percentage rate (APR): the simple interest rate including any fees charged by the creditor

• Allows comparison among potential lenders

10

Credit Cards

• Applying for a credit card — potential creditors obtain information from you, about you, and about the economy– Personal information

• Cash inflows• Cash outflows• Credit history• Capital• Collateral

11

Credit Cards

• Credit check– Credit report: a statement of creditworthiness

based on information such as whether you have made late payments, and any unpaid current bills

– Credit scoring often determines whether or not you are approved for credit

12

Credit Cards

– Interpreting credit ratings• High ratings usually provide easy credit approval• How ratings make obtaining credit difficult

13

Credit Cards

• Focus on Ethics: Guarding your financial information– Financial institutions must provide privacy

policies telling what information they collect and what information they intend to share

– Evaluate your credit report regularly– Creditors may also consider debt level and

economic situation

14

Credit Cards

– The credit decision• You should receive a reply within 30 days• If you are rejected, the creditor must give an

explanation• Laws prohibit discrimination in credit based on

race or gender• Creditors may not consider criminal records,

political preferences, or religion

15

Credit Cards

• Types of credit cards– Visa, MasterCard and American Express

most popular– Visa and MasterCard allow partial payments– American Express requires full payments

16

Credit Cards

– Retail (or proprietary) credit card: a credit card that is honored by a specific retail establishment

• Retail stores and gas stations• Limits purchases to a single merchant

• Credit limit — maximum amount of credit allowed

• Annual fee• Incentives to use the card

17

Credit Cards

• Prestige cards: credit cards, such as gold or platinum cards, issued by a financial institution to individuals who have an exceptional credit standing

• Grace period — period between time of purchase and when payment is due

• Cash advances– Usually charge high interest plus a fee

18

Credit Cards

• Interest rate — usually between 15 and 20 percent– Finance charge: the interest that you must

pay as a result of using credit

• Credit card statement details differences in new balance and previous balance

19

Credit Cards

• Comparing credit cards– Acceptance by merchants– Annual fee– Interest rate

• Watch for “teaser rates”

– Maximum limit

20

Tips on Using Credit Cards

• Use a credit card only if you can cover the bill

• Impose a tight credit limit• Pay credit card bills before investing money• Use savings if necessary to pay the credit card

bill on time• If you cannot avoid credit card debt, pay it off

before other debt

21

Tips on Using Credit Cards

• Avoid credit repair services

• Avoid credit card fraud

• Deter identity theft

22

Financial Planning Online:The Best Credit Card for You• Go to:

http://www.bankrate.com/brm/rate/cc_home.asp

• This Web site provides links to help you get the best overall credit card rate, the lowest introductory rate, frequent flier credit cards, and other special features.

23

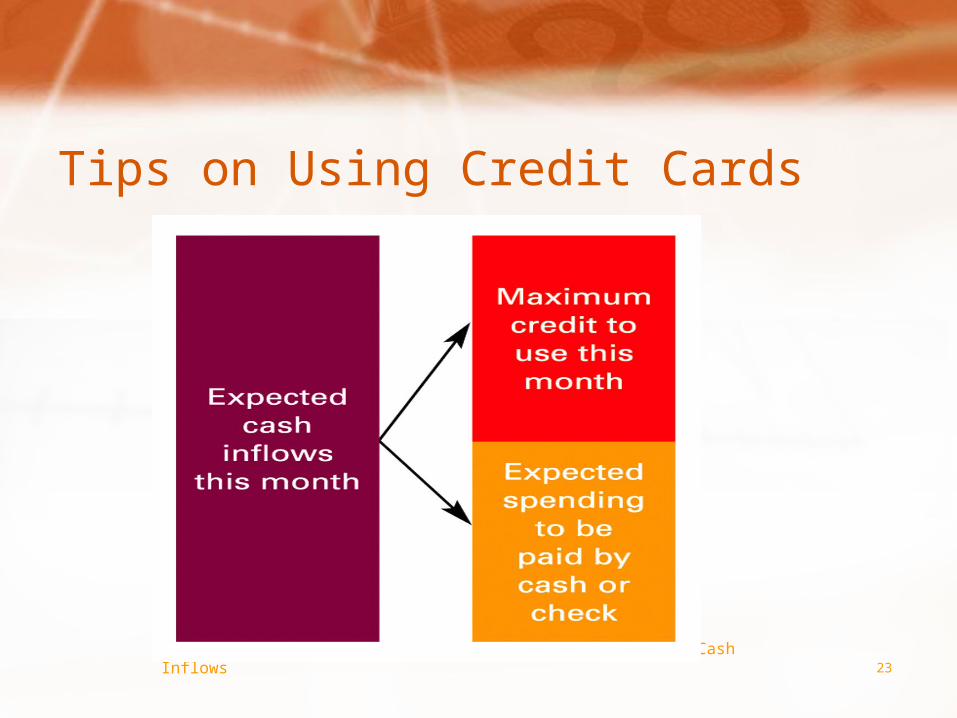

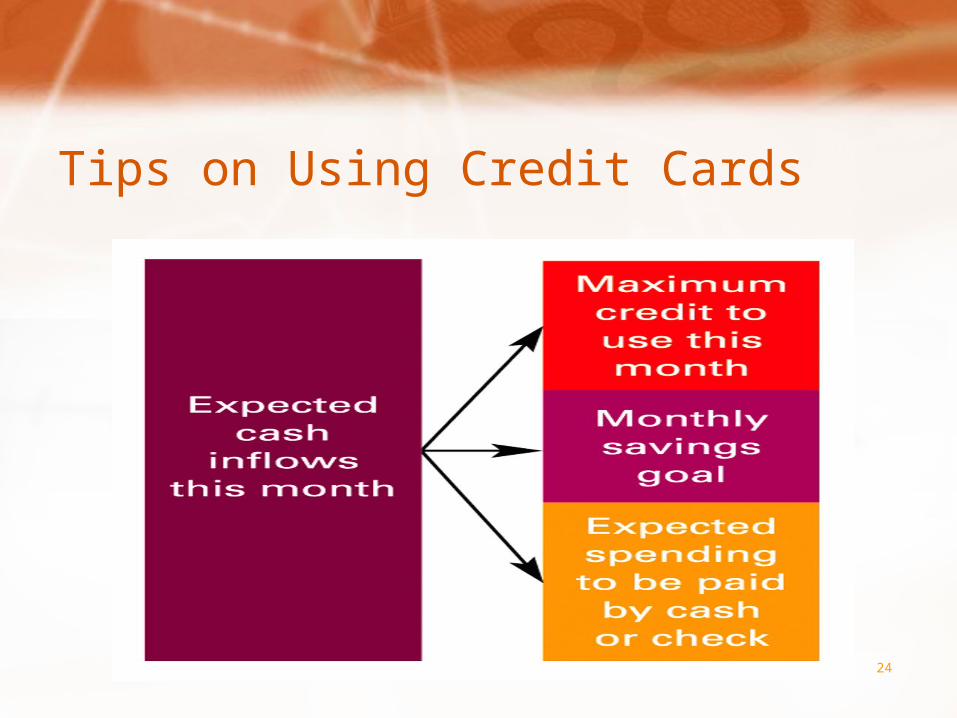

Tips on Using Credit Cards

Exhibit 7.3: Self-Imposed Credit Limit Based on Monthly Cash Inflows

24

Tips on Using Credit Cards

Exhibit 7.4: Self-Imposed Credit Limit Based on Monthly Cash Inflows and a Monthly Savings Goal

25

Dealing With Credit Debt

• If you find yourself with excessive credit card debt– Spend as little as possible– Consider ways to increase income– Borrow from a family member– Get a debt consolidation loan– Sell assets for cash– Reduce everyday expenses

26

Dealing With Credit Debt

– If all else fails you may need to file for personal bankruptcy

• Chapter 7 allows the discharge of almost all debts, but also have to surrender assets to pay debt

• Chapter 13 allows you to keep your assets, but the court takes control of your finances and devised a 3 – 5 year repayment plan

27

Financial Planning Online: Estimating the Time Necessary to Pay Off Your Balance

• Go to: http://www.financenter.com/products/sellingtools/calculators

• Click on: “Budget,” then “What will it take to pay off my balance?”

• This Web site provides an estimate of the number of payments you need to make to pay off your credit card balance.

28

Financial Planning Online:Identity Theft• Go to: http://www.consumer.gov/idtheft/

• This Web site provides information on how thieves can steal your identity and how you can prevent identity theft.

29

How Credit Management Fits Within Your Financial Plan• Key credit management decisions

for your financial plan are:– What limit should you impose on your

credit card?– When should you use credit?

30

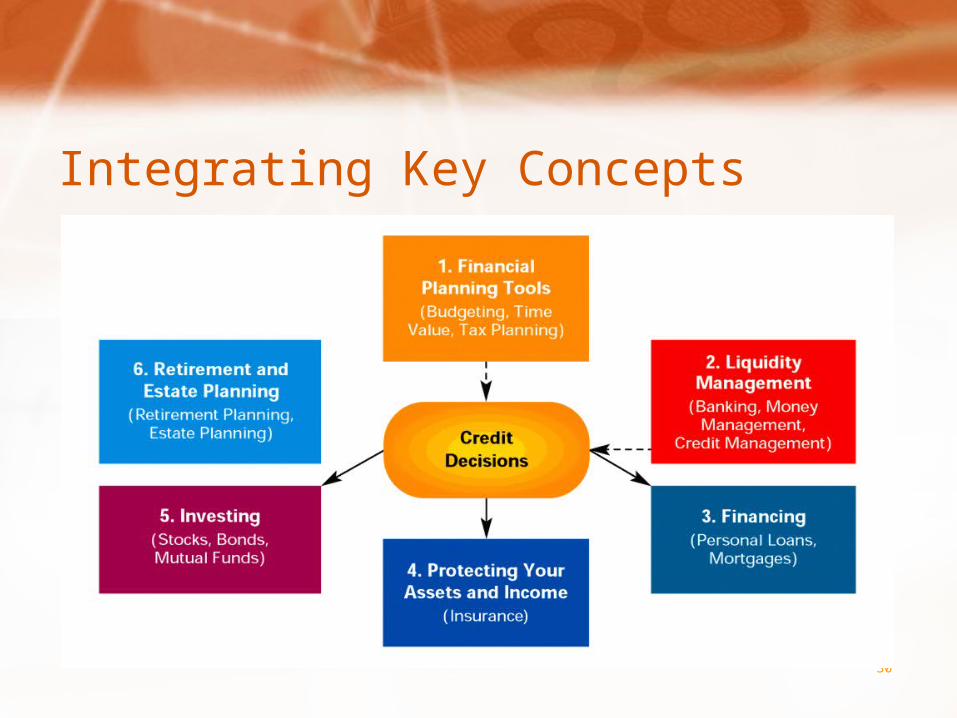

Integrating Key Concepts

31

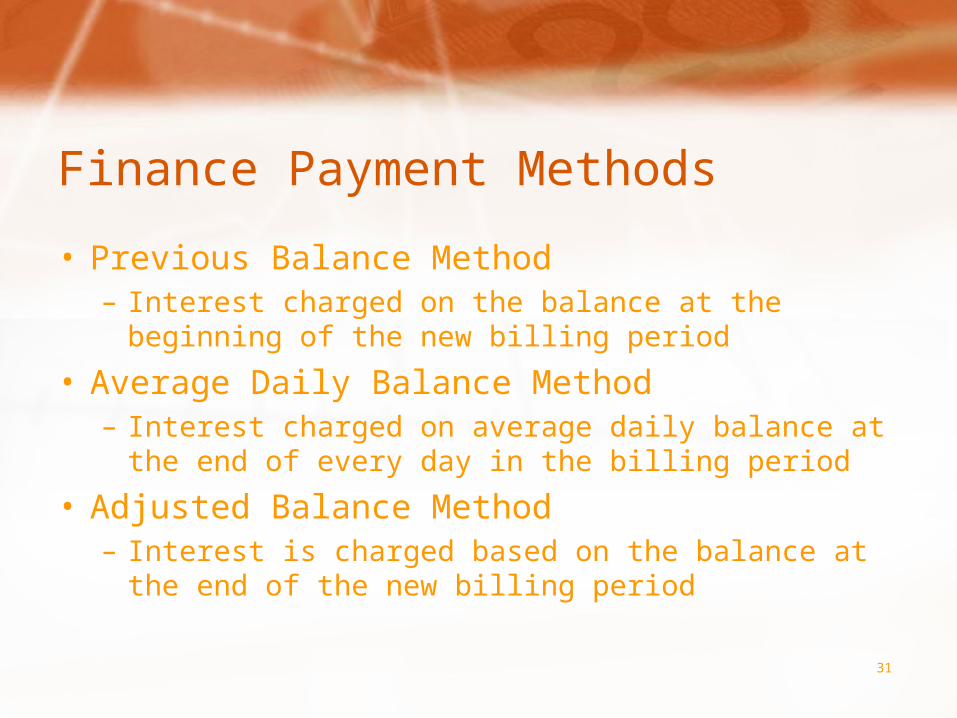

Finance Payment Methods

• Previous Balance Method– Interest charged on the balance at the beginning of

the new billing period

• Average Daily Balance Method– Interest charged on average daily balance at the end

of every day in the billing period

• Adjusted Balance Method– Interest is charged based on the balance at the end

of the new billing period