Embed Size (px)

Citation preview

1

Interest Rate Fluctuations

Chapters 5

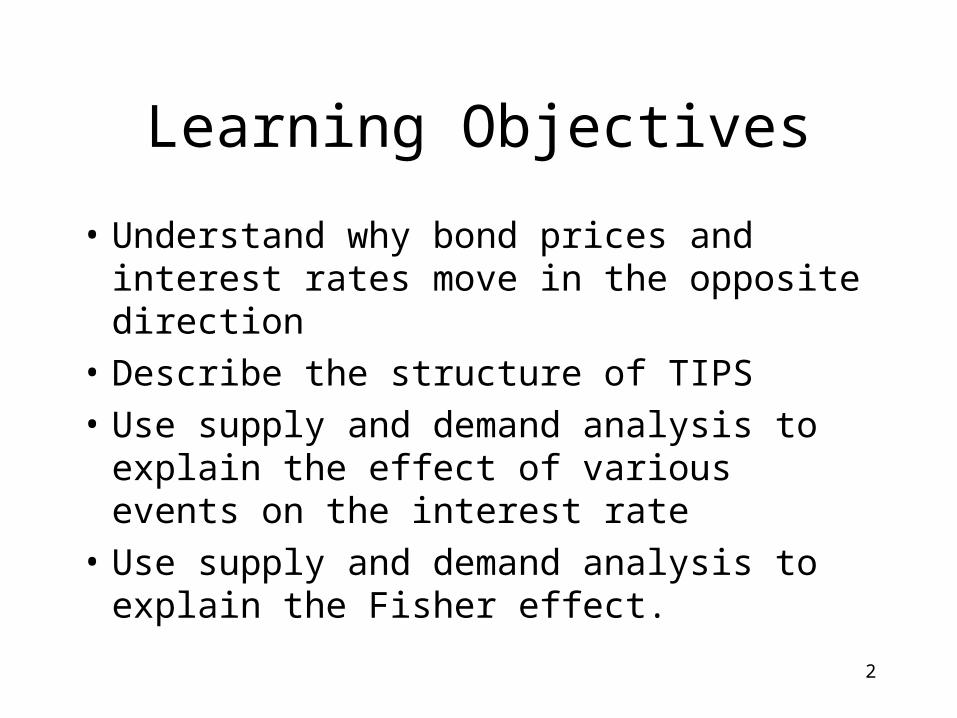

Learning Objectives

• Understand why bond prices and interest rates move in the opposite direction

• Describe the structure of TIPS

• Use supply and demand analysis to explain the effect of various events on the interest rate

• Use supply and demand analysis to explain the Fisher effect.

2

3

Relationship Between Price and Yield to Maturity

.

4

TIPS (Treasury Inflation Protection Securities)

• Originally issued in 1997.

• Interest and principal payments are adjusted for inflation.

• In times of high inflation the $ amount paid to investors rises.

• Return on TIPS relative to regular Treasurys provides information on expected inflation.

Yields on 1-month T-bills2001-2008

5

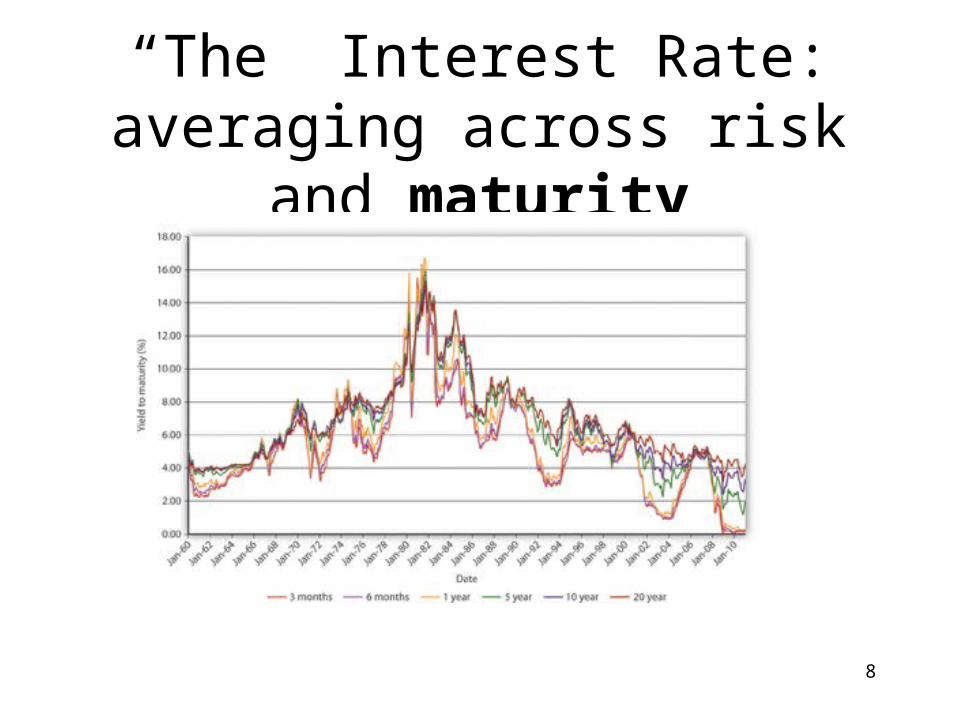

“The” Interest Rate: averaging across risk and maturity

6

“The” Interest Rate: averaging across risk and maturity

7

“The” Interest Rate: averaging across risk and maturity

8

Economists can’t predict …

… but they can explain after the fact.

9

Supply and Demand of Bonds

Supply: borrowers (issuers of bonds)

Demand: lenders (buyers of bonds)

10

N=1, FV=1000

Price (PV) Yield (I/Y)

750

800

850

900

950

11

N=1, FV=1000

Price (PV) Yield (I/Y)

750 33.33

800 25.00

850 17.65

900 11.11

950 5.26

12

13

Supply and Demand

Analysis ofthe Bond Market

Movement along the curve

Versus

Shifts of the curve

14

15

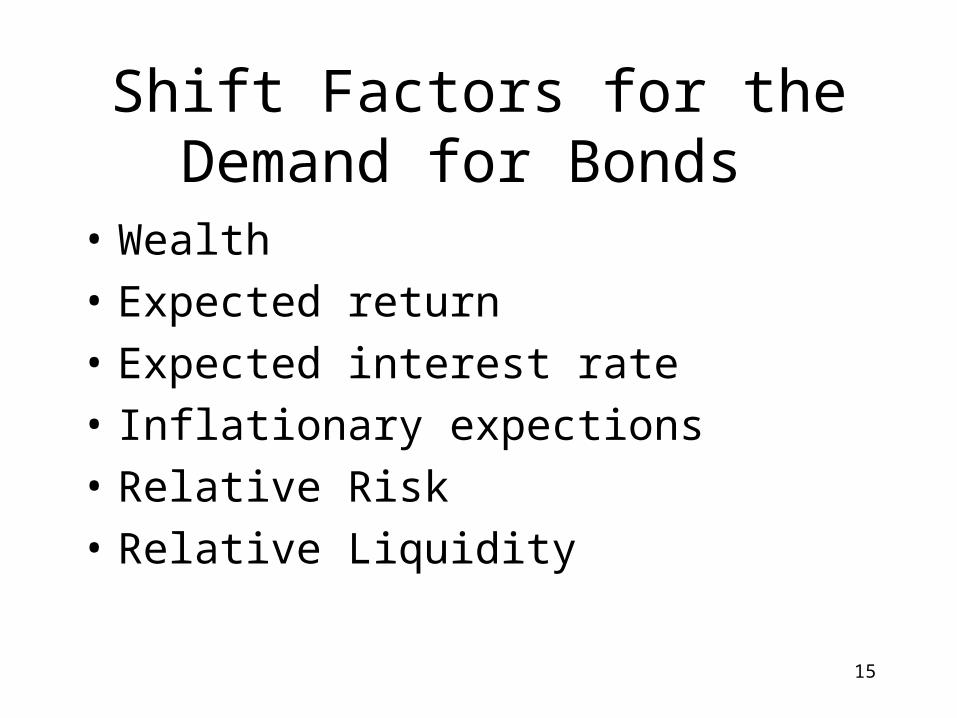

Shift Factors for the Demand for Bonds

• Wealth

• Expected return

• Expected interest rate

• Inflationary expections

• Relative Risk

• Relative Liquidity

16

Shifts in the Bond Demand Curve

17

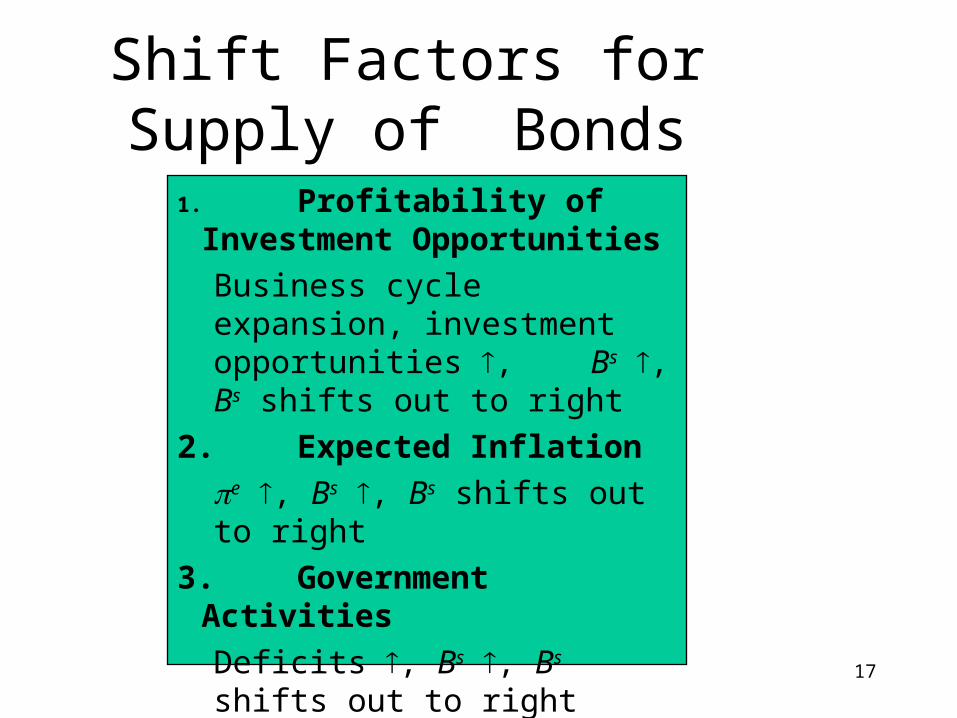

1. Profitability of Investment Opportunities

Business cycle expansion, investment opportunities , Bs , Bs shifts out to right

2.Expected Inflation

e , Bs , Bs shifts out to right

3.Government Activities

Deficits , Bs , Bs shifts out to right

Shift Factors for Supply of Bonds

18

Shifts in the Bond Supply Curve

19

Changes in e: the Fisher Effect

If e 1. Bd shifts in to

left2. Bs , Bs shifts

out to right3. P , i

© 2005 Pearson Education Canada Inc.

20

• What will happen to bond prices if stock trading commissions decrease? Why?

• What will happen to bond prices if bond trading commissions increase? Why?

• What will happen to bond prices if the government implements tax increases? Why?

21

• If government revenues drop significantly (and remember all else stays the same, including government expenditures), what will likely happen to bond prices? Why?

• If the government guaranteed the payment of bonds, what would happen to their prices? Why?

• What will happen to bond prices if the government implements regulatory reforms that reduce regulatory costs for businesses? Why?

• If government revenues increase significantly, what will likely happen to bond prices? Why?

• What will happen to bond prices if terrorism ended and the world’s nations unilaterally disarmed and adopted free trade policies? Why?

• What will happen to bond prices if world peace brought substantially lower government budget deficits?

22

Changes in the money supply

Two effects:

The initial effect of more money to invest lowers the interest rate, but if market participants expect inflation then the Fisher effect will cause the interest rate to increase.

23

24