Embed Size (px)

Citation preview

1

Ee

Demands on Our Coal IndustryMaking the Case for 55 Foot Channels

Bruce A. HartshornHampton Roads Navigational Summit April 4, 2012

2

Forward-Looking Statements

Statements in this presentation which are not statements of historical fact are “forward-looking statements” within the Safe

Harbor provision of the Private Securities Litigation Reform Act of 1995. Such statements are not guarantees of future

performance. Many factors could cause our actual results, performance or achievements, or industry results, to be materially

different from any future results, performance or achievements expressed or implied by such forward looking-statements.

These factors are discussed in detail in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and in our other

filings with the SEC. We make forward-looking statements based on currently available information, and we assume no

obligation to update the statements made today or contained in our Annual Report or other filings due to changes in

underlying factors, new information, future developments, or otherwise, except as required by law.

Third Party Information

This presentation, including certain forward-looking statements herein, include information obtained from third party sources

that we believe to be reliable. However, we have not independently verified this third party information and cannot assure you

of its accuracy or completeness. While we are not aware of any misstatements regarding any third party data contained in

this presentation, such data involve risks and uncertainties and are subject to change based on various factors, including

those discussed detail in our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q and in our other filings with the

SEC. We assume no obligation to revise or update this third party information to reflect future events or circumstances.

Legal Disclaimers

3

• DTA - owned by Alpha Natural Resources, Peabody Energy and Arch Coal

• Pier IX - owned by Kinder Morgan Terminals• CSX provides rail service to both

Dominion Terminal Associates and Pier IX Terminal, Newport News, VA Lambert’s Point Terminal, Norfolk, VA

• Norfolk Southern owns and provides rail service

Hampton Roads Coal

Terminals

Coal to Hampton Roads primarily originates in Central Appalachia - Virginia, West Virginia, and Kentucky

4

1936

1938

1940

1942

1944

1946

1948

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

Historic Coal Exports in Hampton RoadsM

illio

n S

hort

Tons

1957: 52 million

1970: 48 million

1991: 59 million

2011:42.2 million

1980: 50 million

5

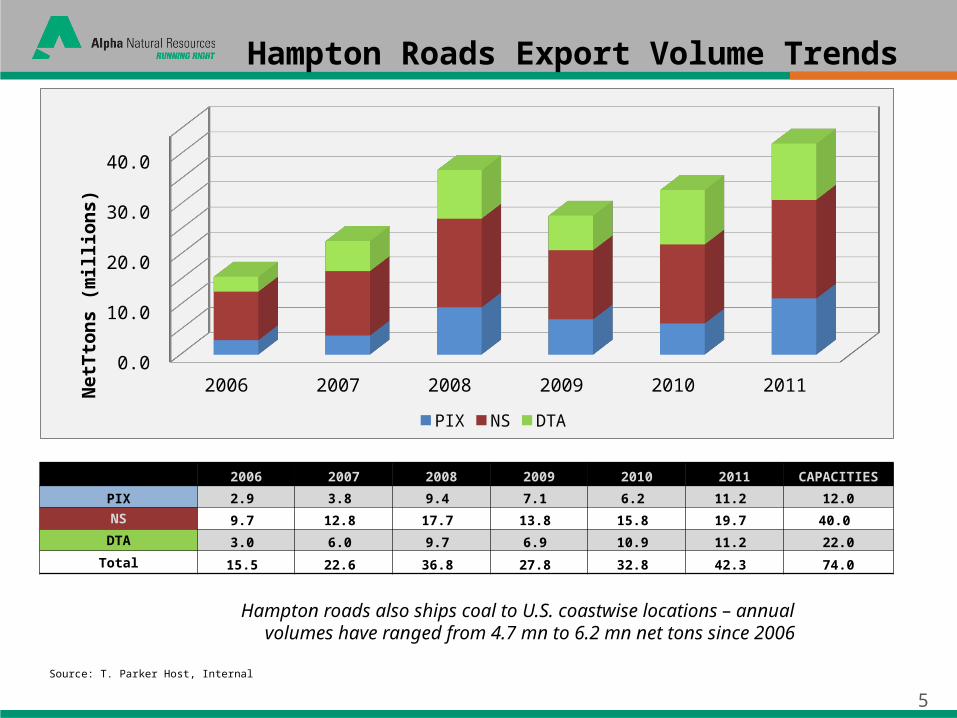

Hampton Roads Export Volume Trends

Hampton roads also ships coal to U.S. coastwise locations – annual volumes have ranged from 4.7 mn to 6.2 mn net tons since 2006

2006 2007 2008 2009 2010 2011 CAPACITIES

PIX 2.9 3.8 9.4 7.1 6.2 11.2 12.0NS 9.7 12.8 17.7 13.8 15.8 19.7 40.0

DTA 3.0 6.0 9.7 6.9 10.9 11.2 22.0

Total 15.5 22.6 36.8 27.8 32.8 42.3 74.0

Source: T. Parker Host, Internal

2006 2007 2008 2009 2010 20110.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0

PIX NS DTA

NetTtons

(millions

)

6

Hampton Roads Exports by Coal Type

• Metallurgical volumes more than doubled from 2006, on strength in international steel markets and propelled by strong growth in Asia

• Steam volumes generally trending up on increasing world coal demand

2006 2007 2008 2009 2010 20110.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

0.0 2.1

8.7 6.6

4.5

8.5

15.5

20.5

28.1

21.1

28.4

33.6

Steam Metallurgical

Net

To

ns

(mill

ion

s)

Source: T. Parker Host, Internal

7

Hampton Roads Top Ten Export Countries - 2006 vs. 2011

2006 SHIPMENTS (mn net tons) ITALY 3.4 BRAZIL 2.5 BELGIUM 1.8 UNITED KINGDOM 1.7 FRANCE 1.1 INDIA .8 SPAIN .7 TURKEY .7 EGYPT .6 SWEDEN .4

Source: T. Parker Host, Internal

ITALY25%

BRAZIL19%

BELGIUM13%

UNITED KINGDOM12%

FRANCE8%

INDIA6%

SPAIN5%

TURKEY5%

EGYPT4%

SWEDEN3%

2006

2011 SHIPMENTS (mm net tons) ITALY 4.9 BRAZIL 4.8 NETHERLANDS 4.6 INDIA 2.9 FRANCE 2.8 UKRAINE 2.5 KOREA 2.3 JAPAN 2.2 U.K. 1.8 TURKEY 1.7

ITALY16%

BRAZIL16%

NETHERLANDS15%

INDIA10%

FRANCE9%

UKRAINE8%

KOREA7%

JAPAN7%

U.K.6%

TURKEY5% 2011

8

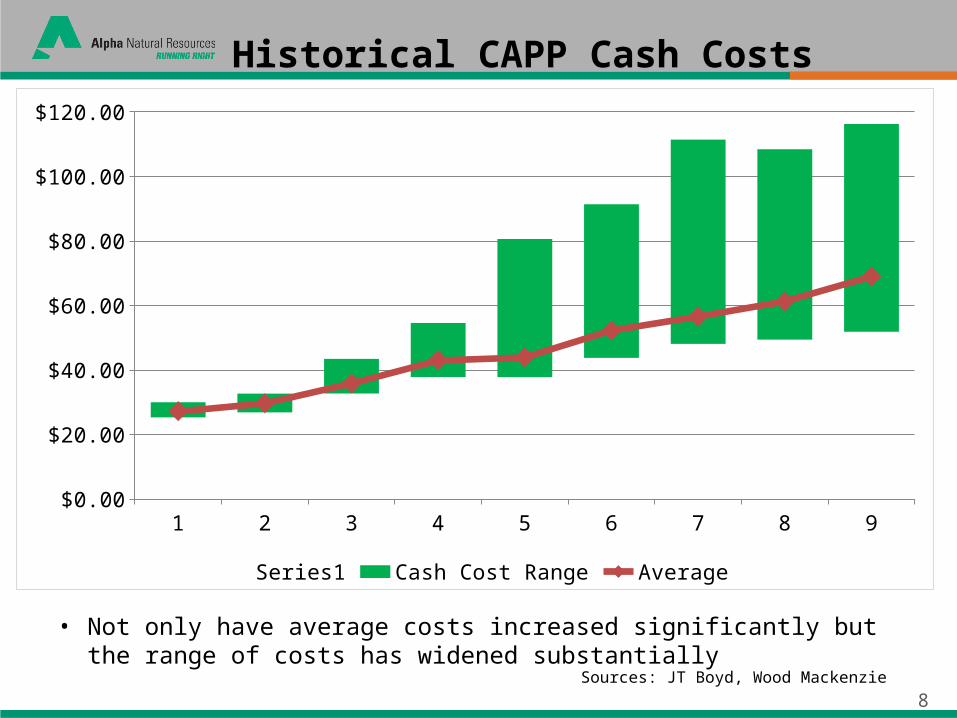

Sources: JT Boyd, Wood Mackenzie

Historical CAPP Cash Costs

Sources: JT Boyd, Wood Mackenzie

1 2 3 4 5 6 7 8 9$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

Series1 Cash Cost Range Average

• Not only have average costs increased significantly but the range of costs has widened substantially

9 Source: SSY

Capesize Fleet (150-180,000 dwt) by Year of Build

April 2012

0.0

4.0

8.0

12.0

16.0

20.0

24.0P

re-8

51

98

51

98

61

98

71

98

81

98

91

99

01

99

11

99

21

99

31

99

41

99

51

99

61

99

71

99

81

99

92

00

02

00

12

00

22

00

32

00

42

00

52

00

62

00

72

00

82

00

92

01

02

01

12

01

22

01

32

01

42

01

5

Millio

n D

wt

150-159,999 160-169,999 170-180,000

10

M/V CAPE DOVER

Capesize VesselYear Built: 2006

LOA: 290 mBeam: 47m

185,805 MT DWT

11

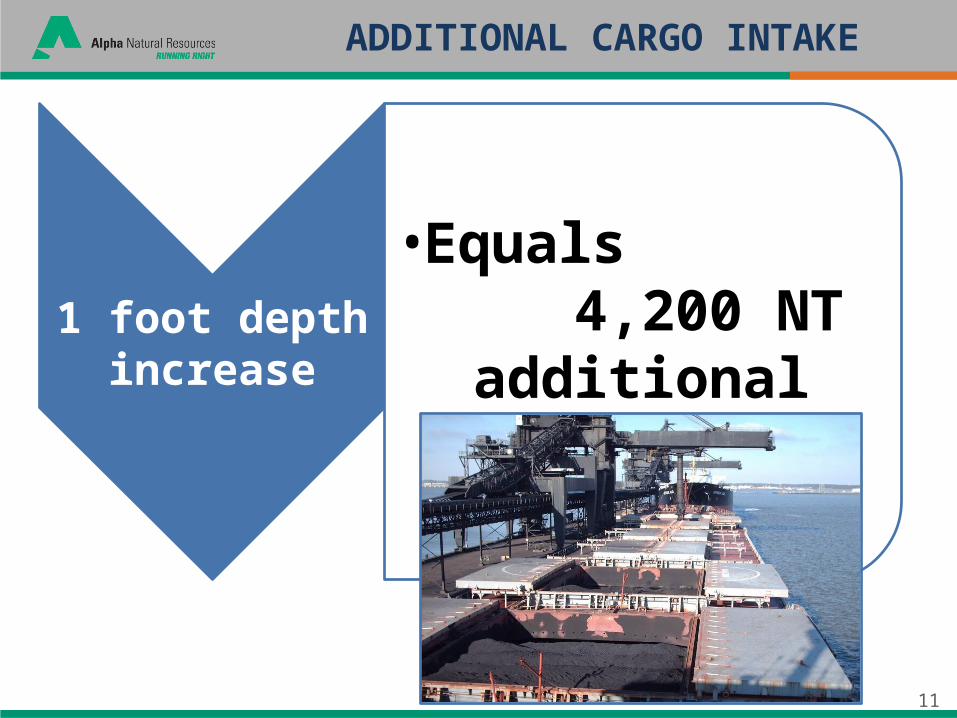

1 foot depth increase

•Equals 4,200 NT additional

cargo intake

ADDITIONAL CARGO INTAKE

12

CARGO INTAKE: M/V CAPE DOVER

55 ft: 172,017 NT

(+13.91%)

50 ft: 151,017

NT

13

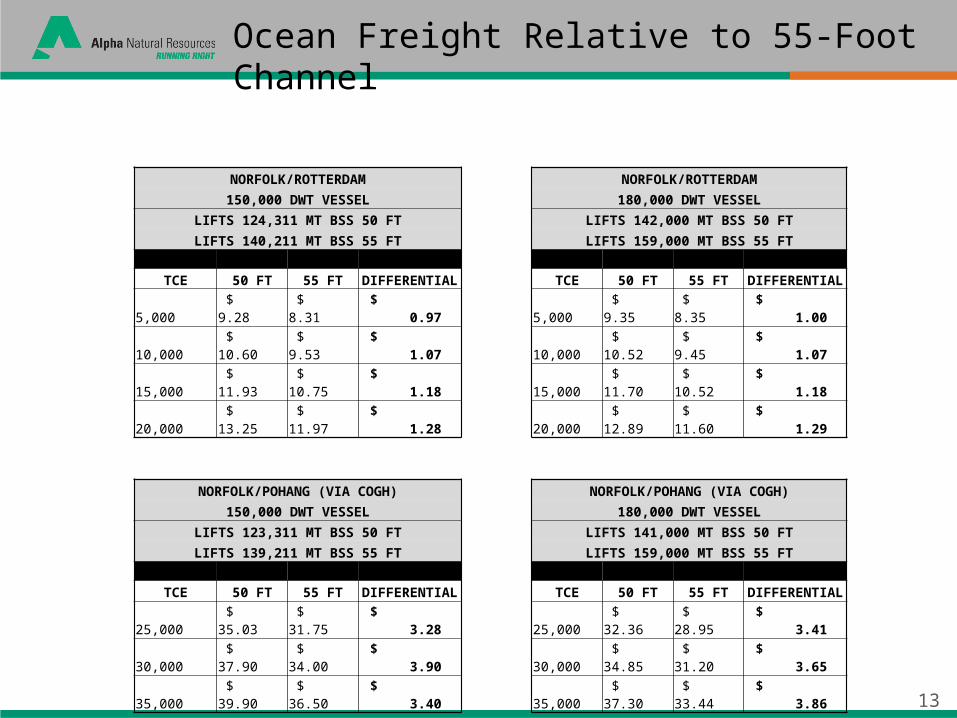

NORFOLK/ROTTERDAM NORFOLK/ROTTERDAM

150,000 DWT VESSEL 180,000 DWT VESSEL

LIFTS 124,311 MT BSS 50 FT LIFTS 142,000 MT BSS 50 FT

LIFTS 140,211 MT BSS 55 FT LIFTS 159,000 MT BSS 55 FT

TCE 50 FT 55 FT DIFFERENTIAL TCE 50 FT 55 FT DIFFERENTIAL

5,000 $ 9.28 $ 8.31 $ 0.97 5,000 $ 9.35 $ 8.35 $ 1.00

10,000 $ 10.60 $ 9.53 $ 1.07 10,000 $ 10.52 $ 9.45 $ 1.07

15,000 $ 11.93 $ 10.75 $ 1.18 15,000 $ 11.70 $ 10.52 $ 1.18

20,000 $ 13.25 $ 11.97 $ 1.28 20,000 $ 12.89 $ 11.60 $ 1.29

NORFOLK/POHANG (VIA COGH) NORFOLK/POHANG (VIA COGH)

150,000 DWT VESSEL 180,000 DWT VESSEL

LIFTS 123,311 MT BSS 50 FT LIFTS 141,000 MT BSS 50 FT

LIFTS 139,211 MT BSS 55 FT LIFTS 159,000 MT BSS 55 FT

TCE 50 FT 55 FT DIFFERENTIAL TCE 50 FT 55 FT DIFFERENTIAL

25,000 $ 35.03 $ 31.75 $ 3.28 25,000 $ 32.36 $ 28.95 $ 3.41

30,000 $ 37.90 $ 34.00 $ 3.90 30,000 $ 34.85 $ 31.20 $ 3.65

35,000 $ 39.90 $ 36.50 $ 3.40 35,000 $ 37.30 $ 33.44 $ 3.86

Ocean Freight Relative to 55-Foot Channel

14

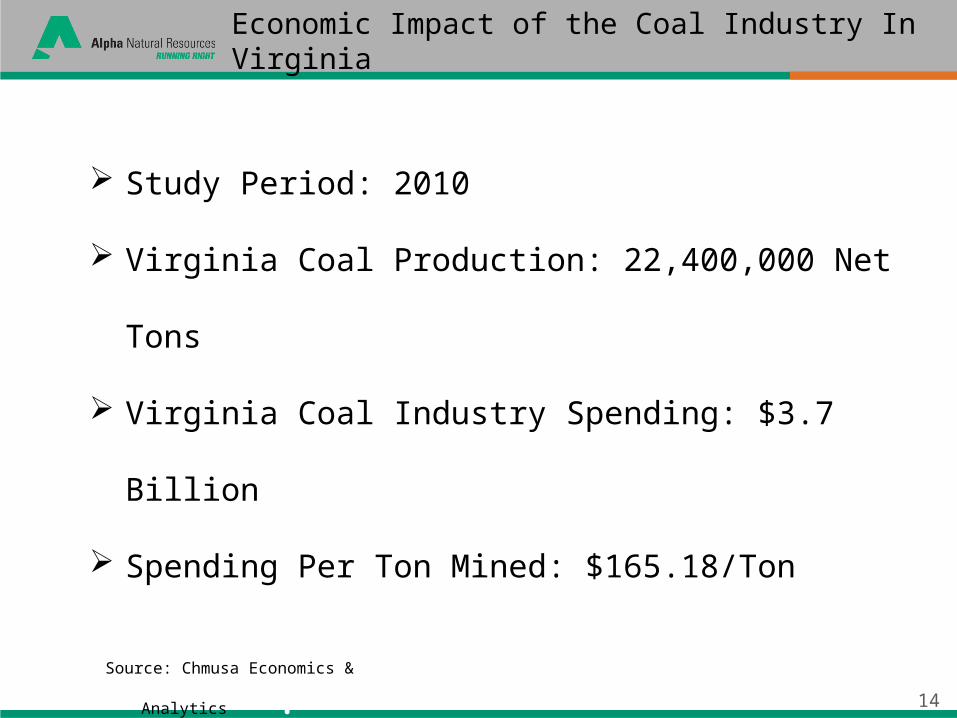

Economic Impact of the Coal Industry In Virginia

Source: Chmusa Economics & Analytics**.

*8222

Study Period: 2010

Virginia Coal Production: 22,400,000 Net Tons

Virginia Coal Industry Spending: $3.7 Billion

Spending Per Ton Mined: $165.18/Ton

15

Cost of Dredging

to 55 feet:$150,000,00

0

Potential Annual

Economic Benefit /

Destruction: $1,650,000,

000*

55-FOOT DREDGE PROJECT

*Basis 10.0 million tons

1616

www.alphanr.com