Embed Size (px)

Citation preview

1

Determinants of Capital Structure of Firms in the Manufacturing Sector of Firms

in Indonesia

Dissertation

To obtain the degree of

Doctor of Business Administration

at the Maastricht School of Management,

under authority of the Dean Director Prof. dr. Peter P. de Gijsel

to be defended in public on May, 2012

by

Siti Rahmi Utami

born in Jakarta (Indonesia)

2

Published by:

Maastricht School of Management

P.O. Box 1203

6201 BE Maastricht

The Netherlands

Siti Rahmi Utami, Determinants of Capital Structure of Firms in the Manufacturing Sector of

Firms in Indonesia. DBA Dissertation, Maastricht School of Management, Maastricht 2012. –

With references. – With summary in English.

Key words: Capital Structure/Pecking Order Theory/Trade-off Theory/Firm Life Cycle/Signalling

Theory/Asymmetric Information/Agency Cost Theory

ISBN:

Cover: Stoerebinken, The Netherlands

Printing: Gildeprint, The Netherlands

© 2012 by Siti Rahmi Utami, Maastricht School of Management. All rights reserved. No part of

this publication may be reproduced, stored in a retrieval system or transmitted in any form or by

any means, electronic, mechanical, photocopying, recording or otherwise, without prior written

permission of the publisher.

3

This dissertation is approved of by the Doctoral Supervisor:

Prof. Eno L. Inanga

Maastricht School of Management, The Netherlands

Composition of the Evaluation Committee:

Prof. Dr. Ir. E. J. de Bruijn

Twente University, The Netherlands

Prof. Dr. Geert Braam RA

4

ACKNOWLEDGEMENTS

It is with a lot of gratitude and appreciation that I acknowledge the help of my supervisor,

Professor Eno L. Inanga, who has helped me to complete this Draft DBA thesis. The Draft DBA

thesis would not have reached this stage in the present form without his help. He has given me

support throughout the entire process. I am hugely indebted to him for all the hours he spent

reading my texts, writing suggestions and comments for me, and helping me to shape my thinking

in many ways. I greatly appreciate his expertise in the field of my research.

Likewise, I would also like to express my gratefulness to Professor Dadan, from Trisakti

University, Indonesia, for his encouragement and guidance. I also owe many thanks to the

administrative support I enjoyed from the Doctoral Office at MSM, as well as the administration

office at TIBS, Indonesia, are worthy of a mention with special thanks.

I must express my profound thanks to my parents (especially my father, Professor Gani

SH), without their support, I would not have achieved this stage. Last, but not least, I would also

like to thank to my friends, I have learned many things from them.

5

TABLE OF CONTENTS

ACKNOWLEDGEMENTS ................................................................................................................ 4

EXECUTIVE SUMMARY ................................................................................................................. 9

1. INTRODUCTION ....................................................................................................................... 11

1.1 Background of the Research ............................................................................................... 11

1.1.1. The Importance of Capital Structure Theory........................................................................ 11

1.1.2. Research Motivation ............................................................................................................. 15

1.2 Problem Identification .............................................................................................................. 17

1.3 Research Questions .................................................................................................................. 19

1.3.1 Major Research Questions .................................................................................................... 19

1.3.2 Minor Research Questions .................................................................................................... 19

1.4 Research Objectives ................................................................................................................. 20

1.5 Scope and Limitation of the Study ............................................................................................ 20

1.6 Expected Contribution .............................................................................................................. 22

1.7 Organisation of the Study ......................................................................................................... 23

2. AN OVERVIEW OF THE CAPITAL STRUCTURE OF INDONESIAN MANUFACTURING

FIRMS ............................................................................................................................................ 24

2.1. Indonesian Capital Market ...................................................................................................... 24

2.1.1 History of Indonesia Stock Exchange .................................................................................... 24

2.1.2 Stock Price Index in the Indonesian Capital Market ............................................................. 24

2.1.3. Description of the LQ45 Index ............................................................................................. 26

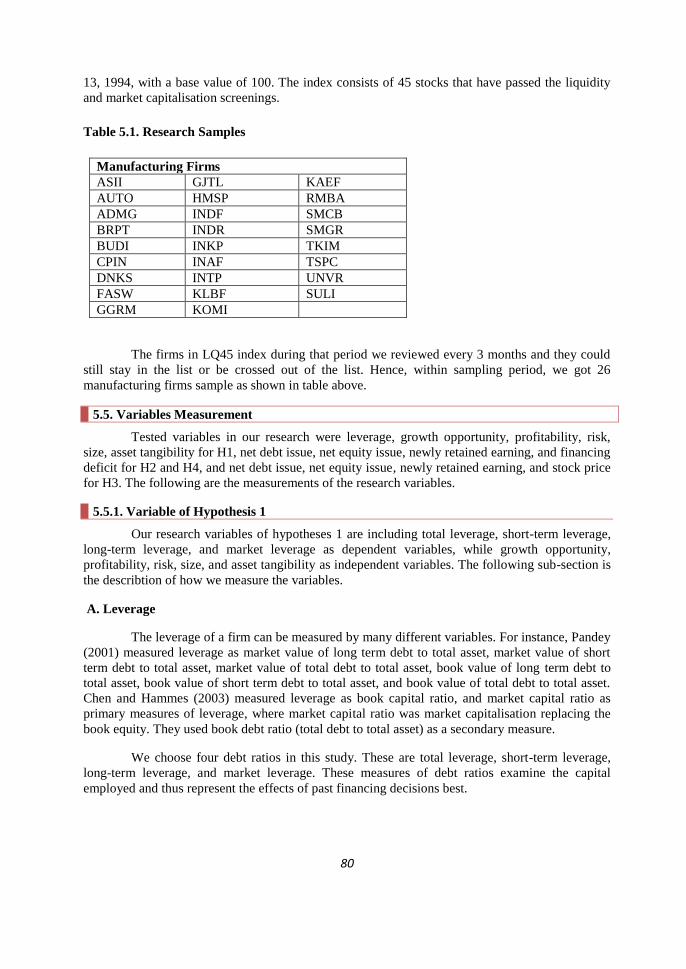

2.2. Characteristics of the Research Sample .................................................................................. 26

2.3 Leverage Analysis ..................................................................................................................... 34

3. LITERATURE REVIEW .............................................................................................................. 36

3.1 Theories of Capital Structure ................................................................................................... 36

3.1.1 Modigliani-Miller Theory ...................................................................................................... 36

3.1.2. The Capital Structure Theory ............................................................................................... 37

3.2. The Conclusions What Variables We Use for Our Research, and Why These, Theories

Predictions of the Relationship between Variables, and Some Previous Research Findings ......... 40

3.2.1 Selected Variables regarding Capital Structure for Research Question 1a, 1b, 1c, 1d, and 1e 40

6

3.2.2 Selected Variables for Research Question 2 .......................................................................... 46

3.2.3 Selected Variables for Research Question 3a, 3b, and 3c ..................................................... 48

3.2.4 Selected Variables for Research Question 4 .......................................................................... 51

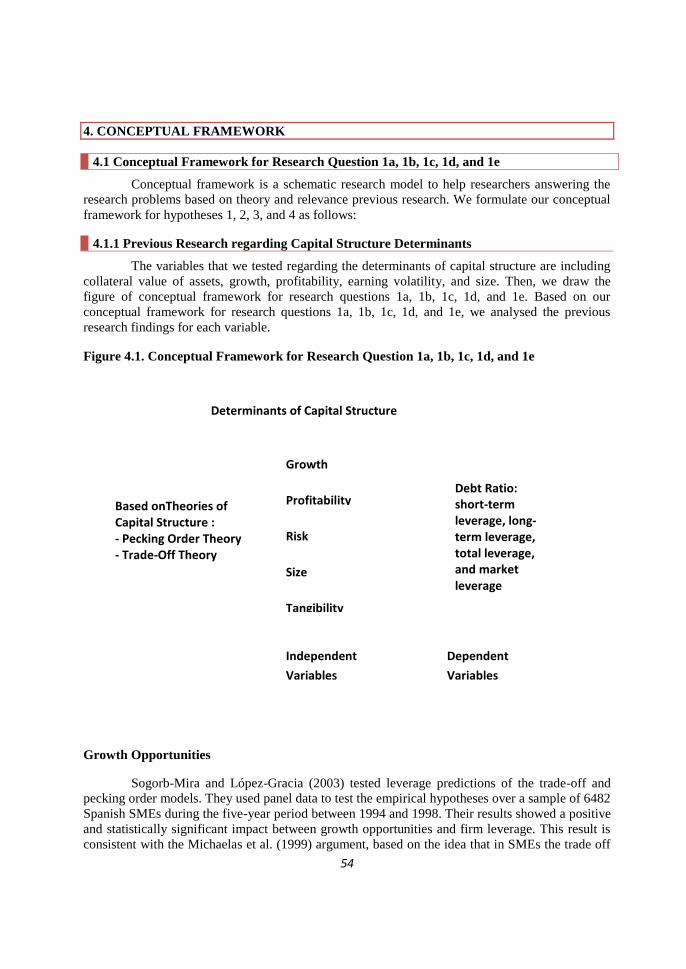

4. CONCEPTUAL FRAMEWORK ................................................................................................. 54

4.1 Conceptual Framework for Research Question 1a, 1b, 1c, 1d, and 1e .................................... 54

4.1.1 Previous Research regarding Capital Structure Determinants ............................................. 54

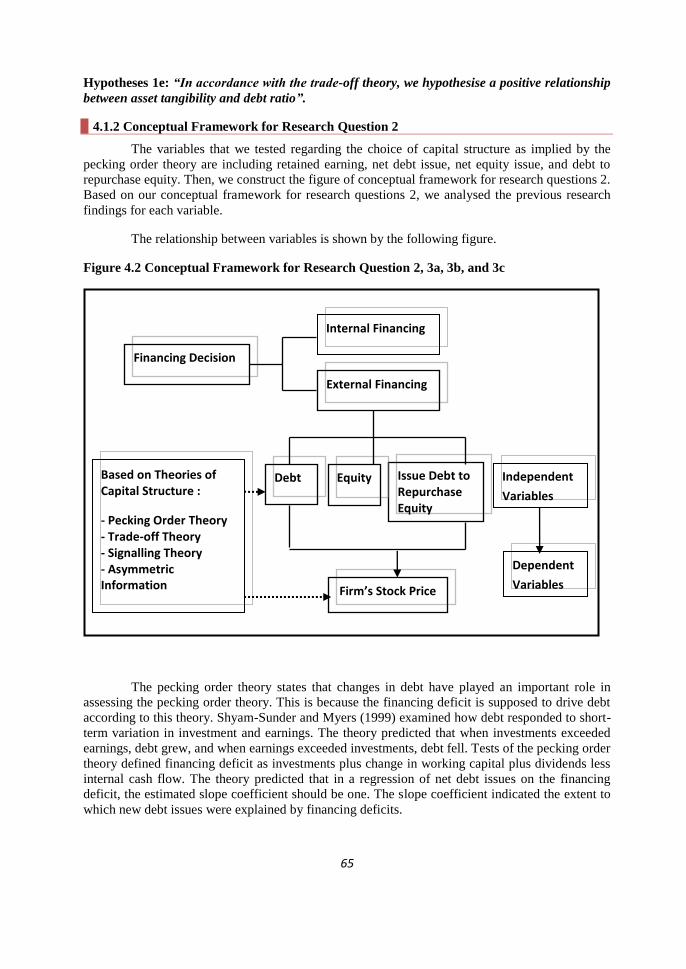

4.1.2 Conceptual Framework for Research Question 2 ................................................................. 65

4.1.3 Conceptual Framework for Research Question 3 ................................................................. 68

4.1.4 Conceptual Framework for Research Question 4 ................................................................. 72

5. RESEARCH METHODOLOGY.................................................................................................. 76

5.1 Research Design ....................................................................................................................... 76

5.2Research Strategy ...................................................................................................................... 77

5.2.1. Quantitative Strategy ............................................................................................................ 77

5.2.2. Mixed Method Strategy ......................................................................................................... 78

5.3 Data Collection ........................................................................................................................ 78

5.4. Sampling Design and Procedure ............................................................................................. 79

5.5. Variables Measurement ........................................................................................................... 80

5.5.1. Variable of Hypothesis 1 ...................................................................................................... 80

5.5.2 Measuring Variables of Hypotheses 2, 3, and 4 .................................................................... 82

5.6. Hypotheses Testing ................................................................................................................... 83

5.6.1. Hypothesis 1 .......................................................................................................................... 84

5.6.2. Hypothesis 2 ......................................................................................................................... 84

5.6.3. Hypothesis 3 ......................................................................................................................... 86

5.6.4. Hypothesis 4 ......................................................................................................................... 86

5.7. Regression Analysis ................................................................................................................. 91

A. The Un-standardised Beta Coefficients ..................................................................................... 91

B. The Standardised Beta Coefficients ........................................................................................... 91

C. Analysis of Variance (ANOVA).................................................................................................. 91

D. The Coefficient of Determination (R2) ....................................................................................... 91

E. Descriptive Statistics .................................................................................................................. 92

F. Regression Assumptions of Hypothesis 1-4 ................................................................................ 92

5.8. The Credibility of Research Findings ...................................................................................... 94

7

5.8.1 Reliability .............................................................................................................................. 94

5.8.2 Validity .................................................................................................................................. 94

5.8.3 Generalisability ..................................................................................................................... 94

5.9. The Limitations of Research Design ........................................................................................ 94

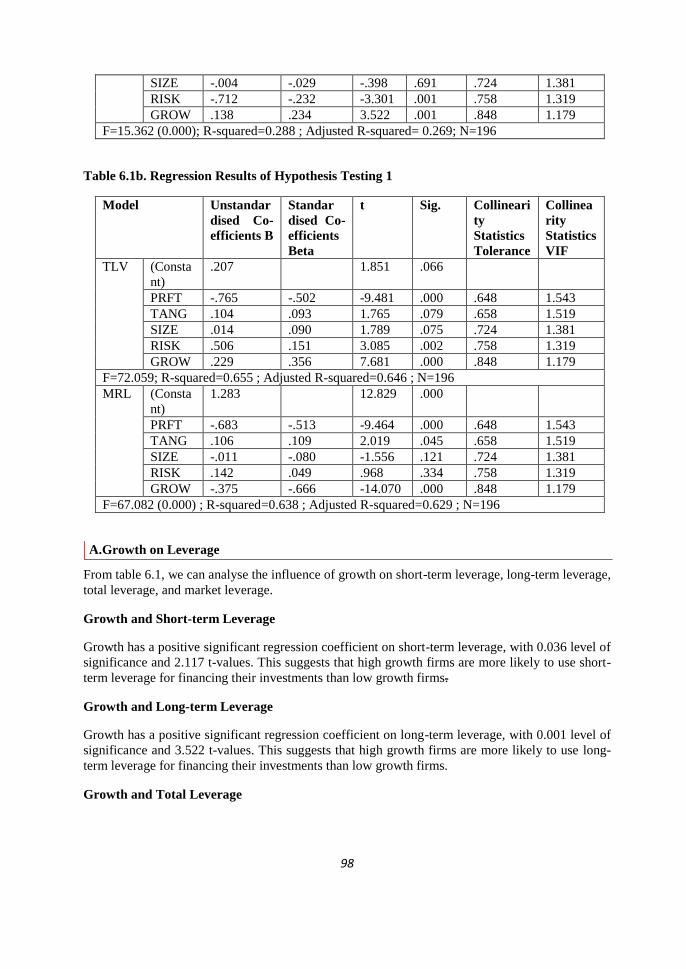

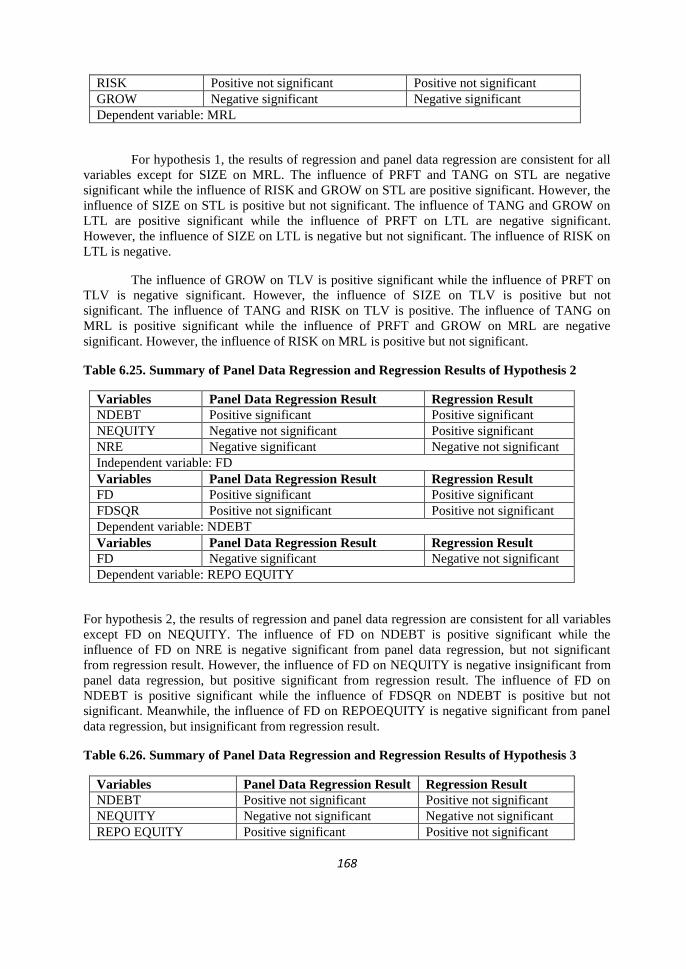

6. PRESENTATION OF DATA AND ANALYSIS OF RESULTS .................................................... 96

6.1 Research Question 1, Hypotheses, Hypotheses Testing, and Result Analysis .......................... 96

6.1.1. Research Question 1 ............................................................................................................. 96

6.1.2. Hypothesis One (H1) ............................................................................................................ 96

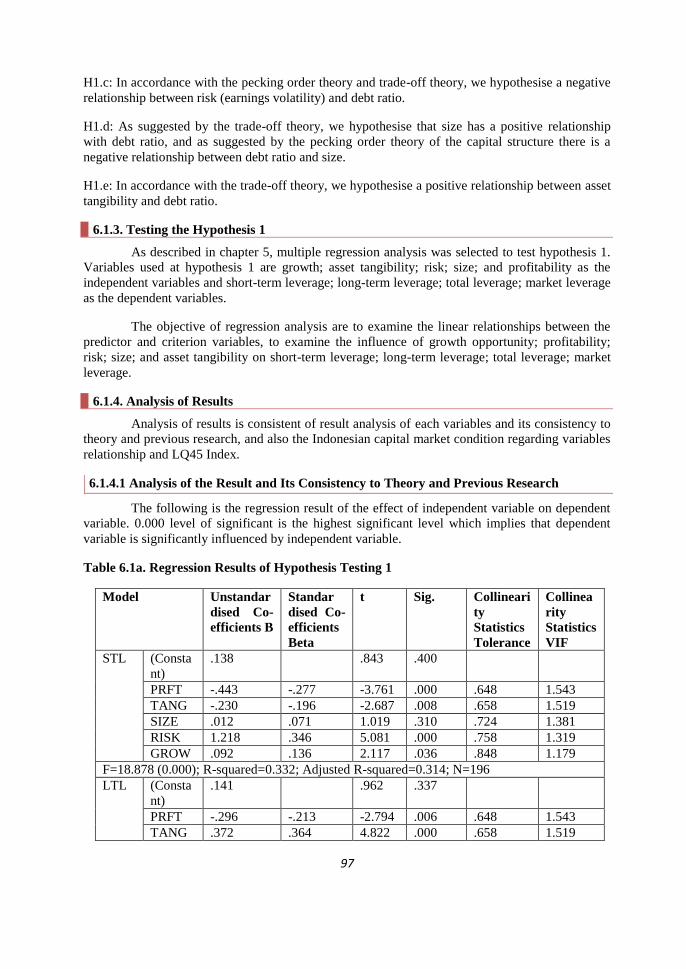

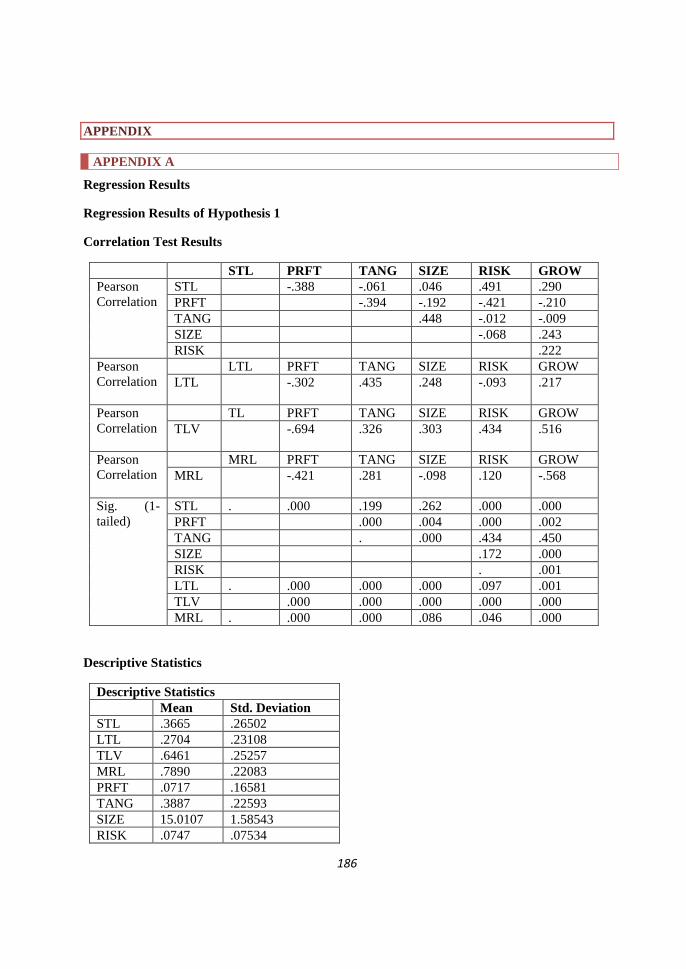

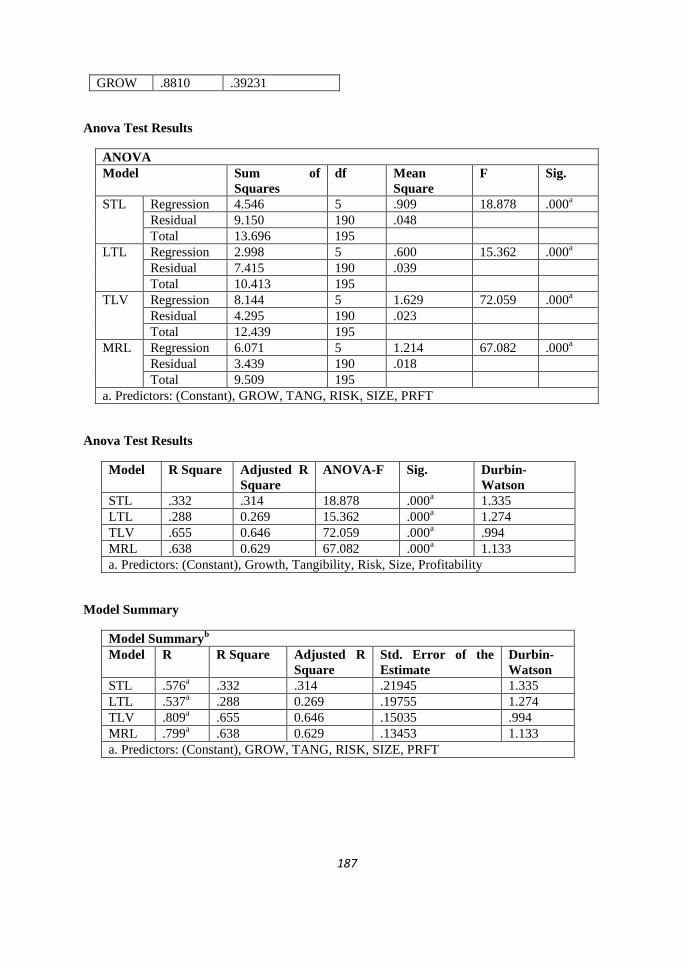

6.1.3. Testing the Hypothesis 1 ....................................................................................................... 97

6.1.4. Analysis of Results ................................................................................................................ 97

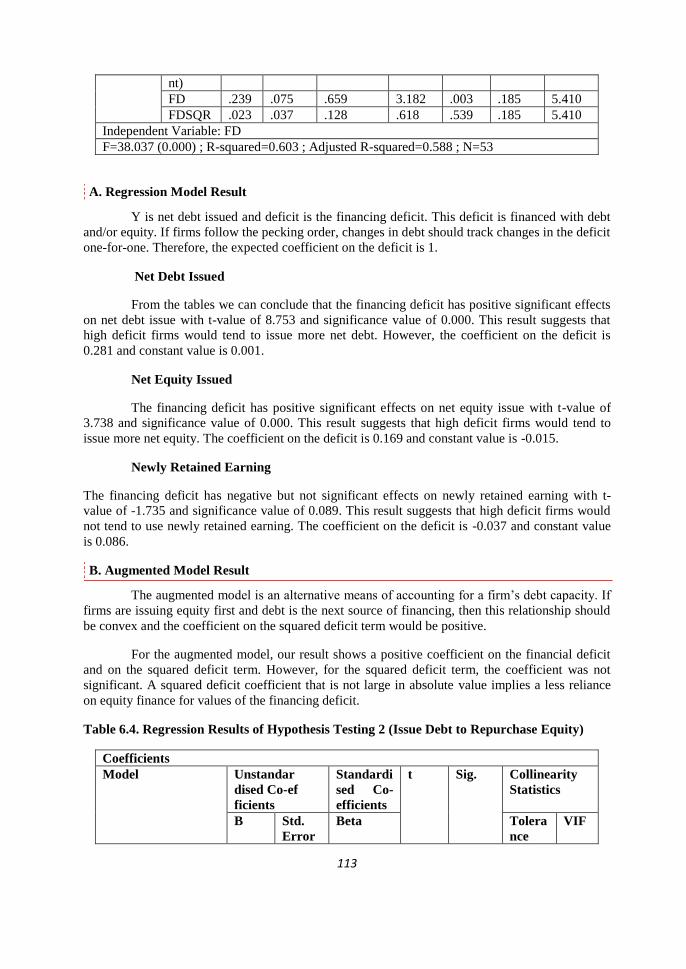

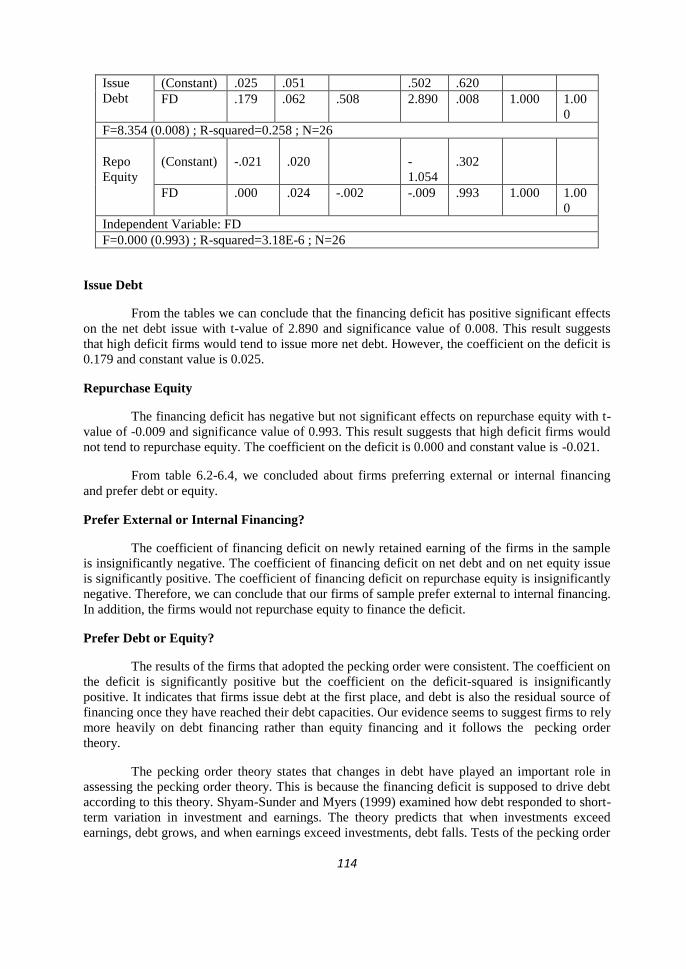

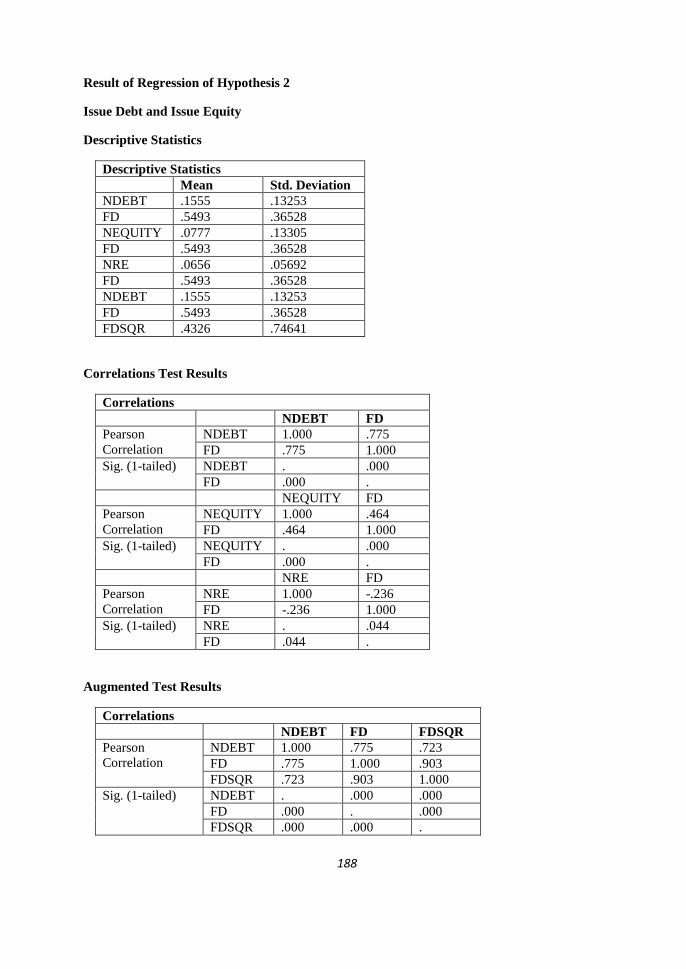

6.2. Research Question 2, Hypothesis 2, Hypothesis Testing, and Result Analysis ...................... 111

6.2.1. Research Question 2 ........................................................................................................... 111

6.2.2. Hypothesis 2 ....................................................................................................................... 111

6.2.3. Testing the Hypothesis 2 ..................................................................................................... 111

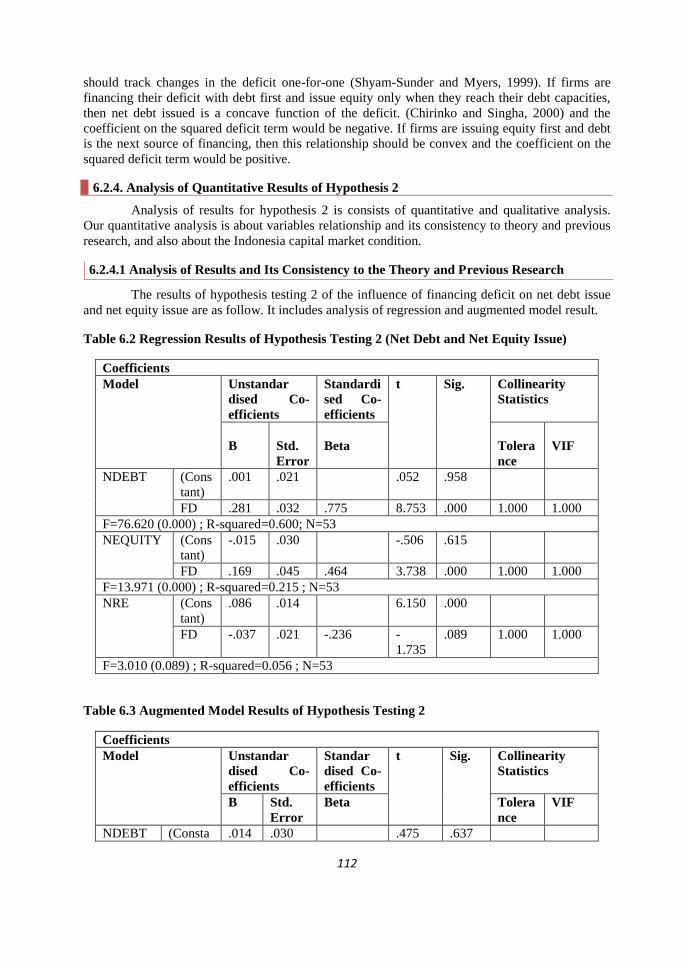

6.2.4. Analysis of Quantitative Results of Hypothesis 2 ............................................................... 112

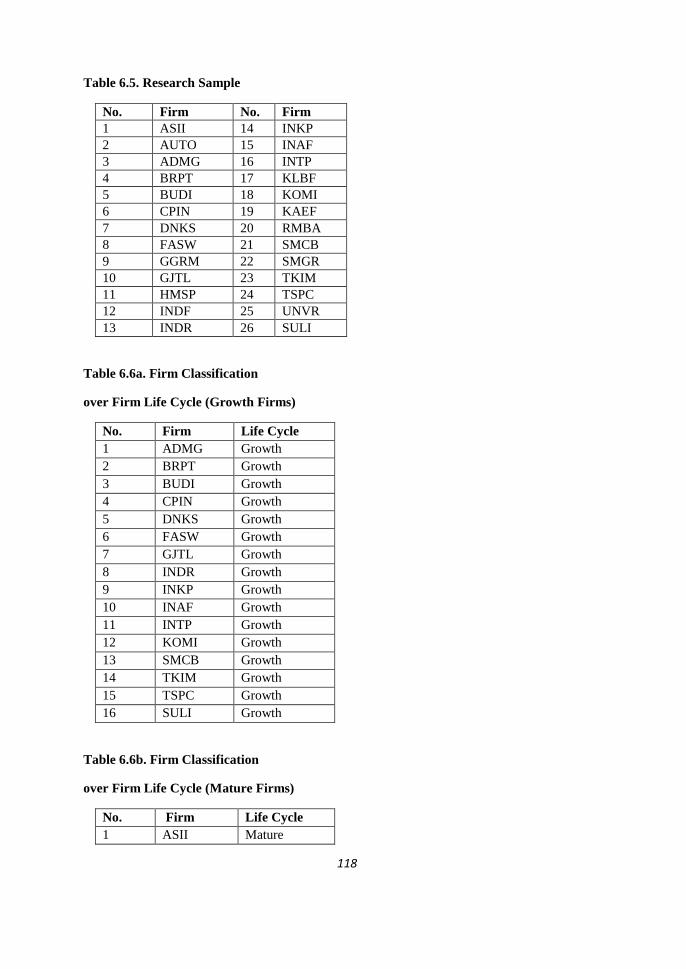

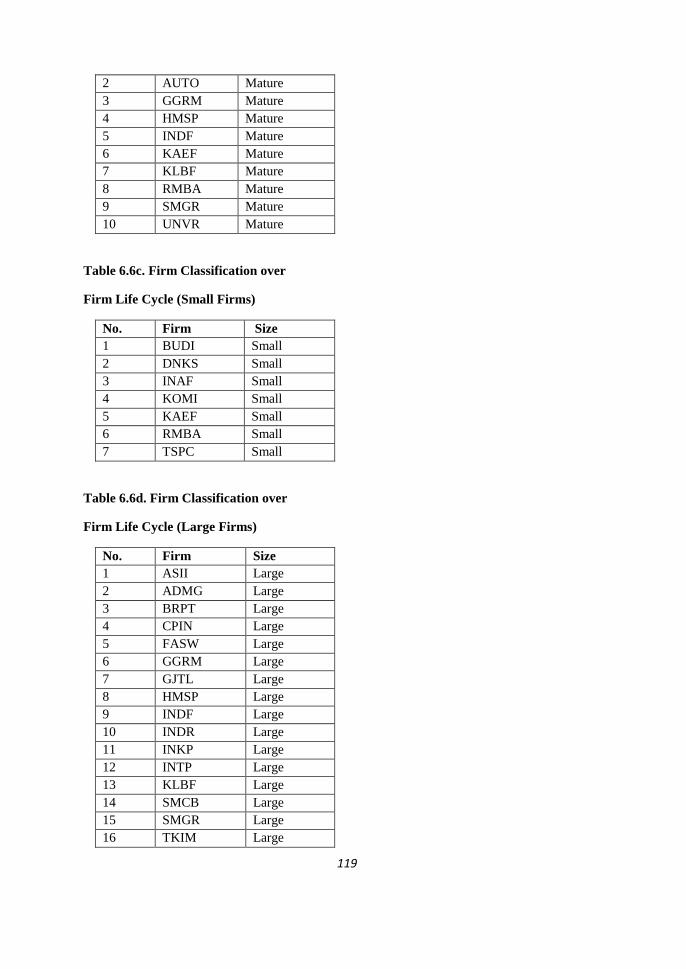

6.2.5 Qualitative Analysis of Hypothesis 2 ................................................................................... 117

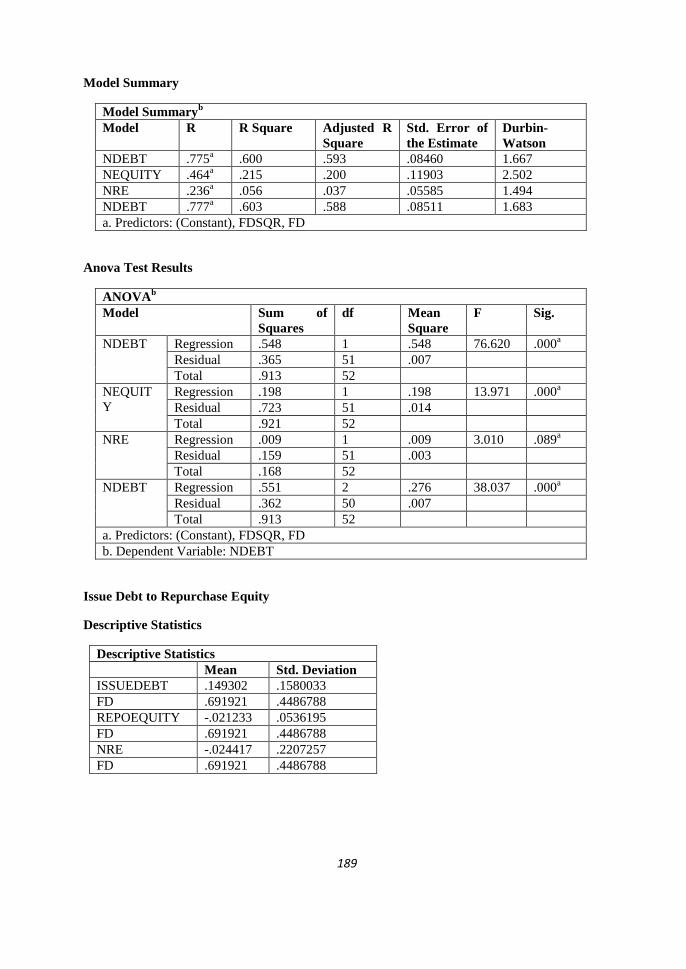

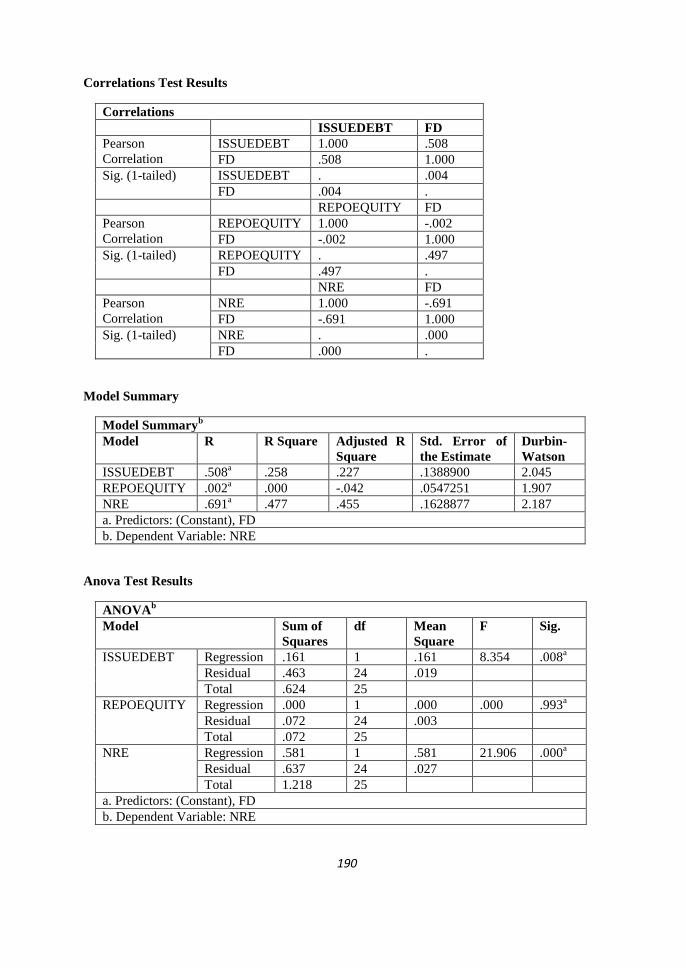

6.3. Research Question 3, Hypothesis, Hypothesis Testing, and Result Analysis ........................ 129

6.3.1. Research Question Three .................................................................................................... 129

6.3.2. Hypothesis 3 ....................................................................................................................... 129

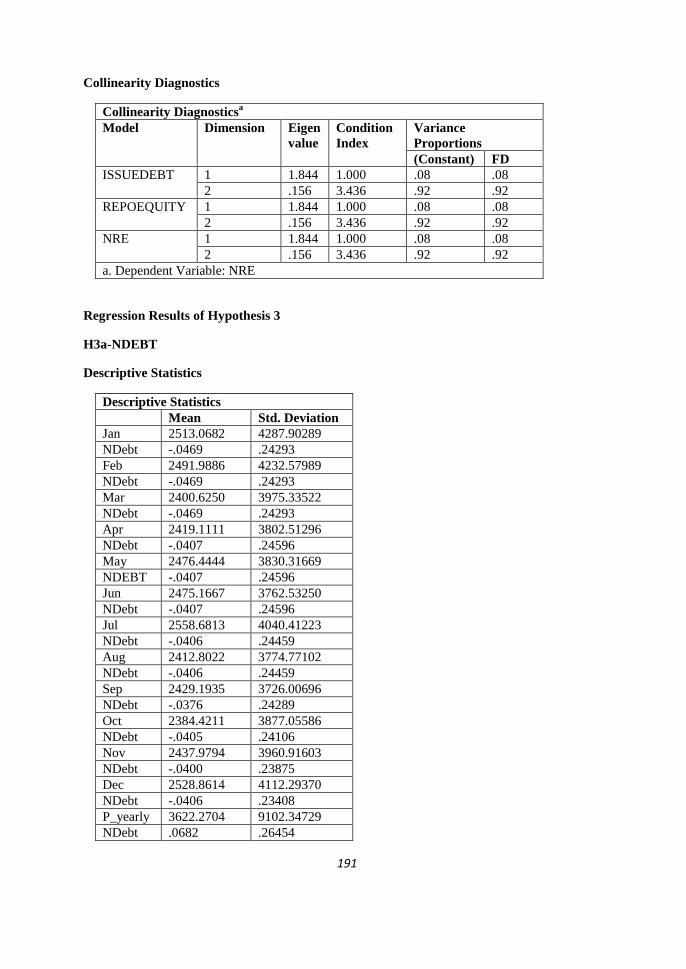

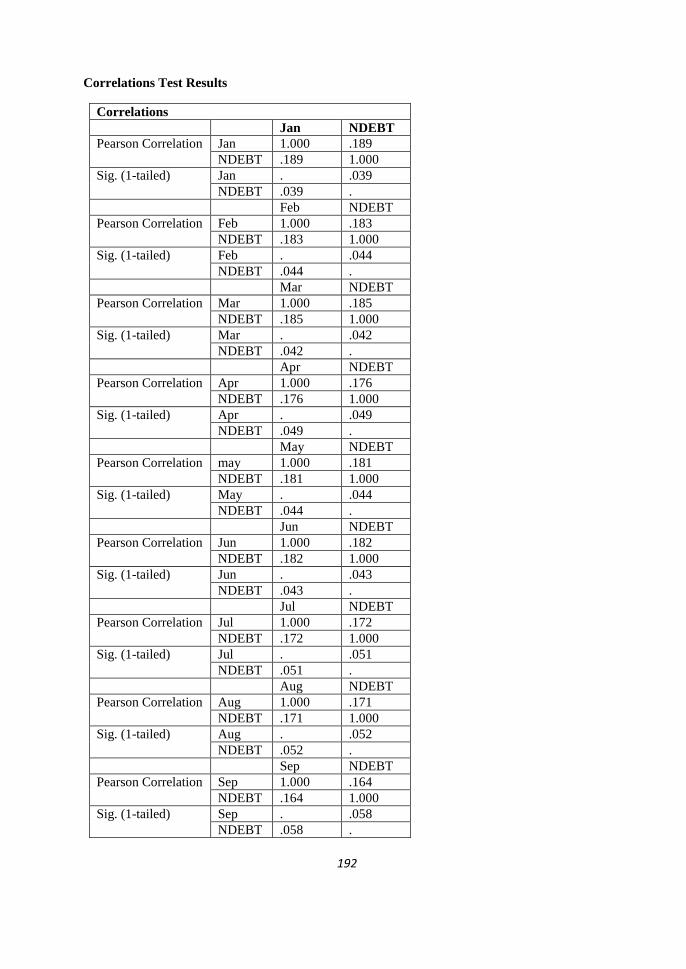

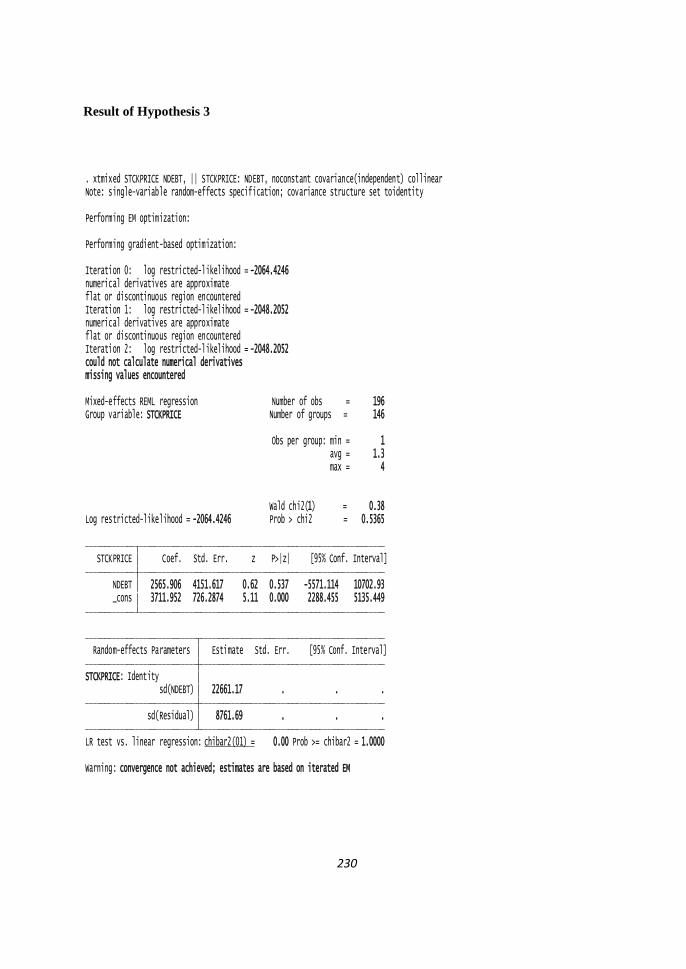

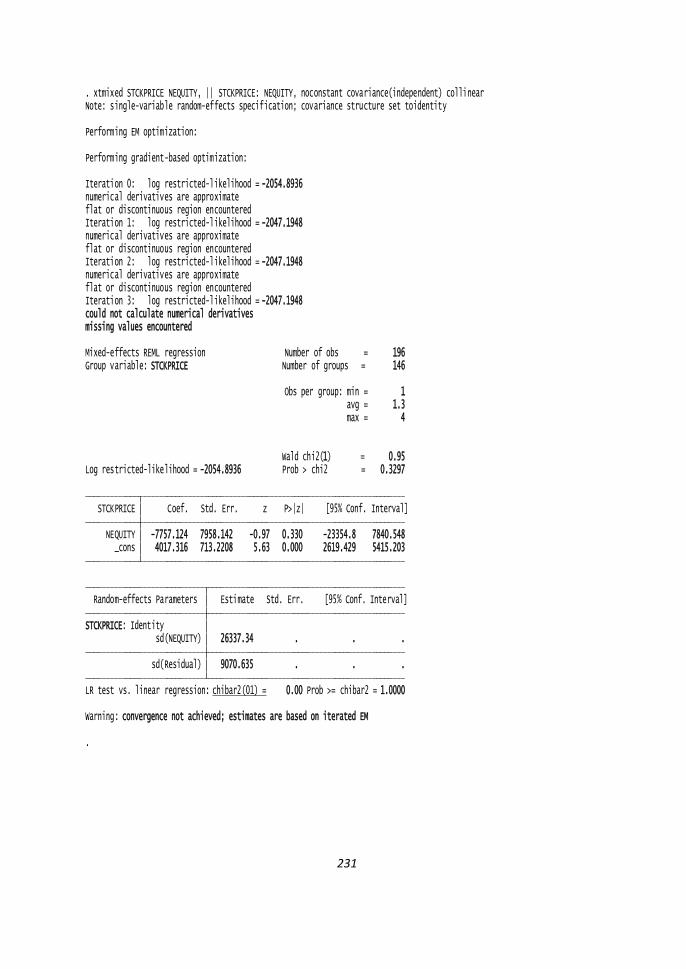

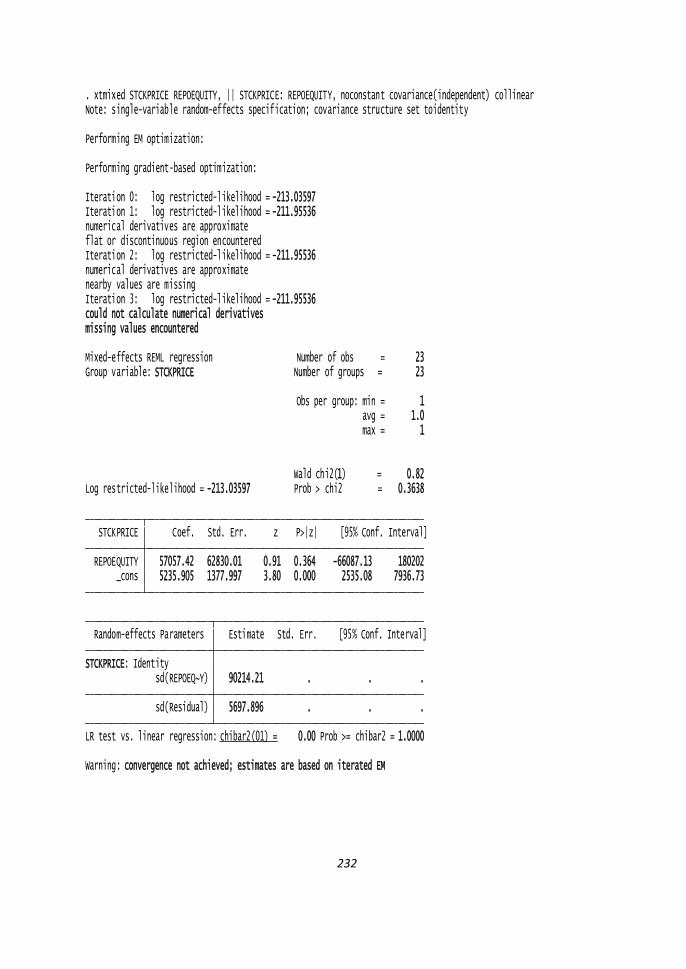

6.3.3. Testing the Hypothesis 3 ..................................................................................................... 130

6.3.4. Analysis of Results .............................................................................................................. 130

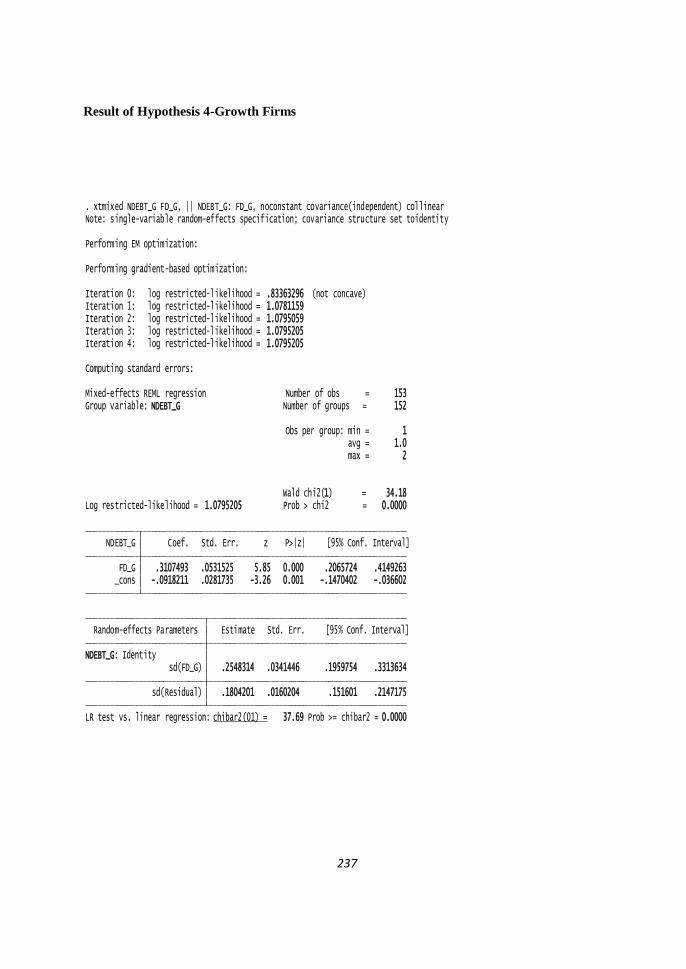

6.4. Research Question 4, Hypothesis, Hypothesis Testing, and Result Analysis ......................... 137

6.4.1. Research Question 4 ........................................................................................................... 137

6.4.2. Hypothesis 4 ....................................................................................................................... 137

6.4.3. Testing Hypothesis 4 ........................................................................................................... 137

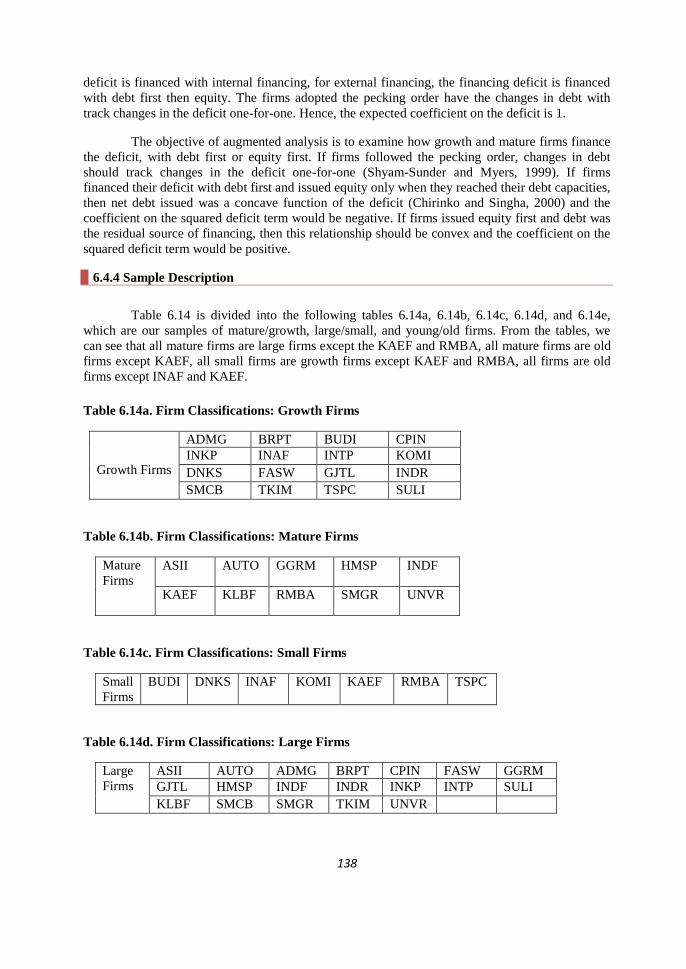

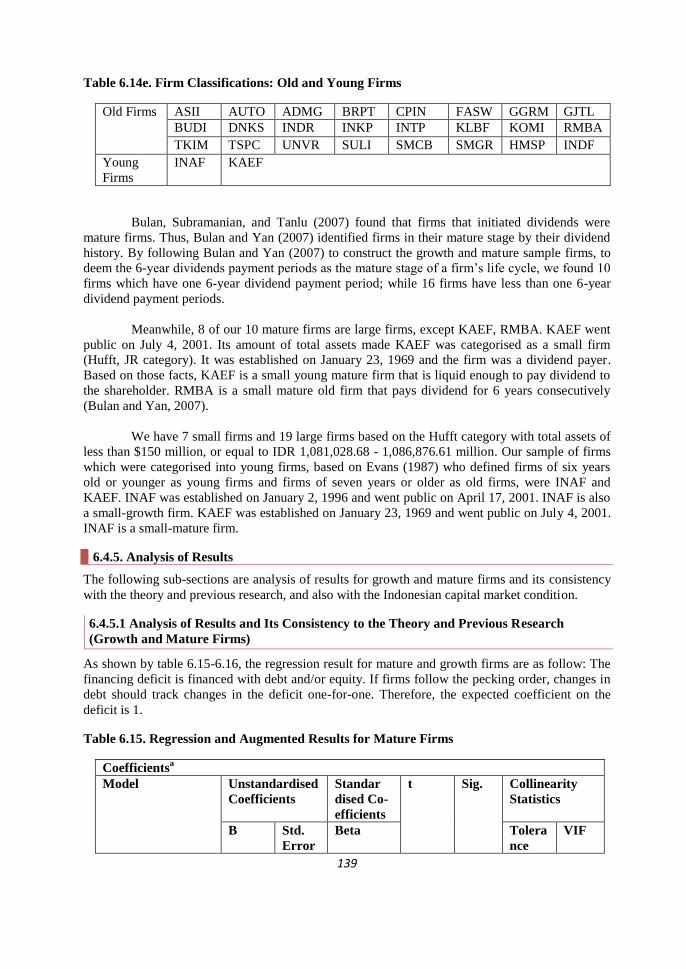

6.4.4 Sample Description ............................................................................................................. 138

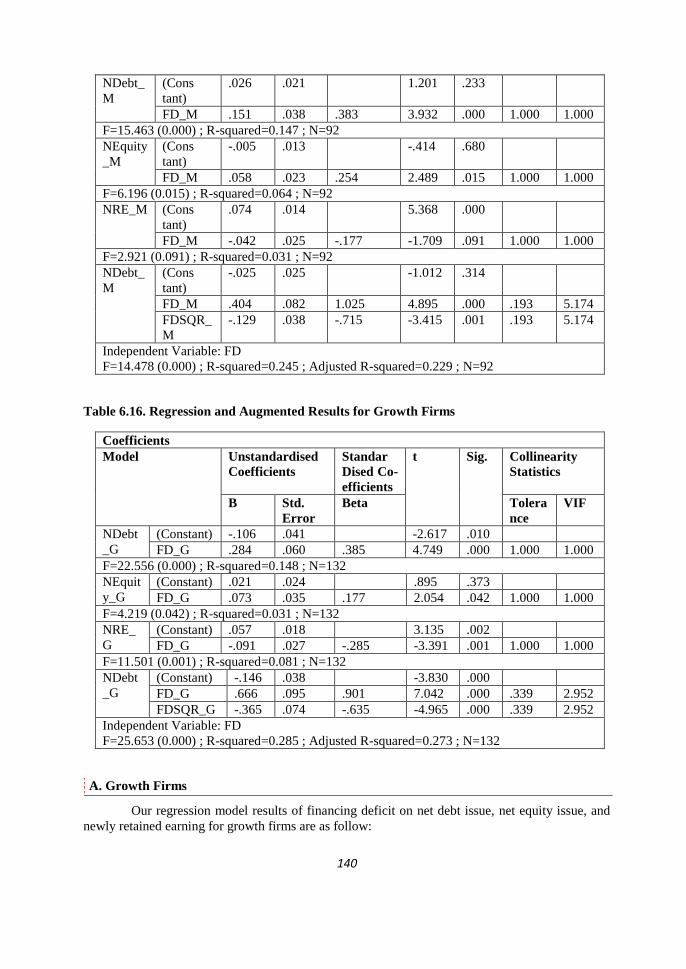

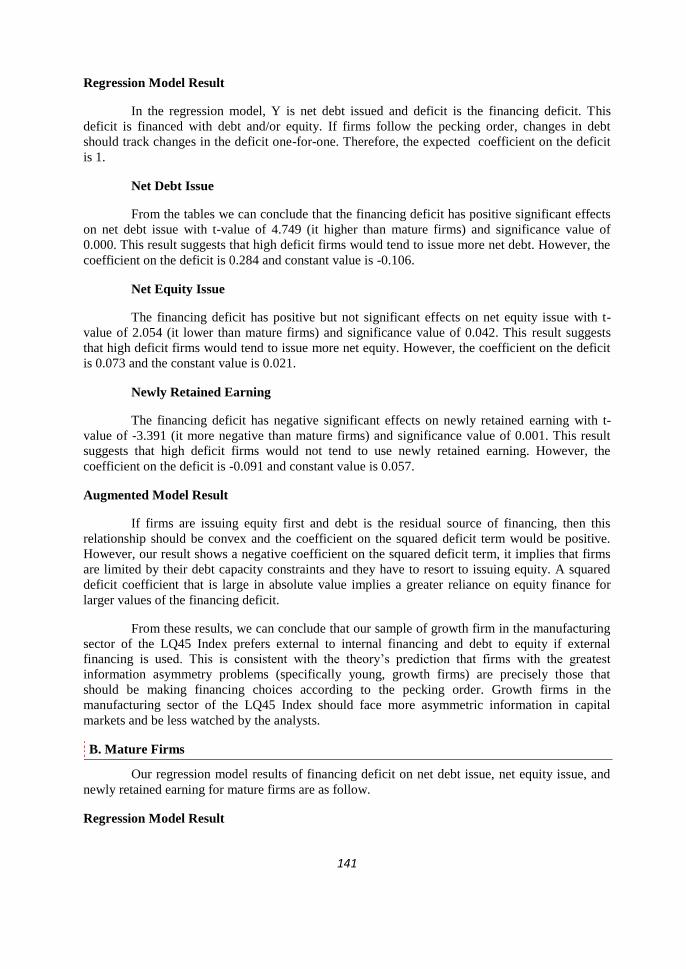

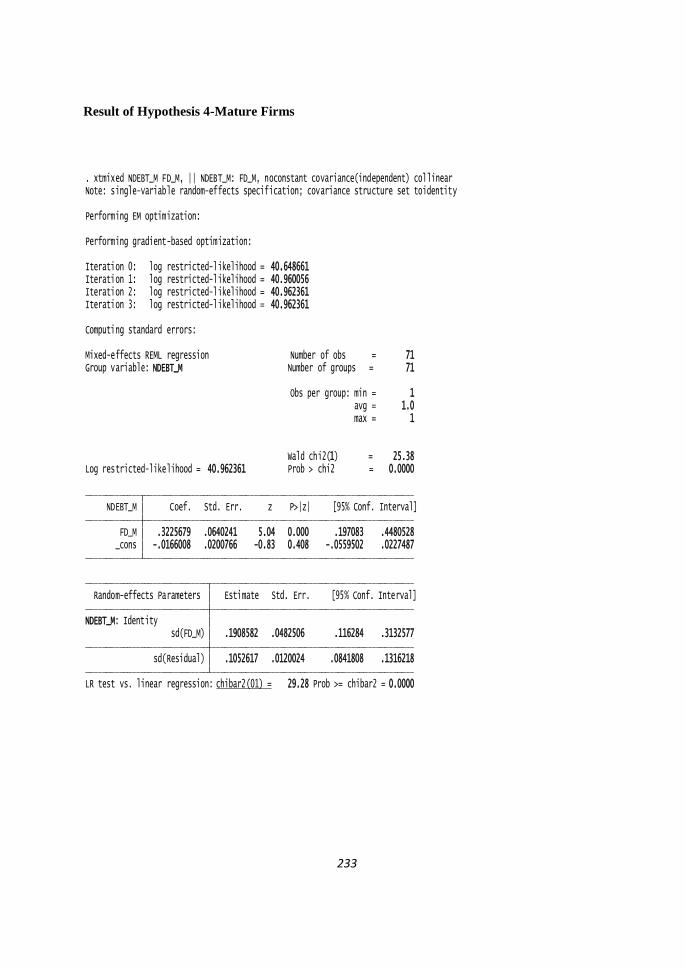

6.4.5. Analysis of Results .............................................................................................................. 139

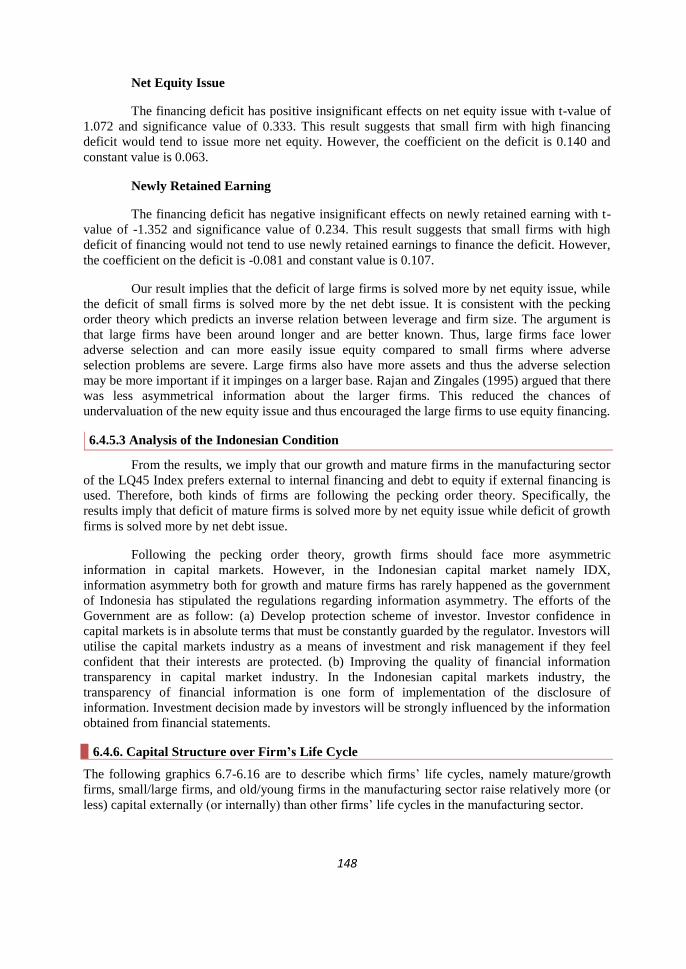

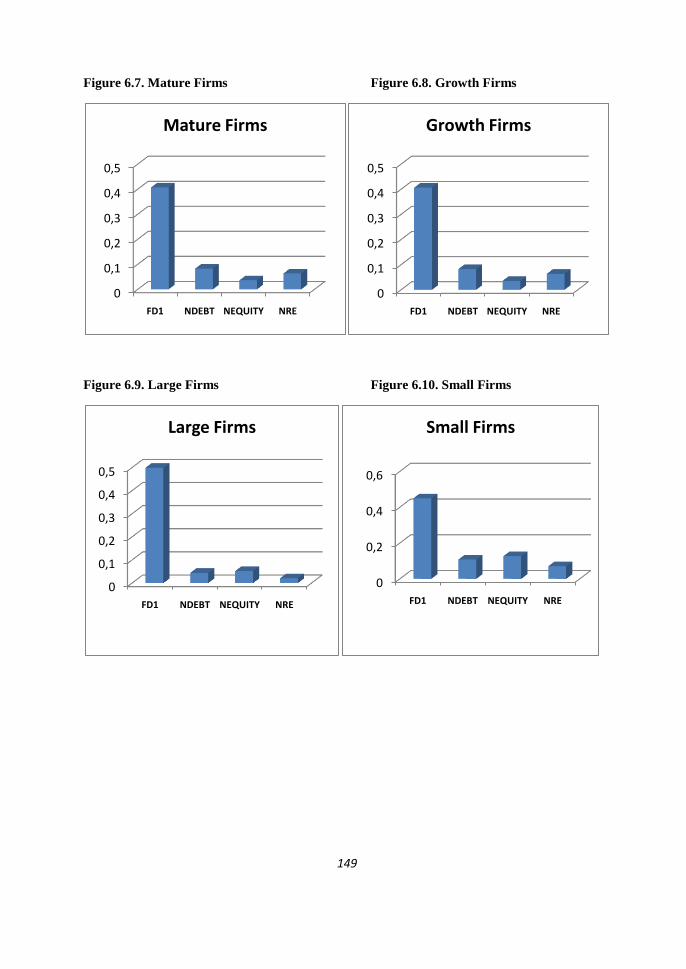

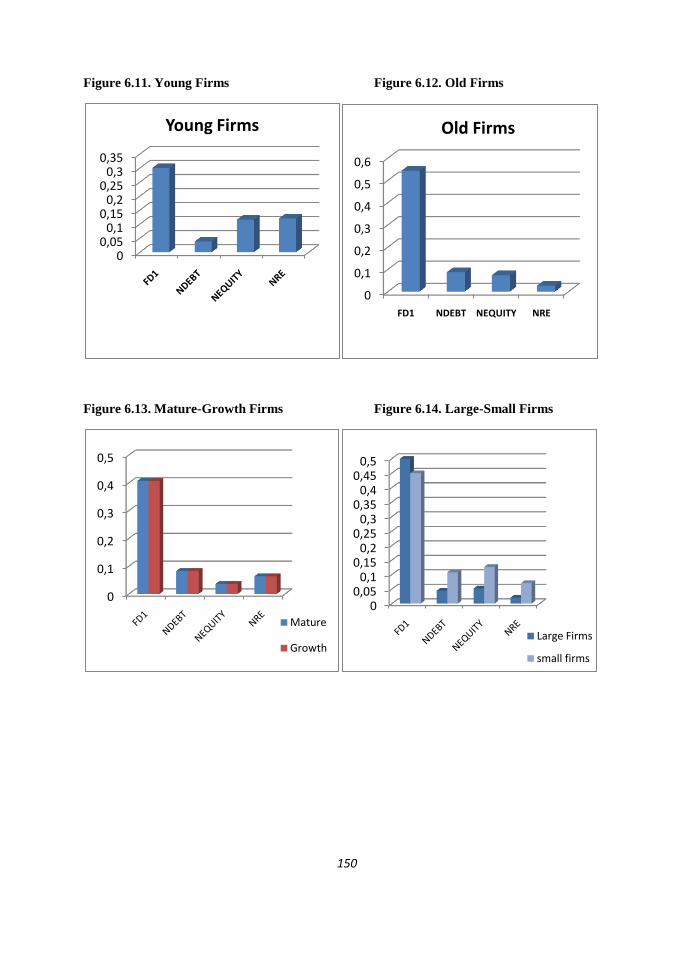

6.4.6. Capital Structure over Firm’s Life Cycle ........................................................................... 148

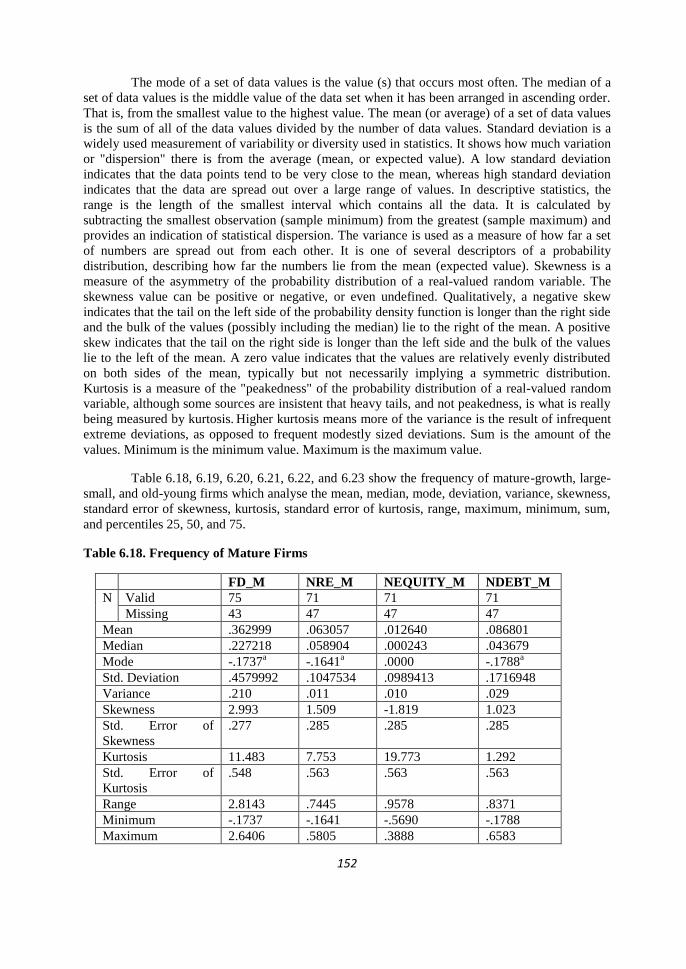

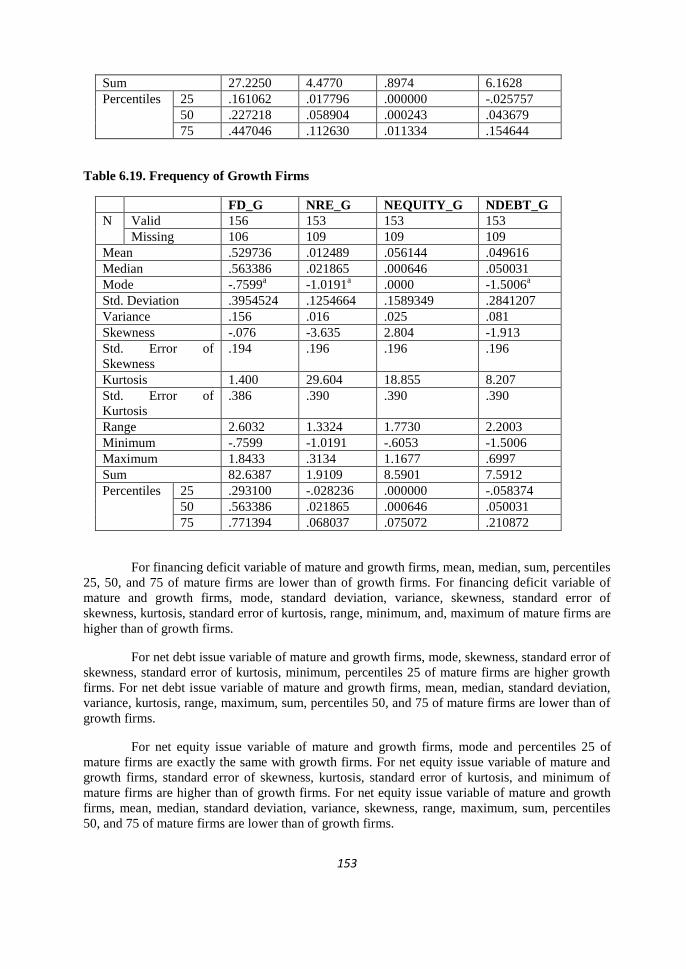

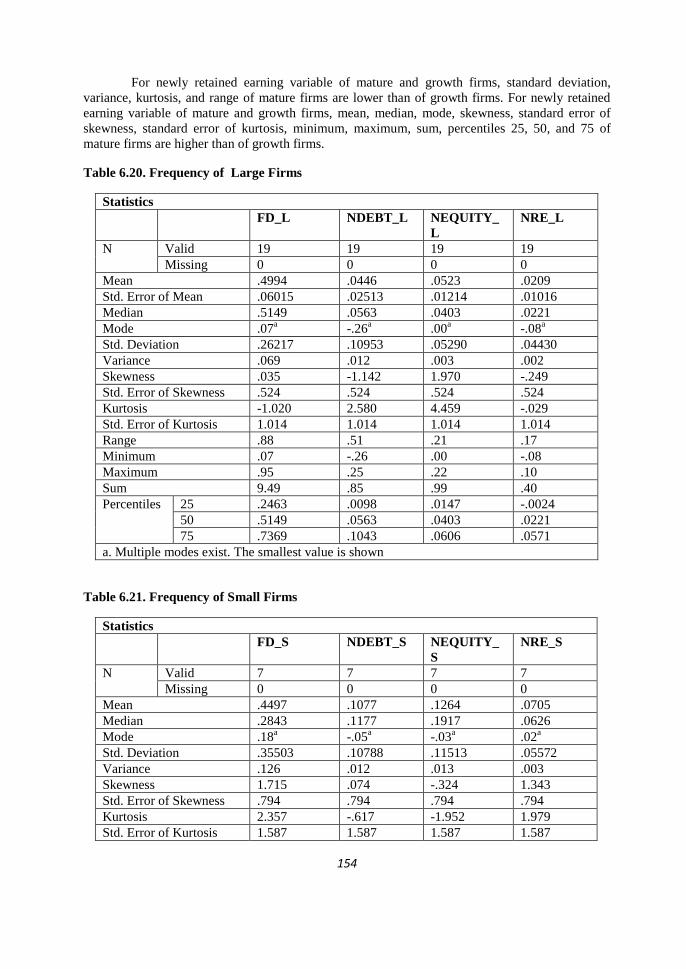

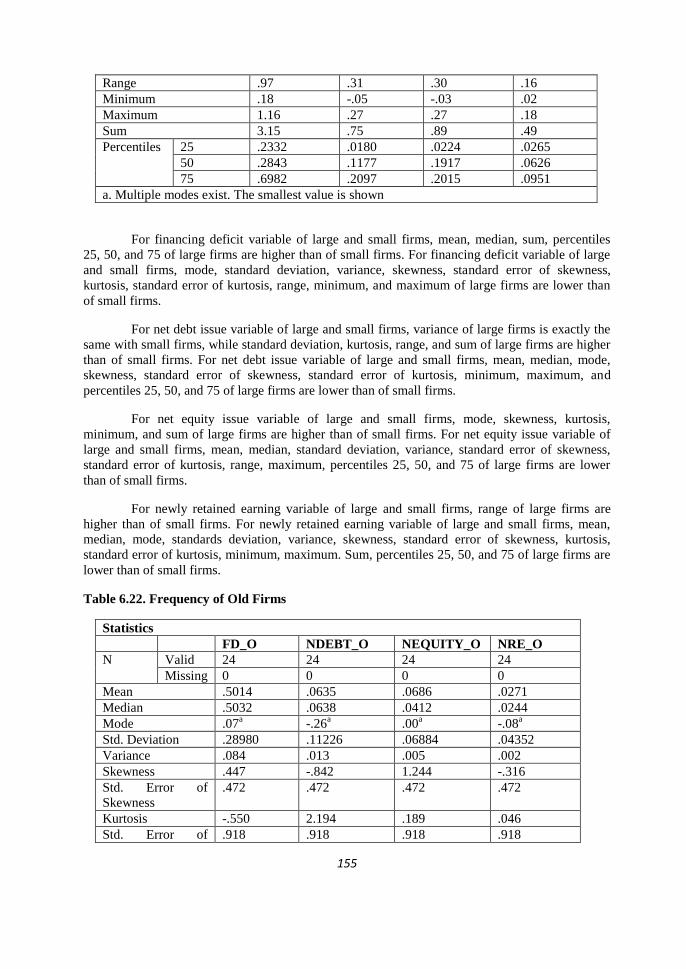

6.4.7 Frequency ............................................................................................................................ 151

6.5. Statistical Power Analysis of Hypotheses 1, 2, 3, and 4 ........................................................ 157

6.6. Regression Assumptions of Hypotheses 1, 2, 3, and 4 ........................................................... 163

1. Multicollinearity ....................................................................................................................... 163

2. Autocorrelation ........................................................................................................................ 165

8

3. Heteroscedasticity .................................................................................................................... 166

4. Normally Distributed ................................................................................................................ 166

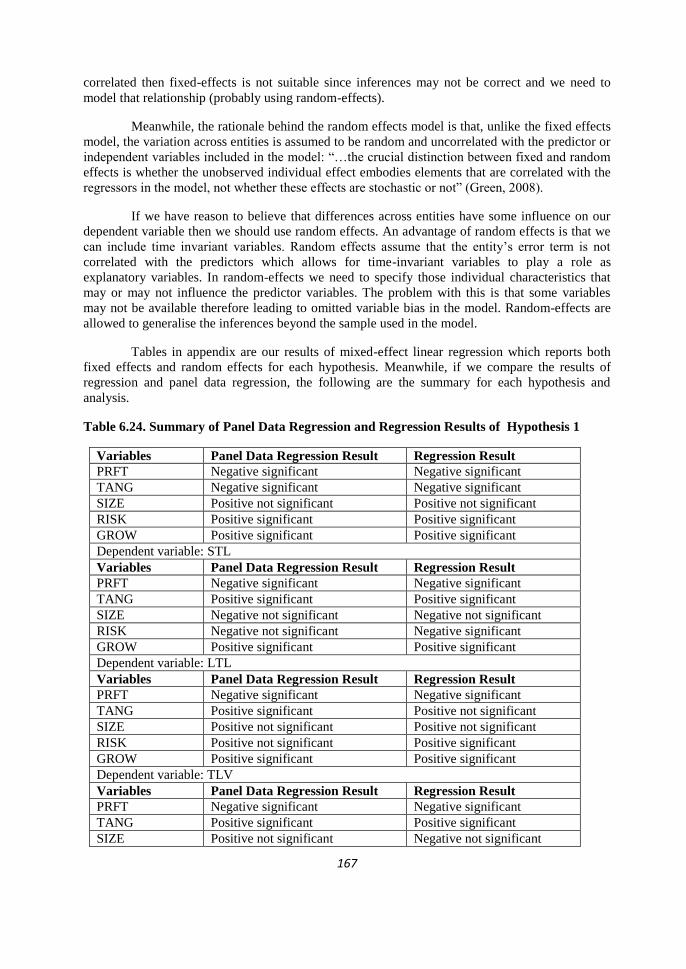

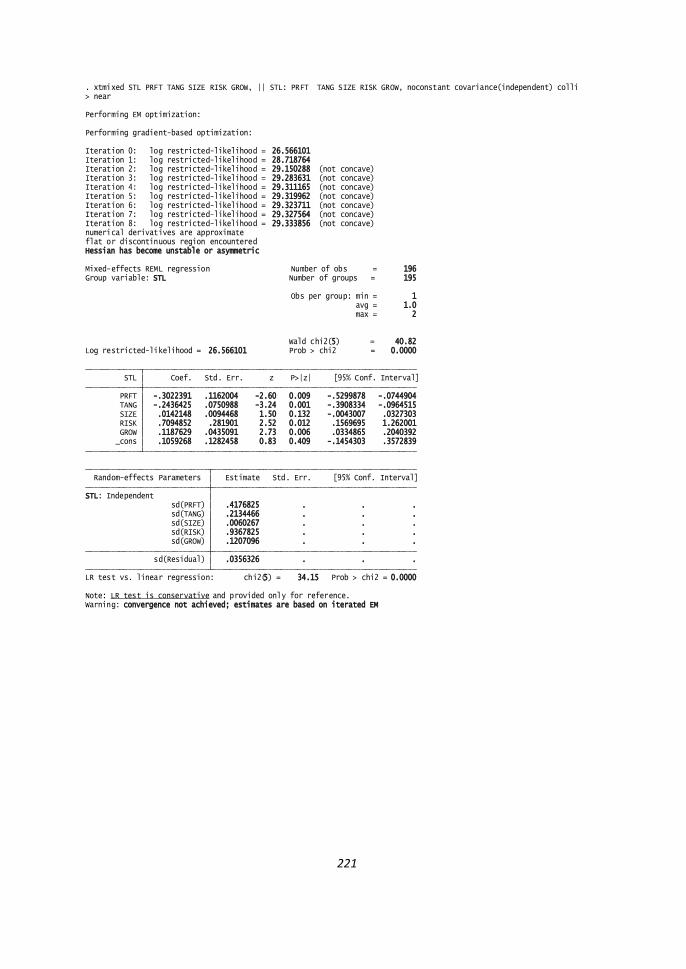

6.7. Results of Panel Data Regression Analysis and the Comparison to Regression Analysis .... 166

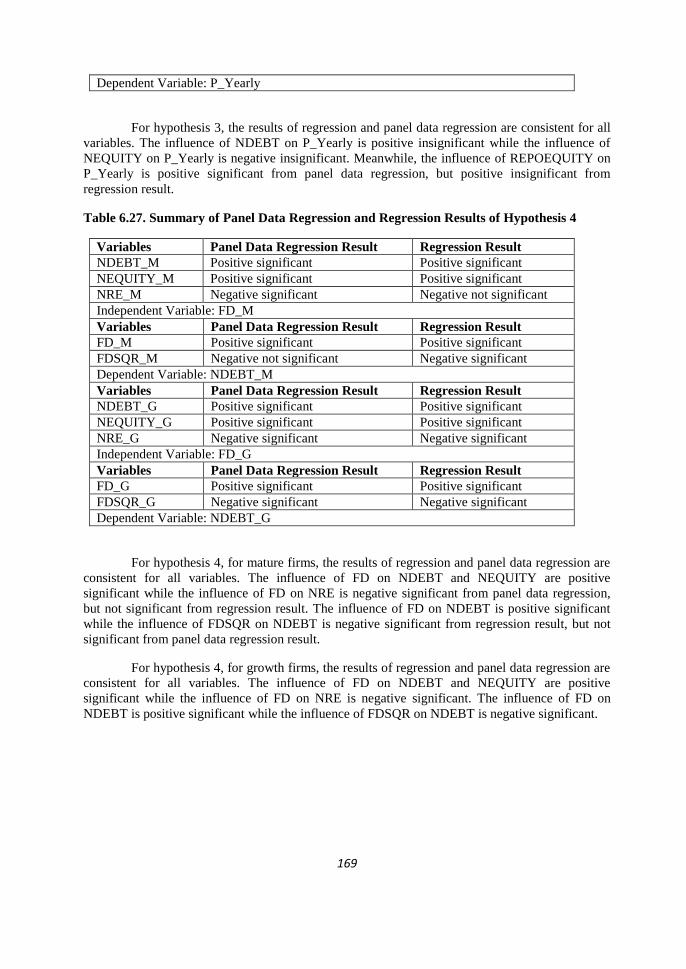

7. CONCLUSION ......................................................................................................................... 170

7.1. Conclusion ............................................................................................................................. 170

7.2 Conclusion regarding Result and Its Consistency with Condition of Indonesian Capital Market

171

7.3. To What Extent is the Study Scientifically Relevance ............................................................ 174

7.4. Recommendations and Suggestions for Further Research .................................................... 175

7.5. Suggestions for Managers ..................................................................................................... 176

7.6. Managerial Implication ......................................................................................................... 176

BIBLIOGRAPHY .......................................................................................................................... 177

APPENDIX ................................................................................................................................... 186

APPENDIX A ............................................................................................................................... 186

APPENDIX B ............................................................................................................................... 206

APPENDIX C ............................................................................................................................... 213

APPENDIX D ............................................................................................................................... 220

APPENDIX E ............................................................................................................................... 241

9

EXECUTIVE SUMMARY

The objectives of this research are: to investigate the determinants of capital structure of

the firms in the manufacturing sector in Indonesian capital market; to analyse how firms in the

manufacturing sector raise capital for investments, internally or externally (with debt, equity, or

debt to repurchase equity); to examine if debt policy does matter; what will happen to the firm‟s

stock price if firms issue new debt, issue new equity, or issue debt to repurchase equity; and to

examine within the context of a firm‟s life cycle whether we can expect that growth-small firms

follow the pecking order more closely than mature-large firms. Therefore, we examine 4 major

hypotheses. By using regression analysis we test all hypotheses, while for hypothesis 2 we use

qualitative analysis, too, and for hypotheses 2 and 4 we also apply an augmented model.

Overall, our results showed that under the linear regression model, firms exhibit as

follows. For hypothesis 1, profitability has a negative significant regression coefficient on short-

term leverage; long-term leverage; total leverage, and on market leverage. Tangibility has a

negative significant regression coefficient on short-term leverage, while tangibility has a positive

significant regression coefficient on long-term and market leverage. Tangibility also has a positive

but not significant regression coefficient on total leverage.

Size, has a positive, yet not significant regression coefficient on short-term leverage and

total leverage, while size has a negative, yet not significant regression coefficient on long-term

leverage, and size has a negative significant regression coefficient on market leverage. Risk has a

positive significant regression coefficienton short-term leverage and total leverage while risk has a

negative significant regression coefficient on long-term leverage. Risk also has a positive but not

significant regression coefficient on market leverage. Growth has a positive significant regression

coefficient on short-term, long-term, and total leverage; however, growth has a negative

significant regression coefficient on market leverage.

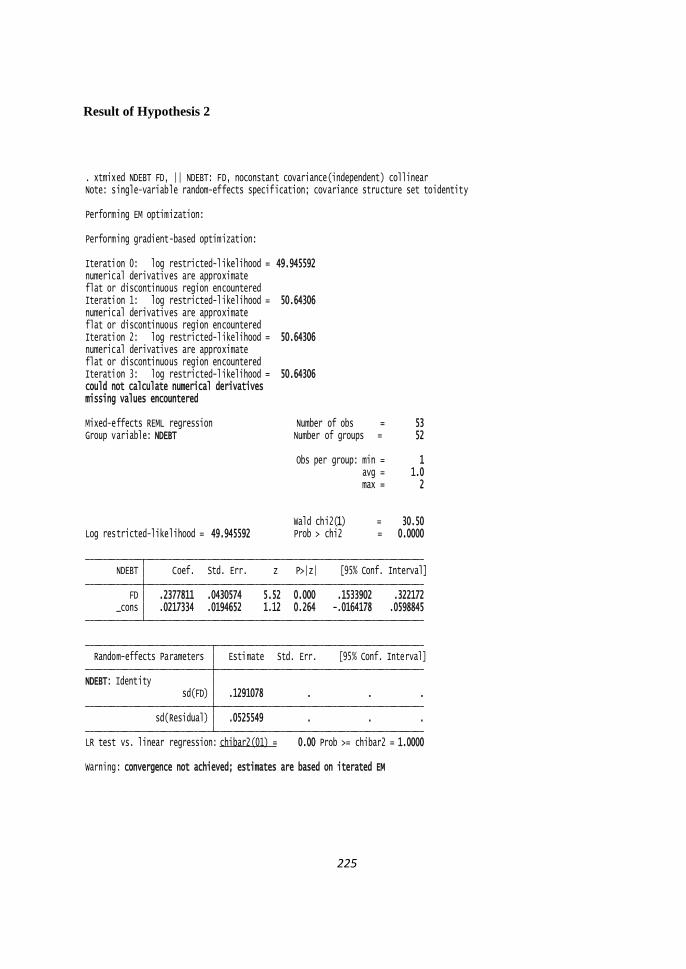

For hypothesis 2, we can conclude that the financing deficit has positive significant

effects on the net debt issue and on net equity issue. This result suggests that high deficit firms

would tend to issue more net debt and net equity to finance their financing deficit. The financing

deficit has negative, yet not significant effects on newly retained earning. This result suggests that

high deficit firms would not tend to use newly retained earning to finance the financing deficit.

The financing deficit has negative, but not significant effects on repurchase equity. This result

suggests that high deficit firms would not tend to repurchase equity to finance the financing

deficit. From the descriptive table, we see that the amount of net debt issue is more than net equity

issue and it is consistent with regression results.

For the augmented model, our result shows a positive coefficient on the financial deficit

and also on the squared deficit term. However, for the squared deficit term, the coefficient was not

significant. Therefore, we conclude that our firm sample firm prefers external to internal financing

and debt to equity if external financing is used.

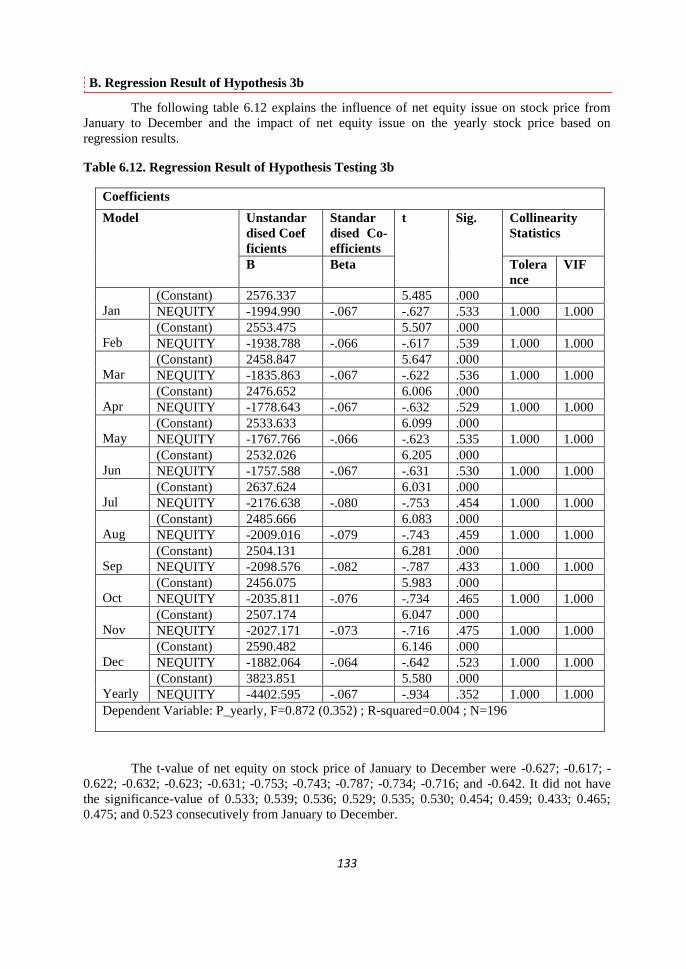

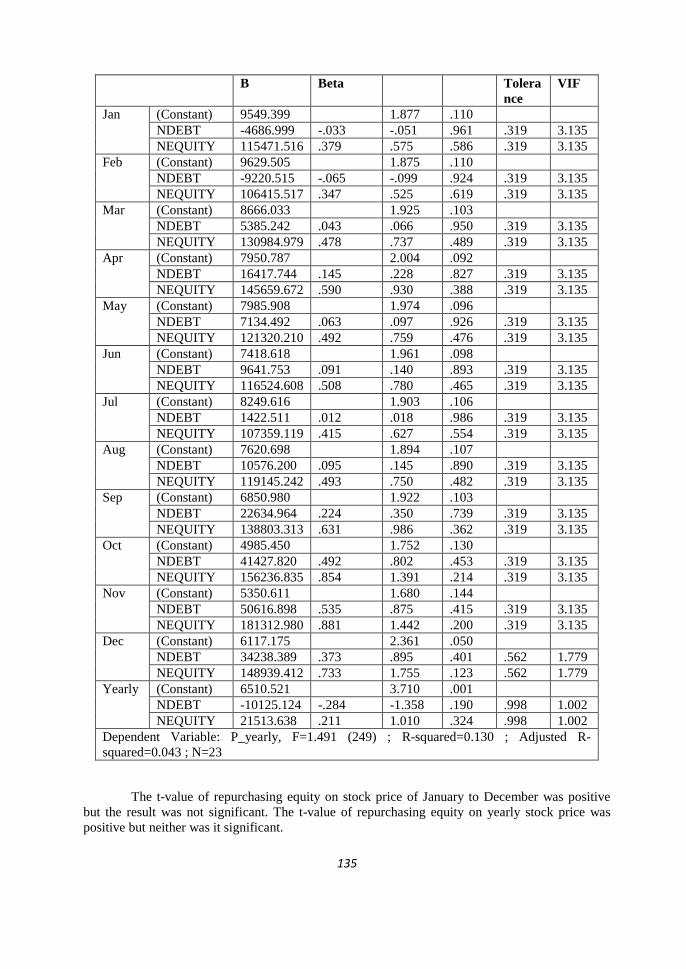

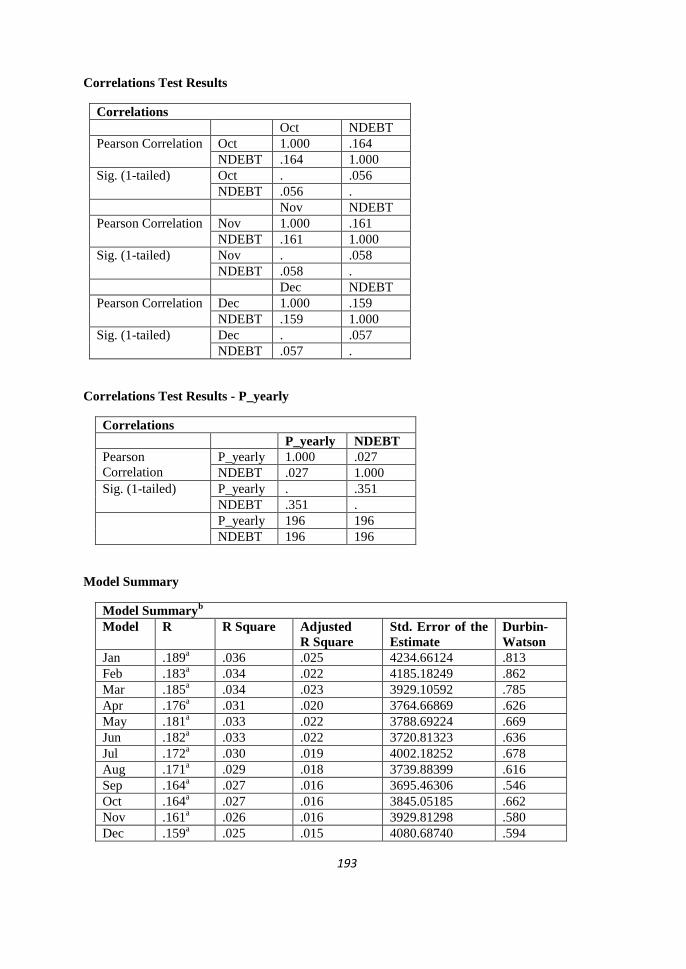

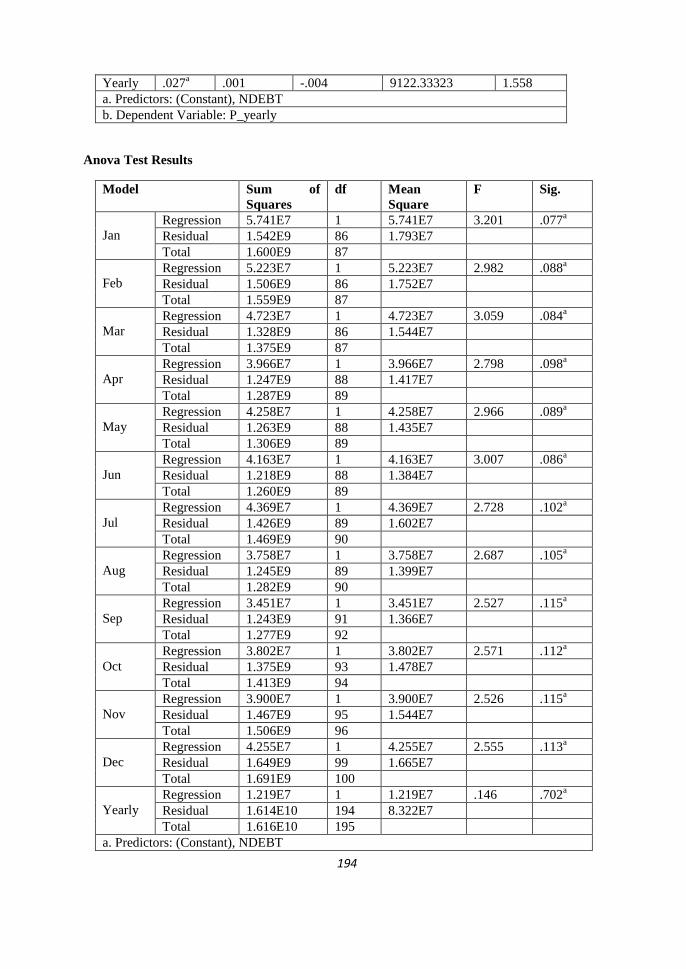

For hypothesis 3, the results indicate that net debt has no positive significant impact on

the stock price of from January to December and on the yearly stock price. Net equity has no

negative significant impact on the stock price from January to December and on the yearly stock

price. This result suggests that firms that issue more net equity would tend to have decreasing

10

stock price, while issuing more net debt, the firm would tend to have increasing stock price. The

result also suggests that firms repurchasing equity would tend to have increasing monthly and

yearly stock price.

For hypothesis 4, the growth firms, we conclude that the financing deficit has positive

significant effects on the net debt issue and on the net equity issue, and financing deficit has

negative significant effects on newly retained earning. For mature firms, we conclude that the

financing deficit has positive significant effects on the net debt issue and the net equity issue,

while a financing deficit has negative insignificant effects on newly retained earning. From these

results, we conclude that our mature and growth firm prefers external to internal financing and

debt to equity if external financing is used. Overall, we find that the pecking order theory describes

the financing patterns of growth firms better than mature firms.

11

1. INTRODUCTION

1.1 Background of the Research

1.1.1. The Importance of Capital Structure Theory

At the time a firm faces a financial deficit that affects its financial condition, the manager

of the firm should be able to make a managerial decision as well as a financial decision in order to

maintain the viability of the firm. One way that can be chosen is to undertake a capital

restructuring, especially debt restructuring. The decision taken on debt restructuring, of course,

requires expertise and analystic capabilities so managers can make the right decisions of financial

restructuring for the company. An ideal composition of capital structure which consists of debt and

equity, will minimise the cost of capital and maximise the firm‟s value. Therefore, it is important

for the firm‟s manager to understand the theory of capital structure.

The sources of funds include retained earnings, debt, and equity. Retained earning is the

cheapest fund for the funding source as it does not have explicit costs in the same way as funds

obtained from outside sources. When the company uses debt to finance investments which has an

impact on costs rising in its capital structure, the company will have a financial risk, because the

company must consider their priority in the structure of debt, debt maturity, decision of mixed debt

to certain parties or to the investor, and other types of debt contracts (Peirson, Brown, Easton and

Howard, 2002; Barclay et al., 2003).

If a firm uses stocks as its capital structure, either common stocks or preferred stocks,

then the shareholders of those stocks are the owner of the company. While debt has due date, the

stocks do not have one. Thus the repayment of stocks is not necessarily required since stocks are

liquidated if the company went bankrupt. Issuing the stocks may reduce the authority of the old

owners in the company. To maintain the dominance of the existing owner of the company, the

issuance of stocks is managed not to cross the line of power. The cost of the issuance of stocks is

dividend which will be distributed to shareholders. Furthermore, debt can be treated as tax-

deductible expenses, but common stock dividend payments and preferred stocks are not tax-

deductible.

Firm‟s capital structure decision can be viewed from the following theories: Modigliani-

Miller theory, pecking order theory, and trade-off theory. The theory of business finance in a

modern sense starts with the Modigliani and Miller (1958) capital structure irrelevance

proposition. Before them, there was no generally established theory of capital structure. The

debate about how and why firms choose their capital structure began in 1958 (Myers, 2001), when

Modigliani and Miller (1958) published their famous arbitrage argument showing that „the market

value of any firm is independent of its capital structure‟. Modigliani and Miller start their theory

by assuming that the firm has a particular set of expected cash flows. When the firm chooses a

certain proportion of debt and equity to finance its assets, what it has to do is to divide up the cash

flows among investors. Investors and firms are assumed to have equal access to financial markets,

which allows for homemade leverage. As a result, the leverage of the firm has no effect on the

market value of the firm. Modigliani and Miller‟s theory influenced the early development of other

capital structure theory.

12

The introduction of taxation effects implies that firms should, theoretically, try to

increase their debt levels as much as possible (Miller, 1988). However, other theorists (for

example Stiglitz, 1974; 1988) added limitations to the optimal level of firm debt by arguing that

bankruptcy costs enhance as the firm‟s level of debt increases, and this places a higher limit on

the amount of debt that should be present in a firm‟s capital structure. This evolved into the static

trade-off theory, which proposes that firms attempt to achieve an optimal capital structure that

maximises the value of the firm by balancing the tax benefits, with the bankruptcy costs,

associated with increasing levels of debt (Myers, 1984).

Some researchers have identified problem areas in the capability of the static trade-off

theory to explain actual firm behaviour. For example Myers (2001) argued that the static trade-off

theory implies that highly profitable firms should have high debt ratios in order to shield their

large profits from taxation, whereas in reality, highly profitable firms tend to have less debt than

less profitable firms. Warner (1977) suggested that bankruptcy costs are much lower than the tax

advantages of debt, implying much higher debt levels than predicted by the theory.

There is, however, also some empirical evidence and theoretical support for the idea that

firms, at least in part, raise their capital structure to take advantage of the interest tax shield (net of

the interest tax burden to investors), while ensuring that they avoid acquiring excessively high

financial distress costs. For example, Kayhan and Titman (2004) found that, over the long term,

firms do tend to move towards target debt ratios consistent with the theory. Static trade-off theory

therefore offers one possible explanation of how firms choose their capital structure.

Myers observed how firms actually structure their balance sheets, and found that firms

tend to follow a „pecking order‟ in financing their projects: first they use internal equity, then debt,

and only then do they use external equity (Myers, 1984). In contrast to Ross (1977), who argued

that firms use more debt to overcome information asymmetries and signal better prospects, Myers

(2001) used information asymmetries to argue that managers are unlikely to issue equity, because

they fear it will signal that the stock price is overvalued. In addition to the evidence presented by

Myers, several other studies have given support to the pecking order theory. For instance , Allen

(1993), like Fama and French (1988), found that leverage is inversely related to profitability,

which supports the pecking order theory view that debt is only issued when there is insufficient

retained income to finance investment.

Therefore, capital structure decision is influenced by a pecking order preference, which

has advantages and disadvantages based on the pecking order theory, and trading off cost and

benefit of using debt based on trade-off theory, in order to maximise return and minimise cost of

capital. Besides capital structure, the decision is influenced by the pecking order preference and

the trading off cost and benefit of using debt, capital structure decision is influenced by the firm‟s

life cycle where the firm exist and may consider the firm‟s characteristics.

Capital structure life stage theory is conspicuously underdeveloped. Although mentioned

in text-books (Damodaran, 2001) and obliquely in some research (for example Morgan and Abetti,

2004), and even referred to in the development of some of the other major theories (for example

Myers, 2001), the idea that the capital structure of a firm may be related to its life stage, appears to

have received very little direct theoretical or empirical examination. Some of the organisational

life stage theory research has suggested that changing life stages may require changes in the way

the firm is financed. Thus the firm‟s financing characteristics change from one life stage to the

next stage.

13

The pecking order theory describes the financing patterns of growth firms better than of

mature firms as mature firms are more closely followed by analysts and are better known to

investors, and hence should suffer less from problems of information asymmetry. Our result is

consistent with the theory, and also consistent with the previous research findings of Shyam-

Sunder and Myers (1999). They propose a direct test of the pecking order and find strong support

for the theory among a sample of large firms.

Older and more mature firms are more closely followed by analysts and are better known

to investors, and hence, should suffer less from problems of information asymmetry. For example,

a good reputation (such as a long credit history) mitigates the adverse selection problem between

borrowers and lenders. Thus, mature firms are able to obtain better loan rates compared to their

younger firm counterparts (Diamond, 1989).

The theory‟s prediction that firms with the greatest information asymmetry problems

(specifically young growth firms) are exactly those which should be raising financing choices

according to the pecking order theory. In general, the significant difference between mature and

young firms is not that mature firms are larger, but because they are more mature which implies

that mature firms are older, more stable, higher profitable with few growth opportunities and good

credit histories. Growth firms are thus more suited to use internal funds first, and then debt before

equity for their financing needs.

As mentioned above, capital structure decision is also affected by a firm‟s characteristics.

These characteristics are potentially contentious (Titman and Wessels 1988). Each theory of

capital structure gives the different implication on how the firm‟s characteristics influence the

firm‟s capital structure choices. In order to identify which of the firm‟s characteristics that have

significant effect on capital structure based on theories in the context of Indonesian firms, so this

research concentrates on a group of variables identified in the previous literature. The selected

explanatory variables are firm size, risk, profitability, tangibility and growth opportunities.

For profitability, the pecking order theory, based on works by Myers and Majluf (1984)

suggests that firms prefer internal funds rather than external funds. If external finance is required,

the first choice is to issue debt, hybrid, then eventually equity as a last resort (Brealey and Myers,

1991). This behaviour may be due to the costs of issuing new equity, as a result of asymmetric

information or transaction costs. All things being equal, the more profitable the firms are, the more

internal financing they will have, and therefore we should expect a negative relationship between

leverage and profitability. However, from the trade-off theory point of view more profitable firms

are exposed to lower risks of bankruptcy and have greater incentive to employ debt to exploit

interest tax shields.

For tangibility, according to the pecking order theory and the trade-off theory, a firm with

a large amount of fixed asset can borrow at a relatively lower rate of interest by providing the

security of these assets to the creditors. Having the incentive of getting debt at a lower interest

rate, a firm with a higher percentage of fixed asset is expected to borrow more as compared to a

firm whose cost of borrowing is higher because of having less fixed assets. Thus, we expect a

positive relationship between tangibility of assets and leverage. From a pecking order theory

perspective, firms with few tangible assets are more sensitive to informational asymmetries. These

firms will thus issue debt rather than equity when they need external financing (Harris and Raviv,

1991), leading to an expected negative relation between the importance of intangible assets and

leverage.

14

For size,, according to trade-off theory, first, large firms don‟t consider the direct

bankruptcy costs as an active variable in deciding the level of leverage as these costs are fixed by

constitution and constitute a smaller proportion of the total firm‟s value. And also, larger firms

being more diversified have lesser chances of bankruptcy (Titman and Wessels 1988). Following

this, one may expect a positive relationship between size and leverage of a firm. According to

pecking order theory, Rajan and Zingales (1995) argue that there is less asymmetrical information

about the larger firms. This reduces the chances of undervaluation of the new equity issue and,

thus, encourages the large firms to use equity financing. This means that there is a negative

relationship between size and leverage of a firm.

For risk, according to these theories, the pecking order theory and trade-off theory, we

can expect that firms with higher income variability have lower leverage (Bradley et al. , 1984;

Kester, 1986; Titman and Wessels, 1988), since higher variability in earnings indicates that the

probability of bankruptcy increases. Firms that have a high operating risk can lower the volatility

of the net profit by reducing the level of debt. A negative relation between the operating risk and

the leverage is also expected from a pecking order theory perspective: firms with a high volatility

of results try to accumulate cash during good years, to avoid under-investment issues in the future.

For growth, by applying pecking order arguments, growing firms place a greater demand

on the internally generated funds of the firm. Consequentially, firms with a relatively high growth

will tend to issue securities less subject to information asymmetries, i.e. short-term debt. This

should lead to firms with relatively higher growth having more leverage. Following trade-off

theory, for companies with growth opportunities, the use of debt is limited as in the case of

bankruptcy, the value of growth opportunities will be close to zero, growth opportunities are

particular cases of intangible assets (Myers, 1984; Williamson, 1988 and Harris and Raviv, 1990).

Firms with less growth prospects should use debt because it has a disciplinary role (Jensen, 1986;

Stulz, 1990). Firms with growth opportunities may invest suboptimally, and therefore creditors

will be more reluctant to lend for long horizons. This problem can be solved by short-term

financing (Titman and Wessels, 1988) or by convertible bonds (Jensen and Meckling, 1976; Smith

and Warner, 1979).

Furthermore, while the literature is rich in studies that examine the importance of firm-

specific factors in determining a firm‟s financing choice, empirical evidence on the effect of

capital structure choice on stock market reaction is limited. When a firm issues, repurchases or

exchanges one security for another, it changes its capital structure. What are the valuation effects

of these changes? There are several theories which explain the relationship between capital

structure and stock price.

Based on signalling through capital structure, as the increased level of leverage is

accompanied by a higher risk of bankruptcy, the increased level of debt indicates the confidence of

the management in the future prospects of the firm. Hence, it carries greater conviction than a

mere announcement of undervaluation of the firm by the management. On the other hand, an issue

of equity is a signal that the firm is overvalued. The market concludes that the management has

decided to offer equity because it is valued higher than its intrinsic worth by the market. The

markets normally react favourably to moderate increases in leverage and negatively to a fresh

issue of equity.

Under the trade-off theory, firms will only take actions if they expect profits. An

implication of the theory is that the market reaction to both equity and debt securities will be

positive. The market response to a leverage change consists of two pieces of information: the

revelation of the information that the firm‟s conditions have changed, necessitating financing, and

the impact of the financing on security valuations. The information contained in security issuance

15

decisions could be either bad news or good news. It might be bad news if the company is issuing

securities, because the company actually needs more resources than anticipated to carry out

operations. It would be good news if the company is issuing securities to take advantage of a

promising new opportunity that was not previously anticipated. A company may also issues

securities to anticipate a change in future needs. This indicates that the trade-off theory by itself

places no apparent limitations on the effect of market valuation of issuing decisions.

Jung et al. (1996) suggest an agency perspective and argue that equity issues by firms

with poor growth prospects reflect agency problems between managers and shareholders. If this is

the case, then stock prices would react negatively to news of equity issues. The pecking order

theory is usually interpreted as predicting that securities with more adverse selection (equity) will

result in more negative market reaction. Securities with less adverse selection (debt) will result in

less negative or no market reaction. This does of course, still rest on some assumptions about

market anticipations.

Literature offers various explanations for buybacks. One of these explanations has

theoretical backgrounds and some are formed from empirical studies. The undervaluation

hypothesis is explaining our hypotheses. Stock repurchases offer flexibility in the choice to

distribute excess funds and when to distribute these funds. This flexibility in timing is valuable

because firms can wait to repurchase until the stock price is undervalued. The undervaluation

hypothesis is based on the argument that information asymmetry between insiders and

shareholders can cause a company to be misvalued. If insiders trust that the stock is undervalued,

the firm may repurchase stock as a signal to the market or investing in its own stock and get

mispriced shares. This hypothesis implies that the market interprets the action as an indication that

the stock is undervalued (in Dittmar, 1999). Because of the asymmetric information between

managers and shareholders, announcements of share repurchase are considered to expose private

information that managers have about the value of the company.

The information/signalling hypothesis has three immediate implications: repurchase

announcements should be accompanied by positive price changes; repurchase announcements

should be followed (though not necessarily immediately) by positive news about profitability or

cash flows; and repurchase announcements should be immediately followed by positive changes in

the market‟s expectation about future profitability (Gustavo Grullon and Roni Michaely, 2002).

1.1.2. Research Motivation

How do firms finance their operations? What factors influence these choices? How do

these choices affect the stock price? And how do firms finance their operations over the firm‟s life

cycle? These are important questions that have motivated the researcher to conduct this research.

Based on theories explanation above, we understand that a firm‟s characteristics, cost and

benefit, market reaction, and a firm‟s life cycle influenced the choice of a firm‟s capital structure,

and it is important for the manager of a firm to understand the theory of capital structure. There

have been many previous studies which examine one of thatfactors in influencing the choice of a

firm‟s capital structure; however, there have been few that analyse all factors on the whole in

affecting the choice of a firm‟s capital structure.

Based on that motivation, through this research, we examine those factors on the choice

of a firm‟s capital structure by formulating research hypotheses. We examine all the following

issues, the determinants of capital structure of the firms in Indonesia, study how firms in

manufacturing sector raise capital for investments; investigate what will happen to the firm‟s stock

16

price if firms issue new debt, issue new equity, and issue debt to repurchase equity; and examine

how firms in Indonesia raise capital for investments over their life cycle stages.

Our motivation to test Hypothesis 1 is that the test of determinants of capital structure of

the firms in manufacturing sector in Indonesia is important as these firms have different

characteristics. We test it on the basis of the pecking order theory and the trade-off theory. The

trade-off theory and the pecking order theory imply that growth opportunities and asset tangibility

have a positive relationship with the debt ratio, while the relationship between risk (earnings

volatility) and debt ratio is negative. The pecking order hypothesis implies that a firm‟s

profitability and size have a negative relationship with the level of debt. Under trade-off theory

size and profitability have a positive relationship with the debt ratio.

The important thing when examining hypothesis 2 in this research, is that we would like

to test how firms in the manufacturing sector in LQ45 index finance the firms‟ deficit, as these

firms are experiencing financial deficit over the period of time (see table). Our analysis is related

to Shyam-Sunder and Myers (1999) and Frank and Goyal (2003), who propose to test the standard

pecking order using a regression of debt issued on the financing deficit. The argument is that the

original pecking order predicts that firms issue debt whenever their internal cash flows are

insufficient to finance real investments (and other uses of funds such as dividends). The financing

deficit, i.e. uses of funds minus internal sources of funds, therefore drives debt issuance.

Our motivation to test hypothesis 3 is that, as empirical evidence on the effect of capital

structure choice on stock market reaction is limited, hence, we examine the relationship between

capital structure and stock price, based on the pecking order theory, the trade-off theory, the

signalling theory, and asymmetric information. Based on signalling through capital structure, the

markets normally react favourably to moderate increases in leverage and negatively to a fresh

issue of equity.

Under the trade-off theory, firms will only take actions if they expect benefits. An

implication of the theory is that the market reaction to both equity and debt securities will be

positive. The market response to a leverage change could be either good news or bad news. It is

good news if the firm issues securities to take advantage of a promising new opportunity that has

not previously been anticipated. It might be bad news if the firm issues securities because the firm

actually needs more resources than anticipated to conduct operations.

The pecking order theory is usually interpreted as predicting that securities with more

adverse selection (equity) will result in a more negative market reaction. Securities with less

adverse selection (debt) will result in less negative or no market reaction. Meanwhile, the

explanations for buybacks are based on the information/signalling hypothesis that has three

immediate implications: repurchase announcements should be accompanied by positive price

changes; repurchase announcements should be followed (though not necessarily immediately) by

positive news about profitability or cash flows; and repurchase announcements should be

immediately followed by positive changes in the market‟s expectation about future profitability.

The most interesting part of this research is testing hypothesis 4. We examined capital

structure choices over the firm´s life cycle as our sample consists of 10 mature firms and 16

growth firms, where we define mature firms as firms that have 6-year dividend payment periods.

Frank and Goyal (2003) argue that the support for the standard pecking order in Shyam-Sunder

and Myers depends critically on their sample selection. Shyam-Sunder and Myers consider 157

firms that have no reporting gaps in their statement of cash-flows from 1971 to 1989. Frank and

Goyal (2003) show that the results do not extent to an unbalanced sample, i.e. when reporting gaps

17

are allowed and to the time period from 1990 to 1998. Frank and Goyal (2003) argue that the

sample selection of Shyam-Sunder and Myers picks large mature firms and that the standard

pecking order is not a good description of the capital structure decisions for small, young firms in

their larger sample. Hence, it is important to examine capital structure choices over firm life cycle.

Therefore, we then construct the following variables for our analysis: book leverage,

market leverage, net equity issued, net debt issued, financing deficit, stock price, tangibility,

profitability, risk, growth, and size. We first classify firms into two cohorts according to their life

cycle stage, namely, firms in their growth stage and firms in their mature stage. We then focus on

the pecking order theory of financing proposed by Myers (1984) and Myers and Maljuf (1984).

This theory is based on asymmetric information between investors and firm managers. Due to the

valuation discount that less-informed investors apply to newly issued securities, firms resort to

internal funds first, then debt and equity last to satisfy their financing needs. In the context of a

firm‟s life cycle, we expect that asymmetric information problems are more severe among young,

growth firms compared to firms that have reached maturity. Hence, the theory predicts that

younger, fast-growth firms should be following the pecking order more closely.

Our research findings could be the comparison to the findings of previous research and

theories. This is how this thesis adds to the scientific literature.

1.2 Problem Identification

In order to keep developing, the firms in the manufacturing sector need to finance their

financial deficit or even new projects, hence it is important to firms to implement the theories of

capital structure described earlier in choosing carefully their capital structure for financing the

investment. Firm managers can consider the cost and benefit of each capital structure preferences

based on the theories as each preference will affect market reaction which is reflected by the firm‟s

stock price valued by the market and the firm‟s life cycle which influences the choice of the firm‟s

capital structure.

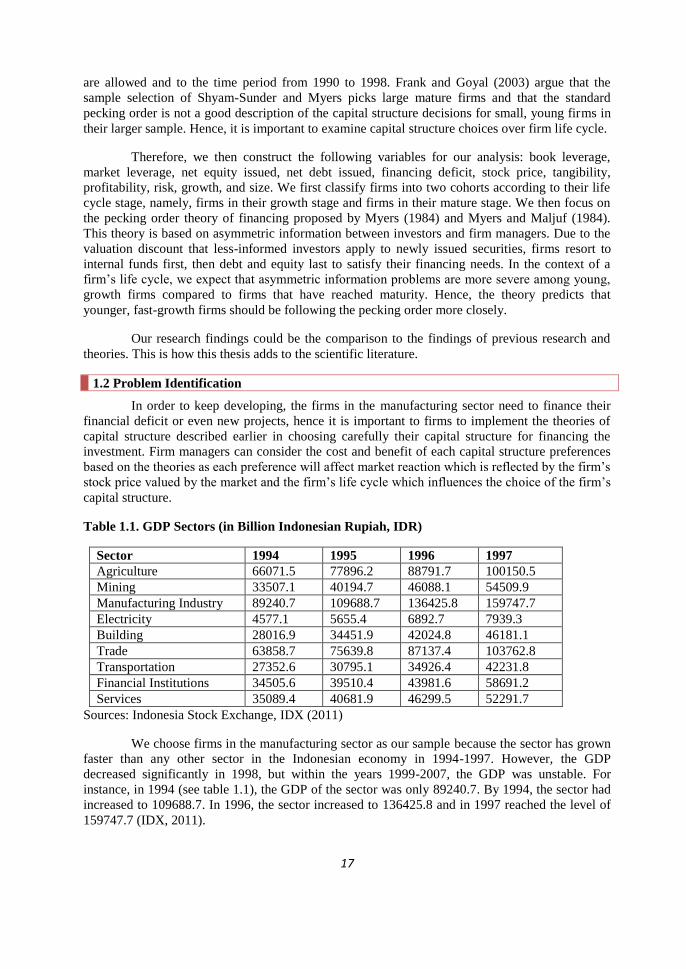

Table 1.1. GDP Sectors (in Billion Indonesian Rupiah, IDR)

Sector 1994 1995 1996 1997

Agriculture 66071.5 77896.2 88791.7 100150.5

Mining 33507.1 40194.7 46088.1 54509.9

Manufacturing Industry 89240.7 109688.7 136425.8 159747.7

Electricity 4577.1 5655.4 6892.7 7939.3

Building 28016.9 34451.9 42024.8 46181.1

Trade 63858.7 75639.8 87137.4 103762.8

Transportation 27352.6 30795.1 34926.4 42231.8

Financial Institutions 34505.6 39510.4 43981.6 58691.2

Services 35089.4 40681.9 46299.5 52291.7

Sources: Indonesia Stock Exchange, IDX (2011)

We choose firms in the manufacturing sector as our sample because the sector has grown

faster than any other sector in the Indonesian economy in 1994-1997. However, the GDP

decreased significantly in 1998, but within the years 1999-2007, the GDP was unstable. For

instance, in 1994 (see table 1.1), the GDP of the sector was only 89240.7. By 1994, the sector had

increased to 109688.7. In 1996, the sector increased to 136425.8 and in 1997 reached the level of

159747.7 (IDX, 2011).

18

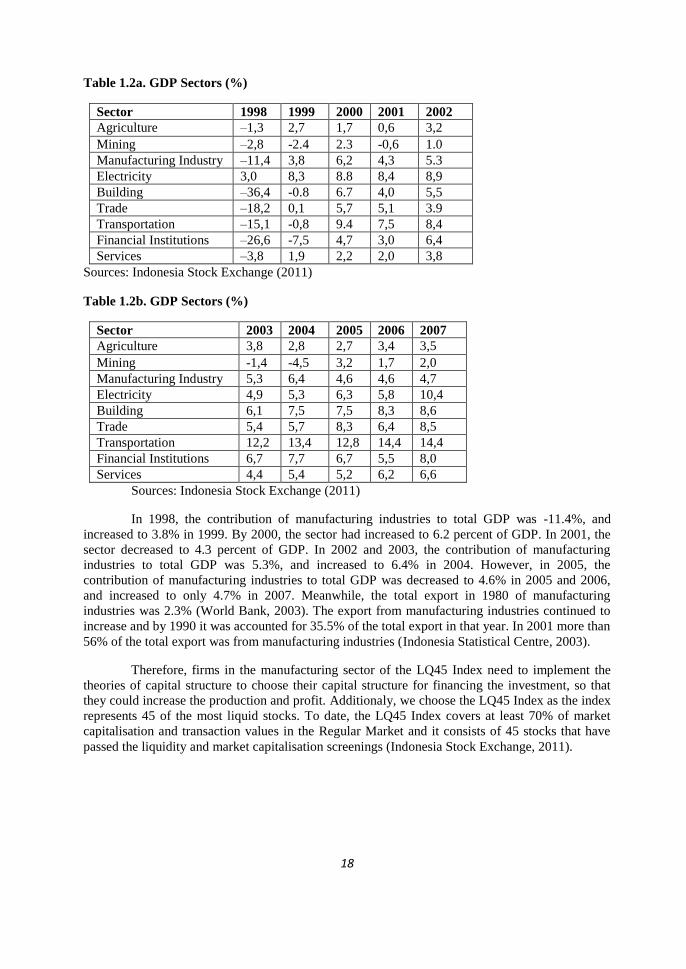

Table 1.2a. GDP Sectors (%)

Sector 1998 1999 2000 2001 2002

Agriculture –1,3 2,7 1,7 0,6 3,2

Mining –2,8 -2.4 2.3 -0,6 1.0

Manufacturing Industry –11,4 3,8 6,2 4,3 5.3

Electricity 3,0 8,3 8.8 8,4 8,9

Building –36,4 -0.8 6.7 4,0 5,5

Trade –18,2 0,1 5,7 5,1 3.9

Transportation –15,1 -0,8 9.4 7,5 8,4

Financial Institutions –26,6 -7,5 4,7 3,0 6,4

Services –3,8 1,9 2,2 2,0 3,8

Sources: Indonesia Stock Exchange (2011)

Table 1.2b. GDP Sectors (%)

Sector 2003 2004 2005 2006 2007

Agriculture 3,8 2,8 2,7 3,4 3,5

Mining -1,4 -4,5 3,2 1,7 2,0

Manufacturing Industry 5,3 6,4 4,6 4,6 4,7

Electricity 4,9 5,3 6,3 5,8 10,4

Building 6,1 7,5 7,5 8,3 8,6

Trade 5,4 5,7 8,3 6,4 8,5

Transportation 12,2 13,4 12,8 14,4 14,4

Financial Institutions 6,7 7,7 6,7 5,5 8,0

Services 4,4 5,4 5,2 6,2 6,6

Sources: Indonesia Stock Exchange (2011)

In 1998, the contribution of manufacturing industries to total GDP was -11.4%, and

increased to 3.8% in 1999. By 2000, the sector had increased to 6.2 percent of GDP. In 2001, the

sector decreased to 4.3 percent of GDP. In 2002 and 2003, the contribution of manufacturing

industries to total GDP was 5.3%, and increased to 6.4% in 2004. However, in 2005, the

contribution of manufacturing industries to total GDP was decreased to 4.6% in 2005 and 2006,

and increased to only 4.7% in 2007. Meanwhile, the total export in 1980 of manufacturing

industries was 2.3% (World Bank, 2003). The export from manufacturing industries continued to

increase and by 1990 it was accounted for 35.5% of the total export in that year. In 2001 more than

56% of the total export was from manufacturing industries (Indonesia Statistical Centre, 2003).

Therefore, firms in the manufacturing sector of the LQ45 Index need to implement the

theories of capital structure to choose their capital structure for financing the investment, so that

they could increase the production and profit. Additionaly, we choose the LQ45 Index as the index

represents 45 of the most liquid stocks. To date, the LQ45 Index covers at least 70% of market

capitalisation and transaction values in the Regular Market and it consists of 45 stocks that have

passed the liquidity and market capitalisation screenings (Indonesia Stock Exchange, 2011).

19

1.3 Research Questions

The research is going to answer the following major and minor research questions:

1.3.1 Major Research Questions

Our major research questions are as follow:

1. What are the determinants of capital structure of the firms in the manufacturing sector in

Indonesia?

2. How do firms in the manufacturing sector in Indonesia raise capital for investments,

internally or externally (with debt, equity, or debt to repurchase equity)?

3. Does debt policy matter?

4. In the context of firm‟s life cycle, can we expect that growth [and small] firms follow the

pecking order theory more closely than mature [and large] firms?

1.3.2 Minor Research Questions

Our minor research questions are as follow:

1. What are the determinants of capital structure of the firms in the manufacturing sector in

Indonesia?

a. As implied by the trade-off theory and the pecking order theory, do growth

opportunities have a positive relationship with the debt ratio?

b. As in the pecking order hypothesis, does the firm‟s profitability have a negative

relationship with the level of debt? And as implied by the trade-off theory, does the

firm‟s profitability have a positive relationship with the debt ratio?

c. In accordance with the pecking order theory and trade-off theory, is there a negative

relationship between risk (earnings volatility) and debt ratio?

d. As suggested by the trade-off theory, does size have a positive relationship with the

debt ratio? And as suggested by the pecking order theory of the capital structure, is

there a negative relationship between the level of debt and the size of the firm?

e. In accordance with the trade-off theory, is there a positive relationship between the

asset tangibility and the level of debt?

2. How do firms in the manufacturing sector in Indonesia raise capital for investments,

internally or externally (with debt, equity, or debt to repurchase equity)?

3. Does debt policy matter?

Based on the asymmetric information, the firms use equity financing only as the last

resort and based on signalling theory, the markets normally react favourably to moderate

increases in leverage and negatively to a fresh issue of equity.

20

(a) If a firm issues new debt, what will happen to the firm‟s stock price?

(b) If a firm issues new equity, what will happen to the firm‟s stock price?

(c) If a firm issues debt to repurchase equity, what will happen to the firm‟s stock price?

4. In the context of firm‟s life cycle, can we expect that growth [and small] firms follow the

pecking order theory more closely than mature [and large] firms?

1.4 Research Objectives

Based on research questions, the objectives of this research are to:

1. Determine the determinants of capital structure of firms in the manufacturing sector in the

Indonesian capital market.

a. Investigate the relationship between growth and debt ratios as implied by the trade-off

theory and the pecking order theory.

b. Examine the relationship between a firm‟s profitability and debt ratios as implied by

the trade-off theory and the pecking order theory.

c. Determine the relationship between risk (earnings volatility) and debt ratios as implied

by the trade-off theory and the pecking order theory.

d. Investigate the relationship between size and debt ratios as suggested by the trade-off

theory and the pecking order theory.

e. Analyse the relationship between asset tangibility and debt ratios as implied by the

trade-off theory.

2. Investigate how firms in manufacturing sector raise capital for investments, internally or

externally (with debt, equity, or debt to repurchase equity).

3. Examine whether debt policy matters:

(a) Analyse if a firm issues new debt, what will happen to the firm‟s stock price.

(b) Analyse if a firm issues new equity, what will happen to the firm‟s stock price.

(c) Analyse if a firm issues debt to repurchase equity, what will happen to the firm‟s

stock price.

4. Examine in the context of firm‟s life cycle, do growth [and small] firms follow the pecking

order theory more closely than mature [and large] firms.

1.5 Scope and Limitation of the Study

The scope of the study is to investigate the determinants of capital structure of the firms

in the manufacturing sector in Indonesia, examine how firms in the manufacturing sector raise

capital for investments, internally or externally (with debt, equity, or debt to repurchase equity),

investigate if debt policy matters, what will happen to the firm‟s stock price if firms issue new

debt, issue new equity, and issue debt to repurchase equity. Finally, we examine in the context of

21

firm‟s life cycle, do growth [and small] firms follow the pecking order theory more closely than

mature [and large] firms.

Manufacturing companies that exist throughout the 13-year period with no missing data

are included in the study. Data availability is a major limitation in capital structure studies in

emerging capital markets. We use data of the Indonesia Stock Exchange Main Board companies,

with the selected time period of 1994-2007 to capture the differences in economic conditions of

the Indonesian economy. To enlighten it, we explain those periods that describe the differences in

economic conditions.

Before the Crisis Period (Before 1997)

Before the economic crisis triggered by the financial crisis in mid 1997, Indonesia was

among the few developing countries which were rated as highly successful in its development.

Within thirty years, from 1965 to 1995, GDP per capita in real terms grew on average by 6.6%

annually (World Bank 1997). The role of manufacturing industry in GDP experienced a significant

increased, from 7.6% in 1973 to nearly 25% in 1995.

Crisis Period (1997-1998)

In 1995 Indonesia was still enjoying an economic growth of 8.2%, later in 1996, or the

last year before the crisis happened, it still grew with 7.8%, and in 1997 dropped to 4.9%. So, until

1997, the year of the crisis, at least, economic growth still remained positive despite showing a

declining trend. The crisis that began with the fall of the Thai Baht in July 1997, then gave a direct

result on the value of IDR which depreciated exponentially, from Rp2.400 per Dollar in mid-1997

to Rp16.000 per Dollar in June 1998. The decline in food production triggered high inflation in

1998, added pressuring on foreign exchange reserves that have already declined.

In 1998, when the crisis reached its peak, Indonesia's economic growth contracted by

13.6% and other macroeconomic indicators showed worsening values, such as inflation which

increased to 77.6%. The crisis that hit Indonesia since mid 1997 has gradually decreased and by

the end of the reporting year 1998/99 Indonesian economy began to show improvement.

Inflationary pressures continued to decline from October 1998 onwards, so that the annual

inflation rate had reached 82.4% in September 1998, and was successfully reduced to 45.4% at the

year-end report. The success in reducing inflationary pressures reflected in the strengthening trend

of the IDR.

1999-2000

In 1999, inflation rate was under control, from almost 80% in 1998 to 2% in the

following year, With these conditions, the interest rate could drop from about 80% to 11-12%. By

mid-1999, the economic crisis in Indonesia had surpassed its lowest point and began to grow

again. Throughout the year, the economy grew slightly with an increase in GDP of 0.3%.

Entering early 2000, the process of economic recovery had begun to appear since the

third quarter of 1999. Monetary stability was also controllable, as reflected in the achievement of

low inflation and stronger exchange rate until the end of 1999. Economic growth was increasing

higher than forecasted to 4.8%. The IDR tended to weaken and volatile since May 2000.

Meanwhile, pressure on the inflation rate increased and inflationary pressures also emerged as a

result of the weakening of the IDR.

22

2001-2004

During the 2001, economic and monetary conditions in general showed a deteriorating

trend. Worsening the economic and monetary conditions, among others, indicated by the slowing

economic growth, a weakening exchange rate, and high inflation pressures. During 2001,

Indonesia's economy grew only by 3.3%, the exchange rate depreciated by 17.7% so that to

achieve an average of Rp.10.255 per USD Dollar, and CPI inflation reached 12.55%.

During 2002, the general economic condition in Indonesia showed a positive growth

which was indicated by more stable macroeconomic conditions. Overall, in 2002, the exchange

rate appreciated significantly by 10.10% so as to achieve an average of Rp 9.316 per US Dollar.

These stable monetary conditions have affected the level of CPI inflation during 2002,

experiencing a declining trend to reach 10.03%. Overall, during 2002 the Indonesian economy

only grew by 3.7%.

In 2003, to face the challenges, the Government and the Bank of Indonesia have taken a

series of policies to encourage the process of economic recovery while maintaining

macroeconomic stability. In the process, various policies have contributed significantly in

supporting the achievement of stable macro economic conditions during 2003, which indicated by

the strengthening of the IDR and declining of inflation rate. The year 2004 brang hope, optimism,

as well as a new challenge. In 2004, macroeconomic stability maintained, international confidence

increased, and clarity of the economic agenda eached.

2005-2007

The year 2005 was a dynamic and challenging one for the economy of Indonesia. On the

average, the Rupiah reached Rp 9.713 per U.S. Dollar during 2005, or a depreciation by 8.6%

compared to an average of 2004. Meanwhile, the CPI inflation, which until the third quarter of

2005 was recorded at 9.1% (year on year, yoy) had increased to 17.1% (yoy) in late 2005. Overall

economic growth in Indonesia in 2005 reached 5.6% or achieved an increase of 5.1% from the

previous year.

Entering the beginning of 2006, Indonesia economic conditions are still very influenced

by the rising of fuel prices (fuel) and high interest rates. Inflation rate of consumer price index

(CPI) which is very high in early 2006 reached 17.03% (yoy) gradually decreased to 6.60% (yoy)

in late 2006 and maintained stability in the rupiah. With inflation and interest rates which

gradually declined, since the beginning of the second half of 2006, the economy grew in the good

trend so as the overall in 2006, growth reached 5.5% (yoy), slightly lower than the previous year.

Entering 2007, Indonesia's economy to regain macroeconomic stability. The Rupiah, in

the second half of 2007 was depreciated significantly and reached the weakest level in August

2007, with a monthly average of Rp 9372 per U.S. Dollar. Maintained macroeconomic stability

kept a high economic growth in 2007, and even reached the highest level in the post-crisis period,

namely 6.32%.

1.6 Expected Contribution

By conducting this research, we expected some contributions for the firms. In this research, the

purpose of our research will not be to produce a theory that is generalisable to all populations. Our

objective is trying to explain what is happening in the Indonesian capital market with

manufacturing firms of the LQ45 Index, regarding how firms finance their operations. What

factors influence the choices of capital structure? How do these choices affect the stock price? And

23

how do firms finance their deficit over a firm‟s life cycle? The findings of this study will lead

firms to make the decision of choosing capital structure by considering the firm‟s characteristics,

market reaction reflected by stock price, and the life cycle stage of the firm.

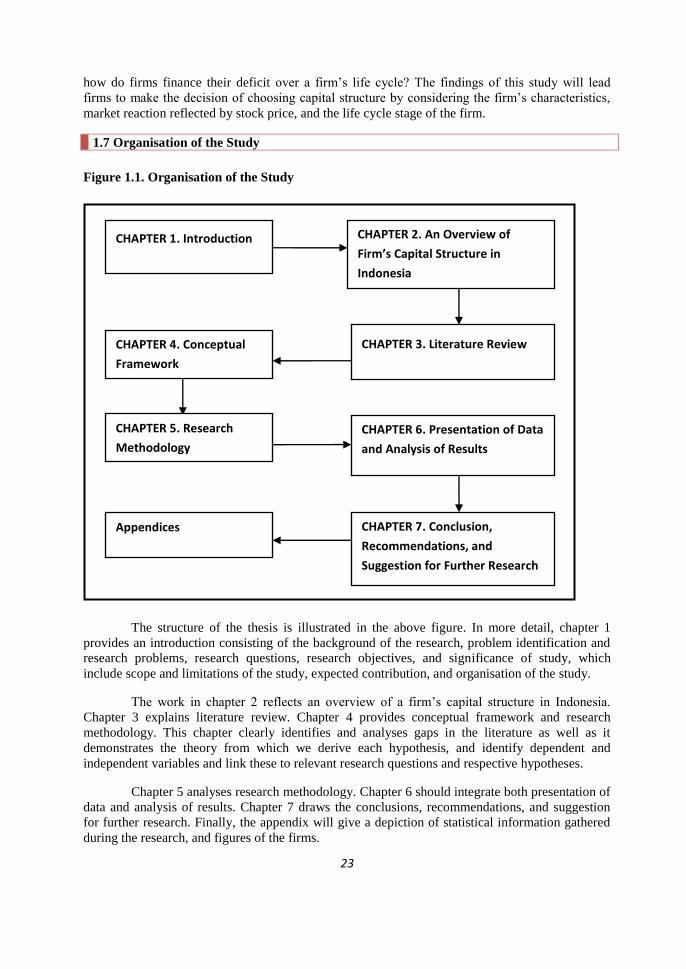

1.7 Organisation of the Study

Figure 1.1. Organisation of the Study

The structure of the thesis is illustrated in the above figure. In more detail, chapter 1

provides an introduction consisting of the background of the research, problem identification and

research problems, research questions, research objectives, and significance of study, which

include scope and limitations of the study, expected contribution, and organisation of the study.

The work in chapter 2 reflects an overview of a firm‟s capital structure in Indonesia.

Chapter 3 explains literature review. Chapter 4 provides conceptual framework and research

methodology. This chapter clearly identifies and analyses gaps in the literature as well as it

demonstrates the theory from which we derive each hypothesis, and identify dependent and

independent variables and link these to relevant research questions and respective hypotheses.

Chapter 5 analyses research methodology. Chapter 6 should integrate both presentation of

data and analysis of results. Chapter 7 draws the conclusions, recommendations, and suggestion

for further research. Finally, the appendix will give a depiction of statistical information gathered

during the research, and figures of the firms.

CHAPTER 1. Introduction CHAPTER 2. An Overview of

Firm’s Capital Structure in

Indonesia

CHAPTER 3. Literature Review CHAPTER 4. Conceptual

Framework

CHAPTER 6. Presentation of Data

and Analysis of Results

CHAPTER 7. Conclusion,

Recommendations, and

Suggestion for Further Research

Appendices

CHAPTER 5. Research

Methodology

24

2. AN OVERVIEW OF THE CAPITAL STRUCTURE OF INDONESIAN

MANUFACTURING FIRMS

2.1. Indonesian Capital Market

The capital market plays an important role in the economy of a country, including

Indonesia, because it serves two functions at the same time. First, the capital market serves as an

alternative for a company's capital resources. The capital gained from the public offering can be

used for the company's business development, expansion, and so on. Second, the capital market

serves as an alternative for public investment. People could invest their money according to their

preferred returns and risk characteristics of each instrument.

2.1.1 History of Indonesia Stock Exchange

Below is the brief history of the Indonesia Stock Exchange. The first Stock Exchange in

Indonesia was built in Batavia (currently known as Jakarta) in December 1912. The Batavia Stock

Exchange was closed during the years 1914 -1918. It was re-opened in 1925 and new stock

exchanges were established in Semarang and Surabaya. However, between 1919 and 1924, the

Indonesia Stock Exchange (IDX) was still closed.

The Jakarta Stock Exchange (JSX) was re-closed during the years 1942 – 1952. On

August 10, 1977, the Exchange was re-activated by President Soeharto. It was supervised under

the management of the Capital Market Supervisory Agency (Badan Pengawas Pasar Modal, or

BAPEPAM). The re-activation of the capital market was also marked by the going public of PT

Semen Cibinong as the first issuer listed in the JSX. July 10th is celebrated as the anniversary of

the Capital Market in Indonesia.

In 1977 – 1987, the activity of stock trading in the JSX was dull. There were only 24

listed companies in the JSX. Most people preferred to invest their money in banks rather than the

capital market. December Package 1987) was issued to give ways for companies to go public and

for foreign investors to invest their money in Indonesia in 1987. In 1988 – 1990, deregulation

packages in banking and capital market were made. The JSX welcomed foreign investors. The

activities of the JSX were improving. On June 16, 1989, the Surabaya Stock Exchange started to

operate and was managed by the Surabaya Stock Exchange Inc.

On July 13, 1992, the JSX was privatised, and this date is celebrated as the anniversary of

the Jakarta Stock Exchange. The JSX introduced its computerized Jakarta Automatic Trading

System (JATS) on May 22, 1995. On November 10, 1995, the Government of Indonesia issued

Regulations No. 8 year 1995 on the capital market. This regulation was effective from January

1996. The JSX started to implement the remote trading system in 2002. In 2007, the Surabaya

Stock Exchange was merged into Jakarta Stock Exchange. As a result, the JSX changed its name

into the Indonesia Stock Exchange.

2.1.2 Stock Price Index in the Indonesian Capital Market

In order to give more complete information on the stock exchange development to the

public, the Indonesian Stock Exchange (IDX) has spread the indicators of the stock price

25

movement through the printed and electronic media. One indicator of the stock price movement is

the Stock Price Index. At present, the JSX has 9 constituent Stock Price Indices and 10 sectors:

Composite Stock Price Index (CSPI), Main Board Index (MBX), Kompas 100, Liquid 45

(LQ45), Jakarta Islamic Index, Development Board Index (DBX), Indonesian Securties Rating

Agency (PEFINDO25), BISNIS-27, and Sustainable Responsible Investment-Indonesian

Biodiversity Foundation. The sectors include mining, agriculture, consumers, miscellaneous-

industry, manufacture, infrastructure, finance, trade, basic-industry, and property.

The following indices are guidelines for investors to make stock investment in the

Indonesian capital market.

1. The Composite Stock Price Index (CSPI), the index that uses all of the Companies Listed as a

component of index calculation. The Composite Stock Price Index (CSPI) was introduced the

first time on April 1st, 1983 as an indicator of the movement of all listed stock prices in the

JSX, for both the regular and the preferred stocks. The base day for the CSPI‟s calculation is

on August 10th

, 1982. At that date, the index was determined at 100, and the listed number of

stocks at that time was thirteen.

2. The JSX LQ45 Index was created to provide the market with an index that represents 45 of

the most liquid stocks. To date, the LQ45 Index covers at least 70% of the market

capitalisation and transaction values in the Regular Market. The LQ45 Index of historical

calculation was defined on July 13, 1994, with a base value of 100. The index consists of 45

stocks that have passed the liquidity and market capitalisation screenings.

3. The Jakarta Islamic Index was launched on July 3, 2000. The index consists of 30 stocks that

have passed the selection under the direction of the Sharia Supervisory Board of the Majelis

Ulama Indonesia. Stocks from listed companies with business activities that comply with the

Islamic sharia can be included into the index.

4. The Kompas 100 Index is an index consisting of 100 shares of Listed Companies that are

selected, based on considerations of liquidity and market capitalisation, in line with

predetermined criteria.

5. The Index BUSINESS-27 is a collaboration between the IDX and Bisnis Indonesia Daily. The

Stock index Listed Companies are selected based on fundamental criteria, technical or

liquidity of transactions and accountability and corporate governance.

6. The PEFINDO-25 Index is a collaboration between the BEI and the PEFINDO rating

agencies, which is intended to provide additional information for investors, especially for the

shares of small and medium-sized listed companies (Small Medium Enterprises/SME).

7. The Sustainable Responsible Investment-KEHATI Index is the index established for

cooperation between the BEI and the Indonesian Biodiversity Foundation (KEHATI). This

index is expected to provide additional information to investors who want to invest in stocks

that have excellent performance in encouraging sustainable business, and have awareness of

the environment and run good corporate governance.

8. The Main Board Index (MBX) and the Development Board Index (DBX). On July13th

, 2000,

the JSX launched a new rule on stock listing: the Two Board Listing System. This system is

implemented to stimulate the Indonesian Capital Market and also to recover public confidence

for the Exchange through the arrangement of good corporate governance.

9. Sectoral indices, the index that uses all the Listed Companies included in each sector. Today

there are 10 sectors in the IDX, namely agriculture; mining;, primary industrie;, miscellaneous

industry;, consumer goods; property; infrastructure; finance; trade and services; and

manufacture.

26

2.1.3. Description of the LQ45 Index

We chose the LQ45 Index as our population as LQ45 Index consists of 45 stocks with

high liquidity. The Indonesia Stock Exchange regularly monitors the performance progress of the

stock components which are included in the calculation of the LQ45 index. Every three months an

evaluation on the movement sequence of the shares is conducted. Replacement shares will be

conducted every six months, i.e. at the beginning of February and August. Therefore, we chose the

LQ45 index as our population in this research.

Since its launch in February 1997, the primary measure of liquidity transaction is the

value of transactions in the regular market. In accordance with market developments, and to

sharpen further the criteria of liquidity, since the review in January 2005, the number of trading

days and the frequency of transactions has been included as a measure of liquidity. Thus, the

criterium of stock that is to be included in the calculation of the LQ45 Index is as follows:

1. Has been listed on the Stock Exchange at least 3 months

2. Log in 60 stocks based on the value of transactions in the regular market

3. Of the 60 stocks, 30 stocks with the largest transaction value will automatically be included on

the calculation of the index LQ45.

4. To get 45 shares 15 shares will be selected again by using the criteria of day transaction in

regular market, frequency of transaction in regular market and market capitalisation. 15 stocks

selection methods are the following:

a. 30 of the remaining stocks, 25 stocks are selected based on transactions day in the regular

market.

b. 25 of the stocks 20 stocks will be selected based on the frequency of transactions in the

regular market.

c. 20 of the stocks will be selected 15 stocks based on market capitalisation, so it will get 45

shares for calculation of the LQ45 Index.

5. In addition to considering the liquidity criteria and market capitalisation mentioned above, will

be seen also the financial condition and prospects of the company's growth.

2.2. Characteristics of the Research Sample

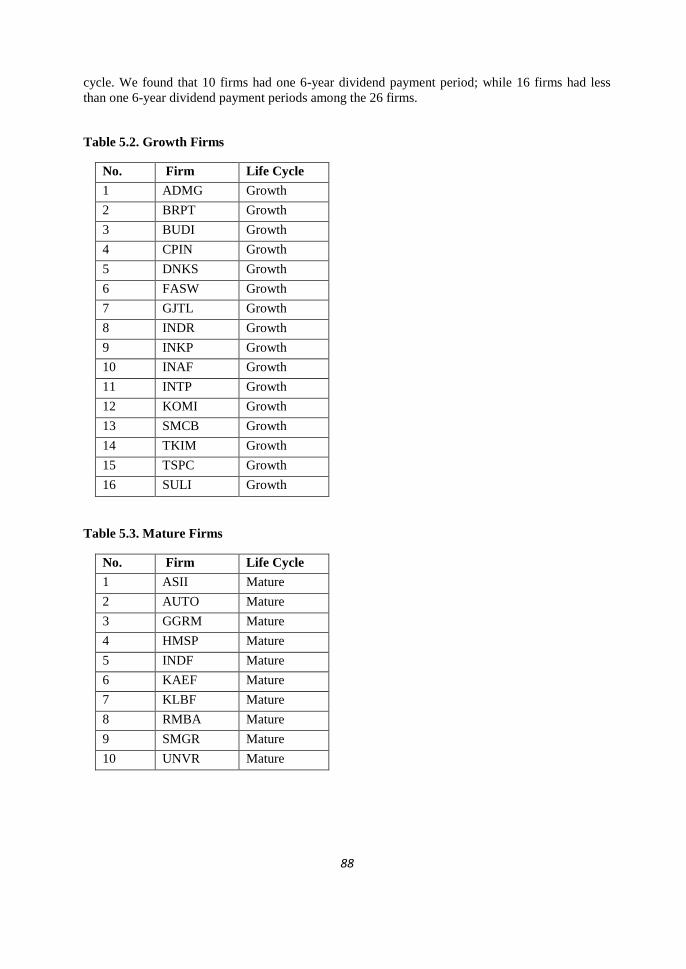

We constructed two samples of firms according to their life cycle stage, namely, firms in

their growth stage and firms in their mature stage. Bulan and Yan (2009) defined the growth stage

as the first six-year-period after the year of the firm‟s initial public offering (IPO). They treated the

IPO as the starting point of the growth stage (or the “new growth” stage). Hence, we follow them

to identify the growth stage. We took Grullon, Michaely and Swaminathan (2000), DeAngelo,

DeAngelo and Stulz (2005) and Bulan, Subramanian and Tanlu as the references (2007) who

found that firms initiated dividends were mature firms. Thus, we identified firms in their mature

stage by their dividend history.

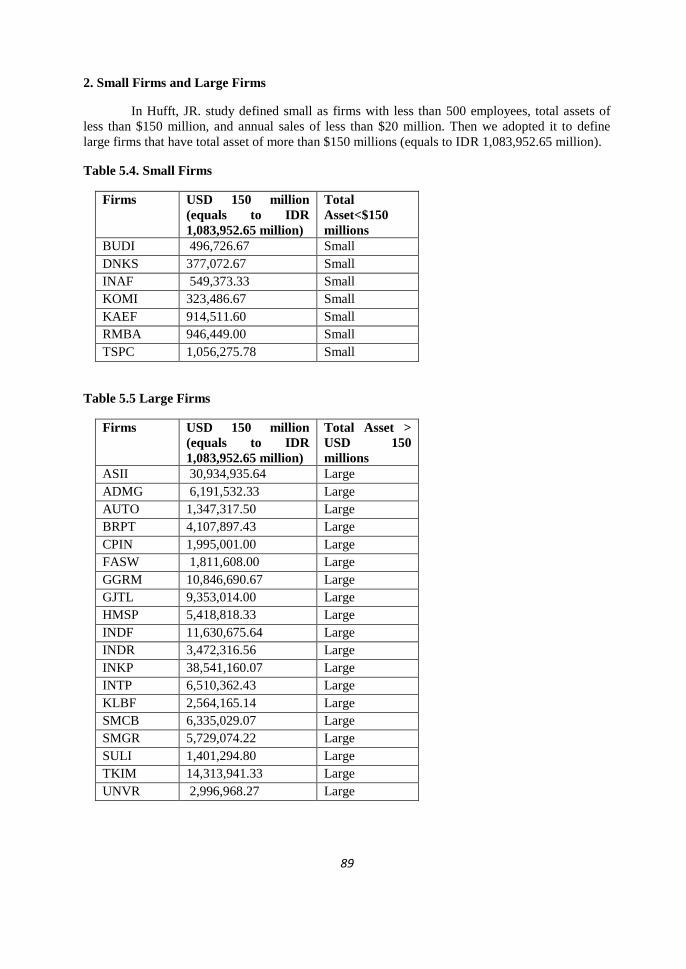

Meanwhile, we defined six years old or younger as young firms and seven years or older

as old firms. We followed Bulan and Yan (2007) and Evans (1987) to set the length of each stage

to be 6 years. Finally, we defined "small" as firms with total assets of less than $150 million, and

large firms that have total asset of more than $150 millions (Hufft, JR), it equals to IDR

1,081,028.68 or 1,086,876.61.

27

1. Astra International Tbk (ASII)

ASII is a company engaged in the sector of miscellaneous industry, by the industrial sub

sector of Automotive and Components. It was established on February 20, 1957 and was listed at

the IDX on April 4, 1990. Its IPO price was IDR 14850. In the period of 1996 to 2009 the price

was very volatile. In July 2010 the price was increased significantly to IDR 50700.