Embed Size (px)

Citation preview

Immersion Day Experience #1Technical #1Date: 9/23/2021

Best Practice Workshop: When to employ, and How to prepare, submit and negotiate Offers in Compromise, Collection Due Process (CDPs) Hearing Requests and a Collection Appeal Protests (CAPs). Including advanced strategies w/Case Studies. Best Practices when dealing with Appeals.

#1. How to Represent Your Clients With CONFIDENCE!

Introduction to AppealsUsing CDP’s and CAP’s

!"#$#%&#"'(Parham Khorsandi, Esq., Managing Partner, Victory Tax Lawyers,LLP (866) 640-0640

2

Introduction

© Roz Strategies. All rights reserved.

a) Appeals can be a useful tool, if used properly. b) Main use is to get a higher-level IRS employee

to work the case outside of collectionsc) Secondary use is a form of strategy

© Roz Strategies. All rights reserved.

d) 3 types I. Collection Due Process (CDP) Hearing Form

12153II. Equivalency Hearing (EH) Form 12153III. CAP – Collection Appeal Request Form 9423

Collections v. Appeals

© Roz Strategies. All rights reserved.

a. When your client owes money to the IRS, they all start in IRS Collectionsb. Mainly two types of IRS Collections:

I. ACS: Automated Collection SystemI. “The 1-800 Goons”II. Limited substantiationIII. New agent each time (new answers)IV. NationwideV. 12,000 new collection agents – untrained and senseless

Collections v. Appeals (cont.)II. RO: Revenue Officer

I. Local Officer based on geographyII. Cannot change ROIII. Aggressive and more detailed than ACS (Automated Collection System)IV. Must substantiate everything

c. Can go from Collections to Appeals by filing a CDP, EH, or CAPd. Especially with aggressive RO, or ineffective ACS

Collection Due Process Hearing Request

© Roz Strategies. All rights reserved.

a. CDP Hearing Request must be filed within 30 days of a “Final Notice of Intent to Levy”b. “Final Notice of Intent to Levy” includes:

I. LT11II. Letter 1058III. CP 90 (RO or Social Security Levy)IV. Each tax year has its own final notice

Collection Due Process Hearing Request (cont.)

© Roz Strategies. All rights reserved.

c. CDP takes the case out of and halts IRS Collectionsd. ACS on a CDP: Takes the whole account out of Collections and into Appeals

Collection Due Process Hearing Request (cont)

© Roz Strategies. All rights reserved.

e. RO on a CDP: Only takes the certain year out of Collections and into Appeals

f. ***CDP tolls the CSED*** so beware

I. Only the year that a “Final Notice” was issued goes to Appeals, the remaining stay with the RO

II. PRO TIP: Use this strategy to play the RO against the Appeals Officer. See who gives you a better “deal”. If RO gives better deal, you can withdraw from Appeals. If Appeals gives you a better deal, RO has to go with Appeals determination

© Roz Strategies. All rights reserved.

g. Example of CDP: Taxpayer has 4 years of SFR filings with the IRS and owes $600K. IRS recently did all 4 years of SFR at the same time. Case gets assigned to an aggressive RO, who issues a Final Notice (Letter 1058) on all 4 years. Try to gauge the RO’s temperament….he’s no good. File a CDP request to get out of Collections and into Appeals. File it timely to ensure it pauses Collections. RO MUST send the case to Appeals.

Case Study:

© Roz Strategies. All rights reserved.

h. What if Taxpayer also had another tax year with a balance, and a Final Notice was issued 2 years ago? What would change, if anything?

Equivalency Hearing Request

© Roz Strategies. All rights reserved.

a. Same exact form as CDPb. Must check the box for “Equivalency Hearing” on the Form 12153c. Must file within 1 year of Final Noticed. ACS on Equivalency Hearing: Still takes the whole account out of collections and into

Appeals – should not toll CSEDS

Equivalency Hearing Request (cont.)

© Roz Strategies. All rights reserved.

e. Pro Tip: Use this strategy when there is a lot of waiting that needs to be done. For example, Tax Returns to post, client not getting back to you in time, wants to start IA payments later.

f. Pro Tip: Use EH with ACS when close to a CSED to run out the clock!g. RO on Equivalency Hearing: Will not take TP out of Collections. RO can still pursue

Collections.

© Roz Strategies. All rights reserved.

h. Example: Taxpayer has old balances with ACS. Will be expiring very soon. Taxpayer gets a Final Notice on any period. Waits until the 31st + day and checks the box on the Form for EH. Does not toll statues, and out of Collections.

CAP: Collection Appeal Request Form 9423

© Roz Strategies. All rights reserved.

a. Used to get an immediate Appeals Officer hearing on a narrow issueb. Only in the following situations:

I. Federal Tax Lien: In limited situations where a lien cannot be filed with an IA (securities, security clearance – with very good documentation)

II. Rejection of Installment Agreement – once you send a formal installment agreement, and it gets rejected. Can file a CAP

III. Levy or Proposed Levy – Used when RO threatens to levy

CAP: Collection Appeal Request Form 9423 (cont.)

© Roz Strategies. All rights reserved.

IV. Termination of Installment Agreement – Erroneously have an IA terminated. 1. Or the 2 year period for financial review is up, and they are trying to

terminate the IA.2. You can send a CAP stating there is no financial change, and try to

reinstate the IA.

CAP: Collection Appeal Request Form 9423 (cont.)

© Roz Strategies. All rights reserved.

V. Seizure – Trying to take a home/ personal property and file a CAP to show there is an alternative collections method.

VI. Modification of Installment Agreement – IRS is trying to modify an IA erroneously

CAP: Collection Appeal Request Form 9423 (cont.)

© Roz Strategies. All rights reserved.

c. Must have “Manager Conference” before sending the case to Appeals through CAPd. CAP can have value if used properly. The Appeals Officer’s job to make sure the IRS

is following the correct procedure, NOT to analyze the whole case. It is very limited in its scope.

CAP: Collection Appeal Request Form 9423 (cont.)

© Roz Strategies. All rights reserved.

e. Almost always will “sustain” the Collection Action. But can be used to force the IRS to take a deeper look into the case.

f. Best used with an RO to stop a levy, or to Appeal a Rejection of an IA.g. Does not toll statutes

© Roz Strategies. All rights reserved.

h. Example of CAP: Taxpayer came to my office with an aggressive RO assigned. Taxpayer owes $2.2M. RO had levied his ex-wife’s bank account $180,000 3 days ago. Hires our office. We immediately talk to the RO. He wont release the levy. I speak with manager, and she agrees with RO. I file my CAP and RO cannot pursue further collections. Case goes to Appeals for determination on the levied funds. Considered Separate Property, and we win on the CAP appeal hearing. Levied funds were sent back to TP’s bank.

In Appeals….Now what?

© Roz Strategies. All rights reserved.

a) CDP/EH: You can present your financials to Appeals for an OIC, IA or CNCi. Settlement Officer or Appeals Officer will contact you with a Conference Dateii. Must provide 433A and Substantiated Documents before Conferenceiii. Must substantiate all income and expensesiv. Usually more detailed than ACS, but they have a lot of discretion

In Appeals….Now what?

© Roz Strategies. All rights reserved.

v. Can get to a proper resolution in Appeals and close the case outvi. If you disagree with CDP you have Tax Court rightsvii. If you disagree with EH you have NO Tax Court rightsviii. Takes about 4-6 months for Appeals to be assignedix. Takes about 3-4 months for unfavorable Appeals case to go back to Collections

In Appeals….Now what? (cont.)

© Roz Strategies. All rights reserved.

b) CAP: IRS is following the incorrect procedurei. Less to do with the Facts more to do with the Lawii. IRS did not follow a correct procedure and its up to Appeals to correct itiii. Can be used to re-calculate CSEDs, stop collections, get a real answeriv. Cannot disagree with Appeals in CAPv. No Tax Court Rightsvi. After the determination by Appeals, the case always goes back home (same RO

or ACS)

Case Study 1 – How to Approach

© Roz Strategies. All rights reserved.

i. RO is extremely aggressive and is setting tight deadlinesii. You ate trying to comply but can’t meet his deadlinesiii. RO is not willing to provide any more time and is threatening to levyiv. LT11’s were issued on all periods 2 years agov. You have proved some docs, but need to substantiate a few more expensesHow do you prevent the Revenue Officer from Levying?

Case Study 2

© Roz Strategies. All rights reserved.

i. Barbara Bui is a current client of yours. She has balances from 2012 through 2014 from when she had a good accountant.

ii. That accountant closed her business, and Barbara has not filed since. Your office is preparing the tax returns for 2015 through 2020.

iii. Barbara is a big shot, and it takes her a long time to respond to an email and get documents together.

iv. She has good intentions but is slow. Her account is with ACS and she owes about $110K.

v. 2012 and 2013 had Final Notices received about 3 years ago.vi. You received an LT11 from ACS for tax period 2014.

What are the next steps?

Case Study 3 – How to Approach

© Roz Strategies. All rights reserved.

i. Client owes $164,509 for 2002-2009ii. All other years are filed and no balances dueiii. 2002-2008 were SFRs and were assessed on 3/8/2010iv. 2009 is also an SFR and was assessed on 2/15/2011v. Original return dates for 2002-2009 per Transcripts is 5/19/2011vi. Client received “Final Notice of Intent to Levy” for all years on 8/26/2015vii. Last activity per Transcripts was a “pending” Installment Agreement on 9/20/19

Catalog Number 14169I www.irs.gov Form 9423 (Rev. 2-2020)

Form 9423 (February 2020)

Department of the Treasury - Internal Revenue Service

Collection Appeal Request (Instructions are on the reverse side of this form)

1. Taxpayer’s name 2. Representative (attach a copy of Form 2848, Power of Attorney)

4. Taxpayer’s business phone 5. Taxpayer’s home phone 6. Representative’s phone

10. ZIP code

11. Type of tax (tax form) 12. Tax periods being appealed 13. Tax due

Collection Action(s) Appealed14. Check the Collection action(s) you are appealing

Federal Tax Lien Levy or Proposed Levy Seizure

Rejection of Installment Agreement Termination of Installment Agreement Modification of Installment Agreement

Explanation15. Explain why you disagree with the collection action(s) you checked above and explain how you would resolve your tax problem.

Attach additional pages if needed. Attach copies of any documents that you think will support your position. Generally, the Internal Revenue Service Independent Office of Appeals will ask the Collection Function to review, verify and provide their opinion on any new information you submit. We will share their comments with you and give you the opportunity to respond

Under penalties of perjury, I declare that I have examined this request and any accompanying documents, and to the best of my knowledge and belief, they are true, correct and complete. A submission by a representative, other than the taxpayer, is based on all information of which the representative has any knowledge.

16. Taxpayer’s or Authorized Representative’s signature (only check one box) 17. Date signed

IRS USE ONLY18. Revenue Officer's name 19. Revenue Officer's signature 20. Date signed

21. Revenue Officer's phone 22. Revenue Officer's email address 23. Date received

24. Collection Manager’s name 25. Collection Manager’s signature 26. Date signed

27. Collection Manager’s phone 28. Collection Manager’s email address 29. Date received

JOHNNIE L. SMITH PARHAM KHORSANDI

111-11-1111 (800) 883-8301 (424) 269-2880

Los Angeles

CA 72847

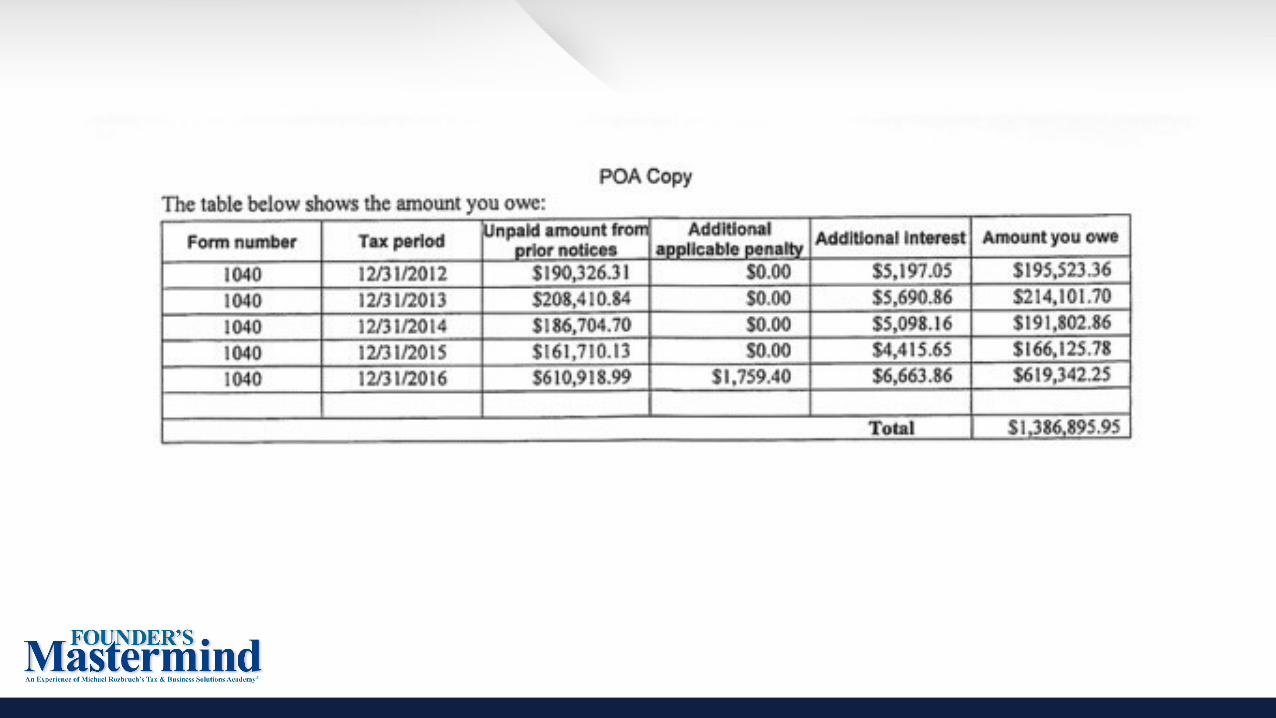

1040 2012, 2013, 2014, 2015, 2016 1,386,895.95

✖

ON AUGUST 27TH, 2021, WE HAD RECEIVED FORM 9297 FROM REVENUE OFFICER, RICHARD ANDREWS WITH A LIST OF REQUESTED DOCUMENTS AND UNREASONABLE ACTION ITEMS DUE ON SEPTEMBER 10TH, 2021. IN AN EFFORT TO PROVIDE A COMPLETE PACKAGE OF ALL DOCUMENTS AND INFORMATION REQUESTED ON FORM 9297 TO RO ANDREWS, WE HAD MADE A REQUEST FOR A 2 WEEK DEADLINE EXTENSION. THIS REQUEST WAS DENIED SOLEY BECAUSE IT WAS MADE 2 DAYS BEFORE THE DEADLINE. WITHIN THE TWO WEEKS OF INITIALLY RECEIVING FORM 9297, WE HAD BEEN WORKING CLOSELY WITH THE TAXPAYER TO GATHER THE REQUIRED INFORMATION FOR FORM 433-A, ALONG WITH SUPPORTING DOCUMENTS SUCH AS SIX MONTHS OF BANK STATEMENTS, PAYSTUBS, AND OTHER SUBSTANTIATION. THE TAXPAYER WORKS LONG HOURS AND DOES NOT HAVE MUCH FLEXIBILITY TO TAKE TIME AWAY FROM WORK THROUGHOUT THE WEEK. REVENUE OFFICER ANDREWS DID NOT FIND THESE CIRCUMSTANCES TO BE PREMISE FOR AN EXTENSION.

✖

3. SSN/EIN

7. Taxpayer’s street address14525 London Ave

8. City 9. State

Catalog Number 14169I www.irs.gov Form 9423 (Rev. 2-2020)

Instructions for Form 9423, Collection Appeal RequestFor Liens, Levies, Seizures, and Rejection, Modification or Termination of Installment AgreementsA taxpayer, or third party whose property is subject to a collection action, may appeal the following actions under the Collection Appeals Program (CAP):

a. Levy or seizure action that has been or will be taken.b. A Notice of Federal Tax Lien (NFTL) that has been or will be filed.c. The filing of a notice of lien against an alter-ego or nominee's property.d. Denials of requests to issue lien certificates, such as subordination, withdrawal, discharge or non-attachment.e. Rejected, proposed for modification or modified, or proposed for termination or terminated installment agreements.f. Disallowance of taxpayer's request to return levied property under IRC 6343(d).g. Disallowance of property owner's claim for return of property under IRC 6343(b).

How to Appeal If You Disagree With a Lien, Levy, or Seizure Action1. If you disagree with the decision of the IRS employee, and wish to appeal, you must first request a conference with the employee's

manager. If you do not resolve your disagreement with the Collection manager, submit Form 9423 to request consideration by Appeals. Let the Collection office know within two (2) business days after the conference with the Collection manager that you plan to submit Form 9423. The Form 9423 must be received or postmarked within three (3) business days of the conference with the Collection manager or collection action may resume.

Note: If you request an appeal after IRS makes a seizure, you must appeal to the Collection manager within 10 business days after the Notice of Seizure is provided to you or left at your home or business.

2. If you request a conference and are not contacted by a manager or his/her designee within two (2) business days of making the request, you can contact Collection again or submit Form 9423. If you submit Form 9423, note the date of your request for a conference in Block 15 and indicate that you were not contacted by a manager. The Form 9423 should be received or postmarked within four (4) business days of your request for a conference as collection action may resume.

3. On the Form 9423, check the collection action(s) you disagree with and explain why you disagree. You must also explain your solution to resolve your tax problem. Submit Form 9423 to the Collection office involved in the lien, levy or seizure action.

4. In situations where the IRS action(s) are creating an economic harm or you want help because your tax problem has not been resolved through normal channels, you can reach the Taxpayer Advocate Service at 877-777-4778.

How to Appeal An Installment Agreement Which Has Been Rejected, Proposed for Modification or Modified, or Proposed for Termination or Terminated

1. If you disagree with the decision regarding your installment agreement, you should appeal by completing a Form 9423, Collection Appeal Request.

2. You should provide it to the office or revenue officer who took the action regarding your installment agreement, within 30 calendar days.Note: A managerial conference is not required. However, it is strongly recommended a conference be held with the manager whenever possible.Important: Never forward your request for an Appeals conference directly to Appeals. It must be submitted to the office which took the action on your installment agreement.

What Will Happen When You Appeal Your CaseNormally, we will stop the collection action(s) you disagree with until your appeal is settled, unless we have reason to believe that collection or the amount owed is at risk.

You May Have a RepresentativeYou may represent yourself at your Appeals conference or you may be represented by an attorney, certified public accountant or a person enrolled to practice before the IRS. If you want your representative to appear without you, you must provide a properly completed Form 2848, Power of Attorney and Declaration of Representative. You can obtain Form 2848 from your local IRS office, by calling 1-800-829-3676, or by going to www.irs.gov.

Decision on the AppealOnce Appeals makes a decision regarding your case, that decision is binding on both you and the IRS. You cannot obtain a judicial review of Appeals' decision following a CAP. However, there may be other opportunities to obtain administrative or judicial review of the issue raised in the CAP hearing. For example, a third party may contest a wrongful levy by filing an action in district court. See Publication 4528, Making an Administrative Wrongful Levy Claim Under Internal Revenue Code (IRC) Section 6343(b).Note: Providing false information, failing to provide all pertinent information or fraud will void Appeals' decision.

Refer to Publication 594, The IRS Collection Process, and Publication 1660, Collection Appeal Rights, for more information regarding the Collection Appeals Program. Copies of these publications can be obtained online at www.irs.gov.

The information requested on this Form is covered under Privacy Acts and Paperwork Reduction Notices which have already been provided to the taxpayer.

Privacy Act