Embed Size (px)

Citation preview

1

Enhanced Loss Mitigation Strategy

October 21, 2014

2

Our Mission:

Minnesota Housing finances affordable housing for low- and moderate-income households while fostering strong communities.

3

Enhanced Loss Mitigation Strategy

Goal: To develop a new strategic loss mitigation approach to reduce

foreclosure losses and increase the number and success rate of permanent,

affordable loan modifications among identified high loss, high risk delinquent

loans.

4

Whole Loan Portfolio CharacteristicsJune, 2012

• Portfolio size: 14,426 loans, $1.320 Billion• Last origination in September, 2009• 58% Government, 42% Conventional• DQ rate of 6.91%, spiked at 8.85% by year end• FC rate of .67 ran up to 2.2% by Feb, 2013• Net losses on Conventional loans averaging

$54,919, $65,900 in some neighborhoods

5

2009 – 2012 Loss Mitigation Program

• US Bank as local sub servicer since 2005• Loan Modification Tools:– 0% Deferral loans– Capitalization of past interest– Extended maturity– Interest rate reductions

• Modification success rate- 71% current

6

7

Research: Locations of High Loss Loans

• Narrowed to 2009 – 2011 period as most like current market conditions

• 708 total loans with booked loss, analysis focused on top 20%

• Mapped by zip code, fell into largely inner city neighborhoods

• Cross referenced with market data on high price decline areas

8

Metro Areas with High Average

Booked Loss and Significant Home

Sales Price Declines

9

Research: Added Risk Characteristics

• Conventional (insured or uninsured)• Originated between 2003 and 2007• Between $100,000 and $200,000• Used Entry Cost Assistance

10

Research: Booked Losses

• Loans in price decline area showed a 61% higher loss

• Loans in price decline areas + risk characteristics = added 44% higher loss

• 30% of all losses were from price decline areas + risk characteristics

• 72% probability that a loss for loans in decline areas + risk characteristics – over $50K

11

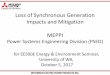

Developing ELMS

• Form a target list, applied location/risk characteristics to current 60 day + DQ and FC

• Review US Bank’s current collections and loss mitigation processes

• ELMS “Specialist” concept, embed at US Bank• Use new contact, communication, and

counseling techniques• Added Principal Reduction (capped @ 90% of

projected REO loss), and offer aggressively

12

US Bank’s Role

• Positive “partner attitude”• Experience with our portfolio and mission• Joint development of criteria and process• Willingness to integrate Specialist role and

authority

13

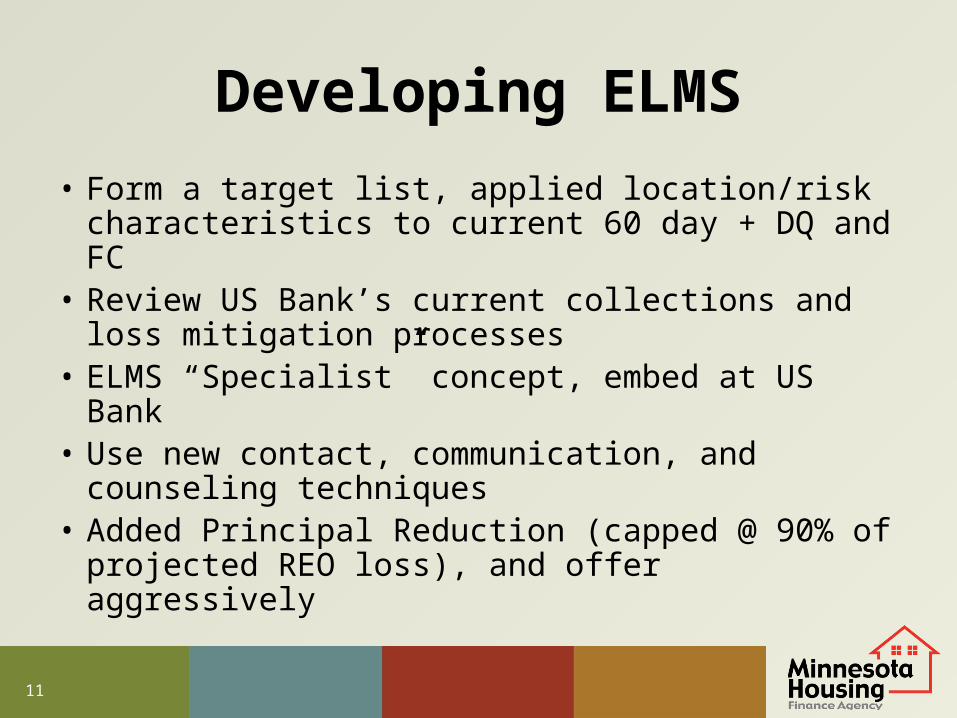

ELMS Results

• 2 phase program, 350 total eligible borrowers• Program term August 1, 2012 to December

31,2013 (Ph 2 launched May 1, 2013)• 17 brought current w/out modification• 108 received a modification (48 with PR), 77%

still current• PR investment $1.6 million, saved $2.4 million

in proj REO loss

14

Takeaways

• Personal contact key in gaining borrower commitment

• Principal Reduction gave borrowers a “fresh start”

• Impact of Specialist counseling skills• Mission impact for urban neighborhoods